Customer Identification Program & Customer Due Diligence ...

13

Customer Identification Program & Customer Due Diligence/Account Due Diligence 1

Transcript of Customer Identification Program & Customer Due Diligence ...

Customer Identification Program &

Customer Due Diligence/Account Due Diligence

1

Introduction to the Bank Secrecy Act (BSA)Per the Financial Crimes Enforcement Network (FinCEN), “The Bank Secrecy Act (BSA) requires U.S. financial institutions to assist U.S. government agencies to detect and prevent money laundering. Specifically, the act requires financial institutions to keep records of cash purchases of negotiable instruments, file reports of cash transactions exceeding $10,000 and to report suspicious activity that might signify money laundering, tax evasion or other criminal activities.”

The BSA Department was established to comply with the regulatory guidelines created by the BSA/AML legislation.

The BSA Department oversees many functions of the Bank, such as the Customer Identification Program (CIP), Customer/Account Due Diligence (CDD/ADD), Beneficial Ownership, Currency Transaction Reports (CTRs), etc.

2 2

Customer Identification Program (CIP)

Section 326 of the USA PATRIOT Act requires each bank to implement a written CIP. The CIP is intended to enable the bank to form a reasonable belief that it knows the true identity of each customer.

At a minimum, the Bank must obtain the following identifying information from each customer before opening the account:

•Name

•Date of Birth

•Physical Address (A PO Box is NOT Acceptable)

•Identification number (SSN, ITIN, EIN)

3 3

The CIP Verification ProcessThe information provided by the customer will be verified using the following:

❑ Primary Identification (legible copies!)

❑ Secondary Identification

❑ E-Funds

❑ CIF – Completion of ID Fields

❑ ASK QUESTIONS!!!

✓ For Existing Clients: ALWAYS verify whether the identification on file is current/unexpired when opening a new account or loan. Update records as needed.

✓ The client’s name and address must match the ID provided exactly. The account should not be opened until the discrepancy has been resolved.

✓ Refer to the CIP Program and Customer Identification Program Verification of Identification for New Bank Clients for scenario specific details of acceptable documents.

Please Note: If the customer refuses to provide the required documentation, or if the documentation contains discrepancies, the account should NOT be opened.

4 4

CIP Requirements❑ The client’s name and address must match the ID provided exactly. The client’s name must be consistent on each document.

❑ For Existing Clients: Always verify whether the identification on file is current/unexpired when opening a new account orloan. Update records as needed.

❑ Non US Persons:

o Must have a Tax Identification Number (TIN) or Individual Taxpayer Identification Number (ITIN) in order to open anaccount.

o Must present two forms of primary identification, with at least one documenting their country of citizenship.

❑ The following businesses require pre-approval from the BSA Department and Account Services prior to account opening:

o Money Service Business

o Convenience Store/Gas Station

o Privately Owned ATM Client

o Foreign/Offshore/Out of State Entity

o Higher Risk Charity/Non-Governmental Organization (NGO) – Operates or provides services outside of the US.

5 5

Red Flags/Suspicious Activity▪ Reluctance to provide information or provides insufficient information

▪ Discrepancies in the information provided (variance in name, date of birth, address, etc.)

▪ E-Funds indicates Social Security Number issued prior to the individual’s date of birth or inactive due to death.

▪ E-Funds Address Alert: Watch for a “non-residential” alert. A PO Box, lock box or mail stop are not acceptable.

▪ E-Funds indicates multiple inquiries in a short period of time.

▪ ID documents appear to have been altered or not in the legal format for the specific document being provided.

▪ A Driver Authorization Card is NOT acceptable as a primary form of Identification. In addition, IDs that state “Not For Federal Purposes” or “Not Valid Identification” are NOT acceptable.

▪ Example:

6 6

Red Flags/Suspicious Activity Cont.

Suspicious Activity Referral Form (SARF) – Submit a SARF for any suspicious or questionable activity. The form can be found on the front page of the Intranet. DO NOT email the Fraud and Disputes mailbox or the Compliance mailbox. The SARF should go directly to the BSA Officer or to a BSA Compliance Specialist, as this information is highly confidential. Call the BSA Department with any questions/concerns.

Willful Blindness - Deliberate avoidance of knowledge of the facts or purposeful indifference. For example, a person may not have been aware of the violation, but their lack of awareness was the result of a choice.

✓Courts have held that willful blindness is the equivalent of actual knowledge of the illegal source of funds or of the intentions of a customer in a money laundering transaction.

7 7

Customer Due Diligence (CDD) & Account Due Diligence (ADD)

The CDD/ADD enables the Bank to predict with relative certainty the types of transactions in which a client is likely to engage.The information collected is used to assess the risks associated with each client and to recognize and report suspicious activity.CDD/ADD also assists account officers with building client relationships and cross selling opportunities. Effective policies andprocedures enable the Bank to comply with regulatory requirements.

✓ CDD/ADD is required for all new CIF’s. Don’t be afraid to ask questions or to have the client clarify a response! It’s important to get all the information up front, so that we don’t have to reach out later, due to an insufficient response.

✓ CDD/ADD must be updated for existing client(s) if any information has changed or if a new account is opened. All fields are required.

✓ Be as descriptive as possible. The BSA Department relies on the accuracy of this information to assess risk, complete reviews and to report suspicious activity.

✓ The BSA Designee works with the BSA Department and follows up with CDD/ADD for all new CIFs and new accounts for existing customers.

A positive attitude and customer service oriented responses will ensure a smooth process.

8 8

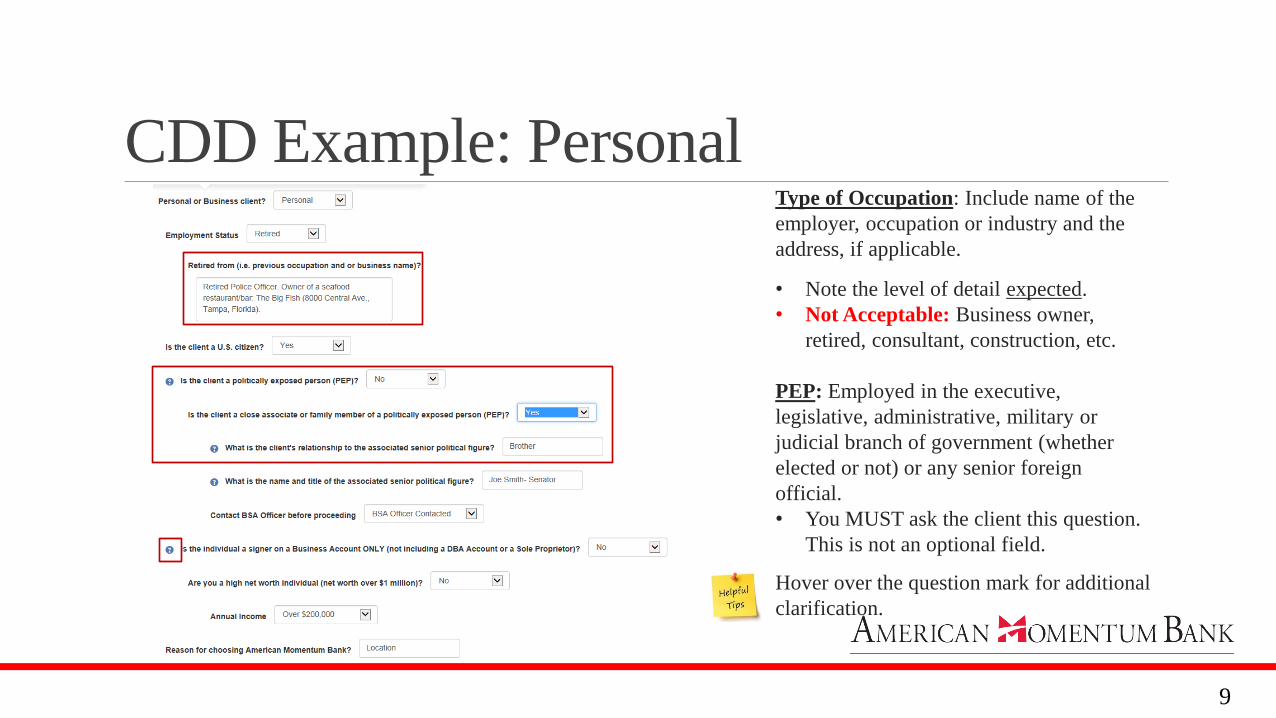

CDD Example: PersonalType of Occupation: Include name of the

employer, occupation or industry and the

address, if applicable.

• Note the level of detail expected.

• Not Acceptable: Business owner,

retired, consultant, construction, etc.

PEP: Employed in the executive,

legislative, administrative, military or

judicial branch of government (whether

elected or not) or any senior foreign

official.

• You MUST ask the client this question.

This is not an optional field.

Hover over the question mark for additional

clarification.

9 9

CDD Example: Business

• Nature of the Business: Note the detail

• Professional Service Provider: Acts as intermediary between client and the bank and may conduct financial dealings for their clients. (E.g. Lawyer, accountant, investment broker, etc.)

• Estimated Annual Sales aka Annual Revenue: Insert the dollar amount of sales or revenue (eg. 40,000). Do not use 40.

• A “Yes” response to the following will require BSA Approval prior to account opening.

• MSB

• Privately Owned ATM

• PEP

• High Risk NGO

• Transact with MRBs

• Manufacture/Distribute/Sell Hemp or CBD related products

10 10

ADD Example: PersonalEstimated Monthly Averages

• This information should be provided by the client. Associates should not be filling this section out using their “best guess”.

• “Other” Box: Should include transaction types not already listed.

• Describe the “Other” activity in either text box.

Account Purpose: The type of activity we should expect to see in the account.

◦ Do not input the nature of the business in this section.

Types of Deposits: Be as clear/specific as possible.

Reminder: Verify dollar amount and volume are in the correct box. Please do not transpose these numbers.

11 11

ADD Example: BusinessAccount Purpose: Activity in which the client is likely to engage IN DETAIL.

◦ Example: To receive rental payments from tenants, make payments to suppliers, payroll and general business expenses.

Monthly Averages: The client should be able to provide an estimate of their expected monthly activity.

12 12

BSA Contact Information

For BSA/AML related assistance, please contact the BSA Department by:

• “Compliance Associates” email group

•Phone

• Extension #3025

• (813)549-4756

1316