Csc Vol2ch13

48

VOLUME 2 13-1 T his chapter introduces the basic concepts of financial planning and building the relation- ship between the client and the advisor. This cursory overview is intended to familiarize you with the issues of financial planning as they relate to investing. More in-depth cover- age of the broader issues is found in the Professional Financial Planning Course (PFPC), which is also offered by CSI. The first part of this chapter deals with gathering information and communicating with the client. The second part of this chapter introduces the process of financial planning and the use of a six-step program to begin the process. The third part discusses the advisor’s Code of Ethics and Standards of Conduct. Cases are presented illustrating how these standards are applied. The next part discusses tax planning issues in a basic manner and introduces topics such as capital gains, dividend tax credits, and other tax matters related to investments. The last part builds on this tax information and discusses specific tax strategies and opportunities. Although clients seek out financial advisors who are technically competent in the investment and financial planning area, it is not enough for advisors to “know their stuff.” Advisors must be able to deal effectively with clients through the stages of information gathering, ongoing com- munication and education. As well, dealings with clients must be carried out in a way that is compliant with industry rules and regulations and that adheres to ethical standards. The financial planning approach to managing wealth has benefits for both clients and invest- ment advisors. Financial planning involves analysis of investors’ age, wealth, career, marital sta- tus, taxation status, estate considerations, risk tolerance, investment objectives, legal concerns and other matters. Accordingly, a very comprehensive view of present circumstances can be formed and future goals better defined. In addition, the very discipline and self-analysis required to flesh out a plan causes investors to have a clearer understanding of themselves and their goals, making success in achieving those objectives far more realistic and likely. Implicit in this arrangement is that there is a financial planner at the centre of the plan who coordinates the advice solicited from experts in various fields. An investment advisor will give advice on investments or, if registered as a portfolio manager, on portfolio management, but will not give advice in areas where he or she is not an expert. For example, an advisor will not give advice on the legal aspects of an estate plan; a lawyer is best suited to set up such documents as wills. Accountants may be engaged to give tax advice, and other experts will provide advice as well, but all within their own fields of expertise. The financial planner then creates a plan that takes all of these inputs into account. The financial planner benefits as well, forming professional relationships with experts in these other disciplines, and receiving advice and information from this networking activity. The need for individuals and families to clearly plan how financial goals are to be achieved has become more and more important as job security, general economic conditions and the viability of various social programs have become commonplace worries. While previous generations have relied on a more simplistic planning tool, the budget, today’s complicated economic environ- ment means that we must conscientiously plan for our financial future. Chapter 13 Financial Planning and Taxation © CSI Global Education Inc. (2006)

description

CSC Book

Transcript of Csc Vol2ch13

VOLUME 2

13-1

This chapter introduces the basic concepts of financial planning and building the relation-ship between the client and the advisor. This cursory overview is intended to familiarizeyou with the issues of financial planning as they relate to investing. More in-depth cover-

age of the broader issues is found in the Professional Financial Planning Course (PFPC), which isalso offered by CSI.

The first part of this chapter deals with gathering information and communicating with theclient. The second part of this chapter introduces the process of financial planning and the useof a six-step program to begin the process. The third part discusses the advisor’s Code of Ethicsand Standards of Conduct. Cases are presented illustrating how these standards are applied. Thenext part discusses tax planning issues in a basic manner and introduces topics such as capitalgains, dividend tax credits, and other tax matters related to investments. The last part builds onthis tax information and discusses specific tax strategies and opportunities.

Although clients seek out financial advisors who are technically competent in the investmentand financial planning area, it is not enough for advisors to “know their stuff.” Advisors must beable to deal effectively with clients through the stages of information gathering, ongoing com-munication and education. As well, dealings with clients must be carried out in a way that iscompliant with industry rules and regulations and that adheres to ethical standards.

The financial planning approach to managing wealth has benefits for both clients and invest-ment advisors. Financial planning involves analysis of investors’ age, wealth, career, marital sta-tus, taxation status, estate considerations, risk tolerance, investment objectives, legal concernsand other matters. Accordingly, a very comprehensive view of present circumstances can beformed and future goals better defined. In addition, the very discipline and self-analysis requiredto flesh out a plan causes investors to have a clearer understanding of themselves and their goals,making success in achieving those objectives far more realistic and likely.

Implicit in this arrangement is that there is a financial planner at the centre of the plan whocoordinates the advice solicited from experts in various fields. An investment advisor will giveadvice on investments or, if registered as a portfolio manager, on portfolio management, but willnot give advice in areas where he or she is not an expert. For example, an advisor will not giveadvice on the legal aspects of an estate plan; a lawyer is best suited to set up such documents aswills. Accountants may be engaged to give tax advice, and other experts will provide advice aswell, but all within their own fields of expertise. The financial planner then creates a plan thattakes all of these inputs into account. The financial planner benefits as well, forming professionalrelationships with experts in these other disciplines, and receiving advice and information fromthis networking activity.

The need for individuals and families to clearly plan how financial goals are to be achieved hasbecome more and more important as job security, general economic conditions and the viabilityof various social programs have become commonplace worries. While previous generations haverelied on a more simplistic planning tool, the budget, today’s complicated economic environ-ment means that we must conscientiously plan for our financial future.

Chapter 13

Financial Planning and Taxation

© CSI Global Education Inc. (2006)

Before that plan is prepared, there are four objectives that must be considered. The planto be created:

• Must be achievable;

• Must accommodate small changes in lifestyle and income level;

• Should not be intimidating; and

• Should provide for not only the necessities but also some luxuries or rewards.

Each person or family will have a unique financial plan with which to reach goals.However, there are some basic procedures that can be followed to begin a simple finan-cial plan. These steps are common to all.

A. INFORMATION GATHERING, COMMUNICATION AND EDUCATION

1. Information Gathering

A financial advisor contributes to a client’s well being by understanding the differencebetween the client’s current status and future requirements and goals, and by helping toresolve these differences. To do this effectively, information must be gathered about theclient. To acquire this information, an advisor has to follow intuition and instinct whileapplying some sound techniques for gathering data and assessing the client’s requirements.

Financial advisors are required to know the essential details about each of their clientsincluding:

• The client’s current financial and personal status;

• The client’s investment goals and preferences; and

• The client’s risk tolerance.

Successful financial advisors go beyond just knowing the essential details of a client’s sit-uation. They understand the client’s unique personal needs and goals including:

• The process the client uses to make important decisions;

• The way in which the client prefers to communicate with the advisor;

• The psychological profile of the client; and

• The needs, goals, and aspirations of the client’s family, if applicable.

A financial advisor does far more than just manage the financial lives of clients and pro-vide advice to help them achieve their financial goals. Clients must also be encouragedto assess and re-examine their goals in the context of their evolving business and person-al lives. Clients’ motivations must be understood. Sometimes the advisor has to dig deepto find them, because clients’ motivations are not always readily apparent. The advisormust work with the clients to understand what makes them tick and how they can bestbuild a financial strategy.

There are a number of methods to identify and define clients’ motivations for pursuing aparticular financial objective. Most of them involve actively listening to clients and inter-preting their statements in the context of their unique personality, background, characterand context. As this process continues, the advisor will most likely come face to face witha client’s most intense emotions, for which money, itself, is merely a symbol.

If a person’s money was presented as a spectrum of emotions, it would range from redto blue to yellow and many combinations in between. In money, we find anxiety, securi-ty, pride, satisfaction, fear, anger, loss, guilt, joy, hope, greed, lust, and sorrow. These

Financial Planning and Taxation

13-2© CSI Global Education Inc. (2006)

PRE-TEST

emotions are present in the wealthy individual who inherits money from his father andthey are present in the self-made woman who earned every penny from her own hardwork, independence and tolerance for risk. It is the advisor’s job to help the client artic-ulate those emotions and build a financial strategy to keep them under control.

2. Communicating with the Client

The job of gathering information about the client is really just the start of the clientcommunication process. This process also includes regular contact and education.Clients rely on a financial advisor for a number of reasons, but almost all of them shareone characteristic. They all want someone to understand and attend to the details oftheir financial lives. Clients may feel too busy or disinclined to attend to these detailsthemselves, preferring to let a financial advisor do the job for them.

Calling clients on a regular basis reassures them that their financial advisor has theirinterests in mind. It also enables the advisor to keep current with the client’s financialand personal characteristics that may influence investment decisions.

A financial advisor should call the client with news about their investments, whether itis good news or bad. In fact, by telling them bad news before they hear it from someother source, the client relationship can be strengthened. Clients want to know theyhave an advisor who is watching out for their interests, one who is thinking about themand is prepared to take the time and effort to call them, even when the news is notfavourable.

3. Educating the Client

Clients aim to achieve specific financial goals and they rely on their financial advisor’sadvice to help them be successful. The advisor’s job will be easier if clients understandwhy specific decisions about the plan have been made. The advisor can explain in sim-ple terms the technical nature of the plan’s individual elements. (“A global equity fundinvests in stocks on markets around the world.” etc.)

The greater challenge is to earn clients’ full co-operation and trust in making these deci-sions. In fact, without a client’s co-operation, advisors cannot do their job. To gain thistrust, advisors have to explain how specific investments will help clients achieve their goals.

A key job of the financial advisor is to determine clients’ tolerance for risk. Before thatis done, however, it is essential that clients understand the various types of risk aboveand beyond market risk. Quite often, this involves educating clients about the varioustypes of risk, including:

• The risk of not investing or of investing too conservatively;

• The risk of not diversifying;

• Purchasing power risk;

• Default risk; and

• Currency risk.

CSC CHAPTER 13

VOLUME 2

13-3© CSI Global Education Inc. (2006)

B. THE PROCESS OF FINANCIAL PLANNINGThe financial planning process can be broken down into six distinct steps.

1. Collect all relevant data.

2. Identify goals and objectives.

3. Identify financial problems and constraints.

4. Develop a written financial plan.

5. Implement or coordinate the implementation of the recommendations.

6. Periodically review and revise the plan and make new recommendations.

1. Collect all Relevant Data

The first task to be accomplished is for the investor to gather the information necessaryto complete the plan. This includes tax information (past and current tax returns) bankstatements, pay slips, and other documents such as wills and insurance policies.

a) Personal Data

There is a broad range of personal factors that should be considered before makinginvestment recommendations. These include age, marital status, number of dependants,and health and employment status. An analysis of these factors may reveal special port-folio restrictions or investment objectives and thus help define an acceptable level of riskand appropriate investment goals.

b) Net Worth and Family Budget

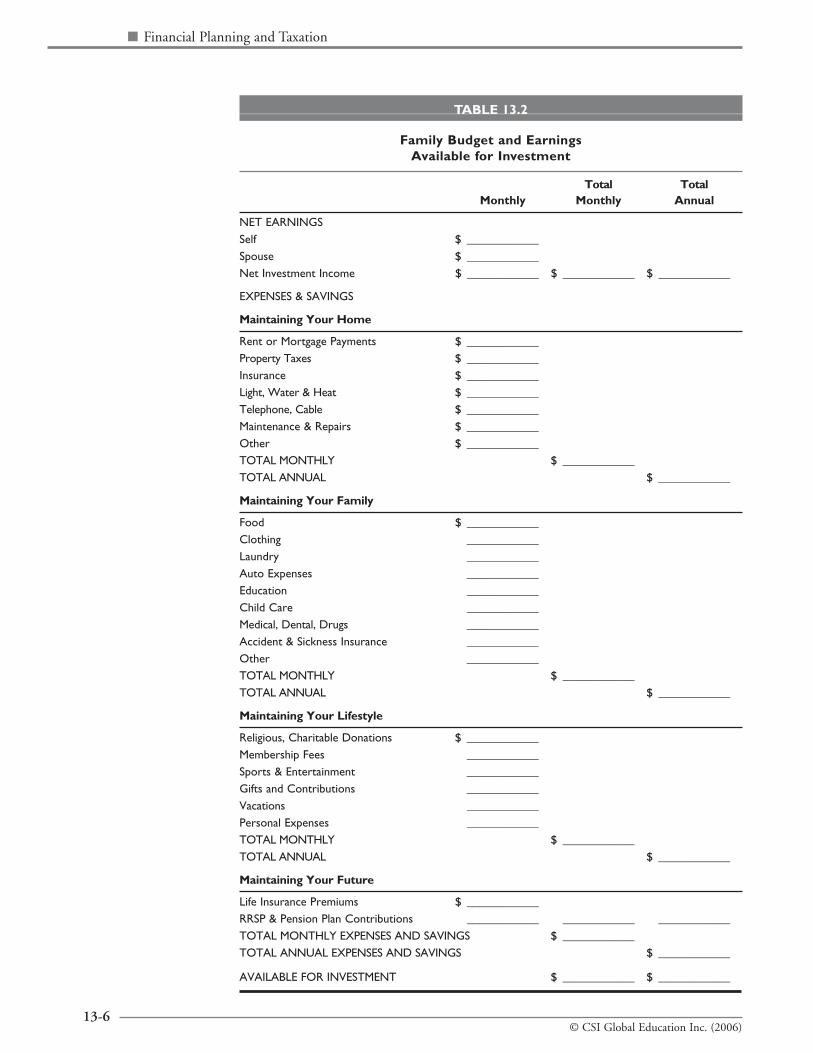

The advisor can obtain a precise financial profile by showing the investor how to pre-pare a Statement of Net Worth and a Family Budget if the investor does not alreadyhave these documents available. Tables 13.1, 13.2 and 13.3 show how this informationmay be presented. It is important to determine the exact composition of the investor’sassets and liabilities, the amount and nature of current income and the potential forfuture investable capital or savings. This information will be invaluable in determiningthe amount of income a portfolio will have to generate and the level of risk that may beassumed to achieve the investor’s financial goals.

c) Record Keeping

Part of any financial plan includes advice or perhaps instructions for the investor onkeeping and maintaining adequate and complete records. It is important for familymembers to be aware of where records are kept so that they can access this informationin an emergency. A document should be prepared which gives the location and detailsof wills, insurance policies, bank accounts, investment accounts as well as any otherfinancial information. There should also be a list of the professional advisors used by theinvestor, such as the name and contact information of any lawyers, accountants, finan-cial planners, IAs or doctors consulted by the investor.

2. Identify Objectives

Setting personal investment objectives is a difficult task. The individual must objectivelyassess personal strengths and weaknesses as well as realistically review career potentialand earnings potential. While to some, this in-depth review can be considered tediousand perhaps unnecessary, it should be noted that it is not possible to set realistic finan-cial goals without one considering how to reach that goal. While many investors dreamof striking it rich in the financial markets, those who actually reach that goal have doneso by design, not by chance.

Financial Planning and Taxation

13-4© CSI Global Education Inc. (2006)

TABLE 13.1

Statement of Net Worth

A S S E T S

Readily Marketable Assets

Cash (bank accounts, Canada Savings Bonds, etc.) $ ______________Guaranteed investment certificates and term deposits ______________Bonds – at market value ______________Stocks – at market value ______________Mutual funds – at redemption value ______________Cash surrender value of life insurance ______________Mortgages at principal value ______________Other ______________

Non-liquid Financial Assets

Pensions – at vested value ______________RRSPs ______________Tax shelters – at cost or estimated value ______________Annuities ______________Other ______________

Other Assets

Home – at market value ______________Recreational properties – at market value ______________Business interests – at market value ______________Antiques, art, jewelry, collectibles, gold and silver ______________Cars, boats, etc. ______________Other real estate interests ______________Other ______________TOTAL ASSETS $

L I A B I L I T I E S

Personal Debt

Mortgage on home $ ______________Mortgage on recreational property ______________Credit card balances ______________Investment loans ______________Consumer loans ______________Other loans ______________Other ______________

Business Debt

Investment loans ______________Loans for other business-related debt ______________

Contingent Liabilities

Loan guarantees for others ______________TOTAL LIABILITIES $

ASSETS ______________NET WORTH Minus LIABILITIES ______________

NET WORTH $ ______________

CSC CHAPTER 13

VOLUME 2

13-5© CSI Global Education Inc. (2006)

TABLE 13.2

Family Budget and EarningsAvailable for Investment

Total TotalMonthly Monthly Annual

NET EARNINGSSelf $ ____________Spouse $ ____________Net Investment Income $ ____________ $ ____________ $ ____________

EXPENSES & SAVINGS

Maintaining Your Home

Rent or Mortgage Payments $ ____________Property Taxes $ ____________Insurance $ ____________Light, Water & Heat $ ____________Telephone, Cable $ ____________Maintenance & Repairs $ ____________Other $ ____________TOTAL MONTHLY $ ____________TOTAL ANNUAL $ ____________

Maintaining Your Family

Food $ ____________Clothing ____________Laundry ____________Auto Expenses ____________Education ____________Child Care ____________Medical, Dental, Drugs ____________Accident & Sickness Insurance ____________Other ____________TOTAL MONTHLY $ ____________TOTAL ANNUAL $ ____________

Maintaining Your Lifestyle

Religious, Charitable Donations $ ____________Membership Fees ____________Sports & Entertainment ____________Gifts and Contributions ____________Vacations ____________Personal Expenses ____________TOTAL MONTHLY $ ____________TOTAL ANNUAL $ ____________

Maintaining Your Future

Life Insurance Premiums $ ____________RRSP & Pension Plan Contributions ____________ ____________ ____________TOTAL MONTHLY EXPENSES AND SAVINGS $ ____________TOTAL ANNUAL EXPENSES AND SAVINGS $ ____________

AVAILABLE FOR INVESTMENT $ ____________ $ ____________

Financial Planning and Taxation

13-6© CSI Global Education Inc. (2006)

TABLE 13.3

Basic Tax Calculation

EARNINGS

Salary, Wages & Commission $ ____________Pension & Annuity Income ____________Interest Income ____________Dividend Income (grossed up by 25%) ____________Capital Gains ____________Other ____________TOTAL INCOME $ ____________

DEDUCTIONS

RPP contribution ____________RRSP contribution ____________Child Care expenses ____________Capital Gains deduction ____________Other deductions ____________TOTAL DEDUCTIONS $ ____________

NET TAXABLE INCOME $ ____________

TAX CREDITS

Personal ____________Age ____________Married ____________Children ____________Disability ____________Allowable Charitable & Medical ____________TOTAL CREDITS $ ____________

INCOME TAX PAYABLE

Federal Tax $ ____________Less Tax Credits ____________Less Dividend Tax Credit ____________ ____________Basic Federal Tax ____________Provincial Tax Payable ____________Net Tax Payable ____________NET INCOME AFTER TAX $ ____________

CSC CHAPTER 13

VOLUME 2

13-7© CSI Global Education Inc. (2006)

a) Evaluating Personal Circumstances

Since investments are selected to suit individual needs, it is essential to develop a clearinvestor profile. Only by studying all factors that potentially affect a financial plan cansuitable recommendations be made or an individual’s investment strategy be designed.

Examples: Billy H. is a commissioned salesperson. His income is very high but it is veryerratic. Billy is very risk tolerant and invests in more speculative vehicles. Ronnie W. is ageologist who works in the mining industry. Income is steady from the unionized plant.Ronnie is a risk-averse individual and invests mostly in GICs.

Despite the proclamations of both investors, the planner must consider the personal cir-cumstances of each individual. A person such as Billy H., whose income source isuncertain, should be placed in relatively conservative investments, with a portion of theportfolio in liquid securities. The planner may decide to create a small portion of theportfolio for speculative investments to address this need but should consider the broad-er picture – that income may be uncertain. If Billy were in real estate sales, investmentsin the real estate sector of the market would not be a good idea. Investing in the realestate sector would increase the risk of the portfolio, as a downturn in real estate wouldhurt both his income and his investments.

The other investor, Ronnie W., is risk-averse by nature, but could be limiting invest-ment choices because of an unrealistic fear. This fear should be addressed to ensure thatit does not limit future decisions. Ronnie W. could invest in blue chip issues because oftheir relatively high quality and moderate risk.

Unless the advisor delves into personal circumstances such as job security, investmentexperience and possibly marital circumstances, important issues can be overlooked.

b) Determine Investment Objectives

An individual’s investment objectives are determined by a thorough analysis of his orher current financial position and future requirements. The New Account ApplicationForm (Exhibit 13.1) requires that investment objectives be clearly stated and that theygovern investment actions. Investment objectives generally can be described as a desirefor income, growth of capital, preservation of capital, tax minimization or liquidity.These investment objectives were described more fully in Chapter 9.

c) Life Cycle Analysis

To add perspective to the process of setting objectives, it can be helpful to think interms of the life cycle. Life Cycle Theory states that the risk-return relationship of aportfolio changes because investors have different needs at different points in their lives.On this basis, it is assumed that younger investors can assume more risk in the pursuitof higher returns and that the risk-return relationship reverses itself as the investor ages.In general, there are four definable stages in a person’s adult life.

• Early Earning Years - to age 35: At this time the investor is starting a career, build-ing net worth and assuming family and home ownership responsibilities. The mostfrequent priorities are to have a savings plan and near-cash investments for emer-gencies. However, when funds are available for investing, growth is usually the pri-mary objective because of the magnitude and duration of expected future earnings.

• Mid Earning Years - to age 55: In this stage an individual’s expenses usually declineand income and savings usually increase. As a result, savings continue to be a veryimportant factor in the growth of an investor’s investment capital. Because suchinvestors have more discretionary income, investment objectives tend to focus ongrowth and tax minimization.

Financial Planning and Taxation

13-8© CSI Global Education Inc. (2006)

• Peak Earning Years - to retirement: As an investor approaches retirement, preserva-tion of capital becomes an increasingly important objective. During this period, theaverage term of maturity of fixed income investments should be shortened and thequantity of higher risk common shares reduced.

• Retirement Years: During this period investors most frequently have fixed incomesand only limited opportunities for employment. Therefore the primary investmentobjectives of retired investors are preservation of capital and income with the rela-tive importance of each being determined by comparing the level of retirementincome to budget requirements. When income is adequate, preservation of capital ismore important. There must be enough growth in the portfolio so that the clientdoes not run out of money.

While convenient, the life cycle approach to financial planning is to be considered amere guideline in developing any plan. It is true that some investors might easily con-form to this life cycle model, but many individuals’ financial or other circumstancessimply do not fit into the convenient four-stage approach outlined here. Special circum-stances require an individualized approach.

Although life cycle analysis can be helpful, it is far more important to consider theinvestor’s personal situation, financial position and responsibilities, tolerance for risk,and investment knowledge. Only by assessing these factors in depth and relating themto the expressed needs of the client can the planner help an individual develop specificinvestment objectives.

One tool to help the investor and planner to both clarify the investor’s current situationand identify planning needs is the financial planning pyramid.

CSC CHAPTER 13

VOLUME 2

13-9© CSI Global Education Inc. (2006)

E X H I B I T 13. 1

New Account Application Form Account Supervision

(to be completed by Advisor) Office Account I.A.

(1) (a) Name Mr.

Mrs

Miss ...............................................................................................................................................................

Home .............................................................................................................................................................................

Address..........................................................................................................................................................................

Date of Birth................................................Client’s Social Insurance Number .............................................................Client’s Citizenship ..............................

Type of Account Requested:(b) Is Advisor registered in the Province or Yes............ Cash........................................................RRSP/RRIF......................................U.S. Funds .......

Country in which the client resides? No............. Margin .....................................................Other ................................................D.A.P .......................................................Pro ...................................................CDN Funds......

(2) Special Instructions: Hold in Account ................................... Register And Deliver ........................................DAP..................................Duplicate Confirmation ...............................And/Or Statement................................

Name: ...................................................................................................................... Name: .......................................................................................................Address: .................................................................................................................. Address: ..................................................................................................................................................................................................................................... ............................................................................................................................................................................Postal Code: .................................................. .........................................................Postal Code: ....................................

(3) Client’s Name......................................................................................... Type of Business .......................................................................................Employer: Address ..................................................................................... Client’s Occupation....................................................................................

(4) Family Information:Spouse’ Name.......................................................................................................... No. of Dependents.....................................................................................Occupation............................................................................................................... Employer....................................................................................................

Type of Business ......................................................................................

(5) How long have you known client?...............................Advertising Lead................Phone In.................................. Have you met the client face to face?....................................................................................Personal Contact ...............Walk In .................................... Yes ............... No ................Referral by: ............................................................................................(name) (if customer, give account no.) ..............................................................................

(6) If yes for Questions 1, 2, or 3, provide details in (11)1. Will any other person or persons: (a) Have trading authorization in this account? No ........... Yes ..........

(b) Guarantee this account? No ........... Yes ..........(c) Have a financial interest in such accounts? No ........... Yes ..........

2. Do any of the signatories have any other accounts or control the trading in such accounts? No ........... Yes ..........3. Does client have accounts with other Brokerage firms? (Type____________) No ........... Yes ..........4. Is this account (a) discretionary or (b) managed (a) ........... (b) ...........

Insider Information5. Is client a senior officer or director of a company whose shares are traded on an exchange or in the OTC markets? No ........... Yes ..........6. Does the client, as an individual or as part of a group, hold or control such a company? (____________________) No ........... Yes ..........

(7) (a) General Documents Attached Obtaining (b) Trading Authorization Documents: Attached Obtaining– Client’s Agreement ................ ................ – For an Individual’s Account ............... ................– Margin Agreement ................ ................ – For a Corporation, Partnership, Trust, etc. ...............– Cash Agreement ................ ................ – Discretionary Authority ............... ................– Guarantee ................ ................ – Managed Account Agreement ............... ................– Other ................ ................

(8) INVESTMENT KNOWLEDGE Sophisticated ..................... EST. NET LIQUID ASSETSGood ..................... (Cash and securities less loansLimited ..................... outstanding against securities) A ...................................................Poor/Nil .....................

ACCOUNT OBJECTIVES ACCOUNT RISK FACTORS EST. NET FIXED ASSETS B ...................................................Income ..............% Low ..............% (Fixed assets less liabilitiesCapital Gains Medium ..............% outstanding against fixed assets)

Short Term ..............% High ..............% EST. TOTAL NET WORTH (A + B = C) C...................................................Medium Term ..............% 100% APPROXIMATE ANNUAL INCOMELong Term ..............% FROM ALL SOURCES D...................................................

100%EST. SPOUSE’S INCOME E ...................................................

(9) Bank Reference: Name....................................................................... Bank credit check-acceptable? Yes................ No ................Branch ..................................................................... Or Credit Bureau check-acceptable? Yes................ No ................Refer to.................................................................... Above credit checks considered unnecessaryAccounts.................................................................. Explain in (11)

(10) Deposit and/or Security Received......................................................................................................................................................................................................Initial .................................. Buy .................................... Solicited ............................. Amount ........................................................................................Order ................................. Sell..................................... Unsolicited ......................... Description ..................................................................................

(11) Advisor’s Signature .................................................................................................. Designated Officer, Director ......................................................................

or Branch Manager’s ApprovalDate ......................................................................................................................... Date of Approval........................................................................................Comments: ...............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................

Client Signature ..................................................................................... Date ..........................................................................

Financial Planning and Taxation

13-10© CSI Global Education Inc. (2006)

Phones: Home............................

Business.......................

Other ............................

Fax ...............................

(Please Print)

(Street)

(City) (Province) (Postal Code)

d) The Financial Planning Pyramid

Although the financial planning pyramid may appear simplistic, it often helps for theplanner to use visual aids in dealing with investors. The financial planning pyramidhelps the planner and the investor alike visualize goals and objectives and review invest-ment strategy. If the investor is interested in IPOs for example, but lacks a will and theproper insurance coverage, it is obvious that, by starting at the top with an IPO, thegroundwork has not been done and the plan will be unstable. The investor must have agood strong base from which to work to successfully reach the goals and objectives set.

EXHIBIT 13.2

The Financial Planning Pyramid

3. Identify Financial Problems and Constraints

The client’s tolerance for risk, investment knowledge and time horizon all impose con-straints on the recommendations to be put forth in the financial plan. Constraints pro-vide some discipline in the fulfilment of a client’s objectives. Constraints, which mayloosely be defined as those items that may hinder or prevent the advisor from satisfyingthe client’s objectives, are often not given the importance they deserve in the policy for-mation process. This may result from the fact that objectives are a more comfortingconcept to dwell on than the discipline of constraints.

4. Develop a Written Financial Plan

After reviewing and assessing the information, a plan of action must be developed forthe investor to follow. This plan of action may require the input of other professionals.If this is the case, the advisor should prepare a list of instructions for these professionalsas well. Clearly defined goals and tasks, as well as a schedule for achievement can be ofenormous benefit to the investor. The financial plan should be simple, easy to imple-ment and easy to maintain.

5. Implement Recommendations

It is important to implement a financial plan in a timely manner. Once the preparatorywork of analyzing, determining and calculating is finished, it is up to the investor todecide to put all the carefully thought-out ideas and strategies in motion.

CSC CHAPTER 13

VOLUME 2

13-11© CSI Global Education Inc. (2006)

At this point the investor should review the plan, the goals, the objectives and the risktolerance levels. The investor should be in agreement with them before any products arepurchased or deals are struck. The investment advisor must ensure that the investorunderstands each product chosen and is aware of the potential risks as well as the poten-tial rewards.

6. Review, Revise and Make Recommendations

The last step in this whole process is the review. A financial plan should never remainstatic. Just as investments rise and fall in market value, a person’s financial situation canchange. As well, economic changes, tax increases and health issues all can threaten eventhe “best-laid plans”. While there is no set time frame for such a review, an annualreview is the minimum required. Mini-reviews may be necessary depending on the cir-cumstances (i.e., changing tax, economic, and employment status). In extreme circum-stances, such as a job loss, it may be necessary to devise a completely new financial plan.

Revisions can include reviewing a will, changing beneficiaries and ensuring that theinvestor is continuing to take advantage of all tax savings techniques. Recommendationscan be simple – no changes are necessary – or could entail a great number of changes. It isimportant that the advisor follow up with the investor to ensure that suggestions arecarried out.

7. Conclusion

This overview of the financial planning process provides the investor with the structureof a basic financial plan but does not deal with specialized issues such as trusts, estatefreezes, the need for insurance, etc. To complete a thorough analysis of needs andrequirements, these areas must be addressed as well; however, it is beyond the scope ofthis text to do so. A more thorough discussion of these topics is provided in theProfessional Financial Planning Course (PFPC) and Wealth Management Techniques(WMT) Course, both offered by CSI.

The next section discusses the importance of working with the client in an ethical andprofessional manner.

C. ETHICS AND THE FINANCIAL ADVISORA critical element in building a solid trusting relationship with a client is behaving in anethical manner.

Ethics can be defined as a set of moral values that guide behaviour. Moral values areenduring beliefs that reflect standards of what is right and what is wrong.

The securities industry has a Code of Ethics that establishes norms based upon the prin-ciples of trust, integrity, justice, fairness, honesty, responsibility and reliability. Peopleregistered to sell securities and mutual funds (registrants) must adhere to this code. Thecode encompasses the following five primary ethical values:

A. Registrants must use proper care and exercise independent professional judgement.

B. Registrants must conduct themselves with trustworthiness and integrity, and act inan honest and fair manner in all dealings with the public, clients, employers andcolleagues.

C. Registrants must, and should encourage others to, conduct business in a profession-al manner that will reflect positively on themselves, their firms and their profession.Registrants should also strive to maintain and improve their professional knowledgeand that of others in the profession.

Financial Planning and Taxation

13-12© CSI Global Education Inc. (2006)

D. Registrants must act in accordance with the Securities Act(s) of the province orprovinces in which registration is held and the requirements of all Self-RegulatoryOrganizations (SROs) of which the firm is a member must be observed.

E. Registrants must hold client information in the strictest confidence.

It is important to understand the difference between ethical behaviour and compliancewith rules. The rules set out standards. Some rules purely codify consensus practices.For example, stock trades settle three days after the trade date (T+3). Other rulesapproximate ethics by incorporating ethical behaviour, such as the law against stealing.However, compliance with rules only results in conformity with externally establishedstandards.

While there are rules to deal with the most significant or common situations, rules can-not encompass every possible situation that may occur in day-to-day business.Following rules does not involve any judgement. People follow rules because they must,not necessarily because they believe it is morally correct. However, ethical behaviourrequires internally established moral judgements. Ethical decision making is a systemthat can be applied to any situation.

The following short case illustrates an example of an action that would be compliantwith rules but would violate ethical standards.

Case # 1 – Handling an Ethical Issue

A financial advisor, Betty Cho, is considering recommending that a client, Henry King, invest in a smallbut promising Internet company, NetTrack Enterprises. Betty’s brother-in-law, Fred Wong, is NetTrack’smain shareholder and CEO.

While there may not be a clear violation of industry rules or regulations, if Ms. Cho recommendsNetTrack to her client, there is certainly an ethical issue that she is facing.

If she was acting in an ethically sound manner, Betty needs to:

1. Recognize that she faces a moral issue if she makes an investment recommendation in a situationin which she has a potential or actual conflict of interest.

2. Assess her options in terms of moral criteria and develop a morally appropriate strategy for man-aging conflict-of-interest situations. For instance, she should disclose to Henry that one of herrelations has a major interest in NetTrack. She must consider whether her professional objectivityregarding NetTrack’s promise might be compromised, or appear to be compromised, by her rela-tionship to Fred.

3. Make a commitment to a morally appropriate strategy such as disclosure.

4. Have the courage to carry out the moral strategy by letting Henry know that Fred Wong is herbrother-in-law.

D. STANDARDS OF CONDUCTThe securities industry has established Standards of Conduct, which expand on theCode of Ethics shown above and set out certain requirements for behaviour. Theserequirements are based in large part on the provincial securities acts and SRO rules. Abrief summary of some of the key standards is discussed next. The complete CanadianSecurities Industry Standards of Conduct are found in Appendix A to this chapter.

1. Know Your Client and Suitability

a) Rationale behind KYC

As discussed earlier, an advisor must make a concerted effort to know the client – tounderstand the financial and personal status and aspirations of the client. Thus, theadvisor will make recommendations for the client to invest funds in securities thatreflect, to the best knowledge of the advisor, these considerations. The advisor, having

CSC CHAPTER 13

VOLUME 2

13-13© CSI Global Education Inc. (2006)

provided sound advice, will therefore be above reproach for potentially unsuitable pur-chases and sales of securities for a client if the client does not heed the advisor’s advice.

b) What Information Should be Collected

The advisor must make a diligent and business-like effort to learn the essential financialand personal circumstances and the investment objectives of each client. Client accountdocumentation should reflect all material information about the client’s current status,and should be updated to reflect any material changes to the client’s status in order toassure suitability of investment recommendations.

In the fall of 2001, the IDA implemented revisions to its know-your-client regulationsgiving full service brokers the opportunity to accept non-recommended trades without asuitability obligation. To meet this regulatory requirement, clients are required to sign adisclosure agreement document that gives their consent that non-recommended tradeswill not be subject to a suitability review.

2. Trustworthiness, Honesty and Fairness

Advisors help clients think through their financial goals. In this role, clients need toknow that the advisor is working to promote their best interests.

When clients trust their advisor, they do not personally have to verify everything thatthe advisor tells them. For example, they do not have to check the tax and estate impli-cations of every investment recommendation or ask for details about its risk or volatility.They certainly do not waste time wondering if the advisor has made a recommendationthat serves the advisor’s interest rather than the client’s own interest.

There are two parts to a trust relationship: trust in an advisor’s competence and integrity.Both are essential. Competence, without integrity, leaves clients at the mercy of a self-serving professional. Integrity, without competence, puts clients in the hands of a well-meaning but inept professional.

In order to ensure that advisors and other registrants display absolute trustworthiness,the standards of conduct sets out a number of requirements for registrants.

One of the most important is the requirement that a client’s interest must be the fore-most consideration in all business dealings. In situations where the advisor may have aninterest that competes with that of the client, the client’s interest must be given priority.Furthermore, advisors must disclose all real and potential conflicts of interest in order toensure fair, objective dealings with clients. This is why Betty Cho, in Case #1, shoulddisclose her relationship with NetTrack’s main shareholder, her brother-in-law.

In order to ensure that advisors are competent, they must meet proficiency requirementsfor their registration category. As well, the Canadian investment industry has a manda-tory continuing education program, which helps ensure that investment industry profes-sionals have the information, and skills they need to serve their clients with the utmostprofessionalism.

Case #2 – Gaining a Client’s Trust

When Ottawa financial advisor Jo-Ann Carter assumed the account of 75-year-old Ena Beyer, sheknew she had a challenge on her hands.

Mrs. Beyer, a widow, held more than $350,000 in a non-registered mutual fund account – and theentire amount was invested in a combination of GICs and a mortgage fund. After the first meetingwith her client, it was evident that her investment knowledge was very limited and that she reliedalmost entirely on her son for financial advice.

Therein lay the problem. Her son, a systems-services professional employed by a high-tech firm, hadbeen generating great returns for his own portfolio by investing in various Canadian and U.S. technolo-gy stocks.

Financial Planning and Taxation

13-14© CSI Global Education Inc. (2006)

When Mrs. Beyer passed over a sheet of paper listing some of her son’s recommendations, Carterimmediately shook her head. The proposed list of holdings included an excessive amount in equities,especially aggressive high-growth situations, and not nearly enough in dividend-paying blue-chip namesand fixed-income securities.

Convinced that the son’s proposed strategy was overly aggressive for someone with Mrs. Beyer’s clientprofile, Carter recommended to her a much more conservative approach. Mrs. Beyer balked at thesuggestions for change, siding with her son over someone she was meeting only for the first time.

The easy way out for Carter would have been to go along with what the son suggested and Mrs.Beyer wanted. Carter could easily have rationalized the choices, since one of Mrs. Beyer’s objectiveswas to pass on an inheritance to her son. By questioning the son’s judgement, Carter risked losing anattractive account, and one that would generate a good chunk of commission income right away.

But in good conscience, Carter could not go along with Mrs. Beyer’s requests without making furtherinquiries to determine what in fact was in Mrs. Beyer’s best interests. Carter asked her to set up ameeting with her son so that the three of them could discuss her situation together.

A few weeks later, the agreed-on meeting started poorly. Mrs. Beyer’s son, Roy, seemed skeptical ofCarter’s abilities and was a little suspicious about her intentions. Undeterred, Carter patientlyexplained her responsibility as an advisor, her concerns about his mother’s account and the reasonsfor her recommendations.

After the first meeting, Roy said he was not yet convinced, but would think about it. His mother con-curred. “It took some time, but after a couple more meetings, her son was impressed with my recom-mendations,” says Carter. “In the end, we had totally revamped the asset mix to ensure prudent alloca-tion of his mother’s investments.”

With Mrs. Beyer more comfortable knowing her son was involved, Carter also felt more assured thatshe would be able to get better results for her client. “We now meet regularly and the trust that hasdeveloped between the three of us is very strong.” More recently, this trust went even farther, andMrs. Beyer’s account became a discretionary managed account, since Roy has found himself increasinglytoo busy to oversee his mother’s investments.

3. Fiduciary Duty and Professionalism

When trust relationships are open-ended and involve “caring for” or “looking after” aclient’s interests, there is a fiduciary relationship between advisors and their clients.Fiduciary or trust relations in ethics and law are needed where there is an imbalance ofknowledge or control between two morally related parties, such as a parent and a child,a physician and a patient, or a lawyer and a client. Fiduciary relationships are agent-principal relationships in which the principal has a certain vulnerability and the agenthas greater expertise or authority.

In order to ensure that investment advisors and other registrants display the utmost inprofessionalism, the standards of conduct sets a number of requirements. These require-ments include that all methods of soliciting and conducting business must be such as tomerit public respect and confidence, and that all personal business affairs be conductedin a professional and responsible manner.

Case # 3 – Being Aware of a Client’s Vulnerability

There are times when Ron Springfield must advise a surviving spouse about what to do with inheritedassets. But the time immediately following the death of a loved one is a time for grieving, not decision-making, says Springfield, who over the years has guided many surviving spouses through this vulnerableperiod.

His widowed clients include Martina, whose retirement life in a peaceful small town in the BC interiorwas shattered by the sudden death, at age 67, of Ivan, her husband of 35 years. Amid the flurry of con-tacting friends and relatives and making funeral arrangements, Martina also worried about what shehad to do about her deceased husband’s RRSP and his other investment accounts. It was all over-whelming, particularly since it was Ivan, and not her, who had been the main overseer of the family’sfinances.

Martina felt some relief when she contacted Springfield by phone at the brokerage office. He assuredher that no immediate action was required on her part. “The perception that most people in your sit-

CSC CHAPTER 13

VOLUME 2

13-15© CSI Global Education Inc. (2006)

uation have, is that things need to be done very quickly,” Springfield told Martina. “The reality is that aslong as you have enough cash on hand to pay the bills, there is really no great rush. When you’re readyto sit down and talk, give me a call.”

Though the timing of Ivan’s passing was unexpected, such eventualities had been provided for in thefinancial plan crafted for the couple. Ivan’s death triggered the payment of a life insurance policy thathad been designed to cover any of his tax liabilities at death. The two largest tax payouts had to dowith the deemed sale of rental property owned by Ivan, and the deemed sale of a portfolio of stocks,most of which had been held for at least 10 years and that had built up considerable capital gains.

Additionally, the life-insurance policy had been over-funded, so as to ensure that Martina, the benefici-ary, would have a cash reserve to cover all of the one-time expenses associated with a death. For her,these included the costs of plane fare to enable her son and his young family to make the trip to theWest Coast from their home in New Brunswick.

While mourners gathered to comfort the grieving widow, Springfield was quietly taking care of busi-ness. Shortly after the death, his assistant produced an estate-evaluation report listing the market valueof Ivan’s investment and RRSP assets as of the date of his death, and the maturity dates of his bondand GIC holdings.

The report laid out clearly the information needed by Martina’s executor, lawyer or accountant inorder to do their jobs. “This is a lot easier to do right after the death than several weeks later,” saysSpringfield.

Meanwhile, Springfield reviewed Martina’s own investment account, which he has been looking after formany years. He saw that a five-year GIC was just about to expire, and that some stocks and mutualfunds had recently paid quarterly dividends into her account.

In the weeks and months to come, the probate process would play out, and Martina would seek advicefrom Springfield on how to invest her existing and inherited assets. But now was hardly the time forreinvestment decisions. Springfield knew from his conversation with Martina that she would need themoney for short-term expenses like visitation, funeral, catering and other related expenses. After con-sulting with Martina, he transferred the available cash from Martina’s investment account to her dailychequing account at her bank.

Less may be more, when it comes to helping clients who are bereaved or otherwise going through aperiod when they are feeling very vulnerable. “A death in the family immediately changes a client’s pro-file,” says Springfield. “People have a lot more need for liquidity. You try to get everything accumulatedand make it easier for them.”

4. Conclusion

In addition to being skilled in the areas of investment and financial management, finan-cial advisors must be able to deal effectively with clients through the stages of informa-tion gathering, ongoing communication and education. As well, as the investmentindustry is built on trust and confidence, advisors must adhere to strict rules and regula-tions with respect to dealing with clients, and abide by the industry Code of Ethics thatestablishes trust, integrity, justice, fairness honesty, responsibility and reliability.

In Appendix B, two case studies are used to illustrate the integration of the portfoliomanagement principles outlined earlier, with the skill set required in building a relation-ship with the client. The situation in the first example – the Casuso family – containsmany of the variables that an investment manager has to assess in order to make suitableinvestment recommendations. While the family is fictitious and the ultimate selectionsare only one person’s view, the case study is a useful summary of the process.

Financial Planning and Taxation

13-16© CSI Global Education Inc. (2006)

POST-TEST

E. TAXES AND TAXATION ISSUESThis section discusses the fundamentals of taxation in Canada and deals with currentissues only. Individuals seeking advice or information on prior taxation years are referredto the CRA.

Proper tax planning should be a part of every investor’s overall financial strategy. Theminimization of tax, however, must not become the sole objective nor can it be allowedto overwhelm the other elements of proper financial management. The investor mustkeep in mind that it is the after-tax income or return that is important. Choosing aninvestment based solely on a low tax status does not make sense if the end result is alower after-tax rate of return than the after-tax rate of return of another investment thatis more heavily taxed.

While all investors wish to lighten their individual tax burden, the time and effort spenton tax planning must not outweigh the rewards reaped. Tax planning is an ongoingprocess with many matters being addressed throughout the year. The best tax advantagesare usually gained by planning early and planning often, allowing reasonable time forthe plan to work and to produce the desired results.

While the tax authorities do not condone tax evasion, tax avoidance by one or more ofthe following means is a legitimate end:

• Full utilization of allowable deductions;

• Conversion of non-deductible expenses into tax-deductible expenditures;

• Postponing the receipt of income;

• Splitting income with other family members, when handled properly; and

• Selecting investments that provide a better after-tax yield.

Although this discussion will highlight some of the taxation issues that affect taxpayers,none of the suggestions made here should be considered specific recommendations.Each case is unique and should be reviewed with proper consideration given to all rele-vant factors.

As tax plays a significant part in the overall financial plan and can affect the choice ofinvestments greatly, every attempt should be made to keep abreast of the ever-changingrules and interpretations. CRA can provide significant material to the investor by way ofregulations and rulings upon request. Contact the local CRA offices (or their website atwww.cra-arc.gc.ca) for further information. If the client is a U.S. citizen, U.S. tax lawswill also have to be taken into account.

1. The Income Tax System

The federal government imposes income taxes by federal statute (the Income Tax Act,often referred to as the ITA). All Canadian provinces have separate statutes whichimpose a provincial income tax on residents of the province and on non-residents whoconduct business or have a permanent establishment in that province. The federal gov-ernment collects provincial income taxes for all provinces except three:

• Quebec, which administers its own income tax on both individuals and corpora-tions; and

• Ontario and Alberta, which administer their own income tax on corporations.

Canada imposes an income tax on world income of its residents as well as the Canadiansource income on non-residents. Companies incorporated in Canada under federal or

CSC CHAPTER 13

VOLUME 2

13-17© CSI Global Education Inc. (2006)

PRE-TEST

provincial law are usually considered resident of Canada. Also, foreign companies withmanagement and control in Canada are considered resident in Canada and are subjectto Canadian taxes.

a) Taxation Year

All taxpayers must calculate their income and tax on a yearly basis. Individuals use thecalendar year while corporations may choose any fiscal year, as long as this time periodis consistent year over year. No corporate taxation year may be longer than 53 weeks. Achange of fiscal year-end may be made only with the approval of the Minister ofFinance.

Professionals and personal service corporations now must use a year-end of December.

b) Calculation of Income Tax

Calculating income tax involves four steps:

• Calculating all sources of income from employment, business or investments;

• Making allowable deductions to arrive at taxable income;

• Calculating the gross or basic tax payable on taxable income; and

• Claiming various tax credits, if any, and calculating the net tax payable.

Once total income has been determined, there are a number of prescribed deductionsand exemptions that may be made in calculating taxable income. For individuals, thesedeductions and exemptions may include registered pension plan contributions and reg-istered retirement savings plan contributions, childcare expenses, certain net capital andnon-capital losses of other years and other minor items. In the case of corporations,deductions in arriving at taxable income include charitable donations, certain net capitaland non-capital losses of other years and dividends received from other taxableCanadian companies and foreign affiliates.

2. Types of Income

There are four general types of income. Each is treated differently under Canadian taxlaws:

a) Income from Employment

Employment income is taxed on a gross receipt basis. This means that the taxpayer can-not deduct for tax purposes all the related costs incurred in earning income as a businessdoes. However, employees are permitted to deduct a few employment-related expensessuch as pension contributions, union dues, childcare expenses and other minor items.

b) Income from Business

Business income arises from the profit earned from producing and selling goods or ren-dering services. Self-employment income falls in this category. In contrast to propertyincome, business income requires activity on the part of the recipient. It is taxed on anet-income basis, calculated using GAAP. To encourage Canadian-controlled privatecorporations to expand, some companies are allowed a Small Business deduction, whichcan reduce the overall tax rate.

c) Income from Capital Property

Dividend and interest income is considered income from capital property. Any incomederived from pension plans, RRIFs, Old Age Security (OAS) or Canada Pension Plan(CPP) is also included in this category. This type of income is passive in nature sincethe property owner rarely does anything other than own the income-producing proper-ty. Individuals may deduct reasonable expenses such as property taxes, repairs and main-

Financial Planning and Taxation

13-18© CSI Global Education Inc. (2006)

tenance and, possibly financing costs on the acquisition of the property (such as interestpaid on a margin loan). Only net income is subject to tax.

d) Capital Gains and Losses

Both corporations and individuals are subject to taxes on capital gains. A capital gain(loss) results when a capital property is disposed of at a sale price greater (lower) than itscost. Costs of disposition are also included in arriving at a capital gain or capital loss.

3. Calculating Income Tax Payable

a) Tax Rates

Basic tax rates are applied to taxable income. Rates of federal tax applicable to individu-als in 2003 (excluding tax credits) are as follows:

TABLE 13.4

Federal Income Tax Rates for 2004

TAXABLE INCOME TAX

• up to $35,000 16%

• between $35,001 and $70,000 $5,600 + 22% on the next $34,999

• between $70,001 and $113,804 $13,300 + 26% on the next $43,803

• above $113,804 $24,689 + 29% on the remainder

In the past a high income surtax was added to the basic federal tax amount. This waseliminated in January 2001.

Currently, all provinces levy their own tax based on taxable income. Adding the provin-cial rate to the federal rate gives the taxpayer’s combined marginal tax rate. (The mar-ginal tax rate is the tax rate that would have to be paid on any additional dollars of tax-able income earned.)

Example: An Ontario resident with taxable income of $30,000 would be subject to a16% federal tax rate and a provincial tax rate of 6.05% giving him a combined marginaltax rate of 22.05%.

Given an investor’s marginal tax rate, the tax consequences of certain investment deci-sions can be estimated. In this way an advisor can respond to a client’s need to minimizetaxes and select securities for the portfolio that offer the investor a higher after-tax yield.In addition to incorporating marginal tax rates into the decision-making process, the taxplanning concepts outlined in this chapter should also be considered.

b) Payment of Income Tax

Employers are required to withhold income tax on salaries and wages and remit thisamount on their employees’ behalf to the government. Some individuals, and all corpo-rations, pay their taxes by instalments:

• Individuals who receive more than 25% of their income from sources that do notwithhold tax are required to pay quarterly instalments on March, June, Septemberand December 15 unless federal taxes payable for that year or for the prior twoyears are $2,000 or less. These instalments are based on either the tax reported forthe preceding year, the tax reported for the preceding and second preceding year oran estimate of the tax for the current year, whichever is least. Interest is charged ondeficient instalments. Adjustment for over- or underpayment is made at the year-end through the annual tax return.

CSC CHAPTER 13

VOLUME 2

13-19© CSI Global Education Inc. (2006)

• Corporations must pay federal and provincial tax instalments at each month end,using the methodology outlined above.

4. Tax on Dividends

a) Dividends from Taxable Canadian Corporations

Individual taxpayers receive preferential tax treatment on dividends received from tax-able Canadian corporations. The taxpayer is required to gross-up the amount of the div-idend by 25%. For example, if an individual receives a $160 dividend, it would bereported for tax purposes as $200 (125% of $160) in net income. The additional $40 isreferred to as the gross up and the $200 is known as the taxable amount of dividend.

The taxpayer calculates net income using the $200 amount, and can then claim a creditin the amount of:

13.33% of the taxable amount of dividend

or

13.33% x $200 = $26.67

All provinces levy provincial taxes on income, which are calculated as a percentage oftaxable income on an ascending graduated scale, in a similar fashion as the federal gov-ernment. Unlike other provinces, Quebec collects its own provincial taxes.

The dividend gross-up and federal tax credit are shown on the T5 form sent annually toshareholders. The source of the T5, i.e. who issues it, depends on how the shares areheld. Registered shareholders receive the T5 from the dividend-paying corporation itself;investment dealers holding shares in street name issue the T5 to the beneficial owners.Quite often the investment dealer will combine all dividends paid to the investor duringthe year and issue just one T5 for all of them.

Stock dividends and dividends that are reinvested in shares are treated in the same man-ner as cash dividends.

b) Minimizing Taxable Income on After-Tax Yield of Investments

Dividends from taxable Canadian corporations (but not foreign corporations) are sub-ject to less tax than interest but usually more tax than capital gains. Accordingly, a shiftfrom interest bearing investments into dividend-paying Canadian stocks may reducetaxes and improve after-tax yield.

Depending on the tax rate, capital gains tax can be substantially lower that tax onCanadian dividends. This is illustrated in Tables 13.5 and 13.6. At a marginal tax rateof 29%, the difference in taxes owed is $50.83. But at a marginal tax rate of 22%, thedifference declines to $1.67, with dividends having the advantage. In both cases, there isa substantial difference between the tax owed on interest and the tax owed on capitalgains.

Financial Planning and Taxation

13-20© CSI Global Education Inc. (2006)

TABLE 13.5

Comparison of Tax Consequences of Investment Income in a 29% Marginal Tax Bracket

Interest Income Canadian Dividend Capital Gains Income Income

Income Received $ 1,000.00 $ 1,000.00 $ 1,000.00

Taxable Income $ 1,000.00 $ 1,250.00 $ 500.00

(Grossed up by 25%) (50% of $1,000)

Federal Tax (29%) $ 290.00 $ 362.50 $ 145.00

Less Dividend Tax Credit (13.33%) $ 166.67

Federal Tax Owed $ 290.00 $ 195.83 $ 145.00

TABLE 13.6

Comparison of Tax Consequences of Investment Income in a 22% Marginal Tax Bracket

Interest Income Canadian Dividend Capital Gains Income Income

Income Received $ 1,000.00 $ 1,000.00 $ 1,000.00

Taxable Income $ 1,000.00 $ 1,250.00 $ 500.00

(Grossed up by 25%) (50% of $1,000)

Federal Tax (22%) $ 220.00 $ 275.00 $ 110.00

Less Dividend Tax Credit (13.33%) $ 166.67

Federal Tax Owed $ 220.00 $ 108.33 $ 110.00

c) Tax on Foreign Dividends

Individuals who receive dividends from non-Canadian sources usually receive a netamount from these sources, as taxes are usually deducted at source. Such investors maybe allowed a deduction from the Canadian income tax otherwise payable. The allowablecredit is essentially the lesser of the foreign tax paid or the Canadian tax payable on theforeign income, subject to certain adjustments. Details on what foreign tax is allowed asa deduction are available from the CRA.

d) Capital Dividends

A private corporation may elect to pay a dividend out of its capital dividend account,which is the non-taxable portion of the net capital gains realized by the corporationsince 1971. The dividend is not included in the income of the investor at the time ofreceipt and has no effect on the adjusted cost base of the shares on which the dividendwas paid.

e) Tax on Interest

For investment contracts acquired after 1989, taxpayers are required to report interestincome (from such investments as CSBs, GICs, and bonds) on an annual accrual basis,regardless of whether or not the cash is actually received. An “investment contract” is

CSC CHAPTER 13

VOLUME 2

13-21© CSI Global Education Inc. (2006)

specifically defined, and includes virtually all debt obligations, as well as certain annuityand insurance contracts.

f) Tax on Income Earned from Strip Bonds

Strip bonds are purchased at a discount and mature at par. The income earned, whilenot received until maturity, must be reported on an annual accrual basis. For the pur-poses of CRA, the income earned is considered to be interest income.

5. Tax Deductible Items Related to Investment Income

a) Carrying Charges

Tax rules permit individuals to deduct certain carrying charges for tax purposes.Acceptable carrying charge deductions include:

• Interest paid on funds borrowed to earn investment income unless the funds are usedfor a rental property that is under construction or is vacant while being renovated;

• Investment counseling fees (other than a commission paid to registered investmentcounselors). Counseling fees for RRSPs and RRIFs are not deductible;

• Fees paid for administration or safe custody of investments. Administration andtrustee fees for self-directed RRSPs and RRIFs are not deductible;

• Safety deposit box charges; and

• Accounting fees paid for the recording of investment income.

b) Interest on Borrowed Funds

A taxpayer may deduct the interest paid on funds borrowed to purchase securities if:

• The taxpayer has a legal obligation to pay the interest;

• The purpose of borrowing the funds is to earn income; and,

• The income produced from the securities purchased with the borrowed funds is nottax exempt.

The interest is deductible whether the transaction is or is not at arm’s length. (Arm’s lengthis an expression used to describe a transaction between persons whereby each acts in theirown interests. In general, unrelated persons usually deal with each other at arm’s length,while transactions with related persons are considered a non-arm’s length transaction.)

If the interest paid to borrow funds exceeds the amount of interest earned on a debtsecurity, the loss or difference between the two amounts is not tax deductible. However,in the case of convertible debentures, normally all carrying charges are deductible sincethe debentures may be converted into common shares which could theoretically payunlimited dividends.

c) Carrying Costs on Equity Investments

Part of the carrying costs of preferred shares with a fixed dividend rate may be disal-lowed as a tax deduction if the carrying costs exceed the grossed-up amount of the pre-ferred dividend.

Carrying charges on common shares are, for the most part, tax deductible even for non-dividend paying growth securities since earnings may later rise and dividends may bepaid in future.

Thus, carrying cost deductibility is based on the income potential of the investment made.

Financial Planning and Taxation

13-22© CSI Global Education Inc. (2006)

6. Capital Gains and Losses

Investors and their advisors should have a general understanding of the concepts of cap-ital gains and losses when developing an investment strategy.

Basically, a capital gain arises from the disposition of a capital property for more than itscost (i.e., the selling price is higher than the cost price). For tax purposes, however, thecalculation may not be so simple because:

• Additional costs are often involved in the purchase and sale of property other thanthe cost price, e.g., commission paid on the purchase and sale of listed securities;and

• The past value of certain properties on which capital gains are calculated is difficultto determine, e.g., real estate held for many years.

For these and other reasons, CRA applies complex rules for calculating capital gains.Although capital gains result in an additional tax burden to the taxpayer, only part of acapital gain is taxed.

Generally, CRA treats share dispositions as being capital in nature. However, an excep-tion may occur if the taxpayer’s actions, indicated by intention, show that the taxpayeris in the business of trading securities to realize a speculative profit from the shares. Inthis case, CRA may argue that gains realized are fully taxable as ordinary income (andlosses fully deductible). Factors which CRA would review in assessing whether trading isspeculative (their definition) in nature include:

• Short periods of ownership;

• A history of extensive buying and selling of shares or quick turnover of securities;

• Special knowledge of, or experience in, securities markets;

• Substantial investment of time spent studying the market and investigating poten-tial purchases;

• Financing share purchases primarily on margin or some other form of debt; and,

• The nature of the shares (i.e. speculative, non-dividend type).

Although none of these individual factors alone may be sufficient for CRA to character-ize the taxpayer’s trading activities as a business, a number of these factors in combina-tion may be sufficient to do so. In every instance, the particular circumstances of thedisposition would need to be evaluated before a determination can be made.

Taxpayers may elect that all gains and losses on the sale of Canadian securities be treat-ed as capital gains or losses during their lifetime provided they are neither a trader nordealer in securities nor a non-resident. CRA interprets a dealer or trader in securities tobe a taxpayer who participates in the promotion or underwriting of a particular issue ofshares or who, to the public, is a dealer in shares. In general, an employee of a corpora-tion engaged in these activities is not a dealer. If, however, as a result of employment, anemployee engages in insider trading to realize a quick gain, the taxpayer will be consid-ered to be a trader of those particular shares.

CSC CHAPTER 13

VOLUME 2

13-23© CSI Global Education Inc. (2006)

a) Tax on Disposition of Shares

The general rules of capital gains (i.e., the proceeds of disposition minus the adjustedcost base plus any costs of disposing of the property) apply to the sale of shares.

Example: An investor buys 100 ABC common shares at $6, and sells the 100 shares at $10two years later. In the year of sale, the investor’s tax liability, would be as follows:

Gross proceeds from sale (100 x $10) $ 1,000.00

Less: Adjusted cost base – Cost of shares (100 x $6) including commission $ 617.00____________

$ 383.00

Less: Commission on Sale 25.00____________Capital Gain $ 358.00____________Taxable Capital Gain (50% of $358) $ 179.00

Investors who receive stock dividends or who subscribe to dividend reinvestment plansmust declare these as income in the year the dividend is paid. Investors should keep arecord of stock dividends and reinvestments as they increase the adjusted cost base ofthe investment. When the stock is sold, the higher adjusted cost base will reduce anycapital gain.

b) Valuing Identical Shares

The adjusted cost base of shares sold is generally composed of the purchase price pluscommission expense. However, investors often own a number of the same class of sharesthat were bought at different prices. When a taxpayer owns identical shares in a compa-ny, the method used to calculate the adjusted cost base of such shares is known as theaverage cost method. An average cost per share is calculated by adding together the costbase of all such stock and dividing by the number of shares held.