CURRENT DEVELOPMENTS IN THE DIVISION OF CORPORATION FINANCE

106

CURRENT CURRENT DEVELOPMENTS DEVELOPMENTS IN THE IN THE DIVISION OF DIVISION OF CORPORATION CORPORATION FINANCE FINANCE National Conference on Current SEC & PCAOB Developments December 6, 2004

-

Upload

bevis-hodges -

Category

Documents

-

view

23 -

download

0

description

CURRENT DEVELOPMENTS IN THE DIVISION OF CORPORATION FINANCE. National Conference on Current SEC & PCAOB Developments December 6, 2004. Disclaimer. - PowerPoint PPT Presentation

Transcript of CURRENT DEVELOPMENTS IN THE DIVISION OF CORPORATION FINANCE

CURRENT CURRENT DEVELOPMENTS DEVELOPMENTS

IN THE IN THE DIVISION OF DIVISION OF

CORPORATION CORPORATION FINANCEFINANCE

National Conference on Current SEC & PCAOB

DevelopmentsDecember 6, 2004

2

2

The Securities and Exchange The Securities and Exchange Commission, as a matter of policy, Commission, as a matter of policy, disclaims responsibility for any disclaims responsibility for any private publication or statement by private publication or statement by any of its employees. Therefore, the any of its employees. Therefore, the views expressed today are our own, views expressed today are our own, and do not necessarily reflect the and do not necessarily reflect the views of the Commission or the other views of the Commission or the other members of the staff of the members of the staff of the Commission.Commission.

DisclaimerDisclaimer

3

3

Corporation FinanceCorporation Finance

OverviewOverview

Financial Reporting and Financial Reporting and Disclosure IssuesDisclosure Issues

4

4

Corporation FinanceCorporation Finance

OVERVIEWOVERVIEW

Craig OlingerCraig Olinger

5

5

Accounting Branch ChiefsAccounting Branch Chiefs

Health Care & Insurance Health Care & Insurance James AtkinsonJames AtkinsonConsumer Products Consumer Products

Michael MoranMichael Moran

George OhsiekGeorge OhsiekComputers & On Line ServicesComputers & On Line Services

Stephen KrikorianStephen Krikorian

Brad SkinnerBrad SkinnerNatural Resources & FoodNatural Resources & Food Jill DavisJill DavisStructured Finance, Transportation & LeisureStructured Finance, Transportation & Leisure

Linda CvrkelLinda Cvrkel

Michael FayMichael Fay

David HumphreyDavid Humphrey

6

6

Accounting Branch ChiefsAccounting Branch Chiefs

Manufacturing & ConstructionManufacturing & ConstructionJohn CashJohn Cash

Rufus DeckerRufus Decker

Financial ServicesFinancial ServicesJohn NolanJohn Nolan

Kevin VaughnKevin Vaughn

Real Estate & Business ServicesReal Estate & Business ServicesKathleen CollinsKathleen Collins

Donna DiSilvioDonna DiSilvio

Emerging Growth CompaniesEmerging Growth Companies

Hugh WestHugh West

7

7

Accounting Branch ChiefsAccounting Branch Chiefs

Electronics & Machinery Electronics & Machinery Brian CascioBrian Cascio

Daniel GordonDaniel Gordon

TelecommunicationsTelecommunicationsTerry FrenchTerry French

Robert LittlepageRobert Littlepage

Kyle MoffattKyle Moffatt

8

8

Financial Reporting and Financial Reporting and DisclosureDisclosure

SOX Section 404 and 302SOX Section 404 and 302

Use of Other AuditorsUse of Other Auditors

Louise DorseyLouise Dorsey

Stephanie HunsakerStephanie Hunsaker

9

9

SOX Section 404 and 302

Effective Date for 404404 vs. 302 RequirementsInteraction of 404 and 302Evaluating ICFRManagement’s ReportFAQs

10

10

Effective Date of 404 for Accelerated Filers•10-K due March 16, 2005•11/17/04 – SEC postponed final phase-in period for one year Annual report deadline still 75 days

Quarterly report deadlines still 40 days

•Accelerated filing phase-in resumes for FYE ending on or after 12/15/05 Annual report- due in 60 days

Quarterly report- due in 35 days

11

11

Effective Date of 404 for Accelerated Filers•11/30/04 – Exemptive Order

•45 Day Extension for cos. with

<$700 mil market cap at end of 2nd Qtr

•10-K still due March 16, 2005

All required items except 404 reports

12

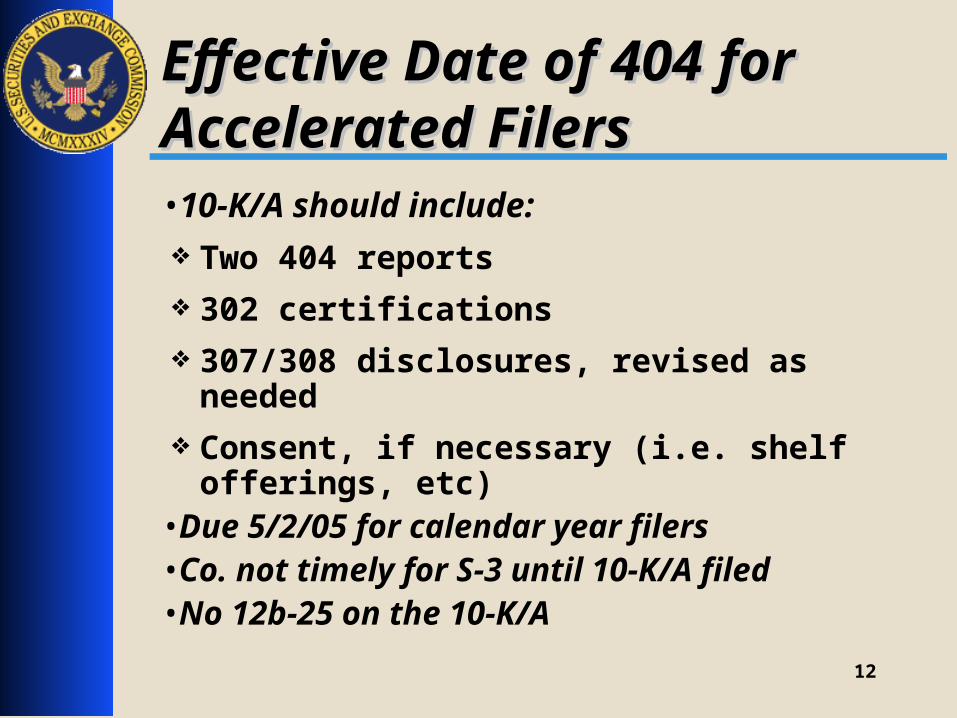

12

Effective Date of 404 for Effective Date of 404 for Accelerated FilersAccelerated Filers•10-K/A should include: Two 404 reports

302 certifications

307/308 disclosures, revised as needed

Consent, if necessary (i.e. shelf offerings, etc)

•Due 5/2/05 for calendar year filers•Co. not timely for S-3 until 10-K/A filed•No 12b-25 on the 10-K/A

13

13

404 vs 302 Requirements

404 – ICFR•Annually assess ICFR•Review conducted as of year-end•Quarterly evaluation of any changes in ICFR•Documentation requirements for auditor to test•Internal control report

302 – DCP•Quarterly assess DCP•Review conducted as of quarter and year-end•Quarterly evaluation of any changes in DCP•N/A – no auditor testing requirements•Officers’ certification

14

14

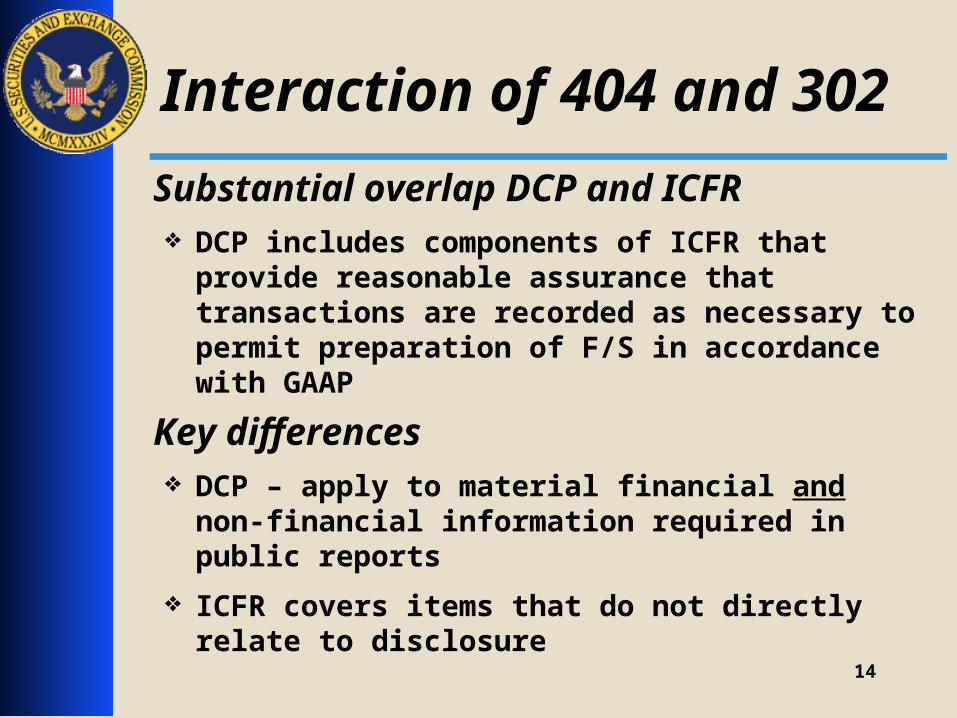

Interaction of 404 and 302

Substantial overlap DCP and ICFR DCP includes components of ICFR that provide

reasonable assurance that transactions are recorded as necessary to permit preparation of F/S in accordance with GAAP

Key differences DCP – apply to material financial and non-financial

information required in public reports

ICFR covers items that do not directly relate to disclosure

15

15

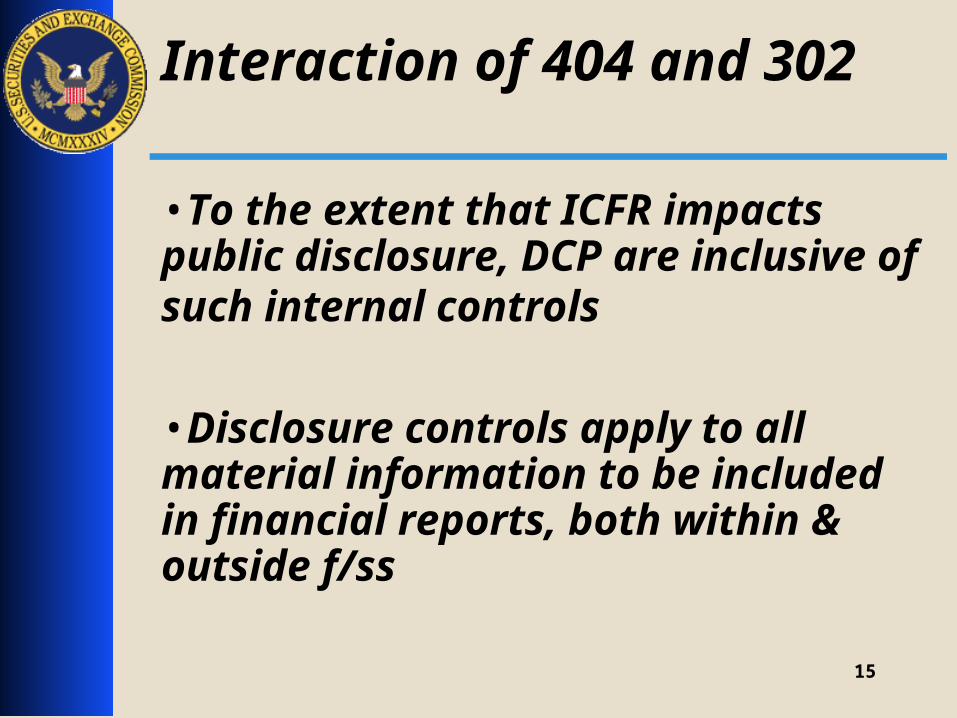

Interaction of 404 and 302

•To the extent that ICFR impacts public disclosure, DCP are inclusive of such internal controls

•Disclosure controls apply to all material information to be included in financial reports, both within & outside f/ss

16

16

Interaction of 404 and 302

Question

Could you have a situation where CFO/CEO reach a conclusion in their 302 certifications that DCP are effective at reasonable assurance level, even though there is a material weakness in ICFR?

17

17

Interaction of 404 and 302

Answer

Generally officers will not be able to conclude DCP are effective when material weaknesses have been identified in IFCR

But……

There may be some limited circumstances

18

18

Interaction of 404 and 302

Some elements of ICFR are not directly subsumed within the definition of DCP

Example in 404 adopting release– pure safeguarding of assets

19

19

Interaction of 404 and 302

Likely impossible to conclude DCP are effective when material weaknesses exist in certain areas:

Example:

Material weakness in fraud prevention

Multiple material weaknesses

20

20

Interaction of 404 and 302

QuestionWhat if a company has to restate its F/S because it or the auditor discovers a material weakness in ICFR that is also part of the company’s DCP?

21

21

Interaction of 404 and 302

ANSWERNeed to consider whether the disclosures provided under Item 307 in original filing must be:

modified, supplemented or corrected

in order to explain relationship between failure of DCP and restated F/S

22

22

Interaction of 404 and 302

•If officers conclude original conclusions are no longer correct:

Disclose this fact based on duty to correct a misstatement when it became known and Rule 12b-20

23

23

Interaction of 404 and 302

Question

Can the officers conclude DCP were not effective as of end of reporting period covered by amended report, but conclude DCP are effective as of date the amendment filed?

24

24

Interaction of 404 and 302

Answer

Yes – Company should expand disclosure to explain how mgmt determined DCP are now effective given the material weakness and other matters identified

25

25

Interaction of 404 and 302

Other Areas for Disclosure?•MD&A Disclosure

Material weakness in ICFR may constitute a material trend or uncertainty that should be disclosed in MD&A

Detailed discussion of material weakness

quantification and analysis of associated uncertainties & trends

26

26

Evaluating ICFR

•Will vary among companies•No specific method or procedures required •Must be based on procedures sufficient to evaluate both design & operating effectiveness•Documentation & evidential matter is key

Inquiry alone not adequate!

27

27

Evaluating ICFR

Mgmt must attain the level of “reasonable assurance” when formulating conclusions regarding effectiveness of ICFR

Reasonable Assurance•Conforms to current auditing literature (AU 319)•Mgmt must use judgment •Implies consideration by mgmt of the cost of the control and its benefits in reducing risk

28

28

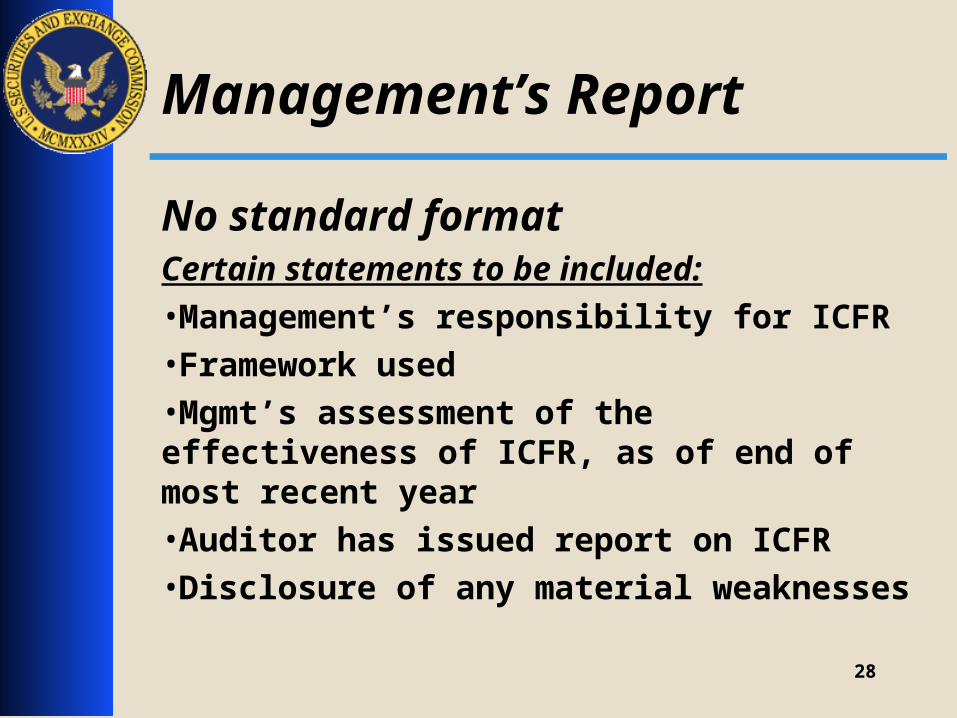

Management’s Report

No standard formatCertain statements to be included:•Management’s responsibility for ICFR•Framework used•Mgmt’s assessment of the effectiveness of ICFR, as of end of most recent year•Auditor has issued report on ICFR•Disclosure of any material weaknesses

29

29

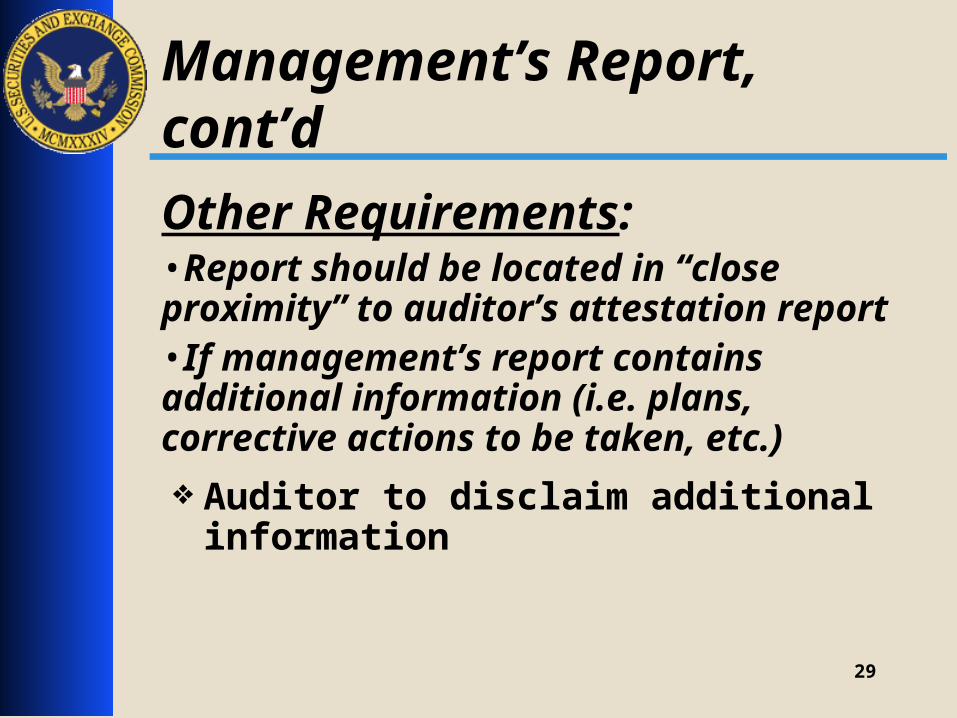

Management’s Report, cont’d

Other Requirements:•Report should be located in “close proximity” to auditor’s attestation report•If management’s report contains additional information (i.e. plans, corrective actions to be taken, etc.)

Auditor to disclaim additional information

30

30

Management’s Report

2 Possible Options•Effective

•Not Effective Prohibited from concluding effective

ICFR if one or more material weaknesses

31

31

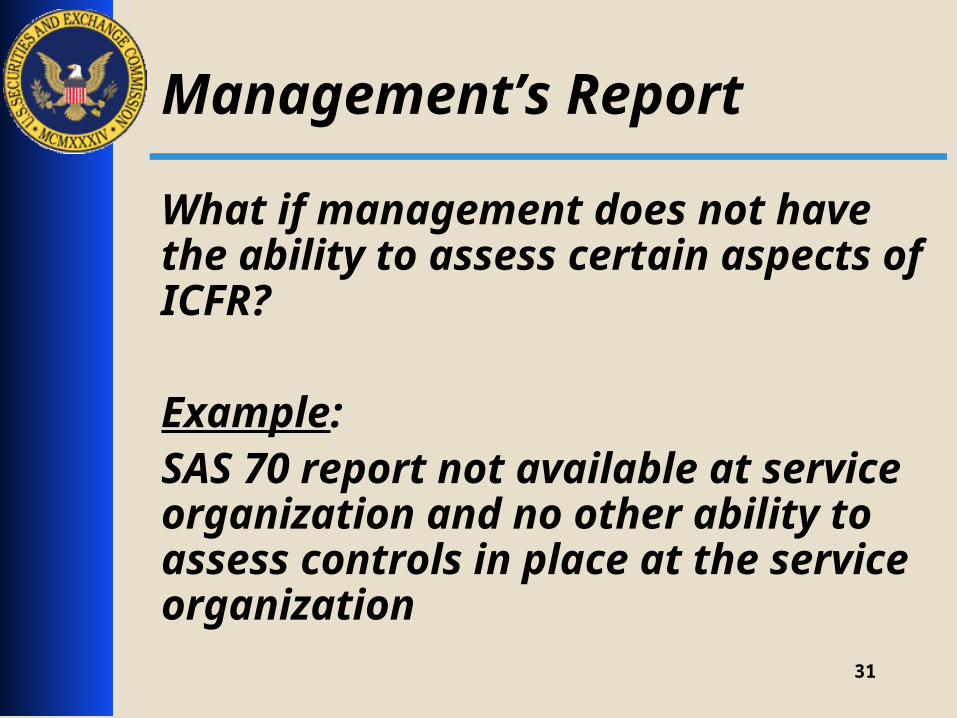

Management’s Report

What if management does not have the ability to assess certain aspects of ICFR?

Example:SAS 70 report not available at service organization and no other ability to assess controls in place at the service organization

32

32

Management’s Report

NO scope limitation permitted in report Mgmt must conclude if ICFR

effective or not effective based on extent of scope limitation

33

33

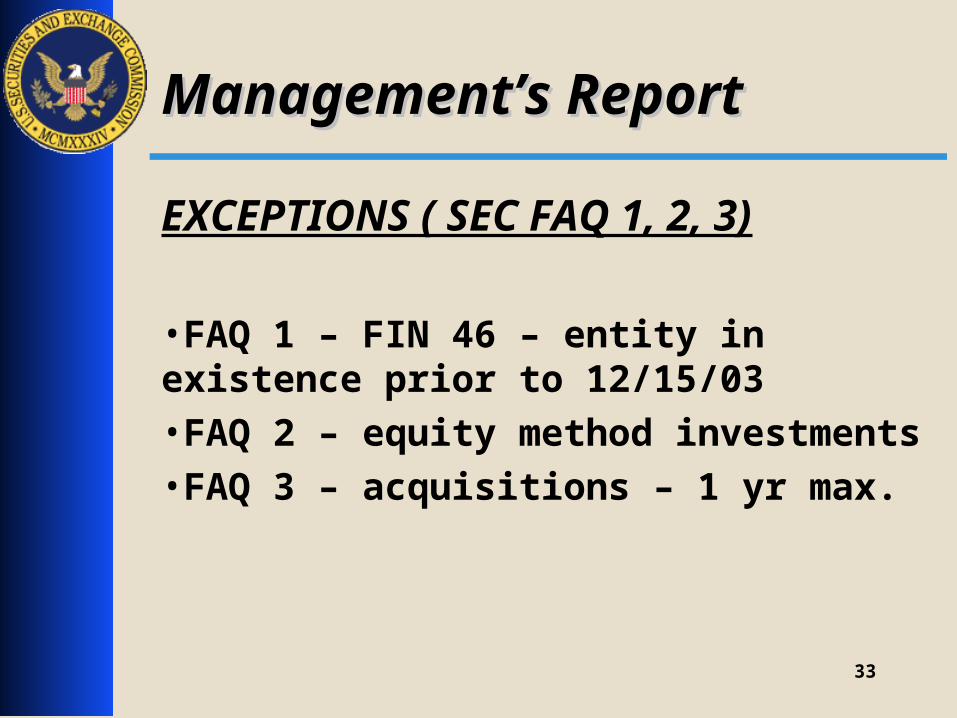

Management’s ReportManagement’s Report

EXCEPTIONS ( SEC FAQ 1, 2, 3)

•FAQ 1 – FIN 46 – entity in existence prior to 12/15/03•FAQ 2 – equity method investments•FAQ 3 – acquisitions – 1 yr max.

34

34

Required Communications

•Mgmt must communicate all significant deficiencies & material weaknesses they detect to audit committee & external auditor Part of 302 certification

•Mgmt also must provide written representations to auditor

35

35

SEC FAQs

•23 FAQ’s•Updated October 6, 2004•www.sec.gov/info/accountants/controlfaq1004.htm

•PCAOB also issued 3 separate sets of Staff Q&As (39) June 23, 2004

October 6, 2004

November 22, 2004

36

36

SEC FAQs

Scope Limitations – Questions 1–3•FAQ 1 – consolidated VIEs, proportionate consolidations What is the meaning of “does not have the

right or authority to assess”? Neither legal rights nor ability of mgmt to

remediate deficiencies are necessarily tied to mgmt’s ability to assess ICFR

Facts and circumstances will dictate when mgmt has the ability

37

37

SEC FAQs

•FAQ 2- Equity investee Not intended to prohibit registrants from

assessing ICFR of investees under the equity method

38

38

SEC FAQs

•FAQ 3 – Recent business acquisition

Intent of issuing FAQ 3 is not to negatively impact mgmt’s business decisions

Will likely not object to anyone who decides to use this relief in the year of acquisition

“Business” as defined in EITF 98-3 or Article 11 of S-X

39

39

SEC FAQs

FAQ 4 – Conclusion that ICFR is not effective Registrant will still be considered timely &

current re:

Rule 144, S-2/S-3/S-8 eligibility

40

40

SEC FAQs

FAQ 9 – Disclosure of changes to ICFR made in preparation of 1st Mgmt report Giving relief for the 302 requirement to

disclose material changes in ICFR

HOWEVER…..

If change is driven from material weakness, notwithstanding the relief that is being given, registrants should carefully consider disclosing the material weakness and the resulting changes

41

41

SEC FAQs

Other most frequent:

FAQ 8 – Transition reports

FAQ 14 – SAS 70 reports

FAQ 21 – Consents

FAQ 22 – Annual “glossy” reports

FAQ 23 – Supplementary information

42

42

Other Questions

IPO -Initial 404 assessment

Due with first annual report once effective date passes

Discontinued operations not finalized as of end of year

No relief

43

43

Other Questions

Registrants in Chapter 11 No automatic exemption from 404

If registrant qualifies for modified reporting under SLB 2 then registrant does not need to comply with 404

Must request relief in advance

44

44

What we are seeing

Significant deficiencies & material weaknesses identified are being disclosed in Form 8-K and Form 10-QTypical areas where significant deficiencies/material weaknesses have been identified:

Personnel issues

Financial systems

Restatements due to lack of controls

45

45

Final Remarks

We know there will be material weaknesses

Key is disclosure

What the problem is

What it impacts

How are you going to remediate

Timetable for remediation

46

46

Use of Other Auditors

EXAMPLE:

•U.S. auditor relies on work of foreign audit firm to perform work on foreign subs of registrant

•U.S. firm chooses not to place reliance on work of other audit firm (i.e. no reference to other auditor)

47

47

Use of Other Auditors

•Foreign firm must be registered with PCAOB if:

Performing a “substantial portion of the audit”

•Foreign firm must be “recognized” by SEC

48

48

Use of Other Auditors

“Recognition” of Foreign Firm•Registration with PCAOB does not supercede existing means by which a firm demonstrates its qualifications to practice before the SEC US affiliation and Appendix K compliance

Demonstration to OCA of knowledge and experience of applying U.S. GAAP, PCAOB standards, SEC rules and SEC independence requirements

49

49

Use of Other Auditors

Other Questions:

•What if U.S. firm uses local persons as independent contractors? i.e., Individuals, not firms

•Is the U.S. firm required to travel to the foreign location as part of the audit?

50

50

Other Auditor Issues

Licensing Requirements•Have seen instances where auditor is not licensed in the state or country where principal audit procedures were conducted

Problematic in certain instances

Addressing on case-by-case basis

Contact DCF with questions on real life fact patterns

51

51

BREAKBREAK

52

52

Financial Reporting and Financial Reporting and DisclosureDisclosure

Tagged Data InitiativeTagged Data Initiative

Joel LevineJoel Levine

53

53

Tagged Data InitiativeTagged Data Initiative

Concept releaseConcept release – –

Use of tagged data to Use of tagged data to facilitate timely and facilitate timely and accurate financial analysis.accurate financial analysis.

54

54

Tagged Data InitiativeTagged Data Initiative

Possible benefits from tagged data:Possible benefits from tagged data: Information that is tagged can be Information that is tagged can be

searched, retrieved, and analyzed by searched, retrieved, and analyzed by automated means.automated means.

Reduces time, cost and errors Reduces time, cost and errors commonly associated with manual commonly associated with manual information collection and analysis.information collection and analysis.

55

55

Tagged Data InitiativeTagged Data Initiative

Rule proposal –Rule proposal –

Voluntary program allowing Voluntary program allowing registrants to furnish registrants to furnish financial information in financial information in XBRL format.XBRL format.

56

56

Concept ReleaseConcept Release

Concept release sought comment on:Concept release sought comment on:Adequacy of XBRL format and Adequacy of XBRL format and

technologies.technologies.

Types of information to be tagged.Types of information to be tagged.

Sufficiency of standard taxonomies.Sufficiency of standard taxonomies.

57

57

Concept Release Concept Release

A taxonomy is a list of standard A taxonomy is a list of standard financial reporting elements (terms) financial reporting elements (terms) with their definitions and other with their definitions and other information. These elements may be information. These elements may be tagged with:tagged with: Monetary valuesMonetary values

Text – words or labelsText – words or labels

58

58

Concept ReleaseConcept Release

Concept release also sought comment Concept release also sought comment on:on:

Commission’s role in development and Commission’s role in development and maintenance of standard taxonomies.maintenance of standard taxonomies.

Impact on investors, registrants, and Impact on investors, registrants, and accountants.accountants.

59

59

Concept ReleaseConcept Release

Comment period ended Nov. 15th:Comment period ended Nov. 15th:XBRL standard is generally sufficient XBRL standard is generally sufficient

for tagging financial information.for tagging financial information.

Technical complexity of XBRL.Technical complexity of XBRL.

Eventually, a broader range of Eventually, a broader range of information in filings could be tagged information in filings could be tagged (e.g., MD&A, industry guide data, loan (e.g., MD&A, industry guide data, loan covenants, and officer compensation).covenants, and officer compensation).

60

60

Concept ReleaseConcept Release

(Continued)(Continued)

Taxonomies should be developed and Taxonomies should be developed and maintained by the private sector, subject maintained by the private sector, subject to public review and comment and to public review and comment and Commission oversight.Commission oversight.

Impact on investors – quicker data Impact on investors – quicker data consumption allowing more time for consumption allowing more time for substantive financial analytics. substantive financial analytics.

61

61

Concept ReleaseConcept Release

(Continued)(Continued)

Impact on registrants – need to learn data Impact on registrants – need to learn data tagging concepts and software tools; tagging concepts and software tools; consider taxonomy extensions; after consider taxonomy extensions; after startup, tagging effort should be nominal startup, tagging effort should be nominal and routine.and routine.

Impact on accountants – potential for Impact on accountants – potential for enhanced financial analysis, risk enhanced financial analysis, risk assessments, and internal control testing assessments, and internal control testing once XBRL is integrated into accounting once XBRL is integrated into accounting systems and audit tools are developed.systems and audit tools are developed.

62

62

Concept ReleaseConcept Release

(Continued)(Continued)

Auditor attestation of tagged data:Auditor attestation of tagged data: Will build investor confidence in Will build investor confidence in

reliability of tagged data.reliability of tagged data. AICPA Interpretation No. 5 of SSAE AICPA Interpretation No. 5 of SSAE

No. 10 (AT Section 101): No. 10 (AT Section 101): “Attest Engagements on Financial “Attest Engagements on Financial Information Included in XBRL Information Included in XBRL Instance Documents”Instance Documents” currently currently provides sufficient guidance.provides sufficient guidance.

63

63

Voluntary ProgramVoluntary Program

Registrants would tag their financial Registrants would tag their financial information in XBRL format using a information in XBRL format using a US GAAP standard taxonomyUS GAAP standard taxonomy::

Investment ManagementInvestment Management

InsuranceInsurance

Banking and Savings InstitutionsBanking and Savings Institutions

Commercial and IndustrialCommercial and Industrial

64

64

Voluntary ProgramVoluntary Program

Regarding the XBRL documents:Regarding the XBRL documents:

Supplemental to official filing. Exhibit 100 Supplemental to official filing. Exhibit 100 to Exchange Act or Investment Company to Exchange Act or Investment Company Act filings.Act filings.

Furnished rather than “filed.”Furnished rather than “filed.”

Include in initial filing, an amendment, or Include in initial filing, an amendment, or an 8-K (6-K for foreign private issuers).an 8-K (6-K for foreign private issuers).

Information consistent with official filing.Information consistent with official filing.

65

65

Voluntary ProgramVoluntary Program

(Continued)(Continued)

Excluded from Section 302 certifications.Excluded from Section 302 certifications.

No audit opinions or review reports.No audit opinions or review reports.

Label data unaudited (unreviewed).Label data unaudited (unreviewed).

Volunteers could start and end their Volunteers could start and end their participation at any time; may submit XBRL participation at any time; may submit XBRL data regularly or from time to time.data regularly or from time to time.

66

66

Voluntary ProgramVoluntary Program

No stated end date. If adopted, after No stated end date. If adopted, after some period of time we may:some period of time we may:Leave voluntary program in place Leave voluntary program in place

indefinitely, change one or more indefinitely, change one or more features in the program, or terminate features in the program, or terminate the program.the program.

67

67

Voluntary ProgramVoluntary Program

Rule proposal sought comment on:Rule proposal sought comment on: Is there a better way to test XBRL?Is there a better way to test XBRL? Should we permit tagging of less than a Should we permit tagging of less than a

complete set of financial statements?complete set of financial statements? Concerns about company extensions?Concerns about company extensions? Eliminate 8-K or 6-K filing options?Eliminate 8-K or 6-K filing options? Should mgmt. certify XBRL data?Should mgmt. certify XBRL data? Should auditors attest to XBRL data?Should auditors attest to XBRL data? How to assess usefulness of the data?How to assess usefulness of the data?

68

68

Voluntary ProgramVoluntary Program

Comment period ended Nov. 1st:Comment period ended Nov. 1st:Generally supportive of voluntary Generally supportive of voluntary

program and proposed features.program and proposed features.

Standard taxonomies thought to be Standard taxonomies thought to be sufficiently developed for purposes of sufficiently developed for purposes of the program.the program.

Software tools may prove challenging Software tools may prove challenging to use in their current state.to use in their current state.

69

69

Voluntary ProgramVoluntary Program

All comment letters we received are All comment letters we received are available on our website:available on our website:

www.sec.govwww.sec.gov

Under “Regulatory Actions.”Under “Regulatory Actions.”

70

70

Tagged Data InitiativeTagged Data Initiative

What we’re doing:What we’re doing: Learning more about XBRL.Learning more about XBRL.

Evaluating comments received.Evaluating comments received.

Determining appropriate form of Determining appropriate form of adopting release.adopting release.

Developing internal capabilities to Developing internal capabilities to receive and analyze XBRL formatted receive and analyze XBRL formatted data.data.

71

71

Financial Reporting and Financial Reporting and DisclosureDisclosure Statement of Cash Flows and Statement of Cash Flows and

Long-Term Customer ReceivablesLong-Term Customer Receivables

Private-equity valuationPrivate-equity valuation

Non-GAAP Managed Basis Non-GAAP Managed Basis MeasuresMeasures

Dividend Policy DisclosuresDividend Policy Disclosures

Todd E. HardimanTodd E. Hardiman

72

72

Statement of Cash FlowsStatement of Cash FlowsL/T Customer ReceivablesL/T Customer Receivables

Are the cash flow effects of Are the cash flow effects of customer receivables operating customer receivables operating

or investing cash flows?or investing cash flows?

73

73

Statement of Cash FlowsStatement of Cash FlowsL/T Customer ReceivablesL/T Customer Receivables

Paragraph 22a of Statement 95:Paragraph 22a of Statement 95:

22. Cash inflows from operating activities 22. Cash inflows from operating activities are:are:

a. Cash receipts from sales of goods or a. Cash receipts from sales of goods or services, including receipts from services, including receipts from collection or sale of accounts, and collection or sale of accounts, and both short- and long-term notes both short- and long-term notes receivable from customers arising receivable from customers arising from those sales.from those sales.

74

74

Statement of Cash FlowsStatement of Cash FlowsL/T Customer ReceivablesL/T Customer Receivables

Paragraph 16a of Statement 95:Paragraph 16a of Statement 95:

16. Cash inflows from investing activities are:16. Cash inflows from investing activities are:

a. Receipts from collections or sales of loans a. Receipts from collections or sales of loans made by the enterprise and of other entities’ made by the enterprise and of other entities’ debt instruments (other than cash debt instruments (other than cash equivalents, certain debt instruments that equivalents, certain debt instruments that are acquired specifically for resale as are acquired specifically for resale as discussed in Statement 102, and securities discussed in Statement 102, and securities classified as trading securities as discussed classified as trading securities as discussed in Statement 115) that were purchased by in Statement 115) that were purchased by the enterprise.the enterprise.

75

75

Statement of Cash FlowsStatement of Cash FlowsL/T Customer ReceivablesL/T Customer Receivables

Statement 95 deliberations:Statement 95 deliberations:

Explicit consideration of Installment Explicit consideration of Installment SalesSales

Exposure Draft - split presentationExposure Draft - split presentation

Final standard – ALL cash flows from Final standard – ALL cash flows from inventory sales are operating cash flowsinventory sales are operating cash flows

76

76

Statement of Cash FlowsStatement of Cash FlowsL/T Customer ReceivablesL/T Customer Receivables

Effect of Statement 102Effect of Statement 102 - - Statement of Statement of Cash Flows – Exemption of Certain Cash Flows – Exemption of Certain Enterprises and Classification of Enterprises and Classification of Cash Flows from Certain Securities Cash Flows from Certain Securities Acquired for ResaleAcquired for Resale Are cash flows of a financial institution’s Are cash flows of a financial institution’s

trading account and similar items, such trading account and similar items, such as loans acquired for resale, as loans acquired for resale, similar tosimilar to inventoryinventory??

77

77

Statement of Cash FlowsStatement of Cash FlowsL/T Customer ReceivablesL/T Customer Receivables

Example - Captive Finance Subsidiary Example - Captive Finance Subsidiary

Assumptions:Assumptions:

Registrant (Parent) sells Product A for $10Registrant (Parent) sells Product A for $10

Customer pays no cashCustomer pays no cash

Captive finance sub issues loan to Captive finance sub issues loan to customer for $10 and remits $10 to Parentcustomer for $10 and remits $10 to Parent

78

78

Statement of Cash FlowsStatement of Cash FlowsL/T Customer ReceivablesL/T Customer Receivables

Example - Captive Finance Sub., continuedExample - Captive Finance Sub., continued

Stand-alone Parent perspective:Stand-alone Parent perspective:•Operating cash inflow of $10Operating cash inflow of $10

Stand-alone Sub perspective:Stand-alone Sub perspective:•Investing cash outflow of $10Investing cash outflow of $10

Consolidated entity perspective:Consolidated entity perspective:•Non-cash transactionNon-cash transaction

79

79

Statement of Cash FlowsStatement of Cash FlowsL/T Customer ReceivablesL/T Customer Receivables

Example - Captive Finance Sub., continuedExample - Captive Finance Sub., continued

•Conclusions:Conclusions: Consolidated entity perspectiveConsolidated entity perspective

Analogies to EITF 85-12 not persuasiveAnalogies to EITF 85-12 not persuasive

ALL Cash flows from sale of inventory are ALL Cash flows from sale of inventory are operating cash flows regardless ifoperating cash flows regardless if Collection from customer or sale to othersCollection from customer or sale to others On account or in form of a note or loanOn account or in form of a note or loan Short-term or long-termShort-term or long-term

80

80

Financial Reporting and Financial Reporting and DisclosureDisclosure

Valuation of Privately-Held-Valuation of Privately-Held-Company Equity Securities Company Equity Securities

Issued as CompensationIssued as Compensation

(VPES or “Cheap Stock”)(VPES or “Cheap Stock”)

81

81

VPES or “Cheap Stock”VPES or “Cheap Stock”

CircumstancesCircumstances•No Quoted Market PricesNo Quoted Market Prices•No Recent Sales of the Same or a Similar No Recent Sales of the Same or a Similar Company SecurityCompany Security

Valuation MethodologiesValuation Methodologies•Generally, Two Step ApproachGenerally, Two Step Approach Enterprise Value DeterminationEnterprise Value Determination

Enterprise Value Allocation (if Multiple Equity Enterprise Value Allocation (if Multiple Equity Classes)Classes)

82

82

VPES or “Cheap Stock”VPES or “Cheap Stock”

Theme #1Theme #1: The Approach Used to : The Approach Used to DetermineDetermine Enterprise Value Must be Appropriate for the Enterprise Value Must be Appropriate for the Company’s Stage of DevelopmentCompany’s Stage of Development Stages of Development Stages of Development

No revenue/founder’s capitalNo revenue/founder’s capital Initiate product development/Outside financingInitiate product development/Outside financing Achieve product development milestonesAchieve product development milestones Saleable productSaleable product Operating profitabilityOperating profitability Sustained OperationsSustained Operations

83

83

VPES or “Cheap Stock”VPES or “Cheap Stock”

Theme #1Theme #1: - continued: - continued

Three Broad Approaches to Determine Three Broad Approaches to Determine Enterprise ValueEnterprise Value

Market ApproachMarket Approach

Income ApproachIncome Approach

Asset-Based ApproachAsset-Based Approach

84

84

VPES or “Cheap Stock”VPES or “Cheap Stock”

Theme #1Theme #1: : - continued- continued

ObservationObservation::

Asset-based approach likely not appropriate Asset-based approach likely not appropriate for IPO reporting periodsfor IPO reporting periods

85

85

VPES or “Cheap Stock”VPES or “Cheap Stock”

Theme #2Theme #2: The Method Used to : The Method Used to Allocate Allocate Enterprise Value Enterprise Value Must be Appropriate for the Company’s Stage of Must be Appropriate for the Company’s Stage of DevelopmentDevelopment

Required if Multiple Classes of StockRequired if Multiple Classes of Stock

Three Broad MethodsThree Broad Methods

Probability-Weighted Expected Return MethodProbability-Weighted Expected Return Method

Possible Future Outcomes might include IPO, Possible Future Outcomes might include IPO, Remaining Private, Merger or Sale, DissolutionRemaining Private, Merger or Sale, Dissolution

Option-Pricing MethodOption-Pricing Method

Current-Value MethodCurrent-Value Method

86

86

VPES or “Cheap Stock”VPES or “Cheap Stock”

Theme #2Theme #2: -continued: -continued Two Trends in IPO Filing ReviewsTwo Trends in IPO Filing Reviews

Use of Current Value Allocation Use of Current Value Allocation MethodMethod

Averaging Allocation MethodsAveraging Allocation Methods

87

87

VPES or “Cheap Stock”VPES or “Cheap Stock”

Theme #2Theme #2 - continued - continued Use of Current Value Allocation Use of Current Value Allocation

MethodMethod

Observation:Observation:

Current-Value method likely not Current-Value method likely not appropriate for IPO reporting periodsappropriate for IPO reporting periods

88

88

VPES or “Cheap Stock”VPES or “Cheap Stock”

Theme #2Theme #2 - continued - continued Averaging Allocation MethodsAveraging Allocation Methods

Observations:Observations:Select the allocation method that is most Select the allocation method that is most appropriate for the circumstancesappropriate for the circumstances

Averaging disparate results of different Averaging disparate results of different allocation methods may not be appropriateallocation methods may not be appropriate

89

89

VPES or “Cheap Stock”VPES or “Cheap Stock”

Theme #3Theme #3: Discounts: Discounts•Objective and Reliable Support NeededObjective and Reliable Support Needed•Appropriateness of:Appropriateness of:

TypeType of Discount of Discount

Lack of Control DiscountLack of Control Discount

Disproportionate Returns?Disproportionate Returns?

90

90

VPES or “Cheap Stock”VPES or “Cheap Stock”

Theme #3Theme #3: Discounts - continued: Discounts - continued•Appropriateness of:Appropriateness of:

MagnitudeMagnitude of Discount of Discount No Bright LinesNo Bright Lines

Burden on ManagementBurden on Management

Sufficient Objective SupportSufficient Objective Support

Facts and Circumstances of EntityFacts and Circumstances of Entity

91

91

Financial Reporting and Financial Reporting and DisclosureDisclosure

Non-GAAP Managed-Basis Non-GAAP Managed-Basis MeasuresMeasures

92

92

Non-GAAP Managed-Basis Non-GAAP Managed-Basis MeasuresMeasures

•Financial Institutions and Retailing Financial Institutions and Retailing CompaniesCompanies Remove sale treatment of loan and receivable Remove sale treatment of loan and receivable

securitizations accounted for as salessecuritizations accounted for as sales

•Non-Financial InstitutionsNon-Financial Institutions Include revenue of businesses managed on Include revenue of businesses managed on

behalf of othersbehalf of others

93

93

Non-GAAP Managed-Basis Non-GAAP Managed-Basis MeasuresMeasures

Non-Financial InstitutionsNon-Financial Institutions

System Wide RevenuesSystem Wide Revenues Frequently calculated asFrequently calculated as

Registrant’s revenues +Registrant’s revenues +

Managed entities revenue – Managed entities revenue –

Registrant’s management feesRegistrant’s management fees

Appropriate or prohibited?Appropriate or prohibited?

94

94

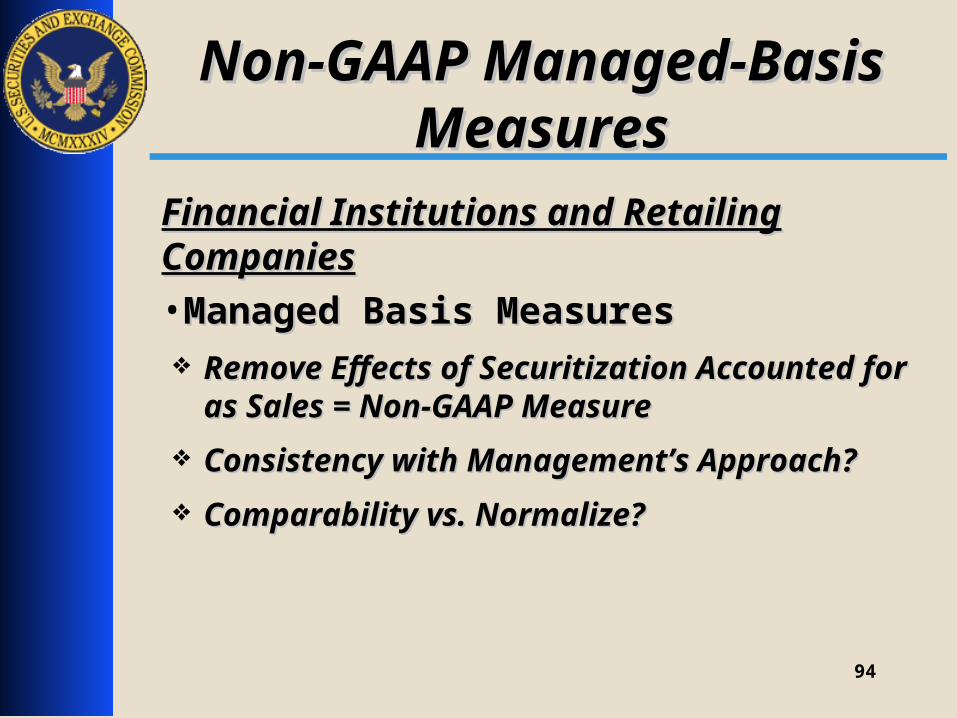

Non-GAAP Managed-Basis Non-GAAP Managed-Basis MeasuresMeasures

Financial Institutions and Retailing Financial Institutions and Retailing CompaniesCompanies•Managed Basis MeasuresManaged Basis Measures Remove Effects of Securitization Accounted for Remove Effects of Securitization Accounted for

as Sales = Non-GAAP Measureas Sales = Non-GAAP Measure

Consistency with Management’s Approach?Consistency with Management’s Approach?

Comparability vs. Normalize?Comparability vs. Normalize?

95

95

Non-GAAP Managed-Basis Non-GAAP Managed-Basis MeasuresMeasures

Financial Institutions and Retailing Financial Institutions and Retailing CompaniesCompanies

Disclosures required by Statement 140Disclosures required by Statement 140 Not a Non-GAAP MeasureNot a Non-GAAP Measure

Goal is to Highlight Sources of Risk and Goal is to Highlight Sources of Risk and Benefit Stemming from Retained InterestBenefit Stemming from Retained Interest

96

96

Financial Reporting and Financial Reporting and DisclosureDisclosure

Management’s Statement of Management’s Statement of Intent to Pay Future DividendsIntent to Pay Future Dividends

and the Need forand the Need for

Dividend Policy Disclosures Dividend Policy Disclosures

97

97

Dividend Policy DisclosuresDividend Policy Disclosures

•Income Deposit Security (IDS)Income Deposit Security (IDS)Yield =Yield =

Coupon on DebtCoupon on Debt

plusplus

Intended DividendIntended Dividend

Equal to Cash in Excess of Operating Equal to Cash in Excess of Operating NeedsNeeds

Paid quarterlyPaid quarterly

98

98

Dividend Policy DisclosuresDividend Policy Disclosures

•Why Focus on Disclosures about Intended Why Focus on Disclosures about Intended Dividends?Dividends?

SignificanceSignificance CompanyCompany

Assumes Best Use of Excess Cash is Payout to Assumes Best Use of Excess Cash is Payout to Shareholders, Not Reinvestment in BusinessShareholders, Not Reinvestment in Business

MarketingMarketing Contrast to equity IPO where return on Contrast to equity IPO where return on

investment stems primarily from stock investment stems primarily from stock appreciationappreciation

99

99

Dividend Policy DisclosuresDividend Policy Disclosures

•Why Focus on Disclosures about Intended Why Focus on Disclosures about Intended Dividends?Dividends?DiscretionaryDiscretionary

No Contractual Obligation to Pay No Contractual Obligation to Pay Different from REITs – Not Obligated by Tax Different from REITs – Not Obligated by Tax

Code to Pay Out Most of their CashCode to Pay Out Most of their Cash Board Discretion as to Timing and Amount (can Board Discretion as to Timing and Amount (can

be $0), regardless of policybe $0), regardless of policy Shareholder has No Contractual Demand Shareholder has No Contractual Demand

Right Right Lack of PrecedentLack of Precedent

100

100

Dividend Policy DisclosuresDividend Policy Disclosures

•Key Elements of DisclosureKey Elements of Disclosure:: Clear articulation of what the dividend policy Clear articulation of what the dividend policy

will be, how the company arrived at it, and how will be, how the company arrived at it, and how they expect to be able to pay itthey expect to be able to pay it

Identification of Risks and LimitationsIdentification of Risks and Limitations Inclusion of Forward-looking information to Inclusion of Forward-looking information to

support ability to pay intended dividends support ability to pay intended dividends Analysis - Liquidity and Capital ResourcesAnalysis - Liquidity and Capital Resources

Note: Note: NotNot a One-Size Fits All Model: address a One-Size Fits All Model: address specific facts and circumstancesspecific facts and circumstances

101

101

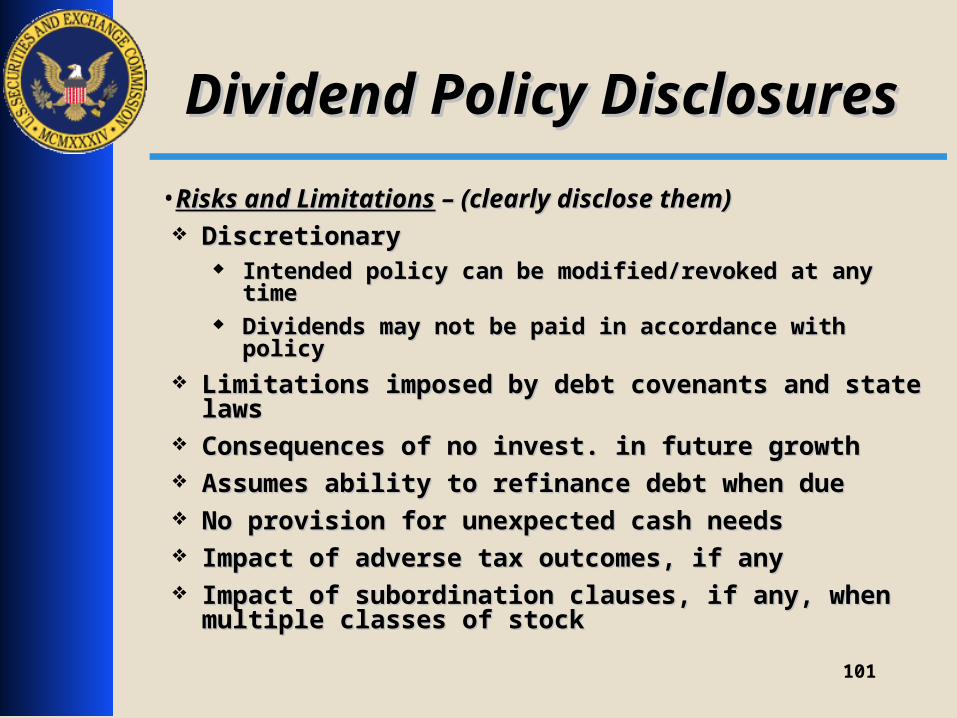

Dividend Policy DisclosuresDividend Policy Disclosures

•Risks and LimitationsRisks and Limitations – (clearly disclose them) – (clearly disclose them) DiscretionaryDiscretionary

Intended policy can be modified/revoked at any time Intended policy can be modified/revoked at any time Dividends may not be paid in accordance with policyDividends may not be paid in accordance with policy

Limitations imposed by debt covenants and state lawsLimitations imposed by debt covenants and state laws Consequences of no invest. in future growth Consequences of no invest. in future growth Assumes ability to refinance debt when due Assumes ability to refinance debt when due No provision for unexpected cash needsNo provision for unexpected cash needs Impact of adverse tax outcomes, if anyImpact of adverse tax outcomes, if any Impact of subordination clauses, if any, when multiple Impact of subordination clauses, if any, when multiple

classes of stockclasses of stock

102

102

Dividend Policy DisclosuresDividend Policy Disclosures

•Forward-looking infoForward-looking info - - (include in filing)(include in filing)

Must support the assertion registrant Must support the assertion registrant will have will have cashcash necessary to pay the necessary to pay the intended dividends intended dividends

Intended dividends policy should not be Intended dividends policy should not be stated for periods in excess of period stated for periods in excess of period supported by expected future cash flows supported by expected future cash flows (for example, next 12 months)(for example, next 12 months)

103

103

Dividend Policy DisclosuresDividend Policy Disclosures

•Forward-looking infoForward-looking info - - (include in filing)(include in filing) Balance Forward-Looking “estimated cash available” Balance Forward-Looking “estimated cash available”

with comparable Historical Amounts of “cash available”with comparable Historical Amounts of “cash available”

Identify Differences from Historical Amounts – perhapsIdentify Differences from Historical Amounts – perhaps

Increased costs due to being publicIncreased costs due to being public

Increased interest expense (Income Deposit Sec.)Increased interest expense (Income Deposit Sec.)

Changes in levels of capital expendituresChanges in levels of capital expenditures

Explain why mgt. believes they can pay intended Explain why mgt. believes they can pay intended dividend if historical amounts indicate otherwisedividend if historical amounts indicate otherwise

Identify need, if any, to borrow to pay dividendsIdentify need, if any, to borrow to pay dividends

104

104

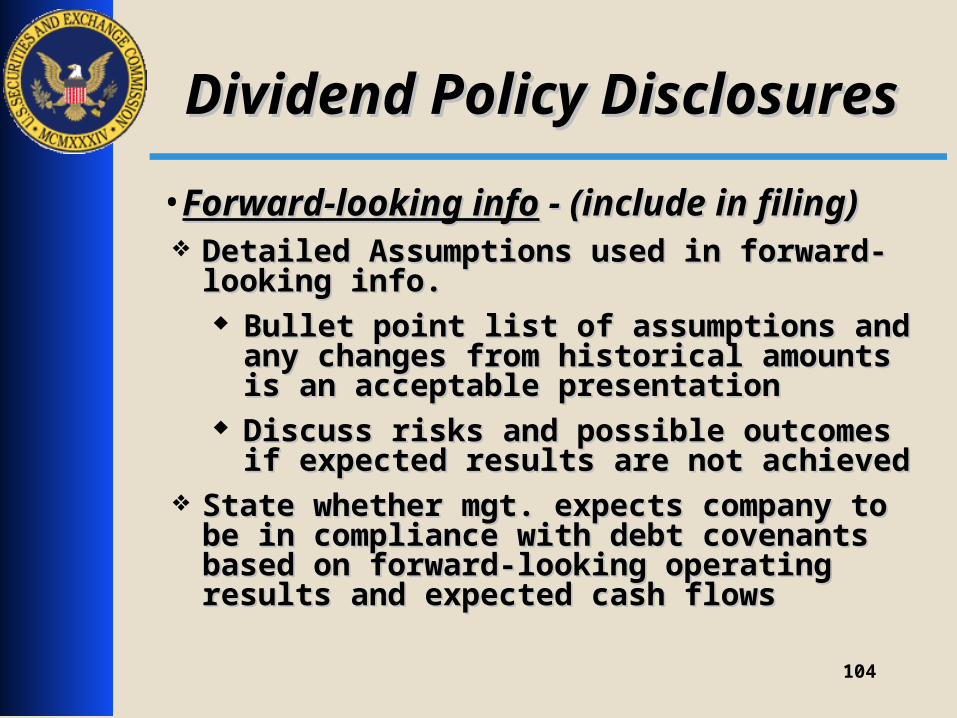

Dividend Policy DisclosuresDividend Policy Disclosures

•Forward-looking infoForward-looking info - (include in filing) - (include in filing) Detailed Assumptions used in forward-looking Detailed Assumptions used in forward-looking

info.info. Bullet point list of assumptions and any Bullet point list of assumptions and any

changes from historical amounts is an changes from historical amounts is an acceptable presentationacceptable presentation

Discuss risks and possible outcomes if Discuss risks and possible outcomes if expected results are not achievedexpected results are not achieved

State whether mgt. expects company to be in State whether mgt. expects company to be in compliance with debt covenants based on compliance with debt covenants based on forward-looking operating results and expected forward-looking operating results and expected cash flowscash flows

105

105

Dividend Policy DisclosuresDividend Policy Disclosures

• MD&A -Liquidity and Capital ResourcesMD&A -Liquidity and Capital Resources Intended dividend policy for the next year, and how they Intended dividend policy for the next year, and how they

intend to fund it (e.g., cash from operations or intend to fund it (e.g., cash from operations or borrowings/credit facility)borrowings/credit facility)

Assumptions re: Cash available for dividends Assumptions re: Cash available for dividends

Effect of new securities and financing agreements, if anyEffect of new securities and financing agreements, if any

Increased interest expenseIncreased interest expense

Effect of paying out cash as dividends rather than Effect of paying out cash as dividends rather than retaining for expansion and reinvestment in the businessretaining for expansion and reinvestment in the business

106

106

ConclusionConclusion

Questions and AnswersQuestions and Answers

??

???

?