Human Computer Interaction CSC 4730 User System Interface CSC 8570

description

VOLUME 1

7-1

A. INTRODUCTION

This chapter provides an introduction to derivatives and derivative markets, beginningwith a basic description of a derivative. The differences between derivatives that trade onan exchange and those that trade over-the-counter are outlined followed by a description

of the types of underlying assets upon which derivatives are based. The rationale for the use ofderivatives by the four main participants in the market is discussed. An overview of the termi-nology and the basic strategies employed is presented. Special attention is given to the use ofderivatives by mutual fund managers and portfolio managers.

Finally the last section of the chapter describes two different types of derivatives: rights and war-rants. Unlike the derivatives already discussed, these instruments are most commonly issued by acorporation raising capital. Their use and valuation, both from the perspective of the companyand the investor, are explained.

B. WHAT IS A DERIVATIVE?A derivative is a financial contract whose value is derived from, or dependent upon, the value ofsome other asset. The other asset, known as the derivative’s underlying asset or underlying inter-est or security, can be a financial asset, such as a stock or bond, a currency, or even an interestrate or equity index. It can also be a real asset or commodity, such as crude oil, gold, or wheat.Because of the link between the value of a derivative and its underlying asset, derivatives can actas a substitute for, or as an offset to, a position in the underlying asset. As such, derivatives areoften used to manage the risk of an existing or anticipated position in the underlying asset, aswell as to speculate on the value of the underlying asset. While some derivatives have complexstructures, they all fall into one of two basic types: options or forwards.

• Options are contracts between two parties: a buyer and a seller. The buyer of an option hasthe right, but not the obligation, to buy or sell a specified quantity of the underlying asset inthe future at a price agreed upon today. The seller of the option is obligated to complete thetransaction if called upon to do so. An option that gives its owner the right to buy theunderlying asset is known as a call option; the right to sell the underlying asset is known asa put option.

• Forwards are also contracts between a buyer and a seller. With forwards, however, both par-ties obligate themselves to trade the underlying asset in the future at a price agreed upontoday. Neither party has given the other any right; they are both obligated to participate inthe future trade.

Despite this fundamental difference between options and forwards, all derivatives share somefeatures.

1. Features Common to All Derivatives

All derivatives are contractual agreements between two parties, often known as counterparties.One counterparty is the buyer, and the other is the seller. The agreements spell out the rightsand/or obligations of each party. Derivatives have a price. Buyers try to buy derivatives as cheap-ly as possible while sellers try to sell them for as much as possible.

Chapter 7

Derivatives

© CSI Global Education Inc. (2005)

PRE-TEST

All derivatives have an expiration date. Both parties must fulfill their obligations orexercise their rights under the contract on or before the expiration date. After that date,the contract is automatically terminated.

When a derivative contract is drawn up, it includes a price or formula for determiningthe price of an asset to be bought and sold in the future, either on or before the expira-tion date.

With forwards, no up-front payment is required. Sometimes one or both parties make aperformance bond or good-faith deposit, which gives the party on the other side of thetransaction a higher level of assurance that the terms of the forward will be honoured.

With options, the buyer makes a payment to the seller when the contract is drawn up.This payment, known as a premium, gives the buyer the right to buy or sell the under-lying asset at a pre-set price on or before the expiration date.

Another feature of derivatives is that, unlike financial assets such as stocks and bonds,derivatives can be considered a zero-sum game. In other words, aside from commissionfees and other transaction costs, the gain from an option or forward contract by onecounterparty is exactly offset by the loss to the other counterparty. The large financiallosses incurred by some well-known users of derivatives (such as Barings Bank,Metallgesellschaft, or Orange County) were really large wealth transfers: every dollar lostby these parties represented a dollar gained by the counterparties on the other side ofthe contracts.

2. Derivative Markets

In Chapter 5 you learned that most bonds trade in the OTC market and a small num-ber trade on organized exchanges. In Chapter 6 you learned that stocks trade onexchanges and OTC markets as well. The same is true for derivatives.

Whereas the primary difference between exchange-traded and OTC stocks and bonds istrading mechanics, the difference between exchange-traded and OTC derivatives ismuch more pronounced.

a) Over-the-Counter Derivatives

The OTC derivatives market is an active and vibrant market that consists of a loosely con-nected and lightly regulated network of brokers and dealers who negotiate transactionsdirectly with one another primarily over the telephone and/or computer terminals. TheOTC market is dominated by financial institutions such as banks and brokerage housesthat trade with their large corporate clients and other financial institutions. This markethas no trading floor and no regular trading hours. Traders do not meet in person to nego-tiate transactions and the market stays open 24 hours a day. At nights and during week-ends and holidays, some traders and support staff are still working at their trading desks.

One of the attractive features of OTC derivatives (especially to the corporations andinstitutional investors that use them) is that contracts can be custom designed to meetthe needs of specific users. As a result, OTC derivatives tend to be somewhat more com-plex than exchange-traded derivatives, as special features can be added to the basic prop-erties of options and forwards.

b) Exchange-Traded Derivatives

A derivative exchange is a legal corporate entity organized for the trading of derivativecontracts. The exchange provides the facilities for trading, either a trading floor or anelectronic trading system or, in some cases, both. The exchange also stipulates the rulesand regulations governing trading in order to maintain fairness, order, and transparencyin the marketplace. Derivatives exchanges evolved in response to the OTC issues ofstandardization, liquidity and credit risk.

Derivatives

7-2© CSI Global Education Inc. (2005)

There are two derivative exchanges in Canada: the Bourse de Montréal (or just theBourse) and the Winnipeg Commodity Exchange (WCE). The Bourse lists options onstocks, bonds and indexes, and futures (forwards that are exchange-traded) on bondsand indexes. The WCE lists futures and futures options on agricultural goods such ascanola, wheat and barley.

3. Key Differences Between Exchange-Traded and OTC Derivatives

Readers may ask how organized exchanges and OTC markets successfully co-exist whenthe interests that underlie derivative instruments in both markets are basically the same.One would think that over time, one of the two markets would prevail.

The co-existence has proven successful and long-lasting because the two markets differin significant ways, each market offering advantages to users depending on their particu-lar needs.

a) Standardization and Flexibility

One of the most important differences between exchange-traded and OTC derivatives isflexibility. In the OTC market, the terms and conditions of a contract can be tailored tothe specific needs of their users. The users may choose the most appropriate terms tomeet their particular needs. In contrast, for exchange-traded derivatives, the exchangespecifies the contracts that are available to be traded on the exchange; each contract hasstandardized terms and other specifications, which may or may not meet the needs ofcertain derivatives users.

b) Privacy

Another important difference is the private nature of OTC derivatives. In an OTCderivative transaction, neither the general public nor others (including competitors)know about the transaction. On exchanges, all transactions are recorded and known tothe general public, although the exchanges do not announce, nor do they necessarilyknow, the identities of the ultimate counterparties to every transaction.

c) Liquidity and Offsetting

Because they are private and custom designed, OTC derivatives cannot be easily termi-nated or transferred to other parties in a secondary market. In many cases, these con-tracts can only be terminated through negotiations between the two parties.

By contrast, the standardized and public nature of exchange-traded derivatives meansthat they can be terminated easily by taking an offsetting position in the contract. As auser’s needs may change in line with changing economic, market and business condi-tions, it is sometimes advantageous to be able to terminate a derivative before it expires.(The concept of expiration as it applies to derivatives is explained later in the chapter inthe sections on options and forwards.)

d) Default Risk

Another downside to the private nature of OTC derivatives is that default or credit riskis a major concern. Default risk is the risk that one of the parties to a derivative contractcannot meet its obligations to the other party. Given this risk, many derivative dealers inthe OTC market do not deal with customers that are unable to establish certain levels ofcreditworthiness. In addition, the size of most contracts in the OTC market may begreater than most investors can manage. For this reason, the OTC market is restrictedto large institutional and corporate customers. Individual investors are generally limitedto dealing in exchange-traded derivatives.

Default risk is not a significant concern with exchange-traded derivatives.Clearinghouses, which are set up by exchanges to ensure that markets operate efficiently,

CSC CHAPTER 7

VOLUME 1

7-3© CSI Global Education Inc. (2005)

guarantee the financial obligations of every party and contract. The existence of clear-inghouses means that market participants need not be concerned with the honesty orreliability of other trading parties. The integrity of the clearinghouse is the only con-cern. In the history of U.S. and Canadian derivatives exchanges, a clearinghouse hasnever failed to meet its obligations, so this concern is minimal.

The clearing corporation becomes, in effect, the buyer for every seller and the seller forevery buyer. By being on the opposite side of all trades, the clearing corporation mini-mizes the risk of default. Although individual trades are negotiated between the twoparties through the exchange, once the contract has been made, the clearing corporationis the counterparty. The Canadian Derivatives Clearing Corporation (CDCC) is thesole clearing corporation for all exchange-traded options and futures in Canada.

e) Regulation

A final difference between OTC and exchange-traded derivatives arises out of the factthat OTC contracts are private and exchange-traded contracts are public. While deriva-tive transactions on exchanges are extensively regulated by the exchanges themselves andgovernment agencies, OTC derivative transactions are generally unregulated. On theone hand, the largely unregulated environment in the OTC markets permits unrestrict-ed and explosive growth in financial innovation and engineering. Generally, no govern-ment approval is needed to offer new types of derivatives. The innovative contracts aresimply created by parties that see mutual gain in doing business with each other. Thereare no costly constraints or bureaucratic red tape. On the other hand, the regulatedenvironment of exchange-traded derivatives brings about fairness, transparency, and anefficient secondary market.

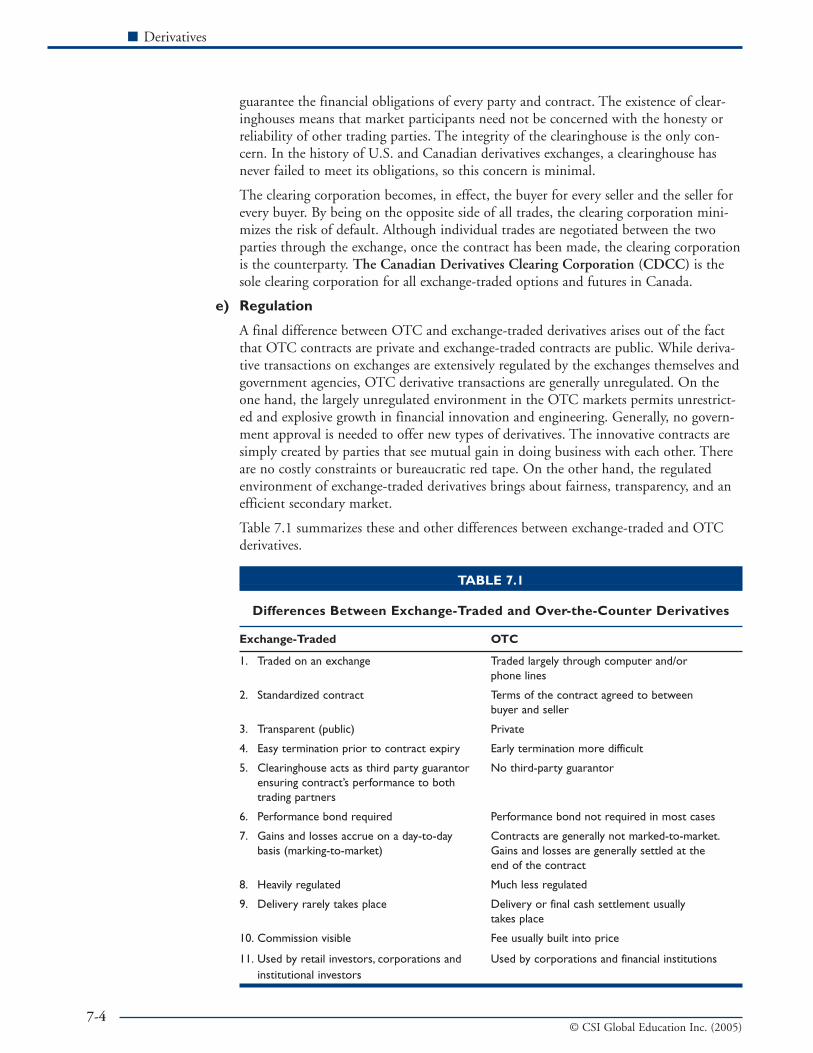

Table 7.1 summarizes these and other differences between exchange-traded and OTCderivatives.

TABLE 7.1

Differences Between Exchange-Traded and Over-the-Counter Derivatives

Exchange-Traded OTC

1. Traded on an exchange Traded largely through computer and/or phone lines

2. Standardized contract Terms of the contract agreed to betweenbuyer and seller

3. Transparent (public) Private

4. Easy termination prior to contract expiry Early termination more difficult

5. Clearinghouse acts as third party guarantor No third-party guarantorensuring contract’s performance to bothtrading partners

6. Performance bond required Performance bond not required in most cases

7. Gains and losses accrue on a day-to-day Contracts are generally not marked-to-market.basis (marking-to-market) Gains and losses are generally settled at the

end of the contract

8. Heavily regulated Much less regulated

9. Delivery rarely takes place Delivery or final cash settlement usually takes place

10. Commission visible Fee usually built into price

11. Used by retail investors, corporations and Used by corporations and financial institutionsinstitutional investors

Derivatives

7-4© CSI Global Education Inc. (2005)

C. TYPES OF UNDERLYING ASSETSThere are generally two major categories of underlying assets for derivative contracts –commodities and financial assets. A brief summary follows outlining the assets thatunderlie derivative contracts traded on organized exchanges in the U.S. and Canada. Inthe OTC markets, the choice of underlying assets is limited only by the imaginationand needs of market participants.

1. Commodities

Commodity futures and options are commonly used by producers, merchandisers, andprocessors of commodities to protect themselves against fluctuating commodity prices.Most of these commodities, like soybeans, crude oil and copper, are used mainly forconsumption purposes while others, like gold, are used primarily for investment purpos-es. Speculators also use commodities to profit from the fluctuating prices. Dependingon the commodity, prices are affected by supply and demand, agricultural production,weather, government policies, international trade, demographic trends, and economicand political conditions. The following are the types of commodities that underlie deriv-ative contracts:

• Grains and oilseeds such as wheat, corn, soybeans and canola;

• Livestock and meat such as pork bellies, hogs, live cattle and feeder cattle;

• Forest, fibre and food such as lumber, cotton, orange juice, sugar, cocoa, and coffee;

• Precious and industrial metals such as gold, silver, platinum, copper, and aluminum;and

• Energy products such as crude oil, heating oil, gasoline, natural gas, and propane.

Other than the energy category, most commodity derivatives are exchange-traded con-tracts.

2. Financials

The last two decades have witnessed an explosive growth in derivatives, especially infinancial derivatives. This growth has been fueled by:

• increasingly volatile interest rates, exchange rates, and equity prices;

• financial deregulation and intensified competition among financial institutions;

• globalization of trade and the tremendous advances in information technology; and

• extraordinary theoretical breakthroughs in financial engineering.

The most commonly used financial derivatives are summarized below.

a) Equity and Equity Indexes

Equity is the underlying asset of a large category of financial derivatives. The predomi-nant equity derivatives are equity options – options on individual stocks. These deriva-tives are traded mainly on organized exchanges such as the Bourse de Montréal inCanada, and the CBOE, International Securities Exchange (ISE), Boston OptionsExchange (BOX), and American Stock Exchange (AMEX) in the U.S. All other majortrading nations have equity derivatives listed on one or more of their exchanges.

Equity futures (more commonly known as single stock futures) have been trading onNorth American exchanges since early in 2000. The Bourse de Montréal listed a futurescontract on Nortel Networks from January 2000 until November 2004. After some ini-tial success, the contract did not sustain the interest needed to ensure its long-term via-bility, which undoubtedly had something to do with the troubles involving Nortel dur-

CSC CHAPTER 7

VOLUME 1

7-5© CSI Global Education Inc. (2005)

ing this period. The Bourse has not listed any other single-stock futures contracts. Inthe U.S., the joint-venture exchange known as OneChicago has listed single-stockfutures on a large number of stocks since 2002. These contracts have been only margin-ally successful.

Equity index derivatives have been one of the most spectacular success stories of thefinancial markets in the last 20 years. These contracts are based on equity indexes suchas the S&P/TSX 60 Index in Canada and the S&P 500 Index in the U.S. More recent-ly, options on exchange-traded funds (ETFs) such as the iUnits S&P/TSX 60 IndexFund have been listed. The introduction of “mini” equity index futures contracts, whichare based on a relatively small amount of the underlying asset, has fuelled the growth ofequity index derivatives in the last few years.

In contrast to most commodity futures and some other financial futures and options,equity index futures and options are settled by the delivery of cash rather than the deliv-ery of the stocks that make up the underlying index. (This does not apply to options onETFs, which are settled by the physical delivery of the underlying ETFs.) This isdesigned to eliminate the potential difficulty and costs of trading a basket of the under-lying stocks.

b) Interest Rates

Exchange-traded interest rate derivatives are generally based on interest rate sensitivesecurities rather than on interest rates directly. In Canada, underlying assets includeBankers’ Acceptances and Government of Canada bonds. All interest rate futures trad-ing in Canada takes place at the Bourse de Montréal. Futures options are available on 3-month Bankers’ Acceptances futures.

In the U.S., underlying assets for exchange-traded interest rate derivatives includeEurodollars, which are traded at the CME (Chicago Mercantile Exchange), as well asU.S. Treasury notes and bonds, which are traded at the CBOT (Chicago Board ofTrade). Futures options are available on these contracts.

In the OTC market, interest rate derivatives are generally based on well-defined floatinginterest rates, which are not easily manipulated by market participants. Examples ofsuch underlying assets include LIBOR (the interest earned on Eurodollar deposits inLondon) and the yields on Treasury bills and Treasury bonds. Because these OTC deriv-atives are based on an interest rate rather than an actual security, the contracts are set-tled in cash.

c) Currencies

The most commonly used underlying assets in currency derivatives are the U.S. dollar,British pound, Japanese yen, Swiss franc, and the Euro. The types of contracts tradedinclude currency futures and options on organized exchanges (including a popularCanadian dollar futures contract listed on the CME) and currency forwards and curren-cy swaps in the OTC market. There are no currency derivative contracts listed on anyCanadian exchanges.

Derivatives

7-6© CSI Global Education Inc. (2005)

D. WHO USES DERIVATIVES AND WHY DO THEY USE THEM?

Derivatives users can be divided into four groups: individual investors, institutionalinvestors, businesses and corporations, and derivative dealers. The first three groups arethe end-users of derivatives. These parties use derivatives either to speculate on the priceor value of an underlying asset, or to protect the value of an anticipated or existing posi-tion in the underlying asset. The latter application, a form of risk management, isknown as hedging.

The last group, derivative dealers, are the intermediaries in the markets, buying and sell-ing to meet the demands of the end users. Derivative dealers do not normally take largepositions in derivative contracts. Rather, they try to balance their risks and earn profitsfrom the volume of deals they do with their customers.

1. Individual Investors

For the most part, individual investors are able to trade exchange-traded derivativesonly. They are active investors in exchange-traded options markets and, to a lesserextent, futures markets.

Individual investors should only use derivatives if they fully understand all of theirpotential risks and rewards. Furthermore, investors should consider speculative strategiesonly if they have a high degree of risk tolerance, because there is the potential to sufferlarge losses in derivatives trading. Risk management strategies, on the other hand, canbe beneficial to all investors, from the most conservative to the most aggressive.Examples of these strategies are provided in the following sections on options and for-wards.

Individual investors in Canada can trade exchange-traded derivatives directly by openinga special type of account with a full-service or discount brokerage firm registered tooffer such accounts. To deal with investors in exchange-traded derivatives, investmentadvisors at full-service firms and investment representatives at discount firms must bespecially licensed. Licensing requires successful completion of CSI’s DerivativesFundamentals Course (DFC) and either the Options Licensing Course (OLC) or FuturesLicensing Course (FLC).

Many individual investors speculate in derivatives markets indirectly through the pur-chase of a mutual fund or hedge fund that uses derivatives.

2. Institutional Investors

Institutional investors that use derivatives include mutual fund managers, hedge fundmanagers, pension fund managers, insurance companies, and more. Like individualinvestors, institutional investors use derivatives for both speculation and risk manage-ment. Unlike individual investors, most institutional investors are able to trade OTCderivatives in addition to exchange-traded derivatives.

Many institutional investors use derivatives to quickly carry out changes to their portfo-lio’s asset allocation. In today’s ever changing financial environment, portfolio managersfrequently need to shift funds from one market segment to another market segment,from one type of market to another type of market, and from one country to anothercountry. For example, the manager of a global equity mutual fund may decide to sell allor a significant portion of the fund’s British stocks and use the proceeds to buy a basketof French and German stocks. Quickly exiting and entering a market in the convention-al way – buying and selling the actual stocks – can be inefficient and more costly thanone might imagine. There are costs associated with trading, including commission fees,

CSC CHAPTER 7

VOLUME 1

7-7© CSI Global Education Inc. (2005)

bid-ask spreads, and other administrative fees. These transaction costs can be quite highin some cases, and may impact on the decision to enter or exit a market. In addition,buying or selling a large quantity of certain securities may produce adverse price pres-sures on the market. This represents a hidden cost to the transaction. A large sell ordermay push the price down so that less money will be received from selling the securities.Conversely, a large buy order may bid up the price so that it will cost more than thecurrent available price to complete the transaction. These adverse price effects could beespecially severe in thinly traded equity or bond markets.

If the switch is permanent or long-term in nature, it is usually accomplished by liqui-dating positions in one market and transferring the funds into the other market. Quitefrequently, however, the switch from market to market is only temporary. For example,the manager of the global equity fund may want to switch out of British stocks and intoFrench and German stocks for only a few months. When market conditions subse-quently change, a reverse switch and other shifts of funds are quite possible. In thesecases, it is usually more efficient and cost-effective to carry out the switch temporarilyusing derivatives rather than trading in the underlying assets directly.

In Exhibit 7.1, the manager of the global equity fund effects the temporary portfolioswitch using futures contracts rather than the underlying stocks. This strategy allows themanager to secure the desired asset allocation without incurring the costs associatedwith such a shift.

EXHIBIT 7.1

Using Futures Contracts to Facilitate a Temporary Asset Allocation Switch

The manager of the Razor Global Equity Fund has $100 million invested in European equities, 20% ofwhich is in British stocks. Of the remaining 80%, 25% is in German stocks, 20% is in French stocks, and35% is in a mixture of Italian, Spanish, Swedish, and Finnish stocks. She believes that this is the rightlong-term allocation for the fund, but she also believes that over the next six months the German andFrench markets will significantly outperform the British market. She figures that, over the next sixmonths, a 0% allocation to British stocks, a 35% allocation to German stocks, a 30% allocation toFrench stocks, and a combined 35% allocation to Italian, Spanish, Swedish, and Finnish stocks will giveher portfolio above-average returns with an appropriate amount of risk.

Rather than disrupt the portfolio by buying and selling a very large amount of stock and incurring thetransaction costs, and then reversing the whole process again in six months, the portfolio managerdecides to use equity index futures to implement the switch. Specifically, she will use 6-month futureson British, German, and French equity indexes.

For simplicity, assume that the current value of the stocks represented by each of these equity indexfutures contracts is $100,000.To implement the switch, the portfolio manager would have to sell 200British equity index futures contracts and buy 100 each of the German and French equity indexfutures contracts.The buying and selling of these contracts would entail much lower transaction coststhan buying and selling a total of $40 million worth of British, German, and French stocks.

In six months, when the portfolio manager offsets the futures positions, the overall return on the fundwill be similar to that of the desired weighting of 0% British stocks, 35% German stocks, 30% Frenchstocks, and 35% of other European stocks.This is because any gain or loss on the British equity indexfutures will offset any loss or gain on the actual British stocks in the fund, while the gain or loss on theGerman and French equity index futures will amplify the gain or loss on the actual German and Frenchstocks in the fund.

Derivatives

7-8© CSI Global Education Inc. (2005)

3. Corporations and Businesses

Corporations that use derivatives come in all shapes and sizes, but for the most partthey tend to be larger companies that make use of borrowed money, have multinationaloperations that generate or require foreign currency, or produce or consume significantamounts of one or more commodities.

Corporations and businesses use derivatives primarily for hedging purposes. In particu-lar, these users tend to focus on derivatives that help them hedge interest rate, currency,and commodity price risk.

Corporations that hedge with derivatives do so because they would rather focus theirefforts on running their primary business instead of trying to guess where interest rates,currencies or commodity prices are going.

a) Hedging

Hedging is the attempt to eliminate or reduce the risk of either holding an asset forfuture sale or anticipating a future purchase of an asset. Hedging with derivativesinvolves taking a position in a derivative with a payoff that is opposite to that of theasset to be hedged. For example, if a hedger owns an asset, and is concerned that theprice of the asset could fall in the future, a short position in a forward contract based onthe asset would be appropriate. A decline in the price of the asset will result in a loss onthe asset being held, but would be offset by a profit on the short forward contract.Another solution would be to buy a put option on the underlying asset.

On the other hand, if a hedger anticipates buying an asset in the future, and is con-cerned that the price could rise by the time the purchase is made, buying a forward con-tract or a call option would be appropriate. A price increase will result in a higher pricebeing paid by the hedger, but this would be offset by a profit on the forward or calloption.

A hedger starts with a pre-existing risk that is generated from a normal course of busi-ness. For example, a farmer growing wheat has a pre-existing risk that the price of wheatwill decline by the time it is harvested and ready to be sold. In the same way, an oilrefiner that holds storage tanks of crude oil waiting to be refined has a pre-existing riskthat the price of the refined product may decline in the interim.

To reduce or eliminate these price risks, the farmer and the refiner could take derivativepositions that will profit if the price of their assets declined. Any losses in the underly-ing assets would be offset by gains in the derivative instruments. That being said, anygains in these assets might be offset by derivative losses of roughly the same size,depending on the type of derivative chosen and the overall effectiveness of the hedge.

b) To Hedge or Not to Hedge?

The decision to hedge increasingly is becoming a corporate level decision. Where oncethe use of derivatives by a company was poorly understood and cause for concern, it isnow expected that a company’s Board of Directors use derivatives in an appropriatefashion as a risk management tool. Exhibit 7.2 illustrates this shift in attitude. Althoughit often seems like a simple decision, the determination of whether or not to hedge andhow to hedge can often be complex. Hedging does not always result in the completeelimination of all risks.

In reality, the proper use of derivatives involves first understanding the derivative con-tracts that can be used for a particular hedge and then deciding on an appropriate levelof balance between risk and return that is consistent with the hedger’s overall strategy.

CSC CHAPTER 7

VOLUME 1

7-9© CSI Global Education Inc. (2005)

EXHIBIT 7.2

Hedging or not hedging: a legal matter?

There can be many good reasons for hedging and sometimes good reasons for not hedging.To hedgeor not to hedge? Corporate boardrooms are not the only place this intriguing question is debated andanswered.This question is increasingly decided in courtrooms.

Take the case of Farmers Cooperative (FC), a grain elevator co-op in Indiana. It engaged in the businessof buying, storing, and selling grain. In the late 1970s, FC’s profits had declined steadily.Acting on theadvice of its accountant, FC’s Board of Directors authorized FC’s manager to begin hedging usingfutures contracts. FC continued to experience substantial operating losses, as less than 1 percent ofgrain sales were actually hedged. Shareholders figured that a proper hedge would have saved the com-pany large amounts of money, so they sued the Board of Directors.

The plaintiffs argued that the Board breached its duty by using an inexperienced manager and by failingto supervise the manager.The plaintiffs also argued that the Board members failed to learn enoughabout hedging to protect the shareholders’ interests.The plaintiffs won the lawsuit and the directorswere ordered to pay over $400,000 to the plaintiffs.

A lesson to be learned? Directors must be informed or must get informed about the advantages anddisadvantages of hedging and how derivatives markets work.They must also supervise management toensure that a hedging program is executed properly. Ignorance cannot be used as a legal defense.

4. Derivative Dealers

The last group of users is the derivative dealers. Derivative dealers play a crucial role inthe OTC markets by taking the other side of the positions entered into by end users.Dealers in the exchange-traded market take the form of market makers that stand readyto buy or sell contracts at any time.

In Canada, the primary OTC derivative dealers are the big six banks and their invest-ment dealer subsidiaries, as well as the Canadian subsidiaries of large foreign banks andinvestment dealers. Exchange-traded market makers include banks and investment deal-ers as well as professional individuals.

E. OPTIONS1. Key Terms and Definitions

An option contract gives the buyer (also known as the long position or holder or ownerof the option) the right, but not the obligation, to buy or sell an underlying asset. Theseller of the option (also known as the short position or option writer) is obligated to buyor sell the underlying asset if the option buyer eventually chooses to do so. The right tobuy or sell is for a specified amount of the underlying asset, at a specified price (knownas the strike price or exercise price), within a specified period of time that ends on theexpiration date. The expiration date of an OTC option can be any day the two counter-parties agree to. The expiration date of an exchange-traded option is determined by theexchange on which the option trades. For example, exchange-traded equity options inboth Canada and the U.S. expire on the Saturday following the third Friday of the expi-ration month.

Traditionally, options have been listed with relatively short terms of nine months or lessto expiration. They are useful for investors who want to profit or protect themselvesfrom short-term market fluctuations. The exchanges have begun listing options withmuch longer expirations. These options are called Long-Term Equity AnticiPationSecurities (LEAPS). LEAPS are simply long-term option contracts and offer the samerisks and rewards as regular options.

Derivatives

7-10© CSI Global Education Inc. (2005)

To obtain the right to buy or sell the underlying asset, option buyers must pay sellers afee, known as the option price or option premium. Once the premium has been paid,the option buyer has no further obligation to the writer, unless the buyer decides toexercise the option. Therefore, the most that the buyer of an option can lose is the pre-mium paid. On the other hand, writers of options must always stand ready to fulfiltheir obligation to buy or sell the underlying asset. To provide evidence of their abilityto fulfil their obligation at all times, writers of exchange-traded options are required toprovide and maintain sufficient margin in their option accounts. Writers of OTCoptions typically do not have this requirement.

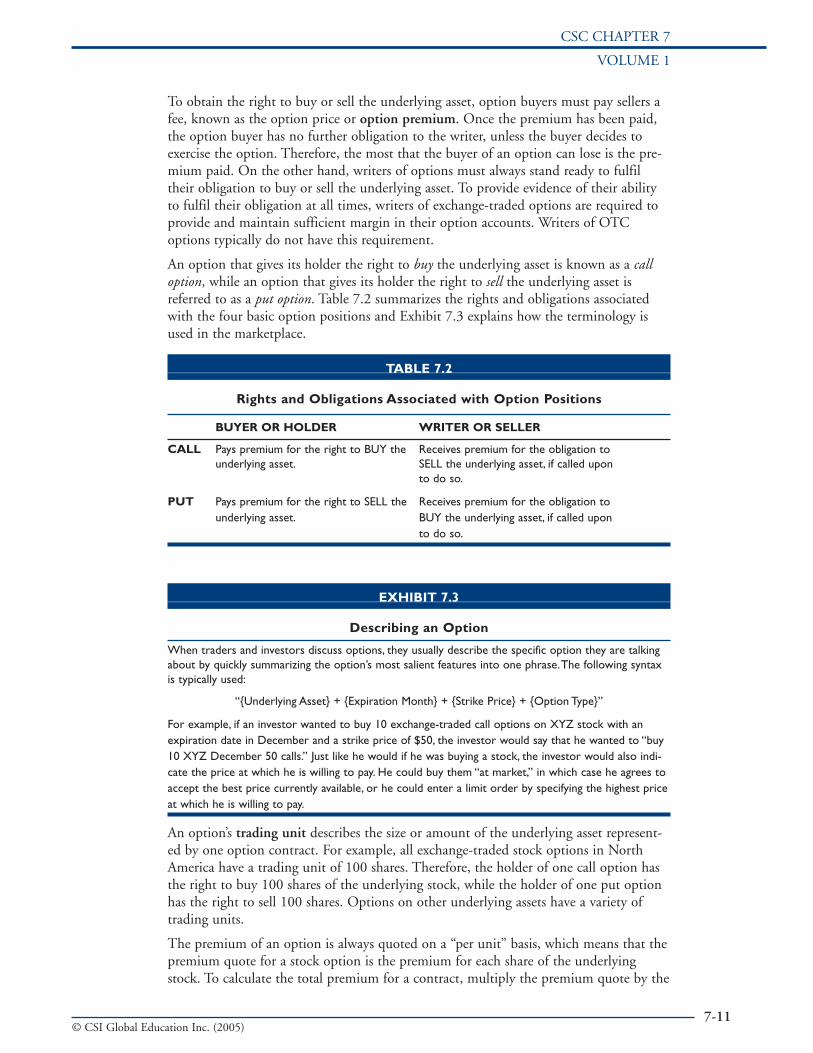

An option that gives its holder the right to buy the underlying asset is known as a calloption, while an option that gives its holder the right to sell the underlying asset isreferred to as a put option. Table 7.2 summarizes the rights and obligations associatedwith the four basic option positions and Exhibit 7.3 explains how the terminology isused in the marketplace.

TABLE 7.2

Rights and Obligations Associated with Option Positions

BUYER OR HOLDER WRITER OR SELLER

CALL Pays premium for the right to BUY the Receives premium for the obligation to underlying asset. SELL the underlying asset, if called upon

to do so.

PUT Pays premium for the right to SELL the Receives premium for the obligation tounderlying asset. BUY the underlying asset, if called upon

to do so.

EXHIBIT 7.3

Describing an Option

When traders and investors discuss options, they usually describe the specific option they are talkingabout by quickly summarizing the option’s most salient features into one phrase.The following syntaxis typically used:

“{Underlying Asset} + {Expiration Month} + {Strike Price} + {Option Type}”

For example, if an investor wanted to buy 10 exchange-traded call options on XYZ stock with anexpiration date in December and a strike price of $50, the investor would say that he wanted to “buy10 XYZ December 50 calls.” Just like he would if he was buying a stock, the investor would also indi-cate the price at which he is willing to pay. He could buy them “at market,” in which case he agrees toaccept the best price currently available, or he could enter a limit order by specifying the highest priceat which he is willing to pay.

An option’s trading unit describes the size or amount of the underlying asset represent-ed by one option contract. For example, all exchange-traded stock options in NorthAmerica have a trading unit of 100 shares. Therefore, the holder of one call option hasthe right to buy 100 shares of the underlying stock, while the holder of one put optionhas the right to sell 100 shares. Options on other underlying assets have a variety oftrading units.

The premium of an option is always quoted on a “per unit” basis, which means that thepremium quote for a stock option is the premium for each share of the underlyingstock. To calculate the total premium for a contract, multiply the premium quote by the

CSC CHAPTER 7

VOLUME 1

7-11© CSI Global Education Inc. (2005)

option’s trading unit. For example, if a stock option is quoted with a premium of $1, itwill cost the buyer $100 for each contract.

Options that can be exercised at any time up to and including the expiration date arereferred to as American-style options. If the option can be exercised only on the expira-tion date, it is referred to as a European-style option. All exchange-traded stock optionsin North American are American-style options. Most index options are European-styleoptions.

When an investor establishes a new position in an option contract, it is called an open-ing transaction. An opening buy transaction results in a long position in the option,while an opening sell transaction results in a short position in the option. On or beforean option’s expiration date, one of three things will happen to all long and short optionpositions.

1. Positions may be liquidated prior to expiration by way of an offsetting transaction,which, in effect, cancels the position. Offsetting a long position involves selling thesame type and number of contracts, while offsetting a short position involves buy-ing the same type and number of contracts.

Unless they are specifically designed to be transferable, OTC options can only beoffset through negotiations between the long and short parties. Exchange-tradedoptions, however, can be offset simply by an entering an offsetting order on theexchange on which the option trades.

2. The party holding the long position can exercise the option. When this happens,the party holding the short position is said to be assigned on the option. For theowners of call options, the act of exercising involves buying the underlying assetfrom the assigned writer at a price equal to the strike price. For the owners of putoptions, exercising involves selling the underlying asset to the assigned put writer ata price equal to the strike price.

3. The party holding the long position can let the option expire. Buyers of optionshave rights, not obligations. If they do not want to exercise their options beforethey expire, they do not have to; it is totally up to them.

Owners of options will exercise only if it is in their best financial interest, which canonly occur when an option is in-the-money.

• A call option is in-the-money when the price of the underlying asset is higher thanthe strike price. If this is the case, the call option holder can exercise the right tobuy the underlying asset at the strike price and then turn around and sell it at thehigher market price.

• A put option is in-the-money when the price of the underlying asset is lower thanthe strike price. If this is the case, the put option holder can exercise the right to sellthe underlying asset at the higher strike price, which would create a short position,and then cover the short position at the lower market price.

The in-the-money portion of a call or put option is referred to as the option’s intrinsicvalue. For example, if XYZ stock is trading at $60, a call option on XYZ stock with astrike price of $55 has $5 of intrinsic value. Similarly, a put option on XYZ with astrike price of $65 has $5 of intrinsic value.

Intrinsic Value of an In-the-Money Call Option = Price of Underlying – Strike Price

$5 = $60 - $55

Intrinsic Value of an In-the-Money Put Option = Strike Price – Price of Underlying

$5 = $65 - $60

Derivatives

7-12© CSI Global Education Inc. (2005)

If an option is not in-the-money, it has zero intrinsic value. For example, a call optionon XYZ with a $65 strike price has no intrinsic value, as does a put option with a strikeprice of $55.

Prior to the expiration date, most options trade for more than their intrinsic value. Theamount that an option is trading above its intrinsic value is known as the option’s timevalue.

For example, if a call option on XYZ with a strike price of $55 is trading for $6 whenXYZ stock is trading at $60, the option has $1 of time value.

Time Value of an Option = Option Price – Option’s Intrinsic Value

$1 = $6 - $5

If you re-arrange the equation for the time value of an option, you’ll see thatthe price of any option is simply the sum of its intrinsic and time values.

Option Price = Intrinsic Value + Time Value

Intrinsic value is a relatively easy concept to understand: it is the amount thatthe owner of an in-the-money option would earn by immediately exercising theoption and offsetting any resulting position in the underlying asset. Time value,on the other hand, is a more nebulous concept.

Simply put, time value represents the value of uncertainty. Option buyers wantoptions to be in-the-money at expiration; option writers want the reverse. Thegreater the uncertainty about where the option will be at expiration, either in-the-money or out-of-the-money, the greater the option’s time value.

Owners of options will definitely not exercise if they are out-of-the-money or at-the-money.

• A call option is out-of-the-money when the price of the underlying asset is lowerthan the strike price.

• A put option is out-of-the-money when the price of the underlying asset is higherthan the strike price.

• Call and put options are at-the-money when the price of the underlying assetequals the strike price.

In either of these cases, it is not in the financial best interest of an option holder to exer-cise. If a call option is out-of-the-money, it does not make financial sense for the calloption holder to buy the underlying asset at the strike price (by exercising the call)when it can be purchased at a lower price in the market. Similarly, if a put option isout-of-the-money, it does not make financial sense for the put option holder to sell theunderlying asset at the strike price (by exercising the put) when it can be sold at a high-er price in the market.

Since there is no advantage to exercising an at-the-money option (for which the strikeprice equals the market price of the underlying asset), at-the-money options are normal-ly left to expire worthless.

2. Option Exchanges

Options have been trading on organized exchanges since 1973, when the ChicagoBoard Options Exchange (CBOE) first opened for business. It listed options on individ-ual common stocks. Two innovations borrowed from the futures market, standardiza-tion and a clearing corporation’s guarantee against default, combined with an increasingawareness of the risk management potential of options, led to phenomenal growth inthe options market.

CSC CHAPTER 7

VOLUME 1

7-13© CSI Global Education Inc. (2005)

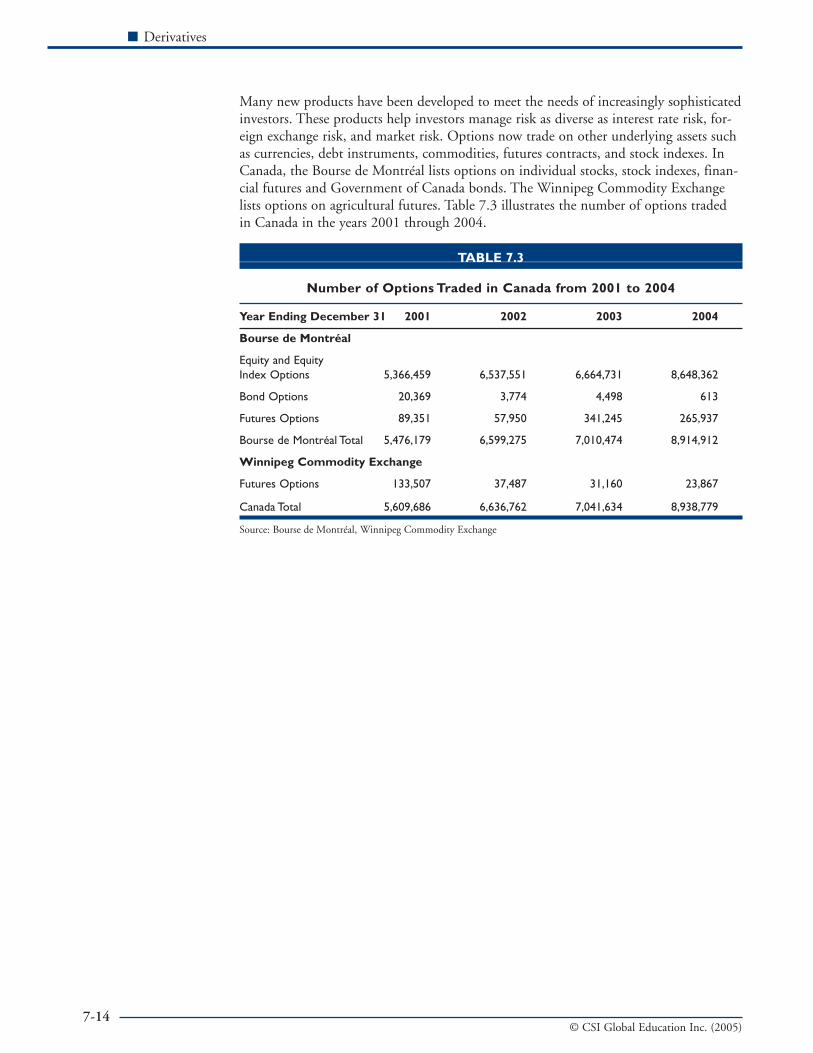

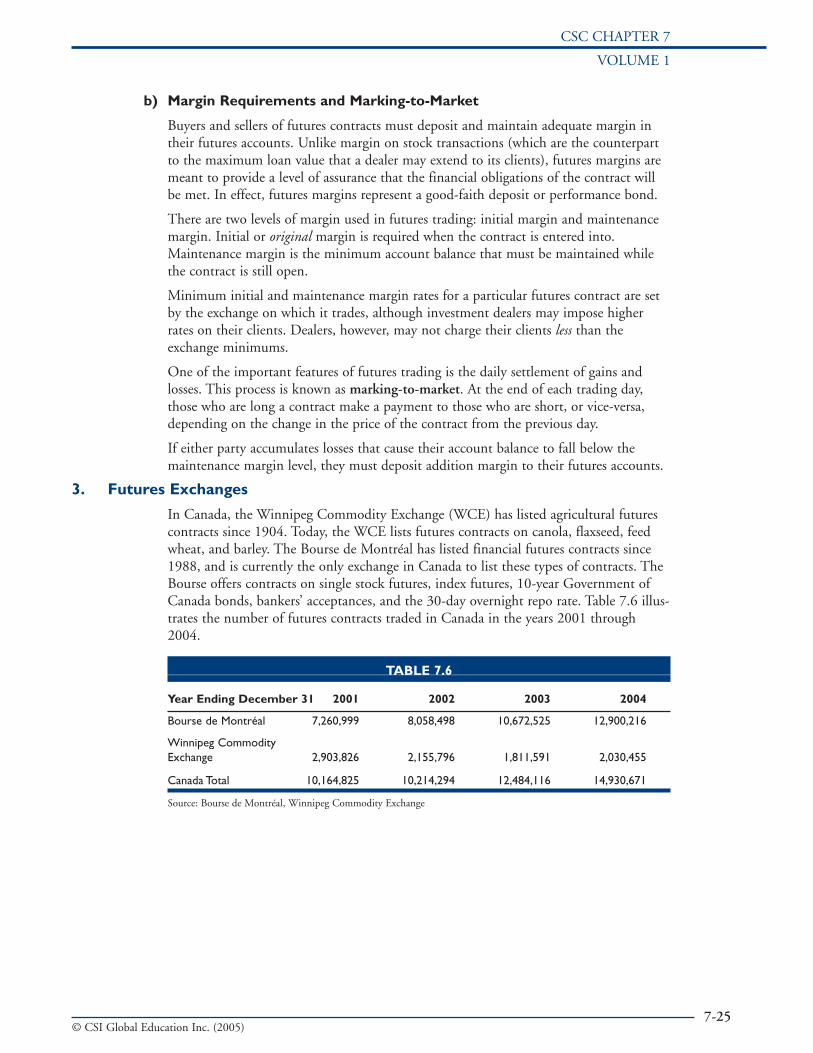

Many new products have been developed to meet the needs of increasingly sophisticatedinvestors. These products help investors manage risk as diverse as interest rate risk, for-eign exchange risk, and market risk. Options now trade on other underlying assets suchas currencies, debt instruments, commodities, futures contracts, and stock indexes. InCanada, the Bourse de Montréal lists options on individual stocks, stock indexes, finan-cial futures and Government of Canada bonds. The Winnipeg Commodity Exchangelists options on agricultural futures. Table 7.3 illustrates the number of options tradedin Canada in the years 2001 through 2004.

TABLE 7.3

Number of Options Traded in Canada from 2001 to 2004

Year Ending December 31 2001 2002 2003 2004

Bourse de Montréal

Equity and Equity Index Options 5,366,459 6,537,551 6,664,731 8,648,362

Bond Options 20,369 3,774 4,498 613

Futures Options 89,351 57,950 341,245 265,937

Bourse de Montréal Total 5,476,179 6,599,275 7,010,474 8,914,912

Winnipeg Commodity Exchange

Futures Options 133,507 37,487 31,160 23,867

Canada Total 5,609,686 6,636,762 7,041,634 8,938,779

Source: Bourse de Montréal, Winnipeg Commodity Exchange

Derivatives

7-14© CSI Global Education Inc. (2005)

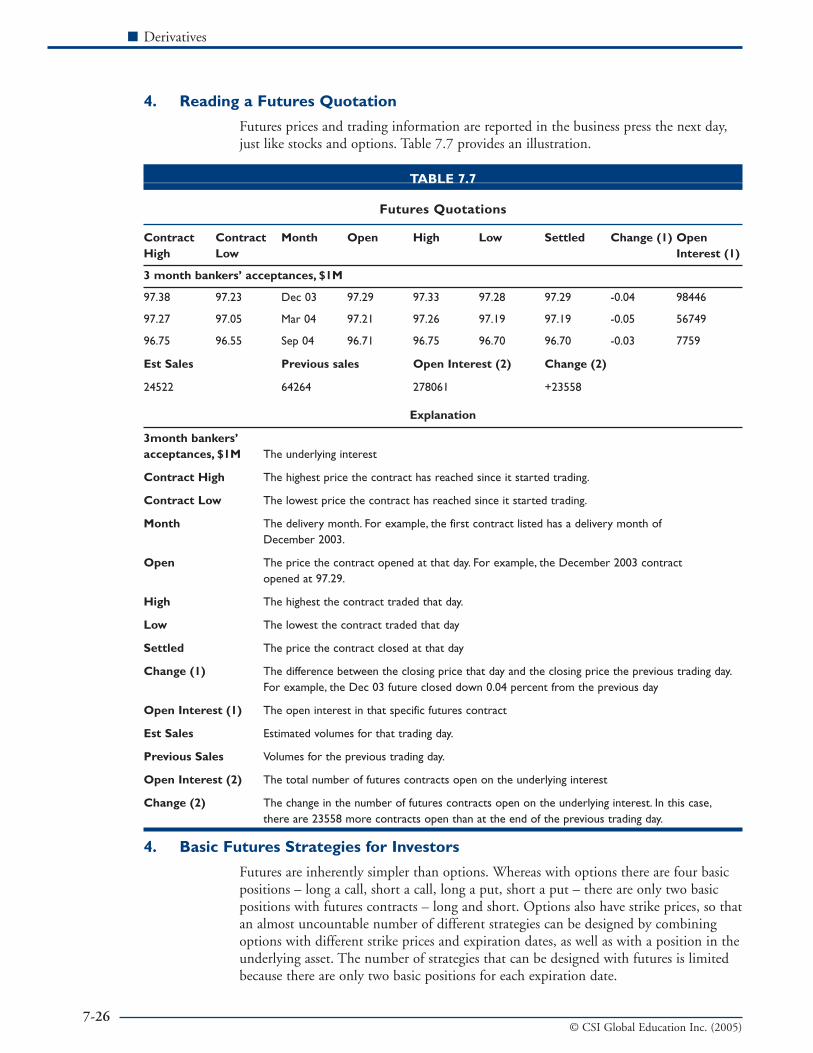

3. Reading an Options Quotation

Exchange-traded option prices and trading information are reported in the businesspress the next day, just like stocks. Table 7.4 provides an illustration.

TABLE 7.4

Equity Option Quotation

XYZ INC. 17¾ 319 10,404Bid Ask Last Opt Vol Op Int

Mar. $17.50 3.80 4.05 3.95 50 1595

$17.50P 2.35 2.60 2.40 5 3301

Sept. $17.50 1.10 1.35 1.25 41 3403

$17.50P .95 1.05 1.00 30 1058

Dec. $20.00P 1.85 2.00 1.90 193 1047

Explanation

XYZ INC.The underlying equity for the option.

17¾The closing market price of the underlying equity.

Opt Vol. The total trading day’s volume in all series of XYZ’s options (50 + 5 + 41 + 30 + 193 = 319).The trading volume for each series is listed in thecolumn below. For example, 50 XYZ March 17.50 calls were traded on the dayshown, representing 5,000 underlying XYZ (50 x 100).

Mar. The options’ expiration month (March, September, December)

$17.50 The exercise price of each series.

$17.50P The option is a put.

3.80 The closing bid price for each XYZ option expressed as a per share price.

4.05 The closing asked price for each XYZ option expressed as a per share price.

3.95 The last sale price (last premium traded) of an option contract for the dayexpressed as a per share price. For example, the 3.95 figure for the XYZ March17.50 calls is the last sale price for this series on the trading day in question.

Op Int The open interest – the total number of option contracts in the series that are currently outstanding and have not been closed out or exercised. For example, the figure 1595 refers to the open interest for the XYZ March 17.50 calls.The figure 10404 refers to the open interest of all series of XYZ options, including the series that did trade as well as the series that did not trade.

4. Basic Option Strategies for Individual and Institutional Investors

The range and complexity of options trading strategies are practically limitless.

This section illustrates and examines eight option strategies used by individual and insti-tutional investors. Each strategy will be either a speculative or risk management strategy,and each will be based on exchange-traded options on the shares of a fictitious compa-ny, XYZ Inc. It is important to note that these strategies and the majority of the resultsare equally applicable to options on any underlying asset.

All of the strategy discussions involve either a long or short position in an XYZ call orput option. Sometimes the option position will be the only part of the strategy, while inother cases the option position will be combined with a position or expected position inXYZ stock. There are other, more complex strategies that are commonly employed butthey are beyond the scope of this book.

CSC CHAPTER 7

VOLUME 1

7-15© CSI Global Education Inc. (2005)

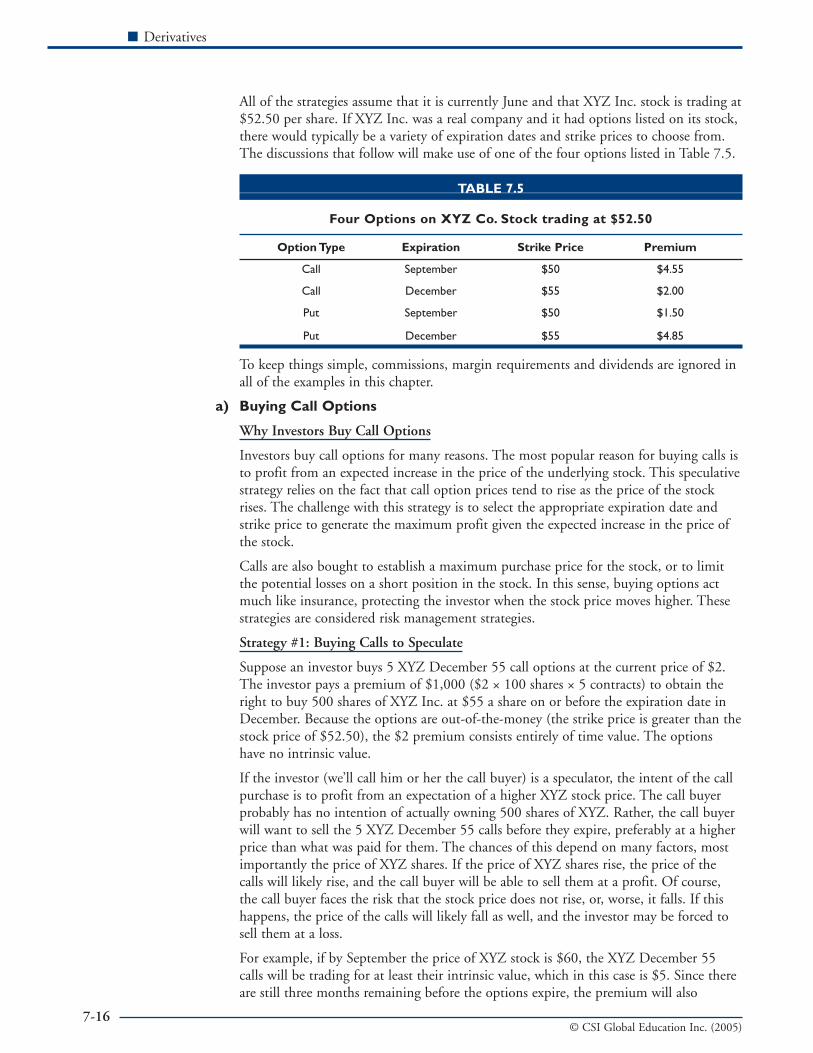

All of the strategies assume that it is currently June and that XYZ Inc. stock is trading at$52.50 per share. If XYZ Inc. was a real company and it had options listed on its stock,there would typically be a variety of expiration dates and strike prices to choose from.The discussions that follow will make use of one of the four options listed in Table 7.5.

TABLE 7.5

Four Options on XYZ Co. Stock trading at $52.50

Option Type Expiration Strike Price Premium

Call September $50 $4.55

Call December $55 $2.00

Put September $50 $1.50

Put December $55 $4.85

To keep things simple, commissions, margin requirements and dividends are ignored inall of the examples in this chapter.

a) Buying Call Options

Why Investors Buy Call Options

Investors buy call options for many reasons. The most popular reason for buying calls isto profit from an expected increase in the price of the underlying stock. This speculativestrategy relies on the fact that call option prices tend to rise as the price of the stockrises. The challenge with this strategy is to select the appropriate expiration date andstrike price to generate the maximum profit given the expected increase in the price ofthe stock.

Calls are also bought to establish a maximum purchase price for the stock, or to limitthe potential losses on a short position in the stock. In this sense, buying options actmuch like insurance, protecting the investor when the stock price moves higher. Thesestrategies are considered risk management strategies.

Strategy #1: Buying Calls to Speculate

Suppose an investor buys 5 XYZ December 55 call options at the current price of $2.The investor pays a premium of $1,000 ($2 × 100 shares × 5 contracts) to obtain theright to buy 500 shares of XYZ Inc. at $55 a share on or before the expiration date inDecember. Because the options are out-of-the-money (the strike price is greater than thestock price of $52.50), the $2 premium consists entirely of time value. The optionshave no intrinsic value.

If the investor (we’ll call him or her the call buyer) is a speculator, the intent of the callpurchase is to profit from an expectation of a higher XYZ stock price. The call buyerprobably has no intention of actually owning 500 shares of XYZ. Rather, the call buyerwill want to sell the 5 XYZ December 55 calls before they expire, preferably at a higherprice than what was paid for them. The chances of this depend on many factors, mostimportantly the price of XYZ shares. If the price of XYZ shares rise, the price of thecalls will likely rise, and the call buyer will be able to sell them at a profit. Of course,the call buyer faces the risk that the stock price does not rise, or, worse, it falls. If thishappens, the price of the calls will likely fall as well, and the investor may be forced tosell them at a loss.

For example, if by September the price of XYZ stock is $60, the XYZ December 55calls will be trading for at least their intrinsic value, which in this case is $5. Since thereare still three months remaining before the options expire, the premium will also

Derivatives

7-16© CSI Global Education Inc. (2005)

include some time value. Assuming the calls have $1.70 of time value, they will be trad-ing at $6.70. Therefore, the investor could choose to sell the options at $6.70 and real-ize a profit of $4.70 a share, equal to the difference between the current premiumminus the premium paid, or $2,350 total ($4.70 × 100 shares × 5 contracts).

If, however, XYZ shares are trading at $45 a share in September, the XYZ December 55calls might be worth only $0.25. At this time, and indeed, at all other times before expi-ration, the investor will have to decide whether to sell the options or hold on in thehope that the stock price (and the options’ price) recovers. If the investor decides to sellat this time, a loss equal to $1.75 a share, or $875 total ($1.75 × 100 shares × 5 con-tracts) will result.

The decision to sell prior to expiration is not an easy one. On the one hand, sellingbefore expiration allows the call buyer to earn any time value that remains built into theoption premium. On the other hand, the option buyer gives up any chance of reapingany further increases in the option’s intrinsic value. The call buyer’s outlook for the priceof the stock obviously plays a crucial role in the decision.

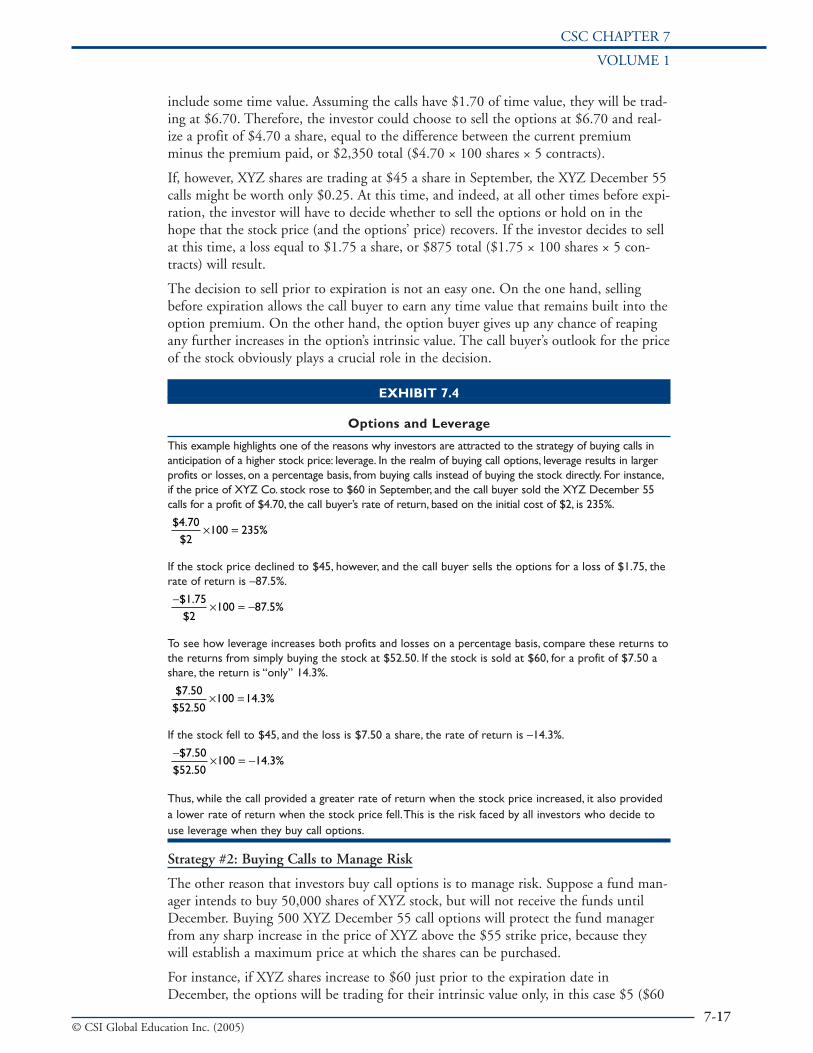

EXHIBIT 7.4

Options and Leverage

This example highlights one of the reasons why investors are attracted to the strategy of buying calls inanticipation of a higher stock price: leverage. In the realm of buying call options, leverage results in largerprofits or losses, on a percentage basis, from buying calls instead of buying the stock directly. For instance,if the price of XYZ Co. stock rose to $60 in September, and the call buyer sold the XYZ December 55calls for a profit of $4.70, the call buyer’s rate of return, based on the initial cost of $2, is 235%.

If the stock price declined to $45, however, and the call buyer sells the options for a loss of $1.75, therate of return is –87.5%.

To see how leverage increases both profits and losses on a percentage basis, compare these returns tothe returns from simply buying the stock at $52.50. If the stock is sold at $60, for a profit of $7.50 ashare, the return is “only” 14.3%.

If the stock fell to $45, and the loss is $7.50 a share, the rate of return is –14.3%.

Thus, while the call provided a greater rate of return when the stock price increased, it also provideda lower rate of return when the stock price fell.This is the risk faced by all investors who decide touse leverage when they buy call options.

Strategy #2: Buying Calls to Manage Risk

The other reason that investors buy call options is to manage risk. Suppose a fund man-ager intends to buy 50,000 shares of XYZ stock, but will not receive the funds untilDecember. Buying 500 XYZ December 55 call options will protect the fund managerfrom any sharp increase in the price of XYZ above the $55 strike price, because theywill establish a maximum price at which the shares can be purchased.

For instance, if XYZ shares increase to $60 just prior to the expiration date inDecember, the options will be trading for their intrinsic value only, in this case $5 ($60

−× = −

$ .$ .

. %7 50

52 50100 14 3

$ .$ .

. %7 5052 50

100 14 3× =

−× = −

$ .$

. %1 752

100 87 5

$ .$

%4 70

2100 235× =

CSC CHAPTER 7

VOLUME 1

7-17© CSI Global Education Inc. (2005)

– $55). Since the call buyer now has the money to buy the shares, the calls can be exer-cised, at which point the call buyer will purchase 50,000 shares of XYZ at the strikeprice of $55. Since the options originally cost $2, the call buyer’s net purchase price isactually $57 a share.

If, however, XYZ shares are trading at $45 just prior to the expiration date, the callbuyer will let the options expire and will buy the shares at the going price of $45 each.The investor’s effective cost is $47, which includes the $2 paid for the calls.

b) Writing Call Options

Why Investors Write Call Options

Investors write call options primarily for the income they provide. The income, in theform of the premium, is the writer’s to keep no matter what happens to the price of theunderlying asset or what the buyer eventually does. Call-writing strategies are primarilyspeculative in nature, but they can be used to manage risk as well.

Call option writers can be classified as either covered call writers or as naked call writ-ers. Covered call writers own the underlying stock, and will use this position to meettheir obligations if they are assigned. Naked call writers do not own the underlyingstock. If a naked call writer is assigned, the underlying stock must first be purchased inthe market before it can be sold to the call option buyer. Since call option buyers willonly exercise if the price of the stock is above the strike price, assigned naked call writersmust buy the stock at one price (the market price) and sell at a lower price (the strikeprice). Naked call writers hope, however, that this loss is less than the premium theyoriginally received, so that the overall result for the strategy is a profit.

Since all exchange-traded stock options have an American-style exercise feature, callwriters (and put option writers for that matter) face the risk of being assigned at anytime prior to expiration. That being said, prior to expiration most call buyers will find itmore advantageous to sell their options rather than exercise them because by selling theyreceive the option’s time value as well as its intrinsic value. Only the intrinsic value iscaptured when an option is exercised. So the chance of being assigned before expirationis not as great as one might think. But it does happen, particularly when the time valueis small, and option writers must be aware of this.

Strategy #1: Covered Call Writing

Suppose an investor writes 10 XYZ September 50 call options at the current price of$4.55. The investor receives a premium of $4,550 ($4.55 × 100 shares × 10 contracts)to take on the obligation of selling 1,000 shares of XYZ Inc. at $50 a share on or beforethe expiration date in September. Because the options are in-the-money (the strike priceis less than the stock price), the $4.55 premium consists of both intrinsic and timevalue. Intrinsic value is equal to $2.50 and time value is equal to $2.05.

If the investor already owned (or purchased at the same time as the options were writ-ten) 1,000 shares of XYZ, the overall position is known as a covered call. (We’ll call thisinvestor the covered call writer.) If at expiration in September the price of XYZ stock isgreater than $50 (i.e., the options are in-the-money), the covered call writer will beassigned and will have to sell the stock to the call buyer at $50 a share. From the cov-ered call writer’s perspective, however, the effective sale price is $54.55, because of theinitial premium of $4.55.

If, however, the price of the stock at expiration in September is less than $50, the cov-ered call writer will not be assigned and the options will expire worthless. Call buyerswill not elect to buy the stock at $50 when it can be purchased for less in the market.The covered call writer will retain the shares and the initial premium. In this case, the

Derivatives

7-18© CSI Global Education Inc. (2005)

premium reduces the covered call writer’s effective stock purchase price by $4.55 ashare. That is, if the covered call writer bought the XYZ stock at, say, $50, and theoptions expired worthless, the covered call writer’s effective purchase price is now$45.45 ($50 – $4.55). In this sense, writing the call slightly reduces the risk of owningthe stock.

Strategy # 2: Naked Call Writing

Suppose a different investor writes 10 XYZ September 50 call options at the currentprice of $4.55. If this investor did not already own the shares, the investor is considereda naked call writer (and that’s what we’ll call him or her). The best that the naked callwriter can hope for is that the price of XYZ stock will be lower than $50 at expiration.If this happens, the calls will expire worthless and the naked call writer will earn a profitequal to $4.55 a share, the initial premium received. This is the most that the call writercan expect to earn from this strategy.

If the price of the shares increase, the naked call writer will realize a loss if the stockprice is higher than the strike price plus the premium received, in this case $54.55. Ifthis happens, the naked call writer will be forced to buy the stock at the higher marketprice and then turn around and sell them to the call buyer at the $50 strike price.When the stock price is greater than $54.55, the cost of buying the stock is greater thanthe combined proceeds from selling the stock and the premium initially received.

For example, if the price of the XYZ rose to $60 at expiration, the naked call writer willsuffer a $10 loss on the purchase and sale of the shares (buy at $60, sell at $50). Thisloss is offset somewhat by the initial premium of $4.55, so that the actual loss is $5.45 ashare, or $5,450 in total ($5.45 × 100 shares × 10 contracts).

c) Buying Put Options

Why Investors Buy Put Options

Investors buy put options for many reasons. A popular reason for buying puts is to prof-it from an expected decline in the price of the stock. This speculative strategy relies onthe fact that put option prices tend to rise as the price of the stock falls. Just like buyingcalls, the selection of an expiration date and strike price are crucial to the success of (orlack thereof ) the strategy.

Puts are also bought for risk management purposes. Because puts can be used to lock ina minimum selling price for a stock, they are very popular with investors who ownstock. Buying puts can protect investors from a decline in the price of a stock below thestrike price.

Strategy #1: Buying Puts to Speculate

Suppose an investor buys 10 XYZ September 50 put options at the current price of$1.50. The put buyer pays a premium of $1,500 ($1.50 × 100 shares × 10 contracts) toobtain the right to sell 1,000 shares of XYZ Inc. at $50 a share on or before the expira-tion date in September. Because the options are out-of-the-money (the strike price isless than the stock price), the $1.50 premium consists entirely of time value. The optionhas no intrinsic value.

The put buyer could have an opinion about the price of XYZ stock exactly oppositethat of the call buyer. That is, the put buyer might believe that the price of XYZ stockwill fall and that put options on XYZ can be bought and sold for a profit. The putbuyer might have no intention of actually selling 1,000 shares of XYZ stock. In fact, theput buyer in this case probably doesn’t even own 1,000 XYZ shares to sell.

CSC CHAPTER 7

VOLUME 1

7-19© CSI Global Education Inc. (2005)

If the stock price falls, the XYZ September 50 put options will likely rise in value. Thiswill allow the put buyer to sell his options for a profit. Of course, if the stock price rises,the put options will most likely lose value and the put buyer may be forced to sell theoptions at a loss.

For example, if XYZ stock is trading at $45 one month before the September expirationdate, the XYZ September 50 puts will be trading for at least their intrinsic value, or $5.Since there is still one month before the expiration date, the options will have sometime value as well. Assuming they have time value of $0.25, the options will be tradingat $5.25. Therefore, the put buyer could choose to sell the puts for $5.25 and realize aprofit of $3.75 a share, which is equal to the difference between the current put priceand the put buyer’s original purchase price. Based on 10 contracts, the put buyer’s totalprofit is $3,750 ($3.75 × 100 shares × 10 contracts).

If, however, XYZ were trading at $60 a share, the XYZ September 50 puts might beworth only $0.05. Because the options are so far out-of-the-money, and because there isonly one month left until the options expire, the options will not have a lot of timevalue. The low option price tells us the market does not believe there is much of achance for XYZ shares to fall below $50 anytime over the next month.

The put buyer would have to decide whether to sell the options at this price, or hold onin hope that the price of XYZ does fall to below $50. If the stock does fall, the price ofputs will rise. If the stock doesn’t fall below $50, the puts will be worthless when theyexpire. If the put buyer decides to sell the options at $0.05, a loss equal to $1.45 a share($0.05 – $1.50), or $1,450 total ($1.45 × 100 shares × 10 contracts) would result.

Strategy #2: Buying Puts to Manage Risk

Suppose a different investor buys 10 XYZ September 50 put options at the current priceof $1.50, but in this case the put buyer actually owns 1,000 shares of XYZ. In this casethe put purchase will act as insurance against a drop in the price of the stock. Recallthat put buyers have the right to sell the stock at the strike price. Therefore, buying aput in conjunction with owning the stock, a strategy known as a married put or a puthedge, gives the put buyer the right to sell the stock at the strike price. If the price ofthe stock is below the strike price of the put when the puts expire, the put buyer willmost likely exercise the puts and sell the stock to the put writer. The strike price acts asa floor price for the sale of the stock.

For example, if XYZ shares are trading at $45 just prior to the expiration date inSeptember, the puts will be trading very close to their intrinsic value of $5, because theputs are in-the-money and there is very little time left until the expiration date. The putbuyer may choose to exercise the puts and sell the stock at the $50 strike price. The putbuyer has been protected from the drop in the stock price below $50. The protectionwas not free, however, because the put buyer had to pay $1.50 for the puts. The putbuyer’s effective sale price is actually only $48.50, after deducting the cost of the puts.But this sale price is still better than the stock’s $45 market price.

The put buyer, for whatever reason, may not want or even be able to sell the stock. Ifso, the puts should be sold. Any profit on the sale of the puts reduces the put buyer’seffective stock purchase price. If the put buyer originally bought the stock at a price of,say, $40, and then sold the puts at $5, for a net profit of $3.50, the effective stock pur-chase price becomes $36.50. Eventually, when the shares are sold, the put buyer willmeasure the total profit on the stock purchase as the difference between the sale priceand the effective purchase price of $36.50.

Derivatives

7-20© CSI Global Education Inc. (2005)

d) Writing Put Options

Why Investors Write Put Options

Investors write put options primarily for the income they provide. The income, in theform of the premium, is the writer’s to keep no matter what happens to the price of theunderlying asset or what the buyer eventually does. Like their call-writing cousins, put-writing strategies are primarily speculative in nature, but they can be used to managerisk as well.

Put option writers can be classified as either covered or naked. Covered put writing,however, is not nearly as common as covered call writing because, technically, a coveredput write combines a short put with a short position in the stock. It’s a simple fact of thestock markets that there are many more long positions in stocks than there are shortpositions.

A more common, “nearly” covered put writing strategy is known as a cash-secured putwrite. A cash-secured put write involves writing a put and setting aside an amount ofcash equal to the strike price. If possible, the cash should be invested in a short-term,liquid money market security such as a Treasury bill so that it will earn some interest. Ifthe cash-secured put writer is assigned, the cash (or proceeds from selling the T-bill) willbe used to buy the stock from the exercising put buyer.

Naked put writers have no position in the stock and have not specifically earmarked anamount of cash to buy the stock. That being said, naked put writers must be preparedto buy the stock, so they should always have the financial resources to do so. Naked putwriters hope to profit from a stock price that stays the same or goes up. If this happens,the price of the puts will likely decline as well, and the chance of being assigned willalso be less. The naked put writer may then choose to buy back the options at the lowerprice to realize a profit. If the stock price does not rise, the put writer may be assigned,and may suffer a loss. Depending on how low the stock price is and the amount of pre-mium received, naked put writers may still profit even if they are assigned.

Strategy # 1: Cash-Secured Put Writing

Suppose an investor writes 5 XYZ December 55 put options at the current price of$4.85. The put writer receives a premium of $2,425 ($4.85 × 100 shares × 5 contracts)to take on the obligation of buying 500 shares of XYZ Inc. at $55 a share on or beforethe expiration date in December. Because the options are in-the-money (the strike priceis greater than the stock price), the $4.85 premium consists of both intrinsic value andtime value. Intrinsic value is equal to $2.50 and time value is equal to $2.35.

If the put writer had set aside an amount of cash equal to the purchase value of thestock, the strategy is known as a cash-secured put write. The put writer in this casewould have to set aside $27,500 ($55 strike price × 100 shares × 5 contracts).

Some investors actually use cash-secured put writes as a way to buy the stock at an effec-tive price that is lower than the current market price. The effective price is equal to thestrike price minus the premium received.

For example, if at expiration in December the price of XYZ stock is less than $55, theput writer will be assigned and will have to buy 500 shares of XYZ at the strike price of$55 a share. The effective purchase price is actually $50.15, because the put writerreceived a premium of $4.85 when the options were written. This effective purchaseprice is less than the $52.50 price of the stock when the cash-secured put write wasestablished.

If at expiration in December the price of XYZ stock is greater than $55, the cash-secured put writer will not be assigned because the options are out-of-the-money. The

CSC CHAPTER 7

VOLUME 1

7-21© CSI Global Education Inc. (2005)

cash-secured put writer, however, gets to keep the premium of $4.85, and will have todecide whether to use the cash to buy the stock at the market price.

Strategy #2: Naked Put Writing

Suppose a different investor writes 5 XYZ December 55 put options at the current priceof $4.85. If the put writer does not set aside a specific amount of cash to cover thepotential purchase of the stock, the put writer is considered a naked put writer. Thenaked put writer wants the price of XYZ to be higher than $55 at expiration. If thishappens, the puts will expire worthless and the put writer will earn a profit equal to$4.85 a share, the initial premium received.

If the price of XYZ stock falls, however, the naked put writer will most likely realize aloss, because put buyers will exercise their options to sell the stock at the higher strikeprice. (The naked put writer in this case will suffer a loss only if XYZ stock is tradingfor less than $50.15 at option expiration.) The naked put writer will have to buy stockat a price that is higher than the market price. If the put writer did not want to hold theshares in anticipation of a higher price, they could be sold.

For example, if the price of XYZ fell to $45 at expiration, the naked put writer will suf-fer a $10 loss on the purchase and sale of the shares (buy at the strike price of $55, sellat the market price of $45). This loss is offset somewhat by the initial premium of$4.85, so that the actual loss is $5.15 a share, or $2,575 in total ($5.15 × 100 shares × 5contracts).

5. Basic Option Strategies for Corporations

Unlike individual and institutional investors, corporations do not normally speculatewith derivatives. They’re just not interested in risking their shareholders’ money bettingon the price of an underlying asset. They are, however, interested in managing risk, andthey often use options to do so. The risks that corporations most often manage are relat-ed to interest rates, exchange rates, or commodity prices. For instance, corporations reg-ularly take on debt to help finance their operations. Sometimes the interest rate on thedebt is a floating rate that rises and falls with market interest rates. Just like the investorwho buys a call to establish a maximum purchase price for a stock, corporations can buya call to establish a maximum interest rate on floating-rate debt.

a) Call Option Strategies

Suppose a Canadian company knows it will buy US$1 million worth of goods from aU.S. supplier in three months time. Based on the current exchange rate of C$1.42 perU.S. dollar, the U.S. dollar purchase will cost the company C$1.42 million. The com-pany can do two things to secure the US$1 million: buy it now and pay C$1.42 mil-lion, or wait three months and pay whatever the exchange rate is at that time. The com-pany would prefer to do the latter and wait, but by doing this, it faces the risk that thevalue of the U.S. dollar will strengthen relative to the Canadian dollar. This would causethe Canadian dollar cost of the purchase to be higher than C$1.42 million. To protectitself against this risk, the corporation can buy a call option on the U.S. dollar.

Suppose the corporation buys a three-month U.S. dollar call option with a strike priceof C$1.45. This option is an OTC option and would most likely be written by the cor-poration’s bank. If at the end of three months the exchange turns out to be C$1.50, thecorporation will exercise the call and buy the U.S. dollars from its bank for C$1.45 mil-lion. If, however, the U.S. dollar weakens so that in three months the exchange rate isC$1.40, the corporation will let the option expire and will buy the U.S. dollars at thelower exchange rate. The purchase of the call option has capped the exchange rate atC$1.45 plus the cost of the option.

Derivatives

7-22© CSI Global Education Inc. (2005)

b) Put Option Strategies

Suppose a Canadian oil company will have 1 million barrels of crude oil to sell in sixmonths time. The current price of crude oil is US$25 a barrel, but the company is notsure what the price will be in six months. To lock in a minimum sale price, the compa-ny buys a put option on 1 million barrels of crude oil with a strike price of US$23 abarrel. This will protect the company from an oil price lower than US$23 a barrel.

If in six months the price of crude oil is less than US$23, the company will exercise itsput option and sell the oil to the put option writer at the strike price. If the price isgreater than US$23, the company will let the option expire and will sell the oil at thegoing market price.

F. FORWARDSA forward is a contract between two parties: a buyer and a seller. The buyer of a forwardagrees to buy the underlying asset from the seller on a future date at a price agreed upontoday. Unlike options, both parties are obligated to participate in the future trade.

Forwards can trade on an exchange or over the counter. When a forward is traded on anexchange, it is known as a futures contract. Futures are usually classified into twogroups depending on the type of underlying asset. Contracts that have a financial asset— a stock, bond, currency, interest rate or index — as the underlying asset are referredto as financial futures. Contracts that have a physical asset (such as gold, crude oil, soy-beans, and more) as the underlying asset are known as commodity futures.

When a forward is traded over the counter, it is generally referred to as a forward agree-ment. The predominant types of forward agreements are based on interest rates and cur-rencies. Forward agreements on commodities exist, but the size of trading in these con-tracts is small compared to trading in interest rate and currency forwards.

Sometimes an OTC forward agreement will involve a series of cash flows exchangedbetween two parties on specified future dates. This type of contract is known as a swap.Swaps are used extensively by large corporations and financial institutions to help man-age their exposure to certain types of currency and interest rate risk.

For example, Company A has a $10 million loan outstanding on which it pays a float-ing rate of interest. When interest rates rise, Company A’s interest payments go up.Company A can transform this loan into a fixed-rate loan by entering into an interestrate swap. Such a swap might require Company A to pay Company B a fixed rate ofinterest (based on a $10 million amount) in exchange for Company B paying CompanyA a floating rate of interest (based on the same $10 million amount). By entering intothis interest rate swap, Company A has effectively transformed its $10-million floating-rate loan into a $10-million fixed-rate loan. Readers who are interested in learning moreabout swaps are encouraged to enroll in CSI’s Derivatives Fundamentals Course.

While forwards are certainly an interesting topic on which much can be said, the mar-ket is dominated by institutional traders and large corporations, not investment advisorsand individual investors. Futures, on the other hand, are accessible to a much broadersegment of the market, including investment advisors and individual investors. Theremainder of this section will focus on the key features of futures and some basic futuresstrategies.

CSC CHAPTER 7

VOLUME 1

7-23© CSI Global Education Inc. (2005)

1. Futures: Key Terms and Definitions

Futures are simply exchange-traded forward contracts, and as such they have many ofthe features inherent to all forward contracts. They are agreements between two partiesto buy or sell an underlying asset at some future point in time at a predetermined price.Like all exchange-traded derivatives, futures are standardized with respect to the amountof the asset underlying each contract, expiration dates, and delivery locations. There isno single expiration date for the different futures contracts available. For example,futures on the S&P/TSX 60 Index expire on the third Friday of the contract month,while futures on 10-year Government of Canada bonds expire on the third business daybefore the last business day of the month. As is the case with exchange-traded options,the expiration date is set by the exchange on which the contract is listed.

Many commodity futures require additional standardization for things such as the qualityof the underlying asset and the delivery location. As usual, standardization allows users tooffset their contracts prior to expiration and provides the backing of a clearinghouse.