CUSTOMS LAW CHAPTER 1- 1 - GENERAL PROVISIONS- 1 law.pdfarticle 20 (customs opinion) .....- 14 -...

109

OG# 847 CUSTOMS LAW CHAPTER 1 .............................................................................................. - 1 - GENERAL PROVISIONS ....................................................................... - 1 - ARTICLE 1 (THE BASIS) ............................................................................. - 1 - ARTICLE 2 (RESPONSIBLE AUTHORITY) .................................................... - 1 - ARTICLE 3 (DEFINITIONS) ......................................................................... - 1 - ARTICLE 4 (UNIFORM APPLICATION OF CUSTOMS LAW)........................... - 6 - ARTICLE 5 (THE CUSTOMS TERRITORY OF THE COUNTRY) ......................... - 6 - ARTICLE 6 (CUSTOMS AREAS). ................................................................. - 6 - ARTICLE 7 (SCOPE OF WORK OF CUSTOMS) .............................................. - 7 - CHAPTER 2 .............................................................................................. - 7 - CUSTOMS ADMINISTRATION ........................................................... - 7 - ARTICLE 8 (ORGANIZATION) .................................................................... - 7 - ARTICLE 9 (SERVICE UNIFORM AND CONDITIONS OF SERVICE) ................................................................................................. - 7 - ARTICLE 10 (MOVEMENT OF GOODS) ....................................................... - 8 - ARTICLE 11 (RESPONSIBILITIES) ............................................................... - 8 - ARTICLE 12 (PROVIDING INFORMATION) ................................................ - 10 - ARTICLE 13 (CONFIDENTIALITY) ............................................................ - 11 - ARTICLE 14 (CUSTOMS CONTROLS OUTSIDE OF CUSTOMS OFFICES) ....... - 11 - ARTICLE 15 ( RIGHTS AND OBLIGATIONS OF IMPORTERS AND EXPORTERS) ............................................................................. - 11 - ARTICLE 16 (BROKERAGE) ...................................................................... - 11 - ARTICLE 17 (TAKING OF DECISIONS) ...................................................... - 12 - ARTICLE 18 (REVIEW OF CUSTOMS DECISIONS) ....................................... - 12 - CHAPTER 3 ............................................................................................ - 13 - TAKING CARE OF AN OBJECTION ................................................ - 13 - ARTICLE 19 (ARBITRATION).................................................................... - 13 - ARTICLE 20 (CUSTOMS OPINION) ............................................................ - 14 - ARTICLE 21( REVIEW OF ADMINISTRATIVE FINES FOR SMUGGLING) ........ - 14 - ADMINISTRATIVE FINES FOR SMUGGLING, REFERENCED IN ARTICLE 170 OF THIS LAW, SHALL BE IMPOSED ON THE BASIS OF AGREEMENT BY THE PARTIES

Transcript of CUSTOMS LAW CHAPTER 1- 1 - GENERAL PROVISIONS- 1 law.pdfarticle 20 (customs opinion) .....- 14 -...

OG# 847

CUSTOMS LAW

CHAPTER 1 ..............................................................................................- 1 -

GENERAL PROVISIONS.......................................................................- 1 -

ARTICLE 1 (THE BASIS) ............................................................................. - 1 -

ARTICLE 2 (RESPONSIBLE AUTHORITY) .................................................... - 1 -

ARTICLE 3 (DEFINITIONS)......................................................................... - 1 -

ARTICLE 4 (UNIFORM APPLICATION OF CUSTOMS LAW)........................... - 6 -

ARTICLE 5 (THE CUSTOMS TERRITORY OF THE COUNTRY)......................... - 6 -

ARTICLE 6 (CUSTOMS AREAS). ................................................................. - 6 -

ARTICLE 7 (SCOPE OF WORK OF CUSTOMS) .............................................. - 7 -

CHAPTER 2 ..............................................................................................- 7 -

CUSTOMS ADMINISTRATION ...........................................................- 7 -

ARTICLE 8 (ORGANIZATION) .................................................................... - 7 -

ARTICLE 9 (SERVICE UNIFORM AND CONDITIONS OF

SERVICE) .................................................................................................- 7 -

ARTICLE 10 (MOVEMENT OF GOODS)....................................................... - 8 -

ARTICLE 11 (RESPONSIBILITIES)............................................................... - 8 -

ARTICLE 12 (PROVIDING INFORMATION) ................................................ - 10 -

ARTICLE 13 (CONFIDENTIALITY) ............................................................ - 11 -

ARTICLE 14 (CUSTOMS CONTROLS OUTSIDE OF CUSTOMS OFFICES) ....... - 11 -

ARTICLE 15 ( RIGHTS AND OBLIGATIONS OF IMPORTERS

AND EXPORTERS) ............................................................................. - 11 -

ARTICLE 16 (BROKERAGE)...................................................................... - 11 -

ARTICLE 17 (TAKING OF DECISIONS) ...................................................... - 12 -

ARTICLE 18 (REVIEW OF CUSTOMS DECISIONS)....................................... - 12 -

CHAPTER 3 ............................................................................................- 13 -

TAKING CARE OF AN OBJECTION................................................- 13 -

ARTICLE 19 (ARBITRATION).................................................................... - 13 -

ARTICLE 20 (CUSTOMS OPINION) ............................................................ - 14 -

ARTICLE 21( REVIEW OF ADMINISTRATIVE FINES FOR SMUGGLING)........ - 14 -

ADMINISTRATIVE FINES FOR SMUGGLING, REFERENCED IN ARTICLE 170 OF

THIS LAW, SHALL BE IMPOSED ON THE BASIS OF AGREEMENT BY THE PARTIES

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

II

(TARAZI TARFIN). OTHERWISE, THE MATTER SHALL BE SUBMITTED TO THE

CUSTOMS ARBITRATION ADMINISTRATION FOR DETERMINATION. ......... - 14 -

ARTICLE 22(METHOD OF EXECUTIONS) .................................................. - 15 -

CHAPTER 4 CUSTOMS TARIFF AND VALUATION OF GOODS... -

15 -

ARTICLE 23 (THE CUSTOMS TARIFF) ....................................................... - 15 -

ARTICLE 24 (VALUATION OF GOODS)..................................................... - 15 -

ARTICLE 25 (EXCHANGE RATE) .............................................................. - 16 -

ARTICLE 26 (PERISHABLE GOODS) .......................................................... - 16 -

CHAPTER 5 ............................................................................................- 18 -

FAVOURABLE TARIFF.......................................................................- 18 -

ARTICLE 27 (CASES FOR GRANTING FAVOURABLE TARRIF)..................... - 18 -

ARTICLE 28 (REQUEST FOR FAVOURABLE TARIFF) .................................. - 19 -

CHAPTER 6 ORIGIN OF GOODS.....................................................- 21 -

ARTICLE 29 (PRODUCTION OF GOODS IN A COUNTRY) ............................ - 21 -

ARTICLE 30 (PRODUCTION OF GOODS IN MORE THAN ONE COUNTRY).... - 21 -

ARTICLE 31(CERTIFICATE OF ORIGIN) .................................................... - 22 -

ARTICLE 32 (PREFERENTIAL ORIGIN) ..................................................... - 22 -

ARTICLE 33(RETURN OF GOODS)............................................................. - 22 -

ARTICLE 34 (ENTRY AND EXIT OF GOODS)............................................. - 23 -

ARTICLE 35 (PLACE FOR PRESENTATION OF GOODS)............................. - 24 -

ARTICLE 36 (TRANSPORTATION OBSTACLES TO PRESENTATION OF GOODS). -

24 -

ARTICLE 37 (PRESENTATION OF AIR SHIPMENTS AT AIRPORT OF FINAL

DESTINATION)......................................................................................... - 25 -

ARTICLE 38 (PRESENTING MANIFESTS TO CUSTOMS)............................... - 25 -

ARTICLE 39 (CUSTOMS SUPERVISION ON AIRCRAFT ) ............................ - 26 -

ARTICLE 40 (EXEMPTION FROM OBLIGATION TO PRESENT A MANIFEST) . - 26 -

ARTICLE 41 (AIRCRAFT’S FORCED LANDING) ......................................... - 27 -

ARTICLE 42 (CUSTOMS DECLARATION FOR POSTAL GOODS) ................... - 27 -

ARTICLE 43 (EXEMPTION FROM DECLARATION)...................................... - 28 -

ARTICLE 44 (EXPORT SHIPMENTS).......................................................... - 29 -

ARTICLE 45 (CUSTOMS CONTROL ON TRANVELERS LUGGAGE) ............... - 29 -

ARTICLE 46 ( PRESENTATION OF GOODS FROM THE DETERMINED LOCATION

TO CUSTOMS) .......................................................................................... - 29 -

ARTICLE 47 (GOODS VERIFICATION AND TAKING OF SAMPLES) .............. - 29 -

ARTICLE 48 (SUBMISSION OF A SUMMARY DECLARATION)..................... - 30 -

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

III

ARTICLE 49 (UNLOADING AND TRANSSHIPPING AT DESIGNATED SITES) .. - 32 -

CHAPTER 8 ............................................................................................- 32 -

TEMPORARY STORAGE OF GOODS .............................................- 32 -

ARTICLE 50 (PLACES OF TEMPORARY STORAGE) .................................... - 32 -

ARTICLE 51 (REMOVING GOODS FROM TEMPORARY STORAGE) .............. - 33 -

ARTICLE 52 (NON-ALLOWED GOODS )................................................... - 33 -

CHAPTER 9 ............................................................................................- 34 -

CUSTOMS DECLARATION................................................................- 34 -

ARTICLE 53 (ASSIGNING A CUSTOMS DESIGNATION FOR NON-AFGHAN

GOODS) ................................................................................................... - 34 -

ARTICLE 54 (TIME PERIOD FOR COMPLETING CUSTOMS DECLARATION). - 34 -

ARTICLE 55 (DECLARATION OF THE GOODS FOR A CUSTOMS PROCESS) .. - 35 -

ARTICLE 56 (ACCEPTANCE OF THE DECLARATION)................................. - 35 -

ARTICLE 57 (VOLUNTARY AMENDMENT OR WITHDRAWAL OF

DECLARATIONS)...................................................................................... - 36 -

ARTICLE 58 (VERIFICATION OF THE DECLARATION) .............................. - 36 -

ARTICLE 59 (COMPOSITE DECLARATION)............................................... - 36 -

ARTICLE 60 (PARTIAL CONTROL) ........................................................... - 37 -

ARTICLE 61 (THE IDENTIFICATION OF THE GOODS) ................................ - 37 -

ARTICLE 62 (RELEASE OF GOODS) .......................................................... - 37 -

ARTICLE 63 (GOODS INELIGIBLE FOR RELEASE) ..................................... - 39 -

ARTICLE 64 (CUSTOMS AMENDMENT OR INVALIDATION OF DECLARATIONS) -

39 -

CHAPTER...............................................................................................- 40 -

CUSTOMS PROCESSES ......................................................................- 40 -

ARTICLE 65 (RELEASE OF GOODS FOR FREE CIRCULATION) .................... - 40 -

ARTICLE 66 (CONDITIONAL RELEASE OF GOODS) ................................... - 40 -

ARTICLE 67 ( CLASSIFICATION OF MIXED GOODS)................................... - 40 -

ARTICLE 69 ([CUSTOMS] PROCESSES WITH ECONOMIC IMPACTS) ............ - 41 -

ARTICLE 70 (CONDITIONS FOR GRANTING AN AUTHORIZATION)............. - 41 -

ARTICLE 71 (SECURITY) ......................................................................... - 42 -

ARTICLE 72 (RELEASE FROM THE PROCESSES WITH ECONOMIC IMPACTS) - 42

-

ARTICLE 73 (TRANSFER OF THE RIGHTS AND OBLIGATIONS)................... - 42 -

ARTICLE 74 (THE TIME FOR DETERMINING THE CUSTOMS DEBT) ............ - 42 -

ARTICLE 75 (TRANSIT PROCESS)...................................................... - 44 -

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

IV

ARTICLE 76 (RELEASE FROM THE PROCESS OF TRANSIT) ........................ - 44 -

ARTICLE 77 (TRANSIT VIA THIRD COUNTRIES)........................................ - 44 -

ARTICLE 78 (TRANSIT SECURITY) .......................................................... - 45 -

ARTICLE 79 (EXEMPTIONS FROM GIVING SECURITY) .............................. - 45 -

ARTICLE 80 (OBLIGATION OF PERSONS RESPONSIBLE FOR TRANSIT GOODS)... -

46 -

ARTICLE 81(CUSTOMS WAREHOUSING) ................................................. - 46 -

ARTICLE 82 (WAREHOUSE TYPES).......................................................... - 47 -

ARTICLE 83 (WAREHOUSE KEEPER AND HIS RESPONSIBILITIES) .............. - 47 -

ARTICLE 84 (APPROVAL (PERMIT) FOR OPERATING A CUSTOMS WAREHOUSE)

............................................................................................................... - 47 -

ARTICLE 85 (TRANSFER OF RIGHTS AND RESPONSIBILITIES) ................... - 48 -

ARTICLE 86 (DISTINCTIVE CASES) .......................................................... - 48 -

ARTICLE 87 (TIME FOR DEPOSITS IN WAREHOUSE) ................................. - 49 -

ARTICLE 88 (HANDLING OF GOODS UNDER CUSTOMS WAREHOUSING

PROCESS)................................................................................................ - 49 -

ARTICLE 89 (TEMPORARY WITHDRAWALS FROM WAREHOUSE).............. - 49 -

ARTICLE 90 (TRANSFER OF GOODS)........................................................ - 51 -

ARTICLE 91 (CUSTOMS VALUE OF WAREHOUSED GOODS.)...................... - 51 -

ARTICLE 92 (INWARD PROCESSING) ........................................................ - 51 -

ARTICLE 93 (TYPES OF INWARD PROCESSING OPERATIONS) .................... - 52 -

ARTICLE 94 (APPLICATION FOR APPROVAL OF INWARD PROCESSING) ... - 52 -

ARTICLE 95 (TIME PERIOD FOR EXPORTATION IN INWARD PROCESSING). - 52 -

ARTICLE 96 (RATE OF YIELD OF INWARD PROCESSING) ........................... - 53 -

ARTICLE 97 (RELEASE FOR FREE CIRCULATION FROM INWARD PROCESSING) -

53 -

ARTICLE 98 (COMPENSATING PRODUCTS OF INWARD PROCESSING)........ - 53 -

ARTICLE 99 (CUSTOMS DUTIES ON COMPENSATING PRODUCTS OF INWARD

PROCESSING)........................................................................................... - 54 -

ARTICLE 100 (COMPENSATING PRODUCTS OF INWARD PROCESSING AFTER

OUTWARD PROCESSING).......................................................................... - 55 -

ARTICLE 101 (DRAWBACK CASES) ......................................................... - 55 -

ARTICLE 102 (DRAWBACK DECLARATION)............................................. - 55 -

ARTICLE 103 (TEMPORARY EXPORTATIONS PURSUANT TO DRAWBACKS). - 55

-

ARTICLE 104(DRAWBACK REFUNDS) ..................................................... - 56 -

ARTICLE 105 (PROCESS UNDER THE CUSTOMS CONTROL) ....................... - 56 -

ARTICLE 106 (APPROVAL FOR PROCESSING UNDER CUSTOMS CONTROL) - 56 -

ARTICLE 107 (APPROVAL CONTENTS FOR PROCESSING UNDER CUSTOMS

CONTROL) ............................................................................................... - 58 -

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

V

ARTICLE 108 (DEBT AMOUNT IF PROCESS IS NOT COMPLETED)............... - 58 -

ARTICLE 109 (IMPORT OF COMPENSATING PRODUCTS OF PROCESSING UNDER

CUTOMS CONTROL) ................................................................................. - 58 -

ARTICLE 110 (THE TEMPORARY IMPORTATION PROCESS) ....................... - 58 -

ARTICLE 111 (APPROVAL FOR TEMPORARY IMPORTATION).................... - 59 -

ARTICLE 112(CONDITIONS FOR APPROVAL FOR TEMPORARY IMPORTATION) . -

59 -

ARTICLE 113 (SPECIAL CONDITIONS IN TEMPORARY IMPORTATION PROCESS)-

60 -

ARTICLE 114 (THE DUTY AMOUNT PAYABLE FOR GOODS UNDER THE

TEMPORARY IMPORTATION PROCESS WITH PARTIAL RELIEF)................... - 60 -

ARTICLE 115 (CHANGE OF CUSTOMS DESIGNATION OF TEMPORARILY

IMPORTED GOODS)................................................................ - 61 -

ARTICLE 116 (OUTWARD PROCESSING)................................................... - 61 -

ARTICLE 117 (APPLICATION FOR THE APPROVAL OF OUTWARD PROCESSING)

............................................................................................................... - 61 -

ARTICLE 118 (CONTENTS OF OUTWARD PROCESSING APPROVAL) ........... - 62 -

ARTICLE 119 (IMPORT DUTY FOR COMPENSATING PRODUCTS OF THE

OUTWARD PROCESSING)....................................................... - 63 -

ARTICLE 120 (GOODS REPAIRED WITHOUT CHARGE IN THE OUTWARD

PROCESSING)........................................................................................... - 63 -

ARTICLE 121 (TRANSFER OF RIGHTS OF THE OUTWARD PROCESSING

APPROVAL) ............................................................................................. - 65 -

ARTICLE 122 (EXPORT PROCESS FOR AFGHAN GOODS) .......................... - 65 -

ARTICLE 123 ( EXPORTATION OF NON-AFGHAN GOODS) ........................ - 65 -

CHAPTER 11..........................................................................................- 65 -

FREE ZONES AND FREE WAREHOUSES......................................- 65 -

ARTICLE 124 (THE MEANING OF CUSTOMS DUTY FREE ZONES) ............... - 65 -

ARTICLE 125 (FREE ZONES DESIGNATION).............................................. - 67 -

ARTICLE 126 (CUSTOMS SUPERVISION IN FREE ZONES) .......................... - 67 -

ARTICLE 127(CONDITIONS FOR ENTRANCE AND EXIT OF GOODS)............ - 68 -

ARTICLE 128 (CUSTOMS STATUS OF GOODS IN DUTY FREE ZONES) ........ - 68 -

ARTICLE129 (TIME LIMITS) .................................................................... - 69 -

ARTICLE 130 (AUTHORIZED ACTIVITIES) ................................................ - 69 -

ARTICLE 131 (APPROVED REGISTERS) .................................................... - 69 -

ARTICLE 132(TARIFF ON CONSUMED AND MISSING GOODS).................... - 70 -

ARTICLE 133 (ABANDONMENT OR DESTRUCTION OF GOODS IN FREE ZONES) . -

70 -

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

VI

CHAPTER 12..........................................................................................- 70 -

CUSTOMS DESIGNATIONS...............................................................- 70 -

ARTICLE 134 (DESTRUCTION OR ABANDONMENT OF GOODS) ................. - 70 -

ARTICLE 135 (DESTRUCTION OF GOODS) ................................................ - 71 -

ARTICLE 136(PROCEEDS FROM ABANDONED GOODS) ............................. - 71 -

CHAPTER 13..........................................................................................- 71 -

CUSTOMS DEBT...................................................................................- 71 -

ARTICLE 137 (FORM OF SECURITY)........................................................ - 71 -

ARTICLE 138 (THE LIMIT OF A SINGLE SECURITY FOR MULTIPLE OPERATIONS)

............................................................................................................... - 72 -

ARTICLE 139 (THE SECURITIES AMOUNT) .............................................. - 72 -

ARTICLE 140 (CASH DEPOSITS) .............................................................. - 72 -

ARTICLE 141 (GUARANTOR) .................................................................. - 73 -

ARTICLE 142 (OTHER KINDS OF SECURITY) ............................................ - 73 -

ARTICLE 143 (ADDITIONAL SECURITIES) ................................................ - 73 -

ARTICLE144 (RELEASE OF SECURITY).................................................... - 73 -

ARTICLE 145 (LAWFUL ACTIVITIES WHICH CAUSE CUSTOMS DEBT)........ - 74 -

ARTICLE 146 (UNLAWFUL ACTIVITIES CAUSING A CUSTOMS DEBT)........ - 74 -

ARTICLE 147 (CUSTOMS DEBT ON REMOVAL OF GOODS FROM SUPERVISION

WITHOUT PERMISSION)............................................................................ - 75 -

ARTICLE 148 (NON OCCURRENCE OF DEBT) ........................................... - 75 -

ARTICLE 149 (RESPOSIBILITY OF PARTNERSHIPS)................................... - 75 -

ARTICLE150 (DATE OF DETERMINING CUSTOMS DEBT) ........................... - 75 -

ARTICLE 151 (ENTRY OF DEBT INTO ACCOUNTS) .................................... - 76 -

ARTICLE 152 (DIFFERENCES IN ACCOUNT ENTRIES) ............................... - 76 -

ARTICLE 153 (NOTIFICATION ABOUT DEBT ENTRY) ................................ - 77 -

ARTICLE 154 (SITUATIONS FOR SETTLING AND EXTINQUISHING OF

CUSTOMS DEBTS) .................................................................................... - 77 -

ARTICLE 155 (PAYMENT TERM FOR CUSTOMS DEBT).............................. - 77 -

ARTICLE 156 (DEFERRAL OF DEBT PAYMENT)........................................ - 78 -

ARTICLE 157 (MANNER OF PAYMENT) .................................................... - 78 -

ARTICLE 158 (NON PAYMENT OF DEBT WITHIN THE PRESCRIBED TERM). - 79 -

ARTICLE 159 ( REFUND OR REMISSION OF AN ERRONEOUS ENTRY) ......... - 80 -

ARTICLE 160 (REMISSION OR REFUND FOR DEFECTIVE GOODS)............... - 80 -

ARTICLE161 (LIMIT OF THE AMOUNTS TO BE REFUNDED)....................... - 81 -

ARTICLE162 (INTEREST ON REFUNDS) .................................................... - 81 -

ARTICLE 163 (ERRONEOUS REFUNDS) .................................................... - 81 -

CHAPTER 14 CUSTOMS VIOLATIONS AND PENALTIES......- 81 -

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

VII

ARTICLE 164 (CUSTOMS POLICE ADMINISTRATION).............................. - 81 -

ARTICLE 165 (CUSTOMS VIOLATIONS) .................................................... - 84 -

ARTICLE 166 (ADMINISTRATIVE VIOLATIONS AND SANCTIONS)............. - 84 -

ARTICLE 167 (PENALTIES)...................................................................... - 86 -

ARTICLE 168 (MULTIPLE OFFENSES) ...................................................... - 86 -

ARTICLE 169 ( METHOD FOR COLLECTION OF FINES)............................. - 87 -

ARTICLE 170 (DISCRETIONARY ADMINISTRATIVE PENALTIES) ............... - 88 -

ARTICLE171 (LICENSE REVOCATION) .................................................... - 89 -

ARTICLE 172 (SMUGGLING OF GOODS) ................................................... - 89 -

ARTICLE 173 (SANCTIONS APPLICABLE TO SMUGGLING) ........................ - 91 -

ARTICLE 174 ( SMUGGLING OBJECTS) ..................................................... - 91 -

ARTICLE 175 (VEHICLES) ....................................................................... - 92 -

ARTICLE 176 (THE SEIZURE OF SMUGGLING OBJECTS)............................ - 92 -

ARTICLE 177 (PERISHABLE GOODS; LIVESTOCK) .................................... - 93 -

ARTICLE 178 (COMPENSATION FOR DAMAGES)....................................... - 93 -

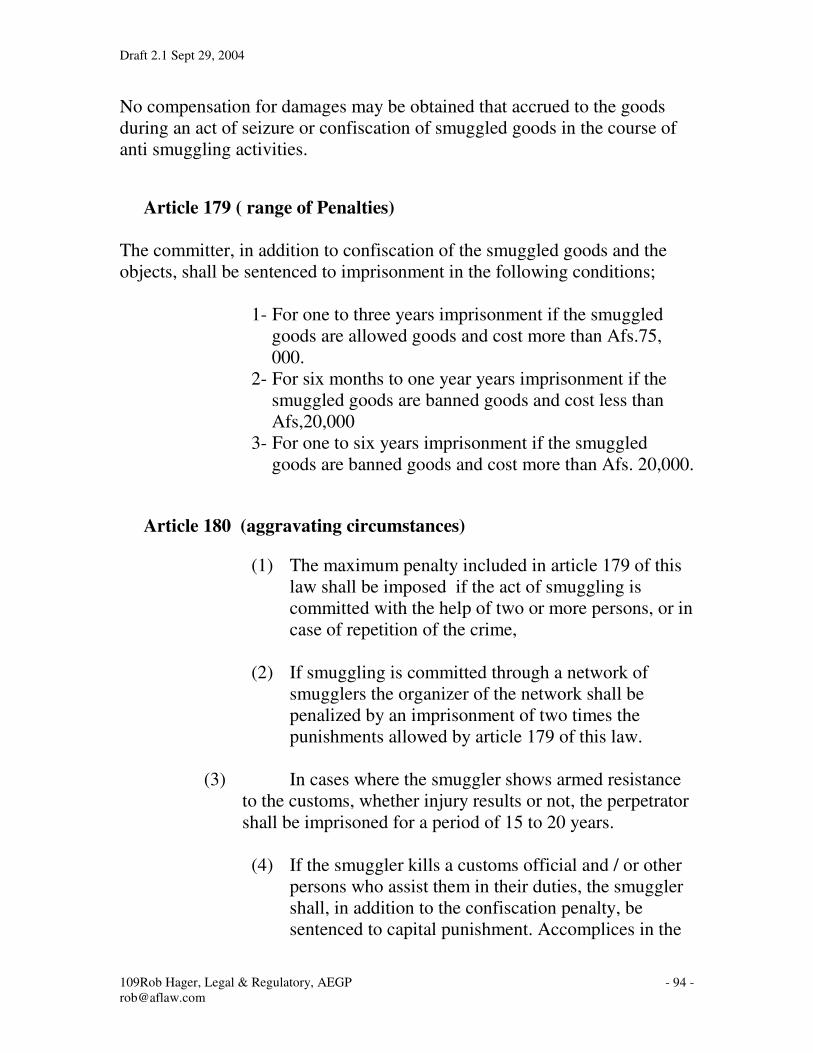

ARTICLE 179 ( RANGE OF PENALTIES) .................................................... - 94 -

ARTICLE 180 (AGGRAVATING CIRCUMSTANCES) ................................... - 94 -

ARTICLE181 (PATICIPATION OF GOVERNMENT EMPLOYEES IN SMUGGLING

ACTIVITY) ............................................................................................... - 95 -

ARTICLE 182 (EVALUATION OF ADMINISTRATIVE VIOLATIONS).............. - 95 -

ARTICLE 183 (AUTHORITY FOR ACCESS TO INFORMATION).................... - 95 -

ARTICLE 184 (REPORT AND COLLECTION OF EVIDENCE) ......................... - 95 -

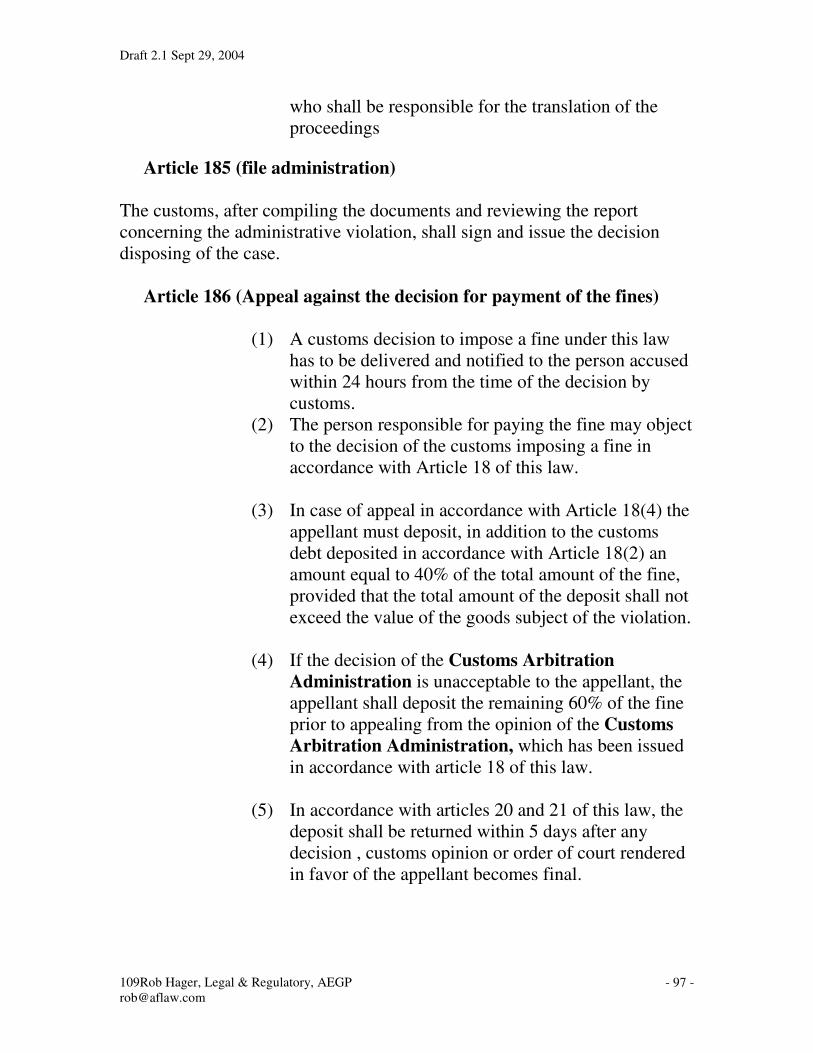

ARTICLE 185 (FILE ADMINISTRATION) .................................................... - 97 -

ARTICLE 186 (APPEAL AGAINST THE DECISION FOR PAYMENT OF THE FINES) -

97 -

CHAPTER 15 DISTRIBUTION OF REVENUES AND GRANTING

OF INCENTIVES...................................................................................- 98 -

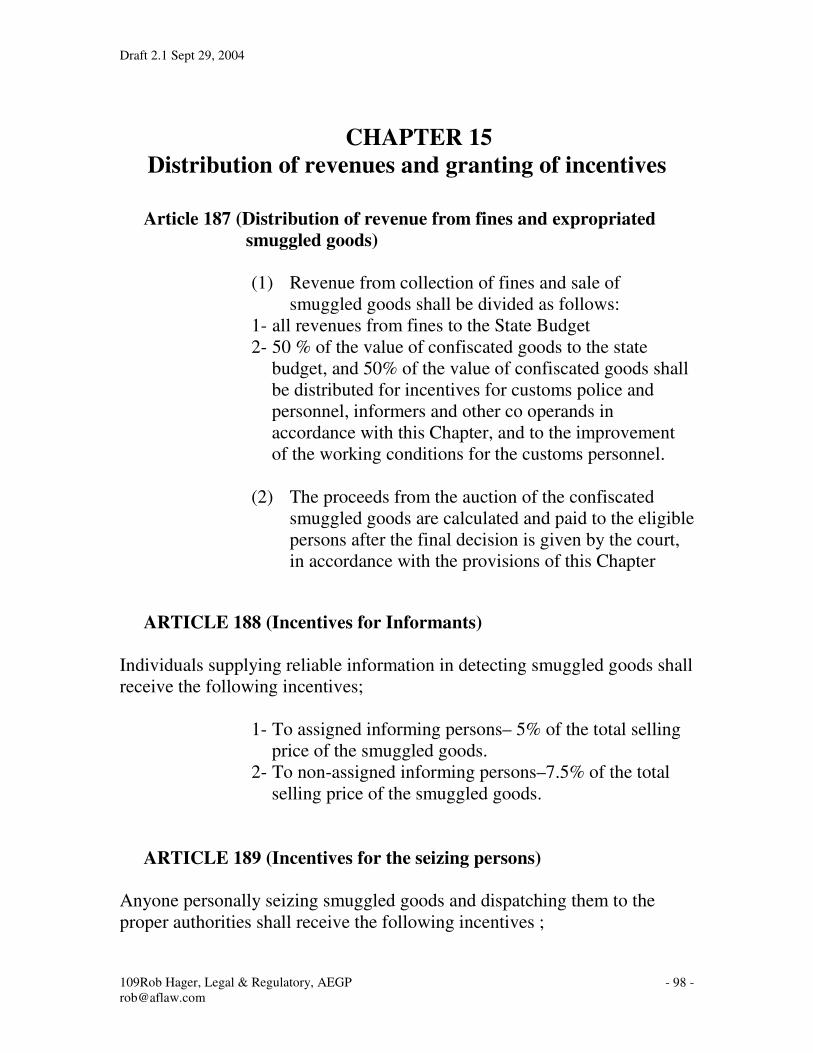

ARTICLE 187 (DISTRIBUTION OF REVENUE FROM FINES AND EXPROPRIATED

SMUGGLED GOODS)................................................................................. - 98 -

ARTICLE 188 (INCENTIVES FOR INFORMANTS) .................................... - 98 -

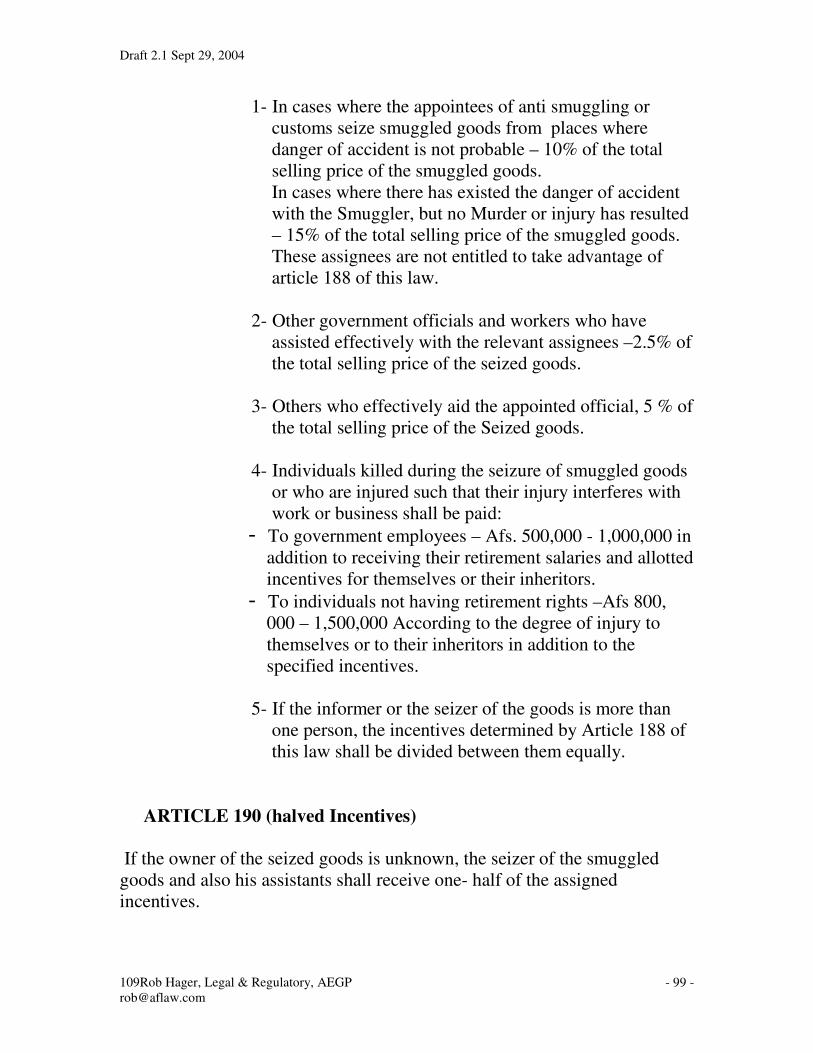

ARTICLE 189 (INCENTIVES FOR THE SEIZING PERSONS) ....................... - 98 -

ARTICLE 190 (HALVED INCENTIVES) ................................................... - 99 -

CHAPTER 16........................................................................................- 101 -

MISCELLANEOUS .............................................................................- 101 -

ARTICLE191 (ASSISTING CUSTOMS ADMINISTRATIONS) .................... - 101 -

ARTICLE 192 (PRESENTATION OF ANNUAL CUSTOMS REPORT) ........... - 101 -

ARTICLE 193: (PREFERENTIAL PROVISIONS) ......................................... - 101 -

ARTICLE 194 (DATE OF ENFORCEMENT) ............................................... - 102 -

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 1 -

CHAPTER 1

GENERAL PROVISIONS

Article 1 (the basis)

This law has been enacted in the light of Art 42 of the Constitution in order

to ensure the collection of revenues of the State through the customs of the

country, arranging for the organization of customs, defining the scope of

authority of relevant officials, the methodology for supervising and

controlling the movement of goods in and out of Afghanistan, and providing

for prevention of customs violations.

Article 2 (Responsible authority)

The Ministry of Finance is responsible for the collection of customs

revenues of the country, and for enforcing the provisions of this law and any

other relevant customs legislation.

Article 3 (Definitions)

For the purposes of this law, the following definitions shall have the

meanings set forth below:

1- ‘Person’ means:

- a natural person; [or]

- a legal person,

2- "Persons established [in Afghanistan]" means:

- In the case of a natural person, any person who is

resident in the Afghanistan for more than 183 days per

year.

- A legal person who has a registered central or a

permanent business agency in Afghanistan.

3- "Customs" means the state agency which carries out

and controls custom affairs of export, import, and transit

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 2 -

goods, travelers and responsible staff baggage and

parcel post in accordance with customs legislation.

4- “Customs legislation” means this Law, and any other

enforced legislation, international conventions and

treaties containing customs provisions to which

Afghanistan is a party and relevant rules and

procedures.

5- “Customs Areas” means the areas where the customs

exercise their activities as well as areas where the

customs exercise direct and indirect control or

supervision of the relevant affairs.

6- ‘Customs decision’ (tasmim) means any official order

(hedayat e rasmi) by customs officials pertaining to the

application of Customs legislation to a particular case

which affects one or more specific or identifiable

persons.

7- 'Customs opinion' means the decision of the Customs

Arbitration Admninistration (Edaara Hakamiyet e

Gumruki) taken with regard to a disputed [customs]

case.

8- ‘Customs status’ means the categorization of goods as

Afghan or non-Afghan goods.

9- ‘Afghan goods’ means goods:

- Wholly obtained or produced in the customs territory of

the State in accordance with the provisions of Article 29

of this law;

- imported from other countries, which have been released

for free circulation in the customs territory of the State;

- Obtained or produced in the customs territory of the

State, either from goods referred to in subparagraph (2)

alone, or from goods referred to both in subparagraphs

(1) and (2) above.

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 3 -

10- ‘Non-Afghan goods’ means goods other than those

referred to in subparagraph 9 of this Article.

11- ‘Customs debt’ means a payment obligatory on a

person, on account of customs duty, charges (haq ul

zamat), dues (awarez), penalties (jerima), and any other

monetary obligations (eltezamat e puli) that apply to

specific goods or actions under customs legislation.

12- ‘Customs Debtor’ means any person liable for the

payment of a customs debt.

13- "Responsible Person" is the declarant, except when

[this] Law indicates otherwise.

14- ‘Import duty’ means customs duty on the importation

of goods.

15- ‘Export duty’ means customs duty on the exportation

of goods.

16- ‘customs supervision' means the inspection done by

customs authorities with a view to ensuring that customs

legislation and, other provisions applicable to goods

subject to customs supervision are observed, and may

include measures for exercising customs control, when

necessary.

17- ‘customs control’ means executing specific actions,

such as examining goods, verifying the existence and

the authenticity of customs documents, examining the

accounts and other records, inspecting means of

transport, luggage and other goods carried by or on

persons, seizing goods, and reporting suspects to the

judicial and justice authorities, with a view to ensuring

that customs legislation and any other provisions

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 4 -

applicable to goods subject to customs supervision are

respected in the customs territory of the State.

18- “Customs designation” means :

- the placing of goods under a customs process,

- their entry into a free zone, free warehouse, or duty free

shop.

- their destruction, or

- Their abandonment and transfer to the State.

19- ‘Customs process’ means the following stages

(marahel):

- release for free circulation within the customs territory of

the State;

- conditional release of goods under customs supervision

- transit;

- customs warehousing;

- inward processing;

- outward processing;

- processing under customs control;

- temporary importation;

- Exportation.

20- ‘Suspensive process’ means the following customs

processes which entails suspension of the payment of

the customs debt:

- transit;

- customs warehousing;

- inward processing

- processing under customs control;

- temporary importation;

21- “Suspensive goods” means goods placed under [one or

more of the] suspensive processes mentioned in section

20 of this article.

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 5 -

22- "Favorable tariff" means a reduction in, suspension of,

or exemption from the otherwise applicable import duty

stated in the Customs Tariff,

23- "Customs declaration" means the act or document

whereby a person expresses, the wish to place goods

under a given customs designation or process.

24- "Time of acceptance of the declaration" means the

time when the customs declaration presented to customs

is accepted by the relevant [customs] office .

25- "Declarant" means any person who prepares and

presents a customs declaration.

26- "Presentation of goods at customs" means the

notification to the customs, in accordance with the

relevant procedures, of the arrival of goods at customs

or at any other place designated or approved by the

Customs.

27- "Release of goods" means the act whereby the customs

make goods available to the declarant for placement or

disposition under a customs designation or process.

28- "Holder of authorization" means the person to whom

an authorization has been granted.

29- "Customs Duty" means an amount of money assessed

on imports or exports in accordance with the

classification and rates stated in the Customs tariff,

30- "Force majeure" means a natural disaster, war,

unexpected political and economic upheavals, or similar

act beyond the control of the person affected.

31- "Commercial policy measures" means the imposition

of quotas, ceilings, countervailing duties on subsidized

foreign goods, anti-dumping duties, or other similar

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 6 -

provisions for advancing national (keshwar) commercial

interests.

32- “Remission” (lit. “cession” -Wogozari) means a

decision to waive all or part of a customs debt prior to

entry or after entry and before payment in accordance

with article 151.

33- “refund” means the total or partial repayment of a

customs debt which has been paid;

Article 4 (Uniform Application of Customs law)

(1) Customs legislation shall apply uniformly throughout

the customs territory of the country.

(2) Customs legislation may also apply in other countries,

within the framework of either international

conventions or other provisions governing specific

customs activities, provided that they do not conflict

with the laws of another country,

(3) Customs legislation may be applied in cooperation

with customs administration of other countries at joint

facilities [places], either inside or outside of

Afghanistan’s customs territory, in accordance with

international agreements and conventions.

Article 5 (the customs territory of the country)

The customs territory of the country shall include the land, and water

territory, and the airspace of Afghanistan.

Article 6 (Customs areas).

(1) Customs areas may be established at border crossing

points, international airports, duty free zones, customs

warehouses and any other points within the Customs

Territory as provided for in this Law.

(2) Customs areas may be established, altered or

abolished upon the recommendation of the Customs

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 7 -

Administration and the approval of the Ministry of

Finance.

Article 7 (Scope of work of Customs)

In order to secure (taamin) the interests of the State, Customs shall apply the

necessary controls in accordance with this law and other Customs

Legislation with respect to international shipments and import and export

goods in the customs territory of the country.

CHAPTER 2

Customs Administration

Article 8 (Organization)

(1) Customs Administration comprises the General

Directorate, the Regional Directorates and their

Branches. All Customs shall work under the

supervision of [and subordinate to] the general

directorate of customs of Ministry of Finance.

(2) The General Director of Customs is appointed upon

the recommendation of the Ministry of Finance in

accordance with the provisions of this law.

(3) The Deputy Directors General of Customs are

appointed, upon the proposal of the General Director

of Customs, and confirmation of the Ministry of

Finance, in accordance with the provisions of this

law.

(4) The other civil service (momorin) and auxiliary (ajir)

personnel of the Customs are employed in accordance

with the procedures established by the law.

Article 9 (service uniform and conditions of service)

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 8 -

(1) Customs personnel shall wear the service uniform. In

the event that service needs make it necessary to work

without wearing a uniform, the customs personnel

must show their Identity Cards.

(2) Customs officers are not allowed to accept directly or

indirectly, rewards in cash or kind for the customs

services performed.

(3) Customs officers are not allowed to carry on any kind

of business, or advising activity, that is incompatible

with the faithful performance of customs duties.

Article 10 (Movement of Goods)

Goods may cross the State border, and designated customs borders at

customs warehouses, at duty free zones, in airports, and at any other

facilities under customs control, only at [customs] areas where customs

officers are present.

Article 11 (Responsibilities)

)١( (1) Loading, unloading, movement, and

transshipment of goods through specified customs borders

as well as their release from a customs process, is carried

out with the permission of the customs in accordance with

Customs legislation.

(2) The customs is responsible for:

1. determining the value of goods and collecting the related

customs debt.

2. supervising, detecting, reporting and preventing

smuggling;

3 detecting and evaluating violations of this law;

4 participating in preparing and signing international

agreements and conventions in customs matters, in

accordance with Customs legislation;

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 9 -

5 preparing, collecting and, upon agreement of the

Minister of Finance, distributing foreign trade statistical

data to the Ministry of Commerce and other public

institutions;

6 supervising customs goods, throughout the entire

customs territory of the State;

7 exercising customs control over customs areas,

8 maintaining customs records

9 carrying out all other activities determined in Customs

legislation.

(3) In order to improve the enforcement of Customs

legislation, Customs, with the approval of the

Minister of Finance may, subject to Article 13, sign

agreements with state or non-state domestic or

foreign, organizations, for exchanging information.

(4) Customs shall establish customs verification teams to

verify the conformity of the quantity and quality of

the goods transported with the customs documents

accompanying them at exit from border crossing

points and in airports, as well as at the exit of the

inland customs offices, and at the facility of

importers. If the goods and transportation are in

conformity with the customs documents, the customs

verification team will confirm the customs documents

and stamp them. If the goods and transportation are

not in conformity with the customs documents, they

will draw up the appropriate written report, and

submit it to the relevant customs office for

investigation.

(5) Customs administrations shall assign mobile customs

verification teams to verify customs compliance of

transporters in the customs territory along roads. The

members of the mobile teams shall examine the

customs documents and the goods upon presentation

of their identity card and shall draw up the

appropriate written report, to the relevant customs

administration in accordance with the relevant

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 10 -

procedures.

(6) In cases of feeling danger to [ life or ] health, or to

the environment, customs may, upon notice to the

declarant have goods presented to customs destroyed

or removed from the area in accordance with the

relevant procedure.

(7) When customs receives information from other public

authorities that are working in the customs territory of

the state with regard to violations of customs

legislation, the customs shall submit a written report,

to the relevant customs administration for further

investigation (rasidigi)..

(8) If police authorities check vehicles that have been

sealed by Customs, the vehicle shall be transferred to

the nearest customs office to obtain the agreement of

Customs for removal of the seal and to perform

controls (bazrasi). In this case, the police and

customs will submit a written report to the customs

administration for investigation.

Article 12 (Providing information)

(1) Customs may provide information free of charge to

requesting parties concerning the application of

customs legislation in the forms prepared by the

ministry of finance, except when it pertains to an

ongoing import or export operation or would be

inconsistent with the provisions of Article 13 of this

law.

(2) Incase the provision of information shall involve

expense, customs may collect the expenses from the

applicant.

(3) The Ministry of Finance may in prepared forms,

when needed require the necessary information to be

supplied by relevant persons.

(4) Information provided by persons as required in

section 3 is effective when signed.

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 11 -

Article 13 (Confidentiality)

The following information is covered by the obligation of professional

secrecy and the customs will not disclose such information without

permission of the person concerned and legal authority to do so:

1- The valuation of a specific goods,

2- Details [e.g. names and addresses] of suppliers of

goods,

3- The results of testing, and

4- Other information which is provided to Customs on a

confidential basis.

Article 14 (Customs Controls outside of customs offices)

Customs, when the needs of the trade so require and upon request of the

person concerned, may allow some of the customs controls to be carried out

at the premises pertinant to the importer. The Director of Customs for the

area, taking into account the conditions, shall establish the cost of this

service and collect them from the importer or his agent.

Article 15 ( RIGHTS AND OBLIGATIONS OF IMPORTERS

AND EXPORTERS)

the customs clearance of import and export goods shall be executed by a

customs broker to who has been licensed by the Ministry of Finance. Postal

goods referenced in Article 42 of this law and travellers luggage referenced

in Article 45 of this law shall be an exception to this provision.

Article 16 (brokerage)

(1) Brokerage is a non-governmental business which

persons may carry out upon obtaining a license from

the Ministry of Finance

(2) The conditions for obtaining the license and the rights

and obligations of the customs broker shall be

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 12 -

regulated by separate rules (loyaha) approved by the

MOF.

Article 17 (Taking of decisions)

(1) Customs may make a decision with regard to a

particular [customs] transaction upon the request of

the person [concerned]. The applicant must furnish

[all] the information and documents required by

customs to make the decision.

(2) Customs are obliged to take the decision mentioned in

Section 1 within a maximum of 30 days and

announce it to the applicant.

(3) In case the customs decision mentioned in section 2 is

detrimental to the interests of the applicant or any

other [interested] party, the customs shall notify their

decision in writing together with the reasons to the

applicant and shall explain that the applicant has the

right to object.

Article 18 (review of customs decisions)

(1) A customs decision may be reviewed upon

submission of an application by the applicant. In case

a decision was due to the submission of incorrect

information by the applicant, review will not be

permitted except in accordance with Article 186.

(2) Customs decisions mentioned in para 1 shall be

enforceable and the customs debt [assessed] (other

than penalties paid in accordance with Article 186)

shall be collected and shall remain in trust (taht

amanat) until final decision

(3) An interested party may request a review of a

disputed customs decision through any competent

regional customs authority to the General Directorate

of Customs, within 10 days from the day of

notification of the decision by the Customs. The

General Directorate of Customs must take and issue a

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 13 -

decision within 20 days on the outcome of the review.

In the event the General Director of Customs does not

issue a decision within this time period, the request

shall be presumed to have been decided in favor of

the person making it.

(4) In case of an objection to a decision made by the

General Directorate of Customs or the rejection of the

request by the General Directorate of customs, it may

be submitted to the Customs Arbitration

Administration.

(5) An objection to a customs decision shall be made by

filing a notice of objection mentioned in para 4 shall

be presented to the Customs Arbitration

Administration within fifteen days of receiving a

customs decision [from the General Directorate of

Customs], along with security for costs in the amount

of 2 percent of the contested amount.

Chapter 3

Taking care of an objection

Article 19 (arbitration)

(1) The Customs Arbitration Administration shall be

established within the framework of the Ministry of

Finance for the purpose of taking care of the

objections to the decisions of customs

administrations.

(2) The Arbitration Administration shall be composed of

three members to be appointed upon proposal of the

Minister of Finance by the Head of State.

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 14 -

Article 20 (customs opinion)

(1) The order of the customs arbitration administration

shall be final and enforceable where the amount of

customs debt in dispute is up to 50000 Afs.

(2) If the amount of the customs debt in dispute is

greater than Afs. 50,000 the parties may in case of

dissatisfaction refer the opinion to the relevant

commercial Court. The order of court shall be final

and enforceable.

Article 21( review of administrative fines for smuggling)

Administrative fines for smuggling, referenced in Article 170 of this law,

shall be imposed on the basis of agreement by the parties (tarazi tarfin).

Otherwise, the matter shall be submitted to the Customs Arbitration

Administration for determination.

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 15 -

Article 22(Method of executions)

The manner of taking care of the objections sent to the customs arbitration

administration shall be regulated in a separate regulation.

Chapter 4

Customs tariff and valuation of Goods

Article 23 (The customs tariff)

(1) The customs tariff is a document enacted in

accordance with this law and the import and export

duty of goods is determined based on the

classification [of such goods in the tariff].

(2) The Customs Tariff shall be approved by the

Minister of Finance, upon recommendation of

General Director of Customs.

(3) No treaty, international agreement, or other

legislative documents shall affect the Customs Tariff

referenced in this law, unless the customs related

provisions of such treaties, international agreement or

other legislative documents are included in the

customs tariff as an amendment or annex.

(4) The General Directorate of Customs is responsible for

carrying out the tariff classification of goods

concerning description and coding in accordance with

the Harmonized System of the World Customs

Organization and for assessing any corresponding

duty under the Customs Tariff.

Article 24 (Valuation of Goods)

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 16 -

(1) The customs value of goods for the purpose of collecting customs debts

shall be determined by relevant customs in accordance with a separate

regulation.

(2) In order to combat false valuation of certain goods with suspicious

values, their minimum value shall be determined by General Directorate of

Customs in accordance with the relevant procedures.

A list of the goods mentioned above and specific values assigned to them

shall be published.

Article 25 (Exchange rate)

1. The value of goods according to legislation shall be

computed in Afghan currency.

2. When the value of goods is expressed in foreign

currency and there is need to determine customs

value, the exchange rate shall be determined in

accordance with the Da Afghanistan Bank exchange

rate.

(1) The exchange rate shall be [the rate] announced by

The Afghanistan Bank on the last working day of the

month and shall be valid for a period starting from the

6th day of every month and ending on the 6th day of

the following month.

(2) Whenever the exchange rate published by the Da

Afghanistan Bank differs by 5% or more from the

rate announced in accordance with paragraph (2) of

this article, a new rate will be provided and it shall be

effective from the second working day following its

announcement and notification to Customs as the rate

effective for the rest of that period.

Article 26 (perishable goods)

Customs value for perishable goods, at the request of the declarant, shall be

determined by the Director of Customs of the area [mahal] in accordance

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 17 -

with customs legislation, without applying the evaluation criteria established

for other goods

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 18 -

Chapter 5

FAVOURABLE TARIFF

Article 27 (cases for granting favourable tarrif)

(1) A favorable tariff shall be granted as provided in

customs legislation in accordance with Article 23(3),

and in the cases referred to in paragraph 2 of this

Article.

(2) The following import goods shall be exempted from

paying customs duty:

1- Goods imported by officials of the State during official

travels not in excess of Afs. 100,000 as provided by the

Customs tariff..

2- Office materials and equipments of political

representatives and International Agencies, materials

intended to be used in residency of representatives of

foreign countries in Afghanistan, after confirmation of

competent authorities.

3- Items intended for personal use by foreigners working

in Afghanistan according to the terms and conditions of

[their] contract.

4- Allowed books, gazettes, magazines and newspapers.

5- Goods provided for government projects funded by

loans or imported to the country by or for public and

private domestic, foreign, and International relief and

development agencies.

6- Personal effects used by Afghan delegations or Afghan

international workers and their family members abroad.

7- Travelers' personal goods in accordance with the

Customs Tariff.

8- Commercial samples and advertising gifts.

9- Post parcels valued at Afs 5000 or less.

10- honorary decorations or awards;

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 19 -

11- samples sent to organizations protecting

copyrights or industrial or commercial patent rights;

12- Used movable property belonging to natural

persons, who transfers their normal place of residence

from another country to Afghanistan, as provided in

the Customs Tariff;

13- a consignment of less than Afs 1000 value;

14- Pure-bred breeding animals and insects and laboratory

animals, biological or chemical substances needed for

scientific researches;

15- therapeutic substances of human origin and blood

grouping and tissue typing reagents,;

16- substances for the quality control of

medicinal products;

17- Fuels, lubricants and equipments related to transport

vehicles of goods, which are necessary for the normal

functioning of such vehicles, in accordance with the

relevant procedure.

18- Other goods may be included in exempted goods upon

recommendation of Ministry of Finance and approval of

Council of Ministers, as required.

Article 28 (request for favourable tariff)

(1) To obtain the benefits of a favorable tariff a declarant

may present a request before or after completion of

the customs process.

(2) If a favorable tariff is restricted to a certain volume of

imports, it ceases to be valid in the following

conditions:

1- quotas, when the stipulated limit on the volume of

imports is reached;

2- Tariff ceilings, according to specific provisions in the

relevant laws.

(3) The manner, and the conditions on which a

favourable tariff is granted, any quantitative or value-

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 20 -

based limits on imported goods or benefits based on

their origin, nature, or end-use, shall be determined in

a separate procedure.

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 21 -

CHAPTER 6

Origin of Goods

Article 29 (production of goods in a country)

(1) When goods are wholly originated or produced in a

country, that country shall be known as the origin of

those goods. Such goods includes:

1- mineral products extracted within that country;

2- vegetable products harvested therein;

3- live animals born and raised therein;

4- products derived from animals raised therein;

5- products of hunting or fishing carried on therein;

6- products of sea fishing and other products taken from

the sea outside a country’s territorial waters by vessels

flying the flag of that country and registered or recorded

therein;

7- goods obtained or produced from the products referred

to in sub-paragraph 6 of this article on board factory

ships which fly the flag of that country and are

registered or recorded therein;

8- products taken from the seabed or subsoil beneath the

seabed outside the territorial waters provided that the

country has exclusive rights to exploit that seabed or

subsoil;

9- waste and scrap products derived from manufacturing

operations and out of use articles, provided that they

were collected therein and are fit only for the recovery

of raw materials;

(2) Goods, which are obtained or produced wholly from

goods referred to in paragraph (1) of this Article, or

their derivatives at any stage of production.

Article 30 (Production of goods in more than one country)

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 22 -

Goods whose production involves more than one country shall be deemed to

originate from the country where they underwent their last substantial

processing [transformation].

Article 31(Certificate of origin)

(1) The manner of Certification of a document proving

the origin of goods shall be arranged in accordance

with a separate procedures.

(2) Certification of documents proving the origin of

goods may be issued by the responsible authorities for

the region in which the goods were produced.

(3) in case the custom authorities have doubt with regard

to a certificate of origin, such authorities may require

additional proofs ensuring that the documents of

origin comply with customs legislation.

(4) The procedure referred to in paragraph (1) of this

article shall provide the conditions under which a

country is considered as the origin of goods, which

shall be applied in the following cases:

1- to implement the Customs Tariff, excluding the

measures referred to in Article 23(2) of this law; [and]

2- To implement State measures restricting trade in

particular goods.

Article 32 (Preferential origin)

The preferential conditions for determination of the origin of goods for

purposes of taking advantage from the preferential facilities [measures]

contained in international agreements, as well as the method of issuing

certificates of preferential origin, shall be arranged in a separate procedures.

Article 33(return of goods)

(1) Afghan or non-Afghan goods that have been released

for free circulation in the State, which, after having

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 23 -

been exported there from, are then brought back into

the customs territory of the State are referred to as

“returned goods.” Returned goods which have been

processed outside of Afghanistan shall be subject to

the conditions of the process of outward processing.

(2) Goods which within three years of export are returned

to the customs territory of the State for purposes of

release for free circulation, shall at the request of the

person concerned be exempt from import duty. The

General Directorate of Customs may extend this

period in light of [special] circumstances;

(3) When, prior to their exportation from the customs

territory of the State, the returned goods had been

released for free circulation at a favorable tariff

because of their use for a particular purpose,

exemption from duty under paragraph 1 shall be

granted only if they are to be re-imported for the same

purpose.

(4) Any import duty paid on goods when they were first

released for free circulation shall be credited against

the amount of import duty chargeable when the same

goods are returned.

Chapter7

Presentation of Goods at Customs

Article 34 (Entry and Exit of Goods)

(1) The time of entry or exit is considered to take place

when goods, cross the State border to enter or leave

the customs territory of the State.

(2) The driver of a commercial means of transport

entering or leaving the customs territory of the State,

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 24 -

must submit to the customs a manifest of the goods

carried on the means of transport before the following

time:

1- the captain of an aircraft or vessel, when the goods can

be removed from the aircraft or vessel; [or]

2- any other means of transport, when the vehicle enters

into the customs territory of the State.

(3) A Manifest of Goods need not contain details about

the goods of travelers who are themselves required to

make a declaration under Article 45 of this law.

(4) A “Manifest of Goods” shall contain information

regarding the nationality, flag, and crew of the means

of transport, as well as all the information necessary

for the identification of the cargo, as provided for in a

separate procedures.

(5) Goods brought into the customs territory of the State

shall, at the time of their entry, be subject to customs

supervision and control by the customs. Such goods

shall not be moved without the permission of the

customs.

(6) Goods shall remain under customs control and

supervision until determination and effectuation of

their final customs designation.

Article 35 (Place for Presentation of Goods)

General Directorate of Customs may specify a place for Presentation of

goods and their transfer to customs. The time for completing such transfer

of imported goods from the border customs house to the approved place, and

the routes permitted therefore, shall be provided in a separate procedures.

Article 36 (Transportation Obstacles to Presentation of Goods)

(1) When, by reason of unforeseeable circumstances or

force majeure, the owner of goods can not transfer the

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 25 -

goods to the location specified in Article 35 of this

law, the owner of goods shall be obliged to inform the

customs authority of the situation.

(2) Where the unforeseeable circumstances or force

majeure do not result in total loss of the goods, such

person is also obliged to inform the customs of the

precise location of the goods.

(3) When by reason of unforeseeable circumstances or

force majeure, an aircraft is forced to enter or land

temporarily in the customs territory of the State, the

captain of his representative, shall be obliged to

report the situation immediately to the Customs .

(4) The customs shall be obliged to take the measures

necessary to enable the customs supervision of goods

mentioned in this Article, and that they are

subsequently conveyed to a customs office or other

designated places.

Article 37 (Presentation of Air shipments at airport of final

destination)

(1) When goods are brought into the customs territory of

the State from another country by air, and are

consigned under cover of a single transport document

by the same mode of transport to another airport in

Afghanistan, they shall be presented at customs,

without delay, at the airport where they are unloaded.

(2) Specific provisions regarding customs control,

supervision and other customs executions at the time

of entry and exit for goods from the customs territory

of the State are laid down in a separate procedure.

Article 38 (presenting manifests to customs)

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 26 -

(1) Aircrafts carrying imported or exported goods fly in

air corridors (dahlez hawai) designated, in accordance

with the Law of Civil Aviation, and must land and

take off only from international airports approved for

international flights.

(2) The captain of aircraft carrying goods and destined to

leave, must present customs officer the customs

declaration or manifest of goods on board to be

exported from the customs territory of the State. The

customs must verify that the goods so indicated in the

manifest of declaration correspond to those on board

the aircraft.

Article 39 (Customs Supervision on Aircraft )

(1) Aircraft, cabin, flight crew, travelers, crew luggage,

traveler baggage, and transported goods, except as

provided in Article 37(1), are subject to customs

supervision at the first airport of arrival in

Afghanistan.

(2) An airport authorized for international traffic in

accordance with Civil Aviation Law, is subject to

customs supervision.

(3) The Captain of an aircraft must, as soon as the aircraft

lands at an authorized airport, submit to the customs

office a manifest of all goods carried on the aircraft,

except for goods mentioned in Article 34(3) of this

Law.

(4) The provisions of paragraphs (1), (2) and (3) of this

article, shall also be applicable whenever an aircraft is

departing to a destination outside the country.

Article 40 (Exemption from obligation to present a manifest)

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 27 -

The following shall not present a manifest to the customs :

1- aircraft flying from one airport to another in

Afghanistan unless they have any stops at an airport

outside Afghanistan or transport goods subject to the

customs control and supervision;

2- private aircraft for personal use which is not carrying

goods subject to customs control and supervision

Article 41 (Aircraft’s forced landing)

If, in cases of emergency or force majeure, an aircraft has to land at an

airport not authorized for receiving international air traffic, the captain of the

aircraft must, immediately after landing and stopping, inform the nearest

customs authority, which shall place the aircraft, cabin, flight crew, travelers

and goods under customs supervision.

Article 42 (Customs declaration for postal goods)

(1) All postal goods containing consignments for

commercial purposes as well as postal goods

containing consignments of an aggregate value, for

each consignment exceeding the threshold value of

Afs 5000, or other value as may be provided in the

relevant regulations, are subject to a customs

declaration.

(2) Postal goods shall be accepted and delivered between

a foreign post office and the State’s Post office under

customs supervision. In case of consignments by

small package freight shippers, the General

Directorate of Customs may authorize immediate

release of goods under a security and upon submitting

the relevant declaration for all goods imported within

a fixed period of time, as provided by the Procedure.

(3) Postal shipments shall remain under customs

supervision while customs requirements are

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 28 -

completed in the post office. The Postal and Parcel

Directorate of Customs shall designate post offices

where the customs requirements may be completed.

Article 43 (exemption from declaration)

The following postal consignments are not subject to preparation and

presentation of declaration:

1- postcards and letters containing personal messages only;

2- printed matters not liable for import duty;

3- all other consignments sent by letter or parcel post,

which have no commercial value.

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 29 -

Article 44 (Export shipments)

Pursuant to export provisions of this Law and international regulations, the

Directorate of Customs may prescribe restrictions and special conditions on

postal shipments sent abroad.

Article 45 (Customs control on tranvelers luggage)

(1) When entering or leaving Afghanistan, a traveler is

obliged to declare the relevant consignments to

customs, and show them upon request.

(2) Customs may inspect the goods for the purpose of

verifying the correspondence of the declaration

mentioned in paragraph 1 of this article with the

consignment.

(3) Goods carried by diplomatic couriers, and certified in

written by their relevant agencies shall not be subject

to the provisions of Articles 42 to 44 of this law.

Article 46 ( presentation of goods from the determined location

to customs) Goods which arrive at the place for Presentation of goods at customs shall

be presented, without delay, except for delay due to no fault of the person

presenting the goods. Any person who makes a presentation of goods at

customs shall provide within the time limit prescribed any required

declaration, documents, or information, and shall provide all necessary

assistance as may be requested by the customs .

Article 47 (Goods verification and taking of samples)

(1) During presentation of goods at customs, the Customs

may take a sample of the goods, to assign them a

tariff classification, or customs designation. The

taking of samples may also be made at the request of

the owner of goods or his agent.

(2) The importer, exporter or agent shall be entitled to be

present when samples are taken, and when necessary,

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 30 -

the customs may oblige them to be present [during

such period];

(3) The sample shall be examined in a place designated

and during the time prescribed by the General

Directorate of Customs; where the samples are not

destroyed during the examination, they will be

returned to the owner or his agent, otherwise the

Customs shall not be liable for the payment of

compensation.

(4) The owner or agent responsible for the goods shall be

responsible to pay the cost of transferring to the

examination sites, unpacking, weighing, repacking

and any other operation involved in the sampling and

exanimation process.

Article 48 (Submission of a Summary declaration)

(1) The responsible person for goods shall submit a

summary declaration within one hour after the

presentation of goods at customs. The customs may

allow an additional period for submitting the

declaration, until the first working day following the

day of presentation of goods at customs.

(2) The customs shall be obliged to retain the summary

declaration. Goods entered in the summary

declaration will be placed in temporary storage

pending the presentation of a completed declaration.

(3) If a completed customs declaration has been

submitted, in accordance with the relevant Procedure,

prior to the expiry of the period referred to in

paragraph (1) of this article, the owner of the goods or

his representative shall not be obliged to submit a

summary declaration.

(4) The owner of the goods or his representative and

travelers shall not be required to file a summary

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 31 -

declaration for goods described in article 42 of this

law, unless this would jeopardize customs supervision

of the goods.

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 32 -

Article 49 (unloading and transshipping at designated sites)

(1) Goods shall be unloaded or transshipped from the

means of transport carrying them at designated places

with the permission of the customs, except where

there is imminent danger necessitating the immediate

unloading of all or part of the goods. In the latter

case, the owner of goods or his agent shall

immediately inform the customs.

(2) The customs may at any time require goods to be

unloaded and unpacked in order to inspect the goods

and their means of transport. The person who

introduced the goods or his agent shall be entitled to

be present while the goods are examined.

(3) The customs are obliged to notify their intention to

proceed with the examination to the person

responsible or his agent. If within two hours there is

no reply, the customs may proceed with the

examination of goods in their absence.

CHAPTER 8

TEMPORARY STORAGE OF GOODS

Article 50 (Places of temporary storage)

(1) From the moment of acceptance of the summary

declaration and until the time of acceptance of the

customs declaration referred to in Article 3(23) of this

Law, such goods shall be considered as “goods in

temporary storage”. Goods in temporary storage shall

be stored in customs areas or any other place

determined by the customs.

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 33 -

(2) Good referred to in paragraph (1) shall not be subject

to any form of handling. The provisions of article 47

of this law and such forms of handling as are

designed to ensure their preservation in the original

state (without modifying their appearance or technical

characteristics) shall be an exception to this rule.

(3) The customs may require the owner of the goods or

his agent to provide security with a view to [ensuring]

payment of any customs debt and fulfillment of his

obligations provided for by this law.

Article 51 (Removing goods from temporary storage)

(1) If the summary declaration is not submitted within the

periods determined in accordance with Article 48, the

Director General of Customs shall, taking into

account Article 54(3) of this law, without delay take

all measures necessary, including, after providing

notice to person responsible for goods, for the

purpose of sale of, or assigning a customs

designation for, the goods left at customs, in

accordance with the relevant procedure.

(2) The customs may, at the expense of the owner of the

goods, transfer the goods mentioned in paragraph (1)

of this Article to a place which is under customs

supervision, and keep them there until a

determination is made concerning the sale or customs

designation of the goods.

Article 52 (Non-allowed Goods )

(1) When it shall be established that goods are smuggled,

according to the provisions of this law, customs, in

such cases may upon final decision by a responsible

authority, take necessary measures for sale or other

authorized action with respect to the goods.

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 34 -

(2) Goods that are prohibited in accordance with 53(2)

shall be seized by customs, and treated in accordance

with Paragraph (1) of this Article.

(3) Customs, upon request of the holder of a trademark or

patent or other proprietary rights in accordance with

the relevant procedures, may prohibit the release into

free circulation, and the exportation of goods,

provided that they are recognized in accordance with

applicable Law to be counterfeited or pirated goods.

Chapter 9

CUSTOMS DECLARATION

Article 53 (assigning a customs designation for non-afghan goods)

(1) Customs are obliged to assign a customs designation

for Non-Afghan goods presented at customs in

accordance with customs legislation.

(2) Customs may, for reasons of public morality, public

security, protection of environment, health and life of

humans, animals or plants, the protection of national

treasures possessing artistic, historic or archaeological

value or the protection of industrial and commercial

property and other state policies , may adopt

prohibitions or restrictions in accordance with

relevant legislative documents.

Article 54 (Time period for completing customs declaration)

(1) The declarant is obliged to complete customs

declaration within 5 days from the date on which the

summary declaration is submitted.

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 35 -

(2) Where circumstances so warrant the customs may set

a shorter period or authorize an extension of the

periods referred to in paragraph 1 of this Article.

(3) The temporary storage period shall be 30 days and

terminate at any time that duties, storage and other

obligations accrued under this law equal the value of

the goods. In no event shall the period be extended in

the absence of presenting justifying reasons, by the

responsible customs authority to the General

Directorate of Customs.

Article 55 (Declaration of the goods for a customs process)

(1) A request to place goods under an initial customs

process or for release of goods shall be made in the

customs declaration.

(2) The customs declaration made in accordance with the

requirements of customs in one of the following

means shall be acceptable:

1- In writing ; or

2- by an oral declaration

3- using data-processing techniques; or

4- any other act by which the person responsible for the

goods expresses his wish to place goods under a

Customs designation or process

(3) The customs declaration shall be accompanied by the

customs documents required in accordance with the

relevant procedure governing the related customs

designation or process.

Article 56 (Acceptance of the declaration)

(1) Declarations, which are prepared or submitted by the

person responsible for goods in compliance with the

Draft 2.1 Sept 29, 2004

109Rob Hager, Legal & Regulatory, AEGP

- 36 -

conditions laid down in Article 55, shall be accepted

by the customs without delay, provided that the goods

to which they refer are available for customs

inspection.

(2) Where acceptance of a customs declaration requires

the fulfillment of additional obligations by persons,

such person shall sign it upon being required by

customs to do so.