Cyprus Tax Update · 2018-07-12 · Email: [email protected]. EY I Assurance I Tax I...

29

Cyprus Tax Update Kyiv May 2018

Transcript of Cyprus Tax Update · 2018-07-12 · Email: [email protected]. EY I Assurance I Tax I...

Cyprus Tax Update

Kyiv

May 2018

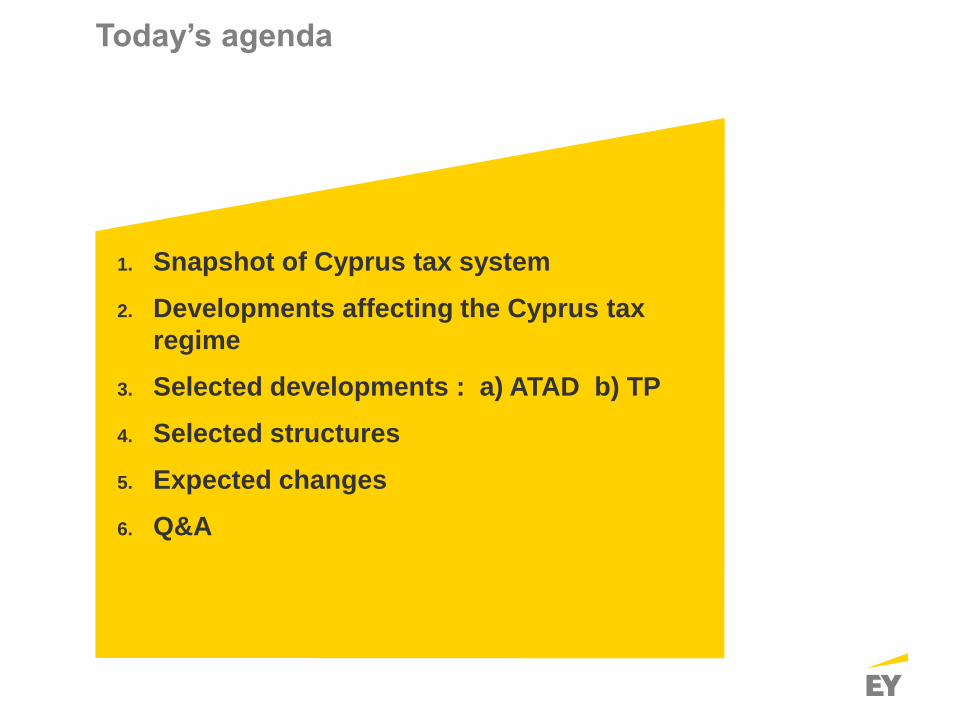

Today’s agenda

1. Snapshot of Cyprus tax system

2. Developments affecting the Cyprus tax

regime

3. Selected developments : a) ATAD b) TP

4. Selected structures

5. Expected changes

6. Q&A

Page 3

Snapshot of Cyprus tax regime

Page 4

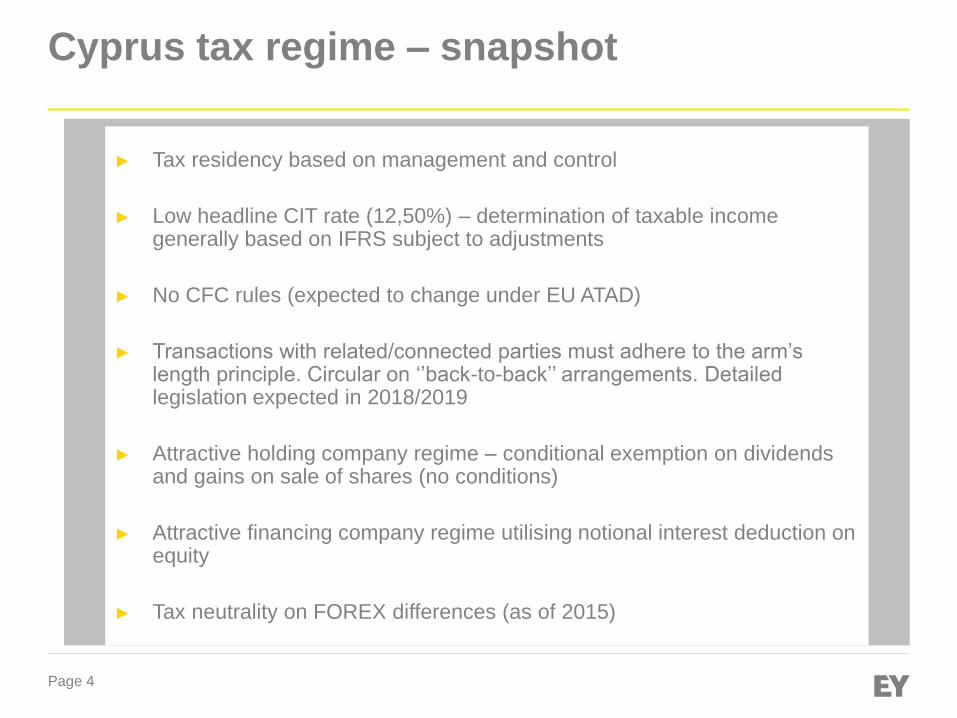

Cyprus tax regime – snapshot

► Tax residency based on management and control

► Low headline CIT rate (12,50%) – determination of taxable income generally based on IFRS subject to adjustments

► No CFC rules (expected to change under EU ATAD)

► Transactions with related/connected parties must adhere to the arm’s length principle. Circular on ‘’back-to-back’’ arrangements. Detailed legislation expected in 2018/2019

► Attractive holding company regime – conditional exemption on dividends and gains on sale of shares (no conditions)

► Attractive financing company regime utilising notional interest deduction on equity

► Tax neutrality on FOREX differences (as of 2015)

Page 5

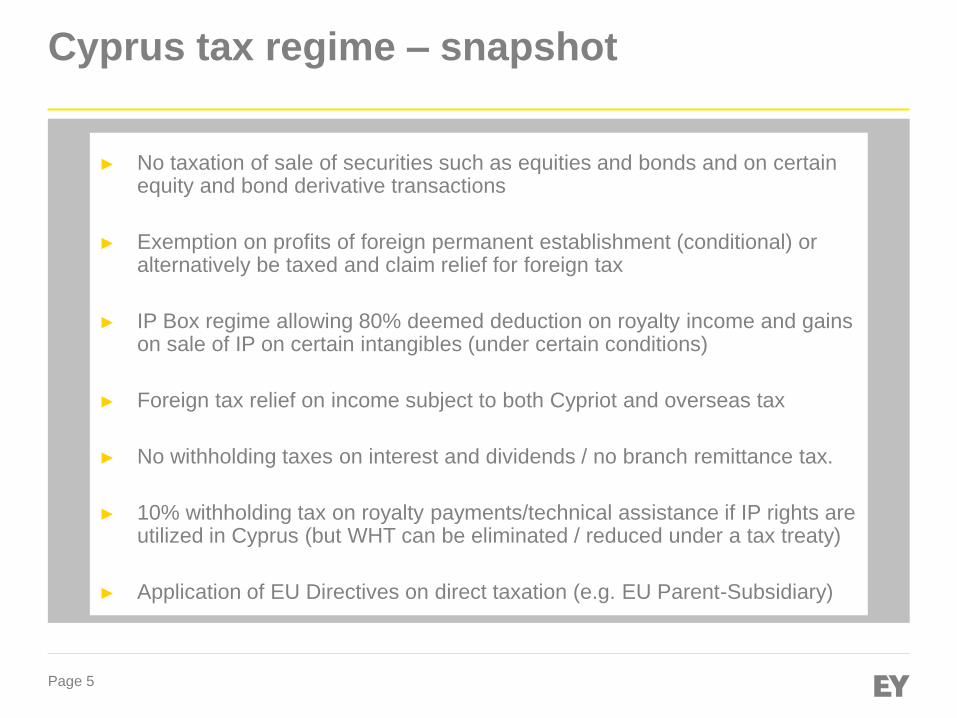

Cyprus tax regime – snapshot

► No taxation of sale of securities such as equities and bonds and on certain equity and bond derivative transactions

► Exemption on profits of foreign permanent establishment (conditional) or alternatively be taxed and claim relief for foreign tax

► IP Box regime allowing 80% deemed deduction on royalty income and gains on sale of IP on certain intangibles (under certain conditions)

► Foreign tax relief on income subject to both Cypriot and overseas tax

► No withholding taxes on interest and dividends / no branch remittance tax.

► 10% withholding tax on royalty payments/technical assistance if IP rights are utilized in Cyprus (but WHT can be eliminated / reduced under a tax treaty)

► Application of EU Directives on direct taxation (e.g. EU Parent-Subsidiary)

Page 6

Cyprus tax regime – snapshot

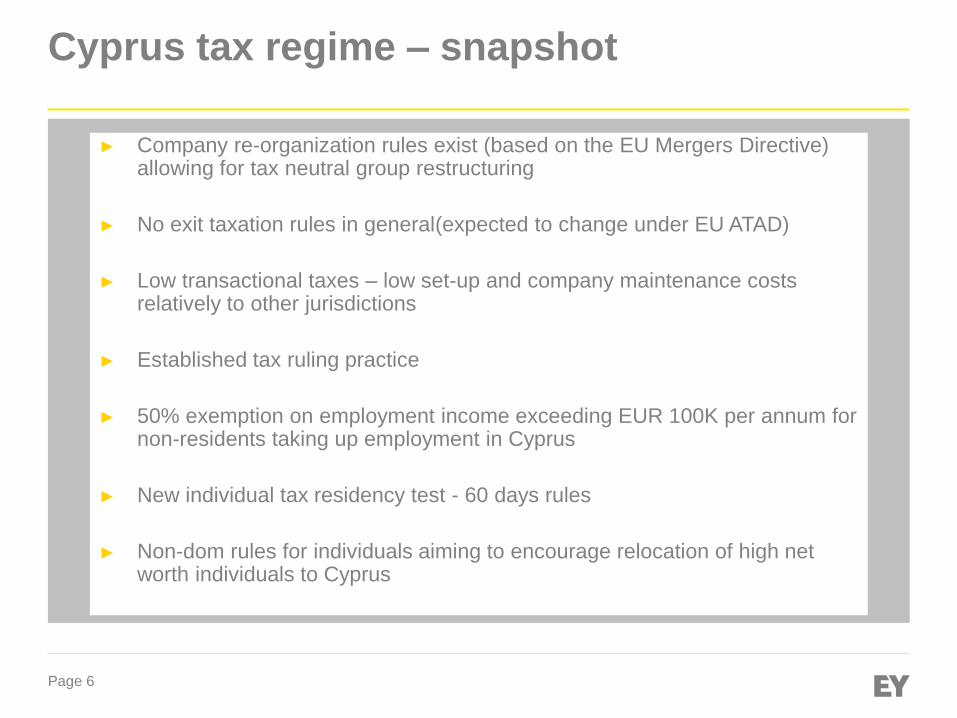

► Company re-organization rules exist (based on the EU Mergers Directive) allowing for tax neutral group restructuring

► No exit taxation rules in general(expected to change under EU ATAD)

► Low transactional taxes – low set-up and company maintenance costs relatively to other jurisdictions

► Established tax ruling practice

► 50% exemption on employment income exceeding EUR 100K per annum for non-residents taking up employment in Cyprus

► New individual tax residency test - 60 days rules

► Non-dom rules for individuals aiming to encourage relocation of high net worth individuals to Cyprus

Page 7

Developments affecting the Cyprus tax regime

Page 8

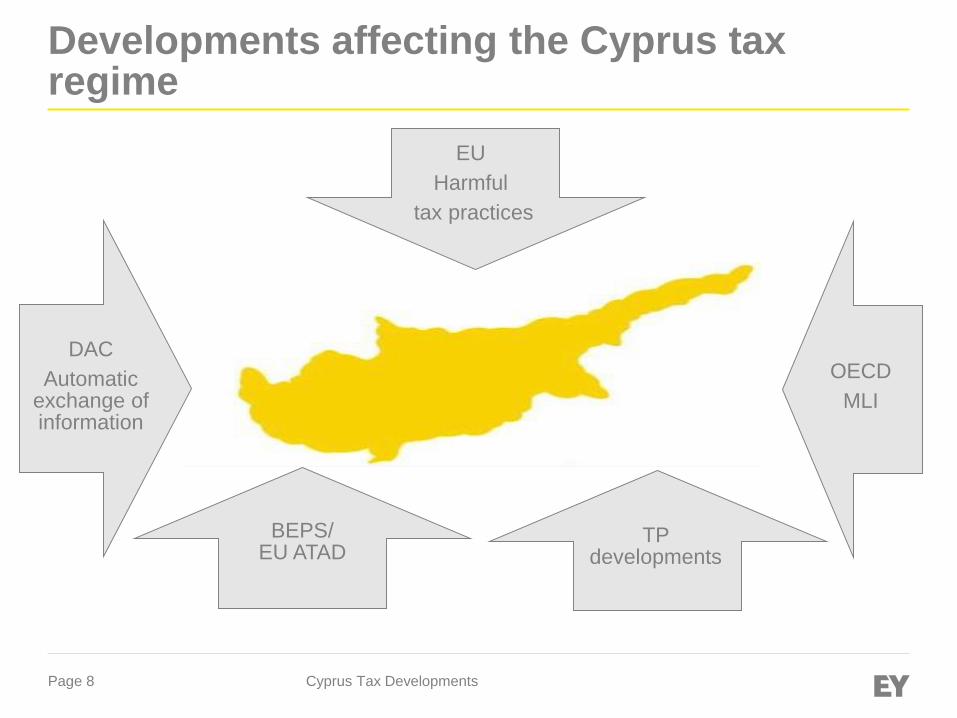

Developments affecting the Cyprus tax regime

OECD

MLI

Cyprus Tax Developments

DAC

Automatic exchange of information

EU

Harmful

tax practices

BEPS/ EU ATAD

TP developments

Page 9 Cyprus Tax Developments

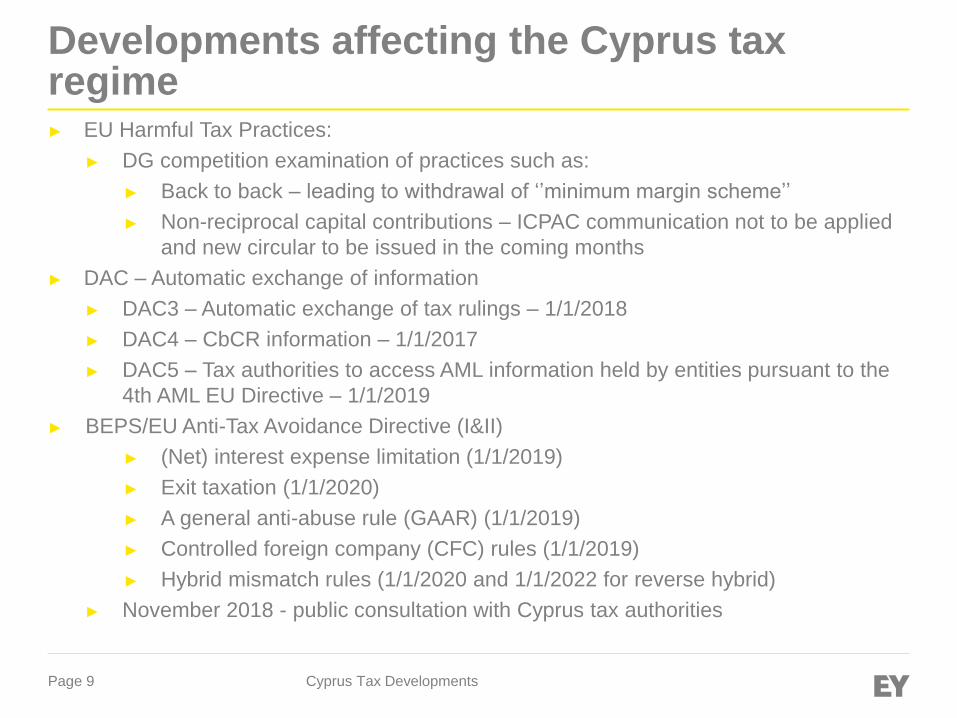

► EU Harmful Tax Practices:

► DG competition examination of practices such as:

► Back to back – leading to withdrawal of ‘’minimum margin scheme’’

► Non-reciprocal capital contributions – ICPAC communication not to be applied

and new circular to be issued in the coming months

► DAC – Automatic exchange of information

► DAC3 – Automatic exchange of tax rulings – 1/1/2018

► DAC4 – CbCR information – 1/1/2017

► DAC5 – Tax authorities to access AML information held by entities pursuant to the

4th AML EU Directive – 1/1/2019

► BEPS/EU Anti-Tax Avoidance Directive (I&II)

► (Net) interest expense limitation (1/1/2019)

► Exit taxation (1/1/2020)

► A general anti-abuse rule (GAAR) (1/1/2019)

► Controlled foreign company (CFC) rules (1/1/2019)

► Hybrid mismatch rules (1/1/2020 and 1/1/2022 for reverse hybrid)

► November 2018 - public consultation with Cyprus tax authorities

Developments affecting the Cyprus tax regime

Page 10 Cyprus Tax Developments

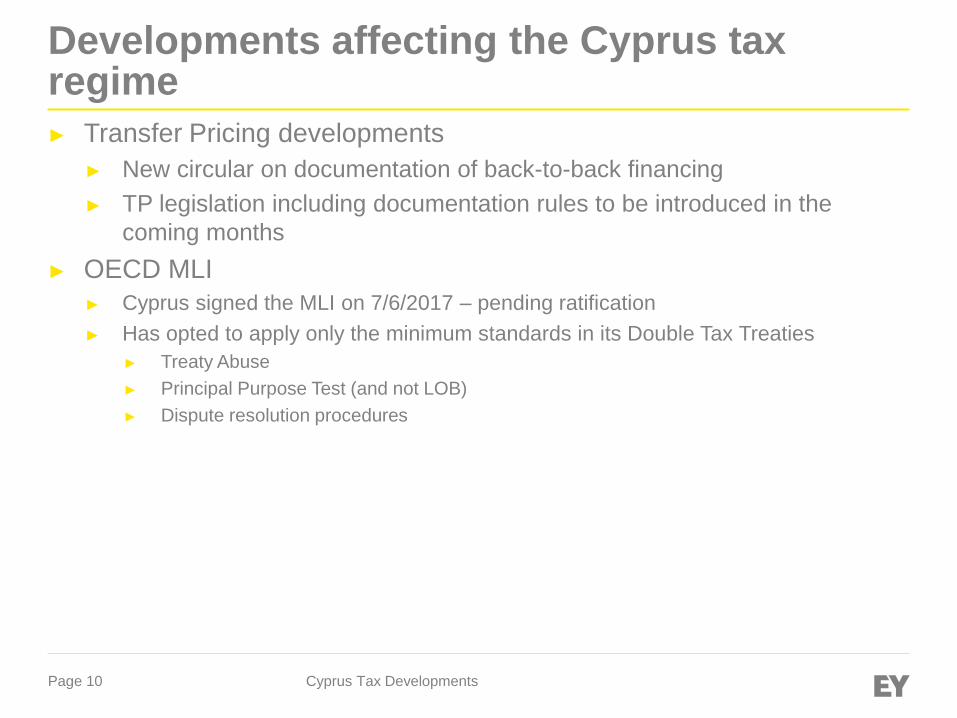

► Transfer Pricing developments

► New circular on documentation of back-to-back financing

► TP legislation including documentation rules to be introduced in the

coming months

► OECD MLI

► Cyprus signed the MLI on 7/6/2017 – pending ratification

► Has opted to apply only the minimum standards in its Double Tax Treaties

► Treaty Abuse

► Principal Purpose Test (and not LOB)

► Dispute resolution procedures

Developments affecting the Cyprus tax regime

Page 11

Selected matters – EU ATAD

Page 12

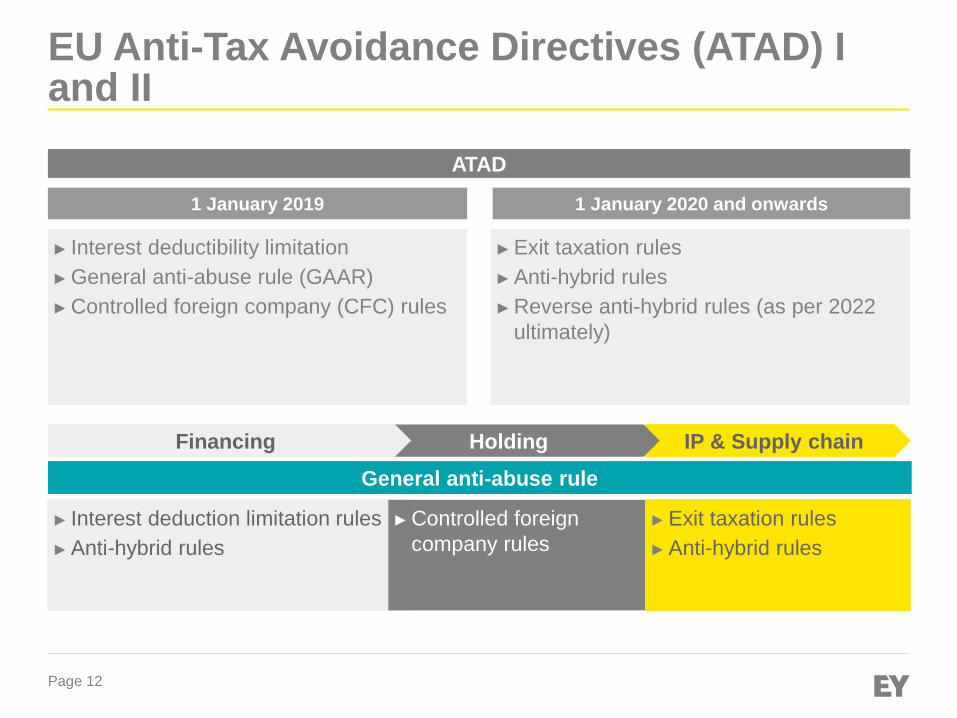

EU Anti-Tax Avoidance Directives (ATAD) I and II

► Exit taxation rules

► Anti-hybrid rules

► Reverse anti-hybrid rules (as per 2022

ultimately)

► Interest deductibility limitation

► General anti-abuse rule (GAAR)

► Controlled foreign company (CFC) rules

1 January 2019 1 January 2020 and onwards

IP & Supply chain

► Interest deduction limitation rules

► Anti-hybrid rules

► Controlled foreign

company rules

► Exit taxation rules

► Anti-hybrid rules

Holding

General anti-abuse rule

Financing

ATAD

Page 13

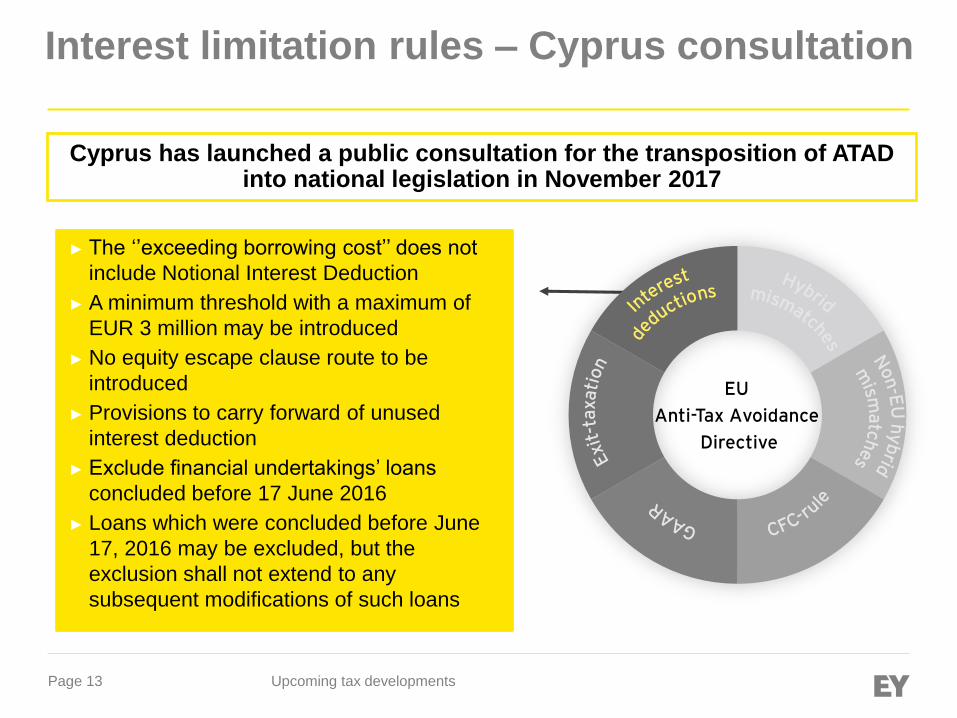

Interest limitation rules – Cyprus consultation

Upcoming tax developments

► The ‘’exceeding borrowing cost’’ does not

include Notional Interest Deduction

► A minimum threshold with a maximum of

EUR 3 million may be introduced

► No equity escape clause route to be

introduced

► Provisions to carry forward of unused

interest deduction

► Exclude financial undertakings’ loans

concluded before 17 June 2016

► Loans which were concluded before June

17, 2016 may be excluded, but the

exclusion shall not extend to any

subsequent modifications of such loans

Cyprus has launched a public consultation for the transposition of ATAD into national legislation in November 2017

EU

Anti-Tax Avoidance

Directive

Page 14

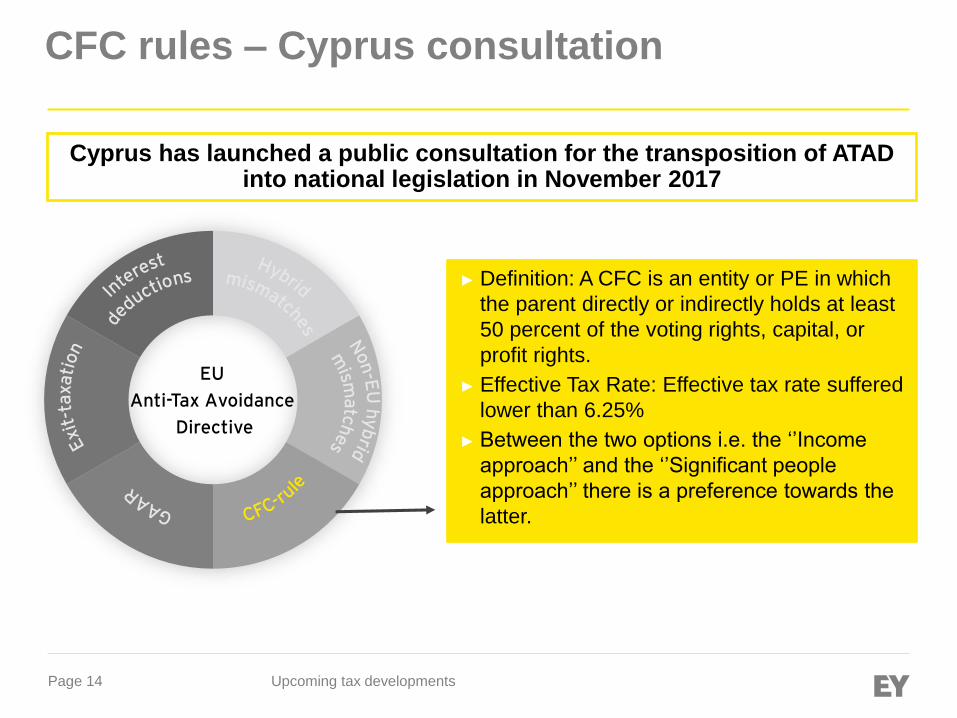

CFC rules – Cyprus consultation

Upcoming tax developments

Cyprus has launched a public consultation for the transposition of ATAD into national legislation in November 2017

EU

Anti-Tax Avoidance

Directive

► Definition: A CFC is an entity or PE in which

the parent directly or indirectly holds at least

50 percent of the voting rights, capital, or

profit rights.

► Effective Tax Rate: Effective tax rate suffered

lower than 6.25%

► Between the two options i.e. the ‘’Income

approach’’ and the ‘’Significant people

approach’’ there is a preference towards the

latter.

Page 15

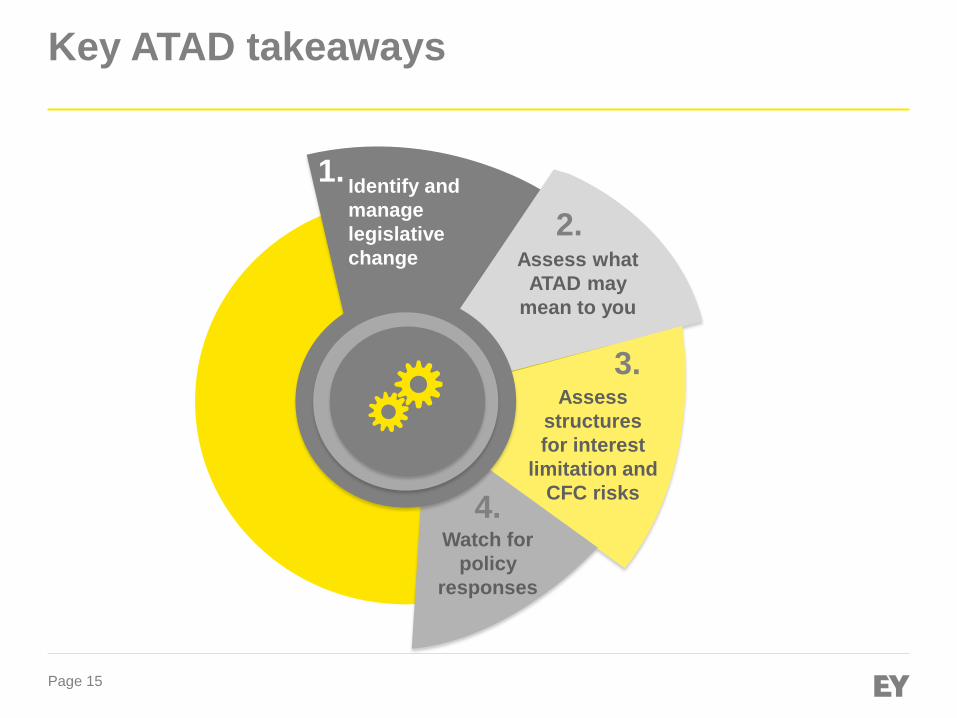

Key ATAD takeaways

Identify and

manage

legislative

change

1.

Assess what

ATAD may

mean to you

2.

Assess

structures

for interest

limitation and

CFC risks

3.

Watch for

policy

responses

4.

Page 16

Selected matters – Transfer Pricing

Page 17

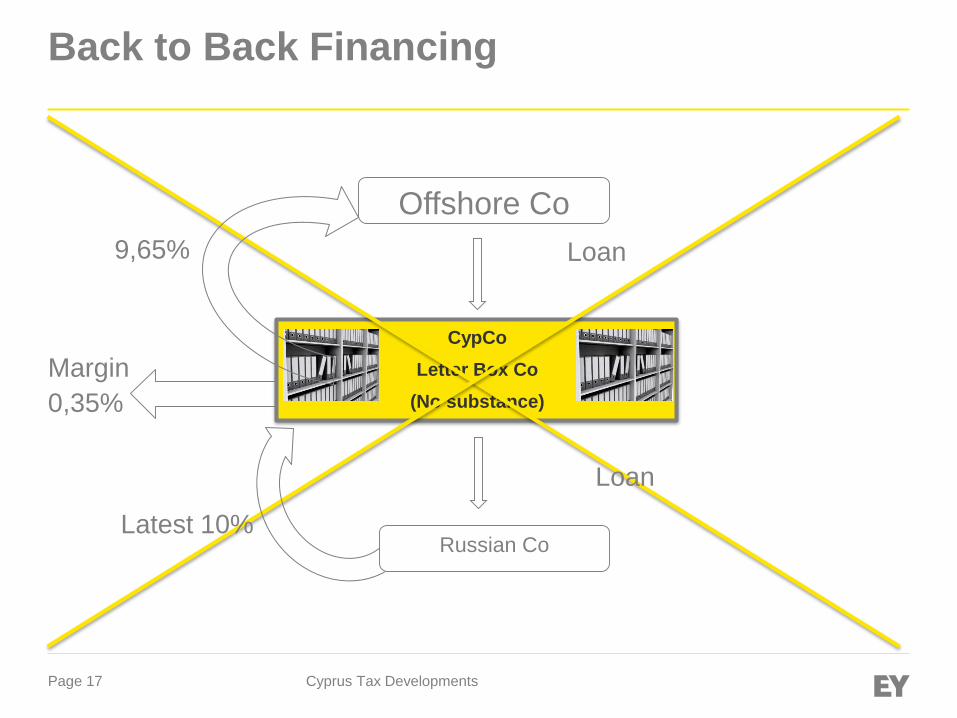

Back to Back Financing

CypCo

Letter Box Co

(No substance)

Offshore Co

9,65%

Latest 10%

Loan

Loan

Cyprus Tax Developments

Margin

0,35%

Russian Co

Page 18

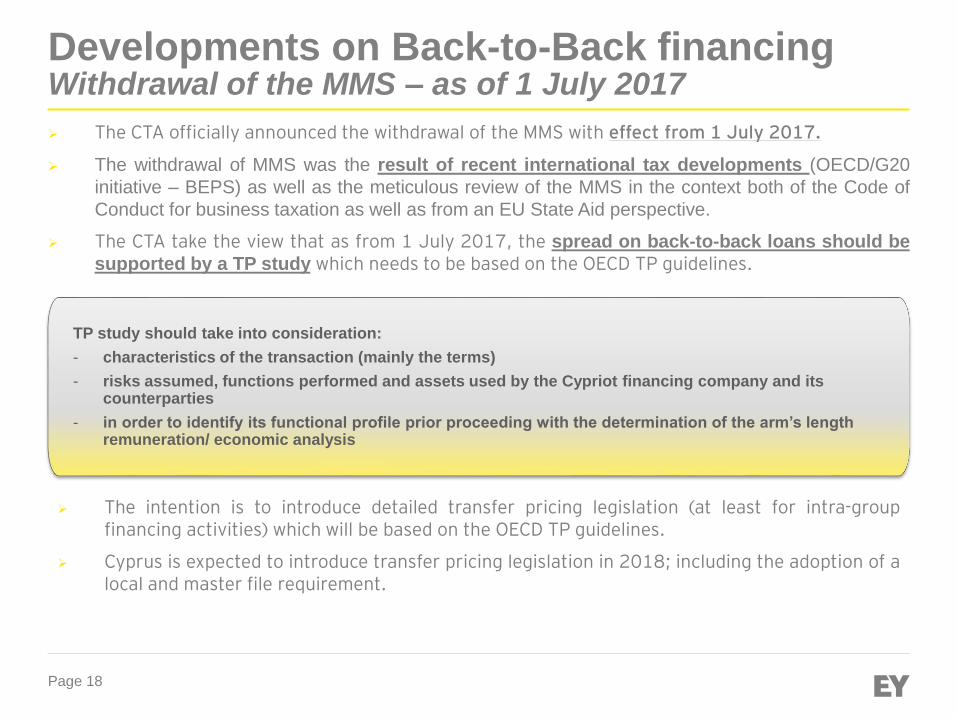

Developments on Back-to-Back financingWithdrawal of the MMS – as of 1 July 2017

The CTA officially announced the withdrawal of the MMS with effect from 1 July 2017.

The withdrawal of MMS was the result of recent international tax developments (OECD/G20

initiative – BEPS) as well as the meticulous review of the MMS in the context both of the Code of

Conduct for business taxation as well as from an EU State Aid perspective.

The CTA take the view that as from 1 July 2017, the spread on back-to-back loans should be

supported by a TP study which needs to be based on the OECD TP guidelines.

TP study should take into consideration:

- characteristics of the transaction (mainly the terms)

- risks assumed, functions performed and assets used by the Cypriot financing company and its counterparties

- in order to identify its functional profile prior proceeding with the determination of the arm’s length remuneration/ economic analysis

The intention is to introduce detailed transfer pricing legislation (at least for intra-groupfinancing activities) which will be based on the OECD TP guidelines.

Cyprus is expected to introduce transfer pricing legislation in 2018; including the adoption of alocal and master file requirement.

Page 19

Selected matters – New IP Box Structures

Page 20

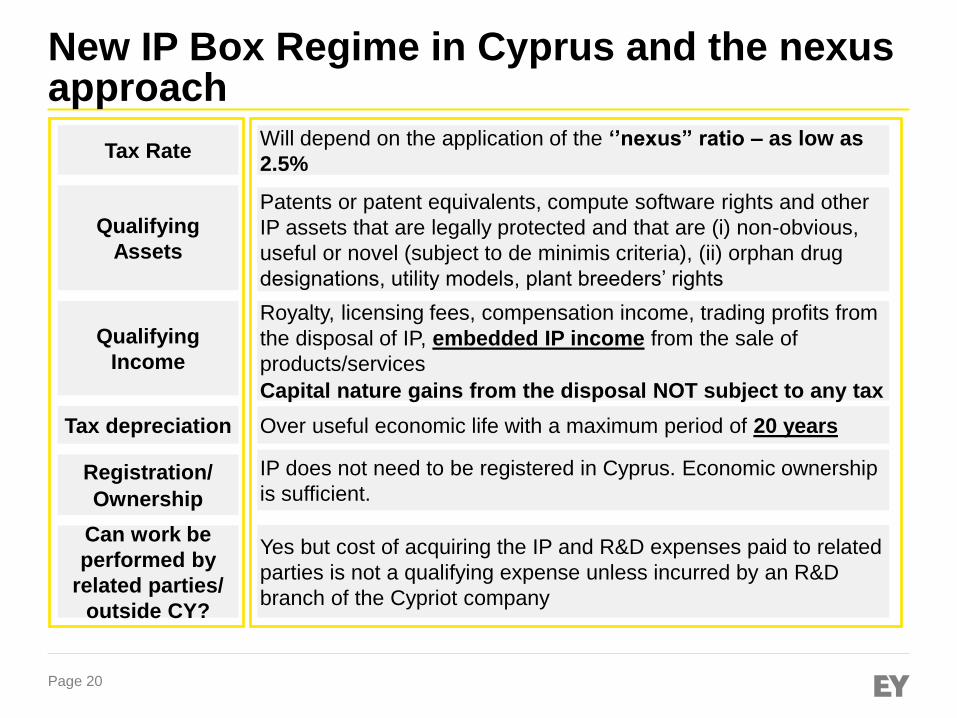

New IP Box Regime in Cyprus and the nexus approach

Qualifying

Assets

Registration/

Ownership

Qualifying

Income

Can work be

performed by

related parties/

outside CY?

Patents or patent equivalents, compute software rights and other

IP assets that are legally protected and that are (i) non-obvious,

useful or novel (subject to de minimis criteria), (ii) orphan drug

designations, utility models, plant breeders’ rights

IP does not need to be registered in Cyprus. Economic ownership

is sufficient.

Royalty, licensing fees, compensation income, trading profits from

the disposal of IP, embedded IP income from the sale of

products/services

Capital nature gains from the disposal NOT subject to any tax

Yes but cost of acquiring the IP and R&D expenses paid to related

parties is not a qualifying expense unless incurred by an R&D

branch of the Cypriot company

Tax RateWill depend on the application of the ‘’nexus” ratio – as low as

2.5%

Tax depreciation Over useful economic life with a maximum period of 20 years

Page 21

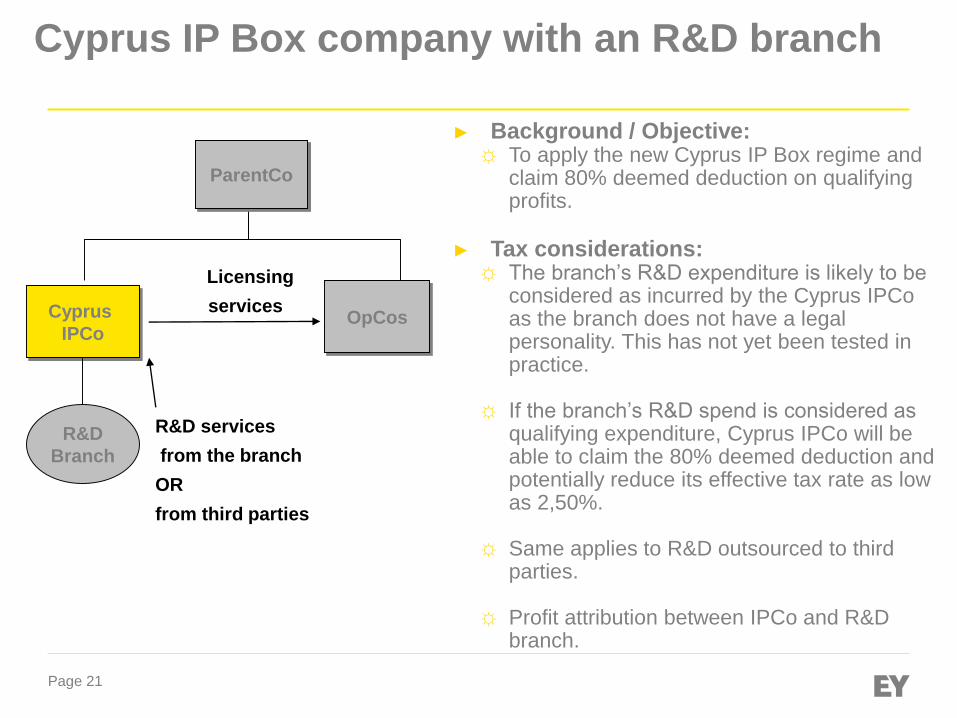

Cyprus IP Box company with an R&D branch

► Background / Objective:☼ To apply the new Cyprus IP Box regime and

claim 80% deemed deduction on qualifying profits.

► Tax considerations:☼ The branch’s R&D expenditure is likely to be

considered as incurred by the Cyprus IPCo as the branch does not have a legal personality. This has not yet been tested in practice.

☼ If the branch’s R&D spend is considered as qualifying expenditure, Cyprus IPCo will be able to claim the 80% deemed deduction and potentially reduce its effective tax rate as low as 2,50%.

☼ Same applies to R&D outsourced to third parties.

☼ Profit attribution between IPCo and R&D branch.

Cyprus

IPCoOpCos

R&D

Branch

R&D services

from the branch

OR

from third parties

Licensing

services

ParentCo

Page 22

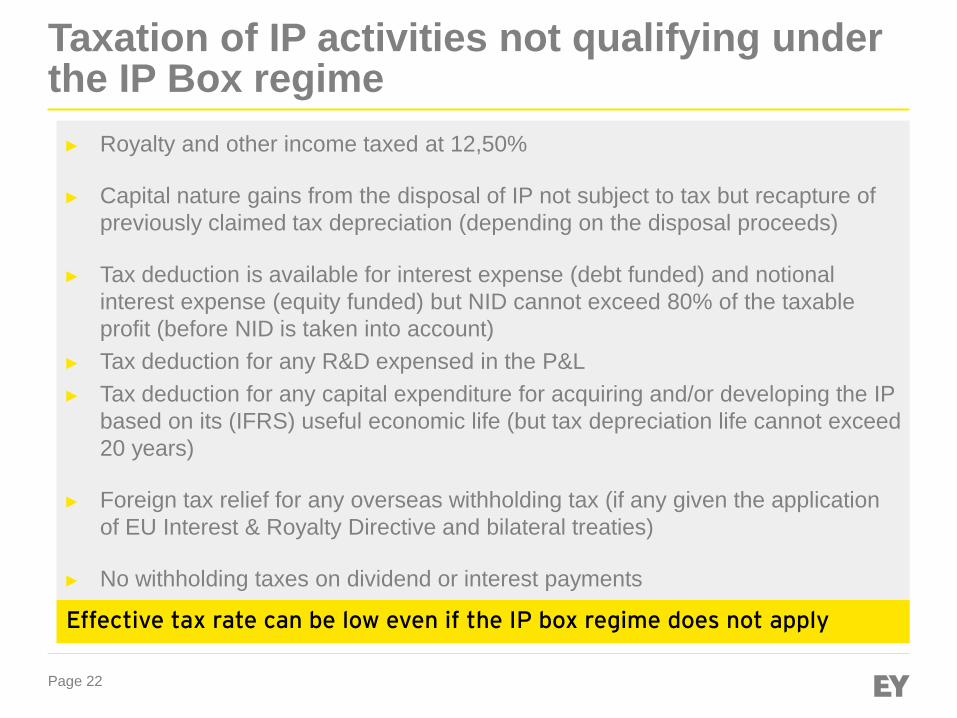

Taxation of IP activities not qualifying under the IP Box regime

► Royalty and other income taxed at 12,50%

► Capital nature gains from the disposal of IP not subject to tax but recapture of

previously claimed tax depreciation (depending on the disposal proceeds)

► Tax deduction is available for interest expense (debt funded) and notional

interest expense (equity funded) but NID cannot exceed 80% of the taxable

profit (before NID is taken into account)

► Tax deduction for any R&D expensed in the P&L

► Tax deduction for any capital expenditure for acquiring and/or developing the IP

based on its (IFRS) useful economic life (but tax depreciation life cannot exceed

20 years)

► Foreign tax relief for any overseas withholding tax (if any given the application

of EU Interest & Royalty Directive and bilateral treaties)

► No withholding taxes on dividend or interest payments

Effective tax rate can be low even if the IP box regime does not apply

Page 23

Selected matters – Investment into foreign (RE) funds

Page 24

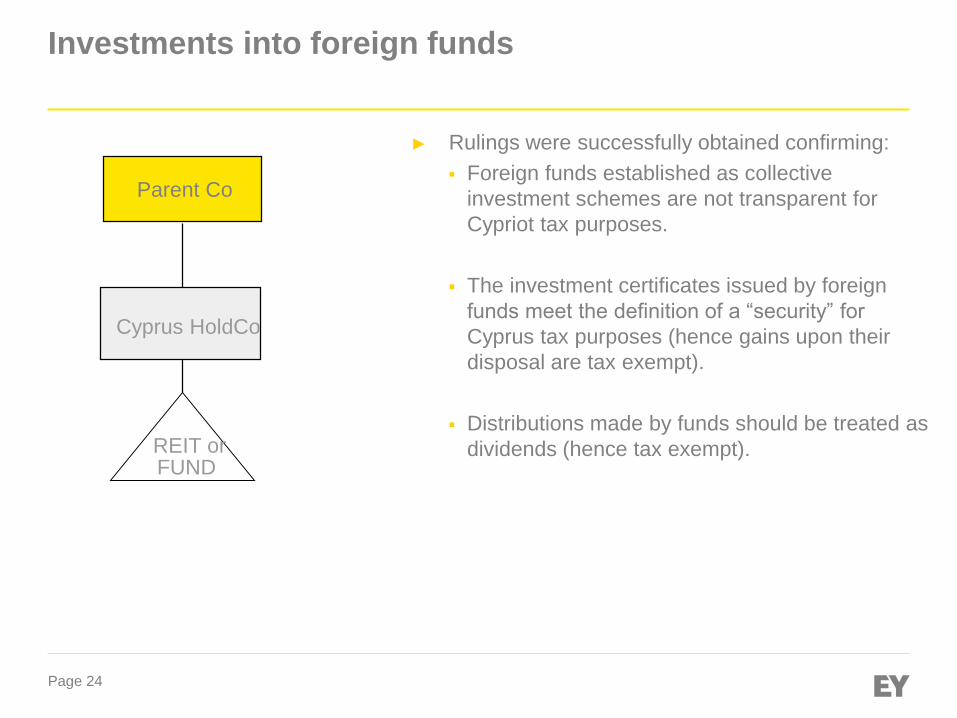

Investments into foreign funds

► Rulings were successfully obtained confirming:

Foreign funds established as collective

investment schemes are not transparent for

Cypriot tax purposes.

The investment certificates issued by foreign

funds meet the definition of a “security” for

Cyprus tax purposes (hence gains upon their

disposal are tax exempt).

Distributions made by funds should be treated as

dividends (hence tax exempt).

Parent Co

Cyprus HoldCo

REIT or FUND

Page 25

Expected changes

Page 26

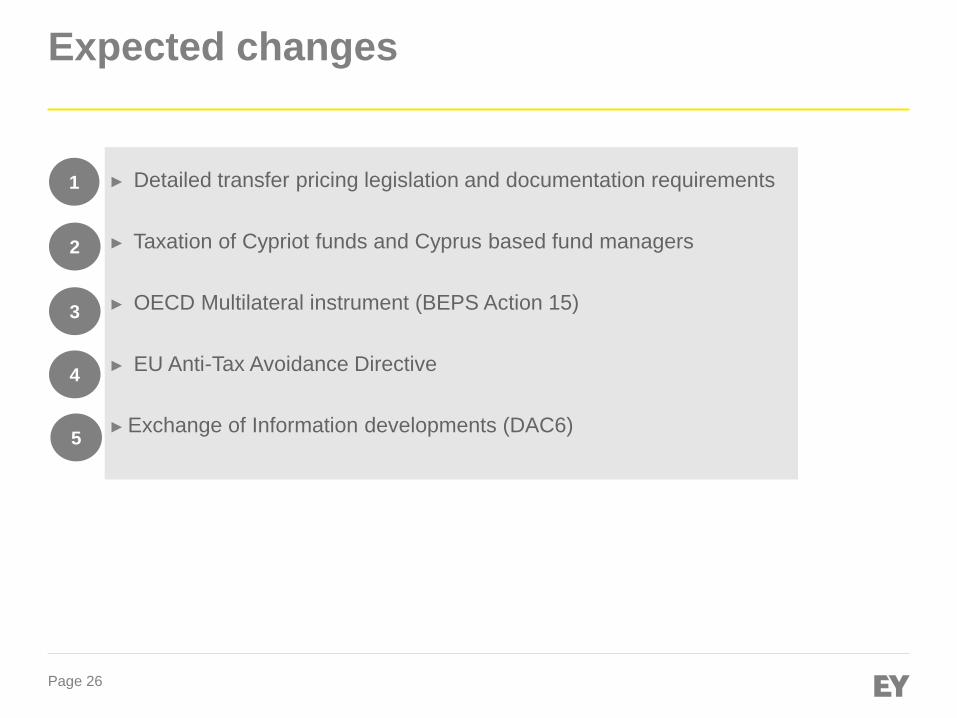

Expected changes

► Detailed transfer pricing legislation and documentation requirements

► Taxation of Cypriot funds and Cyprus based fund managers

► OECD Multilateral instrument (BEPS Action 15)

► EU Anti-Tax Avoidance Directive

► Exchange of Information developments (DAC6)

1

2

3

4

5

Page 27

Questions and Answers

Page 28

Contacts

Philippos RaptopoulosPartner, Head of Tax CyprusTel.: +357 25209740Mob.: +357 96795016Fax: +357 25209998Email: [email protected]

EY I Assurance I Tax I Transactions I Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com

© 2018 All Rights Reserved