Customer Engagement Study - Ausgrid/media/Files/Network/Planning for the... · 3 Customer...

88

Customer Engagement Study Prepared for: Ausgrid July 2013

Transcript of Customer Engagement Study - Ausgrid/media/Files/Network/Planning for the... · 3 Customer...

Customer Engagement Study Prepared for: Ausgrid July 2013

2

Customer Engagement Study July 2013

1. Contents

1. Background ........................................................................................................................ 3

2. Key Objectives and Areas of Coverage ............................................................................... 4

3. Research Design ................................................................................................................. 6

3.1 Qualitative Research Design ............................................................................................ 6

3.2 Quantitative Research Design .......................................................................................... 7

4. Main Findings................................................................................................................... 11

4.1 Awareness of Ausgrid .................................................................................................... 11

4.3 Safety ............................................................................................................................ 19

4.4 Construction/Design Standards ..................................................................................... 23

4.6 Connection Fees ............................................................................................................ 30

4.7 Energy Efficiency Programs ............................................................................................ 32

4.8 Demand Management ................................................................................................... 35

4.9 Metering Technology ..................................................................................................... 40

4.10 Awareness and Perceptions of Time Based Pricing ...................................................... 47

4.11 Communication and Engagement ................................................................................ 50

4.12 Support for Vulnerable Households ............................................................................. 51

5. Conclusions ...................................................................................................................... 54

APPENDICES…………………………………………………………………………………………………………………………..62

3

Customer Engagement Study July 2013

1. Background

Ausgrid is a state owned corporation whose shareholder is the New South Wales Government. The Ausgrid electricity network provides power to 1.6 million homes and businesses throughout Sydney, the Hunter and the Central Coast.

On 2 March 2011 EnergyAustralia changed its name to Ausgrid, after selling the retail part of its business. Ausgrid has continued to work to provide a safe and reliable electricity network for its customers, both in Sydney and north of the Hawkesbury River.

Ausgrid aims to be a leader in distributing electricity and providing energy services and its main activities include:

• asset ownership and management of the electricity distribution and transmission network;

• infrastructure related construction and maintenance services; • a range of other services, including street lighting, safety check-ups, energy reviews;

and, • metering and 24-hour electrical repairs.

Ausgrid will deliver these activities ensuring that:

• its network is safe and reliable; • its customers value its service; • its staff are proud to work there; and, • its community recognises its values, contributions, citizenship and achievements.

To ensure customer needs, perceptions and preferences are fully understood and to allow a focus on areas where changes can be made and forecasted for, Ausgrid plans to carry out a number of customer engagement activities during 2013.

A part of that customer engagement has involved a large scale consumer and small to medium enterprise qualitative and quantitative research study, gauging satisfaction levels, and perceptions across a range of aspects. This report contains the findings of that research.

4

Customer Engagement Study July 2013

2. Key Objectives and Areas of Coverage This research allowed for sensitive exploration of all of the issues that may be impacting on customers’ perceptions, as well as accurate measurement of the prevalence of these views amongst the customer bases. It involved sensitive qualitative consultation with groups of customers from the various expenditure/usage and income segments, followed by a quantification of the key findings emerging from the qualitative exploration amongst a robust sample of customers across the Ausgrid footprint. The areas of investigation included the following broad areas: 1. Reliability Customer perceptions and experiences regarding power interruptions, their frequency

and duration, and the communication required before, during and after outages; The relationship between reliability and price, and customers willingness to pay to

achieve minimal disruptions; and,

2. Pricing Exploration of perceptions surrounding pricing and the recent increases; The degree to which appliance use and purchase has been impacted as a result, and

the extent to which this is impacted by seasons and temperatures; Future changes/behaviours if price were to remain constant; and, Exploration of reactions to pricing options which reflects costs.

3. Construction/design standards Views regarding connection costs and equity in connection pricing; Customer feelings regarding aspects surrounding construction including the role of

aesthetics and overground/underground options; The perceptions regarding environmental and safety considerations and options; and, Willingness to pay for construction options, and attitudes about a contribution to

connection costs

4. Metering Technology Attitudes towards advanced metering and the perceived value of the various features

of it, such as access to real time information, remote reading and time-based pricing; Willingness to pay for access to the technology

5

Customer Engagement Study July 2013

5. Demand Management/energy efficiency Customer attitudes toward a range of energy efficiency initiatives; Comprehension of and reactions to demand management initiatives; and, Willingness to pay for efficiency and demand management programs.

6. Support for vulnerable households Feelings regarding the support of vulnerable customers, and where responsibility

should lie; Levels of support felt necessary; Views regarding which segments of the community should receive support; and, The extent to which customers are prepared to pay to help ensure this support can be

provided.

7. Communication and Engagement Exploration of customer needs and wants with regard to information provided by

Ausgrid and the level of communication engagement and involvement felt optimal; and,

Ratings of information provided currently with regard to transparency, timeliness, extent of coverage and ease of understanding;,

The above areas of investigation were explored in relation to any individual income/usage segments, and trends or patterns across age, gender, household type and location.

6

Customer Engagement Study July 2013

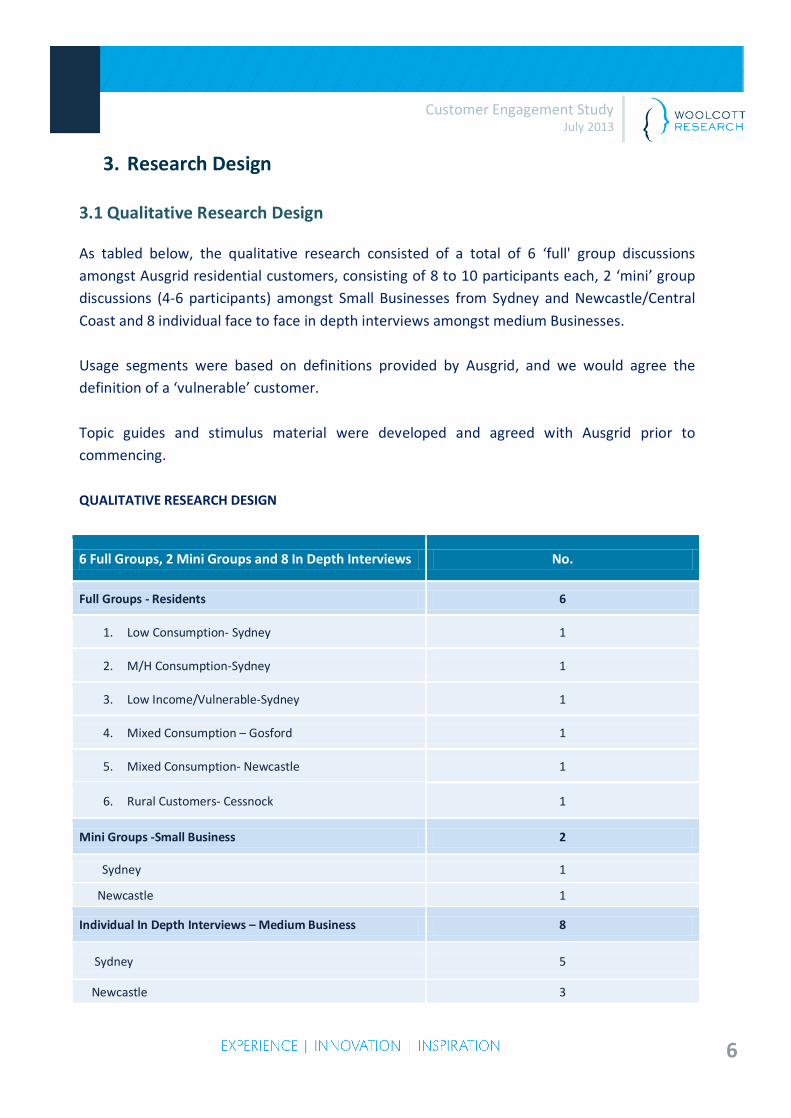

3. Research Design 3.1 Qualitative Research Design As tabled below, the qualitative research consisted of a total of 6 ‘full' group discussions amongst Ausgrid residential customers, consisting of 8 to 10 participants each, 2 ‘mini’ group discussions (4-6 participants) amongst Small Businesses from Sydney and Newcastle/Central Coast and 8 individual face to face in depth interviews amongst medium Businesses. Usage segments were based on definitions provided by Ausgrid, and we would agree the definition of a ‘vulnerable’ customer. Topic guides and stimulus material were developed and agreed with Ausgrid prior to commencing. QUALITATIVE RESEARCH DESIGN

6 Full Groups, 2 Mini Groups and 8 In Depth Interviews No.

Full Groups - Residents 6

1. Low Consumption- Sydney 1

2. M/H Consumption-Sydney 1

3. Low Income/Vulnerable-Sydney 1

4. Mixed Consumption – Gosford 1

5. Mixed Consumption- Newcastle 1

6. Rural Customers- Cessnock 1

Mini Groups -Small Business 2

Sydney 1

Newcastle 1

Individual In Depth Interviews – Medium Business 8

Sydney 5

Newcastle 3

7

Customer Engagement Study July 2013

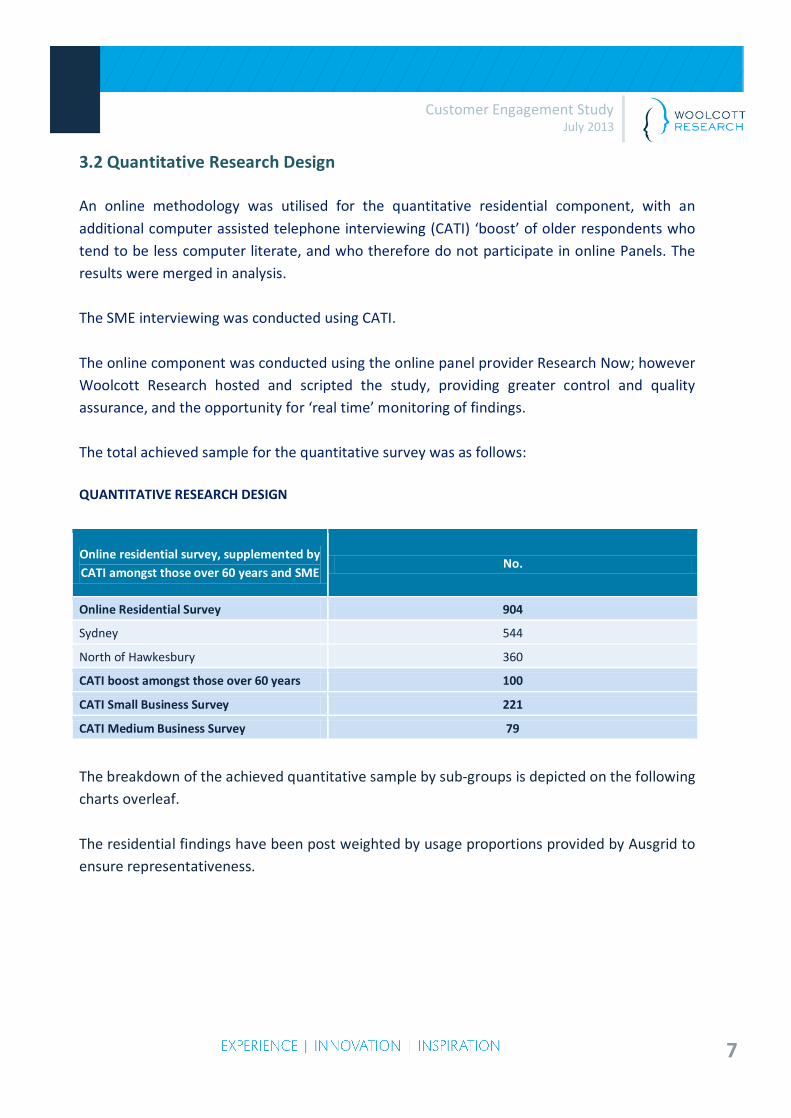

3.2 Quantitative Research Design An online methodology was utilised for the quantitative residential component, with an additional computer assisted telephone interviewing (CATI) ‘boost’ of older respondents who tend to be less computer literate, and who therefore do not participate in online Panels. The results were merged in analysis. The SME interviewing was conducted using CATI. The online component was conducted using the online panel provider Research Now; however Woolcott Research hosted and scripted the study, providing greater control and quality assurance, and the opportunity for ‘real time’ monitoring of findings. The total achieved sample for the quantitative survey was as follows: QUANTITATIVE RESEARCH DESIGN

Online residential survey, supplemented by CATI amongst those over 60 years and SME

No.

Online Residential Survey 904

Sydney 544

North of Hawkesbury 360

CATI boost amongst those over 60 years 100

CATI Small Business Survey 221

CATI Medium Business Survey 79

The breakdown of the achieved quantitative sample by sub-groups is depicted on the following charts overleaf. The residential findings have been post weighted by usage proportions provided by Ausgrid to ensure representativeness.

8

Customer Engagement Study July 2013

Residential sample breakdown:

Residential (n=904)

%

Employment Status:

Employed full-time 35

Employed part-time 15

Employed casual 5

Not employed, but looking for work 3

Home duties 9

Retired 28

Other 4

Refused 1

No. in Household:

0 4

1 19

2 35

3 16

4 16

5 6

6+ 3

Residential

(n=904) %

Gender:

Male 45

Female 55

Age:

18-24 6

25-34 17

35-44 16

45-54 16

55-59 10

60-64 13

65+ 22

Dwelling Status:

Own/paying off home 70

Rent (lease in name) 24

Rent (lease not in name) 7

9

Customer Engagement Study July 2013

Residential sample breakdown (cont.):

Residential

(n=904) %

Household Make Up:

Young single/couple 14

Family with at least one child

under 15 24

Family with children 15 and

over only still living at home 9

Family with older children

(who may have left home) 17

Mature single/couple 33

Other 3

Household Classified as Vulnerable:

Yes 13

No 87

Residential

(n=904) %

Responsible for Electricity Bill:

Yes 93

No 7

Average Electricity Bill per Quarter:

Under $350 per quarter 43

Between $351 -$750 per

quarter 51

Over $751 per quarter 6

Household Income Bracket:

Under $800 per week 31

$800-$1,200 per week 29

Over $1,200 per week 31

Refused 9

10

Customer Engagement Study July 2013

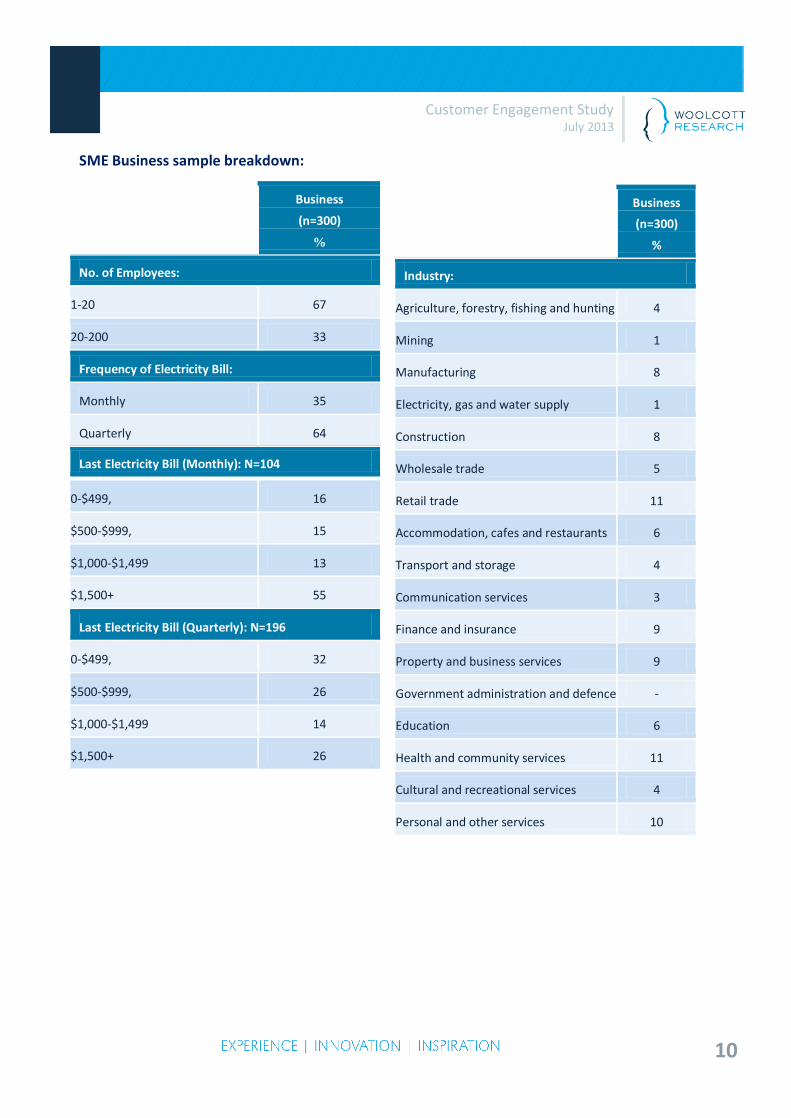

SME Business sample breakdown:

Business

(n=300)

%

Industry:

Agriculture, forestry, fishing and hunting 4

Mining 1

Manufacturing 8

Electricity, gas and water supply 1

Construction 8

Wholesale trade 5

Retail trade 11

Accommodation, cafes and restaurants 6

Transport and storage 4

Communication services 3

Finance and insurance 9

Property and business services 9

Government administration and defence -

Education 6

Health and community services 11

Cultural and recreational services 4

Personal and other services 10

Business

(n=300)

%

No. of Employees:

1-20 67

20-200 33

Frequency of Electricity Bill:

Monthly 35

Quarterly 64

Last Electricity Bill (Monthly): N=104

0-$499, 16

$500-$999, 15

$1,000-$1,499 13

$1,500+ 55

Last Electricity Bill (Quarterly): N=196

0-$499, 32

$500-$999, 26

$1,000-$1,499 14

$1,500+ 26

11

Customer Engagement Study July 2013

4. Main Findings

4.1 Awareness of Ausgrid To assess the level and depth of awareness of Ausgrid, at the beginning of the qualitative research participants were asked whether they knew of Ausgrid prior to that day. The responses indicated there was relatively high awareness of Ausgrid when prompted, however few knew very much about the organisation and its role in any depth. Most of those aware had just heard the name. Some had seen Ausgrid workers in the street, upgrading, digging, or changing power poles, but there was very little awareness of any detail beyond that. Some questioned whether Ausgrid was partly private or Government owned.

“Who owns them? Macquarie Bank??”

A minority had heard that there was talk of privatisation of Ausgrid, and there was some low level awareness that Ausgrid used to be EnergyAustralia, however overall there was a lot of confusion about the roles of the distributor versus the retailers. Overall most in the qualitative research felt that the ‘relationship’ they had was with the retailer only, and the retailer was generally the organisation they thought of in regard to who to call if there was a blackout or problem with supply. Also the retailer sent the bill each quarter and therefore participants clearly saw themselves as ’customers’ of the retailers, rather than the distributor. At the beginning of the qualitative discussions, as soon as it became clear the groups were about energy, recent price rises were immediately and spontaneously raised, in an emotional and somewhat vexed manner. The majority did not understand why there had been recent price rises and where exactly they had come from. Some participants linked them with the Carbon Tax, some with upgrading as a result of previous neglect. There was quite a wide ranging assumption that all energy companies, including Ausgrid were trying to make as much money as possible (for shareholders if they assume it is a private company) or for the government.

“Our usage has gone down but our bill has gone up.”

12

Customer Engagement Study July 2013

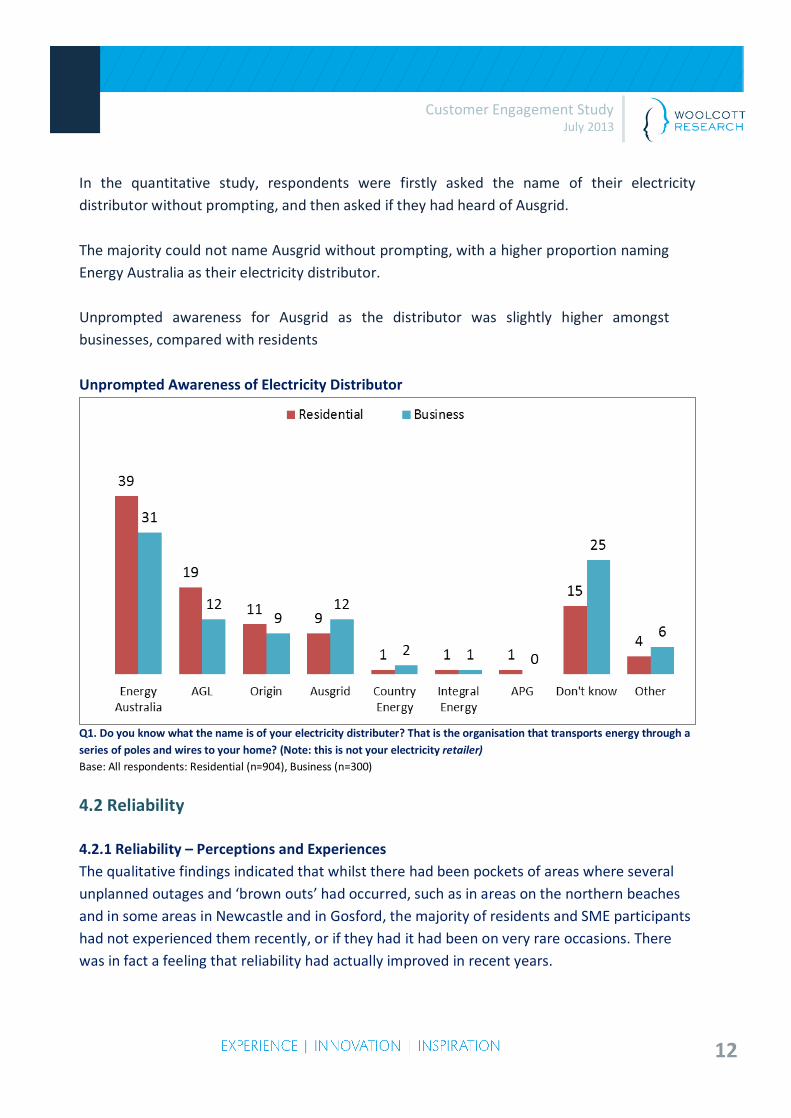

In the quantitative study, respondents were firstly asked the name of their electricity distributor without prompting, and then asked if they had heard of Ausgrid. The majority could not name Ausgrid without prompting, with a higher proportion naming Energy Australia as their electricity distributor. Unprompted awareness for Ausgrid as the distributor was slightly higher amongst businesses, compared with residents Unprompted Awareness of Electricity Distributor

Q1. Do you know what the name is of your electricity distributer? That is the organisation that transports energy through a series of poles and wires to your home? (Note: this is not your electricity retailer) Base: All respondents: Residential (n=904), Business (n=300)

4.2 Reliability 4.2.1 Reliability – Perceptions and Experiences The qualitative findings indicated that whilst there had been pockets of areas where several unplanned outages and ‘brown outs’ had occurred, such as in areas on the northern beaches and in some areas in Newcastle and in Gosford, the majority of residents and SME participants had not experienced them recently, or if they had it had been on very rare occasions. There was in fact a feeling that reliability had actually improved in recent years.

13

Customer Engagement Study July 2013

When outages had occurred, it appeared that the power was generally not interrupted for very long, and so outages were no longer considered a big inconvenience, even for the small to medium businesses.

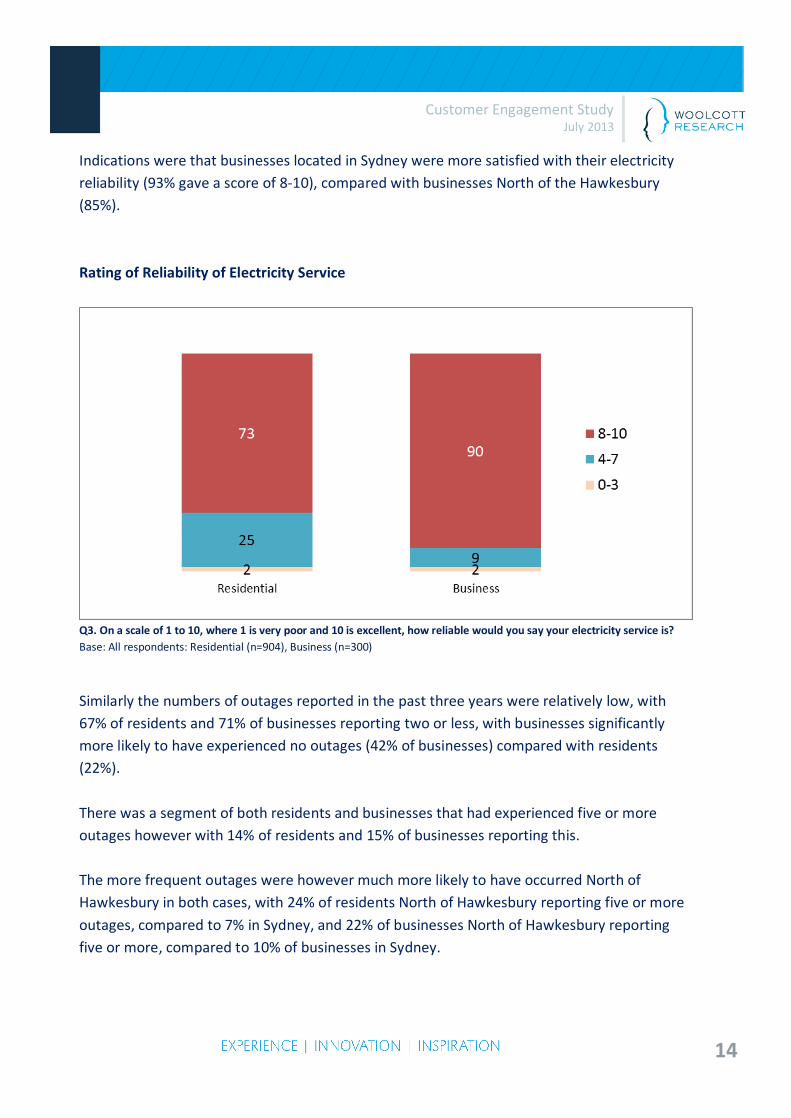

“If it does happen it can be fun. The kids have the candles etc.” Usually the cause for the unplanned outage was assumed to be beyond the distributor’s control, and caused by things such as car crashes or trees and branches coming down on power lines. When there was an outage, those affected initially assessed whether it was just their house or business, or the whole of the street or neighbourhood. After a certain length of time (usually around one or two hours) some would ring their retailer to find out when the power was expected to return, whilst others just waited or asked the neighbours if they knew what was happening. Few of those who had been affected wanted to know very much information about the outage and those who rang the retailer felt that they generally found out all they needed to know. Most only wanted to know when the electricity would come back on, with a minority wanting to know the reason for the outage just to reassure them that there were no serious issues. When ringing a retailer for information a recorded message which provided an estimate of when the electricity would return was felt to be sufficient. The idea of an SMS sent to those affected by an outage was tested in the qualitative research, and the majority felt that this was a very positive idea, however it was felt this should just be one of the sources of information, with others being media commentary or a proactive landline phone call to those without a mobile. For a pre-planned power interruption it was expected a warning by letter or a card would be provided on site, such as under the door, with information about when it would happen and for how long. Most reported that this was usually already provided. In the quantitative research the majority of respondents gave a very high score (of 8-10) for the reliability of their electricity service. Businesses in particular gave a significantly higher rating of scores 8-10.

14

Customer Engagement Study July 2013

Indications were that businesses located in Sydney were more satisfied with their electricity reliability (93% gave a score of 8-10), compared with businesses North of the Hawkesbury (85%). Rating of Reliability of Electricity Service

Q3. On a scale of 1 to 10, where 1 is very poor and 10 is excellent, how reliable would you say your electricity service is? Base: All respondents: Residential (n=904), Business (n=300)

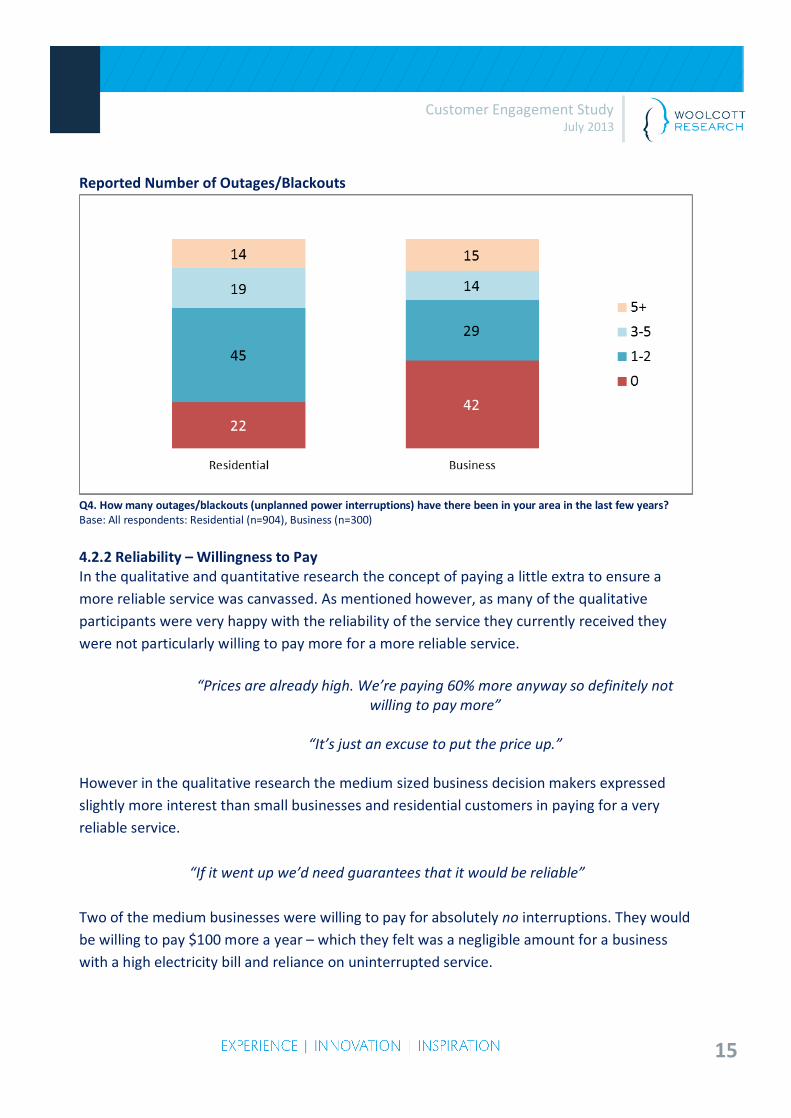

Similarly the numbers of outages reported in the past three years were relatively low, with 67% of residents and 71% of businesses reporting two or less, with businesses significantly more likely to have experienced no outages (42% of businesses) compared with residents (22%). There was a segment of both residents and businesses that had experienced five or more outages however with 14% of residents and 15% of businesses reporting this. The more frequent outages were however much more likely to have occurred North of Hawkesbury in both cases, with 24% of residents North of Hawkesbury reporting five or more outages, compared to 7% in Sydney, and 22% of businesses North of Hawkesbury reporting five or more, compared to 10% of businesses in Sydney.

15

Customer Engagement Study July 2013

Reported Number of Outages/Blackouts

Q4. How many outages/blackouts (unplanned power interruptions) have there been in your area in the last few years? Base: All respondents: Residential (n=904), Business (n=300)

4.2.2 Reliability – Willingness to Pay In the qualitative and quantitative research the concept of paying a little extra to ensure a more reliable service was canvassed. As mentioned however, as many of the qualitative participants were very happy with the reliability of the service they currently received they were not particularly willing to pay more for a more reliable service.

“Prices are already high. We’re paying 60% more anyway so definitely not

willing to pay more”

“It’s just an excuse to put the price up.”

However in the qualitative research the medium sized business decision makers expressed slightly more interest than small businesses and residential customers in paying for a very reliable service.

“If it went up we’d need guarantees that it would be reliable” Two of the medium businesses were willing to pay for absolutely no interruptions. They would be willing to pay $100 more a year – which they felt was a negligible amount for a business with a high electricity bill and reliance on uninterrupted service.

16

Customer Engagement Study July 2013

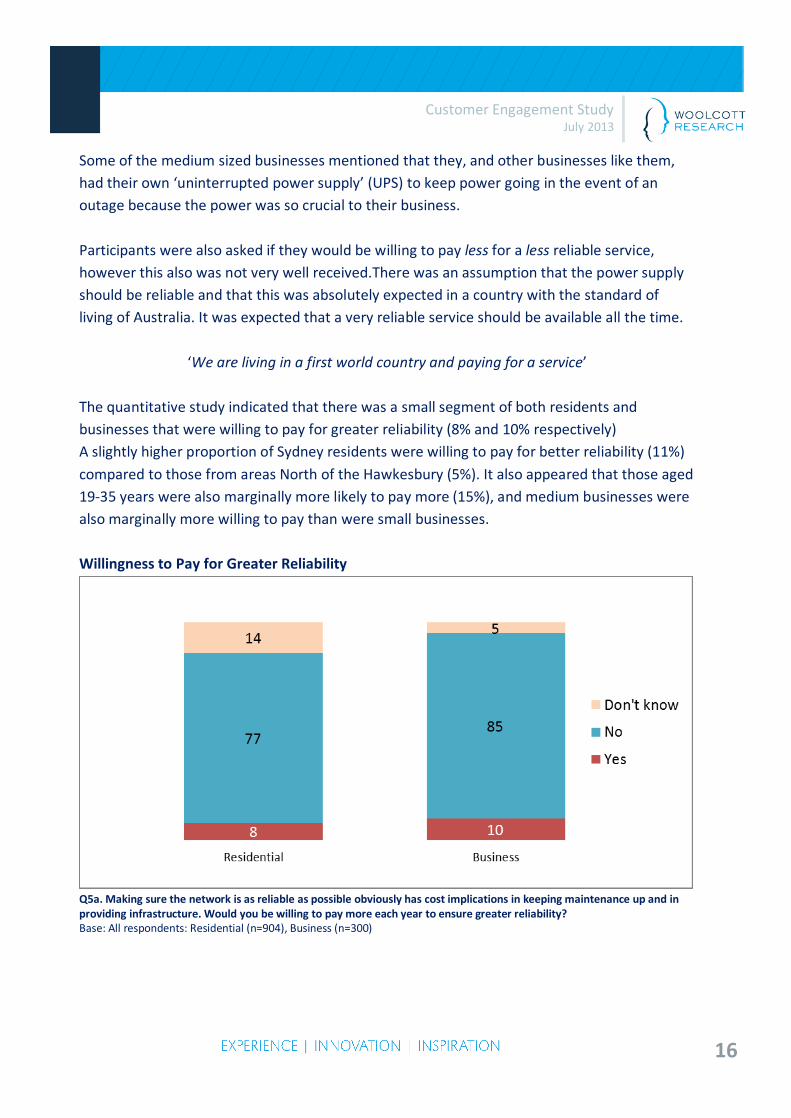

Some of the medium sized businesses mentioned that they, and other businesses like them, had their own ‘uninterrupted power supply’ (UPS) to keep power going in the event of an outage because the power was so crucial to their business. Participants were also asked if they would be willing to pay less for a less reliable service, however this also was not very well received.There was an assumption that the power supply should be reliable and that this was absolutely expected in a country with the standard of living of Australia. It was expected that a very reliable service should be available all the time.

‘We are living in a first world country and paying for a service’ The quantitative study indicated that there was a small segment of both residents and businesses that were willing to pay for greater reliability (8% and 10% respectively) A slightly higher proportion of Sydney residents were willing to pay for better reliability (11%) compared to those from areas North of the Hawkesbury (5%). It also appeared that those aged 19-35 years were also marginally more likely to pay more (15%), and medium businesses were also marginally more willing to pay than were small businesses. Willingness to Pay for Greater Reliability

Q5a. Making sure the network is as reliable as possible obviously has cost implications in keeping maintenance up and in providing infrastructure. Would you be willing to pay more each year to ensure greater reliability? Base: All respondents: Residential (n=904), Business (n=300)

17

Customer Engagement Study July 2013

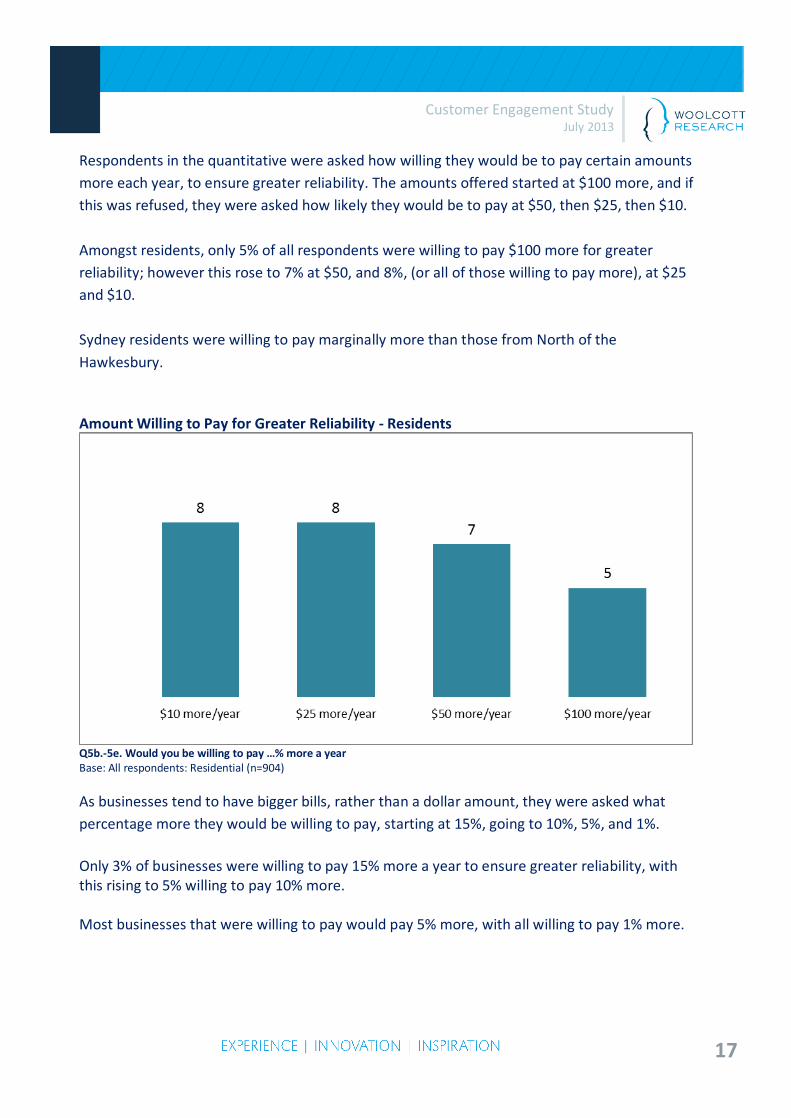

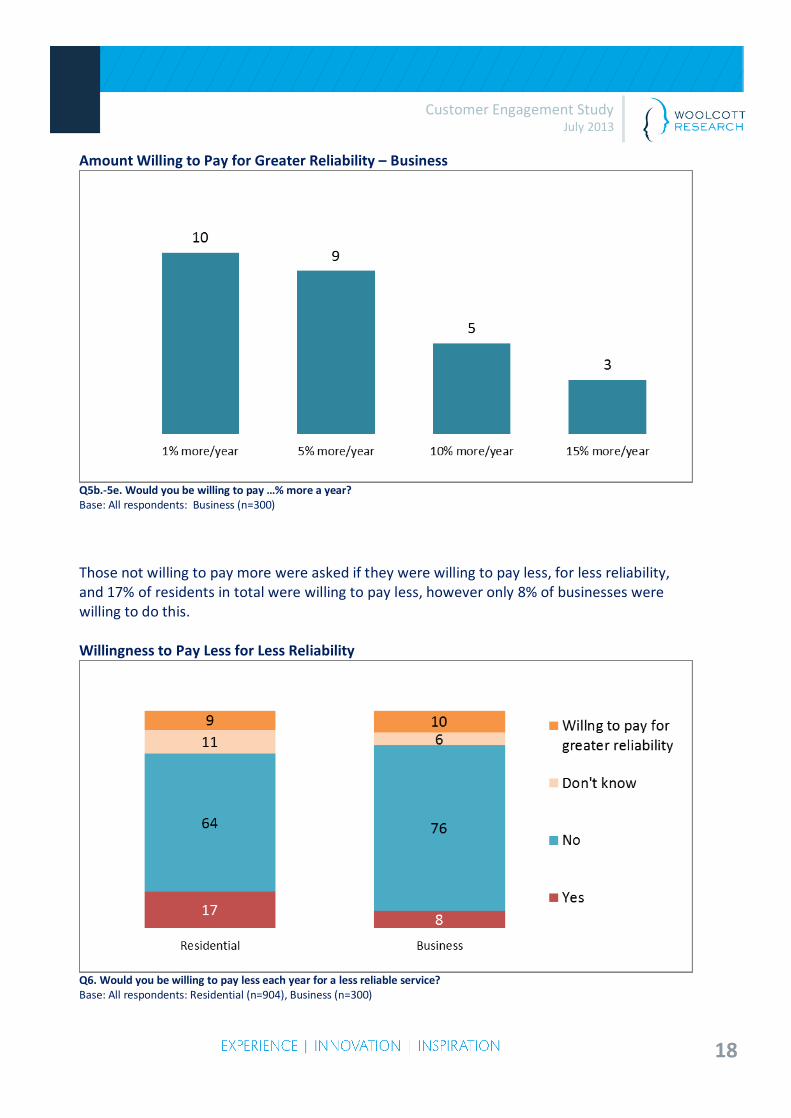

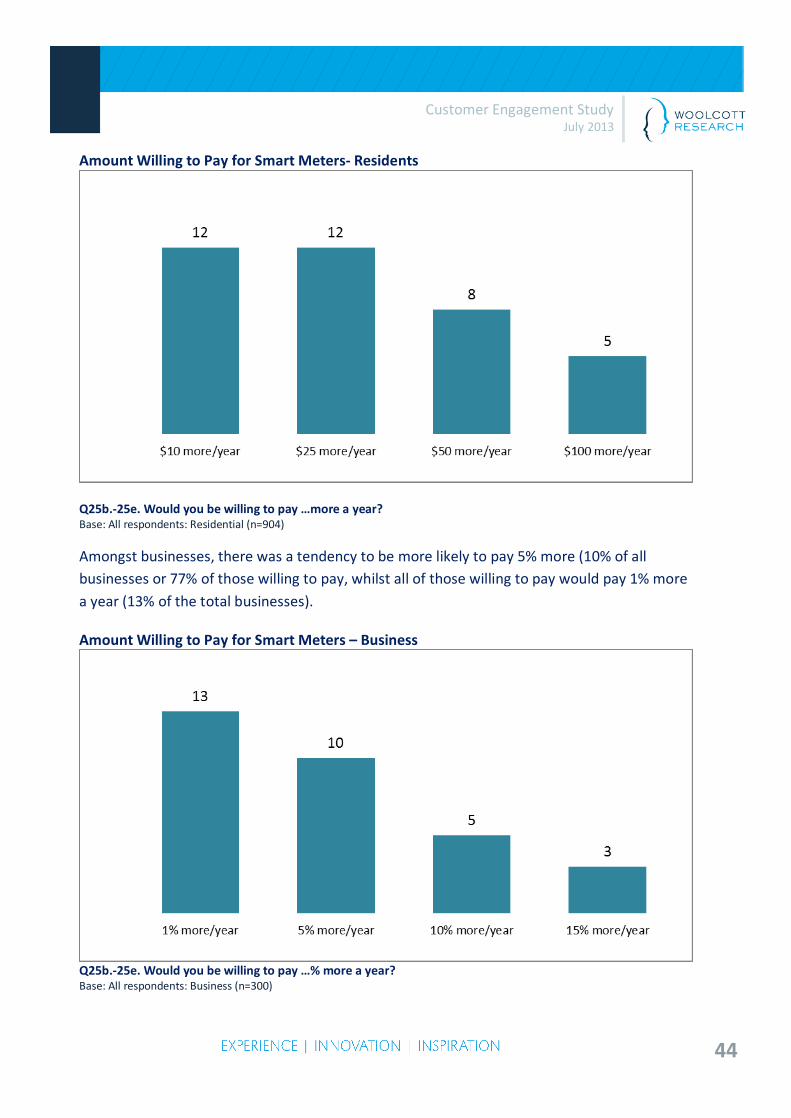

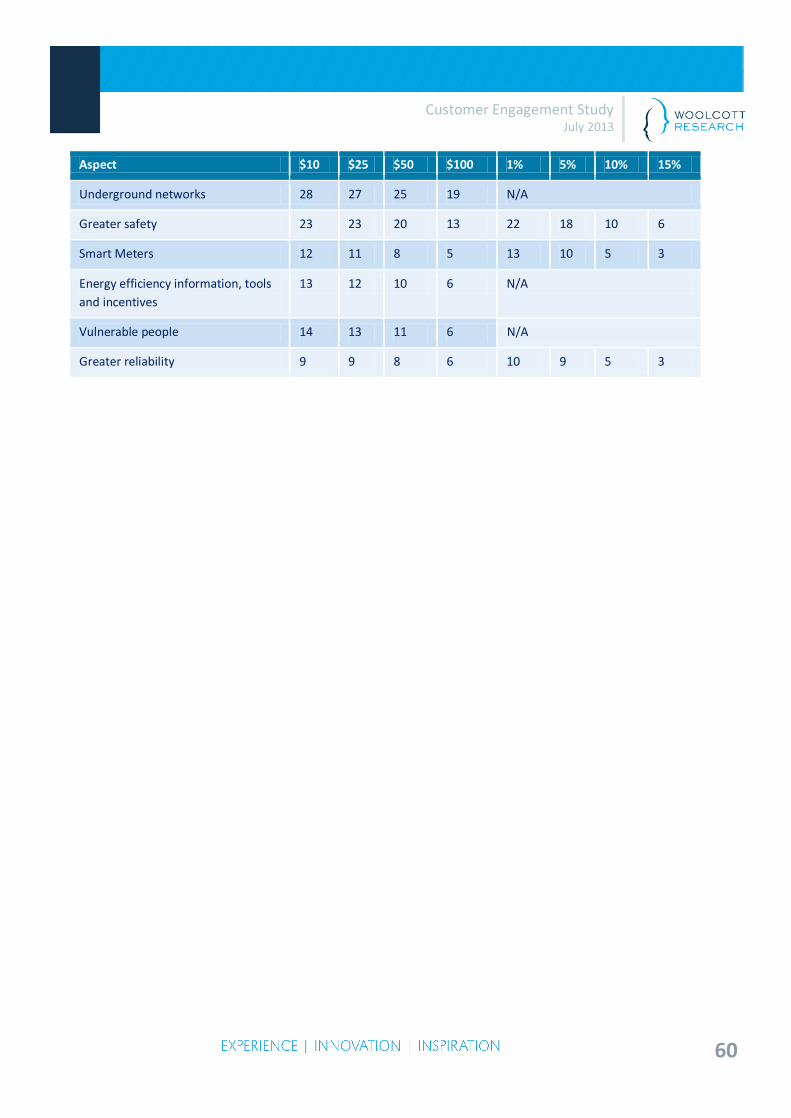

Respondents in the quantitative were asked how willing they would be to pay certain amounts more each year, to ensure greater reliability. The amounts offered started at $100 more, and if this was refused, they were asked how likely they would be to pay at $50, then $25, then $10. Amongst residents, only 5% of all respondents were willing to pay $100 more for greater reliability; however this rose to 7% at $50, and 8%, (or all of those willing to pay more), at $25 and $10. Sydney residents were willing to pay marginally more than those from North of the Hawkesbury. Amount Willing to Pay for Greater Reliability - Residents

Q5b.-5e. Would you be willing to pay …% more a year Base: All respondents: Residential (n=904) As businesses tend to have bigger bills, rather than a dollar amount, they were asked what percentage more they would be willing to pay, starting at 15%, going to 10%, 5%, and 1%. Only 3% of businesses were willing to pay 15% more a year to ensure greater reliability, with this rising to 5% willing to pay 10% more. Most businesses that were willing to pay would pay 5% more, with all willing to pay 1% more.

18

Customer Engagement Study July 2013

Amount Willing to Pay for Greater Reliability – Business

Q5b.-5e. Would you be willing to pay …% more a year? Base: All respondents: Business (n=300)

Those not willing to pay more were asked if they were willing to pay less, for less reliability, and 17% of residents in total were willing to pay less, however only 8% of businesses were willing to do this. Willingness to Pay Less for Less Reliability

Q6. Would you be willing to pay less each year for a less reliable service? Base: All respondents: Residential (n=904), Business (n=300)

19

Customer Engagement Study July 2013

4.3 Safety 4.3.1 Safety – Perceptions and Experiences When the qualitative participants were asked about what they felt were the safety risks involved in the provision of power, participants generally thought of injuries for workers and of the possibility of power lines coming down and causing fires, but they could envision little beyond those aspects. When prompted with some suggestions, including the possibility that children could be injured if they were able to get into substations, participants were surprised as it was thought that there already was very secure fencing around these facilities. Some thought they had noticed safety precautions such as gravel placed around the outside of substations to prevent fires spreading if they occurred, but most had not thought about the possibility of substations as a safety hazard. A minority mentioned that they thought living near pylons could be dangerous to peoples’ health. Some of the small and medium business decision makers mentioned their OH&S requirements for staff which they thought would be in place for all businesses, and they expected Ausgrid also would have to adhere to them in order to keep their staff safe.

“They have duty of care- like us” There was some slight unprompted recall of the Ausgrid taglines of ‘dial before you dig’ and ‘look up and live’ in regard to safety information that had been provided and these campaigns were well regarded. There was also some vague recall of information about safety that had come with the electricity bill. It was generally thought however that a lot of the safety information would be common sense and that there is not a lot that Ausgrid could do to prevent do about human error and stupid actions. When asked about the need for signage most felt that there were probably enough signs for the general public about safety with regard to electricity, for example on and near substations. In the quantitative research, residents did not mention many of the risks with the possibility of fatalities and electric shocks occurring being the main aspect. Businesses appeared able to

20

Customer Engagement Study July 2013

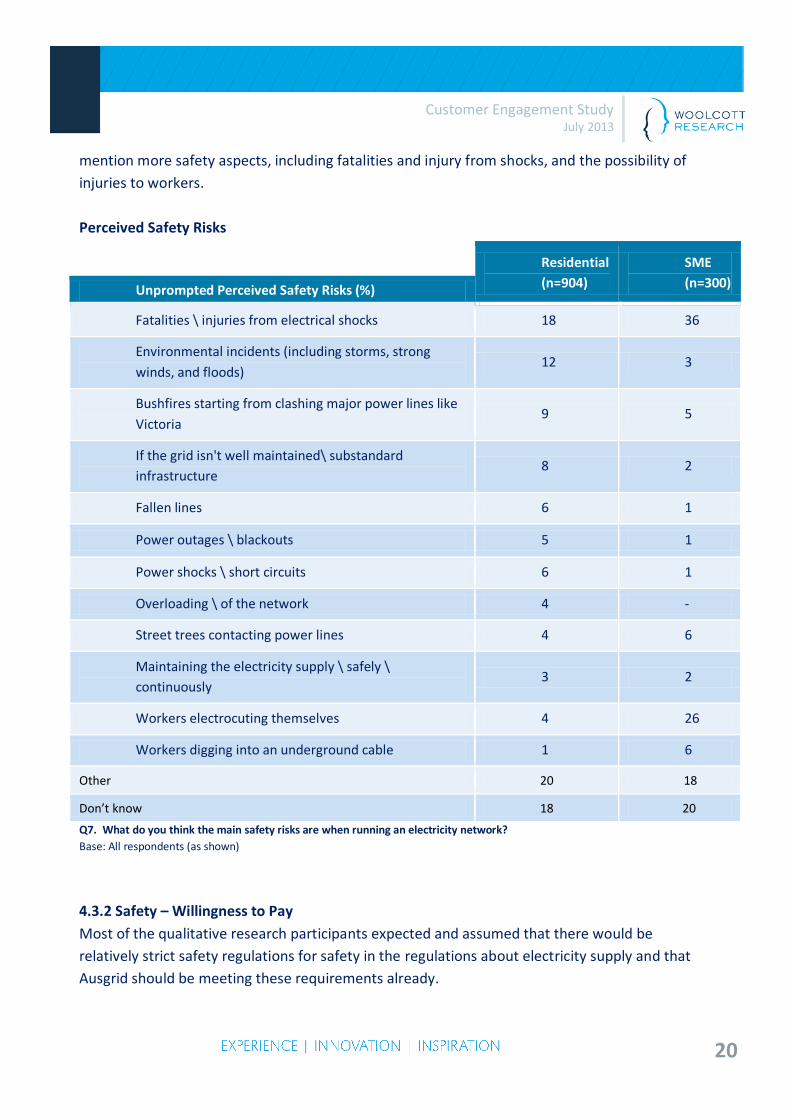

mention more safety aspects, including fatalities and injury from shocks, and the possibility of injuries to workers. Perceived Safety Risks

Residential (n=904)

SME (n=300) Unprompted Perceived Safety Risks (%)

Fatalities \ injuries from electrical shocks 18 36

Environmental incidents (including storms, strong winds, and floods)

12 3

Bushfires starting from clashing major power lines like Victoria

9 5

If the grid isn't well maintained\ substandard infrastructure

8 2

Fallen lines 6 1

Power outages \ blackouts 5 1

Power shocks \ short circuits 6 1

Overloading \ of the network 4 -

Street trees contacting power lines 4 6

Maintaining the electricity supply \ safely \ continuously

3 2

Workers electrocuting themselves 4 26

Workers digging into an underground cable 1 6

Other 20 18 Don’t know 18 20 Q7. What do you think the main safety risks are when running an electricity network? Base: All respondents (as shown)

4.3.2 Safety – Willingness to Pay Most of the qualitative research participants expected and assumed that there would be relatively strict safety regulations for safety in the regulations about electricity supply and that Ausgrid should be meeting these requirements already.

21

Customer Engagement Study July 2013

Participants trusted that the government regulations would be very stringent and that Ausgrid simply would not be allowed by the authorities to have hazardous old equipment or poor maintenance records. Therefore they did not feel that there would be a real need to have safety requirements over and above the regulations, and many were not willing to pay more for more safety measures when this idea was put to them.

“They should be doing regular maintenance and monitoring anyway”

“That would be passing the ownership of their safety requirements onto my ability to pay. The obligation is theirs not mine.”

“If they charge any more, we’ll have to go back to candles.”

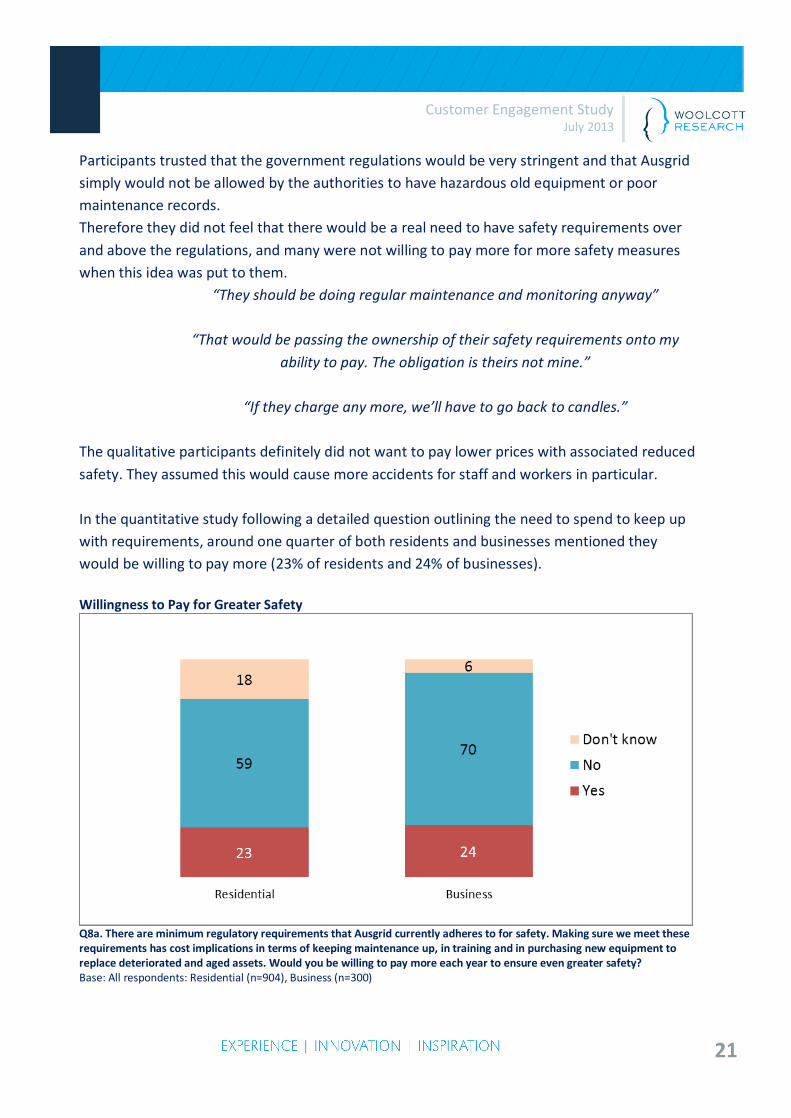

The qualitative participants definitely did not want to pay lower prices with associated reduced safety. They assumed this would cause more accidents for staff and workers in particular. In the quantitative study following a detailed question outlining the need to spend to keep up with requirements, around one quarter of both residents and businesses mentioned they would be willing to pay more (23% of residents and 24% of businesses). Willingness to Pay for Greater Safety

Q8a. There are minimum regulatory requirements that Ausgrid currently adheres to for safety. Making sure we meet these requirements has cost implications in terms of keeping maintenance up, in training and in purchasing new equipment to replace deteriorated and aged assets. Would you be willing to pay more each year to ensure even greater safety? Base: All respondents: Residential (n=904), Business (n=300)

22

Customer Engagement Study July 2013

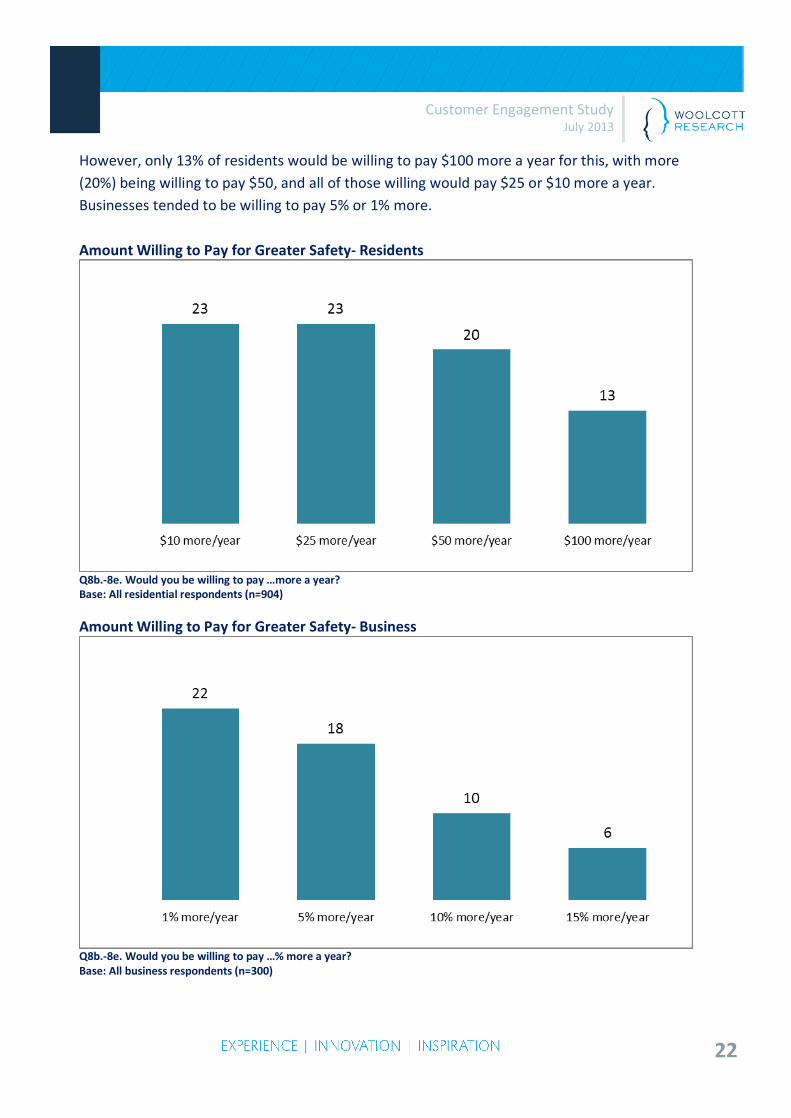

However, only 13% of residents would be willing to pay $100 more a year for this, with more (20%) being willing to pay $50, and all of those willing would pay $25 or $10 more a year. Businesses tended to be willing to pay 5% or 1% more. Amount Willing to Pay for Greater Safety- Residents

Q8b.-8e. Would you be willing to pay …more a year? Base: All residential respondents (n=904)

Amount Willing to Pay for Greater Safety- Business

Q8b.-8e. Would you be willing to pay …% more a year? Base: All business respondents (n=300)

23

Customer Engagement Study July 2013

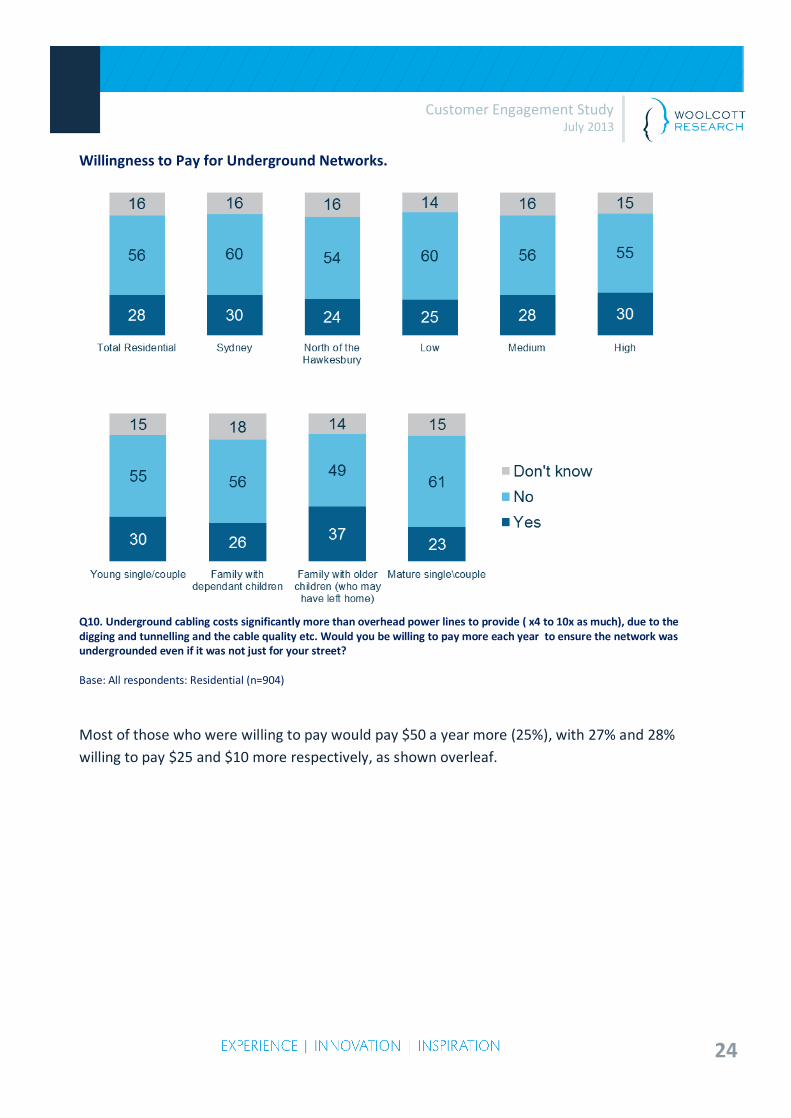

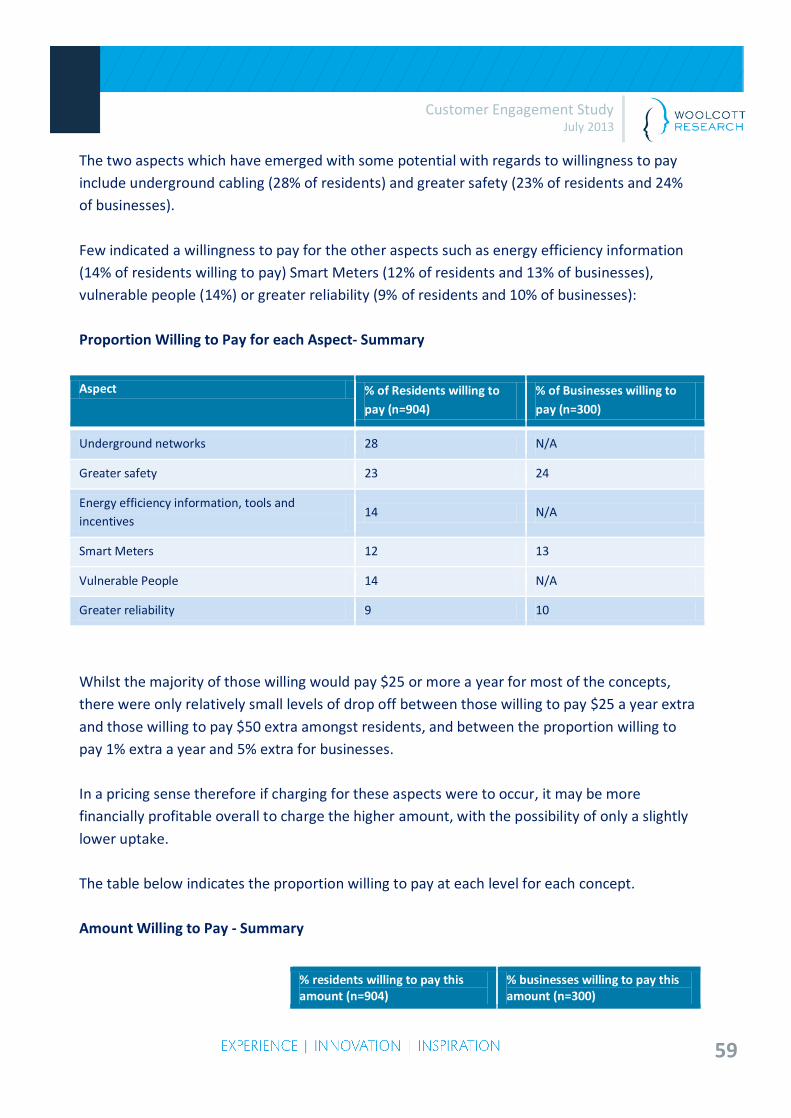

4.4 Construction/Design Standards 4.4.1 Ranking of Construction Factors The qualitative participants were asked to rank the importance of four factors which could be taken into account by Ausgrid in decision making around new construction/design standards. The overall ranking was reasonably consistent across all the groups and amongst residents and businesses. Price was consistently ranked as the most important aspect to take into account in any construction and design standards used by Ausgrid, and this was seen as particularly important at the moment because of the recent price increases which had been seen to be significant. However, whilst the pricing aspect was seen as very important, it was thought that safety standards could not be compromised to any degree in construction and design as a result of using the cheaper options. Safety was not placed at a higher level than price in the rankings however because it was assumed that relatively strict regulations were already in place and that these would remain, and would have to be taken into account in decision making. The aesthetics of the construction style was thought to play a part, and options such as underground or less visible cabling and pole options were thought to be ‘nice to have’ but not essential for most at the expense of price. However it appeared there was a definite segment of residential customers who would be prepared to pay more for this but only if the construction was to be in their street or in their wider local area. These people tended to be those with higher incomes from the higher socioeconomic group. Environmental issues were thought to be important by a relatively small segment of participants but most could not see how construction and design in electricity distribution could have a big impact on the environment, and it therefore was ranked as lower than the other dimensions tested. 4.4.2 Willingness to Pay for Underground Construction The quantitative research indicated that there was indeed a segment of residents in particular who were willing to pay for underground networks; with 28% indicating that they were willing ‘even if it was not just for your street’. Those on higher incomes and those with older children were the most likely segments to pay more.

24

Customer Engagement Study July 2013

Willingness to Pay for Underground Networks.

Q10. Underground cabling costs significantly more than overhead power lines to provide ( x4 to 10x as much), due to the digging and tunnelling and the cable quality etc. Would you be willing to pay more each year to ensure the network was undergrounded even if it was not just for your street? Base: All respondents: Residential (n=904)

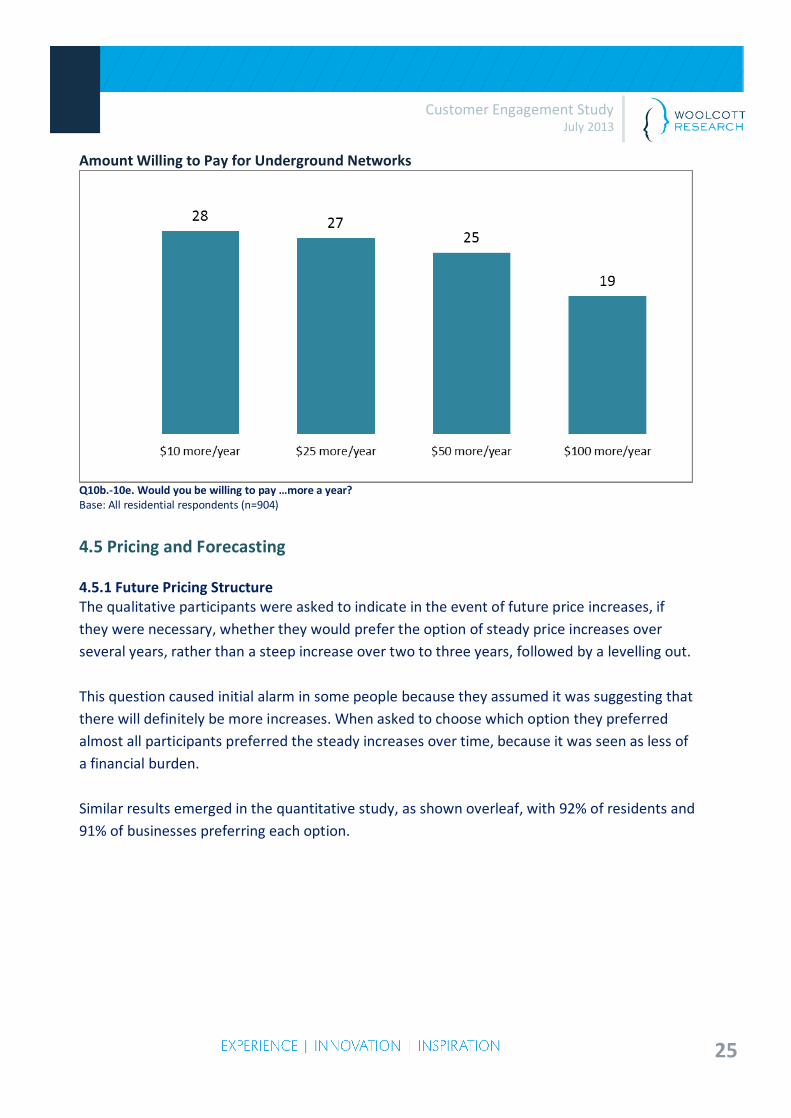

Most of those who were willing to pay would pay $50 a year more (25%), with 27% and 28% willing to pay $25 and $10 more respectively, as shown overleaf.

25

Customer Engagement Study July 2013

Amount Willing to Pay for Underground Networks

Q10b.-10e. Would you be willing to pay …more a year? Base: All residential respondents (n=904)

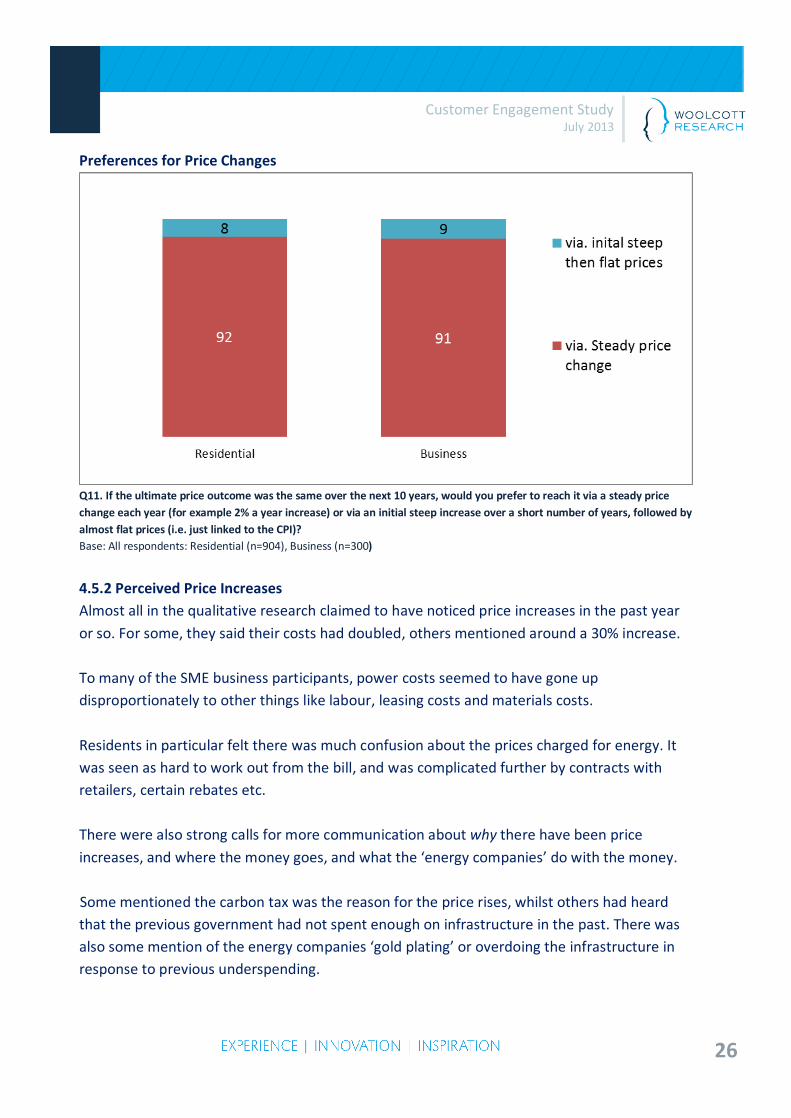

4.5 Pricing and Forecasting 4.5.1 Future Pricing Structure The qualitative participants were asked to indicate in the event of future price increases, if they were necessary, whether they would prefer the option of steady price increases over several years, rather than a steep increase over two to three years, followed by a levelling out. This question caused initial alarm in some people because they assumed it was suggesting that there will definitely be more increases. When asked to choose which option they preferred almost all participants preferred the steady increases over time, because it was seen as less of a financial burden. Similar results emerged in the quantitative study, as shown overleaf, with 92% of residents and 91% of businesses preferring each option.

26

Customer Engagement Study July 2013

Preferences for Price Changes

Q11. If the ultimate price outcome was the same over the next 10 years, would you prefer to reach it via a steady price change each year (for example 2% a year increase) or via an initial steep increase over a short number of years, followed by almost flat prices (i.e. just linked to the CPI)? Base: All respondents: Residential (n=904), Business (n=300)

4.5.2 Perceived Price Increases Almost all in the qualitative research claimed to have noticed price increases in the past year or so. For some, they said their costs had doubled, others mentioned around a 30% increase. To many of the SME business participants, power costs seemed to have gone up disproportionately to other things like labour, leasing costs and materials costs. Residents in particular felt there was much confusion about the prices charged for energy. It was seen as hard to work out from the bill, and was complicated further by contracts with retailers, certain rebates etc. There were also strong calls for more communication about why there have been price increases, and where the money goes, and what the ‘energy companies’ do with the money. Some mentioned the carbon tax was the reason for the price rises, whilst others had heard that the previous government had not spent enough on infrastructure in the past. There was also some mention of the energy companies ‘gold plating’ or overdoing the infrastructure in response to previous underspending.

27

Customer Engagement Study July 2013

The quantitative research confirmed that the majority felt they had experienced significant price rises, with 45% of residents reporting their prices had increased ‘a lot’ and another 31% ‘slightly’. A higher proportion of businesses felt the prices had increased ‘a lot’ (52%), with 20% feeling they had increased ‘slightly’. Awareness of Recent Price Changes

Q12. Have you noticed any change in the level of your electricity bill over the past year or so? Base: All respondents: Residential (n=904), Business (n=300)

4.5.3 Incidence of Reducing Electricity Usage The qualitative residential participants all claimed to have made a lot of changes to the way they used electricity in order to save money, some with considerable success, including:

• changing to low energy light bulbs;

• looking at star ratings for appliances when purchasing;

• making sure power sockets are turned off;

• turning off lights when not in use;

• having full loads for washing machines and dishwashers;

• using cold water to wash in;

• not using dryers unless very wet; and

• some had timers on when in the shower.

Some of the Newcastle and Gosford residents had been visited by somebody doing an energy audit, to help them see how they can save energy. This was felt to be a very comprehensive

28

Customer Engagement Study July 2013

service, and they reportedly left behind devices such as ‘sausages’ for the bottom of the door, energy saving light bulbs, and a letter explaining how to be more efficient.

Most in the qualitative claimed their energy saving behaviours had become habitual, and they believed they would continue this way, even if prices were reduced. Extremes in weather also had an evident effect on some behaviours, causing people to for example use an extra blanket on particularly cold days (e.g. when sitting in front of the TV), draw the curtains on cold/hot days, and only use air-conditioning on ‘extreme’ weather days However, there was some reluctance to trade off air-conditioning usage in order to save electricity, especially on particularly hot days. Many claimed they only used air conditioning quite sparingly anyway. Some had adopted longer term solutions to saving electricity, including lowering the temperature on the water heater, or changing heating to oil or something else. Few had switched from electricity to gas as a result of the increases; although a few were thinking about solar in the future. There was some comment from those in unit blocks around wastage by the building management, and this produced some anger. Things like the outside lights being left on all day, rules around when washing machines and driers can be used (thus limiting off peak usage); and rules about drying clothes on balconies/outside made it difficult for the residents to cut back as much as they would like. Overall there was consternation amongst residents regarding what they would do if prices were to increase more, as most, particularly the lower bill level groups and pensioners, felt they were already doing everything they could. “Everyone’s doing the best they can and it would be hard to do more” A small segment of residents refused to compromise their lifestyle to any great degree, and felt they were justified in using what they wanted if they were paying for it. The business participants felt there was a limitation around what many business owners could do in regards to energy efficient behaviour, for example in cutting back air-conditioning and light usage, due to OH&S regulations, and the employers responsibility to ensure a comfortable workplace.

However changes that had been instigated in the business environment included:

29

Customer Engagement Study July 2013

• Ensuring lights and computers were turned off at night; and,

• Purchasing more energy efficient appliances – especially freezers that had to stay on for 24h

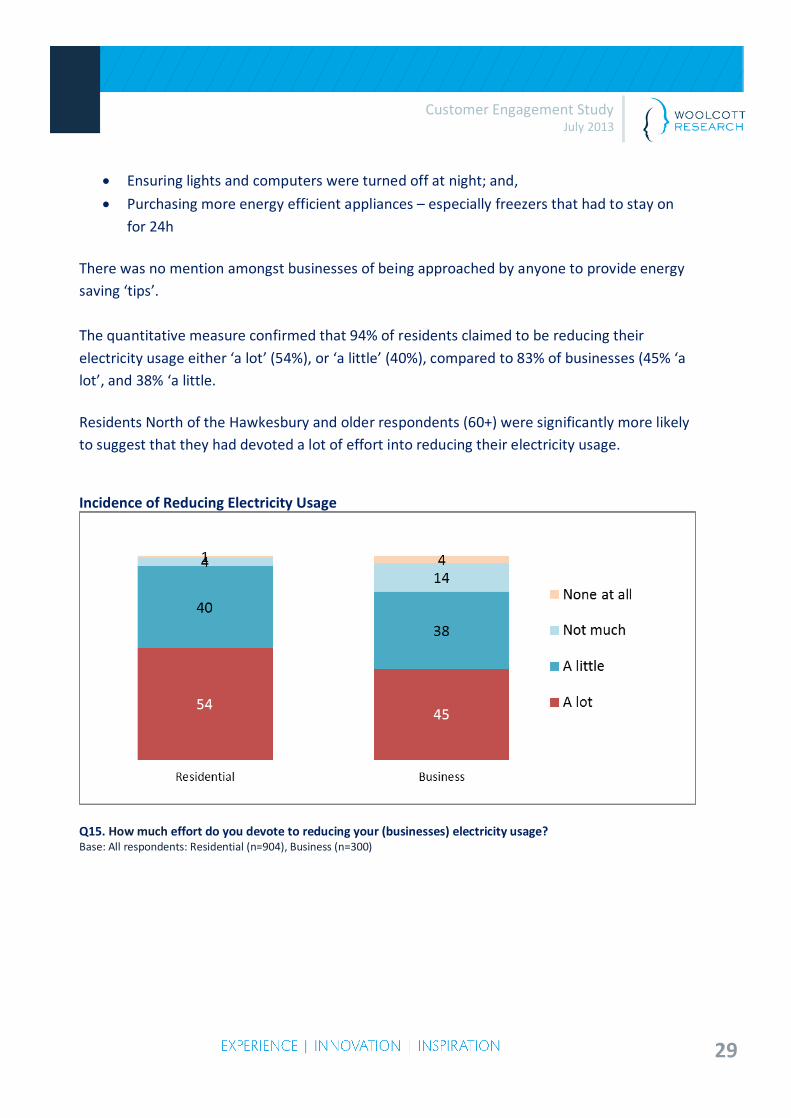

There was no mention amongst businesses of being approached by anyone to provide energy saving ‘tips’. The quantitative measure confirmed that 94% of residents claimed to be reducing their electricity usage either ‘a lot’ (54%), or ‘a little’ (40%), compared to 83% of businesses (45% ‘a lot’, and 38% ‘a little. Residents North of the Hawkesbury and older respondents (60+) were significantly more likely to suggest that they had devoted a lot of effort into reducing their electricity usage.

Incidence of Reducing Electricity Usage

Q15. How much effort do you devote to reducing your (businesses) electricity usage? Base: All respondents: Residential (n=904), Business (n=300)

30

Customer Engagement Study July 2013

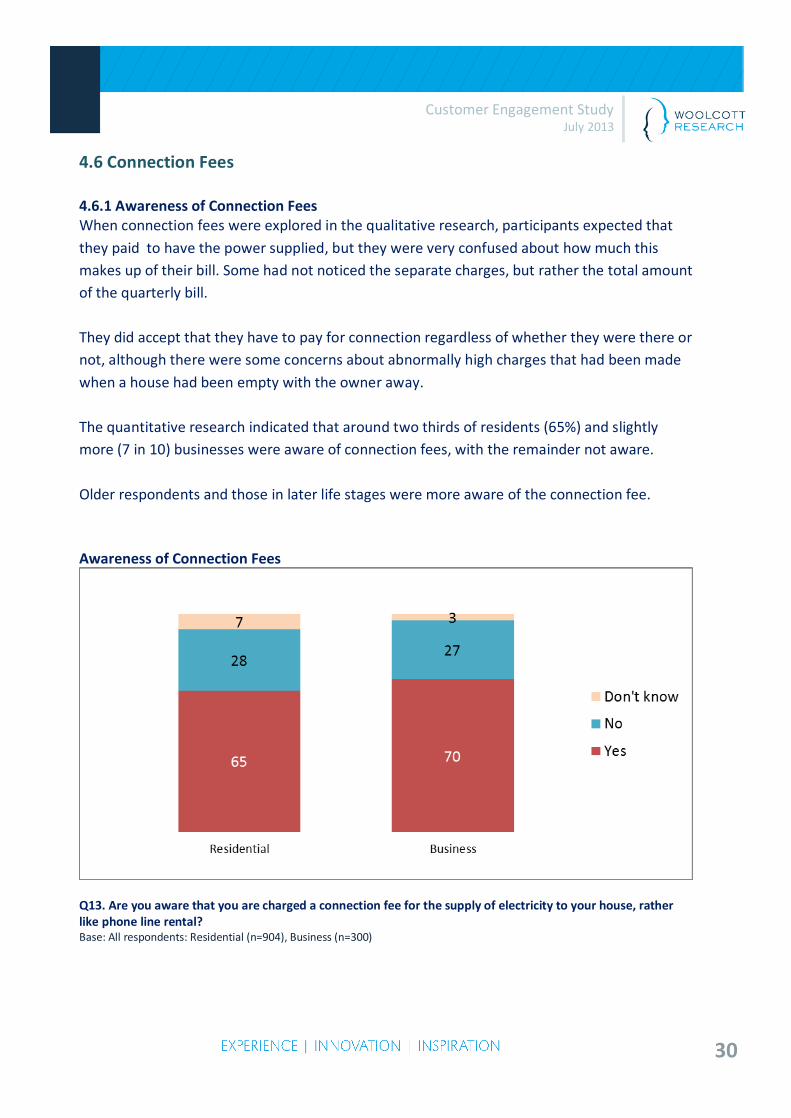

4.6 Connection Fees 4.6.1 Awareness of Connection Fees When connection fees were explored in the qualitative research, participants expected that they paid to have the power supplied, but they were very confused about how much this makes up of their bill. Some had not noticed the separate charges, but rather the total amount of the quarterly bill. They did accept that they have to pay for connection regardless of whether they were there or not, although there were some concerns about abnormally high charges that had been made when a house had been empty with the owner away. The quantitative research indicated that around two thirds of residents (65%) and slightly more (7 in 10) businesses were aware of connection fees, with the remainder not aware. Older respondents and those in later life stages were more aware of the connection fee. Awareness of Connection Fees

Q13. Are you aware that you are charged a connection fee for the supply of electricity to your house, rather like phone line rental? Base: All respondents: Residential (n=904), Business (n=300)

31

Customer Engagement Study July 2013

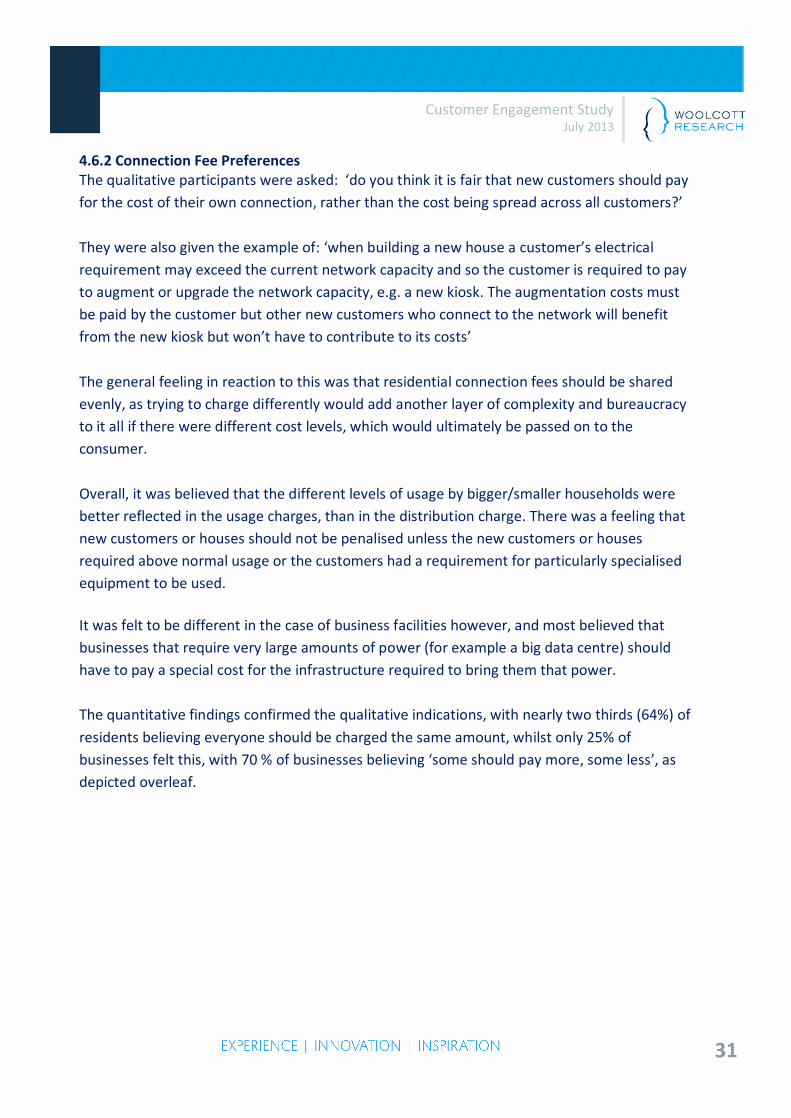

4.6.2 Connection Fee Preferences The qualitative participants were asked: ‘do you think it is fair that new customers should pay for the cost of their own connection, rather than the cost being spread across all customers?’ They were also given the example of: ‘when building a new house a customer’s electrical requirement may exceed the current network capacity and so the customer is required to pay to augment or upgrade the network capacity, e.g. a new kiosk. The augmentation costs must be paid by the customer but other new customers who connect to the network will benefit from the new kiosk but won’t have to contribute to its costs’ The general feeling in reaction to this was that residential connection fees should be shared evenly, as trying to charge differently would add another layer of complexity and bureaucracy to it all if there were different cost levels, which would ultimately be passed on to the consumer. Overall, it was believed that the different levels of usage by bigger/smaller households were better reflected in the usage charges, than in the distribution charge. There was a feeling that new customers or houses should not be penalised unless the new customers or houses required above normal usage or the customers had a requirement for particularly specialised equipment to be used. It was felt to be different in the case of business facilities however, and most believed that businesses that require very large amounts of power (for example a big data centre) should have to pay a special cost for the infrastructure required to bring them that power. The quantitative findings confirmed the qualitative indications, with nearly two thirds (64%) of residents believing everyone should be charged the same amount, whilst only 25% of businesses felt this, with 70 % of businesses believing ‘some should pay more, some less’, as depicted overleaf.

32

Customer Engagement Study July 2013

Preferred Connection Fee Payment Variability

Q14. And do you feel all households should pay the same amount for this connection fee, or do you think some households should pay more, some less? Base: All respondents: Residential (n=904), Business (n=300)

4.7 Energy Efficiency Programs 4.7.1. Awareness of Energy Efficiency Programs In the qualitative research most participants indicated there was quite a lot of activity and encouragement concerning energy efficiency currently, and they mentioned aspects such as pamphlets coming in the bills from retailers, advertising in magazines and TV and participatory in-home energy audits where someone would come to the home and suggest where and how energy savings could be made. In Newcastle, there was some awareness of ‘Honeysuckle Place’ the Smart Grid Smart City showroom, and also some activity in shopping centre kiosks around energy efficiency. But again there was confusion about who was responsible for this. Some also recalled ‘the Government’ had been active in programs such as supplying energy efficient light bulbs. Overall many felt that most people generally know what to do in relation to saving energy and using it efficiently now, although some would like to learn more about specific aspects which

33

Customer Engagement Study July 2013

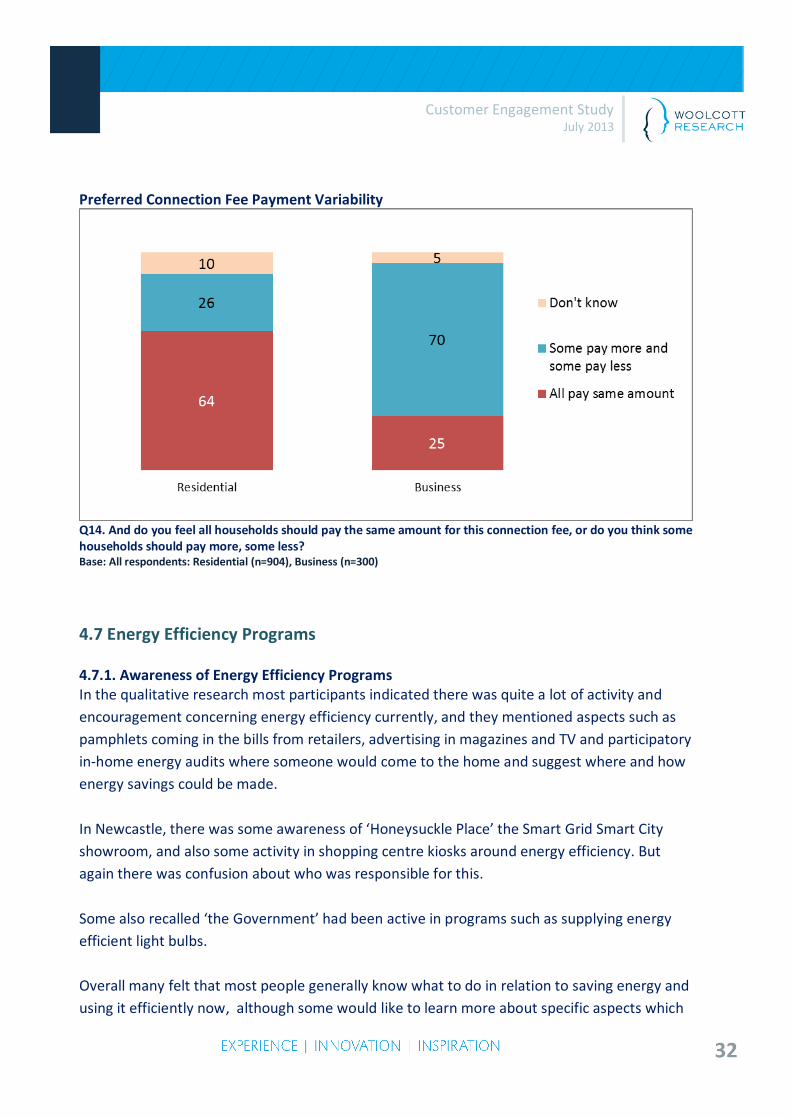

they were still not sure about such as which appliances used more power, and how much power is wasted if appliances are left on standby. 4.7.2 Perceptions Regarding Ausgrid’s Role in Energy Efficiency It was believed by most in the qualitative research that people do still need to be educated about how to use energy efficiently; however some tended to believe it was the retailer responsibility, not necessarily the distributor. Retailers had been seen to be already playing an active role in this area, and it was assumed that they were trying to appear as ‘good citizens’ by doing so and therefore should keep doing it. There was only minor recognition that retailers may not be interested in helping people save power, as this would impact their profits. When the quantitative respondents were asked a direct question about whether Ausgrid should help in this regard, 85% of residences and 84% of businesses believed they should. This feeling was highest amongst medium sized businesses (91% believed Ausgrid should do this). Energy Efficiency Aid

Q16. Do you think Ausgrid should try and help people/businesses to be more energy efficient? Base: All respondents: Residential (n=904), Business (n=300)

34

Customer Engagement Study July 2013

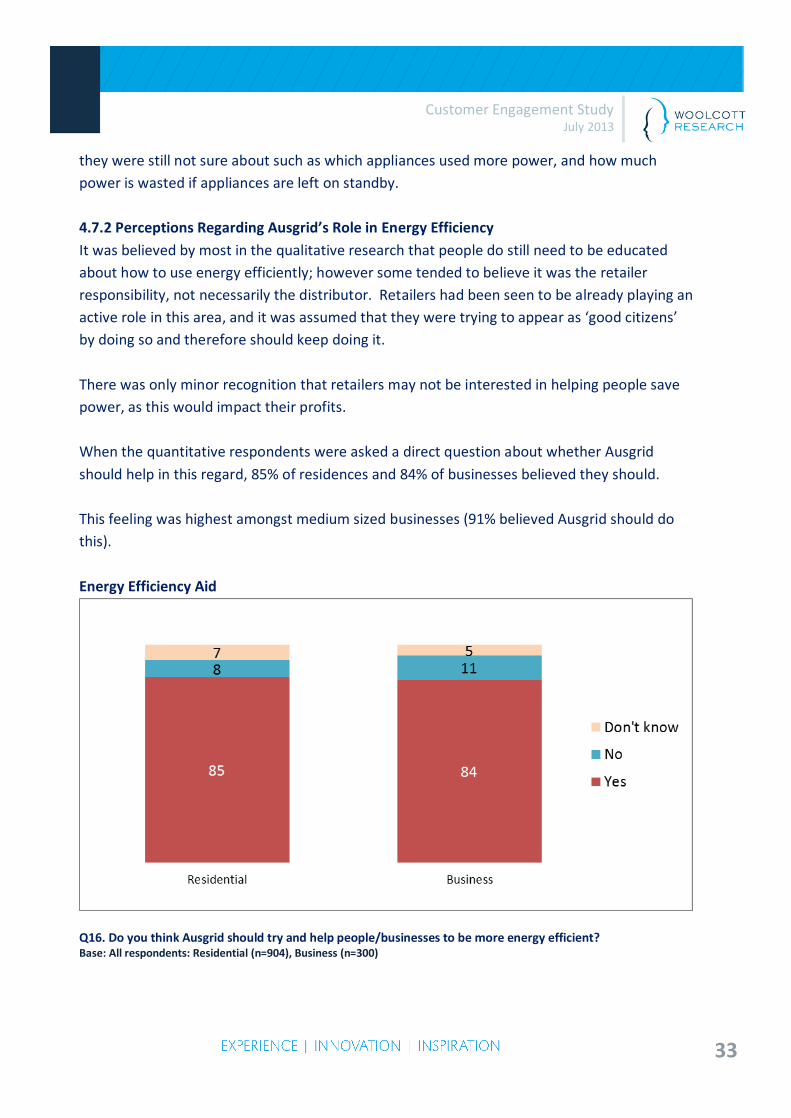

4.7.3 Willingness to Pay for Energy Efficiency Education There was little willingness to pay to have Ausgrid take on energy efficiency initiatives evident in the qualitative exploration, and the quantitative research confirmed that only 14% of residents in total would be willing to pay for this. This level was higher amongst the 18-34 year olds, with a sharp drop off in willingness amongst those aged 35 and over. Willingness to Pay for Energy Efficiency Information, Tools and Incentives- Residents

Q17. Would you be willing to pay more for Ausgrid to provide information, tools and incentives for energy efficiency? Base: All respondents: Residential (n=904) Note: This question was only asked of residents When questioned about the actual amount they would be willing to pay, only around half of those who were willing to pay (6% of all residents ) were willing to pay $100 or more a year, with this proportion increasing to 10% willing to pay $50 a year, and 12% and 13% respectively willing to pay $25 and $10. Amount Willing to Pay for Energy Efficiency Information, Tools and Incentives – Residents

35

Customer Engagement Study July 2013

Q17b.-17e. Would you be willing to pay …more a year? Base: All respondents: Residential (n=904) 4.8 Demand Management 4.8.1 Understanding of Demand Management Most in the qualitative research were aware that demand fluctuates during the day and was dependant on the weather to a degree, but many believed that daytime usage between 9 am and 5 pm would be when demand is at its highest, because of the strain from business usage. Some therefore questioned the example given in the qualitative research of the evening/dinner time usage peak. Some mentioned that they had experienced outages at times of heaviest demand such on abnormally hot days, with heavy use of air conditioning, but these outage occasions were felt to be very rare, and only ever occurred in extreme conditions. The feeling was that the peak times (e.g. during a heat wave or cold spell) were exactly the times that one would want to use the power, for air conditioning or heating, pool use etc. and they expected to have the choice to be able to use as much power as required at those times if that is the level of lifestyle you are willing to pay for.

36

Customer Engagement Study July 2013

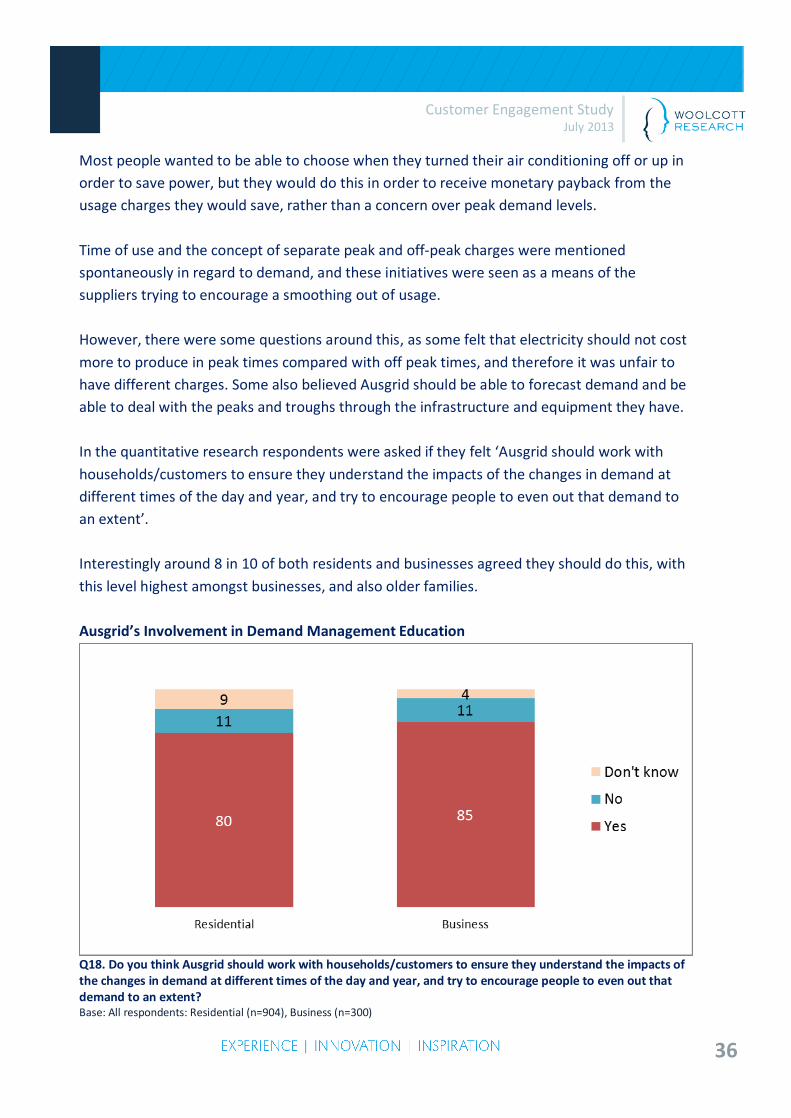

Most people wanted to be able to choose when they turned their air conditioning off or up in order to save power, but they would do this in order to receive monetary payback from the usage charges they would save, rather than a concern over peak demand levels. Time of use and the concept of separate peak and off-peak charges were mentioned spontaneously in regard to demand, and these initiatives were seen as a means of the suppliers trying to encourage a smoothing out of usage. However, there were some questions around this, as some felt that electricity should not cost more to produce in peak times compared with off peak times, and therefore it was unfair to have different charges. Some also believed Ausgrid should be able to forecast demand and be able to deal with the peaks and troughs through the infrastructure and equipment they have. In the quantitative research respondents were asked if they felt ‘Ausgrid should work with households/customers to ensure they understand the impacts of the changes in demand at different times of the day and year, and try to encourage people to even out that demand to an extent’. Interestingly around 8 in 10 of both residents and businesses agreed they should do this, with this level highest amongst businesses, and also older families. Ausgrid’s Involvement in Demand Management Education

Q18. Do you think Ausgrid should work with households/customers to ensure they understand the impacts of the changes in demand at different times of the day and year, and try to encourage people to even out that demand to an extent? Base: All respondents: Residential (n=904), Business (n=300)

37

Customer Engagement Study July 2013

4.8.2 Awareness of Demand Management Schemes, and Willingness to Participate Participants in the qualitative were not aware of any rebate offers such as that described, i.e. ‘Programs where customers agree to allow Ausgrid to control the use of high energy demand appliances like air conditioners during peak demand times in return for a rebate or discount’, and the majority rejected this rebate idea because they felt it took away control from the customer, and gave the feeling that a ‘big brother’ type organisation was in power. Most felt it would require a high rebate to encourage participation, more than $100, to make up for putting up with the discomfort or impact on lifestyle. A small segment were however interested, and felt they would agree to that. The rebate idea was also not acceptable for most businesses in the qualitative research:

“If you are in business, you have the power on because you have to.”

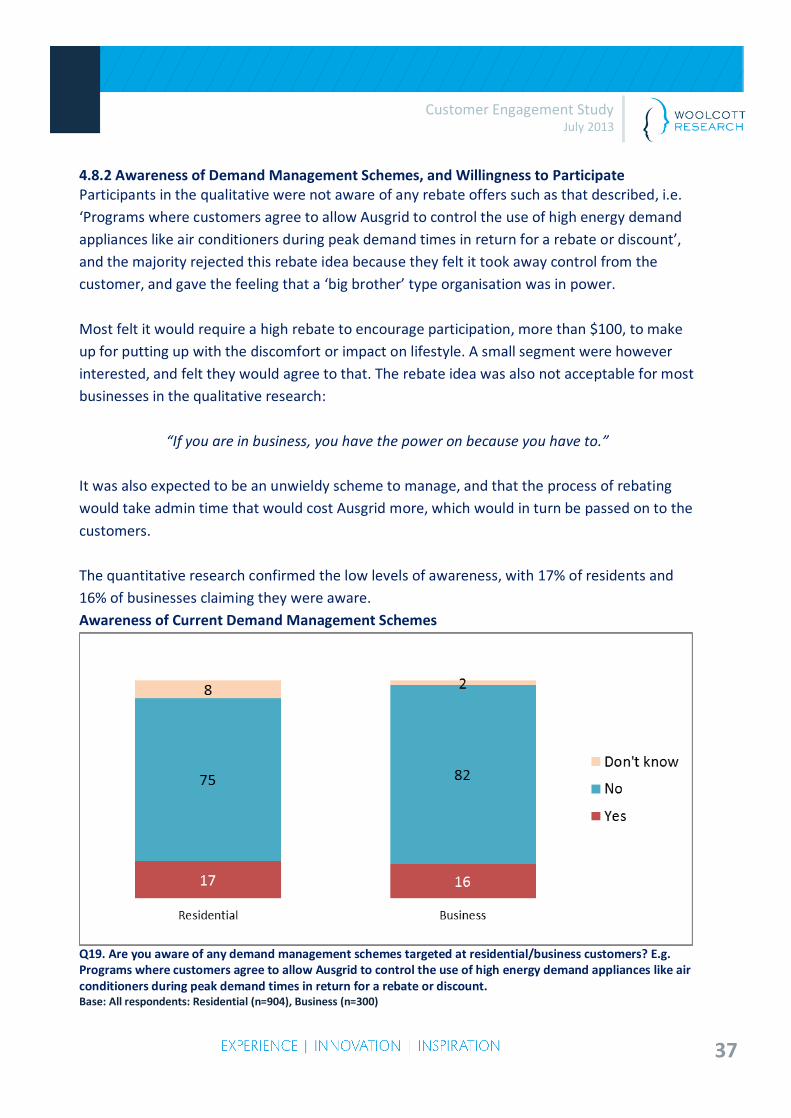

It was also expected to be an unwieldy scheme to manage, and that the process of rebating would take admin time that would cost Ausgrid more, which would in turn be passed on to the customers. The quantitative research confirmed the low levels of awareness, with 17% of residents and 16% of businesses claiming they were aware. Awareness of Current Demand Management Schemes

Q19. Are you aware of any demand management schemes targeted at residential/business customers? E.g. Programs where customers agree to allow Ausgrid to control the use of high energy demand appliances like air conditioners during peak demand times in return for a rebate or discount. Base: All respondents: Residential (n=904), Business (n=300)

38

Customer Engagement Study July 2013

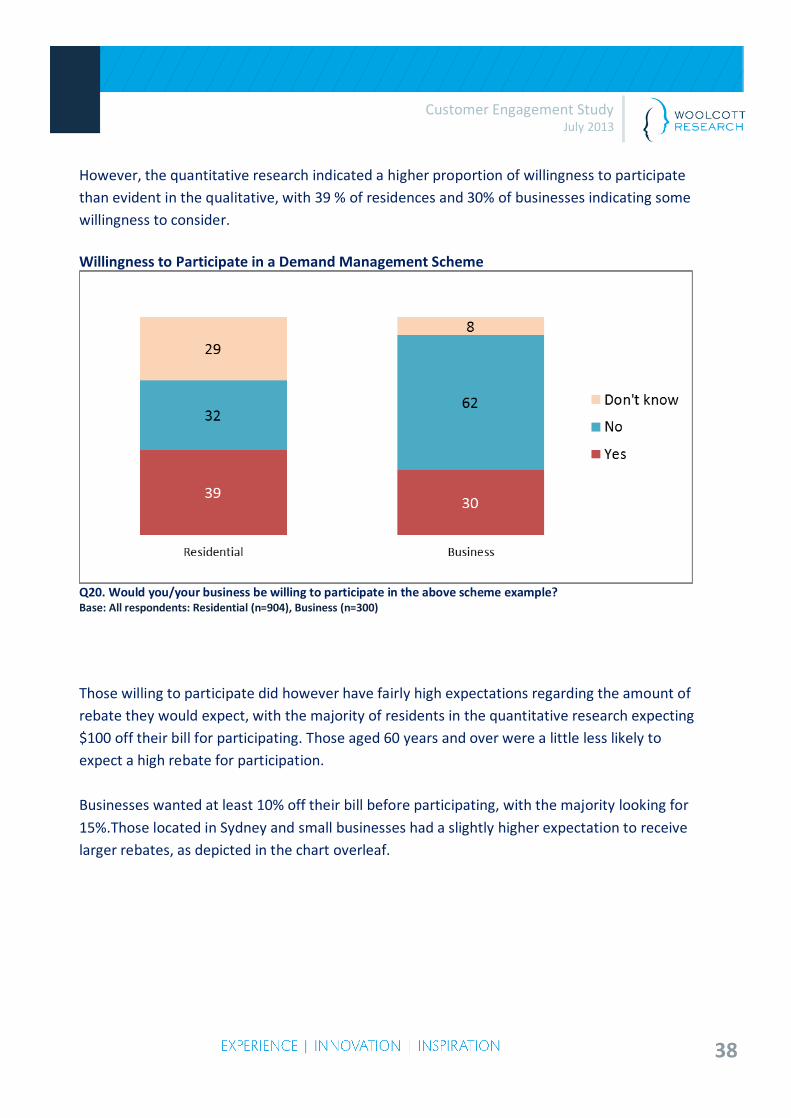

However, the quantitative research indicated a higher proportion of willingness to participate than evident in the qualitative, with 39 % of residences and 30% of businesses indicating some willingness to consider. Willingness to Participate in a Demand Management Scheme

Q20. Would you/your business be willing to participate in the above scheme example? Base: All respondents: Residential (n=904), Business (n=300)

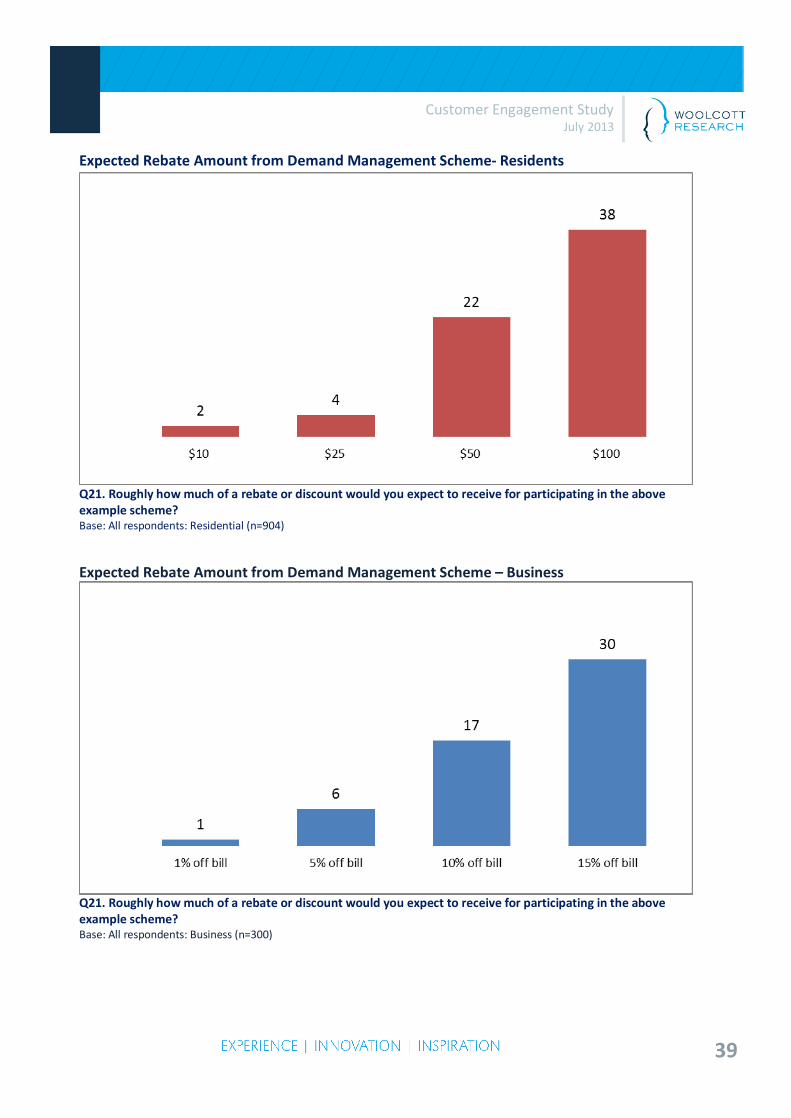

Those willing to participate did however have fairly high expectations regarding the amount of rebate they would expect, with the majority of residents in the quantitative research expecting $100 off their bill for participating. Those aged 60 years and over were a little less likely to expect a high rebate for participation. Businesses wanted at least 10% off their bill before participating, with the majority looking for 15%.Those located in Sydney and small businesses had a slightly higher expectation to receive larger rebates, as depicted in the chart overleaf.

39

Customer Engagement Study July 2013

Expected Rebate Amount from Demand Management Scheme- Residents

Q21. Roughly how much of a rebate or discount would you expect to receive for participating in the above example scheme? Base: All respondents: Residential (n=904)

Expected Rebate Amount from Demand Management Scheme – Business

Q21. Roughly how much of a rebate or discount would you expect to receive for participating in the above example scheme? Base: All respondents: Business (n=300)

40

Customer Engagement Study July 2013

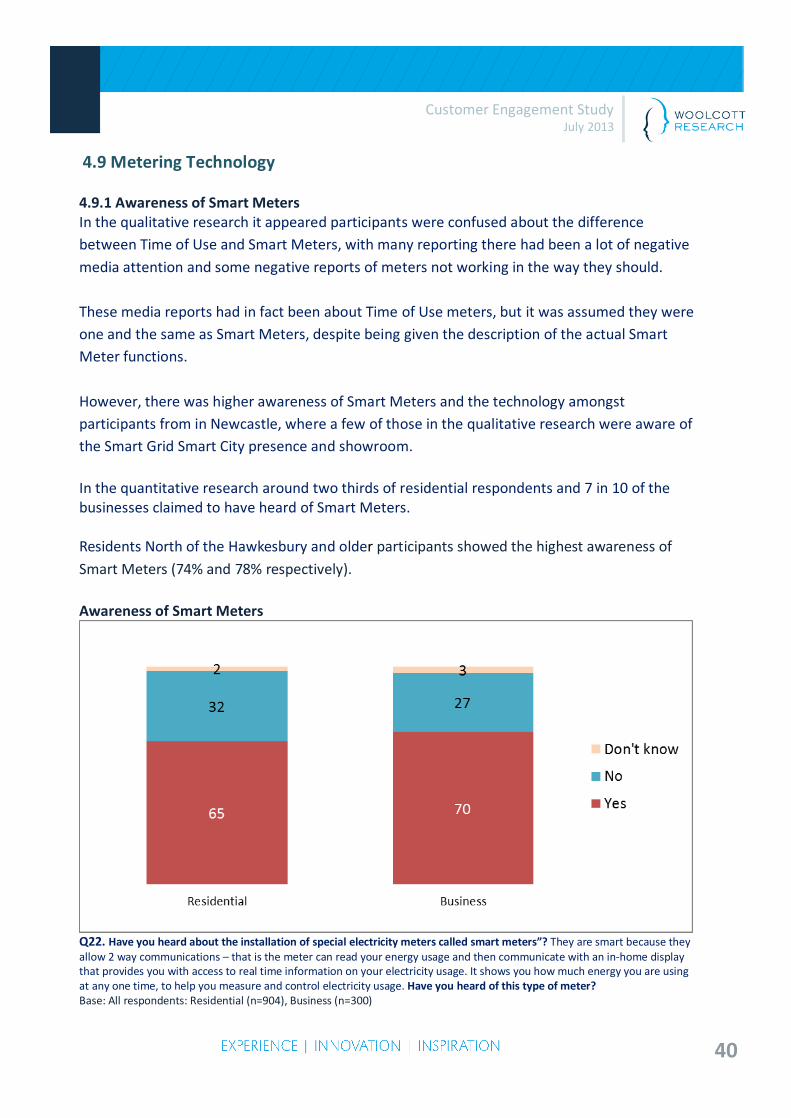

4.9 Metering Technology 4.9.1 Awareness of Smart Meters In the qualitative research it appeared participants were confused about the difference between Time of Use and Smart Meters, with many reporting there had been a lot of negative media attention and some negative reports of meters not working in the way they should. These media reports had in fact been about Time of Use meters, but it was assumed they were one and the same as Smart Meters, despite being given the description of the actual Smart Meter functions. However, there was higher awareness of Smart Meters and the technology amongst participants from in Newcastle, where a few of those in the qualitative research were aware of the Smart Grid Smart City presence and showroom. In the quantitative research around two thirds of residential respondents and 7 in 10 of the businesses claimed to have heard of Smart Meters. Residents North of the Hawkesbury and older participants showed the highest awareness of Smart Meters (74% and 78% respectively). Awareness of Smart Meters

Q22. Have you heard about the installation of special electricity meters called smart meters”? They are smart because they allow 2 way communications – that is the meter can read your energy usage and then communicate with an in-home display that provides you with access to real time information on your electricity usage. It shows you how much energy you are using at any one time, to help you measure and control electricity usage. Have you heard of this type of meter? Base: All respondents: Residential (n=904), Business (n=300)

41

Customer Engagement Study July 2013

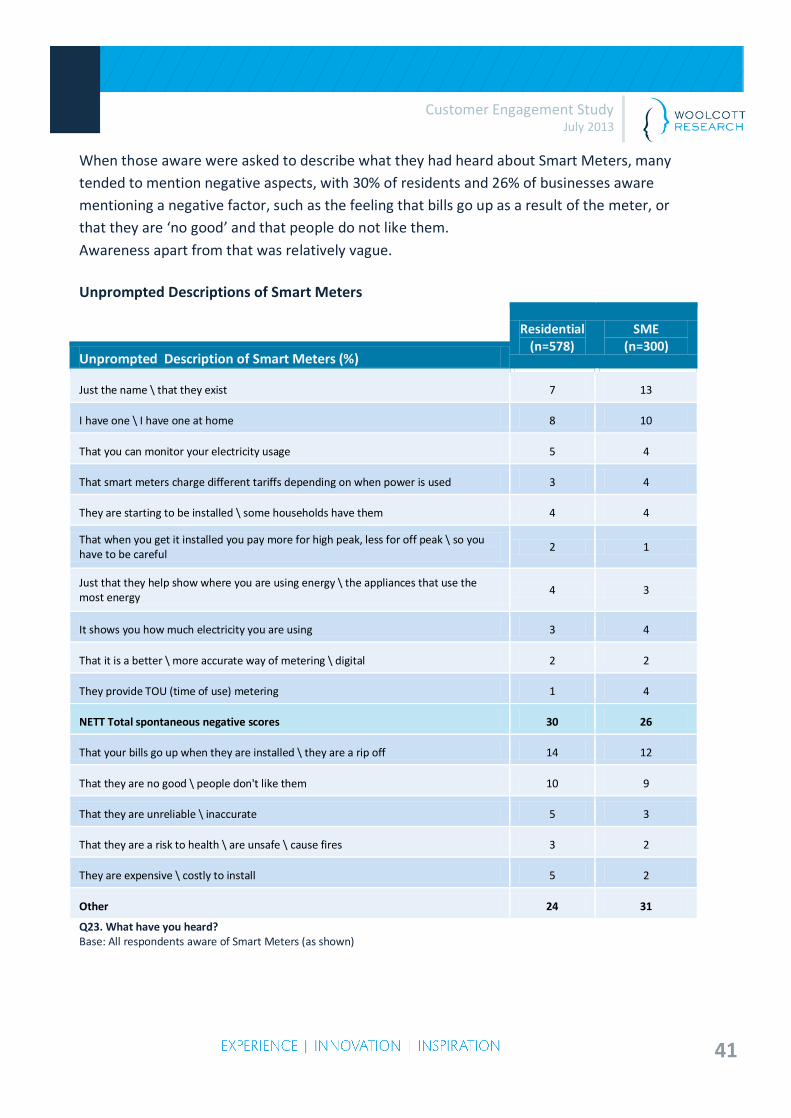

When those aware were asked to describe what they had heard about Smart Meters, many tended to mention negative aspects, with 30% of residents and 26% of businesses aware mentioning a negative factor, such as the feeling that bills go up as a result of the meter, or that they are ‘no good’ and that people do not like them. Awareness apart from that was relatively vague. Unprompted Descriptions of Smart Meters

Residential (n=578)

SME (n=300)

Unprompted Description of Smart Meters (%) Just the name \ that they exist 7 13 I have one \ I have one at home 8 10 That you can monitor your electricity usage 5 4 That smart meters charge different tariffs depending on when power is used 3 4 They are starting to be installed \ some households have them 4 4 That when you get it installed you pay more for high peak, less for off peak \ so you have to be careful 2 1 Just that they help show where you are using energy \ the appliances that use the most energy 4 3 It shows you how much electricity you are using 3 4 That it is a better \ more accurate way of metering \ digital 2 2 They provide TOU (time of use) metering 1 4 NETT Total spontaneous negative scores 30 26 That your bills go up when they are installed \ they are a rip off 14 12 That they are no good \ people don't like them 10 9 That they are unreliable \ inaccurate 5 3 That they are a risk to health \ are unsafe \ cause fires 3 2 They are expensive \ costly to install 5 2 Other 24 31 Q23. What have you heard? Base: All respondents aware of Smart Meters (as shown)

42

Customer Engagement Study July 2013

4.9.2 Interest in Smart Meters A segment of the qualitative participants were interested in the idea of Smart Meters, particularly those from bigger households and those who were heavier users to help them plan and control usage, and further limit expenditure. It was also felt they could help identify faulty appliances, such as a fridge that was overusing. However, there was a relatively strong belief amongst many that it would be only necessary to study it for a short period of time (say a week); to get an idea of patterns of usage and to make changes, and therefore it would be preferable to rent one for that time. Some also felt it would be a hassle to have to keep checking it, and in reality whilst remote access may be interesting to see what was being used when you were not there, again it was more of a one off need.

“It’s for people with too much time on their hands”

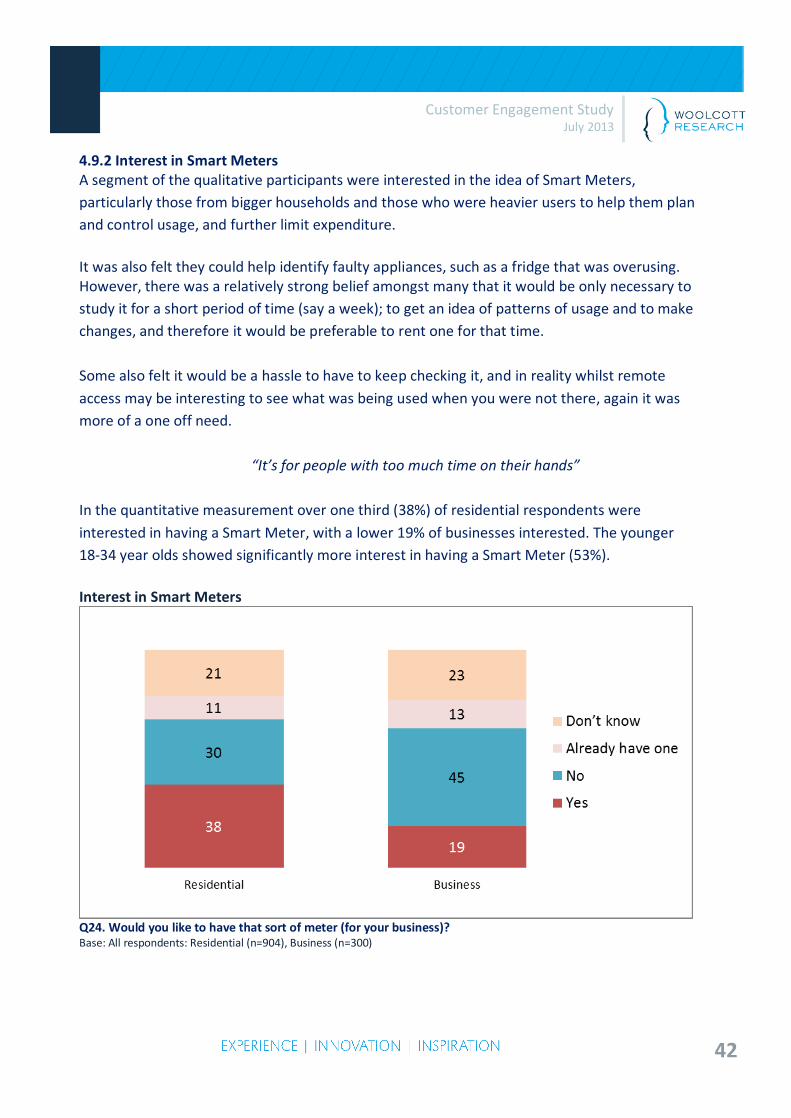

In the quantitative measurement over one third (38%) of residential respondents were interested in having a Smart Meter, with a lower 19% of businesses interested. The younger 18-34 year olds showed significantly more interest in having a Smart Meter (53%).

Interest in Smart Meters

Q24. Would you like to have that sort of meter (for your business)? Base: All respondents: Residential (n=904), Business (n=300)

43

Customer Engagement Study July 2013

4.9.3 Willingness to Pay for Smart Meters Whilst there were some interested in having a Smart Meter there was little willingness to pay for evident in the group discussions, although some felt that if it was proven that it could help them save they may be interested.

o Those willing felt a cost of around $50 was worth paying, but more as a one off payment.

o Some stated that it was ‘just a gimmick’ and another means of making money for Ausgrid.

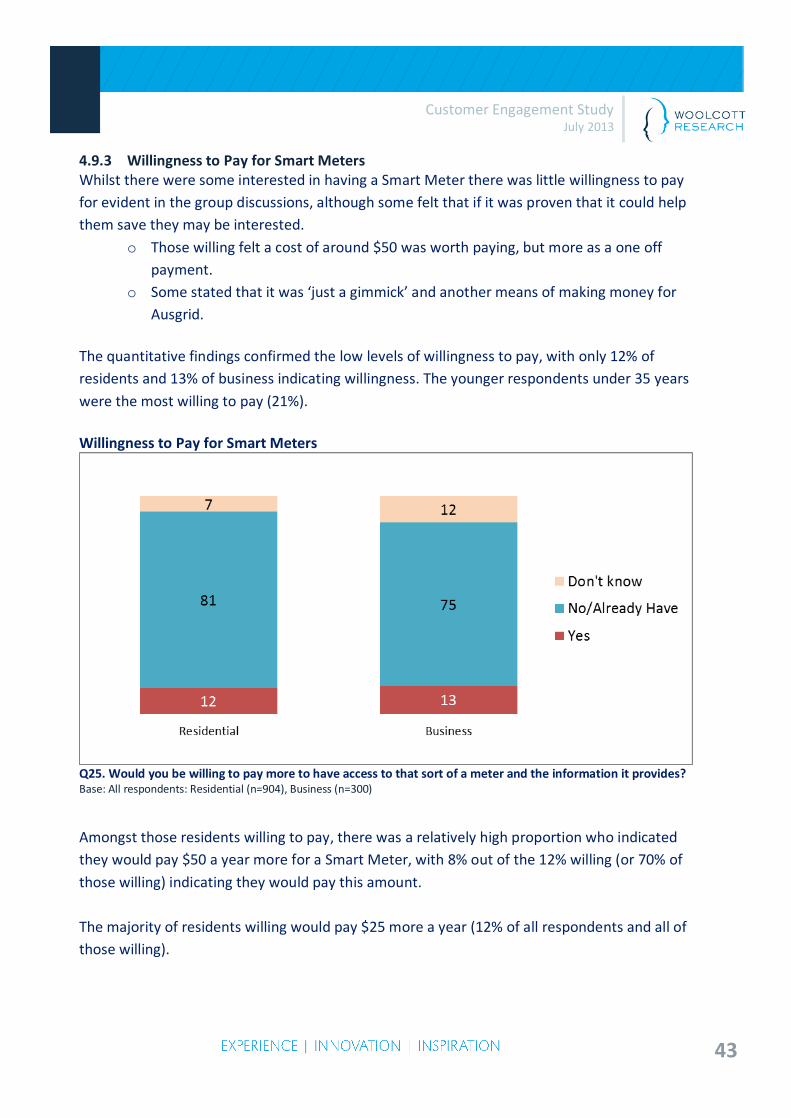

The quantitative findings confirmed the low levels of willingness to pay, with only 12% of residents and 13% of business indicating willingness. The younger respondents under 35 years were the most willing to pay (21%).

Willingness to Pay for Smart Meters

Q25. Would you be willing to pay more to have access to that sort of a meter and the information it provides? Base: All respondents: Residential (n=904), Business (n=300) Amongst those residents willing to pay, there was a relatively high proportion who indicated they would pay $50 a year more for a Smart Meter, with 8% out of the 12% willing (or 70% of those willing) indicating they would pay this amount. The majority of residents willing would pay $25 more a year (12% of all respondents and all of those willing).

44

Customer Engagement Study July 2013

Amount Willing to Pay for Smart Meters- Residents

Q25b.-25e. Would you be willing to pay …more a year? Base: All respondents: Residential (n=904)

Amongst businesses, there was a tendency to be more likely to pay 5% more (10% of all businesses or 77% of those willing to pay, whilst all of those willing to pay would pay 1% more a year (13% of the total businesses). Amount Willing to Pay for Smart Meters – Business

Q25b.-25e. Would you be willing to pay …% more a year? Base: All respondents: Business (n=300)

45

Customer Engagement Study July 2013

4.9.4 Reactions to Metering Charges When the concept of costs involved in the provision and maintenance of meters was raised in the qualitative research, most participants had never considered this aspect. They tended not to see it as a cost that consumers should pay, and presumed it was just a cost of doing business for Ausgrid, which should not be charged to the customer.

“Providing meters is just part and parcel of the service” Further to that, most felt that the concept of ‘unbundling’ the meter costings from the bill, and having to shop around and take up a separate contract with another supplier was just another complication which they did not need, unless they wanted a particular type of meter. There would have to be significant savings for it to be worthwhile. They also felt that this could lead to cheaper meters being sold by those without expertise, which could impact safety and accuracy. In that sense there was more confidence in Ausgrid as ‘the experts’ in the field. Most could not recall their meter being serviced or repaired, and they could not see the point of replacing something that already works. Across the groups one or two were interested in the opportunity to save money by shopping around, but there were concerns about then having separate bills and keeping track of what was what. One or two of the medium businesses were particularly interested in the concept as it provided another opportunity for them to proactively save costs. The quantitative research also indicated that whilst there was a segment of both residents and businesses who were interested in the idea if it resulted in a cost saving, a higher proportion were negative, seeing it resulting in extra costs, and as being more complex to understand.

46

Customer Engagement Study July 2013

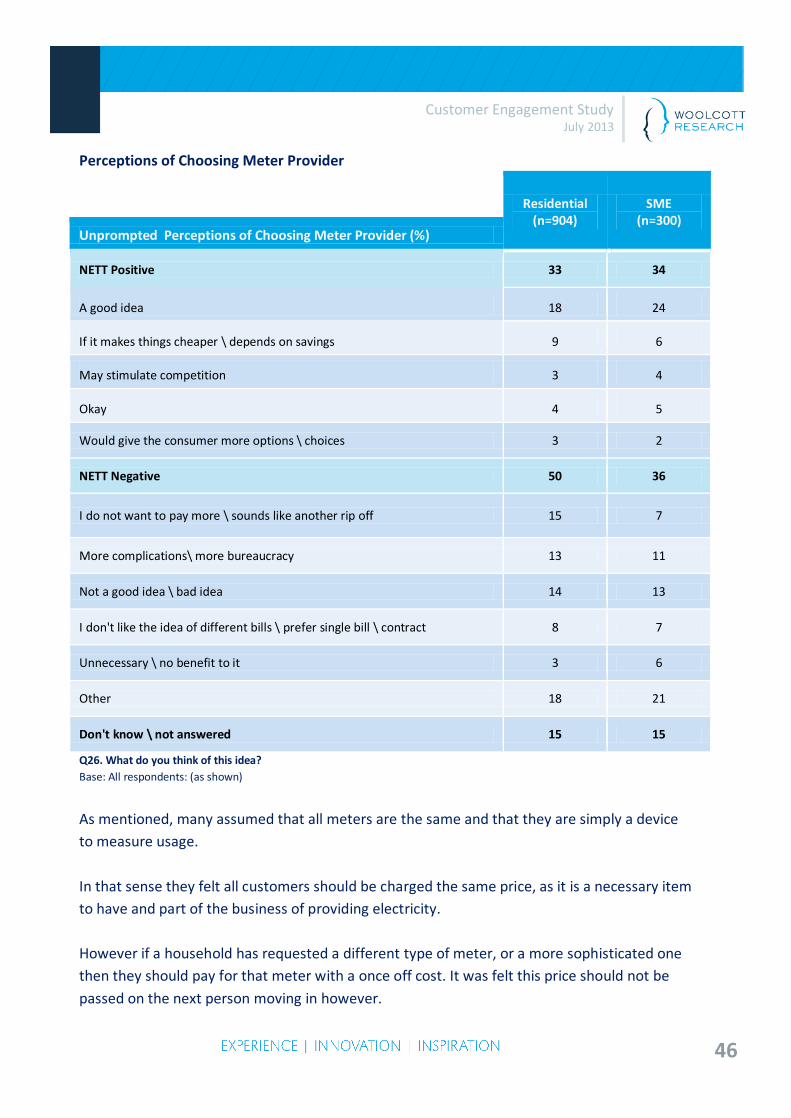

Perceptions of Choosing Meter Provider

Residential

(n=904) SME

(n=300) Unprompted Perceptions of Choosing Meter Provider (%) NETT Positive 33 34 A good idea 18 24

If it makes things cheaper \ depends on savings 9 6

May stimulate competition 3 4

Okay 4 5

Would give the consumer more options \ choices 3 2

NETT Negative 50 36 I do not want to pay more \ sounds like another rip off 15 7

More complications\ more bureaucracy 13 11

Not a good idea \ bad idea 14 13

I don't like the idea of different bills \ prefer single bill \ contract 8 7

Unnecessary \ no benefit to it 3 6

Other 18 21 Don't know \ not answered 15 15 Q26. What do you think of this idea? Base: All respondents: (as shown)

As mentioned, many assumed that all meters are the same and that they are simply a device to measure usage. In that sense they felt all customers should be charged the same price, as it is a necessary item to have and part of the business of providing electricity. However if a household has requested a different type of meter, or a more sophisticated one then they should pay for that meter with a once off cost. It was felt this price should not be passed on the next person moving in however.

47

Customer Engagement Study July 2013

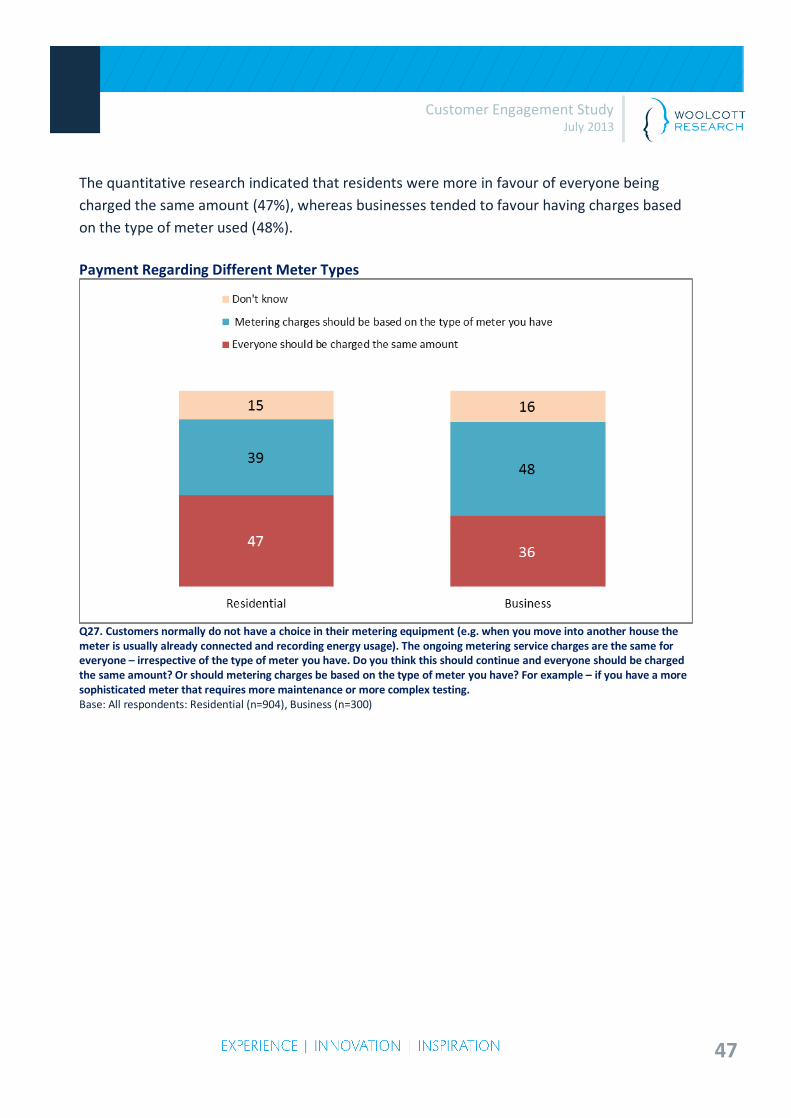

The quantitative research indicated that residents were more in favour of everyone being charged the same amount (47%), whereas businesses tended to favour having charges based on the type of meter used (48%). Payment Regarding Different Meter Types

Q27. Customers normally do not have a choice in their metering equipment (e.g. when you move into another house the meter is usually already connected and recording energy usage). The ongoing metering service charges are the same for everyone – irrespective of the type of meter you have. Do you think this should continue and everyone should be charged the same amount? Or should metering charges be based on the type of meter you have? For example – if you have a more sophisticated meter that requires more maintenance or more complex testing. Base: All respondents: Residential (n=904), Business (n=300)

48

Customer Engagement Study July 2013

4.10 Awareness and Perceptions of Time Based Pricing Some of the qualitative participants, particularly those from Gosford or Newcastle reported that they were using time based pricing now, with mention of off peak, shoulder and peak charges. Those using it felt that it worked well and had helped them better plan and save, for example doing washing/dishwashing late at night. They liked that it offered the opportunity for personal control of usage. Some however could not understand why electricity would cost less at certain times, but they did understand when it was explained in terms of demand. Overall, most felt to be quite a good means of evening out demand, provided the cost of peak use was not too extreme. Many of those living in units tended to believe that it was not possible for them to take full advantage of Time of Use pricing, with body corporate rules about washing and driers, and noise after hours. Others felt that their electricity usage was a necessity when they did use it, and did not want to be hindered from using at peak times, when they felt it was necessary or desirable for them to do so.

“If I’m using it, I’m using it’

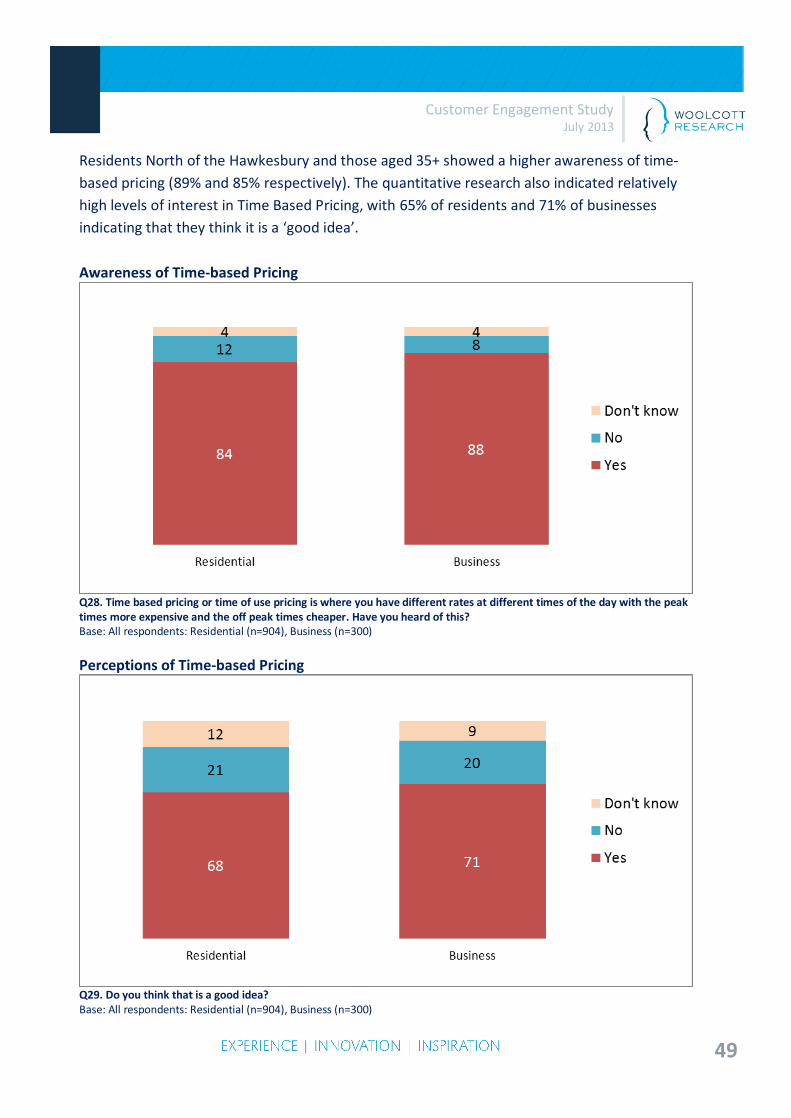

The perceived usefulness to business depended very much on what sort of business it was, with some feeling they were simply unable to change their electricity needs from peak to off peak, as the peak hours were when they most needed electricity. Some felt the ‘shoulder’ time was useful for them (2pm till 7pm) as they could schedule some things for that time, and some medium businesses (such as manufacturing and hospitality) felt they could schedule some of their operations for off peak times, (such as regular emailing, other sorts of processing, using shifts of workers) but they did feel that the majority of their usage had to be between daytime hours. “Customers want services during the day” The quantitative research confirmed the high levels of awareness of time based pricing, with 84% of residents and 88% of businesses indicating they were aware of it.

49

Customer Engagement Study July 2013

Residents North of the Hawkesbury and those aged 35+ showed a higher awareness of time-based pricing (89% and 85% respectively). The quantitative research also indicated relatively high levels of interest in Time Based Pricing, with 65% of residents and 71% of businesses indicating that they think it is a ‘good idea’. Awareness of Time-based Pricing

Q28. Time based pricing or time of use pricing is where you have different rates at different times of the day with the peak times more expensive and the off peak times cheaper. Have you heard of this? Base: All respondents: Residential (n=904), Business (n=300) Perceptions of Time-based Pricing

Q29. Do you think that is a good idea? Base: All respondents: Residential (n=904), Business (n=300)

50

Customer Engagement Study July 2013

4.11 Communication and Engagement The reactions from the qualitative research suggest that the majority do not expect a great deal of communication from Ausgrid, and most tended to felt they received enough information about electricity currently from either Ausgrid (for example when doing work in the area), or the retailer (with regard to their bills and energy efficiency). Communicating further with customers was not felt to be Ausgrid’s role, particularly if it meant it could impact on costs. However, there was a call for specific communication, particularly to help clarify why electricity costs have increased dramatically, and where the money was going. Some (more particularly the businesses) felt Ausgrid should communicate more about their corporate structure, their governance, and about their relationship with the NSW Government as this was not clear to them, and it impacted on their reactions to price increases. That is, as discussed earlier, some were not sure of the ownership of Ausgrid, and they therefore presumed any increases in charges were to benefit shareholders, possibly corporate organisations. A few were curious to know what the long term thinking was within Ausgrid about energy sources such as solar or nuclear, and some wanted to know more about the technology and products that were available to help them reduce their costs, such as meters and any other options there may be. None were however particularly willing to pay extra for further communication.

51

Customer Engagement Study July 2013

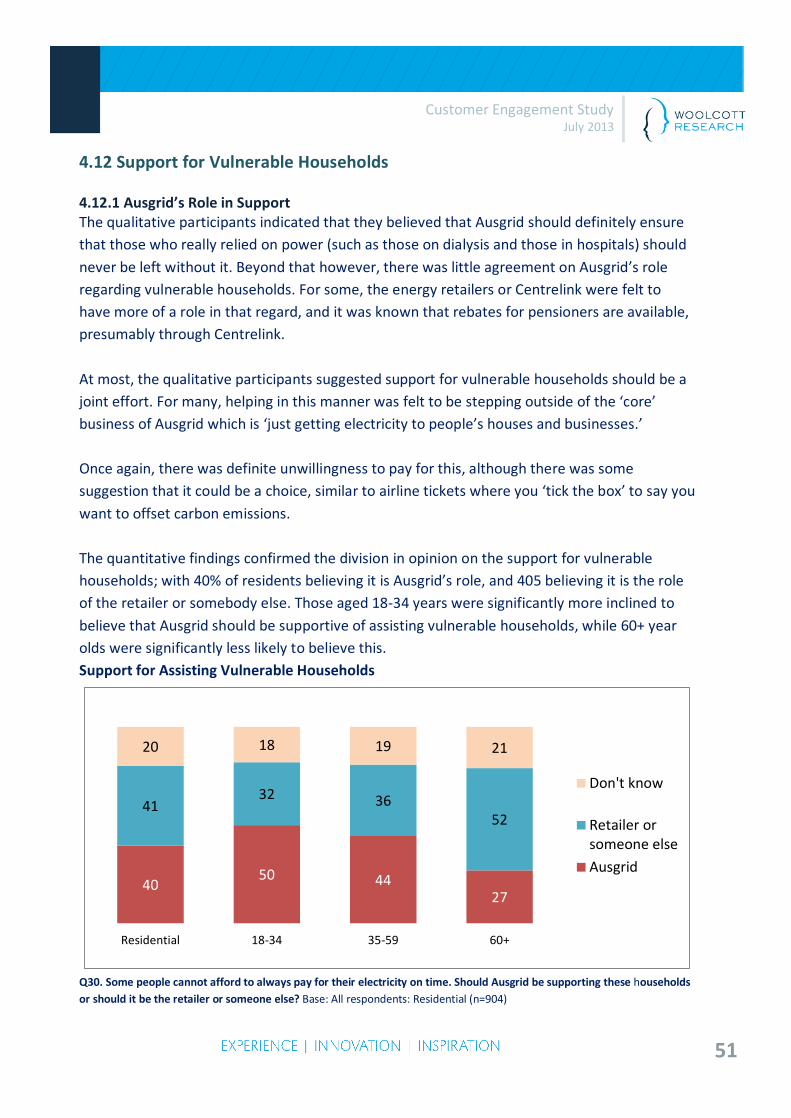

4.12 Support for Vulnerable Households 4.12.1 Ausgrid’s Role in Support The qualitative participants indicated that they believed that Ausgrid should definitely ensure that those who really relied on power (such as those on dialysis and those in hospitals) should never be left without it. Beyond that however, there was little agreement on Ausgrid’s role regarding vulnerable households. For some, the energy retailers or Centrelink were felt to have more of a role in that regard, and it was known that rebates for pensioners are available, presumably through Centrelink. At most, the qualitative participants suggested support for vulnerable households should be a joint effort. For many, helping in this manner was felt to be stepping outside of the ‘core’ business of Ausgrid which is ‘just getting electricity to people’s houses and businesses.’ Once again, there was definite unwillingness to pay for this, although there was some suggestion that it could be a choice, similar to airline tickets where you ‘tick the box’ to say you want to offset carbon emissions. The quantitative findings confirmed the division in opinion on the support for vulnerable households; with 40% of residents believing it is Ausgrid’s role, and 405 believing it is the role of the retailer or somebody else. Those aged 18-34 years were significantly more inclined to believe that Ausgrid should be supportive of assisting vulnerable households, while 60+ year olds were significantly less likely to believe this. Support for Assisting Vulnerable Households

4050 44

27

4132 36

52

20 18 19 21

Residential 18-34 35-59 60+

Don't know

Retailer orsomeone else

Ausgrid

Q30. Some people cannot afford to always pay for their electricity on time. Should Ausgrid be supporting these households or should it be the retailer or someone else? Base: All respondents: Residential (n=904)

52

Customer Engagement Study July 2013

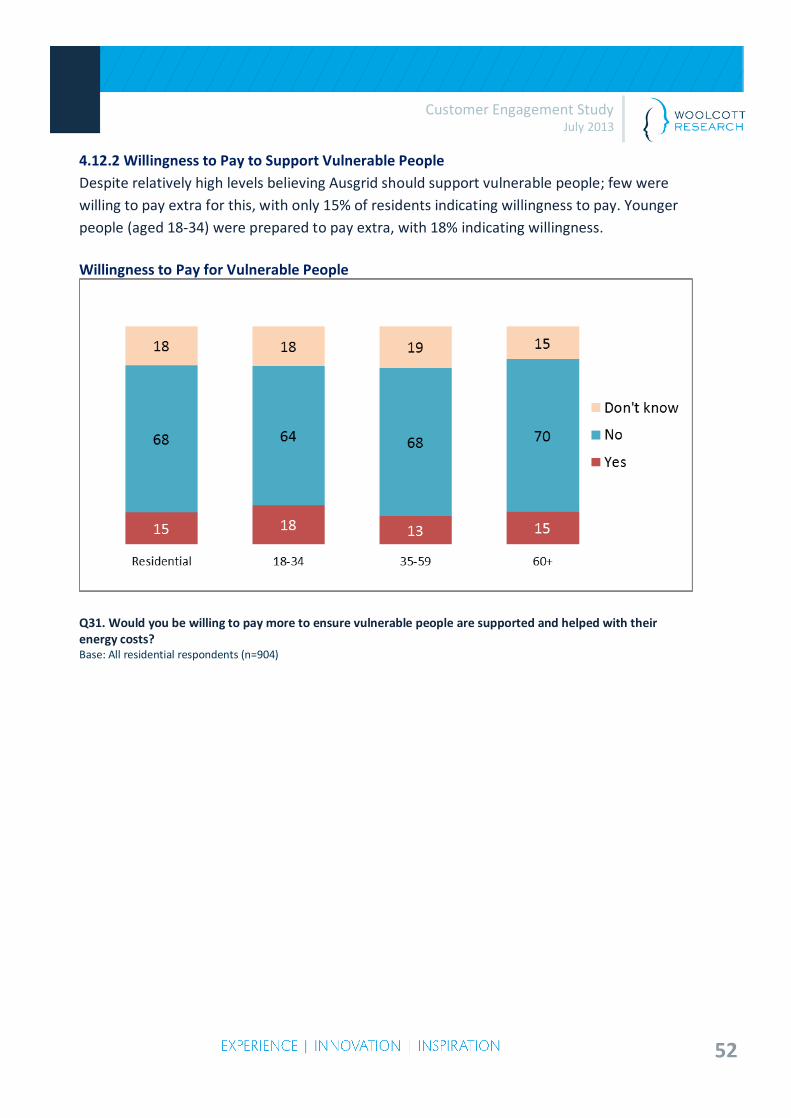

4.12.2 Willingness to Pay to Support Vulnerable People Despite relatively high levels believing Ausgrid should support vulnerable people; few were willing to pay extra for this, with only 15% of residents indicating willingness to pay. Younger people (aged 18-34) were prepared to pay extra, with 18% indicating willingness.

Willingness to Pay for Vulnerable People

Q31. Would you be willing to pay more to ensure vulnerable people are supported and helped with their energy costs? Base: All residential respondents (n=904)

53

Customer Engagement Study July 2013

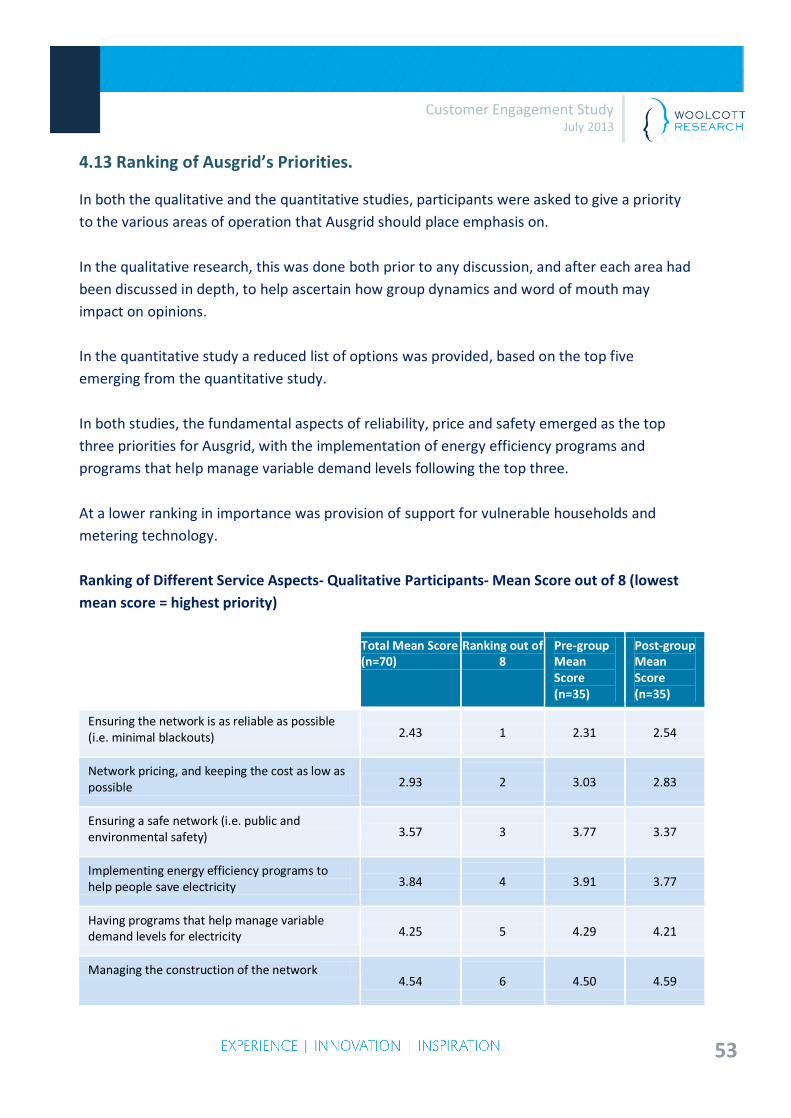

4.13 Ranking of Ausgrid’s Priorities. In both the qualitative and the quantitative studies, participants were asked to give a priority to the various areas of operation that Ausgrid should place emphasis on. In the qualitative research, this was done both prior to any discussion, and after each area had been discussed in depth, to help ascertain how group dynamics and word of mouth may impact on opinions. In the quantitative study a reduced list of options was provided, based on the top five emerging from the quantitative study. In both studies, the fundamental aspects of reliability, price and safety emerged as the top three priorities for Ausgrid, with the implementation of energy efficiency programs and programs that help manage variable demand levels following the top three. At a lower ranking in importance was provision of support for vulnerable households and metering technology. Ranking of Different Service Aspects- Qualitative Participants- Mean Score out of 8 (lowest mean score = highest priority)

Total Mean Score (n=70)

Ranking out of 8

Pre-group Mean Score (n=35)

Post-group Mean Score (n=35)

Ensuring the network is as reliable as possible (i.e. minimal blackouts) 2.43 1 2.31 2.54

Network pricing, and keeping the cost as low as possible 2.93 2 3.03 2.83

Ensuring a safe network (i.e. public and environmental safety) 3.57 3 3.77 3.37

Implementing energy efficiency programs to help people save electricity 3.84 4 3.91 3.77

Having programs that help manage variable demand levels for electricity 4.25 5 4.29 4.21

Managing the construction of the network 4.54 6 4.50 4.59

54

Customer Engagement Study July 2013

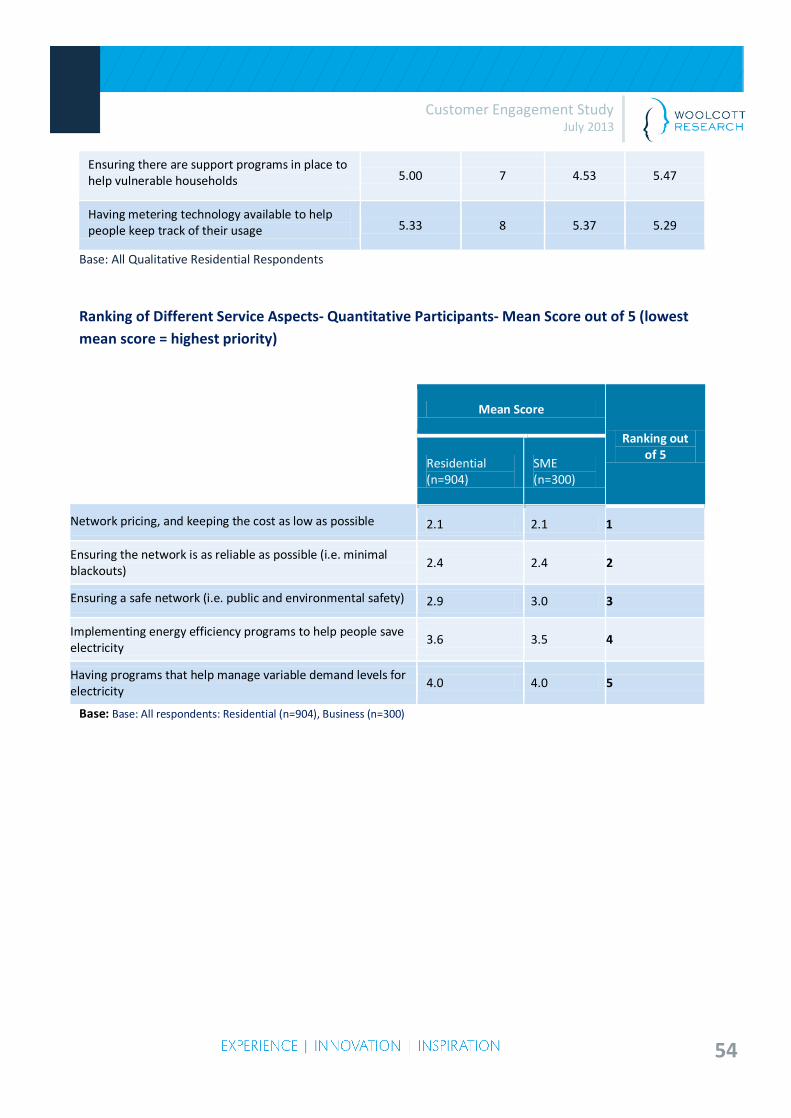

Ensuring there are support programs in place to help vulnerable households 5.00 7 4.53 5.47

Having metering technology available to help people keep track of their usage 5.33 8 5.37 5.29

Base: All Qualitative Residential Respondents Ranking of Different Service Aspects- Quantitative Participants- Mean Score out of 5 (lowest mean score = highest priority)

Mean Score

Ranking out of 5

Residential (n=904)

SME (n=300)

Network pricing, and keeping the cost as low as possible 2.1 2.1 1

Ensuring the network is as reliable as possible (i.e. minimal blackouts)

2.4 2.4 2

Ensuring a safe network (i.e. public and environmental safety) 2.9 3.0 3

Implementing energy efficiency programs to help people save electricity

3.6 3.5 4

Having programs that help manage variable demand levels for electricity

4.0 4.0 5

Base: Base: All respondents: Residential (n=904), Business (n=300)

55

Customer Engagement Study July 2013

5. Conclusions and Implications General Awareness The findings suggest that unprompted awareness of Ausgrid as the electricity distributor was relatively low, with businesses slightly more likely to be aware than residents. When prompted however awareness of the Ausgrid name was high, with businesses being significantly more aware than residents. The qualitative research suggested however that while the ‘brand’ name was known when prompted, actual knowledge of the organisation and its ownership was vague, with some confusion around government or private ownership. This confusion led to some scepticism and lack of trust, with some of those who suspected there was private ownership attributing price rises to the need to provide shareholders with a return. These findings suggest it may be useful for Ausgrid to better inform its customers about the structure and ownership, to eliminate that suspicion. Perceived Reliability Customers were generally very satisfied with the reliability of their service, with the majority of respondents scoring their reliability at over eight points out of ten. Many felt it had improved over recent years. Businesses gave a significantly higher rating in scores 8-10 (90% for businesses compared to 73% for residents. Given this already high standard, there was little willingness to pay more for a higher level of reliability. Safety Many customers found it quite difficult to envision safety risks that might ensue from electricity distribution, with the main risks perceived including the risk of fatalities and injuries from electric shocks; (18% residential, 36% businesses), and workers electrocuting themselves (4% residential, 26% businesses). Around two in ten of both residents and businesses were however willing to pay more for greater levels of safety. Underground vs. Overhead Construction

56

Customer Engagement Study July 2013

Whilst many of the residential customers did not feel underground cabling was worth paying extra for, there was a segment of just over a quarter (28%) of residents who indicated that they that were willing to pay more for this. Families with older children were significantly more willing to pay (37%), and residents with higher incomes were slightly more willing to pay (30%), as were Sydney residents (30%). Pricing/Forecasting A significant proportion of both residents and businesses had seen high increases in their electricity bills over the past year (52% of businesses claimed their bills had risen a lot and 45% of residents felt this). This feeling caused some angry discussion within the qualitative research, with few having a clear understanding of why the increases had been so steep. It would seem there is a need to better explain this if prices were to rise again in the future. These rises did inhibit many from expressing any willingness to pay more for the aspects being covered by the research. When questioned regarding whether they would, in the event of the need for a “one-off’ type price rise, prefer steady increases over several years, rather than an initial steep increase and then a levelling out, there was a clear preference for the steady increases (92% of residents and 91% of businesses) because it reduced the shock of the steep increase in one year. Connection Fees Over two thirds of respondents were aware of connection fees associated with their electricity supply. When questioned about how connection fees should be charged, there was a significant divide between residents and businesses: residents had a strong preference (64%) for everyone paying the same amount while businesses showed a strong preference for some paying more and some paying less (70%). Energy Efficiency Programs The majority of residents in the research claimed they had made some effort (a little or a lot) to reduce their electricity usage as a result of the higher prices (95% of resident and 93% of businesses). Residents North of the Hawkesbury and older respondents (60+) were significantly more likely to suggest that they had devoted ‘a lot’ of effort into reducing usage (63% and 64% respectively).

57

Customer Engagement Study July 2013