Gauging Slacktivism in China: Taking Micro-blog Users as an Example

Upload

the-world-bankCategory

view

329download

0

Africa: Enhancing growth and reducing poverty in a volatile world

Shanta DevarajanWorld Bank

http://blogs.worldbank.org/africacan

Before the global crisis

• Africa was experiencing sustained, relatively rapid economic growth– As fast as all developing countries (except China

and India)

For the first time in 20 years, Africa’s growth is equal to that of developing countries (except China and India)

Per capita income

-4

-2

0

2

4

6

8

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Ann

ual c

hang

e in

real

GD

P pe

r ca

pita

(%)

Developing countries Developing countries, excluding China and India

Sub-Saharan Africa High-income countries

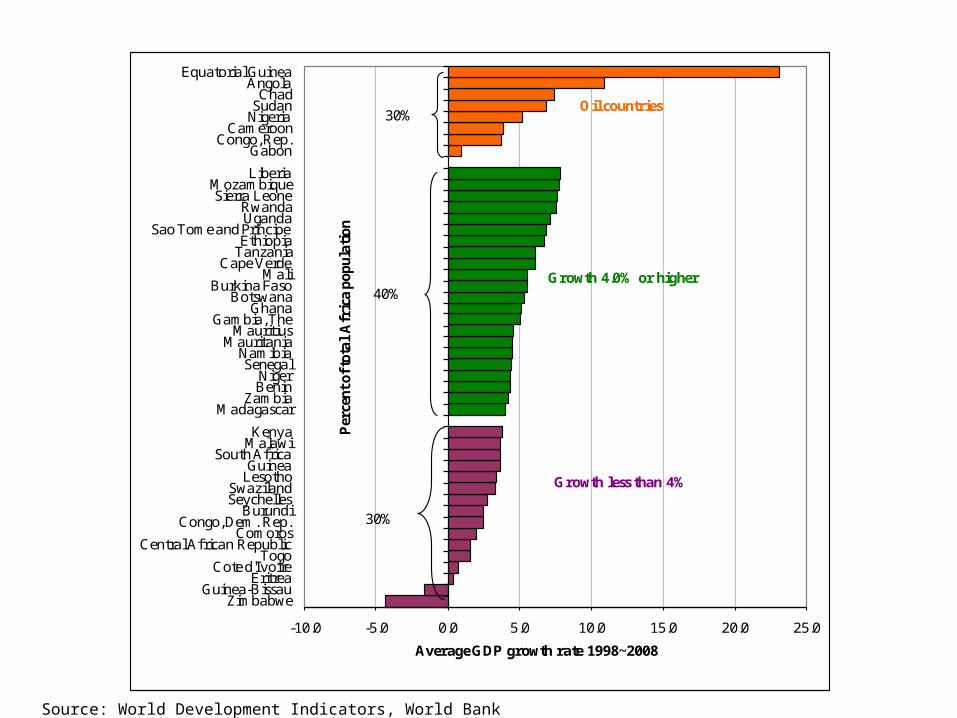

Before the global crisis

• Africa was experiencing sustained, relatively rapid economic growth– As fast as all developing countries (except China

and India)– Broad-based: 22 non-oil countries had 4+ percent

average GDP growth from 1998-2008

-10.0 -5.0 0.0 5.0 10.0 15.0 20.0 25.0

ZimbabweGuinea-Bissau

EritreaCote d'Ivoire

TogoCentra l African Republic

ComorosCongo, Dem. Rep.

BurundiSeychellesSwaziland

LesothoGuinea

South AfricaMalawiKenya

MadagascarZambia

BeninNiger

SenegalNamibia

MauritaniaMauritius

Gambia, TheGhana

BotswanaBurkina Faso

MaliCape Verde

TanzaniaEthiopia

Sao Tome and PrincipeUgandaRwanda

Sierra LeoneMozambique

LiberiaGabon

Congo, Rep.Cameroon

NigeriaSudanChad

AngolaEquatorial Guinea

Average GDP growth rate 1998~2008

30%

Perc

ent o

f tot

al A

fric

a po

pula

tion

40%

30%

Oil countries

Growth 4.0% or higher

Growth less than 4%

Source: World Development Indicators, World Bank

Before the global crisis

• Africa was experiencing sustained, relatively rapid economic growth– Broad-based: 22 non-oil countries had 4+ percent

average GDP growth from 1998-2008– Due to

• Higher commodity prices• Increases in aid, debt relief and capital flows• Improved macroeconomic policies

Inflation in Africa

1724

29 31 33 31 33 30 3227 28 31 33

13 137 6 6 7 6 5 4 2 3 2 2

0

20

40

60

80

100

120

140

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Aver

age

Infla

tion

Rat

e %

0

5

10

15

20

25

30

35

40

45

Num

ber o

f Cou

ntrie

s Inflation>20%

10%<inflation<=20%

Inflation<=10%

Median inflation rate

Although least integrated, Africa may be the worst hit by the crisis

• Private capital flows

Source: IMF, World Economic Outlook, 2008

If FDI flows, more important recently, were to fall, growth would suffer

Europe and Central Asia

Latin America & the Caribbean

Sub Saharan Africa0

5

10

15

20

25

1995-1999

FDI as a percent of fixed investment

Source: World Bank, Global Economic Prospects 2010: Crisis, finance, and growth

Although least integrated, Africa may be the worst hit by the crisis

• Private capital flows• Remittances

Remittances

2006 2007 2008 2009f 2010f$12

$14

$16

$18

$20

$22

$24 Workers' Remittances - SSA

Base Case Low Case

Bill

ions

of U

.S. d

olla

rs

Source: Ratha and Mahopatra (2009)

Although least integrated, Africa may be the worst hit by the crisis

• Private capital flows• Remittances• Tourism

Tourist arrivals(compared with equivalent period in 2008)

Country Percentage change Period

Gambia -32.4 Jan-Apr 09

Tanzania -10.0 Jan-Apr 09

Mauritius -9.9 Jan-Mar 09

Kenya -7.0 Jan-Apr 09

Senegal -6.3 Jan-Apr 09

Source: World Bank staff estimates

Although least integrated, Africa may be the worst hit by the crisis

• Private capital flows• Remittances• Tourism• Primary commodity prices

Terms of trade shocks(change in trade balance as percentage of 2006 GDP)

Bottom 5, 2008Seychelles -13.90Eritrea -11.68Togo -7.79Cape Verde -7.25Senegal -7.07

Top 5, 2008Nigeria 22.92Gabon 28.23Congo, Rep. 30.53Angola 34.77Equatorial Guinea 49.12

Bottom 5, 2009Equatorial Guinea -26.05Angola -19.00Congo, Rep. -17.15Gabon -15.69Nigeria -13.01

Top 5, 2009Ethiopia 1.39

Mauritius 2.44

Togo 3.44

Eritrea 3.39Seychelles 5.92

2007 2008 2009 201014.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

30.0

Government Revenue in Sub-Saharan Africa

Oil-exporting Coun-treis

Middle-Income Coun-tries

Low-income Countries

Fragile Countries

Gov

ernm

ent R

even

ue, E

xclu

ding

Gra

nts (

% o

f GDP

)

Note: 2008 includes 2008/09 fiscal year; 2009 includes 2009/10 fiscal yearSource: Regional Economic Outlook, IMF (October 2009)

Although least integrated, Africa may be the worst hit by the crisis

• Private capital flows• Remittances• Tourism• Primary commodity prices• Foreign aid

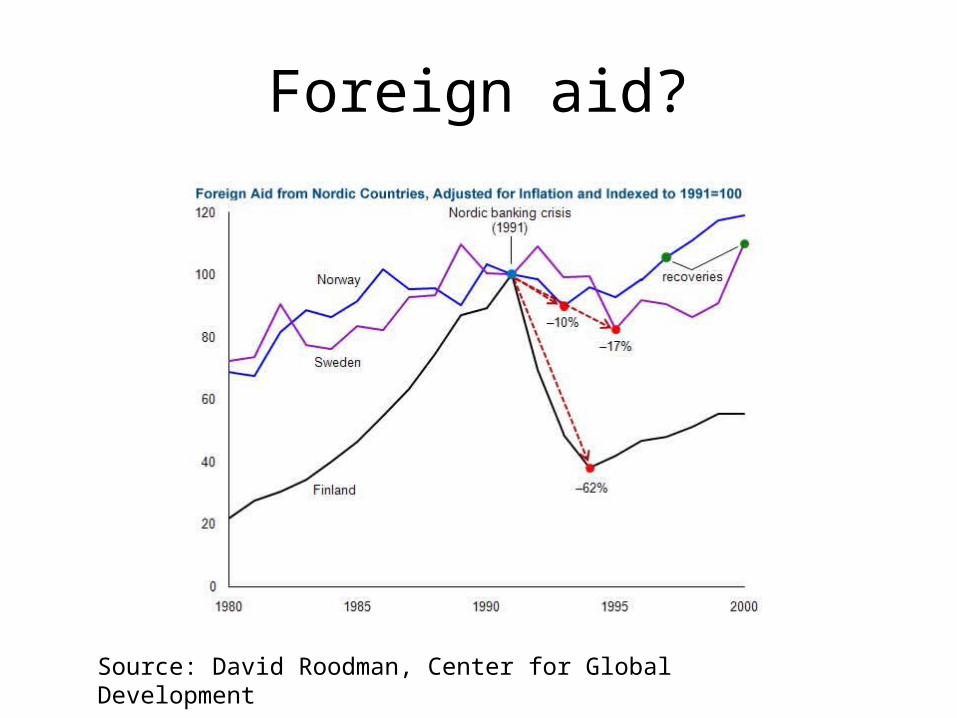

Foreign aid?

Source: David Roodman, Center for Global Development

Impact: Decline in growth

0

1

2

3

4

5

6

Africa Sub-Saharan Africa

2008 (actual)2009 (February forecast)2009 (May forecast)2009 (October forecast)

Source: African Economic Outlook database

Result: Growth declines

• Per capita income declines– For the first time in a decade

• Human crisis– 7-10 million thrown into poverty– 30-50,000 additional children dying before their

first birthday• Possible reversals in economic reforms—

didn’t happen

Revenue, Expenditure and Deficit (relative to earlier projections)

Source: Krumm, Dhar and Choi, “Fiscal Response to the Global Crisis inLow Income African Countries”, August 2009

Fiscal Stance County

Debt Distress Risk

Fiscal Projection Changes

CountryDebt Distress Risk

Fiscal Projection Changes

Revenue Expenditure

Balance(Ex. Grant)

Balance(In. Grant) Revenue Expenditur

eBalance

(Ex. Grant)Balance

(In. Grant)

Fiscal Tightening

Ethiopia Moderate Ghana Moderate

Rwanda Moderate

Partial Adjustment

Mozambi-que Low Uganda Low

No Adjustment Senegal Low Burkina

Faso High

Stimulus

Zambia Low Kenya Low

Tanzania Low

-5

0

5

-0 .5

-4 .1

3.6

2.3

-1.0

0.0

1.0

2.0

0 .31 .1

-0.8

1.3

-2.0

-1.0

0.0

1.0

2.00.5

-1.3

1.9 2.0

-0 .5

-0 .3

-0 .1

0.1

-0.5

-0.1

-0.5

-0.3

-4 .0

-3 .0

-2 .0

-1 .0

0.0

1.0

-2.8-3 .1

0.2

-0.2

-2.5-2.0-1.5-1.0-0.50.00.5

-1.5

0.4

-2 -1.9 -1 .5

-1 .0

-0 .5

0 .0

0 .5

-0 .8

0.0

-1.0

0 .4

-2.0-1.5-1.0-0.50.00.51.0

-1.0

0.8

-1.7

-0.9-2 .0

-1 .0

0.0

1.0

2.0

0.1

1.8

-1.6 -1 .6

-1 .5-1 .0-0 .50.00.51.0

-0 .20 .9

-1.1-1.4

Policy responses

• Time-bound bailout programs– E.g., Tanzania’s emergency rescue program limits

government guarantees and loans to two years• Accelerated reform programs

– E.g., Nigeria is deregulating its downstream petroleum sector, reducing costly and regressive subsidies

Implications

• Policy environment has never been better• External resources are as productive as they

have ever been• Continued reforms and additional resources

could accelerate progress towards the Millennium Development Goals

Africa’s medium-term challenges

Business climate

Low competitiveness

OECD

Latin America & Caribbean

Middle East & North Africa

East Asia & Pacific

Eastern Europe & Central Asia

South Asia

Sub-Saharan Africa

10.5

18.6

22.5

23.1

26.8

32.4

33.6

Time to export (days)

Source: World Bank, Doing Business Database

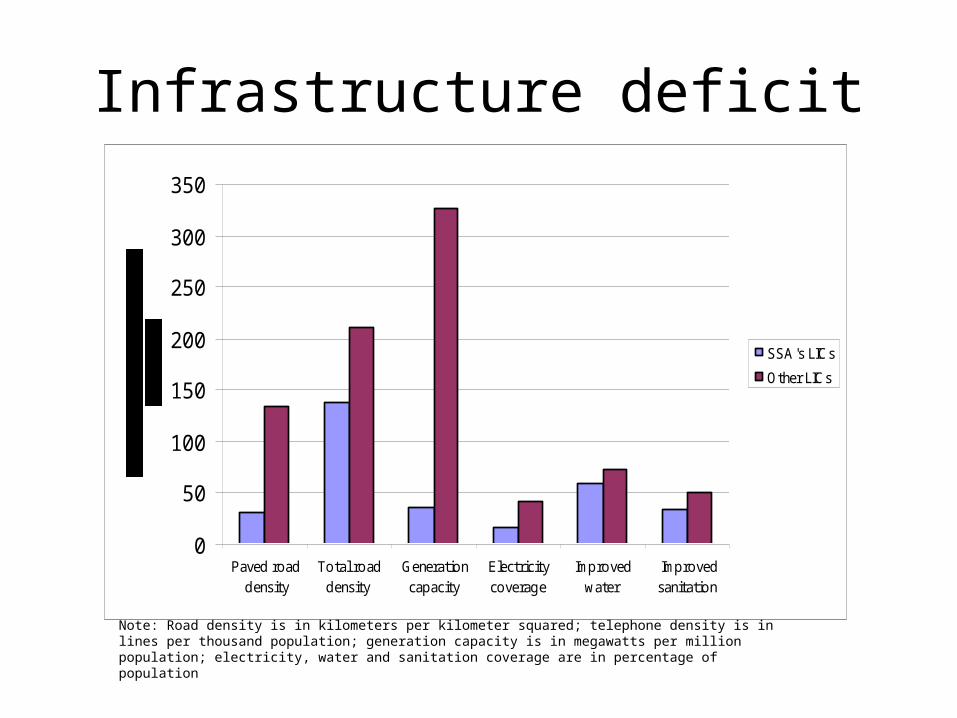

Infrastructure deficit

0

50

100

150

200

250

300

350

Paved roaddensity

Total roaddensity

Generationcapacity

Electricitycoverage

Improvedwater

Improvedsanitation

SSA's LICsOther LICs

Note: Road density is in kilometers per kilometer squared; telephone density is in lines per thousand population; generation capacity is in megawatts per million population; electricity, water and sanitation coverage are in percentage of population

Youth unemployment

Population Pyramid in SSA in 2005 (UN)

10 5 0 5 10

0-4

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

Age

Male (%) Female

Population Pyramid in More developed regions in 2005 (UN)

10 5 0 5 10

0-4

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

Age

Male (%) Female

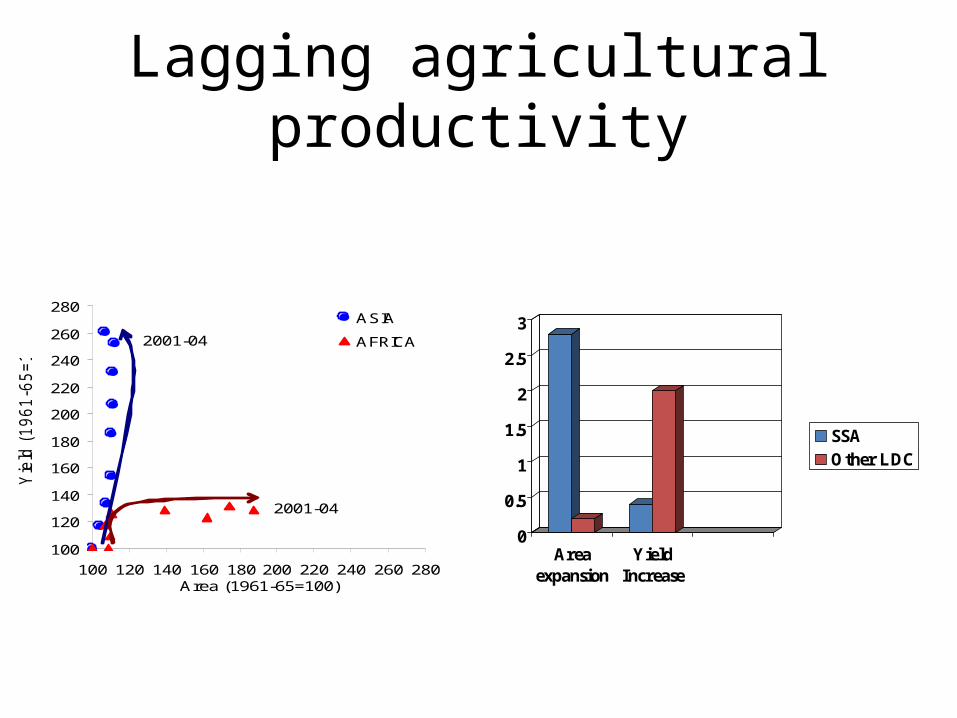

Lagging agricultural productivity

100

120

140

160

180

200

220

240

260

280

100 120 140 160 180 200 220 240 260 280Area (1961-65=100)

Yiel

d (1

961-

65=1

00)

ASIA

AFRICA2001-04

2001-04

0

0.5

1

1.5

2

2.5

3

Areaexpansion

YieldIncrease

SSAOther LDC

Potential Impact of Climate Change on Agriculture: Projected Percentage

Change in Agricultural Productivity in 2080

Note: Scenario: SRES A2.Source: Cline 2007.

Climate Risks and Development: The “Poor Countries’ Danger”

Back to Infrastructure deficit

0

50

100

150

200

250

300

350

Paved roaddensity

Total roaddensity

Generationcapacity

Electricitycoverage

Improvedwater

Improvedsanitation

SSA's LICsOther LICs

Note: Road density is in kilometers per kilometer squared; telephone density is in lines per thousand population; generation capacity is in megawatts per million population; electricity, water and sanitation coverage are in percentage of population

SELECTED CORRIDORS

OF THE STUDY

23.5 4

5 5 57

8

11

02468

101214

Paki

stan

Braz

il

USA

Chi

na

Wes

tern

Euro

pe –

long

dist

ance

Afric

a-D

urba

n-Lu

saka

Afric

a- L

omé

-O

uaga

doug

ou

Afric

a –

Mom

basa

Kam

pala

Afric

a-D

oual

a-N

djam

énaA

vera

ge tr

ansp

ort p

rices

(in

US

cen

ts p

er tk

m)

Central Africa East Africa West Africa Southern Africa France

Variable costs (USD per veh-km) 1.31 0.98 1.67 1.54 0.72

Fixed costs (USD per veh-km) 0.57 0.35 0.62 0.34 0.87

Total transport costs (USD per veh-km) 1.88 1.33 2.29 1.88 1.59

Transport costs are not excessively high in Africa comparing to France for example

However, average transport prices in Africa are high in a global comparison

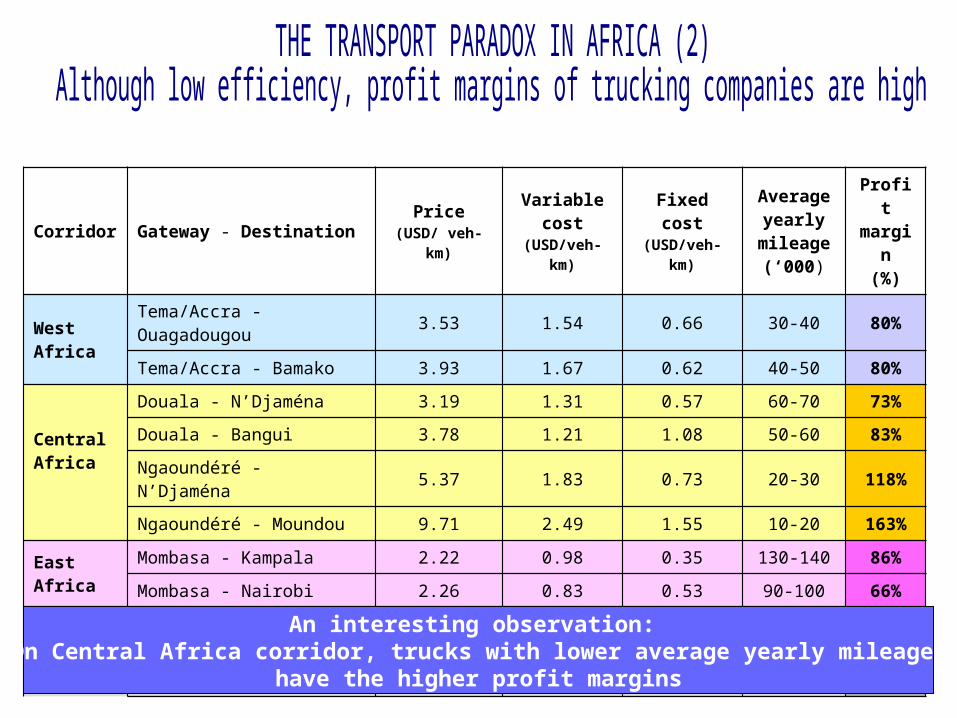

Corridor Gateway - Destination Price(USD/ veh-km)

Variable cost

(USD/veh- km)

Fixed cost(USD/veh- km)

Average yearly

mileage (‘000)

Profit margin

(%)

West Africa

Tema/Accra - Ouagadougou 3.53 1.54 0.66 30-40 80%

Tema/Accra - Bamako 3.93 1.67 0.62 40-50 80%

Central Africa

Douala - N’Djaména 3.19 1.31 0.57 60-70 73%Douala - Bangui 3.78 1.21 1.08 50-60 83%Ngaoundéré - N’Djaména 5.37 1.83 0.73 20-30 118%Ngaoundéré - Moundou 9.71 2.49 1.55 10-20 163%

East Africa

Mombasa - Kampala 2.22 0.98 0.35 130-140 86%

Mombasa - Nairobi 2.26 0.83 0.53 90-100 66%

Southern Africa

Lusaka - Johannesburg 2.32 1.54 0.34 160-170 18%

Lusaka - Dar-es-Salaam 2.55 1.34 0.44 160-170 62%

An interesting observation: On Central Africa corridor, trucks with lower average yearly mileage

have the higher profit margins

Average transport prices (constant and current) from Mombasa to Kigali

0

50

100

150

200

250

300

35019

89

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Years

US$

/Ton

0

100

200

300

400

500

600

700

800

900

US$/Ton

Current transport tariffs (left) Real transport tariffs - GDP deflator (right)

After liberalizationBefore liberalization

Africa’s time

• Before the crisis, policies were steadily improving and showing results

• During the crisis, policies continued to improve• Policy environment has never been better• Medium-term challenges, while daunting, can also

be met with a combination of resources and reform• Africa may be poised for sustained, rapid growth, as

India was 20 years ago, and China 30 years ago