DERIVATIVES - alphaacademyindiaalphaacademyindia.com/media/download_tab/CA_Final... · CA,...

65

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 1 DERIVATIVES UNIT I – FUTURES & FORWARD Q.2. Suppose that you enter into a short future….. Solution: Total loss before margin call triggers = 5,00,000 – 3,00,000 = 2,00,000 Required change in price = ₹ 2,00,000 1000 = ₹200 per gram Therefore, an increase in price (since we are seller) of ₹200 will trigger the margin call. If we do not meet the margin call then exchange/broker has the right to unilaterally square off the position, adjust the losses against the margin already deposited & refund back the balance amount if any. Q.5. ABC Ltd., a non-dividend paying company is quoting….. Solution: (a) F = S0 x e rt = 85 x e 0.08 x 6 12 = ₹ 85 x e 0.04 = ₹ 85 x 1.04081 = ₹ 88.46885 ~ ₹ 88.47 (b) Since actual price (₹ 88) < futures fair price (₹ 88.47), therefore, futures contract are undervalued, hence will long the futures & short the spot to earn risk free gain of ₹ 0.47 (88.47 - 88). (c) Since actual price (₹ 94) > futures fair price (₹ 88.47) therefore future contract are overvalued, hence will short the futures & long the spot to earn risk free gain of ₹ 5.53 (94 – 88.47) Proof of Arbitrage Table for point (c) Today On due date Particulars Action Amount Action If ₹ 80 If ₹ 95 Futures Short @94 - Settle +14 -1 Spot Long (85) Short +80 +95 Loan Borrow @8% p.a.cc +85 Repay* (88.47) (88.47) Net Arbitrage Gain 5.53 5.53

Transcript of DERIVATIVES - alphaacademyindiaalphaacademyindia.com/media/download_tab/CA_Final... · CA,...

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 1

DERIVATIVES UNIT I – FUTURES & FORWARD

Q.2. Suppose that you enter into a short future…..

Solution:

Total loss before margin call triggers = 5,00,000 – 3,00,000

= 2,00,000

Required change in price = ₹ 2,00,000

1000 = ₹200 per gram

Therefore, an increase in price (since we are seller) of ₹200 will trigger the margin call.

If we do not meet the margin call then exchange/broker has the right to unilaterally

square off the position, adjust the losses against the margin already deposited & refund

back the balance amount if any.

Q.5. ABC Ltd., a non-dividend paying company is quoting…..

Solution:

(a) F = S0 x ert

= 85 x e0.08 x 6

12

= ₹ 85 x e0.04

= ₹ 85 x 1.04081

= ₹ 88.46885 ~ ₹ 88.47

(b) Since actual price (₹ 88) < futures fair price (₹ 88.47), therefore, futures contract

are undervalued, hence will long the futures & short the spot to earn risk free

gain of ₹ 0.47 (88.47 - 88).

(c) Since actual price (₹ 94) > futures fair price (₹ 88.47) therefore future contract

are overvalued, hence will short the futures & long the spot to earn risk free gain

of ₹ 5.53 (94 – 88.47)

Proof of Arbitrage Table for point (c)

Today On due date

Particulars Action Amount Action If ₹ 80 If ₹ 95

Futures Short @94 - Settle +14 -1

Spot Long (85) Short +80 +95

Loan Borrow @8%

p.a.cc

+85 Repay* (88.47) (88.47)

Net Arbitrage Gain 5.53 5.53

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 2

*FV = PV x ert

= 85 x e0.08 x 6/12

= 85 x 1.04081

= 88.47

Q.6. X Ltd. a company that historically has not paid….

Solution:

F = S0 x ert

61.21 = S0 x e0.08 x 3

12

= S0 x e0.02

= S0 x 1.02020

S0 = 61.21 / 1.0202

= ₹ 60

Since Actual Spot Price (₹ 64) > Fair Spot Price (₹ 60), therefore, Stock in Spot is

Overvalued. Hence will Short in Spot & Long in Futures to earn risk free gain of ₹ 4

today (64 – 60)

Proof of Arbitrage Table

Today On due date

Particulars Action Amount Action If ₹ 50 If ₹ 70

Futures Long @61.21 - Settle (11.21) (8.79)

Spot Short 64 Long (50) (70)

Investment Invest @8%

p.a.cc

(60) Liquidate +61.21 +61.21

Net Arbitrage Gain +4 0 0

Note: Alternatively, we could have invested full amount of ₹ 64 and realized gain on

Due date which will be equivalent to Future Value of ₹ 64 compounded @ 8% p.a.

c.c. for 3 months

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 3

Q.9. A 3-month forward contract on a stock….

Solution:

F = S0 x ert

96.50 = 92 x er x 3/12

1.04891 = e0.25r

Taking Log on both the sides

Ln (1.04891) = Ln (e0.25r)

Ln (1.04891) = 0.25r

Using Interpolation:

Ln 1.04 0.03922

0.01 Ln 1.04891 ? 0.00957

Ln 105 0.04879

Since, 0.01 = 0.00957

Therefore, 0.00891 = 0.00891 x 0.00957

0.01

= 0.008527

= 0.03922 + 0.008527

= 0.04774

Replacing Ln 1.04891 with 0.04774

0.4774 = 0.25r

Therefore, r = 19.098% p.a. compounded continuously

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 4

Q.10. A forward contract on a share that is selling…..

Solution:

F = S0 x ert

100 = 97.05 x ert 6/12

1.0304 = e0.50r

Alternative-1: using ex table values

Since, e0.03 = 1.03045 ~ 1.0304

Replacing 1.0304 in the LHS of above equation by e0.03

e0.03 = e0.50r

when bases are same, powers can be compared

0.03 = 0.50r

r = 6% p.a.cc

Alternative-2: Using Log Natural

1.0304 = e0.50r

Taking Ln on both the sides

Ln (1.0304) = Ln (e0.50r)

Ln (1.0304) = 0.50r

Ln (1.03) 0.02956

0.01 1.0304 ? 0.00966

Ln (1.04) 0.03922

Since, 0.01 --- 0.00966

Therefore, 0.0004 --- ?

= .0004 x 00966

.01

= 0.0003864

= 0.02956 + 0.0003864

= 0.02995

Replacing Ln 1.0304 by 0.02995

0.02995 = 0.50r

r = 5.99 ~ 6% p.a.cc

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 5

Q.14. Calculate the price of a 6 months futures contract

Solution:

Working Note 1: Calculation of PV of dividend income:

PV (I) = FV

ert

I = 2

e0.12 x 4/12

I = 2

e0.04

I = 2

1.04081

I = 1.92

Calculation of Fair Futures Price

F = (S0 – I*) x ert

F = (75 – 1.92) x e0.12 x 6/12

= 73.08 x e0.06

= 73.08 x 1.06184

= 77.60

Futures contract value = 77.60 x 100

= 7760

Since actual futures price (₹ 7400) < futures fair price (7760), therefore Futures

Contract are Undervalued. Hence, we will go Long Future & Short Spot & Invest the

proceeds at risk tree rate of return to earn risk free arbitrage gains of ₹ 360 (equivalent

to the extent of mispricing).

Proof of Arbitrage Table:

Today Dividend date On due date

Particulars Action Amt Action Amt Action If ₹ 70 If ₹ 80

Futures Long @

₹ 7400

- Short -400 +600

Spot Short 7500 Long -7000 -8000

Investment Invest

@12%

p.a.cc

7500 Liquidate +7963.80 +7963.80

Dividend Paid (200) - - -

Loan Borrow @

12% p.a.cc

for 2 month

+ 200 Repay -204.04 -204.04

Net Arbitrage Gain 360 360

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 6

Since actual futures prices (₹ 7900) > fair futures price (₹ 7760), therefore, Futures

Contract are Overvalued. Hence, we will go Short in Futures & Long in Spot by

borrowing at risk free rate of interest to earn risk free arbitrage gain of ₹ 140.

Proof of Arbitrage Table:

Today Dividend date On due date

Particulars Action Amt Action Amt Action If ₹ 70 If ₹ 80

Futures Short @

₹ 7900

- Long +900 -100

Spot Long (7500) Short +7000 +8000

Loan Borrow

@ 12%

p.a. cc

+7500 Repay -

7963.80

-7963.8

Dividend Received 200 - - -

Investment Invest @

12% p.a.cc

for 2 month

(200) Liquidate +204.04 +209.04

Net Arbitrage Gain 140 140

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 7

Q.18. An index consists of following four stocks…..

Solution:

Working Note 1: Calculation of present Market Cap

Stock Price No. of Shares M. Cap

A 50 10 500

B 80 5 400

C 20 5 100

D 100 5 500

Total M. Cap = 1500

Working Note 2: Calculation of PV of dividend income

= ₹ 10

e0.12 𝑥 1/12

= 10

e0.01

= 10

1.01005

= ₹ 9.90 x 10 lakh shares

= ₹ 99 lakhs

Calculation of Future Market Cap:

F = (S0 - I) x Crt

= (1500 - 99) x e0.12 x 3/12

= 1401 x e0.03

= 1401 x 1.03045

= ₹ 1443.66

Calculation of futures contract price on index (Using Cross Multiplication)

Market Cap Index Points

Since, 1500 lakhs equivalent to 12 pts

1443.66 ?

= 1443.66 x 1200

1500

= 1154.93 Pts ~ 1155 Pts

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 8

Q.20. Nifty spot is 1300 points. You are considering…..

Solution:

Calculation of Theoretical Futures Value:

F = S0 x e(r - y) x t

= 1300 x e(0.08 – 0.02) x 3/12

= 1300 x e0.015

= 1300 x 1.015125

= ₹ 1319.67

Action: Since, Actual Futures Price (₹ 1325) > Fair (Theoretical) Futures Price

(1319.67), therefore, it is Overvalued. Hence, we will Short in Future & Long in Nifty

constituents by borrowing at risk free rates to earn arbitrage gain of ₹ 5.33 (1325 –

1319.67).

Q.25. The spot price of Wheat is ` 8000 per ton…

Solution:

F = (S0 + S) x e(r - c) x t

= (8000 + 300) x e(0.08 – 0.02) x 12/12

= 8300 x e0.06

= 8300 x 1.06184

= ₹ 8813.27

Q.27. The following information about copper scrap is given……

Solution:

Futures price

(1+Risk−free rate)1 = Spot price + PV of storage costs - PV of Convenience Yield

10,800

(1.12)1 = 10,000 + 500 - PV of Convenience Yield

Hence the Present Value of Convenience Yield is $857.14 per ton.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 9

Q.31. Identify the action to be taken in terms of the hedging through Nifty…….

Solution:

S. No. Stock

Beta

Stock

Position

Stock Value

(` in Lakhs)

Hedging

required

Action in

futures

Amount

(` in Lakhs)

(i) 1.0 Short 10 Full Long 10

(ii) 0.25 Long 25 50% Short 3.125

(iii) 3.40 Long 60 110% Short 224.4

(iv) 0.75 Short 55 None - -

(v) 1.4 Short 35 140% Long 68.6

Q.36. A portfolio manager owns 3 stocks……

Solution:

(a)

Security MV of security Proportion Beta Beta Portfolio

1 400 Lacs 4/13 1.1 0.34

2 600 Lacs 6/13 1.2 0.55

3 300 Lacs 3/13 1.3 0.3

1300 Lacs 1.19

Security Proportion Beta Portfolio Beta

Portfolio P 1.19 p x 1.19

Risk free 1 – p 0 0

0.8

p = 67.23 %

(1— p) = 32.77%

1300 Lacs

Instead of selling the existing portfolio for 426 lacs for risk free securities the portfolio

manager can use stock index futures to hedge the operations.

No. of futures contracts to be purchased/sold = Total value of portfolio x (β2 − β1)

Value of 1 stock index

Here,

β1 = Existing Beta index

β2 = New Beta Index

Dispose & Substitute (bal fig)

= 426

Retain 67.23% x 1300 lacs

= 874

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 10

Instead of changing the composition of the portfolio the portfolio manager shall retain

the entire portfolio & should go short for stock index futures

No. of SIF contracts = 1300 lacs x (0.8−1.19)

1350 x 100

= (375) contracts - Sold

Negative Quantity indicates sale of contracts & Positive Quantity indicates Purchases.

(b) No. of future contract to increase the beta from 1.19 to 1.5 the portfolio manager

buy 299 contracts

No. of SIF contracts = 1300 lacs x (1.5−1.19)

1352 x 100

= 299 contract - Buy

Q.37. The portfolio composition of Mr. X is given below……

Solution:

Let Fe, be, Fc, bc, Ff, bf, Fp & bp are the fund and beta values of equity, cash, index

futures and portfolio respectively.

Let n = No of future contracts

Beta for cash = 0

Then we have,

Fe x be + Fc x bc + Ff x bf = Fp x bp

or 8,00,000 x 0.69 + 2,00,000 x 0 + (930 x 200 x n x 1) = 1.1 x 10,00,000

or 5.52+ 1.86 n = 11

or 0.186 n = 5.48

or n = 2.946 i.e. 3 future contracts.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 11

Q.38. A company is long 10MT of copper @ ` 474 per kg (spot)……

Solution:

The optional hedge ratio to minimize the variance of Hedger's position is given by:

H = ρσS

σF

Where

σS = Standard deviation of ∆S

σF = Standard deviation of ∆F

ρ = coefficient of correlation between ∆S and ∆F

H = Hedge Ratio

∆S = change in Spot price

∆F = change in Future price

Accordingly,

H = 0.75 x 0.04

0.06 = 0.5

No. of contract to be short = 10 x 0.5 = 5

Amount = 5000 x ₹ 474 = ₹ 23,70,000

Q.46. The following information is available about standard gold. ….

Solution:

FP

(1+Rf)t = SP + PVS - PVC

PVC = SP + PVS - FP

(1+Rf)t

Accordingly,

= ₹ 15600 + ₹ 900 - ₹ 17100

(1+0.085)1

= ₹ 15600 + ₹ 900 - ₹ 15760

= ₹ 16500 - ₹ 15760 = ₹ 740

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 12

Q.47. Mr. A bought a futures contract of Britannia that……

Solution:

(a) Working Note 1: PV of dividend income:

= 5

e0.08 x 12/12

= 5

1.08329

= 4.616

Calculation of fair futures prices:

F = (S0 - I) x ert

= (200 – 4.616) x e0.08 x 1

= 195.384 x e0.08

= 195.384 x 1.08329

= ₹ 211.66

(b) F = (S0 - I) x ert

= [186 – 4.616] x e0.08 x 1

= 181.384 x 1.08329

= ₹ 196.49

(c) Gain / (loss):

Absolute terms = (211.66 – 196.49) x 1000

= 15170

% terms = 211.66−196.49

211.66

= 7.17%

(d) Margin call:

Maintenance margin = ₹ 10000 per contract

Initially margin deposited was ₹ 20000 but after loss of ₹ 15170 position comes

to below maintenance margin of ₹ 10000 i.e. comes down to ₹ 20000 - ₹ 15170

= ₹ 4830, therefore, Amount of margin call will be ₹ 15170 [20000 - 4830] in order

to bring back the Maintenance Margin amount of ₹ 20000.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 13

UNIT II - OPTIONS

Q.55. A stock with a current market price of ` 50 has the following…….

Solution:

Exercise Price Spot Price Total Premium Intrinsic Value Extrinsic Value

40 50 10 10 -

48 50 7 2 5

50 50 5 0 5

55 50 3 0 3

62 50 1 0 1

Q.56. A put option on Abhishek Industries stock has an exercise price……

Solution:

Calculation of Value of Put

Exercise Price Spot Price Value of Put Option

VP = Max (E-S1 , 0)

20 16 4 (20 - 16)

20 18 2 (20 - 18)

20 20 0

20 22 0

20 24 0

Q.57. A call option has an exercise price of ` 50. On the expiry date…….

Solution:

Call Option Exercise Price = ₹ 50

Spot price on maturity date (S1) = ₹ 60

(i) Call is priced at ₹8:

Fair VC = Max (S1 – E, 0)

= Max (60 – 50, 0)

Fair VC = 10

Since, Actual VC (₹ 8) < Fair VC (₹ 10), therefore, Call Option is undervalued, Hence,

we will Buy Call Option & Sell in Spot to earn risk free arbitrage gain of ₹ 2.

Particulars Stock Amount

Buy CO Ex Price = ₹ 50 (8)

Exercise CO +1 (50)

Sell Stock in Spot -1 60

Net Arbitrage Gain ₹ 2

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 14

(ii) Call is priced at ₹ 12:

Since actual VC (₹ 12) > Fair VC (₹ 10), therefore, Call Option is overvalued. Hence,

we will Sell Call Option & Buy Stock in spot to earn risk free arbitrage gain of ₹ 2.

Particulars Stock Amount

Sell CO Ex Price = ₹ 50 12

CO Exercised on us -1 50

Buy Stock in Spot +1 (60)

Net Arbitrage Gain 2

Q.58. A put option has an exercise price of ` 100. On the expiry date……

Solution:

Calculation of FV of Put Option:

Fair VP = Max (E – S1, 0)

= Max (100 – 80, 0)

Fair VP = 20

(i) Since Actual VP (₹ 14) < Fair VP (₹ 20), therefore, Put Option is

undervalued. Hence, we will Buy PO & Buy in Spot to earn risk free

arbitrage gain of ₹ 6.

Proof of Arbitrage:

Particulars Stock Amount

Buy PO Ex. Price = ₹ 100 (14)

Buy Stock in spot +1 (80)

Exercise PO -1 100

Net Arbitrage Gain 6

(ii) Since Actual VP (₹ 23) > Fair VP (₹ 20), therefore, Put Option is

overvalued. Hence, we will Sell PO & Sell in Spot to earn to risk free

arbitrage gain of ₹ 3.

Proof of Arbitrage:

Particulars Stock Amount

Sell PO Exercise Price = ₹ 100 23

PO Exercised on us +1 (100)

Sell in spot -1 80

Net Arbitrage Gain ₹ 3

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 15

Q.61. The shares of Wipro Ltd. are selling at ` 550 per share…….

Solution:

(i) Pay off table for holder of Call Option

Exercise Price Stock Price Gross Payoff Less: Premium

Paid

Net Pay

Off

560 500 0 -40 -40

560 520 0 -40 -40

560 540 0 -40 -40

560 560 0 -40 -40

560 580 20 -40 -20

560 600 40 -40 0

560 620 60 -40 20

560 640 80 -40 40

(ii) Pay off graph for Mr. Balwant:

(iii) Pay off table for Writer of Call Option:

Exercise Price Stock Price Premium

received

Less: Gross Payoff Net Pay Off

560 500 40 0 40

560 520 40 0 40

560 540 40 0 40

560 560 40 0 40

560 580 40 -20 20

560 600 40 -40 0

560 620 40 -60 -20

560 640 40 -80 -40

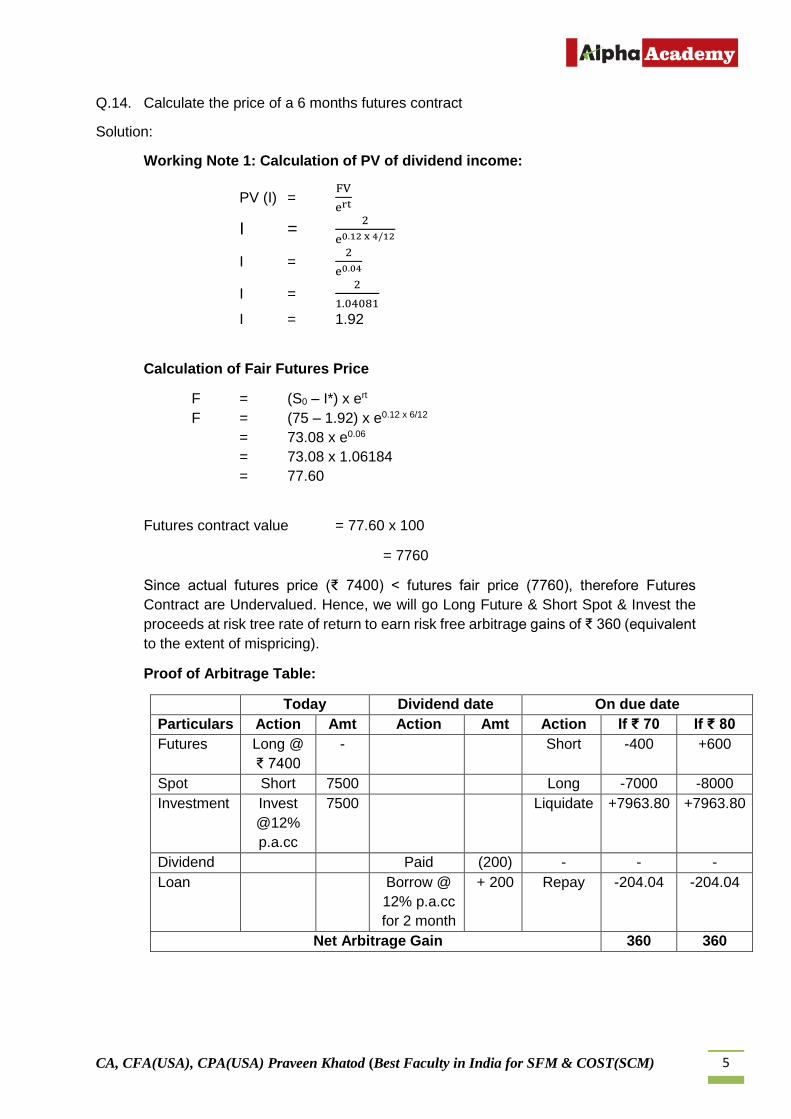

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 16

(iv) Pay off graph for Call Writer:

Q.62. The CMP of TCS Computers Ltd. is ` 120. Mr. Raju buys three……

Solution:

(i) Pay off table for holder of Put Option

Exercise Price Stock Price Gross

Payoff

Less:

Premium

Paid

Net Pay Off

110 85 25 -8 17

110 90 20 -8 12

110 95 15 -8 7

110 100 10 -8 2

110 105 5 -8 -3

110 110 0 -8 -8

110 115 0 -8 -8

110 120 0 -8 -8

110 125 0 -8 -8

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 17

(ii) Pay off graph for Mr. Raju:

(iii) Pay off table for Writer of Put Option:

Exercise Price Stock Price Premium

received

Less: Gross Payoff Net Pay Off

110 85 8 -25 -17

110 90 8 -20 -12

110 95 8 -15 -7

110 100 8 -10 -2

110 105 8 -5 +3

110 110 8 0 +8

110 115 8 +5 +8

110 120 8 +10 +8

110 125 8 +15 +8

(iv) Pay off graph for Put Writer:

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 18

Q.65. A put and a call option each have an expiration date 6 months……

Solution:

(a) VS + VP = VC + PV of Ex Price

$9 + $2 = VC + $10

(1+0.03)

VC = 1.29

(b) VS + VP = VC + PV of Ex Price

VS = $4 + $10

(1.03) - $1

VS = 12.71

(c) VP = VC + PV of Ex Price - VS

= $5 + 10

(1.03) – 12

VP = 2.71

Q.75. A company’s share price is now $60. Six months hence……

Solution:

(a) Step-1: Calculate delta (∆)

∆ = Spread in Option Values

Spread in Stock Prices

= $ 10−$0

$75−$50

∆ = 0.40

Now, perfectly hedged position can be created in either of the following two ways:

(i) Buy 0.40 shares & Sell 1 CO or

(ii) Buy 1 CO & Sell 0.40 shares

Let us assume that we Sell 0.40 share & Buy 1 CO

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 19

(b) Calculation of value of hedged position on maturity dates:

Possible stock

prices on maturity

Value of Shares Value of CO Net Inflow/

(Outflow)

$ 75 (30)

[0.4 shares x $ 75]

+10 ($20)

$ 50 (20)

[0.4 shares x $ 50]

- ($20)

The value of perfectly hedged position would be $20 outflow irrespective of the

stock price outcome.

(c) PV of Guaranteed Outcome:

= − (−$20)

1.03

= $19.42

Calculation of VC today: + ∆ SO – VC = PV of guaranteed outcome

0.40 x $60 – VC = +19.42

VC = $4.58

Q.77. In above problem, calculate the value of the European put……

Solution:

Alternative-1:

VP Probability VP x P

0 .125 0

0 .125 0

0 .125 0

20 .125 2.5

0 .125 0

20 .125 2.5

20 .125 2.5

50 .125 6.25

VP on maturity 13.75

Calculation of PV of VP:

VP = 13.75

(1.0010)3

= 13.71

Alternative-2:

VS + VP = VC + PV of Ex Price

5000 + VP = 8.72 + 5020

(1.0010)3

VP = 13.69

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 20

Q.79. A company’s stock is currently traded in the market at ` 80…….

Solution:

We will calculate VC on each & every node & compare its value with all the subsequent

nodes then select the highest one.

After 1

Year

After 2

Year

If option is exercised

after 1 Year

If option is exercised

after 2 Year

Vc (Max of

both Vc

88

VC = 13

96.8

VC = 21.8

13 x 0.90

(1.08)1

= 10.83

[21.8 x 0.90+4.2 x 0.10] x 0.90

(1.08)2

= 15.46

15.46 79.2

VC = 4.2

72

VC = 0

79.2

VC = 4.2

0 x 0.10

(1.08)1

= 0

[4.2 x 0.90+0 x 0.10] x 0.10

(1.08)2

= 0.32

0.32 64.8

VC = 0

VC as of today 15.78

Calculation of probabilities:

Rf = % Upside x P + % downfall x (1 - P)

0.08 = .10 P + (-.10) (1 - P)

0.08 = .10 P - .10 + 0.10P

0.18 = 0.20P

P = .90

1 – P = 0.10

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 21

Q.81. From the following data for certain stock, find the value of a call option……

Solution:

Applying the Black Scholes Formula,

Value of the Call option now:

C = SN (d1) – Ke(- rt) N(d2)

d1 = Ln (S/K) + (r + σ2 / 2) t

σ√t

d2 = d1 - σ√t

d1 = Ln (1.0667) + (12%+(0.08))

0.5

.40 √0.5

= 0.0645+(0.2)0.5

0.40 x 0.7071

= 0.1645

0.2828

= 0.5817

d2 = 0.5817 – 0.2828

= 0.2989

Nd1 = N (0.5817)

= 0.7195

Nd2 = N (0.2989)

= 0.6175

C = SO x N(d1) - E x N(d2)

ert

= 80 x Nd1 - 75

1.0060 x Nd2

= 80 x 0.7195 - 75 x 0.6175

1.0060

= 57.56 - 74.55 x 0.6175

= 57.56 - 46.04

= ₹ 11.52

Where,

C = Theoretical call premium

S = Current stock price

t = time until option expiration

K = option striking price

r = risk-free interest rate

N = Cumulative standard normal distribution

e = exponential term

σ = Standard deviation of continuously compounded

annual return.

Ln = natural logarithm

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 22

Q.86. The market received rumour about ABC corporation’s tie up…..

Solution:

Cost of Call and Put Options

= (₹ 2 per share) x (100 share call) + (₹ 1 per share) x (100 share put)

= ₹ 2 x 100 + 1 x 100

= ₹ 300

(i) Price increases to ₹43. Since the market price is higher than the strike price of the

call, the investor will exercise it.

Ending position = (- ₹ 300 cost of 2 option) + (₹ 1 per share gain on call) x 100

= - ₹ 300 + 100

Net Loss = - ₹ 200

(ii) The price of the stock falls to ₹ 36. Since the market price is lower than the strike

price, the investor may not exercise the call option.

Ending Position = (- ₹ 300 cost of 2 options) + (₹4 per stock gain on put) x 100

= - ₹ 300 + 400

Gain = ₹ 100

Q.87. Mr. A purchased a 3-month call option for 100 shares in XYZ Ltd…..

Solution:

Since the market price at the end of 3 months falls to ₹ 350 which is below the exercise

price under the call option, the call option will not be exercised. Only put option

becomes viable.

₹

The gain will be:

Gain per share (₹ 450 - ₹ 350) 100

Total gain per 100 shares 10,000

Cost or premium paid (₹ 30 x 100) + (₹ 5 x 100) 3,500

Net gain 6,500

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 23

Q.88. An investor purchased Reliance November Futures (600 shares lot size)……

Solution:

Particulars Computation Amount

Futures

Gain on settlement of futures

(1180 – 1150) x 600 shares x 1 lot +18000

Transaction cost (brokerage) on

purchase of Futures

1150 x 600 x 0.045% (310.50)

Transaction cost (brokerage) on sale

of Futures

1180 x 600 x 0.045% (318.60)

Net gain on Futures 17370.90

Call Option

Loss on premium of CO (16 – 10) x 600 shares (3600)

Brokerage on Selling CO (1190 – 10) x 0.045% x 600 shares (318.60)

Brokerage on Buying CO (1190 - 16) x 0.045% x 600 shares (316.98)

Net Loss on Options (4235.58)

Overall profit for investor 13135.32

Solution of Options Strategy related questions

89. Mr. Ramesh owns 10,000 shares……

Solution:

Since, Mr Ramesh own 10,000 Shares and feels that due to bad news stock price may

fall then he should do hedging in order to protect his spot position.

If he is highly bearish then he should Buy Put Option.

Alternatively, If he is mildly bearish then he should Sell Call Option.

90. A highly diversified portfolio….

Solution:

Current value of portfolio `15 lakhs, B=0.50 Put Option with Ex. Price = `9500, Premium

= `1000, Lot Size = 50

No. of Options to be traded = 15,00,000 x 0.50

9500 x 50 = 1.579 ~ 2 Put Options should be bought

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 24

91. Rakesh is bullish to a limited extent

Solution:

Given

Call option Ex. Price Premium Put Option Ex. Price Premium

`1100 `55 `1000 `45

`1200 `20 `900 `15

Two strategies are possible in the bullish market

(a) Buy CO EL & Sell CO EH

(b) Buy PO EL & Sell PO EH

800 900 1000

0

1100

0

1200

0

1300

0

(+65) (+65)

Premium

Buy CO EL 1100 55 Paid

Sell CO EH 1200 20 Recd

35 Net Paid

(-35) (-35) (-35) (-35) -40

-30

-20

-10

0

10

20

30

40

50

60

70

N

e

t

p

a

y

o

f

f

(a)

Stock prices on maturity date

800 900 1000

0

1100

0

(+30) (+30)

Ex. Premium Premium

Buy PO EL 900 15 Paid

Sell PO EH 1000 45 Recd

30 Net Recd

(-70) (-70) -80

-60

-40

-20

0

20

40

60

80 N

e

t

p

a

y

o

f

f

(b)

Stock price on maturity date

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 25

92. Gangaram is bearish on the stocks of Geodesic……

Solution:

Bearish

Two strategies are possible in the bearish market

(a) Sell CO EL & Buy CO EH

(b) Sell PO EL & Buy PO EH

(a) Sell CO EL & Buy CO EH

(-7) (-7) (-7)

100 110 120 130

(+3) (+3)

Ex. Premium Premium

Sell CO Ex. PriceL `110 5 Receive

Buy CO Ex. PriceH `120 2 Paid

3 Receive

-15

-10

-5

0

5

10

15

N

e

t

p

a

y

o

f

f

Stock price on maturity date 140

(-2) 80 90 100 110

(+8) (+8)

Ex. Premium Premium

Sell PO EL 90 2 Receive

Buy PO EH 100 4 Paid

2 Paid

-15

-10

-5

0

5

10

15

N

e

t

p

a

y

o

f

f

Stock price on maturity date 120

(b) Sell PO EL & Buy PO EH

(-2) (-2)

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 26

93. For each of the following cases, name the strategy adopted….

Solution:

Type of

option

Ex. Price

(buy)

Ex. Price

(sell)

Premium

(buy)

Premium

(sell)

(i) Call option 60

(EL)

70

(EH)

9 4 Buy CO EL & sell CO EH

= Bull Spread

(ii) Call option 80

(EH)

75

(EL)

2 6 Buy CO EH & sell CO EL

= Bear Spread

(iii) Put option 70

(EH)

65

(EL)

9 5 Buy PO EH & sell PO EL

= Bear Spread

(iv) Put option 50

(EL)

60

(EH)

4 11 Buy PO EL & sell PO EH

= Bull Spread

(i) Bull spread: - Buy CO EL & sell CO EH

Ex. Price Premium Stock Price Gross Pay Net Pay Off

60 9 Paid 60 0 -9

70 4 Recd 70 0 +4

5 Paid Net -5

(ii) Bear Spread :- Buy CO EH & sell CO EL

Ex. Price Premium Stock Price Gross Pay Off Net Pay off

80 2 Paid 80 0 -2

75 6 Receive 75 0 +6

+4

50 60 70 80

(+5) (+5)

(-5) (-5) -10

-5

0

5

10

N

e

t

p

a

y

o

f

f

Stock price on maturity date

BEP

(-1) (-1) 70 75 80 85

(+4) (+4)

-10

-5

0

5

10

N

e

t

p

a

y

o

f

f

Stock price on maturity date

BEP

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 27

(iii) Bear Spread :- Buy PO EH & Sell PO EL

Ex. Price Premium Stock Price Gross Pay-off Net payoff

Buy 70 9 Paid 70 0 -9

Sell 65 5 Receive 65 0 +5

-4 Paid

(iv) Bear Spread :- Buy PO EL & Sell PO EH

Ex. Price Premium Stock Price Gross Pay off Net pay off Buy 50 4 paid 50 0 -4

Sell 60 11 Receive 60 0 +11

+ 7

(-4) (-4) 60 65 70 75

(+1) (+1)

-10

-5

0

5

10

N

e

t

p

a

y

o

f

f

Stock price on maturity date

BEP

40 50 60 70

(+7) (+7)

(-3) (-3)

-10

-5

0

5

10

N

e

t

P

a

y

o

f

f

Stock price on maturity date

BEP

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 28

94. A call option on Adani Exports Ltd……

Solution:

Call option EP `50 Premium `4

Put option EP `50 Premium `5

(a) Buy a CO & Buy a PO with same Ex. Price

Buy CO `50 `4 paid

Buy PO `50 `5 paid

`9 net paid

(b) If you expect stagnant markets

Sell CO Ex. price `50 premium `4 receive

Sell PO Ex. Price `50 premium `5 receive

`9 receive net

40 50 60 70

(+11)

-10

-5

0

5

10

N

e

t

p

a

y

o

f

f

Stock price on maturity date

(-9)

(+1)

40 50 60 70

(+9)

-10

-5

0

5

10

N

e

t

p

a

y

o

f

f

Stock price on maturity date (-1)

(-11)

(-1)

(+1)

(-11)

(+11)

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 29

95. A call option on ABB Ltd. with an exercise…..

Solution:

CO Ex. Price `50 premium `4

PO Ex. Price `45 premium `3

(a) If you expect high volatility

Buy CO Ex. Price `50 premium `4 paid

Buy PO Ex. Price `45 premium `3 paid

`7 net paid

(b) If you expect stagnant markets

Sell CO ex. Price `50 premium `4 receive

Sell PO ex. Price `45 premium `3 receive

`7 net receive

40 45 50 55

(+3)

-10

-5

0

5

10

N

e

t

p

a

y

o

f

f

Stock price on maturity date

(-2) (-2)

(-7) (-7)

60

40 45 50 55

(+7)

-10

-5

0

5

10

N

e

t

p

a

y

o

f

f

Stock price on maturity date

(-3)

(+2)

(+7)

60

(+2)

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 30

96. An investor anticipates bearish volatility…..

Solution:

Strip – Bearish Volatility

Qty. Ex. Price Premium

Buy PO 2 `100 `7 * 2 Paid

Buy CO 1 `100 `9 * 1 Paid

`23 Net Paid

Pay off table

Ex. Price Stock Price Premium Gross Pay-off Qty Net Pay-off

PO `100 `100 `7 0 2 -14

CO `100 `100 `9 0 1 -9

-23 Net Paid

98. An investor notices a call option…..

Solution:

Straps

Qty. Total premium

Buy CO Ex. Price `80 premium `6 2 12 paid

Buy PO Ex. Price `80 premium `7 1 7 paid

19 net paid

30

80 90 100 110

(+17)

-20

-10

0

10

20

N

e

t

P

a

y

o

f

f

Stock price on maturity date

(-23)

(-13)

-30

120 (-3) (-3)

70 80 90

(-9) -20

-10

0

10

20

N

e

t

p

a

y

o

f

f

Stock price on maturity date

(-19)

(+1)

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 31

99. A stock is selling at ` 62……

Solution:

Butterfly

For volatile market – using CO

Premium Qty. Total premium

Sell CO EL `55 10 receive 1 10

Buy CO EM `60 7 paid 2 14

Sell CO EH `65 5 receive 1 5

1 net receive

For volatile market – using PO

Qty Total premium

Sell PO EL 70 Prem 6 receive 1 6

Buy PO EM 75 Prem 9 Paid 2 18

Sell PO EH 80 Prem 14 receive 1 14

2 Net receive

50 55 60 65

(+1)

-10

-5

0

5

10

N

e

t

p

a

y

o

f

f

Stock price on maturity date (-4)

(+1)

70

(+1) (+1)

60 65 70 75

(+2)

-5

0

5

N

e

t

p

a

y

o

f

f

Stock price on maturity date (-3)

(+2)

80

(+2) (+2)

85

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 32

For stable market – using CO

Qty Premium Total premium

Buy CO EL 1 55 10 10

Sell CO EM 2 60 7 14

Buy CO EH 1 65 5 5

-1 Net paid

For stable market – using PO

Qty Premium Total premium

Buy PO EL 1 70 6 6

Sell PO EM 2 75 9 18

Buy PO EH 1 80 14 14

-2 Net paid

(-1) 55 50 60 65

-10

-5

0

5

10

N

e

t

p

a

y

o

f

f

Stock price on maturity date

(-1)

70

(+4)

(-1) (-1)

65 70 75 80

-10

-5

0

5

10

N

e

t

p

a

y

o

f

f

Stock price on maturity date

(-2)

85

(+3)

(-2) (-2) (-2)

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 33

FOREIGN EXCHANGE RISK

MANAGEMENT Q.11. A New Delhi Banker has offered….

Solution:

1 CY£ = ₹ 98.6033

1 NZ$ = ₹ 31.0021

(i) NZD $ / CYP i.e.

NZ$

CY£ =

NZ$

₹ x

₹

CY£

= 1

31.0021 x 98.6033

= 3.1805

1 CY£ = NZ$ 3.1805

(ii) CYP / NZD i.e.

CY£

NZ$ =

CY£

₹ x

₹

NZ$

= 1

98.6033 x 31.0021

= 0.3144

1 NZ$ = CY£ 0.3144

Q.15. Consider the following quotations in Mumbai…..

Solution:

1 AED = ₹ 13.75

1 SEK = ₹ 6.25

1 NZD = ₹ 29

1 INR = € 0.0148

(a) 1 AED = SEK 2.20

SEK

AED =

SEK

INR x

INR

AED

= 1

6.25 x 13.75

= 2.20

(b) 1 NZD = € 0.4292

€

NZD =

€

INR x

INR

NZD

= 0.0148 x 29

= 0.4292

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 34

Q.16. Consider the following and determine the cross rates….

Solution:

1. 1 NOK = ₹ 6.44

1 GBP = ₹ 47.10

1 GBP = NOK 7.3137

NOK

GBP =

NOK

₹ x

₹

GBP

= 1

6.44 x 47.10

= 7.3137

2. 1 AUD = USD 0.6051

1 AUD = USD 0.6051

(a) 1 INR = USD 0.0209

USD

INR =

USD

AUD x

AUD

INR

= 0.6051 x 1

28.97

= 0.0209

(b) 1 USD = INR 47.8764

INR

USD =

INR

AUD x

AUD

USD

= 28.97 x 1

0.6051

= 47.8764 ~ 47.88

3. 1 GBP = INR 74.5 – 75.00

1 GBP = $ 1.62 – 1.63

1 $ = INR 45.7055

Bid (INR

$) = Bid (

INR

GBP) x Bid (

GBP

$)

= 74.5 x 1

1.63

= 45.7055 ~ 45.71

Ask (INR

$) = Ask (

INR

GBP) x Ask (

GBP

$)

= 75 x 1

1.62

= 46.2963 ~ 46.30

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 35

Q.17. Suppose the exchange rate between US dollar and the French franc…..

Solution:

$ 1 = FF 5.90

1 £ = $ 1.50

1 £ = FF 8.85

FF

£ =

FF

$ x

$

£

= 5.90 x 1.50

= 8.85

Q.21. Calculate the merchant rates given the following interbank…..

Solution:

1. Merchant Bank Bid Rate = Interbank Bid Rate – Buying Margin

= 66.3250 – 0.030%

= ₹ 66.3051 ~ 66.31

Merchant Bank Ask Rate = Interbank Ask Rate + Selling Margin

= 66.4525 + 0.130%

= 66.5389 ~ 66.54

1 GBP = ₹ 66.31 – 66.54

2. Merchant Bank Bid Rate = 32.2525 – 0.025%

= 32.244 ~ 32.24

Merchant Bank Ask Rate = 32.3500 + 0.125%

= 32.3904 ~ 32.39

1 DEM = ₹ 32.24 – 32.39

3. Merchant Bank Bid Rate = 44.44000 – 0.080%

= 44.4044 ~ 44.04

Merchant Bank Ask Rate = 44.5100 + 0.150%

= 44.5768 ~ 44.58

1$ = ₹ 44.04 – 44.58

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 36

Q.23. An all-inclusive 15-day trip covering Paris-Rome-Vienna…….

Solution:

Particulars Amount in

Foreign Currency

Relevant Rate Amount in ₹

Traveler’s cheque $ 15,500 ₹ 47.60 737800

Amount paid to travel agent - - 25000

Gifts – Europe € 1200 ₹ 50.98 61176

Gifts - London £ 750 ₹ 77.11 57832.5

Contingency Amount $ 275 ₹ 48.23 13263.25

Total tour cost ₹ 895071.75

Q.40. Deep Sea Fishing Co Ltd concluded an export order for….

Solution:

(a) Estimating rupee inflow for the contract value

Contract Value 1,825 x 10 18,250 USD

Down Payment 18,250 x 1/4 4,562.50 USD

Installments 18,250 x 3/4 13,687.50 USD

Payment Dollars Rate INR

Down Payment 4,562.5 45.5 207,594

Installments 13,687.5 45.4 621,413

829,007

(b) Actual receipt amounted to ₹ 8,28,457 as shown in the table below. The actual

receipts have been lower than the amount estimated on contract date.

Computing actual receipts

Nature of payment Dollar Amount Rate Rupees

Advance payment 4,562.50 45.50 2,07,593

Shipment 1 1,368.75 45.40 62,141

Shipment 2 1,368.75 45.30 62,004

Shipment 3 1,368.75 45.20 61,867

Shipment 4 1,368.75 45.30 62,005

Shipment 5 1,368.75 45.20 61,867

Shipment 6 1,368.75 45.00 61,594

Shipment 7 1,368.75 45.50 62,278

Shipment 8 1,368.75 45.70 62,552

Shipment 9 1,368.75 45.60 62,415

Shipment 10 1,368.75 45.40 62,141

8,28,457

(c) Difference: ₹ 550. It arises on account of differences in exchange rates as

between the date on which the transaction is initially recorded, and the date(s)

on which payments are received. This is inherent in any transaction involving

foreign currency.

(d) Type of Risk: The type of exchange risk involved is known as Transaction Risk.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 37

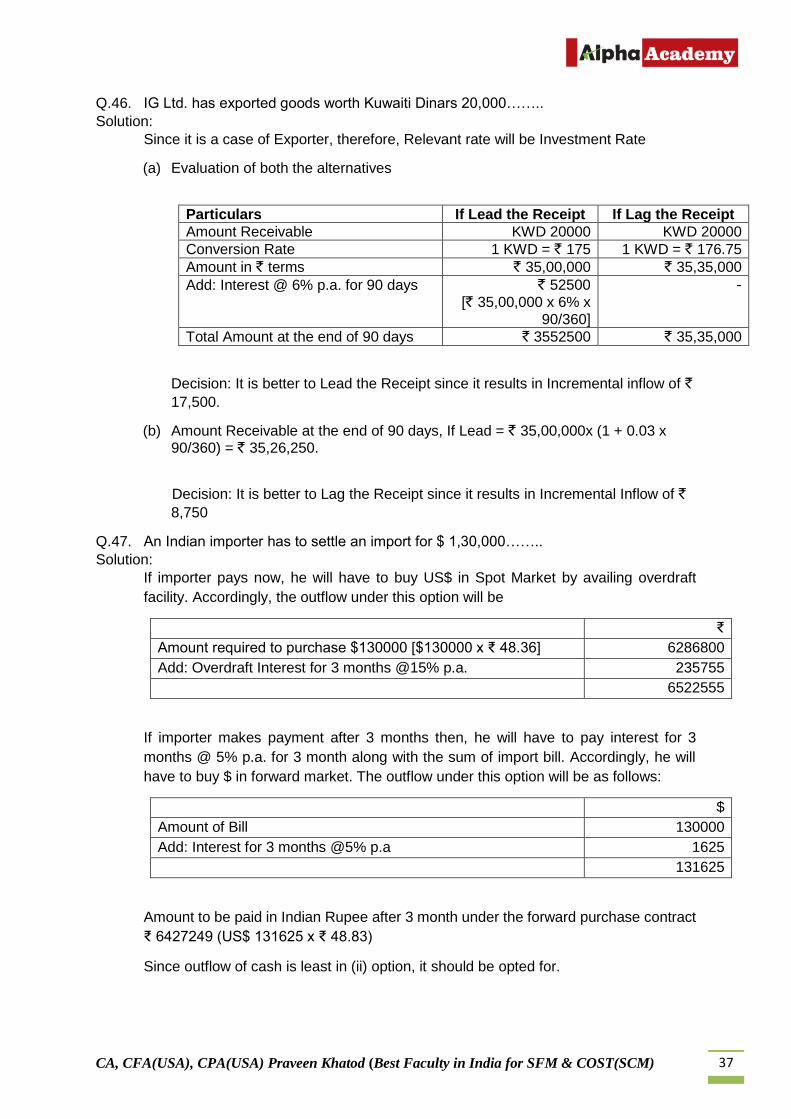

Q.46. IG Ltd. has exported goods worth Kuwaiti Dinars 20,000……..

Solution:

Since it is a case of Exporter, therefore, Relevant rate will be Investment Rate

(a) Evaluation of both the alternatives

Particulars If Lead the Receipt If Lag the Receipt

Amount Receivable KWD 20000 KWD 20000

Conversion Rate 1 KWD = ` 175 1 KWD = ` 176.75

Amount in ` terms ` 35,00,000 ` 35,35,000

Add: Interest @ 6% p.a. for 90 days ` 52500

[` 35,00,000 x 6% x

90/360]

-

Total Amount at the end of 90 days ` 3552500 ` 35,35,000

Decision: It is better to Lead the Receipt since it results in Incremental inflow of `

17,500.

(b) Amount Receivable at the end of 90 days, If Lead = ` 35,00,000x (1 + 0.03 x 90/360) = ` 35,26,250.

Decision: It is better to Lag the Receipt since it results in Incremental Inflow of `

8,750

Q.47. An Indian importer has to settle an import for $ 1,30,000……..

Solution:

If importer pays now, he will have to buy US$ in Spot Market by availing overdraft

facility. Accordingly, the outflow under this option will be

₹

Amount required to purchase $130000 [$130000 x ₹ 48.36] 6286800

Add: Overdraft Interest for 3 months @15% p.a. 235755

6522555

If importer makes payment after 3 months then, he will have to pay interest for 3

months @ 5% p.a. for 3 month along with the sum of import bill. Accordingly, he will

have to buy $ in forward market. The outflow under this option will be as follows:

$

Amount of Bill 130000

Add: Interest for 3 months @5% p.a 1625

131625

Amount to be paid in Indian Rupee after 3 month under the forward purchase contract

₹ 6427249 (US$ 131625 x ₹ 48.83)

Since outflow of cash is least in (ii) option, it should be opted for.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 38

Q.49. The following 2-way quotes appear in the foreign exchange market…..

Solution:

(i) US $ required to get ₹ 25 lakhs after 2 months at the Rate of ₹ 47/$

Therefore, ₹ 25,00,000

₹ 47 = US $ 53191.489

(ii) ₹ required to get US$ 2,00,000 now at the rate of ₹ 46.25/$

Therefore, US $ 200,000 x ₹ 46.25 = ₹ 92,50,000

(iii) Encashing US $ 69000: now vs 2 month later

Proceed if we can encash in open mkt $ 69000 x ₹ 46 = ₹ 31,74,000

Opportunity gain

= 31,74,000 x10

100 x

2

12 ₹ 52 900

Likely sum at end of 2 months 32,26,900

Proceeds if we can encash by forward rate:

$ 69000 x ₹ 47.00 32,43,000

It is better to encash the proceeds after 2 months and get opportunity gain.

Q.55. An exporter expects the next remittance of €115,000/-…….

Solution:

By taking forward cover the exporter freezes his receipt at € 1,15,000 x ₹ 67 = ₹

77,05,000.

• If the spot rate turns out to be higher at ₹ 68 he misses out on receiving the extra

₹ 1,15,000. This is because under the forward contract he is obliged to sell at ₹

67.

• If the spot rate was lower at ₹ 66 and had he not taken forward cover, he would

have received Re 1 per € less, i.e. he would have received ₹ 1,15,000 less.

Hence, he has gained by forward cover.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 39

Q.58. You, a foreign exchange dealer of your bank, are informed that……

Solution:

Amount realized on selling Danish Kroner 10,00,000 at ₹ 6.5150 per Kroner = ₹

65,15,000.

Cover at London:

Bank buys Danish Kroner at London at the market selling rate.

Pound sterling required for the purchase (DKK 10,00,000 + DKK 11.4200) = GBP

87,565.67 Bank buys locally GBP 87,565.67 for the above purchase at the market

selling rate of ₹ 74.3200.

The rupee cost will be = ₹ 65,07,88

Profit (₹ 65,15,000 - ₹ 65,07,881) = ₹ 7,119

Cover at New York:

Bank buys Kroners at New York at the market selling rate.

Dollars required for the purchase of Danish Kroner (DKK10,00,000/7.5670)

= USD 1,32,152.77

Bank buys locally USD 1,32,152.77 for the above purchase at the market selling rate

of ₹ 49.2625.

The rupee cost will be = ₹ 65,10,176.

Profit (₹ 65,15,000 - ₹ 65,10,176) = ₹ 4,824

The transaction would be covered through London which gets the maximum profit of ₹

7,119 or lower cover cost at London Market by (₹ 65,10,176 - ₹ 65,07,881) = ₹ 2,295

Q.60. You are expecting to receive US $ 500,000 any time between…….

Solution:

You are going to receive $. The money may reach you either three months or six

months from today. When you approach the bank with this issue the Bank will take a

conservative view, and will reckon that the worst happens.

Since in the transaction you will sell and the bank will buy dollars, the relevant rate is

Bid rate for $ namely 67.65 and 67.50. The worse rate is ₹ 67.50 (Remember, banker

always wins). This will give you fewer rupees than the rate of 67.65. The bank will

quote a rate of 67.50, for a six month forward option contract, with an option for you to

deliver $ between three and six months.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 40

Q.61. You are expecting to pay SGD 100,000 any time between three and six months……

Solution:

You are going to PAY SGD any time between three months and six months from today.

When you approach the bank with this issue the Bank will take a conservative view,

and will reckon that the worst happens.

Since in the transaction you will buy and the bank sell buy SGD, the relevant rate is

Ask rate for SGD namely 55.00 and 55.35. The worse rate is ₹ 55.35 (Remember,

banker always wins). This will make you pay more rupees than the rate of 55.00. The

bank will quote a rate of 55.35 for a six-month forward option contract, with an option

for you to buy SGD between three and six months.

Q.63. The finance director of P Ltd., has been studying exchange rates…….

Solution:

FORWARD MARKET HEDGE:

Since, we are an importer and we have to pay $ 51 lakh in 3 months, therefore, relevant

rate is Ask rate i.e. 1 $ = ₹ 45

Outflow under forward = $ 51,00 000 x ₹ 45

Cover = ₹ 22,95,00,000

MONEY MARKET HEDGE:

Step-1: Identify

Since, we are an importer, therefore we have FC liability

Step-2: Create

We will create FC denominated asset equivalent to PV of FC denominated liability

discounted at USA deposit rates.

= $ 51,00,000

(1+0.08 x 3/12)

= $ 5000000

Step-3: Borrow

Borrow in India. Since after borrowing ₹ we have to Sell ₹ and Buy $ therefore,

Relevant Rate is Ask Rates.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 41

1$ = ₹ 40 – 42

= $ 50,00,000 x ₹ 42

= ₹ 21 crores

Step-4: Convert

Convert ₹ to $ at spot ask rate.

= $ 21 crores

₹ 42

= $ 50,00,000

Step-5: Invest

Invest in USA, $ 50,00,000 at deposit rate i.e. 8% p.a. for 3 months

Step-6: FV of Borrowings

= ₹ 21,00,00,000 + (₹ 21,00,00,000 x 0.16 x 3

12)

= ₹ 21,84,00,000

Step-7: Settle

Use the proceeds from deposit in USA to meet the import obligation.

Decision: Company should opt for money market hedge strategy, this would meet the

expectation of finance director to achieve a cost not more than ₹ 22,00,00,000.

Q.67. ABC Technologic is expecting to receive a sum of US$ 4,00,000…….

Solution:

The company can hedge position by selling future contracts as it will receive amount

from outside.

Number of Contracts = $ 4,00,000

$ 1,000 = 40 contracts

Gain by trading in futures = (₹ 45 - ₹ 44.50) 4,00,000 = ₹ 2,00,000

Net Inflow after 3 months = ₹ 44.50 x ₹ 4,00,000 + 2,00,000 = ₹ 1,80,00,000

Effective Price realization = ₹ 1,80,00,000

₹ 4,00,000 = ₹ 45 per US$

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 42

Q.72. On march 1, 2015, B Ltd. bought from a foreign firm electronic equipment…….

Solution:

Option (A): Forward hedge

Cost at forward rate = $1,00,000 (9,00,000/9)

Cost at current spot rate = $ 90,000 (9,00,000/10)

Exchange Loss = $ 1,00,000 - $ 90,000 = $ 10,000

Tax shield on exchange loss = $10,000 x 0.40 = $ 4000

Net Cost of using forward market = $ 1,00,000 - $ 4000 = $ 96000

Option (B): Money Market Hedge

Post tax interest rates in US and LC are 7.2% and 4.8% respectively. Each LC

deposited at 4.8% now grows into LC 1.012 in 3 months.

A Inc, should buy and invest LC 8,89,328 (9,00,000/1.012) for 3 months

Spot purchase and deposit at 4.8% (LC) 8,89,328

Payment accumulated of LC deposits to make payment to LC Supplier 9,00,000

Exchange rate for spot purchase $1 = 10 LC

Borrow US $ at 7.2% to finance spot purchased 88,932.80

Repay $ loan with interest (88,932.80 x 1.018) 90,533.59

Option (C) No hedge

Cost at future spot Rate = $ 1,12,500 (9,00,000/8)

Cost at Current spot rate = $ 90,000 (9,00,000/10)

Exchange loss = $ 1,12,500 - $ 90,000 = $ 22,500

Tax shield on exchange loss = $ 22,500 x 0.40 = $ 9000

Net cost if not hedged = $ 1,12,500 - $ 9,000 = $ 1,03,500.

The money market hedge (Option B) is best.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 43

Q.73. PQ an UK company, has a substantial portfolio of its trade…..

Solution:

Note that this for the is not a pure money market hedge, as no discounting takes place

in order for the amount borrowed to equal the amount due.

(i) Method 1 £

Borrow PV of $ 5 m now and convert into sterling

($ 5,000,000/1.035) = $ 4830918 converted at £ 1 = $ 1.4455 3,342,039

Method 2

Sell $ 5m forward at 1.4165: that is for 3,529,827

Borrow PV of £ 3,529,827 discounted at 5.75% that is

(£ 3,529,827 / 1.0575) 3,337,898

Method 1 gives £ 4,141 more than Method 1, therefore, Method 1 is preferable.

(ii) The spot rate is today's rate. In this question, $ 1.4455 could be exchanged for

£ 1 today.

The forward rate is the rate which could be agreed for delivery at some specified

future date. In this question the bank is agreeing to purchase $ 1.4165 for £ 1 in

12 months' time.

The relationship between the two is a function of interest-rate differentials. In

effect, the bank would protect its position by borrowing $ 1.4455, paying interest

at 3.5 per cent bringing it up to $ 1.4961, then, lending £1 on which it would earn

interest of 5.75 per cent, bringing it up to £ 1.0575. $ 1.4961/ £1.0575 = $ 1.4147

per pound. The bank divides by a higher figure to earn a margin.

Exchange rates and interest rates are subject to such volatility that it is not safe to

regard the forward rate as a reliable predictor of what the spot rate will be at the

appropriate future date. If future spot rates were predictable there would be no

need to hedge. However, it is argued that in the long term the various rates are

reconcilable; for example, a country with relatively high interest rates will cede

growth opportunities to others, and its economy will weaken.

(b) If the dispute is expected to be settled in due course, then the bank is likely to be willing

to extend the arrangement — but at a price which reflects the exchange rate at the

time originally specified. If there is no hope of the debt being settled, then PQ plc will

have to buy currency at the spot rate and deliver it to the bank on the agreed basis.

The actual solution could, of course, be anywhere between these two extremes, and a

`mixed' solution reached.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 44

Q.79. Nitrogen Ltd, a UK company is in the process of negotiating……

Solution:

(i) Receipt under three proposals

(a) Invoicing in Sterling

Invoicing in £ will produce = € 4 million

1.1770 = £ 3398471

(b) Use of Forward Contract

Forward Rate = € 1.1770 + 0.0055 = 1.1825

Using Forward Market hedge Sterling receipt would be € 4 million

1.1825 = £ 3382664

(c) Use of Future Contract

The equivalent sterling of the order placed based on future price (€ 1.1760)

= € 4.00 million

1.1760 = £ 3401360

Number of Contracts = £ 3401360

62,500 = 54 Contracts (to the nearest whole number)

Thus, € amount hedged by future contract will be = 54 x £ 62,500 = £ 3375000

Buy Future at € 1.1760

Sell Future at € 1.1785

€ 0.0025

Total profit on Future Contracts = 54 x € 62,500 x € 0.0025 = € 8438

After 6 months

Amount Received € 4000000

Add: Profit on Future Contracts € 8438

€ 4008438

Sterling Receipts

On sale of € at spot = € 4008438

1.1785 = € 3401305

(ii) Proposal of option (c) is preferable because the option (a) & (b) produces least receipts.

Alternative solution:

Assuming that 6 month forward premium is considered as discount, because generally

premium is mentioned in ascending order and discount is mentioned in descending order.

(i) Receipt under three proposals

(a) Invoicing in Sterling

Invoicing in £ will produce = € 4 milion

1.1770 = £3398471

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 45

(b) Use of Forward Contract

Forward Rate = € 1.1770-0.0055 - 1.1715

Using Forward Market hedge Sterling receipt would be € 4 milion

1.1715 = £ 3414426

(c) Use of Future Contract

The equivalent sterling of the order placed based on future price (€ 1.1760)

= € 4.00 milion

1.1760 = £ 3401360

Number of Contracts = € 3401360

62,500 = 54 Contracts (to the nearest whole number)

Thus, € amount hedged by future contract will be = 54 x £62,500 = £3375000

Buy Future at € 1.1760

Sell Future at € 1.1785

€ 0.0025

Total profit on Future Contracts = 54 x £ 62,500 x € 0.0025 = € 8438

After 6 months

Amount Received € 4000000

Add: Profit on Future Contracts € 8438

€ 4008438

Sterling Receipts

On sale of € at spot = € 4008438

1.1785 = €3401305

(ii) Proposal of option (b) is preferable because the option (a) & (c) produces least receipts.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 46

Q.83. On 15th January you booked a forward sale contract for French Francs……

Solution

Since it is a case of Cancellation of Forward Contract on due date, therefore, Bank will

enter into Opposite Action with the Customer at Spot Merchant Rates.

Calculation of Cancellation Rate

Bid (₹

FFR) = Bid (

₹

$) x Bid (

$

FFR)

= 34.7900 x 1

5.0300

= ₹ 6.92

Interbank bid rate = ₹ 6.92

Less: Margin @ 0.15% = -0.15%

Merchant bank bid rate = ₹ 6.91

Original Action – Sell 1 FFR = ₹ 6.95

Opposite Action – Buy 1 FFR = ₹ 6.91

Gain 1 FFR = ₹ 0.04

Contract amount FFR 2,50,000

Total gain recoverable = ₹ 10000

from customer

Answer: Bank will recover ₹ 10000 from the customer. In addition, bank may also

recover minimum flat charges on account of cancellation request.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 47

Q.86. Suppose you as a banker entered into a forward purchase contract for US$ 50,000….

Solution

Since it is a case of extension of forward contract banker will cancel the original forward

contract by taking opposite action @ 5th June forward contract & will book new forward

contract for 5th July i.e. extended maturity.

Here, at the time of Cancellation, relevant rate is ask rate

Interbank Spot 5th June = 1 $ = ₹ 59.2425

Add: margin = 0.10%

Merchant bank spot 5th June ask rate = 1$ = 59.3017 ~ 59.3025

Original Action – Buy $ 1 = ₹ 59.6000

Opposite Action – Sell $ 1 = ₹ 59.3025

Loss $ 1 = ₹ 0.2975

Contract size = $ 500000

Total loss payable = ₹ 14875

Interbank 5th July bid rate = ₹ 59.6300 (bid rate)

Less: margin = 0.10%

Merchant bank 5th July bid rate = ₹ 59.5704 ~ ₹ 59.5700

Answer: Banker will pay ₹ 14875 to the customer as extension charges & will quote

new forward rate of $ 1 = ₹ 59.5700

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 48

Q.94. The risk free rate of interest in USA is 8% p.a. and in UK is…….

Solution:

2 year Forward Rate will be calculated as follows:

F = S x e(ruk

- rus

)t

Where F = Forward Rate

S = Spot Rate

rUK = Risk Free Rate in UK

rUS = Risk Free Rate in US

t = Time

Accordingly,

F = 0.75e(0.05-0.08)2

= 0.75 x 0.9418

= 0.7064

Thus,

1 US $ = £ 0.7064

If forward rate is 1 US $ = 0.85 £ then an arbitrage opportunity exists. Take following

steps.

(a) Should borrow UK £

(b) Buy US $

(c) Enter into a short forward contract on US $

Accordingly,

The riskless profit would be

(a) Say borrow £ 0.7064e-(0.05) (2) = £ 0.6392 and invest in UK for 2 years.

(b) Now buy US $ at US $ 1e-(0.08)2 = US $ 0.8521, so that after two year

it can be used to close out the position.

(c) After two year the investment in US $ will become US $ 0.8521 e(0.08)

(2) = US $ 0.8521 x 1.1735 = 1 US $

(d) Sell this US $ for £ 0.85 and repay loan of £ 0.6392 along with interest

i.e £ 0.7064.

Thus, arbitrage profit will be

UK £ 0.85 — UK £ 0.7064 = UK £ 0.1436 say UK £ 0.144

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 49

Q.96. Presently, the dollar is worth 140 yen in the spot market…….

Solution:

It has been assumed that we are based in Japan & hence given quotation becomes a

direct quote for us.

1+rh

1+rf =

f1

S0

1+0.04 x 360̅̅ ̅̅ ̅̅

90

1+Rf x 360̅̅ ̅̅ ̅̅90

= 138

140

Rf = 9.85% p.a.

Since, Actual Interest rate (7%) < Fair Interest rate (9.85%), therefore, an investor

should borrow in USA & Invest in japan to earn free arbitrage gain.

Step-1: Borrow: $ 100000

Step-2: Convert:

At spot rate

= $ 100000 x ¥ 140

= ¥ 14000000

Step-3: Invest: In Japan @ 4% p.a. for 90 days

Step-4: Forward cover: Enter into forward over $1 = ¥ 138

Step-5: FV of investment:

= ¥ 14000000 x (1 + 0.04 x 90/360)

= ¥ 14140000

Step-6: Re-convert:

At forward rate agreed earlier

$ 102463.77 = ¥ 14140000

¥ 138

Step-7: Repayment:

The borrowed amount along with interest

= $ 100000 x 1 + .07 x 90

360

= $ 101750

Step-8: Count arbitrage gain:

= $ 102463.77 - $ 101750

= $ 713.77 or ¥ 98500 ($ 713.77 x ¥ 138)

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 50

Q.98. This is the beginning of a new accounting year……….

Solution:

Euroland opportunities: Spot 1 £ = € 1.50 (Indirect quote)

1st year

= 1+rh

1+rf =

S0

F1

= 1+0.06

1+0.05 =

1.50

F1

= F1 = 1.4858

£ 1 = € 1.4858

2nd year

1+rh

1+rf =

F1

F2 alternatively,

(1+rh)2

(1+rf)2 = S0

F2

1.06

1.05 =

1.4858

F2 or,

1.1236

1.1025 =

1.50

F2

F2 = 1.4717 F2 = 1.4718

£ 1 = € 1.4717

3rd year

1+rh

1+rf =

F2

F3

1+0.06

1+0.05 =

1.4717

F3

F3 = 1.4578

1 £ = € 1.4578

4th year

1+rh

1+rf =

F3

F4

1+0.06

1+0.05 =

1.4578

F4

F4 = 1.4440

1 £ = € 1.4440

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 51

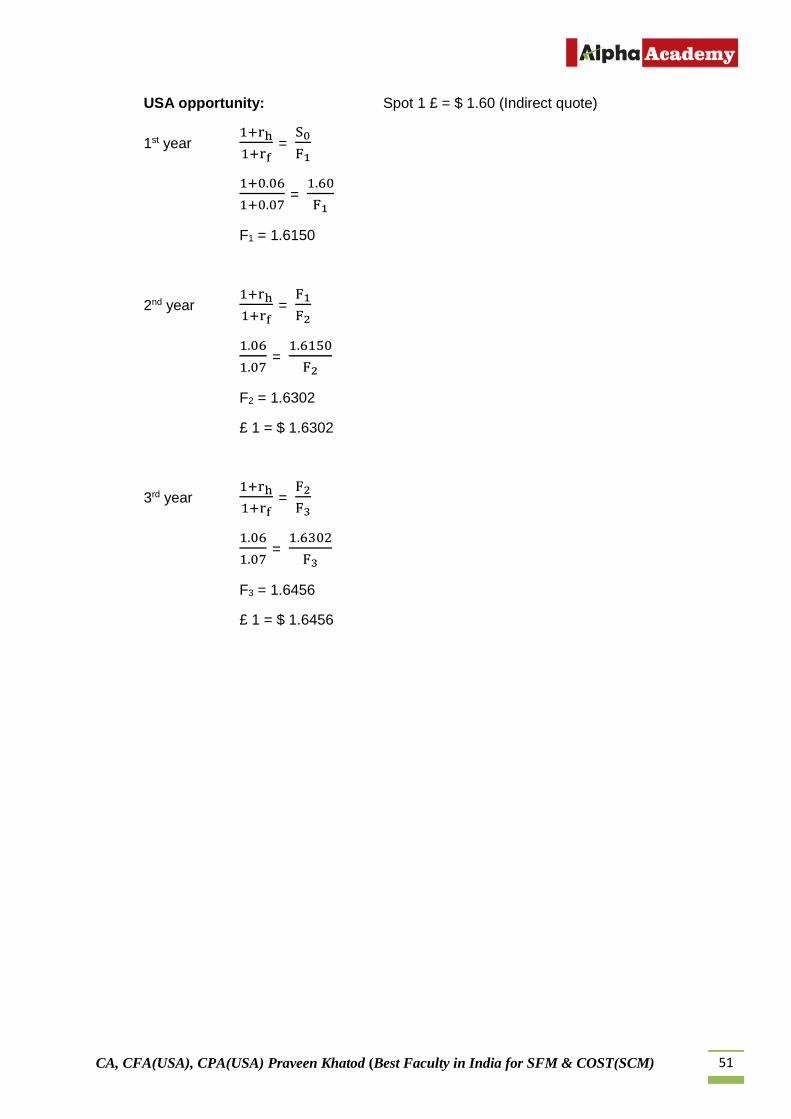

USA opportunity: Spot 1 £ = $ 1.60 (Indirect quote)

1st year 1+rh

1+rf =

S0

F1

1+0.06

1+0.07 =

1.60

F1

F1 = 1.6150

2nd year 1+rh

1+rf =

F1

F2

1.06

1.07 =

1.6150

F2

F2 = 1.6302

£ 1 = $ 1.6302

3rd year 1+rh

1+rf =

F2

F3

1.06

1.07 =

1.6302

F3

F3 = 1.6456

£ 1 = $ 1.6456

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 52

Q.101. The United States Dollar is selling in India at ` 45.50…….

Solution:

(i) According to Interest Rate Parity Theorem, a country whose interest rates are

comparatively lower its currency will appreciate. On the contrary, whose rates

are higher will depreciate. In the present case, USA $ will appreciate & ₹ will

depreciate.

(ii) Using Interest Rate Parity Theorem,

1+rh x n/12

1+rf x n/12 =

F1

S0

1+0.08 x 6/12

1+0.02 x 6/12 =

F1

45.50

F1 = 46.85

1 $ = ₹ 46.85

(iii) % app/dep

On LHS currency i.e. $ = F1−S0

S0 x 100 x

12

n

= 46.85−45.50

45.50 x 100 x

12

6

= 5.93% p.a. Premium on $

On RHS currency i.e. ₹ = S0−F1

F1 x 100 x

12

n

= 45.50−46.85

46.85 x 100 x

12

6

= -5.76% p.a. Discount on ₹

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 53

Q.102. Spot rate 1 US $ =` 48.0123….

Solution:

Spot Rate = ₹ 4000000 /83312 = 48.0123

Forward Premium on US$ = [(48.8190 — 48.0123)/48.0123] x 12/6 x 100

= 3.36%

Interest rate differential = 12% - 8%

= 4% (Negative Interest rate differential)

Since the negative Interest rate differential is greater than forward premium there is a

possibility of arbitrage inflow into India.

The advantage of this situation can be taken in the following manner:

1. Borrow US$ 83312 for 6 months

Amount to be repaid after 6 months

= US $ 83312 (1 + 0.08 x 6/12) = US $ 86644.48

2. Convert US$ 83312 into Rupee and get the principal i.e. ₹ 40,00,000

Interest on Investments for 6 months = ₹ 4000000 x 0.06

= ₹ 240000

Total amount at the end of 6 months = ₹ (4000000 + 240000)

= ₹ 4240000

Converting the same at the forward rate

= ₹ 4240000 / ₹ 48.8190

= US $ 86851.43

Hence the gain is US $ (86851.43 - 86644.48) = US$ 206.95 OR

₹ 10103 i.e., ($ 206.95 x ₹ 48.8190)

Evaluation of Decision to take Covered Interest Rate Arbitrage OR Uncovered Interest

Rate Arbitrage

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 54

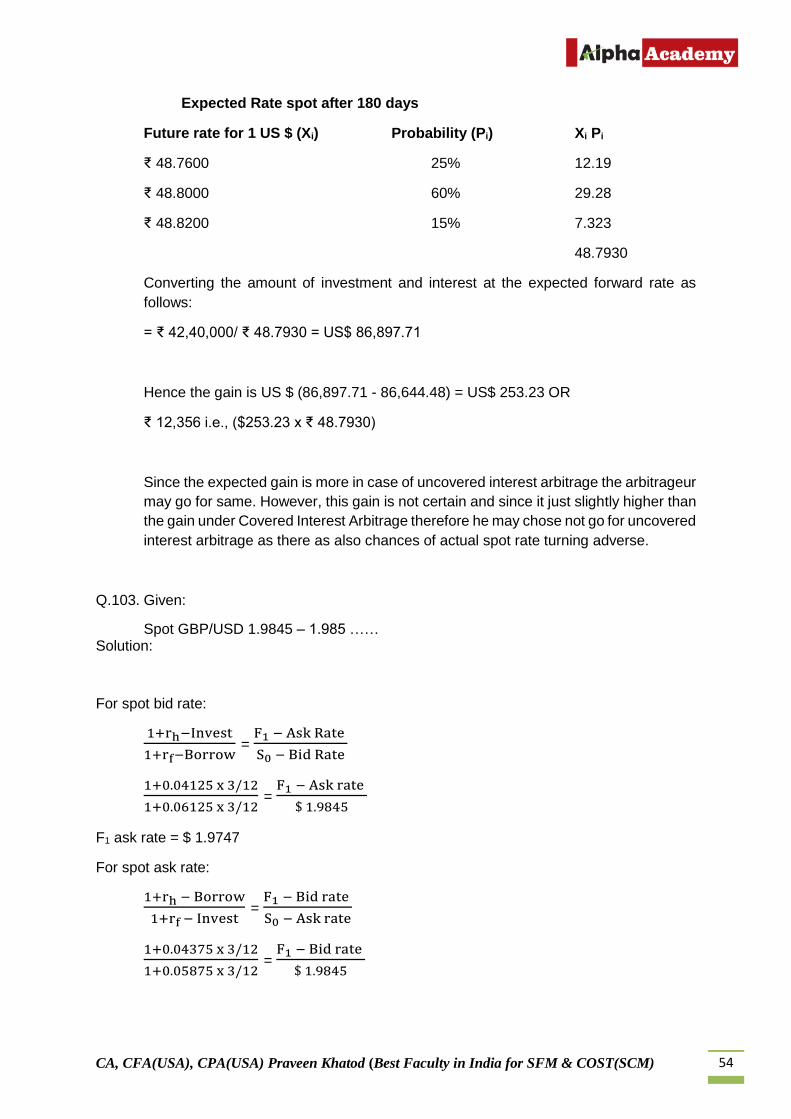

Expected Rate spot after 180 days

Future rate for 1 US $ (Xi) Probability (Pi) Xi Pi

₹ 48.7600 25% 12.19

₹ 48.8000 60% 29.28

₹ 48.8200 15% 7.323

48.7930

Converting the amount of investment and interest at the expected forward rate as

follows:

= ₹ 42,40,000/ ₹ 48.7930 = US$ 86,897.71

Hence the gain is US $ (86,897.71 - 86,644.48) = US$ 253.23 OR

₹ 12,356 i.e., ($253.23 x ₹ 48.7930)

Since the expected gain is more in case of uncovered interest arbitrage the arbitrageur

may go for same. However, this gain is not certain and since it just slightly higher than

the gain under Covered Interest Arbitrage therefore he may chose not go for uncovered

interest arbitrage as there as also chances of actual spot rate turning adverse.

Q.103. Given:

Spot GBP/USD 1.9845 – 1.985 …… Solution:

For spot bid rate:

1+rh−Invest

1+rf−Borrow =

F1 − Ask Rate

S0 − Bid Rate

1+0.04125 x 3/12

1+0.06125 x 3/12 =

F1 − Ask rate

$ 1.9845

F1 ask rate = $ 1.9747

For spot ask rate:

1+rh − Borrow

1+rf − Invest =

F1 − Bid rate

S0 − Ask rate

1+0.04375 x 3/12

1+0.05875 x 3/12 =

F1 − Bid rate

$ 1.9845

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 55

F1 bid rate = $ 1.9747

3 m, F £ 1 = $ 1.9744 or more (ask rate)

3 m, F £ 1 = $ 1.9782 or less (bid rate)

Since, above rates acts as a no arbitrage zone the actual rates should fall in those zones & at

the same time satisfy Bid Ask Rate Rule i.e. Bid Rate < Ask Rate. Since it is not so in the

present case, therefore, we have switched bid rate & ask rates.

Accordingly.

3 m forward rate £ 1 = $ 1.9741 – 1.9782

Spot rate £ 1 = $ 1.9845 – 1.9855

Swap points = 98 - 73

Q.107. Following are the spot exchange rates quoted in three different forex markets…..

Solution:

The arbitrageur can proceed as stated below to realize arbitrage gains.

(i) Buy ₹ 1 from USD 10,000,000

At Mumbai 48.3 x 10,000,000

₹ 483,000,000

(ii) Convert ₹ 1 to GBP at London 483,000,000

77.52 GBP 6,230,650.155

(iii) Convert GBP to USD at New York

6,230,650.155 x 1.6231 USD = 10,112,968.26

There is net gain of USD = 10,112968.26 less 10,000,000

i.e USD = 112,968.26

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 56

Q.108. Following are the foreign exchange rates:

$1 = ` 40.50 / 40.75….…

Solution:

Step 1: Calculation Cross currency rates using any 2 quotations say:

$ 1 = ₹ 40.50 – 40.75

$ 1 = £ 0.60 – 0.61

Bid rate (₹

£) = B (

₹

$) x B (

$

£)

= 40.50 x 1

0.61

= 66.39

Ask rate (₹

£) = ask rate (

₹

$) x ask rate (

$

£)

= 40.75 x 1

0.60

= 67.92

Therefore, £ 1 = ₹ 66.39 – 67.92 (Cross Currency)

However, £ 1 = ₹ 65 – 66 (actual quote)

Step-2: Check for Overlapping exchange rate concept to identity arbitrage

Since the Bid rate of Cross (₹ 66.39) > Ask rate of Actual quote, therefore there

exists arbitrage opportunity.

To earn risk free arbitrage gains, an arbitrageur should Buy £ with ₹ under

Actual Quote and Sell them under Cross Currency Quote.

Proof of Arbitrage:

Let us assume an arbitrageur has ₹ 100000 with him

Convert ₹ 100000 into £ = £ 1515.15

[₹ 100000/66]

Convert £ 1515.15 into $ = $ 2483.85

[£ 1515.15/0.61]

Convert $ 2483.85 into ₹ = ₹ 100596.13

[$ 2483.85 x ₹ 40.50]

Net arbitrage gain = ₹ 100596.13 - ₹ 100000

= ₹ 596.13

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 57

Q.110. Imagine that the current Yen/Euro rate is Yen 120…….

Solution:

Today spot rate € 1 = ¥ 120, assuming we are based in Japan so given quote becomes

a direct quote for us:

Year 1 1+Ih

I+If =

Expected S1

S0

1.06

1.03 =

E(S1)

120

E(S1) 1 € = ¥ 123.4951 ~ ¥ 123.50

Year 2 1+Ih

I+If =

E(S2)

E(S1)

1.03

1.05 =

ES2

123.50

E(S2) 1 € = ¥ 121.1476 ~ ¥ 121.15

Year 3 1+Ih

I+If =

E(S3)

E(S2)

1.035

1.03 =

ES3

121.15

E(S3) 1 € = ¥ 121.7381 ~ ¥ 121.74

Q.114. In International Monetary Market……

Solution:

Buy £ 62500 x 1.2806 = $ 80037.50

Sell E 62500 x 1.2816 = $ 80100.00

Profit $ 62.50

Alternatively, if the market comes back together before December 15, the dealer could

unwind his position (by simultaneously buying £ 62,500 forward and selling a futures

contract. Both for delivery on December 15) and earn the same profit of $ 62.5.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 58

Q.117. On January 28, 2005 an importer customer requested a Bank to remit Singapore Dollar

(SGD) 25,00,000 under an irrevocable LC. ……

Solution:

On January 28, 2005 the importer customer requested to remit SGD 25 lakhs.

To consider sell rate for the bank:

US $ = ₹ 45.90

Pound 1 = US $ 1.7850

Pound 1 = SGD 3.1575

Therefore, SGD 1 = ₹ 45.90∗ 1.7850

SGD 3.1575

SGD 1 = ₹ 25.9482

Add: Exchange margin (0.125%) ₹ 0.0324

₹ 25.9806

On February 4, 2005 the rates are

US $ = ₹ 45.97

Pound 1 = US $ 1.7775

Pound 1 = SGD 3.1380

Therefore, SGD 1 = ₹ 45.97∗ 1.7775

SGD 3.1380

SGD 1 = ₹ 26.0394

Add: Exchange margin (0.125%) ₹ 0.0325

₹ 26.0719

Hence, loss to the importer

= SGD 25,00,000 (₹ 26.0719 - ₹ 25.9806) = ₹ 2,28,250

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 59

Q.135. Diva Jewellery Exporters, Delhi received orders…….

Solution:

WN#1 Calculation of Cross Currency Rates between ₹ and €

The relevant rate is Bid Rate since we have to sell €

If exposure is hedged

Bid Rate: ₹

€ =

₹

$ x

$

€

For January = 46.04 x 1.2803 = 58.945

For February = 46.11 x 1.2800 = 59.0208

For March = 46.13 x 1.2828 = 59.175564

If exposure is left uncovered

Bid Rate: ₹

€ =

₹

$ x

$

€

For January = 45.98 x 1.2786 = 58.790028

For February = 46.05 x 1.2806 = 58.97163

For March = 46.07 x 1.2811 = 59.020277

(i) If the exposure is hedged

Calculation of Expected Inflow under both the Invoicing Currency options

Month If Invoice in $ If Invoice in €

US$ Conversion

Rate

Equivalent

₹

€ Conversion

Rate

(Refer

WN#1)

Equivalent

₹

January 63950 $ 1 = ₹

46.04

2944258 50000 € 1 = ₹

58.945

2947250

February 96100 $ 1 = ₹

46.11

4431171 75000 € 1 = ₹

59.0208

4426560

March 128150 $ 1 = ₹

46.13

5911560 100000 € 1 = ₹

59.175564

5917556

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 60

Choice of Currency for invoicing, if hedging is done

January – €

February – $

March – €

(ii) If the exposure is left uncovered

Calculation of Expected Inflow under both the Invoicing Currency options

Month If Invoice in $ If Invoice in €

US$ Conversion

Rate

Equivalent

₹

€ Conversion

Rate

(Refer

WN#1)

Equivalent

₹

January 63950 $ 1 = ₹

45.98

2940421 50000 € 1 = ₹

58.790028

2939501

February 96100 $ 1 = ₹

46.05

4425405 75000 € 1 = ₹ 58.97163

4422872

March 128150 $ 1 = ₹

46.07

5903871 100000 € 1 = ₹

59.020277

5902028

Choice of Currency for invoicing, if hedging is done

January – $

February – $

March – $

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 61

Q.138. Task PLC is a UK based exporter. It…….

Solution:

Evaluation of MMH

Step 1: Identify

• The company has a foreign currency asset for $350,000.

Step 2: Create

• We must now create a liability

Step 3: Borrow

• Borrow in $ an amount which will mature in value to $ asset of Step 1

• Rate: 9% per annum or 2.25% per quarter.

• Borrowing: $ 350,000 / 1.0225 = S 342,300.

Step 4: Convert

• Sell $ and buy £.

• The relevant rate is the Ask rate, namely, 1.5905 per £.

• £ s received on conversion is (£ 342,300 /1.5905) = 215,215

Step 5: Invest

• £ 215,215 will be invested at 5% for 3 months

Step 6: Future Value

• FV of Investment = £ 217,904 [£ 215,2 l 5 x 1.0125]

Step 7: Settle

• The liability of $ 342,300 @ 2.25% per quarter matures to $ 350,000. This

will be settled with the amount of $ 350,000 receivable from customer.

Evaluation of Forward Cover

WN 1: Realization if forward contract is used

• Applicable rate is the 3-month Forward Ask Rate; $ 1.6140 per £

• Realization three months later = £ 350,000 / 1.6140. = £ 216,852

WN 2: Comparison of the two hedges

Under money market hedge, the amount is received NOW. Under forward contract,

money is received in future. We can compare these two figures, by either discounting

the "future receipts to its present value", or by compounding the spot receipts to its

"future value". We use the three-month deposit rate (at 5% p.a.) to compound the

present receipts, thus making it comparable to receipts under forward market rates.

Amount received by the company Now (£) 3 months later (£)

Forward Market 2,16,852

Money market hedge 2,15,214 2,17,904

Decision:

Money Market Hedge gives a higher £ realization and should be preferred.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 62

Q.139. Bask PLC is a UK based importer. It has………

Solution:

Part (a)

Step 1: Identify

• Transaction is import.

• Foreign currency liability of $ 350,000 exists

Step 2: Create

• We must create a Dollar Asset. To this end, importer has to generate dollar

funds.

Step 3: Borrow

• Borrow in Home Currency, Pounds, an amount equivalent to the PV of $

asset of 350,000.

• $ Deposit rate for applicable period is 2.5%.

• Amount of Borrowing = Present value of $ 350,000 discounted at 2.5% is $

3,41,463.

Step 4: Convert

• Relevant rate is spot Bid rate (Indirect quote; bid is on pounds) = 1.5865

• Actual borrowing $ 341,463 / 1.5865 would be £ 2,15,230.

Step 5: Invest

• The $ 3,41,463 is invested for 6 months at 2.5% per half year

Step 6: Future Value

• FV of Borrowing = £ 2,24,916 (£ 2,15,230 x (1 + 0.09 x 6/12))

Step 7: Settle

• $ Asset of 341,463 matures to $ 350,000

• This is used to settle the $ liability of 350,000 of Step 1

Part (b):

Compare the money market hedge and forward rate: We compare cost of purchase of

$ to yield maturity proceeds equivalent to import liability, and forward contract rates.

6 months later

Forward Market 2,25,733 (3,50,000/1.5505)

Money Market Hedge 2,24,916*

Decision: Maturity value of the cost of £-funds under money market hedge is lower

than quantum of £s involved for performing forward exchange contract at 1.5505.

Hence we must opt for money market hedging.

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 63

Q.157. Given the following information:

Solution:

In this case, DM is at a premium against the Can$.

Premium = [(0.67 — 0.665) /0.665] x (12/3) x 100 = 3.01 per cent

Interest rate differential = 9-7 = 2 per cent.

Since the interest rate differential is smaller than the premium, it will be profitable to

place money in Deutschmarks the currency whose 3-months interest is lower.

The following operations are carried out:

(i) Borrow Cans 1000 at 9 per cent for 3- months;

(ii) Change this sum into DM at the spot rate to obtain DM

= (1000/0.665) = 1503.7

(iii) Place DM 1503.7 in the money market for 3 months to obtain a sum of DM

Principal: 1503.70

Add: Interest @ 7% for 3 months = 26.30

Total 1530.00

(iv) Sell DM at 3-months forward to obtain Can$= (1530x0.67) = 1025.1

(v) Refund the debt taken in Cans with the interest due on it, i.e.,

Can$

Principal 1000.00

Add: Interest @9% for 3 months 22.50

Total 1022.50

Net arbitrage gain = 1025.1 - 1022.5 = Can$ 2.6

CA, CFA(USA), CPA(USA) Praveen Khatod (Best Faculty in India for SFM & COST(SCM) 64

Q.160. You are given the following information by your banker:

Solution:

We have to work out the $/£ cross rates

$/£bid rate = ($/₹)bid x (₹/£)bid

= 1

(₹/$)ask x (₹/£)bid

= 1

48.75

= 1.4523

$/£ask rate = ($/₹)ask x (₹/£)ask

= 1

(₹/$)bid x (₹/£)ask

= 1

48.70

= 1.4548

$/£ cross rate = 1.4523/1.4548

Similarly we can work out the 6 months forward rate

(72.40