D & G case study.doc

10

Dougall & Gilligan Global Agency Dougall & Gilligan GlobalAgency (D & G), one of the larger advertising agencies in the world with over 11,000 employees, had its origin in 11! through a predecessor firm" #ts head$uar ter is in the %ew or' city of ""A" *oreign busi ness of D & G now accounts for + - of the total commission and fee income" .esides, the ten largest clients provides !/ - of the income" D & G is the corporate umbrella under which five operating units are there, D & G being the largest" 1) Wh at ar e th e company’s fi na ncial co nd ition and pe rformance, its funds requirements, and business risk? Sources and Applications of Funds (11!1") aor uses of funds increases in intangible assets (23/"+ ) and net fi4ed assets (2!3"5 )" 6his is consistent with the ac$uisition strategy pursued by the company over the past years" Another significant uses of funds are dividends (27 ), currency losses (2+0 ust in 1!), stoc' repurchases and other adustments that could reduce shareholders e$uity" oreover, cash position has improved over this period (25/ )" 6hese uses were fin ance d lar gel y by the company8s pro fit abl e ope rat ions (2! 70 ), the iss uanc e of convertible subordinated debentures (231 ) and stoc' issuance (2+ )" 9ther minor sour ces of funds are incr ea ses in ban' loans (2!5 ) , ac cr ua ls and de fe rr ed compensations" (refer 6able 1) #able 1$ Source and %ses of Funds (11!1") 1 Sources %ses %et #ncome !1" #ncrease in :ash 5/"/ #ncrease in .an' %otes !5"0 #ncrease in Accounts ;eceivables 1!"0 #ncrease in Accounts <ayable +" #ncrease in 9ther :lient .illables "3 #ncrease in Accruals !0"5 #ncrease in 9ther :urrent Assets 5"1 #ncrease in :onv" ub" Debentures 31"0 #ncrease in %et *i 4ed Assets !3"5 #nc rea se i n Def" :o mp ens ati on and ;e ser ves !!"0 #ncrease in 9ther Assets /"0 #ncrease in Acrruals <ost=;etirement //"5 #ncrease in #ntangibable Assets 3/"+ #ncrease in 9ther >iabilities 7"3 Decrease in >ong 6erm Debt 10"0 toc' #ssuance +"0 Dividends 7"+ Adustment in hareholders ?$uity (toc' ;epurchases, :urrency >osses, Assets write offs)@ 173"+ #otal "&'$1 #otal "&'$1 @6here is not enough information in the case about the specifics of some of t hese transactions" e put them all t ogether recog niBing that the total change in sharehold ers e$uity is affected by retained earnings (difference between net income and dividends), stoc' repurchases, foreign currency translations losses or gains and other adustments"

-

Upload

vrusti-rao -

Category

Documents

-

view

220 -

download

0

Transcript of D & G case study.doc

8/14/2019 D & G case study.doc

http://slidepdf.com/reader/full/d-g-case-studydoc 1/10

Dougall & Gilligan Global Agency

Dougall & Gilligan GlobalAgency (D & G), one of the larger advertising agencies in theworld with over 11,000 employees, had its origin in 11! through a predecessor firm" #ts

head$uarter is in the %ew or' city of ""A" *oreign business of D & G now accountsfor + - of the total commission and fee income" .esides, the ten largest clients provides!/ - of the income" D & G is the corporate umbrella under which five operating units arethere, D & G being the largest"

1) What are the company’s financial condition and performance, its funds

requirements, and business risk?

Sources and Applications of Funds (11!1")

aor uses of funds increases in intangible assets (23/"+ ) and net fi4ed assets (2!3"5)" 6his is consistent with the ac$uisition strategy pursued by the company over the pastyears" Another significant uses of funds are dividends (27 ), currency losses (2+0 ust in 1!), stoc' repurchases and other adustments that could reduce shareholderse$uity" oreover, cash position has improved over this period (25/ )" 6hese uses werefinanced largely by the company8s profitable operations (2!70 ), the issuance ofconvertible subordinated debentures (231 ) and stoc' issuance (2+ )" 9ther minorsources of funds are increases in ban' loans (2!5 ), accruals and deferredcompensations" (refer 6able 1)

#able 1$ Source and %ses of Funds (11!1")

1

Sources %ses

%et #ncome !1" #ncrease in :ash 5/"/

#ncrease in .an' %otes !5"0 #ncrease in Accounts ;eceivables 1!"0

#ncrease in Accounts <ayable +" #ncrease in 9ther :lient .illables "3

#ncrease in Accruals !0"5 #ncrease in 9ther :urrent Assets 5"1

#ncrease in :onv" ub" Debentures 31"0 #ncrease in %et *i4ed Assets !3"5

#ncrease in Def" :ompensation and ;eserves !!"0 #ncrease in 9ther Assets /"0

#ncrease in Acrruals <ost=;etirement //"5 #ncrease in #ntangibable Assets 3/"+ #ncrease in 9ther >iabilities 7"3 Decrease in >ong 6erm Debt 10"0

toc' #ssuance +"0 Dividends 7"+ Adustment in hareholders ?$uity (toc'

;epurchases, :urrency >osses, Assets write

offs)@ 173"+

#otal "&'$1 #otal "&'$1

@6here is not enough information in the case about the specifics of some of these transactions" e put them all together recogniBing that the

total change in shareholders e$uity is affected by retained earnings (difference between net income and dividends), stoc' repurchases, foreign

currency translations losses or gains and other adustments"

8/14/2019 D & G case study.doc

http://slidepdf.com/reader/full/d-g-case-studydoc 2/10

Financial atios

6he first thing to note is that the company bills their customers and pays the media for theads placed" 6herefore, the company has a lot of receivables and payables" 9n average,commissions and fees to D&G are only 1/- of these billings"

6he current ratio is slightly lower than the industry median (1"04 vs" 1"14 for theindustry) and it has fluctuated very little over the past 5 years" A $uic' ratio does notma'e sense here because the firm does not have inventories" Average collection periodfluctuated without any particular trend, and it is lower than the industry (5! vs" +! days)"6otal debt=to=e$uity ratio is higher than the industry median ("/4 vs" 5"+4) 6his ratio isso high because it includes accounts payables (+7- of total liabilities)"6imes interest earned has increased over the period, reflecting a slight improvement inthe company8s ability to service" Cowever, it is well below the industry median (5"4 vs"1/"34)<rofitability has increased over the years and it is above the industry" <rofit before ta4esare "3- vs" /"1- for the industry" 6he company8s <? ratio has fluctuated over the years

and it is currently at !"14 vs" the 13"+4 industry median" (refer 6able !)

#able $ Financial atios

!

1991 1992 1993 1994 Industry

Liquidity Ratios

Current Ratio 1.05 1.09 1.10 1.06 1.1

Average collection period 51.42 45.65 38.48 42.15 52

Debt Ratios

Total Debtto!"uit# 6.98 6.20 $.43 6.89 4.5%T Debt & !nterpri'e (alue 0.11 0.12 0.14 0.14

%T Debt & Tangible A''et' 0.13 0.15 0.12 0.12

)ntere't *earing Debt & !*)T 2.$0 2.51 2.14 2.63

Coverage Ratios

Ti+e' )ntere't !arned ,!*)T&)ntere't- 4.44 4.09 4.68 4.61 13.8

Profitability

et /roit argin 4.$ 5.3 5.$ 5.6

/roit *eore Tae' & ale' 9.2 9.8 10.2 9.8 3.1

Market!alue Ratios

/&! Ratio 24.15 29.93 30.00 26.0$ 18.5

Dividend ield 0.35 0.31 0.28 0.33

P"# Ratios for Co$%etitors

oote7 Cone and *elding 18

)nterpublic roup 19

+nico+ roup 16

:// roup 2$

ean 20

edian 18.5

8/14/2019 D & G case study.doc

http://slidepdf.com/reader/full/d-g-case-studydoc 3/10

*usiness isks

Cyclical risk E orldwide spending on advertising has increased in 15=+, drivingcompany8s revenues" Cowever, spending on advertising is highly correlated with thelevel of economic activity in a country" .ecause it is a discretionary e4pense it is one ofthe costs that companies cut first in the event of an economic turndown"

Seasonal risk E 6here is a moderate seasonality in the demand for advertising serviceswith an increase towards the year=end"

Currency risk E *oreign business account for +- of total commission and fees" D&Ghas no hedging strategy and incurs significant translation gainslosses when 2foreigncurrency e4change rate changes"

Uncertainty of the information technology development E Advertising agencies areaggressively pursuing participation in interactive communication an the internet" 6his is anew area for advertising and its future and development are uncertain"

Competition E 6he company is one of the three largest players in the industry, and thecompetition is intense" uccess is determined by the balance between efficient operationsand a creative edge"

Liquidity- Although they try to collect payments and pay at about the same time, a smallincrease in the gap of collections vs" payables could have a large effect on the company8sneed for cash"

Company specific risk - 6he company8s beta is 1"/ compared to 1"1 industry average"

) +o the eistin- means of financin- unduly restrict the company?

6he following table summariBes the past financing decisions of the company and itsimplications"

#able .$ /haracteristics of 0ast Financin-

/

8/14/2019 D & G case study.doc

http://slidepdf.com/reader/full/d-g-case-studydoc 4/10

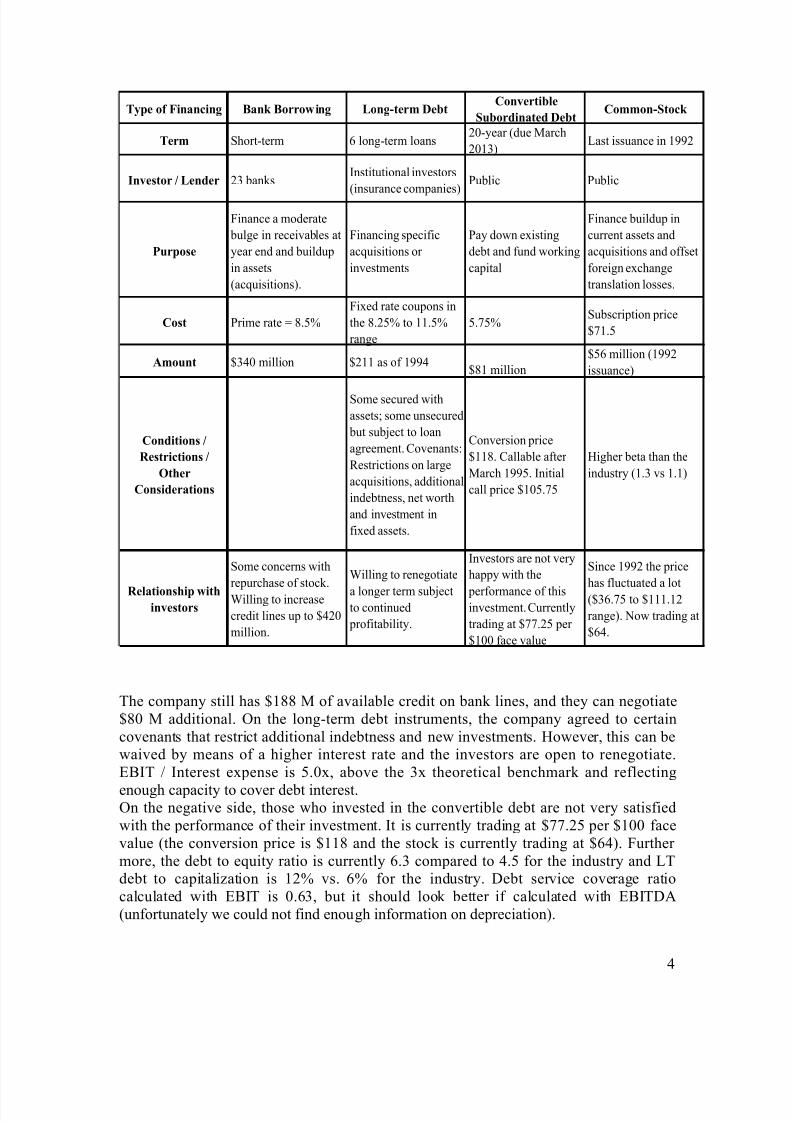

6he company still has 2133 of available credit on ban' lines, and they can negotiate230 additional" 9n the long=term debt instruments, the company agreed to certaincovenants that restrict additional indebtness and new investments" Cowever, this can bewaived by means of a higher interest rate and the investors are open to renegotiate"?.#6 #nterest e4pense is +"04, above the /4 theoretical benchmar' and reflecting

enough capacity to cover debt interest"9n the negative side, those who invested in the convertible debt are not very satisfiedwith the performance of their investment" #t is currently trading at 277"!+ per 2100 facevalue (the conversion price is 2113 and the stoc' is currently trading at 25)" *urthermore, the debt to e$uity ratio is currently "/ compared to 5"+ for the industry and >6debt to capitaliBation is 1!- vs" - for the industry" Debt service coverage ratiocalculated with ?.#6 is 0"/, but it should loo' better if calculated with ?.#6DA(unfortunately we could not find enough information on depreciation)"

5

#ype of Financin- *ank *orro1in- 2on-!term +ebt/on3ertible

Subordinated +ebt/ommon!Stock

#erm hort=term long=term loans!0=year (due arch

!01/)>ast issuance in 1!

4n3estor 5 2ender !/ ban's#nstitutional investors

(insurance companies)<ublic <ublic

0urpose

*inance a moderate

bulge in receivables at

year end and buildup

in assets

(ac$uisitions)"

*inancing specific

ac$uisitions or

investments

<ay down e4isting

debt and fund wor'ing

capital

*inance buildup in

current assets and

ac$uisitions and offset

foreign e4change

translation losses"

/ost <rime rate F 3"+-

*i4ed rate coupons in

the 3"!+- to 11"+-

range

+"7+-ubscription price

271"+

Amount 2/50 million 2!11 as of 15231 million

2+ million (1!

issuance)

/onditions 5

(estrictions 5

6ther

/onsiderations

ome secured with

assetsG some unsecured

but subect to loan

agreement" :ovenantsH

;estrictions on large

ac$uisitions, additional

indebtness, net worth

and investment in

fi4ed assets"

:onversion price

2113" :allable after

arch 1+" #nitial

call price 210+"7+

Cigher beta than the

industry (1"/ vs 1"1)

(elationship 1ithin3estors

ome concerns with

repurchase of stoc'"Ailling to increase

credit lines up to 25!0

million"

Ailling to renegotiate

a longer term subectto continued

profitability"

#nvestors are not very

happy with the

performance of thisinvestment" :urrently

trading at 277"!+ per

2100 face value

ince 1! the price

has fluctuated a lot(2/"7+ to 2111"1!

range)" %ow trading at

25"

8/14/2019 D & G case study.doc

http://slidepdf.com/reader/full/d-g-case-studydoc 5/10

#n summary, D&G faces some restrictions as a conse$uence of its past financingdecisions, but we believe that the company will be able to finance the e4pansion proectand will have to choose among different alternatives"

+

8/14/2019 D & G case study.doc

http://slidepdf.com/reader/full/d-g-case-studydoc 6/10

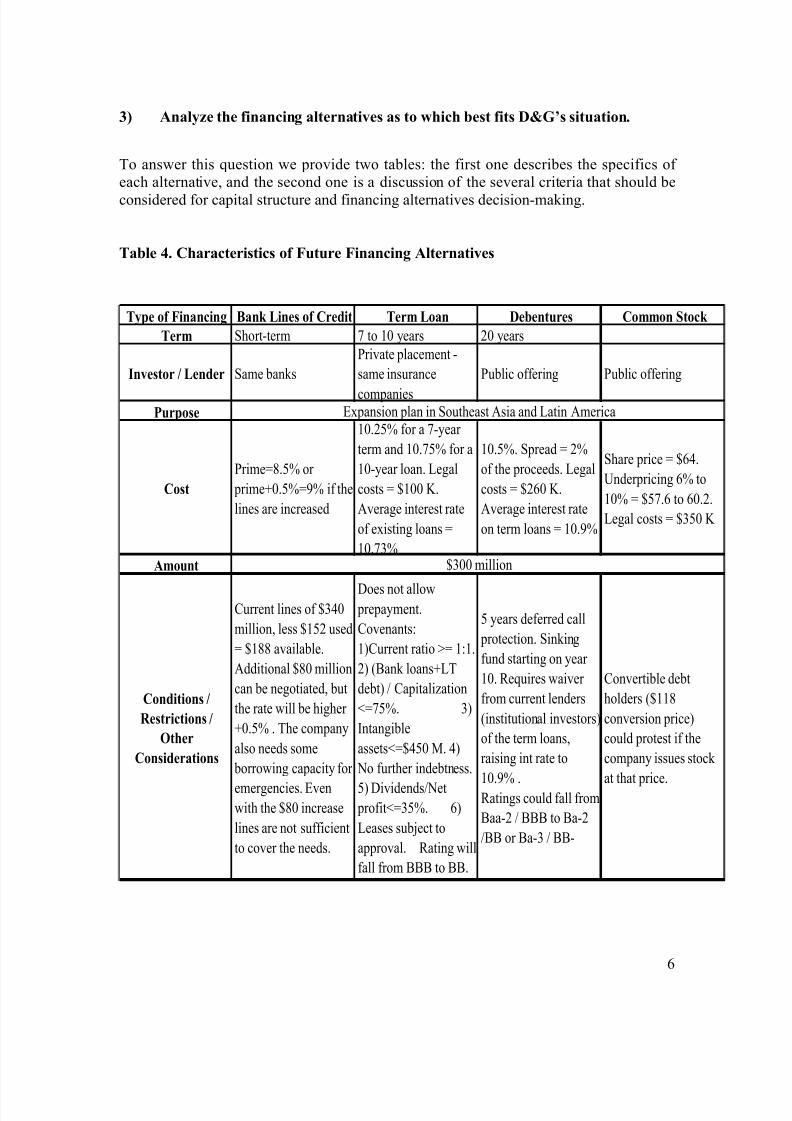

.) Analy7e the financin- alternati3es as to hich best fits +89’s situation$

6o answer this $uestion we provide two tablesH the first one describes the specifics ofeach alternative, and the second one is a discussion of the several criteria that should be

considered for capital structure and financing alternatives decision=ma'ing"

#able "$ /haracteristics of Future Financin- Alternati3es

#ype of Financin- *ank 2ines of /redit #erm 2oan +ebentures /ommon Stock

#erm hort=term 7 to 10 years !0 years

4n3estor 5 2ender ame ban's

<rivate placement =

same insurance

companies

<ublic offering <ublic offering

0urpose

/ost

<rimeF3"+- or

primeI0"+-F- if the

lines are increased

10"!+- for a 7=year

term and 10"7+- for a

10=year loan" >egal

costs F 2100 J"

Average interest rate

of e4isting loans F

10"7/-

10"+-" pread F !-

of the proceeds" >egal

costs F 2!0 J"

Average interest rate

on term loans F 10"-

hare price F 25"

nderpricing - to

10- F 2+7" to 0"!"

>egal costs F 2/+0 J

Amount

/onditions 5

(estrictions 5

6ther

/onsiderations

:urrent lines of 2/50

million, less 21+! used

F 2133 available"

Additional 230 million

can be negotiated, but

the rate will be higher

I0"+- " 6he company

also needs some

borrowing capacity for

emergencies" ?venwith the 230 increase

lines are not sufficient

to cover the needs"

Does not allow prepayment"

:ovenantsH

1):urrent ratio KF 1H1"

!) (.an' loansI>6

debt) :apitaliBation

LF7+-" /)

#ntangible

assetsLF25+0 " 5)

%o further indebtness"

+) Dividends%et profitLF/+-" )

>eases subect to

approval" ;ating will

fall from ... to .."

+ years deferred call

protection" in'ing

fund starting on year

10" ;e$uires waiver

from current lenders

(institutional investors)

of the term loans,

raising int rate to

10"- ";atings could fall from

.aa=! ... to .a=!

.. or .a=/ ..=

:onvertible debt

holders (2113

conversion price)

could protest if the

company issues stoc'

at that price"

?4pansion plan in outheast Asia and >atin America

2/00 million

8/14/2019 D & G case study.doc

http://slidepdf.com/reader/full/d-g-case-studydoc 7/10

#able :$ /riteria for +ecision!;akin-

7

/riteria *ank 2ines of /redit #erm 2oan +ebentures /ommon Stock

<*4#!<0S Analysis

+ebt (atios

10"70- !1"- !1"- 10"70-

/"37 /"37 /"37 !"/1

7"!0 7"!0 7"!0 /"/1

/o3era-e (atios

!"+ !"7 !"7+ +"0+

0"!! 0"+7 0"+7 0"/

<rimeF3"+- or

primeI0"+-F- if the

lines are increased

10"!+- for a 7=year term

and 10"7+- for a 10=year

loan" >egal costs F 2100

J" Average interest rate of

e4isting loans F 10"7/-

10"+-" pread F !- of the

proceeds" >egal costs F

2!0 J" Average interest

rate on term loans F 10"-

hare price F 25"

nderpricing - to 10- F

2+7" to 0"!" >egal costs

F 2/+0 J

(atin-s

6he companyMs credit

rating could be

downgraded from ... to

.."

;atings could fall from

.aa=! ... to .a=! ..

or .a=/ ..=

6here is not enough

information to assess the

chance of a better credit

rating, but certainly it

should not be adusted

downward"

6hese are basically the direct costs of each type of financing in the form of interest rate, legal and out=of=poc'ete4penses"

<,plicit /osts

6his ratio measures the ability to cover not only interests but also principal payments" 6he formula is ?.#6

(#nterest I <rincipal payments(1=ta4 rate)" ;emember that principal payments are adusted by the ta4 rate

because they are not deductible " 6he number for .an' lines of credit is smaller because the we included the

whole amount of debt as a current maturity"

>6 Debt to

:apitaliBation

#nterest .earingDebt to ?.#6

Debt to ?$uity

6imes #nterest

?arned

Debt ervice

:overage

.oth the term loan and the debentures alternative increase substantially the >6 debt to capitaliBation ratio

6hese figures are the same for the three types of debt and contrast sharply with the ratio that the company

currently has of !"/1 (that would be maintained if the company goes with e$uity)"

All the ratios seem very high" Cowever, it is important to note that in this case debt includes the huge ammount

in accounts receivables" Any type of debt would increase this ratio to 7"!, but an e$uity offering would reduce it

significantly" 6he company currently has a "/ ratio compared with a 5"+ for the industry"

6his is ?.#6#nterest ?4pense" :urrently, the company has a +"0+ ratio that compers favorably to the industry

figure of /" A common stoc' issuance would not have any effect on this, but any 'ind of debt would reduce the

coverage of interests" %otice that the difference among the three types of debt comes from the different interest

rates"

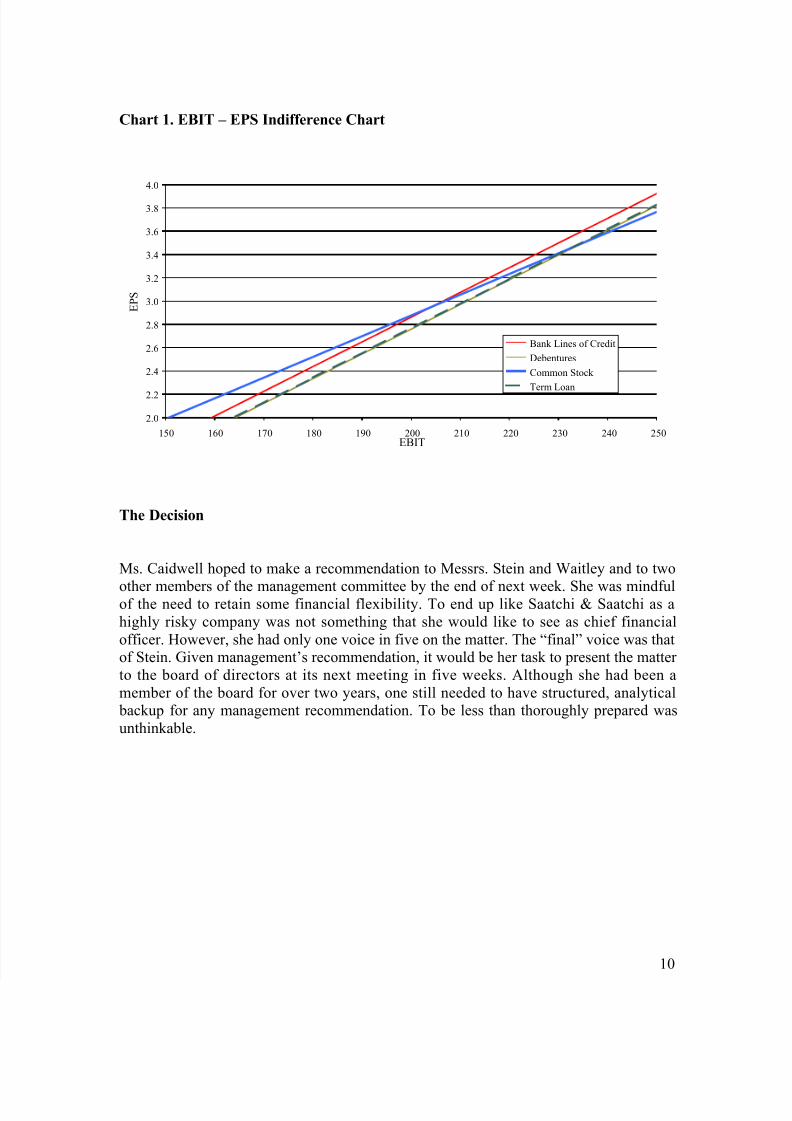

nder the current scenario (21! proected ?.#6) the best alternative is e$uity" 6he indifference point

between .an' >ines and ?$uity is 2!0+ " .elow that e$uity is better, above 2!0+ debt is better" .ecause long

term debt has higher costs, the indiference point between debt and e$uity in this case is higher, 2!/+ " 9nly if

?.#6 is higher than 2!/+ it would be better to be financed with long term debt" 6he two long term debt

alternatives (term loans and debentures) are very simmilar in terms of costs" ee additional analysis and graph"

8/14/2019 D & G case study.doc

http://slidepdf.com/reader/full/d-g-case-studydoc 8/10

#able :$ /riteria for +ecision!;akin-$ /ontinued=

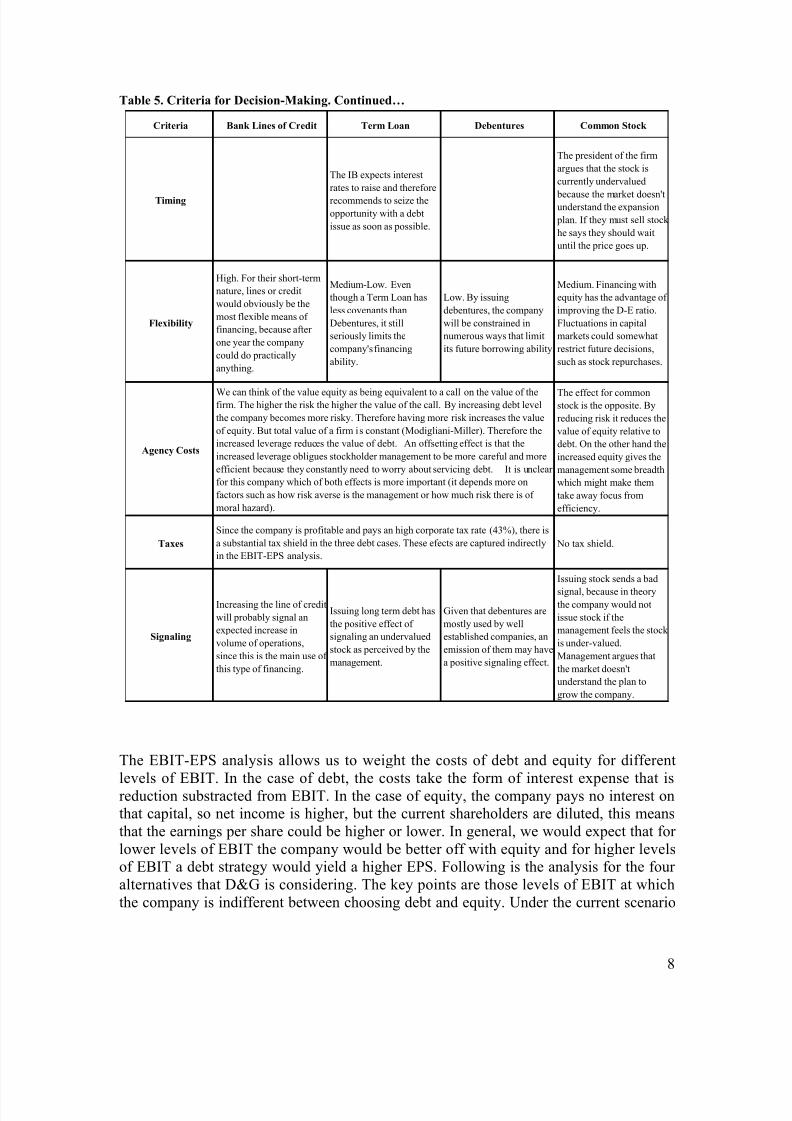

6he ?.#6=?< analysis allows us to weight the costs of debt and e$uity for different

levels of ?.#6" #n the case of debt, the costs ta'e the form of interest e4pense that isreduction substracted from ?.#6" #n the case of e$uity, the company pays no interest onthat capital, so net income is higher, but the current shareholders are diluted, this meansthat the earnings per share could be higher or lower" #n general, we would e4pect that forlower levels of ?.#6 the company would be better off with e$uity and for higher levelsof ?.#6 a debt strategy would yield a higher ?<" *ollowing is the analysis for the fouralternatives that D&G is considering" 6he 'ey points are those levels of ?.#6 at whichthe company is indifferent between choosing debt and e$uity" nder the current scenario

3

/riteria *ank 2ines of /redit #erm 2oan +ebentures /ommon Stock

#imin-

6he #. e4pects interest

rates to raise and therefore

recommends to seiBe the

opportunity with a debt

issue as soon as possible"

6he president of the firm

argues that the stoc' is

currently undervalued

because the mar'et doesnMtunderstand the e4pansion

plan" #f they must sell stoc'

he says they should wait

until the price goes up"

Fle,ibility

Cigh" *or their short=term

nature, lines or credit

would obviously be the

most fle4ible means of

financing, because after

one year the company

could do practically

anything"

edium=>ow" ?ven

though a 6erm >oan has

less covenants than

Debentures, it still

seriously limits the

companyMs financing

ability"

>ow" .y issuing

debentures, the company

will be constrained in

numerous ways that limit

its future borrowing ability"

edium" *inancing with

e$uity has the advantage of

improving the D=? ratio"

*luctuations in capital

mar'ets could somewhat

restrict future decisions,

such as stoc' repurchases"

A-ency /osts

6he effect for commonstoc' is the opposite" .y

reducing ris' it reduces the

value of e$uity relative to

debt" 9n the other hand the

increased e$uity gives the

management some breadth

which might ma'e them

ta'e away focus from

efficiency"

#a,es %o ta4 shield"

Si-nalin-

#ncreasing the line of credit

will probably signal an

e4pected increase in

volume of operations,

since this is the main use of

this type of financing"

#ssuing long term debt has

the positive effect of

signaling an undervalued

stoc' as perceived by the

management"

Given that debentures are

mostly used by well

established companies, an

emission of them may have

a positive signaling effect"

#ssuing stoc' sends a bad

signal, because in theorythe company would not

issue stoc' if the

management feels the stoc'

is under=valued"

anagement argues that

the mar'et doesnMt

understand the plan to

grow the company"

ince the company is profitable and pays an high corporate ta4 rate (5/-), there is

a substantial ta4 shield in the three debt cases" 6hese efects are captured indirectly

in the ?.#6=?< analysis"

e can thin' of the value e$uity as being e$uivalent to a call on the value of thefirm" 6he higher the ris' the higher the value of the call" .y increasing debt level

the company becomes more ris'y" 6herefore having more ris' increases the value

of e$uity" .ut total value of a firm is constant (odigliani=iller)" 6herefore the

increased leverage reduces the value of debt" An offsetting effect is that the

increased leverage obligues stoc'holder management to be more careful and more

efficient because they constantly need to worry about servicing debt" #t is unclear

for this company which of both effects is more important (it depends more on

factors such as how ris' averse is the management or how much ris' there is of

moral haBard)"

8/14/2019 D & G case study.doc

http://slidepdf.com/reader/full/d-g-case-studydoc 9/10

(21! proected ?.#6) the best alternative is e$uity" 6he indifference point between.an' >ines and ?$uity is 2!0+ " .elow 2!0+ e$uity is better, but above that point,debt is better" .ecause long=term debt has higher costs, the indifference point betweendebt and e$uity in this case is higher, 2!/+ " 9nly if ?.#6 is higher than 2!/+ it would be better to be financed with long term debt" 6he two long=term debt alternatives (term

loans and debentures) are very similar in terms of costs"

#able >$ <*4#!<0S Analysis

*ank 2ines

of /redit#erm 2oan +ebentures

/ommon

Stock

?.#6 !/+"+ !/+"+ !/+"+ !/+"+

#nterest on e4isting debt /3"1 /3"1 /3"1 /3"1

#nterest on new debt !7"0 /1"+ /1"3 =

?.6 170"5 1+" 1+"+ 17"5

6a4es 7/"/ 71"/ 71"! 35"

%et #ncome 7"1 5"+ 5"/ 11!"+

%umber of hares !" !" !" /!"1

?< /"1+ /"+!0 /"+1/ /"+03

#nterest ;ate - 10"+0- 10"!- %A

:ash %eed /00 /00 /00 /00

6a4 ;ate 5/-

8/14/2019 D & G case study.doc

http://slidepdf.com/reader/full/d-g-case-studydoc 10/10

/hart 1$ <*4# <0S 4ndifference /hart

#he +ecision

s" :aidwell hoped to ma'e a recommendation to essrs" tein and aitley and to two

other members of the management committee by the end of ne4t wee'" he was mindfulof the need to retain some financial fle4ibility" 6o end up li'e aatchi & aatchi as ahighly ris'y company was not something that she would li'e to see as chief financialofficer" Cowever, she had only one voice in five on the matter" 6he NfinalO voice was thatof tein" Given management8s recommendation, it would be her tas' to present the matterto the board of directors at its ne4t meeting in five wee's" Although she had been amember of the board for over two years, one still needed to have structured, analytical bac'up for any management recommendation" 6o be less than thoroughly prepared wasunthin'able"

10

?.#6=?<

!"0

!"!

!"5

!"

!"3

/"0

/"!

/"5

/"

/"3

5"0

1+0 10 170 130 10 !00 !10 !!0 !/0 !50 !+0?.#6

? < )

.an' >ines of :redit

Debentures

:ommon toc'

6erm >oan