Decentralization and macroeconomic performance in...

21

Decentralization and macroeconomic performance in China: regional autonomy has its costs Andrew Feltenstein a, * , Shigeru Iwata b,1 a International Monetary Fund, 700 19th St. NW, Washington, DC 20431, United States b Department of Economics, University of Kansas, 226L Summerfield Hall, Lawrence, KS 66045, United States Received 1 May 2002; accepted 1 January 2004 Abstract We give an empirical examination of the impact of fiscal and economic decentralization in China on the country’s economic growth and inflation, using a vector autoregressive (VAR) model with latent variables. Our econometric investigation offers strong evidence that there is a connection between decentralization and macroeconomic performance in China. Economic decentralization appears to be positively related to growth in real output for the entire postwar period in China. Fiscal decentralization seems to have adverse implications for the rate of inflation, especially after the late 1970s. Decentralization would therefore seem to be good for growth and bad for price stability. D 2004 Elsevier B.V. All rights reserved. JEL classification: E31; H21; O53 Keywords: Fiscal; Decentralization; Stability; China 1. Introduction This paper investigates empirically whether decentralization in China has been beneficial for growth and inflation. Decentralization, whether in the form of fiscal 0304-3878/$ - see front matter D 2004 Elsevier B.V. All rights reserved. doi:10.1016/j.jdeveco.2004.01.004 * Corresponding author. Tel.: +1 202 6239437; fax: +1 202 623 6440. E-mail addresses: [email protected] (A. Feltenstein)8 [email protected] (S. Iwata). 1 Tel.: +1 785 8642867. Journal of Development Economics 76 (2005) 481 – 501 www.elsevier.com/locate/econbase

Transcript of Decentralization and macroeconomic performance in...

Journal of Development Economics 76 (2005) 481–501

www.elsevier.com/locate/econbase

Decentralization and macroeconomic performance in

China: regional autonomy has its costs

Andrew Feltensteina,*, Shigeru Iwatab,1

aInternational Monetary Fund, 700 19th St. NW, Washington, DC 20431, United StatesbDepartment of Economics, University of Kansas, 226L Summerfield Hall, Lawrence, KS 66045, United States

Received 1 May 2002; accepted 1 January 2004

Abstract

We give an empirical examination of the impact of fiscal and economic decentralization in China

on the country’s economic growth and inflation, using a vector autoregressive (VAR) model with

latent variables. Our econometric investigation offers strong evidence that there is a connection

between decentralization and macroeconomic performance in China. Economic decentralization

appears to be positively related to growth in real output for the entire postwar period in China.

Fiscal decentralization seems to have adverse implications for the rate of inflation, especially after

the late 1970s. Decentralization would therefore seem to be good for growth and bad for price

stability.

D 2004 Elsevier B.V. All rights reserved.

JEL classification: E31; H21; O53

Keywords: Fiscal; Decentralization; Stability; China

1. Introduction

This paper investigates empirically whether decentralization in China has been

beneficial for growth and inflation. Decentralization, whether in the form of fiscal

0304-3878/$ -

doi:10.1016/j.

* Corresp

E-mail add1 Tel.: +1

see front matter D 2004 Elsevier B.V. All rights reserved.

jdeveco.2004.01.004

onding author. Tel.: +1 202 6239437; fax: +1 202 623 6440.

resses: [email protected] (A. Feltenstein)8 [email protected] (S. Iwata).

785 8642867.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501482

federalism, or in the form of reduced government interference in the private sector, is

generally thought to help an emerging economy. Although the devolution of economic

power has been a central element in the reform process of many transition economies,

there is relatively little empirical work examining the relationship between such

decentralization and changes in the macroeconomy.

Decentralization may improve allocative efficiency, but it may also make stabilization

policies more difficult to carry out. See, e.g., Prudhomme (1994) and Tanzi (1995). China

has instituted rapid economic decentralization, and has simultaneously experienced both

growth and instability. There is a growing consensus in the academic literature about the

mechanisms that create the links between decentralization and economic growth and

inflation in post-reform China (Brandt and Zhu, 2000; Jin et al., 1999; Lardy, 1998;

Naughton, 1995; Yusuf, 1994). A simplified version of such a mechanism may be described

as follows.

Although the aggregate effective tax burden may not have changed, fiscal

decentralization has caused tax revenues to shift from the central government to

regional governments. The regional governments, infused with new revenue,

begin to build local infrastructure. This infrastructure encourages investment, both

of the non-state as well as the state-owned enterprises (SOEs). The non-state

firms tend to respond to the increased local infrastructure with higher rates of

investment than the SOEs, given their greater efficiency. As the SOEs attempt

to keep up with the rates of investment of non-state firms, a further adjustment

occurs. The SOEs, observing the increased rate of capital formation of the non-

state sector, increase their own rate of investment beyond the rate that would

be optimal. The SOEs are able to do so because they have access to local

bank loans that are not justified on economic grounds. This access to the

banking system thereby distinguishes them from the non-state firms.2 The banks

that passively grant these loans are themselves financed by discount lending by the

People’s Bank. The resulting monetary expansion leads to increased inflation, while the

higher output of both the SOEs and non-state enterprises cause an increase in aggregate

real income.

In this paper, we provide a formal empirical examination of decentralization in Chinese

economy, based on published data. We find that (i) decentralization plays indeed a fairly

important role in a VARmodel of growth and inflation, (ii) the pattern of the relation does not

appear to be restricted to the post-reform period, but rather characterizes the entire postwar

economy in China.

The next section will review China’s experiences with decentralization. Section 3 will

discuss our data set, including construction of measures of decentralization. Section 4 will

develop our econometric models, while Section 5 reports the results of estimation and tests

2 This access to local bank loans is a facet of the bsoft budget constraintQ that is a key feature of many

transition economies (see Maskin 1999 and Qian and Xu 1998 for recent theoretical work on the topic). One

might claim that a key distinction between SOEs in China and in a country such as, e.g., Brazil is that the

Brazilian banking system does not lend to the SOEs with the same degree of passivity as does the Chinese

banking system.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501 483

that have been carried out with those models. The final section is a summary and

conclusion.

2. Background

2.1. Decentralization in China

Between 1949 and 2001, the Chinese economy experienced frequent cycles, with

economic policy shifting between decentralization and recentralization programs. In the

early 1950s, the Soviet model of central planning shaped the relationships between the

State Council and local governments. The central authority exercised direct administrative

control over local governments through three central planning mechanisms: the physical

planning of production, centralized allocation of materials, and budgetary control of

revenues and expenditures.

Concentration of power at the center reduced the initiative of local governments

and hindered production, leading, in 1957, to the move to decentralization. A wave of

recentralization, however, began in the early 1960s, when almost all large and

medium-sized enterprises were returned to the central authority. A new decentral-

ization movement started in 1964 and continued throughout the Cultural Revolution

period.

Before 1979, China’s budgetary policy essentially consisted in generalized tax

collection and profit remittances controlled by the central government and then

redistributed as needed to the provinces. This system of beating from one potQ was

changed in the 1980 intergovernmental reform, under which different jurisdictions were

assigned different expenditure responsibilities and were also made responsible for

collecting necessary revenues.

Chinese fiscal decentralization has had certain features relevant to our study.3 China has

never had a true central tax administration. All taxes, with the exception of excises, have

been collected by local governments and then shared with the central government.

Accordingly, as decentralization has progressed, local governments that wish to promote

growth have tended to reduce their tax effort and revenue sharing with the central

government. This has resulted in the stagnation of revenue from indirect taxes despite

rapid growth in the economy.

2.2. Growth and inflation

2.2.1. Pre-reform period

The Chinese economy in the pre-reform period has been characterized by a cycle of

policy shifts, or bstop and goQ economic programs. Decentralization programs, intended to

3 For a review of Chinese fiscal decentralization, see Bell et al. (1993), Lardy (1998), Tseng et al. (1994),

Hofman (1993), World Bank (1994, 1996) and G. Ma (1995). A broad historical, as well as analytical, survey of

Chinese fiscal and macroeconomic policies is given in J. Ma (1997).

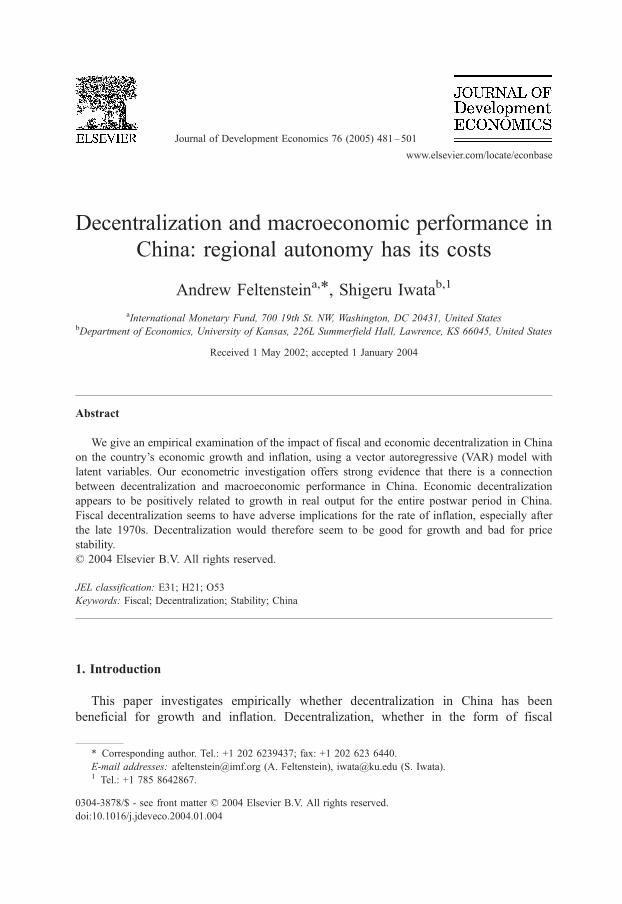

Fig. 1. Decentralization–recentralization cycle.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501484

rejuvenate a stagnate centralized economy, tended to cause overheating instead. Because

prices were controlled, inflation was not an immediate concern. Rather, it brought about

excess demand, oversaving and overinvestment at the expense of current output. To bring

the economy back to a more sustainable path, economic policy then shifted back to

recentralization programs. Such policies eventually led, however, to a decline in growth

(see Fig. 1).

2.2.2. Post-reform period

Economic decentralization in the post-reform period explicitly aimed at introducing

a free market economy by gradually removing price controls. Decentralized resource

allocation allowed an increase in investment in efficient non-state firms, leading to a

rise in aggregate economic growth. On the other hand, productivity in the inefficient

state sector lagged behind that in the non-state sector.4 Thus, the state sector came to

increasingly depend upon transfers from external sources to maintain employment by

supporting the ailing SOEs. By weakening the central government’s credit control, fiscal

federalism in effect creates a situation in which the central government has to finance

transfers to SOEs by money creation.5

These developments lead us to the following general view. Economic

decentralization (defined as the shift of economic activities from the state to

non-state sector) was a major cause of high growth. Fiscal decentralization

(defined as the shift of fiscal activities from the central to local governments) led

to fiscal instability and inflation. Conversely, some authors have argued that fiscal

4 See Groves et al. (1994), Dollar (1990) and Jefferson et al. (1999) for further discussion of changes in

Chinese productivity. The general relationship between fiscal policy and growth is examined in Easterly and

Rebelo (1993).5 Such a mechanism is described in Brandt and Zhu (2000) who say, bEmployment and investment growth in

China’s inefficient state sector have been supported by the government with transfers in the form of cheap credits

from the state-owned banks and money creation. . . . While this increases output growth, it also forces the

government to rely more heavily on money creation to finance the transfers to the state sector, which causes

inflation to increase as well.QWorld Bank (1994) maintains that China’s inflation can be explained by the effect of

decentralization on both the public sector deficit and control over monetary expansion.

Fig. 2. Economic growth and inflation in postreform period.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501 485

federalism is a key element in the success of China’s economic reform (Jin et

al., 1999). Thus, fiscal decentralization, i.e., fiscal federalism, created an

environment in which economic decentralization could exist and have a positive

effect upon economic growth. At the same time, the resulting interaction between

the two types of decentralization leads to monetary expansion and inflation (see

Fig. 2).

3. Data

Our data set consists of a macroeconomic time series from 1952 to 1996. The

data were derived primarily from Chinese Statistical Yearbook, International

Financial Statistics, Monthly Bulletin of Statistics of China (various issues), and

World Bank data. We recognize that measurement errors can arise from poor handling

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501486

of data and distortions by government bureaucrats. It is also possible that some

observed variables in China do not reflect properly economic activity. In earlier

periods, prices were not market determined but controlled by the central government.

Nonetheless, we treat the data as if there were no serious problems in its quality and

relevance. We do so because we believe that doing so is a useful route to take, at least for a

first trial.6

3.1. GNP and price series

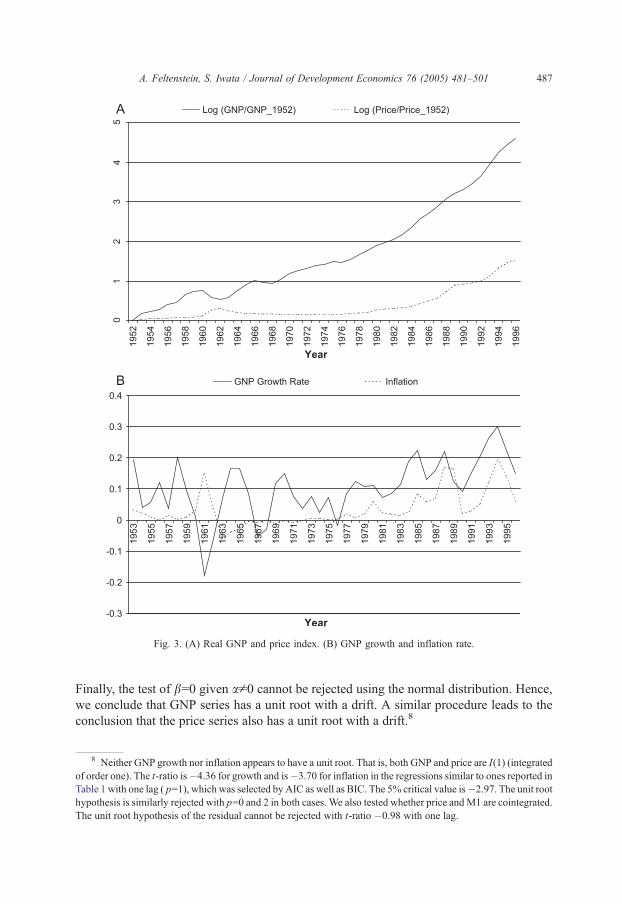

The two basic series for our study are the Chinese real gross national product (GNP)

and the retail price index.7 The series, for the period 1952–1996 are displayed in Fig. 3A,

while their first differences, GNP growth and the inflation rate, are shown in Fig. 3B.

An upward trend in real GNP is interrupted twice by sharp declines in 1961 and 1968

(Fig. 3A). The first drop is about a 35% decline from the previous year, the period

known as the bGreat FamineQ (1959–1961), an outcome of the economic and social

programs of the bGreat Leap Forward.Q The second drop, of about 10%, occurred in

the early part of the Cultural Revolution (1966–1976). The rate of inflation during the

entire 10 years period of the Cultural Revolution was virtually zero (Fig. 3B), a result of

extremely tight price controls. While GNP growth and inflation do not appear to be

correlated over the full period 1952–1996, they do after the initiation of the economic

reform in 1979. The simple correlation is 0.33 for 1952–1996, but this conceals a sharp

contrast between the pre- and post-reform period. The correlation is �0.59 for the

period 1952–1978, while it is 0.71 for the period 1979–1996. This striking change is

consistent with the point mentioned in Section 2.2.2 and emphasized by Brandt and Zhu

(2000).

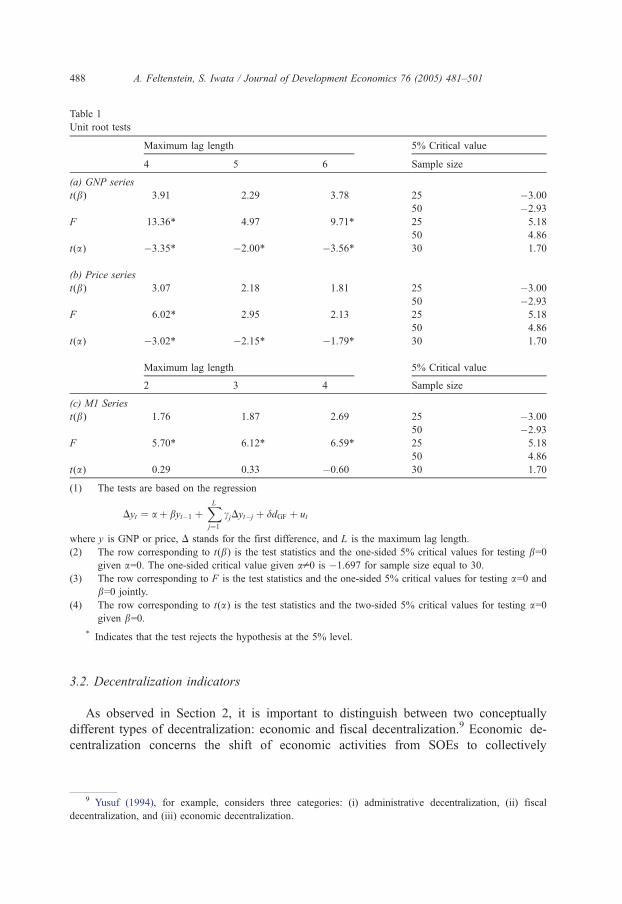

Table 1 provides the Dickey–Fuller test for GNP and price series. Based on a regression

of growth on a constant, lagged log of GNP, and 2–4 lags of growth, the test t(b) of the unitroot (i.e., b=0) for GNP given no drift (a=0) cannot be rejected. The F-test of a=b=0 is,

however, rejected. Then we test a=0, given that there is a unit root, and find it rejected [t(a)].

7 More precisely, our output series is the national income of the material product system, rather than GNP, as

published data of the latter began in 1978.

6 We treat the data as if there are no measurement errors, not because we have some reasons to believe the

measurement errors are entirely insignificant, but because a careless attempt to correct the data would frequently

make a situationworse and because even biased estimates often carry useful information. For example, some authors

suspect that official data overstate growth and understate inflation during the reform period (Lardy, 1998, Feltenstein

and Ha, 1991, Feltenstein et al., 1990). World Bank (1997) even provides estimates of the size of errors—

overstatement of the rate of growth by about 1.3 percentage points a year for 1986–1995. We experimentally re-

estimated our VAR model with the error corrected data based on the size of errors suggested by World Bank. The

results (not shown) are not importantly different from those reported in Section 5. On the other hand, the relevancy

of the measured variables, e.g., that of the measured price variable under price controls, is to some extent an

empirically testable proposition. We examined whether the price variable plays a qualitatively different role in our

VAR model between the period of the tight price control and the post reform period. When the Cultural Revolution

dummy (1966–1976) was included in the VAR, we found the dummy to not be significant, and there were no

changes in other parameter estimates. Hence, the price controls appear not to have been very important in our VAR

model.

Fig. 3. (A) Real GNP and price index. (B) GNP growth and inflation rate.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501 487

Finally, the test of b=0 given ap0 cannot be rejected using the normal distribution. Hence,

we conclude that GNP series has a unit root with a drift. A similar procedure leads to the

conclusion that the price series also has a unit root with a drift.8

8 Neither GNP growth nor inflation appears to have a unit root. That is, both GNP and price are I(1) (integrated

of order one). The t-ratio is�4.36 for growth and is�3.70 for inflation in the regressions similar to ones reported in

Table 1 with one lag ( p=1), which was selected by AIC as well as BIC. The 5% critical value is�2.97. The unit root

hypothesis is similarly rejected with p=0 and 2 in both cases. We also tested whether price and M1 are cointegrated.

The unit root hypothesis of the residual cannot be rejected with t-ratio �0.98 with one lag.

Table 1

Unit root tests

Maximum lag length 5% Critical value

4 5 6 Sample size

(a) GNP series

t(b) 3.91 2.29 3.78 25 �3.00

50 �2.93

F 13.36* 4.97 9.71* 25 5.18

50 4.86

t(a) �3.35* �2.00* �3.56* 30 1.70

(b) Price series

t(b) 3.07 2.18 1.81 25 �3.00

50 �2.93

F 6.02* 2.95 2.13 25 5.18

50 4.86

t(a) �3.02* �2.15* �1.79* 30 1.70

Maximum lag length 5% Critical value

2 3 4 Sample size

(c) M1 Series

t(b) 1.76 1.87 2.69 25 �3.00

50 �2.93

F 5.70* 6.12* 6.59* 25 5.18

50 4.86

t(a) 0.29 0.33 �0.60 30 1.70

(1) The tests are based on the regression

Dyt ¼ a þ byt�1 þXLj¼1

cjDyt�j þ ddGF þ ut

where y is GNP or price, D stands for the first difference, and L is the maximum lag length.

(2) The row corresponding to t(b) is the test statistics and the one-sided 5% critical values for testing b=0given a=0. The one-sided critical value given ap0 is �1.697 for sample size equal to 30.

(3) The row corresponding to F is the test statistics and the one-sided 5% critical values for testing a=0 and

b=0 jointly.

(4) The row corresponding to t(a) is the test statistics and the two-sided 5% critical values for testing a=0given b=0.

* Indicates that the test rejects the hypothesis at the 5% level.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501488

3.2. Decentralization indicators

As observed in Section 2, it is important to distinguish between two conceptually

different types of decentralization: economic and fiscal decentralization.9 Economic de-

centralization concerns the shift of economic activities from SOEs to collectively

9 Yusuf (1994), for example, considers three categories: (i) administrative decentralization, (ii) fiscal

decentralization, and (iii) economic decentralization.

Table 2

Decentralization indicators

Economic

decentralization

indicators

Tax The total tax revenue from individually or collectively owned

units divided by the total tax revenue from all types of units

Output The total value of gross output produced by individually or

collectively owned units divided by the total value of gross

output produced by all types of units

Sales The total value of retail sales by individually or collectively owned

units divided by the total value of retail sales by all types of units

Fiscal

decentralization

indicators

Expenditure The total expenditure of local governments divided by the total

expenditure of central and local governments

Revenue The total revenue of local governments divided by the total

revenue of central and local governments

Extra Budgetary

Revenue

The total extrabudgetary revenue divided by the total

government budgetary revenue

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501 489

owned enterprises (COEs) and private businesses.10 Fiscal decentralization concerns

the shift of government fiscal activities from the central to local levels. We interpret

economic decentralization as a major driving force toward market economy and

privatization. Historically, fiscal decentralization tends to enhance economic

decentralization.

Neither type of decentralization is, however, directly observable. Instead, we observe

them through their indicators. The degree of economic decentralization may be measured

by the relative size of tax contributions, output, and sales volume (dTaxT, dOutputT, anddSalesT11) of the non-state firms, while the degree of fiscal decentralization may be

measured through the relative size of expenditures and revenues of local governments as

well as extrabudgetary funds12 (dExpenditureT, dRevenueT, and dExtra BudgetT13). SeeTable 2 for more details.

11 Although all three indicators are strongly pairwise correlated (Table 3), dSalesT rarely helps to explain

growth and inflation.12 Extrabudgetary funds, which are in the public sector but are not subject to central budgetary control,

reflect the degree of fiscal independence of local governments. Extrabudgetary funds comprise a set of non-

budgetary levies and charges of government of administrative units that are under the control of

governments at various levels. They have largely been used by local governments to avoid revenue sharing

with the central government.13 Although all three indicators measure the extent of fiscal federalism, dRevenueT is not necessarily a good

indicator because the local governments tend to pass less and less tax collection on to the central government as

they become more independent. This tendency can be seen as a declining slope of the dRevenueT curve after 1978in Fig. 5B.

10 Although both SOEs and COEs are bpublic sectorQ enterprises, collectives, mostly township and village

enterprises (TVEs) located in rural areas, operate in a fashion more similar to commercial enterprises than to

traditional public enterprises (Broadman, 1995) in two important respects. First, COEs are not required to perform

the function of providing social services. Second, unlike SOEs, collectives generally have operated in an

environment without easy access to direct fiscal and quasi-fiscal government subsidies and a bankruptcy safety

net, therefore facing harder budget constraints.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501490

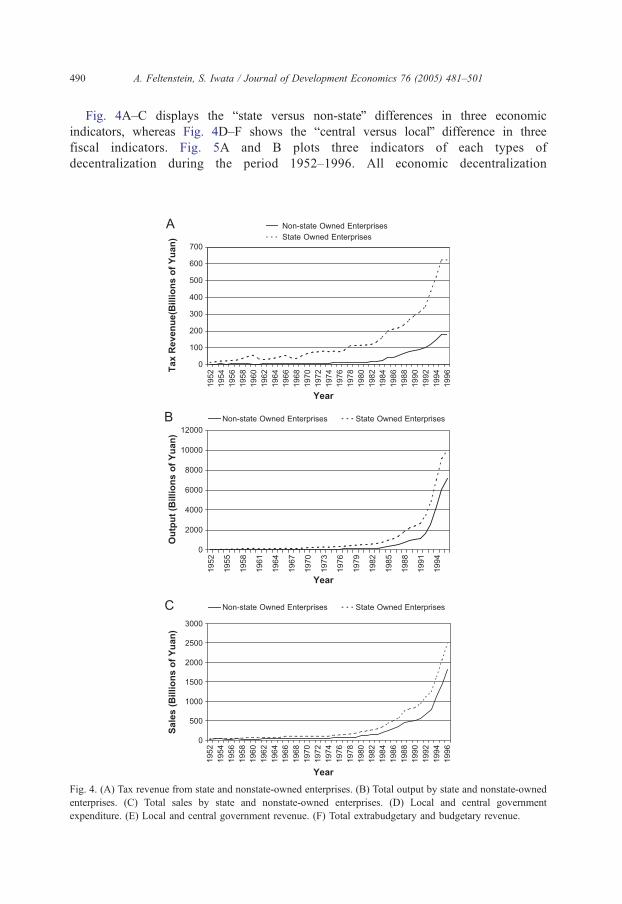

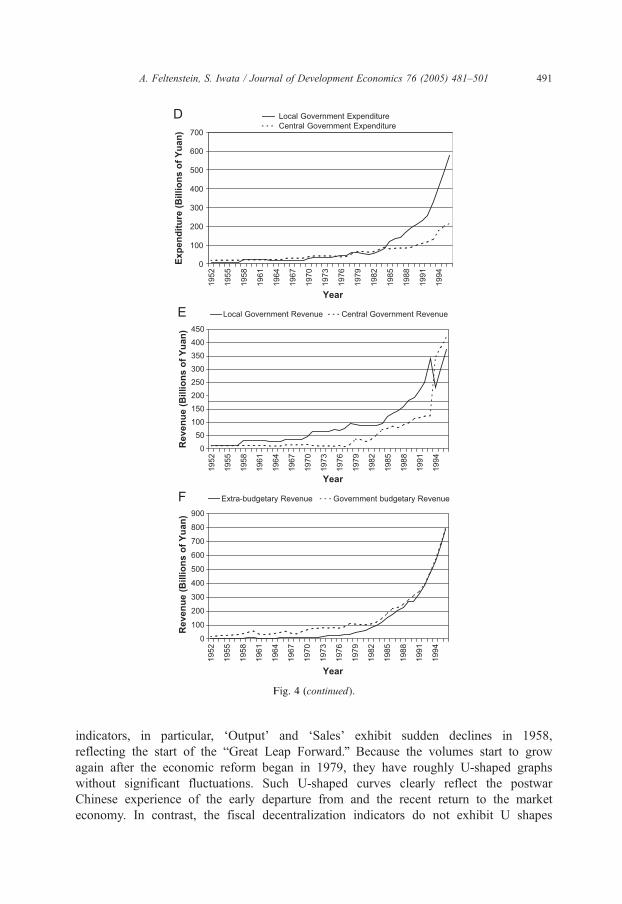

Fig. 4A–C displays the bstate versus non-stateQ differences in three economic

indicators, whereas Fig. 4D–F shows the bcentral versus localQ difference in three

fiscal indicators. Fig. 5A and B plots three indicators of each types of

decentralization during the period 1952–1996. All economic decentralization

Fig. 4. (A) Tax revenue from state and nonstate-owned enterprises. (B) Total output by state and nonstate-owned

enterprises. (C) Total sales by state and nonstate-owned enterprises. (D) Local and central government

expenditure. (E) Local and central government revenue. (F) Total extrabudgetary and budgetary revenue.

Fig. 4 (continued).

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501 491

indicators, in particular, dOutputT and dSalesT exhibit sudden declines in 1958,

reflecting the start of the bGreat Leap Forward.Q Because the volumes start to grow

again after the economic reform began in 1979, they have roughly U-shaped graphs

without significant fluctuations. Such U-shaped curves clearly reflect the postwar

Chinese experience of the early departure from and the recent return to the market

economy. In contrast, the fiscal decentralization indicators do not exhibit U shapes

Fig. 5. (A) Economic decentralization indicators. (B) Fiscal decentralization indicators.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501492

and tend to have more period-by-period fluctuations.14 This appears to reflect much

of policy cycles corresponding to the central government’s stop-and-go economic

programs.

14 dExpenditureT and dEx-BudgetT exhibit steady upward trends for the most of the period, while dRevenueTdeclines from the mid-1970s to the early 1980s and then drops drastically after 1994.

Table 3

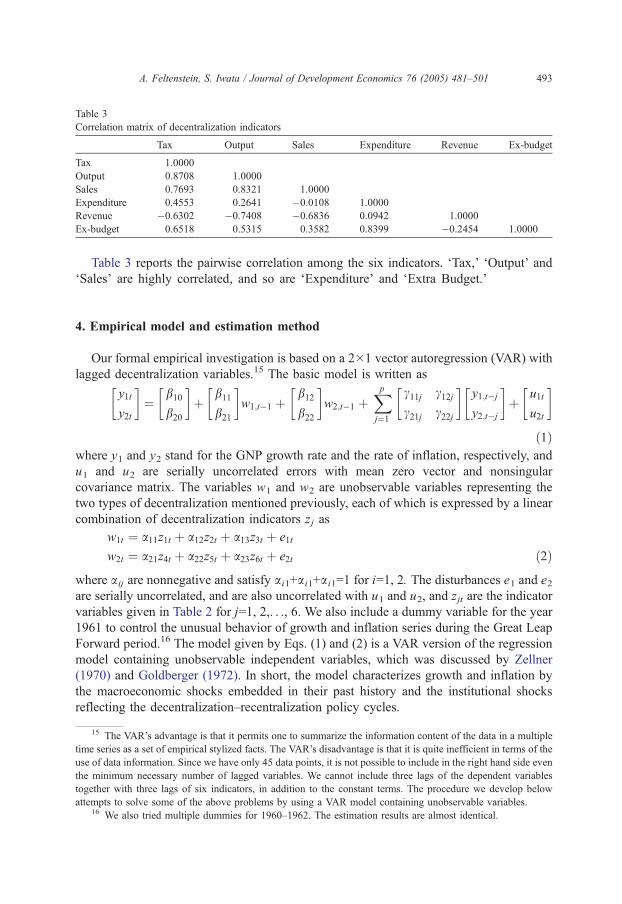

Correlation matrix of decentralization indicators

Tax Output Sales Expenditure Revenue Ex-budget

Tax 1.0000

Output 0.8708 1.0000

Sales 0.7693 0.8321 1.0000

Expenditure 0.4553 0.2641 �0.0108 1.0000

Revenue �0.6302 �0.7408 �0.6836 0.0942 1.0000

Ex-budget 0.6518 0.5315 0.3582 0.8399 �0.2454 1.0000

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501 493

Table 3 reports the pairwise correlation among the six indicators. dTax,T dOutputT anddSalesT are highly correlated, and so are dExpenditureT and dExtra Budget.T

4. Empirical model and estimation method

Our formal empirical investigation is based on a 2�1 vector autoregression (VAR) with

lagged decentralization variables.15 The basic model is written as�y1t

y2t

�¼�

b10

b20

�þ�

b11

b21

�w1;t�1 þ

�b12

b22

�w2;t�1 þ

Xpj¼1

�c11j c12jc21j c22j

��y1;t�j

y2;t�j

�þ�u1t

u2t

�

ð1Þwhere y1 and y2 stand for the GNP growth rate and the rate of inflation, respectively, and

u1 and u2 are serially uncorrelated errors with mean zero vector and nonsingular

covariance matrix. The variables w1 and w2 are unobservable variables representing the

two types of decentralization mentioned previously, each of which is expressed by a linear

combination of decentralization indicators zj as

w1t ¼ a11z1t þ a12z2t þ a13z3t þ e1t

w2t ¼ a21z4t þ a22z5t þ a23z6t þ e2t ð2Þ

where aij are nonnegative and satisfy ai1+ai1+ai1=1 for i=1, 2. The disturbances e1 and e2are serially uncorrelated, and are also uncorrelated with u1 and u2, and zjt are the indicator

variables given in Table 2 for j=1, 2,. . ., 6. We also include a dummy variable for the year

1961 to control the unusual behavior of growth and inflation series during the Great Leap

Forward period.16 The model given by Eqs. (1) and (2) is a VAR version of the regression

model containing unobservable independent variables, which was discussed by Zellner

(1970) and Goldberger (1972). In short, the model characterizes growth and inflation by

the macroeconomic shocks embedded in their past history and the institutional shocks

reflecting the decentralization–recentralization policy cycles.

15 The VAR’s advantage is that it permits one to summarize the information content of the data in a multiple

time series as a set of empirical stylized facts. The VAR’s disadvantage is that it is quite inefficient in terms of the

use of data information. Since we have only 45 data points, it is not possible to include in the right hand side even

the minimum necessary number of lagged variables. We cannot include three lags of the dependent variables

together with three lags of six indicators, in addition to the constant terms. The procedure we develop below

attempts to solve some of the above problems by using a VAR model containing unobservable variables.16 We also tried multiple dummies for 1960–1962. The estimation results are almost identical.

Table 4

VAR estimation

Model (a) (b) (c) (d) (e) (f)

Indicator equations

Tax 0.5437

(0.3510)

0.7113**

(0.2701)

0.5254*

(0.3055)

1.0000 0.3757

(0.2977)

0.8227**

(0.0892)

Output 0.4326

(0.3199)

0.1332

(0.2112)

0.4139

(0.2616)

– 0.1616

(0.1635)

–

Sales 0.0237

(0.2133)

0.1555

(0.1661)

0.0607

(0.1940)

– + –

Expenditure 0.5901*

(0.2916)

0.6680

(0.5517)

0.5888*

(0.2816)

1.0000 0.1643

(0.0873)

0.1773

(0.0892)

Revenue + 0.3320

(0.5517)

+ – 0.2983

(0.1783)

–

Extra budget 0.4099

(0.2916)

+ 0.4112

(0.2816)

– + –

Growth equation

Intercept �0.0757

(0.0584)

�0.0835

(0.0963)

�0.0929

(0.0595)

�0.0938*

(0.0522)

�0.0621

(0.0458)

�0.1154*

(0.0441)

Economic

decentralization

0.5123**

(0.1995)

0.7393**

(0.2365)

0.6308**

(0.2281)

0.8536**

(0.2136)

– –

Fiscal

decentralization

0.1977*

(0.0834)

0.1075

(0.1628)

0.2197*

(0.0866)

0.0902

(0.1014)

– –

Decentralization – – – – 0.6525**

(0.1891)

0.9474**

(0.2191)

Growth (�1) 0.3386**

(0.1101)

0.4791**

(0.1260)

0.2319*

(0.1154)

0.4350**

(0.1314)

0.3263**

(0.1093)

0.4158**

(0.1180)

Growth (�2) �0.3659**

(0.1106)

�0.2776*

(0.1248)

�0.2522*

(0.1196)

�0.2476*

(0.1246)

�0.3539**

(0.1093)

�0.2397*

0.1133

Growth (�3) – – �0.2536*

(0.1170)

– – –

Inflation (�1) �0.3896*

(0.2041)

�0.4113*

(0.2318)

�0.4148*

(0.2334)

�0.2411

(0.2348)

�0.4122*

(0.1934)

�0.2924

(0.2102)

Inflation (�2) �0.3761*

(0.1982)

�0.2934

(0.2379)

�0.2992

(0.2141)

�0.2624

(0.2408)

�0.3560*

(0.1978)

�0.2779

(0.2185)

Inflation (�3) – – �0.1577

(0.2404)

– – –

Population

Growth (�1)

– �1.5368

(2.0755)

– – – –

Population

growth (2)

– �1.0796

(1.5037)

– – – –

GF dummy �0.1776**

(0.0501)

�0.1949**

(0.0781)

�0.1387**

(0.0502)

�0.1706**

(0.0578)

�0.1843**

(0.0477)

�0.1822**

(0.0532)

Inflation equation

Intercept �0.0771*

(0.0348)

�0.1595**

(0.0513)

�0.0800*

(0.0356)

�0.1091**

(0.0292)

�0.0675*

(0.0256)

�0.0914**

(0.0295)

Economic

decentralization

0.1699*

(0.0818)

0.2975*

(0.1243)

0.1539

(0.0951)

0.3036**

(0.1195)

– –

Fiscal

decentralization

0.1392*

(0.0599)

0.1641**

(0.0547)

0.1435*

(0.0641)

0.1423**

(0.0567)

– –

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501494

Model (a) (b) (c) (d) (e) (f)

Inflation equation

Decentralization – – – – 0.3110**

(0.0983)

0.4432**

(0.1280)

Growth (�1) 0.0598

(0.0637)

0.0828

(0.0723)

0.0819

(0.0707)

0.1011

(0.0735)

0.0721

(0.0653)

0.1169

(0.0695)

Growth (�2) �0.0030

(0.0614)

�0.0043

(0.0625)

�0.0371

(0.0700)

0.0474

(0.0697)

�0.0135

(0.0627)

0.0409

(0.0641)

Growth (�3) – – 0.0566

(0.0710)

– – –

Inflation (�1) 0.4246**

(0.1152)

0.2934*

(0.1283)

0.4065**

(0.1317)

0.4647**

(0.1314)

0.4469**

(0.1157)

0.5068**

(0.1230)

Inflation (�2) �0.5386**

(0.1163)

�0.3502**

(0.1467)

�0.5260**

(0.1275)

�0.5057**

(0.1347)

�0.5350**

(0.1170)

�0.4931**

(0.1270)

Inflation (�3) – – �0.0403

(0.1393)

– – –

M1 Growth (�1) – 0.1416**

(0.033)

– – – –

M1 Growth (�2) – 0.0077

(0.0349)

– – – –

GF dummy 0.1496**

(0.0027)

0.1409**

(0.0266)

0.1441**

(0.0286)

0.1458**

(0.0323)

0.1547**

(0.0270)

0.1554 **

(0.0293)

Log likelihood 245.6336 251.5695 245.8565 240.0178 244.5202 238.0027

AIC �10.6016 �10.3128 �10.7428 �10.6675 �10.5962 �10.4287

(1) Figures in parentheses are standard errors.

(2) GF stands for Great Famine.

(3) + stands for the value of the estimate smaller than 0.0001 in magnitude.

(4) Akaike Information Criterion (AIC) is calculated according to

AIC ¼ � 2=nð Þ loglikelihoodð Þ þ 2K=nð Þwhere K is the number of parameters and n is the sample size.

(5) The column headed by (a) pertains to our base model given by Eqs. (1) and (2), while columns (b)–(f)

stand for five variations. Model (b) includes the exogenous variables having influence on GNP growth and

inflation. It adds the first and second lags of the population growth variables to the right hand of the GNP growth

equation, and adds the first and second lags of growth of the money supply (M1) to the right-hand side of the

inflation equation. Model (c) extends the maximum lag length of the dependent variables from 2 to 3. These two

models are to check for the possible effect of additional right-hand variables on the estimated coefficients of the

decentralization variables. In the remaining three models, we gradually impose additional restrictions to see if the

data support such restrictions. Model (d) uses one indicator (dTaxT and dExpenditureT) as a proxy for each

economic and fiscal decentralization, respectively, by setting a11=a21=1.0. In Models (e) and (f), we discard the

distinction between the two types of decentralization and combine all indicators into a single decentralization

variable. Model (e) includes all six indicators, while Model (f) uses only dTaxT and dExpenditureT.* One side 5% level of significance.** One side 1% level of significance.

Table 4 (continued)

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501 495

The model given by Eqs. (1) and (2) with lag length p=2 is our base line model

[Model (a)]. We specify five variations: Models (b)–(f) for comparison purposes (see

Table 5, note 6 for the detail). Estimation of the models is done by the maximum

likelihood method.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501496

5. Empirical results

Our interest centers on the following two questions: First, how important are the two

types of decentralization variables in describing economic growth and inflation in the

postwar economy in China? Second, is there any drastic regime shift in the structure of the

economy in China between pre- and post-reform periods?

5.1. Impact of decentralization

The estimation results for the VAR models are reported in Table 4. The values of the

Akaike Information Criterion (AIC) are similar for all models. There is no single model

that is especially unfavorable from this criterion. The important findings are summarized

as follows: First, two types of decentralization variables, economic and fiscal, are found to

be positive and highly significant (at the 1% or 5% level in most cases) in both the GNP

growth and inflation equations of Models (a)–(d). The single decentralization variables in

Models (e) and (f) are even more significant in both equations. Second, in Models (a)–(d)

the economic decentralization variable is relatively more significant in the GNP growth

equation, while the fiscal decentralization variable is relatively more significant in the

inflation equation.17

The strong association between economic decentralization and GNP growth supports

the view that the institutional change toward a more competitive market has been a cause

of growth in China. The similarly strong association between fiscal decentralization and

inflation favors the view that fiscal federalism often leads to inflation.

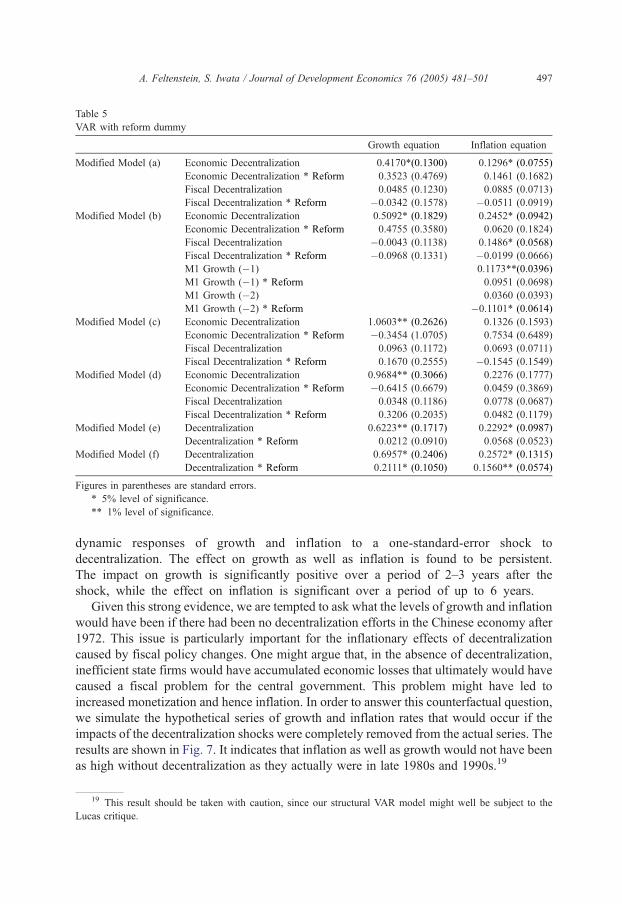

In order to go a step further in capturing the structural dynamics of the relation, we

estimate a structural VAR model by adding the decentralization variable to system (1) and

imposing identification restrictions.18 The coefficient estimates for the first two equations

are very close (not shown here) to those of Model (f) in Table 5. Fig. 6 presents the

17 Other findings are (i) highly significant lagged variables in the growth equation and in the inflation

equation are the dependent variables own first and second lags. No lagged growth variables are significant in the

inflation equation. The F-test result (not shown) implies that growth does not Granger cause inflation. (ii) The

estimated weights for the unobserved decentralization variables reveal that dTaxT and dExpenditureT dominate

other variables in economic and fiscal decentralization, respectively. dSalesT has almost no contribution to

explaining GNP growth and inflation. (iii) The strong significance of Great Leap Forward dummies in both

growth and inflation equations shows 1961 to be an outlier.18 For simplicity we do not distinguish fiscal and economic decentralization. The decentralization variable is

constructed using the weights estimated in Model (f). The model is given by

yt ¼ b0 þXpj¼1

&jyt�j þ ut

where yt=[ y1t,y2t,wt], b0 is a 3�1 vector , and &j is a 3�3 matrix of constants. To identify the decentralization

shock, we assume that decentralization is contemporaneously affected by neither the growth nor inflation shocks.

In other words, we assume

C ¼c11 0 0

c21 c22 c23c31 c32 c33

35

24

where ut=Ce t and Var(et)=I3, an identity matrix. We include up to third lags for all three variables in our VAR

model.

Table 5

VAR with reform dummy

Growth equation Inflation equation

Modified Model (a) Economic Decentralization 0.4170*(0.1300) 0.1296* (0.0755)

Economic Decentralization * Reform 0.3523 (0.4769) 0.1461 (0.1682)

Fiscal Decentralization 0.0485 (0.1230) 0.0885 (0.0713)

Fiscal Decentralization * Reform �0.0342 (0.1578) �0.0511 (0.0919)

Modified Model (b) Economic Decentralization 0.5092* (0.1829) 0.2452* (0.0942)

Economic Decentralization * Reform 0.4755 (0.3580) 0.0620 (0.1824)

Fiscal Decentralization �0.0043 (0.1138) 0.1486* (0.0568)

Fiscal Decentralization * Reform �0.0968 (0.1331) �0.0199 (0.0666)

M1 Growth (�1) 0.1173**(0.0396)

M1 Growth (�1) * Reform 0.0951 (0.0698)

M1 Growth (�2) 0.0360 (0.0393)

M1 Growth (�2) * Reform �0.1101* (0.0614)

Modified Model (c) Economic Decentralization 1.0603** (0.2626) 0.1326 (0.1593)

Economic Decentralization * Reform �0.3454 (1.0705) 0.7534 (0.6489)

Fiscal Decentralization 0.0963 (0.1172) 0.0693 (0.0711)

Fiscal Decentralization * Reform 0.1670 (0.2555) �0.1545 (0.1549)

Modified Model (d) Economic Decentralization 0.9684** (0.3066) 0.2276 (0.1777)

Economic Decentralization * Reform �0.6415 (0.6679) 0.0459 (0.3869)

Fiscal Decentralization 0.0348 (0.1186) 0.0778 (0.0687)

Fiscal Decentralization * Reform 0.3206 (0.2035) 0.0482 (0.1179)

Modified Model (e) Decentralization 0.6223** (0.1717) 0.2292* (0.0987)

Decentralization * Reform 0.0212 (0.0910) 0.0568 (0.0523)

Modified Model (f) Decentralization 0.6957* (0.2406) 0.2572* (0.1315)

Decentralization * Reform 0.2111* (0.1050) 0.1560** (0.0574)

Figures in parentheses are standard errors.

* 5% level of significance.

** 1% level of significance.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501 497

dynamic responses of growth and inflation to a one-standard-error shock to

decentralization. The effect on growth as well as inflation is found to be persistent.

The impact on growth is significantly positive over a period of 2–3 years after the

shock, while the effect on inflation is significant over a period of up to 6 years.

Given this strong evidence, we are tempted to ask what the levels of growth and inflation

would have been if there had been no decentralization efforts in the Chinese economy after

1972. This issue is particularly important for the inflationary effects of decentralization

caused by fiscal policy changes. One might argue that, in the absence of decentralization,

inefficient state firms would have accumulated economic losses that ultimately would have

caused a fiscal problem for the central government. This problem might have led to

increased monetization and hence inflation. In order to answer this counterfactual question,

we simulate the hypothetical series of growth and inflation rates that would occur if the

impacts of the decentralization shocks were completely removed from the actual series. The

results are shown in Fig. 7. It indicates that inflation as well as growth would not have been

as high without decentralization as they actually were in late 1980s and 1990s.19

19 This result should be taken with caution, since our structural VAR model might well be subject to the

Lucas critique.

Fig. 6. Impulse responses to the decentralization shock.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501498

5.2. Is the post-reform period a new paradigm?

Our models implicitly assume that the Chinese economy has been reacting to

decentralization in the same manner before and after the reform. To determine whether this

assumption is consistent with the data, we first conduct tests for a structural break in 1979.

The standard Chow test based on Model (d) (with F-ratios 1.9246 and 1.7507 for the

growth and inflation equation, respectively) cannot reject the null hypothesis of no

structural break. Similar results are obtained for the other models using likelihood ratio

tests. These results are particularly interesting when compared with the results obtained

when the VAR does not include any decentralization variables. The Chow test statistics

without decentralization variables (3.56 and 4.68 for the growth and inflation equation) are

larger than the critical value at the 5% level (2.53). Failure to include decentralization

indicators would therefore lead to erroneous conclusions supporting a structural break in

1979.20

Given little evidence of structural change in the entire process, we next investigate the

possibility of a change in the impact of decentralization on the economy after 1979. To test

this assumption we modify our Models (a)–(c) by replacing bij with bij+dijdt�1 for i=1, 2

and j=1, 2 in Eq. (1), where dt is a reform dummy defined by dt=1 for tz1979 and=0

otherwise.21 In all modified models except for Model (f) in Table 5, we find no interaction

terms with the reform dummy to be significant.22

20 Perhaps the less than expected support for a structural break might be a result of singling out 1979 as a

break point. The results of the CUSUM test (Brown et al., 1975) (not shown), however, provide clear evidence

against this view. No structural change is observed during the period from 1975 to 1996.21 We call the resulting models the dmodified Models (a)–(c)T. If dij is significantly positive in this model

while is bij not, then the effect of decentralization observed in Table 4 may be specific to the reform period. If bij

is significantly positive while d ij is not, then there is no change in the reaction of the economy to the

decentralization shocks before and after the reform started.22 Although the modified Model (f) shows a somewhat significant effect of the reform dummy, especially in

the inflation equation, we cannot reject the null hypothesis of no change in the impact of the decentralization after

1979. The stability of the coefficients of the decentralization variables in the growth and inflation equations is

confirmed by the results of the rolling vector autoregressions (not shown). Except for the initial period of the

inflation equation, the parameters appear to be stable.

Fig. 7. Impact of decentralization: (a) growth and (b) inflation. Note: The solid line represents the actual time

path, while the broken line represents the hypothetical time path that would be obtained without the

decentralization shocks.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501 499

Lastly, we take an additional step to examine how relevant the past history of the

Chinese economy can be for forecasting the country’s post-reform macroeconomic

performance. More specifically, we would like to see whether the inflation and economic

growth of the 1980s and 1990s could have been forecast, based on the known effects of

decentralization up to the 1970s. The forecasts based on the pre-reform data would

perform poorly if there were a dramatic structural break around 1979. Table 6 presents the

root mean squared error (RMSE) and the mean absolute error (MAE) for the one-step-

ahead forecasts, during the period 1980–1996, based on three models. Model (a)’s

performance is uniformly 15–30% better in terms of RMSE and MAE than the VAR

model without decentralization variables.23

Thus, if the effect of decentralization shocks on the economy is explicitly taken into

account, there appears to be little evidence that the post-reform period is a new

paradigm. This finding suggests that there is an important continuation process in the

23 In fact, among the 17 years of the post-reform period, the growth forecasts based on Model (a) outperform

those based on the simple VAR in all years but 1986, 1991 and 1995, while the inflation forecasts based on Model

(a) outperform the simple VAR in all years but 1981, 1983, 1986 and 1992. Model (a) predicts the 1988 growth

peak and its 1990 trough. The simple VAR model fails to predict the growth boom that started after 1990, which

Model (a) correctly captures. Although the improvement by Model (a) is not as striking in the inflation forecasts

as in growth, the 15% reduction of the RMSE is quite remarkable, given that the simple VAR forecasts here are

better than in the growth case.

Table 6

Forecast performance of VAR models

Growth Inflation

RMSE MAE RMSE MAE

Model (a) 0.0579 0.0482 0.0477 0.0361

Model (d) 0.0689 0.0574 0.0501 0.0364

VAR without decentralization variables 0.0762 0.0652 0.0561 0.0446

RMSE ¼ffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffi1=Hð Þ

PTþHt¼Tþ1 yt � ytð Þ2

qand MAE ¼ 1=Hð Þ

PTþHt¼Tþ1 jyt � yyt j, where yt and yt stand for the actual

value and its one-step ahead forecast, respectively.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501500

post war Chinese economy. This development is closely related to China’s bincremental

approachQ to economic transition, which contrasts to the bbig bang approachQ adopted by

a number of other countries. China’s reform has brought about a remarkable rate of

growth together with relatively low inflation.

6. Summary and conclusions

In this paper, we give a formal empirical examination of the impact of recent fiscal

and economic decentralization in China on economic growth and inflation. Our

econometric investigation offers evidence that there is, indeed, a connection between

decentralization and the performance of the macro economy in China. Economic

decentralization appears to be positively related to growth in real output. Fiscal

decentralization, however, seems to have adverse implications for the rate of inflation,

due to inadequacies in the financial system. Decentralization would therefore seem to

be good for growth and bad for inflation. The paper also found little evidence of a

structural break in the Chinese economy in 1979, if decentralization shocks are

explicitly taken into account. This aspect of continuation in the postwar Chinese

economic data has been largely neglected, but might be helpful in explaining the

country’s recent economic growth and inflation.

Acknowledgements

An earlier version of this paper was prepared as part of a project on decentral-

ization and provincial development in China, which was sponsored by the World

Bank. The work of the second author was supported by University of Kansas General

Research allocation #3533-20-0003-1001. We thank John Keating, Mohsin Khan and

De-Min Wu for helpful comments, and Yi Geng and Dongyi Liu for research

assistance. We especially thank Shahid Yusuf for suggesting the topic, as well as

offering invaluable support and advice. Finally, we would like to thank an anonymous

referee for a number of clarifying suggestions. The views expressed in this paper are

those of the authors and do not necessarily reflect the opinions of the International

Monetary Fund.

A. Feltenstein, S. Iwata / Journal of Development Economics 76 (2005) 481–501 501

References

Bell, M., Khor, H.E., Kochhar, K., 1993. China at the Threshold of a Market Economy. International Monetary

Fund, Washington, DC.

Brandt, L., Zhu, X., 2000. Redistribution in a decentralized economy: growth and inflation in China under reform.

Journal of Political Economy 108, 422–439.

Broadman, H.G., 1995. Meeting the challenge of Chinese Enterprise Reform. World Bank Discussion Papers 283.

Brown, R.L., Durbin, J., Evans, J.M., 1975. Techniques for testing the constancy of regression relationships over

time. Journal of the Royal Statistical Society. Series B 37, 149–163.

Dollar, D., 1990. Economic reform and allocative efficiency in China’s state-owned industry. Economic

Development and Cultural Change 34, 89–105.

Easterly, W., Rebelo, S., 1993. Fiscal policy and economic growth: an empirical investigation. Journal of

Monetary Economics 32, 417–458.

Feltenstein, A., Ha, J., 1991. Measurement of repressed inflation in China: the lack of coordination between

monetary policy and price controls. Journal of Development Economics 36, 279–294.

Feltenstein, A., Lebow, D., Van Wijnbergen, S., 1990. Savings, commodity market rationing and the real rate of

interest in China. Journal of Money, Credit and Banking, 234–252 (May).

Goldberger, A., 1972. Maximum-likelihood estimation of regressions containing unobservable independent

variables. International Economic Review 13.

Groves, T., Hong, Y., McMillan, J., Naughton, B., 1994. Autonomy and incentives in Chinese state enterprises.

Quarterly Journal of Economics Review, 183–209.

Hofman, B., 1993. An analysis of Chinese fiscal data over the reform period. China Economic Review 4, 213–230.

Jefferson, G.H., Sigh, I., Xing, J., Zhang, Z., 1999. China’s industrial performance: a review of recent findings.

In: Jefferson, G.H., Singh, I. (Eds.), Enterprise Reform in China: Ownership, Transition, and Performance.

Oxford University Press, New York.

Jin, H., Qian, Y., Weingast, B.R., 1999. Regional decentralization and fiscal incentives: federalism, Chinese style,

Working paper, Department of Economics, University of Maryland.

Lardy, Nicholas R., 1998. China’s Unfinished Economic Revolution. Brooking Institution Press, Washington, DC.

Ma, G., 1995. Income Distribution in the 1980s. China’s Quiet Revolution. St. Martin Press, New York.

Ma, J., 1997. Intergovernmental Relations and Economic Management in China. MacMillan, London.

Maskin, E.S., 1999. Recent theoretical work on the soft budget constraint. American Economic Review 89,

421–425.

Naughton, Barry, 1995. Growing Out of the Plan: Chinese Economic Reform, 1978–1993. Cambridge University

Press, New York.

Prudhomme, R., 1994. bThe dangers of decentralization.Q World Bank, unpublished manuscript.

Qian, Yingyi, Xu, Chenggang, 1998. Innovation and bureaucracy under soft and hard budget constraints. Review

of Economic Studies 66, 156–164.

Tseng, W., Khor, H.E., Kochar, K., Mihaljek, D., Burton, D., 1994. Economic Reform in China: A New Phase.

International Monetary Fund, Washington, DC.

Tanzi, V., 1995. Fiscal Federalism and Decentralization: A Review of Some Efficiency and Macroeconomics

Aspects, ABCDE Conference. The World Bank, Washington DC.

World Bank, 1994. China: Country Economic Memorandum, Macroeconomic Stability in a Decentralized

Economy. The World Bank, Washington DC.

World Bank, 1996. The Chinese Economy: Fighting Inflation, Deepening Reforms. The World Bank,

Washington, DC.

World Bank, 1997. China 2020: Development Challenges in the New Century. The World Bank, Washington, DC.

Yusuf, S., 1994. China’s macroeconomic performance and management during transition. Journal of Economic

Perspectives 8, 71–92.

Zellner, A., 1970. Estimation of regression relationships containing unobservable independent variables.

International Economic Review, 11.