Decomposition of systemic risk drivers in evolving ... · Decomposition of Systemic Risk Drivers in...

27

Decomposition of systemic risk drivers in evolving financial networks Sergio Rubens S. Souza Banco Central do Brasil – Research Department

Transcript of Decomposition of systemic risk drivers in evolving ... · Decomposition of Systemic Risk Drivers in...

Decomposition of systemic risk drivers

in evolving financial networks

Sergio Rubens S. SouzaBanco Central do Brasil – Research Department

The views expressed in this presentation

are those of the authors and do not

necessarily reflect those of the Banco

Central do Brasil.

3Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Introduction

This study has applications in financial networks monitoring. In

this activity, it is essential that systemic risk is correctly

measured and understood.

Motivation: to provide tools to extract richer information on the

contribution of systemic risk sources to systemic risk.

Drivers: network topology (exposures), capital ratios, market

and funding liquidity, nature of shocks (see Gai and Kapadia

(2010), Loepfe et al. (2013), Roukny et al (2013)).

4Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Introduction

We focus on network topology and capital ratios as risk drivers

Regulation has emphasized restrictions over capital ratios of FIs

Contagion literature has emphasized the influence of network topology

They are the basis for many network risk measures proposed by the

literature, that build on a vulnerability matrix. E.g.:

Eisenberg & Noe (2001)’s computation of shock-related losses

Battiston et al. (2012)’s DebtRank

Bardoscia et al. (2015)’s DebtRank with cycles

Silva et al. (2015)’s Impact susceptibility, Network impact fluidity

and Weighted impact diffusion influence.

5Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

What we do

We present a methodology to quantify the influence of the

network topology and capital buffers on systemic risk

measurements in evolving financial networks.

We apply this methodology to analyze global banking network

data from 2005 to 2014, obtained from the BIS-CBS database.

We build counterfactual networks to analyze the influence of isolated

risk drivers.

We decompose the variation of systemic risk measurements along the

period into effects from network topology and capital buffer.

6Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Methodology

Given two financial networks, our methodology consists on

defining transformations that affect one risk driver at a time.

Starting from one of the networks and performing them

sequentially, we reproduce the Vulnerability matrix of the other.

We define: Network topology: Exposures Matrix A = (aij)

Capital buffer: E = (ei )

Vulnerability matrix V (does i propagate default to j?)

7Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Methodology – basics

Let:

Financial network: given by a pair (A, E)

(A, E): initial financial network (from)

(A′, E′): reference financial network (to)

ν: (A, E) → A / E = (aij / ej)

A / E: (aij / ej): vulnerability network

m(A, E): risk measurements that depend only on A / E

8Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Methodology – basics

We define the transformations:

The transformations scale down the levels of the variables of the

reference network to the levels of the initial network total exposures.

Transformations are linear.

9Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Methodology – order of transformations is irrelevant

Consecutive applications of the transformations t and r on the

initial network (A, E) lead to the vulnerability matrix of the

reference network (A′ / E′) regardless of order:

Why this is so:

Transformations t and r are linear

Vulnerability matrix is zero-degree homogeneous in (t, r)

10Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Methodology – decomposing effects of risk-drivers

Order of transformations irrelevant → we can define the effect

of risk drivers as the financial network changes from

(A, E) → (A′ / E′) as:

summing up:

m(A′, E′) - m(A, E) = ΔAm + ΔEm

11Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Methodology – decomposing effects of communities

We extend the methodology to find the effects of groups of

members k;

We define the transformation pk(A, E) as a composition of

transformations tk(A, E) and uk(A, E), similar to t and r;

We show that the order of transformations is also irrelevant:

Thus, the risk variation can be written as:

m(A′, E′) - m(A, E) = 𝑘=1𝑁 ∆𝑘𝑚

12Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Data

Quarterly data on cross-border exposures from the BIS-CBS

database, Mar 2005 – Dec 2014.

Banks’ consolidated positions of worldwide offices, excl inter-office exp

Central banks exposures not informed.

Reporting countries: 26. America, Europe, Asia and Oceania.

Pairwise exposures reported may be:

Immediate borrower basis (claims allocated to the country of the

immediate counterparty)

Ultimate risk basis (claims allocated to whom bears the final risk)

13Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

How we model the financial system network

Pairwise exposures: immediate borrower basis

Our methodology does not support conditional counterparties

Ultimate risk basis: if the guarantor defaults, he is not liable for the

guarantee unless the debtor also fails.

We only consider exposures between reporting countries.

These are 70% of total exposures reported.

We assume this network is a banking system. Each country is

a representative bank.

To estimate the countries’ loss-absorbing capabilities, we use the total

tier 1 capital of the country’s largest banks. We use BvD’s Bankscope.

Medium- and small-sized FIs do not hold significant amount fgn claims.

14Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Risk drivers data

Sep 08 Sep 08 Dec 12Dec 12

15Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Systemic risk measure adopted – intuition

Weighted impact diffusion influence (Silva et al. 2015)

This is a measure of the destructive stress that a country can pose to

the financial system. It is the network members’ vulnerability to

destructive impacts originating or being propagated by the country.

Related to a quantification of default cascade paths from the country.

Computation:

Given the network’s total

communicability, we subtract

from that the communicability

of a network in which q does

not initiate or continue a path.

16Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Systemic risk measures – intuition

Weighted impact diffusion influence (Silva et al. 2015)

It is the network’s communicability shortfall, weighted by the country’s

importance, occurred when q’s power of diffusing impacts is disabled.

Gpq(V) is the communicability p→q (Estrada and Hatano (2008))

17Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Analyses – 2 types

Counterfactual scenarios: fix the reference network at a given

date, varying the initial network along time. Use the initial

network to get the risk driver under study.

What would be the risk evolution had only one risk factor varied along

time? Use this analysis to disentangle effects from different risk drivers

and observe one of them isolated.

Effect decomposition as the network varies along time

How much do individual risk drivers (network topology or capital buffer

distribution) contribute to the evolution of risk measures along time?

18Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Analyses of counterfactual scenarios

How much do network topology and capital buffer

distribution contribute to risk measures along time?

1) Mar 2005 – Dec 2006Fragility increases

2) Mar 2007 – Dec 2009Subprime crisis

3) Mar 2010 – Dec 2012Onset European

sovereign crisis

4) Mar 2013 – Dec 2014Network comparatively

safer

1 23 4

19Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Counterfactual – weighted impact diffusion influence

We fix the reference network at Sep/2008 and check the

effects of network topology alone along time.

Keeping the capital buffer distribu-

tion of Sep 2008, we see that:

• Risk from the US and

European countries increased

fast until Mar 2008.

• Risk from the US kept high

levels until Sep 2010

• Risk from European countries

only decreased significantly

after Dec 2012.

20Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Counterfactual – weighted impact diffusion influence

We fix the reference network at Sep/2008 and check the

effects of capital buffer distribution alone along time.

Keeping the network topology of

Sep 2008, we see that:

• Risk from all countries

decreased fast until Mar 2008.

• After that, risk from all countries

remained mostly constant.

• Exception: risk, for the US and

European countries, increased

until Jun/09.

21Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Effect decomposition – incremental contribution

We compute a period-by-period decomposition of the network

weighted impact diffusion influence into the two risk sources:

More risk than the previous period

Less risk than the previous period

22Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Effect decomposition – incremental contribution

We compute a period-by-period decomposition of the network

weighted impact diffusion influence into the two risk sources:

• Network topology is a more

important volatility contributor

than capital buffer.

• Risk variation from capital buffer

is predominantly negative along

the period.

23Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

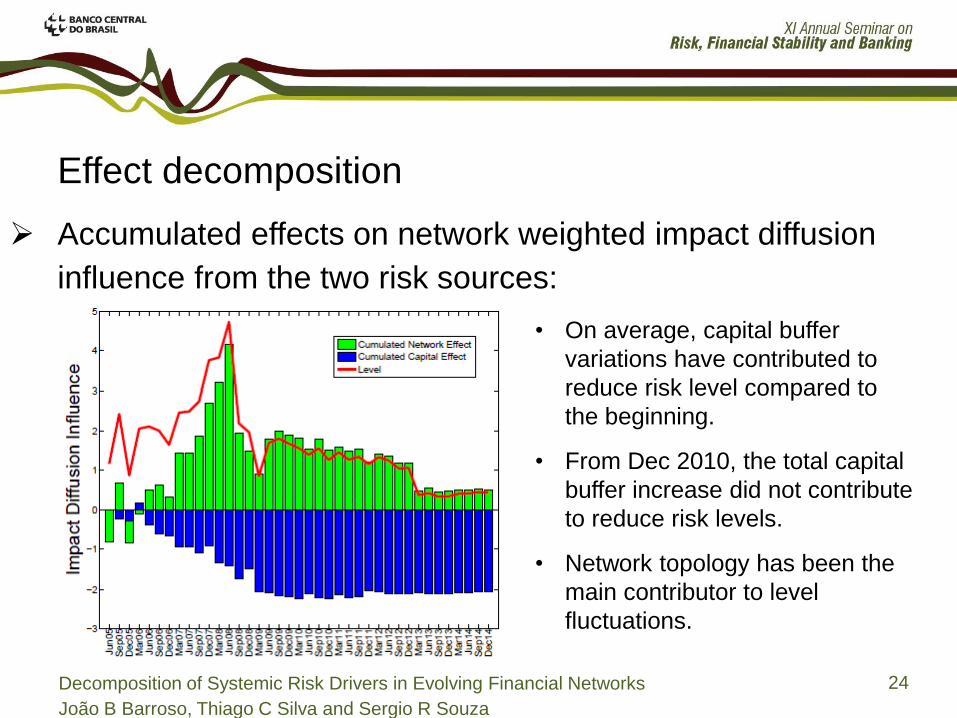

Effect decomposition

Accumulated effects on network weighted impact diffusion

influence from the two risk sources:

More risk than the first period

Less risk than the first period

24Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

Effect decomposition

Accumulated effects on network weighted impact diffusion

influence from the two risk sources:

• On average, capital buffer

variations have contributed to

reduce risk level compared to

the beginning.

• From Dec 2010, the total capital

buffer increase did not contribute

to reduce risk levels.

• Network topology has been the

main contributor to level

fluctuations.

25Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

To summarize…

We presented a methodology to enhance the network analysis

of financial networks. The methodology allows:

The analysis of the evolution of isolated risk drivers in a given scenario

The quantification of the effects of risk drivers contributions to risk

measures

The quantification of the effects of groups of network members in risk

measures.

26Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

To summarize…

Applying this methodology to the BIS-CBS global claims

networks, we found:

The isolated effects analyses (counterfactual scenario in Sep 2008) show

that prior to the crisis, capital buffers contribute strongly to reducing risks

while exposures increase them. From Sep 2008 onwards, none of the

factors seems, individually, to be able to reduce risk.

The decomposition of systemic risk drivers shows that, after the crisis,

exposures were the main contributor for sharply reducing the systemic risk

measure, in a context in which capital buffers were also varying. Besides,

exposures are responsible for a major share of the risk measure’s volatility,

while capitalization contributed steadily to lowering down the risk measure

level, compared to Mar 2005.

27Decomposition of Systemic Risk Drivers in Evolving Financial Networks

João B Barroso, Thiago C Silva and Sergio R Souza

THANK YOU

Sergio R Stancato de Souza