Debt Investments in Competitors under the Federal ...

33

Fordham Journal of Corporate & Financial Law Fordham Journal of Corporate & Financial Law Volume 9 Issue 3 Article 2 2004 Debt Investments in Competitors under the Federal Antitrust Laws Debt Investments in Competitors under the Federal Antitrust Laws Hanno F. Kaiser Follow this and additional works at: https://ir.lawnet.fordham.edu/jcfl Part of the Banking and Finance Law Commons, and the Business Organizations Law Commons Recommended Citation Recommended Citation Hanno F. Kaiser, Debt Investments in Competitors under the Federal Antitrust Laws, 9 Fordham J. Corp. & Fin. L. 605 (2004). Available at: https://ir.lawnet.fordham.edu/jcfl/vol9/iss3/2 This Article is brought to you for free and open access by FLASH: The Fordham Law Archive of Scholarship and History. It has been accepted for inclusion in Fordham Journal of Corporate & Financial Law by an authorized editor of FLASH: The Fordham Law Archive of Scholarship and History. For more information, please contact [email protected].

Transcript of Debt Investments in Competitors under the Federal ...

Fordham Journal of Corporate & Financial Law Fordham Journal of Corporate & Financial Law

Volume 9 Issue 3 Article 2

2004

Debt Investments in Competitors under the Federal Antitrust Laws Debt Investments in Competitors under the Federal Antitrust Laws

Hanno F. Kaiser

Follow this and additional works at: https://ir.lawnet.fordham.edu/jcfl

Part of the Banking and Finance Law Commons, and the Business Organizations Law Commons

Recommended Citation Recommended Citation Hanno F. Kaiser, Debt Investments in Competitors under the Federal Antitrust Laws, 9 Fordham J. Corp. & Fin. L. 605 (2004). Available at: https://ir.lawnet.fordham.edu/jcfl/vol9/iss3/2

This Article is brought to you for free and open access by FLASH: The Fordham Law Archive of Scholarship and History. It has been accepted for inclusion in Fordham Journal of Corporate & Financial Law by an authorized editor of FLASH: The Fordham Law Archive of Scholarship and History. For more information, please contact [email protected].

ARTICLES

DEBT INVESTMENTS IN COMPETITORS UNDERTHE FEDERAL ANTITRUST LAWS

Hanno F. Kaiser*

INTRODUCTION

When a firm extends credit to a competitor, or a bank or aninvestment fund holds debt in two or more competing firms, thequestion arises whether these investments are likely to substantiallylessen competition or unreasonably restrain trade. Conceivably, thelender could exploit its contractual position to exercise control over theborrower and/or to gain access to the borrower's confidentialinformation. In addition, holding a financial interest in the debtor mightcreate an incentive for the creditor to unilaterally raise prices followingthe investment or enable the creditor, the debtor, and other firms in theindustry to engage in coordinated interaction that harms consumers.

This Article examines whether debt investments are, in fact, likelyto produce meaningful anticompetitive effects of that nature.' Takingcomparable minority equity investments as a benchmark, the answer ismostly negative. Unlike partial ownership, debt investments do notsignificantly reduce the investor's incentives to compete and are largely

"Associate, Latham & Watkins LLP, New York. The views expressed in this article arethose of the author and do not purport to reflect the views of Latham & Watkins LLP.The author can be reached at: [email protected]. The author would like to thank BrucePrager, Su Sun, and David Barnes for their helpful comments.

I. Surprisingly, there is very little case law, agency practice, or legal scholarshipaddressing the competitive effects of debt investments as such. If debt investments arediscussed at all, they usually appear as an afterthought to the analysis of partialownership.

606 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LAW

ineffectual as commitment devices. With respect to corporate controland information exchange, the answer depends on the financialcondition of the target. As long as the borrower is solvent (and, as aconsequence, has viable refinancing options), the creditor's influencewill generally not be meaningful. However, once the creditor canaccelerate the loan and thereby cause the borrower's bankruptcy, thecreditor's de facto influence over the target increases significantly andmay even exceed the influence conferred by comparable equityinvestments (unless the creditor eliminates competitive concerns bymaking its debt investment passive). Based on these findings, thisArticle recommends deferential treatment of most debt investments incompetitors under the federal antitrust laws. Unless the investment hascertain clearly defined features that permit an inference of probablecompetitive harm and the creditor refuses to eliminate such concerns,debt investments are presumably efficient.

The discussion below is organized as follows: Part I outlines aframework of analysis that has successfully been applied to equityinvestments. Part II extends the equity framework to the competitiveanalysis of debt investments, with a special focus on the use of debt as acommitment device to enable collusion. Part III discusses the treatmentof debt investments by the courts. Part IV summarizes the key findingsand concludes with policy recommendations.

I. COMPETITIVE EFFECTS OF PARTIAL OWNERSHIP

In a typical minority investment case, company A acquires a non-controlling equity stake in its competitor, company B. That acquisitionmay be challenged under §7 of the Clayton Act ("§7"), which applies tothe acquisition of any part of the stock or the assets of a company.3 In

2. The terms "minority equity investment," "equity investment," and "partialownership" are used interchangeably, as are "creditor," "lender," and "debt investor"and "debtor," "borrower," and "target."

3. 15 U.S.C. § 18 (2004). Section 7 applies to partial ownership even if theacquirer does not obtain control over the target. See, e.g., Denver & Rio Grande W.RR. Co. v. U.S., 387 U.S. 485, 501 (1967) ("A company need not acquire control ofanother company in order to violate [§7]."); U.S. v. E.I. du Pont de Nemours & Co.,353 U.S. 586, 592 (1957) ("[A]ny acquisition of all or any part of the stock of anothercorporation, competitor or not, is within the reach of [§7] whenever the reasonablelikelihood appears that the acquisition will result in a restraint of commerce or in the

2004] DEBT INVESTMENTS & FEDERAL ANTITRUSTLA W 607

assessing whether the acquisition is likely to substantially lessencompetition, courts and agencies have focused on the target,specifically, whether post-acquisition, A would be able to exercisecontrol over B's competitive decisions; and/or whether A would gainaccess to B's confidential business information.4 Only recently has therebeen an increased emphasis on how investments in a competitor mightchange the competitive behavior of the investor.5

creation of a monopoly of any line of commerce."). Challenges under §7 havefrequently been accompanied by claims of violations of § § 1-2 of the Sherman Act, 15U.S.C. §§ 1, 2 (2004) [hereinafter §§1, 2]. This Article does not focus on monopolization

offenses involving debt.4. See, e.g., du Pont, 353 U.S. at 602-03, 607 (stating that 23% stock acquisition

violates §7 where acquirer had gained influence over the target, a customer, and was

receiving information from the target); F. & M. Schaefer Corp. v. C. Schmidt & Sons,Inc., 597 F.2d 814, 818 (2d. Cir. 1979) (stating that acquisition of 29% of competitor's

stock violates §7 as acquirer would have obtained power to designate directors, gainedaccess to sensitive information, and discouraged the target's management); Briggs Mfg.

Co. v. Crane Co., 185 F. Supp. 177, 180-82, 184 (E.D. Mich. 1960) (stating that §7includes within its scope a percentage interest sufficient to elect nominees to the board

of directors who could influence the competitive decisions of the target and divulgeinformation to the acquirer); Am. Crystal Sugar Co. v. Cuban-Am. Sugar Co., 259 F.2d524, 526, 531 (2d Cir. 1958) (stating that 23% stock acquisition violates §7 where

acquirer was seeking to control the target); Hamilton Watch Co. v. Benrus Watch Co.,

114 F. Supp. 307, 313, 317 (D.Conn. 1953), aff'd, 206 F.2d 738 (2d Cir. 1953) (stating

that acquisition of 24% of competitor's stock with the intent to obtain boardrepresentation violates §7). Numerous agency challenges have focused on the corporatecontrol and information exchange aspects of partial ownership. See, e.g., U.S. v. AT&T

Corp., Proposed Final Judgment and Competitive Impact Statement, 65 Fed. Reg. 38,584 (D.O.J. June 21, 2000); U.S. v. The Gillette Co., 1990 WL 126485 (D.D.C. July 25,1990) [hereinafter Gillette I]; U.S. v. The Gillette Co., Proposed Final Judgment and

Competitive Impact Statement, 55 Fed. Reg. 12,567 (D.O.J. Apr. 4, 1990); U.S. v. TheGillette Co., Public Comments and Response, 55 Fed. Reg. 28,312 (D.O.J. July 10,1990) [hereinafter Gillette /]; U.S. v. Rockwell Int'l Corp., Proposed Final Judgment

and Competitive Impact Statement, 45 Fed. Reg. 69,314 (D.O.J. Apr. 4, 1980);Medtronic, Inc., Analysis to Aid Public Comment, 63 Fed. Reg. 53,919 (F.T.C. Oct. 7,1998); Shell Oil Co., Texaco Inc., Analysis to Aid Public Comment, 62 Fed. Reg.

67,868 (F.T.C. Dec. 30, 1997); Time Warner, Inc., Proposed Consent Agreement with

Analysis to Aid Public Comment, 61 Fed. Reg. 50,301 (F.T.C. Sept. 25, 1996).5. The following consent orders have focused on changes in the financial

incentives of the investor. U.S. v. AT&T Corp., Proposed Final Judgment and

Competitive Impact Statement, 64 Fed. Reg. 2506 (D.O.J. Jan. 14, 1999); U.S. v. USWest, Inc., Proposed Final Judgment and Competitive Impact Statement, 61 Fed. Reg.

58,703 (D.O.J. Nov. 18, 1996); In the Matter of Golden Grain Macaroni Co., 78 F.T.C.

608 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LAW

A. Effects on the Target

The theories of anticompetitive harm from acquiring corporatecontrol and information access are straightforward. As a shareholder, Acan sabotage the target through strategic voting at the shareholdermeetings, designation of hostile directors, shareholder lawsuits (the costsof which would be borne mainly by the other shareholders), abusiveinformation requests, etc.6 The significance of A's influence depends,among other things, on the size of its stake in B in absolute terms andrelative to the other shareholders; the concentration of the market; andwhether B is a private or a public company. As a practical matter,passive investments of less than 15% have rarely been challenged incourt, whereas shareholdings sufficient to designate at least one directorhave been subject to intense litigation under both the federal antitrustlaws and state corporation laws. The shareholder/director threshold notonly is of obvious importance for the exercise of corporate control butalso changes the nature of the investor's access to sensitive informationof the target.

A shareholder has a common law right, based on its beneficialownership of corporate assets, to inspect "the books of his corporation at

63 (1971), modified in other respects, 472 F.2d 882 (9th Cir. 1972). For acomprehensive analysis of the unilateral effects of partial ownership, see Daniel P.O'Brien & Steven C. Salop, Competitive Effects of Partial Ownership: FinancialInterest and Corporate Control, 67 ANTITRUST L.J. 559 (2000) [hereinafter O'Brien &Salop, Competitive Effects]; Jon B. Dubrow, Challenging the Economic IncentivesAnalysis of Competitive Effects in Acquisitions of Passive Minority Equity Interests, 69ANTITRUST L.J. 113 (2001); Daniel P. O'Brien & Steven C. Salop, The CompetitiveEffects of Passive Minority Equity Interests: Reply, 69 ANTITRUST L.J. 611 (2001)[hereinafter O'Brien & Salop, Competitive Effects: Reply]; David Reitman, PartialOwnership Arrangements and the Potential for Collusion, 42 J. INDUS. ECON. 313(1994); Wilson A. Alley, Partial Ownership Arrangements and Collusion in theAutomobile Industry, 45 J. INDUS. ECoN.191 (1997). For a discussion of thecoordinated effects of passive equity investments among competitors, see David Gilo,The Anticompetitive Effect of Passive Investment, 99 MICH. L. REv. 1, 2-3 (2000).

6. O'Brien & Salop, Competitive Effects: Reply, supra note 5, at 613.Alternatively, A could use its inside position to organize a cartel. Cross investments areparticularly useful as facilitating devices. Where the creditor has significant marketpower, abusive conduct may constitute (attempted) monopolization in violation of §2.

7. The shareholder/director distinction is also reflected in §8 of the Clayton Act,15 U.S.C. § 19 (2004), prohibiting simultaneous service as a director or officer ofcompeting companies.

2004] DEBT INVESTMENTS & FEDERAL ANTITRUST LAW

a proper time and place and for a proper purpose."' The scope of theshareholder's inspection right is broad and encompasses the list ofshareholders, board minutes, financial records, sales journals, invoices,contracts, correspondence, sales projections and business plans.9 Themain qualification of the right to access is the good faith or properpurpose requirement, pursuant to which the company may deny arequest for access if the shareholder's purposes are either unrelated to itsinterest as an investor or inimical to the corporation. Among theimproper purposes are harassment, blackmail, and the aid of acompetitor.'0 With respect to the latter, the mere fact that a shareholderis a competitor (or a shareholder of a competitor) does not defeat theright to information access," even though it may limit the scope of, orrequire the imposition of conditions upon, the inspection. 2 Only wherethe shareholder's primary purpose is to obtain competitively sensitiveinformation to harm the corporation and to aid a competitor may thecompany deny access to its books and records. 13 The shareholder mayenforce its information right through the state courts (traditionally by

8. Lau v. DSI Enter., Inc., 477 N.Y.S.2d. 151 (N.Y. App. Div. 1984). Most statesalso provide the shareholder with statutory inspection rights. The shareholder mayinspect the books in person and with the help of his or her agents. JAMES D. Cox ET AL.,ON CORPORATIONS § 13.05 (2d. Ed. 2003).

9. Meyer v. Ford Industries, Inc., 538 P.2d 353 (Or. 1975); Kortfim v. WebastoSunroofs, Inc., 769 A.2d 113, 117 n.8 (Del. Ch. 2000). To ensure the company'sinterest in protecting highly sensitive information (e.g., trade secrets), courts have beenwilling to grant limited protective orders excluding specific items from review andplacing narrowly tailored non-disclosure obligations on the shareholder. Id. at 13.

10. For an overview of proper and improper purposes, see COX, supra note 8, at§ 13.03. Once the shareholder seeks to enforce his or her right in court, the burden ofshowing improper motives generally falls upon the corporation. Crane Co. v. AnacondaCo., 382 N.Y.S.2d 707, 711 (N.Y. 1976); Indianapolis Street Railway Company v.Cohen, 181 N.E. 365, 368 (Ind. 1932).

11. Skoglund v. Ormand Indus., Inc., 372 A.2d 204, 212 (Del. Ch. 1976) ("[If]misuse of the information obtained threatens harm to the corporation, it has a remedy inthe courts in an appropriate action.").

12. Kortim, 769 A.2d at 11.13. If the disclosure of sensitive information is incidental to an otherwise proper

purpose, the request for information must be granted. Skoglund, 372 A.2d at 207 ("If aproper purpose is established, it is no defense that the stockholder may also haveanother, or secondary purpose, which may be improper.").

609

610 FORDHAMJOURATAL OF CORPORATE & [Vol. IXFINANCIAL LA W

writ of mandamus) if the corporation refuses to comply with a properdemand for access. 14

A director's right to inspect the corporate books and records is moreextensive than that of a shareholder, because it is a corollary to thedirector's fiduciary duties. 5 Without access to information, the directorcannot manage the company.16 The scope of the director's informationright is all encompassing; every company record that is reasonablyrelated to the director's position is at the director's disposal. 7 Unlikethe shareholder's inspection right, which is qualified by the properpurpose requirement, the director's right has been described as absolute,unqualified,' 8 and (by a majority of the courts) without regard tomotive.19 Thus, even a hostile director is entitled to receive what theother directors are given, because "[t]he duty to manage the corporationrests alike upon each and every one of the directors. 'z Of course, theshareholders may remove a director from the board. Until then,however, courts have held that the company's remedies against misuseof information are generally ex post -

14. Carter v. Wilson Constr. Co., Inc., 348 S.E.2d 830 (N.C. 1986); Cox, supranote 8, at § 13.08.

15. Henshaw v. Am. Cement Corp., 252 A.2d 125, 128-29 (Del Ch. 1969); Moorev. State Bank of Hallsville, 561 S.W.2d 722, 724-25 (Mo. App. 1978); Cox, supra note8, at§ 13.11.

16. Machen v. Machen & Mayer Elec. Mfg. Co., 85 A. 100, 102 (Pa. 1912) ("It isthe duty of directors to manage the affairs of the corporation... and for that purposethey should secure all information affecting the corporation from every availablesource... [including] the books and documents of the corporation itself.").

17. Kortim, 769 A.2d at 118; Machen, 85 A. 100at 104.18. Machen, 85 A. 100 at 104 ("The right of a director to inspect the books ... is

unqualified .... The protection of the interests of the company.., require that [adirector's] right to an inspection of the books be absolute."); See also Moore, 561S.W.2d at 725; Lau v. DSI Enterprises, Inc., 477 N.Y.S.2d. 151 (N.Y. App. Div. 1984).

19. Pilat v. Broach Sys., Inc., 260 A.2d 13, 17 (N.J. Super. Ct. Law Div. 1969) ("Ashowing of hostile intent ... will not affect a director's right of inspection."); Dusel v.Castellani, 350 N.Y.S.2d 258 (1973); Davis v. Keilson Offset Co. Inc., 79 N.Y.S.2d540, 542 (1948). For an inspection right qualified by the absence of a hostile purpose,see Paschall v. Scott, 247 P.2d 543, 548-49 (1952); Hemingway v. Hemingway, 19 A.766 (1890).

20. Machen, 237 Pa. at 218.21. Dusel, 350 N.Y.S.2d at 258; Moore, 561 S.W.2d. at 725. See also Kortiim, 769

A.2d at 124 (holding that the director's "inspection rights shall be unrestricted, except

2004] DEBT INVESTMENTS & FEDERAL ANTITRUSTLAW 611

Consequently, with respect to corporate information, a director is aninsider with real-time access to company contracts, customerinformation, business plans, and records circulated among the boardmembers. A shareholder, in contrast, relies on company disclosuresmade voluntarily or compelled through the courts. Given thatcompetitively sensitive information tends to expire quickly, delay isoften as effective as denial.22 A minority equity stake that does notentitle its holder to designate at least one director is therefore generallynot sufficient to provide an investor with a meaningful listening line intothe strategic decision making process of the target.

B. Effects on the Investor

Partial ownership, even if it is a purely passive minority interest, islikely to adversely impact the competitive incentives of the investor-

23competitor. Those effects may be classified as either unilateral orcoordinated.

Unilateral theories of competitive harm assume that the investor (A)and the target (B) are not attempting to collude and make theircompetitive decisions independently of one another.24 Even if A'sinvestment in B does not confer any control or information rights, A willtake into account the effect of its decisions on B in order to maximizethe sum of its own profits plus the return on its investment in B.Consider the following example:

for the... restriction that no information derived from the inspection will be sharedwith" a competing subsidiary).

22. That is true for most price information and contract terms. However, tradesecrets, information about marginal cost, and long term contracts are examples ofcompetitively relevant information that is less time sensitive.

23. O'Brien & Salop, Competitive Effects, supra note 5, at 571-73, 575-76;O'Brien & Salop, Competitive Effects: Reply, supra note 5, at 613; Gilo, supra note 5,at 8-9. In this context, competitive effects "arise solely because [partial ownership]arrangements link the fortunes of actual or potential competitors, producing a positivecorrelation among their profits." HERBERT HOvENKAMP, FEDERAL ANTITRUST POLICY:

THE LAW OF COMPETITION AND ITS PRACTICE 548 (2nd Ed. 1999); see also R.J.Reynolds & B.R. Snapp, The Competitive Effects of Partial Equity Interests and JointVentures, 4 INT'L J. INDUS. ORG. 141, 142 (1986); but see Dubrow, supra note 5, at131-37 (being critical of the overly abstract nature of the underlying model).

24. O'Brien & Salop, Competitive Effects, supra note 5, at 568-69.

612 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LAW

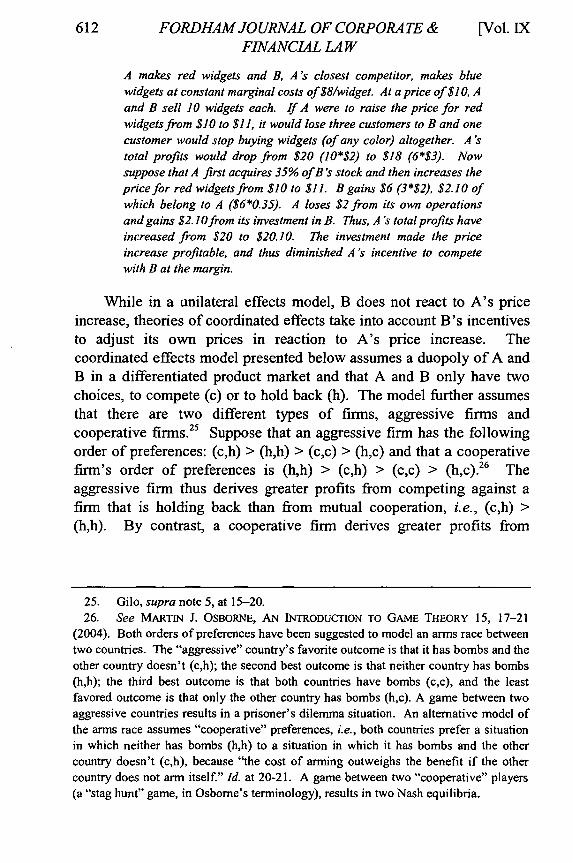

A makes red widgets and B, A 's closest competitor, makes bluewidgets at constant marginal costs of $8/widget. At a price of $10, A

and B sell 10 widgets each. If A were to raise the price for redwidgets from $10 to $11, it would lose three customers to B and onecustomer would stop buying widgets (of any color) altogether. A 's

total profits would drop from $20 (10*$2) to $18 (6*$3). Nowsuppose that A first acquires 35% of B's stock and then increases theprice for red widgets from $10 to $11. B gains $6 (3*$2), $2.10 ofwhich belong to A ($6*0.35). A loses $2 from its own operationsand gains $2. 10from its investment in B. Thus, A's total profits haveincreased from $20 to $20.10. The investment made the priceincrease profitable, and thus diminished A's incentive to competewith B at the margin.

While in a unilateral effects model, B does not react to A's priceincrease, theories of coordinated effects take into account B's incentivesto adjust its own prices in reaction to A's price increase. Thecoordinated effects model presented below assumes a duopoly of A andB in a differentiated product market and that A and B only have twochoices, to compete (c) or to hold back (h). The model further assumesthat there are two different types of firms, aggressive firms andcooperative firms. Suppose that an aggressive firm has the followingorder of preferences: (c,h) > (h,h) > (c,c) > (h,c) and that a cooperativefirm's order of preferences is (h,h) > (c,h) > (c,c) > (h,c). 6 Theaggressive firm thus derives greater profits from competing against afirm that is holding back than from mutual cooperation, i.e., (c,h) >(h,h). By contrast, a cooperative firm derives greater profits from

25. Gilo, supra note 5, at 15-20.26. See MARTIN J. OSBORNE, AN INTRODUCTION TO GAME THEORY 15, 17-21

(2004). Both orders of preferences have been suggested to model an arms race betweentwo countries. The "aggressive" country's favorite outcome is that it has bombs and the

other country doesn't (c,h); the second best outcome is that neither country has bombs(h,h); the third best outcome is that both countries have bombs (c,c), and the leastfavored outcome is that only the other country has bombs (h,c). A game between twoaggressive countries results in a prisoner's dilemma situation. An alternative model ofthe arms race assumes "cooperative" preferences, i.e., both countries prefer a situationin which neither has bombs (h,h) to a situation in which it has bombs and the othercountry doesn't (c,h), because "the cost of arming outweighs the benefit if the othercountry does not arm itself." Id. at 20-21. A game between two "cooperative" players(a "stag hunt" game, in Osborne's terminology), results in two Nash equilibria.

2004] DEBT INVESTMENTS & FEDERAL ANTITRUSTLAW 613

mutual cooperation than from competing with a firm that is holdingback, i.e., (h,h) > (c,h). 7

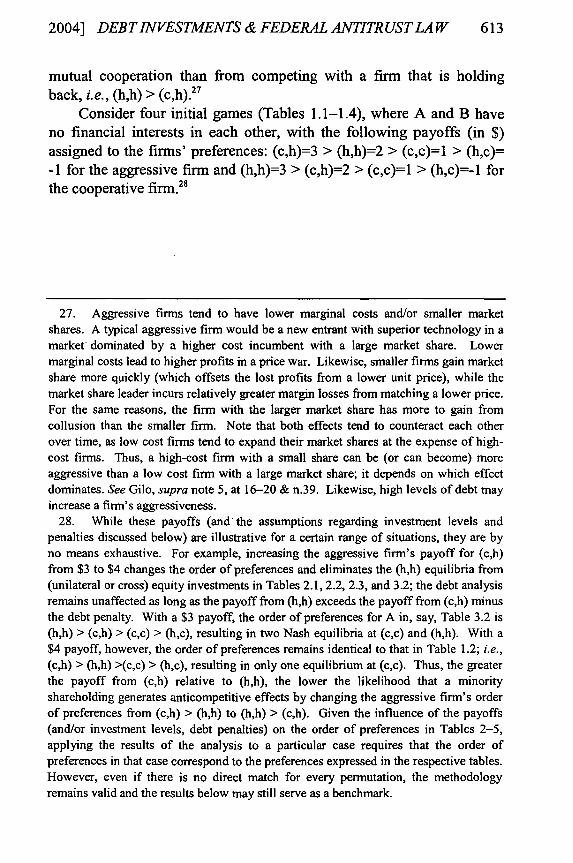

Consider four initial games (Tables 1.1-1.4), where A and B haveno financial interests in each other, with the following payoffs (in $)assigned to the firms' preferences: (c,h)=3 > (h,h)=2 > (c,c)=l > (h,c)=-1 for the aggressive firm and (h,h)=3 > (c,h)=2 > (c,c)=1 > (h,c)=- I forthe cooperative firm.28

27. Aggressive firms tend to have lower marginal costs and/or smaller marketshares. A typical aggressive firm would be a new entrant with superior technology in amarket dominated by a higher cost incumbent with a large market share. Lowermarginal costs lead to higher profits in a price war. Likewise, smaller firms gain marketshare more quickly (which offsets the lost profits from a lower unit price), while themarket share leader incurs relatively greater margin losses from matching a lower price.For the same reasons, the firm with the larger market share has more to gain fromcollusion than the smaller firm. Note that both effects tend to counteract each otherover time, as low cost firms tend to expand their market shares at the expense of high-cost firms. Thus, a high-cost firm with a small share can be (or can become) moreaggressive than a low cost firm with a large market share; it depends on which effectdominates. See Gilo, supra note 5, at 16-20 & n.39. Likewise, high levels of debt mayincrease a firm's aggressiveness.

28. While these payoffs (and the assumptions regarding investment levels andpenalties discussed below) are illustrative for a certain range of situations, they are byno means exhaustive. For example, increasing the aggressive firm's payoff for (c,h)from $3 to $4 changes the order of preferences and eliminates the (h,h) equilibria from(unilateral or cross) equity investments in Tables 2.1, 2.2, 2.3, and 3.2; the debt analysisremains unaffected as long as the payoff from (h,h) exceeds the payoff from (c,h) minusthe debt penalty. With a $3 payoff, the order of preferences for A in, say, Table 3.2 is(h,h) > (c,h) > (c,c) > (h,c), resulting in two Nash equilibria at (c,c) and (h,h). With a$4 payoff, however, the order of preferences remains identical to that in Table 1.2; i.e.,(c,h) > (h,h) >(c,c) > (h,c), resulting in only one equilibrium at (c,c). Thus, the greaterthe payoff from (c,h) relative to (hh), the lower the likelihood that a minorityshareholding generates anticompetitive effects by changing the aggressive firm's orderof preferences from (c,h) > (hh) to (hh) > (c,h). Given the influence of the payoffs(and/or investment levels, debt penalties) on the order of preferences in Tables 2-5,applying the results of the analysis to a particular case requires that the order ofpreferences in that case correspond to the preferences expressed in the respective tables.However, even if there is no direct match for every permutation, the methodologyremains valid and the results below may still serve as a benchmark.

614 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LAW

B+ B- B+ B-c h c h C h C h1 3 -C 1 3 1 1 -1c 1 -2

A+ h13 A+ 1 A- h A- 1

Table 1.1 Table 1.2 Table 1.3 Table 1.4

Table 1.1 pictures a game between two aggressive firms. 29 Tables1.2 and 1.3 describe games between an aggressive and a cooperativefirm, and Table 1.4 describes a game between two cooperative firms. InTable 1.1, (c) is the dominant strategy for both A and B, resulting in a(c,c) equilibrium. This outcome is referred to as a prisoner's dilemma,because even though (h,h) would yield greater benefits for both players,coordination would break down as A and B each have an incentive tocheat.30 In Table 1.2, A's dominant strategy is (c), whereas B does nothave a dominant strategy. However, as A's choice to compete is clear,B will choose likewise and the resulting equilibrium is (c,c). Theoutcome for Table 1.3 is identical to that of Table 1.2, with the positionsof A and B reversed. In Table 1.4, both firms value mutual cooperation(h,h) more highly than competing against a finn that is holding back(c,h). As a result, there are two Nash equilibria (c,c) and (h,h). Thus, inthe games described in Tables 1.1, 1.2, and 1.3, both firms choose tocompete, whereas in Table 1.4 they (may) choose to cooperate.31

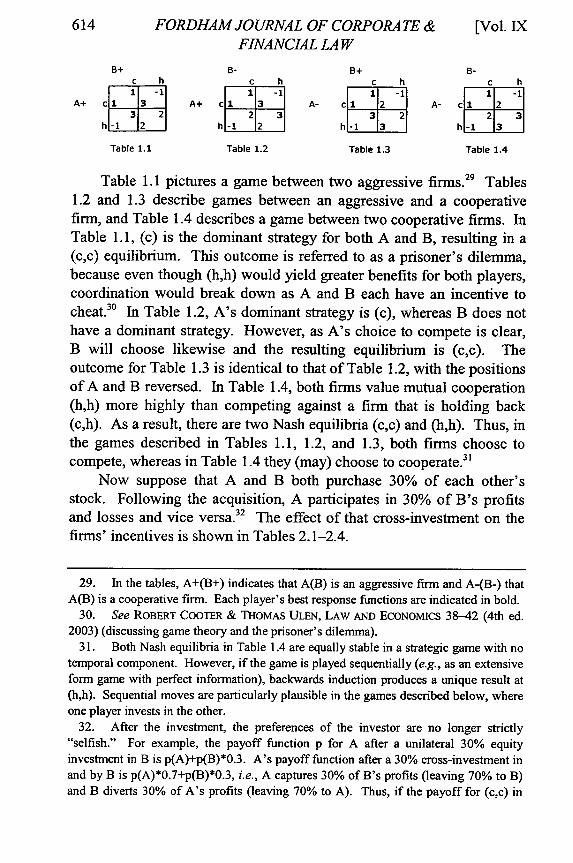

Now suppose that A and B both purchase 30% of each other'sstock. Following the acquisition, A participates in 30% of B's profitsand losses and vice versa.32 The effect of that cross-investment on thefirms' incentives is shown in Tables 2.1-2.4.

29. In the tables, A+(B+) indicates that A(B) is an aggressive firm and A-(B-) thatA(B) is a cooperative firm. Each player's best response functions are indicated in bold.

30. See ROBERT COOTER & THOMAS ULEN, LAW AND ECONOMICs 38-42 (4th ed.2003) (discussing game theory and the prisoner's dilemma).

31. Both Nash equilibria in Table 1.4 are equally stable in a strategic game with notemporal component. However, if the game is played sequentially (e.g., as an extensiveform game with perfect information), backwards induction produces a unique result at(h,h). Sequential moves are particularly plausible in the games described below, whereone player invests in the other.

32. After the investment, the preferences of the investor are no longer strictly"selfish." For example, the payoff function p for A after a unilateral 30% equityinvestment in B is p(A)+p(B)*0.3. A's payoff function after a 30% cross-investment inand by B is p(A)*0.7+p(B)*0.3, i.e., A captures 30% of B's profits (leaving 70% to B)and B diverts 30% of A's profits (leaving 70% to A). Thus, if the payoff for (c,c) in

2004] DEBT INVESTMENTS & FEDERAL ANTITR USTLA W

B+C h10.2

A+ 1. 1 .8h.1. 2..b0.e 21

Table 2.1

B-c h1T 072

A+ 1 1.8

0.1.11 2.7hi- 1 2.3

Table 2.2

B+c h

A- c i 11

1.8 2.31h 0.2 12.7

Table 2.3

B-C hC1. l1 -o.11

A- 1 I.,1

Table 2.4

In each of the Tables 2.1-2.4 two equilibria exist at (c,c) and (h,h).Compared to the pre-investment situation (Tables 1.1-1.3), where (c)was the dominant strategy for the aggressive firm, the cross-investmenthas enabled stable coordination by decreasing the payoffs for competingagainst a firm that is holding back (c,h) across the board33 and, in Tables2.2 and 2.3, by increasing the aggressive firm's payoff from mutualcooperation (h,h).34 The cross-investment, by modifying the respectivepayoffs, has changed the order of preferences for the aggressive firmfrom (c,h) > (h,h) to (h,h) > (c,h). That change constitutes acharacteristic anticompetitive effect of a financial interest in acompetitor within the coordinated effects model. Consequently, equitycross-investments of sufficient size have a distinct anti-competitivepotential.

The effect of unilateral equity investments is shown below. Apurchases 30% of B's stock. B has no equity interest in A.

B+c h

0.7 -0.7A+ c 1.3 2.7

2.1 1.4h -0. 12.6

Table 3.1

B-c h

0..7-0.7A+ C1.3 2.7

1.4 2.11h-0.4 2.9

Table 3.2

c hI0.7 -0.7

A- c 1.3 1.7I 2.1 1.4

h -0.1 3.6

Table 3.3

B-C h

c 0.7 -0.7A- 1.3 1.7

h 1.41 2.110.4 13.9

Table 3.4

Only in Table 3.2, where investor A is an aggressive firm and targetB is a cooperative firm, does the investment lead to a new equilibrium at

Table 1.1 is (1,1), the payoff after a 30% unilateral investment of A in B as expressed inTable 3.1 is (1.3,0.7) and after a 30% cross-investment as expressed in Table 2.1 is(1,1), i.e., A keeps 70% of its own and gets 30% of B's profits and vice versa.

33. Compare, for example, A's payoff for (c,h)=3 in Table 1.1 to (c,h)= 1.8 in Table2.1.

34. Compare, for example, A's payoff for (h,h)=2 in Table 1.2 to (h,h)=2.3 inTable 2.2.

616 FORDHAM JOURNAL OF CORPORA TE & [Vol. IXFINANCIAL LAW

(h,h).35 An investment by a cooperative firm (A) in an aggressive firm(B) as in Table 3.3 does not change the equilibrium results. In Table3.1, (c) remains the dominant strategy for both players and in Table 3.4(h,h) remains the likely outcome. Interestingly, where A and B are bothaggressive firms as shown in Table 3.1, the investment increases theinvestor's (A's) gains from (c,c) by 30% compared to the pre-investmentsituation in Table 1.1.36 Thus, only where (i) the incentives of A and Bare not symmetrical and (ii) the aggressive firm invests in thecooperative firm (but not vice versa) does a sufficient unilateral equityinvestment change the incentives of the investor.37

II. COMPETITIVE EFFECTS OF DEBT INVESTMENTS

Debt investments, such as loans or bonds, differ significantly fromequity investments in terms of corporate control (over the debtor) andfinancial interest (of the creditor). Courts and agencies have beenchiefly concerned with equity investments. There has only been a smallnumber of cases where anticompetitive effects of debt investments havebeen central to the courts' or the agencies' analysis. 3 As with partialownership, the courts' main concerns have been corporate control andaccess to information, not the incentives of the creditor from thefinancial investment.39 The following analysis explains why, as a rule,lenient treatment of debt investments under the antitrust laws is welljustified.

35. In Table 1.2, before the investment, A's order of preference was (c,h) > (hh).In Table 3.2, after the unilateral investment in B, it is (h,h) > (c,h).

36. Consequently, an aggressive firm may choose to invest in another aggressivefirm and still compete vigorously, e.g., where in a growing market, A predicts that itwill not be able to expand capacity proportionally to the increase in demand so that Aand B will both earn economic profits.

37. See Gilo, supra note 5, at 16 ("[I1f all firms in the industry are equally trigger-happy, the only way passive investment can facilitate collusion is if each firm in theindustry passively invests in a competitor."). In contrast, "[i]n markets in which somefirms are more trigger-happy than others, it is enough if the more trigger-happy firmsinvest in a competitor for collusion to be facilitated." Id. at 17.

38. See infra Part III.39. See Gilo, supra note 5, at 33 ("In debt cases the courts have focused only on

whether the creditor would attempt to exert its influence over the debtor through itsposition as creditor.").

2004] DEBT IN VESTMENTS & FEDERAL ANTITRUST LAW

A. Debt and Equity

A firm generates cash flow from its capital, which is the propertyand the money that the firm requires to do business.40 There are twomain sources of capital, equity and debt, and two constituenciesrepresenting these sources, shareholders and creditors. In economicterms, shareholders and creditors are both security holders in the firmwith different claims to the firm's cash flows from operations and, in theevent of liquidation, from the sale of assets.4' Shareholders have a claimto the residual cash flows, left over after meeting all other promisedpayments. Creditors have a prior claim to interest and principalpayments on a periodic basis and a prior claim to the firm's assets in theevent of liquidation.42 The creditors' claims are contractual in nature,fixed in time and capped in value.43 In contrast the shareholders' claimsare based on a property right and are indefinite in both time and value.

Among the most significant differences between equity and debt arethe consequences of the different attitudes of shareholders and creditorstowards risk."4 Both creditors and shareholders are in control of theirdownside risk: the shareholders because their liability is limited to theinvestment and the creditors because they cannot lose more than theprincipal of the loan. However, the upside potential of the shareholder isunlimited while the creditor has a fixed rate of return no matter howlarge a part of the firm's profits are generated as a result of its capitalcontribution. Shareholders make (and lose) money at the margin,creditors do not. Consequently, shareholders are willing to pay forpotential upsides with an increased risk of default, while creditors, whoare compensated ex ante for the expected default risk, are opposed to

40. See RICHARD A. BOOTH, FINANCING THE CORPORATION § 1:04 (2002).41. Morey W. McDaniel, Bondholders and Corporate Governance, 41 Bus. LAW

413,416 (1986).42. ASWATH DAMODARAN, APPLIED CORPORATE FINANCE: A USER'S MANUAL 214

(John Wiley & Sons 1999).43. In practice, debt is generally rolled over so that its fixed maturity is more of a

legal distinction than an economic reality, which is nevertheless important for

classification purposes. See generally id. at 214-24 (discussing the many varieties ofdebt including secured, unsecured and hybrid debt instruments).

44. There are, of course, other significant differences, for example, that under the

U.S. tax laws dividend payments are made from after-tax cash flows while interestpayments are deductible as expenses. See BOOTH, supra note 40, at § 3:14.

617

618 FORDHAM JOURNAL OF CORPORA TE & [Vol. IXFINANCIAL LAW

any alteration of that risk.45 The conflict between shareholders andcreditors becomes more and more pronounced the more highlyleveraged the firm is, i.e., the higher the ratio of debt to equity. That isbecause the shareholders as a group have less to lose (in absolute terms)and more to gain (in relative terms), while the creditors only stand tolose as illustrated by the following example:46

Consider a company with $100 in cash as its only asset. The

company's debt is $80 (a loan from B) and its stock, owned by A, isworth $20. An investment opportunity arises that has a 50% chance

of yielding $150 and a 50% chance of yielding $10. From A 's pointof view, this is an investment risk worth taking. If the project yields$10, A receives $0. If the project yields $150, A receives $70. Given

that the chances for either outcome are 50%, the expected stock

value is ($70+$0)/2=$35, compared to a present equity value of $20.

B, as a creditor, would be adamantly opposed to the investment. Ifthe project yields $150, B receives $80. If the project yields $10, Breceives $10. Thus, the expected value of the debt is

($80+$10)/2=$45. Note that the expected value of the companywould decline from $100 to $80 ($45+$35), which confirms that

increasing shareholder value does not necessarily coincide withincreasing firm value.

The risk of creditor expropriation by the company's management, 7

as described in the example above, is the primary reason for includingprotective covenants in credit agreements and bond indentures.48

Typical covenants restrict dividends, additional debt, risk alteringinvestments such as major acquisitions, and the disposition of significant

45. McDaniel, supra note 41, at 418.46. The example is based on Yakok Amihud et al., A New Governance Structure

for Corporate Bonds, 51 STAN. REV. 447, 454 (1999); RICHARD A. BREALEY &STEWART C. MYERS, PRINCIPLES OF CORPORATE FINANCE 517-18 (Irwin/McGraw Hill6th ed. 2000).

47. BOOTH, supra note 40, at § 3:12 (explaining that management is theshareholders' agent to whom it owes fiduciary duties. Management generally owes nofiduciary duties to the firm's creditors.) See BREALEY & MEYERS, supra note 46, at721-22; McDaniel, supra note 41, at 419-21 (illustrating that the conflict between

shareholders and creditors and the resulting management agency problem is not limitedto ex post alteration of risk through investment decisions. Other ways of benefitingshareholders at the expense of creditors are dividend distributions, spin-offs, andincreasing the debt/equity ratio through taking on additional debt or stock repurchases.)

48. BREALEY & MYERS, supra note 46, at 720; McDaniel, supra note 41, at 424.

2004] DEBT INVESTMENTS & FEDERAL ANTITRUST LA W

assets.49 In addition, credit agreements may contain "state-of-the-firm"covenants, requiring, e.g., minimum financial ratios, and net worth orequity cushions.50 Virtually every credit agreement provides for creditorinformation rights, generally in the form of an affirmative duty of thedebtor to supply the creditor with relevant information.5 These veto andinformation rights are significant from an antitrust point of view, as theyhave given rise to claims of corporate control and information exchangein violation of §7 and § 1 based on the acquisition of debt.52

B. Corporate Control and Information Exchange

Even though credit agreements generally require the borrower toprovide the lender with regularly updated financial information (auditreports, financial statements, notice of reportable events) and give thelender a right to request additional financial and other information,53

these provisions should not require the borrower to make accessiblecompetitively sensitive information and records, such as detailedstrategic plans, marketing plans, and customer specific pricinginformation. The lender has a legitimate interest in receivinginformation only to the extent necessary for assessing changes in thecredit risk. Where the creditor's request goes beyond what is required toassess the risk of default, the debtor is under no obligation to providethat information.54 And even where the creditor rightfully demanded the

49. Robert M. Lloyd, Financial Covenants in Commercial Loan Documentation:

Uses and Limitations, 58 TENN. L. REV. 335, 340-43 (1991); see also BOOTH, supranote 40, at § 3:06; Amihud et al., supra note 46, at 454-55.

50. Lloyd, supra note 49, at 340-43.51. Amihud et al., supra note 46, at 463-65.52. See infra Part III.53. Financial statements are the lender's primary source of information about a

borrower. The frequency with which financial statements are required depends on theborrower's creditworthiness. Public company borrowers are usually required to make

available SEC filings. In addition, creditors require notices of litigation, regulatoryaction, ERISA compliance and-depending on the borrower's business--otherinformation, such as age of receivables or inventory turnover from a retailer borrower.

See SANDRA STERN, STRUCTURING AND DRAFrING COMMERCIAL LOAN AGREEMENTS

5.01 [4]-[5] (A. S. Pratt & Sons rev. ed. 2001).54. Consequently, where the debtor voluntarily provides detailed information to a

competing creditor, inferences of collusion may be warranted; the loan could be afacilitating device. However, where there is no evidence of collusion and a debtor first

619

620 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LA W

information, so that the debtor's refusal results in a breach of anaffirmative covenant, the only remedy generally available to the creditoris acceleration of the loan.55

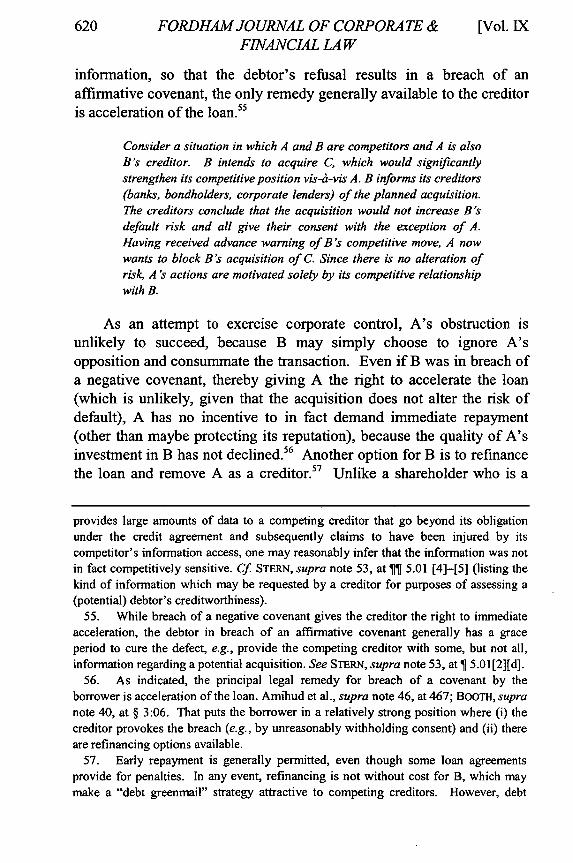

Consider a situation in which A and B are competitors and A is alsoB's creditor. B intends to acquire C, which would significantly

strengthen its competitive position vis-6-vis A. B informs its creditors(banks, bondholders, corporate lenders) of the planned acquisition.The creditors conclude that the acquisition would not increase B'sdefault risk and all give their consent with the exception of A.Having received advance warning of B's competitive move, A nowwants to block B's acquisition of C. Since there is no alteration ofrisk, A's actions are motivated solely by its competitive relationshipwith B.

As an attempt to exercise corporate control, A's obstruction isunlikely to succeed, because B may simply choose to ignore A'sopposition and consummate the transaction. Even if B was in breach ofa negative covenant, thereby giving A the right to accelerate the loan(which is unlikely, given that the acquisition does not alter the risk ofdefault), A has no incentive to in fact demand immediate repayment(other than maybe protecting its reputation), because the quality of A'sinvestment in B has not declined.56 Another option for B is to refinancethe loan and remove A as a creditor.17 Unlike a shareholder who is a

provides large amounts of data to a competing creditor that go beyond its obligationunder the credit agreement and subsequently claims to have been injured by itscompetitor's information access, one may reasonably infer that the information was notin fact competitively sensitive. Cf. STERN, supra note 53, at 5.01 [4]-[5] (listing thekind of information which may be requested by a creditor for purposes of assessing a(potential) debtor's creditworthiness).

55. While breach of a negative covenant gives the creditor the right to immediateacceleration, the debtor in breach of an affirmative covenant generally has a graceperiod to cure the defect, e.g., provide the competing creditor with some, but not all,information regarding a potential acquisition. See STERN, supra note 53, at 5.01 [2][d].

56. As indicated, the principal legal remedy for breach of a covenant by theborrower is acceleration of the loan. Amihud et al., supra note 46, at 467; BOOTH, supranote 40, at § 3:06. That puts the borrower in a relatively strong position where (i) thecreditor provokes the breach (e.g., by unreasonably withholding consent) and (ii) thereare refinancing options available.

57. Early repayment is generally permitted, even though some loan agreementsprovide for penalties. In any event, refinancing is not without cost for B, which maymake a "debt greenmail" strategy attractive to competing creditors. However, debt

2004] DEBT INVESTMENTS & FEDERAL ANTITR UST LA W 621

partial owner of the company, A can be removed against his will."Lastly, B may seek to compel A's consent by enforcing the covenant ofgood faith implicit in every loan agreement (e.g., by threateninglitigation for bad faith acceleration)i 9

The creditor's influence over the debtor increases significantlywhere the debtor is in financial distress, because the distressed debtorhas fewer (and therefore more expensive) refinancing alternatives. If thedebtor is in a financially hopeless situation, refinancing options may nolonger be available at all. Once accelerating, the loan would result in thedebtor's insolvency, the creditor has gained significant de factoinfluence over the debtor's management. A nearly insolvent borrowerwill most likely be in breach of a number of state-of-the-firm covenants,giving its creditors the right to accelerate the loan. The debtor thusrelies on its creditors to grant periodic waivers of covenants for itssurvival. Under these circumstances a creditor-competitor might be ableto justify a refusal to grant a waiver solely on the basis of its creditorinterests, regardless of its (further) motivations as a competitor.'

Therefore, as long as the debtor remains solvent and has viablerefinancing options, debt investments do not provide the creditor withmeaningful corporate control or information access rights. Where suchrights exist under a credit agreement, their enforceability by a competingcreditor is likely to be severely limited. However, once the debtor is infinancial distress and consequently has run out of viable refinancingalternatives, the creditor's influence increases significantly to a pointwhere it may well exceed the influence conferred by a comparable

greenmail could expose A to contractual liability under the loan agreement and may inaddition be actionable as a business tort, and, if A has sufficient market power, as(attempted) monopolization. For purposes of this Article, debt is assumed to berepayable at any time without penalties.

58. In the case of a syndicated loan, B may require consent of (some of) the otherlenders in order to remove A.

59. EDWARD F. MANNINO, LENDER LIABILITY AND BANKING LITIGATION

§§ 5.03[3][a], [b][ii] (Law Journals Seminars Press rev. ed. 2004) (1989) (discussingthe scope of the good faith performance obligation implicit in every contract).

60. However, accelerating the loan, even under these circumstances, is not withoutrisk, as courts have found creditors liable "for breaching the implied duty of good faithin accelerating a loan even where the borrower was in default and such action waspermitted under the lender's security agreement." Id. at § 5.03 [3][b][ii].

622 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LA W

equity investment, provided that the creditor has a legal basis forunilaterally accelerating the loan.61

C. Financial Interest

Does extending a loan to competitor B change the competitiveincentives of creditor A? Unlike a shareholder that participates in theresidual cash flows of the target, the loan agreement does not allow A toshare in an increase of B's value. Thus, as a creditor, A would notrecapture any portion of the profits from sales diverted to B as a result ofa unilateral price increase. Debt, unlike equity, does not automaticallylink the economic fortunes of the parties.

One exception to the rule that creditor A does not profit from debtorB's operational gains might be a situation where B is a company indistress. Suppose that A purchases B's distressed debt at a discount.Subsequently, A raises its own prices to supra-competitive levels, whichcauses operational losses of $2 for A and operational gains of $6 for B.B's gain lowers its risk of default, as a result of which the value of B'sdebt increases. If the gains from A's debt investment in B exceed $2,the price increase would be profitable. However, unlike equity, whichprovides A with a continuous income stream from its investment in B,the debt appreciation is a one shot deal with a ceiling. If A loses $2from the price increase in the first period and gains $3 from bondappreciation to par, the price increase is profitable. In the second period,however, A continues losing $2, while the bonds no longer appreciate.B's operational gains now increase the value of B's residual cash flow,

61. Where a syndicate of lenders has provided a loan, a single creditor may not havethe right to unilaterally accelerate the loan. Usually, acceleration requires the consent of amajority (or a super-majority) of the lenders in the syndicate. Where the debtor is alreadyin default and relies on the continued grant of waivers by the syndicate, a member of thesyndicate may be able to veto the extension of the waiver. Many syndicated loandocuments require a threshold investment for exercising a veto, e.g., one-third of thesyndicated loan. In that instance, a debt holding below the threshold level does not conferany meaningful power of the nature discussed above to the creditor even if the debtor hasno other refinancing options. See Vantico Holdings S.A. v. Apollo Mgmt., LP, 247 F.Supp. 2d. 437, 447 (S.D.N.Y. 2003) (describing a case where lender's debt ownershiprequirement for vetoing borrower's decisions was 34%).

2004] DEBTINVESTMENTS & FEDERAL ANTITRUSTLAW 623

in which A has no stake. 62 As a consequence, the unilateral effects of(passive) debt investments are generally much less significant than thoseof partial ownership.

63

D. Coordinated Effects

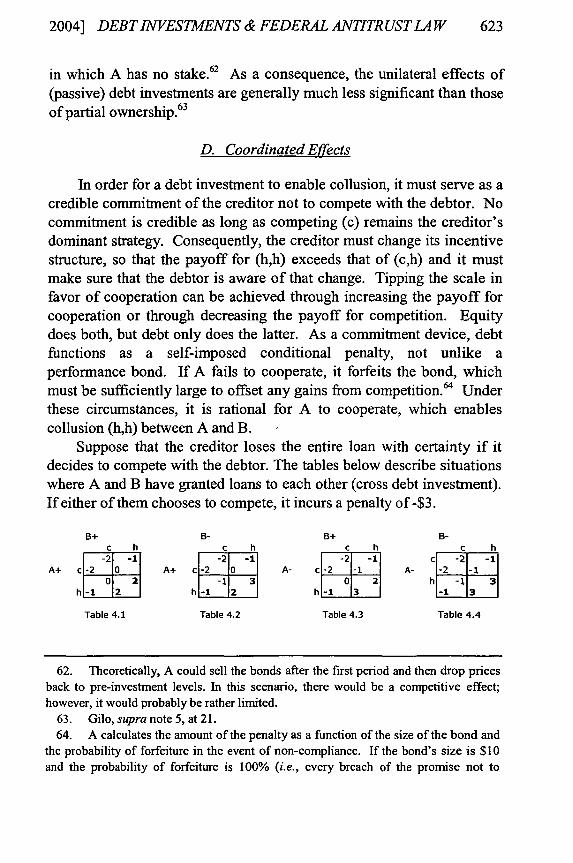

In order for a debt investment to enable collusion, it must serve as acredible commitment of the creditor not to compete with the debtor. Nocommitment is credible as long as competing (c) remains the creditor'sdominant strategy. Consequently, the creditor must change its incentivestructure, so that the payoff for (h,h) exceeds that of (c,h) and it mustmake sure that the debtor is aware of that change. Tipping the scale infavor of cooperation can be achieved through increasing the payoff forcooperation or through decreasing the payoff for competition. Equitydoes both, but debt only does the latter. As a commitment device, debtfunctions as a self-imposed conditional penalty, not unlike aperformance bond. If A fails to cooperate, it forfeits the bond, whichmust be sufficiently large to offset any gains from competition. 64 Underthese circumstances, it is rational for A to cooperate, which enablescollusion (h,h) between A and B.

Suppose that the creditor loses the entire loan with certainty if itdecides to compete with the debtor. The tables below describe situationswhere A and B have granted loans to each other (cross debt investment).If either of them chooses to compete, it incurs a penalty of -$3.

B+ B- B+ B-c h c h c h C h

-2 -- 2 -1 -2 -1 -21 -11

A+ -2 0 A+ C 0 A- -2 -1 A-

Table 4.1 Table 4.2 Table 4.3 Table 4.4

62. Theoretically, A could sell the bonds after the first period and then drop pricesback to pre-investment levels. In this scenario, there would be a competitive effect;however, it would probably be rather limited.

63. Gilo, supra note 5, at 21.64. A calculates the amount of the penalty as a function of the size of the bond and

the probability of forfeiture in the event of non-compliance. If the bond's size is $10and the probability of forfeiture is 100% (i.e., every breach of the promise not to

624 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LAW

Compared to the initial games (Tables 1.1-1.4), new (h,h) equilibriaappear in Tables 4.1-4.3. The debt penalty renders (c,h) and (c,c)unprofitable. Holding back (h) becomes the new dominant strategy for Aand B across the board. Thus, in a situation where the party deciding tocompete triggers a penalty sufficient to wipe out any gains from suchcompetition, cross debt investments may have distinct anticompetitiveeffects.65

The effects of unilateral debt investments are shown in the tablesbelow. In these examples, A extends credit to B. If A competes, itincurs a penalty of-$3.

1+ B- B+ B-

e h c h c h c h1 -1 1 -1 -1c 1 -

A+ C-2 0 A+ c-2 A- - A-

h-1 3 2 -1 h -1 h 1

Table 5.1 Table 5.2 Table 5.3 Table 5.4

Following the debt commitment, holding back (h) has becomeinvestor A's dominant strategy. However, because the debt investmentis unilateral, B's competitive incentives remain unaffected. Thus,whether B chooses to compete or to hold back depends entirely onwhether B is an aggressive firm (in which case B will compete) or acooperative firm (in which case B will hold back). Only in Table 5.2does A's investment create an equilibrium at (h,h). However, and moreimportantly, in Tables 5.1 and 5.3, the debt investment creates a (h,c)equilibrium, which effectively precludes A from fighting back if Bdecides to compete. Thus, the unilateral debt investor faces a significantrisk of error. If B is an aggressive firm or if B turns into an aggressivefirm subsequent to A's investment, A may set a trap for itself The latteris an important difference to the equity investments discussed above,where partial ownership in an aggressive firm was merely ineffectual asa commitment device; see Tables 3.1 and 3.3. In contrast, debt

compete will lead to complete forfeiture), the expected value of the penalty is $10. Ifthe probability of forfeiture drops to 50%, the expected value of the penalty is $5.

65. The qualifier ("may") is warranted because triggering the debt penalty bycompetitive actions (and competitive actions only) with a sufficient degree of reliabilityis highly unlikely.

2004] DEBT INVESTMENTS & FEDERAL ANTITR USTLA W

investments in an aggressive competitor leave the investor worse offcompared to the initial games in Tables 1.1 and 1.3.

The model above rests on the assumption that the creditor's choiceto compete does, in fact, trigger the penalty. However, creating and/ormaintaining that condition in the real world would be a daunting task,because explicit non-compete and penalty provisions are unlawful under§ 1 and thus unenforceable in court. Commentators and litigants havetherefore focused on the debtor's bankruptcy as the de facto linkbetween competitive action on the part of the creditor and the incurringof the penalty, i.e., the loss of the loan.66 Bankruptcy, however, is a poordevice for connecting the market behavior of a creditor to the inability ofa competing debtor to repay a loan with any degree of reliability. As athreshold matter, the debtor must remain at the brink of bankruptcy forthe duration of the arrangement. As soon as the debtor returns to aminimal state of financial health, the creditor's commitment is no longercredible and competitive behavior might ensue. Moreover, as aconsequence of the debtor's required state of continued financialweakness, the debtor will not only be vulnerable to the creditor'scompetitive actions but also to unrelated events in the marketplace (e.g.,changes in input costs, interest rates, shifts in demand, etc.). Thecreditor therefore faces a significant risk of incurring the penalty byaccident. Even if the triggering condition could be calibrated to thecreditor's actions with sufficient accuracy, there would still be nopredictable connection between the debtor's insolvency and the loss ofthe loan. What happens to a significant loan in bankruptcy is highlyuncertain. It may be repaid in full, in part, not at all, deferred, orconverted into equity, to name just a few possibilities in reorganization.Only if the debtor's assets are, in fact, entirely non-competitive andworthless (in which case coordination would probably not significantlylessen competition to begin with) would the creditor lose its loan withsufficient certainty.67

66. Gilo, supra note 5, at 21. For case discussions, see infra Part III.67. Creating a stable cartel equilibrium with a weak competitor is less troublesome

from an antitrust perspective than collusion among strong competitors. However, insettings with more than two firms involved, A could be the only aggressive firm thatmakes a broader cartel equilibrium among, say, A, B, C, and D impossible. If Acommits itself through a loan to the weakest competitor B, it may not gain much fromB's cooperation in a (h,h,h,h) state; however, A may gain substantially from not havingto compete with C and D.

625

626 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LAW

Another problem with debt as a commitment device is that thedebtor's required state of financial weakness might change itscompetitive incentives so that coordination ultimately breaks down.Suppose that A invests in B in order to change its (A's) dominantstrategy from (c) to (h). As a consequence of its financial weakness, B'smarket share deteriorates to the point that B has more to gain fromstarting a price war with A (c,h) than from continued cooperation (h,h).As long as B remains susceptible to A's attack, A is caught in its owntrap, as (h,c) remains a better choice than (c,c), see Tables 5.1 and 5.3above. B can use the threat of bankruptcy to compete against A withimpunity. Once B returns to financial health (e.g., after having gainedsufficient market share at A's expense), A's strategic commitment is nolonger effective.

While cross debt investments have a tendency to increase theprobability of a collusive equilibrium, the same cannot be said forunilateral debt investments without further qualifications. Unless certainthreshold conditions are met, unilateral debt as a commitment device isby and large ineffectual, because there is no predictable link between thecreditor's actions and the triggering of the penalty. Thus, from afinancial interest point of view, debt investments have no significantanticompetitive potential unless (i) the debtor is in poor financial health;(ii) the creditor (and only the creditor), through specific competitiveactions, can significantly increase the probability of the debtor'sinsolvency; (iii) once the debtor has become insolvent, its assets wouldexit the market; 68 and (iv) liquidation of the assets is insufficient to

68. The assets exit the market when the insolvent company ceases to exist as agoing concern with the consequence that its production capacity will no longer beavailable to serve market demand. The assets do not exit the market if they are boughtby a financial investor or a strategic buyer with the intent to continue operations and toreintroduce capacity into the market. Thus, implicit in the "exiting the market"assumption is that B has a non-competitive asset base. If B's assets were competitive,the firm would be a takeover target and its assets would likely remain in the marketunder different management. The "exiting the market" condition also relates to abroader issue. If B's assets are non-competitive, then A could drive B from themarketplace by competitive means and subsequently enjoy monopoly profits. Thus, forA, the desirability of (c,h) relative to (h,h) increases with B's weakness. Conversely, astrong rival makes (h,h) more desirable (yet less obtainable) relative to (c,h). Thatrelationship further underscores the partially self-refuting character of a debt-commitment strategy. A more complete model would have to take the relative strengthsand weaknesses of the rivals into account.

2004] DEBT INVESTMENTS & FEDERAL ANTITRUST LAW

guarantee repayment of the creditor's loan.69 Moreover, (v) taking intoaccount the overall probability of the creditor's competitive actionresulting in the ultimate loss of the loan, the debt penalty must be ofsufficient size to offset any gains from competition. As a result, theanticompetitive potential of debt investments from the financial interestin a competitor is much more limited than that of a (passive) minorityequity stake. 70

III. DEBT INVESTMENTS IN THE COURTS

Courts have addressed the competitive effects of debt investmentsin Metro-Goldwyn-Mayer, Inc. v. Transamerica Corp., Mr. Frank, Inc.v. Waste Management, Inc., and, most recently, Vantico Holdings S.A. v.Apollo Management LP.7 The consent order in United States v. TheGillette Co. also touches upon competitive effects of debt holdings, eventhough the primary focus is on the partial ownership aspects of thetransaction.72 Thus, there is little guidance as to how courts and

69. As a consequence, the ideal debt commitment device would be a substantialunsecured loan. In contrast, fully secured senior debt would be a poor choice for acompetitor, as chances of (at least partial) repayment are higher even in the event of abankruptcy with minimal assets. Here, the inherent tensions between the roles of theinvestor as a competitor and as a creditor come to a head. As a practical matter,obtaining board approval for a significant unsecured loan to a competitor in distress is atall task for any firm's management, in particular as there is a significant risk ofshareholder lawsuits should the debtor default on the loan.

70. Gilo, supra note 5, at 21.71. MGM, Inc. v. Transamerica Corp., 303 F. Supp. 1344, 1350 (S.D.N.Y. 1969);

Mr. Frank, Inc. v. Waste Mgmt., Inc., 591 F. Supp. 859, 867 (N.D. Ill. 1984); VanticoHoldings, S.A. v. Apollo Mgmt. Ltd. P'ship, 247 F. Supp. 2d 437,456 (S.D.N.Y. 2003).The author represented Apollo Management LP in the Vantico litigation.

72. Gillette 11, supra note 4; Gillette I, supra note 4. In 1989, Gillette had agreedto purchase (i) Wilkinson's world-wide wet shaving business and (ii) a 23% non-votingequity stake and 50% of the subordinated debt (valued at $69 million) in Eemland,Wilkinson's corporate parent. Gillette I, supra note 4, at 28,314. Following the DOJ'schallenge, Gillette abandoned the acquisition of Wilkinson's U.S. business. Gillette II,supra note 4, at *1. The consent decree allowed Gillette to keep its 23% equity stakeand its debt holdings in Eemland, provided that Gillette refrained from, inter alia,acquiring additional equity and debt, from seeking board representation, and frominfluencing Eemland's business. Specifically with respect to debt, the consent decreestipulated that:

627

628 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LAW

agencies would analyze competitor debt investments, which forcescorporate lenders to operate under significant uncertainty.73

A. MGM v. Transamerica (1969)74

The seminal case concerning debt investments under the antitrustlaws is MGM v. Transamerica, decided by the district court for theSouthern District of New York in 1969.75 Tracy Investment Company("Tracy") made a cash tender offer for 17% of MGM's shares, which, ifsuccessful, would have given Tracy "working control" of and boardrepresentation at MGM.76 The tender offer was valued at $36.5 million,$30 million of which was to be financed through a loan fromTransamerica Financial Corp ("Financial").77 The loan was fullysecured, inter alia, by the MGM shares.7

' The crux of the case was thatFinancial's parent, Transamerica Corp., happened to be the controllingshareholder of United Artists, a direct competitor of MGM. 79 The courtconsidered two issues: (i) did the share pledge (i.e., using MGM's sharesas collateral for the loan) violate §7; and (ii) assuming that the parties

Gillette shall not.., use or attempt to use its creditor position in Eemland: (a) toprevent or restrict Eemland's ability to refinance or obtain additional credit or capital;(b) to initiate any action the effect of which reasonably could be expected to causeEemland to become insolvent or bankrupt; or (c) in the event of a proposedreorganization of Eemland because of insolvency or bankruptcy concerns, to voteagainst any reorganization plan proposed or supported by Eemland.

Gillette II, supra note 4, at *5.73. The legal classification of debt investments under the antitrust laws is not just a

domestic problem; it also raises questions under the merger control regimes of otherjurisdictions. In Vantico, the German Federal Cartel Office investigated whether a 35%debt investment constituted a concentration under §37(I)(4) of the Act againstRestraints of Competition ("GWB"). Ultimately, the agency did not take any actionafter the debt was repaid. However, Cartel Office staff acknowledged that there wasdisagreement within the Cartel Office as to whether debt investments would beprosecuted under §37(I)(4) GWB on a going forward basis.

74. 303 F. Supp. 1344 (S.D.N.Y. 1969).75. Id. at 1344.76. Id. at 1346-49.77. Id. at 1346.78. Id. at 1347.79. Id. at 1346 ("The root of the controversy lies in the fact that the cash tender

offer is being financed by Financial, whose parent, Transamerica, owns 99.6% ofUnited Artists Corporation, a major competitor of MGM.").

2004] DEBT INVESTMENTS & FEDERAL ANTITRUST LAW

removed the pledge, would the loan by itself violate §7?8o With respectto (i), the court decided that the share pledge constituted a violation of§7, because Financial could have chosen to acquire the MGM shares inthe event of Tracy's bankruptcy.8 ' With respect to (ii) the court merelyenjoined Tracy and Financial from exchanging MGM-relatedinformation.12 The court explicitly held that the debtor-creditorrelationship by itself posed no threat to competition.

The MGM court was concerned with threats to competition fromcorporate control and information exchange. The creditor's financialinterest did not factor into the analysis. 84

A bare debtor-creditor relationship, standing by itself, gives thecreditor no control over the debtor's right to vote its stock. In thisrespect the relationship differs sharply from those which have beencondemned because a company, either by contract, stock ownership,market position or similar factors, possesses the power to control orinfluence its competitor's decisions. 8 5

Even though the bare debtor-creditor relationship lacksanticompetitive potential, there may be "surrounding circumstances"that could conceivably lead to a substantial lessening of competition,"including the expressed purpose of the relationship, the debtor'ssolvency or insolvency, the terms and size of the loan, the percentagewhich it bears to the debtor's entire debt and capital structure, theexistence of other contracts or relationships between the parties, etc. 86

Consistent with the analysis above, most of the circumstances identifiedby the MGM court are in fact necessary (albeit not sufficient) conditionsfor control through debt investment, in particular insolvency and theresulting lack of refinancing options combined with a significant loan.

80. Id. at 1350 ("Reduced to its simplest terms the essential question before us is:Does the status of a major MGM competitor (Transamerica-United Artists-Financial) asa substantial creditor of the prospective controlling shareholder (Tracy) pose a sufficientthreat to competition to run afoul of §7?").

81. Id. at 1349.82. Id. at 1352, 1354.83. Id. at 1350 ("In the case before us... it is difficult to foresee the probability of

anti-competitive effects flowing from the debtor-creditor relationship alone.")84. Id. at 1351.85. Id. at 1350.86. Id. at 1351.

629

630 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LAW

However, the threat of insolvency must at least be probable. The merefact that "Tracy has not advanced any present plans for refinancing,absent which Financial might have considerable power over it"88 was notsufficient to establish a §7 violation.8 9 Thus, under MGM, absent specialcircumstances, debt investments in competitors are lawful under §7.90

B. Mr. Frank v. Waste Management, Inc. (1984)91

In 1984, the district court for the Northern District of Illinoisdecided Mr. Frank v. Waste Management, Inc.92 Waste ManagementInc. ("WMI") provided waste disposal services.93 Chem-Clear, acompetitor in the same geographic market, was one of WMI's potentialacquisition targets.94 Chem-Clear was in financial distress; nevertheless,it received a $140,000 loan from WMI.9' Mr. Frank, Inc. ("Mr. Frank"),a customer of WMI and Chem-Clear, brought suit against WMI's"pattern of acquisitions" in violation of, inter alia, §7.96 The courtdenied WMI's motion for summary judgment and found that there were

87. See id. at 1350 ("[T]he mere possibility of anti-competitive effects isinsufficient .... In the absence of circumstances indicating a probability that thecreditor would use its position to influence MGM..., we do not believe that such adebtor-creditor relationship should be categorically outlawed as a matter of law.")(emphasis added).

88. Id. at 1351.89. Id. at 1351-52 ("[Tlhe question of whether a debtor-creditor relationship must

be enjoined as threatening competition in violation of [§]7 depends upon whether suchprobability is revealed by surrounding circumstances.") (emphasis added).

90. Responding to comments regarding the prop'osed final judgment in Gillette,the Justice Department relied on the absence of special circumstances under MGM tojustify its refusal to require Gillette to give up its debt position in Eemland. Gillette I,supra note 4, at 28,323.

91. 591 F. Supp. 859, 859 (N.D. Ill. 1984).92. Id.93. Id. at 862.94. Id.95. Id. at 867.96. Id. at 865. In addition to its loan to Chem-Clear, WMI also had ties to two

other waste disposal service companies in the same geographic area. This Articlefocuses on Chem-Clear, because "WMI's only present interest in Chem-Clear is thatChem-Clear owes WMI approximately $140,000." Id. at 862 (emphasis added).

2004] DEBTINVESTMENTS & FEDERAL ANTITRUSTLAW 631

triable issues of fact.97 The court held that "WMI's status as asubstantial creditor could give it appreciable power over Chem-Clear'sactions."98 The court focused solely on the corporate control dimensionof the relationship. "If... Mr. Frank is able to prove that WMI'screditor's interest gives WMI significant control over Chem-Clear, thenthat interest would be a 'contemporary violation' of the Clayton Act." 99

Three factors surrounding the loan influenced the court's reasoning, thefact (i) that Chem-Clear was "in financial straits," (ii) that the loan was"substantial," and (iii) that "WMI did not press for collection while itand Chem-Clear negotiated WMI's proposed takeover of Chem-Clear,"i.e., the existence of a relationship between the parties beyond theloan. '0 These factors also appear in the MGM court's list of"surrounding circumstances," which is significant because there is noindication that the Mr. Frank court was aware of the MGM decision.' 0 '

The Mr. Frank opinion contains an important discussion of theapplicability of §7 to debt investments, a logical prerequisite for theanalysis, which is missing entirely in the MGM decision where the courtsimply assumed that debt investments fall within the scope of §7.102 InMr. Frank, the court addressed the issue of §7 applicability in thecontext of determining whether a loan constitutes an "asset" under §7103

and held that "Chem-Clear's $140,000 debt to WMI may constitutean... 'asset' because Chem-Clear is in financial straits."'0 4 It follows econtrario that but for Chem-Clear's dire financial situation, the debt assuch would not have been an asset and not be subject to §7 scrutiny.Thus, only qualified debt, i.e., debt in connection with othercircumstances that give the creditor "appreciable power over [thedebtor's] actions" ' 5 constitutes an asset, the acquisition of which may

97. See id. at 871 (holding that defendants motion for summary judgment wasdenied in all aspects except those concerning divestiture and price fixing allegations).

98. Id. at 867.99. Id.

100. Id. at 862.101. The Mr. Frank decision contains no reference to MGM.102. MGM, Inc., 303 F. Supp. at 1350.103. Mr. Frank, Inc., 591 F. Supp. at 866 (stating that "[Assets] is not a word of art,

nor is it given a built-in definition by statute .... As used in this statute, and dependingupon the factual context, 'assets' may mean anything of value.").104. Id. at 867 (emphasis added).105. Id.

632 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LAW

be analyzed under §7.106 The court appears to have employed thefollowing analytical framework: As a rule, debt investments areanalyzed under § 1, because debt as such is not an asset for purposes of§7.107 However, in rare circumstances where the debt investment isqualified by giving the creditor "appreciable power over [the debtor's]actions," debt falls within the definition of an asset and §7 isapplicable.' That analysis is appealing, because its rule/exceptioncharacter reflects the different effects of debt investments and partialownership. In a partial ownership situation, the potential effectsstandard of §7 is the rule, unless the investment is in fact competitivelyharmless, in which case the actual effects standard of the "solely forinvestment" exemption, which is substantively identical to that of § 1,applies.'0 9 In a debt investment situation, the rule/exception relationshipis reversed. The actual effects standard of § 1 is the rule, unless theinvestment is of a narrowly defined type that confers meaningfulcorporate control to the competing lender, which justifies the applicationof §7's potential effects standard. Thus, Mr. Frank stands for theproposition that debt investments in competitors, unless they convey ameaningful degree of corporate control over the target to the investor,fall outside of the scope of §7.

106. See id. at 866.107. See id. at 867.108. Id.109. See U.S. v. Tracinda Inv. Corp., 477 F. Supp. 1093 (C.D. Cal. 1979):

An acquisition may escape a challenge under Section 7, even though it may be inviolation of the section's substantive provisions, if it falls within the specificexemptions provided for in Section 7, one of which provides that acquisitions of stockwhere the acquisition is made solely for the purposes of investment are not included inthe prohibition of Section 7.

Id. at 1098; The Anaconda Co. v. Crane Co., 411 F. Supp 1210 (S.D.N.Y. 1975):In cases where the "solely for investment" exemption does not apply, a plaintiff needonly show a reasonable probability of a lessening of competition .... [However,o]nce it is established to the satisfaction of the Court that the acquisition is "solely forinvestment," the statute requires a showing that the defendant is "using the (stock) byvoting or otherwise to bring about, or in attempting to bring about, the substantiallessening of competition."

Id. at 1219.

2004] DEBT INVESTMENTS & FEDERAL ANTITRUSTLA W

C. Vantico v. Apollo (2003)"0

Apollo Management LP ("Apollo"), a private equity fundmanagement company, acquired 35% of Vantico's senior bank debt at asubstantial discount to par through one of its funds (Fund V)."' Anotherfund, Fund IV, held a controlling equity stake in ResolutionPerformance Products, LLC ("Resolution"), a competitor of Vantico.Vantico sued to enjoin Apollo from purchasing more debt and fromvoting its debt against a restructuring plan that was proposed by a majorsubordinated bondholder." 2 The district court denied the injunction,finding that the acquisition of debt by Apollo did not violate §7, § 1, or§2.' 13 Following MGM, the court implicitly assumed the applicability of§7 to debt and started its analysis with the observation that "[t]he merefact that a company's horizontal competitor may have acquired the debtof the company and is a creditor is not a sufficient basis to conclude thatsuch an acquisition is a violation of §7."' 14 Even though Vantico claimedto be on the brink of insolvency, the court found that the "circumstancescreated by the acquisition... does [sic] not establish a probability ofanti-competitive effects.""' 5 The court arrived at that result after acareful analysis of Apollo's incentives as a fund manager." 6 Unlike aholding company that serves the interests of one shareholderconstituency (i.e., the shareholders in the holding), a fund managerserves the interests of multiple constituencies; in Apollo's case those ofthe investors in Fund V (debt in Vantico) and Fund IV (equity inResolution)." 7 While a holding company might have an incentive toconsider anticompetitive trade-offs between investments, a fundmanager generally does not." 8

[W]hile the insolvency of a competitor might be of some benefit tothe investors in Fund IV, which controls Resolution, it would

110. Vantico Holdings, S.A. v. Apollo Mgmt. Ltd. P'ship, 247 F. Supp. 2d 437(S.D.N.Y. 2003).111. Id. at 442-43, 447.112. The bondholder was in fact funding the litigation. Id. at 446, 458.113. Id. at 457-58.114. Id. at 455.115. Id. at456.116. Id.117. Id. at 442-43.118. Id. at 456.

633

634 FORDHAM JOURNAL OF CORPORATE & [Vol. IXFINANCIAL LA W

significantly harm the investors in Fund V, and risk therecoverability of Fund V's $160 million investment [in Vantico.]Consequently, Apollo has little or no incentive to engage in the anti-. • - 119

competitive behavior that is envisioned by Vantico.

The Vantico case is significant because the court made the financial

incentives analysis of the investor the centerpiece of its opinion.1 20