Deciphering SAFE, Convertible Notes & Term Sheets

29

Startup Law 101 Tytus Cytowski Managing Partner DECIHPERING SAFE, CONVERTIBLE NOTES & TERM SHEETS

-

Upload

tytus-cytowski -

Category

Law

-

view

45 -

download

0

Transcript of Deciphering SAFE, Convertible Notes & Term Sheets

Startup Law 101

Tytus CytowskiManaging Partner

DECIHPERING SAFE, CONVERTIBLE NOTES & TERM SHEETS

CYTOWSKI LLC

2

• Tips for Startups• Financing Road Map• Term Sheet• SAFE• Convertible Debt• Equity Financing• Economic Terms• Control Terms• Other Terms• Q&A

AGENDA

CYTOWSKI LLC

3

Key Business Issues

• Valuation and Price of Capital• How Much Money to Raise• Time Frame

Key Legal Issues

• Economic Rights and Control

TIPS FOR STARTUPS

CYTOWSKI LLC

4

TERM SHEET

STARTUP FINANCING

DEBT

HOW WILL YOU FINANCE?

EQUITY

CONVERTIBLE NOTE

PREFERRED STOCK

COMMON STOCK

ECONOMICCONTROL

OTHER

SAFE

Roadmap

INDIE VC

CYTOWSKI LLC

5

• Non binding agreement between founders and investors.• Why is it important if non binding?

BREAKDOWN OF A TERM SHEET

• SAFE vs. CONVERTIBLE NOTE vs. EQUITY (PREFERED EQUITY)• ECONOMIC TERMS – regulate return the investors will ultimately get at

exit.

• CONTROL – provisions allowing to affirmatively exercise control over the startup.

• OTHER – usually not that relevant, may be used as a smokescreen

TERM SHEET - BASICS

CYTOWSKI LLC

6

SAFE

CYTOWSKI LLC

7

Simple Agreement For Future Equity

CYTOWSKI LLC

8

• Definition: money converts to future equity in next financing• Not a loan and no interest• Spray & Pray Investors

Features:• Conversion mechanics• Discount Price• Valuation Cap

Example:• Ticket to a baseball game

SAFEBasics

CYTOWSKI LLC

9

CONVERTIBLE NOTE

CYTOWSKI LLC

10

• Definition: a regular loan which will convert to equity at such time as another round of financing is raised

• Used for bridge financing

Benefits:• No need to negotiate the valuation of the company (the main

drive)• Less paperwork• No decision making power for investors

CONVERTIBLE NOTEBasics

CYTOWSKI LLC

11

Downsides:

• Draws a line of what the company will be worth at the time of the first series financing.

• Potential investors may refuse to fund the company unless the debt investors remove or change the cap.

• Is a liability on the company’s balance sheet - may raise legal issues of insolvency.

CONVERTIBLE NOTEBasics

CYTOWSKI LLC

12

Discount price

• Automatic conversion into equity of the same type and under the same conditions as negotiated with subsequent investors but at a better price.

• Price typically range between 10 and 30 %

CONVERTIBLE NOTEKey terms

CYTOWSKI LLC

13

Valuation Caps

• Investor-favorable term that puts a ceiling on the conversion price of the debt.

• Protection against overvaluation of the company by the new investors and resulting loss of influence.

• Effectively used caps can create alignment between entrepreneurs and seed investors as long as they are thoughtfully negotiated

CONVERTIBLE NOTEKey terms

CYTOWSKI LLC

14

Interest rate

• Minimum upside the investor wants to have for the investment• Should not be high as it is not the essence of the convertible debt• Usually between 6 to 12 %

CONVERTIBLE NOTEKey terms

CYTOWSKI LLC

15

Conversion Mechanics

• Describe the time and the way in which the debt will convert.• The debt does not convert and stays outstanding if the company does not

reach its financing goal, unless the creditors agree to extend it.• Outstanding debt as gives the creditor control and possibility to initiate

bankruptcy proceedings. • Mechanism applicable in the sale of the company may be arranged for in many

ways, the most popular being the payment of the interest and the debt or its multiple.

CONVERTIBLE NOTEKey terms

CYTOWSKI LLC

16

EQUITY FINANCING(“PRICED ROUND”)

CYTOWSKI LLC

17

Common Stock (“Seed” Preferred)• Usually no rights or preferences• No downside protection (i.e., liquidation preference) for investors• Its valuation must be determined • Sets price for option grants • VCs are not interested in it, usually issued during friends and family

rounds.

Preferred Stock• Provides extensive economic and governance rights, preferences

and privileges to the shareholder• Issuance is expensive and time consuming • The only type of stock accepted by large VC’s

EQUITY FINANCING

CYTOWSKI LLC

18

• Price per share is a measure of what is being paid for the equity.• The concepts of pre-money and post money valuation.

EXAMPLE:Investor says “I’ll invest 2 million at a valuation of $10 million”.

Post Money Pre-money

Pays $2,000,000 Pays $2,000,000

Buys 20% of the company Buys only 16.6% of the company

ECONOMIC TERMSPrice/Valuation

• Conclusion: The pre-money understanding of valuation is more favorable towards the founders.

CYTOWSKI LLC

19

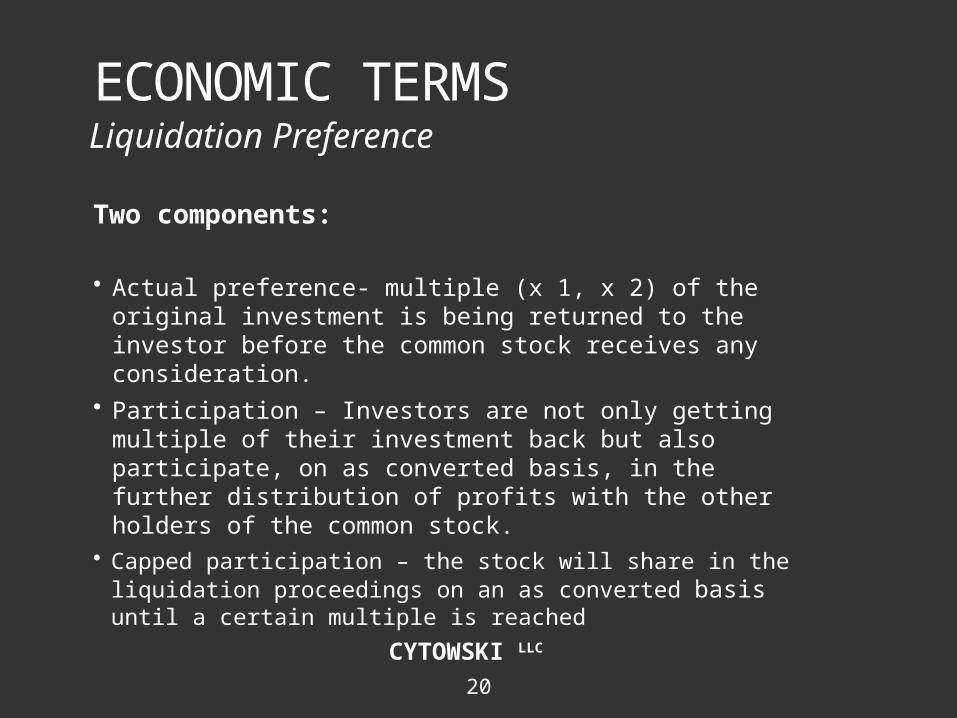

• Liquidation preference = the way proceeds are shared in a liquidity event.

• What is a liquidity event? Sale of the company or the majority of its assets, not only bankruptcy or winding down of the company.

• How does it work? The money is returned to a particular, preferred series of the company’s stock ahead of other series of stock.

ECONOMIC TERMSLiquidation Preference

CYTOWSKI LLC

20

Two components:

• Actual preference- multiple (x 1, x 2) of the original investment is being returned to the investor before the common stock receives any consideration.

• Participation – Investors are not only getting multiple of their investment back but also participate, on as converted basis, in the further distribution of profits with the other holders of the common stock.

• Capped participation – the stock will share in the liquidation proceedings on an as converted basis until a certain multiple is reached

ECONOMIC TERMSLiquidation Preference

CYTOWSKI LLC

21

EXAMPLE:

Let’s assume that the company is being sold for $20 million. There are 3 founders, each one of them is holding 20% of the common stock and an Investor who invested $4 million. If Investor’s stock has 2x preference and his/her stock is at the same time participating, it effectively means that he/she will get his/her $8 million first and then will participate equally with the other founders totaling $11 million.

Each founder will receive merely $3 million profit from this apparently beneficial transaction.

ECONOMIC TERMSLiquidation Preference

CYTOWSKI LLC

22

CONTROL TERMS

CYTOWSKI LLC

23

• Usually one director will be chosen by the founders and one by the investors

• Odd number of seats necessary in order to avoid a stalemate

• Observers

• Board of Directors seat given directly to the CEO - initially a founder

Board of DirectorsCONTROL TERMS

CYTOWSKI LLC

24

A right of an investor to block certain actions of the typically include:

• changing of the terms of stock owned by the VC

• issuing more stock

• Issuing stock senior or equal to the VC’s preferred

• selling the company

• changing the certificate or bylaws, i.e. size of board of directors

• Declaring or paying dividend

• Borrow money

Veto RightsCONTROL TERMS

CYTOWSKI LLC

25

• Drag along agreement gives a subset of the investors the ability to “drag along”, i.e. simply force all of the other investors and the founders to sell the company at the same time, to the same buyer.

• Desired provision - following the majority of the common stock, not the preferred. what may force preferred investors to convert some of their holdings to common stock to generate a majority what in turn results in a benefit to the common stockholders as it lowers the overall liquidation preference.

CONTROL TERMSDrag along

CYTOWSKI LLC

26

OTHER TERMS OF THE TERM SHEET

CYTOWSKI LLC

27

• Private Equity Background or Downside Protection• Do not provide venture returns at the beginning.

Watch out for:• Automatic dividends – can drag you to the insolvency zone. • Cumulative dividends – pose accounting problems

OTHERDividends

CYTOWSKI LLC

28

Right of First Refusal (ROFR)• Investor’s right to purchase certain amount of shares in a future

financing before any other interested entity.• Very common and Venture Capital investors will insist on it• Helps to control the shareholder base of the company what benefits all

constituents• Watch out for the super pro rata right

Voting rights• Voting rights establish the voting dynamics within the corporation,

usually between the common stock and various series of preferred stock.

OTHERROFR & VotingRights

CYTOWSKI LLC

29

Q&A