DECRIMINALISATION OF TAX LAW BY ADMINISTRATIVE PENALTIES .... Dr. Funda Basaran Yavaslar.pdf ·...

18

DECRIMINALISATION OF TAX LAW BY ADMINISTRATIVE PENALTIES ON TAX DUTIES COMMENT TO REPORT OF PROF. DR. LORENZO DEL FEDERICO PROF. DR. FUNDA BAŞARAN YAVAŞLAR LAW FACULTY OF MARMARA UNIVERSITY, ISTANBUL/TURKEY

Transcript of DECRIMINALISATION OF TAX LAW BY ADMINISTRATIVE PENALTIES .... Dr. Funda Basaran Yavaslar.pdf ·...

DECRIMINALISATION OF TAX

LAW BY ADMINISTRATIVE

PENALTIES ON TAX DUTIES COMMENT TO REPORT OF PROF DR LORENZO DEL

FEDERICO

PROF DR FUNDA BAŞARAN YAVAŞLAR

LAW FACULTY OF MARMARA UNIVERSITY

ISTANBULTURKEY

OBJECTIVE DISCRIMINATION

MAIN OBJECTIVE OF

CRIMINAL LAW

PUNISHING THE ILLEGAL ACT

MAIN OBJECTIVE IN

DECRIMINALIZATION

COMPENSATION OF THE

DAMAGE ARISING DUE TO THE

ILLEGAL ACT

The purpose of decriminalization is different from the object of punishment

prescribed by the criminal law and consequently decriminalization needs a

paradigm change Value judgments and rules of criminal law or criminal law

doctrine can no longer influence how the action shall be evaluated

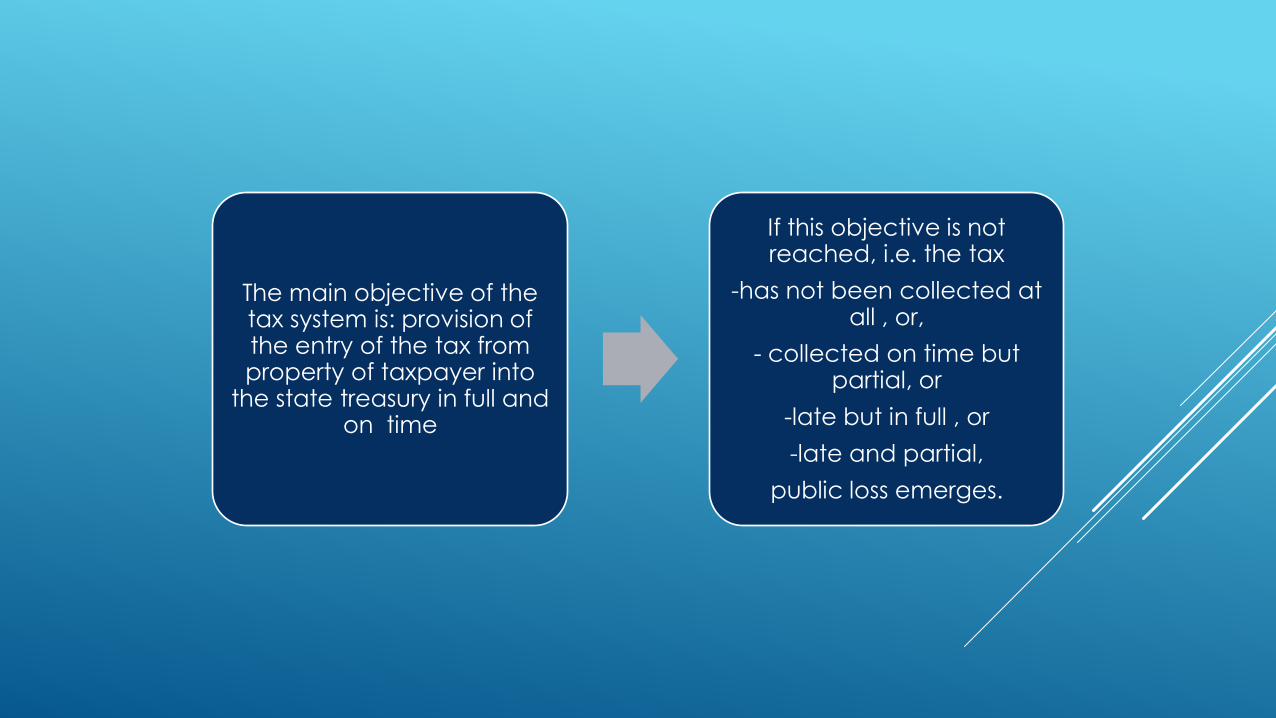

The main objective of the tax system is provision of the entry of the tax from property of taxpayer into

the state treasury in full and on time

If this objective is not reached ie the tax

-has not been collected at all or

- collected on time but partial or

-late but in full or

-late and partial

public loss emerges

Less tax income =

public loss =

Violation of the public order

Default of public service or incomplete

performance thereof in quantities or qualities

Performance of public service at higher cost

- indebtedness

- privatization

- hellip

Depriving the taxpayer acting in

contradiction with the law of hisher

freedom (imprisonment) does not

compensate the damage On the

contrary since the person in jail cannot

perform hisher joboccupation heshe

will neither generate revenue nor pay

tax

THE SANCTION TO BE APPLIED TO THE

ILLEGAL ACT IN DECRIMINALIZATION

THE OCCURRED DAMAGE

MEANS IN DETERRENT

NATURE

SANCTION

THE MISSING TAX AMOUNT

INFLATION DIFFERENCE DUE

TO LATE COLLECTION

THE ADDITIONAL PUBLIC COST ARISING IN

ORDER FOR THE PROVISION OF

PUBLIC SERVICE

THE OCCURRED

DAMAGE

MEA

NS IN

DETE

RR

EN

T N

ATU

RE THE SURCHARGE (ADDITIONAL PAYMENT) AT

LEAST DOUBLE THE AMOUNT OF THE BENEFIT PROVIDED BY THE TAXPAYER DUE TO PARTIAL

ANDOR LATE PAYMENT BUT THE MARKET PRICE HERE CAN BE TAKEN INTO ACCOUNT

AS AN OBJECTIVE CRITERIA

DEPRIVING OF A RIGHT WITH RESPECT TO TAXATION (FOR INSTANCE PROHIBITION OF

BENEFITING FROM TAX INCENTIVE PROHIBITION FOR APPLYING FOR

RECONCILATION)

THANK YOU FOR THE ATTENTION PROF DR FUNDA BAŞARAN YAVAŞLAR

1

Decriminalization of Tax Law by Administrative Penalties on Tax Duties

-Comment to Report of Prof Dr Lorenzo Del Federico-

Prof Dr Funda BASARAN YAVASLAR

Table of contents

1 The Meaning of Decriminalization

2 The Reasons for A Need of Decriminalization in Tax Law

3 Conclusion

Head of Chair for Fiscal Law Law Faculty of Marmara University

2

1 The Meaning of Decriminalization

11 Decriminalization in terms of its lexical meaning refers to rendering an illegal action as

ldquonon-criminalrdquo in other words to remove an action from the legal category of criminal

offence This can be achieved in two ways1

-either an action is removed completely from the scope of sanction law in a way that it

wouldnrsquot be subjected to any legal norm involving sanction

-or such action is only rendered as non-crime but remains as an illegal act and therefore

continues to be a matter of public sanction

ldquoDecriminalization of Tax Law by Administrative Penalties on Tax Dutiesrdquo which is the

subject of this third session of the meeting refers to this second meaning Accordingly

failure to fulfill tax duty continues to be regarded as an illegal action and sanctions continue

to be applied on the perpetrator The only difference is that such illegal action shall no

longer be considered as a ldquocrimerdquo

12 Therefore first of all it is required to determine what is considered as ldquocrimerdquo in order

to determine the illegality that will be subjected to decriminalization

There are three different approaches raised in the general theory of criminal law as to what

constitutes a crime2 ldquoopinions taking qualitative distinction as basisrdquo ldquoopinions taking

quantitative distinction as basisrdquo and ldquoopinions taking both qualitative and quantitative

distinctions as basisrdquo Opinions taking qualitative distinction as basis focus more on the

objective and subjective criteria Thus in that regard a qualification is made by taking into

consideration the action the perpetrator the moral element but in particular the legal

benefit which has been breached In this context as far as the qualification of crime is

1 K Bayraktar Ceza Hukukunda Succedil Olmaktan Ccedilıkarma Akımı İHFM 1-4 p198-199 (1984) T Demirbaş Ceza

Hukuku Genel Huumlkuumlmler ch3 p193 (Seccedilkin 2013) R Praetorius Entkriminalisierung und alternative Sanktionen Kriminalpolitik ch18 181 (H-J Lange Ed Springer 2008) 2 S Doumlnmezer S Erman Ceza Hukuku Genel Kısım C1 no493 f p344 f (Filiz 1985) F Haft Strafrecht

Allgemeiner Teilch3 p12 f (CH Beck 1984) F S Mahmutoğlu Succedil-Kabahat Ayırımı- İdari Ceza Hukukursquonun Temelleri 32 p33-36 (İ Ulusan F Başaran Yavaşlar eds Seccedilkin 2009) R Maurach Deutsches Strafrecht Allgemeiner Teil ch13 141 f (CF Muumlller 1971) W Mitsch Recht der Ordnungswidrigkeiten ch3 p30 (Springer 1995) P Noll Schweizerisches Strafrecht Allgemeiner Teil I Allgemeine Voraussetzungen der strafbarkeit ch6 p 21 f (Schultess Polygrapisch 1981) I Oumlzgenccedil Tuumlrk Ceza Hukuku Genel Huumlkuumlmler ch12 151 f (Seccedilkin 2008) N Toroslu Ceza Hukuku Genel Huumlkuumlmlerch2 2 and 3 p 91 f (Savaş 2013)

3

concerned it is important to identify ldquowhether the protected legal benefit is of social

valuerdquo ldquowhether the perpetrator is characterized as covetous manipulative or only as an

undisciplined or despicable personrdquo ldquowhether the action involves penetrating into and

encroachment upon a foreign powerrdquo or ldquowhether the requirements regarding the goal

idealized for ensuring the public order have been interruptedrdquo thus whether there is an

action of crime (someone or something seriously exposed to danger)

Opinions taking quantitative distinction as basis on the other hand focus on the sanction to

be imposed by indicating that the damage and danger in case of crimes is greater

Whereas opinions taking both qualitative and quantitative distinction in basis the crime is

qualified by taking into consideration both the significance of the breached legal benefit or

act as well as the extent of the damage incurred

ECHR on the other hand in fact binds itself with the qualification made by the national

legislator in two of the three criteria3 which it uses to determine the existence of crime

3For example FIN ECHR 23 Nov 2006 Jussila versus Finland application no 7305301

(httphudocechrcoeintengappno[7305301]itemid[001-78135] accessed 18 Nov 2015) bdquo30 The Courtrsquos established case-law sets out three criteria to be considered in the assessment of the applicability of the criminal aspect These criteria sometimes referred to as the ldquoEngel criteriardquo were most recently affirmed by the Grand Chamber in Ezeh and Connors v the United Kingdom ([GC] nos 3966598 and 4008698 sect 82 ECHR 2003-X)

ldquo [I]t is first necessary to know whether the provision(s) defining the offence charged belong according to the legal system of the respondent State to criminal law disciplinary law or both concurrently This however provides no more than a starting point The indications so afforded have only a formal and relative value and must be examined in the light of the common denominator of the respective legislation of the various Contracting States The very nature of the offence is a factor of greater import However supervision by the Court does not stop there Such supervision would generally prove to be illusory if it did not also take into consideration the degree of severity of the penalty that the person concerned risks incurring rdquo

31 The second and third criteria are alternative and not necessarily cumulative It is enough that the offence in question is by its nature to be regarded as criminal or that the offence renders the person liable to a penalty which by its nature and degree of severity belongs in the general criminal sphere (see Ezeh and Connors cited above sect 86) The relative lack of seriousness of the penalty cannot divest an offence of its inherently criminal character (see Oumlztuumlrk v Germany 21 February 1984 sect 54 Series A no 73 see also Lutz v Germany 25 August 1987 sect 55 Series A no 123) This does not exclude a cumulative approach where separate analysis of each criterion does not make it possible to reach a clear conclusion as to the existence of a criminal charge (see Ezeh and Connors cited above sect 86 citing inter alia Bendenoun cited above sect 47)rdquo Also please see DE ECHR 21 Feb1984 Oumlztuumlrk versus Germany application no 854479 sect 53 (httphudocechrcoeintsitesengpagessearchaspxi=001-57553 retrieved 7 Dec 2015) F ECHR 24 Feb 1994 Bendenoun versus France applicaiton no 1254786 sect 47 (httphudocechrcoeintsitesengpagessearchaspxi=001-57863 retrieved 7 Dec 2015) S ECHR 23 Juli 2002 Janosevic versus Sweeden application no 3461997 no 65 (httphudocechrcoeintengfulltext[taxaudit]documentcollectionid2[GRANDCHAMBERCHAMBER]itemid[001-60628] retrieved 7 Dec 2015) According to this decision (no68) ldquohellip the lack of

4

because consequently qualification of illegality as a crime in the national law as well as

punishment of such illegality by aggravated means is the decision of the national legislator

Therefore the only authentic answer given by ECHR to the question of what constitutes

ldquocrimerdquo which we set out as our starting point in order to identify the subject of

decriminalization is observed within the criteria of ldquothe nature of the illegal actionrdquo On the

other hand it determines on whether or not the illegality is of criminal quality by its nature

is made by considering how the illegality is interpreted in the majority of the other states

that are party to the Convention and by identifying that the illegality is not directed only to a

certain group designated with special status (eg as in the case of disciplinary law) but on

the contrary directed to ldquoall citizensrdquo due to its nature (eg as in the case of traffic

legislation) Considering that the criteria of being ldquodirected to all citizensrdquo is a relative

concept the only concrete criteria for the determination of the existence of the crime is

whether or not the relevant illegality is qualified as a crime in the majority of the states that

are party to the Convention Thus ECHR takes the value judgment of the majority as basis

13 The conclusion of all these explanations is that by way of decriminalization the

legislator ceases to characterize an illegality which ldquoviolates a great legal benefitrdquo or

ldquoseverely violates a legal benefitrdquo or ldquowhich constitutes a crime according to many statesrdquo

as not an act of crime Therefore the legislator has an extremely conscious preference in

this respect Hence the legislator becomes no longer interested in either the degree of

fault or the significance of the breached legal benefit or action or the extent of the damage

incurred or even any criteria deemed important in determining whether or not a crime

exists The reason of this is that as will be examined in more detail below the purpose of

subjective elements does not necessarily deprive an offence of its criminal character indeed criminal offences based solely on objective elements may be found in the laws of the Contracting States (see Salabiaku v France judgment of 7 October 1988 Series A no 141-A p 15 sect 27) In this connection the Court notes that the present system of tax surcharges has replaced earlier purely criminal procedures It appears that the change from the earlier system which was one of penalties for intentional or negligent conduct to the new system based on objective factors was prompted by the need for greater efficiency (see paragraph 32 above) Furthermore the present tax surcharges are not intended as pecuniary compensation for any costs that may have been incurred as a result of the taxpayers conduct Rather the main purpose of the relevant provisions on surcharges is to exert pressure on taxpayers to comply with their legal obligations and to punish breaches of those obligations The penalties are thus both deterrent and punitive The latter character is the customary distinguishing feature of a criminal penalty (see Oumlztuumlrk cited above pp 20-21 sect 53) In the Courts opinion the general character of the legal provisions on tax surcharges and the purpose of the penalties which are both deterrent and punitive suffice to show that for the purposes of Article 6 of the Convention the applicant was charged with a criminal offencerdquo (Bold emphasis belong to the Author)

5

decriminalization is different from the object of punishment prescribed by the criminal law

and consequently decriminalization needs a paradigm change Value judgments and rules of

criminal law or criminal law doctrine can no longer influence how the action shall be

evaluated

14 When we focus solely on tax law it is initially required to make the following

determination legislators of many countries4 have accepted ldquotax evasionrdquo or ldquothe conducts

precluding the Administration from detecting taxrdquo as a crime Therefore in the event that

the legislator applies a 100 decriminalization and does not include crime in the tax law in

any way this would mean that no circumstances including ldquotax evasionrdquo shall be considered

as a criminal illegality

2 The Reasons for a Need of Decriminalization in Tax Law

21 It is necessary to ask why a legislator ceases to render an illegality as a crime which it

normally renders as a crime What could be the legitimate reason of decriminalizing an

illegality In my opinion in terms of tax law these questions can be answered as follows

The principal reason for the existence of tax system is to levy tax on the assets of the

taxpayer and transfer to the treasury In other words the entire tax system is established on

the objective of ldquogenerating tax revenue in full and on timerdquo Generating no or lower amount

of tax or generating of tax in an untimely manner either results in a default in public service

or incomplete performance thereof in terms of quantity or quality or causes the

performance of the public service by incurring a higher amount of expenses (through means

such as indebtedness privatization) even if the public service will be performed completely

and with the targeted quality

Such a system of course can be tried to be protected by implementing severe sanctions

like imprisonment just like it is the case in the criminal law However here it is required to

make a choice regarding to the tool to be used to achieve the goal Which one serves best to

the goal of ldquogenerating tax revenuerdquo ldquoimprisoning the taxpayer and so restricting his

4 R Seer A L Wilms General Report bdquoSurcharges and Penalties in Tax Lawldquowithin this book Sec 13 G

Dannecker O Jansen Generalbericht in Steuerstrafrecht in Europa und den Vereinigten Staaten 2 bb and cc p30 -31 (G Dannecker O Jansen eds Linde 2007)

6

freedom and impeding him from continuing to execute his activities subjected to taxrdquo or

ldquoimposing severe fines or deprivation of rights obstructing his economic activities and in this

way killing or paralyzing him economicallyrdquo Or does it serve better to the goal of

ldquogenerating tax revenuerdquo to compensate the damage due to his illegal actions as well as to

retrieve all the benefits gained or which may be gained by the tax-payer through such

illegality

If we are to focus on the main goal of the tax legislation the second way thus

decriminalization should be preferred5

22 As can be seen the purpose of decriminalization is different The main goal with

decriminalization is to remedy the damage inflicted on the goal of the tax system due to the

illegal act thus the compensation of the damage6 The occurred damage consists from the

missing tax amount inflation difference due to the late collection and the additional public

cost arising in order for the provision of public service

5 See K Tipke Die Steuerrechtsordnung BdIII ch36 54 p1756 f (Otto Schmidt 2012) ldquoIm Allgemeinen

besteht auch kein Beduumlrfnis dafuumlr Steuerhinterzieher ldquohinter Gitterrdquo zu bringen Sie gefaehrden nicht die oumlffentliche Sicherheit Die Freiheitsstrafe sollte gemeingefaehrlichen Gewalttaetern vorbehalten bleiben Steuerhinterzieher werden durch Freiheitsstrafen nur daran gehindert ihrem Erwerb nachzugehen und dadurch Steuerschulden auszuloumlsen Wenn dem Staat Geld vorenthalten wird so passt dazu die Geldstrafe oder eine andere Geldsanktionrdquo Also please see M Streck Harzburger Protokoll 1999 p83 ( ldquoWarum stecken wir Lesitungstraeger dieser Gesellschaft in ein Gefaengnis wo sie nur Kosten verursachen warum sagen wir nicht sie koumlnnten das Gefaegnis dadurch vermeiden dass sie den dreifachen Betrag der hintergezogenen Steuer zahlen Waere das nicht eher im Sinn des sect 370 AO der das Steueraufkommen sichern sollrdquo) and J Weigell Uumlberlegungen zum Steuer(straf)recht in Festschrift fuumlr M Streck p 609 (Ed B Binnewies R Spatscheck Otto Schmidt 2011) (K Tipke p 1756 footnotes 149 and 150) For a different approach please see R Seer (Steuerrecht Materielles Steuerstraf- und ordnungswidrigkeitenrecht ch23 p1368-1369 [K Tipke et al eds Otto Schmidt 2015]) who is defending the idea of depenalisation due to the unsuitability of taxpenalty law for compensation of structural enforsement deficits in taxation procedure ldquoDie wesentliche Rechtfertigung der Strafe ist die Herstellung eines Schuldausgleiches unter gleichzeitiger Beruumlcksichtigung spezial- und generalpraeventiver Gesichtspunkte Das Steuerstrafverfahren ist dementsprechend ein Individualverfahren das nach Schuld und Verantwortung fragt Das Steuerrecht ist deshalb ungeeignet strukturelle Vollzugsdefizite (s sect 3 Rz113 ff) auszugleichen und die gebotene Belastungsgleichheit herzustellen Aufgrud seines intensiven Eingriffscharakters bleibt das Mittel der Strafe die ultima ratio im Instrumentarium des Gesetzgebers (BVerfGE 39 1 [47]) Steuerliches Fehlverhalten im Massenverfahren ist deshalb primaer nicht durch das dafuumlr untaugliche Steuerstrafrecht sondern durch eine effiziente Ausgestaltung des hierfuumlr bestimmten Besteuerungsverfahren herzustellen hellip Statt die Strafbarkeitszone ndash ohne Ruumlcksicht auf Vollzugsfaehigkeit ndash normativ auszudehnen liesse sich die gewuumlnschte Praevention besser durch ein den Bereich der einfachen Steuerhinterziehung abdeckendes verschuldenabhaengigges Steuerzuschlagsystem erreichen (sog Entpoumlnalisierung des Steuerrechts)rdquo 6 A proposal for a surtaxsystem which bases on implementing the current market interest rate on the

determined tax after contolling of tax affair independent of fault see R Seer Steuerordnungswidrigkeiten im deutschen Recht in İdari Ceza Hukuku Sempozyumu 4 p242 (İ Ulusan F Başaran Yavaşlar eds Seckin 2009) and Konsensuale Paketloumlsungen im Steuerstrafrecht in Festschrift fuumlr G Kohlmann V p552 (Otto Schmidt 2003)

7

In my opinion as an additional deterrent measure the benefits gained by the perpetrator

through the illegal act should also be removed from that person Here the market interest

rate can be taken into account as an objective criteria and thus a reasonable surcharge may

be imposed Ultimately ldquono one could benefit from hisher illegal conductrdquo It can be also

considered to hinder the perpetrator from benefitting from certain advantageous tax

regulations such as by way of ldquoprohibition on applying for reconciliationldquo

I would like to point out here that differently from the criminal law in decriminalization

compensation and deterring are the primary focus like in the case of civil law rather than

punishing and deterring like in the case of criminal law

23 A last question Is the achievement of the eventual goal of ldquofinancing the public

expenditurerdquo with the least amount of damages constitutes the sole benefit of

decriminalization

If the legislator takes a hundred percent decriminalization decision in a way not to allow any

crime in the tax system also the following results will be achieved

Legislation duties shall be facilitated because in this way legislation shall be relieved from

-on one side difficulty of characterizing what is crime what is misdemeanor or contradictory

to another type of legislation

-accordingly on the other side difficulty of determining penalties in compliance with

equality and proportionality principals

Duties of criminal jurisdiction shall be facilitated because the tax crimes burden shall be

removed from the prosecutors and criminal judges who should carry out any research

themselves according to ex officio principle allowing them to focus on the subjects remaining

within the natural frame of criminal law and to achieve faster results

The criminal legislation which should be applied as the ultimate remedy for protecting the

public order for restricting peoplersquos freedom shall be more deterrent

Instead of long and complicated criminal prosecutions and investigations commissioning the

administration with the assignment and authorization to determine the illegal conduct shall

8

enable a fastest indemnification of the loss arising from the illegal action in an easy

procedure

Finally the problems due to double jeopardy under the same legislation (ne bis in idem) shall

be eliminated

3 Conclusion

Although it might seem unfair at first sight the decriminalization provides reasonable

solutions for the heavy problems of current tax surcharge system besides being a better tool

to achieve the ultimate goal of tax law

The only factor which endangers this whole positive picture could be that whether the tax

payers would be more daring to perform illegalities which may lead to tax evasion in a

decriminalized system However it is possible to overcome this danger by means of a well-

audited functional and gapless tax control system Because eventually even the existence

of severe penalties donrsquot constrain the taxpayers from intending to ldquocommit tax offencesrdquo in

a weak inefficient control system containing legal gaps

OBJECTIVE DISCRIMINATION

MAIN OBJECTIVE OF

CRIMINAL LAW

PUNISHING THE ILLEGAL ACT

MAIN OBJECTIVE IN

DECRIMINALIZATION

COMPENSATION OF THE

DAMAGE ARISING DUE TO THE

ILLEGAL ACT

The purpose of decriminalization is different from the object of punishment

prescribed by the criminal law and consequently decriminalization needs a

paradigm change Value judgments and rules of criminal law or criminal law

doctrine can no longer influence how the action shall be evaluated

The main objective of the tax system is provision of the entry of the tax from property of taxpayer into

the state treasury in full and on time

If this objective is not reached ie the tax

-has not been collected at all or

- collected on time but partial or

-late but in full or

-late and partial

public loss emerges

Less tax income =

public loss =

Violation of the public order

Default of public service or incomplete

performance thereof in quantities or qualities

Performance of public service at higher cost

- indebtedness

- privatization

- hellip

Depriving the taxpayer acting in

contradiction with the law of hisher

freedom (imprisonment) does not

compensate the damage On the

contrary since the person in jail cannot

perform hisher joboccupation heshe

will neither generate revenue nor pay

tax

THE SANCTION TO BE APPLIED TO THE

ILLEGAL ACT IN DECRIMINALIZATION

THE OCCURRED DAMAGE

MEANS IN DETERRENT

NATURE

SANCTION

THE MISSING TAX AMOUNT

INFLATION DIFFERENCE DUE

TO LATE COLLECTION

THE ADDITIONAL PUBLIC COST ARISING IN

ORDER FOR THE PROVISION OF

PUBLIC SERVICE

THE OCCURRED

DAMAGE

MEA

NS IN

DETE

RR

EN

T N

ATU

RE THE SURCHARGE (ADDITIONAL PAYMENT) AT

LEAST DOUBLE THE AMOUNT OF THE BENEFIT PROVIDED BY THE TAXPAYER DUE TO PARTIAL

ANDOR LATE PAYMENT BUT THE MARKET PRICE HERE CAN BE TAKEN INTO ACCOUNT

AS AN OBJECTIVE CRITERIA

DEPRIVING OF A RIGHT WITH RESPECT TO TAXATION (FOR INSTANCE PROHIBITION OF

BENEFITING FROM TAX INCENTIVE PROHIBITION FOR APPLYING FOR

RECONCILATION)

THANK YOU FOR THE ATTENTION PROF DR FUNDA BAŞARAN YAVAŞLAR

1

Decriminalization of Tax Law by Administrative Penalties on Tax Duties

-Comment to Report of Prof Dr Lorenzo Del Federico-

Prof Dr Funda BASARAN YAVASLAR

Table of contents

1 The Meaning of Decriminalization

2 The Reasons for A Need of Decriminalization in Tax Law

3 Conclusion

Head of Chair for Fiscal Law Law Faculty of Marmara University

2

1 The Meaning of Decriminalization

11 Decriminalization in terms of its lexical meaning refers to rendering an illegal action as

ldquonon-criminalrdquo in other words to remove an action from the legal category of criminal

offence This can be achieved in two ways1

-either an action is removed completely from the scope of sanction law in a way that it

wouldnrsquot be subjected to any legal norm involving sanction

-or such action is only rendered as non-crime but remains as an illegal act and therefore

continues to be a matter of public sanction

ldquoDecriminalization of Tax Law by Administrative Penalties on Tax Dutiesrdquo which is the

subject of this third session of the meeting refers to this second meaning Accordingly

failure to fulfill tax duty continues to be regarded as an illegal action and sanctions continue

to be applied on the perpetrator The only difference is that such illegal action shall no

longer be considered as a ldquocrimerdquo

12 Therefore first of all it is required to determine what is considered as ldquocrimerdquo in order

to determine the illegality that will be subjected to decriminalization

There are three different approaches raised in the general theory of criminal law as to what

constitutes a crime2 ldquoopinions taking qualitative distinction as basisrdquo ldquoopinions taking

quantitative distinction as basisrdquo and ldquoopinions taking both qualitative and quantitative

distinctions as basisrdquo Opinions taking qualitative distinction as basis focus more on the

objective and subjective criteria Thus in that regard a qualification is made by taking into

consideration the action the perpetrator the moral element but in particular the legal

benefit which has been breached In this context as far as the qualification of crime is

1 K Bayraktar Ceza Hukukunda Succedil Olmaktan Ccedilıkarma Akımı İHFM 1-4 p198-199 (1984) T Demirbaş Ceza

Hukuku Genel Huumlkuumlmler ch3 p193 (Seccedilkin 2013) R Praetorius Entkriminalisierung und alternative Sanktionen Kriminalpolitik ch18 181 (H-J Lange Ed Springer 2008) 2 S Doumlnmezer S Erman Ceza Hukuku Genel Kısım C1 no493 f p344 f (Filiz 1985) F Haft Strafrecht

Allgemeiner Teilch3 p12 f (CH Beck 1984) F S Mahmutoğlu Succedil-Kabahat Ayırımı- İdari Ceza Hukukursquonun Temelleri 32 p33-36 (İ Ulusan F Başaran Yavaşlar eds Seccedilkin 2009) R Maurach Deutsches Strafrecht Allgemeiner Teil ch13 141 f (CF Muumlller 1971) W Mitsch Recht der Ordnungswidrigkeiten ch3 p30 (Springer 1995) P Noll Schweizerisches Strafrecht Allgemeiner Teil I Allgemeine Voraussetzungen der strafbarkeit ch6 p 21 f (Schultess Polygrapisch 1981) I Oumlzgenccedil Tuumlrk Ceza Hukuku Genel Huumlkuumlmler ch12 151 f (Seccedilkin 2008) N Toroslu Ceza Hukuku Genel Huumlkuumlmlerch2 2 and 3 p 91 f (Savaş 2013)

3

concerned it is important to identify ldquowhether the protected legal benefit is of social

valuerdquo ldquowhether the perpetrator is characterized as covetous manipulative or only as an

undisciplined or despicable personrdquo ldquowhether the action involves penetrating into and

encroachment upon a foreign powerrdquo or ldquowhether the requirements regarding the goal

idealized for ensuring the public order have been interruptedrdquo thus whether there is an

action of crime (someone or something seriously exposed to danger)

Opinions taking quantitative distinction as basis on the other hand focus on the sanction to

be imposed by indicating that the damage and danger in case of crimes is greater

Whereas opinions taking both qualitative and quantitative distinction in basis the crime is

qualified by taking into consideration both the significance of the breached legal benefit or

act as well as the extent of the damage incurred

ECHR on the other hand in fact binds itself with the qualification made by the national

legislator in two of the three criteria3 which it uses to determine the existence of crime

3For example FIN ECHR 23 Nov 2006 Jussila versus Finland application no 7305301

(httphudocechrcoeintengappno[7305301]itemid[001-78135] accessed 18 Nov 2015) bdquo30 The Courtrsquos established case-law sets out three criteria to be considered in the assessment of the applicability of the criminal aspect These criteria sometimes referred to as the ldquoEngel criteriardquo were most recently affirmed by the Grand Chamber in Ezeh and Connors v the United Kingdom ([GC] nos 3966598 and 4008698 sect 82 ECHR 2003-X)

ldquo [I]t is first necessary to know whether the provision(s) defining the offence charged belong according to the legal system of the respondent State to criminal law disciplinary law or both concurrently This however provides no more than a starting point The indications so afforded have only a formal and relative value and must be examined in the light of the common denominator of the respective legislation of the various Contracting States The very nature of the offence is a factor of greater import However supervision by the Court does not stop there Such supervision would generally prove to be illusory if it did not also take into consideration the degree of severity of the penalty that the person concerned risks incurring rdquo

31 The second and third criteria are alternative and not necessarily cumulative It is enough that the offence in question is by its nature to be regarded as criminal or that the offence renders the person liable to a penalty which by its nature and degree of severity belongs in the general criminal sphere (see Ezeh and Connors cited above sect 86) The relative lack of seriousness of the penalty cannot divest an offence of its inherently criminal character (see Oumlztuumlrk v Germany 21 February 1984 sect 54 Series A no 73 see also Lutz v Germany 25 August 1987 sect 55 Series A no 123) This does not exclude a cumulative approach where separate analysis of each criterion does not make it possible to reach a clear conclusion as to the existence of a criminal charge (see Ezeh and Connors cited above sect 86 citing inter alia Bendenoun cited above sect 47)rdquo Also please see DE ECHR 21 Feb1984 Oumlztuumlrk versus Germany application no 854479 sect 53 (httphudocechrcoeintsitesengpagessearchaspxi=001-57553 retrieved 7 Dec 2015) F ECHR 24 Feb 1994 Bendenoun versus France applicaiton no 1254786 sect 47 (httphudocechrcoeintsitesengpagessearchaspxi=001-57863 retrieved 7 Dec 2015) S ECHR 23 Juli 2002 Janosevic versus Sweeden application no 3461997 no 65 (httphudocechrcoeintengfulltext[taxaudit]documentcollectionid2[GRANDCHAMBERCHAMBER]itemid[001-60628] retrieved 7 Dec 2015) According to this decision (no68) ldquohellip the lack of

4

because consequently qualification of illegality as a crime in the national law as well as

punishment of such illegality by aggravated means is the decision of the national legislator

Therefore the only authentic answer given by ECHR to the question of what constitutes

ldquocrimerdquo which we set out as our starting point in order to identify the subject of

decriminalization is observed within the criteria of ldquothe nature of the illegal actionrdquo On the

other hand it determines on whether or not the illegality is of criminal quality by its nature

is made by considering how the illegality is interpreted in the majority of the other states

that are party to the Convention and by identifying that the illegality is not directed only to a

certain group designated with special status (eg as in the case of disciplinary law) but on

the contrary directed to ldquoall citizensrdquo due to its nature (eg as in the case of traffic

legislation) Considering that the criteria of being ldquodirected to all citizensrdquo is a relative

concept the only concrete criteria for the determination of the existence of the crime is

whether or not the relevant illegality is qualified as a crime in the majority of the states that

are party to the Convention Thus ECHR takes the value judgment of the majority as basis

13 The conclusion of all these explanations is that by way of decriminalization the

legislator ceases to characterize an illegality which ldquoviolates a great legal benefitrdquo or

ldquoseverely violates a legal benefitrdquo or ldquowhich constitutes a crime according to many statesrdquo

as not an act of crime Therefore the legislator has an extremely conscious preference in

this respect Hence the legislator becomes no longer interested in either the degree of

fault or the significance of the breached legal benefit or action or the extent of the damage

incurred or even any criteria deemed important in determining whether or not a crime

exists The reason of this is that as will be examined in more detail below the purpose of

subjective elements does not necessarily deprive an offence of its criminal character indeed criminal offences based solely on objective elements may be found in the laws of the Contracting States (see Salabiaku v France judgment of 7 October 1988 Series A no 141-A p 15 sect 27) In this connection the Court notes that the present system of tax surcharges has replaced earlier purely criminal procedures It appears that the change from the earlier system which was one of penalties for intentional or negligent conduct to the new system based on objective factors was prompted by the need for greater efficiency (see paragraph 32 above) Furthermore the present tax surcharges are not intended as pecuniary compensation for any costs that may have been incurred as a result of the taxpayers conduct Rather the main purpose of the relevant provisions on surcharges is to exert pressure on taxpayers to comply with their legal obligations and to punish breaches of those obligations The penalties are thus both deterrent and punitive The latter character is the customary distinguishing feature of a criminal penalty (see Oumlztuumlrk cited above pp 20-21 sect 53) In the Courts opinion the general character of the legal provisions on tax surcharges and the purpose of the penalties which are both deterrent and punitive suffice to show that for the purposes of Article 6 of the Convention the applicant was charged with a criminal offencerdquo (Bold emphasis belong to the Author)

5

decriminalization is different from the object of punishment prescribed by the criminal law

and consequently decriminalization needs a paradigm change Value judgments and rules of

criminal law or criminal law doctrine can no longer influence how the action shall be

evaluated

14 When we focus solely on tax law it is initially required to make the following

determination legislators of many countries4 have accepted ldquotax evasionrdquo or ldquothe conducts

precluding the Administration from detecting taxrdquo as a crime Therefore in the event that

the legislator applies a 100 decriminalization and does not include crime in the tax law in

any way this would mean that no circumstances including ldquotax evasionrdquo shall be considered

as a criminal illegality

2 The Reasons for a Need of Decriminalization in Tax Law

21 It is necessary to ask why a legislator ceases to render an illegality as a crime which it

normally renders as a crime What could be the legitimate reason of decriminalizing an

illegality In my opinion in terms of tax law these questions can be answered as follows

The principal reason for the existence of tax system is to levy tax on the assets of the

taxpayer and transfer to the treasury In other words the entire tax system is established on

the objective of ldquogenerating tax revenue in full and on timerdquo Generating no or lower amount

of tax or generating of tax in an untimely manner either results in a default in public service

or incomplete performance thereof in terms of quantity or quality or causes the

performance of the public service by incurring a higher amount of expenses (through means

such as indebtedness privatization) even if the public service will be performed completely

and with the targeted quality

Such a system of course can be tried to be protected by implementing severe sanctions

like imprisonment just like it is the case in the criminal law However here it is required to

make a choice regarding to the tool to be used to achieve the goal Which one serves best to

the goal of ldquogenerating tax revenuerdquo ldquoimprisoning the taxpayer and so restricting his

4 R Seer A L Wilms General Report bdquoSurcharges and Penalties in Tax Lawldquowithin this book Sec 13 G

Dannecker O Jansen Generalbericht in Steuerstrafrecht in Europa und den Vereinigten Staaten 2 bb and cc p30 -31 (G Dannecker O Jansen eds Linde 2007)

6

freedom and impeding him from continuing to execute his activities subjected to taxrdquo or

ldquoimposing severe fines or deprivation of rights obstructing his economic activities and in this

way killing or paralyzing him economicallyrdquo Or does it serve better to the goal of

ldquogenerating tax revenuerdquo to compensate the damage due to his illegal actions as well as to

retrieve all the benefits gained or which may be gained by the tax-payer through such

illegality

If we are to focus on the main goal of the tax legislation the second way thus

decriminalization should be preferred5

22 As can be seen the purpose of decriminalization is different The main goal with

decriminalization is to remedy the damage inflicted on the goal of the tax system due to the

illegal act thus the compensation of the damage6 The occurred damage consists from the

missing tax amount inflation difference due to the late collection and the additional public

cost arising in order for the provision of public service

5 See K Tipke Die Steuerrechtsordnung BdIII ch36 54 p1756 f (Otto Schmidt 2012) ldquoIm Allgemeinen

besteht auch kein Beduumlrfnis dafuumlr Steuerhinterzieher ldquohinter Gitterrdquo zu bringen Sie gefaehrden nicht die oumlffentliche Sicherheit Die Freiheitsstrafe sollte gemeingefaehrlichen Gewalttaetern vorbehalten bleiben Steuerhinterzieher werden durch Freiheitsstrafen nur daran gehindert ihrem Erwerb nachzugehen und dadurch Steuerschulden auszuloumlsen Wenn dem Staat Geld vorenthalten wird so passt dazu die Geldstrafe oder eine andere Geldsanktionrdquo Also please see M Streck Harzburger Protokoll 1999 p83 ( ldquoWarum stecken wir Lesitungstraeger dieser Gesellschaft in ein Gefaengnis wo sie nur Kosten verursachen warum sagen wir nicht sie koumlnnten das Gefaegnis dadurch vermeiden dass sie den dreifachen Betrag der hintergezogenen Steuer zahlen Waere das nicht eher im Sinn des sect 370 AO der das Steueraufkommen sichern sollrdquo) and J Weigell Uumlberlegungen zum Steuer(straf)recht in Festschrift fuumlr M Streck p 609 (Ed B Binnewies R Spatscheck Otto Schmidt 2011) (K Tipke p 1756 footnotes 149 and 150) For a different approach please see R Seer (Steuerrecht Materielles Steuerstraf- und ordnungswidrigkeitenrecht ch23 p1368-1369 [K Tipke et al eds Otto Schmidt 2015]) who is defending the idea of depenalisation due to the unsuitability of taxpenalty law for compensation of structural enforsement deficits in taxation procedure ldquoDie wesentliche Rechtfertigung der Strafe ist die Herstellung eines Schuldausgleiches unter gleichzeitiger Beruumlcksichtigung spezial- und generalpraeventiver Gesichtspunkte Das Steuerstrafverfahren ist dementsprechend ein Individualverfahren das nach Schuld und Verantwortung fragt Das Steuerrecht ist deshalb ungeeignet strukturelle Vollzugsdefizite (s sect 3 Rz113 ff) auszugleichen und die gebotene Belastungsgleichheit herzustellen Aufgrud seines intensiven Eingriffscharakters bleibt das Mittel der Strafe die ultima ratio im Instrumentarium des Gesetzgebers (BVerfGE 39 1 [47]) Steuerliches Fehlverhalten im Massenverfahren ist deshalb primaer nicht durch das dafuumlr untaugliche Steuerstrafrecht sondern durch eine effiziente Ausgestaltung des hierfuumlr bestimmten Besteuerungsverfahren herzustellen hellip Statt die Strafbarkeitszone ndash ohne Ruumlcksicht auf Vollzugsfaehigkeit ndash normativ auszudehnen liesse sich die gewuumlnschte Praevention besser durch ein den Bereich der einfachen Steuerhinterziehung abdeckendes verschuldenabhaengigges Steuerzuschlagsystem erreichen (sog Entpoumlnalisierung des Steuerrechts)rdquo 6 A proposal for a surtaxsystem which bases on implementing the current market interest rate on the

determined tax after contolling of tax affair independent of fault see R Seer Steuerordnungswidrigkeiten im deutschen Recht in İdari Ceza Hukuku Sempozyumu 4 p242 (İ Ulusan F Başaran Yavaşlar eds Seckin 2009) and Konsensuale Paketloumlsungen im Steuerstrafrecht in Festschrift fuumlr G Kohlmann V p552 (Otto Schmidt 2003)

7

In my opinion as an additional deterrent measure the benefits gained by the perpetrator

through the illegal act should also be removed from that person Here the market interest

rate can be taken into account as an objective criteria and thus a reasonable surcharge may

be imposed Ultimately ldquono one could benefit from hisher illegal conductrdquo It can be also

considered to hinder the perpetrator from benefitting from certain advantageous tax

regulations such as by way of ldquoprohibition on applying for reconciliationldquo

I would like to point out here that differently from the criminal law in decriminalization

compensation and deterring are the primary focus like in the case of civil law rather than

punishing and deterring like in the case of criminal law

23 A last question Is the achievement of the eventual goal of ldquofinancing the public

expenditurerdquo with the least amount of damages constitutes the sole benefit of

decriminalization

If the legislator takes a hundred percent decriminalization decision in a way not to allow any

crime in the tax system also the following results will be achieved

Legislation duties shall be facilitated because in this way legislation shall be relieved from

-on one side difficulty of characterizing what is crime what is misdemeanor or contradictory

to another type of legislation

-accordingly on the other side difficulty of determining penalties in compliance with

equality and proportionality principals

Duties of criminal jurisdiction shall be facilitated because the tax crimes burden shall be

removed from the prosecutors and criminal judges who should carry out any research

themselves according to ex officio principle allowing them to focus on the subjects remaining

within the natural frame of criminal law and to achieve faster results

The criminal legislation which should be applied as the ultimate remedy for protecting the

public order for restricting peoplersquos freedom shall be more deterrent

Instead of long and complicated criminal prosecutions and investigations commissioning the

administration with the assignment and authorization to determine the illegal conduct shall

8

enable a fastest indemnification of the loss arising from the illegal action in an easy

procedure

Finally the problems due to double jeopardy under the same legislation (ne bis in idem) shall

be eliminated

3 Conclusion

Although it might seem unfair at first sight the decriminalization provides reasonable

solutions for the heavy problems of current tax surcharge system besides being a better tool

to achieve the ultimate goal of tax law

The only factor which endangers this whole positive picture could be that whether the tax

payers would be more daring to perform illegalities which may lead to tax evasion in a

decriminalized system However it is possible to overcome this danger by means of a well-

audited functional and gapless tax control system Because eventually even the existence

of severe penalties donrsquot constrain the taxpayers from intending to ldquocommit tax offencesrdquo in

a weak inefficient control system containing legal gaps

The purpose of decriminalization is different from the object of punishment

prescribed by the criminal law and consequently decriminalization needs a

paradigm change Value judgments and rules of criminal law or criminal law

doctrine can no longer influence how the action shall be evaluated

The main objective of the tax system is provision of the entry of the tax from property of taxpayer into

the state treasury in full and on time

If this objective is not reached ie the tax

-has not been collected at all or

- collected on time but partial or

-late but in full or

-late and partial

public loss emerges

Less tax income =

public loss =

Violation of the public order

Default of public service or incomplete

performance thereof in quantities or qualities

Performance of public service at higher cost

- indebtedness

- privatization

- hellip

Depriving the taxpayer acting in

contradiction with the law of hisher

freedom (imprisonment) does not

compensate the damage On the

contrary since the person in jail cannot

perform hisher joboccupation heshe

will neither generate revenue nor pay

tax

THE SANCTION TO BE APPLIED TO THE

ILLEGAL ACT IN DECRIMINALIZATION

THE OCCURRED DAMAGE

MEANS IN DETERRENT

NATURE

SANCTION

THE MISSING TAX AMOUNT

INFLATION DIFFERENCE DUE

TO LATE COLLECTION

THE ADDITIONAL PUBLIC COST ARISING IN

ORDER FOR THE PROVISION OF

PUBLIC SERVICE

THE OCCURRED

DAMAGE

MEA

NS IN

DETE

RR

EN

T N

ATU

RE THE SURCHARGE (ADDITIONAL PAYMENT) AT

LEAST DOUBLE THE AMOUNT OF THE BENEFIT PROVIDED BY THE TAXPAYER DUE TO PARTIAL

ANDOR LATE PAYMENT BUT THE MARKET PRICE HERE CAN BE TAKEN INTO ACCOUNT

AS AN OBJECTIVE CRITERIA

DEPRIVING OF A RIGHT WITH RESPECT TO TAXATION (FOR INSTANCE PROHIBITION OF

BENEFITING FROM TAX INCENTIVE PROHIBITION FOR APPLYING FOR

RECONCILATION)

THANK YOU FOR THE ATTENTION PROF DR FUNDA BAŞARAN YAVAŞLAR

1

Decriminalization of Tax Law by Administrative Penalties on Tax Duties

-Comment to Report of Prof Dr Lorenzo Del Federico-

Prof Dr Funda BASARAN YAVASLAR

Table of contents

1 The Meaning of Decriminalization

2 The Reasons for A Need of Decriminalization in Tax Law

3 Conclusion

Head of Chair for Fiscal Law Law Faculty of Marmara University

2

1 The Meaning of Decriminalization

11 Decriminalization in terms of its lexical meaning refers to rendering an illegal action as

ldquonon-criminalrdquo in other words to remove an action from the legal category of criminal

offence This can be achieved in two ways1

-either an action is removed completely from the scope of sanction law in a way that it

wouldnrsquot be subjected to any legal norm involving sanction

-or such action is only rendered as non-crime but remains as an illegal act and therefore

continues to be a matter of public sanction

ldquoDecriminalization of Tax Law by Administrative Penalties on Tax Dutiesrdquo which is the

subject of this third session of the meeting refers to this second meaning Accordingly

failure to fulfill tax duty continues to be regarded as an illegal action and sanctions continue

to be applied on the perpetrator The only difference is that such illegal action shall no

longer be considered as a ldquocrimerdquo

12 Therefore first of all it is required to determine what is considered as ldquocrimerdquo in order

to determine the illegality that will be subjected to decriminalization

There are three different approaches raised in the general theory of criminal law as to what

constitutes a crime2 ldquoopinions taking qualitative distinction as basisrdquo ldquoopinions taking

quantitative distinction as basisrdquo and ldquoopinions taking both qualitative and quantitative

distinctions as basisrdquo Opinions taking qualitative distinction as basis focus more on the

objective and subjective criteria Thus in that regard a qualification is made by taking into

consideration the action the perpetrator the moral element but in particular the legal

benefit which has been breached In this context as far as the qualification of crime is

1 K Bayraktar Ceza Hukukunda Succedil Olmaktan Ccedilıkarma Akımı İHFM 1-4 p198-199 (1984) T Demirbaş Ceza

Hukuku Genel Huumlkuumlmler ch3 p193 (Seccedilkin 2013) R Praetorius Entkriminalisierung und alternative Sanktionen Kriminalpolitik ch18 181 (H-J Lange Ed Springer 2008) 2 S Doumlnmezer S Erman Ceza Hukuku Genel Kısım C1 no493 f p344 f (Filiz 1985) F Haft Strafrecht

Allgemeiner Teilch3 p12 f (CH Beck 1984) F S Mahmutoğlu Succedil-Kabahat Ayırımı- İdari Ceza Hukukursquonun Temelleri 32 p33-36 (İ Ulusan F Başaran Yavaşlar eds Seccedilkin 2009) R Maurach Deutsches Strafrecht Allgemeiner Teil ch13 141 f (CF Muumlller 1971) W Mitsch Recht der Ordnungswidrigkeiten ch3 p30 (Springer 1995) P Noll Schweizerisches Strafrecht Allgemeiner Teil I Allgemeine Voraussetzungen der strafbarkeit ch6 p 21 f (Schultess Polygrapisch 1981) I Oumlzgenccedil Tuumlrk Ceza Hukuku Genel Huumlkuumlmler ch12 151 f (Seccedilkin 2008) N Toroslu Ceza Hukuku Genel Huumlkuumlmlerch2 2 and 3 p 91 f (Savaş 2013)

3

concerned it is important to identify ldquowhether the protected legal benefit is of social

valuerdquo ldquowhether the perpetrator is characterized as covetous manipulative or only as an

undisciplined or despicable personrdquo ldquowhether the action involves penetrating into and

encroachment upon a foreign powerrdquo or ldquowhether the requirements regarding the goal

idealized for ensuring the public order have been interruptedrdquo thus whether there is an

action of crime (someone or something seriously exposed to danger)

Opinions taking quantitative distinction as basis on the other hand focus on the sanction to

be imposed by indicating that the damage and danger in case of crimes is greater

Whereas opinions taking both qualitative and quantitative distinction in basis the crime is

qualified by taking into consideration both the significance of the breached legal benefit or

act as well as the extent of the damage incurred

ECHR on the other hand in fact binds itself with the qualification made by the national

legislator in two of the three criteria3 which it uses to determine the existence of crime

3For example FIN ECHR 23 Nov 2006 Jussila versus Finland application no 7305301

(httphudocechrcoeintengappno[7305301]itemid[001-78135] accessed 18 Nov 2015) bdquo30 The Courtrsquos established case-law sets out three criteria to be considered in the assessment of the applicability of the criminal aspect These criteria sometimes referred to as the ldquoEngel criteriardquo were most recently affirmed by the Grand Chamber in Ezeh and Connors v the United Kingdom ([GC] nos 3966598 and 4008698 sect 82 ECHR 2003-X)

ldquo [I]t is first necessary to know whether the provision(s) defining the offence charged belong according to the legal system of the respondent State to criminal law disciplinary law or both concurrently This however provides no more than a starting point The indications so afforded have only a formal and relative value and must be examined in the light of the common denominator of the respective legislation of the various Contracting States The very nature of the offence is a factor of greater import However supervision by the Court does not stop there Such supervision would generally prove to be illusory if it did not also take into consideration the degree of severity of the penalty that the person concerned risks incurring rdquo

31 The second and third criteria are alternative and not necessarily cumulative It is enough that the offence in question is by its nature to be regarded as criminal or that the offence renders the person liable to a penalty which by its nature and degree of severity belongs in the general criminal sphere (see Ezeh and Connors cited above sect 86) The relative lack of seriousness of the penalty cannot divest an offence of its inherently criminal character (see Oumlztuumlrk v Germany 21 February 1984 sect 54 Series A no 73 see also Lutz v Germany 25 August 1987 sect 55 Series A no 123) This does not exclude a cumulative approach where separate analysis of each criterion does not make it possible to reach a clear conclusion as to the existence of a criminal charge (see Ezeh and Connors cited above sect 86 citing inter alia Bendenoun cited above sect 47)rdquo Also please see DE ECHR 21 Feb1984 Oumlztuumlrk versus Germany application no 854479 sect 53 (httphudocechrcoeintsitesengpagessearchaspxi=001-57553 retrieved 7 Dec 2015) F ECHR 24 Feb 1994 Bendenoun versus France applicaiton no 1254786 sect 47 (httphudocechrcoeintsitesengpagessearchaspxi=001-57863 retrieved 7 Dec 2015) S ECHR 23 Juli 2002 Janosevic versus Sweeden application no 3461997 no 65 (httphudocechrcoeintengfulltext[taxaudit]documentcollectionid2[GRANDCHAMBERCHAMBER]itemid[001-60628] retrieved 7 Dec 2015) According to this decision (no68) ldquohellip the lack of

4

because consequently qualification of illegality as a crime in the national law as well as

punishment of such illegality by aggravated means is the decision of the national legislator

Therefore the only authentic answer given by ECHR to the question of what constitutes

ldquocrimerdquo which we set out as our starting point in order to identify the subject of

decriminalization is observed within the criteria of ldquothe nature of the illegal actionrdquo On the

other hand it determines on whether or not the illegality is of criminal quality by its nature

is made by considering how the illegality is interpreted in the majority of the other states

that are party to the Convention and by identifying that the illegality is not directed only to a

certain group designated with special status (eg as in the case of disciplinary law) but on

the contrary directed to ldquoall citizensrdquo due to its nature (eg as in the case of traffic

legislation) Considering that the criteria of being ldquodirected to all citizensrdquo is a relative

concept the only concrete criteria for the determination of the existence of the crime is

whether or not the relevant illegality is qualified as a crime in the majority of the states that

are party to the Convention Thus ECHR takes the value judgment of the majority as basis

13 The conclusion of all these explanations is that by way of decriminalization the

legislator ceases to characterize an illegality which ldquoviolates a great legal benefitrdquo or

ldquoseverely violates a legal benefitrdquo or ldquowhich constitutes a crime according to many statesrdquo

as not an act of crime Therefore the legislator has an extremely conscious preference in

this respect Hence the legislator becomes no longer interested in either the degree of

fault or the significance of the breached legal benefit or action or the extent of the damage

incurred or even any criteria deemed important in determining whether or not a crime

exists The reason of this is that as will be examined in more detail below the purpose of

subjective elements does not necessarily deprive an offence of its criminal character indeed criminal offences based solely on objective elements may be found in the laws of the Contracting States (see Salabiaku v France judgment of 7 October 1988 Series A no 141-A p 15 sect 27) In this connection the Court notes that the present system of tax surcharges has replaced earlier purely criminal procedures It appears that the change from the earlier system which was one of penalties for intentional or negligent conduct to the new system based on objective factors was prompted by the need for greater efficiency (see paragraph 32 above) Furthermore the present tax surcharges are not intended as pecuniary compensation for any costs that may have been incurred as a result of the taxpayers conduct Rather the main purpose of the relevant provisions on surcharges is to exert pressure on taxpayers to comply with their legal obligations and to punish breaches of those obligations The penalties are thus both deterrent and punitive The latter character is the customary distinguishing feature of a criminal penalty (see Oumlztuumlrk cited above pp 20-21 sect 53) In the Courts opinion the general character of the legal provisions on tax surcharges and the purpose of the penalties which are both deterrent and punitive suffice to show that for the purposes of Article 6 of the Convention the applicant was charged with a criminal offencerdquo (Bold emphasis belong to the Author)

5

decriminalization is different from the object of punishment prescribed by the criminal law

and consequently decriminalization needs a paradigm change Value judgments and rules of

criminal law or criminal law doctrine can no longer influence how the action shall be

evaluated

14 When we focus solely on tax law it is initially required to make the following

determination legislators of many countries4 have accepted ldquotax evasionrdquo or ldquothe conducts

precluding the Administration from detecting taxrdquo as a crime Therefore in the event that

the legislator applies a 100 decriminalization and does not include crime in the tax law in

any way this would mean that no circumstances including ldquotax evasionrdquo shall be considered

as a criminal illegality

2 The Reasons for a Need of Decriminalization in Tax Law

21 It is necessary to ask why a legislator ceases to render an illegality as a crime which it

normally renders as a crime What could be the legitimate reason of decriminalizing an

illegality In my opinion in terms of tax law these questions can be answered as follows

The principal reason for the existence of tax system is to levy tax on the assets of the

taxpayer and transfer to the treasury In other words the entire tax system is established on

the objective of ldquogenerating tax revenue in full and on timerdquo Generating no or lower amount

of tax or generating of tax in an untimely manner either results in a default in public service

or incomplete performance thereof in terms of quantity or quality or causes the

performance of the public service by incurring a higher amount of expenses (through means

such as indebtedness privatization) even if the public service will be performed completely

and with the targeted quality

Such a system of course can be tried to be protected by implementing severe sanctions

like imprisonment just like it is the case in the criminal law However here it is required to

make a choice regarding to the tool to be used to achieve the goal Which one serves best to

the goal of ldquogenerating tax revenuerdquo ldquoimprisoning the taxpayer and so restricting his

4 R Seer A L Wilms General Report bdquoSurcharges and Penalties in Tax Lawldquowithin this book Sec 13 G

Dannecker O Jansen Generalbericht in Steuerstrafrecht in Europa und den Vereinigten Staaten 2 bb and cc p30 -31 (G Dannecker O Jansen eds Linde 2007)

6

freedom and impeding him from continuing to execute his activities subjected to taxrdquo or

ldquoimposing severe fines or deprivation of rights obstructing his economic activities and in this

way killing or paralyzing him economicallyrdquo Or does it serve better to the goal of

ldquogenerating tax revenuerdquo to compensate the damage due to his illegal actions as well as to

retrieve all the benefits gained or which may be gained by the tax-payer through such

illegality

If we are to focus on the main goal of the tax legislation the second way thus

decriminalization should be preferred5

22 As can be seen the purpose of decriminalization is different The main goal with

decriminalization is to remedy the damage inflicted on the goal of the tax system due to the

illegal act thus the compensation of the damage6 The occurred damage consists from the

missing tax amount inflation difference due to the late collection and the additional public

cost arising in order for the provision of public service

5 See K Tipke Die Steuerrechtsordnung BdIII ch36 54 p1756 f (Otto Schmidt 2012) ldquoIm Allgemeinen

besteht auch kein Beduumlrfnis dafuumlr Steuerhinterzieher ldquohinter Gitterrdquo zu bringen Sie gefaehrden nicht die oumlffentliche Sicherheit Die Freiheitsstrafe sollte gemeingefaehrlichen Gewalttaetern vorbehalten bleiben Steuerhinterzieher werden durch Freiheitsstrafen nur daran gehindert ihrem Erwerb nachzugehen und dadurch Steuerschulden auszuloumlsen Wenn dem Staat Geld vorenthalten wird so passt dazu die Geldstrafe oder eine andere Geldsanktionrdquo Also please see M Streck Harzburger Protokoll 1999 p83 ( ldquoWarum stecken wir Lesitungstraeger dieser Gesellschaft in ein Gefaengnis wo sie nur Kosten verursachen warum sagen wir nicht sie koumlnnten das Gefaegnis dadurch vermeiden dass sie den dreifachen Betrag der hintergezogenen Steuer zahlen Waere das nicht eher im Sinn des sect 370 AO der das Steueraufkommen sichern sollrdquo) and J Weigell Uumlberlegungen zum Steuer(straf)recht in Festschrift fuumlr M Streck p 609 (Ed B Binnewies R Spatscheck Otto Schmidt 2011) (K Tipke p 1756 footnotes 149 and 150) For a different approach please see R Seer (Steuerrecht Materielles Steuerstraf- und ordnungswidrigkeitenrecht ch23 p1368-1369 [K Tipke et al eds Otto Schmidt 2015]) who is defending the idea of depenalisation due to the unsuitability of taxpenalty law for compensation of structural enforsement deficits in taxation procedure ldquoDie wesentliche Rechtfertigung der Strafe ist die Herstellung eines Schuldausgleiches unter gleichzeitiger Beruumlcksichtigung spezial- und generalpraeventiver Gesichtspunkte Das Steuerstrafverfahren ist dementsprechend ein Individualverfahren das nach Schuld und Verantwortung fragt Das Steuerrecht ist deshalb ungeeignet strukturelle Vollzugsdefizite (s sect 3 Rz113 ff) auszugleichen und die gebotene Belastungsgleichheit herzustellen Aufgrud seines intensiven Eingriffscharakters bleibt das Mittel der Strafe die ultima ratio im Instrumentarium des Gesetzgebers (BVerfGE 39 1 [47]) Steuerliches Fehlverhalten im Massenverfahren ist deshalb primaer nicht durch das dafuumlr untaugliche Steuerstrafrecht sondern durch eine effiziente Ausgestaltung des hierfuumlr bestimmten Besteuerungsverfahren herzustellen hellip Statt die Strafbarkeitszone ndash ohne Ruumlcksicht auf Vollzugsfaehigkeit ndash normativ auszudehnen liesse sich die gewuumlnschte Praevention besser durch ein den Bereich der einfachen Steuerhinterziehung abdeckendes verschuldenabhaengigges Steuerzuschlagsystem erreichen (sog Entpoumlnalisierung des Steuerrechts)rdquo 6 A proposal for a surtaxsystem which bases on implementing the current market interest rate on the

determined tax after contolling of tax affair independent of fault see R Seer Steuerordnungswidrigkeiten im deutschen Recht in İdari Ceza Hukuku Sempozyumu 4 p242 (İ Ulusan F Başaran Yavaşlar eds Seckin 2009) and Konsensuale Paketloumlsungen im Steuerstrafrecht in Festschrift fuumlr G Kohlmann V p552 (Otto Schmidt 2003)

7

In my opinion as an additional deterrent measure the benefits gained by the perpetrator

through the illegal act should also be removed from that person Here the market interest

rate can be taken into account as an objective criteria and thus a reasonable surcharge may

be imposed Ultimately ldquono one could benefit from hisher illegal conductrdquo It can be also

considered to hinder the perpetrator from benefitting from certain advantageous tax

regulations such as by way of ldquoprohibition on applying for reconciliationldquo

I would like to point out here that differently from the criminal law in decriminalization

compensation and deterring are the primary focus like in the case of civil law rather than

punishing and deterring like in the case of criminal law

23 A last question Is the achievement of the eventual goal of ldquofinancing the public

expenditurerdquo with the least amount of damages constitutes the sole benefit of

decriminalization

If the legislator takes a hundred percent decriminalization decision in a way not to allow any

crime in the tax system also the following results will be achieved

Legislation duties shall be facilitated because in this way legislation shall be relieved from

-on one side difficulty of characterizing what is crime what is misdemeanor or contradictory

to another type of legislation

-accordingly on the other side difficulty of determining penalties in compliance with

equality and proportionality principals

Duties of criminal jurisdiction shall be facilitated because the tax crimes burden shall be

removed from the prosecutors and criminal judges who should carry out any research

themselves according to ex officio principle allowing them to focus on the subjects remaining

within the natural frame of criminal law and to achieve faster results

The criminal legislation which should be applied as the ultimate remedy for protecting the

public order for restricting peoplersquos freedom shall be more deterrent

Instead of long and complicated criminal prosecutions and investigations commissioning the

administration with the assignment and authorization to determine the illegal conduct shall

8

enable a fastest indemnification of the loss arising from the illegal action in an easy

procedure

Finally the problems due to double jeopardy under the same legislation (ne bis in idem) shall

be eliminated

3 Conclusion

Although it might seem unfair at first sight the decriminalization provides reasonable

solutions for the heavy problems of current tax surcharge system besides being a better tool

to achieve the ultimate goal of tax law

The only factor which endangers this whole positive picture could be that whether the tax

payers would be more daring to perform illegalities which may lead to tax evasion in a

decriminalized system However it is possible to overcome this danger by means of a well-

audited functional and gapless tax control system Because eventually even the existence

of severe penalties donrsquot constrain the taxpayers from intending to ldquocommit tax offencesrdquo in

a weak inefficient control system containing legal gaps

The main objective of the tax system is provision of the entry of the tax from property of taxpayer into

the state treasury in full and on time

If this objective is not reached ie the tax

-has not been collected at all or

- collected on time but partial or

-late but in full or

-late and partial

public loss emerges

Less tax income =

public loss =

Violation of the public order

Default of public service or incomplete

performance thereof in quantities or qualities

Performance of public service at higher cost

- indebtedness

- privatization

- hellip

Depriving the taxpayer acting in

contradiction with the law of hisher

freedom (imprisonment) does not

compensate the damage On the

contrary since the person in jail cannot

perform hisher joboccupation heshe

will neither generate revenue nor pay

tax

THE SANCTION TO BE APPLIED TO THE

ILLEGAL ACT IN DECRIMINALIZATION

THE OCCURRED DAMAGE

MEANS IN DETERRENT

NATURE

SANCTION

THE MISSING TAX AMOUNT

INFLATION DIFFERENCE DUE

TO LATE COLLECTION

THE ADDITIONAL PUBLIC COST ARISING IN

ORDER FOR THE PROVISION OF

PUBLIC SERVICE

THE OCCURRED

DAMAGE

MEA

NS IN

DETE

RR

EN

T N

ATU

RE THE SURCHARGE (ADDITIONAL PAYMENT) AT

LEAST DOUBLE THE AMOUNT OF THE BENEFIT PROVIDED BY THE TAXPAYER DUE TO PARTIAL

ANDOR LATE PAYMENT BUT THE MARKET PRICE HERE CAN BE TAKEN INTO ACCOUNT

AS AN OBJECTIVE CRITERIA

DEPRIVING OF A RIGHT WITH RESPECT TO TAXATION (FOR INSTANCE PROHIBITION OF

BENEFITING FROM TAX INCENTIVE PROHIBITION FOR APPLYING FOR

RECONCILATION)

THANK YOU FOR THE ATTENTION PROF DR FUNDA BAŞARAN YAVAŞLAR

1

Decriminalization of Tax Law by Administrative Penalties on Tax Duties

-Comment to Report of Prof Dr Lorenzo Del Federico-

Prof Dr Funda BASARAN YAVASLAR

Table of contents

1 The Meaning of Decriminalization

2 The Reasons for A Need of Decriminalization in Tax Law

3 Conclusion

Head of Chair for Fiscal Law Law Faculty of Marmara University

2

1 The Meaning of Decriminalization

11 Decriminalization in terms of its lexical meaning refers to rendering an illegal action as

ldquonon-criminalrdquo in other words to remove an action from the legal category of criminal

offence This can be achieved in two ways1

-either an action is removed completely from the scope of sanction law in a way that it

wouldnrsquot be subjected to any legal norm involving sanction

-or such action is only rendered as non-crime but remains as an illegal act and therefore

continues to be a matter of public sanction

ldquoDecriminalization of Tax Law by Administrative Penalties on Tax Dutiesrdquo which is the

subject of this third session of the meeting refers to this second meaning Accordingly

failure to fulfill tax duty continues to be regarded as an illegal action and sanctions continue

to be applied on the perpetrator The only difference is that such illegal action shall no

longer be considered as a ldquocrimerdquo

12 Therefore first of all it is required to determine what is considered as ldquocrimerdquo in order

to determine the illegality that will be subjected to decriminalization

There are three different approaches raised in the general theory of criminal law as to what

constitutes a crime2 ldquoopinions taking qualitative distinction as basisrdquo ldquoopinions taking

quantitative distinction as basisrdquo and ldquoopinions taking both qualitative and quantitative

distinctions as basisrdquo Opinions taking qualitative distinction as basis focus more on the

objective and subjective criteria Thus in that regard a qualification is made by taking into

consideration the action the perpetrator the moral element but in particular the legal

benefit which has been breached In this context as far as the qualification of crime is

1 K Bayraktar Ceza Hukukunda Succedil Olmaktan Ccedilıkarma Akımı İHFM 1-4 p198-199 (1984) T Demirbaş Ceza

Hukuku Genel Huumlkuumlmler ch3 p193 (Seccedilkin 2013) R Praetorius Entkriminalisierung und alternative Sanktionen Kriminalpolitik ch18 181 (H-J Lange Ed Springer 2008) 2 S Doumlnmezer S Erman Ceza Hukuku Genel Kısım C1 no493 f p344 f (Filiz 1985) F Haft Strafrecht

Allgemeiner Teilch3 p12 f (CH Beck 1984) F S Mahmutoğlu Succedil-Kabahat Ayırımı- İdari Ceza Hukukursquonun Temelleri 32 p33-36 (İ Ulusan F Başaran Yavaşlar eds Seccedilkin 2009) R Maurach Deutsches Strafrecht Allgemeiner Teil ch13 141 f (CF Muumlller 1971) W Mitsch Recht der Ordnungswidrigkeiten ch3 p30 (Springer 1995) P Noll Schweizerisches Strafrecht Allgemeiner Teil I Allgemeine Voraussetzungen der strafbarkeit ch6 p 21 f (Schultess Polygrapisch 1981) I Oumlzgenccedil Tuumlrk Ceza Hukuku Genel Huumlkuumlmler ch12 151 f (Seccedilkin 2008) N Toroslu Ceza Hukuku Genel Huumlkuumlmlerch2 2 and 3 p 91 f (Savaş 2013)

3

concerned it is important to identify ldquowhether the protected legal benefit is of social

valuerdquo ldquowhether the perpetrator is characterized as covetous manipulative or only as an

undisciplined or despicable personrdquo ldquowhether the action involves penetrating into and

encroachment upon a foreign powerrdquo or ldquowhether the requirements regarding the goal

idealized for ensuring the public order have been interruptedrdquo thus whether there is an

action of crime (someone or something seriously exposed to danger)

Opinions taking quantitative distinction as basis on the other hand focus on the sanction to

be imposed by indicating that the damage and danger in case of crimes is greater

Whereas opinions taking both qualitative and quantitative distinction in basis the crime is

qualified by taking into consideration both the significance of the breached legal benefit or

act as well as the extent of the damage incurred

ECHR on the other hand in fact binds itself with the qualification made by the national

legislator in two of the three criteria3 which it uses to determine the existence of crime

3For example FIN ECHR 23 Nov 2006 Jussila versus Finland application no 7305301

(httphudocechrcoeintengappno[7305301]itemid[001-78135] accessed 18 Nov 2015) bdquo30 The Courtrsquos established case-law sets out three criteria to be considered in the assessment of the applicability of the criminal aspect These criteria sometimes referred to as the ldquoEngel criteriardquo were most recently affirmed by the Grand Chamber in Ezeh and Connors v the United Kingdom ([GC] nos 3966598 and 4008698 sect 82 ECHR 2003-X)

ldquo [I]t is first necessary to know whether the provision(s) defining the offence charged belong according to the legal system of the respondent State to criminal law disciplinary law or both concurrently This however provides no more than a starting point The indications so afforded have only a formal and relative value and must be examined in the light of the common denominator of the respective legislation of the various Contracting States The very nature of the offence is a factor of greater import However supervision by the Court does not stop there Such supervision would generally prove to be illusory if it did not also take into consideration the degree of severity of the penalty that the person concerned risks incurring rdquo

31 The second and third criteria are alternative and not necessarily cumulative It is enough that the offence in question is by its nature to be regarded as criminal or that the offence renders the person liable to a penalty which by its nature and degree of severity belongs in the general criminal sphere (see Ezeh and Connors cited above sect 86) The relative lack of seriousness of the penalty cannot divest an offence of its inherently criminal character (see Oumlztuumlrk v Germany 21 February 1984 sect 54 Series A no 73 see also Lutz v Germany 25 August 1987 sect 55 Series A no 123) This does not exclude a cumulative approach where separate analysis of each criterion does not make it possible to reach a clear conclusion as to the existence of a criminal charge (see Ezeh and Connors cited above sect 86 citing inter alia Bendenoun cited above sect 47)rdquo Also please see DE ECHR 21 Feb1984 Oumlztuumlrk versus Germany application no 854479 sect 53 (httphudocechrcoeintsitesengpagessearchaspxi=001-57553 retrieved 7 Dec 2015) F ECHR 24 Feb 1994 Bendenoun versus France applicaiton no 1254786 sect 47 (httphudocechrcoeintsitesengpagessearchaspxi=001-57863 retrieved 7 Dec 2015) S ECHR 23 Juli 2002 Janosevic versus Sweeden application no 3461997 no 65 (httphudocechrcoeintengfulltext[taxaudit]documentcollectionid2[GRANDCHAMBERCHAMBER]itemid[001-60628] retrieved 7 Dec 2015) According to this decision (no68) ldquohellip the lack of

4

because consequently qualification of illegality as a crime in the national law as well as

punishment of such illegality by aggravated means is the decision of the national legislator