Customer Concentration and Cost Structure -...

40

Customer Concentration and Cost Structure Hsihui Chang KPMG Professor of Accounting LeBow College of Business Drexel University Philadelphia, PA 19104 Curtis M. Hall Assistant Professor LeBow College of Business Drexel University Philadelphia, PA 19104 Michael T. Paz PhD Candidate LeBow College of Business Drexel University Philadelphia, PA 19104 May, 2014

Transcript of Customer Concentration and Cost Structure -...

Customer Concentration and Cost Structure

Hsihui Chang KPMG Professor of Accounting

LeBow College of Business Drexel University

Philadelphia, PA 19104

Curtis M. Hall Assistant Professor

LeBow College of Business Drexel University

Philadelphia, PA 19104

Michael T. Paz PhD Candidate

LeBow College of Business Drexel University

Philadelphia, PA 19104

May, 2014

Customer Concentration and Cost Structure

Abstract

This study examines the effects of customer concentration levels on firm cost structure decisions. Customer concentration and associated risks are becoming an increasingly important area of concern given the observed increase in customer base concentration. While prior research has examined the relationship between customer concentration and other important firm-level characteristics, including operations and capital structure, it has not directly examined the relationship between customer concentration and cost structure within firms. We find a negative relationship between customer concentration and cost elasticity, with firms exhibiting lower ratios of variable-to-fixed costs in the presence of higher levels of customer concentration. We also identify supplier industry competition and product specificity as having a moderating influence on the relationship between customer concentration and cost elasticity. Our results are robust to alternate specifications of customer concentration and additional control variables.

JEL: M41; L25.

Keywords: customer concentration; cost structure; cost elasticity; industry competition; product specificity.

1

I . INTRODUCTION

This paper examines the impact of customer concentration on firm cost structure

decisions, which are among the most important strategic decisions made by managers (Banker et

al. 2014). The

only impacts firm operations, but also its ability to realize profit from those operations. More

rigid cost structures (i.e. cost structures that include a higher proportion of fixed costs to variable

costs) generally lead to higher contribution margins relative to more flexible cost structures,

thereby allowing firms to generate higher levels of profit when sales are strong. Cost structure

can also be difficult to change in the short-run, particularly when it contains a high proportion of

fixed costs, due to the difficulties involved in eliminating committed resources. It is therefore not

surprising that cost structure decisions incorporate a variety of operating and environmental

factors, including economic, regulatory, and production considerations. Despite the fact that

both academics and practitioners have highlighted customer-base concentration as a critical

environmental consideration for firms, prior literature has not considered the potential

relationship between customer concentration and firm cost structure.

Customer concentration and relationships with major customers have become an

increasingly important area of interest for both researchers and practitioners as customer bases

become more concentrated (Patatoukas 2012). The manufacturing sector, in particular, has seen

significant increases in customer concentration over the past few decades (Kelly and Gosman

2000). Aside from its financial performance implications, customer concentration also

influences firm-level decisions related to capital structure and operations. For example, the

presence of major customers can impact firm-level decisions related to the breadth and depth of

its product offerings (Ketokivi and Jokinen 2006). Prior literature on the firm-level effects of

2

customer concentration provides conflicting predictions as to its potential impact on firm cost

structure. Economic dependencies which arise between a supplier and their major customers

grow as those customers contribute a higher proportion of firm revenues. This economic

dependence creates significant financial risks for the supplier. By contrast, firms may also derive

operating benefits from their relationships with major customers as a result of mutually

beneficial cooperation. These conflicting effects of customer concentration on the internal

operating environments of firms make it difficult to predict its effect on firm cost structure.

While recent literature has examined the impact of other environmental factors on firm cost

structure decisions, it remains an open empirical question as to how customer concentration

influences such decisions within firms. Thus, it is important to understand the relationship

between customer concentration and firm cost structure within the manufacturing sector.

To address our research question we use cost data from a sample of U.S. manufacturing

firms between the years 1976 through 2013. Following Kallapur and Eldenburg (2005) and

Banker et al. (2014), we specify a log-linear model to examine changes in firm cost structure.

We employ a measure of customer concentration used in prior literature (Patatoukas 2012) to

examine the impact of customer concentration on firm cost elasticity. This measure provides

by calculating the

proportion of total sales revenue contributed by each major customer and summing those

proportions. Our empirical results demonstrate a negative association between customer

concentration and cost elasticity among suppliers within the manufacturing sector, with suppliers

increasing their proportion of fixed-to-variable costs as their customer base becomes more

concentrated. Furthermore, we examine the moderating influence of supplier industry

competition and product specificity and find that both exacerbate the impact of customer

3

concentration on supplier cost elasticity. Our results are robust to alternate specifications of

customer concentration and the inclusion of controls for demand uncertainty, leverage, and asset

and employee intensity.

Our study makes several contributions to the literature. We contribute to the literature on

cost behavior by identifying customer concentration as a determinant of firm cost structure.

This finding may help reconcile conflicting results from prior research related to cost behavior.

Our identification of supplier industry competition and product specificity as moderators of the

relationship between customer concentration and firm cost structure also highlights the

importance of considering interactions between internal and external environmental factors

which influence firm operations. Furthermore, our results add to the growing body of literature

on the impact of customer concentration and major customers on firms by examining how firms

adjust their operations in response to risks and opportunities arising from customer base

concentration.

The rest of the paper is organized as follows: Section II provides an overview of relevant

literature and develops hypotheses related to our research questions. Section III includes a

description of our sample, related descriptive statistics, and our estimation models. Section IV

presents and discusses our empirical results, after which Section V provides our concluding

remarks.

I I . LITERATURE REVIEW AND HYPOTHESIS DEVELOPMENT

Customer Concentration

customer

exhibit a higher level of customer concentration (Patatoukas 2012). The Statement of Financial

4

Accounting Standards (SFAS) 131 (FASB 1997) requires that firms disclose the presence of any

and all customers which contribute 10% of enterprise-wide revenue, either to a single segment or

across multiple segments. T

reflects the traditional view that customer concentration presents significant risks for firms.

Scherer (1970) and Gosman and Kohlbeck (2009) suggest that a customer power increases in

their level of contribution to firm sales revenue. As customer power grows, suppliers face

mounting incentives to retain the business of major customers and, consequently, reduced

bargaining power.

Reductions in supplier bargaining power resulting from customer concentration have

been shown to have a negative impact on operational performance. Lustgarten (1975) finds that

reduced supplier power results in a negative relationship between customer concentration and

profit margins. Galbrath and Stiles (1983) similarly find that more concentrated customer bases

are associated with lower operating profit margins related to downward price pressure from

customers. Gosman and Kohlbeck (2009) document negative relationships between the presence

of major customers and both gross margins and return on assets (ROA). These negative

profitability effects reflect increased levels of idiosyncratic risk associated with the potential

adverse demand, sales growth, stock market, and default risk impacts of losing a major customer

(Albuquerque et al. 2010). Balakrishan et al. (1996) similarly find that firms with higher levels of

customer concentration experience greater declines in ROA in response to adopting Just-in-Time

(JIT) production methods. Customer concentration is also positively related to bankruptcy risk

(Becchetti and Sierra 2003) and the probability of receiving a going concern opinion (Dhaliwal

et al. 2013) stemming from the potential for major customer defection. Cohen and Frazzini

(2008) find that relationships between suppliers and their strong customers create economic

5

dependence between the two firms such that economic shocks to one firm lead to a reciprocal

shock in the other. This economic dependence arises in part from relationship-specific

investments with limited transferability and liquidity (Raman & Shahrur 2008). Bae and Wang

(2010) also find that firms with major customers face increased distress costs upon entering

bankruptcy , resulting in such firms maintaining higher cash levels to stave off the liquidation of

relationship-specific investments in the event of financial distress.

Despite the aforementioned negative effects, customer concentration has also been

shown to accrue benefits to suppliers. Gosman & Kohlbeck (2009) find that major customers are

associated with improved inventory and payables management among suppliers. Lilien (1983)

finds that firms with higher levels of customer concentration spend less money on marketing and

trade show participation. More generally, Patatoukas (2012) find that firms with major customers

benefit from lower sales, general, and administrative (SG&A) costs, higher ROA, and higher

return on equity (ROE). Matsumura and Schloetzer (2012) also document increased asset

turnover in the presence of major customers which they suggest reflects improvements in

demand forecasting and inventory management arising from cooperation between suppliers and

their major customers. A number of other studies support their view that higher levels of

coordination and information sharing between suppliers and their major customers can benefit

suppliers. Kulp et al. (2004) observe increased supplier margins associated supplier-customer

cooperation on inventory replenishment and improved performance associated with supplier-

customer cooperation on product/service development. Additionally, information sharing on

inventory and product needs generally improves both supplier profitability and customer

inventory management, suggesting the existence of financial incentives for supplier-customer

cooperation. Schloetzer (2012) finds additional incentives for customers to cooperate with

6

suppliers through process integration and sharing in the form of improved financial performance

associated with such cooperation. Wasti & Liker (1997), using survey data from a group of

Japanese automotive component suppliers, finds that supplier-customer cooperation on product

design benefits the supplier through improved design for manufacturability and the customer

through enhanced conformity between supplier designs and customer product feature demands.

Prior literature suggests conflicting predictions related to the impact of customer

concentration on firm cost structure. Higher levels of customer concentration are associated with

significant financial and operational risks arising from the potential for losing a major customer.

These risks present significant forecasting and planning difficulties which may prompt firms to

use real options and more elastic (i.e. flexible) cost structures as a hedge against default. On the

other hand, cooperation and demand stability associated with strong customer-supplier

relationships likely improves the ability of suppliers to forecast and plan for future production

requirements. Additionally, major customer relationships may necessitate relationship-specific

investments in order to fulfill customer production requirements. While we expect to observe a

relationship between customer concentration and firm cost structure, the aforementioned

operational impacts of customer concentration do not allow us to predict the direction of this

relationship. Therefore, we hypothesize:

H1: Customer concentration will be related to supplier cost elasticity

The Impact of Supplier Industry Competition

Differences in the level of supplier industry competition may have a moderating

influence on the relationship between customer concentration and firm cost structure. Snyder

(1998) developed an analytical model which examines the impact of customer size on supplier

competition. Their model demonstrates that larger buyers are able to obtain lower overall prices

7

on their purchases due to supplier competition for their business. As the incentives to gain or

ease, such customers bargaining power also increases.

Becker and Thomas (2008) demonstrate this phenomenon empirically by identifying spillover

effects between changes in customer industry concentration and subsequent supplier industry

concentration. They attribute this effect to the positive relationship between customer industry

concentration (i.e. customer size) and customer bargaining power. Subsequent changes in

supplier industry concentration are, therefore, explainable attempts to offset changes in customer

bargaining power associated with industry consolidation. Brown et al. (2009) find that investors

understand and trade on this increased risk, resulting in negative abnormal returns for suppliers

whose customers are involved in a leveraged buyout. This evidence suggests that higher levels

of customer concentration signal the presence of larger customers which may attract direct

competition from rival suppliers. As supplier industry competition increases, the prospect that a

supplier may have to

1998). Simultaneously, suppliers in highly competitive industries seek out new customers in an

effort to stimulate firm growth, increase market share, and generate positive returns for investors.

Customer concentration, therefore, likely heightens the uncertainty created by high levels of

industry competition.

Prior literature provides conflicting evidence related to the impact of industry

highly competitive product markets undertake lower levels of current irreversible capital

investments, including fixed asset purchases, when price uncertainty increases. This suggests

. Recent work by

Banker et al. (2014), however, suggests that the introduction of additional demand uncertainty

8

stimulated by industry competition should result in lower levels of cost elasticity as firms guard

against the potential for demand spikes. Customer concentration likely intensifies the effects of

industry competition on cost elasticity, since customer concentration signals the presence of

attractive customers which must be defended from rival suppliers. Since we expect the industry

competition to moderate the relationship between customer concentration and cost elasticity, we

specify the following hypothesis:

H2: Supplier industry competition levels have a moderating effect on the relationship between customer concentration and supplier cost elasticity

The Impact of Product Specificity

Given that prior literature has demonstrated a negative relationship between the breadth

of supplier product offerings and customer concentration (Ketokivi and Jokinen 2006), we also

examine the potential moderating influence of product specificity on the relationship between

customer concentration and firm cost structure. Customer-specific and unique products arise as a

result of information sharing and product design collaboration between suppliers and their major

customers (Anderson & Decker 2009; Wasti & Liker 1997). While supplier-customer product

design cooperation increases the likelihood that customers will be satisfied with the final product

(and, thus, more likely to purchase), producing unique and/or specialized products requires

costly investments in R&D (Titman & Wessels 1998). Such relationship-specific investments in

assets and product design are generally associated with long-term customer relationships and

product differentiation strategies (Ketokivi & Jokinen 2006). Suppliers undertaking such

relationship-spending, however, tend to benefit from increased barriers to entry as a result of

high levels of product specificity which reduce substitutability (Winter & Szulanski 2001).

It is unclear what impact product specificity will have on the relationship between

customer concentration and supplier cost structure. Investments in relationship-specific assets

9

associated with higher levels of customer concentration have been shown to increase transaction

risk (Dekker et al. 2013), economic dependence (Patatoukas 2012), hold-up problems (Grossman

& Hart 1986), earnings volatility and earnings management (Raman & Shahrur 2008), distress

costs associated with bankruptcy, and opportunity costs associated with increased cash holdings

(Bae & Wang 2010). Additionally, losing a major customer represents the potential to seriously

erode the value of any relationship-specific investments (Dhaliwal et al. 2013). Each of these

effects suggests that product specificity creates uncertainty which will lead to lower levels of

fixed costs within a supplier cost structure. Anderson and Decker (2009), however, point out

that relationship-specific investments can increase the cost of switching suppliers and effectively

deter major customers from switching to new suppliers. Kumar (1996) also points out that

relationship-specific investments reflect the presence of trust between suppliers and their major

customers. This trust is realized in the form of greater cooperation and supply chain

coordination (Joshi & Stump 1999), extended trade credit terms provided to customers during

periods of liquidity shock (Cuñat 2007), and greater overall supply-chain stability and efficiency

through trade credit provision (Yang & Birge 2013). These factors suggest that product

specificity reduces uncertainty, potentially leading to higher levels of fixed costs within a

supplier s cost structure. Accordingly, we hypothesize the following:

H3: Product specificity levels have a moderating effect on the relationship between customer concentration and supplier cost elasticity

I I I . DATA AND METHODOLOGY

Sample

We build our sample beginning with major customer information reported in the

Compustat Segment Files following the methodology proposed by Patatoukas (2012). Major

customer data disclosed in the annual reports of manufacturing firms (SIC Codes 20 39)

10

between 1976 and 2013 is gathered from the Compustat Segment Files, including customer

name, type, and revenue contributed to the supplier firm. This customer information is then

matched to the corresponding supplier data from the Compustat Annual File using gvkey codes.

In order to match customers and supplier with different fiscal year end dates, we use the most

recent customer information available as of the month of the -end date. Our

final matched supplier-customer sample consists of all firms reporting at least one major

customer during the sample period.

After compiling our matched supplier-customer sample, we gather additional supplier

financial information related to operating costs and sales revenue. Following Banker et al.

(2014), we focus on three categories of costs: SG&A costs, COGS, and the number of

employees. Additionally, we gather information on a fourth category of costs: total operating

costs. We discard all observations for which either current or lagged sales or total operating costs

are missing. We are left with a final sample of 46,836 firm-year observations across the entire

sample period. Table 1 reports a description of the sample composition by industry.

Observations from firms in the electronic equipment and components industry,

industrial/commercial machinery and computer equipment industry, and chemicals and allied

products industry make up slightly more than 50% of the sample.

< Insert Table 1 About Here >

Descriptive Statistics

Table 2 presents descriptive statistics for our variables of interest. Differences in

numbers of observations across variables are attributable to missing data. While we excluded

observations which did not have total operating cost data, for example, we did not exclude

observations which were missing any of the three sub-categories of operating costs (SG&A,

11

COGS, or # of Employees). Our descriptive statistics are reported in CPI adjusted dollars

deflated using 1982-1984 as the base year. The average (median) firm in our sample reported

sales revenue of $753 ($51) million dollars and total operating costs of $675 ($50) million. As

shown in Table 1, observations with values of log-changes in revenue, total operating costs,

SG&A costs, COGS, or number of employees in the highest and lowest 0.5% of the distribution

are truncated in order to control for the potential influence of outliers on our results.

< Insert Table 2 About Here >

We construct our customer concentration variable (CC) using major customer data

disclosed by firms under the provisions of SFAS 131 (FASB 1997). We adopt a measure

developed by Patatoukas (2012) which uses a modification of the Herfindahl-Hirschman index to

capture both the total number of majo

of firm customer-

base concentration (CC) in year t, essentially a weighted-average index of customer-specific

revenue to total firm revenue, is described by the equation

(1)

where Salesijt represents firm i sales to customer j in year t and Salesit represents total sales for

firm i in year t. Average (median) customer concentration is 0.1333 (0.0622) for our sample of

firms. We also report results using an alternate specification of our customer concentration

This

threshold has been used in prior literature as a proxy for customer concentration (Bae & Wang

2010; Gosman & Kohlbeck 2009; Gosman et al. 2004). 74.84% of firms in our sample report at

least one customer who contributes 10% or more of overall firm revenues.

Model Specification

12

Following a methodology proposed in prior research (Kallapur and Eldenburg 2005;

Banker et al. 2014), we examine our research questions using a log-linear cost function which

regresses log-transformed changes in costs on concurrent log-transformed changes in sales

revenues. Accordingly, we specify the following log-linear cost function for estimation

0 1 2 3GDP (Rev) 4Size 5 6GDPGrowth 7Size (2) 1-19 1-19

where the term is the log-transformed change in costs for a firm between year t-1 and

year t. We estimate Equation (2) using four separate specifications of the term: total

operating costs (OC), selling, general, and administrative costs (SGA), number of employees

(EMP), and cost of goods sold (COGS). The term is specified as the log-transformed

change in revenue for a firm between year t-1 and year t. RankCC refers to a ranked

transformation of the customer concentration measure. We construct the variable RankCC by

first calculating the value for our customer concentration measure as described in Equation (1)

for each firm-year observation. We then rank each firm into deciles based on their customer

concentration score. RankCC is defined as the decile rank of a firm for year t. Size is defined as

the natural log of sales for a firm in year t. GDPGrowth refers to the log-transformed change in

Gross Domestic Product between year t-1 and year t. We include controls for GDP growth (log

change in GDP) and firm size (natural log of sales) as well as interactions between each variable

and log-changes in revenue. Following the procedure described by Peterson (2009), we cluster

by firm standard errors by firm when conducting our analysis. Our model also includes controls

for industry fixed effects (IndFE) and interactions between our industry indicators and log-

changes in revenue . Additionally, we control for the potential impact of

13

outliers on our analysis by truncating observations with values of Rev), OC) ),

) ) in the highest and lowest 0.5% of the distribution.

The slope coefficient 1 in this regression equation provides an approximate measure of

the change in costs associated with a one percent change in sales revenue. A smaller slope

indicates a lower proportion of variable costs and a higher proportion of fixed costs (Banker et

al. 2014). To capture the relationship between customer concentration and cost elasticity using

our cost function specification, we include an interaction term between a ranked transformation

of our customer concentration measure and the log-change in sales revenue (RankCC* ).

A negative sign on the coefficient of 2 for this interaction term would indicate that higher

customer concentration leads to lower cost elasticity (i.e. higher fixed costs), while a positive

sign on the coefficient of 2 would indicate that higher customer concentration leads to higher

cost elasticity (i.e. higher variable costs).

To capture the moderating effects of supplier industry competition and product

specificity on the relationship between customer concentration and cost elasticity, we include an

additional three-way interaction term between our measures of industry competition or product

specificity, a ranked transformation of our customer concentration measure, and the log-change

in sales revenue . This leads to the following log-linear cost function specifications for

estimation

0 1 2 + 3 + 4 + 5 6Size + 7RankCC (3a) + 8HighComp + 9GDPGrowth 10Size + 1-19IndFE + 1-19

0 1 2 + 3 + 4 + 5 6Size + 7RankCC (3b) 8HighRD + 9GDPGrowth 10Size

14

+ 1-19IndFE + 1-19

where the terms HighComp and HighRD are both indicator variables which indicate the

presence of high levels of competition and research and development (R&D) intensity,

respectively, within a firm We construct the variable HighComp which is included in

Equation (3a) by first estimating -Hirschman Index (HHI) using their

three-digit SIC code as a proxy for supplier industry competition (Ellis et al 2012). We then set

the indicator variable HighCo

median and zero otherwise. Similarly, we calculate the variable HighRD which is included in

Equation (3b) by first estimating R&D intensity as the ratio of R&D expense to sales. We adopt

this measure as a proxy for product specificity following the methodology used by Raman and

Shahrur (2008)

intensity is above the industry median and zero otherwise. All other variable definitions are the

same as those described earlier for Equation (2). We summarize our variable definitions in

Appendix A. Note that while we estimate equations (3a) and (3b) for all four specifications of

the term used in estimating Equation (2), we report only those results for total

operating costs (OC) for the purpose of brevity.

IV. EMPIRICAL RESULTS

Correlation Analysis

Table 3 reports correlations among the variables used in our multivariate tests. Spearman

(Pearson) correlations are reported in the upper (lower) diagonal. We observe a negative and

statistically significant correlation between firm -.167, p < .01) and

Rank -.164, p < .01), results which provide preliminary evidence suggesting that

customer bases are more concentrated among smaller firms. We also observe a positive and

15

statistically significant correlation between our measure of demand uncertainty (UNCERT) and

= .253, p < .01) and Rank

findings from prior literature which show that customer concentration is associated with

increased demand uncertainty due to the potential for major customer defection. The magnitude

of the correlations, however, suggests that our customer concentration measures capture aspects

of the operating environment aside from just demand uncertainty. We explore the potential

relationship between customer concentration and demand uncertainty in robustness tests which

are discussed in Section IV.

< Insert Table 3 About Here >

Regression Results

Table 4 presents the regression results of our primary analysis of the effect of customer

concentration on cost structure. Estimates of Equation (2) for each of the four cost categories,

operating costs (OC), SG&A costs (SGA), number of employees (EMP) and cost of goods sold

(COGS) are shown in Columns 1-4, respectively. As expected, the coefficient 1 for ( )

is positive and significant in the estimates of all four cost categories. The coefficient for the

variable of interest, which is the interaction of the customer concentration measure with changes

in revenue ( ) 2. 2 is negative and significant in all four specifications,

indicating that firms with greater customer concentration have less elastic costs structures.

Interpreting the magnitude of the coefficients 1 2 in Column 1, a one percent increase in

revenue increases operating costs by 0.50 percent, on average, for firms in the lowest decile of

customer concentration, but only increases operating costs by 0.37 percent, on average, for firms

in the highest decile of customer concentration. The results presented in Table 4 provide support

16

for H1 and are consistent with firms choosing greater fixed costs compared to variable costs

when they have more concentrated customer bases.

< Insert Table 4 About Here >

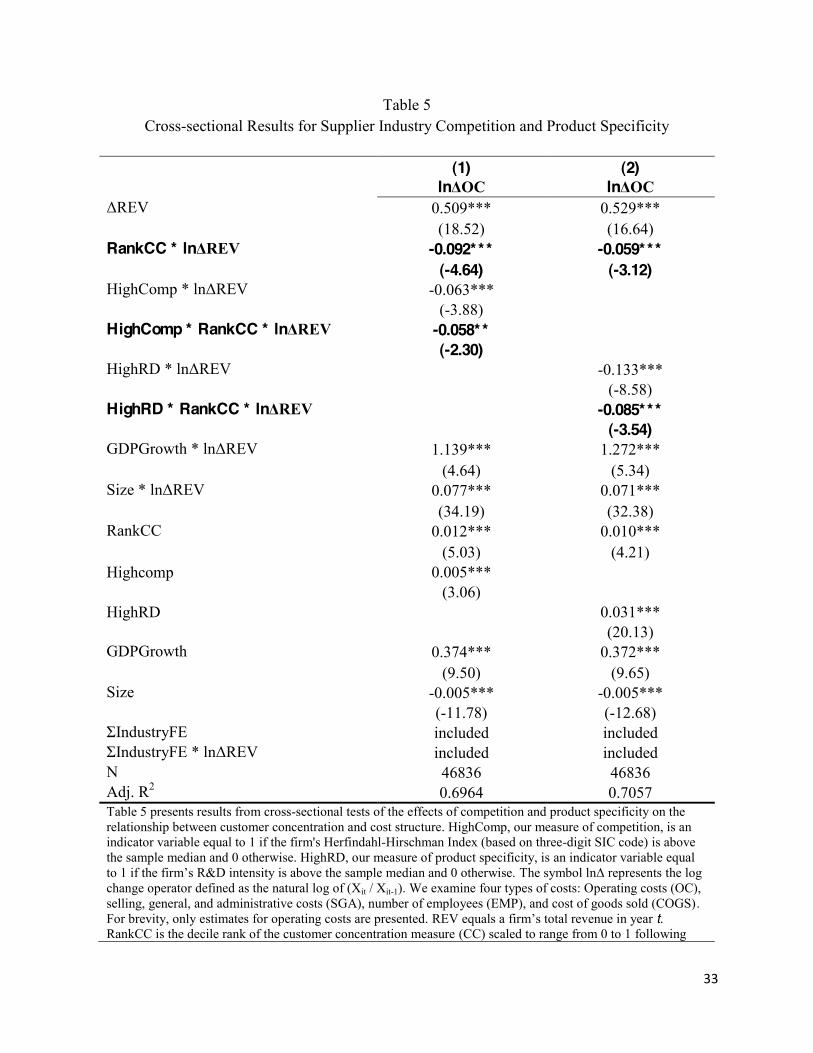

Next we examine the effects of industry competition and product specificity on the

relationship between customer concentration and cost structure. The regression results are

presented in Table 5.1 Column 1 presents estimates for Equation (3a) which examines the effects

of industry competition. The coefficient 4 is for the variable of interest, which is specified as the

three-way interaction of a high competition indicator variable with the customer concentration

measure and changes in revenue (HighComp * )). Additionally we add the

interaction of high competition with changes in revenue to control for the main effect of supplier

industry competition on cost structure as HighComp * ). As we can observe from

Column 1 of Table 5, the coefficients on 3 and 4 are both negative and statistically significant,

providing support for H2. This is consistent with supplier industry competition intensifying the

effect of customer concentration on cost elasticity. On average, a one percent increase in revenue

increases operating costs by 0.42 percent (0.51 - 0.09) for firms with high customer

concentration compared to an increase of 0.30 percent (0.51 - 0.09 -0.06 -0.06) for high customer

concentration firms operating under high competition.

< Insert Table 5 About Here >

Column 2 of Table 5 presents estimates for Equation (3b) which examines the effect of

product specificity on the relationship between customer concentration and cost structure. The

main effect of product specificity on cost structure is captured by 3, the interaction of a high

R&D intensity indicator variable with changes in revenue (HighRD * )). The

1 For brevity, we present only estimates of operation costs in Table 5, but estimates for the other three cost categories lead to the same interpretation. Additionally, operating costs include all of the other three cost categories (SGA, COGS and employee costs).

17

incremental effect of product specificity on the relationship between customer concentration and

cost structure is measured 4 , the three-way interaction term HighRD * ).

As shown in Column 2 of the same table, the coefficients on 3 4 are both negative and

statistically significant, providing support for H3. This result suggests that fixed-to-variable cost

ratios will be higher for firms with higher levels of customer concentration when product

specificity is also high compared to when product specificity is lower.

Additional Analysis and Robustness Checks

To evaluate the robustness of our primary results, we perform the following additional

analysis. First, we include an additional control for the effect of leverage on firm cost structure

decisions. Prior studies have shown that customer concentration is also related to capital

structure decisions. Banerjee et al. (2008) provide evidence that firms with major customers tend

to hold less debt, though Hennessy and Livdan (2009) also find that firms increase in response to

increases in the bargaining power of their business partners. Higher levels of leverage can

potentially affect cost structure by increasing the risk of bankruptcy, which may incentivize

managers to choose more elastic cost structures (Novy-Mark 2011). However, many firms will

use debt financing to pay for fixed assets and relationship-specific investments, both of which

would decrease cost elasticity. We control for the effect of leverage using the indicator variable

HighDebt. We construct the variable HighDebt by first calculating the debt-to-equity ratio for

each firm-year observation. We then set HighDebt equal to one for firm-year observations

which are above the sample median and zero otherwise. Table 6 presents results after controlling

for leverage. In Column 1, we present estimates for a re-specification of Equation (2) which

includes an additional interaction between the HighDebt variable and changes in revenue

(HighDebt )). Columns 2 and 3 present subsample analysis results for Equation (2)

18

with the full sample split between high and low debt firms, respectively 2

remains negative and statistically significant across all three specifications, providing evidence

The difference

between 2 in Columns 2 and 3 are not statistically significant, suggesting that

the effects of customer concentration on firm cost structure is similar across low and high debt

firms. Additionally the coefficient on HighDebt ) is positive and significant at the

10% level which indicates that firms may chose more elastic cost structures to guard against

bankruptcy risk.

< Insert Table 6 About Here >

Second, we control for the previously identified effect of demand uncertainty on firm cost

structure. Customer concentration may also increase demand uncertainty since the reliance on a

small number of major customers can result in large swings in demand if one customer withdrew

their business. We control for the effect of demand uncertainty (UNCERT) by adopting a

measure from Banker et al. (2014). The variable UNCERT is calculated as the standard deviation

of log-changes in sales for all observations for a firm. UNCERT is not calculated for firms with

fewer than 10 firm-year observations, with such firms being excluded from robustness tests

related to demand uncertainty. Estimates for all four cost categories after controlling for demand

uncertainty are presented in Table 7. The sample observations decrease from our main analysis

because the UNCERT measure requires 10 years of observations within our sample period. The

2 is negative and statistically significant in all four columns, providing evidence

that our results are not being driven by demand uncertainty.

< Insert Table 7 About Here >

19

Third, we control for the impact of employee and asset intensity, both important

determinants of cost elasticity. We intentionally excluded such controls from our primary tests

of fixed assets and employees used in production. Therefore, including controls that are

measures of these decisions may unnecessarily bias us against finding the relationship between

customer concentration and cost structure. Nonetheless, we follow Holzhacker et al. (2014) and

modify our cost structure model to include measures of employee (EMPINT) and asset intensity

(ASINT). ASINT is calculated for each firm-year observation as gross property, plant, and

equipment (PPE) divided by sales. EMPINT is calculated for each firm-year observation as the

number of employees (EMP) divided by sales. The results of these regression estimates are

presented in Table 8. Unsurprisingly, greater asset intensity results in lower cost elasticity while

greater employee intensity results in greater cost elasticity. More importantly, the coefficient on

the interaction RankCC and change in revenue ( ) is still negative and

statistically significant after controlling for employee and asset intensity.

< Insert Table 8 About Here >

Fourth, we present several subsample analyses in Table 9 in order to demonstrate the

generalizability of our results. Specifically, we re-estimate Equation (2) for four subsamples of

our full sample. Since the cutoff for mandatory disclosure of a major customer is 10 percent of

total sales, we exclude firms that do not report at least one customer with sales equal to or greater

than 10 percent of its total sales in Column 1. In Column 2, we exclude all firms that cannot be

linked to another publicly traded firm in Compustat because many studies use these links when

examining supply chain relationships. In Column 3, we exclude firms with less than 10 million

dollars in assets because customer concentration is negatively associated with firm size. In

20

Column 4, we examine the subsample of observations after the passage of SFAS 131 in 1997.

The coefficient on 2 is negative and statistically significant across all four subsamples. In

untabulated results, we also measure customer concentration using the raw CC score from

Patatoukas (2012) and using an indicator variable for whether the firm has at least one customer

which accounts for more than 10 percent of its sales. Our results are qualitatively unchanged

when using these measures.

< Insert Table 9 About Here >

Fifth, we investigate potential multicollinearity in our analysis by calculating variable

inflation factors (VIFs) for all regressions reported in Tables 4 through 9. Greene (2008)

suggests a VIF cutoff value of 10 as indicating a high level of multicollinearity. In untabulated

results, VIFs are below 10 for all variables except for in our reported results, suggesting

that multicollinearity is not a significant problem for the majority of variables in our analysis.

The high VIF value for ) is expected given that it is used to form interaction terms in all

of our models. Brambor et al. (2006) suggest that the potential for making inferential errors due

to the exclusion of formative terms in models which include multiplicative interaction terms

outweighs any potential benefits from excluding such terms. Consequently, we continue to

include the term in our analysis.

Finally, we re-estimate our regression models using two alternative methods of dealing

with outlying observations to ensure that our results are robust. First, we winsorize (rather than

truncate) observations with values of Rev), OC) ) (EMP) )

in the highest and lowest 0.5% of the distribution. Second, we re-estimate our regression models

without truncating or winsorizing outlying observations. Results using these methods of dealing

21

with outlying observations yield the same inferences as the results reported in Tables 4 through

9.

V. CONCLUSIONS

We examine the relationship between customer concentration and cost elasticity within

firms. Analyzing cost data for a sample of U.S. manufacturing firms for the period 1976-2013,

we find a negative relationship between customer concentration and cost elasticity, with firms

exhibiting lower proportions of variable-to-fixed costs in the presence of more concentrated

customer bases. This negative relationship is strengthened by the presence of significant supplier

market concentration and product specificity.

Additional analysis shows that these results hold after controlling for the effects of

demand uncertainty, supplier leverage, and both asset and employee sensitivity. Our results are

robust to alternative specifications of customer concentration. We attribute this relationship both

to supplier investments in relationship-specific assets and improved cost efficiency in the

presence of higher levels of customer concentration. These results support findings from prior

literature which suggest that suppliers derive material benefits from their relationships with

major customers.

Our study contributes to the literature by highlighting the importance of considering

customers when examining firm cost structure. Our study also informs results from prior

research related to demand uncertainty and cost structure by highlighting the impact of cross-

sectional differences in customer concentration across industries. Our identification of two

significant moderators of the relationship between customer concentration and firm cost

structure, supplier market competition and product specificity, highlights the need for academics

and practitioners to consider how internal and external operating environment characteristics

22

interact to influence firm-level decisions. Finally, our results add to the growing body of

literature on the impact of customer concentration and major customers on firms by examining

how firms adjust their operations in response to risks and opportunities arising from customer

base concentration.

23

REFERENCES

Albuquerque, A., G. Papadakis, and P. Wysocki, 2010. The Impact of Risk and Monitoring on

CEO Compensation. Working paper, Boston University and University of Miami.

Anderson, S. W., and H. C. Dekker. 2009. Strategic cost management in supply chains part 1:

Structural cost management. Accounting Horizons 23(2): 201-220.

Bae, K., and J. Wang. 2010. Why do firms in customer-supplier relationships hold more cash?

Working paper, York University.

Balakrishnan, R., T. J. Linsmeier, and M. Venkatachalam. 1996. Financial benefits from JIT

adoption: Effects of customer concentration and cost structure. The Accounting Review

71(2): 183-205.

Banerjee, S., S. Dasgupta, and Y. Kim. 2008. Buyer-supplier relationships and the stakeholder

theory of capital structure. Journal of Finance 63(5): 2507-2552.

Banker, R. D., D. Byzalov, and J. M. Plehn-Dujowich. 2014. Demand uncertainty and cost

behavior. The Accounting Review (forthcoming)

Becchetti, L., and J. Sierra. 2003. Bankruptcy risk and productive efficiency in manufacturing

firms. Journal of Banking and Finance 27(11): 2099-2120.

Becker, M. J., and S. Thomas. The Spillover Effects of Changes in Industry Concentration.

Working Paper, University of Pittsburgh.

Brambor, T., W. R. Clark, and M. Golder. 2006. Understanding interaction models: Improving

empirical analyses. Political Analysis 14(1): 63-82.

Brown, D. T., C. E. Fee, and S. E. Thomas. 2009. Financial leverage and bargaining power with

suppliers: Evidence from leveraged buyouts. Journal of Corporate Finance 15 (2): 196

211.

24

Cohen, L., and A. Frazzini. 2008. Economic links and predictable returns. Journal of Finance 63

(4): 1977 2011.

Cuñat, V. 2007. Trade credit: Suppliers as debt collectors and insurance providers. The Review of

Financial Studies 20(2): 491-527.

Dekker. H. C., J. Sakaguchi, and T. Kawai. 2013. Beyond the contract: Managing risk in supply

chain relations. Management Accounting Research 24(2): 122-139.

Dhaliwal, D. S., P. N. Michas, V. Naiker, and D. Sharma. 2013. Major Customer Reliance and

Auditor Going-Concern Decisions. Working Paper, University of Arizona, Monash

University, and Kennesaw State University.

Ellis, J. A., C. E. Fee, and S. E. Thomas. 2012. Proprietary costs and the disclosure of

information about customers. Journal of Accounting Research 50(3): 685-728.

Financial Accounting Standards Board (FASB). 1997. Disclosures about Segments of an

Enterprise and Related Information. Statement of Financial Accounting Standards No.

131. Norwalk, CT: FASB.

Ghosal, V., and P. Loungani. 1996. Product market competition and the impact of price

uncertainty on investment: Some evidence from US manufacturing industries. The

Journal of Industrial Economics 44(2): 217-228.

Gosman, M., T. Kelly, P. Olsson, and T. Warfield. 2004. The profitability and pricing of major

customers. Review of Accounting Studies 9 (1): 117 139.

Gosman, M. L., and M. J. Kohlbeck. 2009. Effects of the existence and identity of major

customers on supplier profitability: Is Wal-Mart different? Journal of Management

Accounting Research 21: 179-201.

Greene, W. 2008. Econometric Analysis. Upper Saddle River, NJ: Pearson/Prentice Hall.

25

Grossman, S. J., and O. D. Hart. 1986. The costs and benefits of ownership: A theory of vertical

and lateral integration. Journal of Political Economy 94(4): 691-719.

Hennessy, C. A., and D. Livdan. 2009. Debt, bargaining, and credibility in firm-supplier

relationships. Journal of Financial Economics 93(3): 382-399.

Holzhacker, M., R. Krishnan, and M. D. Mahlendorf. 2014. The impact of changes in regulation

on cost behavior. Contemporary Accounting Research (forthcoming)

Joshi, A. W., and R. L. Stump. 1999. The contingent effect of specific asset investment on joint

action in manufacturer-supplier relationships: An empirical test of the moderating role of

reciprocal asset investments, uncertainty, and trust. Journal of the Academy of Marketing

Science 27(3): 291-305.

Kallapur, S., and L. Eldenburg. 2005. Uncertainty, real options, and cost behavior: evidence

from Washington State hospitals. Journal of Accounting Research 43 (5): 735-752.

Kelly, T., and M. Gosman. 2000. Increased buyer concentration and its effects on profitability in

the manufacturing sector. Review of Industrial Organization 17 (1): 41 59.

Ketokivi, M., and M. Jokinen. 2006. Strategy, uncertainty, and the focused factor in international

process manufacturing. Journal of Operations Management 24(3): 250-270.

Kulp, S. C., H. L. Lee, and E. Ofek. 2004. Manufacturer benefits from information integration

with retail customers. Management Science 50(4): 431-444.

Kumar, N. 1996. The power of trust in manufacturer-retailer relationships. Harvard Business

Review 74 (November): 92 106.

Lilien, G. L. 1983. A descriptive model of the trade-show budgeting decision process. Industrial

Marketing Management 12(1): 25-29.

26

Lustgarten, S. H. 1975. The impact of buyer concentration in manufacturing industries. The

Review of Economics and Statistics 57(2): 125-132.

Matsumura, E. L., and J. D. Schloetzer. 2012. The Cost of Customer and Supplier Financial

Strength Perspectives: Evidence from the Apparel Industry. Working Paper, University of

Wisconsin Madison and Georgetown University.

Novy-Marx, R. 2011. Operating leverage. Review of Finance 15(1): 103-134.

Patatoukas, P. N. 2012. Customer-base concentration: Implications for firm performance and

capital markets. The Accounting Review 87(2): 363-392.

Peterson, M. A. 2009. Estimating standard errors in finance panel data sets: Comparing

approaches. Review of Financial Studies 22(1): 435-480.

Raman, K., and H. Shahrur. 2008. Relationship-specific investments and earnings management:

Evidence on corporate suppliers and customers. The Accounting Review 83(4): 1041-

1081.

Scherer, F. M. 1970. Industrial Market Structure and Economic Performance. Chicago, IL: Rand

McNally.

Schloetzer, J. D. 2012. Process integration and information sharing in supply chains. The

Accounting Review 87(3): 1005-1032.

Snyder, C. M. 1998. Why do larger buyers pay lower prices? Intense supplier competition.

Economics Letters 58(2): 205-209.

Titman, S., and R. Wessels. 1988. The determinants of capital structure choice. Journal of

Finance 43(1): 1-19.

Wasti, S. N., and J. K. Liker. 1997. Risky business or competitive power? Supplier involvement

in Japanese product design. Journal of Product Innovation Management 14(5): 337-355.

27

Winter, S. G., and G. Szulanski. 2001. Replication as strategy. Organization Science 12(6): 730-

743.

Yang, S. A., and J. R. Birge. 2013. How Inventory Is (Should Be) Financed: Trade Credit in

Supply Chains with Demand Uncertainty and Costs of Financial Distress. Working

Paper, London Business School and The University of Chicago.

28

Appendix A Variable Definitions

Log change operator

REV Total revenues

OC Total operating costs (revenue minus operating income)

SGA Selling, general, and administrative costs

EMP Number of employees (in thousands)

COGS Cost of goods sold

TA Total assets

PPE Gross property, plant, and equipment

DEBT Long term plus short term debt

RD Research and development (R&D) expense

CC Customer-base concentration score for firm i in year t (CCit) equals

where Salesijt represents firm i sales to customer j in year t and Salesit represents total sales for firm i in year t

RankCC Decile rank of the customer concentration variable CC scaled to range from 0 to 1.

HHI Herfindahl-Hirschman Index calculated using three digit SIC code

RDINT R&D intensity =

HighComp High competition indicator variable equals 1 if the firm's HHI is above the sample median, 0 otherwise.

HighRD High product specificity indicator variable equals RDINT is above the sample median, 0 otherwise.

UNCERT Demand uncertainty = for all observations for firm i (at least 10 years)

DebtRatio Debt-to-equity ratio

HighDebt High debt-to-equity indicator variable equals 1 if the is above the sample median, 0 otherwise.

MajCust Major customer indicator variable equals 1 if the firm has at least one customer that accounts for 10% or more of its total sales, 0 otherwise.

ASINT Asset intensity =

EMPINT Employee intensity =

GDPGrowth log change in GDP

Size Natural log of sales

29

Table 1 Sample Composition by Industry

2-Digit

SIC Code

Industry Name N % of Sample

20 Food and Kindred Products 2027 4.33% 21 Tobacco Products 101 0.22% 22 Textile Mill Products 755 1.61%

23 Apparel and Other Finished Products Made from Fabrics and Similar Materials 1234 2.63%

24 Lumber and Wood Products, Except Furniture 404 0.86% 25 Furniture and Fixtures 616 1.32% 26 Paper and Allied Products 819 1.75% 27 Printing, Publishing, and Allied Industries 871 1.86% 28 Chemicals and Allied Products 6794 14.51% 29 Petroleum Refining and Related Industries 449 0.96% 30 Rubber and Miscellaneous Plastic Products 1433 3.06% 31 Leather and Leather Products 369 0.79% 32 Stone, Clay, Glass, and Concrete Products 509 1.09% 33 Primary Metal Industries 1587 3.39%

34 Fabricated Metal Products, Except Machinery & Transportation Equipment 1929 4.12%

35 Industrial and Commercial Machinery and Computer Equipment 7075 15.11%

36 Electronic and Other Electrical Equipment and Components, Except Computer Equipment 9600 20.50%

37 Transportation Equipment 2547 5.44%

38 Measuring, Analyzing, and Controlling Instruments; Photographic, Medical, and Optical Goods; Watches and Clocks 6573 14.03%

39 Miscellaneous Manufacturing Industries 1144 2.44%

Total 46836 100.00%

Table 1 presents the industry composition for the sample of firm-year observations used in this study. The sample consists of manufacturing firms (SIC 2000 - 3999) that report at least one strong customer in the Compustat Customer Segment database.

30

Table 2 Descriptive Statistics (CPI adjusted, 1982-1984 base year)

Percentiles

Variable n Mean Std. Dev. 25th 50th 75th REV 46,836 753 3,785 11 51 254 OC 46,836 675 3,432 13 50 233 SGA 44,301 145 684 4 13 50 EMP 45,309 6 22 0 1 3 COGS 46,836 502 2,824 7 33 164 TA 46,836 841 4,813 12 49 237 PPE 46,759 475 3,155 4 18 104 DEBT 46,836 223 1,796 1 5 52 RD 34,446 42 217 1 3 12 CC 46,836 0.1333 0.1812 0.0189 0.0622 0.1721 HHI 46836 0.1723 0.1535 0.0743 0.1209 0.2149 RDINT 46836 0.4621 6.9614 0.0000 0.0256 0.1140 DebtRatio 46835 0.6495 27.8205 0.0119 0.2683 0.7566 UNCERT 37,974 0.3243 0.2931 0.1545 0.2363 0.3772 ASINT 46759 0.6758 2.8530 0.2268 0.3869 0.6450 EMPINT 45309 1.0730 6.8139 0.4121 0.6976 1.1795 MajCust 46,836 0.7484 0.4339 0.0000 1.0000 1.0000 Table 2 presents descriptive statistics for the sample used in the study. REV year t. OC t. SGA equals selling and general costs in year t number of employees (in thousands) in year t. COGS is cost of goods sold in year t gross property plant and equipment in year t short term plus long term debt for year t. RD is research and development (R&D) expense in year t. CC is the measure of customer concentration following Patatoukas (2012) for year t. HHI is Herfindahl-Hirschman Index for year t . RDINT is intensity for year t. DebtRatio is debt to equity ratio for year t. UNCERT is the measure of demand uncertainty from Banker et al. (2014) for year t. ASINT is asset intensity for year t. EMPINT is a

employee intensity for year t. MajCust equals 1 if a firm has at least one customer that accounts for 10% or more of its total sales, 0 otherwise. in the highest and lowest .5% of the distribution are truncated. Detailed variable definitions are presented in Appendix A.

31

Table 3 Correlations

Variable Name 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

1.REV .990** .929** .936** .979** -.167** -.164** -.094** 1.00** .123** -.103** -.145** -.097** .260** .196** -.482** .039** -.406**

2. OC .995** .942** .931** .985** -.144** -.142** -.103** .990** .093** -.079** -.204** -.067** .253** .194** -.447** .078** -.389**

3.SGA .728** .698** .849** .885** -.125** -.123** -.126** .930** -.022** .023** .040** .081** .146** .145** -.360** .082** -.411**

4. EMP .758** .748** .701** .934** -.196** -.193** -.043** .936** .196** -.181** -.268** -.094** .310** .216** -.523** .121** -.090**

5. COGS .973** .985** .565** .697** -.145** -.143** -.086** .979** .138** -.118** -.278** -.116* .282** .206** -.469** .079** -.352**

6. CC -.017** -.016** -.010 -.040** -.014** .995** -.085** -.167** -.157** .134** .177** .089** -.126** -.070** .253** .041** -.043**

7. RankCC -.018** -.018** -.000 -.047** -.018** .786** -.084** -.164** -.156** .133** .175** .089** -.125** -.069** .250** .041** -.044**

8. GDPGrowth -.060** -.059** -.072** -.036** -.051** -.056** -.072** -.094** .030** -.021** -.022** -.012* .031** -.006 -.000** -.023** .185**

9. Size .391** .381** .427** .497** .342** -.180** -.160** -.086** .123** -.103** -.245** -.097** .260** .196** -.482** .039** -.406**

10. HHI .012** .013** -.011* .052** .019** -.076** -.084** -.017** .097** -.866** -.436** -.174** .208** .073** -.295** -.078** .153**

11. HighComp .000 -.001 .021** -.059** -.007 .115** .133** -.015** -.103** -.631** .380** .152** -.191** -.064** .258** .056** -.174**

12. RDINT -.015** -.014** -.014** -.021** -.013** .147** .079** .003 -.136** -.056** .072** .673** -.295** -.141** .373** .074** -.011*

13. HIGHRD .043** .041** .066** .052** .033** .087** .089** -.011** -.083** -.123** .152** .093** -.163** -.162** .215** .093** .020**

14. DebtRatio .001 .000 -.000 .002 .001 -.007 -.008 .009 .001 -.004 .001 -.001 -.002 .788** -.199** .100** .052**

15. HighDebt ..072** .073** .092** .094** .062** -.079** -.070** -.004 .207** .049** -.064** -.038** -.162** .064** -.118** .077** -.017**

16. UNCERT -.094** -.091** -.106** -.144** -.081** .309** .236** -.018** -.410** -.171** .226** .209** .219** -.002 -.116** -.028** .023**

17. ASINT -.000 -.000 .014** -.005 .000 .124** .065** -.005 -.105** -.037** .053** .520** .061** .000 -.003 .149** .191**

18. EMPINT -.043** -.042** -.102** -.027** -.037** .110** .044** .041** -.213** -.001 -.020** .540** .042** .001 -.029** .150* .740**

**,* indicate statistical significance at the 1 and 5 percent levels, respectively. Significance levels are two-tailed for all variables. Spearman correlations are reported above the diagonal and Pearson correlations are reported below the diagonal.

32

Table 4 Main Results

(1) (2) (3) (4)

ln ln ln MP ln ln 0.507*** 0.285*** 0.157*** 0.744***

(17.88) (7.25) (4.09) (20.28) RankCC * ln -0.138*** -0.209*** -0.133*** -0.092***

(-9.43) (-11.55) (-7.08) (-4.03) GDPGrowth * ln 1.136*** 1.807*** 1.332*** 0.348

(4.57) (5.99) (4.69) (0.86) Size * ln 0.075*** 0.068*** 0.049*** 0.054***

(32.91) (24.39) (18.66) (14.84) RankCC 0.013*** 0.012*** 0.018*** 0.007**

(5.40) (3.48) (4.84) (2.07) GDPGrowth 0.387*** 0.214*** 0.591*** 0.301***

(9.68) (3.69) (9.60) (5.71) Size -0.005*** -0.005*** -0.000 -0.004***

(-11.71) (-9.13) (-0.13) (-6.74) included included included included

ln included included included included n 46836 44086 43580 46819 Adj. R2 0.6929 0.3718 0.2761 0.6076 Table 4 presents results from the following regression:

0 1 2 3GDPGrowth 4Size 5 6GDPGrowth 7Size 1-19 1-19 The term the log change operator defined as the natural log of (Xit / Xit-1). We examine four types of costs: Operating costs (OC), selling, general, and administrative costs (SGA), number of employees (EMP), and cost of goods sold (COGS). REV t. RankCC is the decile rank of the customer concentration measure (CC) scaled to range from 0 to 1 following Patatoukas (2012). GDPGrowth is the log change in GDP for year t. Size equals the natural log of sales in year t. IndustryFE are industry fixed effects based on COGS) in the highest and lowest .5% of the distribution are truncated. T-statistics are presented in parentheses below the coefficients. Standard errors are clustered by firm. *, **, and *** denote statistical significance at the 10, 5, and 1% levels, respectively. Detailed variable definitions are presented in Appendix A.

33

Table 5 Cross-sectional Results for Supplier Industry Competition and Product Specificity

(1) (2)

ln ln

0.509*** 0.529***

(18.52) (16.64)

RankCC * ln -0.092*** -0.059***

(-4.64) (-3.12)

HighComp * ln -0.063***

(-3.88)

HighComp * RankCC * ln -0.058**

(-2.30)

HighRD * ln

-0.133***

(-8.58)

HighRD * RankCC * ln

-0.085***

(-3.54)

GDPGrowth * ln 1.139*** 1.272***

(4.64) (5.34)

Size * ln 0.077*** 0.071***

(34.19) (32.38)

RankCC 0.012*** 0.010***

(5.03) (4.21)

Highcomp 0.005***

(3.06)

HighRD

0.031***

(20.13)

GDPGrowth 0.374*** 0.372***

(9.50) (9.65)

Size -0.005*** -0.005***

(-11.78) (-12.68)

included included ln included included

N 46836 46836 Adj. R2 0.6964 0.7057 Table 5 presents results from cross-sectional tests of the effects of competition and product specificity on the relationship between customer concentration and cost structure. HighComp, our measure of competition, is an indicator variable equal to 1 if the firm's Herfindahl-Hirschman Index (based on three-digit SIC code) is above the sample median and 0 otherwise. HighRD, our measure of product specificity, is an indicator variable equal

the log change operator defined as the natural log of (Xit / Xit-1). We examine four types of costs: Operating costs (OC), selling, general, and administrative costs (SGA), number of employees (EMP), and cost of goods sold (COGS). For brevity, only estimates for operating costs are presented. REV t. RankCC is the decile rank of the customer concentration measure (CC) scaled to range from 0 to 1 following

34

Patatoukas (2012). GDPGrowth is the log change in GDP for year t. Size equals the natural log of sales in year t. IndustryFE are industry fixed effects based on two digit SIC code. Observations with values

REV, OC, SGA, EMP, COGS) in the highest and lowest .5% of the distribution are truncated. T-statistics are presented in parentheses below the coefficients, standard errors are clustered by firm and *, **, and *** denote statistical significance at the 10, 5, and 1% levels, respectively. Detailed variable definitions are presented in Appendix A.

35

Table 6 Robustness Tests: Controls for Debt

(1) (2) (3)

ln ln ln

(Full Sample) (Low Debt) (High Debt) 0.498*** 0.519*** 0.488***

(16.99) (14.47) (12.64) RankCC * ln -0.136*** -0.122*** -0.153***

(-9.29) (-6.28) (-7.11) HighDebt * ln 0.015* (1.75) GDPGrowth * ln 1.139*** 0.939*** 1.376***

(4.57) (2.77) (3.78) Size * ln 0.075*** 0.073*** 0.076***

(32.16) (25.28) (22.01) RankCC 0.013*** 0.009** 0.017***

(5.34) (2.40) (5.58) HighDebt -0.013 (-0.51) GDPGrowth 0.387*** 0.566*** 0.203***

(9.69) (8.68) (4.47) Size -0.005*** -0.004*** -0.006***

(-11.49) (-4.88) (-12.31) included included included

ln included included included N 46836 23242 23594 Adj. R2 0.6930 0.6501 0.7469 Table 6 presents results from cross-sectional and partitioned robustness tests which control for the effects of firm debt. Equation (1) is a cross-sectional analysis which controls for firm debt using an indicator variable. Equations (2) and (3) partition the full sample into low and high debt firms. HighDebt is an indicator variable equal to debt ratio is above the sample median and 0 otherwise. change operator defined as the natural log of (Xit / Xit-1). We examine four types of costs: Operating costs (OC), selling, general, and administrative costs (SGA), number of employees (EMP), and cost of goods sold (COGS).

t. RankCC is the decile rank of the customer concentration measure (CC) scaled to range from 0 to 1 following Patatoukas (2012). GDPGrowth is the log change in GDP for year t. Size equals the natural log of sales in year t. IndustryFE are industry fixed effects based on

.5% of the distribution are truncated. T-statistics are presented in parentheses below the coefficients, standard errors are clustered by firm and *, **, and *** denote statistical significance at the 10, 5, and 1% levels, respectively. Detailed variable definitions are presented in Appendix A.

36

Table 7 Robustness Tests: Controls for Uncertainty

(1) (2) (3) (4)

ln ln ln MP ln ln 0.702*** 0.470*** 0.333*** 0.878***

(24.42) (9.12) (7.30) (18.76) RankCC * ln -0.099*** -0.171*** -0.108*** -0.081***

(-5.98) (-8.78) (-5.36) (-3.14) UNCERT * ln -0.170*** -0.168*** -0.151*** -0.197***

(-8.41) (-6.88) (-5.67) (-7.61) GDPGrowth * ln 0.549** 1.374*** 1.000*** 0.209

(2.07) (4.78) (3.40) (0.45) Size * ln 0.057*** 0.052*** 0.033*** 0.042***

(19.93) (16.35) (10.75) (9.19) RankCC 0.008*** 0.004 0.014*** 0.004

(3.10) (1.27) (3.81) (1.19) UNCERT 0.013** 0.018*** 0.001 0.020**

(2.03) (2.82) (0.09) (2.41) GDPGrowth 0.280*** 0.142** 0.483*** 0.229***

(7.29) (2.50) (7.79) (4.26) Size -0.003*** -0.003*** -0.000 -0.003***

(-7.91) (-6.13) (-0.84) (-4.52) included Included included included

ln included Included included included n 37974 35926 36031 37965 Adj. R2 0.7254 0.3992 0.3002 0.6256 Table 7 presents results from cross-sectional robustness tests which control for the effects of demand uncertainty. UNCERT, a measure of demand uncertainty from Banker et al. (2014), is defined as the standard deviation of log change in sales. the log change operator defined as the natural log of (Xit / Xit-1). We examine four types of costs: Operating costs (OC), selling, general, and administrative costs (SGA), number of employees (EMP), and cost of goods sold (COGS). REV t. RankCC is the decile rank of the customer concentration measure (CC) scaled to range from 0 to 1 following Patatoukas (2012). GDPGrowth is the log change in GDP for year t. Size equals the natural log of sales in year t. IndustryFE are industry fixed effects based on SGA, EMP, COGS) in the highest and lowest .5% of the distribution are truncated. T-statistics are presented in parentheses below the coefficients, standard errors are clustered by firm and *, **, and *** denote statistical significance at the 10, 5, and 1% levels, respectively. Detailed variable definitions are presented in Appendix A.

37

Table 8 Robustness Tests: Controls for Asset and Employee Intensity

(1) (2) (3) (4)

ln ln ln ln 0.507*** 0.285*** 0.157*** 0.744***

(17.88) (7.25) (4.09) (20.28) RankCC * ln -0.138*** -0.209*** -0.133*** -0.092***

(-9.43) (-11.55) (-7.08) (-4.03) ASINT * ln -0.005*** -0.012*** -0.006* -0.007***

(-3.91) (-2.99) (-1.79) (-3.26) EMPINT * ln 0.003*** 0.011*** 0.009*** -0.001

(2.92) (3.61) (3.31) (-0.29) GDPGrowth * ln 1.136*** 1.807*** 1.332*** 0.348

(4.57) (5.99) (4.69) (0.86) Size * ln 0.075*** 0.068*** 0.049*** 0.054***

(32.91) (24.39) (18.66) (14.84) RankCC 0.013*** 0.012*** 0.018*** 0.007**

(5.40) (3.48) (4.84) (2.07) ASINT -0.002* -0.003 -0.006* -0.003***

(-1.88) (-0.84) (-1.81) (-2.75) EMPINT 0.001* 0.009*** 0.010*** 0.001**

(1.73) (3.31) (4.17) (2.23) GDPGrowth 0.387*** 0.214*** 0.591*** 0.301***

(9.68) (3.69) (9.60) (5.71) Size -0.005*** -0.005*** -0.000 -0.004***

(-11.71) (-9.13) (-0.13) (-6.74) included included included Included

ln included included included Included n 46836 44086 43580 46819 Adj. R2 0.6929 0.3718 0.2761 0.6076 Table 8 presents results from cross-sectional robustness tests which control for the effects of asset and employee intensity. divided by sales for year temployees divided by sales for year t. The the log change operator defined as the natural log of (Xit / Xit-1). We examine four types of costs: Operating costs (OC), selling, general, and administrative costs (SGA), number of employees (EMP), and cost of goods sold (COGS). REV in year t. RankCC is the decile rank of the customer concentration measure (CC) scaled to range from 0 to 1 following Patatoukas (2012). GDPGrowth is the log change in GDP for year t. Size equals the natural log of a

sales in year t. IndustryFE are industry fixed effects based on two digit SIC code. Observations

truncated. T-statistics are presented in parentheses below the coefficients, standard errors are clustered by firm and *, **, and *** denote statistical significance at the 10, 5, and 1% levels, respectively. Detailed variable definitions are presented in Appendix A.

38

Table 9 Robustness Tests: Sub-sample Analyses

(1) (2) (3) (3)

ln ln ln ln

(MajCust=1) (Identified Customers) (Sales > $10M) (After 1997)

0.537*** 0.588*** 0.702*** 0.429***

(16.00) (6.75) (19.41) (9.36) RankCC * ln -0.169*** -0.226*** -0.131*** -0.115***

(-9.57) (-4.10) (-7.98) (-5.33) GDPGrowth * ln 1.176*** 1.868** 0.960*** 1.278***

(4.31) (2.45) (3.76) (3.94) Size * ln 0.075*** 0.067*** 0.042*** 0.074***

(29.40) (9.19) (13.68) (23.02) RankCC 0.015*** 0.005 0.008*** 0.007**

(4.38) (0.49) (3.49) (2.01) GDPGrowth 0.481*** 0.448*** 0.095*** 0.541***

(9.89) (3.71) (3.26) (8.83) Size -0.005*** -0.006*** -0.005*** -0.001

(-9.62) (-4.54) (-14.00) (-1.10) included included included included

ln included included included included n 35054 4583 36031 21739 Adj. R2 0.6718 0.7402 0.8301 0.6572 Table 9 presents results for sub-sample analyses of our main results based on the following regression:

0 1 2 3GDPGrowth 4Size 5 6GDPGrowth 7Size 1-19 1-19 Equation (1) includes only firm-year observations which report at least one customer that accounts for 10% or more of its sales (MajCust = 1). Equation (2) includes only firm-year observations with major customers (MajCust = 1) that can be identified using the Compustat database. Equation (3) includes only firm-year observations for firms with greater than $10 million in sales revenue. Equation (4) includes only firm-year observations after 1997.

the log change operator defined as the natural log of (Xit / Xit-1). We examine four types of costs: Operating costs (OC), selling, general, and administrative costs (SGA), number of employees (EMP), and cost of goods sold (COGS). For brevity, only estimates for operating costs are presented. REV equals

t. RankCC is the decile rank of the customer concentration measure (CC) scaled to range from 0 to 1 following Patatoukas (2012). GDPGrowth is the log change in GDP for year t. Size equals the natural log of sales in year t. IndustryFE are industry fixed effects based on two digit SIC code.

are truncated. T-statistics are presented in parentheses below the coefficients. Standard errors are clustered by firm. *, **, and *** denote statistical significance at the 10, 5, and 1% levels, respectively. Detailed variable definitions are presented in Appendix A.

![[Elearnica.ir]-Customer Cost of Electric Service Interruptions](https://static.fdocuments.us/doc/165x107/563dbbbc550346aa9aafd26e/elearnicair-customer-cost-of-electric-service-interruptions.jpg)