David Jones financial analysis

19

David Jones Financial Statement Analysis 2008-2010 FNCE90055 Assignment 1 Tutor: Warren Mckeown Prepared by: Yu Shen(301448) Johnson Kee (289377) Huu-Phuc Truong (384083) Natissja Alias (202664)

-

Upload

natissjaalias -

Category

Documents

-

view

174 -

download

4

description

Assignment for Financial Decision Making subject

Transcript of David Jones financial analysis

David Jones Financial Statement Analysis 2008-2010 FNCE90055 Assignment 1 Tutor: Warren Mckeown

Prepared by:

Yu Shen(301448)

Johnson Kee (289377)

Huu-Phuc Truong (384083)

Natissja Alias (202664)

David Jones Financial Report Analysis• 2011 1

1. Cash Flow Statement Analysis Mature age or growth age

Figure 1. Cash flow trend 2008-2010

In financial year (FY) 2008-2010, positive and relatively stable cash flows from

operating activities (OCF) suggest David Jones (DJ) is in a maturity stage as it shows a

positive and stable OCF. OCF remained approximately the same in FY08-10 except a

slight decrease in FY09, which was presumably caused by the global financial crisis

(GFC) and store renovations.

Outgoing cash flow from investing activities (ICF) decreased enormously in

FY07-08 with a decrease of $464,018,000 causing ICF to rise sharply. Nevertheless,

there is a relatively slight increase in FY09-10, but it is still significantly less than in

FY07-08. Also, ICF is predominantly negative. Together, ICF may suggest either late

growth or early maturity.

-‐600000

-‐500000

-‐400000

-‐300000

-‐200000

-‐100000

0

100000

200000

300000

400000

2006 2007 2008 2009 2010

Net cash )low ($000)

Year

CASH FLOWS FROM OPERATING ACTIVITES CASH FLOWS FROM INVESTING ACTIVITIES

CASH FLOWS FROM FINANCING ACTIVITIES

David Jones Financial Report Analysis• 2011 2

Negative cash flow from financing activities (FCF) also suggests the maturity

phase. Mainly because FY05-10 FCF is predominantly negative except for FY07.

Together, DJ’s cash flow from operating, investing and financing activities

suggest that it is in late growth or early maturity. Thus DJ could be considered as either

a successful mature firm or a firm that is still growing modestly.

David Jones Financial Report Analysis• 2011 3

2. ROA Analysis Table 1. ROA calculations for FY09 and FY101

!"# = !"#$%&'() !"#$%& × !"#$%&'#

!"# = !"#$!"#$% ×

!"#$%!"#$%&# !"!#$ !""#$"

2009 2010

EBIT 225651000 249177000

Sales 1985490000 2053087000

Average total assets

1527102000+ 11246740002

= 1325888000

1194921000 + 11246740002

= 1159797500

Operating margin

2256510001985490000

= 0.1137

2491770002053087000

= 0.1214

Total asset turnover

19854900001325888000

= 1.4975

20530870001159797500

= 1.7702

ROA 0.1702 !" 17.02% 0.2148 !" 21.48%

Percentage change in ROA

!"#$"%&'(" !ℎ!"#$ !" !"# = !"#!"#"! !"#!""#!"#!""#

!"#$"%&'(" !ℎ!"#$ !" !"# = !.!"#$! !.!"#$!.!"#$

!"#$"%&'(" !ℎ!"#$ !! !"# = 0.2620 !" 26.2%

1 Figures used are the adjusted figures from the latest annual report available.

David Jones Financial Report Analysis• 2011 4

Return on assets (ROA) can be disaggregated into operating margin and total

asset turnover. Operating margin reflects the profitability of every dollar of sales made

while turnover reflects the efficiency with which the firm utilizes its assets in the

revenue generating process. Together, ROA reflects the profitability of the firm and its

operating efficiency. DJ’s increase in ROA of 17.02% in FY09 to 21.48% in FY10

suggests improved operating efficiency. By disaggregating ROA, it becomes apparent

that its increase is due to improved turnover, which increased by 18.21%2.

2 Turnover increase is is approximately three times the increase in operating margin of 6.87%

David Jones Financial Report Analysis• 2011 5

3. ROE Analysis Table 2. ROE calculations for FY09 and FY103

!"# = !"#$

!"#$%&# !"#$%!!!"#$%&

2009 2010

NPAT 156522000 170766000

Average owners’ equity

6172479000 + 6848420002

= 651044500

684842000 + 7442380002

= 714540000

ROE 0.2404 !" 24.04% 0.2390 !" 23.90%

Percentage change in ROE

!"#$"%&'(" !ℎ!"#$ !" !"# = !"#!"#"! !"#!""#!"#!""#

!"#$"%&'(" !ℎ!"#$ !" !"# = !.!"#$!!.!"#"!.!"#"

!"#$"%&'(" !ℎ!"#$ !" !"# = −0.0058 !" − 0.58%

Return on equity (ROE) reflects the profitability of utilizing shareholders’

equity. ROE is expressed as a percentage of after-tax net profits on average

shareholders’ equity. DJ suffered a decrease of 0.58% in ROE from FY09 to FY10. This

is a relatively small amount – most likely attributable to the 9.75% increase in average

shareholders’ equity relative to the 9.1% increase in NPAT. This suggests that the more

proportionate increase in shareholders equity compared to NPAT resulted in a decrease

3 Figures used are the adjusted figures from the latest annual report available.

David Jones Financial Report Analysis• 2011 6

in ROE. The decrease in ROE can also be explained using leverage ratios4. Capital

structure leverage ratio dropped from 2.0366 times in FY09 to 1.6231 times in FY10.

This is due to the increase in shareholder equity (9.75%) relative to the decrease in total

assets (-12.53%).

4 ROE can be disaggregated into ROA and leverage

David Jones Financial Report Analysis• 2011 7

4. Return on Accounts Receivable and Payable Analysis Table 3. Accounts receivable turnover and days in accounts receivable outstanding calculations for FY09 and FY10

!""#$%&' !"#"$%&'(" !"#$%&'# = !"!"#

!"#$%&# !""#$%&' !"#"$%&'("

!"#$ !""#$%&' !"#"$%&'(" !"#$#%&'(&) = 365

!""#$%&' !"#"$%&'(" !"#$%&'#

2009 2010

Sales 1985490000 2053087000

Average accounts receivable

22309000+ 4149800002

= 218644500

22750000+ 223090002

= 22529500

Accounts receivable turnover

9.0809 91.1288

Days in accounts receivable

outstanding 40.19 4.01

!"#$"%&'(" !ℎ!"#$ !" !""#$%&' !"#"$%&'(") !!"#$%&" = !"#!"#"!!"#!""# !"#!""#

!"#$"%&'(" !ℎ!"#$ !" !""#$%&' !"#"$%&'(") !"#$%&'# = !".!"##!!.!"!#!.!"!#

!"#$"%&'(" !ℎ!"#$ !" !""#$%&' !"#"$%&'!"# !"#$%&'# = 9.035 !" 903.5%

David Jones Financial Report Analysis• 2011 8

Management of accounts receivables has shown an extraordinary performance

on increasing accounts receivable turnover and days in accounts receivable outstanding.

Accounts receivable turnover increased 900% from FY09-10. FY10 was significantly

higher, because from FY08-09, accounts receivables decreased tremendously.

Consequently, average accounts receivable for FY09 was much higher than for FY10.

From FY09 onwards, DJ has improved its management of collecting accounts

receivables as reflected in reduced days in accounts receivables outstanding. While DJ

took about 40 days to collect receivables in FY09, it took only about 4 days in FY10,

indicating a tenfold improvement. The large decrease in accounts receivable and thus,

an increase in the turnover, was primarily due to the introduction of the DJ/American

Express (Amex) storecard. By doing so DJ was able entrust $374.3 million worth of

primarily debt-funded receivables to Amex.

David Jones Financial Report Analysis• 2011 9

Table 4. Accounts payable turnover and days in accounts payable outstanding calculations for FY09 and FY10

!""#$%&' !"#"$%& !"#$%&'# = !"#$ℎ!"#"

!"#$%&# !""#$%&' !"#"$%&

!"#$ℎ!"#" = !"#$"% !"#$"%&'( − !"#$%%$%# !"#$"%&'( + !"#$

!"#$ !""#$%&' !"#"$%& !"#$#%&'(&) = 365

!""#$%&' !"#"$%& !"#$%&'#

2009 2010

Purchases

224843000

- 257288000 + 1199344000

1186899000

282346000

- 244843000 + 1237358000

1274861000

Average accounts payable

244102000+ 2746080002

= 259355000

244529000+ 2441020002

= 244315500

Accounts payable turnover 4.5763 5.2181

Days in accounts payable

outstanding 79.76 69.95

!"#$"%&'(" !ℎ!"#$ !" !""#$%&' !"#"$%& !"#$%&'# = !"#!"#!!!"#!""# !"#!""#

!"#$"%&'(" !ℎ!"#$ !" !""#$%&' !"#"$%& !"#$%&'# = !.!"#"!!.!"#$ !.!"#$

!"#$"%&'(" !ℎ!"#$ !" !""#$%&' !"#"$%& !"#$%&'# = 0.1402 !" 14.02%

David Jones Financial Report Analysis• 2011 10

Turnover for accounts payable has increased 14.02% in FY09-10, which

indicated DJ has paid outstanding invoices quicker. This might benefit DJ due to early

payment discounts. However, this does not help to realize a stronger net OCF because

more cash is used to pay suppliers.

David Jones Financial Report Analysis• 2011 11

5. Liquidity and Solvency Analysis Table 5. Working capital, current ratio, and quick ratio calculations for FY10

!"#$%&' !"#$%"& = !"##$%& !""#$" − !"##$%& !"#$"!"%"&'

!"#!"#$ !"#$% = !"##$%& !""#$"

!"##$%& !"#$"!"%"&'

!"#$% !"#$% = !"#ℎ !"#$%&!"' !"#ℎ !"#$%&'!()* + !""#$%&' !"#"$%&'("

!"##$%& !"#$"!"%"&'

Current assets 328084000

Current liabilities 313300000

Cash (incl. cash equivalents) 17594000

Accounts receivable 22750000

Working capital 14784000

Current ratio

328084000313300000

= 1.0472

Quick ratio

40344000313300000

= 0.1288

The quick ratio of 0.12877 in FY10 is considerably low due to DJ’s low net cash

flows and low accounts receivables. DJ’s low cash flows were due payment of

dividends and investments into PPE in cash without any borrowings. The low accounts

receivables were a result of the improved management of collecting receivables and

David Jones Financial Report Analysis• 2011 12

transferal of largely debt-funded receivable to Amex. While this ratio may seem

worrying in terms of liquidity, DJ’s size and historical performance suggests that this

would pose little threat to the company. However, it is still something that the firm

needs to monitor.

DJ’s current ratio of above 1 is indicative of adequate liquidity as current

liabilities are covered by current assets 1.04 times over. Also, the current ratio is below

1.5, which signals that DJ has utilized assets productively. However, it is important to

note some issues in interpreting current ratio because a decrease of both current assets

and liabilities when current ratio exceeds 1 will lead to a higher ratio, which could be

misleading. Also, inventories, a major part of the current assets, are evaluated at cost

price. However, inventory is often sold at a profit. Thus, current assets and current ratio

would most likely be understated. Hence, when measuring liquidity, working capital

provides useful information, as the issues mentioned above do not affect it. DJ’s

working capital of $14,784,000 indicates sufficient liquidity to meet its short-term

obligations, if necessary. Together, working capital and current ratio suggest adequate

liquidity.

David Jones Financial Report Analysis• 2011 13

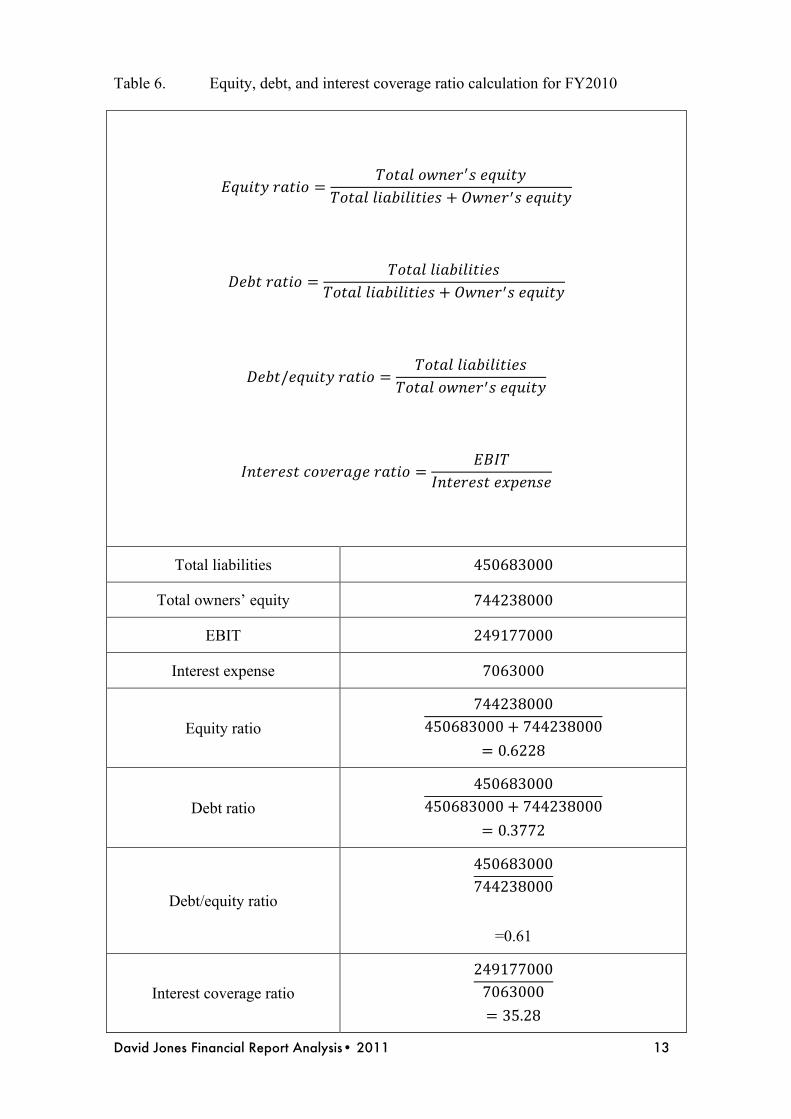

Table 6. Equity, debt, and interest coverage ratio calculation for FY2010

!"#$%& !"#$% =!"#$% !"#$!!! !"#$%&

!"#$% !"#$"!"%"&' + !"#$!!! !"#$%&

!"#$ !"#$% =!"#$% !"#$"!"%"&'

!"#$% !"#$"!"%"&' + !"#$!!! !"#$%&

!"!"/!"#$%& !"#$% =!"#$% !"#$"!"%"&'

!"#$% !"#$!!! !"#$%&

!"#$%$&# !"#$%&'$ !"#$% =!"#$

!"#$%$&# !"#!$%!

Total liabilities 450683000

Total owners’ equity 744238000

EBIT 249177000

Interest expense 7063000

Equity ratio 744238000

450683000+ 744238000

= 0.6228

Debt ratio 450683000

450683000+ 744238000

= 0.3772

Debt/equity ratio

450683000744238000

=0.61

Interest coverage ratio 2491770007063000

= 35.28

David Jones Financial Report Analysis• 2011 14

The debt/equity ratio of 0.61 suggests that on every dollar of equity comes 0.61

dollar of debt. This indicates that DJ has a good solvency as total liabilities are covered

using only 61% of its equity. This implies a low long-term solvency risk. The equity

ratio of 0.6228 also implies a good solvency because more than 50% of the assets are

financed with equity. This suggests lower risks to lenders, thus resulting in lower

interest rates for DJ’s borrowings. Thus, DJ is more likely to meet interest payments.

Consequently, lower interest rates lead to a higher interest coverage ratio, which is

another measure of solvency, because of the lower interest expenses.

David Jones Financial Report Analysis• 2011 15

6. Business Strategy Analysis

DJ’s strategy in FY09-12 is to grow shareholder returns in a sustainable manner.

Through the FY09-FY12 Strategic Plan, there are four main “vehicles” which have been

used to increase the NPAT by 5-10% p.a., which should subsequently increase equity

available to be redistributed as dividends to shareholders:

1. Increase in higher margin categories: Increased the gross profit margin from

39.5% in FY08 to 39.6% in FY09 and from 39.6% in FY09 to 39.7% in FY10.

This has been predominantly achieved by refurbishing 11-14 high value stores5.

2. Opening 4-8 high value new stores: This is to capture the growing customer

base in areas with strong demographics. This increased NPAT (14.8% from

FY07 to FY08 and 9.1% from FY08 to FY09), ultimately helping DJ increase

gross profit margin also. In FY09, agreements were entered to open 4 new

stores6.

3. Delivering costs of doing business (CODB) improvements: By reducing

CODB, costs of goods sold should fall accordingly. This would improve EBIT7,

thus, leading to a higher NPAT. CODB for FY10 was 29.8%, an improvement

of 50 basis points from FY09 (30.3%). This was on top of an improvement of 90

basis points from the FY08 CODB (31.2%).

5 E.g. the Kotara store in the hunter region of NSW and the Bourke St Mall Melbourne Flagship store. 6 Sunshine Plaza (Sunshine Coast, QLD), Whitford (Perth, WA), Macquarie Centre (Sydney, NSW) and Pacific Fair (Gold Coast, QLD). 7 EBIT increased by 9.44% in FY09 to FY10

David Jones Financial Report Analysis• 2011 16

4. Launch of DJ/Amex storecard in time for Christmas FY08: The alliance

announced in Feb 08 caused a significant decrease in accounts receivable

because DJ was able to transfer $374.3 million of accounts receivable to Amex.

Dividends paid on ordinary shares, which by 3.7% in FY08 and 7.14% in FY09,

suggests that DJ is achieving their goal. Also, despite having high capital expenditure in

FY09 due to the store refurbishments, DJ was actually paying high dividends to its

shareholders, suggesting availability of substantial free cash flow.

David Jones Financial Report Analysis• 2011 17

7. Earnings Management Analysis

Figure 2. Percentage changes from FY068

As figure 2 above shows, DJ’s market share price has not mirrored typical

performance indicators such as sales, gross profit, EBIT, and NPAT. This discrepancy

can be explained in two ways: (i) the use of earnings management and (ii) the GFC.

8 Calculated as percentage changes of a given year from FY06. E.g. Percentage change of EBIT FY08 from FY06 was calculated by subtracting EBIT FY06 from EBIT FY08 and then dividing this result by EBIT FY06.

-‐60.00%

-‐40.00%

-‐20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

2006 2007 2008 2009 2010

Percentage change from

FY06

Financial year

Sales Gross proGit EBIT NPAT Total Assets

Total Liabilities Net Assets Market share price ROA ROE

David Jones Financial Report Analysis• 2011 18

While there has been insufficient evidence to argue that DJ has utilized earnings

management, one factor suggests that earnings management might have been used to

achieve steeper increases in NPAT relative to sales performance. DJ’s re-owning of its

flagship Sydney and Melbourne CBD stores in FY06 eliminated $30 million rental

expenses in FY09 and estimated rental expenses of $61 million p.a. in 20 years. This

increased the NPAT due to reduced rental expenses by capitalizing those assets.

However, externalities offer a more plausible explanation for the discrepancy

between share price and NPAT. Market share price is influenced by external factors

such as market expectations of future earnings, natural disasters, global politics and

global financial market situations. Thus, GFC caused the drop in DJ’s share market

price from $4.66 in FY07 to $3.00 in FY09 in spite of a steady increase in NPAT during

FY07 to FY09. In addition, market expectations may have speculated higher NPAT than

DJs actual NPAT. This may have caused the share price of DJ to drop from FY07-09.

However, during Australia’s recovery from the GFC around FY10, expectations of

rising consumer expenditure along with the low share price of $3.00 enticed more

investors to invest with DJ, thus driving market prices up sharply to $4.60. This rise in

share price occurred regardless of modest performance in sales.