Determining the “TRUE COST” of Low Income Customers

30

©1997 Lenhardt & Colton LLC Stephen D. Colton Lenhardt & Colton, LLC 1775 Magnolia Ln N Minneapolis, MN 55441 Ph (612) 550-0687 *** Fax (612) 550-0776 [email protected] Determining the “TRUE COST” of Low Income Customers

-

Upload

raya-walls -

Category

Documents

-

view

28 -

download

1

description

Determining the “TRUE COST” of Low Income Customers. Stephen D. Colton Lenhardt & Colton, LLC 1775 Magnolia Ln N Minneapolis, MN 55441 Ph (612) 550-0687 *** Fax (612) 550-0776 [email protected]. Workshop Objective. - PowerPoint PPT Presentation

Transcript of Determining the “TRUE COST” of Low Income Customers

©1997 Lenhardt & Colton LLC

Stephen D. ColtonLenhardt & Colton, LLC

1775 Magnolia Ln N Minneapolis, MN 55441Ph (612) 550-0687 *** Fax (612) 550-0776

Determining the “TRUE COST” ofLow Income Customers

©1997 Lenhardt & Colton LLC

Workshop Objective

Demonstrate How One UsesActivity Based Costing

to Determine the “True Cost” of Serving Low Income Customers

©1997 Lenhardt & Colton LLC

Definition

“True Cost” means there is a direct causal link between costs incurred and our cost objective, the Low Income Customer market segment.

©1997 Lenhardt & Colton LLC

Today’s Agenda

• Why Do We Need to Know the True Cost of Serving Low Income Customers?

• Why Turn to “Activity Based Costing”?

• Structuring an ABC Project• Analyzing the Data• Using Activity Based Data for

Continuous Improvement.

©1997 Lenhardt & Colton LLC

Why Do We Need to Know?

The Public Policy Question:“How Big is the Aggregate Need?”

The Question for an Individual Utility:“How Do We Live Within the Subsidy?”

©1997 Lenhardt & Colton LLC

How Big is the Aggregate Need?

$1,000,000?$1,000,000?

$20,000,000?$20,000,000?

$500,000,000?$500,000,000?

©1997 Lenhardt & Colton LLC

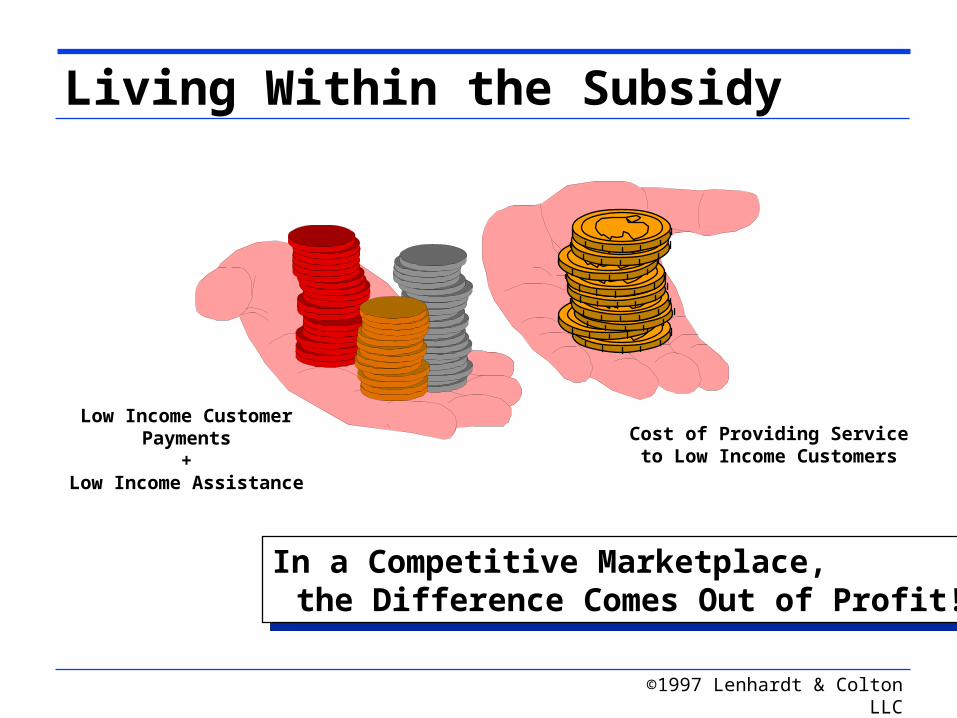

Living Within the Subsidy

Low Income Customer Payments

+Low Income Assistance

Cost of Providing Service to Low Income Customers

In a Competitive Marketplace, the Difference Comes Out of Profit!

In a Competitive Marketplace, the Difference Comes Out of Profit!

©1997 Lenhardt & Colton LLC

• Why Do We Need to Know the True Cost of Serving Low Income Customers?

• Why Turn to “Activity Based Costing”?

• Structuring an ABC Project• Analyzing the Data• Using Activity Based Data for

Continuous Improvement.

Today’s Agenda

©1997 Lenhardt & Colton LLC

Traditional Data Tells Us What???

Description Plan Actual VarianceSalaries & Benefits 500$ 575$ (75)$ Postage 75 80 (5) Telephone 50 45 5 Building Occupancy 25 25 - Other Supplies 20 50 (30) Transfers 50 40 10 903- Customer records & collection expenses

720$ 815$ (95)$

©1997 Lenhardt & Colton LLC

Activity Based Data Reveals Causes

Description Plan Actual VarianceAnswer Customer Inquiries 140$ 165 (25) Resolve Billing Errors 115 120$ (5)$ Apply Customer Payments 75 75 - Negotiate Deferred Pmt Plans 115 110 5 Disconnect Customer Service 255 320 (65) Attend Weekly Staff Meetings 20 25 (5) Total 720$ 815$ (95)$

Cause of Costs

• Normal Credit & Collections Activities

- Qty of Credit & Collections “Actions”

- Current Credit & Collections Process

• High Arrearages at End of Winter

©1997 Lenhardt & Colton LLC

ActivitiesActivities

The Process Model

External CustomersExternal Customers

SuppliersSuppliers

Internal CustomersInternal Customers

Resources ConsumedPeople Costs $$$

Supplies $$$Deprec $$$

Inputs

Outputs

©1997 Lenhardt & Colton LLC

Hierarchy of “Process Terms”

Business Process

Activity

Tasks

Activity Output

Review Application

Run Credit Report

Assign Customer Number

Perform Data Entry

Send Confirmation

1. Setup New Account 2. Connect new service 3. Issue first billing

Initiate New Customer Service

Confirmation Letter

©1997 Lenhardt & Colton LLC

• Why Do We Need to Know the True Cost of Serving Low Income Customers?

• Why Turn to “Activity Based Costing”?

• Structuring an ABC Project• Analyzing the Data• Using Activity Based Data for

Continuous Improvement.

Today’s Agenda

©1997 Lenhardt & Colton LLC

Steps of the ABC Process

1. Identify Activiti

es

2. Trace Costs to Activitie

s

3. Identify Outputs

5. Calc Cost per Output

4. Collect

Demand for

Outputs

6. Calc Market Segment Cost

©1997 Lenhardt & Colton LLC

Step 1: Define Activities

Interviews

Workshops

©1997 Lenhardt & Colton LLC

The APQC Business Process Model

Develop & Manage Human Resources

Manage Information

Manage Financial & Physical Resources

Execute Environmental Management Program

Manage External Relations

Manage Improvement & Change

Understand Markets & Customers

Develop Vision & Strategy

Design Goods & Services

Market & Sell Goods & Services

Produce & Deliver

Goods & Services

Invoice & Service

Customer

Man

ag

em

en

t &

Su

pp

ort

Pro

cess

es

Op

era

tin

g P

roce

sses

©1997 Lenhardt & Colton LLC

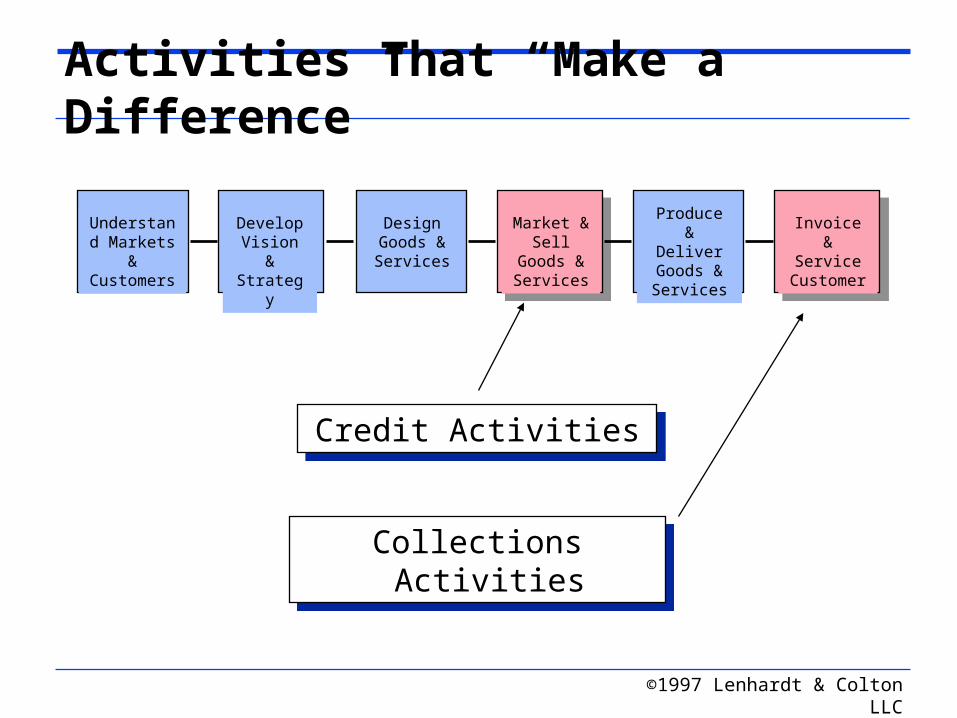

Activities That “Make a Difference”

Understand Markets

& Customers

Develop Vision & Strategy

Design Goods & Services

Market & Sell

Goods & Services

Produce & Deliver

Goods & Services

Invoice & Service

Customer

Credit ActivitiesCredit Activities

Collections ActivitiesCollections Activities

©1997 Lenhardt & Colton LLC

Example of Collections Activities

Collections Activities

• Answer Customer Inquiries

• Resolve Billing Errors

• Apply Customer Pmts

• Negotiate Deferred Payment Plans

• Disconnect Customer Service

• Attend Staff Meetings

Collections Activities

• Answer Customer Inquiries

• Resolve Billing Errors

• Apply Customer Pmts

• Negotiate Deferred Payment Plans

• Disconnect Customer Service

• Attend Staff Meetings

©1997 Lenhardt & Colton LLC

Step 2: Trace Costs to Activities

Description ActualAnswer Customer Inquiries 165$ Resolve Billing Errors 120 Apply Customer Payments 75 Negotiate Deferred Pmt Plans 110 Disconnect Customer Service 320 Attend Weekly Staff Meetings 25 Total 815$

Description ActualAnswer Customer Inquiries 165$ Resolve Billing Errors 120 Apply Customer Payments 75 Negotiate Deferred Pmt Plans 110 Disconnect Customer Service 320 Attend Weekly Staff Meetings 25 Total 815$

Description ActualSalaries & Benefits 575$ Postage 80 Telephone 45 Building Occupancy 25 Other Supplies 50 Transfers 40 903- Customer records & collection expenses

815$

Description ActualSalaries & Benefits 575$ Postage 80 Telephone 45 Building Occupancy 25 Other Supplies 50 Transfers 40 903- Customer records & collection expenses

815$

©1997 Lenhardt & Colton LLC

Step 3: Identify Outputs

Description Actual Activity OutputAnswer Customer Inquiries 165$ One Resolved InquiryResolve Billing Errors 120 One Corrected ErrorApply Customer Payments 75 One Applied PaymentNegotiate Deferred Pmt Plans 110 One Negotiated PlanDisconnect Customer Service 320 One Customer DisconnectionAttend Weekly Staff Meetings 25 One Attended Staff MeetingTotal 815$

Description Actual Activity OutputAnswer Customer Inquiries 165$ One Resolved InquiryResolve Billing Errors 120 One Corrected ErrorApply Customer Payments 75 One Applied PaymentNegotiate Deferred Pmt Plans 110 One Negotiated PlanDisconnect Customer Service 320 One Customer DisconnectionAttend Weekly Staff Meetings 25 One Attended Staff MeetingTotal 815$

©1997 Lenhardt & Colton LLC

Step 4: Collect Demand for Outputs

• Projected Aggregate Annual Demand for each Activity’s Output

• Projected or Actual Demand for each Activity’s Output by Market Segment

©1997 Lenhardt & Colton LLC

Aggregate Annual Demand

Description Actual Activity Output Annual DemandAnswer Customer Inquiries 165$ Resolved Inquiry 4000 InquiriesResolve Billing Errors 120 Corrected Error 55000 CorrectionsApply Customer Payments 75 Applied Payment 600000 ApplicationsNegotiate Pmt Plans 110 Negotiated Plan 800 PlansDisconnect Service 320 Customer Disconnection 2900 DisconnectionsAttend Weekly Staff Mtgs 25 Attended Staff Meeting 48 Staff MeetingsTotal 815$

Description Actual Activity Output Annual DemandAnswer Customer Inquiries 165$ Resolved Inquiry 4000 InquiriesResolve Billing Errors 120 Corrected Error 55000 CorrectionsApply Customer Payments 75 Applied Payment 600000 ApplicationsNegotiate Pmt Plans 110 Negotiated Plan 800 PlansDisconnect Service 320 Customer Disconnection 2900 DisconnectionsAttend Weekly Staff Mtgs 25 Attended Staff Meeting 48 Staff MeetingsTotal 815$

©1997 Lenhardt & Colton LLC

Output Demand by Market Segment

Description Annual DemandLow Income

Demand

NotLow Income

DemandAnswer Customer Inquiries 4000 Inquiries 250 3750Resolve Billing Errors 55000 CorrectionsApply Customer Payments 600000 ApplicationsNegotiate Pmt Plans 800 Plans 705 105Disconnect Service 2900 DisconnectionsAttend Weekly Staff Mtgs 48 Staff Meetings Support ActivityTotal

Description Annual DemandLow Income

Demand

NotLow Income

DemandAnswer Customer Inquiries 4000 Inquiries 250 3750Resolve Billing Errors 55000 CorrectionsApply Customer Payments 600000 ApplicationsNegotiate Pmt Plans 800 Plans 705 105Disconnect Service 2900 DisconnectionsAttend Weekly Staff Mtgs 48 Staff Meetings Support ActivityTotal

©1997 Lenhardt & Colton LLC

Step 5: Calculate Cost per Output

Description Actual Annual Demand Cost / OutputAnswer Customer Inquiries 165$ 4000 Inquiries 42.50$ Resolve Billing Errors 120 55000 Corrections 2.25$ Apply Customer Payments 75 600000 Applications 0.129$ Negotiate Pmt Plans 110 800 Plans 141.60$ Disconnect Service 320 2900 Disconnections 113.65$ Attend Weekly Staff Mtgs 25 48 Staff Meetings n/aTotal 815$

Description Actual Annual Demand Cost / OutputAnswer Customer Inquiries 165$ 4000 Inquiries 42.50$ Resolve Billing Errors 120 55000 Corrections 2.25$ Apply Customer Payments 75 600000 Applications 0.129$ Negotiate Pmt Plans 110 800 Plans 141.60$ Disconnect Service 320 2900 Disconnections 113.65$ Attend Weekly Staff Mtgs 25 48 Staff Meetings n/aTotal 815$

©1997 Lenhardt & Colton LLC

Step 6: Calculate Market Segment Cost

Description Cost / OutputLow Income

DemandLow Income

Segment CostAnswer Customer Inquiries 42.50$ 250 10,600$ Resolve Billing Errors 2.25$ 5000 11,300$ Apply Customer Payments 0.129$ 54000 7,000$ Negotiate Pmt Plans 141.60$ 705 99,800$ Disconnect Service 113.65$ 1650 187,500$ Attend Weekly Staff Mtgs n/a n/a n/aTotal 316,200$

Description Cost / OutputLow Income

DemandLow Income

Segment CostAnswer Customer Inquiries 42.50$ 250 10,600$ Resolve Billing Errors 2.25$ 5000 11,300$ Apply Customer Payments 0.129$ 54000 7,000$ Negotiate Pmt Plans 141.60$ 705 99,800$ Disconnect Service 113.65$ 1650 187,500$ Attend Weekly Staff Mtgs n/a n/a n/aTotal 316,200$

©1997 Lenhardt & Colton LLC

Today’s Agenda

• Why Do We Need to Know the True Cost of Serving Low Income Customers?

• Why Turn to “Activity Based Costing”?

• Structuring an ABC Project• Analyzing the Data• Using Activity Based Data for

Continuous Improvement.

©1997 Lenhardt & Colton LLC

Analyzing the Data

• Total Cost of the Low Income Market Segment

• Differential Cost of the Low Income Segment

• Normalizing the Data- Cost/Sales Ratio- Cost/Customer Ratio- A Caution

©1997 Lenhardt & Colton LLC

• Why Do We Need to Know the True Cost of Serving Low Income Customers?

• Why Turn to “Activity Based Costing”?

• Structuring an ABC Project• Analyzing the Data• Using Activity Based Data for

Continuous Improvement.

Today’s Agenda

©1997 Lenhardt & Colton LLC

Strategies for Continuous Improvement

1. Reduce Costs of Value Added Activities using Root Cause Analysis

2. Reduce the Frequency of Non-Value Added Activities

©1997 Lenhardt & Colton LLC

Description ActualAnswer Customer Inquiries 165$ Resolve Billing Errors 120 Apply Customer Payments 75 Negotiate Deferred Pmt Plans 110 Disconnect Customer Service 320 Attend Weekly Staff Meetings 25 Total 815$

Description ActualAnswer Customer Inquiries 165$ Resolve Billing Errors 120 Apply Customer Payments 75 Negotiate Deferred Pmt Plans 110 Disconnect Customer Service 320 Attend Weekly Staff Meetings 25 Total 815$

Applying These Strategies

Strategy #1Largest dollar Value Added Activity.Use Root Cause Analysis to identify the

Cost Drivers and reduce them, improving the Cost per Output.

Strategy #1Largest dollar Value Added Activity.Use Root Cause Analysis to identify the

Cost Drivers and reduce them, improving the Cost per Output.

Strategy #2A Non-Value Added Activity.Reduce the number of Non-Value

Added Outputs by reducing the “demand” for those outputs.

Strategy #2A Non-Value Added Activity.Reduce the number of Non-Value

Added Outputs by reducing the “demand” for those outputs.