Development in the supply chain of the Philippine Goat ... · Development in the Supply Chain in...

42

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez Page 1 of 42 Development in the Supply Chain of the Philippine Goat Industry: An Assessment 1 Esplana, R. Elmer 2 , Lary Nel B. Abao 3 , Rolando M. Vasquez 4 ______________________________________________________________________________ ABSTRACT The study documents the development of the Philippine Goat Industry within the supply chain. The study used triangulation method that comprising of archival research, key informant interviews, benchmarking, competitiveness and profitability analysis. The study indicates that there have been many improvements in the supply chain of the Philippine goat industry from input supply to consumption. There were also some best practices that can be emulated among the goat industry stakeholders. The study also suggests for more investment opportunities for the goat production. Also, it indicates that the Philippine goat meat (chevon) product is competitive compared with other countries, such as Australia, United States and Canada, in terms of price competitiveness and the goat production is a very profitable entrepreneurial project. This underscores for a better outlook of the industry, in terms of better prices and supply, and higher consumption for both the local, and potentially export market in the coming years. The study results support the goals and objectives of the Department of Agriculture (DA) and Agriculture and Fisheries Modernization Act (AFMA) in contributing to food security, poverty alleviation, improved productivity and increased income and global competitiveness of the livestock sector, in general, and goat industry, in particular. 1 Received the Grand Prize Winner for the Best National R&D AFMA Paper Awards for Socio-economics Category. 19 th National Research Symposium (NRS), Bureau of Agricultural Research, Department of Agriculture, October 6, 2007. The 2007 NRS had a theme “Agriculture and Fisheries R&D Toward Agribusiness Development and Agro-Industrialization.” The main author can be contacted at email address: [email protected] or mobile no. +63 922-8117367. File can also be downloaded online at the CPR Community (Club of Professional Researchers) Website at www.smileyberks.com/cpr. 2 Agriculturist II, Bureau of Animal Industry (BAI) and President of the Club of Professional Researchers (CPR). 3 Agriculturist II, BAI, CPR Treasurer. 4 Agriculturist II, BAI, CPR Member

Transcript of Development in the supply chain of the Philippine Goat ... · Development in the Supply Chain in...

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 1 of 42

Development in the Supply Chain of the Philippine Goat Industry: An Assessment 1

Esplana, R. Elmer2, Lary Nel B. Abao3, Rolando M. Vasquez4 ______________________________________________________________________________

ABSTRACT The study documents the development of the Philippine Goat Industry within the supply chain.

The study used triangulation method that comprising of archival research, key informant

interviews, benchmarking, competitiveness and profitability analysis. The study indicates that

there have been many improvements in the supply chain of the Philippine goat industry from

input supply to consumption. There were also some best practices that can be emulated among

the goat industry stakeholders. The study also suggests for more investment opportunities for the

goat production. Also, it indicates that the Philippine goat meat (chevon) product is competitive

compared with other countries, such as Australia, United States and Canada, in terms of price

competitiveness and the goat production is a very profitable entrepreneurial project. This

underscores for a better outlook of the industry, in terms of better prices and supply, and higher

consumption for both the local, and potentially export market in the coming years. The study

results support the goals and objectives of the Department of Agriculture (DA) and Agriculture

and Fisheries Modernization Act (AFMA) in contributing to food security, poverty alleviation,

improved productivity and increased income and global competitiveness of the livestock sector,

in general, and goat industry, in particular.

1 Received the Grand Prize Winner for the Best National R&D AFMA Paper Awards for Socio-economics Category. 19th National Research Symposium (NRS), Bureau of Agricultural Research, Department of Agriculture, October 6, 2007. The 2007 NRS had a theme “Agriculture and Fisheries R&D Toward Agribusiness Development and Agro-Industrialization.” The main author can be contacted at email address: [email protected] or mobile no. +63 922-8117367. File can also be downloaded online at the CPR Community (Club of Professional Researchers) Website at www.smileyberks.com/cpr. 2 Agriculturist II, Bureau of Animal Industry (BAI) and President of the Club of Professional Researchers (CPR). 3 Agriculturist II, BAI, CPR Treasurer. 4 Agriculturist II, BAI, CPR Member

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 2 of 42

_____________________________________________________________________________ Keywords: Development in the Supply Chain, Assessment of Investment Opportunities in the Goat Industry, Profitability of Goat Production, and Price Competitiveness of Goat Meat _____________________________________________________________________________ I. INTRODUCTION The goat industry in the Philippines has undergone a lot of development since the First National

Small Ruminants Congress in Central Luzon State University in May 2001. In the said congress,

an interim body was formed which initially became the trailblazer for organizing the small

ruminant industry players in the country. There are few local and national associations that

were organized as an offshoot of this congress. One national association is the Federation of

Goat and Sheep Producers Association of the Philippines (FGASPAPI) which was funded

through the support of Livestock Development Council and other livestock agencies including

BAI and Central Luzon State University.

The supply chain as applied to the goat industry in the Philippine is a new concept. There have

been either few or no studies that have been done in the goat industry (in the Philippines) on

documenting and assessing the development based on the supply chain approach.

This study looks at documenting and assessing the development of the goat industry along the

supply chain. This study serves as baseline information for the government, private sector and

industry associations to be aware and updated on the development of the industry in the supply

chain. The study will also help them to identify investment opportunities within the goat

agribusiness supply chain that will support the goals and objectives of the Department of

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 3 of 42

Agriculture toward the attaining of food security, poverty alleviation, improve productivity,

increased income and global competitiveness.

II. OBJECTIVES

The main objective of the study is to document and assess the development of the Philippine goat

industry within the supply chain. Specifically, the study aims to: 1) Provide a baseline

documentation of the developments in the Philippine goat industry from input supply,

production, processing, marketing and consumption; 2) Identify the best practices along the

supply chain approach; 3) Develop competitiveness and profitability analysis of chevon; 4)

Advocate improvement for the inefficiencies, gaps and problems encountered by the industry

along the supply chain; and 5) Recommend strategic directions for the Philippine goat industry.

III. METHODOLOGY The study utilized triangulation method in conducting this study. The components of this method

include: archival research, key informant interviews (one-on-one interview, telephone

interviews/mobile/email communications), benchmarking, competitiveness and profitability

analyses. Below is the framework of the study (Please see Figure 1). The sources of data used

in the study were taken from the Bureau of Animal Industry (BAI) and Bureau of Agricultural

Statistics (BAS). Key informant interviews (KII) were conducted with a representative from the

Federation of Goat and Sheep Producers Association of the Philippines, Inc. and key industry

players in meat processing. To supplement the KII, archival research was done in gathering

existing literature and material from BAI Marketing Development Division (BAI-MDD), printed

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 4 of 42

(published or unpublished) and online publications. Benchmarking was done by documenting the

existing best practices of some goat industry players along the supply chain.

IV. RESULTS AND DISCUSSION Supply Chain: Its importance to the Goat Industry Supply Chain is the core business process in any organization that creates and delivers a product

or service, from concept through development and manufacturing or conversion, and into a

market for consumption. It is called as the “seed to shelf” or “breed to plate” or “farm to fork”

approach. The mission of supply chain,5 as a management approach, is the ability of individual

agribusiness firm/establishment or an industry “to enhance the customer’s experience through

excellence in delivering the right products, services, resources and information seamlessly to the

right place at the right time.” The industry focus of supply chain management includes activities

such as integrated behavior, mutual sharing of information, mutual sharing of risk and rewards,

cooperation, same goal and same focus on serving customers, integration of processes,

5 As quoted from the presentation on Supply Chain Management. Ag BM 460.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 5 of 42

partnership in building and maintaining long-term relationships among each industry

stakeholder. According to Price Water Coopers “Nowadays, it is supply chains that compete

with other supply chains!”

The framework of goat industry supply chain is presented below in Annex A, which the

researchers used in analyzing the development of the industry along the supply chain. Based on

this framework, supply chain starts from the input supply, production, processing, marketing and

consumption of products and services produced by the individual agribusiness

firm/establishment or an industry (goat). In between of each segment of the supply chain is the

relevance of logistics (both inbound and outbound) that interconnect the supply chain from input

supply up to the consumption level of sold and delivered goods and services by the industry. On

the agribusiness firm level, the inter-firm linkages will fall into different boxes (Annex A), but

some linkages will be more important for the overall competitiveness and dynamics of the chain

than others. There are also some cases that in each stage, one firm can be forward and backward

integrate to maximize its potential in maximizing the company’s or firm’s profitability and

competitiveness.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 6 of 42

THE GOAT INDUSTRY IN THE PHILIPPINES INPUT SUPPLY

BGoat inventory are increasing by six percent per year

The country’s goat inventory (as of January 1, 2006) was estimated at 3.73 million head, 5.6-

percent higher compared with last year’s headcount.6 Around 38 percent of the goat population

was female breeders, 33 percent were kids, and 29 percent were classified as fatteners and male

breeders. It is important to note that there was an increase of 23% in goat inventory from

January 1, 2003 to January 1, 2007 for an average annual increase of 6% per year. The total

inventory of goat went up from 3,270,441 heads in January 1, 2003 to 4,037,574 heads in

January 1, 2007.

TABLE 1. GOAT: INVENTORY BY FARM TYPE AND BY CLASSIFICATION, PHILIPPINES, JANUARY 1, 2003-2007 (IN HEADS)

2003

(Jan. 1) 2004

(Jan. 1) 2005

(Jan. 1) 2006

(Jan. 1) 2007

(Jan. 1) Backyard 3,255,189 3,340,670 3,514,371 3,708,014 4,007,004 Commercial 15,252 16,954 20,824 26,171 30,570 Total 3,270,441 3,357,624 3,535,195 3,734,185 4,037,574

Source: BAS

On the other hand, Figure 3 shows the top five producing provinces of goat in terms of

inventory. Western Visayas (Region VI) has the most number of goat inventory at 550,431

heads or 15% of the total population. Ilocos Region (Region I) is the second place with 491,435

heads, or 13% of the population. Central Visayas (Region VII) is third with 471,561 heads.

Davao Region is the fourth with the highest inventory at 335,648 heads for 9%. Region IV

(combined CALABARZON and MIMAROPA) is the top five producer of goat at 293,753 heads

at 8%. The small percentage of commercial inventory (not even one percent of the total) of goat

showed that, in general, there are still more effort to be done by the government (DA and

6 Bureau of Agricultural Statistics, Goat Industry Performance Report: January to December 2005, (May, 2006).

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 7 of 42

livestock agencies) and industry associations (particularly FGASPAPI) to encourage goat

farmers to shift from backyard to commercial type of operation to increase and sustain its supply.

Supplier industries are benefiary from the production and processing technology initially adopted by the other livestock commodities The suppliers of the goat industry are those industries, which provide raw material inputs and

processing technology. Raw materials inputs include: breeds, feeds, animal health products and

production technology. Processing technology includes, among others, meat-processing

equipment, packaging materials and other utilities. Since 2001 up to present, more and more

breeder farms are into the business of supplying either imported breed of goat such as Boer,

Saanen, Anglo Nubian, etc., locally borne crossbreed or upgraded goats either from the imported

breed themselves or with the native goats. According to Neo Abalos, the Secretary/Treasurer of

FGASPAPI, and also the head of the goat business of Abalos & Sons Agro Industrial

Corporation, among the different breeder farms of goat, their group have almost already

perfected the crossbreeding of imported breed and upgrading of native and imported goat, to the

extent that they have now a standard size of goat either for breeding or for slaughtering purposes.

FIGURE 3. GOAT: INVENTORY OF TOP PRODUCING REGIONS, PHILIPPINES,

AS OF JANUARY 1, 2006 (IN HEADS)

Region 4Region 11

Region 713%

Region 113%

Region 615%Others

42%

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 8 of 42

Some goat industry stakeholders in the breeding operations has almost perfected the pure breeding crossbreeding, and upgrading operation with standard weight for either breeding or slaughtering purposes Based on their experience, an F1 breed type from purebred imported will give you an estimated

value of P5,000 per head. In every generation, there is an increase of additional peso value of

P5,000. So for F2, it is sold at P10,000 per head while F3, at P15,000 per head, and so on. In

the case of goat feeds, there are some companies that are producing goat feeds, although,

according to him, the goat raising business is not that sensitive to commercial feeds, as goats

normally eat grasses, which they plant as feeds for their goats. In one hectare of land, they can

already pasture and housed at least 100-doe level of different kinds of goats such as imported,

crossbreed and native type. Another advantage of the goat production compared with other

livestock, particularly hog is that, in terms of vaccinating goat or using animal health products,

the goat producers are not too dependent to veterinary health products. Goats are considered as

robust animals. They can easily adopt and survive in Philippine environment free from animal

diseases.

In the Philippines, with the development of the livestock and poultry industry input suppliers,

the goat industry serves as beneficiary for any developments and new trends in the production

and meat processing technology that are being used by other livestock industry commodities.

Although when it comes to artificial insemination (AI) technology, the goat industry, in general,

is not yet adopting this technology in their individual goat farms.

Imported live goats for breeding are increasing but there still more effort to be done to encourage more investment among farmers to shift from backyard to commercial operation to sustain the stable and availability of goat supply There are seven breed type of goats that are being imported as part of the input supply (Please

see Table 2), although only two are the most popular breed type, which are Anglo-Nubian and

Boer. Boer is much larger and efficient meat producer than any other breed of goats (e.g.

Saanen, Anglo-Nubian, etc.). It produced as high as 48 to 60 percent carcass yield compared to

other goat type, which according to one industry player is only from 40 to 43 percent. Data from

the BAI showed that from 2002 to 2006, there are 1,172 Boer types that were imported. On the

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 9 of 42

average, Boer type has been growing by 16 percent per year. Total importation per year during

the same period had been increasing by 72 percent per year. The increase of importation of

imported goat could be attributed to the growing number of local goat farms or breeder farms

that are investing in upgrading and crossbreeding operation of goats. One problem that can be

traced from the importation figure which the researchers gathered is that, there are some goat

importations which are imported at least in two breeds in one shipment that in the declaration of

imports, one breed cannot directly separated from the other. This is the reason why we placed

the notation in Table 2 that says it is “not properly classified.”

Table 2. Imported Goats by Breed Type from 2002 to 2006 (In No. of Heads)

Breed Type 2002 2003 2004 2005 2006 Total African Pygmies 3 0 0 0 0 3 Anglo- Nubian 8 12 9 0 10 39 Boer 112 287 182 383 208 1172 Nigerian Dwarf 3 0 0 0 0 3 Saanen 0 0 0 0 0 0 Spanish Goat 0 3 0 0 0 3 Ten. Fainting 0 3 0 0 0 3 NPC* 0 0 299 947 697 1,943 Total 126 305 490 1330 915 3,166

Source of Basic Data: BAI-NVQS * Not Properly Classified

In terms of country of origin, imported goats came from three countries such as Australia, United

States, and New Zealand. From 2003 to 2006, imported goats from Australia have been

growing by an average of 66 percent per year. On the other hand, imported goats from the

United States had been in the decreasing trend from 2002 to 2006. Total imported goats from

2002 to 2006 were recorded at 3,166 heads (Table 3).

Table 3. Country of Origin of Imported Goats from 2002 to 2006 (In No. of Heads)

Origin 2002 2003 2004 2005 2006 Total Australia 0 223 467 1,304 865 2,859 New Zealand 0 0 0 4 0 4 USA 126 82 23 22 50 303 Total 126 305 490 1,330 915 3,166

Source of Basic Data: BAI-NVQS

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 10 of 42

PRODUCTION Goat Production Performance: Second to the most stable positive growth from 1995 to 2006, although very minimal Total goat volume of production reached 74.82 thousand metric tons liveweight, a decrease of 3.20

percent over 2005 gross output of 77.29 thousand metric tons (Table 4). The average increase in

production of goat, in general, has been increasing only at a minimal of less than one percent per

year, although in terms of other livestock commodities, hog and goats are consistently in the positive

growth per year (Table 4). Aside from hog industry, the goat industry is the second to the most

stable in the volume of production as presented in the Table 4 below from 1999 to 2006. Emerging

growth has been seen in the dairy industry, which has been increasing at an average of four percent

per year since 1999, from the decreased production in 1995 to 1998 by 9.28 percent.

Table 4. Comparison of Livestock Volume of Production (in Thousand Metric Tons)

and Growth Rates from 1995 to 2006

Volume of Production

(1995-1998)

(1999-2002)

(2003-2006) 2005

(In MT) 2006 (MT) % Change Average

GR Average

GR Average

GR Total Volume of

Production 5.35 3.37 1.41 2,241.18 2,296.74 2.48 Carabao (1.18) 3.36 (0.78) 133.52 130.41 -2.33 Cattle 8.77 (1.53) (2.77) 246.75 238.27 -3.44 Hog 5.74 4.38 2.18 1,771.28 1,840.37 3.90 Goat 0.91 0.28 0.71 77.29 74.82 -3.20 Dairy (9.28) 3.95 4.76 12.34 12.87 4.29

Source of Basic Data: BAS Average GR- Growth rate per year

In terms of value of goat production (at constant prices), the same trend could also be observed

in the average yearly growth rates from 1995 to 2006, which is less than five percent per year. In

2006, the total value of production was recorded at P974.16 million (Table 5).

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 11 of 42

Table 5. Comparison of Livestock Value of Production (in constant prices) and Growth Rates from 1995 to 2006

Value of Production

(1995-1998)

(1999-2002)

(2003-2006) 2005

(P Million) 2006

(P Million) % Change Average GR

Average GR

Average GR

Total Value of Production 5.67 3.35 1.39 39,384.58 40,396.74 2.57 Carabao (1.20) 3.36 (0.81) 1,611.59 1,574.05 -2.33 Cattle 8.75 (1.53) (2.76) 4,804.22 4,639.12 -3.44 Hog 5.74 4.38 2.16 31,900.75 33,145.06 3.90 Goat 0.92 0.26 0.62 1,006.32 974.16 -3.20 Dairy (9.32) 3.95 4.76 61.70 64.35 4.29

Source of Basic Data: BAS Average GR- Growth rate per year Major key players have organized themselves into a national federation to consolidate their voices, but the challenge among them is to work further to influence and convince more possible investors/entrepreneurs in the production of goats The major players of the goat and sheep industry are composed of nine member associations of

Federation of Goat & Sheep Producers & Associations of the Philippines, Inc. (Please see Table

6) These associations include the Goat and Sheep Producers of the Philippines, Region IV Small

Ruminants Raisers Association, Misamis Oriental Goat and Sheep Raisers Association,

Zamboanga Peninsula Small Ruminant Council, Cebu Goat and Sheep Raisers Association,

Eastern Visayas Small Ruminant Raisers Association, Masbate Small Ruminants Organization,

SOCKSARGEN Goat and Sheep Raisers Cooperative and Philippine Boers Breeders

Association.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 12 of 42

Table 6. Major Players Association of the Goat and Sheep Industry Name of Association Location Contact Person Email Address

1. Goat and Sheep Producers of the Philippines

Tarlac Jeff Lim [email protected]

2. Region IV Small Ruminants Raisers Association

Region IV Elmer Rivera [email protected]/ [email protected]

3. Misamis Oriental Goat and Sheep Raisers Association

Misamis Oriental Nani Nietes [email protected]

4. Zamboanga Peninsula Small Ruminant Council

Zamboanga Peninsula

Art Grino [email protected]

5. Cebu Goat and Sheep Raisers Association

Cebu Luis Sanchez [email protected]

6. Eastern Visayas Small Ruminants Raisers Association

Eastern Visayas Lito Rodriguez [email protected]

7. Masbate Small Ruminants Organization

Masbate Jose Ataat [email protected]

8. SOCKSARGEN Goat and Sheep Raisers Cooperative

SOCKSARGEN Gauvian Benzonan [email protected]

9. Philippine Boer Breeders Association

Sixto Villaluz [email protected]

Source of Data: FGASPAPI Table 7 shows the selected private goat farms located in different regions. Of the 44 identified

breeder goat farms, 17 farms are located in Region III. Twelve farms are located in Tarlac, two,

in Nueva Ecija; two, in Pampanga; and one, in Bulacan. There are 10 goat farms in Region VIII,

seven in Leyte and three in Ormoc City. The challenge among the members association of

FGASPAPI is to influence and convince more possible investors/entrepreneurs in the production

of goats to further improve the production goat in the country.

Almost around 1 is 2 goat farms/breeding farms are government-owned farms, but their role should support on how to effectively sustain the production of goats at the farm level

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 13 of 42

Table 7. Selected Private Goat Farms by Regions and Provinces/Cities

and the Available Breed Type

Region Province/City No. of Breed/s Available Farm PbB PbAn BxAn UpB UpAn UpS PbS N xS

NCR QC 1 x x x I Pangasinan 2 x x x x x II Isabela 1 x x III Tarlac 12 x x x x x x Nueva Ecija 2 x x x x x x Bulacan 1 x x x x x Pampanga 2 x x x x x IV Rizal 1 x x x x x x Batangas 1 x x x x x Quezon 1 x x x x x VI Bacolod City 1 x VII Mandaue City* 1 VIII Ormoc City 3 x x x x Leyte 7 x x x x x X Malaybalay City* 1 x x Valencia City* 1 XI Gen. Santos City 2 x x x Sultan Kudarat 1 x x Davao del Sur 1 x x Davao City 1 XII Cotabato 1 x x x x Total 44

Source of Basic Data: BAI Legend: PbB –purebred Boer; PbAn – purebred Anglo Nubian; BxAn – crossbreeding of Boer and Anglo Nubian; UpB – upgraded Boer; UpAn -Upgraded Anglo Nubian; UpS – Upgraded Saanen; PbS- Purebred Saanen; xS-crossbreed Saanen; N- native * Not identified

There are 21 identified government breeder goat farms (Please see Table 8) located in most of

the regions of the country. Region III has the most number of farms (4); followed by Region II

(3). Both Regions VII and Region X have two farms. The most prevalent breed both among the

private and government farms are the purebred Boer type. Boer breed could be found in most of

the major goat producing regions (Region VI, Region III, Region XI, Region IV (Table 7) and

Region VII (Table 8).

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 14 of 42

Table 8. Selected Government Goat Farms by Regions and Provinces/Cities

And the Available Breed Type

Region Province/City No. of Breed/s Available Farm PbB PbAn BxAn UpB UpAn UpS PbS N xS

CAR Baguio City 1 x x I Pangasinan 1 x II Tuguegarao City 1 x Nueva Vizcaya 1 x x Isabela* 1 III Pampanga 1 x Nueva Ecija 3 x x x x x IV Laguna 1 x V Masbate 1 x VI Negros Occidental 1 x VII Negros Oriental* 1 Bohol 1 x x VIII Leyte 2 x IX Zamboanga del Sur 1 x x Basilan 1 x X Misamis Oriental* 1 Bukidnon 1 x XII North Cotabato 1 x x Total 21

Source of Basic Data: BAI Legend: PbB –purebred Boer; PbAn – purebred Anglo Nubian; BxAn – crossbreeding of Boer and Anglo Nubian; UpB – upgraded Boer; UpAn -Upgraded Anglo Nubian; UpS – Upgraded Saanen; PbS- Purebred Saanen; xS-crossbreed Saanen; N- native * Not identified

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 15 of 42

PROCESSING

Goat Products

Goat products and by-products are many and varied.7 The main products are milk and meat (chevon).

According to Southard (2003), the name chevon or goat meat was taken from the French word for

goat, chevre is said to be an excellent flavor similar to beef and venison. Goat milk is used essentially

for the same purposes as cow or carabao milk such as fresh milk, cheese, ice cream, and butter.

Also, because of the milk’s high Vitamin A content, it is increasingly being used in the manufacture

of cosmetics. Goats when properly slaughtered, cleaned, and butchered, can be a source of unique

and delectable meat, which may be used in a wide array of dishes. Goat meat has high water-holding

capacity. As such, it is also a good raw material for processing into different products. By-products,

especially skins, are likewise valuable when processed into leather. Other minor by-products such as

intestines, horns, and hair are processed into high-valued articles and art objects.

Pasteurization of Goat Milk

The fundamental purpose of pasteurization is to ensure that milk is free from disease-producing

microorganisms, with the secondary effect of prolonging the keeping quality of the product.

However, pasteurization does not compensate for the failure to apply recommended sanitary

practices in the production of milk and should not be regarded as the cure-all for poor sanitary

practices in the handling and care of milk.

Slaughtering

The recommended ages for slaughtering goats are between eight months up to two years, although

there are some major goat producers, which subscribe to the idea that to experience the optimum

quality of chevon from either imported crossbreed or upgraded native, slaughtering goats starting

7 The Philippines Recommends for Goat Farming, “Product and By-Product Processing and Utilization,” pp. 85-95.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 16 of 42

from 9 to 10 months and up to 18 months only is most appropriate and highly recommended age.

Going beyond the said age of goat, chevon odor (goaty smell) will be more noticeable. At 9 to 10

months, crossbreed goat can have a weight of at least 30 kilos already. Also, it is recommended that

before slaughtering the goat, it should not allow the breeding bucks to mix with the females and the

castrated male to avoid the goaty smell in the carcass. Fast the goats first, give plenty of water for

18-24 hours, and allow them to relax. This is for ease in evisceration and cleaning of entrails.

Moreover, expected results in goat meat are longer shelf life and low shrinkage. Prior to the actual

start of slaughtering, wash off dirt from the goat’s body to prevent contamination of the carcass.

During slaughter, do not allow the hair to rub against the flesh because it imparts objectionable odor

and flavor to the meat. The following are the average wholesale yield (Ibarra, 1988) of the different

cuts of chevon, with the above fabrication system. With the slaughter weight of 18.97 kg, you can get

a dressing percentage of 43.16% and boneless recovery of 32.33%.

TABLE 9. PERCENT OF CARCASS OF THE DIFFERENT CUTS OF CHEVON

Cut Percent of Carcass Leg 29.21 Loin 13.33 Rib 15.76 Neck 7.15 Shoulder 12.10 Whole carcass 100.00

As to the assessment of conformation and quality of chevon, these are not yet available

from the Philippine Standards.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 17 of 42

Goat By-Products

From unpublished data (Ibarra, 1988), the by-product yields of goats are as follows: TABLE 10. BY-PRODUCTS YIELDS OF GOATS

By-Product Weight Slaughter weight, kg 14.81 Blood, g 602 Spleen, g 23 Compound stomach, g 600 Head (uncleaned), g 1,101 Head (cleaned), g 1,067 Hide, g 1,169 Shank (uncleaned), g 404 Shank (cleaned), g 312 Heart, g 60 Kidney, g 53 Intestines, g 775

Goatskins

Goatskins can be processed both on industrial scale and on cottage industry level. The size of

the skin allows it to be processed in small batches or singly in the backyard. In the rural areas, it

is very easy to process the skins even after slaughter for as long as there are readily available

technologies/recipes at hand for the farmers. There is more value when goatskin is converted into

leather, as when it is consumed on the table.

The characteristics of goatskins are: 1) they are generally thinner in substance compared with

cattle hide, carabao hide, and sheep skin. Even then, the fiber structure is tighter; 2) It has a

natural stretch, making it ideal for the manufacture of upper leather when made into leather

shoes. The leather of goats make the shoe durable which, in effect, stays longer serviceable; 3)

Its tough, hard-wearing grain is a basic property looked into when making shoe uppers and for

fancy leather goods such as purses, wallets, and bookbinding leather; 4) Unlike sheepskins,

goatskins have significantly low fat content. The fat usually interferes in the processing, so in

goatskins, decreasing techniques are eliminated. In addition, the tighter fiber structure is not

disoriented when fat is extracted; therefore, it retains its strength and tight grain.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 18 of 42

Phases of Goatskin Processing

Marketing of Goatskins

Traditionally, hides and skins are sold to tanneries either as raw wet salted or freshly flayed on

the proximity of the tannery from the slaughterhouse, farm, or buying stations. In areas where

tanneries are not easily accessible, skins are sold to hide dealers who in turn sell to tanneries in

wet-salted conditions. Goatskins are sold on a per piece basis. On the other hand, in the tannery

business, finished leather finds market in the footwear/leather craft industry depending on the

type of leather produced and demand of consumers. The following are guidelines in the

marketing of skins: 1) Sell only freshly flayed or properly salted and dried skin. Adopt

recommended flaying procedures and use appropriate tools and equipment in flaying the carcass.

Properly flayed skin commands better prices in tanneries; 2) Sell skins on per kilogram or per

piece basis; and 3) Sort and classify the skins according to grade.

Grading of Goatskins

First Grade Skins. The skins are of pattern; check pieces trimmed back to length not exceeding

7.5cm. Nose, crown, or top of the headpieces is removed, leaving the skin cut-off square

between the cheeks. The shanks are trimmed square at the knee joint. The skins are likewise free

from obvious grain damage, cuts, torn skins, and slippiness. The skin should be clean pelted.

Skins from fallen animals are not included in this grade.

Second Grade Skins. Include cut skins and misshapen skins. The skins are free from torn,

excessive holes, and slippiness. Skins from downers are not included in this grade.

Third Grade Skins. Skins do not conform to the requirements for first or second grade skins.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 19 of 42

MARKETING Market Centers

The market centers for the cattle and the carabaos are usually in the accredited livestock

“oksyon” markets (LOM) of the Bureau of Animal Industry (BAI), but there are livestock

auction markets in some part of the country where goats are also sold which make the different

livestock “oksyon” markets vital in the marketing of goats in the countryside. About 90-95

percent of livestock markets are being used for goat trading. There are about 156 LOMs spread

strategically all over the Philippines (Please see Table 11). Most of the non-operational livestock

markets are either due to lack of transaction, peace and order situation in the area, or they have

converted the facilities into other economic and livestock-related activities (e.g. slaughterhouse,

feed mill, etc.) The top five regions with the most number of operational LOMs are Western

Visayas (33), Central Visayas (26), Southern Tagalog (12), Ilocos Region & Central Mindanao

(9), and Cagayan Valley and Bicol Region (4). The ranking of the top three regions with the

most number of non-operational livestock markets are located in Ilocos (7), Central Luzon (6)

and Southern Tagalog, Western Visayas, and Western Mindanao (4).

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 20 of 42

Table 11. Operation and Non-operational Livestock “Oksyon Market” in the Philippines,

As of December 2006

Region No. of Accredited Livestock Markets Total Percent Share of Accredited Operational Non-operational to total by Region

CAR 1 0 1 0.64 Ilocos 9 7 16 10.26 Cagayan Valley 4 2 6 3.85 Central Luzon 1 6 7 4.49 Southern Tagalog 12 4 16 10.25 CALABARZON 10 2 12 7.69 MIMAROPA 2 2 4 2.56 Bicol 4 3 7 4.49 Western Visayas 33 4 37 23.72 Central Visayas 26 3 29 18.59 Eastern Visayas 11 1 12 7.69 Western Mindanao 1 4 5 3.21 Northern Mindanao 3 3 6 3.85 Southern Mindanao 1 2 3 1.92 Central Mindanao 9 1 10 6.41 CARAGA 1 0 1 0.64 ARMM 0 0 0 0.00 Total 116 40 156 100.00 Percent Share 74.36 25.64 100

Source of Basic Data: BAI-MDD

Historical trend of supply and disposition of goat

Total supply of live goats in 2005 was estimated at 5.95 million head, 6.98 percent higher than

last year's level (Table 12). The growth in the supply of goat was indicated by the increment in

beginning stocks and in the number of live births, which grew by 5.29 percent and 9.53 percent,

respectively. Of the total supply, 34.7 percent were disposed for meat purposes and about 2.60

percent accounted for deaths and losses. Total number of goats slaughtered posted an increase of

7.30 percent compared with the 2004 level. It was recorded at 2.0 million heads in 2005.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 21 of 42

TABLE 12. GOAT: SUPPLY AND DISPOSITION, PHILIPPINES, 2003-2005 (NUMBER OF LIVE ANIMALS IN ‘000 HEAD)

ITEMS 2003 2004 2005 %Change 05/04 TOTAL SUPPLY 5,354,842 5,563,242 5,951,759 6.98 Beginning Inventory 3,270,441 3,357,624 3,535,195 5.29 Born Alive 2,084,090 2,205,128 2,415,244 9.53 Imports 311 490 1,320 169.39 Disposition 1,997,218 2,028,047 2,217,574 9.35 Slaughtered 1,892,548 1,922,072 2,062,290 7.3 Death/Losses 104,670 105,975 155,284 46.53 Ending Inventory 3,357,624 3,535,195 3,734,185 5.63

Source: BAS, BAI

Historical trend of prices by market of Goat Products

The annual average farm gate price of live goat in 2005 was Php 65.43 per kilogram (Please see

Table 13). This was lower than the previous year’s price of Php 65.68 per kilogram. The highest

average farm gate price in 2005 was registered during the month of November at Php

67.71/kilogram. This was 4.85 percent lower compared with the price in the same period in

2004. On the other hand, the lowest farm gate price was recorded during the month of December

at an average of Php 57.60/kilogram or 20.45 percent lower than last year's level. Please see also

Figure 4.

TABLE13. GOAT: MONTHLY FARM GATE PRICE (PHILIPPINES) (P/KG.)LIVE WEIGHT)

MONTH FARMGATE PRICE (Live weight) PHILIPPINES Percent Change

2003 2004 2005P 04/03 05/04 Pesos/ Kg. January 58.05 55.51 64.42 (4.38) 16.05 February 57.97 57.34 64.50 (1.09) 12.49 March 58.50 55.38 65.00 (5.33) 17.37 April 58.93 64.55 65.17 9.54 0.96 May 58.74 65.46 65.91 11.44 0.69 June 58.81 65.93 65.44 12.11 (0.74) July 58.46 69.35 66.22 18.63 (4.51) August 57.57 69.43 66.60 20.60 (4.08) September 58.49 70.00 67.61 19.68 (3.41) October 60.18 70.71 66.98 17.50 (5.28) November 58.55 71.16 67.71 20.92 (4.85) December 62.58 72.41 57.60 15.71 (20.45) Annual Ave. 58.85 65.68 65.43 11.61 (0.38)

Source: BAS

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 22 of 42

Live goats are retailed also in some areas in Metro Manila, particularly in some part of Quezon

City, Caloocan City, and Manila, to name some. The live goat prices monitoring in Metro Manila

started in 2003 which is being done by BAI-MDD up to the present while the chevon and other

cuts prices monitoring started in 1999. This activity has been doing by the Bureau of Animal

Industry as part of their support to the goat industry. From 2003 to 2006, the average price on a

per kilo basis of goat has been increasing per year by 3.58 percent. In 2006, average price of live

goat was recorded at P117.71/kg or 1.50 percent higher than 2005 of P115.97/kg.

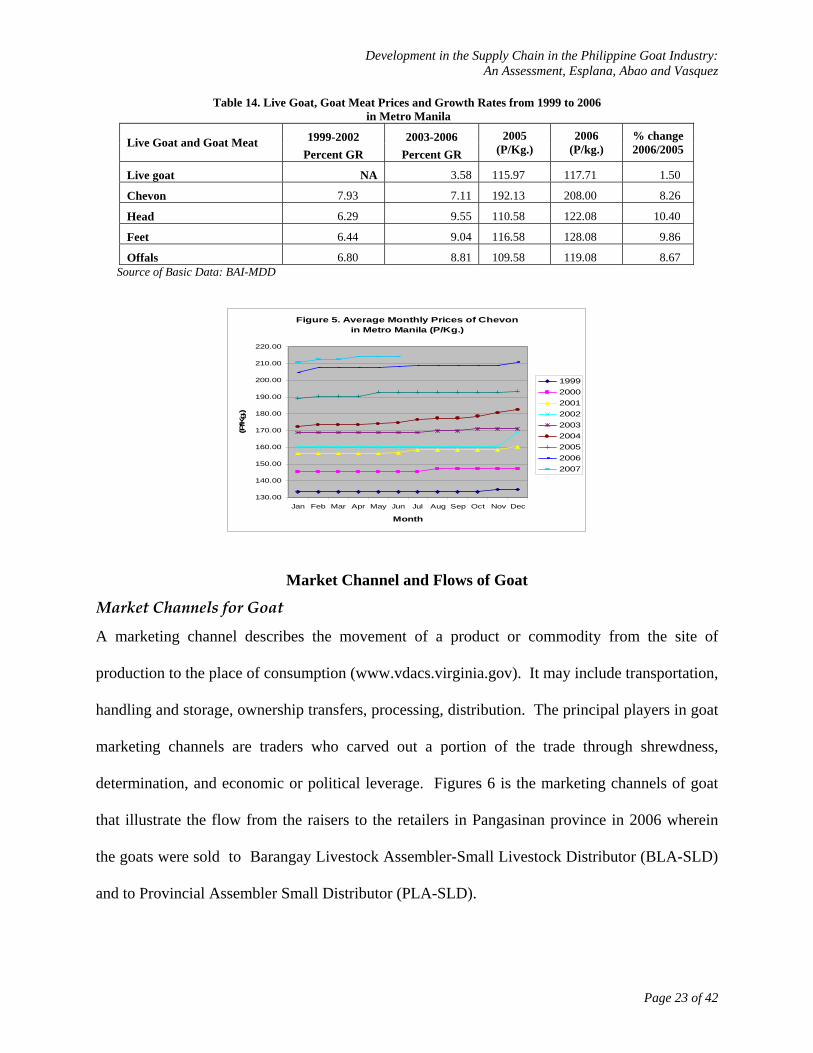

One important observation that we can get from the goat prices are the increasing growth on the

average prices per year of chevon from 1999 to 2006 by more than seven percent per year

(Please see Table 14 & Figure 5). Last year, the average price of chevon went to P208/kg or

8.26-percent higher over 2005. Other part of goat meat such as head, feet and offals had been

increasing by an average of 6.29, 6.44 and 6.80 percent per year, respectively, from 1999 to

2002. The growth is even higher than chevon (7%) for the three cuts from years 2003 to 2006

such 9.55 percent for head, 9.04 percent for feet, and 8.81 percent for offals. The average prices

of the three cuts in 2006 were posted at P122.08/kg for head; P128.08/kg for feet and P119.08/kg

for offals.

FIGURE 4. GOAT: FARM GATE PRICE, (IN PESO LIVEWEIGHT)

PHILIPPINES, 2003-05)

-

1 0 .0 0

2 0 .0 0

3 0 .0 0

4 0 .0 0

5 0 .0 0

6 0 .0 0

7 0 .0 0

8 0 .0 0

nuary

bruary

Marc

hApril

May

June

July

ugust

ember

tober

ember

ember

Pric

e in

PhP

/kg

Live

wei

ght

2 0 0 3 2 0 0 4 2 0 0 5 P

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 23 of 42

Table 14. Live Goat, Goat Meat Prices and Growth Rates from 1999 to 2006 in Metro Manila

Live Goat and Goat Meat 1999-2002 2003-2006 2005 (P/Kg.)

2006 (P/kg.)

% change 2006/2005 Percent GR Percent GR

Live goat NA 3.58 115.97 117.71 1.50

Chevon 7.93 7.11 192.13 208.00 8.26

Head 6.29 9.55 110.58 122.08 10.40

Feet 6.44 9.04 116.58 128.08 9.86

Offals 6.80 8.81 109.58 119.08 8.67 Source of Basic Data: BAI-MDD

Figure 5. Average Monthly Prices of Chevon in Metro Manila (P/Kg.)

130.00

140.00

150.00

160.00

170.00

180.00

190.00

200.00

210.00

220.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Month

(P/K

g.)

199920002001200220032004200520062007

Market Channel and Flows of Goat

BMarket Channels for Goat

A marketing channel describes the movement of a product or commodity from the site of

production to the place of consumption (www.vdacs.virginia.gov). It may include transportation,

handling and storage, ownership transfers, processing, distribution. The principal players in goat

marketing channels are traders who carved out a portion of the trade through shrewdness,

determination, and economic or political leverage. Figures 6 is the marketing channels of goat

that illustrate the flow from the raisers to the retailers in Pangasinan province in 2006 wherein

the goats were sold to Barangay Livestock Assembler-Small Livestock Distributor (BLA-SLD)

and to Provincial Assembler Small Distributor (PLA-SLD).

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 24 of 42

Both types of assembler-distributors brought the animals to the livestock “oksyon” markets

(LOMs) where buyers outside the province and retailers converge. Suppliers outside the

province (SOP) supplied livestock to Inter-Regional Assembler-Large Distributor (IRLA-LLD)

who disposed the ruminants to retailers. From the retailers, meats were sold to the final

consumers.

BFIGURE 6. MARKETING CHANNELS FOR GOATS IN PANGASINAN, 2006

R A IS E R /O P E R A T O R S O P

B L A -S L D

IR L A -L L DB O P

R E T A IL E R

C O N S U M E R

P L A -S L D

Geographic Flow for Goats

Figures 7-8 show the sources and destination points of goats in some areas.8 They illustrate

the flow of goat by location and by province. In Batangas, the major sources of goats were

Lemery, Batangas City, Bauan, and Calatagan. Goats from these areas and from the

provinces of Quezon, Bicol, and Cavite were assembled at the trading centers of Tanauan

City, Batangas City, Lemery, and Padre Garcia.

From these trading centers, livestock were marketed within the province. These were also

sold and brought to the market outlets outside Batangas such as Cavite and Metro Manila.

8 BAS Marketing Costs Structure for Goat (October 2003), “Geographic Flow,” pp. 4-13.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 25 of 42

BFIGURE 7. GEOGRAPHIC FLOW OF GOAT IN BATANGAS, 2006

D E S T I N A T I O N S

L I V E S T O C K

“ O K S Y O N ”

M A R K E T S

S O U R C E S

B A T A N G A ST a n a u a n C i t y

B a t a n g a s C i t yL e m e r y

P a d r e G a r c i a

M E T R O M A N I L AR E G I O N 1P a n g a s i n a n

R E G I O N 5B i c o l

R E G I O N 4 AB a t a n g a s

C a v i t eQ u e z o n

R E G I O N 4 AB a t a n g a s

C a v i t e

BFIGURE 8. GEOGRAPHIC FLOW OF GOAT IN METRO MANILA, 2006

D E S T I N A T I O N S

T R A D I N G C E N T E R S

S O U R C E S

M E T R O M A N I L AQ u e z o n C i t y M a r i k i n a

M a k a t i C i t y M a n i l a

R E G I O N 5M a s b a t e

R E G I O N 7C e b u

M E T R O M A N I L AQ u e z o n C i t y M a r i k i n a

M a k a t i C i t y M a n i l a

R E G I O N 6B a c o l o d

I l o i l o

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 26 of 42

CONSUMPTION Importation and Exportation of Goat Meat

The Philippines has no record or is not importing goat meat from other countries because we are

self-sufficient in goat meat. Actually, the Philippines has a big potential to export goat meat in

other countries such as the Middle East Countries, particularly, Saudi Arabia and United Arab

Emirates where many Overseas Filipino Workers are working. The goat meat is universally

consumed which are also important in everyday diet in Middle East countries. It is usually

roasted and prepared in accordance with religious beliefs. Some other countries, which are

potential market of our goat meat exports, include Taiwan, Malaysia, Singapore, United States,

and Caribbean, to name some.

Marketing assistance provided to the industry

BDA One-Stop Agribusiness Center (OSAC)

A lot of marketing assistance is provided to the ruminants’ industry. The recent initiative is the

creation of DA of a One-Stop Agribusiness Center (OSAC). OSAC is a virtual mini-mart;

exhibit area, agribusiness information hub, and a training-seminar room rolled into one. At

OSAC, producers and buyers can meet conveniently and forge mutual and hopefully lasting

marketing arrangements. It has an exhibit area where the producers can showcase their fresh and

processed products for the appreciation of prospective Filipino and foreign buyers, and the

general public, as well. OSAC adopts an “exhibit theme” once every two or three months,

coinciding with the regular agriculture-related events (such as Farmers’ and Fisher folk’s Month

in May, and World Food Day in October, etc.) or anniversary celebration of respective DA

Family agencies. In the OSAC training and seminar room, producers and buyers can meet

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 27 of 42

regularly to discuss pressing industry developments, forge marketing agreements, plan

participation, in domestic and international food fair and trade missions, and discuss strategies to

further prop up the competitiveness of Philippine agribusiness. The center aims to facilitate and

strengthen the direct linkages among industry players – all to increase their productivity and

incomes, and expand the domestic and export markets for Philippine farm, fishery, and food

products.

BAI’s National Task Force on Price and Volume Watch

In terms of the support by BAI, MDD regularly hosts a monthly meeting for key public and

private sector participants in the livestock and poultry industry. This is the meeting of the

National Task Force on Price and Volume Watch, a monthly formal gathering of key players in

the livestock and poultry industry. Through this meeting, market matching are initiated and

policies affecting the industry are being created and being recommended to the DA Secretary.

The DA-Agribusiness and Marketing Assistance Service (AMAS) is also involved in market-

matching as it maintains directories of key players in the industry.

Participation of Associations in the Development of the Goat Industry

The Federation of Goat & Sheep Producers & Associations of the Philippines, Inc. has also been

helping the industry since 2001. During May 2001, the 1st National Goat and Sheep Congress in

Nueva Ecija was held. This goat federation consolidated the many voices of the country’s goat

and sheep raisers and serves as the unified voice of the small ruminant sub-sector. FGASPAPI is

recognized as the official representative of the small ruminant industry, as it complements an

active conduit in the development and implementation of programs of the Department of

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 28 of 42

Agriculture. It is also a member of the Livestock Development Council and National Agriculture

and Fishery Council consultation meeting. The address of the Federation is located at 198 M.

Paterno St. San Juan Metro Manila with contact no. 7246994 and email address:

PRICE COMPETITIVENESS ANALYSIS

Price competitiveness analysis is an analysis that compares price of local chevon and the prices

of chevon in other country such as in this case, US, Australia, and Canada. The Philippines is

price competitive to imported goat meat in the current FOB price of $US4 to 5 per kilo of chevon

in Canada at either 30 to 35 percent in-quota tariff rates, at $45 exchange rate (Appendix A).

The table shows that import parity over domestic wholesale price is greater than one. At the

price lower than $US4 to 5 per kilo of chevon, assuming it will be $US 3.0 per kilo for the

Australia goat meat, and assuming that there will be a price quotation that will be like this, the

Philippines is still price competitive. Even if it moves to $US3.5/kg, the Philippine goat meat

will still be competitive (Appendix C).

The scenario of having $3.3 kilo price of goat meat in Canadian market already happened during

2004. This was based on the report of AgVentures, Agriculture Business Profiles of Alberta

Agriculture Food and Rural Development in April 2006. This price will not go back again but

rather will continue to increase further as they estimated it at $ 0.15/kg.increase per year due to

higher demand of goat meat not only in Canada, but also the Middle East, Caribbean, Taiwan,

Malaysia, Singapore, Italy, Greece, and United States. Except in the Middle East, the population

or goat meat eaters in those countries are either came from the ethnic groups located primarily in

Metropolitan areas (predominantly males), the middle to high class wage earners (niche market)

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 29 of 42

group or the health conscious individuals. The average retail price of chevon in Metro Manila,

as of May 2007, was posted at P214/kg. with the price ranges from P195 to P240/kg.

T a b l e 1 5 . A v e r a g e R e t a i l P r i c e s * o f C h e v o n a n d B y - p r o d u c t s , M a y 2 0 0 7

(In P/Kg.)

SELLER/DEALER CHEVON HEAD FEET OFFAL LIVE Average 214.00 130.50 136.50 123.50 120.00 Prevailing 200.00 120.00 120.00 110.00 125.00 Lowest 195.00 120.00 120.00 110.00 110.00 Highest 240.00 145.00 170.00 140.00 125.00

*Price quotations from goat sellers/ dealers and wet markets in Metro Manila Source: Marketing Development Division, BAI

The comparison of local imported chevon is presented below which indicates that local is

slightly cheaper than imported Australian chevon. The Philippines is price competitive with the

United States (Appendix B). US chevon is one of the most expensive chevon in the world (Table

16).

Table 16. Comparison of Local Chevon, Landed Cost of Imported and Wholesale Price In Metro Manila (P/kg.)

Chevon Comparative Prices Landed Cost Wholesale Price Philippine local chevon 200* 215 Australian chevon (imported) 202.58 231.8 212.7 243.4 US chevon (imported) 414.93 479.16 435.68 503.12

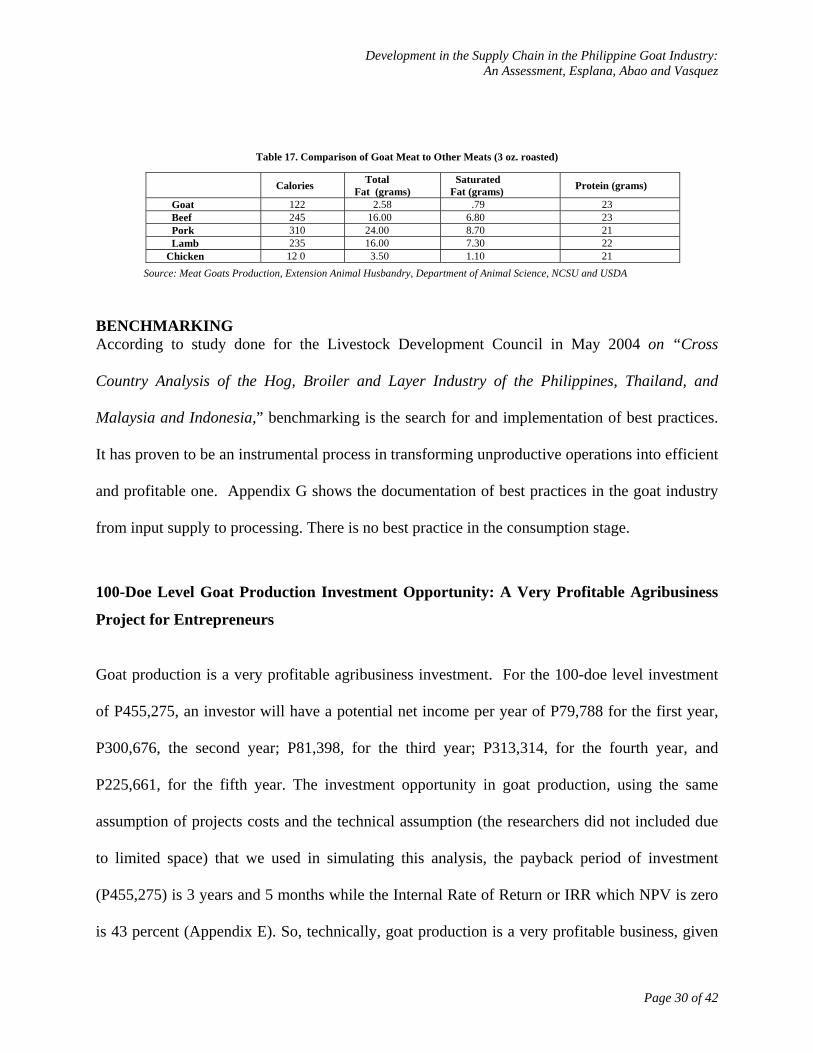

Source: Interview and online quotation price *Prevailing Price Comparison of Goat Meat to Other Meat with 3 oz. roasted in terms of Calories, Total Fat, Saturated Fat and Protein Based on study made by Meat Goats Production, Extension Animal Husbandry, Department of

Animal Science, NCSU, given the similar 3 oz. roasted for the different animal specie, goat has

the lowest calorie, total fat, and saturated fat content. Also, it has higher protein content of 23

grams. This study of NCSU showed that goat meat product is the healthiest meat, among all the

animal specie compared in this study (Table 17).

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 30 of 42

Table 17. Comparison of Goat Meat to Other Meats (3 oz. roasted)

Source: Meat Goats Production, Extension Animal Husbandry, Department of Animal Science, NCSU and USDA

BENCHMARKING According to study done for the Livestock Development Council in May 2004 on “Cross

Country Analysis of the Hog, Broiler and Layer Industry of the Philippines, Thailand, and

Malaysia and Indonesia,” benchmarking is the search for and implementation of best practices.

It has proven to be an instrumental process in transforming unproductive operations into efficient

and profitable one. Appendix G shows the documentation of best practices in the goat industry

from input supply to processing. There is no best practice in the consumption stage.

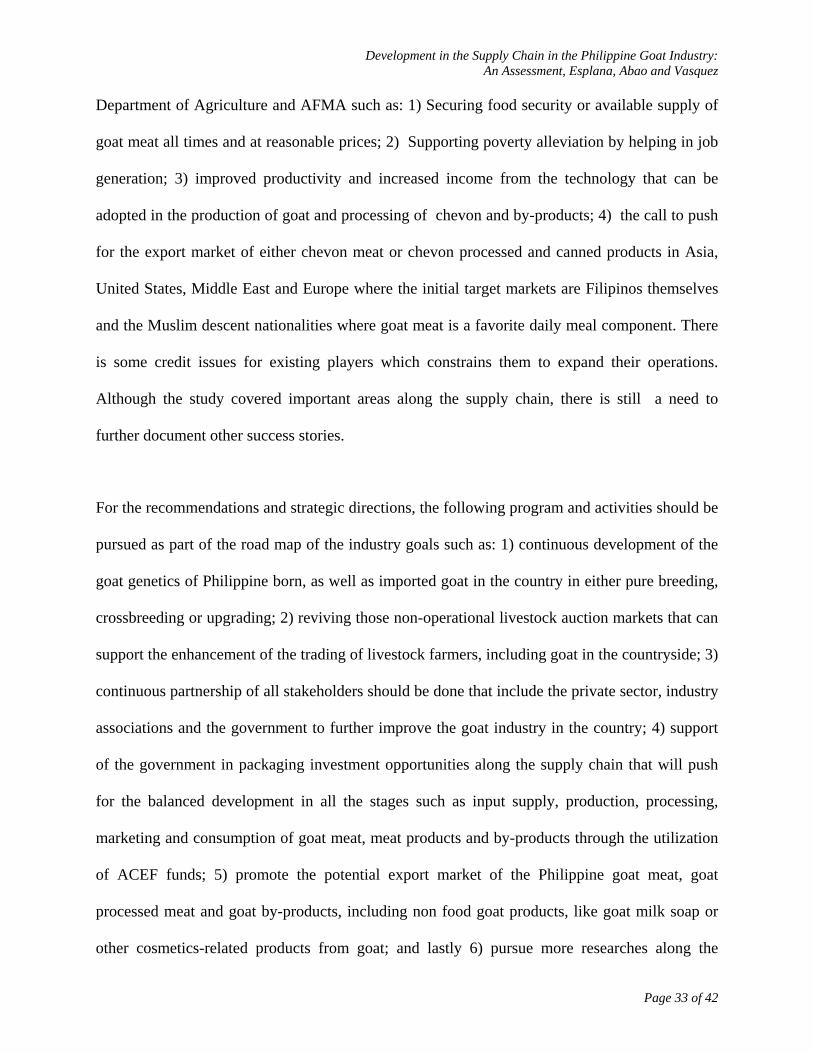

100-Doe Level Goat Production Investment Opportunity: A Very Profitable Agribusiness

Project for Entrepreneurs

Goat production is a very profitable agribusiness investment. For the 100-doe level investment

of P455,275, an investor will have a potential net income per year of P79,788 for the first year,

P300,676, the second year; P81,398, for the third year; P313,314, for the fourth year, and

P225,661, for the fifth year. The investment opportunity in goat production, using the same

assumption of projects costs and the technical assumption (the researchers did not included due

to limited space) that we used in simulating this analysis, the payback period of investment

(P455,275) is 3 years and 5 months while the Internal Rate of Return or IRR which NPV is zero

is 43 percent (Appendix E). So, technically, goat production is a very profitable business, given

Calories Total Fat (grams)

Saturated Fat (grams) Protein (grams)

Goat 122 2.58 .79 23 Beef 245 16.00 6.80 23 Pork 310 24.00 8.70 21 Lamb 235 16.00 7.30 22 Chicken 12 0 3.50 1.10 21

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 31 of 42

this financial analysis. Appendix D shows the breakdown of project costs while Appendix E

shows the Income Statement of the potential investment in goat production project and the net

income analysis.

V. CONCLUSION AND RECOMMENDATIONS The study presented the development of the goat industry along the supply chain. For the input

supply, the good development is the increasing number of breeder farms that are propagating

purebred, crossbreed or upgraded goats in different parts of the country. The goat industry is

beneficiary for any developments in the raw materials sourcing, and both the production and

processing technology being adopted by other livestock commodities, particularly hogs and

chicken.

In production, the establishment of a unified voice of the goat industry through the Federation of

Goat and Sheep Producers Association of the Philippines is an additional development, which

support in the policy advocacy and lobbying for the interest of the industry. They are also

helping in whatever they can, to improve the genetic and breeding practices of the goat industry

players by regularly conducting national congress in support of the livestock agencies of the

Department of Agriculture. This became the venue for collaborating among the industry

stakeholders such as the private sector, industry associations but even the government agencies

both local and national.

In the processing side, new development, as well as best practices could also be seen in terms of

two pioneer companies such as the canning of goat meat products through the Fortress Food

Manufacturing Corporation and manufacturing of goat milk soap in four variants through the

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 32 of 42

initiative of Golden Farm International Trading Company. Golden Farm International, aside

from being a farm, is also into the Research & Development of goat milk soap products, which

the Filipinos should patronize and be proud of. In terms of marketing, there are some success

stories in the trading operation of goat as well as the support of two biggest livestock “oksyon”

market in the Philippines, one is in Padre Garcia, Batangas and the other one is in Urdaneta,

Pangasinan.

In terms of consumption, goat meat or its products are proven to be the healthiest meat, among

other livestock and poultry meat products based on the study done in the United States. There is

also a big potential for the Philippines to export chevon to other countries, given the price

competitiveness of Philippine goat meat with Australia, United States, and Canada (Appendix A-

C).

The profitability analysis also showed that goat production, in general, is a very profitable

agribusiness investment. For the 100-doe level, the IRR is 43 percent and the payback period is 3

years and 5 months (Appendix E).

In terms of inefficiencies and problems of the industry, the study found that the goat inventory

although increasing at 6 percent per year should be improved to much higher level (10 percent

or higher, particularly the commercial farms) by either encouraging & challenging more Filipino

entrepreneurs to invest in the goat production or helping the farmers to shift from backyard

operation to commercial operation, given the potential profitability that can be derived from

commercial operations (Appendix E & F). This will also support the goals and objectives of the

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 33 of 42

Department of Agriculture and AFMA such as: 1) Securing food security or available supply of

goat meat all times and at reasonable prices; 2) Supporting poverty alleviation by helping in job

generation; 3) improved productivity and increased income from the technology that can be

adopted in the production of goat and processing of chevon and by-products; 4) the call to push

for the export market of either chevon meat or chevon processed and canned products in Asia,

United States, Middle East and Europe where the initial target markets are Filipinos themselves

and the Muslim descent nationalities where goat meat is a favorite daily meal component. There

is some credit issues for existing players which constrains them to expand their operations.

Although the study covered important areas along the supply chain, there is still a need to

further document other success stories.

For the recommendations and strategic directions, the following program and activities should be

pursued as part of the road map of the industry goals such as: 1) continuous development of the

goat genetics of Philippine born, as well as imported goat in the country in either pure breeding,

crossbreeding or upgrading; 2) reviving those non-operational livestock auction markets that can

support the enhancement of the trading of livestock farmers, including goat in the countryside; 3)

continuous partnership of all stakeholders should be done that include the private sector, industry

associations and the government to further improve the goat industry in the country; 4) support

of the government in packaging investment opportunities along the supply chain that will push

for the balanced development in all the stages such as input supply, production, processing,

marketing and consumption of goat meat, meat products and by-products through the utilization

of ACEF funds; 5) promote the potential export market of the Philippine goat meat, goat

processed meat and goat by-products, including non food goat products, like goat milk soap or

other cosmetics-related products from goat; and lastly 6) pursue more researches along the

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 34 of 42

supply chain which are market-driven and customer focused. These researches will serve as

good input for all stakeholders, particularly the private sector, industry associations and the

government themselves, to better improve their policy and business decisions.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 35 of 42

Appendix A. Price Competitiveness of Locally Produced Goat Meat and Imported Goat Meat in Canada at Different Price Quotation, Different Tariff Rates, Same Exchange Rates, Same Domestic Wholesale Price

At Different Price Quotation (FOB), Tariff Rates and Same Exchange Rates

Carcass, half- Carcass, half- Carcass, half- Carcass, half- Carcasses, and frozen Carcasses, and frozen Carcasses, and frozen Carcasses, and frozen

Price/Kilo Price/Kilo Price/Kilo Price/Kilo

At 30% in-quota tariff At 30% in-quota tariff At 35% in-quota tariff At 35% in-quota tariff

(Per MT) (Per Kg) (Per MT) (Per Kg)

FOB Price (US$ per MT)* 4,000.00 4.00 5,000.00 5.00 4,000.00 4.00 5,000.00 5.00 Freight and Insurance (US$) 450.00 0.45 450.00 0.45 450.00 0.45 450.00 0.45

CIF Manila ($) 4,450.00 4.45 5,450.00 5.45 4,450.00 4.45 5,450.00 5.45 Times Foreign Exchange rate 45.00 45.00 45.00 45.00

CIF Manila (Php) 200,250.00 200.25 245,250.00 245.25 200,250.00 200.25 245,250.00 245.25 Plus Tariff Rate % 0.30 0.30 0.35 0.35

Tariff Cost (Php) 60,075.00 60.08 73,575.00 73.58 70,087.50 70.09 85,837.50 85.84 Plus Handling Distribution Cost (HDC) 750.00 0.75 750.00 0.75 750.00 0.75 750.00 0.75

Total Landed Cost (Php) 261,075.00 261.08 319,575.00 319.58 271,087.50 271.09 331,837.50 331.84 Plus Trading Cost/Margins (TC/M) at 5% 13,053.75 13.05 15,978.75 15.98 13,554.38 13.55 16,591.88 16.59

Domestic Wholesale Import Parity Price (Php) 274,128.75 274.13 335,553.75 335.55 284,641.88 284.64 348,429.38 348.43

Domestic Wholesale Price (Php)^ 200,000.00 200 200,000.00 200 200,000.00 200 200,000.00 200

Import Parity/Domestic Wholesale 1.37 1.68 1.42 1.74 * FOB price quotation, as of May 2007 ^ As of May 2007 Note: Competitiveness exists if import parity/domestic wholesale price is greater than 1.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 36 of 42

Appendix B. Price Competitiveness of Locally Produced Goat Meat and Imported US Goat Meat at Different Price Quotation, Different Tariff Rates, Same Exchange Rates, Same Domestic Wholesale Price

At Different Price Quotation (FOB), Tariff Rates and Exchange Rates

Carcass, half- Carcass, half- Carcass, half- Carcass, half- Carcasses, and frozen Carcasses, and frozen Carcasses, and frozen Carcasses, and frozen

Price/Kilo Price/Kilo Price/Kilo Price/Kilo

At 30% in-quota tariff At 30% in-quota tariff At 35% in-quota tariff At 35% in-quota tariff

(Per MT) (Per Kg) (Per MT) (Per Kg) (Per MT) (Per Kg) (Per MT)

(Per Kg)

FOB Price (US$ per MT)* 6,580.00 6.58 7,678.00 7.68 6,580.00 6.58 7,678.00 7.68 Freight and Insurance (US$) 500.00 0.50 500.00 0.50 500.00 0.50 500.00 0.50 CIF Manila ($) 7,080.00 7.08 8,178.00 8.18 7,080.00 7.08 8,178.00 8.18 Times Foreign Exchange rate 45.00 45.00 45.00 45.00 CIF Manila (Php) 318,600.00 318.60 368,010.00 368.01 318,600.00 318.60 368,010.00 368.01 Plus Tariff Rate % 0.30 0.30 0.35 0.35

Tariff Cost (Php) 95,580.00 95.58 110,403.00 110.40 111,510.00 111.51 128,803.50 128.80 Plus Handling Distribution Cost (HDC) 750.00 0.75 750.00 0.75 750.00 0.75 750.00 0.75 Total Landed Cost (Php) 414,930.00 414.93 479,163.00 479.16 430,860.00 430.86 497,563.50 497.56 Plus Trading Cost/Margins (TC/M) at 5% 20,746.50 20.75 23,958.15 23.96 21,543.00 21.54 24,878.18 24.88 Domestic Wholesale Import Parity Price (Php) 435,676.50 435.68 503,121.15 503.12 452,403.00 452.40 522,441.68 522.44 Domestic Wholesale Price (Php)^ 200,000.00 200 200,000.00 200 200,000.00 200 200,000.00 200 Import Parity/Domestic Wholesale Price 2.18 2.52 2.26 2.61 * FOB price quotation, as of May 2007 ^ As of May 2007 Note: Competitiveness exists if import parity/domestic wholesale price is greater than 1.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 37 of 42

Appendix C. Price Competitiveness of Locally Produced Goat Meat and Australian Imported Goat Meat at Different Price

Quotation, Tariff Rates, Exchange Rates, and Same Domestic Wholesale Price

At Different Price Quotation (FOB), Tariff Rates and Exchange Rates

Carcass, half- Carcass, half- Carcass, half- Carcass, half- Carcasses, and frozen Carcasses, and frozen Carcasses, and frozen Carcasses, and frozen

Price/Kilo Price/Kilo Price/Kilo Price/Kilo

At 30% in-quota tariff At 30% in-quota tariff At 35% in-quota tariff At 35% in-quota tariff

(Per MT) (Per Kg) (Per MT) (Per Kg) (Per MT) (Per Kg) (Per MT)

(Per Kg)

FOB Price (US$ per MT)* 3,000.00 3.00 3,500.00 3.50 3,000.00 3.00 3,500.00 3.50 Freight and Insurance (US$) 450.00 0.45 450.00 0.45 450.00 0.45 450.00 0.45 CIF Manila ($) 3,450.00 3.45 3,950.00 3.95 3,450.00 3.45 3,950.00 3.95 Times Foreign Exchange rate 45.00 45.00 45.00 45.00 CIF Manila (Php) 155,250.00 155.25 177,750.00 177.75 155,250.00 155.25 177,750.00 177.75 Plus Tariff Rate % 0.30 0.30 0.35 0.35

Tariff Cost (Php) 46,575.00 46.58 53,325.00 53.33 54,337.50 54.34 62,212.50 62.21 Plus Handling Distribution Cost (HDC) 750.00 0.75 750.00 0.75 750.00 0.75 750.00 0.75 Total Landed Cost (Php) 202,575.00 202.58 231,825.00 231.83 210,337.50 210.34 240,712.50 240.71 Plus Trading Cost/Margins (TC/M) at 5% 10,128.75 10.13 11,591.25 11.59 10,516.88 10.52 12,035.63 12.04 Domestic Wholesale Import Parity Price (Php) 212,703.75 212.70 243,416.25 243.42 220,854.38 220.85 252,748.13 252.75 Domestic Wholesale Price (Php)^ 200,000.00 200 200,000.00 200 200,000.00 200 200,000.00 200 Import Parity/Domestic Wholesale 1.06 1.22 1.10 1.26 * FOB price quotation, as of May 2007 ^ As of May 2007 Note: Competitiveness exists if import parity/domestic wholesale price is greater than 1.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 38 of 42

Appendix D. Goat Production Projects Costs and Distribution of Equity and Loan (for the 100-Deo level)

Goat Production Project Costs (Amount In Peso) Percentage (%) share

Housing & Equipment 50,000 10.98 Fencing 80,000 17.57 Forage & Pasture Development 20,000 4.39 Prepaid Expenses 50,000 10.98 Stocks Doe (100) 175,000 38.44 Buck (4) 24,000 5.27 Working Capital 56,275 12.36 Total 455,275 100

Distribution of Equity and Loan for the Project

Equity 236,275 52 Loan 219,000 48 Total 455,275 100

Appendix E. Investment Decision & Profitability Analysis

Investment Decision & Profitability Analysis Year 1 Year 2 Year 3 Year 4 Year 5 Gross Profit Per Year (In Peso) 149,750 489,578 152,227 509,022 374,170 Operating Profit Margin (In %) 0.40 0.65 0.41 0.68 0.65 Net Income per year (In Peso) 79,788 300,676 81,398 313,314 225,661

Net Income per month (In Peso) 6648.96

25,056.33

6,783.14

26,109.50

18,805.04

Net Profit Margin per year (In %) 0.21

0.40

0.22

0.42

0.39 Net Present Value at 12% Discount Rate 476,308 Net Present Value at 15% Discount Rate 402,981 Payback Period 3 years & 5 months Internal Rate of Return 43%

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 39 of 42

Appendix F. Projected Income Statement Under Pure Confinement System for 100-Doe Level Projected Income Statement, Years 1-5

Projected Income Statement Under Pure Confinement System for 100-Doe Level Projected Income Statement, Years 1-5

Particulars Project Year Year 1 Year 2 Year 3 Year 4 Year 5

A. Sales Revenues Sale of Stocks 374,850 749,500 374,850 749,500 374,850 Inventory Value of Stocks 199,000 Total Sales Revenues 374,850 749,500 374,850 749,500 573,850 B. Direct Expenses Operating Expenses (OE) Labor 109,500 109,500 109,500 109,500 109,500 Cost of Concentrate 40,680 63,360 40,680 63,360 40,680 Veterinary Drug & Supply 10,700 16,400 10,700 16,400 10,700 Forage & Pasture Maintenance 0.00 4,000 4,000 4,000 4,000 Light & Water 6,000 6,000 6,000 6,000 6,000 Transportation 5,000 5,000 5,000 5,000 5,000 Repair & Maintenance 0.00 10,000 10,000 10,000 10,000 Land Rental 13,800 13,800 13,800 13,800 13,800 Interests on Loans 39,420 31,862 22,943 12,418 0 Total Operating Expenses 225,100 259,922 222,623 240,478 199,680 C. Operating Income 149,750 489,578 152,227 509,022 374,170 Amortization (F&PD) 4,000 4,000 4,000 4,000 4,000 Amortization (Prepaid Expenses) 10,000 10,000 10,000 10,000 10,000 Depreciation 13,000 13,000 13,000 13,000 13,000 Total Indirect Expenses 27,000 27,000 27,000 27,000 27,000 D. Earnings Before Taxes (EBT) 122,750 462,578 125,227 482,022 347,170 Taxes (35% of EBT) 42,963 161,902 43,830 168,708 121,510 D. Net Income 79,788 300,676 81,398 313,314 225,661

Note: This study prepared detailed Financial Analysis that include Cash Flow and Balance Sheet and the assumption used in doing this financial plan of a 100-doe level goat production module, but will not present fully all the documents due to availability of space. This analysis is only a simulation, which shows that goat production is a very profitable agribusiness opportunity.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 40 of 42

Appendix G. Best Practices in the Different Stages in the Supply Chain

Stages in the Supply

Chain Activities Pioneering Organization/Company/Contact

Person Location of

Agribusiness Establishment

Coverage of Operation Innovation/Creativity/Potential Income Made

Input Supply/ Production

Pure breeding, crossbreeding and upgrading of goat Imported Goat raising

Goat raising

Abalos & Sons Agro Industrial Corp. Head Goat Business, Neo Abalos Ex-Congressman Carlos Padilla Jr. Ketti Chua

Pangasinan Rizal Batangas Isabela Nueva Vizcaya

Cebu City

Breeding & Trading of Livestock Crossbreed native goat with imported goat Boer, Saanen, 400-doe level Crossbreeding of Boer, Africa; Anglo Nubian, Saanen from United States Boer, Anglo Nubian, and Red Boer from Australia

Profit is at P1000 to 2000 per marketable goat for slaughter sold. The selling price of crossbreed goat breeder (F1) is at P5000 per head F2 at 10,000 per head and F3 at 15,000. The higher the level, the higher the profit. 200 purebred and crossbreed breeders of the three types of breeds. Selling price of Purebred bucks, 40,000 per head Sold at P40,000 to P60,000 per head of imported breeder goat.

Processing Development of Processed Chevon Canned Products

Fortress Food Manufacturing Corporation Amelia Coronel, General Manager Golden Farm International Trading Company

Antipolo City Farm site: San Rafael, Bulacan Novaliches

Processed canned chevon such as Chevon Strew, Chevon in Tamarind Soup and Chevon Offals Soup Manufacturing of goat milk soap with variant such as whitening goat milk soap, regular goat milk soap, premium goat milk soap, and sensitive skin goat milk soap

Pioneer in processing canned chevon, initially for local market and eyeing to tap the export market in the coming days, when accreditation requirement has been completed. First goat Halal certified complete processing line from slaughtering to canning. Pioneer in manufacturing goat milk soap from locally produced goat milk.

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 41 of 42

Marketing Livestock Trading Operation Livestock Auction Market Operations

Junar Mejia Padre Garcia LOM Mayor Prudencio V. Gutierrez Urdaneta City LOM Mayor Amadeo Perez

Tara St.., Masbate City, Masbate Padre Garcia, Batangas Brgy. Anonas, Urdaneta City, Pangasinan

Bicol Region , Metro Manila Batangas, Mindoro, Masbate, Bicol Main commodity traded are cattle, carabao, and goat

Major livestock trader of goat in Masbate for Metro Manila market.

One of the best LOMs in the country. The biggest livestock market throughout the country in terms of volume (about 96,200 heads yearly) and income (at least P3.55 million annually). Ninety percent (90%) of the income of the municipality are derived from the LOM. 1,850 animal traded per week Of which 70%, cattle; 20%, carabao, 10% combined horses and other animals.

Revenue of P180,000 to P200,000 comes from animal fees while P35,000 comes from about 35 stalls that are operating within the LOM.

550-600 heads traded cattle per week, 400 heads, carabao; and 140 heads, goats per week.

Source: Interviews & BAI-Livestock Handlers Database 2006.

Annex A. Goat Industry Supply Chain Framework

Input Supply Production Marketing Processing Consumption

Development in the Supply Chain in the Philippine Goat Industry: An Assessment, Esplana, Abao and Vasquez

Page 42 of 42

REFERENCES Alberta Agriculture, Food and Rural Development. Ag-Ventures: Agriculture Business

Profiles. Revised April 2006. Agriculture Magazine. July 2007. Agricultural Utilization Research Institute (AURI). The Feasibility of Meat Goats in

Minnesota: Summary Report. AURI. 1501 State Street Marshall, MN. 56258. Hhttp://www.auri.org. January 20, 2001.

Bureau of Animal Industry. BAI Goat Marketing Bulletin. July 2002. Bureau of Animal Industry. Marketing Development Division Database on Goat

Industry 1999 to 2006. Bureau of Animal Industry. Marketing Development Division Livestock Handlers

Database 2006. Bureau of Agricultural Research. Call for Papers: 19th DA-BAR National Research

Symposium. May 9, 2007. Bureau of Agricultural Statistics. Goat Industry Performance Report: January to

December 2005. May 2006. Bureau of Agricultural Statistics. Marketing Costs Structure for Goat. October 2003. Cluny Exports PTY LTD Agribusiness Specialist. Exporting Australia’s best livestock to

the world. http://www.clunyexports.com.au/?gclid=CMn__Ljf9Y0CFQ-WbgodliBLLQ#.

Esplana, Elmer R. Lary Nel. B. Abao, Cyril L. Soliaban and Fermin M. Diaz. Is RP Ready for the Bird Flu? Socio-economic Impact and Lessons Learned from the Calumpit Incident. June 2006.

Esplana, Elmer. R. Cyril L. Soliaban, Renelle Revilla, Maria Alilia G. Maghirang, and Stevenson S. Ang. Hog Industry Cluster and Analysis: Trends and Emerging Development in the Philippines, FSM 103 Paper submitted to University of Asia and the Pacific in 2005.

Humprey, John. Shaping Value Chains for Development: Global Value Chains in Agribusiness. Deutsche Gesellschaft (GTZ). Federal Ministry for Economic Cooperation and Development. http://www.gtz.de.