CVG Chapter APICS April 20, 2010 vf

68

Kingsgate Marriott at the University of Cincinnati April 20, 2010 Present Supply Chain Management in Turbulent Times Freese & Associates, Inc. and The Cincinnati Chapter of

Transcript of CVG Chapter APICS April 20, 2010 vf

20 April 2010Supply Chain Management in

Turbulent Times

Page 1

Freese & Associates, Inc.

Kingsgate Marriott at the University of CincinnatiApril 20, 2010

Present

Supply Chain Management in Turbulent Times

Freese & Associates, Inc.

and

The Cincinnati Chapter of

20 April 2010Supply Chain Management in

Turbulent Times

Page 2

Freese & Associates, Inc.

Agenda• Supply Chain Management

o Historyo Definitiono Evolution

• The State of Logistics

• Turbulent Timeso The Perfect Storm o Economic & Markets

• SCM Trends

• Economic Direction& Impacts

• Financial Impactsof SCM

• Keys to the Future

• Q & A

20 April 2010Supply Chain Management in

Turbulent Times

Page 3

Freese & Associates, Inc.

Presents

Content Overview, Objectives & Definitions

Supply Chain Management

20 April 2010Supply Chain Management in

Turbulent Times

Page 4

Freese & Associates, Inc.

Supply Chain History

Stonehenge5,000 years ago

Roman Empire2,000 years ago

20 April 2010Supply Chain Management in

Turbulent Times

Page 5

Freese & Associates, Inc.

What is Supply Chain Management?

20 April 2010Supply Chain Management in

Turbulent Times

Page 6

Freese & Associates, Inc.

“Is the integration of business processesfrom original suppliers through end-users

that provides products, services and information that add value for customers”

Supply Chain Management

20 April 2010Supply Chain Management in

Turbulent Times

Page 7

Freese & Associates, Inc.

Suppliers’ SupplierTo

Customers’ Customer

20 April 2010Supply Chain Management in

Turbulent Times

Page 8

Freese & Associates, Inc.

“Supply Chain Management” is More Than Just “Logistics” !

“Demand Management” “Focal Firm” “Supply Management”

CustomerRelationshipManagement

Demand Planning

Operations/Manufacturing

(Product/Service)StrategyOutbound

Logistics

Procurement

InboundLogistics

SalesOrder Mgt.

Process Design and Management

Project Management

Supply Chain Integration

SupplierRelationshipManagement

Post-SalesSupport

Financial Resource Management

20 April 2010Supply Chain Management in

Turbulent Times

Page 9

Freese & Associates, Inc.

•

•Sales,

Manufac

turing,

Purcha

sing,

Transp

ortatio

n

•Sales/

Logisti

cs/Oper

ations

•Incept

ion of

SCM •Full I

mplement

ation

of Coll

aborat

ive

SCM

Prehistoric 2000

Post WWII 1982

How long will it take??

2???

The Evolution of SCM

More AttentionFrom SeniorManagement

More AttentionFrom SeniorManagement

20 April 2010Supply Chain Management in

Turbulent Times

Page 10

Freese & Associates, Inc.

A horizontal process view is the foundation to Supply Chain Management

Supply Chain management processes cut across the silos. It’s horizontal.

20 April 2010Supply Chain Management in

Turbulent Times

Page 11

Freese & Associates, Inc.

Most supply chains are global

D is tr ib u tio nD is tr ib u tio nD is tr ib u tio nD is tr ib u tio n

In te rn a tio n a l T ra d e In te rn a tio n a l T ra d e L o g is tic sL o g is tic s

C u s to m e rsC u s to m e rs

M a n u fa c tu r in gM a n u fa c tu r in gS u p p lie rsS u p p lie rs F in is h e dF in is h e dg o o d sg o o d s

w a re h o u s ew a re h o u s e

In te rn a tio n a l T ra d e In te rn a tio n a l T ra d e L o g is tic sL o g is tic s

C u s to m sC u s to m sC u s to m sC u s to m s

20 April 2010Supply Chain Management in

Turbulent Times

Page 12

Freese & Associates, Inc.

Electronics Supply Chain

Reverse Logistics

Component Manufacturers Distributors

ContractManufacturer

OEMsFinished Goods

Distributors / Channel Partners

Retailers &End Consumers

NationalSemi

AMD

TexasInstrument

LSILogic

Intel

Arrow

Avnet

Pioneer

Premier

Bell

Solectron

SCI

Celestica

Flextronics

Jabil

Sanmina

IBM

HP

Compaq

Lucent

Motorola

Dell

Alcatel

Nortel

Cisco

Ingram Micro

Tech Data Corp

Merisel, Inc

Brightpoint

CellStar

CompUSA

Best Buy

Radio Shack

RetailersRetailers

End ConsumerEnd Consumer

Enterprise SalesE-commerce

purchase

20 April 2010Supply Chain Management in

Turbulent Times

Page 13

Freese & Associates, Inc.

Factory

Seller’s DC Customer’s DC

ConsumersSeller’sPlant

Supplier

SCOR Model

20 April 2010Supply Chain Management in

Turbulent Times

Page 14

Freese & Associates, Inc.

Best in Class Performance & Potential Savings

Source: SRI International

$117.5b10.2%4.3%$1,991bDefense & Industrial

$138.9b9.2%4.9%$3,231bConsumer Packaged Goods

$23.5b8.3%3.3%$470bTelecommunications

$15.3b8.3%4.0%$356bComputers & Electronic

$46.8b11.2%3.9%$641bChemicals & Pharmaceuticals

Potential Savings

MedianLogistics Costs

Best in classTotal Revenue

BillionsIndustry

20 April 2010Supply Chain Management in

Turbulent Times

Page 15

Freese & Associates, Inc.

Benefits of SCM• Strengthens vendor -customer relations• Facilitates planning at all levels• Allows all partners in the supply chain to

monitor shipment progress• Minimizes bottlenecks created by waiting for

proper documents• Enables all parties to participate in process

improvements• Eliminates duplicate efforts• Enhances supply chain security

/

20 April 2010Supply Chain Management in

Turbulent Times

Page 16

Freese & Associates, Inc.

SCM Has ImpactsA study by Georgia Tech showed that a company’s stock price drops

8% when the company experiences a glitch in its supply chain.

A study at Miami University of Ohio showed that when a company adopts a new supply chain innovation, the company’s stock price increases.

A study by Bain & Company showed that companies employing sophisticated supply chain methods enjoyed 12 times greater profit than companies with unsophisticated methods.

Wall Street: New found respect for SCM. In one SCM MBA program in the US, 21/32 grads received job offers from Investment Banking firms because of the importance of SCM to their clients!!

20 April 2010Supply Chain Management in

Turbulent Times

Page 17

Freese & Associates, Inc.

Features Benefits Value• Single focus must be on the creation of value• Key questions include

– Value for whom?– How to create value through supply chain management?– How to measure and quantify the value that is created?

• Significant improvement needed in key areas such as:– Understanding customers’ needs– Performance measurement and KPIs– Quantification of value and determination of ROI

4/23/2010 5:17:13 PM20 April 2010 Supply Chain Management in

Turbulent Times

Page 18

Freese & Associates, Inc.

The Challenge is “Change”:

“Consider how hard it is to change yourself, and you’ll understand what little chance you have of changing others.”(Albert Einstein)

“It is not the strongest of the species that survive, nor the most intelligent, but those most responsive to change” (Charles Darwin)

20 April 2010Supply Chain Management in

Turbulent Times

Page 19

Freese & Associates, Inc.

Presents

Content Overview, Objectives & Definitions

State of LogisticsMagnitudeImpact

20 April 2010Supply Chain Management in

Turbulent Times

Page 20

Freese & Associates, Inc.

U.S. Logistics Cost as Percent of GDP in 2008

103273111487

455216671

58381041

177

854

1,397

InterestTaxes, Obsolescence, Depreciation, InsuranceWarehousing

Truck - IntercityTruck - Local

RailroadsWater (International 33 Domestic 5)

(International 16 Domestic 25)Oil PipelinesAir

Other Carriers:

Motor Carriers:

Subtotal

Subtotal

Subtotal

Carrying Costs - $ 2.026 Trillion All Business Inventory

Transportation Costs

Shipper Related CostsLogistics Administration

TOTAL LOGISTICS COST

$ Billions

30Forwarders

1

20 April 2010Supply Chain Management in

Turbulent Times

Page 21

Freese & Associates, Inc.

U.S. Business Logistics Costs

1

0.921.01 0.97 0.92 0.95

1.03

1.181.31

1.39 1.34

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

$ Tr

illio

ns

20 April 2010Supply Chain Management in

Turbulent Times

Page 22

Freese & Associates, Inc.

The U.S. Business Logistics System Cost is the Equivalent of 9.4 Percent

of Current GDP in 2008

47252122420

460220680

63391040

184

852

1,344

InterestTaxes, Obsolescence, Depreciation, InsuranceWarehousing

Truck - IntercityTruck - Local

RailroadsWater (International 33 Domestic 6)

(International 16 Domestic 24)Oil PipelinesAir

Other Carriers:

Motor Carriers:

Subtotal

Subtotal

Subtotal

Carrying Costs - $ 1.965 Trillion All Business Inventory

Transportation Costs

Shipper Related CostsLogistics Administration

TOTAL LOGISTICS COST

$ Billions

32Forwarders

2

20 April 2010Supply Chain Management in

Turbulent Times

Page 23

Freese & Associates, Inc.

Logistics Cost As A Percent of GDP

3

9.9 10.39.5

8.8 8.6 8.89.5

9.9 10.19.4

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

20 April 2010Supply Chain Management in

Turbulent Times

Page 24

Freese & Associates, Inc.4

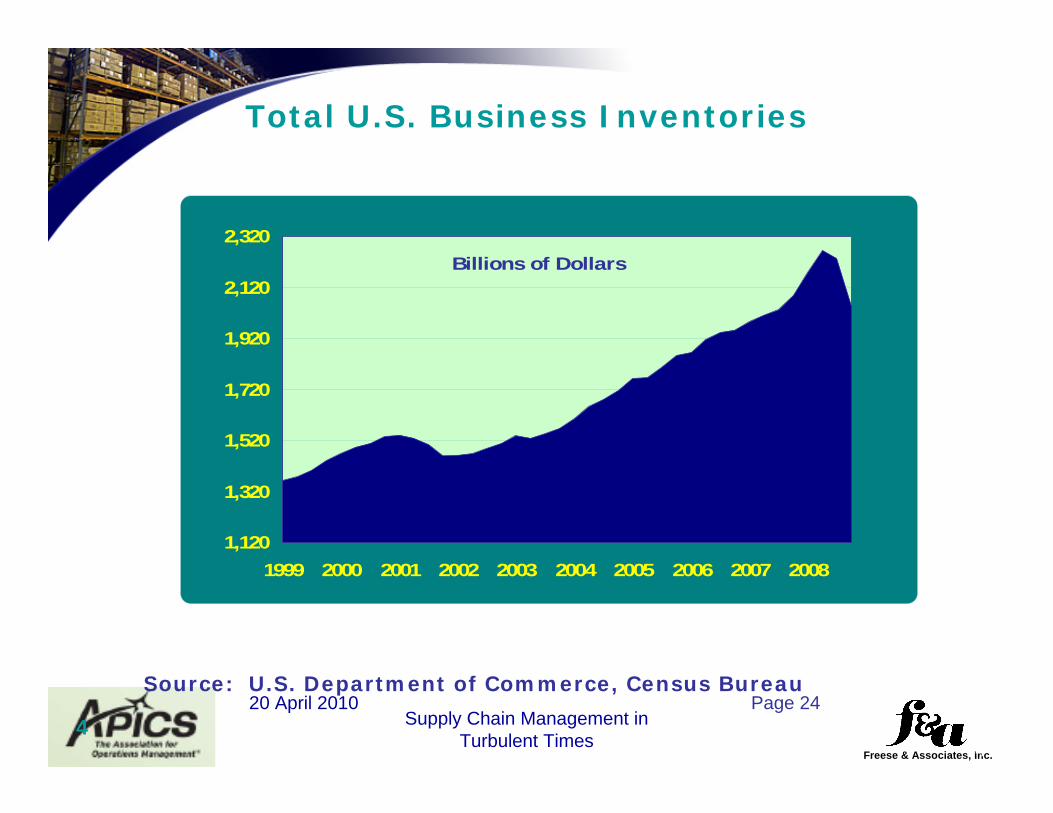

Total U.S. Business Inventories

Source: U.S. Department of Commerce, Census Bureau

1,120

1,320

1,520

1,720

1,920

2,120

2,320

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Billions of Dollars

4

20 April 2010Supply Chain Management in

Turbulent Times

Page 25

Freese & Associates, Inc.

The Inventory to Sales Ratio Rose Sharply in the Second Half of 2008

Source: U.S. Department of Commerce, Census Bureau

5

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

20 April 2010Supply Chain Management in

Turbulent Times

Page 26

Freese & Associates, Inc.

U.S. Average Commercial Paper Rates Have Fallen Dramatically in 2008

Source: Board of Governors of the Federal Reserve System

5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

19991999 2000 2001 2002 2003 2004 2006 2006 2007 2008

Perc

ent

6

20 April 2010Supply Chain Management in

Turbulent Times

Page 27

Freese & Associates, Inc.

The U.S. Business Logistics System Cost is the Equivalent of 9.4 Percent

of Current GDP in 2008

47252122420

460220680

63391040

184

852

1,344

InterestTaxes, Obsolescence, Depreciation, InsuranceWarehousing

Truck - IntercityTruck - Local

RailroadsWater (International 33 Domestic 6)

(International 16 Domestic 24)Oil PipelinesAir

Other Carriers:

Motor Carriers:

Subtotal

Subtotal

Subtotal

Carrying Costs - $ 1.965 Trillion All Business Inventory

Transportation Costs

Shipper Related CostsLogistics Administration

TOTAL LOGISTICS COST

$ Billions

32Forwarders

7

down 13%

$882up 2%

20 April 2010Supply Chain Management in

Turbulent Times

Page 28

Freese & Associates, Inc.

Index of Logistics Costs as a Percent of GDP 1988 - 2008

910

30

50

70

90

110

1988 1990 1995 2000 2005 2008

InventoryTransportationTotal

20 April 2010Supply Chain Management in

Turbulent Times

Page 29

Freese & Associates, Inc.

GDP Growth and Logistics Cost Growth

11

2004 2005 2006 2007 2008

GDPLogistics Costs

20 April 2010Supply Chain Management in

Turbulent Times

Page 30

Freese & Associates, Inc.

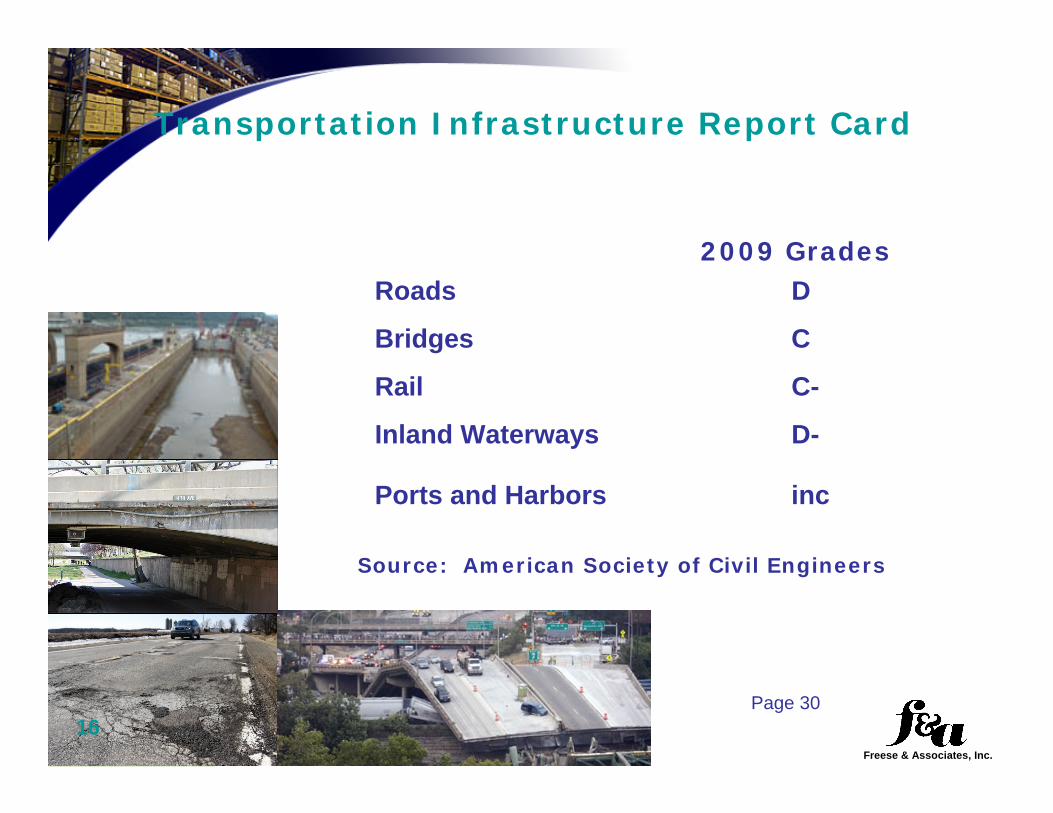

Transportation Infrastructure Report Card

2009 GradesRoads D

Bridges C

Rail C-

Inland Waterways D-

Ports and Harbors inc

Source: American Society of Civil Engineers

16

20 April 2010Supply Chain Management in

Turbulent Times

Page 31

Freese & Associates, Inc.

Summary

17

• 2008 Logistics Costs fell to $1.3 trillion

• Transportation costs rose 2.0 percent and now account for 6.1 percent of nominal GDP

Logistics cost were equivalent to 9.4 percent of GDP in 2008

•

• Inventory carrying costs declined 13.2 percent and now account for 2.9 percent of nominal GDP – both decreased inventories and lower interest rates contributed

21

The weak dollar spurred demand for U.S. goods pushing up exports. Higher shipments of export goods partially offset the drop in domestic shipping demand in 2008.

•

20 April 2010Supply Chain Management in

Turbulent Times

Page 32

Freese & Associates, Inc.

Cost As A Percent of GDP

9.9 10.39.5

8.8 8.6 8.89.5

9.9 10.19.4

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

20 April 2010Supply Chain Management in

Turbulent Times

Page 33

Freese & Associates, Inc.

The Changing Costs of Logistics

• From 2000/2004 Logistics Costs Declined– Low Energy Costs– Deregulation– Increased Information Technology

• Starting in 2005 Logistics Costs Increased– Rising Energy Costs– Rising Inventories– Declining Transportation Capacity

20 April 2010Supply Chain Management in

Turbulent Times

Page 34

Freese & Associates, Inc.

Wholesale Vs. Retail Inventories(Billions of Dollars)

200250

300350

400450

500550

600

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

WholesaleRetail

Source: U.S. Department of Commerce, Bureau of Economic Analysis

20 April 2010Supply Chain Management in

Turbulent Times

Page 35

Freese & Associates, Inc.

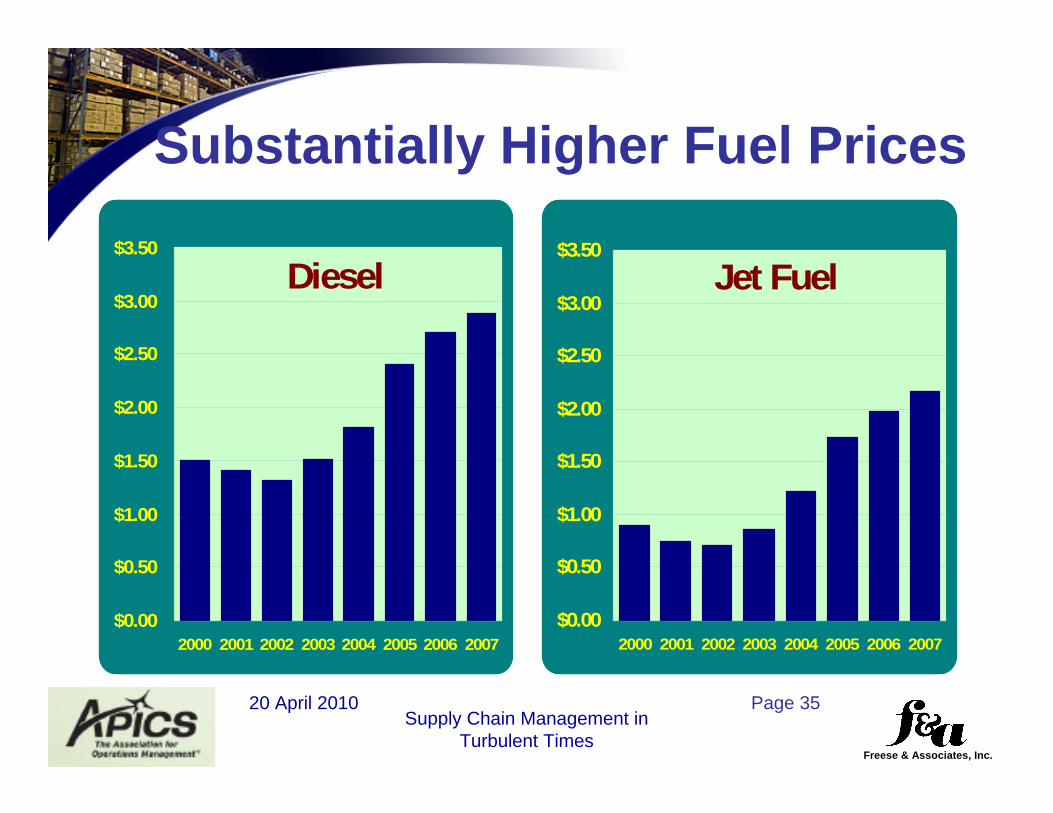

Substantially Higher Fuel Prices

Diesel

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

2000 2001 2002 2003 2004 2005 2006 2007

Jet Fuel

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

2000 2001 2002 2003 2004 2005 2006 2007

20 April 2010Supply Chain Management in

Turbulent Times

Page 36

Freese & Associates, Inc.

Fuel EfficiencyTon-Miles Per Gallon

Barge Railroad Truck

576

413

155

Source: Texas Transportation Institute Study, Nov. 2007

20 April 2010Supply Chain Management in

Turbulent Times

Page 37

Freese & Associates, Inc.

Mode Utilization

Barge Railroad Truck

20 April 2010Supply Chain Management in

Turbulent Times

Page 38

Freese & Associates, Inc.

Global Comparison of Logistics Expenditures

Asia 13-20% GDPChina 15% GDP

Europe 12-14% GDPIndia 13% GDPJapan 11% GDPMexico 14% GDP

EconomyHigher Output--GDPBetter use of resourcesMulti-use InfrastructureBusinessesMarket AccessMarket IntegrationCost EfficiencyConsumersMore Goods and ServicesWider AvailabilityLower Prices/Income

U.S. 9.4% GDP

20 April 2010Supply Chain Management in

Turbulent Times

Page 39

Freese & Associates, Inc.

The cost of logistics in the U. S. was $1.4 trillion in 2007; about 10.1% of our GDP (gross domestic product).

U. S. expenditure on logistics is larger than the national GDP of all but 12 countries. (For example, U. S. logistics expenditures are larger than the GDP of Spain).

Total domestic business inventories carrying costs rose 9 percent and now account for 3.5 percent of nominal GDP.

In 1980 logistics represented 17.9% of America’s GDP. Today it is 10.1%.By comparison, estimated logistics costs represent 15% of China’s GDP and 13% in India.

SOME MAGNITUDES…

Transportation costs rose 5.9 percent and now account for 6.2 percent of nominal GDP

20 April 2010Supply Chain Management in

Turbulent Times

Page 40

Freese & Associates, Inc.

Presents

Content Overview, Objectives & Definitions

Turbulent Times

20 April 2010Supply Chain Management in

Turbulent Times

Page 41

Freese & Associates, Inc.

The Perfect Storm

Credit Crunch

Crude Oil Prices

20 April 2010Supply Chain Management in

Turbulent Times

Page 42

Freese & Associates, Inc.

What We’ve Seen

Gasoline prices have risen lowered And were they stop no one knows

20 April 2010Supply Chain Management in

Turbulent Times

Page 43

Freese & Associates, Inc.

What About the Market?

What Goes Up Can Also Go Down

2007

2008

1938

20 April 2010Supply Chain Management in

Turbulent Times

Page 44

Freese & Associates, Inc.

GDP as an IndicatorUnited States GDP Growth Rate

20 April 2010Supply Chain Management in

Turbulent Times

Page 45

Freese & Associates, Inc.

Economic Indicators

3.25%3.25%3.25%Prime Rate

$58.85$70.60$87.05Oil / Barrel

$917.00$945.00$1,130.00Gold / Once

8.90%9.40%9.70%Unemployment

-6.29%-1.03%5.60%GDP Growth

-0.45%-1.19%2.10%Inflation

8,4699,33710,897DJI Index

May 12, 2009

August 10, 2009

April 7, 2010

20 April 2010Supply Chain Management in

Turbulent Times

Page 46

Freese & Associates, Inc.

ISM Index

Institute For Supply Management March 2010

20 April 2010Supply Chain Management in

Turbulent Times

Page 47

Freese & Associates, Inc.

Current PMI Direction

20 April 2010Supply Chain Management in

Turbulent Times

Page 48

Freese & Associates, Inc.

CPI February 2010

U S Bureau of Labor Statistics April 2010

20 April 2010Supply Chain Management in

Turbulent Times

Page 49

Freese & Associates, Inc.

Industrial Production & Capacity

Federal Reserve Board August 2009

20 April 2010Supply Chain Management in

Turbulent Times

Page 50

Freese & Associates, Inc.

2010 Dow Jones & Company April 2010

DJI 5 Year Trend

20 April 2010Supply Chain Management in

Turbulent Times

Page 51

Freese & Associates, Inc.

How This TranslatesTransportation for 2009, was flat or down because of:

• Volumes being down for trucking the largest segment. – In the current environment it was very difficult for rates to

increase. – For the last two years fuel surcharges have been a significant chunk of revenue. – With fuel prices falling

in the latter part of the year and volumes down many carriers eased off on the surcharges.

• Rail volumes although the fourth highest have ever been flat to slightly up,

– because pricing has been soft and surcharges were removed. • Air Freight was down because,

– volumes are down, – fuel pricing hurt economics.

• Water was down, – both internationally and domestically.

20 April 2010Supply Chain Management in

Turbulent Times

Page 52

Freese & Associates, Inc.

Presents

Content Overview, Objectives & Definitions

The Future

20 April 2010Supply Chain Management in

Turbulent Times

Page 53

Freese & Associates, Inc.

What This Means in SCMSCM Trends:• Reverse globalization - new sourcing strategies, especially Mexico;

rethinking many strategies• Changes in packaging design - and routing to reduce ton-miles• Capacity issues - loss of trucking capacity, excess capacity in container

shipping industry, driver shortages• Transportation Companies - Companies that come through this will be

stronger, more agile players• Impact of the stimulus bill - not enough nor aimed at the right spots to

turn around SCM direction• Need For a Strong National Freight Transportation Policy -

needs to address entire supply chain, funding issues (reduced fuel consumption has hit the already inadequate Highway Trust Fund), best investment strategies, etc.

• Fuel prices will be climbing again - strategies to mitigate fuel volatility

20 April 2010Supply Chain Management in

Turbulent Times

Page 54

Freese & Associates, Inc.

What This All Means in SCM• High fuel prices will led many to reevaluate their entire supply

chains.– companies are reevaluating where they are sourcing their raw materials, – where they are locating their manufacturing centers, and – where they are locating their distribution centers. – No longer is moving manufacturing operations to China seen as a

panacea.

• The rail and parcel/express sectors have weathered the best.

• LTL pricing is under the most pressure because demand is heavily tied to the industrial economy and capital spending, it is not as consolidated as the rail and parcel sectors, and it hasn't had enough capacity taken out relative to lower industry volumes.

20 April 2010Supply Chain Management in

Turbulent Times

Page 55

Freese & Associates, Inc.

The Future

• The Economy

• Oil Prices

• Shrinking Capacity

• And More

Barge Railroad Truck

Diesel

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

2000 2001 2002 2003 2004 2005 2006 2007

20 April 2010Supply Chain Management in

Turbulent Times

Page 56

Freese & Associates, Inc.

Green Trends

• Investors see “green” practices as a reflection of good management practices.

• Today: Public relations tactic.• Tomorrow: Real economic value

strategies.Energy cost inflation will help green ROI get even better.

• Cap and Trade

20 April 2010Supply Chain Management in

Turbulent Times

Page 57

Freese & Associates, Inc.

DC / Warehouse Facility items being considered include:

• Energy Creation measures

• Wind power units – rooftop units - individual fans or horizontal row of blades at roof edge to capture air flow rising up and over building, & stand alone tower units.

Green Trends Influencing Warehousing

20 April 2010Supply Chain Management in

Turbulent Times

Page 58

Freese & Associates, Inc.

• Solar Power Stations• Atop Warehouses / DC’s …. Why…???

Large available flat areas - “just sit there”Solar panels not a great load factorYou pay only for the solar energy produced, at prices equal to or below current retail energy rates.

•Whole Foods Store, CA

•Staples Store

Green Trends Influencing Warehousing

20 April 2010Supply Chain Management in

Turbulent Times

Page 59

Freese & Associates, Inc.

Mega Trends – Shifting Demographics

China’s middle class has grown From 20% to 40% by 2020

By 2010, 450 million Indians will Have middle class incomes

95% of the world populationGrowth through 2050 will occurIn developing nations

Urban areas will produce nearly allOf the population growth over the Next 25 years

20 April 2010Supply Chain Management in

Turbulent Times

Page 60

Freese & Associates, Inc.

What To Do When Supply Chains Go Wrong

20 April 2010Supply Chain Management in

Turbulent Times

Page 61

Freese & Associates, Inc.

• Reducing vulnerability . . .

• Build in flexibility . . .

• Resilience can be a competitive advantage . . .

• When things go wrong . . .

Resilience

20 April 2010Supply Chain Management in

Turbulent Times

Page 62

Freese & Associates, Inc.

• Resilience, a notion borrowed from material science, represents the ability of a material to recover its original shape following a deformation.

• Resilience can be achieved through redundancy

• Flexible or agile supply chains can help a company not only withstand disruptions by adapting quickly to changing conditions, but also better respond to the day-to-day gyrations of the marketplace.

Globalization is stretching supply chains at a time when market volatility is on the increase, exposing companies to greater risk.

Resilience

20 April 2010Supply Chain Management in

Turbulent Times

Page 63

Freese & Associates, Inc.

• Reducing Costs and Eliminating Waste

• Energy Costs and Conservation

• The most popular definition of sustainability can be traced to a 1987 UN conference. It defined sustainable developments as those that "meet present needs without compromising the ability of future generations to meet their needs“ (WECD, 1987).

Sustainability

20 April 2010Supply Chain Management in

Turbulent Times

Page 64

Freese & Associates, Inc.

Sustainability

20 April 2010Supply Chain Management in

Turbulent Times

Page 65

Freese & Associates, Inc.

75 % of the Global 100 Companies Issue Sustainability Reports

20 April 2010Supply Chain Management in

Turbulent Times

Page 66

Freese & Associates, Inc.

Trust

KEY ISSUES IMPACTINGSUPPLY CHAIN MANAGEMENT

Financial Markets

Multiple Supply Chains

20 April 2010Supply Chain Management in

Turbulent Times

Page 67

Freese & Associates, Inc.

Information Challenges

Managing Relationships

Old-line Management

20 April 2010Supply Chain Management in

Turbulent Times

Page 68

Freese & Associates, Inc.

Freese & Associates, Inc.www.FreeseInc.com