December 2017 - NBG · Substantially lower CoR vs persistently high levels of 1H.17 ELA...

46

Corporate presentation December 2017

Transcript of December 2017 - NBG · Substantially lower CoR vs persistently high levels of 1H.17 ELA...

Corporate presentation

December 2017

1 Corporate Presentation – December 2017

No representation or warranty, express or implied, is or will be made in relation to, and no responsibility is or will be

accepted by National Bank of Greece (the Group) as to the accuracy or completeness of the information contained in

this presentation and nothing in this presentation shall be deemed to constitute such a representation or warranty.

Although the statements of fact and certain industry, market and competitive data in this presentation have been

obtained from and are based upon sources that are believed to be reliable, their accuracy is not guaranteed and any

such information may be incomplete or condensed. All opinions and estimates included in this presentation are

subject to change without notice. The Group is under no obligation to update or keep current the information

contained herein.

In addition, certain of these data come from the Group’s own internal research and estimates based on knowledge

and experience of management in the market in which it operates. Such research and estimates and their underlying

methodology have not been verified by any independent source for accuracy or completeness. Accordingly, you

should not place undue reliance on them.

Certain statements in this presentation constitute forward-looking statements. Such forward looking statements are

subject to risks and uncertainties that may cause actual results to differ materially. These risks and uncertainties

include, among other factors, changing economic, financial, business or other market conditions. As a result, you are

cautioned not to place any reliance on such forward-looking statements. Nothing in this presentation should be

construed as a profit forecast and no representation is made that any of these statement or forecasts will come to

pass. Persons receiving this presentation should not place undue reliance on forward-looking statements and are

advised to make their own independent analysis and determination with respect to the forecast periods, which reflect

the Group’s view only as of the date hereof.

Legal

Important Notice – Forward Looking Information

Table of Contents

1 Overview

2 Financial Highlights

3 Profitability

4 Asset Quality

5 Liquidity

6 Macro

7 Appendix I

Appendix II: Financials

Overview

1

4 Corporate Presentation – December 2017

Comprehensive strategy to tap the Greek recovery potential

Utilize high coverage and capital levels to work through NPLs

Deploy liquidity to support the recovery of the Greek economy

Improve profitability to allow for strong organic capital

generation

Overview

5 Corporate Presentation – December 2017

Successfully completed all major strategic objectives since the 2015 recapitalization

Completed divestments in line

with the restructuring plan

Increased loan loss coverage

to the highest levels among

peers

Set the basis for OPEX

reduction

Optimized collateral and

liquidity management

Significantly improved

financial performance across

key metrics

Exceeded NPE and NPL

reduction targets

2016

9m.17 Group PPI increases by

+9% yoy

9m.17 Group OpEx declines by

8% yoy

Exceeded 2017 NPE reduction

targets

Ongoing divestments on track

– expected to enhance further

capital and liquidity position

Clear path towards ELA

exposure elimination in the

short term

€1.1b loan disbursements to

corporates during 9m.17

Loan & Deposit balances lag

RP predictions by c.€4b and

c.€5b respectively, due to

extended economic

uncertainty

2017 9m

Consistently delivering on all strategic objectives

2015

Recapitalization

following the AQR

results

Restructuring plan

approval by EC

Revised strategy and

changed leadership

Overview

Higher NII on funding benefits

and positive growth in

corporate loans offsetting

lower NPL accruals

Substantially lower CoR vs

persistently high levels of

1H.17

ELA elimination; liquidity to be

channeled towards healthy

corporates

Enhancing outperformance

buffer on NPE reduction

>€2.0b in new corporate

disbursements

2018E

6 Corporate Presentation – December 2017

Positioning to take advantage of gradual economic recovery in the following years

- Satisfy healthy corporate credit

demand induced by a growing

macroeconomic environment,

benefiting NIM through mix

improvement and NII through

levering up

- Capitalize on leading debit card

position to increase POS fees and

e-banking transaction fees

- Further improve efficiency

- Utilize high coverage and capital

levels to work through NPLs

reduction

- Achieve all asset quality KPIs

agreed with SSM

- Increase restructuring efforts,

containing re-defaults

- Disengage from ELA funding

- Establish a recurring presence in

the primary wholesale funding

markets

- Capitalize on leading franchise

position to attract deposit inflows

Enhance core income growthA

Improve asset qualityB

Normalize the liquidity positionC

Strategic objectives going forward

Overview

7 Corporate Presentation – December 2017

C) Efficiency Improvement

A) Funding Cost Improvement

1. 2Q15 figures include the Ethniki Insurance Company

2. Down due to restructuring impact

3. Excludes the Ethniki Insurance company agreed to be sold

4. Expected NBG inflows in the 2 years following the imposition of capital controls at c.€3-4b, actual experienced at €1.3b

NBG has delivered most of medium term targets envisaged in the 2015 capital raise

Overview

D) CoR Evolution

B) Business Mix Optimization & Income growth

Greece

2Q15 3Q17 Δ

Time deposits repricing (bps) 185 90 -95

Reduction of ELA (€ b) 17.6 2.3 -15.3

Elimination of Pillar bonds (€ b) 8.7 0.0 -8.7

Deposit inflows (€ b)4 3-4 1.3

Greece

2Q151 3Q173 Δ

Gross Corporate loans / Total

loans (%)39.7 40.0 +30bps ●

Lending yield2 (bps) 411 388 -23 ●

Net Interest Income (€ m) 379 352 -27

Net Interest Margin (bps) 249 305 +56

Fee Income / Assets (bps) 30 43 +13 ●

Greece

2Q151 3Q173 Δ

# of employees (in 000s) 12.4 9.8 -2.6

Employee wage bill (€ m, ann.) 664 544 -120

Cost-to-Core income (%) 62 54 -8ppts

Greece

FY14A FY16A 3Q17A

CoR (bps) 270 212 198 ●

P&L charge (€ m, annualized) 1,000 683 604 ●

8 Corporate Presentation – December 2017

Remaining NPE reduction at €4.9b (€ b)

2017 NPE operational performance ahead of targets Parent NPE reduction targets (SSM perimeter) (€ b)

21.5

-3.5

-4.9 13.1

FY15 Done Remaining FY19

NPEs decline for a 6th quarter in a row adding up to a total reduction of €3.5b since

end 2015

Asset quality

• Operational targets submitted to the SSM contain a

reduction of NPLs and NPEs by €7.4b and €8.5b over the

period 2016-2019, equal to a reduction of c.50% and 40%

respectively; slight revision of targets relating to the timing

of reduction until 2019

• Upon achieving these targets in 2019, NPL and NPE ratios

will have been reduced by c.15ppts, with NPE coverage

around 50%

• Reduction of €3.5b so far, exceeding the 2017 target

15.2 15.3 15.0 15.0

14.0 13.913.6 13.6

12.9

7.7

6.4 0.0 6-0.9 5.6

-1.04.7

-0.9 4.7-0.2 4.6

-0.3 -0.2 0.1

5.0 5.4

21.5 21.5

20.6

19.618.7 18.5 18.2 18.0 18.1

13.1

-8.5

NPLs

NPEs

NPE reduction target

Total targeted:

-€8.5b

FY.17 target exceeded

9 Corporate Presentation – December 2017

1. Latest available data

NBG stands out in asset quality

Coverage

ratio

90dpd

ratio

TBV less

net NPLs

(€b)

TBV (€b)

Unprovided

NPLs (€b)

74% 70% 69%

66%

34%

36%37%

35%

NBG Peer 1 Peer 2 Peer 3

Peer Group1: 90dpd & Coverage (Group) Peer Group1: NPE & Coverage (Group)

56%45%

48%

52%

45%

55%54%

45%

NBG Peer 1 Peer 2 Peer 3

Coverage

ratio

NPE ratio

6.77.3

9.0

5.8

-3.8

-6.7-6.9

-5.8

NBG Peer 1 Peer 2 Peer 3

€2.8b €0.6b €2.1b -€0.1b

Peer Group1: net NPLs vs TBV (Group)

10 Corporate Presentation – December 2017

CET 1 ratio

Acceleration of divestiture plan enhances capital and liquidity substantially and

underlines NBG’s commitment to the successful implementation of the RP

Profitability

Divestments: latest developments

RWAs

(€ bn)39.0 38.5 38.5

16.5% 16.8% 16.6%

2Q17 3Q17 2017 Regulatory

Requirement

CRD IV fully

loaded

CET1:

€6.4bn

CET1:

€6.5bn

CET1:

8.75%

OCR:

12.25%

CET1:

€6.5bn

DTC:

€4.7b

• Ethniki Insurance closing expected in 1Q.18; impact

of: c110bps in capital and c€770m in liquidity

• Following the transaction NBG retains a 25% stake

along with an exclusive bancassurance agreement

• Vojvodjanska and NBG Leasing (Serbia) to close by

YE, Banca Romaneasca in early 2018; RWA

deconsolidation impact of c75bps in capital; liquidity

impact of c€1b

11 Corporate Presentation – December 2017

Selected digital and premium initiatives

Strong digital channels

Source: Company disclosureNotes: (1) Based on C.A.P.I. tracking study during the period April-June 2015*9M annualized

(2) Based on the sum of the four systemic banks

Technology and innovation provide new value added services

Overview

Deeply rooted customer relationships

Reputational excellence in Greece: “premium brand of choice”

Bank of reference in Greece for over 170 years

33%28%

22%17%

NBG Peer 1 Peer 2 Peer 3

33%

26%22%

19%

NBG Peer 1 Peer 2 Peer 3

Best Reputation (Survey) (1) Most Trustworthy (Survey)(1)

30.9% 30.6%

21.5%

17.0%

NBG Peer 1 Peer 2 Peer 3

Core deposit market share (3Q17)(2)

Total deposits/

branch€75.5m €62.2m €58.2m €60.6m

Modern and sophisticated bank offering premium cashless and digital

services

Strategic emphasis on developing and upgrading the i-bank platform

has resulted in significant transaction growth

Extensive e-banking platform with ancillary value adding services (e.g.

money transfers, share trading, payment of dues to tax authorities

and other companies and organizations)

Highly innovative i-bank store platform targeting young age groups

Premium banking provides a personalized service to the affluent

segment

Upgrading digital infrastructure a key priority

First full banking relationship loyalty program:

Number of customers at 175K

Wide network of participating merchants including super markets, gas stations and department stores

14.7m 17.6m

Electronic transactions

28.9m

870K

1,123K

1,340K

1,549K

2014 2015 2016 9M17

€25.0bn €25.8bn

€40.3bn

€50.8bn

2014 2015 2016 9M17*

35.6m

E-banking users

Financial Highlights

2

13 Corporate Presentation – December 2017

NPE reduction continues, ELA disengagement is imminent, agreed capital actions

to provide a buffer against regulatory exercises

Liquidity, Asset Quality & Capital Highlights Key Ratios - Group

9M17 1H17 1Q17 9M16

Liquidity

Loans-to-Deposits ratio 83% 86% 87% 89%

ELA exposure (€ bn) 2.3 3.8 5.6 5.2

Profitability

NIM (bps) 307 306 302 280

Cost-to-Core income 51% 50% 49% 55%

Asset quality

NPE ratio 45.2% 45.0% 44.9% 46.6%

NPE coverage ratio 55.9% 55.7% 56.0% 55.5%

Cost of Risk (bps) 238 260 278 189

Capital

CET1 phased-in 16.8%1 16.5%1 16.0%2 16.4%3

CET1 ratio CRD IV FL 16.6%1 16.3%1 15.8%2 15.9%3

RWAs (€ bn) 38.51 39.01 41.32 40.33

Highlights

Domestic NPE stock reduction continues for a 6th consecutive quarter

• NPE reduction continues in 3Q17, with the stock reduced by €0.2b, reflecting

negative formation of €119m and fully provided write offs of €105m

• Net NPE reduction achieved since end-2015 at €3.5b, exceeding the FY.17 SSM

target

• Group NPE and NPL coverage at sector leading levels (56% and 74%), combined

with the lowest NPL and NPE levels among domestic banks

ELA close to elimination

• ELA exposure reduced by €2.8b since 2Q17, standing at €1.0b in October ‘17

• 1st covered bond transaction since 2009 completed in October, raising €750m at a

yield of 2.90%; 85% of the issue was covered from international investors

• Short term completion of agreed capital transactions of Ethniki Insurance, Banca

Romanesca and Vodvodjanska to provide an additional €1.7b in liquidity

• Superior liquidity position and lowest funding cost among local peers, imply NBG is

best positioned to satisfy future corporate credit demand

CET 1 ratio at 16.8% or 16.6% on a CRD IV FL basis

• Group RWAs at €38.5b of which €34.4b in Greece

• Agreed capital actions expected to complete by early 2018, providing additional

capital buffer ahead of upcoming regulatory exercises

1. Excludes the impact from the agreed sales of S.A.B.A., Ethniki Insurance, Banca Romaneasca and Vojvodjanska Banka

2. Excludes the impact from the agreed sales of UBB, Interlease & S.A.B.A.

3. Excludes CoCos

14 Corporate Presentation – December 2017

€ m 9M17 9M16 YoY 3Q17 2Q17 QoQ

NII 1 193 1 252 -5% 378 405 -7%

Net Fees & Commissions 176 123 +43% 57 59 -4%

Core Income 1 369 1 375 -0% 435 464 -6%

Trading & other income (155) (96) +61% (81) (73) +11%

Income 1 214 1 279 -5% 354 391 -9%

Operating Expenses (701) (762) -8% (238) (232) +3%

Core PPI 667 613 +9% 196 232 -15%

PPI 513 517 -1% 116 159 -27%

Provisions (589) (487) +21% (156) (200) -22%

Operating Profit (77) 30 n/m (40) (41) -3%

Other impairments (4) (59) -93% 2 (1) n/m

PBT (81) (29) >100% (38) (42) -10%

Taxes (23) (11) >100% (6) (10) -41%

PAT (cont. ops) (104) (40) >100% (44) (52) -16%

PAT (discont. ops) (48) (2 891) -98% 19 (97) n/m

Minorities (26) (28) -6% (10) (7) +42%

PAT1 (178) (2 959) -94% (35) (156) -78%

P&L Highlights

1. 9m.17 PAT incorporates a capital loss of €94m and €56m form the agreed sales of the Romanian and Serbian

businesses which have not yet completed. Upon completion capital will benefit from RWA deconsolidation.

9m17 Group core PPI increases by +9% yoy; Q317 provisions level off

Highlights

Group P&L

9m17 group PPI at €513m, flat yoy, on the back of:

• Flat group core income reflecting sustained deleveraging offset by

lower funding costs

• Lower group OpEx (-8% yoy equal to c€60m yoy)

• Increased non core income losses of €155m in 9m.17

More specifically in 3Q:

• NII down by 7% qoq or -€27m qoq, reflects continuing deleverage of

the loan portfolio, as well as reducing exposure to high yielding GGBs

• Net fees and commissions (-4% qoq) are up +43% yoy in the 9m,

benefitting from the elimination of Pillar funding costs and a pick up in

retail and other banking related fee income

• Group OpEx reduction (-8.0% yoy), is driven by domestic personnel

costs (-12.4% yoy), reflecting the 2016 VES

• Domestic credit risk charges are down by 24% qoq, but remain

conservative with a CoR ratio of 198bps; NPE coverage increases by

40bps qoq to 56.6%, the highest among domestic peers

Profitability

3

16 Corporate Presentation – December 2017

231 269 241

-189 -238 -192

9M16 9M17 3Q17

Group Core Operating margin1 (bps)

Group Core PPI bridge (€ m)Group Core PPI decomposition by region (€ m)

1. Core PPI margin and CoR are calculated over net loans

9m17 domestic core PPI +10% yoy, as funding cost benefits and cost savings

outweigh NII pressure

Profitability

198220

185

573

633

1312

11

40

34

211232

196

613

667

3Q16 2Q17 3Q17 9M16 9M17

GRE SEE & Other

613

-60

+53

+61 667

9M16 ΔNII Δfees ΔOpEx 9M17

Group Core

PPI margin

Group

CoR

+10.5%

-14.1%

YoY

42 31 49Group Core

operating

margin

-6.6%

-15.4%

YoY

NII drop reflects mainly

sustained deleveraging

and lower NPL accruals

partially offset by NII

funding cost benefits

On lower NII due to

GGBs (-€14m)

o/w: P2

funding

benefit

€42m

17 Corporate Presentation – December 2017

SEE & Other

Greece

389 383 384 379 352

282 287300 309 305

3Q16 4Q16 1Q17 2Q17 3Q17

NII (€m) NIM (bps)

Domestic NIM maintained north of 300bps

Profitability

Evolution of domestic net loans (€ b)

Domestic NII breakdown

31.9

-0.8 -0.1 -0.2 -0.5

30.3

9M16 Mortgages Consumer SBLs Corporate 9M17

28 23 26 26 26

345

299

338 340 339

3Q16 4Q16 1Q17 2Q17 3Q17

NII (€m) NIM (bps)

3Q16 4Q16 1Q17 2Q17 3Q17 9M16 9M17

Loans 379 361 370 352 339 1,157 1,061

Deposits -44 -40 -37 -37 -36 -144 -110

Bonds 79 81 81 88 74 247 243

Eurosystem

& wholesale-18 -18 -21 -20 -15 -94 -56

Subs &

other-7 -1 -9 -5 -8 2 -21

Total 389 383 384 379 352 1,168 1,116

Reduction of c.€1.6b

in eop net balances in

12months

18 Corporate Presentation – December 2017

17.7 18.0 17.8 17.9 18.1

7.2 7.6 7.0 7.2 7.5

11.1 11.3 11.3 11.1 11.1

36.036.8 36.1 36.2 36.7

3Q16 4Q16 1Q17 2Q17 3Q17

Time

Sight &

other

Savings

+1.3% qoq

Greek deposit yields (bps)

2018 17 17

14

103

95

89 89 90

4744

41 40 39

3Q16 4Q16 1Q17 2Q17 3Q17

Domestic deposits pick up by €0.5b qoq, while time deposit yields bottom out

Profitability

Greek deposits evolution (€ b)

Time

Total

New production

yield

at c75 bps

69% 69% 69% 69% 68% Core deposits/total

Mkt share 37%,

+1.0 ppts yoy

Core

19 Corporate Presentation – December 2017

Greek lending yields1 (bps)

256 257 255 256 254

947933 932 934 935

648 643631 627 625

414403 404 398 390

3Q16 4Q16 1Q17 2Q17 3Q17

1: Calculated on performing loans including FNPEs<90dpd

2: Performing loans derived after deducting 90dpd loans

Domestic deleveraging continues, driven mainly be retail exposures; lending yields

are down slightly but remain at high levels supporting NIM at a +300bps level

Profitability

Greek loan evolution (€ b)

11.7 11.5 11.2 11.0 10.9

2.3 2.3 2.2 2.2 2.2

1.4 1.4 1.4 1.4 1.3

12.6 13.0 13.0 12.8 12.5

28.0 28.2 27.8 27.4 26.9

3Q16 4Q16 1Q17 2Q17 3Q17

Corporate

SBL

Consumer

Mortgages

Consumer

SBLs

Corporate

Mortgages

Total lending yield (bps)

-1.8% qoq

31.9 31.7 31.3 30.8 30.3 Net loans

Performing loans2

402 396 395 393 388

20 Corporate Presentation – December 2017

21 20 21

64 6821 23 20

6465

814 11

27

35

5057

53

155

167

3Q16 2Q17 3Q17 Column1 9M16 9M17

Fund

mgm,

Brokerage

& other

Wholesale

Banking

Fees

Retail

Banking

Fees

5057 53

155167

66

6

13

13

5663

59

168

180

3Q16 2Q17 3Q17 Column1 9M16 9M17

Group fee income by region excl. ELA fees (€ m)

9m17 domestic fee income up by +8% yoy, driven by retail and other banking

related fee income; including PII fee impact, fees are up by +52% yoy

Profitability

Domestic fee decomposition excl. ELA fees (€ m)

Fees/Assets1

Total

SEE &

Other

0.31%

Greece+5%

0.38%0.38%

YoY

+28%

+8%

+2%

0.31%

-1%

YoY

+34%

+5%

-2%

0.38%

+8%

YoY

+0%

+7%

+5%

YoY

+0%

+4%

1: Excluding assets held for sale

ELA cost6 23 51 9 ELA cost 6 23 51 9

21 Corporate Presentation – December 2017

55%

50%

54%

9M16 9M17 3Q17

Domestic OpEx evolution (€ m)

Group OpEx by category (€ m)

9m17 personnel costs decline 12% yoy, leading total costs down by 9% yoy and

cost-to-core income to 50%

Profitability

Headcount evolution (‘000)

Domestic cost-to-core income evolution

Greece Group

9M17 9M16 yoy 9M17 9M16 Yoy

Personnel 399 455 -12.4% 433 489 -11.5%

G&As 175 179 -2.0% 198 203 -2.2%

Depreciation 66 66 +0.2% 70 70 +0.1%

Total 640 700 -8.6% 701 762 -8.0%

154 147 131 132 136

82 8879 81 82

237 235210 213 217

3Q16 4Q16 1Q17 2Q17 3Q17

15.012.2 12.0

9.9 9.9 9.8 9.8

10.1

7.9 7.8

1.9 1.9 2.0 2.0

25.1

20.1 19.8

11.8 11.8 11.8 11.8

FY09 1 FY14 FY15 FY16 1Q17 2Q17 3Q17

G&A &

other

Staff

SEE &

Other

Greece

1. Excludes Ethniki Insurance Company, UBB, BROM & Vojvo employees

111 1

€2.5m one off

due to employee

promotions

Asset quality

4

23 Corporate Presentation – December 2017

15.3 14.4 14.3 13.9 13.9

4.84.8 4.7 4.8 4.6

20.119.2 19.0 18.7 18.5

3Q16 4Q16 1Q17 2Q17 3Q17

FNPEs & other

impaired

90dpd

Domestic NPE stock evolution (€ b)

Domestic NPE stock movement (€ b)Domestic NPE stock per category – 3Q17 (€ b)

Despite low write offs in 3Q, negative formation of -€119m allows the NPE stock to

keep declining

Asset quality

46.4% 45.1% 45.1% 45.2% 45.3%NPE ratio

5.6

2.3 2.2

3.8

1.5

0.3 0.3

2.5

7.0

2.6 2.5

6.3

Mortgages Consumer SBL Corporate

FNPE & other

impaired

90dpd

13.9

18.5

22.0

-0.6-0.3

21.1

-0.7-0.2

20.1

-0.2-0.7

19.2+0.04

-0.2

19.0

-0.01-0.3

18.7

-0.1 -0.1

18.5

+4bps reported

basis,

-59bps qoq ex

deleveraging

24 Corporate Presentation – December 2017

Mortgages (€ m)

* SSM perimeter

Asset quality

NPE formation remains negative in 3Q17, improving to -€119m qoq

Consumer (€ m) NPE formation* (€ m)

SBLs (€ m) Corporate (€ m)

-609

-131

66 43 30

3Q16 4Q16 1Q17 2Q17 3Q17

-101

-50 -34-42 -20

3Q16 4Q16 1Q17 2Q17 3Q17

-81

-4

925

-12

3Q16 4Q16 1Q17 2Q17 3Q17

32

-20

13

-40

-116

3Q16 4Q16 1Q17 2Q17 3Q17-759

-205

54

-14

-119

3Q16 4Q16 1Q17 2Q17 3Q17

25 Corporate Presentation – December 2017

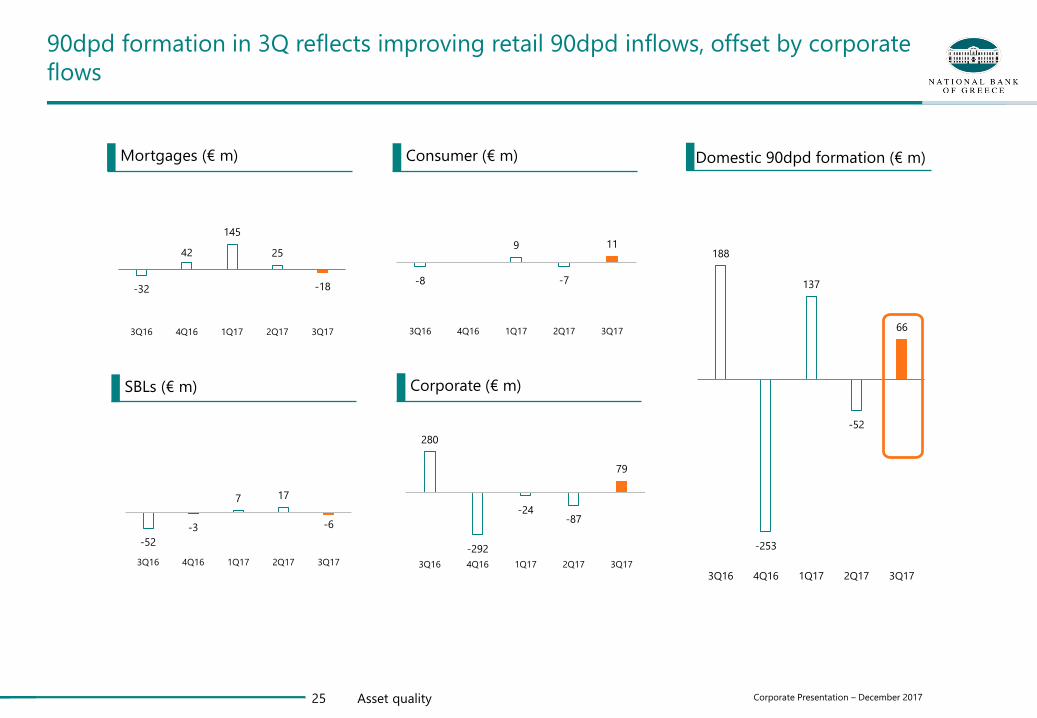

Mortgages (€ m)

Asset quality

90dpd formation in 3Q reflects improving retail 90dpd inflows, offset by corporate

flows

Consumer (€ m) Domestic 90dpd formation (€ m)

SBLs (€ m) Corporate (€ m)

-32

42

145

25

-18

3Q16 4Q16 1Q17 2Q17 3Q17

-8

0 9

-7

11

3Q16 4Q16 1Q17 2Q17 3Q17

-52

-3

7 17

-6

3Q16 4Q16 1Q17 2Q17 3Q17

280

-292

-24-87

79

3Q16 4Q16 1Q17 2Q17 3Q17

188

-253

137

-52

66

3Q16 4Q16 1Q17 2Q17 3Q17

26 Corporate Presentation – December 2017

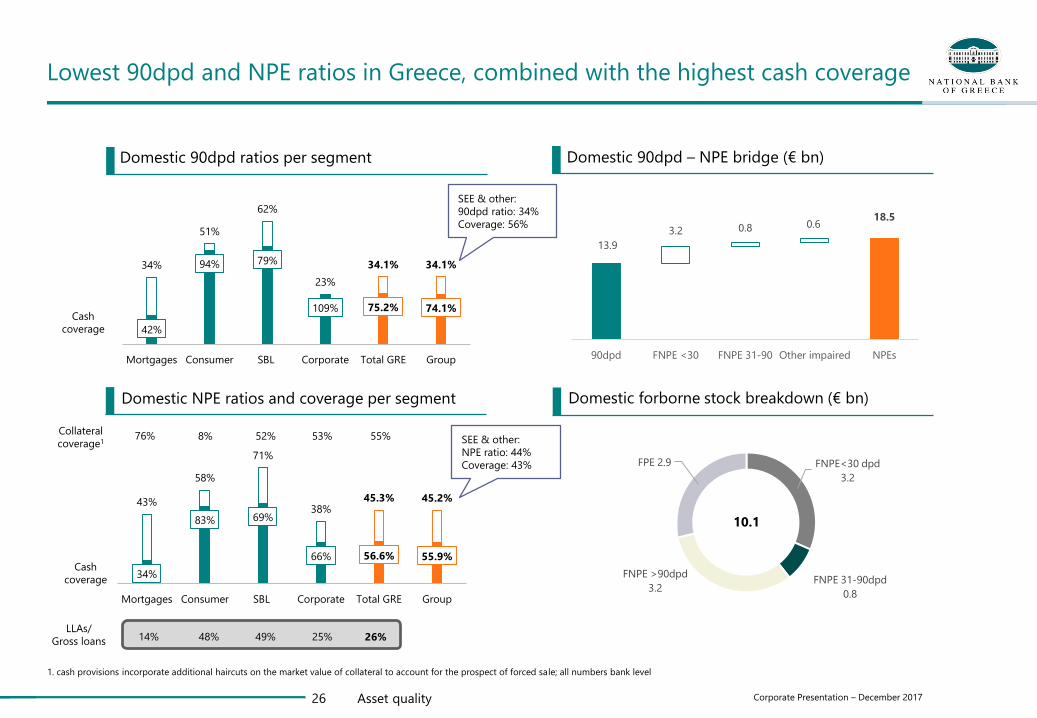

Domestic NPE ratios and coverage per segment

Domestic 90dpd ratios per segment

1. cash provisions incorporate additional haircuts on the market value of collateral to account for the prospect of forced sale; all numbers bank level

Lowest 90dpd and NPE ratios in Greece, combined with the highest cash coverage

Asset quality

Domestic forborne stock breakdown (€ bn)

Domestic 90dpd – NPE bridge (€ bn)

Cash

coverage

Cash

coverage

14% 48% 49% 25% 26%LLAs/

Gross loans

13.9

3.2 0.8 0.618.5

90dpd FNPE <30 FNPE 31-90 Other impaired NPEs

42%

94% 79%

109% 75.2% 74.1%

34%

51%

62%

23%

34.1% 34.1%

Mortgages Consumer SBL Corporate Total GRE Group

34%

83% 69%

66% 56.6% 55.9%

43%

58%

71%

38%45.3% 45.2%

Mortgages Consumer SBL Corporate Total GRE Group

FNPE<30 dpd

3.2

FNPE 31-90dpd

0.8

FNPE >90dpd

3.2

FPE 2.9

10.1

Collateral

coverage176% 8% 52% 53% 55%

SEE & other:

90dpd ratio: 34%

Coverage: 56%

SEE & other:

NPE ratio: 44%

Coverage: 43%

27 Corporate Presentation – December 2017

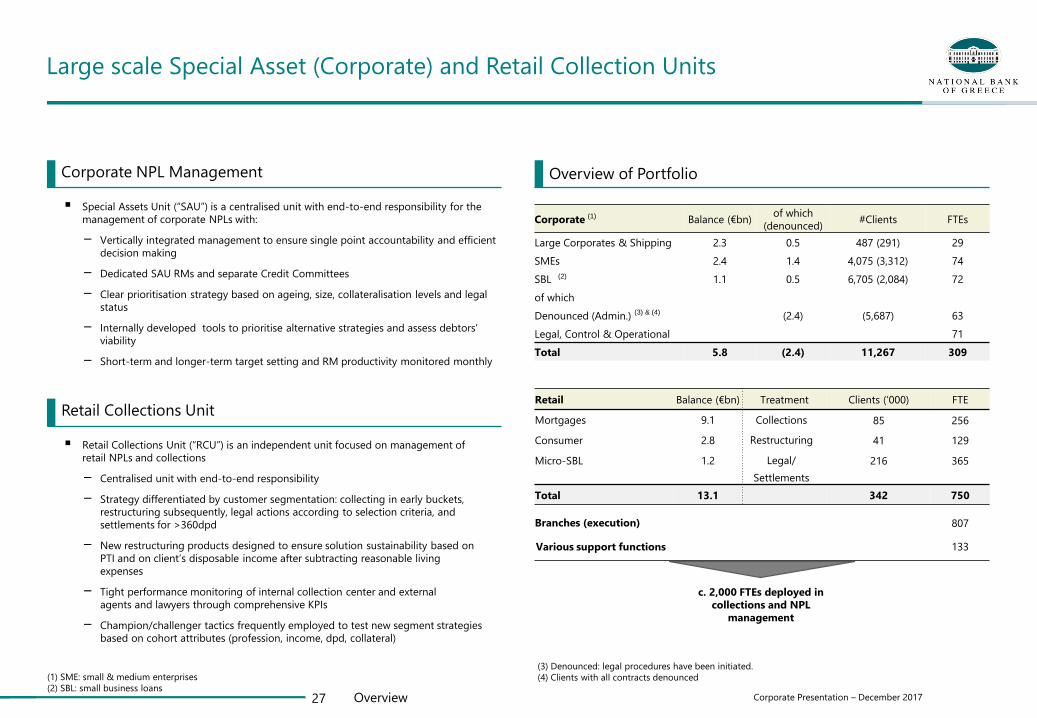

Large scale Special Asset (Corporate) and Retail Collection Units

Corporate NPL Management

Special Assets Unit (“SAU”) is a centralised unit with end-to-end responsibility for the

management of corporate NPLs with:

− Vertically integrated management to ensure single point accountability and efficient

decision making

− Dedicated SAU RMs and separate Credit Committees

− Clear prioritisation strategy based on ageing, size, collateralisation levels and legal

status

− Internally developed tools to prioritise alternative strategies and assess debtors’

viability

− Short-term and longer-term target setting and RM productivity monitored monthly

Overview of Portfolio

Retail Collections Unit

Retail Collections Unit (“RCU”) is an independent unit focused on management of

retail NPLs and collections

− Centralised unit with end-to-end responsibility

− Strategy differentiated by customer segmentation: collecting in early buckets,

restructuring subsequently, legal actions according to selection criteria, and

settlements for >360dpd

− New restructuring products designed to ensure solution sustainability based on

PTI and on client’s disposable income after subtracting reasonable living

expenses

− Tight performance monitoring of internal collection center and external

agents and lawyers through comprehensive KPIs

− Champion/challenger tactics frequently employed to test new segment strategies

based on cohort attributes (profession, income, dpd, collateral)

Retail Balance (€bn) Treatment Clients (‘000) FTE

Mortgages 9.1 Collections 85 256

Consumer 2.8 Restructuring 41 129

Micro-SBL 1.2 Legal/ 216 365

Settlements

Total 13.1 342 750

Branches (execution) 807

Various support functions 133

c. 2,000 FTEs deployed in

collections and NPL

management

(1) SME: small & medium enterprises

(2) SBL: small business loansOverview

Corporate Balance (€bn)of which

(denounced)#Clients FTEs

Large Corporates & Shipping 2.3 0.5 487 (291) 29

SMEs 2.4 1.4 4,075 (3,312) 74

SBL 1.1 0.5 6,705 (2,084) 72

of which

Denounced (Admin.) (2.4) (5,687) 63

Legal, Control & Operational 71

Total 5.8 (2.4) 11,267 309

(1)

(3) Denounced: legal procedures have been initiated.

(4) Clients with all contracts denounced

(3) & (4)

(2)

Liquidity

5

29 Corporate Presentation – December 2017Liquidity

17.6

1

3.2

3.3

2.25

1.969

2.291.3

1.1

0.7410.8

0.4 0.1 0.85

ELA June 2015 Divestment

Plan

Net Loans Net Intragroup

Funding

Net Interbank

Repos

(Corellated)

Net Deposits Net Bond

Redemptions

Waiver

Reinstatement

Net Cash Recapitalization Cash Collateral Other Covered Bond

Maturity

ELA October

2017

ELA reduction – Key items (all amounts in €bn and cash equivalents)

10.0 10.012.5 11.8

8.9 8.2 6.74.6 4.6 3.7

17.615.6 11.5

11.0

6.1 5.1

5.6

5.6 3.8

1

0.9

4.03.8 4.7

5.2

4.4

2.7

27.6

25.624 23.7

1917.1 17

15.4

12.8

7.4

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17

ECB

ELA

Interbank

Eurosystem and Interbank funding evolution (all amounts in €bn and cash equivalents)

Waiver

Reinstatement

Pillars

cancellation

Collateral

optimization Interbank funding

-4,0bn Eurosystem

exposure Sinepia

+0,3bn cash

Correlated assets

repos

-1,2bn Eurosystem

exposure

Jun-17Sep-15Jun-15

Increase of

correlated assets

repos

Oct-17

Total Eurosystem exposure reduced by c. €20b; ELA reduced by c. €16b; on the back of the

divestment plan, interbank access and deleveraging

30 Corporate Presentation – December 2017

Peer group analysis: liquidity position (Group)

1: Excl. EFSF & ESM bonds

2: Estimated based on latest available funding balances & yields

3: Peer average data excluding NBG, based on latest available data

Best in class liquidity and lowest cost of funding place NBG at an advantageous

position vs peers to satisfy demand for credit from healthy corporates

Liquidity

NBG domestic deposit flows per quarter (€ b)

-2.2

-4.8-3.6

0.3 0.8

-0.9

0.0 0.3 0.9

-0.8

0.2 0.5

4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

-€10.6 b +€1.3 b

Peer Group: Domestic funding cost2

0.47%0.56%

0.66% 0.63%

NBG Peer 1 Peer 2 Peer 3

91% 91% 89%86% 87% 85%

83%

141% 138%134%

130% 130% 128%124%

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

Peer domestic

L:D ratio3

NBG Greece

L/D ratio

provides

upside for

selective

credit

growth

Domestic L:D ratio evolution

1.0

6.07.3 7.5

NBG Peer 1 Peer 2 Peer 3

2% 12%12%9%ELA/

Assets1

Macro

6

32 Corporate Presentation – December 2017

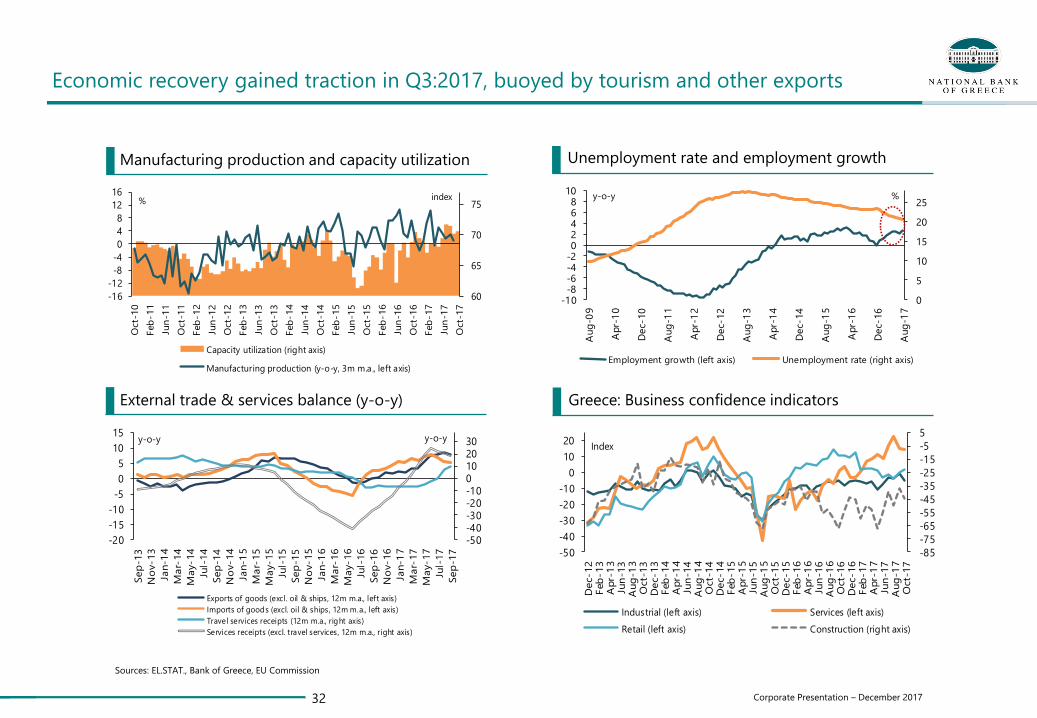

Sources: EL.STAT., Bank of Greece, EU Commission

60

65

70

75

-16

-12

-8

-4

0

4

8

12

16

Oct-

10

Feb

-11

Jun

-11

Oct-

11

Feb

-12

Jun

-12

Oct-

12

Feb

-13

Jun

-13

Oct-

13

Feb

-14

Jun

-14

Oct-

14

Feb

-15

Jun

-15

Oct-

15

Feb

-16

Jun

-16

Oct-

16

Feb

-17

Jun

-17

Oct-

17

Capacity utilization (right axis)

Manufacturing production (y-o-y, 3m m.a., left axis)

% index

-85

-75

-65

-55

-45

-35

-25

-15

-5

5

-50

-40

-30

-20

-10

0

10

20

Dec-12

Feb

-13

Apr-

13

Jun

-13

Aug

-13

Oct-

13

Dec-13

Feb

-14

Apr-

14

Jun

-14

Aug

-14

Oct-

14

Dec-14

Feb

-15

Apr-

15

Jun

-15

Aug

-15

Oct-

15

Dec-15

Feb

-16

Apr-

16

Jun

-16

Aug

-16

Oct-

16

Dec-16

Feb

-17

Apr-

17

Jun

-17

Aug

-17

Oct-

17

Industrial (left axis) Services (left axis)

Retail (left axis) Construction (right axis)

Index

Greece: Business confidence indicators

Economic recovery gained traction in Q3:2017, buoyed by tourism and other exports

External trade & services balance (y-o-y)

Unemployment rate and employment growth

0

5

10

15

20

25

-10-8-6-4-202468

10

Aug

-09

Apr-

10

Dec-

10

Aug

-11

Apr-

12

Dec-

12

Aug

-13

Apr-

14

Dec-

14

Aug

-15

Apr-

16

Dec-

16

Aug

-17

Employment growth (left axis) Unemployment rate (right axis)

%y-o-y

-50-40-30-20-100102030

-20

-15

-10

-5

0

5

10

15

Sep

-13

No

v-13

Jan-1

4

Mar-

14

May-14

Jul-

14

Sep

-14

No

v-14

Jan-1

5

Mar-

15

May-15

Jul-

15

Sep

-15

No

v-15

Jan-1

6

Mar-

16

May-16

Jul-

16

Sep

-16

No

v-16

Jan-1

7

Mar-

17

May-17

Jul-

17

Sep

-17

Exports of goods (excl. oil & ships, 12m m.a., left axis)

Imports of goods (excl. oil & ships, 12m m.a., left axis)

Travel services receipts (12m m.a., right axis)

Services receipts (excl. travel services, 12m m.a., right axis)

y-o-y y-o-y

Manufacturing production and capacity utilization

33 Corporate Presentation – December 2017

2

5

8

11

14

1000

1500

2000

2500

3000

3500

Jun

-15

Jul-

15

Aug

-15

Sep

-15

Oct-

15

No

v-15

Dec-15

Jan-1

6Feb

-16

Mar-

16

Apr-

16

May-16

Jun

-16

Jul-

16

Aug

-16

Sep

-16

Oct-

16

No

v-16

Dec-16

Jan-1

7Feb

-17

Mar-

17

Apr-

17

May-17

Jun

-17

Jul-

17

Aug

-17

Sep

-17

Oct-

17

No

v-17*

FTSE/ATHEX Large Cap (left axis)

10yr Greek Government bond yield (right axis)

Greek non-financial corp. bond yield (BoG Composite Index, right axis)

index %

*as of November 20, 2017

3rd

MoUCap

ital c

on

tro

ls

The fiscal performance remains solid and increasing credibility is gradually factoring into

financial market conditions

Greece: Gen. Gov. Primary balance (as % of GDP) State budget Primary balance (as % of GDP)

Greek Sovereign, corporate bond yields & stock market

-9

-6

-3

0

3

6

-9

-6

-3

0

3

6

Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep

Oct

Nov

Dec

2009 2010 2012 2013

2014* 2015* 2016* 2017*

% GDPsurplus

deficit

*excluding SMP &

ANFA revenue

4,6

4,8

5,0

5,2

5,4

5,6

5,8

6,0

2,2

2,6

3,0

3,4

3,8

4,2

4,6

25/9

/20

17

29/9

/20

17

3/1

0/2

01

7

7/1

0/2

01

7

11/1

0/2

017

15/1

0/2

017

19/1

0/2

017

23/1

0/2

017

27/1

0/2

017

31/1

0/2

017

4/1

1/2

01

7

8/1

1/2

01

7

12/1

1/2

017

16/1

1/2

017

20/1

1/2

017

5yr GGB (left axis) 2yr GGB (left axis)

6m T-bill (left axis) 10yr GGB (right axis)

%%

-16

-12

-8

-4

0

4

-16

-12

-8

-4

0

4

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7e

201

8f

Gen.Gov. total balance Gen.Gov. primary balance

Primary balance (Programme target) Primary balance (Budget 2018)

% GDP

Greek Sovereign bond yields

Sources: EL.STAT., Greek MinFin, Bloomberg, PDMA, EU Commission

34 Corporate Presentation – December 2017

Consumer confidence & household income

The economic recovery will be supported in the near term by higher public investment and an

improving corporate performance, but the adjustment of households and less competitive

firms remains slow. Residential and commercial real estate prices are stabilizing

Real estate prices (y-o-y)

Households assessment of economic conditions

-110

-90

-70

-50

-30

-10

-105-100

-95-90-85-80-75-70-65-60

Q3:2

007

Q1:2

008

Q3:2

008

Q1:2

009

Q3:2

009

Q1:2

010

Q3:2

010

Q1:2

011

Q3:2

011

Q1:2

012

Q3:2

012

Q1:2

013

Q3:2

013

Q1:2

014

Q3:2

014

Q1:2

015

Q3:2

015

Q1:2

016

Q3:2

016

Q1:2

017

Q3:2

017

Intention for home improvements (left axis)

Intention to purchase or build a home (left axis)

Financial situation over the next 12 months (right axis)

Index

IndexConsumer Survey data

-16

-12

-8

-4

0

4

-16

-12

-8

-4

0

4

H1

:200

9

H2

:200

9

H1

:201

0

H2

:201

0

H1

:201

1

H2

:201

1

H1

:201

2

H2

:201

2

H1

:201

3

H2

:201

3

H1

:201

4

H2

:201

4

H1

:201

5

H2

:201

5

H1

:201

6

H2

:201

6

H1

:201

7

Q3:2

017

Office prices (Athens, y-o-y) Retail prices (Athens, y-o-y)

House prices (total, y-o-y)

y-o-y

2017Q3: -0.6% yoy

0,0

0,5

1,0

1,5

2,0

2,5

3,0

Q2:2

016

Q3:2

016

Q4:2

016

Q1:2

017

Q2:2

017

Q3:2

017

Q4:2

017

Payments for arrears clearance (incl. tax refunds, % GDP)

Public investment budget expenditure (% GDP)

as % of GDP

-75

-70

-65

-60

-55

-50

-45

-40

-10

-8

-6

-4

-2

0

2

4

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7e*

Household disposable income (left axis)

Consumer confidence (total, right axis)

y-o-y index

*2017: Ameco & NBG estimates

Oct: -54

Sources: EL.STAT., Greek MinFin, EU Commission, Bank of Greece, Ameco & NBG estimates

Government arrears clearance and public investment

Appendix I

7

36 Corporate Presentation – December 2017

Capital controls framework

• 100% of cash deposited after 22.07.16 can be withdrawn

• €840 equivalent per fortnight per customer (applicable up to

31.08.2017)

• €1.800 equivalent per month per customer (applicable from

1.09.2017)

• Allowed for existing (as of 11.03.16) customers

• Subject to specific criteria, e.g. primary payroll account, for new

customers

• Private individuals can transfer up to €1,000 per month

• Allowed

• Allowed

• Allowed

• Proceeds can be re-invested

• Prohibited when changing to foreign custodian

• Allowed

• < €350k approval at bank level

• Weekly limit for bank-level committee at €112mn

• > €350k approval by the Banking Transactions Approval

Committee

Cash

withdrawal

limit

New account

opening

• Allowed for existing (as of 11.03.16) customers

• Prohibited for new customers

Additional

account

beneficiary

• 100% of incoming funds can be re-transferred abroad

• 10% of incoming funds received before 22.07.16 can be withdrawn

• 30% of incoming funds received between 22.07.16 and 31.08.17

can be withdrawn

• 50% of incoming funds received after 01.09.2017 can be withdrawn

Transfers from

abroad

Outgoing wire

transfers

abroad

Time deposit

break

Purchase of

Greek mutual

funds

Greek capital

market

instruments

Foreign

investments

liquidation

Change of

Custodian Bank

Trade related

payments

Early loan

repayment

Appendix I

37 Corporate Presentation – December 2017

Evolution of RWAs (€ b)

Overview

RWA Evolution | Asset-liability mix

Asset mix (€ b) Liability mix (€ b)

Other,

13.5

DTA, 4.9

SEE & Other net

loans, 2.0

Domestic net

loans; 30.3

EFSF/ESM

bonds; 2.0

Securities;

10.1

Interbank

placements; 1.9Cash; 1.2

65.8

Assets

Total equity and

minorities; 6.8

Other Liabilities;

10.0

Debt securities;

0.5

SEE & Other

deposits; 2.1

Time & Other;

11.1

Current & Sight;

7.5

Savings; 18.1

ELA, 2.3ECB, 3.8

Interbank liabilities,

3.8

65.8

Liabilities

Domestic

deposits 36.0

61.8

-20.7

41.1

-2.6

38.5

-5.0

RWAs

2015

RWAs

2016

RWAs

9M17

Planned

Divestments

38 Corporate Presentation – December 2017

NBG is the first bank that has repaid State aid

Source: Latest company filings

Outstanding Outstanding Outstanding Outstanding

Pillar I (State Preference Shares)

Pillar II

(State Guaranteed Bonds)

Pillar III

(Greek Government Bonds)

CoCos not issued not issued

: outstanding

: repaid

Appendix I

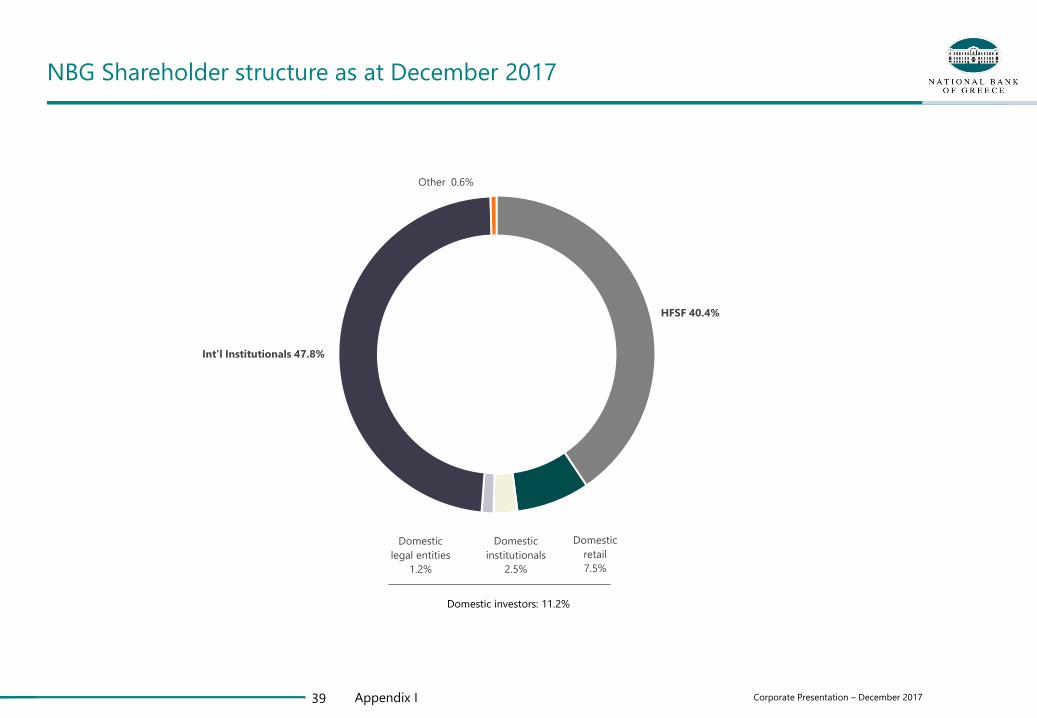

39 Corporate Presentation – December 2017Appendix I

NBG Shareholder structure as at December 2017

HFSF 40.4%

Domestic

retail

7.5%

Domestic

institutionals

2.5%

Domestic

legal entities

1.2%

Int'l Institutionals 47.8%

Other 0.6%

Domestic investors: 11.2%

Appendix II: Financials

41 Corporate Presentation – December 2017

Balance Sheet | Group

Group Balance Sheet & P&L

P&L | Group

€ m 3Q17 2Q17 1Q17 4Q16 3Q16

Cash & Reserves 1 208 1 231 1 218 1 182 1 187

Interbank placements 1 886 2 032 1 975 2 087 2 554

Securities 12 043 15 369 16 679 18 530 19 921

Loans (Gross) 43 174 43 749 44 482 45 046 45 837

Provisions (10 900) (10 968) (11 176) (11 301) (11 867)

Goodwill & intangibles 123 123 115 117 113

Tangible assets 1 076 1 085 1 114 1 111 1 107

DTA 4 917 4 917 4 918 4 918 4 917

Other assets 6 506 6 654 6 772 7 458 8 305

Assets held for sale 5 810 5 681 9 459 9 382 9 669

Total assets 65 843 69 873 75 557 78 531 81 742

Interbank liabilities 9 855 13 945 16 522 18 167 17 753

Due to customers 38 795 38 324 38 132 38 924 38 071

Debt securities 461 523 550 663 1 508

Other liabilities 5 182 5 564 5 862 6 322 7 746

Hybrids - - - - -

Liabilities held for sale 4 122 4 095 6 889 6 870 6 857

Minorities 669 660 689 680 708

Equity 6 757 6 762 6 913 6 909 9 099

Total liabilities and

equity65 843 69 873 75 557 78 531 81 742

Appendix

€ m 3Q17 2Q17 1Q17 4Q16 3Q16

NII 378 405 410 406 417

Net fees 57 59 60 56 51

Core Income 435 464 470 462 468

Trading & other income1 (81) (73) (1) 104 (27)

Income 354 391 469 566 441

Operating Expenses (238) (232) (231) (255) (257)

Core Pre-Provision Income 196 232 239 208 211

Pre-Provision Income 116 159 238 311 184

Provisions (156) (200) (233) (210) (161)

Operating Profit (40) (41) 5 101 23

Other impairments 2 (1) (6) (28) (15)

PBT (38) (42) (1) 74 8

Taxes (6) (10) (7) (9) (6)

PAT (cont. ops) (44) (52) (8) 65 2

PAT (discount. ops) 19 (97) 30 7 21

Minorities (10) (7) (9) 1 (7)

PAT (35) (156) 13 73 16

1. 4Q16 includes €150m gain from the sale of Astir Pallas,

42 Corporate Presentation – December 2017

Greece

Regional P&L: Greece, SEE & other

Appendix

SEE & Other

€ m 3Q17 2Q17 1Q17 4Q16 3Q16

NII 352 379 384 383 389

Net fees 51 53 54 50 45

Core Income 403 432 439 433 434

Trading & other income1 (81) (71) (1) 99 (27)

Income 322 361 438 532 407

Operating Expenses (217) (213) (210) (235) (237)

Core Pre-Provision Income 185 220 228 198 198

Pre-Provision Income 104 149 228 297 171

Provisions (151) (199) (232) (200) (162)

Operating Profit (47) (51) (4) 96 9

Other impairments 3 0 (6) (27) (15)

PBT (44) (50) (10) 70 (6)

Taxes (5) (8) (5) (7) (4)

PAT (cont. ops) (49) (58) (15) 62 (10)

PAT (discount. ops) 18 22 12 14 4

Minorities (10) (7) (9) 2 (7)

PAT (40) (43) 12 77 12

€ m 3Q17 2Q17 1Q17 4Q16 3Q16

NII 26 26 26 23 28

Net fees 6 6 6 6 6

Core Income 32 32 32 30 34

Trading & other income (0) (2) (1) 5 0

Income 32 30 31 35 34

Operating Expenses (21) (19) (21) (20) (21)

Core Pre-Provision Income 11 12 11 10 13

Pre-Provision Income 11 10 10 15 13

Provisions (5) (1) (1) (10) 1

Operating Profit 6 9 9 5 14

Other impairments (0) (1) (0) (1) -

PBT 6 9 9 4 14

Taxes (1) (2) (2) (1) (2)

PAT (cont. ops) 5 6 7 3 12

1. 4Q16 includes €150m gain from the sale of Astir Pallas,.

43 Corporate Presentation – December 2017

Name Abbreviation Definition

Common Equity / Book Value BVEquity attributable to NBG shareholders less minorities (non-controlling interests) and contingent convertible

securities (CoCos)

Common Equity Tier 1 Ratio CET1 ratio CET1 capital, as defined by Regulation No 575/2013 and based on the transitional rules over RWAs

Common Equity Tier 1 Ratio Fully

LoadedCET1 ratio, CRD IV FL CET1 capital as defined by Regulation No 575/2013, without the application of the transitional rules over RWAs

Core Income CI Net Interest Income (“NII”) + Net fee and commission income + Earned premia net of claims and commissions

Core Operating Result (Profit / (Loss)) - Core income less operating expenses and provisions (credit provisions and other impairment charges)

Core Operating Margin - Core operating profit / (loss) annualized over average net loans

Core Pre-Provision Income Core PPI Core Income less operating expenses, before provisions (credit provisions and other impairment charges)

Core Pre-Provision Margin Core PPI margin Core PPI annualized over average net loans

Cost of Risk / Provisioning Rate CoR Credit provisions of the period annualized over average net loans

Cost-to-Core Income Ratio C:CI Operating expenses over core Income

Cost-to-Income Ratio C:I Operating expenses over total income

Deposit Yields - Annualized interest expense on deposits over deposit balances

Forborne -Exposures for which forbearance measures have been extended according to EBA ITS technical standards on

Forbearance and Non-Performing Exposures

Forborne Non-Performing Exposures FNPEsExposures with forbearance measures that meet the criteria to be considered as non performing according to EBA

ITS technical standards on Forbearance and Non-Performing Exposures

Forborne Performing Exposures FPEs

Exposures with forbearance measures that do not meet the criteria to be considered as non performing according

to EBA ITS technical standards on Forbearance and Non-Performing Exposures and forborne exposures under

probation period

Funding cost - The blended cost of deposits, ECB refinancing, repo transactions and ELA funding

Gross Loans -Loans and advances to customers before allowance for impairment, excluding the loan to the Greek State of

€6.0bn

Loan Yield - Annualized loan interest income over gross performing loan balances

Loans-to-Deposits Ratio L:D Net loans over total deposits, period end

Definition of financial data & ratios used

44 Corporate Presentation – December 2017

Name Abbreviation DefinitionNet Interest Margin NIM NII annualized over average interest earning assets

Net Loans - Loans and advances to customers, excluding the loan to the Greek State of €6.0bn

Net Profit / (Loss) - Profit / (loss) for the period attributable to NBG equity shareholders

Non-Performing Exposures NPEs

Non-performing exposures are defined according to EBA ITS technical standards on Forbearance and Non-

Performing Exposures as exposures that satisfy either or both of the following criteria:

a) Material exposures which are more than 90 days past due

b) The debtor is assessed as unlikely to pay its credit obligations in full without realization of collateral, regardless

of the existence of any past due amount or of the number of days past due.

Non-Performing Exposures Coverage Ratio NPE coverage Stock of provisions (allowance for impairment for loans and advances to customers) over non-performing

exposures, period end

Non-Performing Exposures Ratio NPE ratio Non-performing exposures over gross loans, period end

Non-Performing Loans NPLs Loans and advances to customers in arrears for 90 days or more

90 Days Past Due Coverage Ratio 90dpd coverage Stock of provisions over loans and advances to customers in arrears for 90 days or more, period end

90 Days Past Due Formation 90dpd formationNet increase / (decrease) of loans and advances to customers in arrears for 90 days or more, before write-offs and

after restructurings

90 Days Past Due Ratio 90dpd ratio Loans and advances to customers in arrears for 90 days or more over gross loans, period end

Operating Expenses OpEx, costsPersonnel expenses + General, administrative and other operating expenses (“G&As”) + Depreciation and

amortisation on investment property, property & equipment and software & other intangible assets

Operating Profit / (Loss) - Total income less operating expenses and provisions (credit provisions and other impairment charges)

Pre-Provision Income PPI Total income less operating expenses, before provisions (credit provisions and other impairment charges)

Profit / (loss) after tax PAT (cont. ops) Profit / (loss) for the period from continuing operations

Risk Weighted Assets RWAsAssets and off-balance-sheet exposures, weighted according to risk factors based on Regulation (EU) No

575/2013

Tangible Equity / Book Value TBV Common equity less goodwill & intangibles (goodwill, software and other intangible assets)

Total deposits - Due to customers

Definition of financial data & ratios used

This presentation is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy. No part of

this presentation may be construed as constituting investment advice or recommendation to enter into any transaction. No representation or warranty is given with

respect to the accuracy or completeness of the information contained in this presentation, and no claim is made that any future to transact any securities will

conform to any terms that may be contained herein. Before entering into any transaction, investors should determine any economic risks and benefits, as well as

any legal, tax, accounting consequences of doing so, as well as their ability to assume such risks, without reliance on the information contained in this presentation.