DEMAND ONE OF THE KEYS OF CAPITALISM. WHAT IS DEMAND? Demand is the willingness and ability to buy a...

21

DEMAND ONE OF THE KEYS OF CAPITALISM

-

Upload

rhoda-hart -

Category

Documents

-

view

221 -

download

0

Transcript of DEMAND ONE OF THE KEYS OF CAPITALISM. WHAT IS DEMAND? Demand is the willingness and ability to buy a...

DEMAND

ONE OF THE KEYS OF CAPITALISM

WHAT IS DEMAND?• Demand is the willingness and ability to buy a product.• It is both a microeconomic and macroeconomic concept.

• Introduction to Demand

• Demand Schedule for Infiniti Automobiles• Price (x 1000) Quantity Demanded (x 1000) • $ 75 5 $75 DEMAND CURVE• 70 8 • 65 15 • 60 20 • 55 27 • 50 38 price • 45 80• 40 90 • 35 130• 30 200 • 0 INF 0• QD 200

A (60, 20)

B ( 30, 200)

LAW OF DEMAND• As price increases, demand decreases. As price decreases, demand increases.• In economic terms: the quantity demanded of goods

and services varies inversely with its price.

• Foundations for the Law of Demand• The Law of Demand has been proven in almost all

studies.• Price is an obstacle which discourages consumers.• It is also demonstrated every time a store has a sale.

• Fallacies concerning the Law of Demand• 1. “Change –over-time” fallacy• 2. Paradoxical Demand Theory

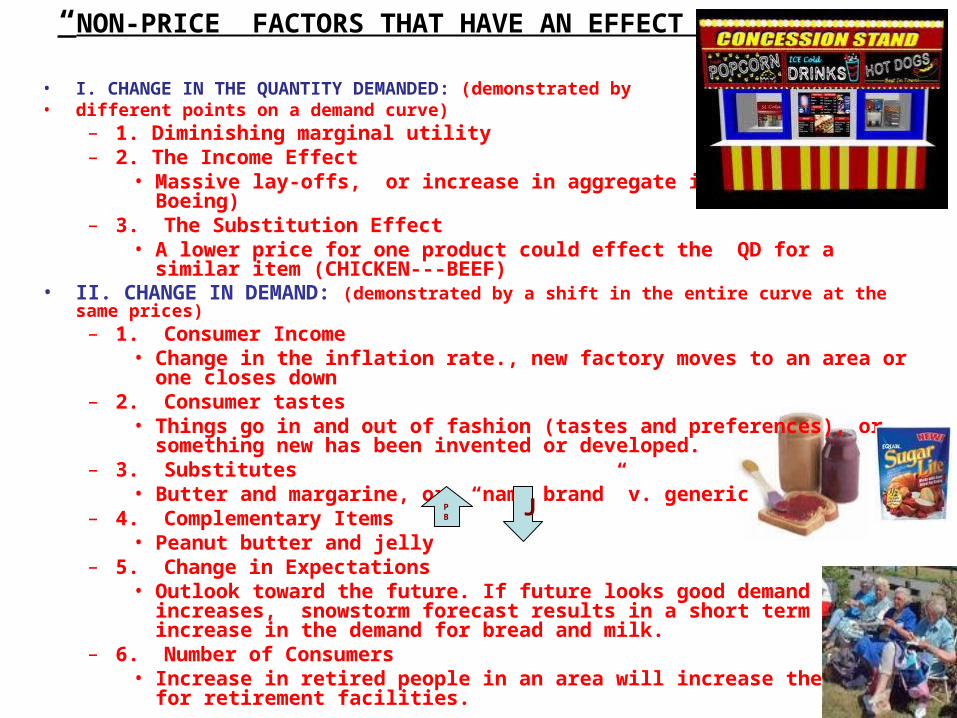

“NON-PRICE” FACTORS THAT HAVE AN EFFECT ON DEMAND

• I. CHANGE IN THE QUANTITY DEMANDED: (demonstrated by • different points on a demand curve)

– 1. Diminishing marginal utility– 2. The Income Effect

• Massive lay-offs, or increase in aggregate income (BMW or Boeing)– 3. The Substitution Effect

• A lower price for one product could effect the QD for a similar item (CHICKEN---BEEF)

• II. CHANGE IN DEMAND: (demonstrated by a shift in the entire curve at the same prices)– 1. Consumer Income

• Change in the inflation rate., new factory moves to an area or one closes down

– 2. Consumer tastes• Things go in and out of fashion (tastes and preferences), or something

new has been invented or developed.– 3. Substitutes

• Butter and margarine, or “name brand” v. generic– 4. Complementary Items

• Peanut butter and jelly – 5. Change in Expectations

• Outlook toward the future. If future looks good demand increases, snowstorm forecast results in a short term increase in the demand for bread and milk.

– 6. Number of Consumers • Increase in retired people in an area will increase the demand for

retirement facilities.

PB

J

EFFECT OF SUPPLY, DEMAND AND PRICE ON THE MARKET

ELASTICITY OF DEMAND• How sensitive is demand to a change in price?

• The demand is elastic when a change in price causes a relatively larger change in quantity demanded.

– Jewelry, clothing, vegetables, ice cream, meat, coffee, sugar

• The demand is inelastic when a change in price causes a relatively small change in the quantity demanded.

• [But the market must be noted—is it nationwide or local]– Gasoline, bread, milk, salt, medical services, candy

• Demand is unit elastic when there is a one-to-one (proportional) change in demand based on price.

• Total Receipts Test for Elasticity: • Formula• Compare Total Receipts of pt. A with pt. B• TR= P X QD • If P and TR move in the same direction the product is inelastic. • If P and TR move opposite then the product is elastic. • If change in P results in no change in TR then the product is unit elastic.

• CALCULATE THE ELASTICITY OF DEMAND:

QD/QS

0 1 2 3 4 5 6 7 8 9

7

6

5

4

3

2

1

PRICE

A

B

Qd/qs

1 2 3 4 5 6 7 8 9

5

4

3

2

1

0

P

R

I

C

EA

B

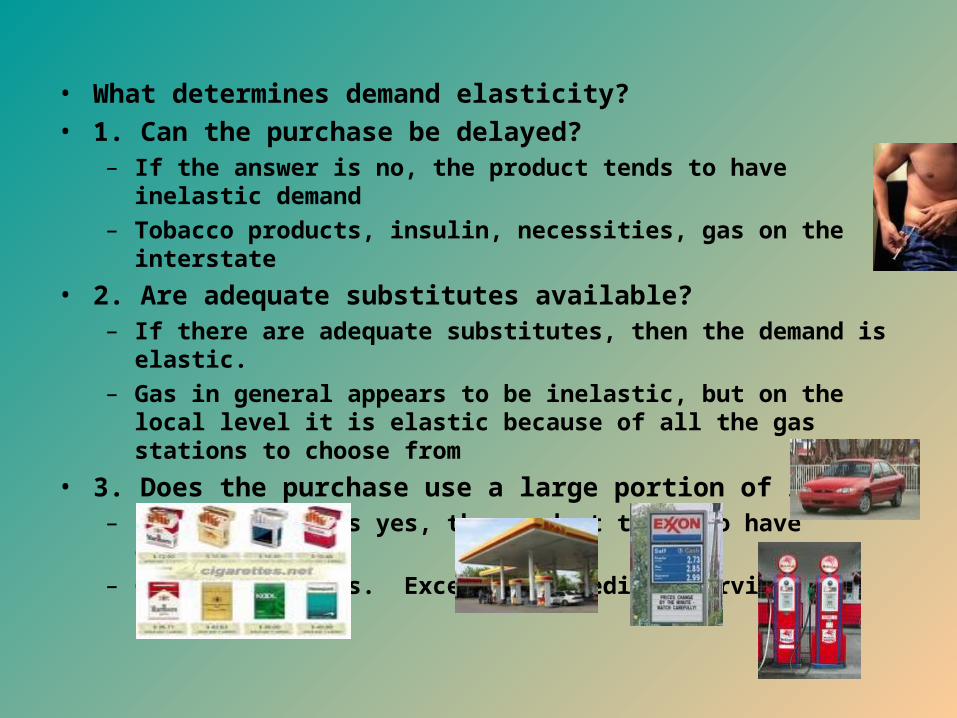

• What determines demand elasticity?• 1. Can the purchase be delayed?

– If the answer is no, the product tends to have inelastic demand

– Tobacco products, insulin, necessities, gas on the interstate

• 2. Are adequate substitutes available?– If there are adequate substitutes, then the demand is elastic.

– Gas in general appears to be inelastic, but on the local level it is elastic because of all the gas stations to choose from

• 3. Does the purchase use a large portion of income?– If the answer is yes, the product tends to have elastic demand.

– Cars, appliances. Exceptions: medical services

SUPPLY

• WHAT IS IT??

PRODUCER

CONSUMER

LAW OF SUPPLY

• The amount supplied of a product increases as price increases.• The Supply Schedule

• Price Quantity Supplied• $30 350• 25 305• 20 235• 15 140• 10 60• 5 0

• SUPPLY CURVE

CHANGE IN THE QUANTITY SUPPLIED

• Quantity supplied is the amount that producers bring to the market at any given price.

• Factors that cause a change in supply:• 1. cost of inputs (raw materials)• 2. productivity levels (lack of or increase in technology)• 3. taxes and/or the level of government subsidies• 4. Number of Sellers• 5. Future expectations

– Price of oil increasing– Bad forecast for wheat—affect bread producers

• 6. Government regulations– Govt. mandate 45 mpg by 2015– Carbon emissions reduction by 50% by 2020

• ELASTICITY OF SUPPLY– Elasticity of Supply is a measure of the way quantity supplied adjusts to a

change in price– Elastic= small increase in price—large increase in supply– Inelastic= small increase in price—little change in supply– Unit=change in price results in a proportional change in supply.

DecreaseIn supply

Increase insupply

ChangeIn theQuantitysupplied

DETERMINANTS OF SUPPLY ELASTICITY

• 1. If companies can respond quickly to an increase price then the elasticity of supply is elastic. – Usually they are products that are relatively easy to produce.—

candy, paper products, etc.• 2. Conversely, if a product takes longer to produce or is more difficult

to make it is more likely to have inelastic supply.—drilling for oil, making more cars, high tech products., consumer durables, food.– Things like substitutes, delay of purchase, % of consumer income

have no bearing on the elasticity of supply—it is purely price.

• THE THEORY OF PRODUCTION• Deals with the relationship between the factors of production and the

output of goods and services.• This theory is based on the short run and only one variable

changed [ labor], and not on the long run—where all the factorschange.

LAW OF VARIABLE PROPORTIONSThis law states that in the short run output will change as one input is

varied while the others are held constant.

How is the output of the final product affected as more units of variable of input or resource are added to a fixed amount of other resources?

(EX)--Farmer changing the brand of fertilizer used while all other factors of growing a crop stay the same.—What will the result be??

THE PRODUCTION FUNCTION

This an illustration of the Law of Variable Proportions. Figure 5.5i

Stage 1= # of workers increase for better

efficiency. Marginal product increases.

Stage 2= Marginal product continues to

rise as new workers are added but not

by as much. Output has reached the point

of diminishing returns.

Stage 3= Here marginal product becomes

negative and the total output decreases.

l l

Stage 1

Stage 2

Stage 3

Diminishingreturns Negative

Returns

COST, REVENUE AND PROFIT MAXIMIZATION• MEASURES OF COST:

• 1. Fixed Costs– These are costs one pays whether a product is being produced or not.– Overhead– Salaries for “salaried” personnel, interest on bonds, rent or mortgage

payments, property taxes– Depreciation

• 2. Variable Costs– Wages for hourly employees– Utility costs– Shipping costs

• 3. Total Cost– The total of fixed and variable costs

• 4. Marginal Costs– This is the cost of the “extra” workers hired to produce additional products.

VC divided by Marginal Product = marginal cost– #Wrks

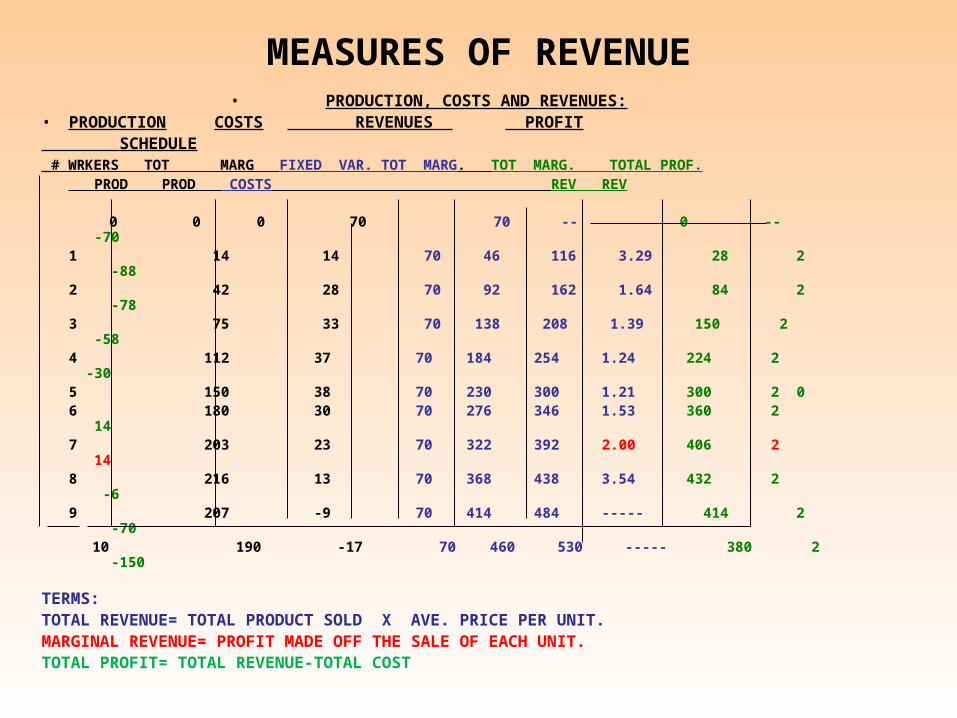

MEASURES OF REVENUE• PRODUCTION, COSTS AND REVENUES:

• PRODUCTION COSTS REVENUES PROFIT SCHEDULE # WRKERS TOT MARG FIXED VAR. TOT MARG. TOT MARG. TOTAL PROF.

PROD PROD COSTS REV REV

0 0 0 70 70 -- 0 -- -701 14 14 70 46 116 3.29 28 2 -882 42 28 70 92 162 1.64 84 2 -783 75 33 70 138 208 1.39 150 2 -584 112 37 70 184 254 1.24 224 2 -305 150 38 70 230 300 1.21 300 2 0 6 180 30 70 276 346 1.53 360 2 147 203 23 70 322 392 2.00 406 2 148 216 13 70 368 438 3.54 432 2 -69 207 -9 70 414 484 ----- 414 2 -70

10 190 -17 70 460 530 ----- 380 2 -150

TERMS:TOTAL REVENUE= TOTAL PRODUCT SOLD X AVE. PRICE PER UNIT. MARGINAL REVENUE= PROFIT MADE OFF THE SALE OF EACH UNIT.TOTAL PROFIT= TOTAL REVENUE-TOTAL COST

12

3

APPLYING COST PRINCIPLES

• COSTS OF A SELF-SERVICE GAS STATION (EX)– 7 GAS PUMPS (6 gasoline and 1 diesel)

– 1 WORKER PER SHIFT, IN SMALL ENCLOSED BOOTH

• HIGH FIXED COSTS

• RELATIVELY SMALL VARIABLE COSTS

• RATIO OF FIXED TO VARIABLE COSTS IS LOW

• STORE PROBABLY OPEN 24/7/365

• COSTS OF INTERNET STORE (EX)INDIVIDUAL

LOW OVERHEAD

WEB ACCESS

E-COMMERCE SOFTWARE

LOW INVENTORY

SPECIALTY WAREHOUSES

SHIP THE PRODUCT

• Marginal Revenue = the change in total revenue divided by marginal product.

• Marginal analysis involves comparing the costs and benefits of decisions that are made in small incremental steps.

• Break even point is the total output the business needs to sell in order to cover its total costs.

• Adding the 8th worker is where the total profit begins to drop.• The profit-maximizing quantity of output= marginal cost and

marginal revenue are equal.

• THE PRICE SYSTEM AT WORK• Price Adjustment Process: The market is voluntary, and benefits both.

• Price Q. demanded Q. Supplied Surplus/shortage

• $1.50 50 150 +100

• 1.25 75 140 +65

• 1.00 110 120 +10

• .75 115 115 ___

• .50 130 100 -30

• .25 200 75 -125

• DEMAND AND SUPPLY CURVES

EQUILIBRIUM• MARKET EQUILIBRIUM

– A SITUATION IN WHICH PRICES ARE RELATIVELY STABLE AND THE QUANTITY OF GOODS AND SERVICES ARE EQUAL TO DEMAND.

• SURPLUS– QUANTITY SUPPLIED IS GREATER THAN DEMAND. SURPLUSES

FORCE PRICES DOWN.• SHORTAGE

– QUANTITY SUPPLIED IS LESS THAN DEMAND. SHORTAGES FORCE PRICES UP.

• EQUILIBRIUM PRICE– THIS IS THE PRICE THAT “CLEARS THE MARKET” BY LEAVING

NEITHER A SURPLUS NOR SHORTAGE AT THE END OF A TRADING PERIOD.

• THE COMPETITIVE PRICE THEORY• PRICES CAN VARY BECAUSE OF: - ADVERTISING• - LOCATION (GAS STATIONS).• - FUTURE EXPECTATIONS• BUT PRICES TEND TO BE REASONABLY COMPETITIVE.• THE MARKET ECONOMY “RUNS ITSELF”.

Change In Supply Change In Demand

D1 S2 S1

D1

D2 S1

Decrease in supply results ina shortage, which forces pricesup.

Increase in demand has resulted again in a shortagewhich has forced prices up.

x

x

xx

EQUILIBRIUM PRICE

S1D1

Decrease in demand has resulted in a surplus of supply therefore forcing prices down.

D2

x

X