Daily Information 12/2/13 Objectives: 1.Explain the concept of risk. 2.Describe risk assessment and...

31

Daily Information 12/2/13 Objectives: 1.Explain the concept of risk. 2.Describe risk assessment and list four risk strategies. Warm Up: What risks do you take every day? How serious are those risks? Discuss this with the person sitting next to Agenda: 1.Warm up 2.Review of assignments 3.Vocab. 4.What is Risk P.P. 5.Lesson assessment activities (base group) 6.Bottom Line

-

Upload

rosalind-lawrence -

Category

Documents

-

view

215 -

download

0

Transcript of Daily Information 12/2/13 Objectives: 1.Explain the concept of risk. 2.Describe risk assessment and...

Daily Information 12/2/13Objectives:

1.Explain the concept of risk.

2.Describe risk assessment and list four risk strategies.

Warm Up:

What risks do you take every day? How serious are those risks?

Discuss this with the person sitting next to you.

Agenda:

1.Warm up2.Review of assignments3.Vocab. 4.What is Risk P.P.5.Lesson assessment activities (base group)6.Bottom Line

Upcoming Assignments

Friday 12/2/13

10 minute writing sample “What have you learned in this class so far?”

Choice novel project review

Resume project update

What Is Risk?

Risk: the chance of injury, damage, or economic loss.

• May be avoidable, unpredictable, and unavoidable.

Loss: a physical injury, damage to property, or disappearance of property

**Could have a major impact on your life

Examples of Risk & Loss

Driving a car (risk)o An accident may occur with another

car causing personal injury and damage to the car (loss)

Snow skiing (risk)o An accident may occur while skiing

such as breaking your leg (loss)

Probability of Risk• Risk does not always equal loss, you may

avoid loss• If you avoid loss once, this does not mean

you will always do so• You must weigh the risk and loss of your

actions. Are they serious? Can you reduce the risk or loss?

**Business owners face additional types of risk including: economic conditions, competition, and technology

Consumer RiskPersonal risk: loss of personal value.o Example: breaking a leg missing fun activity

Some risks result in a financial loss.o Example: driving without insurance paying a lot

of money to repair car

Some risks jeopardize financial resources.o Example: getting sued for causing an injury to

another having your wages garnished to pay for judgment against you

Risk Management• Risk assessment: identifying risks and

deciding how serious they are.

• Use risk strategies to protect yourself against loss.o Reduce risk (change your actions)o Avoid risk (stop a certain behavior)o Transfer risk (buy insurance)o Assume risk (self-insure through

savings)

**Have you ever used risk management? Discuss this with the person sitting next to you.

Risk Assessment

RiskProbability of Occurrence

SeriousnessRating*

PossibleConsequences

Losing my job Medium 10 Missed payments Lower credit rating

Getting in a car accident

Unknown 10 Personal injury Lawsuit

Suffering physical injury from snowboarding

Medium 3 Missed work time Medical bills

Having bike stolen

Low 2 New/used bike purchase

* 1 is low risk; 5 is medium risk; 10 is high risk

Group Activity Within your base group, complete the following

(Page 192 & 193):

Key Terms Review (1-9)

Check Your Understanding (10-20)

Think Critically (21-26)

**Everyone in the group should record the answers and have a copy for when we review as a class!

Daily Information 4/9Objectives:

1.Explain the concepts of risk.2.List the three types of risk that consumers face.3.Describe risk assessment and list four risk strategies.

Warm Up:

Grab a textbook and complete the activity from yesterday.

Agenda:

1.Warm up2.Vocab., Sec. 23.Health Insurance P.P.4.Lesson assessment assignment

Group Activity Complete the following (Page 192 & 193):

Key Terms Review (1-9)

Check Your Understanding (10-20)

Think Critically (21-26)

What is Health Insurance?A plan that shares the risk of medical costs.

• Could be individual or group (employer)

**Better coverage equals higher premiums

Health Insurance Terms In your own words, explain the

difference between a deductable, a premium, and a co-pay. These are all costs you pay for your insurance.

Types of Health CoverageFee-for-service (Unmanaged Care)• You choose medical providers

PPO (MANAGED CARE)• Independent health care providers that work

together to provide health care. Referrals not required.

HMO (MANAGED CARE)• Provides prepaid medical care for its

members

**Managed Care: network of providers

Health CareTypes

Basic Health Care: medical, hospital, surgery

Major Medical: very serious injury or illness beyond basic coverage

Dental and Vision

Long-term care: nursing homes and assisted living

Managing Costs Deductibles and Copays: the

part you pay. If lower, then insurance premium is higher

Stop-Loss Provisions: after you pay a certain amount, insurance pays 100%

Health Spending Accounts FSA-flexible spending account HSA- health savings account

Disability InsuranceProvides income when you cannot work

due to injury or illness (not work related).

• It replaces a portion or percentage of normal earnings.

• Short-term: 30 days

• Long-term: 90 days

Disability Insurance You are unable to work due to an injury. Your

short-term disability insurance coverage provides 66% of your regular pay. If your regular annual salary is $42,000 per year, how much is your insurance providing you per month?

$42,000 x .66 = $27,720

$27,720/12 = $2,310

Life InsurancePays money to a beneficiary upon the death of

the insured person.

• Temporary or Term: provides a death benefit only.

• Permanent: provides a death benefit and builds cash value.

• Group life: is available through employers.

**Create a list of reasons why people may want to buy life insurance with the person sitting next to you.

Focus On . . .page 198 Read the information regarding the health

care reform

Focus On . . .page 198 Health Care Reform• Most Americans will have insurance by 2020.• Purchasing health insurance will be mandatory.• Citizens cannot be denied coverage for pre-existing

conditions.• Tax increases will pay for health care reform.• A major omission from the reform is a control on

health care costs. Do you agree that we should have mandatory health

insurance in the U.S.?

What Is Homeowner’s Insurance?• Homeowner’s insurance:

• protects the policyholder from risk of loss to a home and its contents.

• It covers three types of risk.o Fire and other hazards (peril)o Criminal activityo Personal Liability(when others are injured on your

property)

**Homeowner’s insurance should cover the replacement cost which will pay to rebuild the home if it is completely destroyed.

What if I rent, not own?... **Buy Renter’s Insurance

A renter (tenant) cannot insure the building BUT you can insure your contents.

Always purchase renter’s insurance to protect against risk of loss of personal property.

Just like a homeowners policy, cover things like fire, theft, and other hazards.

Includes personal liability coverage for what happens inside your residence.

***May be provided by a parent or guardian while an individual is still a full time student or under the age of 18

Home InventoryCreate a home inventory in case you need to file a claim.

How Does Insurance Protect Car Owners?• Automobile insurance

protects a car owner from losses as a result of accidents and other events.

• Cost depends on • Model/style of car• Age (and gender)• Driving record of driver.

Types of Auto Insurance Coverage

• Full coverage is required if you have a car loan. It includes:o Liabilityo Collisiono Comprehensiveo Personal injury protectiono Uninsured/Underinsured Motoristo Towing/Rental Car

Insurance Coverage Defined

o Protects against…o Liability: loss as a result of injury to another

person or damage to that person’s propertyo Collision: damage to our own vehicle if you hit

another car or lose control and roll overo Comprehensive: damages to your car from

causes other than collision or rolling overo Uninsured/Underinsured Motorist: damages

caused by a motorist who is at fault and does not have insurance or the means to pay for your damages.

How Can You Reduce Auto Insurance Costs and Maximize Benefits?

• Reducing costs can raise your overall risk but it can help you manage your budget.

• Lower your costs using these strategies:

choose higher deductibles change your driving habits* buy online comparison shop

• Maximize benefits by reviewing your policy or getting umbrella coverage (liability insurance for extraordinary losses).

Change your driving habitsLower premium costs

Take driving training class

Maintain good driving record

Get good grades in school

Choose a car with high safety rating

Install security devices on your car

Park in garage or protected area

Reduce risk Drive while rested instead of

when tired

Keep your car properly serviced

Avoid heavy traffic or bad weather

Drive defensively; be aware of other drivers

Avoid using cell phones, eating or other distractions

Daily Information 4/16Objectives:

1.Explain the purpose of a budget.

2.Identify proper banking procedures.

3.Categorize different types of risk and insurance.

Warm Up:

How can you be prepared in case you need to file a claim for the loss of property due to theft or fire?

Agenda:

1.Warm up2.Crossword puzzle review3.Mind Map4.Bottom Line

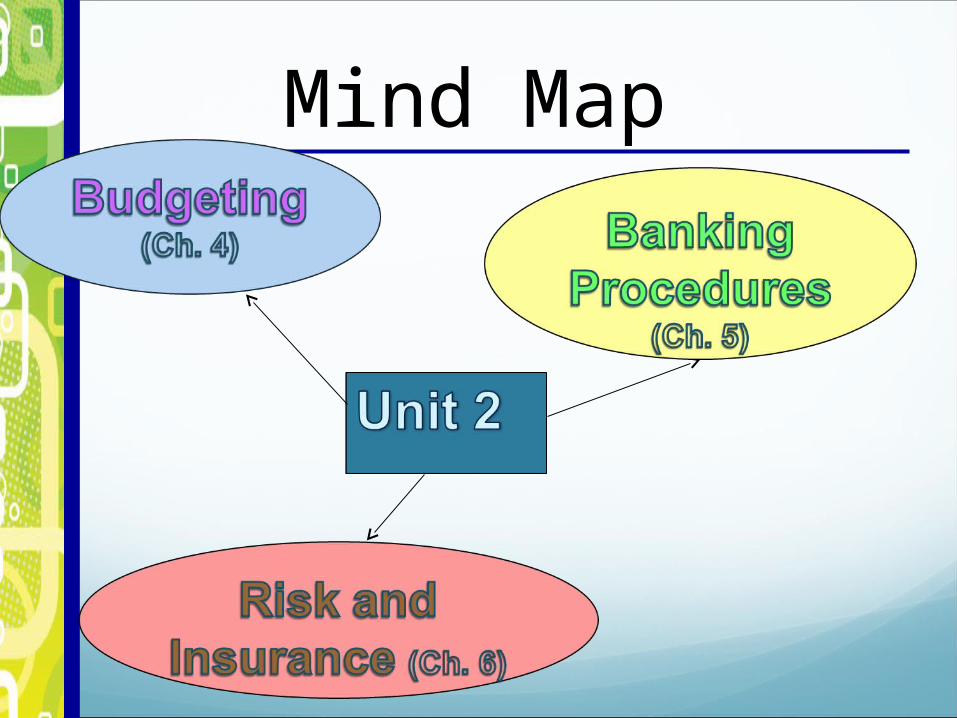

Mind Map

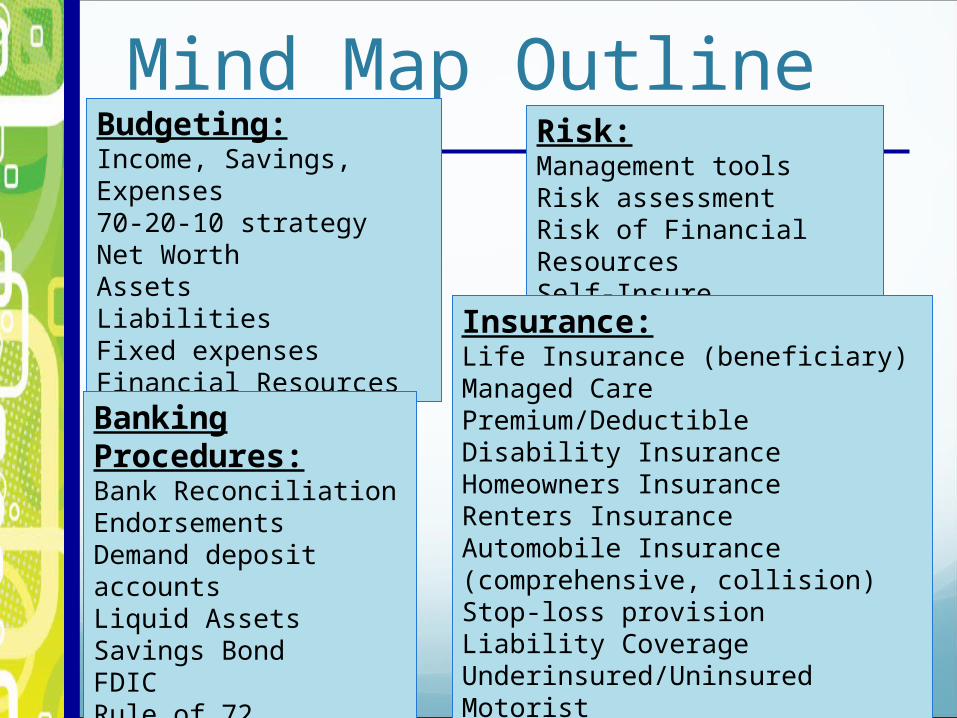

Mind Map Outline Budgeting:Income, Savings, Expenses70-20-10 strategy Net WorthAssetsLiabilitiesFixed expensesFinancial Resources

Banking Procedures:Bank ReconciliationEndorsements Demand deposit accountsLiquid Assets Savings BondFDICRule of 72

Risk:Management toolsRisk assessmentRisk of Financial ResourcesSelf-Insure

Insurance:Life Insurance (beneficiary)Managed CarePremium/DeductibleDisability InsuranceHomeowners InsuranceRenters InsuranceAutomobile Insurance (comprehensive, collision) Stop-loss provision Liability CoverageUnderinsured/Uninsured Motorist