Developments of Islamic Banking in Bangladesh...3 Developments of Islamic Banking Industry in...

13

1 Developments of Islamic Banking in Bangladesh 1 January-March, 2018 Islamic Banking Cell Research Department Bangladesh Bank 1 Prepared by Islamic Banking Cell, Research Department, Bangladesh Bank (Central Bank of Bangladesh). Feedbacks are welcome. Feedbacks may be sent to Nazmun Nahar Mily, Deputy General Manager, Research Department, Bangladesh Bank. (E-mail: [email protected]) and Subarna Ershad, Assistant Director, Research Department, Bangladesh Bank. (E-mail: [email protected]).

Transcript of Developments of Islamic Banking in Bangladesh...3 Developments of Islamic Banking Industry in...

1

Developments of Islamic Banking in Bangladesh1

January-March, 2018

Islamic Banking Cell

Research Department

Bangladesh Bank

1Prepared by Islamic Banking Cell, Research Department, Bangladesh Bank (Central Bank of Bangladesh). Feedbacks are welcome. Feedbacks may be sent to Nazmun Nahar Mily, Deputy General Manager, Research Department, Bangladesh Bank. (E-mail: [email protected]) and Subarna Ershad, Assistant Director, Research Department, Bangladesh Bank. (E-mail: [email protected]).

2

Quarterly Report Preparation Committee

Chairman Dr. Md. Akhtaruzzaman

Economic Adviser

Coordinator Md. Abdul Awwal Sarker

General Manager

Team Member Nazmun Nahar Mily Deputy General Manager

Subarna Ershad Assistant Director

3

Developments of Islamic Banking Industry in Bangladesh during January-March 2018

Islamic banking has expanded three times of its size from 2007, with Compound Annual Growth Rate (CAGR)

of 11.6% and takaful sector has grown 5 times with a CAGR of 19.34% during this period. Islamic banking

sector has already become systemically important in over 12 countries with more than 15% market share

globally.2 The total assets of the Islamic banking industry of IFSB member countries grew from USD 1,391

billion in 2016Q1 to USD 1,480 billion in 2017Q1 (calculated from country-wise aggregated data converted

into USD terms using end-period exchange rates). Total funding/liabilities increased from USD 1,283 billion in

2016Q1 to USD 1,362 billion in 2017Q1. Gross nonperforming financing ratio (gross nonperforming financing

to total financing) showed an improvement with a decrease from 5.9% in 2016Q1 to 5.2% in 2017Q1. On the

liquidity indicators, the liquid assets ratio (liquid assets to total assets) decreased over the period from 35.7% in

2016Q1 to 34.5% in 2017Q1, while liquid assets to short-term liabilities ratio increased from 13.9% in 2016Q1

to 14.6% in 2017Q1.3

Islamic Banking has remarkably captured the interest of both Islamic and contemporary economists. Parker

(1993), observes that the introduction of Islamic banking principles by various western bankers have shown a

positive results which indicates that Islamic banking systems can work effectively in both developed as well as

developing nations regardless of religious boundary. The introduction of interest-free and equity-based Islamic

banking system, proved its significance in the country's banking sector which continued to show strong growth

since its inception in 1983 in tandem with the growth in the economy, as reflected by the increased market share

as well as in mobilizing deposits and financing key sectors of the economy in Bangladesh. This report gives an

overview of the Islamic Banking Industry regarding the developments taking place during the January-March

2018 quarter. As at the end of March 2018, 8 full-

fledged Islamic banks are operating with 1137 branches

out of total 9973 branches of the banking industry; in

addition, 19 Islamic banking branches of 9 conventional

commercial banks and 25 Islamic banking windows of 8

conventional commercial banks are also providing

Islamic financial services in Bangladesh. At the end of

the January-March 2018 quarter, deposits and

investments, of Islamic banking industry grew by

0.61%, 4.00% respectively and remittance lowered by

18.34 % while surplus liquidity declined by 41.77%

compared to the previous quarter. Islamic Banking

Industry accounted for more than one-fifth share of the

entire banking industry in terms of deposits and

investments at the end of the quarter under review.

2 23 October 2017, Press Release, IFSB, Speech by the Acting Secretary General of the IFSB at the IFSB Summit, 2017 3 The IFSB Bulletin Volume 5 Issue 2 | Dec 2017, page-4.

Though surplus liquidity declined compared to

previous quarter as well as corresponding quarter

of the previous year, actually Islamic banks in

Bangladesh have been facing excess liquidity

problem since long as they cannot invest in

Government Treasury Bills and Bonds because of

the very interest bearing nature of those

monetary instruments. During this quarter,

remittances decreased significantly through

Islamic banks of Bangladesh.

4

Highlights on Islamic Banking Sector in Bangladesh, January-March 2018

Total

Deposits

Total Deposits in Islamic banking industry reached at Tk. 215557.93 crores at the end of

January-March 2018 quarter, which increased by Tk. 1298.51 crores or by 0.61%

compared to previous quarter and by Tk. 25300.23 crores or by 13.30% compared to

corresponding quarter of the last year.

Total

Investments

Total Investments (Loans in conventional sense) in Islamic banking sector stood at Tk.

209147.92 crores at the end of January-March 2018 quarter, which went up by Tk.

8045.92 crores or by 4.00% and by Tk. 32054.25 crores or by 18.10% compared to

previous quarter and same quarter of the preceding year respectively.

Investment-

Deposit

Ratio

Investment-Deposit Ratio (Credit-Deposit Ratio in conventional sense) reached at 0.97

in January-March 2018 quarter which was 0.94 at the previous quarter of this year and

0.93 at the end of March 2017.

Surplus

Liquidity

Surplus Liquidity of Islamic banking industry stood at Tk. 5077.98 crores at the end of

January-March 2018 quarter, which was decreased by Tk. 3641.93 crores (41.77%) and

lowered by Tk. 2953.64 crores (36.78%) compared to the previous quarter and

corresponding quarter of the preceding year respectively.

Total

Remittances

Total Remittances mobilized by the Islamic banking sector stood at Tk. 9039.97 crores

at the end of January-March 2018 quarter, which was lower by Tk. 2030.89 crores or by

18.34% compared to the previous quarter and higher by Tk. 2379.80 crores or by

35.73% compared to the same quarter of the preceding year.

Branches

The Number of Branches of Islamic banking sector including Islamic branches/windows

of conventional commercial banks stood at 1181 at the end of the quarter under review

which was 1168 during the previous quarter and 1052 during the same quarter of the last

year.

Manpower Total Manpower in Islamic banking sector was 32309 in number at the end of the

quarter under review which was greater by 1318 persons than that of the last quarter

and by 2262 persons compared to the same quarter of the last year.

5

Table 1: Islamic Banking Activities compared with all banks in Bangladesh

Items

January-March 2018@ October-December

2017@

All Banks Islamic

Banks

Share of Islamic

Banks Among

All Banks

Share of Islamic

Banks Among All

Banks

1 2 3=(2/1*100) 4

Total Deposits (In Crore Taka) 925279.7 215557.93 23.30 23.13

Total Credit (In Crore Taka) 869562.30 209147.92 24.05 23.81

Remittances (In Crore Taka) 31743.47 9039.97 28.48 38.30

Total Excess Liquidity (In Crore Taka) 76888.16 5077.98 6.60 8.98

Total Number of Bank Branches 9973 1139 11.42 11.73

Total Agricultural Credit (In Crore Taka) 40420.62 948.39 2.35 8.26

Source: Statistics Department, DOS & BRPD, Bangladesh Bank.

@ Provisional

6

Table 2: Islamic Banking Activities in Bangladesh, January-March 2018

March-

18#

December

-17#

March-

17# Changes % Changes

Quarter Quarter Quarter Quarterly Annual Quarterly Annual

Total Deposits* ( Taka in Crore) 215557.93 214259.42 190257.70 1298.51 25300.23 0.61 13.30

a) Full-fledged Islamic Banks 204526.34 203698.12 181207.99 828.22 23318.35 0.41 12.87

b) Conventional banks having Islamic banking

branches

6116.58 5866.19 5289.28 250.39 827.30 4.27 15.64

c) Islamic banking windows 4915.01 4695.11 3760.42 219.90 1154.58 4.68 30.70

Total Investments* (Taka in Crore) 209147.92 201101.99 177093.67 8045.92 32054.25 4.00 18.10

a) Full-fledged Islamic Banks 199047.29 191279.35 169071.21 7767.94 29976.07 4.06 17.73

b) Conventional banks having Islamic banking

branches

5670.12 5583.04 4805.41 87.08 864.71 1.56 17.995

c) Islamic banking windows 4430.51 4237.20 3217.05 193.30 1213.46 4.56 37.72

Investment/Deposit Ratio 0.97 0.94 0.93 0.03 0.04 3.37 4.24

a) Full-fledged Islamic Banks 0.97 0.94 0.93 0.03 0.04 3.64 4.31

b) Conventional banks having Islamic banking

branches

0.93 0.95 0.91 -0.02 0.02 -2.60 2.04

c) Islamic banking windows 0.90 0.90 0.86 0.00 0.05 -0.12 5.37

Liquidity Surplus(+)/Deficit(-) (Taka in

Crore)

5077.98 8719.91 8031.62 -3641.93 -2953.64 -41.77 -36.78

a) Full-fledged Islamic Banks 4187.96 7791.84 6662.74 -3603.88 -2474.78 -46.25 -37.14

b) Conventional banks having Islamic banking

branches

431 190.12 855.98 240.87 -424.98 126.69 -49.65

c) Islamic banking windows 459.02 737.95 512.89 -278.93 -53.87 -37.80 -10.50

Total Remittances (Taka in Crore) 9039.97 11070.85 6660.16 -2030.89 2379.80 -18.34 35.73

a) Full-fledged Islamic Banks 8986.51 10980.14 6609.92 -1993.63 2376.59 -18.16 35.95

b) Conventional banks having Islamic banking

branches

44.15 57.45 43.81 -13.31 0.33 -23.16 0.75

c) Islamic banking windows 9.31 33.26 6.43 -23.95 2.88 -72.01 44.82

Total Branches 1181 1168 1052 -29 87 -2.48 8.27

a) Full-fledged Islamic Banks 1137 1124 1008 -29 87 -2.58 8.63

b) Conventional banks having Islamic banking

branches

19 19 19 0 0 0.00 0.00

c) Islamic banking windows 25 25 25 0 0 0.00 0.00

Total Manpower 32309 30991 30047 1318 2262 4.25 7.53

a) Full-fledged Islamic Banks 31728 30408 29478 1320 2250 4.34 7.63

b) Conventional banks having Islamic banking

branches

400 405 393 -5 7 -1.23 1.78

c) Islamic banking windows 181 178 176 3 5 1.69 2.84

* = Excluding Inter-Bank Items

#Provisional

7

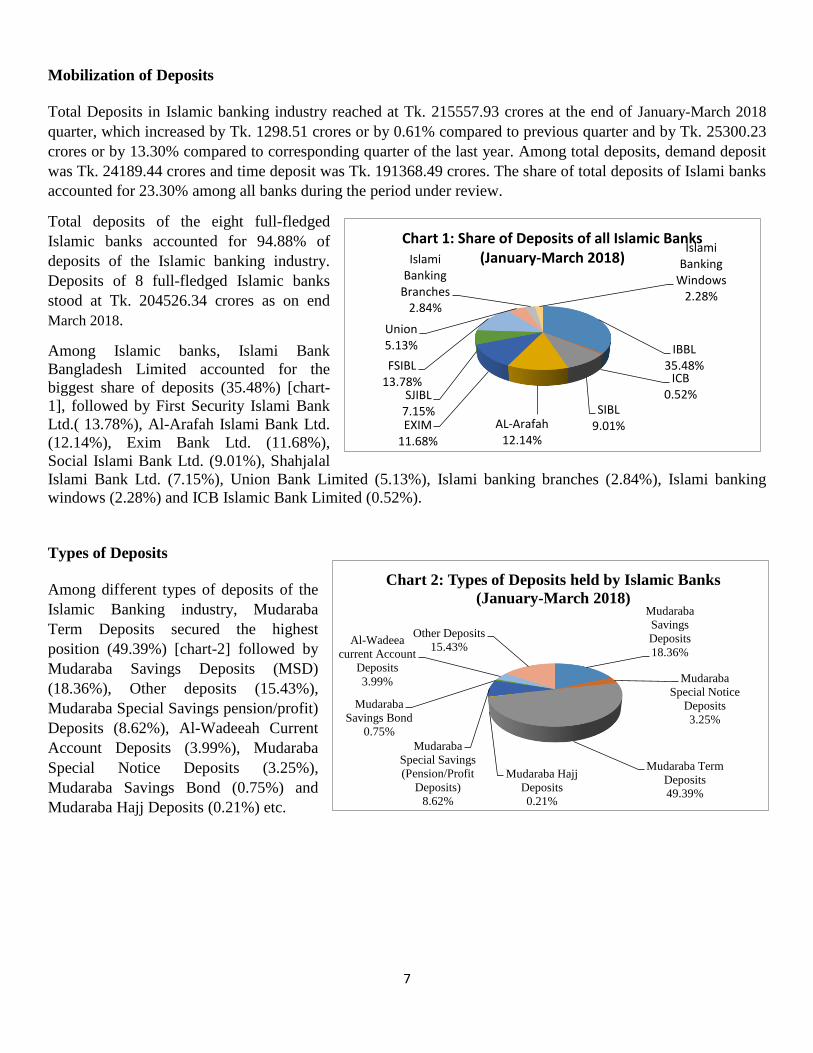

Mobilization of Deposits

Total Deposits in Islamic banking industry reached at Tk. 215557.93 crores at the end of January-March 2018

quarter, which increased by Tk. 1298.51 crores or by 0.61% compared to previous quarter and by Tk. 25300.23

crores or by 13.30% compared to corresponding quarter of the last year. Among total deposits, demand deposit

was Tk. 24189.44 crores and time deposit was Tk. 191368.49 crores. The share of total deposits of Islami banks

accounted for 23.30% among all banks during the period under review.

Total deposits of the eight full-fledged

Islamic banks accounted for 94.88% of

deposits of the Islamic banking industry.

Deposits of 8 full-fledged Islamic banks

stood at Tk. 204526.34 crores as on end

March 2018.

Among Islamic banks, Islami Bank

Bangladesh Limited accounted for the

biggest share of deposits (35.48%) [chart-

1], followed by First Security Islami Bank

Ltd.( 13.78%), Al-Arafah Islami Bank Ltd.

(12.14%), Exim Bank Ltd. (11.68%),

Social Islami Bank Ltd. (9.01%), Shahjalal

Islami Bank Ltd. (7.15%), Union Bank Limited (5.13%), Islami banking branches (2.84%), Islami banking

windows (2.28%) and ICB Islamic Bank Limited (0.52%).

Types of Deposits

Among different types of deposits of the

Islamic Banking industry, Mudaraba

Term Deposits secured the highest

position (49.39%) [chart-2] followed by

Mudaraba Savings Deposits (MSD)

(18.36%), Other deposits (15.43%),

Mudaraba Special Savings pension/profit)

Deposits (8.62%), Al-Wadeeah Current

Account Deposits (3.99%), Mudaraba

Special Notice Deposits (3.25%),

Mudaraba Savings Bond (0.75%) and

Mudaraba Hajj Deposits (0.21%) etc.

IBBL35.48%

ICB0.52%

SIBL9.01%AL-Arafah

12.14%EXIM

11.68%

SJIBL7.15%

FSIBL13.78%

Union5.13%

Islami Banking

Branches2.84%

Islami Banking

Windows2.28%

Chart 1: Share of Deposits of all Islamic Banks (January-March 2018)

Mudaraba

Savings

Deposits

18.36%

Mudaraba

Special Notice

Deposits

3.25%

Mudaraba Term

Deposits

49.39%

Mudaraba Hajj

Deposits

0.21%

Mudaraba

Special Savings

(Pension/Profit

Deposits)

8.62%

Mudaraba

Savings Bond

0.75%

Al-Wadeea

current Account

Deposits

3.99%

Other Deposits

15.43%

Chart 2: Types of Deposits held by Islamic Banks

(January-March 2018)

8

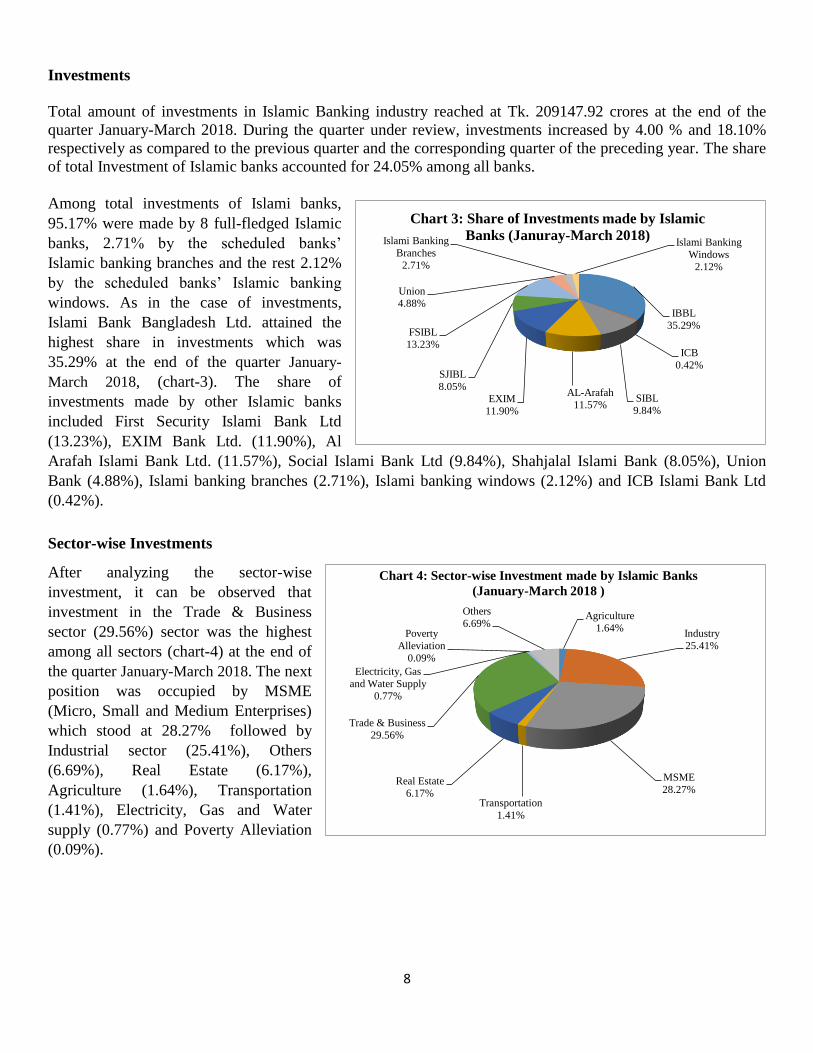

Investments

Total amount of investments in Islamic Banking industry reached at Tk. 209147.92 crores at the end of the

quarter January-March 2018. During the quarter under review, investments increased by 4.00 % and 18.10%

respectively as compared to the previous quarter and the corresponding quarter of the preceding year. The share

of total Investment of Islamic banks accounted for 24.05% among all banks.

Among total investments of Islami banks,

95.17% were made by 8 full-fledged Islamic

banks, 2.71% by the scheduled banks’

Islamic banking branches and the rest 2.12%

by the scheduled banks’ Islamic banking

windows. As in the case of investments,

Islami Bank Bangladesh Ltd. attained the

highest share in investments which was

35.29% at the end of the quarter January-

March 2018, (chart-3). The share of

investments made by other Islamic banks

included First Security Islami Bank Ltd

(13.23%), EXIM Bank Ltd. (11.90%), Al

Arafah Islami Bank Ltd. (11.57%), Social Islami Bank Ltd (9.84%), Shahjalal Islami Bank (8.05%), Union

Bank (4.88%), Islami banking branches (2.71%), Islami banking windows (2.12%) and ICB Islami Bank Ltd

(0.42%).

Sector-wise Investments

After analyzing the sector-wise

investment, it can be observed that

investment in the Trade & Business

sector (29.56%) sector was the highest

among all sectors (chart-4) at the end of

the quarter January-March 2018. The next

position was occupied by MSME

(Micro, Small and Medium Enterprises)

which stood at 28.27% followed by

Industrial sector (25.41%), Others

(6.69%), Real Estate (6.17%),

Agriculture (1.64%), Transportation

(1.41%), Electricity, Gas and Water

supply (0.77%) and Poverty Alleviation

(0.09%).

IBBL

35.29%

ICB

0.42%

SIBL

9.84%

AL-Arafah

11.57%EXIM

11.90%

SJIBL

8.05%

FSIBL

13.23%

Union

4.88%

Islami Banking

Branches

2.71%

Islami Banking

Windows

2.12%

Chart 3: Share of Investments made by Islamic

Banks (Januray-March 2018)

Agriculture

1.64%Industry

25.41%

MSME

28.27%

Transportation

1.41%

Real Estate

6.17%

Trade & Business

29.56%

Electricity, Gas

and Water Supply

0.77%

Poverty

Alleviation

0.09%

Others

6.69%

Chart 4: Sector-wise Investment made by Islamic Banks

(January-March 2018 )

9

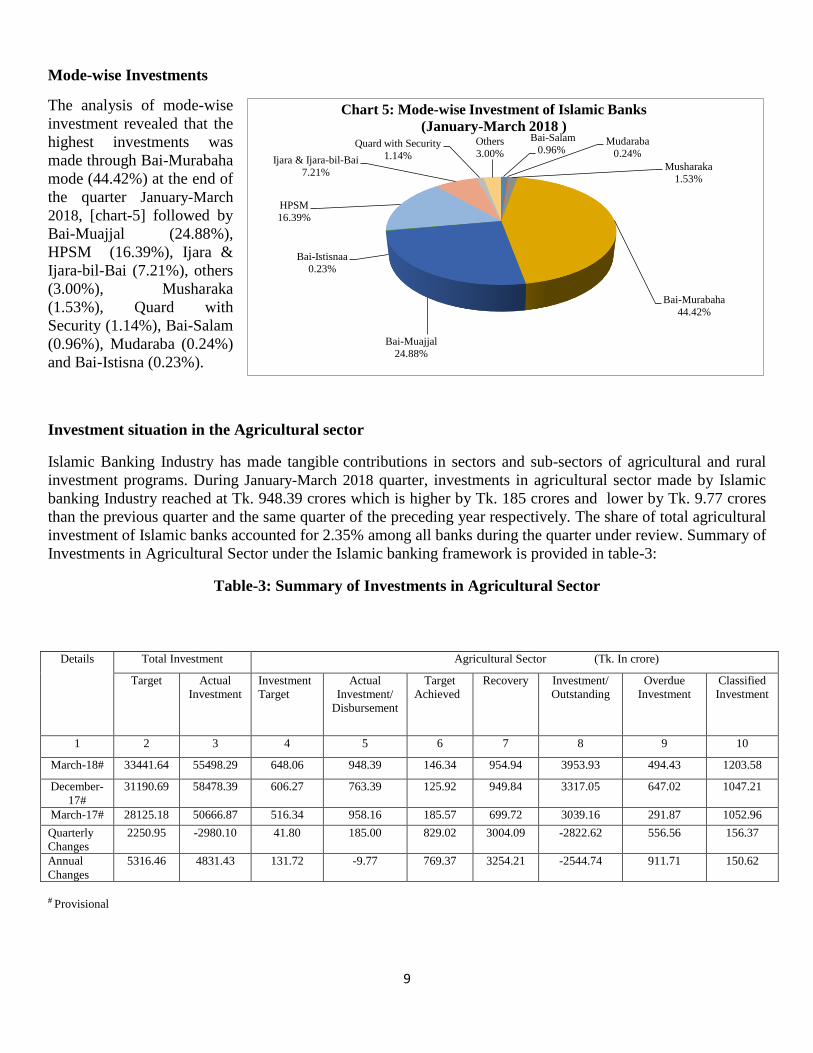

Mode-wise Investments

The analysis of mode-wise

investment revealed that the

highest investments was

made through Bai-Murabaha

mode (44.42%) at the end of

the quarter January-March

2018, [chart-5] followed by

Bai-Muajjal (24.88%),

HPSM (16.39%), Ijara &

Ijara-bil-Bai (7.21%), others

(3.00%), Musharaka

(1.53%), Quard with

Security (1.14%), Bai-Salam

(0.96%), Mudaraba (0.24%)

and Bai-Istisna (0.23%).

Investment situation in the Agricultural sector

Islamic Banking Industry has made tangible contributions in sectors and sub-sectors of agricultural and rural

investment programs. During January-March 2018 quarter, investments in agricultural sector made by Islamic

banking Industry reached at Tk. 948.39 crores which is higher by Tk. 185 crores and lower by Tk. 9.77 crores

than the previous quarter and the same quarter of the preceding year respectively. The share of total agricultural

investment of Islamic banks accounted for 2.35% among all banks during the quarter under review. Summary of

Investments in Agricultural Sector under the Islamic banking framework is provided in table-3:

Table-3: Summary of Investments in Agricultural Sector

Details Total Investment Agricultural Sector (Tk. In crore)

Target Actual

Investment

Investment

Target

Actual

Investment/

Disbursement

Target

Achieved

Recovery Investment/

Outstanding

Overdue

Investment

Classified

Investment

1 2 3 4 5 6 7 8 9 10

March-18# 33441.64 55498.29 648.06 948.39 146.34 954.94 3953.93 494.43 1203.58

December-

17#

31190.69 58478.39 606.27 763.39 125.92 949.84 3317.05 647.02 1047.21

March-17# 28125.18 50666.87 516.34 958.16 185.57 699.72 3039.16 291.87 1052.96

Quarterly

Changes

2250.95 -2980.10 41.80 185.00 829.02 3004.09 -2822.62 556.56 156.37

Annual

Changes

5316.46 4831.43 131.72 -9.77 769.37 3254.21 -2544.74 911.71 150.62

# Provisional

Bai-Salam

0.96%Mudaraba

0.24%

Musharaka

1.53%

Bai-Murabaha

44.42%

Bai-Muajjal

24.88%

Bai-Istisnaa

0.23%

HPSM

16.39%

Ijara & Ijara-bil-Bai

7.21%

Quard with Security

1.14%

Others

3.00%

Chart 5: Mode-wise Investment of Islamic Banks

(January-March 2018 )

10

Liquidity Situation

At the end of the quarter January-

March 2018, surplus liquidity in

the Islamic banking sector stood at

Tk. 5077.98 crores which was

decreased by Tk. 3641.93 crores or

by 41.77% and lowered by Tk.

2953.64 crores or by 36.78% than

the last quarter and the same

quarter of the previous year

respectively. The surplus liquidity

of 8 Islamic banks, Islamic

banking branches of conventional

banks and Islamic windows of

conventional banks stood at Tk.

4187.96 crores, Tk. 431 crores, and

Tk. 459.02 crores respectively. It is observed that at the end of the quarter January-March 2018, surplus

liquidity declined significantly compared to previous quarter as well as corresponding quarter of the previous

year. The share of total excess liquidity of Islamic banks accounted for 6.6% among all banks during the period

under review. Summary of liquidity situation in the Islamic Banking sector is shown in chart 6.

Remittances Mobilized by the Islamic Banking Sector

Islamic Banking Industry of the country is

playing a vital role in collecting foreign

remittances and disbursing the same

transferring among beneficiaries across the

country. During January-March 2018, amount

of remittances reached at Tk. 9039.97 crores

which was lower by Tk. 2030.89 crores or by

18.34% and higher by Tk. 2379.80 crores or

by 35.73% than the previous quarter and the

corresponding quarter of the last year

respectively. Among the Islamic banks,

Islami Bank Bangladesh Ltd. occupied the

top position (79%) in respect of remittance

collection at the end of January-March 2018.

The shares of remittance of other Islamic

banks included Al Arafah Islami Bank Ltd. (9.28%), Social Islami Bank Ltd (4.70%), First Security Islami

Bank Ltd (3.57%), EXIM Bank Ltd. (1.27%), Shahjalal Islami Bank (1.26%), Union Bank Ltd (0.31%), Islamic

banking branches (0.49%), and Islamic banking windows (0.10%).

0

500

1000

1500

2000

2500

3000

648.0

0

1.2

3

715.6

8 1374.0

6

689.0

1

507.0

4

105.4

3

147.5

1

434.3

1

459.0

2

2692.1

7

4.8

9

659.8

1329.2

2

1667.3

5

424.0

6

498.0

3

516.3

2

190.1

2 737.9

5

Ta

ka

in

cro

re

Chart 6:Surplus liquidity of Islamic Banks over two

periods

March-18# December-17#

IBBL79.00%

ICB0.03%

SIBL4.70%

AL-Arafah9.28%

EXIM 1.27%

SJIBL1.26%

FSIBL3.57%

Union0.31%

Islami Banking Branches

0.49%Islami Banking

Windows0.10%

Chart 8: Share of Remittances made by Islami Banks (January-March 2018)

11

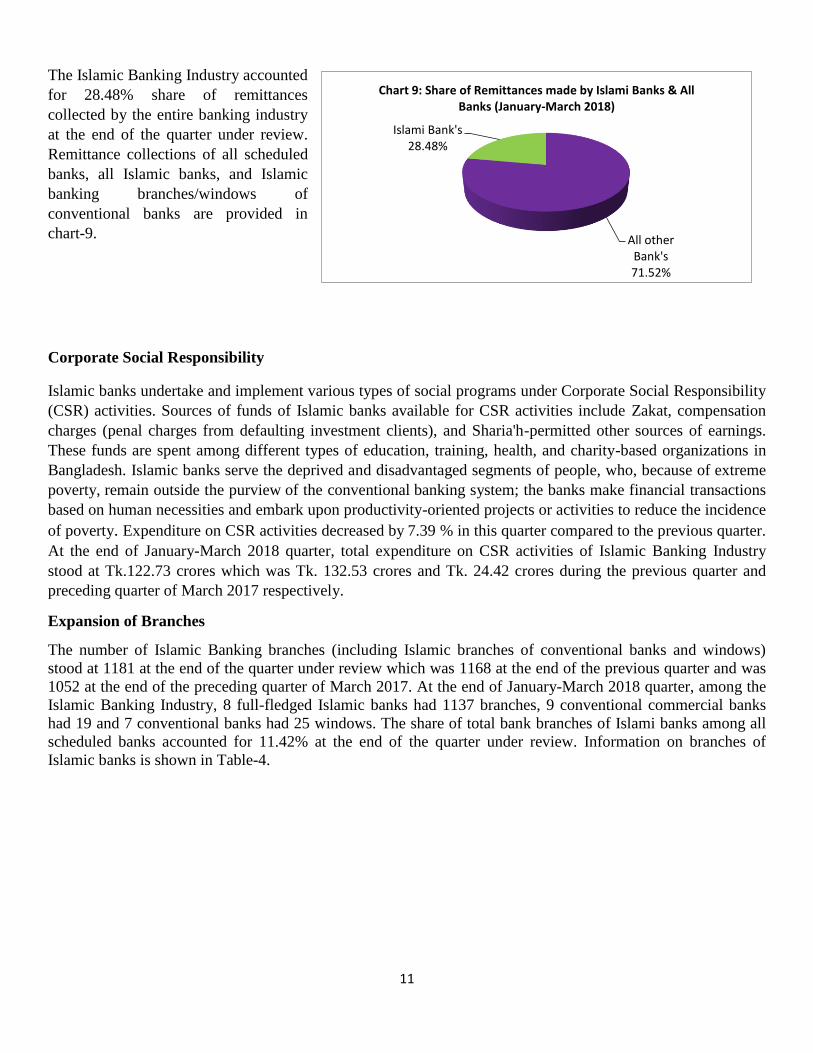

The Islamic Banking Industry accounted

for 28.48% share of remittances

collected by the entire banking industry

at the end of the quarter under review.

Remittance collections of all scheduled

banks, all Islamic banks, and Islamic

banking branches/windows of

conventional banks are provided in

chart-9.

Corporate Social Responsibility

Islamic banks undertake and implement various types of social programs under Corporate Social Responsibility

(CSR) activities. Sources of funds of Islamic banks available for CSR activities include Zakat, compensation

charges (penal charges from defaulting investment clients), and Sharia'h-permitted other sources of earnings.

These funds are spent among different types of education, training, health, and charity-based organizations in

Bangladesh. Islamic banks serve the deprived and disadvantaged segments of people, who, because of extreme

poverty, remain outside the purview of the conventional banking system; the banks make financial transactions

based on human necessities and embark upon productivity-oriented projects or activities to reduce the incidence

of poverty. Expenditure on CSR activities decreased by 7.39 % in this quarter compared to the previous quarter.

At the end of January-March 2018 quarter, total expenditure on CSR activities of Islamic Banking Industry

stood at Tk.122.73 crores which was Tk. 132.53 crores and Tk. 24.42 crores during the previous quarter and

preceding quarter of March 2017 respectively.

Expansion of Branches

The number of Islamic Banking branches (including Islamic branches of conventional banks and windows)

stood at 1181 at the end of the quarter under review which was 1168 at the end of the previous quarter and was

1052 at the end of the preceding quarter of March 2017. At the end of January-March 2018 quarter, among the

Islamic Banking Industry, 8 full-fledged Islamic banks had 1137 branches, 9 conventional commercial banks

had 19 and 7 conventional banks had 25 windows. The share of total bank branches of Islami banks among all

scheduled banks accounted for 11.42% at the end of the quarter under review. Information on branches of

Islamic banks is shown in Table-4.

All other Bank's 71.52%

Islami Bank's 28.48%

Chart 9: Share of Remittances made by Islami Banks & All Banks (January-March 2018)

12

Table 4: Number of Bank Branches of Islamic Banks (January-March 2018)

Name of the Bank Urban Rural Total

A) Full-fledged Islamic Banks 681 456 1137

1| Islami Bank Bangladesh Limited* 231 101 332

2| ICB Islamic Bank Limited 28 5 33

3| Social Islami Bank Limited * 74 77 151

4| Al-Arafah Islami Bank Limited 83 71 154

5| EXIM Bank Limited 74 44 118

6| Shahjalal Islami Bank Limited 70 43 113

7| First Security Islami Bank Limited 87 81 168

8| Union Bank Limited 34 34 68

B) Islamic banking branches of Conventional banks 18 1 19

1| The City bank Limited 1 0 1

2| AB Bank Limited 1 0 1

3| Dhaka Bank Limited 2 0 2

4| Premier Bank Limited 2 0 2

5| Prime Bank Limited 5 0 5

6| Southeast Bank Limited 4 1 5

7| Jamuna Bank Limited 2 0 2

8| Bank Alfalah Limited 1 0 1

9| HSBC Limited 0

C) Islamic banking windows of Conventional banks 25 0 25

1| Sonali Bank Limited 5 0 5

2| Janata Bank Limited**

3| Agrani Bank Limited 5 0 5

4| Pubali Bank Limited 2 0 2

5| Trust Bank Limited 5 0 5

6| Standard Bank Limited 2 0 2

7| Bank Asia Limited 5 0 5

8| Standard Chartered Bank 1 0 1

D) Total=A+B+C 724 457 1181 * Including SME **Janata Bank Limited has obtained permission for starting Islamic Banking window from Bangladesh Bank, but not yet started..

Events Organized by the Islamic banks during the quarter

Islamic banks' Sharia'h Supervisory Boards have inspected 262 branches and 09 meetings held during the

quarter January-March 2018. Total numbers of publications published by the Islamic banks are 10, of which the

number of publication was Islami Bank Bangladesh Ltd. 08 and ICB Islamic Bank Ltd. 01 and Exim Bank Ltd.

01 during the quarter under review. Besides, Islamic banks have organized 62 seminar/workshop/conference

and 102 training course in home and the participants of foreign training course is 51 in number for boost up the

Sharia'h based knowledge of its employees during January-March 2018 quarter.

13

Concluding Remarks and Recommendations

Among different segments of Bangladesh’s Islamic finance Industry, Islamic banking industry dominates. The

Islamic banking segment continued to show rapid expansion in terms of growth of assets, deposits, investments,

and number of account holders. Now the Islamic banking sector accounts for more than 20% market share of

the entire banking sector and it plays a significant role in mobilizing deposits and financing different sectors of

the economy. During the quarter under review it is observed that, total investment increased this quarter mainly

in the sector like MSME, Trade & Business through the operational mechanism of different modes. Islamic

banking sector of the country may conduct some empirical research and surveys to redesign their investment

policies because the investments made by these banks in true modes like Mudaraba and Musharaka are at a

minimal level (only 1.77% of total investments). They should pay more attention in Research & Development

(R&D) to devising the proper guidelines and policies to promoting investments under Mudaraba and Musharaka

modes. Islamic banks may explore and innovate new sharia’h based financial instruments for better liquidity

management. As sharia'h is the backbone of the Islamic banking industry, a comprehensive Islamic legal

infrastructure with clear ground and commitment is necessary to help expedite Islamic financial industry to spur

as it intends for ensuring human welfare.

...............................................................