David J. Cholst Partner [email protected] (312) 845-3862 Presented by: Matthew Eisel, CFA Senior...

23

David J. Cholst Partner [email protected] (312) 845-3862 Presented by: Matthew Eisel, CFA Senior Managing Consultant [email protected] (717) 232-2723 PFM Asset Management LLC One Keystone Plaza, Suite 300 North Front & Market Streets Harrisburg, PA 17101-2044 www.pfm.com 111 West Monroe Street Chicago, IL 60603- 4080 www.chapman.com Demand Deposit SLGS Investment May 17, 2011

-

Upload

walter-peters -

Category

Documents

-

view

218 -

download

0

Transcript of David J. Cholst Partner [email protected] (312) 845-3862 Presented by: Matthew Eisel, CFA Senior...

David J. Cholst

Partner

(312) 845-3862

Presented by: Matthew Eisel, CFA

Senior Managing Consultant

(717) 232-2723

PFM Asset Management LLC

One Keystone Plaza, Suite 300

North Front & Market Streets

Harrisburg, PA 17101-2044

www.pfm.com

111 West Monroe Street

Chicago, IL 60603-4080

www.chapman.com

Demand Deposit SLGS Investment

May 17, 2011

Chapman and Cutler LLP | PFM Asset Management LLC 2

Table of Contents

I. Overview

II. SLGS Regulations – Required Certifications

III. Pricing, Liquidity, and Potential Uses

Chapman and Cutler LLP | PFM Asset Management LLC 3

I. Overview

Chapman and Cutler LLP | PFM Asset Management LLC 4

Definition

Demand Deposit SLGS

One-day certificates of indebtedness that are automatically rolled over each day until redemption is requested (31 CFR §344.7)

Pay interest at a variable rate (reset weekly) (31 CFR §344.7(a))

Exempt from both yield restriction and rebate (Treas. Reg. §1.150-1(b)(2))

Chapman and Cutler LLP | PFM Asset Management LLC 5

History

1972

SLGS Program initiated

1996

Regulations eliminated both the $35mm limit and advance refunding prohibition

1969

Legislation restricted the yield of investments for tax-exempt bond proceeds

1986 Demand Deposit SLGS introduced

Suggested as part of the 1986 Tax Act in response to a Congressional Mandate to make the SLGS Program more flexible

Designed to be an investment vehicle for avoiding the need for arbitrage rebate computations

Prohibited for advance refundings

1989

Limited to bond issues of $35mm or less

Chapman and Cutler LLP | PFM Asset Management LLC 6

Monthly SLGS Statistics

From: https://www.treasurydirect.gov/govt/reports/slgs/slgs_mnthlyslgsstat.htm

Chapman and Cutler LLP | PFM Asset Management LLC 7

Demand Deposit SLGS Outstanding

1/31/1

996

1/31/1

997

1/31/1

998

1/31/1

999

1/31/2

000

1/31/2

001

1/31/2

002

1/31/2

003

1/31/2

004

1/31/2

005

1/31/2

006

1/31/2

007

1/31/2

008

1/31/2

009

1/31/2

010

1/31/2

011$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$3

$517

$1,211

$5,365

(mill

ion

s)

Chapman and Cutler LLP | PFM Asset Management LLC 8

Tax Regulatory Treatment

For purposes of arbitrage, treated as tax-exempt bonds (Treas. Reg. §1.150-1(b))

Excluded from rebate and yield restriction computations (Code Section 148(b)(3)(A)

Treatment for other Code Sections unclear (e.g. Section 149(g))

Treasury Regulations § 1.149(d)-1(b)(3) provide special rules for “mixed escrows” (may apply to Demand Deposit SLGS)

Chapman and Cutler LLP | PFM Asset Management LLC 9

Demand Deposit vs. Time Deposit SLGS

Demand Deposit Time Deposit

Purchase Increment

May be purchased to the penny (same for redemptions)

Must be purchased in whole dollar amounts

Redemption Time

Depending on size, may be redeemed in 1 or 3 business days

Redemptions in 14 days

Redemption Value

Redeemable at par plus accrued interest

Uses market value redemption formula

RateVariable rate instruments typically reset weekly

Fixed and reset daily

31 CFR 344.7, 8, 9 31 CFR 344.4, 5, 6

Chapman and Cutler LLP | PFM Asset Management LLC 10

II. SLGS Regulations – Required Certifications

Chapman and Cutler LLP | PFM Asset Management LLC 11

SLGS Regulations - Required Certifications

1. Eligible Sources of Funds (31 CFR 344.1)

2. Certifications (31 CFR 344.2(e))

3. Impermissible Practices (31 CFR 344.2(f))

4. Subscription (31 CFR 344.8)

Chapman and Cutler LLP | PFM Asset Management LLC 12

1. Eligible Source of Funds (31 CFR 344.1)

Eligible sources are the same as for Time Deposit SLGS and include:

Gross proceeds of a tax-exempt bond issue (or reasonably expected to become gross proceeds)

Former gross proceeds

Amounts held in a commingled fund with gross proceeds

Proceeds of a taxable issue that refunds or is refunded by a tax-exempt issue

Other amounts subject to §148 yield restriction limitations (BAB proceeds that are not excepted)

Chapman and Cutler LLP | PFM Asset Management LLC 13

2. Certifications

Certifications are similar to Time Deposit SLGS (though not as comprehensive) and include:

– Agency Certification (31 CFR 344.2(e)(1))

– Purchased with early liquidation proceeds• Yield means what it means for arbitrage (§ 1.148-5) – not applicable

– No certification required on redemption (31 CFR 344.2(e)(2)(ii))

Chapman and Cutler LLP | PFM Asset Management LLC 14

3. Impermissible Practices (31 CFR 344.2(f))

Generally the same as for Time Deposit SLGS (except for redemptions)

No “cost-free” option

Limitation on yield of purchased SLGS

Chapman and Cutler LLP | PFM Asset Management LLC 15

4. Subscription

Information needed to enter subscription into SLGSafe: (31 CFR 344.8(b))

− Issue date

− Principal amount

− Issuer name and TIN

− Title of officer authorized to purchase (and redeem) SLGS

− Description of tax-exempt bond issue

Time requirements (31 CFR 344.8(a))

− Subscription due At least 5 business days prior to the issue date for issues consisting of

$10 million or less At least 7 days prior to the issue date for issues greater than $10

million

− No more than 60 days in advance

Chapman and Cutler LLP | PFM Asset Management LLC 16

III. Pricing, Liquidity and Potential Uses

Chapman and Cutler LLP | PFM Asset Management LLC 17

Pricing

Tax-exempt and variable rate Priced off of 3-month Treasury Bill (“T-Bill”)

– typically yields 75% of the T-Bill yield Rate usually refreshed each Tuesday, the day after new T-Bill auction Demand Deposit SLGS rate may be higher than one- or two-month Time Deposit

SLGS rate

4/20

/201

0

5/11

/201

0

6/1/

2010

6/22

/201

0

7/13

/201

0

8/3/

2010

8/24

/201

0

9/14

/201

0

10/5

/201

0

10/2

6/20

10

11/1

6/20

10

12/7

/201

0

12/2

8/20

10

1/18

/201

1

2/8/

2011

3/1/

2011

3/22

/201

1

4/12

/201

10.00%0.02%0.04%0.06%0.08%0.10%0.12%0.14%0.16%0.18%

Demand Deposit SLGS vs. 1-Month Time Deposit SLGS

DD SLGS 1-mo TD SLGS

Chapman and Cutler LLP | PFM Asset Management LLC 18

Pricing Considerations

Usually don’t know rate when subscription is placed – Subject to weekly reset (makes market calls a bit more difficult)

Preserve optionality – Outperform if Fed increases target rate (“reinvestment risk” not a big concern)

4/20/2010 5/21/2010 6/21/2010 7/22/2010 8/22/2010 9/22/2010 10/23/2010 11/23/2010 12/24/2010 1/24/2011 2/24/2011 3/27/20110.00%

0.05%

0.10%

0.15%

0.20%

0.25%

Demand Deposit SLGS vs. 6-Month T-Bill

DD SLGS 6-mo T-bill

Chapman and Cutler LLP | PFM Asset Management LLC 19

Comparison to Money Market Funds

Demand Deposit SLGS may provide higher yield than Treasury-only money market funds

4/20/2010 5/21/2010 6/21/2010 7/22/2010 8/22/2010 9/22/2010 10/23/2010 11/23/2010 12/24/2010 1/24/2011 2/24/2011 3/27/20110.00%

0.02%

0.04%

0.06%

0.08%

0.10%

0.12%

0.14%

Demand Deposit SLGS vs. Money Market Fund (Treasury-Only)

DD SLGS Goldman Sachs Financial Square Funds - Government Series

Chapman and Cutler LLP | PFM Asset Management LLC 20

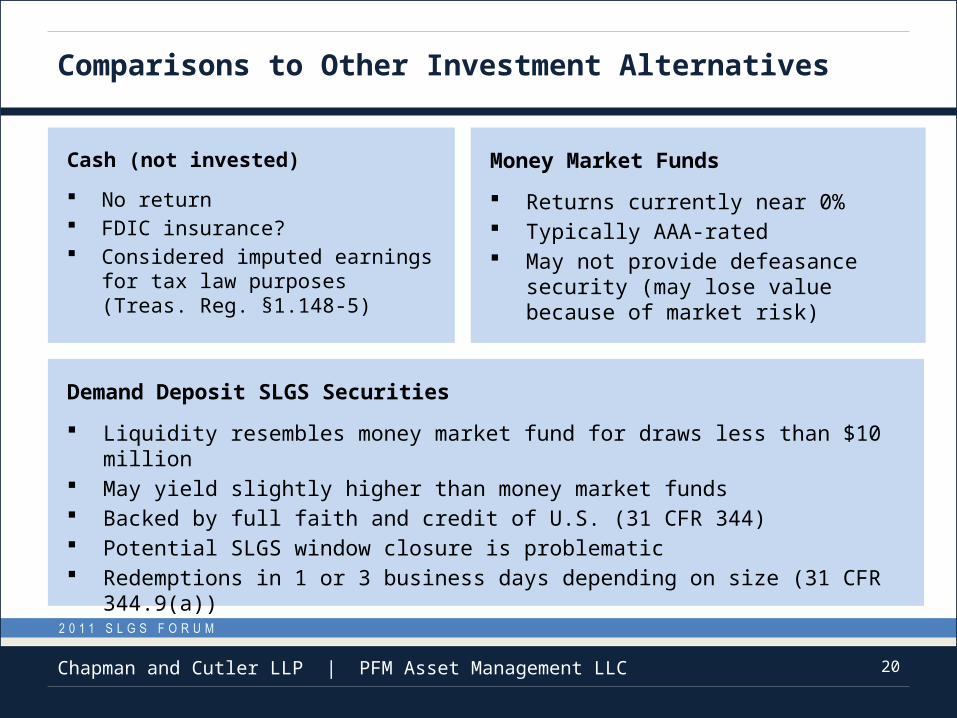

Comparisons to Other Investment Alternatives

Cash (not invested)

No return FDIC insurance? Considered imputed earnings for

tax law purposes (Treas. Reg. §1.148-5)

Demand Deposit SLGS Securities

Liquidity resembles money market fund for draws less than $10 million May yield slightly higher than money market funds Backed by full faith and credit of U.S. (31 CFR 344) Potential SLGS window closure is problematic Redemptions in 1 or 3 business days depending on size (31 CFR 344.9(a))

Money Market Funds

Returns currently near 0% Typically AAA-rated May not provide defeasance security

(may lose value because of market risk)

Chapman and Cutler LLP | PFM Asset Management LLC 21

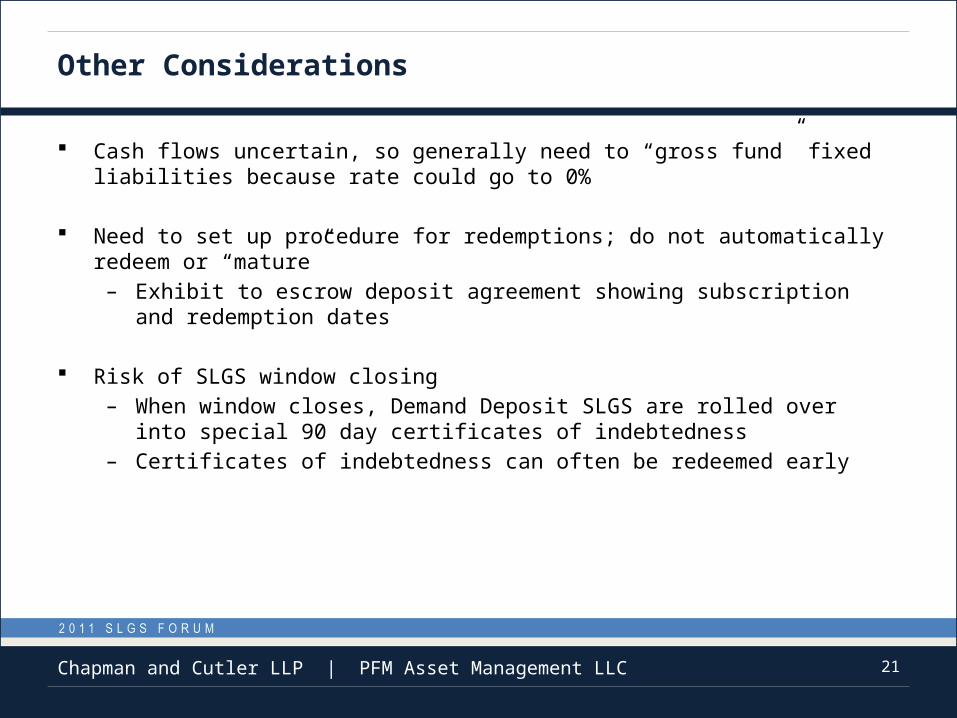

Other Considerations

Cash flows uncertain, so generally need to “gross fund” fixed liabilities because rate could go to 0%

Need to set up procedure for redemptions; do not automatically redeem or “mature”– Exhibit to escrow deposit agreement showing subscription and redemption dates

Risk of SLGS window closing– When window closes, Demand Deposit SLGS are rolled over into special 90 day

certificates of indebtedness – Certificates of indebtedness can often be redeemed early

Chapman and Cutler LLP | PFM Asset Management LLC 22

Common Uses of Demand Deposit SLGS

Escrows May allow for an

escrow that yields above the bond yield

Especially useful for current refundings and float periods

Debt Service Funds Could be useful if

not considered a “bona fide debt service fund” – arbitrage a concern

Project Funds With strict permitted

investments language

Good liquidity and potential to earn positive arbitrage if yield curve is flat or inverted

Chapman and Cutler LLP | PFM Asset Management LLC 23

Unique Considerations and Investment Strategies

Useful for periods of less than 30 days when you want to earn interest – Better alternative to 0% SLGS in 15 to 29 day window unless yield restriction

concerns exist– Less costly and administratively simple alternative to purchasing open market

Treasuries

Use in funds subject to rebate or yield restriction in high interest rate environment – retainable earnings in excess of arbitrage yield