"The Seniority Structure of Sovereign Debt" by Christoph Trebesch, Matthias Schlegl and Mark Wright

Debt and Seniority: An Analysis of the role of hardclaims

by Hart and Moore

Rafael Burjack

FGV-EPGE

September 16, 2010

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 1 / 36

Contents

1 Introduction

2 The ModelThe FirmThe ManagerThe VariablesThe Contract

3 Long-term DebtThe Firm’s Maximization ProblemExample

4 General Long-Term Security StructureThe Security StructureThe Standard Package

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 2 / 36

Introduction

Introduction

The firm wants to set a contract to maximize the aggregate expectedreturn and is run by a manager.

Although, the manager is self-interested and their will may not agree.

The objective of the firm is to set a contract such that the managerwill do the best maximize the expected return.

We allow the firm make contracts with different seniorities.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 3 / 36

Introduction

Literature

Literature has approached issuance of debt by public companies as;

an attempt to reduce taxes;Modigliani and Miller (1993), and Miller (1997)

a signaling device;Hayne Leland and David Pyle (1977) and Stephen Ross (1977)

a way of completing market;Joseph Stiglitz (1974), Franklin Allen and Douglas Gale (1988)

an attempt to raise funds without diluting the value of equity.Stewart Myers and Nicholas Majluf (1984)

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 4 / 36

Introduction

Financial Structure

Although important, these approaches cannot explain the types ofdebt claims observed in practice.

Nevertheless, in reality, firms issue debt with different seniorities andnonpostponable debts.

The reason is that managers are self-interested in practice but theliterature doesn’t take it account.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 5 / 36

Introduction

The role of hard claims is to constraint the managerial excess (EmpireBuilding).

Nonpostponable, short-term1 It forces management to not use money for empire-building investment.2 It triggers liquidation when the assets of the firm are more valuable

elsewhere.

Senior Long-term1 It prevents nonprofitable investment under future earnings.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 6 / 36

Introduction

The role of hard claims is to constraint the managerial excess (EmpireBuilding).

Nonpostponable, short-term1 It forces management to not use money for empire-building investment.2 It triggers liquidation when the assets of the firm are more valuable

elsewhere.

Senior Long-term1 It prevents nonprofitable investment under future earnings.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 6 / 36

The Model

The Environment

2 agents: the manager and investor. Both of them are risk neutral.

The interest rate is zero.

3 Periods; t ∈ {0, 1, 2}.The firm is run by a single manager and consists of assets in placeand a new investment opportunity.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 7 / 36

The Model The Firm

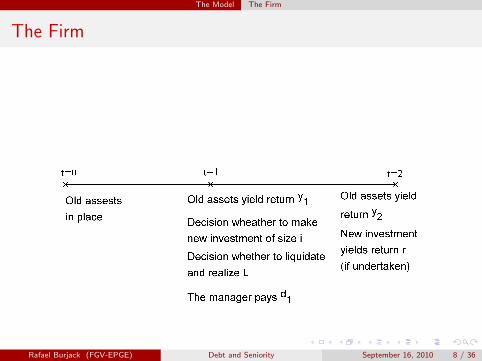

The Firm

Figure: Timing

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 8 / 36

The Model The Manager

The Manager

The manager decides whether to take investment opportunity or not.

We want to study cases where the manager wants projects for empirebuilding.

To simplify, we consider that the manager will always take theopportunity if possible.

He never liquidates the firm voluntarily at t = 1. Because this wouldbe a loss of power.

At t = 2, he retires.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 9 / 36

The Model The Variables

The variables

All the uncertainty comes from the variables

y1, y2, L, i , r .

They are all revealed at t = 1 and there is symmetric informationthroughout.

The variables are observable but are not verifiable.

The payments made to the security-holders are verifiable and they willbe the basis for the contract.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 10 / 36

The Model The Variables

The variables

All the uncertainty comes from the variables

y1, y2, L, i , r .

They are all revealed at t = 1 and there is symmetric informationthroughout.

The variables are observable but are not verifiable.

The payments made to the security-holders are verifiable and they willbe the basis for the contract.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 10 / 36

The Model The Contract

The Contract

The securities can be issued at t = 0 with claims conditional on theamount that is paid out.

We DO NOT allow claims to issued on the return from theinvestment, r , separately from the assets in place, y2. That is, we ruleout project-financing.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 11 / 36

The Model The Contract

The Contract

The securities can be issued at t = 0 with claims conditional on theamount that is paid out.

We DO NOT allow claims to issued on the return from theinvestment, r , separately from the assets in place, y2. That is, we ruleout project-financing.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 11 / 36

The Model The Contract

The Contract

We suppose that both kinds of debt (d1, d2) are senior, in the sensethat any new claims issued by the firm are entitled to payment only ifdate-0 debt-holders have been fully paid off.

It is prohibitively costly to renegotiate with creditors at t = 1.

Thus, if the firm defaults on its short-term debt, in turn, leads toliquidation (L is realized).

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 12 / 36

The Model The Contract

Assumption 1

Assumption 1

y1 < i and y2 ≥ L with probability 1.

This assumption says that the manager needs to raise money frommarket to invest and that liquidation is not worth.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 13 / 36

The Model The Contract

Proposition 1

Proposition 1

Given Assumption 1, the date-0 market value of the firm is maximized bysetting d1 = 0.

Proof: The firm can face three different total returns:

R1 = y1 + y2 + r − i if y1 + y2 + r − d1 − d2 ≥ i

R2 = y1 + y2 if y1 ≥ d1 or y1 + y2 ≥ d1 + d2

R3 = y1 + L if y1 ≤ d1

Liquidation is undesirable because y2 ≥ L. Thus, to maximize the firmreturn we set d1 = 0 to minimize the event of bankrupt.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 14 / 36

The Model The Contract

Proposition 1

Proposition 1

Given Assumption 1, the date-0 market value of the firm is maximized bysetting d1 = 0.

Proof: The firm can face three different total returns:

R1 = y1 + y2 + r − i if y1 + y2 + r − d1 − d2 ≥ i

R2 = y1 + y2 if y1 ≥ d1 or y1 + y2 ≥ d1 + d2

R3 = y1 + L if y1 ≤ d1

Liquidation is undesirable because y2 ≥ L. Thus, to maximize the firmreturn we set d1 = 0 to minimize the event of bankrupt.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 14 / 36

Long-term Debt The Firm’s Maximization Problem

The Firm’s Maximization Problem

Denote by F (y1, y2, i , r) the probability distribution at t = 0.

The return from the existing assets,∫

(y1 + y2)dF (y1, y2, i , r) is fixed.

Then, the firm’s maximization problem can be set as

maxd2

∫y1+y2+r−i≥d2(r − i)dF (y1, y2, i , r) (1)

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 15 / 36

Long-term Debt The Firm’s Maximization Problem

Proposition 2

Proposition 2

The first-best cases

1 If r ≥ i with probability 1, then the first-best can be achieved bysetting d2 = 0 (all equity).

2 If r ≤ i with probability 1, then the first-best can be achieved bysetting d2 large enough.

3 If y1 + y2 = y some constant with probability 1, then the first-bestcan be achieved by setting d2 = y .

4 If i and y1 are deterministic, and r ≡ g(y2) where g(·) is a strictlyincreasing function, then the first-best can be achieved by settingd2 = y1 + g−1(i).

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 16 / 36

Long-term Debt The Firm’s Maximization Problem

First Order Condition

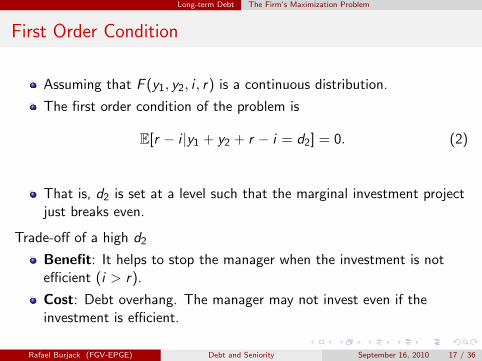

Assuming that F (y1, y2, i , r) is a continuous distribution.

The first order condition of the problem is

E[r − i |y1 + y2 + r − i = d2] = 0. (2)

That is, d2 is set at a level such that the marginal investment projectjust breaks even.

Trade-off of a high d2

Benefit: It helps to stop the manager when the investment is notefficient (i > r).

Cost: Debt overhang. The manager may not invest even if theinvestment is efficient.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 17 / 36

Long-term Debt The Firm’s Maximization Problem

First Order Condition

Assuming that F (y1, y2, i , r) is a continuous distribution.

The first order condition of the problem is

E[r − i |y1 + y2 + r − i = d2] = 0. (2)

That is, d2 is set at a level such that the marginal investment projectjust breaks even.

Trade-off of a high d2

Benefit: It helps to stop the manager when the investment is notefficient (i > r).

Cost: Debt overhang. The manager may not invest even if theinvestment is efficient.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 17 / 36

Long-term Debt The Firm’s Maximization Problem

Condition C and S.O.C.

Condition C

The left-hand side equation of equation (2),

E[r − i |y1 + y2 + r − i = d2]

is continuously differentiable on an interval [d2, d2]. Moreover, whenever(2) holds, it is also the case that

0 <∂

∂d2E[r − i |y1 + y2 + r − i = d2] < 1 (3)

Denote r − i = X and y1 + y2 = Y . Inequality (3) says thatE[X |X + Y = d2] increases with d2 but less than the amount of d2.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 18 / 36

Long-term Debt The Firm’s Maximization Problem

Proposition 3

Proposition 3

Suppose d2 is an optimum debt level.

1 If a dollar is added to every realization of y1, or added to everyrealization of y2 then d2 + 1 is a new optimum debt level.

2 Assume that Condition C holds, and that d2 is an interior optimum in[d2, d2] (in which case it is unique). If a small amount is added toevery realization of i or subtracted from every realization of r , thenthe optimum debt level strictly increases.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 19 / 36

Long-term Debt The Firm’s Maximization Problem

Proposition 3

Proposition 3

Suppose d2 is an optimum debt level.

1 If a dollar is added to every realization of y1, or added to everyrealization of y2 then d2 + 1 is a new optimum debt level.

2 Assume that Condition C holds, and that d2 is an interior optimum in[d2, d2] (in which case it is unique). If a small amount is added toevery realization of i or subtracted from every realization of r , thenthe optimum debt level strictly increases.

1 Intuition: An increase in yi gives the manager more cash to invest att = 1. Then his ability to borrow should be constrained: the debtlevel should rise.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 19 / 36

Long-term Debt The Firm’s Maximization Problem

Proposition 3

Proposition 3

Suppose d2 is an optimum debt level.

1 If a dollar is added to every realization of y1, or added to everyrealization of y2 then d2 + 1 is a new optimum debt level.

2 Assume that Condition C holds, and that d2 is an interior optimum in[d2, d2] (in which case it is unique). If a small amount is added toevery realization of i or subtracted from every realization of r , thenthe optimum debt level strictly increases.

1

2 Intuition: An increase in the mean of i , or a decrease in the mean ofr , implies that investments are less likely to be profitable, andtherefore the manager should be constrained with higher debt.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 19 / 36

Long-term Debt Example

Example

Let y1 and i be deterministic with y1 < i and

y2 ∼ N(µ2, σ

22

)r ∼ N

(µr , σ

2r

)

From F.O.C. we have

d2 = y1 + µ2 −σ22σ2r

[µr − i ]

Proposition 3 is OK.

Intuition If the manager’s ability to raise fresh capital at t = 1 isalmost entirely determined by the y1 and y2, then there is little pointin using d2 to screen out the bad new investments.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 20 / 36

Long-term Debt Example

Example

Let y1 and i be deterministic with y1 < i and

y2 ∼ N(µ2, σ

22

)r ∼ N

(µr , σ

2r

)From F.O.C. we have

d2 = y1 + µ2 −σ22σ2r

[µr − i ]

Proposition 3 is OK.

Intuition If the manager’s ability to raise fresh capital at t = 1 isalmost entirely determined by the y1 and y2, then there is little pointin using d2 to screen out the bad new investments.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 20 / 36

General Long-Term Security Structure The Security Structure

The General Contract

Now, we explore the possibility that more sophisticated long-term securitystructures than simple debt may be optimal.

The general contract is characterized by two functions (N(P),O(P))where P is the total amount paid to security-holders.

O(P) is the amount that the firm has promised at t = 0 to pay att = 2 to a single class of creditors. 0 ≤ O(P) ≤ P.

N(P) is the amount the manager can keep for new investors at t = 1in the attempt to finance new investment.

N(P) = P − O(P)

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 21 / 36

General Long-Term Security Structure The Security Structure

The General Contract

Now, we explore the possibility that more sophisticated long-term securitystructures than simple debt may be optimal.

The general contract is characterized by two functions (N(P),O(P))where P is the total amount paid to security-holders.

O(P) is the amount that the firm has promised at t = 0 to pay att = 2 to a single class of creditors. 0 ≤ O(P) ≤ P.

N(P) is the amount the manager can keep for new investors at t = 1in the attempt to finance new investment.

N(P) = P − O(P)

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 21 / 36

General Long-Term Security Structure The Security Structure

The General Contract

Now, we explore the possibility that more sophisticated long-term securitystructures than simple debt may be optimal.

The general contract is characterized by two functions (N(P),O(P))where P is the total amount paid to security-holders.

O(P) is the amount that the firm has promised at t = 0 to pay att = 2 to a single class of creditors. 0 ≤ O(P) ≤ P.

N(P) is the amount the manager can keep for new investors at t = 1in the attempt to finance new investment.

N(P) = P − O(P)

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 21 / 36

General Long-Term Security Structure The Security Structure

The manager at date 1

1 Given N(P), O(P) and y1, y2, r , i are realized.

2 Since y1 < i1 the manager can invest only if he can raise i − y1 fromthe market.

3 If he does invest,P = y2 + r

4 The most he can offer the market at t = 2 is

P − O(r + y2) = N(r + y2)

5 Then, the manager can invest if and only if

N(r + y2) ≥ i − y1

1We keep the Assumption 1 for the same reason. The Proposition 1 continues toapply.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 22 / 36

General Long-Term Security Structure The Security Structure

The manager at date 1

1 Given N(P), O(P) and y1, y2, r , i are realized.

2 Since y1 < i1 the manager can invest only if he can raise i − y1 fromthe market.

3 If he does invest,P = y2 + r

4 The most he can offer the market at t = 2 is

P − O(r + y2) = N(r + y2)

5 Then, the manager can invest if and only if

N(r + y2) ≥ i − y1

1We keep the Assumption 1 for the same reason. The Proposition 1 continues toapply.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 22 / 36

General Long-Term Security Structure The Security Structure

The slope of N(·)

We have allowed the slope of N(P) to be almost arbitrary.Nevertheless, we can restrict N(·) to have a slope at [0, 1].

Assumption M

The manager can commit himself at t = 1 to lower the return both of theinvestment project and of the assets in place.

For instance, by selling off some fraction of the assets at an artificiallylow price or by hiring extra workers.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 23 / 36

General Long-Term Security Structure The Security Structure

The slope of N(·)

We have allowed the slope of N(P) to be almost arbitrary.Nevertheless, we can restrict N(·) to have a slope at [0, 1].

Assumption M

The manager can commit himself at t = 1 to lower the return both of theinvestment project and of the assets in place.

For instance, by selling off some fraction of the assets at an artificiallylow price or by hiring extra workers.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 23 / 36

General Long-Term Security Structure The Security Structure

The slope of N(·)

(N is increasing) If N(P) is decreasing on P, the manager rises theamount he borrow at t = 1 by lowering the return of the investment.For instance, wasting resources.Thus, if one makes N more flat the investment will occur anyway butwith a higher return because the manager will not waste money.

Slope belongs to [0, 1] If it happens the manager can raise moremoney than he needs to finance the project and save the rest to payback.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 24 / 36

General Long-Term Security Structure The Security Structure

The slope of N(·)

(N is increasing) If N(P) is decreasing on P, the manager rises theamount he borrow at t = 1 by lowering the return of the investment.For instance, wasting resources.Thus, if one makes N more flat the investment will occur anyway butwith a higher return because the manager will not waste money.

Slope belongs to [0, 1] If it happens the manager can raise moremoney than he needs to finance the project and save the rest to payback.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 24 / 36

General Long-Term Security Structure The Security Structure

The new problem

maxN(·)

∫N(r+y2)≥i−y1(r − i)F (y1, y2, i , r) (4)

s.t.

0 ≤ N(P) ≤ P (5)

0 ≤ N(P+)− N(P−) ≤ P+ − P− for all P− ≤ P+ (6)

Is all the flexibility afforded by this general security structure useful?

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 25 / 36

General Long-Term Security Structure The Security Structure

The new problem

maxN(·)

∫N(r+y2)≥i−y1(r − i)F (y1, y2, i , r) (4)

s.t.

0 ≤ N(P) ≤ P (5)

0 ≤ N(P+)− N(P−) ≤ P+ − P− for all P− ≤ P+ (6)

Is all the flexibility afforded by this general security structure useful?

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 25 / 36

General Long-Term Security Structure The Standard Package

The Standard Package

Our next task is to show that our general security structure N(P) canbe represented by a ”standard package” of securities.

The Standard Package

A standard package of debt and equity consists of n classes of debt and asingle class of equity.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 26 / 36

General Long-Term Security Structure The Standard Package

The Standard Package

Our next task is to show that our general security structure N(P) canbe represented by a ”standard package” of securities.

The Standard Package

A standard package of debt and equity consists of n classes of debt and asingle class of equity.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 26 / 36

General Long-Term Security Structure The Standard Package

The Standard Package

The are n classes of debt. The jth class is characterized by:

D j that must be paid to class j at t = 2 and;∆D j the maximum additional amount of indebtedness to class j thatthe firm can take on at date 1.

The firm also can borrow from market the (n + 1)th class of debt att = 1. Which is junior to all existing debt, but senior to equity.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 27 / 36

General Long-Term Security Structure The Standard Package

The Standard Package

The are n classes of debt. The jth class is characterized by:

D j that must be paid to class j at t = 2 and;∆D j the maximum additional amount of indebtedness to class j thatthe firm can take on at date 1.

The firm also can borrow from market the (n + 1)th class of debt att = 1. Which is junior to all existing debt, but senior to equity.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 27 / 36

General Long-Term Security Structure The Standard Package

The Standard Package

Figure: The Shape of the Function N(P)

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 28 / 36

General Long-Term Security Structure The Standard Package

Back to the Example

In the Example, we had;

n = 1 D1 = d2

∆D1 = 0 N(P) = max(P − d2, 0)

If P < d2, all of P must be given to senior debt-holders, and there isnone for new investors.

On the other hand, for P > d2, the firm can issue junior debt andgive N(P) = P − d2 to new investors.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 29 / 36

General Long-Term Security Structure The Standard Package

Back to the Example

In the Example, we had;

n = 1 D1 = d2

∆D1 = 0 N(P) = max(P − d2, 0)

If P < d2, all of P must be given to senior debt-holders, and there isnone for new investors.

On the other hand, for P > d2, the firm can issue junior debt andgive N(P) = P − d2 to new investors.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 29 / 36

General Long-Term Security Structure The Standard Package

Back to the Example

In the Example, we had;

n = 1 D1 = d2

∆D1 = 0 N(P) = max(P − d2, 0)

If P < d2, all of P must be given to senior debt-holders, and there isnone for new investors.

On the other hand, for P > d2, the firm can issue junior debt andgive N(P) = P − d2 to new investors.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 29 / 36

General Long-Term Security Structure The Standard Package

Proposition 4

Proposition 4

If i and y1 are deterministic, then simple debt/equity is optimal.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 30 / 36

General Long-Term Security Structure The Standard Package

Assumption F

Now we want to show the conditions to achieve the first-best when y1and i are stochastic.

Assumption F

F (y1, y2, i , r) is continuously distributed

The joint density function f (P,N) of P = (r + y2) and N = (i − y1)is strictly positive everywhere in the set

T ≡{

(P,N)| P ≤ P ≤ P; 0 ≤ N ≤ P},

where P and P are respectively the minimum and maximum possiblevalue of r + y2

T is the only set that the manager can invest.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 31 / 36

General Long-Term Security Structure The Standard Package

Assumption F

Now we want to show the conditions to achieve the first-best when y1and i are stochastic.

Assumption F

F (y1, y2, i , r) is continuously distributed

The joint density function f (P,N) of P = (r + y2) and N = (i − y1)is strictly positive everywhere in the set

T ≡{

(P,N)| P ≤ P ≤ P; 0 ≤ N ≤ P},

where P and P are respectively the minimum and maximum possiblevalue of r + y2

T is the only set that the manager can invest.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 31 / 36

General Long-Term Security Structure The Standard Package

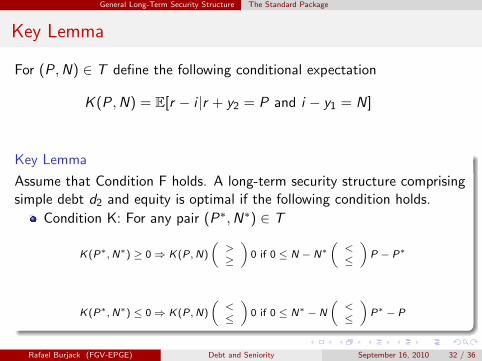

Key Lemma

For (P,N) ∈ T define the following conditional expectation

K (P,N) = E[r − i |r + y2 = P and i − y1 = N]

Key Lemma

Assume that Condition F holds. A long-term security structure comprisingsimple debt d2 and equity is optimal if the following condition holds.

Condition K: For any pair (P∗,N∗) ∈ T

K(P∗,N∗) ≥ 0⇒ K(P,N)

(>≥

)0 if 0 ≤ N − N∗

(<≤

)P − P∗

K(P∗,N∗) ≤ 0⇒ K(P,N)

(<≤

)0 if 0 ≤ N∗ − N

(<≤

)P∗ − P

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 32 / 36

General Long-Term Security Structure The Standard Package

Key Lemma

Intuition first the equation K (·):

K (P,N) = E[r − i |y1 + y2 + r − i = P − N and i − y1 = N]

If the project’s profit r − i rises with both the total net profit P − Nand the external financing requirement N, then Condition K will hold.

Also, implies that there is a cutoff value of P, say P∗, such that theexpected value of a marginal date-1 investment is negative(respectively, positive) if P < P∗ (P > P∗).

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 33 / 36

General Long-Term Security Structure The Standard Package

Proposition 5

Proposition 5

Assume that Assumption F holds. A long-term security structurecomprising simple debt d2 and equity is optimal if:

1 i is deterministic

2 y1 is distributed independently of y2 and r ;

3 E[r |r + y2 = P] is strictly increasing in P, for P ≤ P ≤ P

Intuition: When i is fixed, new investment should not occur for lowvalues of r + y2, since this means low r , on average;

whereas the investment should go ahead for high values of r + y2. Asimple debt/equity security structure implements this quite well.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 34 / 36

General Long-Term Security Structure The Standard Package

Proposition 6

Proposition 6

Assume that Condition F holds. If

1 r is deterministic,

2 y2 is independent of y1 and i and

3 E[i |i − y1 = N] is strictly increasing in N, for P ≤ N ≤ P

Then it is optimal at t = 0 to issue two classes of debt:

a negligible amount of senior debt, with an option to borrow a finiteamount of additional debt of the same seniority at date 1(d1 u 0,∆d1 > 0);

and a large amount of a second class of debt with no option toborrow any more (d2 =∞,∆d2 = 0).

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 35 / 36

General Long-Term Security Structure The Standard Package

Proposition 6

The manager can raise N(P) = min(P,∆d1)

Intuition: Given a fixed r, low (respectively, high) values of i representgood (bad) investment opportunities and should be encouraged(discouraged). To this end, the manager is given an ”overdraftfacility” of ∆d1.

Rafael Burjack (FGV-EPGE) Debt and Seniority September 16, 2010 36 / 36