Currency Trader 0805

45

CHINESE YAWN CHINESE YAWN CHINA REVALUES, MARKETS SHRUG: What’s next? • SECOND-HALF DOLLAR OUTLOOK: Will the buck retain its pluck? • TRADING STRATEGIES: The new carry trade • BRIT POUND sell-off pattern • NEW DAILY FX INDEX • UNDERSTANDING the parabolic indicator

description

trading strategies, FX index, parabolic indicator

Transcript of Currency Trader 0805

CHINESE YAWNCHINESE YAWNCHINA REVALUES, MARKETS SHRUG:

What’s next?• SECOND-HALF

DOLLAR OUTLOOK: Will the buck retain its pluck?

• TRADING STRATEGIES: The new carry trade

• BRIT POUND sell-off pattern

• NEW DAILY FX INDEX

• UNDERSTANDING the parabolic indicator

Contributors . . . . . . . . . . . . . . . . . . . . .6

Letters . . . . . . . . . . . . . . . . . . . . . . . . . .8

Forex Resources . . . . . . . . . . . . . . . . .8

Industry NewsChina abandons yuan peg . . . . . . . . . . .9China uncouples its currency from the U.S.dollar — sort of.By Carlise Peterson

EBS creates new trading platform . . . .11

Global MarketsU.S. dollar: Does the buck stop here? . . . . . . . . . .12Will the dollar continue to surprise in the second half of 2005?By Currency Trader Staff

Near-term British pound vulnerability . . . . . . . . . . . . . .16Interest rates, debt, and housing drive Britishpound outlook for the upcoming months.By Tim Clayton

Spot CheckBritish pound . . . . . . . . . . . . . . . . . . .20The pound has tumbled vs. the dollar as oflate, but does that mean it’s setting up for arebound?By Currency Trader Staff

Big Picture . . . . . . . . . . . . . . . . . . . . .22Detecting the professionals’ footprints:Lessons of the Chinese revaluationWhat China’s currency revaluation can teachus about the way the forex market works.By Barbara Rockefeller

Currency Strategies . . . . . . . . . . . . .28Dollar-yen: The year’s hottest carry tradeHow to play the U.S. dollar/Japanese yeninterest-rate relationship.By Kathy Lien

Indicator Basics . . . . . . . . . . . . . . . .32Parabolic stopHow to calculate and interpret this mechanicalstop-loss and trading approach.By Currency Trader Staff

continued on p. 4

CONTENTS

2 August 2005 • CURRENCY TRADER

4 August 2005 • CURRENCY TRADER

CONTENTS

Have a question about something you’ve seen in Currency Trader?

Submit your editorial queries or comments to

Looking for an advertiser?Consult the list below and click on the company name for a direct link to the ad in this month’s

issue of Currency Trader.

Index of Advertisers

Currency Futures . . . . . . . . . . . . . .36Barclay Group launches new forex indexMarket barometer tracks currency traders on adaily basis. By Currency Trader staff

International Market Summary . . .38

Global News Briefs . . . . . . . . . . . . .40

Events . . . . . . . . . . . . . . . . . . . . . . . . .41

Global Economic Calendar . . . . . . .42

Forex Trade Journal . . . . . . . . . . . .43

Key Concepts and Definitions . . . .44

FXCM Refco

Gain Capital

Investorflix

WorldCupAdvisor.com

MetaStock

Editor-in-chief: Mark [email protected]

Managing editor: Molly [email protected]

Associate editor: Carlise Peterson [email protected]

Associate editor: David Bukey [email protected]

Contributing editor: Jeff [email protected]

Editorial assistant andWebmaster: Kesha Green

Art director: Laura [email protected]

President: Phil [email protected]

Publisher,Ad sales East Coast and Midwest:

Ad sales West Coast and Southwest only:

Allison [email protected]

Classified ad sales: Mark [email protected]

Volume 2, Issue 8. Currency Trader is published monthly by TechInfo, Inc., 150 S. Wacker Drive, Suite 880, Chicago, IL 60606. Copyright © 2005TechInfo, Inc. All rights reserved. Information in this publication may not bestored or reproduced in any form without written permission from the publisher.

The information in Currency Trader magazine is intended for educational pur-poses only. It is not meant to recommend, promote or in any way imply theeffectiveness of any trading system, strategy or approach. Traders are advisedto do their own research and testing to determine the validity of a trading idea.Trading and investing carry a high level of risk. Past performance does notguarantee future results.

For all subscriber services:www.currencytradermag.com

A publication of Active Trader®

CONTRIBUTORS

6 August 2005 • CURRENCY TRADER

CONTRIBUTORS

� Barbara Rockefeller (www.rts-forex.com) is aninternational economist with a focus on foreign exchange.She has worked as a forecaster, trader, and consultant atCitibank and other financial institutions, and currently pub-lishes two daily reports on foreign exchange. Rockefeller isthe author of Technical Analysis for Dummies (2004), 24/7Trading Around the Clock, Around the World (John Wiley &Sons, 2000), The Global Trader (John Wiley & Sons, 2001), andHow to Invest Internationally, published in Japan in 1999. Abook tentatively titled How to Trade FX is in the works.

� Kathy Lien is a chief strategist atFXCM, where she is responsible forresearch and analysis for DailyFX.com,including technical and fundamentalresearch reports, market commentaries,and trading strategies. She was an asso-ciate at JP Morgan Chase, where sheworked for more than three years incredit derivatives, cross markets, and foreign exchangetrading. Lien’s experience encompasses trading both in andout of the forex market, including interest rate derivatives,bonds, equities, and futures. She has written for variousindustry publications and news outlets, including CBSMarketWatch, and she is frequently quoted on Bloombergand Reuters. She is also author of the forthcoming book DayTrading The Currency Market (John Wiley & Sons).

� Tim Clayton is an international economist specializingin the global currency markets, macroeconomics, and inter-est rates for close to 20 years. For the past six years he hasbeen head of economics at UK-based currency specialistsInvestica Ltd. In that role, he oversees the production ofInvestica’s currency reports including daily market analy-sis.

FOREX RESOURCES

8 CURRENCY TRADER • August 2005

LETTERS

FOREX RESOURCES

COESfxTM’s partnership with NetPicks Forex enables NetPicks customers to trade on the COESfx Level 1 TradingPlatform. NetPicks Forex customers trading on COESfx will be able to work with live executable prices, making each par-ticipant, in effect, their own market maker. The COESfx electronic network enables automatic execution of the NetPicksstrategy. Also, all participants on the COESfx network will have the ability to try NetPicks Forex for a free, three-week trialof their Forex Trading Systems. For more information, see the companies’ Web sites: www.coesfx.com andwww.NetPicksforex.com.

In addition, COESfx Inc. has added 10 new currency pairs to its Web-based Electronic Currency Network (ECN), nearly dou-bling the amount of currencies available to retail and institutional investors. The new currency pairs include EUR/CAD,EUR/AUD, AUD/CAD, GBP/AUD, GBP/CAD, GBP/CHF, CHF/JPY, CAD/JPY, AUD/JPY, and AUD/CHF. Spot gold is alsobeing offered on the COESfx ECN — the first in a wide range of spot tradable commodities to be added to the platform.

Interbank FX (www.interbankfx.com) and Equis International (www.equis.com) have partnered to enhanceMetaStock Pro FX, the new real-time version of MetaStock specifically created for forex trading. MetaStock Pro FX usesadvanced charting and technical indicators to help investors analyze the forex market. Interbank FX has developed a pro-prietary execution engine interface called Pro FX Trader 2.0 that is incorporated into the MetaStock Pro FX software. Theintegration allows MetaStock customers the ability to trade live or demo accounts directly from MetaStock Pro FX soft-ware. MetaStock customers can execute from live streaming prices. The Interbank FX engine includes automated trailingstops, wireless trading from PDA devices, direct Interbank dealing to world money center banks, and guaranteed liquidi-ty for up to $10,000,000 per execution. Money managers utilizing MetaStock Pro will also have access to the Interbank FXPAMM 3.0.

Spot forex volume

Iuse [retail forex broker] for trading. They offer freecharting packages but their charts do not display vol-ume. They said that there is no way to show volume in

the charts because trading takes places in many differentplaces throughout the world.

However, there is volume displayed in Figure 5 on page37 of the January 2005 issue of Currency Trader. Also, there isvolume displayed in “Teaching the RSI new tricks” onpages 36 to 39 of the May 2005 issue. Could you pleaseexplain what this volume is?

— Helio J. Leal

It is true that it is impossible to include actual volume for spotforex. The chart in the January issue is mislabeled. The bars belowthe price series in that chart represent an indicator that is not rel-evant to the particular trading approach, but which the authorincluded in the chart. We should have deleted the indicator. Ourapologies for the confusion.

The volume shown in the charts in “Teaching the RSI newtricks” (Currency Trader, May 2005) is called “tick volume,”and it’s essentially an approximation supplied by the quote ven-dor. Basically, the number and size of price changes are used toreflect volume: Every time there is a price change, either an up tickor a down tick, the tick volume increases by 1; if the price changesby 5 pips, the tick volume climbs 5, and so on.

Scarce options info

Iwas wondering if you could point to where I could goto learn more about forex options. Is there a goodbook on the subject you recommend? What other

resources are there at my disposal (i.e., Web sites,newsletters, or training seminars)?

— Steve

Information about spot forex options is scarce becausethese trades are a breed apart (see “Forex options,”Currency Trader, June 2005 and “Currency Basics:Forex options,” Currency Trader, March 2005), and veryfew retail forex brokers offer them. Options on currencyfutures are much more readily accessible to retailtraders.

August 2005 • CURRENCY TRADER 9

MARKET NEWS BY CARLISE PETERSON

O n July 21, the People’s Bank of China(PBOC) announced it was abandoning itspolicy of pegging the value of its currency,the remninbi , or yuan, to the U.S. dollar at

a fixed rate. From now on the yuan will be linked to a bas-ket of as-yet unnamed currencies (which will include thedollar) and allowed to trade in a daily band of plus orminus 0.3 percent.

The move was an immediate 2.1 percent appreciation inthe value of the yuan, from the 8.28 yuan-per-dollar rate that

had prevailed for the past decade, to 8.11 yuan-per-dollar.Although the move was widely praised among govern-

ments and economists as the first step toward greater flexi-bility in China’s forex regime, many analysts saw it mostlyas a political move aimed mostly at appeasing the U.S. andother trading partners.

As expected, the revaluation of the yuan initially raisedthe value of Asian currencies, including the yen vs. the dol-lar. However, these moves were generally short lived (see“Initial market reaction to Chinese revaluation muddled”).

Some analysts doubt China will reval-ue the yuan again any time soon.

“It seems little further appreciation ofthe yuan is likely in the near-term, andwhile some will continue to focus onbasket components and their weights,we doubt that will provide much guid-ance to movements in the yuan — or inthe Euro/dollar or dollar/yen, for thatmatter,” says Mark Austin, global headof currency strategy at HSBC bank.

Glenn Stevens, managing director ofGain Capital, believes the revaluationmoves China in the right direction, muchlike the Mexican peso adjustmentapproximately 10 years ago, whichunpegged the peso from the dollar andallowed it to float freely. He likens thisannouncement to lifting the top off a potof boiling water: While it temporarilyrelieves some immediate pressure,things are still hot.

Most forex watchers seem to be hedg-ing their bets regarding the longer-termimpact of the move.

According to U.K.-based research firmFXToday, “the Chinese move to adjustthe yuan will tend to dominate in theshort term, even though the move is actu-ally fairly limited. Volatility is likely to bea key feature, especially as short specula-tive yen positions were extreme and thiswill have a wider dollar impact.”

China abandons yuan peg

People’s Bank of China statement

Introducing it as a step to “establish and improve the socialist marketeconomic system in China,” on July 21, 2005, the People’s Bank ofChina issued a short statement regarding its new foreign exchange

policy. The highlights:

1. The exchange rate of the U.S. dollar against the remninbi (RMB) will be adjusted to 8.11 yuan per U.S. dollar (a 2-percent downward adjustment from the former rate of 8.28).

2. China will use a “managed floating exchange rate regime based on market supply and demand,” whereby the RMB will no longer be pegged to the U.S. dollar and will instead be valued against a basket of currencies.

3. The daily U.S. dollar/RMB rate will be allowed to float within a ±0.3 percent band around the “central parity” published by the PBOC, and the prices of other currencies against the RMB will be able to move within certain bands to be announced by the PBOC. The PBOC will adjust the RMB exchange rate band “when necessary according to market development as well as the economic and financial situation.”

The full text of the announcement can be found at www.pbc.gov.cn/english/.

Traders and analysts weigh in on the possible impact of the Chinese yuan revaluation

on the world’s foreign exchange market.

continued on p. 10

10 CURRENCY TRADER • August 2005

The reactions of the dollar index, dollar/yen rate, the S&P 500 E-Mini futures, and Euro/dollar rate (clockwise from upperleft) were fairly muted in the first days following the Chinese renminbi revaluation.

FIGURE A — MUCH NOTHING ABOUT ADO?

Source: TradeStation

T he markets didn’t seem to know what to make ofChina’s decision to adjust its currency on July 21.The initial reaction pretty much played out accord-

ing to conventional wisdom regarding the event, but themove had no momentum; traders seemed to digest the nar-row scope of the revaluation and place it in context ofbroader market action and world events.

Figure A shows some of the immediate reaction toChina’s announcement, which occurred around 6 a.m. ET.The dollar index chart (DXY, upper left) shows the buckdropped (challenging its July low) before bouncing back toclose near the middle of its range for the day. It then fol-lowed with three days of higher highs and higher lows.

The U.S. dollar/Japanese yen (USD/JPY, upper right)rate fell hard on the news and stayed down for the remain-der of the New York trading session on July 21, but it beganmarching steadily higher the next morning.

The Euro/U.S dollar (EUR/USD, bottom left) initially got arise out of the news, but it sold off steadily before mounting

a rally in the late morning in New York, then selling off againto close near where it started. Interestingly, it sold offthrough July 26 — counter to what many had predicted,given projected dollar weakness after a yuan revaluation.

The September E-Mini S&P futures (ES, lower right) reflect-ed the stock market’s initial enthusiasm over the news, but likethe EUR/USD rate, the contract reversed to the downsidebefore regaining its footing in the regular day session (after8:30 a.m. CT) trading hours. However, late in the trading ses-sion, the contract retreated to close toward the bottom of itsrange. Three days later, it was essentially marching in place.

The July 21 market action was somewhat clouded by thebreaking news of new bomb threats in London, two weeksafter the July 7 terrorist attacks that rocked that city. TheBritish pound (not shown) initially rallied against the dollaron the news of Chinese revaluation, but sold off when thenews of the explosions broke. However, the market stabi-lized and, by 1:30 p.m. in New York trading, it had ralliednearly to its high of the day.�

Initial market reaction to Chinese revaluation muddled

MARKET NEWS continued

CURRENCY TRADER • August 2005 11

On July 25, the People’s Bank of China said overnightthat foreign media reports calling Beijing’s long-awaitedboost to its currency last week an “initial adjustment”were incorrect. The statement from China, the main focusfor investors, appears to cool expectations of further yuanstrength and attendant appreciation in Asian currencies atthe expense of the dollar.

“The much-ballyhooed RMB revaluation has come andgone with little perceptible change in major currencyrates,” says Brian Dolan, director of research at GainCapital. “In fact, the revaluation is increasingly beingviewed as a non-event, since the scale of the adjustmentwas the absolute minimum expected and the PBOC doesnot appear to be willing to allow [it] to actually float with-in the purported 0.3-percent daily band.

“In the three days of trading since the revaluation to8.1100, the USD/RMB rate has not been below 8.1097, andthe daily range has been around 0.02 percent. This sug-gests that the PBOC has simply adjusted the RMB slight-ly higher, but that they will continue to manage it as afixed-rate peg.”

Dolan adds that the PBOC actions so far indicate theJuly 21 adjustment was a one-time revaluation and that nofurther adjustments are contem-plated in the “foreseeable future.”

“They are especially concernedthat any rush to allow the yuan tofloat, even if it’s a ‘crawling’ adjust-ment within the 0.3 percent dailyband, would expose the yuan tospeculative forces beyond thePBOC’s control,” he says. “Furtheradjustments are likely to be welldown the road and smaller than themarket’s expectations. The PBOChas also noted that this revaluationwas deliberately small to allowChinese firms to gradually adjust toa stronger currency.”

Dolan also says this move sug-gests that continued revaluationspeculation in the short-term is like-ly to be “fruitless,” and that themarket has already reverted to thethemes that were driving currenciesprior to the revaluation, such aswidening U.S. interest rate andgrowth differentials that favor thedollar, and political uncertainty inJapan. �

EBS creates new trading plat form

E BS has come out with an automated tradingprogram for the spot forex trading community.EBS Spot Ai provides direct electronic access

between the customer’s trading systems and the globalforex community trading on the EBS Spot system usingautomated programming interface (API) technology. Theprogram includes risk management and algorithm-based trading such as momentum trading, moving aver-age, and arbitrage models.

The service is suitable for electronic trading and fortraders who want to accomplish high frequency tradesautomatically. It is available for both the interbank trad-ing community and other professional traders (includinghedge funds, fund managers, and commodity tradingadvisors).

EBS developed a customer test facility, the EBS Lab,which enables customers to fine-tune programs beforeimplementing them for real money by testing connectiv-ity, timing, and price integrity, and using EBS Spot mar-ket data to analyze trade program performance.

Chinese yuan revaluation continued from p. 9

HIT YOUR MARK!Advertise in

Active Trader and Currency Trader Magazines

Contact Bob DormanAd sales East Coast

(312) 775-5421

Allison EllisAd sales West Coast

(626) 497-9195

Mark SegerAccount Executive

[email protected](312) 377-9435

R ewind to late 2004. Currency forecasterswere having a field day with doom andgloom scenarios for the deteriorating U.S.greenback. Asian central banks were buying

massive amounts of U.S. Treasuries and market watcherswarned that a financial house of cards was in jeopardy. Theevils of the “twin deficits” (trade and budget) would con-tinue to erode the value of the U.S. dollar, they warned.

As soon as revelers rang in the new year, however, a verydifferent picture began to emerge. Since the opening bell of

2005, U.S. dollar bulls have reasserted control of themarket (Figure 1). From a multi-year peak vs. the

Euro at $1.36 in December 2004, dollar bulls pro-pelled the greenback higher during the first

six months of the year, to a low, around$1.18 in early July (Figure 2).

Whether the buck’s surprising strengthpersists for the remainder of the year hingesupon several economic factors in the U.S. andabroad.

Dumping dollar shorts Currency analysts and economists point toa number of factors that sparked the bull-ishness in the U.S. currency since thebeginning of 2005. One aspect of the mar-ket in late 2004 was that it was simplyweighted down by dollar-short posi-tions. Everyone who had wanted to getshort had already done so, and therewere no more dollar bears to fuel a con-tinuation of the downtrend.

“People were all positioned in the samedirection,” says Sean Callow, senior cur-rency strategist at Westpac InstitutionalBank. “[They] had loaded up on Eurosand were expecting it to gain more.There was an overextension.”

The trade imbalance in the U.S., amajor concern for many currency watch-

ers in late 2004, still hasn’t gone away. TheU.S. current account deficit widened in the

first quarter of 2005 to $195 billion from $188.4billion in the fourth quarter of 2004. But for now,

forex traders have shifted their focus to other factors.

GLOBAL MARKETS

U.S. dollar:Does the buck stop here?

Defying prevailing sentiment, the U.S. dollar

staged a robust rally in the first half of 2005.

What have been the major forces behind this

move — and can it last?

12 August 2005 • CURRENCY TRADER

BY CURRENCY TRADER STAFF

CURRENCY TRADER • August 2005 13

“We are a consuming nation,” saysBrian Dolan, director of research atGain Capital. “We produce very littlein relation to what we consume andthat’s not going to change. We willcontinue to consume at an excessivepace for the next six to nine months.There is very little to suggest [thetrade deficit] is going to be a criticalfactor for the forex market.”

“People in the market had beenhearing about how the U.S. tradedeficit is out of control and the onlyway to fix it is for the U.S. dollar to godown,” adds Jim Glassman, senioreconomist at J.P. Morgan Chase. “But[they] started to realize the reason thetrade deficit was so large was becausethe rest of the world was under per-forming.”

Glassman downplayed concernsthat China or other Asian centralbanks will stop buying U.S.Treasuries.

“They are buying to keep their cur-rencies stable, so that Liz Claiborneand Wal-Mart will continue to viewChina as an attractive place to buildapparel factories,” he says. “If Chinachose to funnel surplus dollars intothe yen or some other currency, therenminbi would rise against the dollarand you are no longer attractive.”

Global growth differentialsIndeed, in the first half of this year pos-itive global growth rate differentialsfavored the U.S., and traders began toshift their focus onto the economicnumbers emerging from the U.S. andthe Euro zone. Currently, slow growthcontinues to plague the Euro zone,while Japan is still struggling toemerge from its battle with deflation.

As global money managers beganscouring various markets for the bestreturn, views on Europe and the Eurozone turned negative throughout thefirst half of the year. The spotlight on Europe ahead of sev-eral key constitutional referendums turned out to be a neg-ative factor for the Euro and encouraged additionalstrength in the U.S. dollar.

The failure by the French to approve the European Union

constitution in a key referendum was followed by anotherresounding “no” vote in the Netherlands in late spring.That news helped launch a new up leg in the dollar throughthe psychologically significant $1.25 area.

continued on p. 14

Euro/U.S. dollar (EUR/USD), weekly

The dollar’s strength is reflected in the EUR/USD rate recently testing lows frommore than a year ago.

FIGURE 2 — EUR/USD

Source: TradeStation

U.S. dollar index (DXY), daily

Despite doom-and-gloom forecasts in late 2004, the U.S. dollar posted a robustrally in the first half of 2005.

FIGURE 1 — DOLLAR COMES ALIVE IN 2005

Source: TradeStation

14 August 2005 • CURRENCY TRADER

“People began to see that the emperor wasn’t wearingany clothes,” Glassman says. “The structural reform isgoing very slowly in Europe and there is resistance to it.”

With the Euro zone expected to post gross domestic prod-uct (GDP) readings around 1.5 percent, vs. 3.5 to 4.0 percentin the U.S. for 2005, traders began to focus on the likely bet-ter returns from the U.S. capital markets.

“At the end of the day, investors are free to put theirmoney anywhere,” Glassman says. “They tend to believethe best returns will come from the regions that are growingthe fastest.”

Looking at the global market from a growth standpoint,"right now, the U.S. is the only game in town," Dolan says.

Second half U.S. economic outlookFor the most part, economists paint a rosy outlook for theU.S. in the second half. First quarter GDP delivered animpressive 3.8-percent reading, while estimates for the sec-ond quarter are a bit lower in the 3.2-percent region.However, looking to the second half, Jonathan Basile, econ-omist at Credit Suisse First Boston, expects growth to rise toaround 3.7 percent.

“We are looking for a bounce-back in economic activityfrom a slower quarter of growth in the second quarter,”Basile says.

He pointed to a mainly auto-related inventory adjust-ment in the U.S. as a factor weighing on growth in the sec-ond quarter. But, overall, Basile forecast a healthy and sus-tainable rate of spending and growth from both businessesand consumers.

“In recent weeks, everybody is more optimistic about thesecond half in the U.S.,” Glassman says. “People thoughtthe economy was slowing down, but now they are seeingthat it had more momentum than [they] originallythought.”

Inflation doesn’t appear to be a problem, despite thehigher crude oil prices, economists say. Basile forecasts coreinflation finishing out the year at around a 2.25-percentannual rate.

Job growth has been steady in the U.S., with non-farmpayrolls averaging around an 180,000 gain for the last sixmonths. In June, non-farm payrolls grew 146,000, while theoverall unemployment rate fell 0.1 percent to 5.0 percent,the lowest level since August of 2001.

“It would take a slowing in business investment to takesome of the wind out of the labor market, and I don’t expectthat to happen,” Basile says.

U.S. Fed deliveredThe Federal Open Market Committee (FOMC) continued itsrate hike campaign throughout 2005. As of its June 30 meet-ing, the FOMC had nudged short-term rates higher at thelast nine consecutive meetings, bringing the overnight FedFunds rate to 3.25 percent, while the discount rate stands at4.25 percent. Statements from U.S. Fed officials have sug-

gested that no pause will likely be seen in the rate hike out-look, with most forecasters targeting a 4.0-percent FedFunds rate by year-end.

The FOMC will meet on Aug. 9 and Sept. 20. While mar-ket players were not surprised by the rate hikes, some ana-lysts suggested the market had underestimated the overallbullish impact on the dollar, from an interest rate differen-tial standpoint. Bullish interest rate differentials shouldcontinue to underpin the U.S. in the second half, most ana-lysts say.

Looking ahead“I expect a retest of the $1.18 area and for the Euro/dollarto push lower,” says Tim Mazanec, senior foreign exchangestrategist at the Investors Bank & Trust. “Although we maybe in the very early stages of structural change in Europe,the uncertainty over elections this autumn and other uncer-tainties, together with low growth, should be bearish for theEuro.”

He points to the $1.1730 area as a medium-term target fortraders to monitor. If that level cracks, it could open thedoor to the $1.12 zone, he says. Dolan also highlights rough-ly the same area.

“If $1.1750 breaks, the dollar has potential to the$1.1350/1.1300 area,” he says.

On the upside, Mazanec sees the $1.2440 area as key. “The Euro needs to stay below that level for traders to

remain confident in the dollar rally,” he says. “Tradingabove it would likely usher in further Euro gains. So, unlesswe trade above $1.2440, sell rallies.”

Glassman held the most bullish view on the dollar. “I would not be shocked if the Euro retreated to $1.10 or

parity [over the intermediate to longer-term],” he says. “Itdidn’t make sense that the Euro was rising when that regionis under performing everyone. I personally believe it belongsat 50 cents. But, it would take a long time to get there.”

Wild cards to watchWhile a positive economic outlook for the second half andbullish interest rate differentials offer optimism for dollarbulls, there are always a number of wild card scenarios thattraders need to be on guard against. Traders should be on thelookout for weaker-than-expected economic data, whichcould stall expectations of continued Fed tightening, analystssay. Or, if a protracted political battle in Washington, D.C.develops over potential Supreme Court nominees, it couldweigh on the U.S. dollar in the short-term, analysts say.

But, aside from unexpected negative events, Glassman isoptimistic.

"If the third quarter shapes up the way people expect withpretty strong numbers, I think there is a little more room foroptimism and a little more room to run on the dollar," hesays. �

Questions or comments? Click here.

GLOBAL MARKETS continued

THE EASIER WAY TO SUBSCRIBE — GO TO:

▼ Trading Strategies and Ideas▼ Technical and Fundamental Analysis▼ Trading Technology▼ Trading as a Business▼ Industry News▼ and much more!

▼ at www.activetradermag.com —the quick and efficient way

▼ In the U.S.: $59.40 for a 1-year subscription (12 issues) or $99.00 for a 2-year subscription (24 issues)That’s a savings of $19.80!

▼ In Canada: $83.40* for a 1-year subscription (12 issues) or $140.00* for a 2-year subscription (24 issues)That’s a savings of $26.80!

▼ Internationally: $95.40* for a 1-year subscription (12 issues) or $160.00* for a 2-year subscription (24 issues)That’s a savings of $30.80!*U.S. dollars

▼ mail a check payable to: Active Trader MagazineP.O. Box 657 Mt. Morris, IL 61054-0567

▼ call 800-341-9384

▼ or use the response card in this issue

www.activetradermag.comBecome a Better Trader

Every Month with:

Go toactivetradermag.com

and click on “Subscribe”

—or call (800) 341-9384

16 August 2005 • CURRENCY TRADER

T here are good reasons to be concerned aboutthe UK second-half economic outlook.Interest rate cuts are realistic, possibly asearly as August. It is also possible the UK

economy will suffer a vicious circle if debt concerns forcegovernment spending cuts and a downward spiral in houseprices.

In the near term, interest-rate expectations remain impor-tant: The narrowing of the UK’s interest rate premium, as theU.S. continues to increase rates while the Bank of England(BOE) cuts rates, will tend to weaken the pound. Also, thepound historically has been vulnerable to sharp moves whenthere is a definitive shift in market sentiment on the curren-cy.

Although the pound will certainly be very vulnerable ifthe yield premium on short-term UK investments disap-pears altogether, the U.S. economy exhibits many of thesame vulnerabilities, particularly over the issues of debt,housing prices, and current account vulnerability. This sim-ilarity should lessen the threat of sharp UK currency losses,although over-shooting will be a risk.

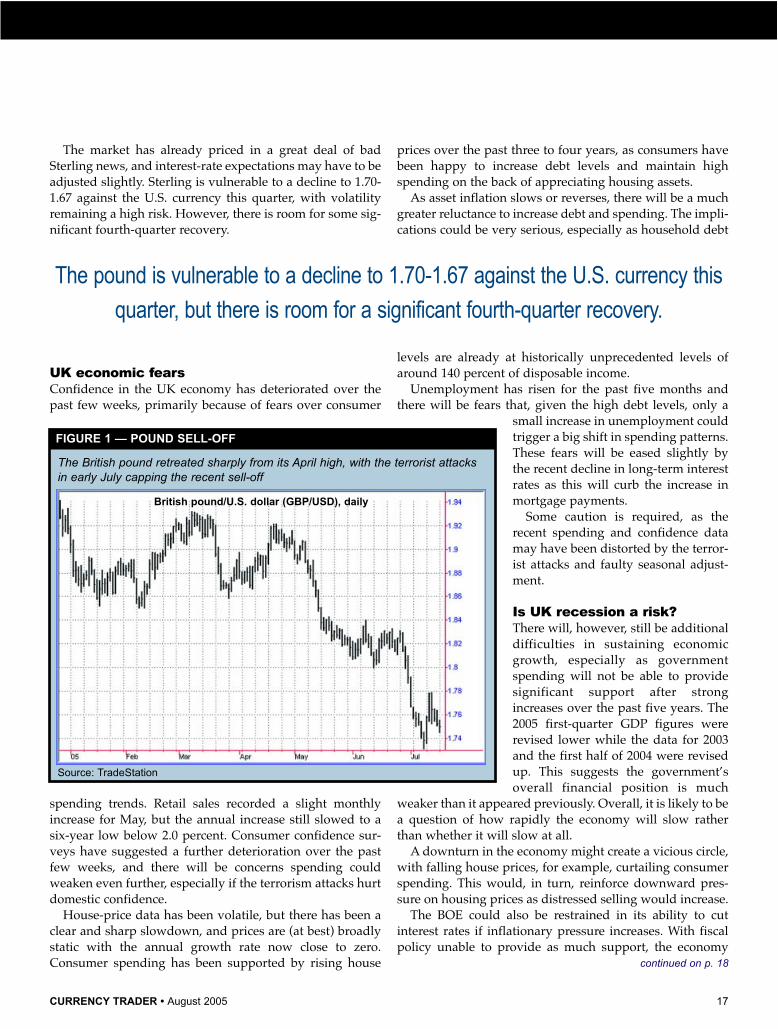

Sharp dropThe pound traded above 1.90 vs. the U.S. dollar in the sec-ond week of May, but has declined sharply since. UK eco-nomic fears were compounded by the London terroristattacks, which on July 7 pushed Sterling down sharply tojust above 1.73 (Figure 1). It quickly rallied back to 1.77 asits risk premium fell slightly and the dollar was subjected toa corrective retreat. As of July 18, the pound had weakenedagain to below 1.75. Figure 2 provides a longer-term pictureof the pound/dollar rate.

GLOBAL MARKETS

Near-term British pound vulnerability

Shared economic vulnerabilities in the U.S. and UK

reduce the odds of a dramatic move in the GBP/USD rate.

BY TIM CLAYTON

CURRENCY TRADER • August 2005 17

The market has already priced in a great deal of badSterling news, and interest-rate expectations may have to beadjusted slightly. Sterling is vulnerable to a decline to 1.70-1.67 against the U.S. currency this quarter, with volatilityremaining a high risk. However, there is room for some sig-nificant fourth-quarter recovery.

UK economic fearsConfidence in the UK economy has deteriorated over thepast few weeks, primarily because of fears over consumer

spending trends. Retail sales recorded a slight monthlyincrease for May, but the annual increase still slowed to asix-year low below 2.0 percent. Consumer confidence sur-veys have suggested a further deterioration over the pastfew weeks, and there will be concerns spending couldweaken even further, especially if the terrorism attacks hurtdomestic confidence.

House-price data has been volatile, but there has been aclear and sharp slowdown, and prices are (at best) broadlystatic with the annual growth rate now close to zero.Consumer spending has been supported by rising house

prices over the past three to four years, as consumers havebeen happy to increase debt levels and maintain highspending on the back of appreciating housing assets.

As asset inflation slows or reverses, there will be a muchgreater reluctance to increase debt and spending. The impli-cations could be very serious, especially as household debt

levels are already at historically unprecedented levels ofaround 140 percent of disposable income.

Unemployment has risen for the past five months andthere will be fears that, given the high debt levels, only a

small increase in unemployment couldtrigger a big shift in spending patterns.These fears will be eased slightly bythe recent decline in long-term interestrates as this will curb the increase inmortgage payments.

Some caution is required, as therecent spending and confidence datamay have been distorted by the terror-ist attacks and faulty seasonal adjust-ment.

Is UK recession a risk?There will, however, still be additionaldifficulties in sustaining economicgrowth, especially as governmentspending will not be able to providesignificant support after strongincreases over the past five years. The2005 first-quarter GDP figures wererevised lower while the data for 2003and the first half of 2004 were revisedup. This suggests the government’soverall financial position is much

weaker than it appeared previously. Overall, it is likely to bea question of how rapidly the economy will slow ratherthan whether it will slow at all.

A downturn in the economy might create a vicious circle,with falling house prices, for example, curtailing consumerspending. This would, in turn, reinforce downward pres-sure on housing prices as distressed selling would increase.

The BOE could also be restrained in its ability to cutinterest rates if inflationary pressure increases. With fiscalpolicy unable to provide as much support, the economy

continued on p. 18

British pound/U.S. dollar (GBP/USD), daily

The British pound retreated sharply from its April high, with the terrorist attacksin early July capping the recent sell-off

FIGURE 1 — POUND SELL-OFF

Source: TradeStation

The pound is vulnerable to a decline to 1.70-1.67 against the U.S. currency this

quarter, but there is room for a significant fourth-quarter recovery.

18 August 2005 • CURRENCY TRADER

could easily slide into recession. The more likely outcome is the housing bubble will

deflate slowly over a period of years. This could prevent afull-scale recession, but would increase the risk of below-trend growth over a sustained period.

The pound will lose interestrate edgeInterest rate trends will inevitably beimportant for Sterling, especially withfurther market speculation overaggressive Bank of England rate cuts.At the June Monetary policy meeting,two members of the nine-person com-mittee called for a rate cut and,although rates were left on hold inJuly, markets are expecting at least tworate cuts over the remainder of 2005.

The BOE is likely to be cautious,especially as there will be fears overinflationary pressure resulting fromhigh energy prices and the weakercurrency. Input prices at the producerlevel rose at the fastest annual rate inmore than 20 years in June with fur-ther strong rises probable for July. Theconsumer inflation rate also increasedfrom 1.9 percent to the 2.0 percent tar-get level in June.

U.S. interest rates are likely to risefurther over the next two months and it is certainly possibleUK rates could fall to meet U.S. rates at around 4.0 percentby early 2006. (The U.S. Federal Reserve pushed U.S. ratesto 3.25 percent at the end of June and is likely to increaserates to 3.5 percent in August.) Although it is more likelythe pound will retain a small premium vs. the U.S. dollar,there will definitely be reduced interest rate support.

UK interest rates were more than 3.5 percent higher thanU.S. rates 12 months ago, and a substantial narrowing of theyield gap would pose a very tough test for the pound con-fidence. As mentioned, Sterling is traditionally vulnerableto big moves when there is a decisive shift in confidence.

The U.S. economic data has remained firm, but there willbe considerable risks associated with high oil prices. TheU.S. economy could slow later in the third quarter and theFed is likely to consider a pause in the tightening processafter its September or November meetings. If there is apause and U.S. rates appear to have peaked, the pound willbe much less vulnerable to selling pressure.

Oil surplus eases trade fearsIn regard to purchasing power, the pound is still slightly over-valued on a trade-weighted basis, although the situation is

not extreme against the dollar; Sterling is certainly more com-fortable now than it was at levels above 1.90. The trade deficitnarrowed slightly to 4.96 billion pounds in May from anupwardly-revised 5.13 billion the previous month. The under-

lying trade concerns will become more significant if underly-ing Sterling confidence deteriorates.

The pound is no longer a petrocurrency, but the UK is stillrunning a net surplus on the oil account, which will supportSterling to some extent if oil prices stay high. This will beparticularly important given rising oil prices, which willput renewed upward pressure on the U.S. trade deficit.

U.S. weaknesses could cushion fallThe underlying UK current account deficit in the region of3 percent of GDP is a source of medium-term concern. TheU.S. economy is, however, also vulnerable because of highdebt levels and a wide current account deficit (the 2005shortfall is likely to be at least 6 percent of GDP).

In this environment, the pound should be cushionedfrom a sharp decline against the U.S. currency, particularlywith central banks unwilling to increase dollar reserve lev-els further. Overall, the similarity of fundamentals betweenthe U.S. and UK should help limit substantial pound/dollarmoves, although they cannot be ruled out.�

For information on the author see p. 6.Questions or comments? Click here.

GLOBAL MARKETS continued

British pound/U.S. dollar (GBP/USD), weekly

In July, the pound dropped below its 2004 lows to its lowest level vs. the U.S.dollar since December 2003.

FIGURE 2 — LONGER-TERM PICTURE

Source: TradeStation

Options Trader is a monthly, full-feature electronic magazine covering trading strategies, systems, market analysis, news and commentary for options traders.

Sign up now for a free subscription. Register at www.optionstradermag.com. All you need to register is an email address.

Each month you can download the current issue from the Internet using technology that combines the high-quality look and feel of a print magazine with the interactive features of Web content.

Subscribe now!www.optionstradermag.com

Sign up now for a FREEsubscription!

20 August 2005 • CURRENCY TRADER

Having made a 13-yearhigh vs. the U.S. dollarat the end of 2004(Figure 1), the British

pound has quickly retreated to levelsnot seen since December 2003. As ofJuly 21, the GBP/USD rate haddropped to 1.7269, which constituteda 10-percent decline over the past 14weeks — a drop the currency pair hadnot matched since 1993.

The decline was, unfortunatelypunctuated by two terrorist attacks inLondon that mark the July lows inFigure 2. In both instances the poundfought back quickly and gamely(especially after the July 21 episodeturned out to be more of a botchedcopy cat attack), so the question onmany forex traders’ minds waswhether Britain’s travails had pushedthe pound to a negative sentimentextreme, in which case the currencywas due for a rebound.

Although in the very near-term thatseems possible (the GBP/USD rate ral-lied strongly on Aug. 1), the larger fac-tors don’t indicate much poundstrength in the GBP/USD rate over thenext few months. “Near-term Britishpound vulnerability” reviews many ofthe fundamental economic issuesweighing on the pound. In addition,the following price analysis shows thepound has performed poorly when ithas been in similar circumstances inthe past.

There have been 38 previousinstances since October 1985 of theGBP/USD rate dropping 10 percent or

SPOT CHECK

After see-sawing the first few months of the year, the GBP/USD rate sold off in earnest in May and June. The pound has declined 10 percent vs. the dollar from December 2004 to July 2005.

Source: TradeStation

Britishpound

The pound has tumbled vs.

the dollar as of late, but does

that mean it’s setting up for

a rebound?

BY CURRENCY TRADER STAFF

FIGURE 1 — TEN-PERCENT SLIDE

The pound initially rebounded strongly after the London terrorist attack on July 7, but it soon turned down again and reached a new low just before the botched bombings on July 21.

Source: TradeStation

FIGURE 2 — JULY LOWS

British pound/U.S. dollar (GBP/USD), daily

British pound/U.S. dollar (GBP/USD), 120-minute

CURRENCY TRADER • August 2005 21

more over a 14-week period (as mentioned, thelast one was in 1993). Table 1 shows the week-to-week performance for the 12 weeks followingthese sell-offs. Not only are both the average andmedian declines negative at every weekly inter-val (which suggests the statistics are stable), thepercent of weeks closing lower (“%<0”) wasonly once less than 60 percent (week 5), andtopped 70 percent in weeks 10 and 11.

However, this negative pattern began toweaken noticeably in week 17 (not shown), andweeks 18 through 20 all had better odds of clos-ing higher than lower, and the average andmedian moves were all positive.

Figure 3 charts the average largest up moves(LUM) and average largest down moves (LDM)for the 12 weeks shown in Table 1. Although bytechnical analysis standards the market was stilloversold on July 26 (the GBP/USD was hoveringaround 1.7400), this longer-term analysis sug-gests British pound bulls should be cautiousover the next several weeks.

It remains to be seen what long-term effectsthe July 21 Chinese currency revaluation willhave (see “China abandons yuan peg” and “Detecting theprofessionals’ footprints: Lessons of the Chinese revalua-tion”), but in the first few days after the event the major cur-

rency pairs seemed to have reverted to their prior trends.Unless the buck suddenly collapses, the currentpound/dollar dynamic seems intact.�

For each of the 12 weeks after 10-percent declines, the GBP/USD ratemade bigger moves to the downside than the upside.

Median largest up move

Median largest down move

4.00%

3.00%

2.00%

1.00%

0.00%

-1.00%

-2.00%

-.300%

-4.00%

-5.00%

-6.00%

-7.00%

Ave

rage

gai

n/lo

ss

1 2 3 4 5 6 7 8 9 10 11 12

Week following 14-week, 10-percent decline (38 prior instances)

Pound/dollar: Median up moves vs. down moves

FIGURE 3 — MEDIAN UP MOVES VS. DOWN MOVES

After declining 10-percent or more over a 14-week period (as was the case on July 22, 2005), the British pound/U.S. dollarrate tended to keep declining over the next 12 weeks. By week 10, the currency pair was lower 71.05 percent of the time,and on average had moved 4.96 percent lower.

TABLE 1 — GBP/USD AFTER 14-WEEK, 10-PERCENT SELL-OFFS

Week 1 LUM LDM W2 LUM LDM W3 LUM LDMAverage -0.21% 1.03% -1.17% -0.68% 1.49% -1.97% -0.92% 1.85% -2.69%Median -0.57% 0.67% -1.13% -0.99% 0.92% -1.74% -1.44% 1.11% -2.38%Standard deviation 1.89% 1.24% 0.91% 2.63% 1.56% 1.58% 3.35% 1.95% 2.18%%<0 60.53% 60.53% 63.16%

W4 LUM LDM W5 LUM LDM W6 LUM LDMAverage -1.23% 2.11% -3.18% -1.41% 2.42% -3.59% -1.50% 2.67% -3.94%Median -1.23% 1.68% -2.63% -1.32% 1.86% -3.05% -1.44% 2.24% -3.49%Standard deviation 3.91% 2.03% 2.66% 4.11% 2.25% 2.89% 4.45% 2.34% 2.98%%<0 60.53% 57.89% 63.16%

W7 LUM LDM W8 LUM LDM W9 LUM LDMAverage -1.63% 2.84% -4.22% -1.68% 2.99% -4.49% -1.61% 3.17% -4.70%Median -1.52% 2.47% -3.84% -1.92% 2.80% -4.51% -1.45% 2.80% -4.52%Standard deviation 4.48% 2.46% 3.04% 4.53% 2.46% 3.14% 4.35% 2.44% 3.19%%<0 60.53% 60.53% 57.89%

W10 LUM LDM W11 LUM LDM W12 LUM LDMAverage -1.67% 3.68% -4.96% -1.60% 3.35% -5.06% -1.41% 3.51% -5.22%Median -1.57% 3.33% -4.92% -1.70% 3.03% -5.26% -1.46% 3.06% -5.60%Standard deviation 4.39% 2.24% 3.05% 4.62% 2.56% 3.12% 4.86% 2.65% 3.14%%<0 71.05% 71.05% 65.79%

Legend: LDM (largest down move) — largest move from the closing price of the pattern to the intraday lowest low.

LUM (largest up move) — largest move from the closing price of the pattern to the intraday highest high.

22 August 2005 • CURRENCY TRADER

How can you know what the professionals aredoing in the spot market? At first glance, theanswer is, “You can’t.” Transactions executedby banks for their clients (or their own

accounts) are confidential, and we don’t even learn the size oftrades; volume is not reported in spot forex as it is in equities.

Professional traders at banks and brokers like Citibank,Deutsche Bank, UBS, and other huge institutions have theinside track on where the “real money” is going. They canthen follow it or, in some instances (if they see it coming),front-run it.

What is real money? Real money clients are major multi-

THE BIG PICTURE

Detecting the professionals’ footprints:

Lessons of the Chinese revaluationOn paper, the Chinese renminbi revaluation is a historic event. But the market’s initial reaction

was fairly muted (if intriguing). Find out how things could play out in the forex

market in the new world of Chinese forex participation.

BY BARBARA ROCKEFELLER

CURRENCY TRADER • August 2005 23

national corporations, global investment houses, centralbanks, and other official institutions. These clients are con-sidered “real money” because they have true underlyingbusiness reasons to buy or sell currencies.

For example, let’s say you are the manager of a globalmutual fund that requires you to have 30 percent of yourfunds invested in Japanese stocks. New investor moneycomes in, and now you have to buy shares in every stocklisted in the Nikkei 225 Stock Index.

To do that, you must buy Japanese yen. Now let’s say theNikkei is reconfigured to add a few new stocks and drop afew old ones. You need to sell the stocks being kicked off thelist and buy the ones being added to it, and the ones beingadded are usually more expensive, contributing to a biggerdemand for yen. If you are the yen trader at a major bankand you are keeping track of the reconfiguration of theNikkei Stock Index, you know that your fund managerswill be buying yen and you can stock up ahead of time.

Then there is the “hot money.” Hot-money traders don’thave an underlying business reason to be doing the trades;

their trades are purely speculative. It’s called hot moneybecause it’s fickle and often short-term in nature. This istraded by speculators such has hedge funds, commoditytrading advisors, high-net worth individuals — or the guysitting just a few desks away who is trading for the bank’sown portfolio, as are his cohorts at the other major banksand brokers. Traders who trade the bank’s own money arecalled “prop” traders, for “proprietary.” Not all proptraders are in-and-out artists, but some are.

Nobody knows the ratio of real money to hot money.Most traders say hot money is a bigger proportion of totaltrading than real money, but real money is the better bet tofollow — if your client is making the trade, others in thesame business are probably making the same trade, andthus you are going to get a price trend (or at least a longer-lasting price move). In fact, the real money will providemarket “support” in some cases. In the extreme case of cen-tral bank intervention, the real money is very real and thesupport level is well-advertised.

That’s the first clue to finding the professionals’ foot-prints — support and resistance, which can be a specific

price right down the fourth decimal place, or a general area10 to 20 points on either side.

Real-money traders often have a timing choice, and theywill be consistent buyers at what they consider a low, orconsistent sellers at what they consider a high. Speculatorsalso estimate support and resistance levels, which arealways mentioned in the endless stream of market com-mentaries available in print and on the Internet. MarketNews, Reuters, Bloomberg, and the sites of banks, brokers,and advisors chew over support and resistance levels everyfew hours, since support and resistance are (usually) mov-ing targets.

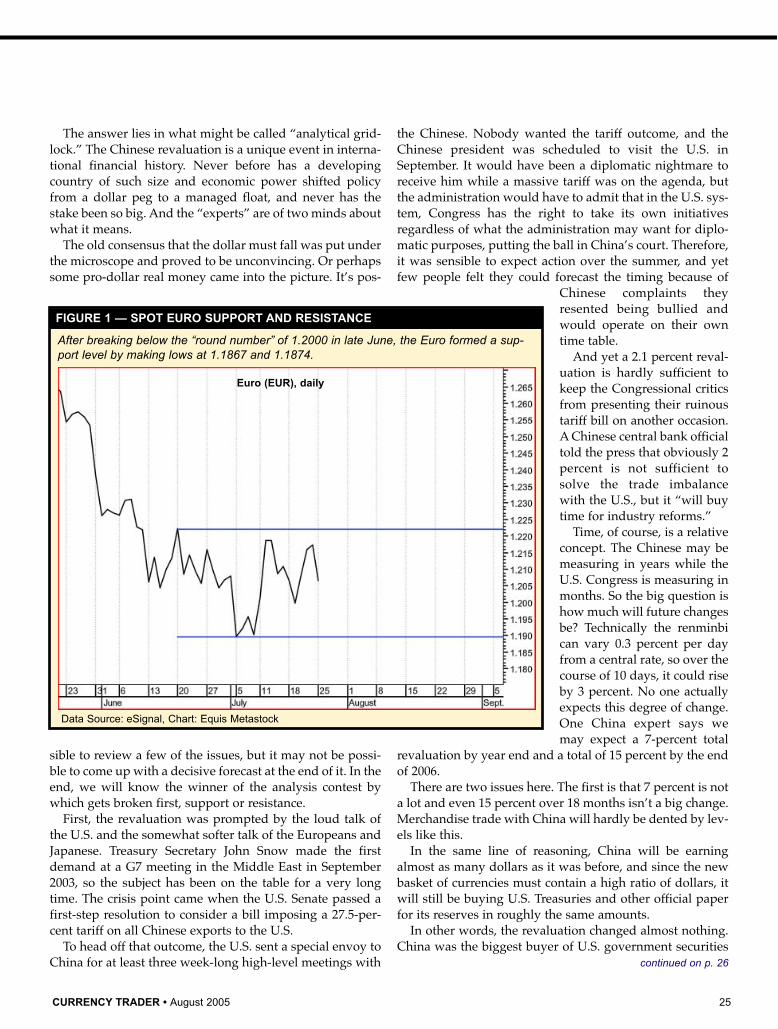

Support, resistance, and footprints Sometimes, however, support and resistance are fixed —almost always a “historic” high or low that was notewor-thy for having been the highest or lowest in a long time. Forexample, on June 24 the Euro/U.S. dollar rate (EUR/USD)passed down through the round number 1.2000 to a low of1.1983, the lowest low since the week of Sept. 3, 2004 (10

months). The market had been watching the round number for a

while, wondering if it constituted some form of magic sup-port, as round numbers sometimes do. The breakout below1.2000 (see Figure 1) implied further Euro losses. Sureenough, on July 5 the Euro hit a fresh low of 1.1867, but onJuly 8 it managed to make a low of only 1.1874 — a mereseven-point difference, but it was not a lower low, whichdidn’t escape anyone’s notice. Moreover, the bar configura-tion of those few days was not favorable to a further Eurodrop: On the date of the lowest low, the close was higherthan the open and the previous day’s close, which provedto be the configuration for most of the next five days.

This was a signal to professionals that a bottom wasforming around the support area of 1.1867-1.1874, and ifyou can’t sell it for a gain, you should buy. You might saythe stage was set for the Euro to rise and the dollar to fall,but at the same time resistance was well-established at theprevious highs around 1.2225.

The next move in this little saga was the mysterious risecontinued on p. 24

When a big move is certain to come on an announcement,

even governments can find it too tempting to resist making a few fast bucks.

24 August 2005 • CURRENCY TRADER

in the Euro on July 20. Between 1 and 3 p.m. ET — whenEuropean traders have already gone home and the U.S.market is almost finished for the day — the Euro flewupward from 1.2042 to 1.2156 by 3 p.m., an enormous moveat any time, and downright astonishing for the time of day.

Everyone was caught by surprise and scratching theirheads in wonderment — yes, there was commentary fromFederal Reserve Chairman Alan Greenspan’s semi-annualtestimony to Congress, but he didn’t actually say anythingnew and certainly nothing dollar-negative. What reallyhappened? One story had it that orders to sell dollars and

buy Swiss francs and Euros were coming out ofSwitzerland, and perhaps from an official institution. Westill didn’t know why the orders had been placed, but thesize of the move as well as the timing pointed to a real-money source rather than a mere speculator.

The next morning the real news broke — China wasrevaluing the renminbi against the dollar by 2.1 percent andinstituting a managed float based on a new and undisclosedbasket of currencies. When the Chinese revaluation reportcame out, the Euro rose against the dollar immediately,from 1.2139 to 1.2255. The dollar/yen rate tumbled from112.31 to 110.34 within the first hour. For a short while, atleast, it looked like resistance was broken and the Euro wasoff to the races.

In the nearly two years the Chinese revaluation was onthe radar screen, two forex forecasts had become the con-sensus. First, the yen would strengthen in line (or more)with the renminbi, since China is now Japan’s leading tradepartner. Second, it was curtains for the dollar, meaning theEuro would rise. The dollar should fall because the relief inthe U.S. trade deficit would be small unless China revaluedby 30 to 40 percent, which was politically impossible, andbecause a shift to pricing the renminbi against a basket ofcurrencies instead of just the dollar would reduce the needfor the People’s Bank of China to buy U.S. Treasuries. Adrop in demand for Treasuries would cause the price to falland the yield to rise, which sounds good until you realizehigher yields could burst the housing bubble (or “froth,” asGreenspan describes it). With the U.S. consumer reducing(or at least not increasing) spending, the U.S. economywould stumble, growth would fall, and the Fed would bethinking about cutting rates some three to six months afterthe event.

Sure enough, the day after the Chinese revaluation, the

yield on the 10-year T-note soared to 4.276 percent on theassumption foreign demand for Treasuries would fall. Noone knows if this is the correct interpretation of events.There’s no evidence of lower demand, and even if officialdemand falls, private demand may be a perfectly adequatesubstitute. Remember, much of the foreign capital inflowinto U.S. government paper comes from the UK andCaribbean havens, where the banks are “fronting” for thereal customers. They may be Middle East oil sheiks — ornewly rich Chinese businessmen.

Were the dramatic moves in the Swiss franc and Euroahead of the announcement evidence the Chinese revalua-tion was leaked ahead of time? And if it was leaked, whydid the Euro rise, and not the yen? After all, the yen madean even bigger move after the release.

We will never know if the puzzling Euro rise was theresult of a pre-announcement leak, and if so, who wasbehind it. Perhaps the Chinese themselves bought someEuros, or Chinese officials with private accounts. Becausethe Chinese were emulating the Monetary Authority ofSingapore’s methodology, maybe it was the MAS. SinceHong Kong and the U.S. were alerted ahead of time, theymight have been the source of the buying, too.

For all we know, other central banks (and therefore theirgovernment officials) were told as well, not to mention theIMF and the Bank for International Settlements, which werecertainly part of the pre-revaluation decision process. Whena big move is certain to come on an announcement, it’s tootempting to resist making a few fast bucks, even if you’re agovernment. One possible reason why the yen didn’t moveis because Japanese Ministry of Finance has been threaten-ing for some time that it would intervene if it saw the yenmove inappropriately.

An event like this comes along very rarely, but when itdoes, you want to be able to jump on the bandwagon,because there’s usually “real money” behind it. The ear-marks of such a move is that it is large, unexplained and inthe opposite direction of the existing trend. In the case of thetrading ahead of the Chinese revaluation, the time of daycontributed to the mystery.

How will it play out?From experience, a big real-money move like this will con-tinue in the same direction, breaking the previous trend andinvalidating the old support levels. But this time the Eurohigh over previous resistance was only an anomaly, and itdoesn’t show up on Figure 1 because the chart was taken asa 5 a.m. ET snapshot of the currency market, excluding dailyhighs and lows. If it was a real-money move, it fizzled; bythe next day, the price was back in the old range. The cur-rencies failed to hang on to gains and the Swiss franc, Euro,and yen all fell back in the first few days after the announce-ment. This is quite confusing. Where’s the follow-through?

THE BIG PICTURE continued

China’s goal is not to revalue; it’s to

build a sustainable forex regime.

CURRENCY TRADER • August 2005 25

The answer lies in what might be called “analytical grid-lock.” The Chinese revaluation is a unique event in interna-tional financial history. Never before has a developingcountry of such size and economic power shifted policyfrom a dollar peg to a managed float, and never has thestake been so big. And the “experts” are of two minds aboutwhat it means.

The old consensus that the dollar must fall was put underthe microscope and proved to be unconvincing. Or perhapssome pro-dollar real money came into the picture. It’s pos-

sible to review a few of the issues, but it may not be possi-ble to come up with a decisive forecast at the end of it. In theend, we will know the winner of the analysis contest bywhich gets broken first, support or resistance.

First, the revaluation was prompted by the loud talk ofthe U.S. and the somewhat softer talk of the Europeans andJapanese. Treasury Secretary John Snow made the firstdemand at a G7 meeting in the Middle East in September2003, so the subject has been on the table for a very longtime. The crisis point came when the U.S. Senate passed afirst-step resolution to consider a bill imposing a 27.5-per-cent tariff on all Chinese exports to the U.S.

To head off that outcome, the U.S. sent a special envoy toChina for at least three week-long high-level meetings with

the Chinese. Nobody wanted the tariff outcome, and theChinese president was scheduled to visit the U.S. inSeptember. It would have been a diplomatic nightmare toreceive him while a massive tariff was on the agenda, butthe administration would have to admit that in the U.S. sys-tem, Congress has the right to take its own initiativesregardless of what the administration may want for diplo-matic purposes, putting the ball in China’s court. Therefore,it was sensible to expect action over the summer, and yetfew people felt they could forecast the timing because of

Chinese complaints theyresented being bullied andwould operate on their owntime table.

And yet a 2.1 percent reval-uation is hardly sufficient tokeep the Congressional criticsfrom presenting their ruinoustariff bill on another occasion.A Chinese central bank officialtold the press that obviously 2percent is not sufficient tosolve the trade imbalancewith the U.S., but it “will buytime for industry reforms.”

Time, of course, is a relativeconcept. The Chinese may bemeasuring in years while theU.S. Congress is measuring inmonths. So the big question ishow much will future changesbe? Technically the renminbican vary 0.3 percent per dayfrom a central rate, so over thecourse of 10 days, it could riseby 3 percent. No one actuallyexpects this degree of change.One China expert says wemay expect a 7-percent total

revaluation by year end and a total of 15 percent by the endof 2006.

There are two issues here. The first is that 7 percent is nota lot and even 15 percent over 18 months isn’t a big change.Merchandise trade with China will hardly be dented by lev-els like this.

In the same line of reasoning, China will be earningalmost as many dollars as it was before, and since the newbasket of currencies must contain a high ratio of dollars, itwill still be buying U.S. Treasuries and other official paperfor its reserves in roughly the same amounts.

In other words, the revaluation changed almost nothing.China was the biggest buyer of U.S. government securities

continued on p. 26

Euro (EUR), daily

After breaking below the “round number” of 1.2000 in late June, the Euro formed a sup-port level by making lows at 1.1867 and 1.1874.

FIGURE 1 — SPOT EURO SUPPORT AND RESISTANCE

Data Source: eSignal, Chart: Equis Metastock

26 August 2005 • CURRENCY TRADER

in the 12 months ending May 2005, when its accumulatedTreasuries totaled $243.5 billion, the second biggest officialholder after Japan. Asian central banks and privateinvestors owned more than half of the $2.03 trillion ofTreasuries held by foreigners, out of the roughly $4.03 tril-lion in marketable U.S. securities outstanding. Whether therevaluation is 2.1 percent or 15 percent, China is still a majorplayer in the capital flow picture. They have the same stakein preserving the value of their asset, which we call theGolden Goose argument (see “The Golden Goose Rule,”Currency Trader, February 2005).

The dollar is still going to be a big piece of the reserve piein China. First, we don’t assume the Chinese would haveleft reserve diversification until after the revaluation. Buteven if they did, the undisclosed basket of currencies thatwill be the basis of the new floating renminbi must consistlargely (probably about 50 percent) of dollars or dollar-pegged currencies such as the Hong Kong dollar. The needfor serious diversification on a transaction basis is low. Theonly reason to diversify much or to talk about diversifica-

tion would be political — to “punish” the U.S. for someother action in the military or diplomatic sphere.

It took a lot of wind out of speculative sails to acknowl-edge these points. Not much has changed. The U.S. will stillbe running massive trade deficits with China, and Chinawill still be holding massive amounts of U.S. paper.

One other thing is becoming clear: By depriving specula-tors of a fat, one-time gain, China is only inspiring them —and probably a new group of speculators, to boot. Hot moneycapital inflows can only rise. Because the Chinese are verysmart about how markets work, you have to wonder if this isnot their intention. They complain about the inflationaryeffect of inflows, but for some interim period, inflows must bewhat they want. Developing economies always want capitalinflow, and China has had it in spades over the past threeyears. This is not really different from the powerhouse U.S.economy funded by European capital inflows in the 1800s.

If hot-money inflows into China grow bigger as the rateis seen to be managed at too tame a level, the Chinese cancontinue to sterilize them by buying up the dollars and then

THE BIG PICTURE continued

CURRENCY TRADER • August 2005 27

investing them in Treasuries, as before; the yield on the 10-year bond can remain constrained. The current thinking isthat rates would be about 1 percent higher were it not forforeign (including Chinese) demand for U.S. paper. Thehousing market is safe from precipitous rate increases.

But hot capital flowing into China can spill over toTaiwan, S. Korea, and elsewhere, in a speculative effort toget them to unpeg, too. This means outright dollar sales, sothe net effect is dollar-negative. In fact, according to thisview, the dollar must fall because the 2.1-percent revalua-tion is too skimpy. It needs to be more like 30 to 40 percentto stop the interest-rate/dollar game and establish stablerelationships.

Therefore, the Chinese choice of a token 2.1 percent reval-uation is not a stabilizing influence on the global imbalance,but potentially a destabilizing one — and discord withinthe Chinese government about the extent and timing ofadditional moves is a frightening prospect.

Do the Chinese really have a plan, and what is it? TheChinese announcement contained magnificent statements

to the effect that China seeks “to enable the market to fullyplay its role in resource allocation,” but China’s goal is notto revalue, it’s to build a sustainable forex regime. It is inthis sense that what’s in China’s best interest is not neces-sarily what’s in the interests of the rest of the world.

Because the Chinese central bank reserves to itself theright to adjust the renminbi band whenever and however itchooses, we now have the tiresome task of following thepace and extent of upcoming renminbi price changes andhow they affect trade and capital flows, if any.

Clearly the benchmark Euro/dollar exchange rate can’tstay stuck forever in the range shown in Figure 1, but untilwe have a better view of the Chinese thinking on the sub-ject — and actions speak louder than words — the maincurrencies are hostage to indecisiveness and range-trading.Keep your eyes peeled for the breakout of either the sup-port or resistance line.�

For information on the author see p. 6.Questions or comments? Click here.

28 August 2005 • CURRENCY TRADER

W hen trading currencies, you’re essential-ly dealing with the relationshipsbetween countries and their economies.The interest rate differential between

countries plays a pivotal role in deciding which currenciesto buy and which to sell.

Markets that offer the highest returns on investmentattract the most capital. In the world of international capitalflows, nations that offer the highest interest rates (alongwith solid credit ratings) will generally attract the most cap-ital and create the most demand for their currencies. Whenyou buy a currency, you earn its interest, while you are obli-gated to pay interest when you sell a currency.

The carry trade is designed to capitalize on the relation-ship between two countries’ interest rates and currencies. Ina nutshell, a carry trade involves buying (or lending) a cur-rency with a high interest rate while selling (or borrowing)a currency with a low interest rate — hence netting a posi-tive interest rate differential. For more information on themechanics of the carry trade, see “Getting a lift from thecarry trade,” Currency Trader, October 2004, p. 32.)

Although earning interest rate differentials on the degreeof 2 to 4 percent may not seem very compelling, the highleverage available in the forex market makes the carry tradean extremely attractive strategy in the right circumstances.Using 10 to 1 leverage (1-percent margin), that 2- to 4-per-

cent interest rate differential becomes a potential 20- to 40-percent profit. Of course, leverage comes with risk, whichmeans losses will be exaggerated the same way as profits.

Another benefit of the carry trade is the added potentialfor capital appreciation — i.e., in the form of price gains ifthe currency you are long gains ground against the curren-cy you are short. The key to the carry trade is determiningwhich countries and currencies offer the most favorablerelationship. Recent history has shown how quickly thingscan change in this respect.

Out with the old, in with the newThroughout 2002, 2003, and part of 2004, the Australian dol-lar (AUD), New Zealand dollar (NZD), and British pound(GBP) were the most popular currencies to buy for carrytrades because these countries offered some of the highestinterest rates in the world. (Their central banks were thefirst to raise rates when the global economy slowed downafter the tech bubble burst in 2000.)

The Japanese yen (JPY), Swiss franc (CHF), and U.S. dol-lar (USD), on the other hand, were the most popular cur-rencies to sell in carry trades because these countries hadsome of the lowest interest rates. The U.S. and Switzerlandwere, in fact, two of the last major countries to raise rates,while Japan still maintains a zero interest rate policy.

The most popular carry trades included AUD/JPY,

TRADING STRATEGIES

Dollar-yen:The year’s hottest carry trade

The buck was on the short side of many carry trades last year, but the current interest rate hike cycle

offers the opportunity to go long the dollar and short the yen.

BY KATHY LIEN

CURRENCY TRADER • August 2005 29

GBP/JPY, GBP/CHF, AUD/USD, and NZD/USD. Carrytraders were able to benefit from interest income as well ascapital appreciation as other traders piled into the sametrades. However, all good things eventually come to an end,and for most of 2005 these currency pairs either sold off orremained range-bound — to the frustration of many carrytraders.

Yet hope is not completely lost for those who still want toget involved in carry trades. The U.S. dollar/Japanese yen(USD/JPY) currency pair has emerged as the hottest carrytrade of 2005. The popularity of this pair as the new carrytrade has even triumphed over any concerns about theJapanese yen rallying on the back of Chinese revaluation.USD/JPY did rally on the announcement, but most losseswere quickly recouped as the market shifted its attentionback to interest rates.

It’s all about the interest rates For carry trades, the most important question to ask is,“Where are interest rates headed?” The carry trades that are

likely to profit in the future are not necessarily the ones thatalready have high interest rate differentials, but rather theones that are setting up to have increasingly higher interestrates going forward. The USD/JPY currency pair fits thisdescription perfectly.

Since June 2004 the U.S. Federal Reserve has increasedinterest rates by 250 basis points, from a 45-year low of 1percent to the current rate (as of July 31) of 3.25 percent. Theonly other major countries with tradable currencies thathave increased interest rates this year are Australia andNew Zealand — and they have hiked rates only once thisyear, compared to four times for the U.S.

The U.S.’s campaign of aggressively raising interest rateshas led to a sharp dollar rally since the beginning of theyear. Figure 1 illustrates the strength of the dollar rally:USD/JPY has soared more than 1,000 pips (points) sinceJanuary; against the Euro, the dollar has rallied 1,600 pips.

There are many ways to explain this rally, but the mostimportant catalyst is interest rates. The U.S. dollar went

continued on p. 30

U.S. dollar/Japanese yen (USD/JPY), daily

The dollar has rallied strongly vs. the yen in 2005 (especially since May), as the Federal Reserve has hiked interest rates 2.5points since last June.

FIGURE 1 — DOLLAR/YEN (USD/JPY) RATE

Source: eSignal (www.esignal.com)

30 August 2005 • CURRENCY TRADER

from being one of the highest-yielding currencies in theworld during the Internet boom (with interest rates as highas 6.5 percent in June 2000) to one of the lowest-yieldingcurrencies in the world when interest rates were subse-quently slashed to 1 percent. This caused a huge flow ofmoney out of dollar-denominated investments, a phenome-non that was exacerbated by capital leaving the U.S. fol-lowing the tech collapse in 2000.

Many hedge funds and speculators at the time sold thedollar, hoping for widening interest rate differentialsbetween the greenback and other currencies. These tradersmade out very well: Most carry trades, such as theAUD/USD and NZD/USD, appreciated more than 35 per-cent in less than two years (see Figure 2). Over the past year,the same speculators are covering their short-dollar trades,hence causing the dollar to rally strongly.

In the case of the EUR/USD, the currency pair went fromoffering a positive interest rate differential of 1.25 percent inMarch 2003 to now offering a negative interest rate differ-ential of 1.25 percent. This provides a perfect reason toexplain why those who were long the EUR/USD as a carrytrade have either closed or reversed their positions. With atleast two to three more interest rate hikes expected from theFederal Reserve (while most other central banks are expect-ed to do nothing), the dollar is still being supported bytraders looking to go long the currency pair for carry.

The yen is the perfect currency to short vs. the U.S. dollar

in a carry trade because of Japan’s zerointerest rate policy. In fact, the yenhappens to be the favorite currency fortraders to sell against in a carry tradebecause for the most part, traders arepaying next to nothing for borrowingthe currency. The Bank of Japan (BOJ)continues to stand pat on rates. Withmixed growth and deflation still a real-ity at this point, the BOJ feels nourgency to raise rates and threatenJapan’s still feeble economic recovery.

This is especially relevant in the cur-rent environment of skyrocketing oilprices. Japan imports 99 percent oftheir oil (the U.S. imports about 50 per-cent). Their lack of domestic sources ofenergy and their need to import vastamounts of crude oil, natural gas, andother energy resources make them par-ticularly sensitive to changes in oilprices. If crude continues to rise, it willsap global demand and weaken pur-chases of Japanese exports. If oil pricesremain firm, the yen should continueto selloff, which would be very benefi-cial for USD/JPY carry traders who are

looking for both increasing interest rate differentials andcapital appreciation.

The fine print: Trade risksThe yield in the USD/JPY currency pair has gone from 2.25percent in the beginning of the year to 3.25 percent as of July— with the possibility of going to 4 percent by November.This has made USD/JPY the hottest carry trade of the year.As long as the U.S. remains on track to raise rates whileJapan’s rates remain unchanged, USD/JPY will continue toaccelerate.

However, there are risks USD/JPY carry traders need toknow about. Because the USD/JPY carry trade is contingentupon a continual tightening campaign by the FederalReserve, traders need to watch the trend of U.S. economicdata to ensure it supports the case for higher rates. Forexample, if U.S. economic data begins to turn sour becauseof weaker consumer demand (in the face of higher oilprices), the Fed may be forced to stop raising rates soonerrather than later, potentially capping interest rates at 3.75percent instead of 4 percent.

Another possible risk is to the Japanese yen. China hasannounced on July 21 it was moving to a managed floatagainst a basket of currencies, revaluing the yuan by a sur-prisingly small 2 percent. There is speculation that furtherrevaluation may occur down the road, given the nominalsize of the latest revaluation.

TRADING STRATEGIES continued

Australian dollar/U.S. dollar (AUD/USD), weekly

Australian dollar/Japanese yen (AUD/JPY), weekly

Carry trades that performed well in previous years included long positions in theAustralian dollar/U.S. dollar rate (top) and the Australian dollar/Japanese yenrate (bottom). However, over the past year, these currency pairs have movedmostly sideways.

Source: TradeStation

FIGURE 2 — CARRY TRADES OF 2003-2004

CURRENCY TRADER • August 2005 31

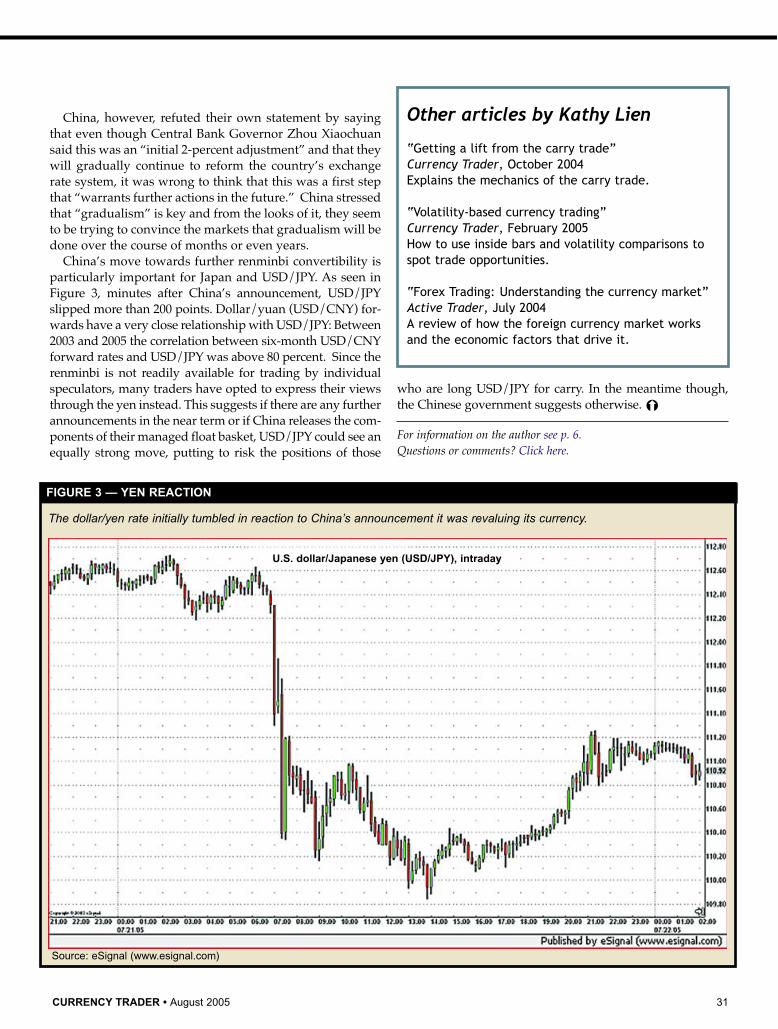

China, however, refuted their own statement by sayingthat even though Central Bank Governor Zhou Xiaochuansaid this was an “initial 2-percent adjustment” and that theywill gradually continue to reform the country’s exchangerate system, it was wrong to think that this was a first stepthat “warrants further actions in the future.” China stressedthat “gradualism” is key and from the looks of it, they seemto be trying to convince the markets that gradualism will bedone over the course of months or even years.

China’s move towards further renminbi convertibility isparticularly important for Japan and USD/JPY. As seen inFigure 3, minutes after China’s announcement, USD/JPYslipped more than 200 points. Dollar/yuan (USD/CNY) for-wards have a very close relationship with USD/JPY: Between2003 and 2005 the correlation between six-month USD/CNYforward rates and USD/JPY was above 80 percent. Since therenminbi is not readily available for trading by individualspeculators, many traders have opted to express their viewsthrough the yen instead. This suggests if there are any furtherannouncements in the near term or if China releases the com-ponents of their managed float basket, USD/JPY could see anequally strong move, putting to risk the positions of those

who are long USD/JPY for carry. In the meantime though,the Chinese government suggests otherwise. �

For information on the author see p. 6.Questions or comments? Click here.

Other articles by Kathy Lien

“Getting a lift from the carry trade”Currency Trader, October 2004Explains the mechanics of the carry trade.

“Volatility-based currency trading”Currency Trader, February 2005How to use inside bars and volatility comparisons tospot trade opportunities.

“Forex Trading: Understanding the currency market”Active Trader, July 2004 A review of how the foreign currency market worksand the economic factors that drive it.

U.S. dollar/Japanese yen (USD/JPY), intraday

The dollar/yen rate initially tumbled in reaction to China’s announcement it was revaluing its currency.

FIGURE 3 — YEN REACTION

Source: eSignal (www.esignal.com)

32 August 2005 • CURRENCY TRADER

T he parabolic stop is a trailing stop techniquedeveloped by Welles Wilder and explained in hisbook New Concepts in Technical Trading (TrendResearch, 1978). It’s the primary component of

what he calls the “Parabolic Time/Price” trading system. The basic principle behind the parabolic stop is a calcula-

tion that automatically raises (in the case of a long trade) orlowers (in the case of a short trade) a stop-loss order thatprotects existing profits in a trade.

For simplicity, the following discussion is given in termsof long trades — the rules are inverted for short trades.

CalculationThe formula for calculating the parabolic stop level fortomorrow’s trading day (when using daily price bars) is:

Ptomorrow = Ptoday + AF * (EPtrade - Ptoday)

where