Demand and Supply

42

Slide 1 of 42 Demand and Supply “Talk is cheap because supply exceeds demand.” -Author Unknown

-

Upload

lumen-learning -

Category

Education

-

view

27 -

download

0

Transcript of Demand and Supply

Slide 1 of 42

Demand and Supply

“Talk is cheap because supply exceeds demand.”-Author Unknown

Slide 2 of 42

Demand and Supply

As we will learn in this module, prices and quantities are determined by participants in each market.

But who are the participants?HouseholdsBusinesses

Slide 3 of 42

These participants interact to determine what is produced and how much it costs!

BusinessBuy ResourcesSell Products

HouseholdsSell ResourcesBuy Products

Resource Market

Product Market

Goods & Services

Land

, L

abor

, C

apita

l, E

ntre

pren

eurs

Goo

ds & S

ervices

Resources

Wages, Rents, Interest, profitsC

onsumptio

n E

xpenditu

res

Costs

Revenue

Participants include businesses and households

Households sell resources to businesses in exchange for payment. They use these

payments to purchase products.

Slide 4 of 42

So what is demand?

A schedule or curve that shows the quantity of a product that customers (households) would purchase at a

given set of possible prices in a particular time.

Slide 5 of 42

An example of a demand schedule

Imagine that I talked to every consumer in an economy (or in this class) and found out what quantity of a good they

would want at particular prices. Perhaps that survey would generate the following results:

At a price of $10, no one would want this good

At a price of $2, 8 units would be demanded

We could plot these data points to see a “demand curve” as is

done on the next slide…

Slide 6 of 42

Demand Curve – price (P) and quantity demand (Qd) have a negative relationship

Note: market demand is the sum of each individual demand

This is the Demand curve

A red box like this usually means that this information is important and will appear on

your test!

Notice the “downward slope” suggesting that as price

increases, consumer want less of this item. This leads us to the

law of demand…

The Law of Demand- All else equal, as price falls, the

quantity demanded increases and as price rises, the

quantity demanded decreases

Slide 7 of 42

Let’s turn our attention to supply

Imagine that I talked to every company in an economy and found out what quantity of a good they would produce at particular prices. Perhaps

the table below would summarize my findings:

We could plot these data points to see a “supply curve” as is done on the next slide…

At a price of $10, producers may be

excited and want to supply 10 units

At a price of $2, only 2 units would be supplied

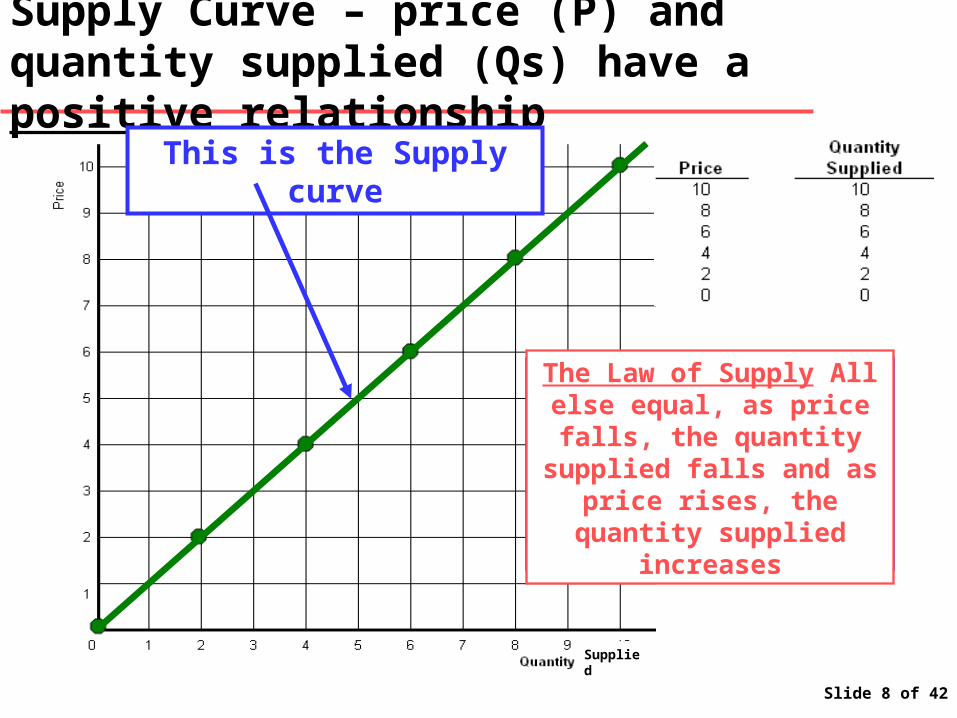

Slide 8 of 42

Supply Curve – price (P) and quantity supplied (Qs) have a positive relationship

This is the Supply curve

Supplied

Notice the “upward slope” suggesting that as price

increases, producers want to make more of this item. This

leads us to the law of supply…

The Law of Supply All else equal, as price falls, the

quantity supplied falls and as price rises, the quantity

supplied increases

Slide 9 of 42

Putting them together gives us a market

For this market, the equilibrium price will be $5

For this market, the equilibrium quantity will be 5 units

If left alone, a market will always

find this “equilibrium”

point.

But how do we know that this

will work?

Now we have a market…we have a demand curve representing the

buyer and a supply curve representing a seller.

So what will happen? How will these “participants” determine price

and quantity?

It is at this point where supply

equals demand. Here, these

participants agree upon price!

Slide 10 of 42

How do we know that the market will price this good at $5 and supply 5 units?

If the price was set at $6

Then quantity demanded (Qd) would be 4 units…

…and quantity supplied (Qs) would be 6 units

Producers would wind up with a surplus

and would eventually

reduce prices to sell the extra

units!

In other words, there would be a surplus of 2 units!

Slide 11 of 42

On the other hand, shortages drive prices up

If the price was set at $2

Then Qs would be 2 units…

…and Qd would be 8 units

Producers would wind up

with a shortage.

Consumers would

eventually offer a higher price!

In other words, there would be a shortage of 6 units!

Slide 12 of 42

Markets are amazing things!

So if left alone, a market…or specifically the participants in it…

will drive prices to this point.

It is at equilibrium that the forces of supply and demand are equal…

And the market clears!

Slide 13 of 42

Let’s explore Supply and Demand in more detail

• There are differences between changes in quantity demand and changes in demand

• There are differences between changes in quantity supplied and changes in supply

Slide 14 of 42

Changes in quantity demand:Movements along the demand curves

A change in price (from $7 to $4) will result in a change in the

quantity demanded (from 3 to 6 units)

Slide 15 of 42

Real world example: airline pricing

What do airlines do if many seats are open a week before the flight?

They sell them at reduced prices, perhaps in Internet specials.

Slide 16 of 42

Changes in quantity supplied:Movements along the supply curves

A change in price (from $5 to $8) will result in a change in the quantity supplied (from 5 to 8

units)

Supplied

Slide 17 of 42

Changes in demand cause a shift in the demand curve (in this case an increase)

Think of it this way…each of the points that make up this line have

shifted to the right!

Previously, at a price of $8, 2 units were

demanded.

Now, given some new information, we demand

4 units at $8.

Note that the new demand curve is shown as D with an

apostrophe after it (D’).

Slide 18 of 42

Here is an example of a decrease in demand

Here, the idea is the same…except we are

demanding LESS of this good!

Slide 19 of 42

Changes in demand have an impact on price and quantity

• If Demand P Q

• If Demand P Q

We are now exploring another Key Learning Outcome: Economic events can shift supply

and demand curves and that affects the price of a good and how much of it we buy!

Slide 20 of 42

Factors affecting demand: Prices of related goods can affect demand

If french fry prices double, demand for ketchup will probably decline

Demand for Ketchup

These goods are compliments

When the price of one goes up, we demand less of the other!

Slide 21 of 42

Factors affecting demand: Price of related goods can affect demand

If beer prices double, demand for wine will probably increase

Demand for Wine

These goods are substitutes

When the price of one goes up, we demand MORE of the other!

Slide 22 of 42

Factors affecting demand: Income can affect demand

If income increases, demand for most goods will probably increase

Demand for normal goods

These goods are normal

When our income goes up, we demand more of these items.

Slide 23 of 42

Factors affecting demand: Income can affect demand

If income increases, demand for inferior goods will probably decrease

Demand for Inferior Goods

Some goods such as Spam are inferior (at least according to me. You may love Spam.)

When our income goes up, we demand less of these items!

Slide 24 of 42

Other factors affecting demand

Expected Future Prices

Population

Tastes and Preferences

If consumers think prices will fall, they may demand less of a product now

As population grows, demand for most goods increases

Fads can affect demand. For example a hot Christmas item such as an Xbox or a “Tickle Me Elmo” may cause demand to increase

Slide 25 of 42

Changes in supply cause a shift in the supply curve (in this case an increase)

Slide 26 of 42

Here is an example of a decrease in supply

Slide 27 of 42

Changes in supply have an impact on price and quantity

• If Supply P Q

• If Supply P Q

Slide 28 of 42

Factors affecting supply: Prices of related goods can affect supply

If price of beef falls, supply of leather will probably fall

Supply of Leather

These goods are compliments in production

Slide 29 of 42

Factors affecting supply: Price of related goods can affect supply

If corn prices fall, supply of soybeans will probably increase

Supply of Soybeans

These goods are substitutes in production

Slide 30 of 42

Factors affecting supply: number of suppliers

As more suppliers enter the market, supply will increase

Slide 31 of 42

Factors affecting supply: Weather

Weather can help or hurt a market

Market for Orange JuiceMarket for Skiing

Cold weather

can destroy

the orange market

Cold weather can help the ski market

Slide 32 of 42

Factors affecting supply: Technology

Improved technology may increase supply

Market for Autos

Slide 33 of 42

Other factors affecting supply

Expected Future Prices

Taxes and Incentives

If producers think prices will fall, they may provide more of a product now

Governments use taxes and incentives to encourage of discourage the production of certain goods

Slide 34 of 42

In Summary

In a command economy, some

central authority has to decide price and

quantity for every good sold.

That is obviously difficult to do and

errors routinely result in surpluses or

shortages.

A market has its own built in rationing system.

Those that want it at the prevailing price get to buy it. Those that do

not want to pay that much can leave it.

If an item becomes very popular, its price may rise and new suppliers

may add to the supply.

If an item loses appeal, it’s price may fall. That will discourage

producers and reduce the amount of goods made.

Therefore, markets serve as great rationing mechanisms!

Here we see another Key Learning Outcome: Many events can shift

supply and demand curves and when they

do, prices and quantities change!

Slide 35 of 42

Supply and Demand:Individual exercises

Review the following six slides and determine the new price and quantity

Answers appear at the end of this presentation.

Slide 36 of 42

#1- Computers

Slide 37 of 42

#2 - Beanie Babies

Slide 38 of 42

#3 - Oil

Slide 39 of 42

#4 - Websites

Slide 40 of 42

#5 – Orange Juice

Slide 41 of 42

#6 - Widgets

Slide 42 of 42

Answers

Q1: New equilibrium price is $2, new equilibrium quantity is 3 units.

Q2: New equilibrium price is $5, new equilibrium quantity is 4 units.

Q3: New equilibrium price is $4, new equilibrium quantity is 1 units.

Q4: New equilibrium price is $2, new equilibrium quantity is 6 units.

Q5: Cannot be determined…Buyers and Sellers do not agree on a price!

Q6: New equilibrium price is $2, new equilibrium quantity is 5 units.

Expect questions like this on the test. If you do not understand these, please let me know!