De Nederlandse Mededingingsautoriteit - acm.nl Nederlandse Mededingingsautoriteit ... disruptive...

34

De Nederlandse Mededingingsautoriteit Market Assessment for ProRail ICT-Systems in Traffic Control Den Haag/Hamburg, June 2008 BSL Management Consultants GmbH & Co. KG

Transcript of De Nederlandse Mededingingsautoriteit - acm.nl Nederlandse Mededingingsautoriteit ... disruptive...

De Neder landse Mededingingsautoriteit

Market Assessm ent for ProRail I CT-System s in Traffic Cont rol

Den Haag/Hamburg, June 2008

BSL Managem ent Consultan ts Gm bH & Co. KG

Page 20282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

Execut ive sum m ary

This analysis on behalf of NMa provides an assessm ent of the m arket for I CT-system s for t raffic cont rol with regard to ProRail. I t has looked at relevantm arkets from an internat ional perspect ive, their funct ioning and com pet it ivenessand t rends for future developm ents.

A view is also taken at ProRail's procurem ent approach for supply and m ainte-nance of hard- and software in this context . Risks and opportunit ies thereof forthe qualit y of ProRail's perform ance are related to internat ional experience.

The assessm ent is based on a broad range of collected evidence, both in TheNetherlands and internat ionally. Part icular emphasis is on current pract ices inother railway system s and a direct view on the m arket from the perspect ive ofkey-suppliers and service-providers them selves.

At the subm arket of hardware equipm ent , railways can part icipate on a highlyeff icient , global compet it ion for standard components, if appropriate condit ionsare set in tendering.

The m arket for software applicat ions however is not a classical, m ature m arket inthe sense of relat ively standardized applicat ions ( "products") . Individual case-by-case solut ions st ill dominate the scenery in Europe, while t rends towards m orestandardisat ion are in their infancy.

Hence, the or igin and market -presence of key-suppliers is internat ional. Theleading-edge of them pushes the use of cost-eff icient , indust r ial standard plat -forms, also from other sectors like aviat ion, for customisat ion on the individualrequirem ents and varying operat ional needs of railways. This gives also thesoftware m arket to a growing extent not only a European, but a global dim ension.On the other hand, the European effort s to im pose som e standards " from above"are widely seen as a longer- term issue that will not imm ediately change demandpat terns and m arket behaviour.

Today's role of ProRail at these m arkets is the one of a buyer, who is st ill facedwith legacy I CT-system s for t raffic-control which were developed in-house m orethan two decades ago. These system s are perceived by m any indust ry-observersto be at the end of their lifespan. Although they are not the single-m ost importantcause of t raff ic perturbat ions in the Dutch railway system , they nevertheless havea st rong and highly visible im pact for the general public due to the som et im esdisrupt ive nature of incidents on operat ions.

I n a recovery effort from a significant spin-off of system knowledge in the contextof the Dutch railway reform in the ninet ies, ProRail has taken im portant steps tobring the system s back into bet ter cont rol. These were nam ely the reassem bly of

BSL Managem ent Consultan ts Gm bH & Co. KG

Page 30282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

an in-house knowledge-base to define system requirem ents for railway operat ionsand the stepwise redevelopm ent of key-m odules in order to bring I CT-system sback to a state of well defined and docum ented qualit y.

ProRail already procures the developm ent of system m odules on an open,com petit ive basis from the internat ional m arket and subsequent ly integrates itinto its present architecture. I t should go further into this direct ion and preventit self from a react ion of "falling-back" to overly excessive in-house st rategies.

ProRail can grasp opportunit ies from market -developments and technology- t rendsand push them act ively for it s own benefit . Experiences from other Europeanrailways, which developed their core I CT-systems for t raff ic-cont rol in decisiveand am bit ious ways, should encourage ProRail t o explicit ly consider furthersystem enhancem ents, that clear ly prom ise a path to bet ter system reliabilit y asby cost -efficient use of indust rial standards, m ore upward com pat ibilit y withongoing technical innovat ions but also, and very im portant ly for The Netherlands,the exploitat ion of som e capacity reserves for the exist ing network infrast ructure.

Page 40282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

Content

1. Background and Object ives 5

2. Met hod of Approach 7

3. Scope of Analysis 8

4. ProRail's t raffic cont rol systems and supplier m arkets 10

4.1 Genesis of system s and suppliers 10

4.2 New st rategy for procurem ent and m arket interact ion 12

4.3 Current use of m arkets by ProRail 14

5. I nternat ional Market Overview 16

5.1 Demand-side 16

5.2 Supply-side 17

6. Market Trends and Developm ents 23

6.1 Demand-side 23

6.2 Supply-side 27

7. I m plicat ions for ProRail 28

8. Conclusions 32

Page 50282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

1 . Background and Object ives

ProRail is a state-owned com pany supervised by the Ministry of Transport( "Minister ie van Verkeer en Waterstaat ") , which holds the business concession ofthe Government of The Netherlands to m anage the Dutch railway network. Aspart of the governm ents' oversight , a working group of the "vaste commissie voorVerkeer en Waterstaat " presented a set of suggest ions, the so-called report "Opde Rails", in 2005 to im prove the perform ance of ProRail. Two years later ProRailprovided a report on proceedings related to these suggest ions, the so-called "Opde Rails progress report " .

I n addit ion, the High Com mission asked the Minist ry to init iate an exam inat ionabout the efficiency and effect iveness of ProRail as a react ion to perturbat ions int raffic cont rol system s – Ut recht and Rot terdam in February 2007 and Am sterdamin March 2007. Two act ivit ies were thereupon launched:

a second opinion about the "Op de Rails progress report " , which was providedin the m eant im e by McKinsey & Com pany,

an assessm ent of (supplier) m arkets for the development and m aintenance ofI nform at ion and Com municat ion Technology ( ICT) in t raffic cont rol by BSL onbehalf of The Netherlands' Compet it ion Authority (Nederlandse Mededingings-autoriteit , "NMa") .

Findings of this assessm ent are summ arised in the following report . I nterfacesbetween the two act iv it ies were discussed mutually between McKinsey and BSL.

Based on the NMa-specif icat ion, the object ives for the t raffic cont rol I CT-m arketassessm ent are

t o determine the com pet it iveness of the respect ive (sub- )m arkets forsystem developm ent and m aintenance,

to provide a judgement about r isks for quality , pr ice and system com pat ibilit yin the case that the m arket was not considered being sufficient ly com pet it ive.

Am ong others the following quest ions were considered as guidelines for theassessm ent :

Which are the relevant m arkets (both in terms of products and geography)that serve ProRail t o obtain their products and serv ices for I CT systems int raffic cont rol? (chapter 4)

How important is the different iat ion between hardware for installat ion andoperat ion of I CT-system s on the one hand and software for the system devel-opment and m aintenance on the other? (chapter 5)

Page 60282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

Who – explicit ly – are the suppliers and custom ers? To what extent do theyact domest ically or internat ionally? ( chapter 5)

Which significant developm ents and t rends can be ident if ied and what is theirpotent ial im pact on the effect iveness of the m arket , e.g. possible ent r ies andexits of m arket players? (chapter 6)

What are ent ry barriers for the various sub-markets, e.g. intellectual propertyr ights or governm ental regulat ions? (chapter 6)

How com pat ible are com ponents and services provided by different suppliers?How im portant is com pat ibilit y for the effect iveness of the m arket? Which riskscan be ident if ied and how can they be mit igated? (chapter 6)

How do current procurem ent and cont ract ing pract ices im pact prices and thespeed of delivery? What can be done to im prove m arket -effect iveness? Whatcan be learned by other infrast ructure m anagers internat ionally in this re-spect? (chapter 7)

The assessm ent builds on an analysis of the system s and suppliers as well as thecurrent procurement by ProRail on the one hand and on the evaluat ion of selectedinternat ional "good-pract ice" exam ples on the other.

Page 70282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

2 . Method of Approach

Based on a com bined approach of the dom est ic situat ion in The Netherlands andinternat ional good-pract ice analysis, the study is built on three m odules.

00

8\P

roje

kte

_2

00

8\0

28

20

01

_N

Ma

_IC

T-S

yst

em

e\R

ep

ort\

02

82

00

1_

Cha

rts_

fue

r_R

ep

ort

.pp

tL

Ma

na

gem

en

t C

on

sult

an

ts G

mb

H &

Co

. K

G

Systemconfigurat ion

Sourcing &procurement

Interviewswith ProRailand current

suppliers

Cont ractprocedureevaluat ion

Supplier 'sperspect ive

I nterviewswith rail-ways andregulators

Customer 'sperspect ive

I nterviewswith

internat ionalsuppliers

ProRail's I CT- landscape I nterna t ional good pract ice

"Lessons lea rned"

Status quoand

out look

Transfe-rabilit y

Outline forProRail's future

market approach

1 2

3

Figure 1: General approach in three separate modules

Module 1 provides in a first part an overview of ProRail's I CT-core applicat ions int raffic control with some at tent ion to their development background and futurechallenges. The second part of this m odule is a descript ion of the I CT- related"sourcing behaviour" of ProRail and an assessment of it s appropriateness to m eetfuture challenges and to obtain products and services in line with internat ionalperform ance standards.

I nform ation was gathered from interviews with technical and procurem ent expertsfrom ProRail's I CT-departm ent , the cent ral procurem ent unit ( "AKI ") , the recent lycreated unit for system m aintenance ( "Beheer non stop", BNS) , NS Reizigers asthe largest operator on the network and the legacy-system m aintainer TriBaseand the IT-com pany Logica as selected business partners of ProRail.

I n the parallel m odule 2, internat ional pract ice was studied in a selected sam pleof European countr ies. I nterviews were conducted with several experts of SwissFederal Railways (SBB) , Germ an Federal Railways (DB AG) , the Spanish infra-st ructure manager ADI F, the Swedish infrast ructure m anager Banverket and tocom plem ent the picture with the European Com m ission (DG TREN) as dr ivingforce for standardisat ion issues.

Page 80282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

Supplementary to the discussions with railways, an exchange with applicat ion andsoftware providers, expert developers and system integrators was conductedabout t heir respect ive views. I nterviews on this behalf covered representat ives of( in alphabet ical order) Accenture, CSC, Funkwerk, Indra, Ster ia and Thales.

This m odule led to an overview of m arket t rends, an external view of ProRail'sI CT-situat ion and an internat ional appraisal of market developm ent st rategies.

Module 3 then draws conclusions about relevant m arkets, their characterist ics andt rends and the result ing im plicat ions for ProRail.

Market analysis refers specifically to software applicat ions and hardware of thesystems. For both sub-markets supply and development on the one hand andm aintenance services on the other are considered.

At tent ion is given to characterist ics of these m arkets, like the set of relevantbuyers (being m ainly state owned rail infrast ructure companies) , the set ofsuppliers in each m arket , degrees of product standardisat ion and specifics of them arket for m aintenance services.

Thereby m odule 3 is ult im ately leading to im plicat ions and suggest ions for thefuture approach of ProRail to deal with the relevant I CT-m arkets.

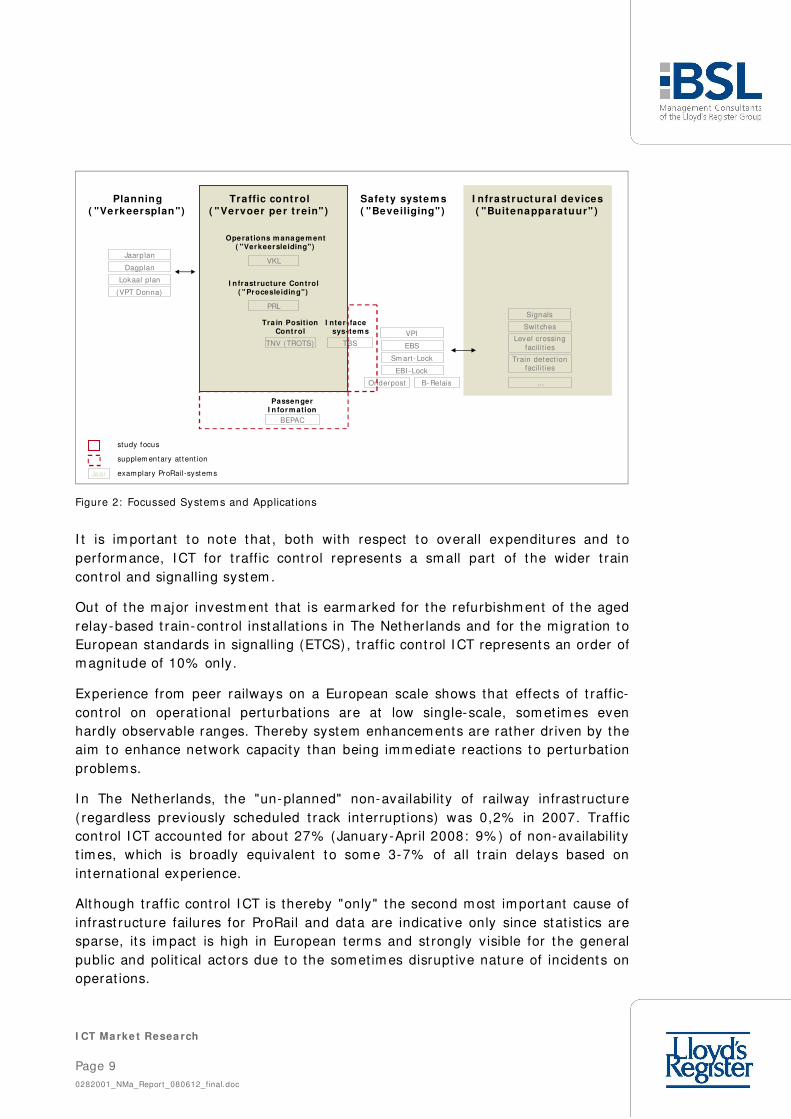

3 . Scope of Analysis

The study concent rates on the supply and the m aintenance of I CT-com ponentswhich are direct ly relevant for qualit y of t raffic operat ions, albeit with som econsiderat ion to inter faces with neighbour ing system s (see figure 2) .

The related com ponents are m ainly t raffic control funct ions, which are covered atProRail by the system fam ily called "Vervoer per Trein" (VPT). Core funct ionalit iescom prise the operat ions m anagem ent ( "Verkeersleiding") and the correspondingm anagem ent of route set t ing infrast ructure ( "Procesleiding") .

The m arket analysis therefore has a focussed scope com pared to the widerexaminat ion of processes at ProRail which was sim ultaneously carr ied-out byMc Kinsey on behalf of the Minist ry of Transport .

Page 90282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

study focus

supplem entary at tent ion

PassengerI n form ation

Operat ions m anagem ent( "Verkeersleiding")

Traffic cont rol( "Vervoer per t rein" )

Safe ty system s( "Beveiliging")

I nfra struct ura l devices( "Buitenapparatuur" )

Tra in Posit ionCont rol

I nter- facesys- tem s

I nfrast ructure Control( "Procesleiding")

VPI

EBS

Sm art - Lock

EBI -Lock

Onderpost B- Relais

Signals

Switches

Level crossingfacil i ties

…

Train detect ionfacil i ties

BEPAC

Planning( "Ve rkeersplan")

(VPT Donna)

Jaarplan

Dagplan

Lokaal plan

VKL

PRL

TNV (TROTS) TBS

Jaar examplary ProRail-system s

Figure 2: Focussed Systems and Applicat ions

I t is im portant to note that , both with respect to overall expenditures and toperform ance, I CT for t raffic cont rol represents a sm all part of the wider t raincont rol and signalling system .

Out of the m ajor investm ent that is earm arked for the refurbishm ent of the agedrelay-based t rain-control installat ions in The Nether lands and for the migrat ion toEuropean standards in signalling (ETCS) , t raffic cont rol I CT represents an order ofm agnitude of 10% only.

Experience from peer railways on a European scale shows that effects of t raffic-cont rol on operat ional perturbat ions are at low single-scale, som et im es evenhardly observable ranges. Thereby system enhancem ents are rather dr iven by theaim to enhance network capacity than being imm ediate react ions to perturbat ionproblems.

I n The Netherlands, the "un-planned" non-availability of railway infrast ructure( regardless previously scheduled t rack interrupt ions) was 0,2% in 2007. Trafficcont rol ICT accounted for about 27% (January-Apr il 2008: 9% ) of non-availabilityt im es, which is broadly equivalent to som e 3-7% of all t rain delays based oninternat ional experience.

Although t raffic cont rol I CT is thereby "only" the second m ost im portant cause ofinfrast ructure failures for ProRail and data are indicat ive only since stat ist ics aresparse, it s im pact is high in European terms and st rongly visible for the generalpublic and polit ical actors due to the somet im es disrupt ive nature of incidents onoperat ions.

Page 100282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

4 . ProRail's t raffic control system s and supplier m arkets

4 .1 Genesis of system s and suppliers

I n order to understand ProRail's current t raffic cont rol system landscape ( "VPT")and the posit ion of incum bent suppliers som e at tent ion to it s genesis is useful.

The VPT- landscape was or iginally an in-house developm ent of "NederlandseSpoorwegen" (NS) , init iated in the mid-eight ies and rolled-out between 1994 and2000. The system architecture reflects the then integrated st ructure of NS.Besides key- funct ions of t rain path allocation and t rain cont rol, several subsys-tems cover imm ediate cont rol of infrast ructural devices and also operator- relatedissues as the planning of t rain-crew rosters.

I n order to connect VPT with the exist ing, st rongly diversif ied system s on thesafety level, var ious kinds of regionally specific interfaces becam e necessary. Thisled – am ong other reasons - to a high degree com plexit y of configurat ions andheterogeneit y of data-m odels, which turned out to be a notor ious problem for therobustness of the system .

I n the context of railway rest ructuring in The Netherlands, which took place inparallel with the roll- out of VPT in the mid-ninet ies, previously internal funct ionsof NS were spun-off into the m arket . This refers also to the sector of t rafficcont rol. Considerable shares of experts, who part icipated in the VPT-developm ent ,were taken over by pr ivate com panies, am ong them

t he NS "Cent rum voor Inform at ieverwerking" (CVI ) , which was acquired byEDS, a global US-com pany with m ore than 9.000 IT-professionals world-widewithin the t ransportat ion sector alone. EDS was granted a 10-year sales guar-antee in this context , which was part ly fulfilled by cont racts from ProRail withregard to VPT,

the form er in-house "NS I ngenieursbureau", which was spun-off as "HollandRail Consult " (now "Movares" with joint venture " I nt raffic") and

NS subsidiary Art icon, which was sold to Arcadis.

Subsequent ly, ProRail had to rely on these suppliers for the developm ent of newapplicat ions and VPT-releases whilst in-house com petence on the subject wasdepleted. This had significant ly shaped the Dutch m arket and is im portant tounderstand the current situat ion.

The m aintenance of VPT was em bedded (1997) into cont racts with Volker Rail,St ructon and BAM, that covered the servicing of the ent ire rail infrast ructurewithin defined regions. Since regional I CT m aintenance-units turned out to be

Page 110282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

( too) sm all in term s of economics and knowledge and since interfaces betweenregional responsibilit ies were difficult to handle, act ivit ies were bundled into an"umbrella organisat ion" in 1998/ 99, of which Volker Rail, Structon and BAM werethe shareholders. The TriBase-consort ium emerged out of this organisat ion oneyear later.

Since then TriBase was the single-source supplier of ProRail for I CT systemm aintenance on the basis of annual cont racts. I n 2004, a 5-year lum p sumcont ract was agreed upon. Under this cont ract a defined m aintenance qualit y-standard based on agreed "performance indicators" was to be assured.

However, system s deteriorated to a state of perturbat ions that heavily affectedt rain operat ions on the network. ProRail's stat ist ics of system failures indicate thatm ore than once a week a new type of problem is detected that – even if m ost lynot fatal - requires root -cause analysis, redesign and eventually the roll-out of asystem release to solve it . This indicates that there are system s within the DutchVPT- landscape which in their current state do no longer m eet good-pract icestandards in Europe. The architecture and key-m odules are seen to be at the endof their life-cycle by several m arket observers.

However, besides the funct ioning of software the spect rum of underlying causesfor perturbat ions deals with a wider range of

m aintenance and upgrade works on I CT, which are affected by incom pletedocumentat ion and a lim ited test ing environm ent to predict system behaviour,

hardware- related issues, as a damaged hard disk being the st art ing point forthe Am sterdam breakdown in March 2007 and

energy and comm unicat ion networks, which are in an ongoing process ofadvancem ent e.g. by replacem ent of copper by fibre opt ic cables.

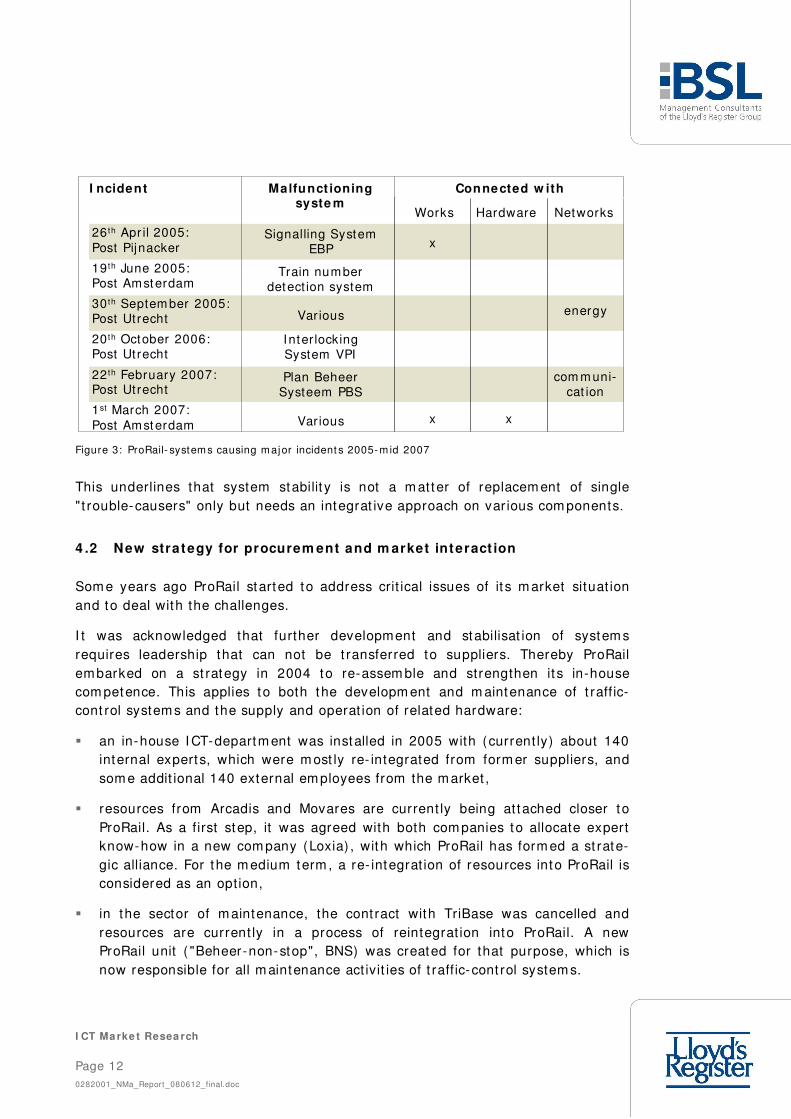

An evaluat ion of reports about the m ost relevant perturbat ions in the period from2005 unt il m id 2007 shows a variety of systems, which init ially caused theincidents (see figure 3) .

Page 120282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

26 th Apr il 2005:Post Pijnacker

19 th June 2005:Post Amsterdam

30 th Septem ber 2005:Post Utrecht

20 th October 2006:Post Utrecht

22 th February 2007:Post Utrecht

1st March 2007:Post Amsterdam

Malfunct ioningsyste m

Works Hardware Networks

Signalling SystemEBP

Train numberdetect ion system

Various

Inter lockingSystem VPI

Plan BeheerSysteem PBS

Various

x

energy

xx

com m uni-cat ion

I ncident Connected w ith

Figure 3: ProRail- system s causing m ajor incident s 2005- m id 2007

This underlines that system stabilit y is not a m atter of replacem ent of single"t rouble-causers" only but needs an integrat ive approach on var ious com ponents.

4 .2 New strategy for procurem ent and m arket interact ion

Som e years ago ProRail started to address crit ical issues of it s m arket situat ionand to deal with the challenges.

I t was acknowledged that further development and stabilisat ion of system srequires leadership that can not be t ransferred to suppliers. Thereby ProRailembarked on a st rategy in 2004 to re-assem ble and strengthen it s in-housecom petence. This applies to both the developm ent and m aintenance of t raff ic-cont rol systems and the supply and operat ion of related hardware:

an in-house I CT-departm ent was installed in 2005 with (current ly) about 140internal experts, which were m ost ly re- integrated from form er suppliers, andsom e addit ional 140 external em ployees from the m arket ,

resources from Arcadis and Movares are current ly being at tached closer toProRail. As a first step, it was agreed with both com panies to allocate expertknow-how in a new com pany (Loxia) , with which ProRail has form ed a st rate-gic alliance. For the m edium term , a re- integrat ion of resources into ProRail isconsidered as an option,

in the sector of m aintenance, the cont ract with TriBase was cancelled andresources are current ly in a process of reintegrat ion into ProRail. A newProRail unit ( "Beheer-non-stop", BNS) was created for that purpose, which isnow responsible for all m aintenance act ivit ies of t raffic-cont rol system s.

Page 130282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

I n doing so ProRail put it self in a posit ion to re-gain system leadership andinit iated fundam ental reor ient at ion of its procurem ent strategy.

I CT-products and services which are current ly bought on the m arket undercompet it ive European tendering from internat ional bidders are

Hardware installat ions (as server, PC's and related equipm ent )

Software programming (as the re-development of applicat ions)

Maintenance services for hardware (as planned for the operat ion of the DoubleNat ional Com puter Cent re DNCC, which im plementat ion will start in 2008)

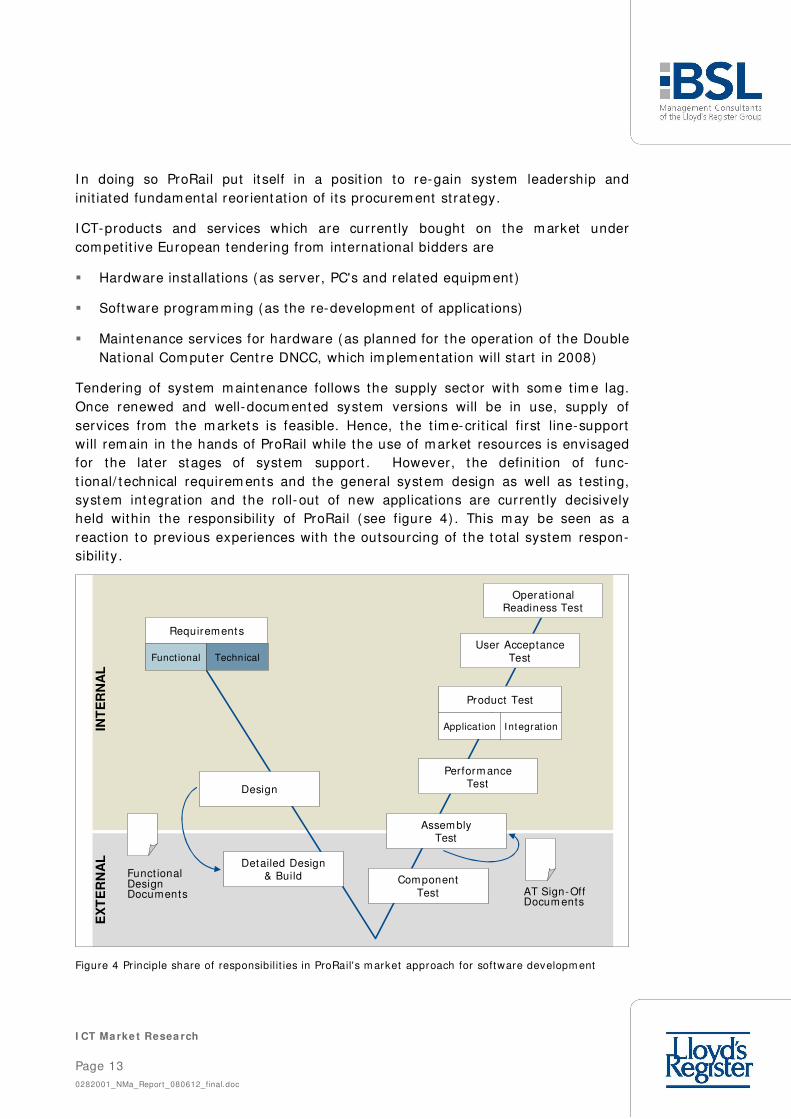

Tendering of system m aintenance follows the supply sector with som e t im e lag.Once renewed and well-docum ented system versions will be in use, supply ofservices from the m arkets is feasible. Hence, the t im e-crit ical first line-supportwill rem ain in the hands of ProRail while the use of m arket resources is envisagedfor the later stages of system support . However, the definit ion of func-t ional/ technical requirem ents and the general system design as well as test ing,system integrat ion and the roll- out of new applicat ions are current ly decisivelyheld within the responsibility of ProRail (see figure 4) . This m ay be seen as areact ion to previous experiences with the outsourcing of the total system respon-sibility .

INT

ER

NA

LE

XT

ER

NA

L

AT Sign-OffDocum ents

Operat ionalReadiness Test

User AcceptanceTest

Requirements

Funct ional Technical

Product Test

Applicat ion I ntegrat ion

Perform anceTest

AssemblyTest

ComponentTest

Detailed Design& Build

Design

Funct ionalDesignDocuments

Figure 4 Pr inciple share of responsibil it ies in ProRail's m arket approach for software developm ent

Page 140282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

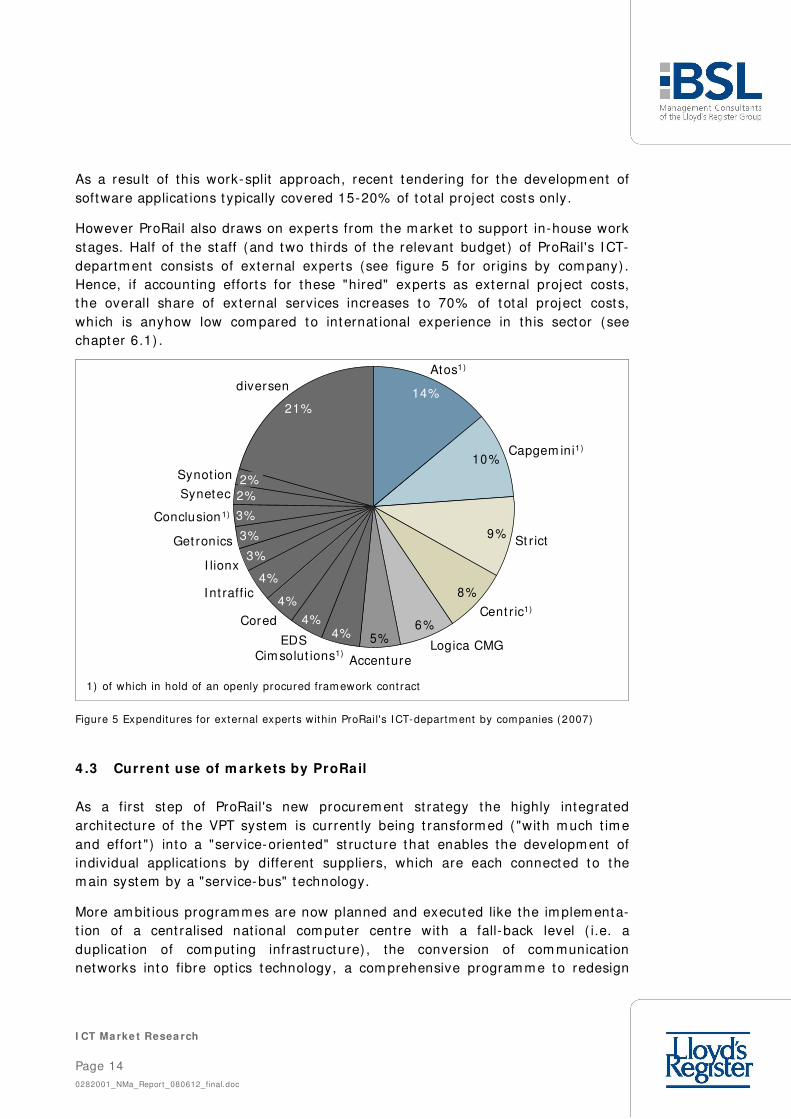

As a result of this work-split approach, recent tendering for the developm ent ofsoftware applicat ions t ypically covered 15-20% of total project cost s only.

However ProRail also draws on experts from the m arket to support in-house workstages. Half of the staff (and two thirds of the relevant budget ) of ProRail's I CT-departm ent consists of external experts (see figure 5 for or igins by com pany) .Hence, if account ing effort s for these "hired" experts as external project costs,the overall share of external services increases to 70% of total project costs,which is anyhow low com pared to internat ional experience in this sector (seechapter 6.1) .

5%6%

8%

9%

10%

14%

Atos1)

Capgem ini1)

St r ict

Cent r ic1)

Logica CMGAccenture

4%

Cim solut ions1)

4%

3%Conclusion1)

2%Synetec2%Synot ion

21%

diversen

EDS

4%

Cored

4%Int raffic

3%I lionx

3%Get ronics

Data base: 2 0 07

1) of which in hold of an openly procured fram ework cont ract

Figure 5 Expenditures for external experts within ProRail's I CT-departm ent by com panies (2007)

4 .3 Current use of m arkets by ProRail

As a first step of ProRail's new procurem ent st rategy the highly integratedarchitecture of the VPT system is current ly being t ransform ed ( "with m uch t im eand effort ") into a "service-oriented" st ructure that enables the developm ent ofindividual applicat ions by different suppliers, which are each connected to them ain system by a "service-bus" technology.

More am bit ious programm es are now planned and executed like the im plem enta-t ion of a cent ralised nat ional com puter centre with a fall-back level ( i.e. aduplicat ion of com put ing infrast ructure) , the conversion of com municat ionnetworks into fibre opt ics technology, a com prehensive program m e to redesign

Page 150282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

t he process of slot -allocat ion and operat ional guidance ( "Herm an") and a pro-gram m e for the rebuilding of t rain cont rol systems for route set t ing processes( "Astr is" ) . I n 2008 investm ents for IT will r ise from 48 m illion € (2007) to90 m illion €.

Under this program m e, the work-stages from technical system design to pro-gram ming and com ponent tests of software-applicat ions are planned and carried-out by suppliers which were chosen by public tender procedures.

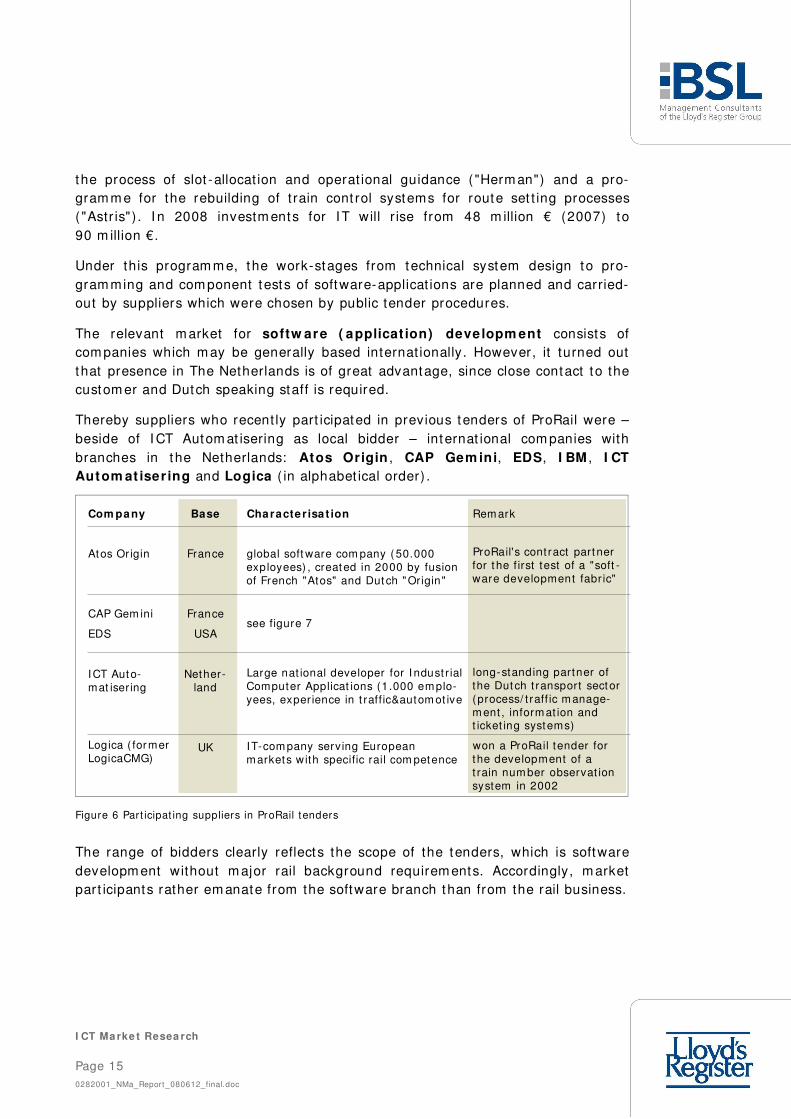

The relevant m arket for softw are ( applicat ion) developm ent consists ofcom panies which m ay be generally based internat ionally. However, it turned outthat presence in The Netherlands is of great advantage, since close contact to thecustom er and Dutch speaking staff is required.

Thereby suppliers who recent ly part icipated in previous tenders of ProRail were –beside of I CT Autom at isering as local bidder – internat ional com panies withbranches in the Netherlands: Atos Origin , CAP Gem ini, EDS, I BM , I CT

Autom at iser ing and Logica ( in alphabet ical order) .

Com pany

Atos Origin

CAP Gem ini

EDS

ICT Auto-mat iser ing

Logica ( formerLogicaCMG)

Base

France

France

USA

Nether-land

UK

Character isa t ion

global soft ware com pany (50.000exployees) , created in 2000 by fusionof French "Atos" and Dut ch "Origin"

see figure 7

Large nat ional developer for I ndust r ialComputer Applicat ions (1.000 emplo-yees, exper ience in t raffic&autom ot ive

IT-com pany serving Europeanmarkets with specific rail com petence

Rem ark

ProRail's cont ract part nerfor t he f irst test of a "soft -ware development fabr ic"

long-standing partner ofthe Dutch t ransport sector(process/ t raff ic manage-m ent , inform at ion andt icket ing systems)

won a ProRail tender forthe development of at rain num ber observat ionsystem in 2002

Figure 6 Part icipat ing suppliers in ProRail tenders

The range of bidders clearly reflects the scope of the tenders, which is softwaredevelopm ent without m ajor rail background requirem ents. Accordingly, m arketpart icipants rather em anate from the software branch than from the rail business.

Page 160282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

The relevant m arket for hardw are-equipm ent has to be considered in anotherway.

The m ost recent m ajor ProRail- tender of this kind has been procured on anegot iated basis to Hewlet t Packard in 2007. However, this was declared to beexcept ional because of special com pat ibilit y reasons and t im e-const raints fordelivery.

I n general, it is recognised that systems have to be ready for easy swit ches toeach new generat ion of technology standards that com e up on the m arket .Thereby ProRail is able to m ake use of the global market for standard equipm ent ,which covers effect ively all suppliers of business com put ing (see chapter 5 fornam es) .

5 . I nternat ional Market Overview

5 .1 Dem and-side

The dem and-side of the European m arket for t raffic cont rol systems is form ed byrailway infrast ructure m anagers respect ively integrated railway com panies.

A widespread percept ion prevails am ong them to have each unique condit ions andrequirem ents that do not allow for the use of "pre- fabricated" products. I CT-m arkets are rather expected to supply individual solut ions than to be classical,m ature m arkets in the sense of relat ively standardised applicat ions. Thereby thedemand-side of the m arket is st ill relat ively "dom est ic" in its nature.

Est im at ions about the m arket volum e for t raffic cont rol systems with accordingtechnical installat ions and data networks are in the order of m agnitude of annually400 mio. € on a European scale.

Current ly urban rail system s account for a third of the m arket . However, theshare of the heavy rail sector will grow over the next years, since saturat ion ofm ain lines increases the dem and for applicat ions to exploit capacity- reserves.

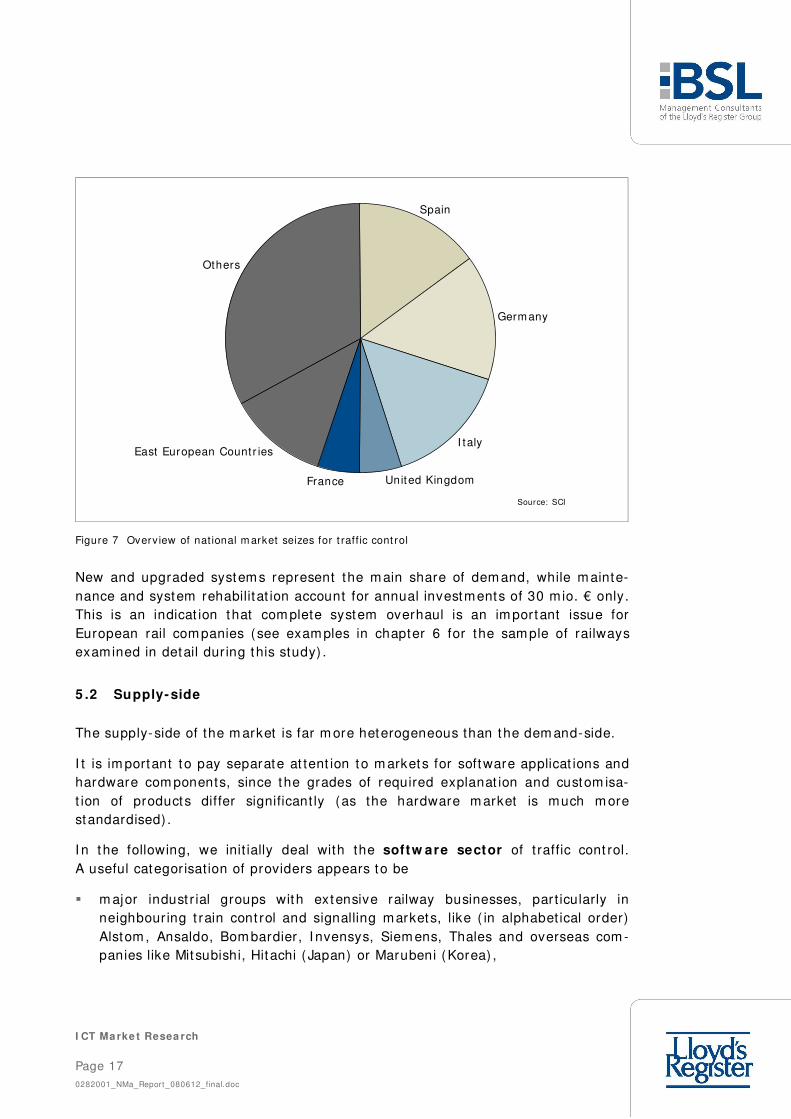

The m ost im portant nat ional m arkets are Germ any, I taly and Spain, which eachaccount for annual m arket volum es of about 65 m io. € according to a recentsurvey.

Fur thermore rail-based systems in the United Kingdom and France generateannual volumes of som e 25 m io. €. Eastern European count ries focus on otherproducts yet and hold only a minor share (see figure 7) .

Page 170282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

Others

France

East European Countr ies

United Kingdom

I taly

Germany

Spain

Source: SCI

Figure 7 Overv iew of nat ional m arket seizes for t raff ic cont rol

New and upgraded system s represent the m ain share of dem and, while m ainte-nance and system rehabilitat ion account for annual investments of 30 mio. € only.This is an indicat ion that com plete system overhaul is an im portant issue forEuropean rail com panies (see exam ples in chapter 6 for the sam ple of railwaysexamined in detail dur ing this study) .

5 .2 Supply-side

The supply-side of the m arket is far m ore heterogeneous than the dem and-side.

I t is im portant to pay separate at tent ion to m arkets for software applicat ions andhardware com ponents, since the grades of required explanat ion and custom isa-t ion of products differ significant ly (as the hardware m arket is much m orestandardised) .

I n the following, we init ially deal with the softw are sector of t raffic cont rol.A useful categor isation of providers appears to be

m ajor indust r ial groups with extensive railway businesses, par t icularly inneighbour ing t rain cont rol and signalling markets, like ( in alphabet ical order)Alstom , Ansaldo, Bom bardier, I nvensys, Siem ens, Thales and overseas com -panies like Mit subishi, Hitachi ( Japan) or Marubeni (Korea) ,

Page 180282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

large, typically m ult inational I T-com panies and system integrators (som et im esalso outsourcing-providers) with varying degrees of specialist expert ise in thet ransportat ion indust ry, like Accenture, Atos Origin, Cap Gemini, CSC, EDS,I ndra, Logica, Ster ia and others,

specialists, either with focused experience and skills in the railway sector, e.g.Funkwerk (ex Vossloh) or with funct ional profiles for cross- indust ry expert isein databases, real- t im e com municat ion, software-m odelling, web-based solu-t ions or software requirem ents' m anagem ent , like again Funkwerk, Telelogic,Tipco, Vivum and m any others; the specialist s have m ainly m ore of a localexposure, but nethertheless often operate internat ionally,

railway infrast ructure m anagers, who are ready to share their proprietarysystem design or m odules/ applicat ions as plat form s for customisat ion in othercount ries. This m ay occur in joint approaches with the indust ry but also on astand-alone basis. ADI F is an infrast ructure manager that is in possession ofadvanced system s and partnering with I NDRA, it s system provider to m arketsolut ions world-wide. SBB is another railway that may consider shar ing itssolut ions with other users.

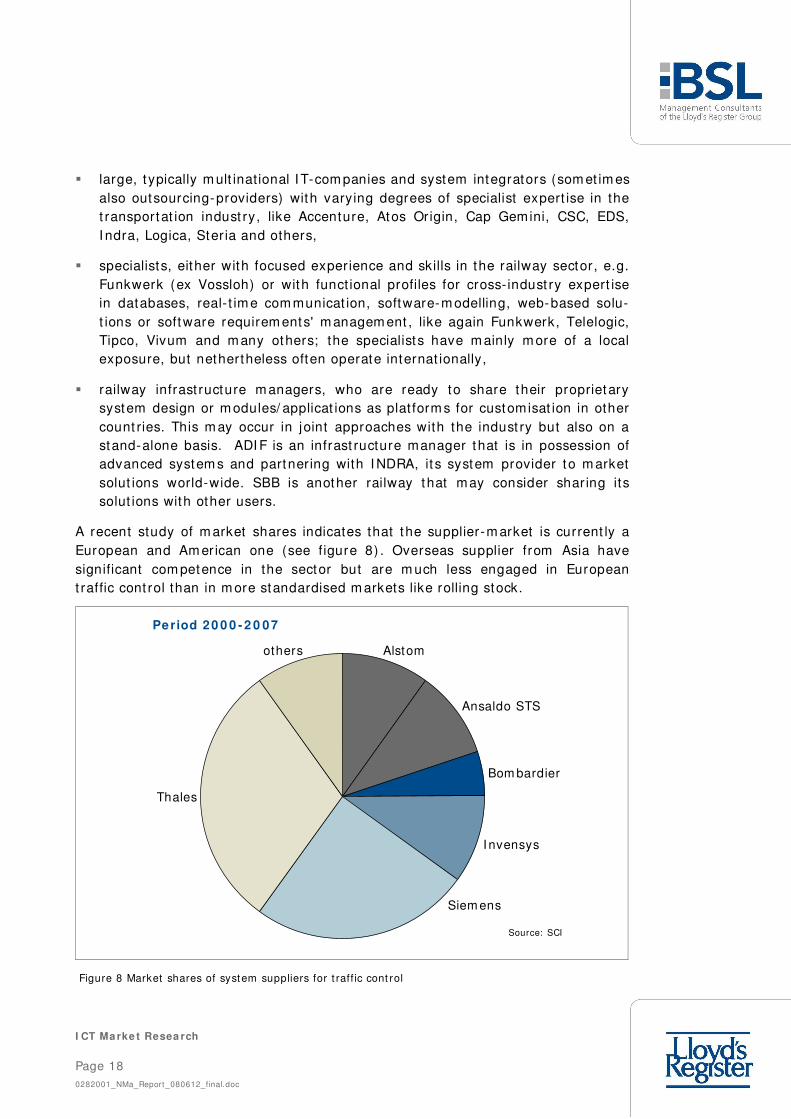

A recent study of m arket shares indicates that the supplier-m arket is current ly aEuropean and Am erican one (see figure 8) . Overseas supplier from Asia havesignificant com petence in the sector but are m uch less engaged in Europeant raffic cont rol than in m ore standardised m arkets like rolling stock.

others

Thales

Siem ens

Invensys

Bom bardier

Ansaldo STS

Alstom

Source: SCI

Period 20 0 0 - 2 0 07

Figure 8 Market shares of system suppliers for t raff ic cont rol

Page 190282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

The ident ified m arket -shares cover t raff ic cont rol hard- and software includingnetworks for data t ransm ission for both European heavy rail and urban railsystem s.

The dom inant role of the industr ial groups is probably influenced by

it s funct ions as prim e cont ractors; subcont ractors for hardware and systemintegrat ion are not accounted separately in these cases

m ajor cont ract values for the rehabilit at ion of comm unicat ion networks, whichmay dominate quant itat ive analyses.

While a strong m arket posit ion of these groups can be acknowledged, it s role isnot as dom inant with a specific focus on the software applicat ion m arket as it m ayappear from an aggregated view on the sector.

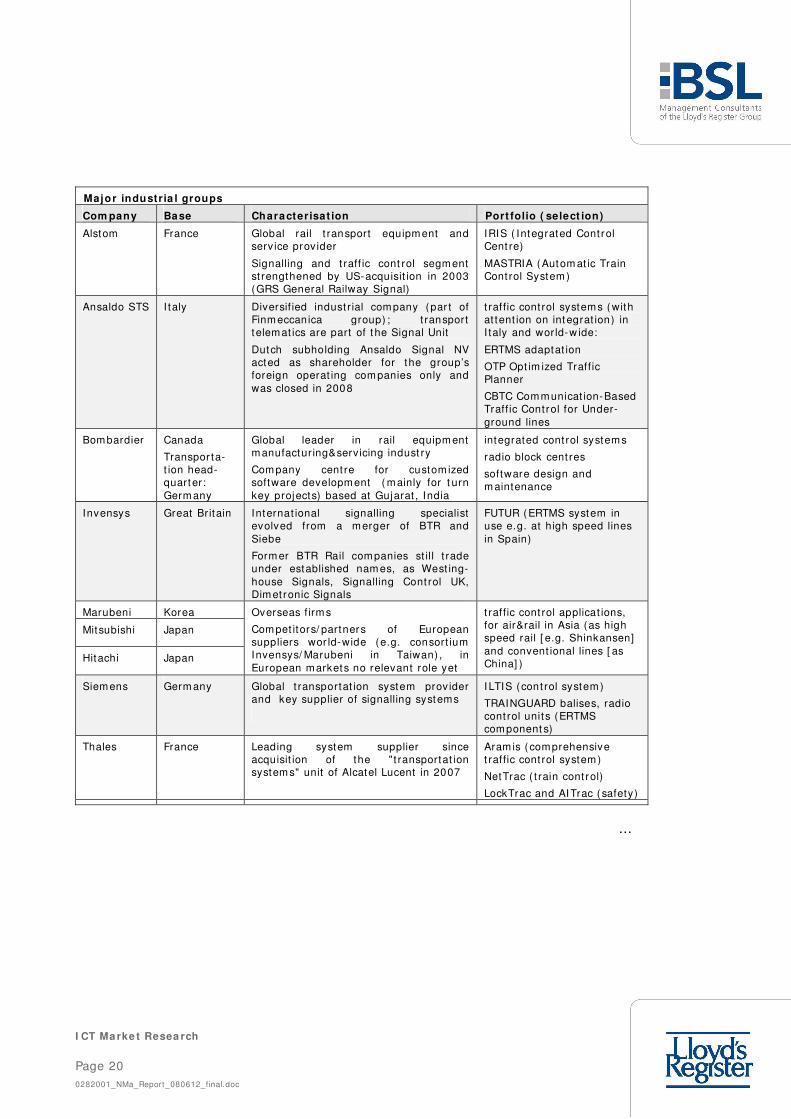

Characterist ics of the above nam ed com panies are presented in the followingtable 9.

When "products" are m ent ioned in the port folio it is im portant to bear in mindthat these are rather concepts (plat form s) for indiv idual adaptat ion on exist ingsystem environm ents than "plug&play"-solut ions. For exam ple, the t raffic cont rolsystem "LEI DI S-N" of DB AG is m arketed by Thales under the brand nam e"Aramis". When it has been sold internat ionally, adaptat ions have been carr iedout of "generally spoken som e 20% " even for the lim ited com plexit ies of railwayslike Israel and Portugal.

Page 200282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

Major industria l groups

Com pany Base Characterisat ion Port folio ( select ion)

Alstom France Global rail t ransport equipm ent andservice provider

Signalling and t raff ic cont rol segm entst rengthened by US-acquisit ion in 2003(GRS General Railway Signal)

IRIS ( Integrated Cont rolCent re)

MASTRIA (Autom at ic TrainCont rol System )

Ansaldo STS I taly Diversif ied indust r ial com pany (par t ofFinmeccanica group) ; t ransporttelemat ics are part of the Signal Unit

Dutch subholding Ansaldo Signal NVacted as shareholder for the group’sforeign operat ing com panies only andwas closed in 2008

t raffic cont rol systems (withat tent ion on integrat ion) inI taly and world-w ide:

ERTMS adaptat ion

OTP Opt im ized Traff icPlanner

CBTC Communicat ion-BasedTraff ic Control for Under-ground lines

Bombardier Canada

Transpor ta-t ion head-quarter:Germ any

Global leader in rail equipmentm anufactur ing&servicing indust ry

Com pany cent re for custom izedsoftware developm ent ( m ainly for t urnkey projects) based at Gujarat , India

integrated cont rol systems

radio block cent res

software design andm aintenance

Invensys Great Britain Internat ional signalling specialistevolved from a merger of BTR andSiebe

Form er BTR Rail com panies st il l t radeunder established nam es, as West ing-house Signals, Signalling Cont rol UK,Dim et ronic Signals

FUTUR (ERTMS system inuse e.g. at high speed linesin Spain)

Marubeni Korea

Mitsubishi Japan

Hitachi Japan

Overseas f irms

Com pet itors/ partners of Europeansuppliers wor ld-wide (e.g. consort iumInvensys/ Marubeni in Taiwan) , inEuropean markets no relevant role yet

t raffic cont rol applicat ions,for air&rail in Asia (as highspeed rail [ e.g. Shinkansen]and convent ional lines [ asChina] )

Siemens Germ any Global t ransportat ion system prov iderand key supplier of signalling systems

I LTIS (cont rol system)

TRAINGUARD balises, radiocont rol units (ERTMScomponent s)

Thales France Leading system supplier sinceacquisit ion of the " t ransportat ionsystem s" unit of Alcatel Lucent in 2007

Aram is ( comprehensivet raffic cont rol system)

NetTrac ( t rain cont rol)

LockTrac and AITrac ( safety)

…

Page 210282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

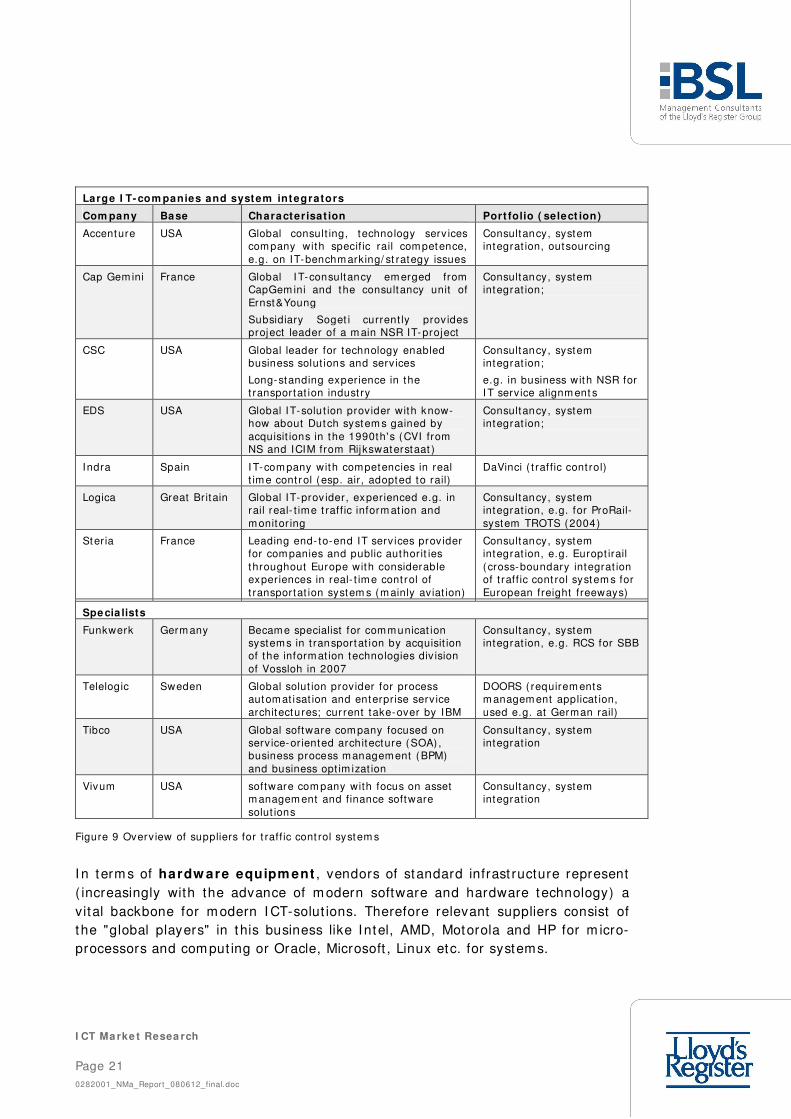

Large I T- com panies and system integrators

Com pany Base Characterisat ion Port folio ( select ion)

Accenture USA Global consult ing, technology serv icescompany with specif ic rail competence,e.g. on IT-benchm arking/ st rategy issues

Consultancy, systemintegrat ion, outsourcing

Cap Gem ini France Global I T-consultancy em erged fromCapGem ini and the consultancy unit ofErnst&Young

Subsidiary Soget i current ly providesproject leader of a m ain NSR IT-project

Consultancy, systemintegrat ion;

CSC USA Global leader for technology enabledbusiness solut ions and serv ices

Long-standing experience in thet ransportat ion indust ry

Consultancy, systemintegrat ion;

e.g. in business with NSR forI T service alignm ent s

EDS USA Global IT-solut ion provider with know-how about Dutch system s gained byacquisit ions in the 1990th's (CVI fromNS and ICIM from Rijkswaterstaat )

Consultancy, systemintegrat ion;

Indra Spain I T-com pany with competencies in realt im e cont rol (esp. air , adopted to rail)

DaVinci ( t raffic cont rol)

Logica Great Britain Global IT-prov ider, experienced e.g. inrail real- t ime t raff ic inform at ion andm onitor ing

Consultancy, systemintegrat ion, e.g. for ProRail-system TROTS (2004)

Steria France Leading end- to-end IT serv ices providerfor com panies and public authorit iesthroughout Europe with considerableexperiences in real- t im e cont rol oft ransportat ion system s (m ainly aviat ion)

Consultancy, systemintegrat ion, e.g. Europt irail(cross-boundary integrat ionof t raff ic cont rol system s forEuropean freight freeways)

Spe cia lists

Funkwerk Germ any Became specialist for communicat ionsystems in t ransportat ion by acquisit ionof the inform at ion technologies div isionof Vossloh in 2007

Consultancy, systemintegrat ion, e.g. RCS for SBB

Telelogic Sweden Global solut ion provider for processautomat isat ion and enterprise serv icearchitectures; cur rent take-over by IBM

DOORS ( requirem entsm anagem ent applicat ion,used e.g. at German rail)

Tibco USA Global software com pany focused onserv ice-oriented architecture (SOA) ,business process management (BPM)and business opt im izat ion

Consultancy, systemintegrat ion

Vivum USA software com pany with focus on assetm anagem ent and finance softwaresolut ions

Consultancy, systemintegrat ion

Figure 9 Overview of suppliers for t raff ic cont rol system s

I n term s of hardw are equipm ent , vendors of standard infrast ructure represent( increasingly with the advance of m odern software and hardware technology) avital backbone for m odern I CT-solut ions. Therefore relevant suppliers consist ofthe "global players" in this business like Intel, AMD, Motorola and HP for m icro-processors and com put ing or Oracle, Microsoft , Linux etc. for systems.

Page 220282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

An overview about the m ost im portant suppliers and their characterist ics isprovided in the following table 10.

Supplie rs of servers and sem iconductors

Com pany Base Characterisat ion Rem arks

ABM USA Mult inat ional sem iconductor com panyand second- largest global supplier ofm icroprocessors

Products include embeddedprocessors for servers,workstat ions and PC

Acer Asian manufacturer of PC's but alsoservers

Minor relevant European railhardware supplier yet

HP Hewlet tPackard

USA Large global m anufacturer ofcomputers and servers (hosts)

acquired EDS in 2008(see f igure 9)

IBM USA Mult inat ional hardware m anufacturerand supplier of host ing serv ices

Global supplier of indust r ialstandard com puterequipm ent

Intel USA World largest sem iconductor com pany

Motorola USA Internat ional supplier of sem iconduc-tors and networks

SunMicrosystems

USA Supplier of workstat ions and servers form any indust rial system providers asAlcatel, Siemens

System s in use world-w ide(Europe, US, Asia)

VIATechnologies

Taiwan Taipeh-based supplier of chips for PC'sand networks

Various subsidiar ies asCentaur Technologies, S3Graphics,..

Figure 10 Overv iew of selected hardware-suppliers for t raff ic cont rol

Sourcing and m aintenance m arkets are typically also very heterogeneous; thefollowing categor isat ion appears to be useful:

Legacy system s at railways (som etim es self-developed) are typically m ain-tained by railways them selves ( "in-house") .

New generat ion system s are often m aintained (e.g. with software releases and24/ 7-service lines) by the developers.

I ndependent / separate m aintenance and service providers for m ature and well-defined system s get into the m arket through com pet it ive bidding for the ser-vice-com ponent only.

Hence, independent providers of m aintenance services are scarce. Services will beoffered depending on individual requirements from medium -scale and rathernat ional based com panies. Whilst the m arket -share of independent m aintenanceproviders will be lim ited, they m ay play an im portant role as com pet itors andbenchm arkers for according services from system developers and internal railwayent it ies.

Page 230282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

6 . Market Trends and Developm ents

6 .1 Dem and-side

This chapter will again init ially deal with developm ents at the softw are ( applica-

t ions) m arket . Secondly, t rends related to custom ers at the hardware m arketwill be highlighted.

Railways' decisions about renewals of t raffic cont rol systems are based onm arket screenings. I nternat ional exam ples show that these m ay lead to theresult that products or plat form s for specific needs of railways are not available onthe m arket yet . This was the case at Swiss Federal Railway SBB, which deemedtheir 15 year old t raffic cont rol system (SURF) not to m atch current requirem entsfor capacit y and availabilit y any m ore. High standards on consistent real- t im edata were expected ( "bring planning close to operat ions") in order to enhancesystem robustness and thereby create addit ional net work-capacity for the veryhigh t raff ic-densit y on the Swiss network, which is very com parable to the Dutchsituat ion.

As alternat ives for an own developm ent , SBB considered r isks and benefit s ofmore fundamental system migrat ion against stepwise updates of single applica-t ions and decided to develop a new t raffic cont rol system ( "Rail Cont rol System ",RCS) "from the scratch" (even with a total renewal of the underly ing network databy a consistent "Unified Network Objects dat abase") in order to avoid that "m orework is spent on interfaces than solving the real problem s".

Following to this decision, an im portant st rategic issue is the degree of industry

part icipat ion st ill in early stages of system definit ion .

This is considered against the background of dramat ic changes that happened inthe fast -paced business environment of I T/ sem iconductor-indust ries dur ing thelast decade regarding the sectors of software and system developm ent tools,procedures and skills as well as m igrat ion processes.

State-of- the-art tools like cert ified "guaranteed system plat form s" are provided ina m uch m ore all-encom passing fashion by service/ system specialists, which alsotake responsibilit y for cont inuous technology adaptat ion. The crit ical resource is inthe knowledge and specificat ion that keeps providers in touch with developm entsto an extent , that even the big railways can hardly (or at ext rem ely high costs) beclose enough to top-t ier developm ents with internal resources to fully understandhow to m ake the best use of it .

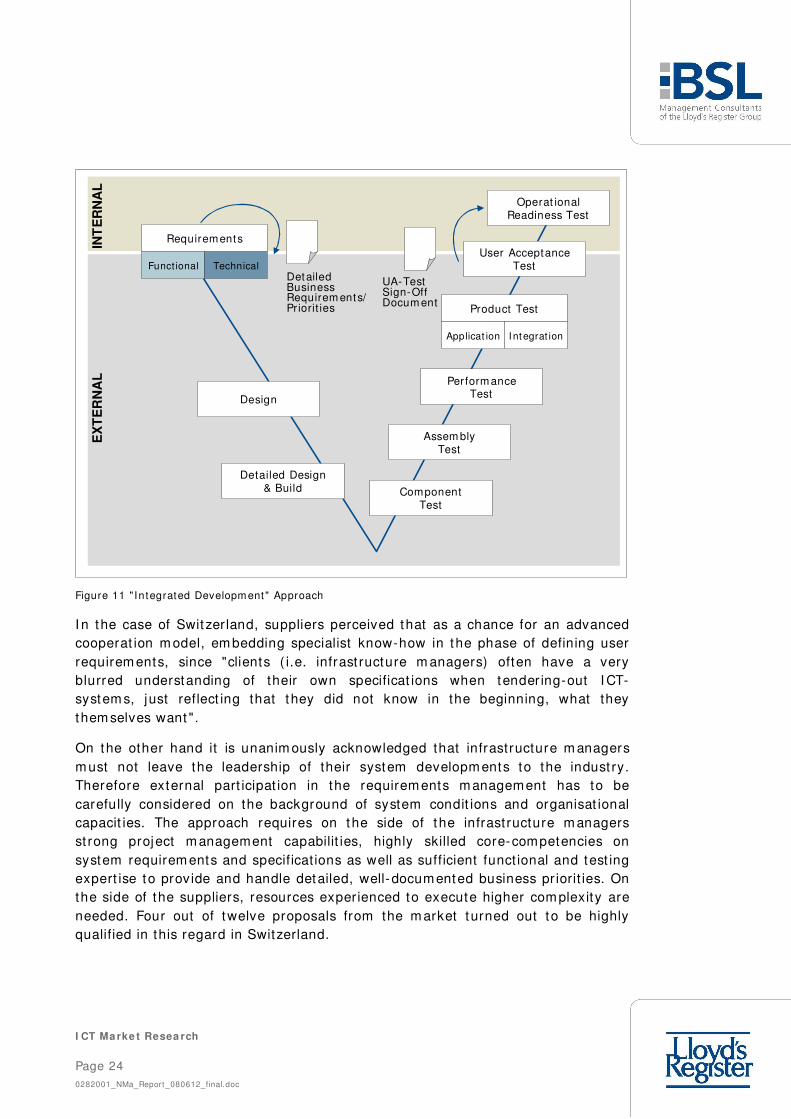

This has been one of the reasons for several European infrast ructure m anagers tointegrate supplier know-how into the requirements m anagem ent of their t raff iccont rol systems (as principally shown in figure 11) .

Page 240282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

INT

ER

NA

LE

XT

ER

NA

L

UA-TestSign-OffDocum ent

Operat ionalReadiness Test

User AcceptanceTest

Requirements

Funct ional Technical

Product Test

Applicat ion Integrat ion

Perform anceTest

Assem blyTest

ComponentTest

Detailed Design& Build

Design

DetailedBusinessRequirem ents/Priorit ies

Figure 11 " In tegrated Developm ent" Approach

I n the case of Switzer land, suppliers perceived that as a chance for an advancedcooperat ion m odel, em bedding specialist know-how in the phase of defining userrequirem ents, since "clients ( i.e. infrast ructure m anagers) often have a veryblurred understanding of their own specificat ions when tender ing-out I CT-system s, just reflect ing that they did not know in the beginning, what theythem selves want ".

On the other hand it is unanim ously acknowledged that infrastructure m anagersm ust not leave the leadership of their system developm ents to the indust ry.Therefore external part icipat ion in the requirem ents m anagement has to becarefully considered on the background of system condit ions and organisat ionalcapacit ies. The approach requires on the side of the infrastructure m anagersst rong project m anagement capabilit ies, highly skilled core-competencies onsystem requirem ents and specificat ions as well as sufficient funct ional and test ingexpert ise to provide and handle detailed, well- documented business pr iorit ies. Onthe side of the suppliers, resources experienced to execute higher com plexity areneeded. Four out of twelve proposals from the m arket turned out to be highlyqualified in this regard in Switzerland.

Page 250282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

After an extensive (1 ½ year long) proof-of-concept in 2005, a consort ium of CSCand Funkwerk (previously Vossloh) started work in a joint team with SBB on at ight ly controlled t im e-and-m ater ial base. The consort ium rolls-out f irst m oduleson- t im e. The result is also considered as a "kind of a product ", from which otherinfrast ructure managers could benefit .

A sim ilar exam ple from The Netherlands is the so-called "HI T"-project of NSReizigers on passenger inform at ion. System requirem ents were pre-defined in thetender only on a high funct ional level. Details were worked out then in aninteract ive process between NSR and the supplier (Funkwerk) , who cont r ibutedhis know-how-base and experience from a sim ilar system developm ent in Norwayand act ively m anaged the interact ion between the related part ies.

By doing so, the developm ent process and the integrat ion of end-users was muchadvanced ( results achieved "much quicker and in bet ter qualit y than in otherprojects" according to NS) . However, in ProRail's view this developm ent atoperators' side also shows the relevance of a sounder em bedding into the contextof exist ing environm ents at the infrast ructure m anager in order to ensurecom pat ibilit y and successful interact ion of system s.

Altogether railways who follow joint approaches with the industry and conse-quent ly define (and lim it ) their roles as a system architecture leader, who createsthe v ision, defines the m ain steps, the best partners to get there and cont rols theprocess, obtain shares of 80-90% of project efforts from external suppliers.

I nit iat ives towards harmonisation and standardisation of system s werepreviously rather seen at the supplier side of the m arket , which has an economicinterest to use exist ing plat forms for internat ional sales act ivit ies. DespiteEuropean efforts for a " top-down"-creat ion of a com m on European m arket nosignificant init iat ive was found on the demand-side to prom ote (or even onlysupport ) convergence of nat ional approaches at the t raffic cont rol sector.EU- interoperabilit y aspirat ions are rather a "push" that meets reluctance than apull by the infrastructure m anagers themselves.

Nevertheless evidence is st rong from the sector of signalling and interlockings,that standardisat ion and innovat ion can be successfully im plem ented by "bot tom -up"-approaches, when procurem ent st rategy accounts for a modularisat ion ofsystem s, brake-up of tender packages and encourages the adaptat ion of "non-railway" but indust rially established technologies.

For instance, Deutsche Bahn AG has pursued such a strategy since 1999 andfound that "m arkets for qualified suppliers are well exist ing, but in need to beact ively m anaged". After several years of effort s, the num ber of suppliers forelect ronic interlockings was increased to six and the num ber of indust rial consor-t ia for operat ional cent res up to three, while com parable system s are procured

Page 260282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

now "certainly not less than" 30% cheaper than the or iginal offers of "incum bentsuppliers" and with m uch m ore com pliance to deadlines.

While such coherent st rategies were a dom ain of som e " first m overs" in theprevious decade, init iat ives to open up m arkets are current ly a t rend at m anyrailways. They expect that "a disclosure and standardisat ion of interfaces willpush t ransparency and compet it ion, since it allows for specific procurem ent ofsingle applicat ions and a cost -eff icient mix of com petit ive suppliers" (see DB AGor ADI F) .

Open standardised interfaces with proprietary inform at ion at the railway (notthe supplier) are a key- issue in order to st rengthen the buyer 's posit ion facingsuppliers, enhance com pat ibility of system s and thereby give m ore opportunit iesfor suppliers to part icipate in tenders. However, interviewees also highlighted thatthe num ber of different suppliers within a system landscape should not exceed arange "in a single-digit level" in order t o keep efforts on interfaces manageableand st rengthen allocatability in case of m id-performance.

Such kind of dem and-side dr iven interest m ay eventually t ransform the m arket toa European/ global dim ension and lend it som ewhat m ore of a product -characterist ic in the m edium - term . However, experiences clearly indicate the needfor infrast ructure m anagers to act ively work with ( "manage") the m arket in orderto m ake use of it s com pet it iveness.

With regard to hardw are m arkets the im portance of absolute f lex ibilit y ofsystem architectures to switch to the m ost recent equipm ent was highlighted by am ajor ity of interviewees.

"Upward-compat ible" , scaleable and dist ributed com put ing/ processing com po-nents bases on indust ry-wide standards enable swift changes to follow andm igrate to new technology-generat ions, since only a very sm all part of assetinventor ies will be m odernised within m aximum windows of 2-3 years unt ilm anufactures stop their product ion of a certain plat form and m ove on. A goodexam ple for that are the m obile comm unicat ion networks for railways (GSM-R) ,which already went through various technological generat ion changes.

However there were st ill observat ions that "railways and their procurem entdepartm ents t ry to oblige their suppliers to guarantee delivery and logist ics overthe next 30 years. I t is like 'going to the m useum ' after a few years t im e and ofcourse it is crazy in terms of 'inventories and spare parts' requirem ents andcapital employed".

Such param eters do certainly m aterially rest r ict m arket access of state-of- the-artsuppliers. Hence, the issue has been acknowledged by m any railways ( includingProRail) and steps are taken to overcom e it .

Page 270282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

6 .2 Supply-side

Som e specialised suppliers and system integrators express a willingness toadvance European m arket creat ion and do believe (broadly in consensus) that -underneath specif ic and individual requirem ents – fundam ental system featuresare surprisingly sim ilar internat ionally. Thereby custom izing of platform s and

concepts is considered as a valid and usable opt ion ( " the railways just don't gofor it " ) .

However, no m ature "ready- to-use" products can be expected from the m arket ,yet cost -efficient , indust rial standard plat forms that can nevertheless accom mo-date customised applicat ions serving the indiv idual requirem ents and varyingoperat ional needs of railways.

Possibly the leading-edge experience in Europe for a supply-side driven marketconsolidat ion (or rather "creat ion") is the im plem entat ion of t he t raffic cont rolsystem "DaVinci" in Spain. I t is a joint developm ent of the system integratorI NDRA and the Spanish infrast ructure m anager ADI F based on a m ission-crit icalplat form already used in air t raff ic cont rol and adopted according to funct ionaldesign specificat ions of ADI F.

This highly integrated system was im plem ented on the ever growing Spanish highspeed lines since 2003 and proved to work – sim ilar to it s equivalent in aviat ion -with ext remely high availability ( "there have been no perturbat ions up to nowwhich had any effects on t rain operat ions") .

An addit ional im plem entat ion on the convent ional Spanish network is underconsiderat ion. Furtherm ore, the system was bought and is being installed (orconsidered) in a num ber of railway systems in Europe (Transport for London) andglobally (South Am erica, China) . Various other European railways (as the Portu-guese REFER, Brit ish Network Rail, Austr ian ÖBB and Russian RZD) have inquiredabout DaVinci and appear to consider it as an advanced solut ion t ransferable intotheir own operat ional environment .

Cross-fert ilisat ion w ith other industr ies related to real- t ime t raffic cont rolm ay lead to the ent ry of further m arket part icipants, which int roduce openstandards from sectors like air t raffic cont rol, where developm ent has progressedin much earlier stages (possibly with a 10-15 year t im e log) .

Major indust rial groups with extensive railway businesses are expected to getunder pressure in the context of these developm ents. Som e st ill appear to t ry tot ie-in custom ers into applicat ion fam ilies with propr ietary knowledge barriers,while the general m arket view is that they will find it increasingly hard to provideand cover enough width and depth of applicat ions for their clients.

Page 280282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

At the sam e t im e they have to acknowledge that the overall client base ( "m arketsize") is very lim ited and I CT-solut ions are rather "by-products" which t ypicallyonly account for a very sm all fract ion of sales com pared to t rain cont rol andsignalling for instance. This leads to constellat ions as the rail- cont rol-cent redevelopm ent consort ium between Siem ens and Funkwerk for DB AG, in whichFunkwerk holds the lead [ ! ] for system developm ent .

Hence it can be expected that in the near future som e industr ial groups m ay

m ake st rategic choices to either abandon I CT (or leave it t o business-partners)or to shift their own approach to open architectures.

7 . I m plicat ions for ProRail

ProRail is facing the challenge to bring it s I CT for t raffic cont rol, which is based onlegacy system s, into a m ore robust configurat ion and at the sam e t im e m anagethe t ransit ion into the future.

I n the context of it s current system landscape and previous outsourcing of key-experts, ProRail is st ill bound to incum bent suppliers. In parallel it has alreadytaken various steps which can be considered as a m ove into the r ight direct ion,nam ely

t o ( re- ) insource know-how about system- requirements and engineering,

thus, to reduce exposure to/ dependability from t ied-in suppliers and serviceproviders,

to address a programm e of pr iorit ies for applicat ion redesigns,

to tender-out software- factory work under the um brella of this programm ecom petit ively and internat ionally ,

t o br ing the resources of "Tribase" under direct m anagem ent cont rol of adedicated ProRail unit (BNS) ,

t o establish an enterpr ise architecture plat form ( "service bus") for bet tersystem integrat ion and

to install a redundant and cent ralised I CT-operat ions cont rol-cent re in order toenhance infrast ructural provisions for business cont inuit y in case of failures.

However, ProRail has undertaken this m ove som e two years ago and is in ongoingefforts to stabilise the situat ion (" fire-f ight ing") .

The current t ransitory situat ion makes an effort to recover from im minent r isks ofsystem m anageability and robustness and price-worthiness.

Page 290282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

I m pacts of dependency from incum bent suppliers can be est im ated on the base ofexam ples from railways, which went through similar t ransit ion processes som eyears ago. Experiences clearly show, that internat ional suppliers with provenexperience in the use of m odern technologies turned out to be m ore com pet it iveas to:

Perform ance: state-of- the-art plat form s can be expected to work pract icallyfailure-proof (see Spain) ,

Delivery-speed: Requirements and deadlines are handled m ore st rict (seeNSR, "HIT") Price levels: reduct ions of up to 30% com pared to or iginal levelsof " incum bent suppliers" were observed (see DB AG and results from pilottenders at ProRail (which were cont racted for the half of ant icipated budgets) ,

Capacity: advanced system s enable a higher quality of t rain-operat ion, whichresults in a m ore dense exploit at ion of networks. SBB expectat ions on its newt raffic cont rol system are capacity gains of 5% .

While a set of act ions already taken by ProRail tackle im portant issues of a future-proof system architecture and accordant m arket approaches to benefit from theseeffects, it should be cont inued and enhanced with explicit considerat ions towards

a coherent perform ance-assured system architecture

a leap to m odern software and hardware technology and tools with inherentadvantages of unit -cost digression and standard "t im es-to-applicat ion"

access system rules and specificat ions in a self-crit ical m anner under value-analysis aspects

assure a system atic and robust access to highly specialised professional skillsin the m arket

cont inuous evolut ion of hard- and software in line with technological changessupport ing the system funct ionalit y in a smooth upward-com pat ible m anner

consistent ly m anaged 24/ 7 system availabilit y and service/ m aintenance.

I n order to cont ribute to a generat ion-change of systems within the VPT-landscape, there is the need t o form alise and form ulate operat ional requirem entsand to determ ine a level of " innovat ion leadership" between t op-t ier develop-m ents of technology and successfully proven pract ices.

Since such system engineering skills are scarce and top- talent is with "at t ract ive"indust ries as telecom or financial services, there are considerable doubts thateven the bigger European infrast ructure m anagers have the cr it ical m ass todevelop this knowledge in-house (to reasonable costs) .

Page 300282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

Thus, since the dr ive of ProRail t o do all system design and specificat ion work in-house can be understood as a react ion to current ly felt and pressing needs toestablish respect ively restore an internal knowledge-base, it appears to go too farand should be bet ter balanced with the m arket .

I nternat ional good pract ice suggests that - start ing now and with a longer- termperspect ive - ProRail needs to consequent ly develop it s approach to the wholeprocurem ent issue and it s business-m odel to interact with the m arket byconsidering at least the following elements:

(1)

Cont inue on the re-building of a highly skilled knowledge-base within ProRail, thathas sovereign insight and m astery of the ra ilw ay- operat ional processes andrules; this "cent re of expert ise" should consider it self as system experts for theoperat ion of t raffic and networks, not as a technology- focused team . I t shouldresource appropriate technologies (as a means to an end) from the m arket forthis purpose, it m ight rethink its hum an resource strategy in order to at t ract som every top experts.

(2)

Cont inue to reassemble and form alise lost or hidden operat ional and safetyprocedures as the prim e and forem ost task of this "cent re of expert ise" in order toestablish a solid foundat ion for all future (and current) "requirem ents m an-

agem ent" ( i.e. a thorough definit ion of specificat ions) , as it is good-pract ice forsystem developm ent in advanced indust ries ( like aviat ion, autom ot ive, financialservices) .

(3)

Cont inue to establish such a professional "requirem ents m anagem ent" incooperat ion with specialised IT-advisors and the support of modern t ools in orderto enhance benefits which have already been seen from efforts of the last twoyears in

higher eff iciency,

an induced form al rigour to define specif icat ions com prehensively andcont radict ion- free

a generic set -up to autom atically der ive a test ing-environm ent for softwareand hardware components

som e cross- fert ilisat ion between railway-specific aspects and

an up- to-date wider knowledge from other indust r ies.

Page 310282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

(4)

As a further step, and building on the previous one, this "cent re of expert ise"should em bark on a self- cr it ical assessm ent of rules and specificat ions withregard to value-added and/ or necessary m astery of forgot ten (oft en unreflected)under ly ing background for solut ions and system design.

(5)

ProRail should adjust ( in parallel) a procurem ent strategy , t hat

packages applicat ions and tasks into a lim ited num ber of lots, t ransferr ingresponsibilit y for funct ioning interfaces to a greater extent to suppliers

puts these packages out in the market for com petit ive internat ional ten-dering among top-providers from the industry

considers to develop m ission-cr it ical systems, in case that m arkets do notoffer sufficient plat forms, to im plementat ion-stage (on a paid- for basis) inparallel by two suppliers for com pet it ive and fall-back reasons, like e.g. theUS Departm ent of Defence (DOD) does for new aircraft

puts ( far greater) em phasis in pr icing on achieved performance standardsor sim ilar object ives of the respect ive business cases behind the projects

(as a development step) com bines the delivery and im plementat ion of anapplicat ion with longer term service cont racts, ideally covering 24/ 7 opera-t ions, service, release m anagem ent and underlying migrat ion of hard-ware/ software-com ponents in line with technological changes.

(6)

As a start ing-point for the technical assessm ent of the current I CT-systemlandscape, ProRail should m andate an I CT- screening with regard to

modernity/ obsolescence of hard- and software

internal/ external system developm ent capabilit ies

future indust ry "musts" and opportunit ies

(7)

By this screening, ProRail should gain a structured overview on generic applica-t ions, plat form s and tools from other indust ries and also fur ther evaluate potent ialtem plates from advanced peer railways, leading into an overall st rategy (orm asterplan ) how to develop the I CT- landscape further and t ranspose it into afuture generat ion.

Page 320282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

(8)

Based on som e of the before-m ent ioned steps ProRail m ay eventually decideabout further stages of outsourcing of system -operat ions, cont inuous devel-opment and technology m anagem ent .

(9)

Railway operat ional expert ise and "Requirem ents Managem ent " rem ains a corecapabilit y for ProRail t hat is unsuitable for external sourcing. The current effort toovercom e the brain-drain should lead t o a well- form alised knowledge-base builtwith further enhanced use of up- to-date and market going modelling tools.

8 . Conclusions

The key-quest ions of the m arket-analysis can be summ arised in the followingstatem ents:

"Which are the relevant m arkets (both in terms of products and geography)that serve ProRail t o obtain their products and services for I CT systems int raffic cont rol?"

The relevant m arket for software developm ent consists of com panies whichm ay be generally based internat ionally. However, it turned out that presencein The Netherlands is of great advantage, since close contact to the custom erand Dutch speaking staff is required.

On the hardware-side, the relevant m arket is global and covers all effect ivesuppliers of business com put ing.

"How important is the different iat ion between hardware for installat ion andoperat ion of I CT-system s on the one hand and software for system develop-m ent and m aintenance on the other?"

The different iat ion is im portant since the grade of explanat ion and custom isa-t ion requirem ents for products differs significant ly. Since the hardware m arketis much m ore standardised, less interact ion with the custom er is necessary.This m akes it easier to procure and deliver globally.

"Who – explicit ly – are the suppliers and custom ers? To what extent do theyact domest ically or internat ionally?"

Suppliers are provided at f igures 9 and 10 of this report , custom ers (by coun-t r ies) in figure 7. While the dem and-side – which m ainly consists of state-owned railways and infrastructure m anagers - is st ill relat ively domest ic in it snature, most suppliers act on a (at least ) European scale.

Page 330282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

"Which signif icant developments and t rends can be ident if ied and what is theirpotent ial im pact on the effect iveness of the m arket , e.g. possible ent ries andexits of m arket players?"

Supplier know-how is going to be increasingly integrated into early phases ofthe requirements m anagem ent of t raff ic cont rol system s by joint -approachestowards system developments.

Harm onisat ion and standardisat ion of systems, which are st ill in it s infancydespite of m uch European efforts, support the effect iveness of the m arkets,since sim ilar indust rial concepts or system plat forms (however adopted) areused internat ionally .

I ndust r ial groups, who t ry to t ie- in their custom er into proprietary knowledgebarr iers, are thereby under pressure. Some m ay m ake st rategic choices toeither abandon I CT (or leave it t o business-partners) or to shift their ownapproach to open archit ectures.

Cross- fert ilisat ion with other indust r ies m ay lead to the ent ry of further m ar-ket part icipants with com petencies in real- t ime t raffic cont rol ( as from avia-t ion) .

"What are ent ry barr iers for the var ious sub-m arkets, e.g. intellectual propertyr ight s or governm ental regulat ions?"

For software (applicat ion) markets, barriers to part icipate on tender proce-dures cover

Ÿ t he degree of technical rather than funct ional specificat ions, which m ayform ally exclude even funct ional adequate solut ions

Ÿ proprietary inform at ion on interface standards which are essent ial to con-nect a system with others within an exist ing architecture.

For hardware m arkets, som e railways st ill restr ict the m arket by requirem entsfor guaranteed delivery and logist ics periods, which are much longer than thelife- t ime of a hardware plat form in the fast -paced technological environment .

This urges suppliers to support outdated technology and thereby limits thenumber of m arket part icipants.

"How com pat ible are com ponents and services provided by different suppliers?How important is com pat ibility for the effect iveness of the m arket? Which riskscan be ident if ied and how can they be mit igated?"

A t rend towards standardised plat form s and open interfaces (however in it sinfancy yet ) supports com pat ibility, since suppliers are able for custom isingapplicat ions onto different environm ents, if t hey are in charge of the

Page 340282001_NMa_Report_080612_final.doc

I CT Ma rke t Resea rch

necessary inform at ion for it . This will give m ore opportunit ies for suppliers topart icipate in t enders.

However, too m any different suppliers m ay be a r isk for the system m anage-m ent in case of perturbat ions. Thereby the num ber of suppliers within asystem should be rest r icted "on a single-scale level" .

"How do current procurement and cont ract ing pract ices im pact pr ices and thespeed of delivery? What can be done to im prove m arket -effect iveness? Whatcan be learned by other infrast ructure m anagers internat ionally in this re-spect?"

I m pacts of dependency from incum bent suppliers can be est im ated on thebase of experiences from railways, which already successfully widened theirm arket : 30-50% higher prices, less st rict handling of delivery- t im es and lowersystem perform ance which leads to less capacity on the network.

Thereby ProRail needs to go further steps onto it s way to m ake full use of them arked (as described in nine recomm endat ions at chapter 7) .

Necessary key-resources need to be developed, while ProRail has to preventit self from a fall-back into overly excessive inhouse-st rategies.