Detecting Common Types of Abuses of Dominance – Experience from Taiwan Lin Gin-Lan Section chief...

32

Detecting Common Types Detecting Common Types of Abuses of Dominance of Abuses of Dominance – Experience from – Experience from Taiwan Taiwan Lin Gin-Lan Lin Gin-Lan Section chief of TFTC Section chief of TFTC

-

Upload

ashley-wells -

Category

Documents

-

view

217 -

download

1

Transcript of Detecting Common Types of Abuses of Dominance – Experience from Taiwan Lin Gin-Lan Section chief...

Detecting Common Types of Detecting Common Types of Abuses of Dominance – Abuses of Dominance –

Experience from TaiwanExperience from Taiwan

Lin Gin-LanLin Gin-Lan

Section chief of TFTCSection chief of TFTC

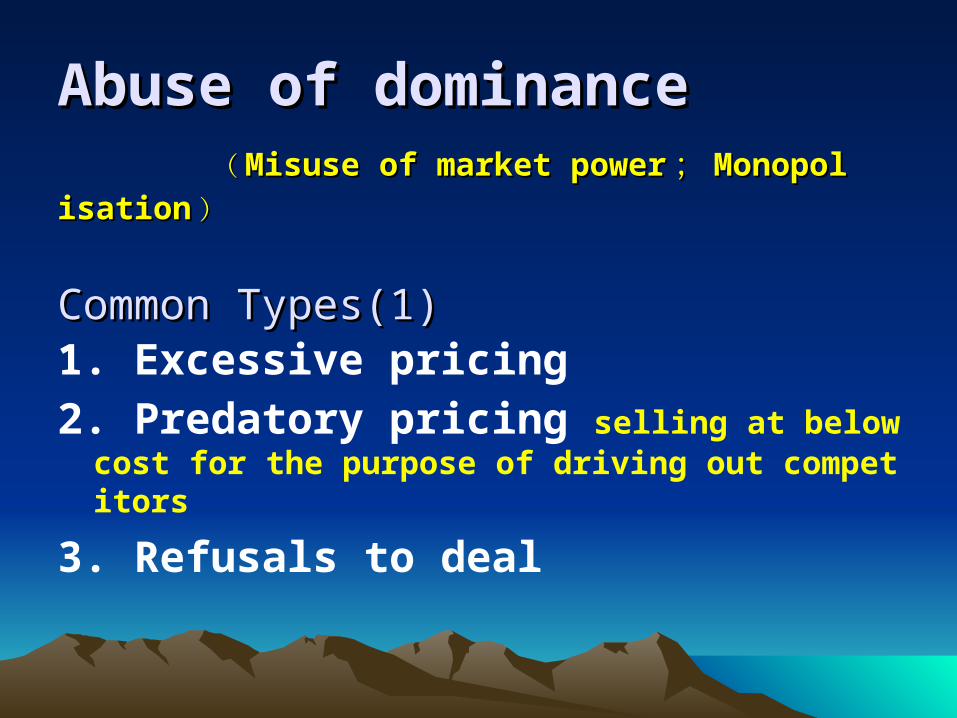

Abuse of dominanceAbuse of dominance (( Misuse of market powerMisuse of market power ;; MonopolisationMonopolisation ))

Common Types(1)Common Types(1)

1. Excessive pricing2. Predatory pricing selling at below cost for the

purpose of driving out competitors

3. Refusals to deal

Common Types(2)Common Types(2)

4. Price discrimination a practice where by a firm charges different customers or classes of customers different prices for the same good for reasons un

related to costs 5. Exclusive dealing requiring a retailer or distri

butor not to sell products competing with the supplier's products

6. Tie-ins

Common Types(3)Common Types(3)

7. Third line forcing requiring purchasers of one product to purchase other products from named suppliers

8. Territorial restrictions the retailer or distributor may not resell outside of a defined territory

9. Customer restrictions the retailer or distributor may only deal with specified customers

10. Resale price maintenance minimum price at which the product may be resold to customers

Analysis of abusing dominanceAnalysis of abusing dominance

• Determining the status of firm• Evaluating the behavior :

Economic analysis

A case of economic analysis A case of economic analysis

with game theorywith game theory • CPC 70% FPCC 30%• Abusing of joint dominance of duopoly gas

oline market• mechanism of joint dominance

- price leadership

- price meeting contract

- advance announcement of a price

change• Static game vs. dynamic game

Static game of pricing strategy Static game of pricing strategy

FPCC

0.5 0.8 1.0

CPC 0.5 (2,2) (4,-2) (6,-4)

0.8 (-2,4) (3,3) (5,-2)

1.0 (-4,6) (-2,5) (4,4)

• Simultaneous moves (payoff form)

Dynamic gameDynamic game of pricing strategy of pricing strategy • sequential moves (game tree) • CPC( first mover ),FPCC( new comer of gasoline market)

Newly types of abusing dominanceNewly types of abusing dominance

• market power evolving from distribution market power evolving from distribution orientationorientation• upstream anti-competition from industryupstream anti-competition from industry

organization perspectiveorganization perspective

A case of newly type of A case of newly type of abusing dominancabusing dominance : SoGo department store vs. branded prode : SoGo department store vs. branded product suppliers which operate outlet store in Souct suppliers which operate outlet store in So

Go Go

1.1. Restriction of outlet stores location on braRestriction of outlet stores location on branded product suppliers (outside a radius nded product suppliers (outside a radius of 2000 meters of SoGo) of 2000 meters of SoGo)

2.2. To create an entry barrier and intend to prTo create an entry barrier and intend to prevent potential competitors from entering event potential competitors from entering the same geographic marketthe same geographic market

3.Relative market position 3.Relative market position

- - 29.54 % market share in Taipei Metropolis 29.54 % market share in Taipei Metropolis

- - NT$19.20 billion of sales in 2001NT$19.20 billion of sales in 2001

- - Superb business location Superb business location

- - 739 of the 766 ( 96.40% )outlets signed the 739 of the 766 ( 96.40% )outlets signed the

disputed restrictive clause disputed restrictive clause

4. Guidelines on trade practices between 4. Guidelines on trade practices between

department store and branded products department store and branded products

supplierssuppliers

Developing Trends in retailing sector (1)

1. scale of chain-store retailing grow rapidly and strengthen its relative dominant position compared to supplier (low costs low sales prices)

2. satisfy consumers with the need of “one-stop shopping”

Developing Trends in retailing sector (2)

3. various promotional programs to stimulate consumption

4. utilize industrialized information technologye-commerce supply chain managementcustomer relations management

5. increasing spot promotional programs in the outlet to stimulate consumption

6. supplier being over-reliant to single retailer

Relevant market in retailing sectorRelevant market in retailing sector 1. supermarkets

- Wellcome - Fressay

2. volume retailers

- Carrefour - Costo

3. convenience stores

- 7-11 - Hi-life 4. department stores(shopping center) - Sogo Department - Breeze shopping center

Types of abuse of an relative dominance Types of abuse of an relative dominance in retailing sector in retailing sector(( 11))

• Improperly charging suppliers additional fees

• Demanding the "most favored" price• Restricting the business area of trading

counterpart• Failing to attribute liability of inventory

shortfall and improperly calculating penalty damage for inventory shortfall

Types of abuse of relative dominance Types of abuse of relative dominance in retailing sector in retailing sector(( 22))

• Failing to articulate the conditions or standards of products return and improperly returning products :

1.return a product without due reasons

2.return a product where the pollution, damage

or expiry is non-fault to the trading counterpart

3.purchase large amount of products with low

price for the promotion, and return at a normal

price after the promotion

Additional Fees (Slotting allowance) Additional Fees (Slotting allowance) charged by chain- store retailer being relativecharged by chain- store retailer being relative dominant position dominant position

1. any kind of fee charged to supplier - secret rebate

- business premises rent subsidy

- promotion fee

- minimum guarantee amount fee

2. any direct deduction from payment account for goods according to supplier agreement

Improperly Charging Additional FeesImproperly Charging Additional Fees

• Fees are not directly related to promoting the sale of the goods

• Amount exceeding the benefit that suppliers may reasonably expect to derive from sale

• Fees are only for the retailers purpose of achieving its own performance target

• Demanding a reduction of purchasing price for already-delivered goods when the supplier is under no obligation

Carrefour case in the year of 2000Carrefour case in the year of 2000

1. The case

Complants alleging Carrefour Corporation‘s

collection of addition slotting allowance, rebates and

patronage grants.

2. Dominace position of carrefour

a. Carefour was established in 1987 and had 23

outlets at that time the alleged disputes occurred.

b. Carrefour had revenues of NT$ 39.77 million in

1999 accounting for 30.75% of the domestic

market

Case summery(1) 1. When suppliers negotiated annual agreements with

Carrefour, the completed agreement consisted of the document drafted unilaterally by Carrefour,including a national agreement with addendum 1 to 3, and a national supplementary agreement. Under the documents, Carrefour was entitled to collect various additional fees from suppliers.

2. A “supplementary fixed rebate” (referred to in the industry as a “secret rebate”) introduced by Carrefour in 1997 is an example of such additional fees ; and it did not directly benefit sales.

Case summery(2)3.The additional fees collected by Carrefour over 1

998 and 1999 amounted to NT$280 million. Hence the dispute clearly involved not just a small but large number of Carrefour’s trading counterparts.

4. Carrefour’s reliance on its relative market position to deny its trading counterparts the freedom to decide whether they would like to accept the additional fees were culpable in terms of commercial ethics, and were sufficient to affect trading order.

Case summery(3) 5. When Carrefour introduced the “supplementary fixed r

ebate transaction clause” into the standard national supplementary agreement drafted unilaterally by Carrefour, as most of the small and medium-sized suppliers were under the pressure to maintain their existing commercial relationship with Carrefour, it had used its relative market power to force the suppiers to accept the additional fees.

6. Carrefour’s conduct was clearly unfair and sufficient to affect trading order in violation of the FTA.Therefore, the commission imposed an administrative fine of NT$4 million on Carrefour.

Fair Trade Commission Guidelines on Fair Trade Commission Guidelines on Additional Fees Charged by Additional Fees Charged by Distribution Businesses Distribution BusinessesPrescribed by the 470th Commissioners' Meeting on November 9, 2000Prescribed by the 470th Commissioners' Meeting on November 9, 2000

1. Purpose of these Principles1. Purpose of these PrinciplesThese Principles have been specially adopted to These Principles have been specially adopted to prevent distribution businesses from abusing prevent distribution businesses from abusing advantageous positions in the market by advantageous positions in the market by improperly charging suppliers additional fees, and improperly charging suppliers additional fees, and thereby to maintain the market trading order and thereby to maintain the market trading order and ensure fair competition. ensure fair competition.

2. Definition of distribution business 2. Definition of distribution business

The term "distribution business" as used in The term "distribution business" as used in these Principles refers to volume retailers, these Principles refers to volume retailers, convenience stores, super/hyper markets, convenience stores, super/hyper markets, department stores, cooperative stores, and all department stores, cooperative stores, and all other businesses engaging in the retail sale of other businesses engaging in the retail sale of assorted goods. assorted goods.

3. Definition of additional fees 3. Definition of additional fees

The term "additional fees" as used in these The term "additional fees" as used in these Principles, with the exception of amounts payable Principles, with the exception of amounts payable for goods by the distribution businesses, refers to for goods by the distribution businesses, refers to fees charged to suppliers by distribution fees charged to suppliers by distribution businesses, or to deductions made from amounts businesses, or to deductions made from amounts payable for goods, or to all kinds of fees payable for goods, or to all kinds of fees demanded of suppliers by distribution businesses demanded of suppliers by distribution businesses by other means. by other means.

4. Factors to be considered in determination 4. Factors to be considered in determination of advantageous market position of advantageous market position

In determining whether a distribution business In determining whether a distribution business holds an advantageous position in the market, the holds an advantageous position in the market, the following factors must be considered: the following factors must be considered: the comparative scales and market shares of the comparative scales and market shares of the distribution business and supplier; the supplier's distribution business and supplier; the supplier's degree of dependence on the distribution business; degree of dependence on the distribution business; the supplier's ability to change its sales channel; the supplier's ability to change its sales channel; and supply of and demand for the goods. and supply of and demand for the goods.

5. Entering into written agreements5. Entering into written agreements

When a distribution business asks a supplier When a distribution business asks a supplier to bear additional fees, it should first negotiate to bear additional fees, it should first negotiate with the supplier with respect to the type of with the supplier with respect to the type of additional fee, its use, and the amount of the additional fee, its use, and the amount of the fee (or the method of its calculation), and fee (or the method of its calculation), and enter into a written agreement with the enter into a written agreement with the supplier.supplier.

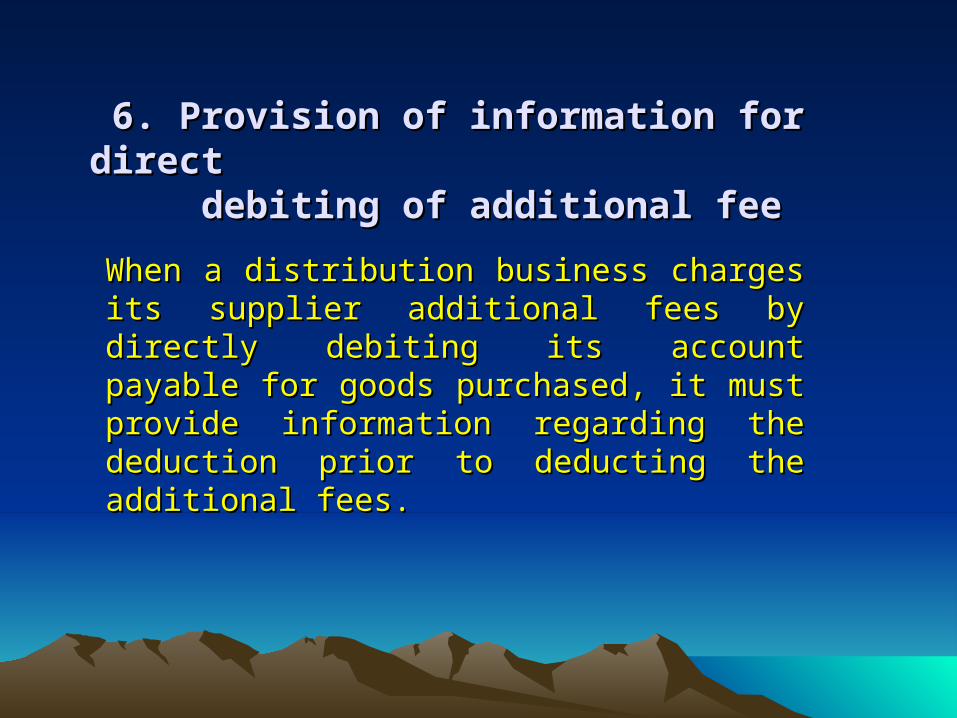

6. Provision of information for direct 6. Provision of information for direct debiting of additional fee debiting of additional fee

When a distribution business charges its supplier When a distribution business charges its supplier additional fees by directly debiting its account additional fees by directly debiting its account payable for goods purchased, it must provide payable for goods purchased, it must provide information regarding the deduction prior to information regarding the deduction prior to deducting the additional fees. deducting the additional fees.

7. Practices constituting improper 7. Practices constituting improper charging of additional fees(1) charging of additional fees(1)

Under anyone of the following circumstances, a distribution Under anyone of the following circumstances, a distribution business shall be deemed to be improperly charging additional business shall be deemed to be improperly charging additional fees: fees:

(1) the fees charged are not directly related to promoting the (1) the fees charged are not directly related to promoting the

sale of the goods; sale of the goods;

(2) the fees charged are contributions to equipment, research (2) the fees charged are contributions to equipment, research

and development, or promotional activities, and while of and development, or promotional activities, and while of

benefit to the supplier in promoting sale of goods or reducing benefit to the supplier in promoting sale of goods or reducing

operating costs, the amount of the fees exceeds in value the operating costs, the amount of the fees exceeds in value the

tangible benefit that the supplier may reasonably expect to tangible benefit that the supplier may reasonably expect to

derive from paying such contributions; derive from paying such contributions;

7. Practices constituting improper 7. Practices constituting improper charging of additional fees(2) charging of additional fees(2)

(3) the fees charged are for the sole purpose of achieving target (3) the fees charged are for the sole purpose of achieving target

figures or other accounting measures at the end of a fiscal figures or other accounting measures at the end of a fiscal

year; year;

(4) when, despite the supplier being under no obligation, a (4) when, despite the supplier being under no obligation, a

reduction in the purchase price is demanded by the reduction in the purchase price is demanded by the

distributor for already-delivered goods; or distributor for already-delivered goods; or

(5) fees are charged in a manner contrary to normal trading (5) fees are charged in a manner contrary to normal trading

principles or commercial ethics. principles or commercial ethics.

8. Violation of these Principles8. Violation of these Principles

If a distribution business having an advantageous If a distribution business having an advantageous market position charges suppliers additional fees market position charges suppliers additional fees in a manner not in accordance with Points 5 and 6 in a manner not in accordance with Points 5 and 6 of these Principles or is found to be in violation of of these Principles or is found to be in violation of Point 7 such that the distribution business market Point 7 such that the distribution business market order is impacted, the distribution business shall order is impacted, the distribution business shall possibly deemed to be in violation of Article 19(1)possibly deemed to be in violation of Article 19(1)(vi) or Article 24 of the Fair Trade Law.(vi) or Article 24 of the Fair Trade Law.

Thank You