Deliverable D25 Business viability studyoban.tubit.tu-berlin.de/D25_Business_Viability_Study.pdf ·...

89

© Copyright by the OBAN Consortium. Deliverable D25 Business viability study Author(s): Editor: Thor Gunnar Eskedal (TNR) co-authors listed on next page Partner(s): Telenor ASA Swisscom AG France Telecom SA Birdstep Technology ASA Istituto Superiore Mario Boella Norwegian Post and Telecommunication Authority Version: f Delivery Month: December 2005 Date: March 14, 2006 Workpackage, Activity: WP5, WP5-A2 Deliverable Type and Number: Report, 25 Distribution – Type: Public Document Code: OBAN-WP5-TNR-251f-D Internet URL: http://www.ist-oban.org

Transcript of Deliverable D25 Business viability studyoban.tubit.tu-berlin.de/D25_Business_Viability_Study.pdf ·...

© Copyright by the OBAN Consortium.

Deliverable

D25 Business viability study

Author(s): Editor: Thor Gunnar Eskedal (TNR) co-authors listed on next page

Partner(s): Telenor ASA Swisscom AG France Telecom SA Birdstep Technology ASA Istituto Superiore Mario Boella Norwegian Post and Telecommunication Authority

Version: f

Delivery Month: December 2005

Date: March 14, 2006

Workpackage, Activity: WP5, WP5-A2

Deliverable Type and Number: Report, 25

Distribution – Type: Public Document

Code: OBAN-WP5-TNR-251f-D

Internet URL: http://www.ist-oban.org

© Copyright by the OBAN Consortium.

IST 6FP Contract No 001889

Deliverable (25) - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

Full Authors List

- From partner Telenor ASA (TNR): Thor Eskedal (ed), Ragnar Andreassen

- From partner Swisscom AG (SCOM): Eric Demierre, Jacques Robadey, Jean-Claude Bischoff, John Charles Francis

- From partner Istituto Superiore Mario Boella (ISMB): Andrea Amelio, Carlo Cambini

- From partner France Telecom SA (FT): Claire Duranton, Sami Bazaia, Lionel de Rivieres

- From partner Norwegian Post and Telecommunication Authority (NPT): Tom Opperud, Runar Langnes

- From partner Birdstep Haakon Bryhni, Otto Rustad

Deliverable (25) - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

Document Revision History

Date Version Author/Editor/Contributor Version Description

November 15, 2005 a Thor Gunnar Eskedal (TNR) Material put into the new deliverable template

January 9, 2006 f Thor Gunnar Eskedal (TNR) Final version

Deliverable (25) - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

Executive summary

Previous years have shown a rapid increase in the number of operative wireless local area networks (WLAN), both for residential and business usage. Public WLANs in terms of wireless hotspots have emerged and are quite widely deployed. In addition, we see that some communities offer WLAN coverage as a public utility. Another trend is the increase in functionality associated with the WLAN protocols, and the technical effort that is taking place, e.g. in the Universal Mobile Access (UMA) initiative, in order to integrate mobility handling traditionally associated with cellular networks into the WLAN domain. A third trend can already to be observed, namely the integration of WLAN capabilities into laptops, handheld devices and advanced mobile terminals. Such factors reflect a convergence in functionality and services between the telecom-driven 3G development and the more recent of WLAN.

A development with commercial WLAN coverage raises several interesting questions with respect to how and by whom mobile broadband services should be offered to the public. There are various scenarios as to which actors will become tomorrow’s broadband mobile access providers, and which technology that will be deployed where.

A key question is the cost of providing radio access coverage. In order to offer WLAN based radio coverage, a reasonably fine-grained mesh of radio basestations is required. The project OBAN proposes to utilise the existing copper access infrastructure in order to support such coverage. This infrastructure is not currently utilised to full commercially potential. Moreover, further spare capacity from residential usage can be expected to be made available in the future.

This report discusses several scenarios for commercial implementation of public WLAN-based broadband access using OBAN technology. The report presents qualitative results, based on a method that describes the various roles involved in service production, considerations as to which stakeholder can take what positions, and the commercial consequences in terms of services and value propositions for relevant stakeholders. Considerations regarding public regulation and technical implementations are also included.

The following scenarios for the fixed access operator are considered:

1. A fixed access operator that owns and operates the radio access points on a wholesale basis. In this scenario, an operator owning an extensive copper-based access infrastructure deploys a public wireless service that is tightly integrated with existing technical operations. It is considered that the access operator may be a dominant actor within a country where open commercial interfaces between access and end-user service provisioning are enforced. A WLAN-based mobile access wholesale service is thus offered to service providers on this basis. More than one service provider may potentially be present at a given access point.

2. A Fixed Access Operator that offers services to mobile-only customers. Here the focus is on an actor that is an integrated internet service provider and access provider, noting that many of today’s customers no longer utilise a fixed telephone subscription, relying entirely on mobile communication. This represents a loss for the traditional fixed operator, which may win back customers by offering WLAN-based access services. It is assumed in this scenario that an open wholesale interface for the access part of the service is not enforced.

3. A fixed access operator that owns and operates the radio access points works in collaboration with hot spot operators. In this scenario, modelled after developments in the Italian market, the fixed access operator plays a role in the emerging WLAN-based residential access industry, while the mobile access operator plays a role in the WLAN-based public hot-spot market. Thus two different types of access point operations are foreseen, targeted at residential and public hot spot sites respectively.

The following scenarios with a mobile access operator is considered:

4. A mobile access operator operates the radio access points. Here the traditional mobile industry takes a somewhat aggressive WLAN position by offering broadband mobile services over WLAN based access. Again, it is considered that the actor taking the position may be a dominant market player that

Deliverable (25) - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

is being forced to open wholesale interfaces towards 3rd party service providers. The fixed access operator is restricted to deliver virtual channels over the access network in such a case. It may, however, offer these channels to other mobile access operators.

The following scenario with a service provider focus is considered:

5. A fixed internet service provider offers wireless roaming, so building a wireless internet service provider community and improving mobile communication services. These three facets all have in common that the service provider also acts as the radio access operator. This is a continuation of the development seen in many markets, where internet service providers offer subscriptions including WLAN routers. The scenarios imply a somewhat more active part of the internet service provider than is currently seen in the sense that active operation of the nodes are considered rather than mere pre-configuration.

In addition, an integrated scenario is addressed as a means to increase customer loyalty:

6. In this scenario, there are no open commercial interfaces anywhere in the value chain. One single actor streamlines its operation and service offering. It is the FMC case based on heterogeneous access technologies, where one subscription brings a “complete communication package” to the users.

The analysis does not conclude that any of these scenarios is a priori preferable to others. Which scenario is considered most relevant will depend on national market considerations and strategic decisions. Actors with significant market power may be expected to be more constrained by public regulation than other players. Scenarios 1 and 4 are targeted to cover such situations where open interfaces are enforced. Where actors are free to organize themselves optimally, scenarios with more integrated operations should be beneficial.

Deliverable (25) - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

Table of Contents

1. Introduction................................................................................................................................................. 3 2. Definition of OBAN and roll out stages..................................................................................................... 4

2.1. Common definitions.............................................................................................................................. 5 2.2. OBAN roll out possibilities................................................................................................................... 6 2.3. OBAN Equipment and functionality..................................................................................................... 8

3. OBAN value proposition........................................................................................................................... 12 3.2. OBAN application examples............................................................................................................... 14

4. Business modelling method/approach ..................................................................................................... 16 4.1. Definition of the term business model ................................................................................................ 16 4.2. Business model elements .................................................................................................................... 17

5. OBAN Business roles and role modelling framework............................................................................ 21 5.1. Roles and role model........................................................................................................................... 21

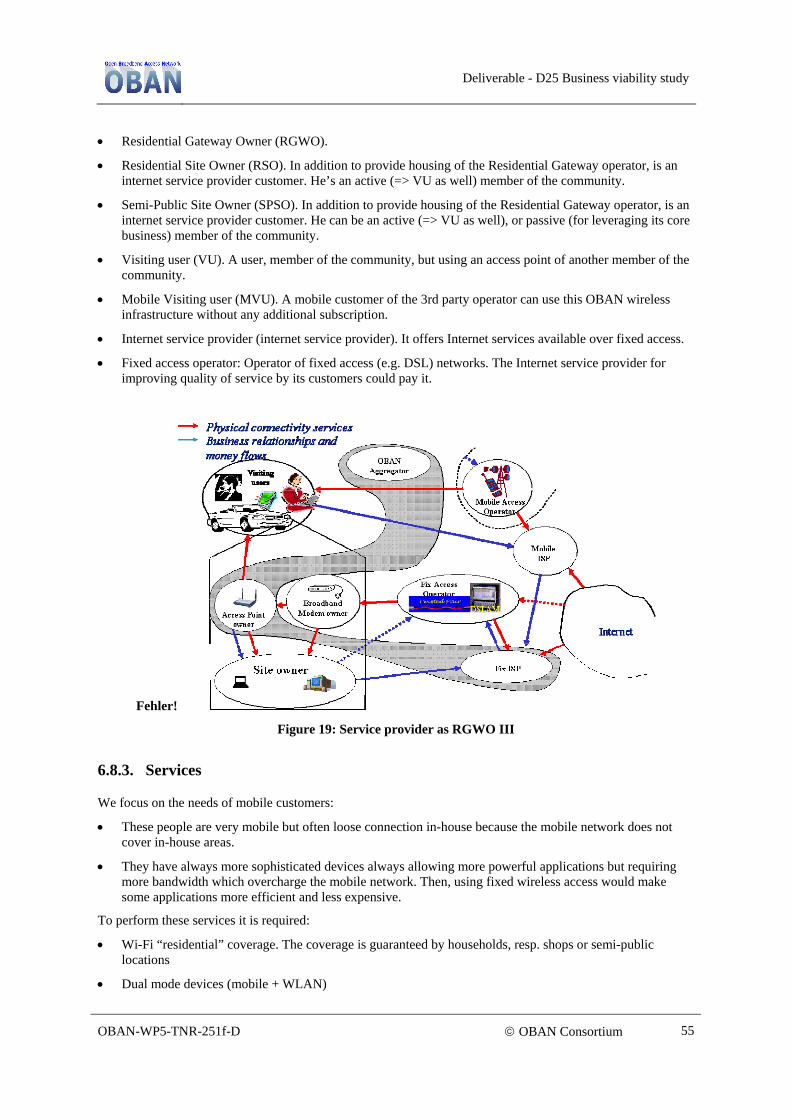

6. OBAN business models ............................................................................................................................. 24 6.1. Short summery of the business models ............................................................................................... 24 6.2. Fixed access operator owns and operates the Residential gateway..................................................... 25 6.3. Integrated fixed access operator and Internet service provider conquers Mobile-only customers ...... 32 6.4. Fixed access operator as residential gateway operator with additional fragmented hot spot operators42 6.5. Mobile access operator operates the RGW ......................................................................................... 47 6.6. Fixed Internet service provider providing wireless roaming............................................................... 50 6.7. Building wireless Internet service provider community...................................................................... 52 6.8. Improving mobile communication services ........................................................................................ 54 6.9. An Integrated Operator develops customers’ loyalty .......................................................................... 56 6.10. Other business models......................................................................................................................... 64

7. Regulatory issues....................................................................................................................................... 67 7.1. Legal framework ................................................................................................................................. 67 7.2. OBAN – service or functionality?....................................................................................................... 69 7.3. Markets and regulation........................................................................................................................ 69 7.4. Regulatory Aspects applied to possible Business Models................................................................... 71

8. WiMAx and other similar technologies................................................................................................... 73 8.1. Wireless mesh networks...................................................................................................................... 73 8.2. 802.16.................................................................................................................................................. 75 8.3. WiMAX .............................................................................................................................................. 75 8.4. 808.20.................................................................................................................................................. 76

9. Concluding remarks ................................................................................................................................. 79 10. References .................................................................................................................................................. 81 11. Abbreviations ............................................................................................................................................ 82

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

2

Preface

This deliverable is part of the Work Package 5 (WP5) work within the OBAN (Open Broadband Access Network) project. The project started up spring 2004 with a total duration of 3 years. The aim of the WP is to analyse the business potential of the OBAN concept and this deliverable is part of a series of deliverables.

In Year 1, a study was conducted analysing the environmental and user impacts of the concept together with a general market survey of WLAN business. Based on this background information, business models for OBAN were studied in 2005 and are documented in this deliverable. Next year the work will continue with techno economic analyses of selected business models.

Parallel to this work plan studies are also going on looking into different charging and pricing schemes and regulatory and legal aspects concerning the business models. The regulatory issues are incorporated in the yearly deliverables to always document the latest developments with regard to national and European regulatory aspects concerning the OBAN concept.

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

3

1. Introduction

The last years have shown a rapid increase in the number of operative wireless local area networks (WLAN), both for residential and business usage. Public WLANs in terms of wireless hotspots are still emerging and are already widely deployed. In addition, we see that some communities offer WLAN coverage as a public utility. Another trend is the increase in functionality associated with the WLAN protocols, and the technical effort that is taking place, e.g. in the Universal Mobile Access (UMA) initiative, in order to integrate mobility handling traditionally associated with cellular networks into the WLAN domain. A third trend already evident is the integration of WLAN capabilities not only in laptops, but in handheld devices and advanced mobile terminals as well. These factors seem to indicate a convergence in functionality and services between the telecom-driven 3G development and the more recent of WLAN.

A development with commercial WLAN coverage raises several interesting questions with respect to how and by whom mobile broadband services will be offered to the public. There are actually several possibilities as to which actors will become tomorrow’s broadband mobile access providers, and which technology that will be employed where. This report discusses several scenarios for how public WLAN-based broadband access can be commercially implemented by using the OBAN technology of copper based access. The report presents qualitative results, based on a method that describes the various roles involved in service production, considerations on which stakeholder can take which positions, and the commercial consequences in terms of services and value propositions for each partaking stakeholder in the various scenarios.

The business models are evaluated in terms of technical feasibility based on the technical work done in the project, and the potential value proposition for the actors involved. Regardless of what market players are involved and how they manoeuvre into strategic positions they will all be subject to regulatory requirements. The Norwegian authority on Post and Telecommunication (NPT) has, according to available European regulatory legislations, evaluated some of the business models described in this report. The market on mobile and fixed access is in a very rapid evolution thus the existing regulatory regime is subject to evolve as well.

The report starts out, in chapter 2, with a definition of OBAN services and how OBAN may be rolled out in stages according to increased functionality. The next chapter provides a general overview of critical business aspects for OBAN, and an analysis of how one may construct businesses based on WiFi technology. We then present the business-modelling framework on which the analysis in the report is based. The method is based on work by Chesbrough and Rosenbloom [5]. In order to apply the method, we need means to describe the value systems for the various business scenarios. For this we use a role model, which is described in chapter 5. Chapter 6 presents the business scenarios and the discussion and assessment of each of them. Some aspects of proposed business models are discussed on the basis of public regulation in chapter 7. Before the conclusion a short chapter is added, looking into the potential of using WiMAX and mesh networks in relation to OBAN.

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

4

2. Definition of OBAN and roll out stages

The WLAN and mobile world is emerging rapidly and has become quite complex. Many wireless businesses based on WLAN are therefore very close to the OBAN vision. Due to this it is very important to clearly define “what OBAN is” and what “OBAN is not”.

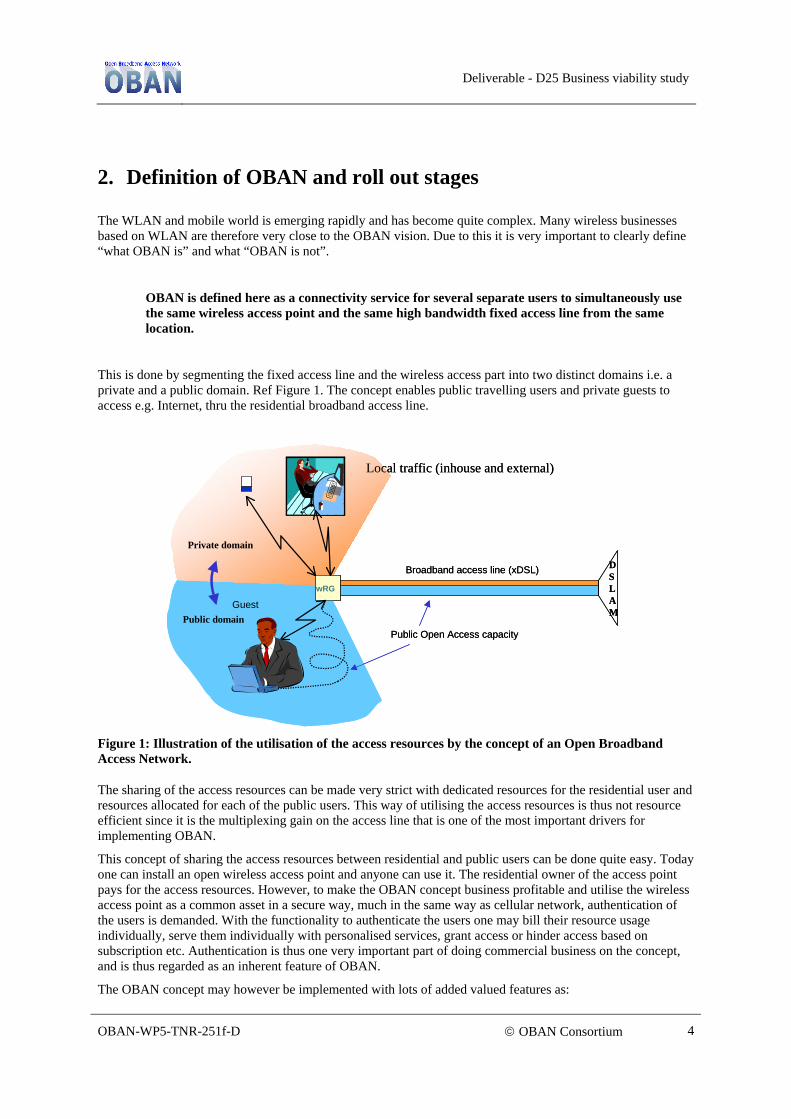

OBAN is defined here as a connectivity service for several separate users to simultaneously use the same wireless access point and the same high bandwidth fixed access line from the same location.

This is done by segmenting the fixed access line and the wireless access part into two distinct domains i.e. a private and a public domain. Ref Figure 1. The concept enables public travelling users and private guests to access e.g. Internet, thru the residential broadband access line.

Broadband access line (xDSL)

wRG

Public Open Access capacity

Guest

Local traffic (inhouse and external)

DSLAM

Private domain

Public domain

Broadband access line (xDSL)

wRG

Public Open Access capacity

Guest

Local traffic (inhouse and external)

DSLAM

Private domain

Public domain

Figure 1: Illustration of the utilisation of the access resources by the concept of an Open Broadband Access Network.

The sharing of the access resources can be made very strict with dedicated resources for the residential user and resources allocated for each of the public users. This way of utilising the access resources is thus not resource efficient since it is the multiplexing gain on the access line that is one of the most important drivers for implementing OBAN.

This concept of sharing the access resources between residential and public users can be done quite easy. Today one can install an open wireless access point and anyone can use it. The residential owner of the access point pays for the access resources. However, to make the OBAN concept business profitable and utilise the wireless access point as a common asset in a secure way, much in the same way as cellular network, authentication of the users is demanded. With the functionality to authenticate the users one may bill their resource usage individually, serve them individually with personalised services, grant access or hinder access based on subscription etc. Authentication is thus one very important part of doing commercial business on the concept, and is thus regarded as an inherent feature of OBAN.

The OBAN concept may however be implemented with lots of added valued features as:

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

5

QoS support. Mobility support between WLAN spots Mobility between WLAN and 2G/3G. Roaming support etc

These features may be implemented if the market player deploying the concepts thinks there will increased business potential in doing so. The ambition level is thus up to the market player that implements OBAN based on profitability considerations.

The technical studies in the project are investigating the possibilities of implementing such features. One vision of the concept is to deploy WLAN as a broadband wireless alternative technology to cellular systems as GSM and UMTS. This demands e.g. seamless mobility between WLAN access points. Such a deployment is very ambitious, and in the short run neither technically feasible nor market profitable. In the future however it may be viable. It is thus important to have all the ambition levels in mind when constructing business models.

In this report the ambition level is linked to each described business model in chapter 6. This is based on the targeted market segments and the service portfolio offered to the customer. Since the concept may include many features or only the basic sharing of the access line with separate authentication there is no strict definition of OBAN besides the concept of sharing the access resources.

The important issues is that OBAN may be realised with a quite broad range of functionality, opening up the possibility for market players to make flexible business models and streamline them to a specific target marked offering a specific service set. Due to this flexibility of adding features to the basic OBAN definition, operators may roll out the concept in stages enhancing it with added features while always keeping a close look at the up take of the service in the market.

2.1. Common definitions

This report uses some terminology that may be closely linked to the OBAN concept and is thus not directly transferable to other contexts. To give a brief introduction to some of the terminology a list of often used terms are defined below.

Note: Some of these definitions are not exhaustive. Here they are only indicative and strictly related to this document. The forthcoming chapters will give an elaborated description of the terms and their use in concrete examples.

OBAN service:

The connectivity service realised by implementating OBAN functionality at the endpoints of the connectivity, at the terminal devices and in the intermediate transport network.

Residential user = home user:

The user of OBAN services that lives in the house or private premises where an OBAN access point is installed.

Visiting user:

A user of OBAN services that use the service at another location that its own residential location. Visiting users will most often pay for the OBAN service as a public service offering from a service provider

Residential gateway (RGW):

A telecom term for the equipment at the end users premises that terminates the fixed access line. In OBAN this term is used for the wireless access point connected to the fixed access line that is augmented with OBAN specific functionality.(ref chapter 2)

Nomadic mobility:

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

6

Mobility where a user can move between wireless access points but the session is terminated for each movement. The user is required to establish a new session. Reauthorisations may be mandatory.

Seamless handover:

Handover between access points where the user notices minimal or no disturbance in the on going session.

Seamless roaming:

Roaming between operators where the on going session is not disturbed

Seamless mobility:

In this report seamless mobility has the same meaning as seamless handover.

2.2. OBAN roll out possibilities

An OBAN service can be rolled out in stages with increasing ambition level regarding the implemented functionality. This may be beneficial in terms of targeted service offerings and in terms of location/environments as rural, suburban, urban and dens environments. A minimal OBAN solution may be defined as:

“OBAN minimal solution consists of enhancing privately WLAN services with authentication functionality to grant access for visiting/public users.

In such a configuration stand alone private WLANs with functionality for authentication can be used to grant access for visiting users. Due to authentication each user may be billed separately. Private guests are automatically treated as visiting users and pay for the usage. However, the residential user can acquires a guest authentication account and thereby let guest use this account on the residential charge. Authentication is thus one of the vital functionalities of OBAN to be able to make business on the concept and is an inherent functionality in the concept.

The use of open access point as a form for OBAN minimal solution is today widespread and many users are free riders on these open access points. There are thus problems with these open access points both in terms of billing and security for the owner in addition to an uncontrolled usage of the access resources. This situation is though being altered gradually as many open WLAN spot owners are getting more conscious about the risk they take of others using their network connection for illegal content e.g. child porn. The OBAN access points will as a minimal solution have one sort of division between the private and the public user so the public users may use access resources and be responsible themselves for the content downloaded.

Taking the situation that a user only has a fixed broadband connection without WLAN, the minimal solution will support the users with connectivity services enabling:

• Broadband wireless access at home through the use of a WLAN RGW.

• Possibly cheaper wireless access than with mobile access

• Possibility to let all visitors access Internet and corporate servers and pay for the access resourses themselves

This minimal OBAN solution may be especially attractive for areas such as coffee shops/restaurants, gas stations, public waiting rooms (dentist, public offices, hairdressers, etc) where both the site owner and the customers may use the network, and there is no need to support mobility.

A solution with mobility between the WiFi spots may also be feasible enhancing the customer’s service experience. This little enhanced OBAN solution would give a user the possibility to move between OBAN access points getting access to Internet through the home users fixed access line and be authenticated at its service provider while moving. This scenario may be useful in e.g. shopping centres where several shops may have WLAN but the customer moves between them and gets access to different WLANs as moving around in the shopping area. This OBAN solution does however require more advanced functionality than the very simple solution described above. Mobility e.g. in terms of Mobile IP between the WLAN access point would be needed and functionality in the terminal may also be required.

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

7

Looking at the extended OBAN connectivity solution it may be defined as:

“OBAN extended solution may be defined as a shared connectivity service with public users, incorporating WLAN seamless mobility, high quality, single billing and security combined with seamless mobility functionality to cellular mobile system access”

This OBAN extended solution requires collaboration between fixed access network operators and mobile operators. This is to be able to offer quality of service across the fixed access line, mobility support between WLAN access point as well as support mobility across fixed and mobile network infrastructure. The added value for the user for the extended OBAN solution is:

• Same added value as for minimal solution

• Quality of service support

• Single billing (depending of the case)

• Very fast seamless handover

• Same or similar security/authority regime as for 3G networks

• Automatically switching between WiFi (OBAN) and cellular

• Same terminal can be used to connect to several networks

• The user receives one bill even if using several types of networks

• All network usage will be charged directly to the user of the service.

• Seamless handover support between networks

All intermediate solutions between the minimal solution and extended solutions are possible. To reduce risk and high investment costs OBAN may be built out gradually from a solution the operator/service provider regards as the minimal to be able to evaluate the technology e.g. in term of usage and willingness to pay for the added value.

The most important difference or value added incentive for operators or service providers to enter into the OBAN business would be the higher bandwidth of WLAN and the potentials this brings fourth. Traditionally travelling users and visiting users would in most places use a mobile network like GSM or UMTS. The capacity of these networks is far lower than the capacity of most of the WiFi standards. Most WiFi equipment will have a raw bit rate of 50Mb/s or higher. The fixed access line could also range from 4-25Mb/s as a shared resource, dependent of the type of access technology. Since the cell radius of WiFi is much less that e.g. 3G networks the capacity per user will be much higher than for 3G. This means that with a continuous OBAN coverage each customer will be able to acquire much higher bandwidth and thereby be able to get much faster access to Internet, render high bandwidth real time applications as video and interactive gaming etc. On line maps and other broadband demanding local information services are also well targeted to use a WiFi OBAN implementation instead of mobile networks.

Also due to the lower cell radius of WiFi, location services may be more detailed and targeted to very small areas as a part of a campus area, a specific block of flats etc. This may open up for specific services as advertisements, special offerings from stores or businesses, detailed tracking and other types of local services. On line synchronisation of presence information, and mail and calendar updates area also services that may be more widespread due to OBAN.

Since most 3G networks will be enhanced with High Speed Downlink Packed Access (HSDPA) and thereby boost the capacity per cell up to about 10-12Mb/s the 3G network will be able to support very many of the services also envisioned for OBAN. This will demand the OBAN network to be targeted to specific services that are especially suited for a short-range WiFi network. Customer that will use high bandwidth applications will however benefit from the higher capacity of WiFi networks.

This OBAN optimal solution requires collaboration with the fixed access network operator for offering QoS, and possibly mobility.

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

8

2.3. OBAN Equipment and functionality

As described in the previous section OBAN may be built out based on different stages due to different ambition levels. One can thus build out a minimal OBAN solution requiring marginal investments or one can build out a more advanced OBAN solution. The incremental cost of each ambition level is important to analyse in terms of the estimated revenue of the more advanced service offering. It is therefore very important to get a good understanding of the equipment and functionality needed and the cost and location of these. E.g. if an OBAN operator needs to involve many other actors to implement the service this would demand a tight cooperation with other actor which could be both a slow process, costly and involve much administrative work to establish agreements.

In this section we will look closer into OBAN equipment and functionality. The functionality can be software that can be installed in existing equipment or software and hardware linked to new network nodes that need to be connected to the transport or signalling paths.

The equipment and functionality listed below may be located both at the end users site, within the transport network suppliers domain and/or at the service providers premises.

a) Network based seamless handover tool (typically Mobile IP Home Agent/Gateway Foreign Agent/Foreign Agent functionality)

b) Authentication and identification functionality (typically Radius server/client functionality)

c) Connectivity handling (e.g. Quality of service and policing of traffic flows support)

d) Site owners network equipment (basically the OBAN Residential Gateway)

e) Terminal devices (with functionality to support WLAN Handover and OBAN authentication)

These equipment and functionality issues may have major impact on the business due to where the equipment/functionality is located and the actor owning, controlling and managing it.

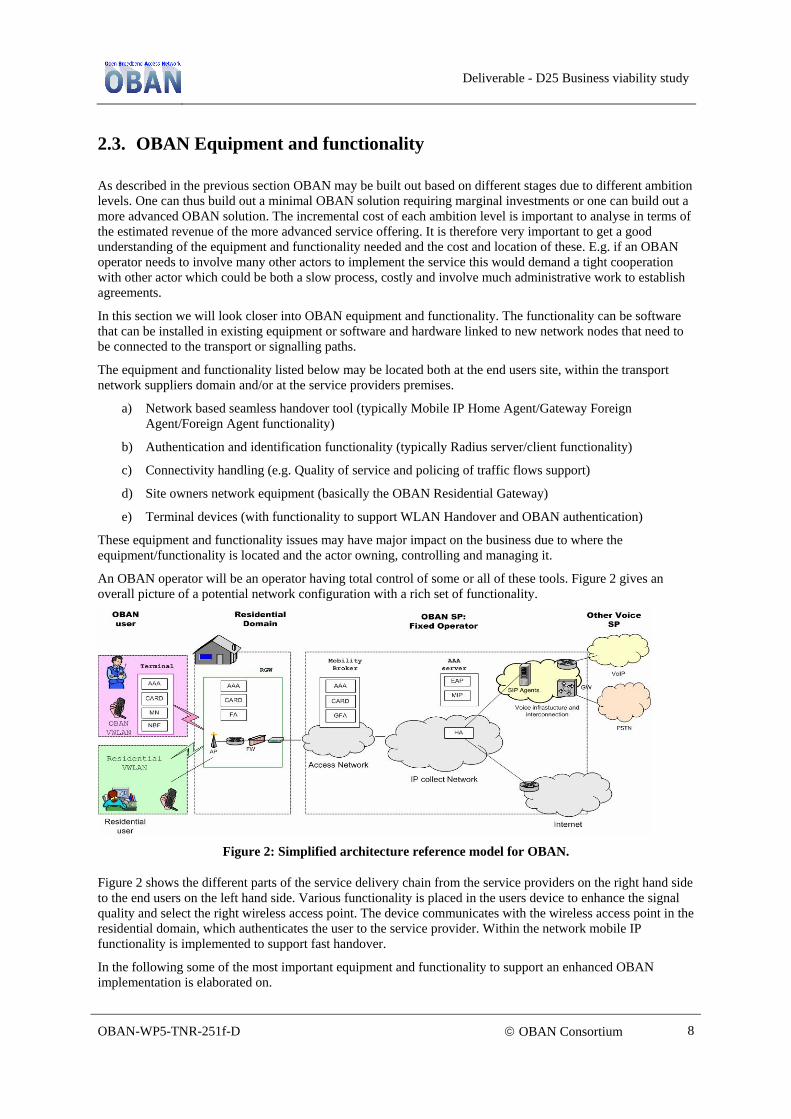

An OBAN operator will be an operator having total control of some or all of these tools. Figure 2 gives an overall picture of a potential network configuration with a rich set of functionality.

Figure 2: Simplified architecture reference model for OBAN.

Figure 2 shows the different parts of the service delivery chain from the service providers on the right hand side to the end users on the left hand side. Various functionality is placed in the users device to enhance the signal quality and select the right wireless access point. The device communicates with the wireless access point in the residential domain, which authenticates the user to the service provider. Within the network mobile IP functionality is implemented to support fast handover.

In the following some of the most important equipment and functionality to support an enhanced OBAN implementation is elaborated on.

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

9

2.3.1. Network based seamless handover tool

This consists of a tool managing the OBAN mobility service. Seamless mobility is one function that will enhance the OBAN experience for OBAN customers, enabling continuous movement across OBAN sites. It has to be noted though that seamless mobility is not demanded to offer OBAN like services.

In addition to the Mobile IP Home agent and Foreign agent, supporting mobility at the end points, the OBAN project has also described a mobility broker. This entity may be located somewhere in the fixed network to support fast handover. In cases where there is long distance between the customers service provider and the RGW a mobility broker may be needed to support real time services. This functional entity may be provided and managed by the OBAN service provider and/or the OBAN transport connectivity provider (e.g. a network operator). The mobility broker would also be a location for legal intercept due to regulatory reasons and should contain the needed functionality to do so. The mobility service means that the operator is capable of identifying OBAN clients to offer them services e.g. based on subscriber profiles.

2.3.2. Authentication and identification functionality

User authentication and identification are the most important functions of OBAN. Even the minimal solution of OBAN will demand this functionality first and foremost to be able to identify the customer and thereby be able to conduct secure charging and billing. From a business point of view the possibility to charge and police traffic from identified users is of great importance to be able to run a business. Control over these functions is from a regulatory point of view only granted to trusted entities, i.e. legal entities as enterprises, operators, and service providers. Since the RGW is located within a residential home zone this entity should not perform charging/ billing functions due to risk of illegal actions from the site owner.

The functionality of authentication is most commonly done in the residential gateway, and in a specified OBAN node called a mobility broker and at the home service provider.

Proper authentication and identification is thus required to enable connectivity, enable services and to perform secure charging.

2.3.3. Connectivity handling

Since OBAN implies public usage of the private access line, separation of the connectivity service is needed to be able to guarantee the home users’ capacity requirements. Much emphasis is put on supporting the home user with good quality, i.e. to give the home user priority over the public users when the resources are scarce. QoS/policy support is thus needed on the WLAN segment and across the fixed access line. The implementation of the QoS mechanisms and the separation of capacity between the home user and the visiting users may take many forms. In some circumstances the home user may accept to install a OBAN RGW if and only if the home user has exactly the same capacity as before and with no interference in his capacity even when he/she does not use it. This is not optimal seen from the perspective of utilising spare capacity. To make best usage of the access line it should be divided on a “on demand” basis but giving the home user priority and giving real time traffic priority over data for both the home users and the visitors. The business model would be different in the different cases e.g. in terms of sponsoring, capacity requirements to the residents’ location, QoS/policy support and charging method.

2.3.4. Equipment located at the site owner

The success of OBAN services highly depends on the connection capability of a site. An OBAN site may be small or large e.g. a small neighbourhood, a whole city or a countrywide implementation. Therefore if seamless mobility is part of the OBAN solution the density of the OBAN connection points should be high. Even if there are possibilities to handover to 3G networks the density of WLAN should be high to support applications with bandwidth requirements exceeding the capability of UMTS. The lower the required modifications by the site owners are, the easier will the penetration of OBAN access points be. If OBAN services could be provided without any modification to the site owners own in house equipment, the density of OBAN access points could quickly become high and OBAN services would have good chances of succeeding.

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

10

Differentiation is needed for the two situations using open access points and situations using access points specially configured for OBAN services.

a) OBAN sites case: this is the situation where the access points are closed and opened only to OBAN customers. This solution considers an access controller for managing those connections and the configuration allows offering QOS and end-to-end security.

b) Open sites case: this is the situation where the access points are open and are accessible to anybody. This configuration will not allow QOS, nor separate charging but allows end-to-end security e.g. by means of VPN functionality.

If installation of hardware by the site owner is needed e.g. for specific network functionalities or for installing the access points in a specific area, e.g. closed to a window, then higher costs will be generated to install OBAN sites. If an operator also needs people to walk into each private residence to install equipment the user would also be more inclined to not allowing it, or be much more hesitant to go for an OBAN solution.

The OBAN component that will be located in the residential premises is the residential gateway. This entity is necessary for providing OBAN services, e.g. supporting access control and mobility. It may consist of software installed on the existing router or broadband modem. The software could be downloaded from the network to the Access Point if it has router functionality with Access Controller capability or to the router if it has Access Controller Capability (not all routers have it).

The Access Controller may perform the following functions:

Note. These are implementation specific so there may be many possibilities.

• for OBAN Voice over WLAN: direct the VoIP data to the “OBAN” SIP server; The VoIP parameters are located in the VoIP device

• for Internet services:

o sneefer for visiting user: the new MAC address of the device connected to the AP/residential gateway is discovered by the AP Access Controller.

o Connection to an OBAN central server with questions about username and password.

If accepted, an HTTP request is performed and the access to the Internet is done through the OBAN security and billing server.

Doing it this way, WLAN connections can only be performed for OBAN customers and through an OBAN server. The Fix Access Operator and/or the fix Internet service provider do not require to know and to participate to the OBAN service. Generally a new AP with routing functionality must be installed.

2.3.5. OBAN Devices

OBAN does not mandate special devises to run OBAN services. Only OBAN specific software needs to be installed in the terminal device. This software is comprised of:

• Access point selection software to support handover between RGW. This functionality selects the Access point with the best bandwidth and quality, support single sign on identifier (SSID) selection to acquire the best transport channel etc.

• OBAN authentication software (based on common security algorithms)

• Mobile IP client

• SIP client (to stream services)

In the first stages of OBAN the terminal devices will be a laptop running a standard WLAN card. The OBAN specific software is installed in the laptop with access point identifiers to the WLAN drivers. In later stages the software will also be adopted to fit into PDAs and small handheld devices.

The customer may have the same subscription (e.g. the 2G/3G subscription) if the customer’s home service provider offers the OBAN services. The same user security credentials are used for the authentication. In an

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

11

OBAN context the users SIM credentials in the home location registrar will be transferred to the OBAN radius server.

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

12

3. OBAN value proposition

As mentioned in the previous chapter OBAN is defined as a connectivity service. With well built out functionality e.g. handover and seamless roaming between 2G/3G wireless networks OBAN may also be seen as a fixed mobile convergence (FMC) enabler. With the extended authentication based on EAP-SIM and QoS and mobility support and integration with 2G/3G control and managements systems a real FMC network could be realised. With a dual mode handset the customer may use one device and be always best connected, have the possibility to receive one bill and be transport network agnostic. The network will take care of adaptation to the connected networks and device capabilities. This could be a realistic case in the future, in the same way as e.g. Seattle wireless has built out citywide WiFi networks in several cities in US with the possibility to use 3G as umbrella coverage.

OBAN may however be rolled out in different stages and with different functionality and in different areas. The business model and value proposition will differ in the different cases. In this chapter some aspects concerning the general value proposition of OBAN is discussed based on some targeted services in the market today. At the end of the chapter a list of services /applications are give that OBAN may be specifically targeted to support. These services may be e.g:

o Detailed location services due to the limited cell radius,

o High bandwidth data applications while mobile since the capacity is much higher that 3G even with the upcoming High Speed Data Access technology enhancements to UMTS.

Added value of OBAN- general value proposition

Considering the various advantages of OBAN services, it is possible to highlight specific applications or specific situation where OBAN brings a significant advantage compared to competing solutions. In the following discussion various issues connected to specific services as well as network possibilities are given. The following services/functionalities are imagined to be the driving aspects for OBAN.

• Internet Access: Internet access is today’s "killer application" driving residential broadband worldwide. In more ambitious future scenarios, the network becomes the repository for personal data storing all personal music, videos, photos and documents. The OBAN high-bitrate mobile vision provides a mechanism for uploading and downloading such material in urban/suburban areas. The mobile office service will be a typical service to reach enterprise data in a secure manner.

• Voice: the WLAN phone may assume the role of a cordless terminal in the home. The lower cost of fixed network calls may drive demand to be connected to the Wi-Fi infrastructure in urban and sub-urban environments. VoIP will however demand good QoS support and require support for fast handover and authentication if used in motion between WiFi access points during a session.

• Video surveillance: Surveillance on public transport (e.g. buses and taxis) where the OBAN network offloads video traffic to the fixed network. This is an ambitious scenario given current Wi-Fi handover speeds, as near continuous coverage is desirable for best surveillance. An umbrella architecture using WiMAX(802.16e) and interworking with 3G would help ensure continuity of service where holes in Wi-Fi coverage occur.

• Location based services: Users on the move may be located based on access line offering a potential for location-based services (e.g. map download to PDA). Since the WLAN spots are much smaller than e.g. 3G cells the location may be very accurate. Body list, shop and address look ups etc may be very precise and constitute a added value for the private and business users, blue and yellow light agencies and enterprises advertising special offers.

• Scheduler and email synchronization:

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

13

Scheduler and emails are regularly synchronized with a specific policy favoring the WLAN access, but allowing mobile access when WLAN access is not accessible for a too long period. The policy could manage that file transfer happens only when connecting on WLAN or WiMAX when available

Among the above mentioned services two of them are more likely to raise the consumer’s interest: voice services and Internet access on the move.

3.1.1. Voice services

Due to the use of the fixed access lines OBAN service providers could build a wireless voice communication offer, which appears to be distinct from a traditional mobile operator’s one. VoIP services are already widespread and opening up for a public VoIP service residential wireless access points would support users with a low cost telephony services also when located out of their own premises. This VoIP service may be implemented as a nomadic service or a seamless mobile service in the extended OBAN definition. Since telephony is regarded as an expensive service and is one of the most used telecommunication services today, the advantages with OBAN would come from offering a public alternative to mobile voice.

In the extended OBAN definition telephone calls, which are running when the person enters a building, may be seamlessly transferred onto the OBAN in-house WLAN access. WiMAX access, if available, could be used both outdoors and indoors when available. This though demands interworking functionality between 3G /WiMAX and WiFi.

Using WLAN access as an extension to the fixed access network should drive to lower rates in general. Nevertheless, there are already some nomadic services, which can be used by visiting users. OBAN includes more functionalities than these “easy solutions” and this will increase the technology cost. The only component, which could drive to a cheaper service, is the contract made with access point owners.

Consumers would prefer a less expensive mobile communication service if it can provide carrier grade quality.

Another difference between OBAN voice and cellular voice service is that OBAN service is first and foremost restricted in mobility. This is due to OBAN and technical requirements that so far do not support vehicular speed handover with real time quality for voice services. However, we assume that this would not be a major drawback for the profitability of voice over OBAN since the mobile communication usage figures show that over 80% of voice calls are made while stationary or in nomadic situations.

3.1.2. Internet Access Services

The bandwidth will usually be higher with WiFi than for cellular access. However the availability of this bandwidth depends on what the access point owner are using it for at the given moment. With complex configurations of the OBAN RGW and configuration of the access line with the help of the fixed operator, it could be possible to improve the utilization of the bandwidth.

WiMAX may be used as an alternative backhaul technology to DSL or cable. The total capacity is high about 54 Mb/s, but this capacity must be shared between more customers.

Due to the enhanced functionality offered by OBAN, service providers could build a wireless Internet access offer on the move, which appears to be distinct from other existing wireless Internet access like 2.5G/3G, Wi-Fi hotspots or residential WLAN.

This offer could bring new added values to the customer:

• More bandwidth compared to 2.5G/ 3G data offers and probably more affordable

• Increased availability and enhanced ergonomics compared to hotspot coverage and also mobility possibilities

To avoid destructing value, the offer should exclude voice services or P2P services. For this purpose, specific technical mechanisms are implemented in the OBAN architecture to be deployed for this offer.

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

14

3.2. OBAN application examples

OBAN is defined here as a connectivity service based on WLAN interfacing a fixed access infrastructure with possible handover and interworking with mobile networks like 2G /3G. This high bandwidth wireless connectivity service may constitute a basis to support several interesting applications that may enhance the application portfolio of the 2G/3G networks. Due to OBAN these services may be more user friendly (i.e. accessible wherever you are), cheap to use due to the network if the networks are charged differently and may be used more flexibly as today e.g. across terminal devices.

The target market for OBAN is primarily the residential market. However, the business market may also deploy OBAN technology, e.g. in term of mobile office solutions, but this has not been the main focus area of the project and the analysis of the business potential.

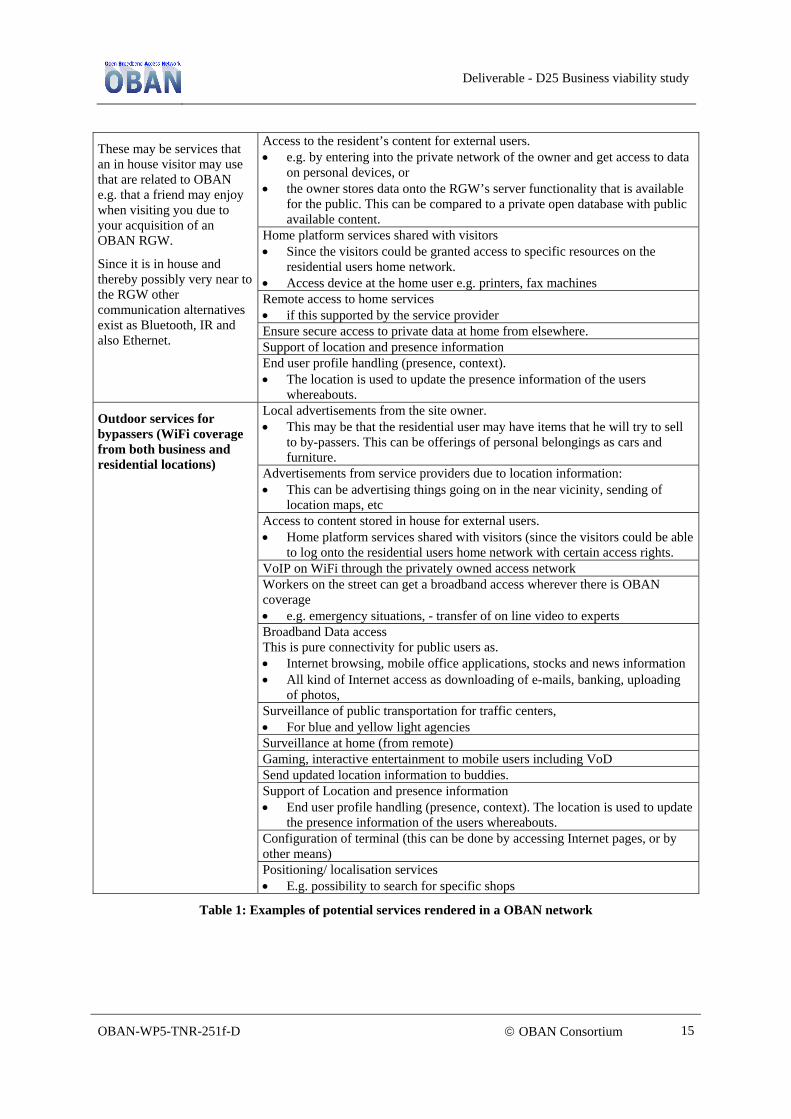

The applications usage by OBAN may be grouped into 3(4) groups due to different users and environments for service rendering:

• In house services enabled by OBAN for the home user

• In house services enabled by OBAN for visiting users (visitors entering into the house, friends, carpenters, plumbers, etc)

• OBAN services for outdoor by-passers

• OBAN services for the business segment

These categories are overlapping in a sense, but could have some different implications. (Not only seen from the user but also from the operators and service providers involved and possibly other market players as well)

Enable the cellular (GSM/UMTS) phone (device) to connect through the fixed (or WiMax, WLL) network. • This means always being reachable on the same devices through a

broadband access link instead of the cellular network. Possibility to use the RGW as a home platform server/controller. • The RGW may be built modular with the possibility to enhance it with open

source gateway application service bundles and universal plug and play and/or multimedia home platform functionality to support private in house networking and roaming.

Possibility to share the access line with visitors and the public and let the visitor pay for their own usage. Possibility for the residential user to use the public part of the access point for work related tasks. • e.g. home office where another party pays for the access resources Automatically synchronization of home server and network server so the in house server always has a backup copy in the network. Synchronization of calendars and other information for “family” and friends use Digital “deposit boxes” for storing of sensitive and critical information • E.g. insurance papers, health information for elderly)

In house services enabled by OBAN for residential user.

These are services that the residential user will see as value added services to himself due to OBAN. This may be due to new services, more easy to apply services, due to cheaper service rendering, better quality on existing services etc.

Sales offers/ advertisements in a public server in the private residences • E.g. directly connected to the RGW or as part of the home network (need

more security and access rights to enter the home network facilities/machines

In house applications enabled by OBAN for visiting user.

Visiting carpenters, plumbers etc could easily reach their office locations for information/and/or get help to do the work in the house by means of pictures/on line video.(manuals, telemedicine) • e.g. Mobile office applications

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

15

Access to the resident’s content for external users. • e.g. by entering into the private network of the owner and get access to data

on personal devices, or • the owner stores data onto the RGW’s server functionality that is available

for the public. This can be compared to a private open database with public available content.

Home platform services shared with visitors • Since the visitors could be granted access to specific resources on the

residential users home network. • Access device at the home user e.g. printers, fax machines Remote access to home services • if this supported by the service provider Ensure secure access to private data at home from elsewhere. Support of location and presence information

These may be services that an in house visitor may use that are related to OBAN e.g. that a friend may enjoy when visiting you due to your acquisition of an OBAN RGW.

Since it is in house and thereby possibly very near to the RGW other communication alternatives exist as Bluetooth, IR and also Ethernet.

End user profile handling (presence, context). • The location is used to update the presence information of the users

whereabouts. Local advertisements from the site owner. • This may be that the residential user may have items that he will try to sell

to by-passers. This can be offerings of personal belongings as cars and furniture.

Advertisements from service providers due to location information: • This can be advertising things going on in the near vicinity, sending of

location maps, etc Access to content stored in house for external users. • Home platform services shared with visitors (since the visitors could be able

to log onto the residential users home network with certain access rights. VoIP on WiFi through the privately owned access network Workers on the street can get a broadband access wherever there is OBAN coverage • e.g. emergency situations, - transfer of on line video to experts Broadband Data access This is pure connectivity for public users as. • Internet browsing, mobile office applications, stocks and news information • All kind of Internet access as downloading of e-mails, banking, uploading

of photos, Surveillance of public transportation for traffic centers, • For blue and yellow light agencies Surveillance at home (from remote) Gaming, interactive entertainment to mobile users including VoD Send updated location information to buddies. Support of Location and presence information • End user profile handling (presence, context). The location is used to update

the presence information of the users whereabouts. Configuration of terminal (this can be done by accessing Internet pages, or by other means)

Outdoor services for bypassers (WiFi coverage from both business and residential locations)

Positioning/ localisation services • E.g. possibility to search for specific shops

Table 1: Examples of potential services rendered in a OBAN network

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

16

4. Business modelling method/approach

Before going into detailed business modelling work, a common view of what a business model is needed. In this chapter we suggest a structured approach to business modelling as to be able to conduct techno economic analyses on selected business cases afterwards. Not only is it valuable to have a common view of the term business model but also to have a common view of what we understand with a business case. Different business models will be evaluated. In this context it is important to decide what parameters distinguish business models from each other. E.g. how big a change in the role/actor model will justify that it is a new business model? E.g. if we just change a pricing scheme from volume based charging to flat rate. Is this a new business case?

4.1. Definition of the term business model

Let us first draw a distinction between some concepts often confused: a ‘business idea’, a ‘business model’, and the concept of a ‘business case’ and a ‘business plan’.

• A ‘business idea’ is just what it seems, an idea for a business, or for a way of making a profit. In order to become a viable business, any business idea needs development, and it needs an organised framework or value creation logic to support it. The necessary framework for supporting a business idea is in our view what deserves the denotation ‘business model’.

• A business model is as the name suggests a model. Hence it contains many indeterminate parameters or variables, only describing the structural aspects of our business. It is a snapshot of the reality where certain aspects of business are put in focus and modelled. Several elements are built in a business model – roles and relationships model, revenue model, cost model, market model, demand model, technology model, value model, etc. Not necessarily are all models developed for each case.

• A business case is (again as the name suggests) an instance of the model, where indeterminate parameters have been given values. We cannot compute the profitability of a business model, without creating a case where all the numbers have been given values either through educated guesswork, or through empirical studies.

• A business plan is often denoted the document that describes the business of a company for a set of services or products. It contains a description of business, market segments, competitors, information about the company and its leaders/board, financial sheets (balance sheet, cost,) etc.

To be sure that all relevant information is gathered to be able to convey concrete information with the business models, several relevant question should be answered. By analysing these questions it is possible to reveal weaknesses in the proposed innovation prospects and help to guide us through the process of service innovations.

A functional definition of the business model term proposed by Chesbrough and Rosenbloom in [Chesborough 2002] has six main business elements:

1. Value proposition, describing the service we are going to sell and why it has value for our customers.

2. Customers and market segments, who our customers are and how they are distributed in various markets and market segments

3. Cost structure and profit potential, how all the costs of bringing our service to market is allocated on various elements, and how we propose to generate revenue and hence profit

4. Internal value chains, how we are proposing to produce and distribute our service, including all the necessary operational aspects

5. Position in the value network, how we propose to be positioned among the actors needed to bring our service to market, and

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

17

6. Strategy for positioning and competition - the strategy we propose to position ourselves in the marketplace and to compete successfully.

7. Technical realisation - how different technical realisations will impact the profitability and how the best technical realisation ought to be.

Business model

Value proposition

Customer and market

Cost structure and Profit potential

Internal value chain

Position in theValue network

Strategy for Positioning, and timing

Technical realisation

Business model

Value proposition

Customer and market

Cost structure and Profit potential

Internal value chain

Position in theValue network

Strategy for Positioning, and competition

Technical realisation

Figure 3: Business elements to construct business models

Osterwalder [Osterwalder 2004] propose a similar set of elements, albeit with some naming differences. Osterwalders 9 elements are the same as Chesborough et al’s, with two differences. First, Osterwalder has exploded parts of some of Chesborough and Rosenbloom’s elements. Second, the element of strategy for positioning and competition is missing as an explicit element in Osterwalders listing.

The term service is used quite a lot, and hence we need to state what we should mean by this.

Service: The service is what is generating revenue through sales in a market. This means that a service is something a customer is willing to pay for, and this may be tangible or intangible. This being said, the end result is always assumed to be that the customer is paying for either kind of service or bundle of services.

If we accept that a ‘business model’ is a description of ‘the logic of making a profit’ then new business models only appear as a result of changes in the logic of making a profit. What constitutes such a ‘change in logic’? Intuitively and informally such a change is happening when ‘the way we are doing business’ is changed. In OBAN this may be a change in the role model, e.g. what market players are involved in OBAN service delivery, or the ownership of the RGW or the way OBAN services are charged.

In chapter 0 several business models will be analysed. Each of them comprises a basic set of information that describes the logic of making profit, e.g. taking on the role of controlling and managing the RGW. The interactions between these different market players in a business model are either direct or indirect stakeholders to OBAN service provisioning. Money flows, service agreements, physical traffic flow etc are all relevant information to show the interaction between the market players, in addition to analysing their position in the value network.

4.2. Business model elements

The following elements need to be analysed to be able to construct a viable business model comprising the different aspect as demand modelling, cost modelling, market modelling etc.

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

18

4.2.1. Value proposition

The value proposition is the more or less concise formulation of the benefit (value) that the customer should get from our offering. The customer could be the end user or an enterprise within the value chain of the service creation and delivery platform. These two market players will look at different aspects concerning the value proposition. For both players the focus is on the fact that revenue generation is caused by the sale of goods in a market. Hence, when describing a value proposition we shall insist on being as concrete as possible with respect to services. The reason is rather obvious: if we do not have a service to sell, no revenue can be generated and any considerations on competition, markets or costs will at best be a purely academic exercise. This is a particular challenge when dealing with innovations: what can be done to investigate “future business models” for services yet to hit the market, or entirely new services based on new uses of technology or even entirely new technology? A good example of this is the way network infrastructure investments have to be decided before broadband services (e.g. OBAN services) can be sold to the market: what are the products we are going to sell that will create the revenues paying for this investment in the long run?

To analyse the potential revenue, several question need to be asked e.g.:

• Is it a tangible service or not

• What problem does the service solve for customers?

• How will the service be sold to customers?

• Does the service come in separate units or packaged with other services?

• How will the service be distributed to customers?

• Does the service substitute or cannibalise other services? Own services or competitor’s services.

Even if a service in itself will not create a revenue stream in terms of increased usage by the end user the service may lead to other types of benefits such as:

• Efficiency improvements: The service will give significant efficiency benefits in the firms’ operations (production, operations, sales, customer care, etc).

• Cost reductions (The service will give a significant cost reducing potential for the firm producing and delivering the service)

• Improved customer satisfaction

• Enhanced service portfolio (e.g. bundling benefits)

4.2.2. Customer and market segments:

The second element concerns the fact that a service needs to be sold to someone, and hence that we need customers forming a market and market segments. When describing a market we need to answer the question:

“What problem does our service solve for the customer in this particular segment?”

We believe that it is beneficial to pose this as a solution to some problem, rather than as some ‘need’ or wishes the customer might have, since it is easier to conjure up some fictitious need than a fake problem. Many failed services are just that because they simply did not bring any new solutions to real problems the customers had, and hence they did not find it worth paying for the service.

The customer would differ related to the position in the value network. One market player is a buyer of services from one market player and a seller “good” to someone else. This may be transport resources, content, service packing etc. However in this study the main focus will be the end user market since it is the end users that supply the money for services for all the involved players. How the money flows within the value chain is of interest and importance, but it is not so easy to grasp due to aspects as cooperation’s, internal service level agreements, regulatory issues etc.

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

19

4.2.3. Internal value chains

If we have a service and a market potential, how are we going to produce the service and bring it to market? The internal value chains of a company may be complex and non-trivial to grasp fully. Further we need a good understanding of the critical production factors or essential inputs needed. We cannot produce a service if we need access to some resource on terms that may never be realised. It is also vital to ascertain that we have the possibility to scale up our production for volumes needed to make a profit. Last, but not least this part of the analysis may reveal that we lack the internal value chains needed, and hence prompt the question of whether such a capability should be built or acquired.

In short: -are we able to produce and deliver the service in mind? If no- what do we need to be able to do it?

4.2.4. Cost structure - technical considerations

The fourth issue is the one of costs. This is probably the best known issue to many, but nevertheless one where we often fail, simply because we are unrealistic with respect to what it will cost to produce, market/sell and distribute the services.

This point demands knowledge of the technical architecture to deliver the service from the service provider to the customer to be able to estimate the CAPEX and OPEX costs.

The technical architecture and functionality may also impact the way the different market players could position themselves in the value network and what function/roles they may take. E.g. the ownership of the RGW may impact the profit potential due to what functionality is implemented.

The functionality of the RGW will also influence the way different market players can use the component.

4.2.5. Position in the value network

Fifth is the issue of how our venture should place itself in the network of players necessary to bring our service to market, hence -‘the value network’. This network is a network of relations between actors in the market place, comprising the producer and all subcontractors, the customers, distributors, etc. This network has the feature that it is essential to the business, and that if it does not exist in advance it may be extremely difficult to establish because of coordination problems leading to deadlock. The value network should include all market players/roles that are important to production, delivery and control/management of the OBAN service provisioning.

The role models depict the value networks and the market players taking on one or more roles comprise the value network. Between each market players service agreements need to be in place and the money flows and physical traffic paths need to be agreed upon and supported.

4.2.6. Strategy for positioning and competition

The last issue is the one of how we will stay in business and prosper. How do we compete successfully? An OBAN operator will be positioned in a market with many other competing market players supplying similar or substituting services. How should the OBAN service providers act upon competing technologies and potential cannibalising services?

There are several ways to position in the market.

• Charging mechanisms

• Cooperation’s and alliances

• Service distinguishing mechanisms (bundling, ..)

• Service support and marketing and distribution

• Branding

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

20

4.2.7. Modelling frameworks applicability to OBAN

The described business-modelling framework is directly applicable to the work on OBAN business modelling in this deliverable. The framework will therefore be followed as close as possible in all models. The internal value chain will however not be covered due to competition reasons and sharing of company internal matters.

To try to describe the viability of each model they are quite detailed regarding technical and commercial aspects. Some knowledge about IP and IP protocols for mobility, security and QOS is thus required to get a good understanding of each model.

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

21

5. OBAN Business roles and role modelling framework

In this chapter we present a structured discussion of some business aspects of wireless access provisioning in the light of technology considered in the OBAN project. The aim is to shed light on the strategic implications of the technology with respect to incumbent and emerging actors in the Telecom market. The discussion is carried out with the use of a role model, with the inclusion of various actor models.

The terms roles and actor is used repeatedly in the following chapters. In this report we use the following definitions.

Business role:

A group of functions enabling an entity taking on the role to provide a set of services to its environment. Examples include end-user, customer, network operator, service provider, service integrator, content provider, content producer, clearing house, billing service provider, APS, etc.

Business actor

An organisation that plays one or more roles. Note: An organisation may imply several notions like an individual, a commercial company, a government agency, a non-governmental organisation, etc.

Some interesting actors in this context are:

• Fixed access operators, mobile access operators (new + incumbent),

• WLAN hotspot operators & aggregators,

• Service providers (ISP + Mobile).

All these actors are operating in the market today and all of them need to evolve their business to be able to compete with other actors.

5.1. Roles and role model

In order to discuss business aspects of OBAN we propose a role model featuring the following roles:

Roles Description

Residential gateway operator (RGWO): Controls the configuration and operation of the residential gateway.

Site owner (SO):

In addition to provide housing of the RGW, the site owner may be a traditional broadband fixed access subscriber.

Residential user(RU) In many cases the same entity as the Site Owner

Visiting user (VU):

A user different from the site owner that accesses services available at the residential gateway.

Mobile service provider (MSP): Offers publicly available mobile services (e.g., speech, messaging, multimedia, Internet access)

Fixed service provider (SP): Offers Internet services available over fixed or dial up access

Mobile access operator (MAO): Operator of wireless access networks that can be used for providing mobile services

Deliverable - D25 Business viability study

OBAN-WP5-TNR-251f-D © OBAN Consortium

22

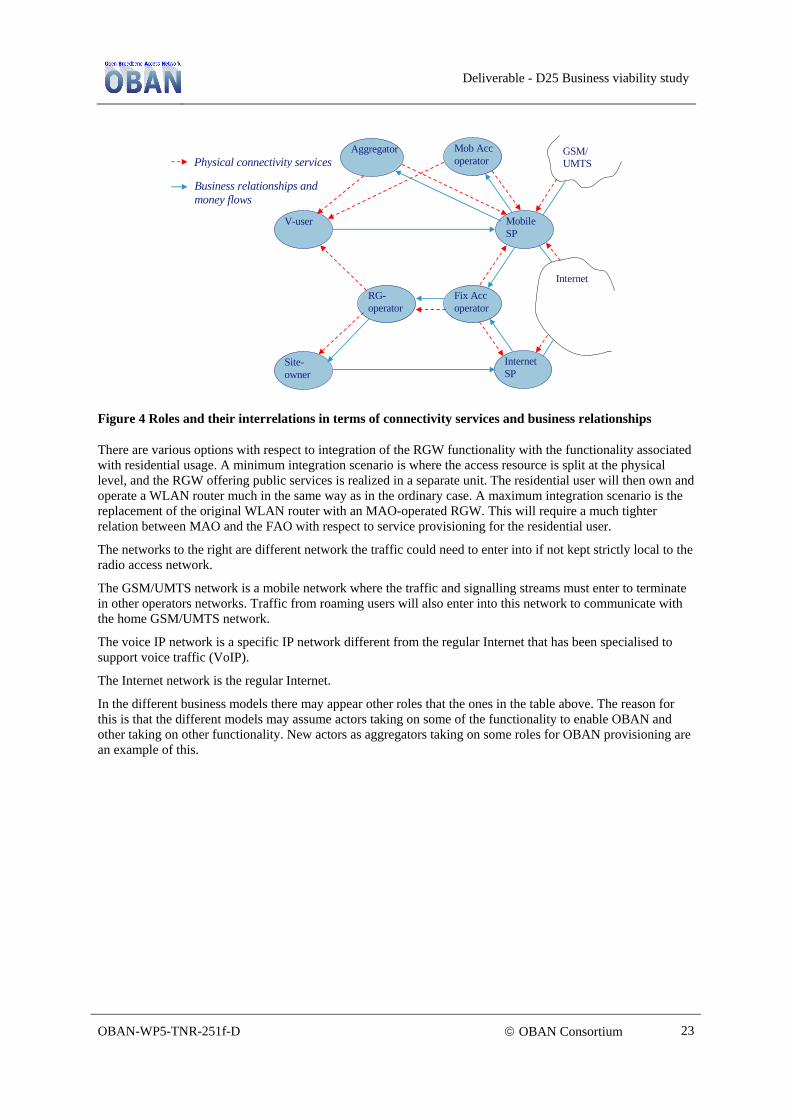

Fixed access operator (FAO):

Operator of fixed access (e.g. DSL) networks. It may sell capacity on a wholesale fashion as operator access, bit stream or other scenarios.

OBAN aggregator The aggregator acts as an intermediary between RGWOs (particularly in the context of hot-spot operations) and service providers. The aggregator handles roaming and access control such that several hot-spot domains to the service provider appear as a single unit.

Table 2: General roles definitions for the OBAN business models

Several actors may want to control the residential gateway (RGW). Therefore, RGW-operation is separated into a role that can be performed by several actors. The basic function of the RGW will be to provide local WLAN-based radio access, separation of domestic (for the site owner) versus external use, and resource management and usage metering. Depending on who actually performs the role, RGW-functionality can be further tailored.

The RGW is located at the premise of the site owner (SO). In anticipation that the RGW may be an evolution of a domestic WLAN router, the SO is given a special status as user (residential user) compared to other occasional users. Other users are named visiting end-users (VU) here. It is envisaged that, in many cases the SO is the same entity as the RGW owner. However the RGW owner may also be the RGWO.

A mobile service provider (MSP) is the unit offering traditional and emerging mobile services to end-users. It offers two-way reachability by operating a location register. The MSP also offers mobile Internet access. In order to offer its services, the MSP needs to use the network and services of a Mobile access operator (MAO). The Mobile access operator has the radio nodes providing regional (usually country-wide) mobile services. It also handles access control, usage metering and mobility handling.

Internet service provider (ISP) is the unit offering traditional end emerging Internet services, such as Internet access, mail etc. In particular, the ISP will offer VoIP services. The ISP handles the interconnect agreements towards other parts of the global Internet. In our context, the ISP offers its services through a fixed access network such as DSL or cable. This access network is operated by a fixed access operator (FAO), which conceptually offers a bitpipe with certain characteristics (service classes, etc.) between access points at the user premise and the ISP premise.

There are several parties left out in the discussion, such as application service providers, content providers, equipment vendors and backbone network operators. Even though these may deliver important premises, we consider that they will not have important strategic roles with respect to the particular aspects discussed here.