Czech & Slovak Republics Philippe Moreels Member of the Board of Directors Prague April 19, 2004...

27

1 Czech & Slovak Republics Philippe Moreels Member of the Board of Directors Prague April 19, 2004 ČSOB Retail Banking ČSOB Retail Banking

-

Upload

myrtle-underwood -

Category

Documents

-

view

222 -

download

4

Transcript of Czech & Slovak Republics Philippe Moreels Member of the Board of Directors Prague April 19, 2004...

1

Czech & Slovak Republics

Philippe MoreelsMember of the Board of Directors

Prague

April 19, 2004

ČSOB Retail BankingČSOB Retail Banking

2

Czech Republic

Slovakia

ČSOB Retail Banking in CR

Highlights

Facts & Figures

Market Share

Bancassurance

Profit Contribution

2003 & 2004 Initiatives

4

2003 HIGHLIGHTSCzech Republic

ČSOB stabilized its number of retail clients at about 3 million

Volume of retail savings slightly decreased by 2% up to CZK 210 billion; Market share in total retail savings remained at 27% excluding deposits of building societies

Market share in mutual funds (assets under management) rapidly increased from 15% in 2002 up to nearly 20% at the end of 2003 while market share in standard bank deposit slightly went down

Volume of outstanding retail loans including mortgages exceeded CZK 25 billion as at the end of 2003; Market share in retail loans improved from 15% at the end of 2002 to 17% at the end of 2003

Market share in outstanding consumer loans reached 6.4% in 2003 which is still highly below ČSOB’s natural market share

5

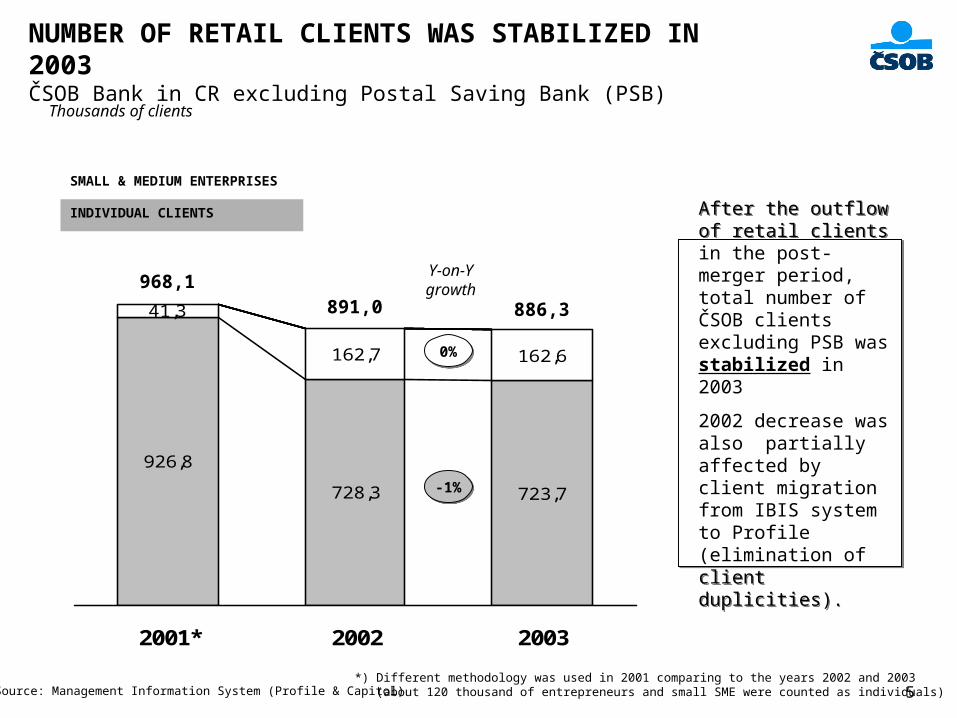

NUMBER OF RETAIL CLIENTS WAS STABILIZED IN 2003ČSOB Bank in CR excluding Postal Saving Bank (PSB)

Source: Management Information System (Profile & Capitol)

926,8

728,3 723,7

41,3

162,7 162,6

2001* 2002 2003

Thousands of clients

-1%-1%

0%0%

SMALL & MEDIUM ENTERPRISES

INDIVIDUAL CLIENTS

After the outflow of retail clients in the post-merger period, total number of ČSOB clients excluding PSB was stabilized in 2003

2002 decrease was also partially affected by client migration from IBIS system to Profile (elimination of client duplicities).

After the outflow of retail clients in the post-merger period, total number of ČSOB clients excluding PSB was stabilized in 2003

2002 decrease was also partially affected by client migration from IBIS system to Profile (elimination of client duplicities).

Y-on-Ygrowth968,1

891,0 886,3

*) Different methodology was used in 2001 comparing to the years 2002 and 2003 (about 120 thousand of entrepreneurs and small SME were counted as individuals)

6

ABOUT 70% OF ČSOB RETAIL CLIENTS ARE SERVED VIA POSTAL SAVING BANK

Source: Management Information System (Profile & Postagon)

2369,0

2105,8 2100,5

46,3 47,9

45,6

2001* 2002 2003

0%0%

4%4%

SMALL & MEDIUM ENTERPRISES

INDIVIDUAL CLIENTS

(pass book clients in percent) Total number of PSB clients remained stable comparing to the previous year.

Number of SME clients was growing on average by 3% from 2001 to 2003.

About 35 thousand PSB clients were transformed from pass book holders to current account (giro-accounts) holders.

Total number of PSB clients remained stable comparing to the previous year.

Number of SME clients was growing on average by 3% from 2001 to 2003.

About 35 thousand PSB clients were transformed from pass book holders to current account (giro-accounts) holders.

Y-on-Ygrowth

2414,6

2152,1 2148,4

-11%-11%

2%2%

*) In 2002 PSB abolished nearly 292.8 thousand saving books with low balances

Thousands of clients

(55%) (53%)

7

ČSOB RETAIL SAVINGS SLIGHTLY DECREASED IN 2003*

Source: ČSOB Regular Reports to CNB; ČSOB AM

45,358,7 68,1 77,9

140,0

149,2 133,0 110,1

4,5

7,0 13,422,2

2000 2001 2002 2003

CZK billion (CAS)

14%14%16%16%

30%30%

-17%-17%-11%-11%

7%7%

TERM DEPOSITS

CURRENT ACCOUNTS

Total savings of ČSOB retail clients (individuals) including PSB decreased by 2% in 2003.

Low interest rate environment encouraged ČSOB clients to invest in mutual funds that raised by 66% in 2003.

Total savings of ČSOB retail clients (individuals) including PSB decreased by 2% in 2003.

Low interest rate environment encouraged ČSOB clients to invest in mutual funds that raised by 66% in 2003.

Y-on-Ygrowth

189,8

214,9 214,5210,2

66%66%91%91%

MUTUAL FUNDS

*) Individuals only; PSB is fully included

55%55%

8

ČSOB MARKET SHARE IN TOTAL SAVINGS OF INDIVIDUALS REMAINED AT 27% IN 2003*

Percent (%)

Source: ČSOB Regular Reports to CNB; ČSOB AM; CNB Statistics*) deposits of building societies are excluded from the market figures; PSB is fully included

28,4%27,4%

29,4%28,3%

19,5%

10,2%

15,1%

12,4%

26,3% 27,1% 27,1%27,8%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

40,0%

2000 2001 2002 2003

Market share in total retail savings was 27.1% in 2003.

Market share in mutual funds went up to nearly 20% as a result of a successful “KEY PLAN” campaign in autumn 2003.

Market share in total retail savings was 27.1% in 2003.

Market share in mutual funds went up to nearly 20% as a result of a successful “KEY PLAN” campaign in autumn 2003.

TOTAL SAVINGS*

MUTUAL FUNDS

BANK DEPOSITS*

9

ČSOB BECAME THE BEST PROVIDER OF MUTUAL FUNDS (NET SALES) IN LATE 2003

Source: ČSOB Asset Management (UNIS, AKAT)

CZK million (CAS)

ČSOB attacked the position of Česká spořitelna in net sales of mutual funds in late 2003 due to successful “KEY PLAN” campaign.

ČSOB increased its market share in total mutual funds (assets under management) sold to individuals from 15% to nearly 20%, while competitors remained flat (ČS has 41% and KB about 16% market share in assets under management).

ČSOB attacked the position of Česká spořitelna in net sales of mutual funds in late 2003 due to successful “KEY PLAN” campaign.

ČSOB increased its market share in total mutual funds (assets under management) sold to individuals from 15% to nearly 20%, while competitors remained flat (ČS has 41% and KB about 16% market share in assets under management).

10

ČSOB OUTSTANDING LOANS PROVIDED TO INDIVIDUALS INCREASED BY 48% WHILE THE RETAIL MARKET GREW BY 33% IN 2003

Source: ČSOB & ČMHB Regular Reports to CNB

0,8 1,4 2,23,9

8,9

10,9

14,4

20,7

0,5

0,5

0,6

0,9

2000 2001 2002 2003

CZK billion (CAS)

82%82%

44%44%

MORTGAGES**

CONSUMER LOANS

ČSOB outperformed the 2003 market in consumer loans and other loans that grew by 82% (market:18%), 40% respectively (market: 1%).

Mortgages offered via ČSOB branches and ČMHB (mortgage bank fully owned by ČSOB) grew by 44% in 2003 which was behind the market development (54%).

ČSOB outperformed the 2003 market in consumer loans and other loans that grew by 82% (market:18%), 40% respectively (market: 1%).

Mortgages offered via ČSOB branches and ČMHB (mortgage bank fully owned by ČSOB) grew by 44% in 2003 which was behind the market development (54%).

Y-on-Ygrowth

10,3

12,8

17,2

25,5

40%40%

OTHER LOANS*

*) include overdrafts, FX loans, investment loans, and loans to non-residents**) mortgage loans provided by ČMHB are included

56%56%65%65%

33%33%

21%21%

21%21%

1%1%

11

ČSOB MARKET SHARE IN RETAIL OUSTANDING LOANS IMPROVED FROM 15.4% IN 2002 TO 17.2% IN 2003

Source: ČSOB Regular Reports to CNB; CNB Statistics

ČSOB market share in consumer loans went up by 2.2% in 2003.

ČSOB market share in mortgages continued to fall down up to 26.3% in 2003. CMHB (CSOB subsidiary) is gradually losing its dominant position on the market, as other banks started to provide mortgages. ČSOB also started to provide own-brand mortgages in 2004, so we expect total market share to increase again.

ČSOB market share in consumer loans went up by 2.2% in 2003.

ČSOB market share in mortgages continued to fall down up to 26.3% in 2003. CMHB (CSOB subsidiary) is gradually losing its dominant position on the market, as other banks started to provide mortgages. ČSOB also started to provide own-brand mortgages in 2004, so we expect total market share to increase again.

6,4%4,3%

4,2%

5,0%

26,3%

37,8%

28,2%

30,9%

17,2%15,4%16,5%16,0%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

40,0%

45,0%

50,0%

2000 2001 2002 2003

Percent (%)

TOTAL RETAIL LOANS*

MORTGAGES**

*) loans of building societies are excluded from the market figures**) mortgage loans provided by ČMHB are included

CONSUMER LOANS

12

7,0

40,5

18,6

20,5

16,6

9,0

12,1

32,5

1,0

Life insurance

Card travel insurance

Travel insurance

Consumer credits

Lost / Stolen cards

Written premium (CZK million, CAS)

*) Life 2002 for 7-12/2002**) Lost/Stolen card 2002 for 7-12/2002, 2003 for 1-9/2003

20032002

• Life insurance: main driver, 15k contracts in 2003, part of “Key plan” campaign In 2003, ČSOB generated more than 1/3 of new ČSOB P life business.

• Consumer credits: 30k insured credits in 2003, 94% cross-insurance ratio in 2003• Travel: 71k travel insurance contracts in 2003• Travel card: 56k travel card insurance contracts in 2003

• Life insurance: main driver, 15k contracts in 2003, part of “Key plan” campaign In 2003, ČSOB generated more than 1/3 of new ČSOB P life business.

• Consumer credits: 30k insured credits in 2003, 94% cross-insurance ratio in 2003• Travel: 71k travel insurance contracts in 2003• Travel card: 56k travel card insurance contracts in 2003

2003 Total:508

402

BANCASSURANCE: INSURANCE IN BANK BRANCHESDynamic growth from a low basis

13

NEARLY HALF OF 2003 ČSOB CONSOLIDATED PROFIT BEFORE TAX WAS GENERATED BY RETAIL DOMAIN

Consolidated (IAS)

2003 GROUP PROFIT BEFORE TAX

RETAIL DOMAIN

(48%)

OTHER BANK

DOMAINS*

22%

12%

14%

Retail/SME CR**

Source: ČSOB

*) Corporate Domain including OB Heller, Financial Markets Domain and Asset Management Domain **) ČSOB Bank including Private Bank is without PSB***) Rest includes Retail Bank SR, ČMSS (55% stake), ČMHB, ČSOB SP, ČSOB Leasing CR and SR

Postal Saving Bank

Rest of Retail Domain***

14

2003 RETAIL ACHIEVEMENTS Czech Republic

PRODUCTS &SALES SUPPORT

DISTRIBUTIONNETWORK

• Successful “Key plan” campaign in October and November 2003 significantly improved sales of saving products of the ČSOB Group

• ČSOB labelled mortgages offered in ČSOB branches since late 2003 (piloted)

• Launch of EMV chip cards

• New branch operational model and service model for SME/Affluent clients implemented

• SME pilot for sale of bancassurance products (joint teams of bank branches and insurance agents)

• ATM network expansion continued – number of ATMs increased from 272 to 403 ATMs in 2003

15

2004 RETAIL INITIATIVESCzech Republic

CLIENTS

PRODUCTS

• New image (new advertising and media agency)• Focus on new client acquisition

• ČSOB mortgage as a key product• Capital guaranteed mutual funds• Customer needs platforms - simplification of product lifecycle • New Internet Banking product for SME clients

• Cost control: staff reduction by 100 FTEs in 1H 2004• Further staffing review planned for 2H 2004.

SALES SUPPORT• Sales campaigns addressing customer need platforms,

continue with the “Key plan”

COSTS

• Bancassurance: co-operation of branches with insurance agents• Further enlargement of ATM network by 100 ATMs

DISTRIBUTION

16

BANCASSURANCE DISTRIBUTION: GOVERNANCE & BRANDINGCurrent focus is on co-operation between ČSOB Bank and ČSOB Insurance as the core of the future Group distribution in CR.

Distribution governance

• Moving into the direction of distribution governance project recommendations: a Bancassurance Steering Committee was established in Q4/2003 as a core component of the future governing committee of the Retail area

• The Retail committee should centrally decide on the product-to-channel allocation, branding, relative pricing and commission levels of the ČSOB brand(s).

Product factories

• Current focus: informal co-ordination of bilateral distribution agreements between Group companies

• Future model: product factories with clearly defined role of providing white-labelled, tailor-made products to the Group distribution channels or third parties. First examples: CSOB mortgages provided by CMHB, mutual funds from CSOB AM tailor-made for PSB.

17

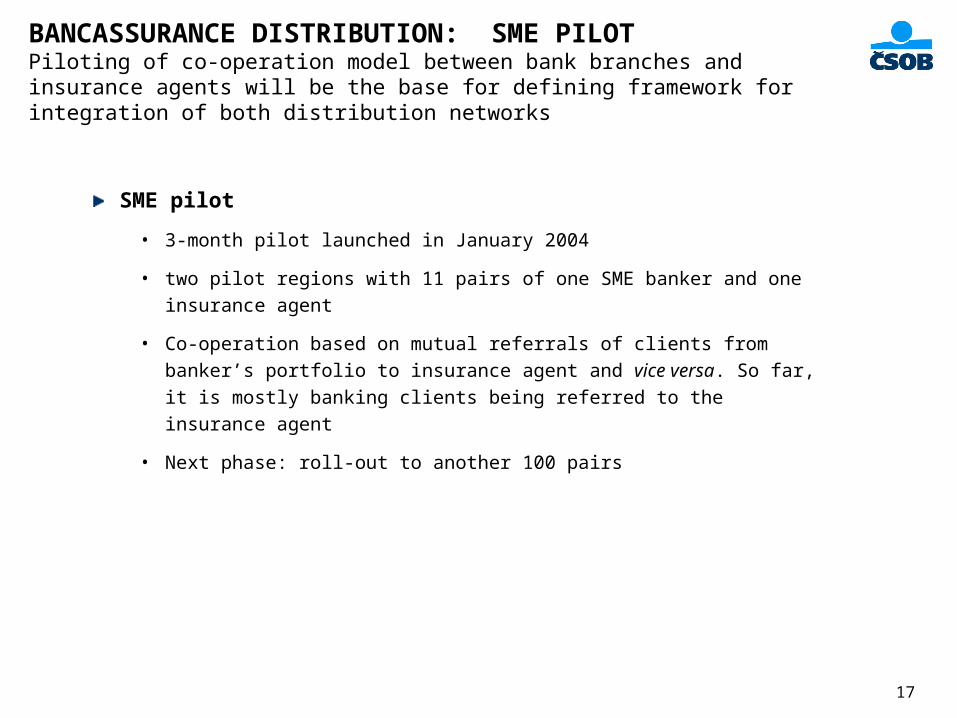

BANCASSURANCE DISTRIBUTION: SME PILOTPiloting of co-operation model between bank branches and insurance agents will be the base for defining framework for integration of both distribution networks

SME pilot

• 3-month pilot launched in January 2004

• two pilot regions with 11 pairs of one SME banker and one insurance agent

• Co-operation based on mutual referrals of clients from banker’s portfolio to

insurance agent and vice versa. So far, it is mostly banking clients being

referred to the insurance agent

• Next phase: roll-out to another 100 pairs

18

Czech Republic

Slovakia

ČSOB Retail Banking in Slovakia

Highlights

Facts & Figures

Market Share

2003 & 2004 Initiatives

20

2003 HIGHLIGHTSSlovak Republic

ČSOB increased its number of retail customers by 9% in 2003 due to continuing retail branch expansion in Slovakia; number of retail clients exceeded 180 thousand

Volume of retail savings grew by 4% up to SKK 19.5 billion; Market share in total retail savings was 5.2% as at the end of 2003

Market share in mutual funds increased up to 6.3% while market share in standard bank deposit remained stable

Volume of outstanding retail loans grew by 150% up to SKK 2.3 billion in 2003; Market share in retail loans reached 4.6% in 2003

ČSOB was one of the most important consumer loan providers in Slovakia; Its market share almost reached 15% in 2003

21

NUMBER OF RETAIL CLIENTS DOUBLED IN 2000-2003 ČSOB Bank in Slovakia

Source: ČSOB Management Information System (Profile)

79,9

115,2

152,3168,614,3

16,5

19,3

18,2

2000 2001 2002 2003

Thousands of clients

11%11%

32%32%

44%44%

-6%-6%

17%17%

16%16%

SMALL & MEDIUM ENTERPRISES

INDIVIDUAL CLIENTS

Total number of retail clients doubled in 2000-2003 as a result of ČSOB retail branch expansion in SR.

2003 growth was affected by client data migration from IBIS system to Profile when duplicities in client data have been cleaned.

Total number of retail clients doubled in 2000-2003 as a result of ČSOB retail branch expansion in SR.

2003 growth was affected by client data migration from IBIS system to Profile when duplicities in client data have been cleaned.

Y-on-Ygrowth

94,2

131,7

171,6

186,9

22

ČSOB RETAIL SAVINGS GREW AT A STABLE ANNUAL RATE OF 4% IN 2001-2003*

Source: ČSOB Regular Reports to NBS; ČSOB AM

3,14,5 5,3 5,9

9,7

13,112,6 11,2

0,0

0,30,8 2,4

2000 2001 2002 2003

SKK billion (SAS)

11%11%18%18%

45%45%

-11%-11%-4%-4%

35%35%

TERM DEPOSITS

CURRENT ACCOUNTS

Total savings of individuals managed by ČSOB SR steadily grew by 4% a year in the last two years.

Shift from bank term deposits, towards mutual funds was very significant in 2003 due to decreasing interest rates on the Slovak market.

Total savings of individuals managed by ČSOB SR steadily grew by 4% a year in the last two years.

Shift from bank term deposits, towards mutual funds was very significant in 2003 due to decreasing interest rates on the Slovak market.

Y-on-Ygrowth

12,8

17,9 18,7 19,5

200%200%167%167%

MUTUAL FUNDS

*) Individuals only, i.e. SME excluded

23

MARKET SHARE IN MUTUAL FUNDS WENT UP FROM 0% IN 2000 TO 6.3% IN 2003 WHILE MARKET SHARE IN BANK DEPOSITS OF INDIVIDUALS REMAINED STABLE

Percent (%)

Source: ČSOB Regular Reports to NBS; ČSOB AM *) deposits of building societies are excluded from the market figures

6,3%

5,1%

4,0%

5,0%5,0%

0,0%

4,8%4,7%

5,1%5,1%

4,0%

5,2%

0,0%

2,5%

5,0%

7,5%

10,0%

2000 2001 2002 2003

ČSOB market share in total savings of individuals managed by universal banks* improved from 4.0% in 2000 to 5.2% in 2003.

Share of mutual funds in total retail savings managed by ČSOB was 12.3% in 2003 while the same ratio was 10.2% for the whole market.

ČSOB market share in total savings of individuals managed by universal banks* improved from 4.0% in 2000 to 5.2% in 2003.

Share of mutual funds in total retail savings managed by ČSOB was 12.3% in 2003 while the same ratio was 10.2% for the whole market.

TOTAL SAVINGS*

MUTUAL FUNDS

BANK DEPOSITS*

24

ČSOB SIGNIFICANTLY INCREASED THE VOLUME OF LOANS PROVIDED TO INDIVIDUALS FROM A LOW BASIS

Source: ČSOB Regular Reports to NBS

0,0

0,30,6

1,3

0,0

0,0

0,1

0,7

0,1

0,1

0,2

0,3

2000 2001 2002 2003

SKK billion (SAS)

117%117%

425%425%

MORTGAGES

CONSUMER LOANS Total loans provided to individuals by ČSOB SR went up by more than 150% in 2003.

Although the growth of mortgages was high, the total volume is still behind original ČSOB’s expectations.

Total loans provided to individuals by ČSOB SR went up by more than 150% in 2003.

Although the growth of mortgages was high, the total volume is still behind original ČSOB’s expectations.

Y-on-Ygrowth

0,1

0,4

0,9

2,3

45%45%

OTHER LOANS*

*) include overdrafts, FX loans, investment loans, and loans to non-residents

25

ČSOB WITH NEARLY 15% MARKET SHARE IS ONE OF THE BIGGEST CONSUMER LOAN PROVIDERS IN SLOVAKIA

Source: ČSOB Regular Reports to NBS; NBS

ČSOB market share in outstanding total loans provided to individuals increased from 0.7% in 2000 to 4.6% in 2003.

Although market share in mortgages went up from 0% in 2000 to 2.6% in 2003, it is still behind desirable level.

ČSOB market share in outstanding total loans provided to individuals increased from 0.7% in 2000 to 4.6% in 2003.

Although market share in mortgages went up from 0% in 2000 to 2.6% in 2003, it is still behind desirable level.

14,9%

0,0%

9,2%

6,0%

2,6%0,9%

0,0%0,7%

2,1%

4,6%

3,2%

0,0%

5,0%

10,0%

15,0%

20,0%

2000 2001 2002 2003

Percent (%)

TOTAL RETAIL LOANS*

MORTGAGES

CONSUMER LOANS

*) loans of building societies are excluded from the market figures

26

2003 RETAIL ACHIEVEMENTS Slovak Republic

• Successful “Housing & Mobility“ campaign focused on financial needs of retail clients (mortgage, consumer loans, non-life insurance, and referrals to building loans)

• Credit card launched in late 2003

• Launch of EMV chip cards

• Retail branch expansion continued; Number of retail branches increased from 47 to 70 in 2003

• ČSOB migrated all retail and SME customers from old to new IT system (Profile)

PRODUCTS &SALES SUPPORT

DISTRIBUTIONNETWORK

27

2004 RETAIL INITIATIVESSlovak Republic

CLIENTS

PRODUCTS

• Enhance image of a retail bank• Continuing focus on new client acquisition

• ČSOB mortgage as a key product• Capital guaranteed mutual funds• Optimising the product portfolio

• Enhanced co-operation with segment management and methodological units in Headquarters Prague (cost synergies)

SALES SUPPORT• Key plan focused on investment products for individuals • Improved co-operation within the Group (United Family)

COSTS

• Retail branch expansion – 80 branches by the end of 2004• ATM expansion by new 25 off-site ATMs • Replacement of old 27 ATMs in branches (new functionalities)

DISTRIBUTION