Asia's rainy day economics. Currency wars and market volatility

Upload

kyra-rogersCategory

view

25download

0description

Private Wealth ManagementDeutsche Bank

Currency Wars and QE2: the implications for global investing

Marshall GittlerChief Strategist, EMEAPlace des Bergues 3CH-1211 Geneve [email protected]+41 (0) 22 739 0463

December, 2010

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 2

Hyperinflation

Currency Wars and QE2 How to fix the global imbalances?

wants to be to

as

is to

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 3

Hyperinflation Deflation— Bond yields fall; yield curve flattens

— Risk premium declines

— Yield spreads with corporate bonds compress

— Stocks rise; wealth effect boosts spending

— Currency declines, exports pick up, economy recovers

Currency wars and QE2 The theoretical impact of QE

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 4

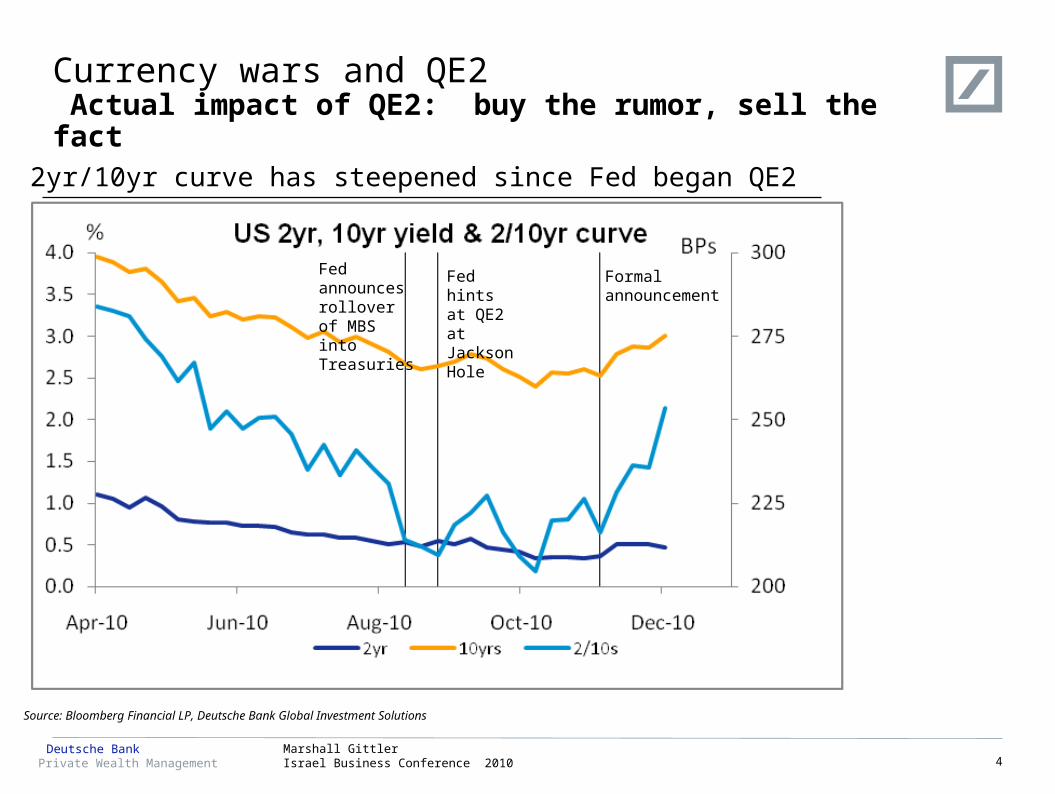

Currency wars and QE2 Actual impact of QE2: buy the rumor, sell the fact

Hyperinflation Deflation

Source: Bloomberg Financial LP, Deutsche Bank Global Investment Solutions

2yr/10yr curve has steepened since Fed began QE2

Fed announces rollover of MBS into Treasuries

Fed hints at QE2 at Jackson Hole

Formal announcement

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 5

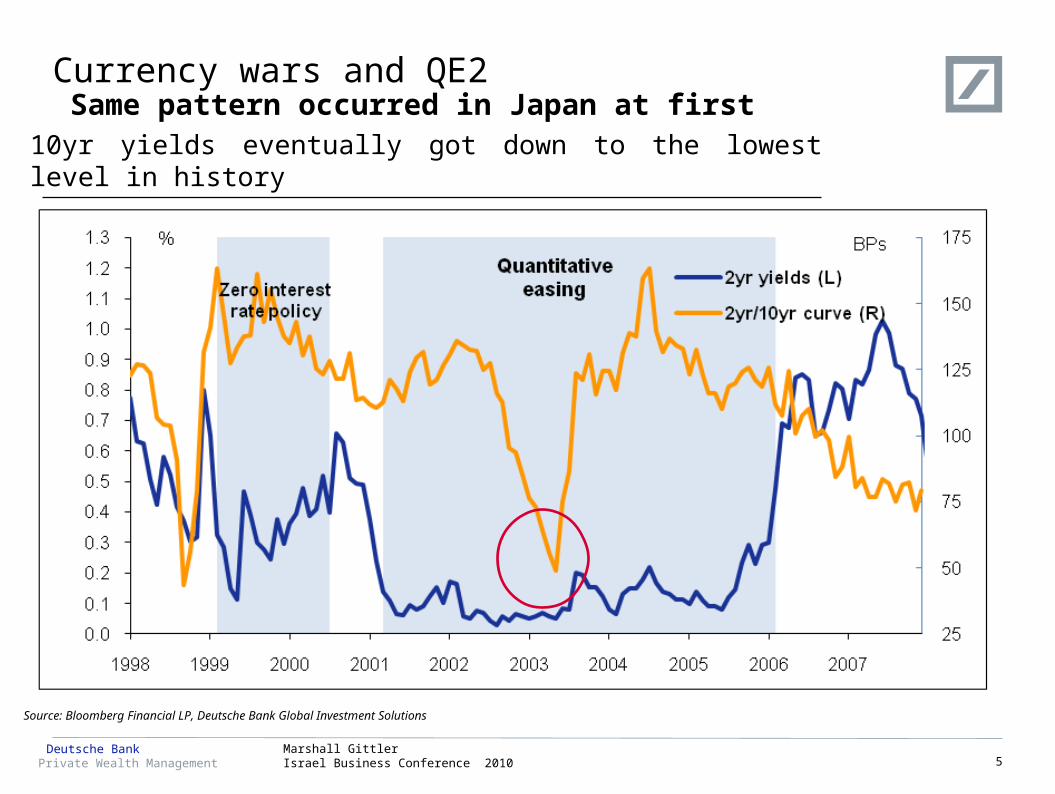

Currency wars and QE2 Same pattern occurred in Japan at first

Hyperinflation Deflation

Source: Bloomberg Financial LP, Deutsche Bank Global Investment Solutions

10yr yields eventually got down to the lowest level in history

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 6

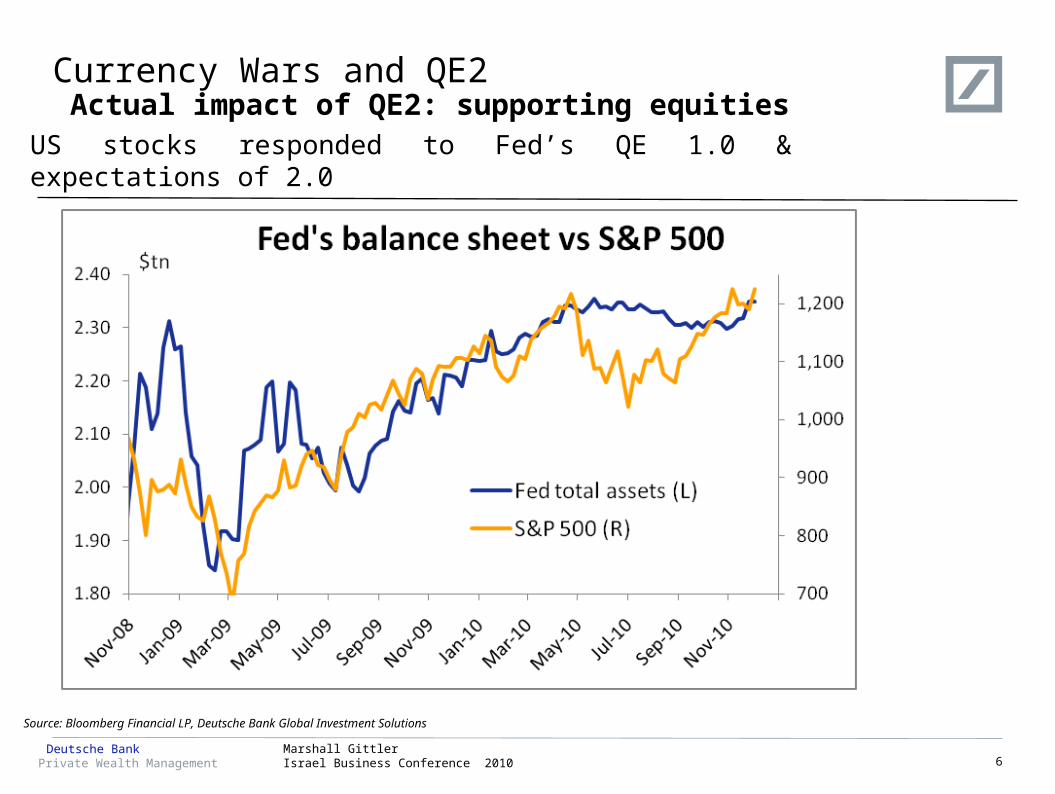

Currency Wars and QE2 Actual impact of QE2: supporting equities

Hyperinflation

Source: Bloomberg Financial LP, Deutsche Bank Global Investment Solutions

US stocks responded to Fed’s QE 1.0 & expectations of 2.0

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 7

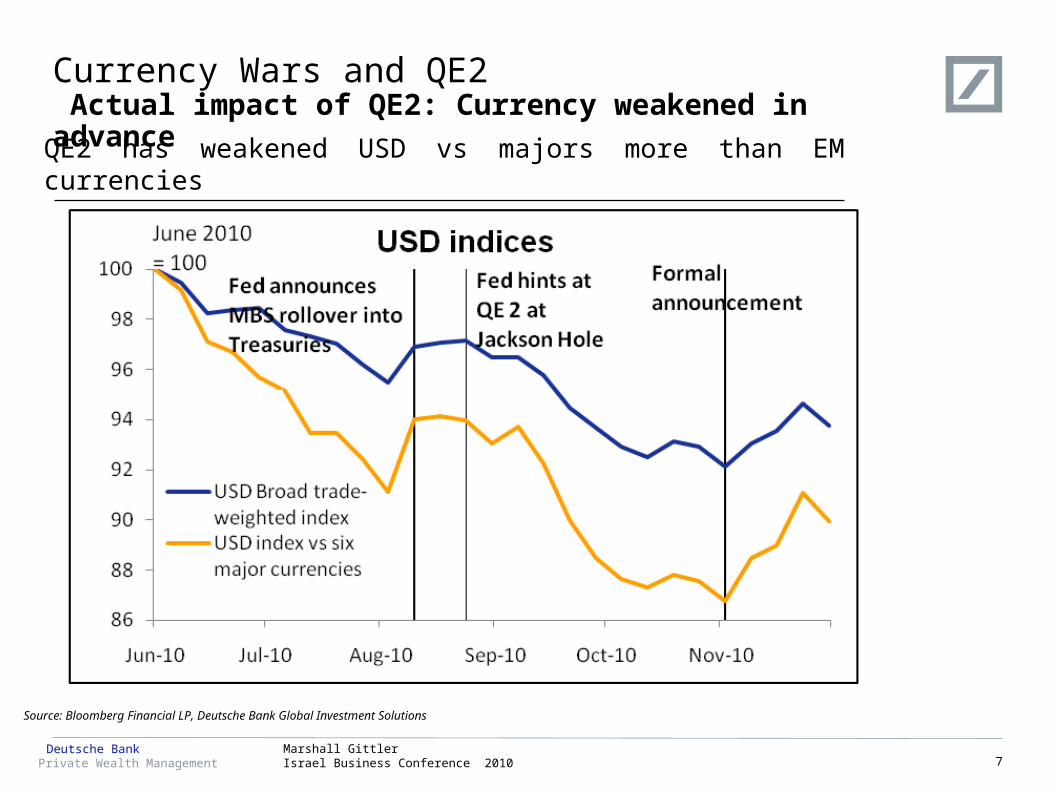

Currency Wars and QE2 Actual impact of QE2: Currency weakened in advance

Hyperinflation Deflation

Source: Bloomberg Financial LP, Deutsche Bank Global Investment Solutions

QE2 has weakened USD vs majors more than EM currencies

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 8

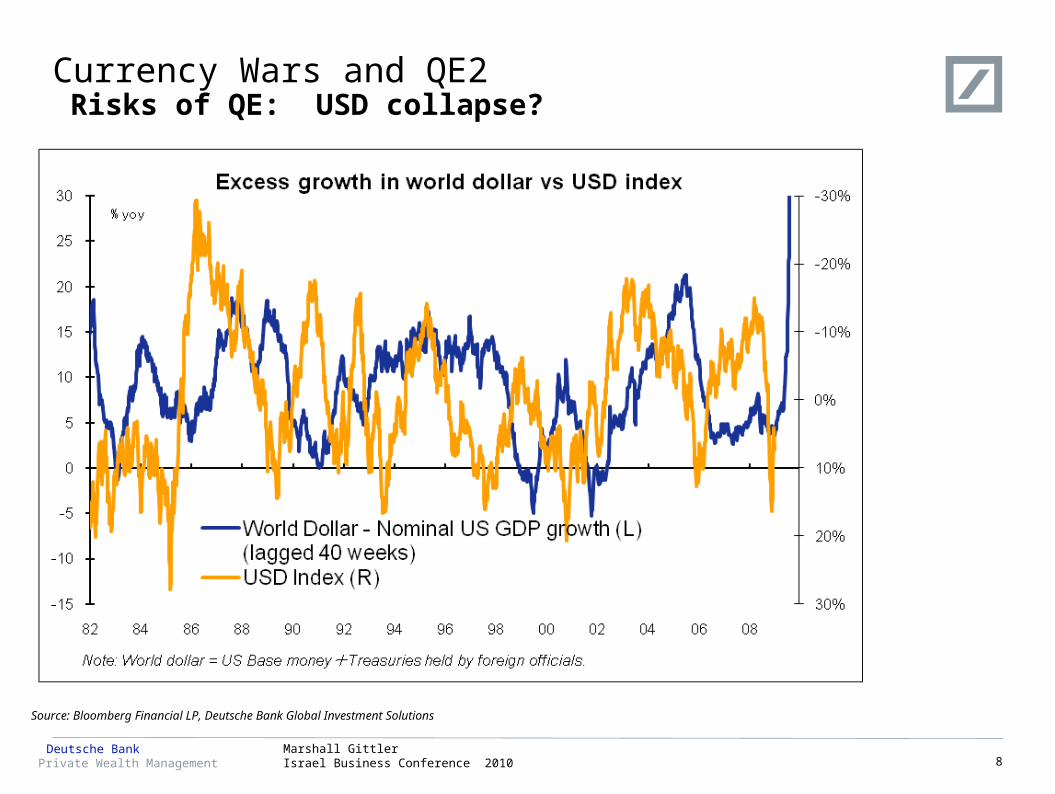

Currency Wars and QE2 Risks of QE: USD collapse?

Hyperinflation Deflation

Source: Bloomberg Financial LP, Deutsche Bank Global Investment Solutions

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 9

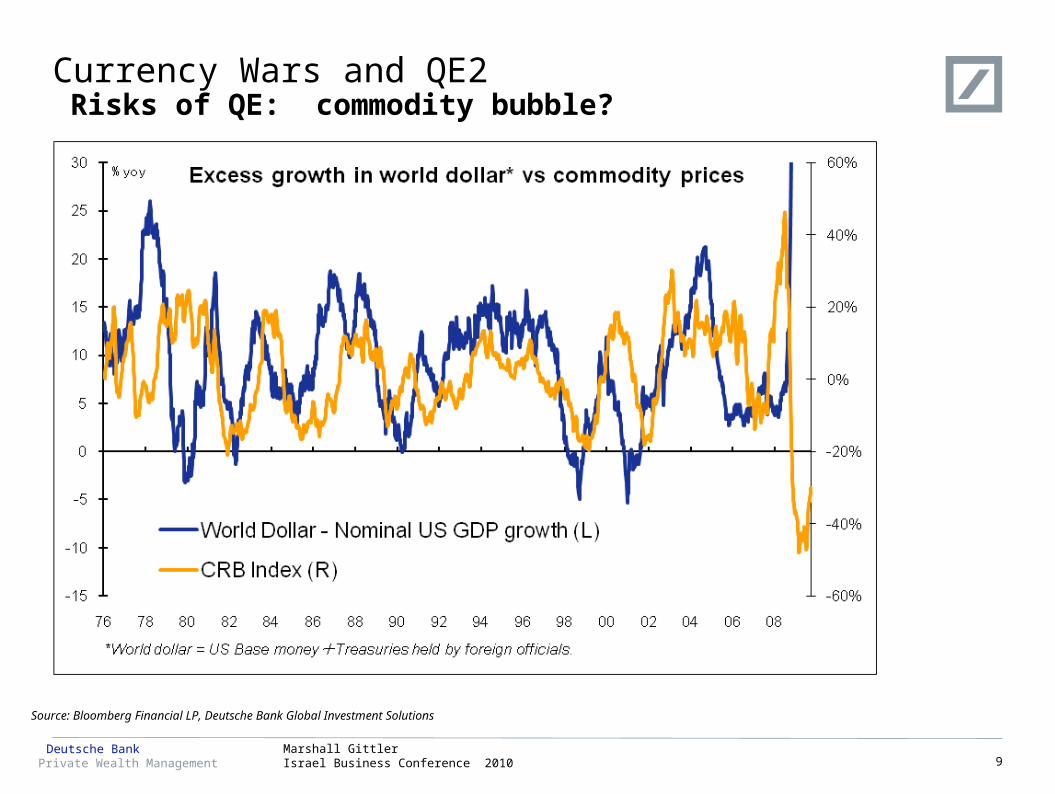

Currency Wars and QE2 Risks of QE: commodity bubble?

Hyperinflation Deflation

Source: Bloomberg Financial LP, Deutsche Bank Global Investment Solutions

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 10

Currency Wars and QE2 Risks of QE: global bubble?

Hyperinflation Deflation

Source: Bloomberg Financial LP, Deutsche Bank Global Investment Solutions

Did Japan’s QE ignite a global bubble? If so, what might 3 CBs QE do?

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 11

Currency Wars and QE2 Lower risk premium = search for yield

Hyperinflation Deflation— QE to force investors into riskier assets— Money likely to flow to countries with:

— a less expansionary monetary policies (e.g., Eurozone, Switzerland or EM countries);

— higher interest rates (e.g. the EM countries); and — higher expected growth rates (e.g., EM countries)

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 12

Currency Wars and QE2 EM bonds: not yet in bubble territory

Hyperinflation Deflation

Source: Bloomberg Financial LP, Deutsche Bank Global Investment Solutions. Data as of 6 Dec 2010.

EM bonds generally have higher nominal & real yields than DM bonds

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 13

Currency Wars and QE2 Other carry trades: DM credit, high-yielding equities

Hyperinflation Deflation— Keeping rates low for long should encourage carry trades— We recommend:

— FX carry trades— Corporate bonds— Equities with a substantial likelihood of high

paybacks— Real estate & REITs

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 14

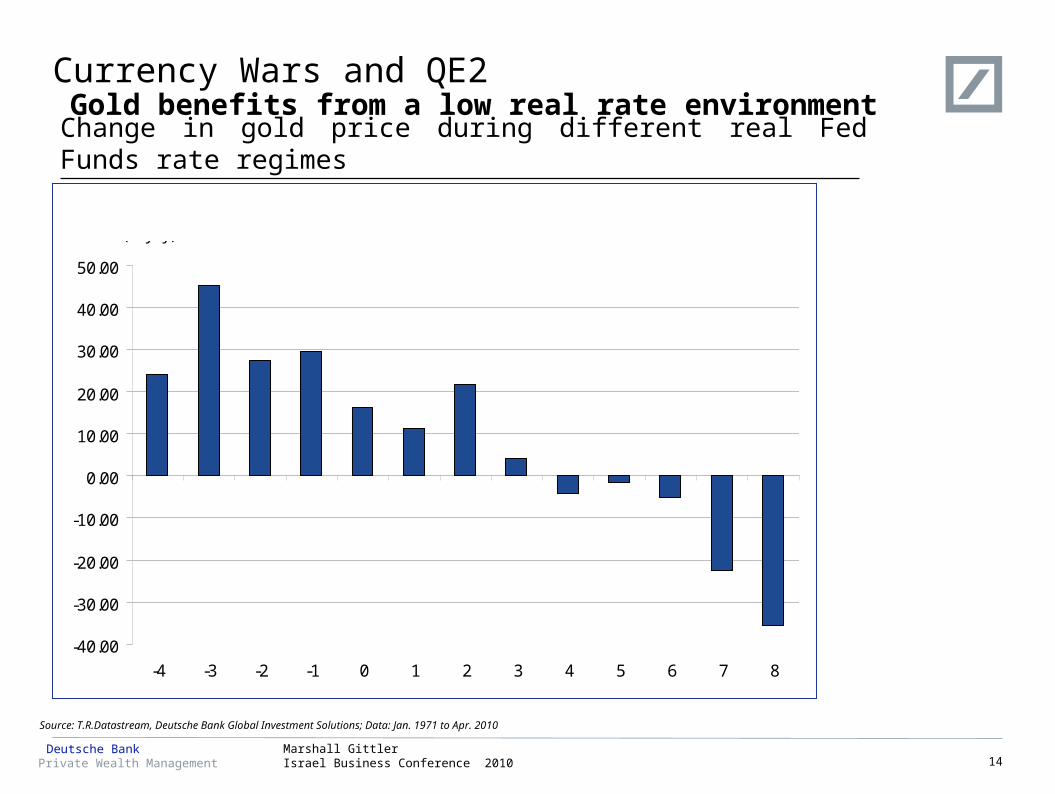

Source: T.R.Datastream, Deutsche Bank Global Investment Solutions; Data: Jan. 1971 to Apr. 2010

-40.00

-30.00

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

-4 -3 -2 -1 0 1 2 3 4 5 6 7 8

Gold (% yoy)

Real Fed Funds Rate (%)

Change in gold price during different real Fed Funds rate regimes

Currency Wars and QE2 Gold benefits from a low real rate environment

Private Wealth ManagementDeutsche Bank Marshall Gittler

Israel Business Conference 2010 15

IMPORTANT NOTICE

Private Wealth Management offers wealth management solutions for wealthy individuals, their families and select institutions worldwide. Deutsche Bank Private Wealth Management, through Deutsche Bank AG, its affiliated companies and its officers and employees (collectively “Deutsche Bank”) have published this document in good faith and on the following basis. This document has been prepared without consideration of the investment needs, objectives or financial circumstances of any investor. Before making an investment decision, investors need to consider, with or without the assistance of an investment adviser, whether the investments and strategies described or provided by Deutsche Bank, are appropriate, in light of their particular investment needs, objectives and financial circumstances. Furthermore, this document is for information/discussion purposes only and does not constitute an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Deutsche Bank does not give tax or legal advice. Investors should seek advice from their own tax experts and lawyers, in considering investments and strategies suggested by Deutsche Bank. Investments with Deutsche Bank are not guaranteed, unless specified. Unless notified to the contrary in a particular case, investment instruments are not insured by the Federal Deposit Insurance Corporation ("FDIC") or any other governmental entity, and are not guaranteed by or obligations of Deutsche Bank AG or its affiliates. Although information in this document has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness, and it should not be relied upon as such. All opinions and estimates herein, including forecast returns, reflect our judgment on the date of this report and are subject to change without notice and involve a number of assumptions which may not prove valid. Investments are subject to investment risk, including market fluctuations, regulatory change, possible delays in repayment and loss of income and principal invested. The value of investments can fall as well as rise and you might not get back the amount originally invested at any point in time. This publication contains forward looking statements. Forward looking statements include, but are not limited to assumptions, estimates, projections, opinions, models and hypothetical performance analysis. The forward looking statements expressed constitute the author’s judgement as of the date of this material. Forward looking statements involve significant elements of subjective judgements and analyses and changes thereto and/or consideration of different or additional factors could have a material impact on the results indicated. Therefore, actual results may vary, perhaps materially, from the results contained herein. No representation or warranty is made by Deutsche Bank as to the reasonableness or completeness of such forward looking statements or to any other financial information contained herein. The terms of any investment will be exclusively subject to the detailed provisions, including risk considerations, contained in the Offering Documents. When making an investment decision, you should rely solely on the final documentation relating to the transaction and not the summary contained herein. This document may not be reproduced or circulated without our written authority. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, including the United States, where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Deutsche Bank to any registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions. Past performance is no guarantee of future results; nothing contained herein shall constitute any representation or warranty as to future performance. Further information is available upon investor's request.