CRTs Are Back (in Four Delicious Flavors)...donors to defer what might be a large tax liability in...

12

Paul S. Lee, far left, is national managing director and Stephen S. Schilling is director of the wealth planning and analysis group, both at Bernstein Global Wealth Management in New York City T he modern versions of charitable remainder trusts (CRTs) have been in existence for almost 45 years, and although various restrictions have been imposed on CRTs to curtail perceived abuses, 1 they remain important charitable giving vehicles that enable donors to have the satisfaction of providing for charity today (for inter vivos gifts) but retain some economic benefits that reduce the cost of being a philanthropist. Those benefits include the receipt of partial tax deduc- tions, diversification of highly appreciated assets in a tax-exempt environment and the retention of an annual stream of payments from the trust. With higher income tax rates and a capital market environment predomi- nated by extremely low interest rates, CRTs will be more popular than they’ve been in over a decade. CRTs can be attractive and flexible, even when the contributed asset is illiquid and not of the type that’s commonly contributed to a charitable trust. Practitioners need to consider the technical and practical issues when donors are contrib- uting four different types of assets: (1) publicly traded stock; (2) artwork (or other collectibles); (3) commercial real property interests; and (4) individual retirement account (or other qualified retirement) assets. Each asset is treated differently under the Internal Revenue Code, and each poses different planning issues and challenges. CRTs Today Income tax rates for individuals have risen significantly with the enactment of the American Taxpayer Relief Act of 2012 2 and the imposition of the 3.8 percent net investment income tax (NIIT). 3 Today, the top tax rates on ordinary income and long-term capital gains (LTCGs) (including the NIIT) are 43.4 percent and 23.8 percent, respectively. In addition, the federal tax rates are more progressive than they’ve been in recent years. For joint filers, the highest income tax rates come into effect when taxable income exceeds $457,500, and the NIIT is applied when modified adjusted gross income exceeds $250,000. 4 As such, significant tax sav- ings may be captured if taxpayers can take advantage of “running the brackets” by having the income taxed at the lower rates. These savings can be accomplished by having taxable income paid over several taxable years. For joint filers, the annual federal tax savings today are as high as $53,247 on ordinary income and $36,070 on LTCGs. 5 For very high income tax states like California, running the brackets on LTCGs can save as much as $79,512 each year. 6 Although CRTs are tax-exempt, the distributions to the non-charitable beneficiary aren’t. The final Treasury regulations issued in 2013 make clear that CRTs are exempt from the NIIT, 7 but the distributions to the non-charitable beneficiary retain their character as net investment income (NII); thus, they’re possibly taxable to the recipient. 8 The distributions are taxed pursuant to the “category and class tier rules” of accounting. 9 Pursuant to these rules, all of the CRT’s income is first divided into three categories of income: ordinary, capital gains and other (excluded). 10 Then, within each category, the income is further subdivided into different classes based on the federal income tax rate applicable to the income, beginning with the class of income with the highest federal income tax rate (including items that would be subject to the NIIT) 11 and ending with the class of income with the lowest tax rate. 12 When a dis- tribution is made to the non-charitable beneficiary, the CRTs Are Back (in Four Delicious Flavors) Consider the practical and technical issues for different types of asset classes By Paul S. Lee & Stephen S. Schilling O CTOBER 2014 TRUSTS & ESTATES / trustsandestates.com 31 SPECIAL EDITION: CHARITABLE GIVING

Transcript of CRTs Are Back (in Four Delicious Flavors)...donors to defer what might be a large tax liability in...

Paul S. Lee, far left, is national managing director

and Stephen S. Schilling is

director of the wealth planning

and analysis group, both at

Bernstein Global Wealth

Management in New York City

T he modern versions of charitable remainder trusts (CRTs) have been in existence for almost 45 years, and although various restrictions have

been imposed on CRTs to curtail perceived abuses,1 they remain important charitable giving vehicles that enable donors to have the satisfaction of providing for charity today (for inter vivos gifts) but retain some economic benefits that reduce the cost of being a philanthropist. Those benefits include the receipt of partial tax deduc-tions, diversification of highly appreciated assets in a tax-exempt environment and the retention of an annual stream of payments from the trust. With higher income tax rates and a capital market environment predomi-nated by extremely low interest rates, CRTs will be more popular than they’ve been in over a decade. CRTs can be attractive and flexible, even when the contributed asset is illiquid and not of the type that’s commonly contributed to a charitable trust. Practitioners need to consider the technical and practical issues when donors are contrib-uting four different types of assets: (1) publicly traded stock; (2) artwork (or other collectibles); (3) commercial real property interests; and (4) individual retirement account (or other qualified retirement) assets. Each asset is treated differently under the Internal Revenue Code, and each poses different planning issues and challenges.

CRTs TodayIncome tax rates for individuals have risen significantly with the enactment of the American Taxpayer Relief

Act of 20122 and the imposition of the 3.8 percent net investment income tax (NIIT).3 Today, the top tax rates on ordinary income and long-term capital gains (LTCGs) (including the NIIT) are 43.4 percent and 23.8 percent, respectively. In addition, the federal tax rates are more progressive than they’ve been in recent years. For joint filers, the highest income tax rates come into effect when taxable income exceeds $457,500, and the NIIT is applied when modified adjusted gross income exceeds $250,000.4 As such, significant tax sav-ings may be captured if taxpayers can take advantage of “running the brackets” by having the income taxed at the lower rates. These savings can be accomplished by having taxable income paid over several taxable years. For joint filers, the annual federal tax savings today are as high as $53,247 on ordinary income and $36,070 on LTCGs.5 For very high income tax states like California, running the brackets on LTCGs can save as much as $79,512 each year.6

Although CRTs are tax-exempt, the distributions to the non-charitable beneficiary aren’t. The final Treasury regulations issued in 2013 make clear that CRTs are exempt from the NIIT,7 but the distributions to the non-charitable beneficiary retain their character as net investment income (NII); thus, they’re possibly taxable to the recipient.8 The distributions are taxed pursuant to the “category and class tier rules” of accounting.9 Pursuant to these rules, all of the CRT’s income is first divided into three categories of income: ordinary, capital gains and other (excluded).10 Then, within each category, the income is further subdivided into different classes based on the federal income tax rate applicable to the income, beginning with the class of income with the highest federal income tax rate (including items that would be subject to the NIIT)11 and ending with the class of income with the lowest tax rate.12 When a dis-tribution is made to the non-charitable beneficiary, the

CRTs Are Back (in Four Delicious Flavors)Consider the practical and technical issues for different types of asset classes

By Paul S. Lee & Stephen S. Schilling

oCToBeR 2014 TRusTs & esTATes / trustsandestates.com 31

SPeciaL ediTion: ChaRiTaBle GiviNG

rboyd

Typewritten Text

Bernstein does not provide tax, legal or accounting advice.

rboyd

Typewritten Text

robertboyd

Typewritten Text

robertboyd

Typewritten Text

robertboyd

Typewritten Text

landwehrma

Cross-Out

distribution is deemed to come from the ordinary income category first (with higher taxed ordinary income having priority over lower taxed ordinary income) until its exhaustion, followed by capital gains, then other income and finally trust corpus.13 Essentially, the CRT tier rules create a historical accounting of the taxable events that occur within the CRT’s tax-exempt structure. The income is then taxed when and if it’s distributed to the non-charitable beneficiary, but the calculation of any taxes payable are determined at the beneficiary level. In other words, the tier rules allow donors to defer what might be a large tax liability in

one taxable year (a sale of highly appreciated property, for example) and spread it over the term of the CRT as distributions are made. Thus, in addition to providing for charity and creating an initial income tax deduction, CRTs are powerful tax deferral vehicles and can provide tax savings to the donor14 by running the brackets each year on the original gain.

Today’s capital market environment is character-ized by extremely low interest rates, as reflected in the current IRC Section 7520 rate of 2.2 percent.15 The long-term average for the rate is 5.8 percent.16 This low interest rate environment has two significant effects on CRT planning. Because: (1) the annuity or unitrust amount must be at least 5 percent,17 (2) the actuarial value of the charitable remainder interest must be at least 10 percent,18 and (3) charitable remainder annuity trusts (CRATs) must satisfy the exhaustion rules,19 life-time term CRATs are only available to donors who are

over age 70. In contrast, charitable remainder unitrusts (CRUTs) are viable even for donors who are as young as age 28. Because most CRTs have lifetime terms (as opposed to terms of years), we’ll only discuss lifetime term CRUTs. On the flip slide, the low interest rate environment makes CRUTs attractive from a return on investment standpoint. Some donors view CRUTs as a way of pre-funding a testamentary charitable gift but retaining a lifetime annuity in the form of a unitrust (5 percent or more of the value of the trust).

Case Studies’ assumptionsWe’ve prepared a series of case studies to illustrate the result of CRUTs funded with the four asset types men-tioned above and have forecasted the likely results based on different unitrust percentages and time frames.20 In each of the case studies, unless stated otherwise, the donors contribute to the CRUT an asset that’s worth $10 million with a zero tax basis. The trustee sells the asset in the CRUT and reinvests the proceeds in globally diversified equities.21 The donors are both age 65, mar-ried and residents of California. The trust is a lifetime term CRUT that pays until the death of the survivor. Accordingly, we made projections based on the donors retaining a 5 percent (minimum), 8 percent or 11.2 per-cent (maximum) unitrust percentage,22 with any result-ing income tax deduction sheltering LTCGs in the year of contribution. All of the wealth values are expressed after inflation and after state and federal income taxes.

Publicly Traded StocksOne of the economic benefits of making a contribution to a CRT is that the donor may be entitled to a charitable income tax deduction equal to the present value of the remainder interest.23 The resulting deduction is a func-tion of a number of factors including the Section 7520 rate, ages of the non-charitable beneficiaries, unitrust percentage retained and fair market value (FMV) of the asset contributed to the CRUT. When a donor contrib-utes highly appreciated stock to a CRUT, whether the donor will be able to calculate the resulting income tax deduction against the FMV of the stock, rather than cost basis, depends on the type of charitable organization that will receive the remainder interest. If the organization is a publicly supported charity, the income tax deduction will be calculated against the FMV of the stock. If the

32 TRusTs & esTATes / trustsandestates.com oCToBeR 2014

SPeciaL ediTion: ChaRiTaBle GiviNG

One of the economic benefits of

making a contribution to a CRT is

that the donor may be entitled to

a charitable income tax deduction

equal to the present value of the

remainder interest.

landwehrma

Cross-Out

organization isn’t a public charity (for example, a private foundation (PF)), then the tax deduction will be based on the cost basis of the stock, unless the stock is “quali-fied appreciated stock” under IRC Section 170(e)(5).24

To be qualified appreciated stock, the stock in ques-tion must be traded on an established securities market, and quotations must be readily available for the stock.25

As such, stock subject to trading restrictions won’t qual-ify for this exception.26 In addition, the qualified appreci-ated stock exception is only available for contributions made by the donor (and family members, including siblings, spouses, ancestors and lineal descendants) that,

in aggregate, are 10 percent or less of the outstanding stock of the corporation.27 Because there’s no time limita-tion on this 10 percent restriction, practitioners should inquire about previous contributions that the donor and family members have made.

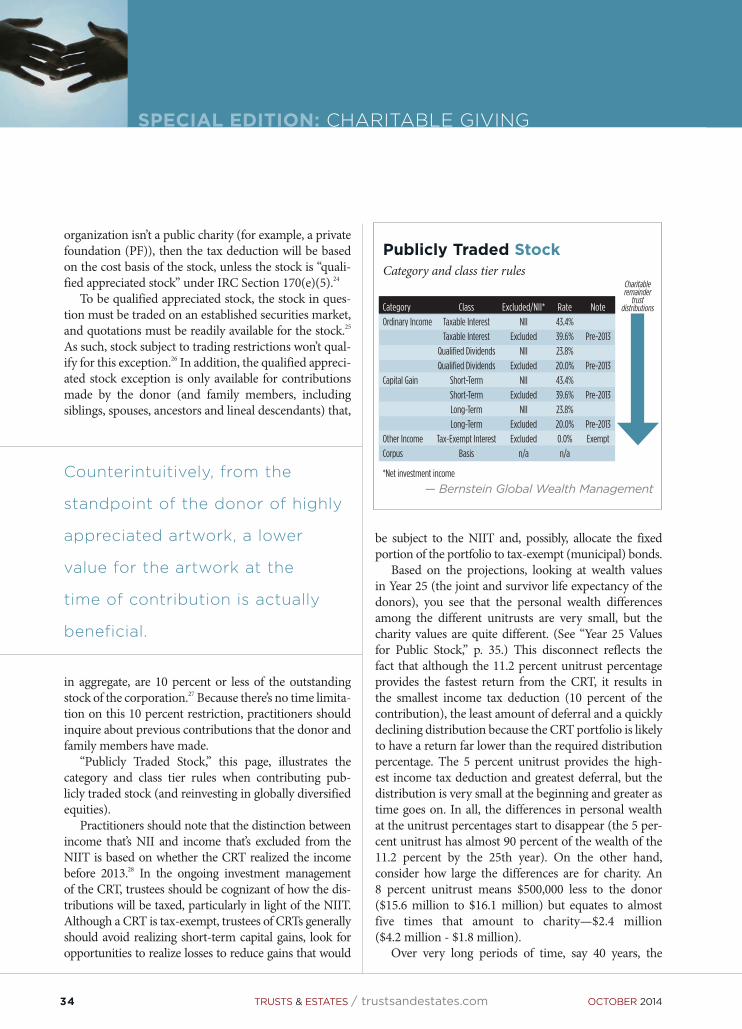

“Publicly Traded Stock,” this page, illustrates the category and class tier rules when contributing pub-licly traded stock (and reinvesting in globally diversified equities).

Practitioners should note that the distinction between income that’s NII and income that’s excluded from the NIIT is based on whether the CRT realized the income before 2013.28 In the ongoing investment management of the CRT, trustees should be cognizant of how the dis-tributions will be taxed, particularly in light of the NIIT. Although a CRT is tax-exempt, trustees of CRTs generally should avoid realizing short-term capital gains, look for opportunities to realize losses to reduce gains that would

be subject to the NIIT and, possibly, allocate the fixed portion of the portfolio to tax-exempt (municipal) bonds.

Based on the projections, looking at wealth values in Year 25 (the joint and survivor life expectancy of the donors), you see that the personal wealth differences among the different unitrusts are very small, but the charity values are quite different. (See “Year 25 Values for Public Stock,” p. 35.) This disconnect reflects the fact that although the 11.2 percent unitrust percentage provides the fastest return from the CRT, it results in the smallest income tax deduction (10 percent of the contribution), the least amount of deferral and a quickly declining distribution because the CRT portfolio is likely to have a return far lower than the required distribution percentage. The 5 percent unitrust provides the high-est income tax deduction and greatest deferral, but the distribution is very small at the beginning and greater as time goes on. In all, the differences in personal wealth at the unitrust percentages start to disappear (the 5 per-cent unitrust has almost 90 percent of the wealth of the 11.2 percent by the 25th year). On the other hand, consider how large the differences are for charity. An 8 percent unitrust means $500,000 less to the donor ($15.6 million to $16.1 million) but equates to almost five times that amount to charity—$2.4 million ($4.2 million - $1.8 million).

Over very long periods of time, say 40 years, the

34 TRusTs & esTATes / trustsandestates.com oCToBeR 2014

SPeciaL ediTion: ChaRiTaBle GiviNG

Publicly Traded StockCategory and class tier rules

— Bernstein Global Wealth Management

Category Class Excluded/NII* Rate Note

OrdinaryIncome TaxableInterest NII 43.4%

TaxableInterest Excluded 39.6% Pre-2013

QualifiedDividends NII 23.8%

QualifiedDividends Excluded 20.0% Pre-2013

CapitalGain Short-Term NII 43.4%

Short-Term Excluded 39.6% Pre-2013

Long-Term NII 23.8%

Long-Term Excluded 20.0% Pre-2013

OtherIncome Tax-ExemptInterest Excluded 0.0% Exempt

Corpus Basis n/a n/a

*Netinvestmentincome

Charitableremainder

trustdistributions

Counterintuitively, from the

standpoint of the donor of highly

appreciated artwork, a lower

value for the artwork at the

time of contribution is actually

beneficial.

landwehrma

Cross-Out

SPeciaL ediTion: ChaRiTaBle GiviNG

Thus, the contribution of highly appreciated artwork to a CRT won’t produce a significant income tax deduc-tion. Furthermore, the IRC won’t allow the donor to use the deduction until the non-charitable term ends, or the CRT sells the artwork.30 In addition, because artwork isn’t cash or a publicly traded security, donors need to get a qualified appraisal and satisfy the charitable contri-bution substantiation requirements.31 Practitioners also need to ensure that donors contribute sufficient cash or marketable securities so the CRT can pay for the costs of maintaining and insuring the art (not to mention the expenses required to administer the CRT). As long as the CRUT holds the artwork, the trustee must obtain an annual valuation of the unmarketable asset, which must be made by an independent trustee or determined by a current qualified appraisal.32 Finally, to ensure that the contribution of the artwork is a completed gift and to avoid self-dealing issues, the donor may not continue to retain enjoyment of the artwork by continuing to hang the artwork on his wall, even if the donor is the trustee of the CRT.33

lower unitrust percentages actually create more personal wealth. Donors in this case study may not live to age 105, but consider a very young donor (age 30) who may only qualify for a 5 percent CRUT but who’s likely to live 40 years or more. In that scenario, the minimum unitrust percentage actually creates greater wealth than the higher unitrust percentages (not to mention the considerably larger amount passing to charity). (See “Year 40 Values for Public Stock,” this page.)

artwork (and Other Collectibles)The contribution of appreciated artwork to a CRT poses a number of planning issues. Because artwork is tangible personal property, the resulting income tax deduction will be based on the cost basis of the artwork, rather than the FMV. Contributions of tangible personal property are limited to cost basis, unless the contribution is for the related use of a publicly supported charity.29 A direct contribution of artwork to a museum would qualify for the related use exception, but a contribution to a CRT wouldn’t, even if the remainder beneficiary is a museum.

oCToBeR 2014 TRusTs & esTATes / trustsandestates.com 35

Year 25 Values for Public StockA small difference in personal wealth results in a large difference to the charity

— Bernstein Global Wealth Management

$23.1

$8.8

$14.3

Total Wealth

Charity

Personal

8.0%5.0%

Unitrust Percentage

11.2%

$19.8

$4.2

$15.6

$17.9$1.8

$16.1

$Millions

Median wealth values. Based on Bernstein’s estimates of the range of returns for the applicable capital markets over the period analyzed. Data does not represent past performance and is not a promise of actual future results or a range of future results.

Year 40 Values for Public StockOver longer lifetimes, lower unitrust percentages benefit all

— Bernstein Global Wealth Management

$38.0Total Wealth

Charity

Personal

8.0%5.0%

Unitrust Percentage

11.2%

$31.5

$2.8

$28.7$28.7

$9.3

$27.5

$28.3

$0.8

$Millions

Median wealth values. Based on Bernstein’s estimates of the range of returns for the applicable capital markets over the period analyzed. Data does not represent past performance and is not a promise of actual future results or a range of future results.

landwehrma

Cross-Out

Unlike publicly traded stock, artwork is illiquid and typically non-income producing. As such, from a structure standpoint, practitioners typically recom-mend using a “flip” net income with make-up provision CRUT (Flip NIMCRUT). The flip event that converts the net income limitation to a unitrust distribution is often the sale of the artwork.34 This method avoids hav-ing to make annual distributions until there’s sufficient liquidity. The conversion to a unitrust doesn’t occur until the first year of the following taxable year, and on conversion, any undistributed amounts in the make-up account are forfeited.35 As such, with a Flip NIMCRUT,

the only opportunity for donors to recapture the previously unpaid distributions that have accumulated in the make-up account is to generate net income in the year of the sale in an amount that exceeds the uni-trust percentage sufficiently to empty the balance in the account. With interest and dividend rates as low as they are today, the only option is to allocate realized gain to income. To that end, the Treasury regulations provide that post-contribution realized gains can be allocated to fiduciary accounting income as long as state law and the governing instrument allow it.36 Counterintuitively, from the standpoint of the donor of highly appreciated artwork, because the income tax deduction won’t be based on FMV and only post-contribution gains can be allocated to income, a lower value for the artwork at the time of contribution is actually beneficial.

For investors and collectors, artwork is considered a collectible under the IRC and is taxable at a federal rate of 28 percent.37 For the artist who created it, the art-work is ordinary income property,38 and for dealers, the artwork is considered inventory, also taxed at ordinary rates.39 Assuming the donor is an investor, the category

and class tier rules would be populated as shown in “Artwork and Collectibles,” this page.

For the projections in this case study, we assumed that the artwork has a $100,000 tax basis and is worth $10 million at contribution to a Flip NIMCRUT. The artwork is then sold a year later for $11 million, and it converts to a unitrust distribution the following taxable year. Based on these facts, consider the wealth values in Year 25. (See “Year 25 Values for Artwork,” p 38.)

What’s notable about the results is that the higher unitrust percentages make a larger difference in personal wealth than the publicly traded stock scenario. Even 25 years later, the lowest unitrust percentage is less than 80 percent of the wealth of the highest one. This discrep-ancy exists despite the fact that much of the collectible gain that’s being deferred would have been taxed at the higher 28 percent rate. Because the income tax deduc-tion is based on cost basis, rather than FMV, choosing a lower unitrust percentage doesn’t increase the deduc-tion by much. As such, donors with less charitable intent should consider higher unitrust percentages.

Commercial Real Property interestsContributions of highly appreciated commercial real property (or interests in the real property through a partnership or limited liability company) to a CRUT have planning issues similar to artwork and publicly traded stock. Like artwork, real property is

36 TRusTs & esTATes / trustsandestates.com oCToBeR 2014

SPeciaL ediTion: ChaRiTaBle GiviNG

artwork and collectiblesCategory and class tier rules

— Bernstein Global Wealth Management

Category Class Excluded/NII* Rate Note

OrdinaryIncome TaxableInterest NII 43.4%

TaxableInterest Excluded 39.6% Pre-2013

QualifiedDividends NII 23.8%

QualifiedDividends Excluded 20.0% Pre-2013

CapitalGain Short-Term NII 43.4%

Short-Term Excluded 39.6% Pre-2013

Long-Term NII 23.8%

Long-Term Excluded 20.0% Pre-2013

OtherIncome Tax-ExemptInterest Excluded 0.0% Exempt

Corpus Basis n/a n/a

*Netinvestmentincome

Charitableremainder

trustdistributions

Practitioners should be wary of

any arrangement in which indirect

personal benefit may be provided

to a disqualified person.

landwehrma

Cross-Out

considered an unmarketable asset. As such, the substan-tiation requirements, independent trustee and qualified appraisal issues discussed above are equally applicable. In addition, because of its illiquidity, most donors con-tribute commercial real property to a Flip NIMCRUT with the ability to retain the net income but convert to a unitrust if the real property is subsequently sold. As with artwork, donors will need to fund the CRT with sufficient cash or marketable securities to provide for the anticipated costs of maintaining the property (and expenses of administering the CRT), particularly if the property isn’t likely to provide sufficient rental income. With a CRUT, additional contributions can be made if a shortfall occurs, whereas that’s not avail-able for CRATs.40 Like publicly traded stock, the chari-table income tax deduction is based on the FMV of the property if the charitable remainder organization is pub-licly supported, and the property is considered a capital asset taxable at a federal rate of 20 percent.41 However, commercial real property has a number of thorny issues that are quite different than stock and artwork.

Often, commercial real estate is encumbered with

debt, and the existence of a mortgage on the property poses a myriad of planning issues (including reducing the FMV of the asset for tax deduction purposes). First, to the extent debt is in excess of basis, a “negative basis”42 issue exists, and the contribution of such property will be deemed a recognition event to the extent of the excess debt.43 In addition, even if debt isn’t in excess of tax basis, the contribution of the encumbered property (even if the debt is nonrecourse or the CRT doesn’t agree to assume the debt) will be considered a “bargain sale” or “part gift/part sale” to a charitable organization.44 Pursuant to the bargain sale rules, the contribution is considered a sale, in part, and a charitable contribution, in part.45 The debt is considered an amount realized on the sale part, and only a portion of the tax basis of the property can be used in determining the amount of gain realized.46 Thus, gain will invariably be recognized on the contribution of highly appreciated encumbered real property to a CRUT. Finally, if the grantor remains personally liable on the debt, the Internal Revenue Service has ruled that the contribution causes the trust to become a grantor trust (because the trust may ultimately be forced to pay the debt, thereby discharging the grantor’s liability), resulting in a disqualification of the trust as a CRT.47

Even if donors can accept the gain recognition issues that encumbered property poses, they need to overcome an unrelated business taxable income (UBTI) problem. The encumbered property will be considered “debt-financed property” if the debt falls within the definition of “acquisition indebtedness” (debt incurred to acquire or improve the property).48 The consequences of UBTI are dire. The IRC imposes a 100 percent excise tax on any UBTI, including a relatively large portion of the gain from the sale of appreciated property.49 There’s an excep-tion for inter vivos transfers to a CRT if the mortgage was placed on the property at least five years before the transfer to the CRT and if the donor held the property for more than five years before the transfer.50 If these requirements are satisfied, then for 10 years following the transfer, the debt won’t be considered acquisition indebtedness, thereby avoiding the UBTI excise tax.51 This provides a valuable 10-year window during which the trustee can either pay off the debt or sell the property. Given the myriad of issues that arise with real property encumbered with debt, many practitioners look for ways to pay off the debt (or shift debt to other properties

38 TRusTs & esTATes / trustsandestates.com oCToBeR 2014

SPeciaL ediTion: ChaRiTaBle GiviNG

Year 25 Values for artworkDonors benefit more from higher unitrust percentages

— Bernstein Global Wealth Management

$23.9Total Wealth

Charity

Personal

8.0%5.0%

Unitrust Percentage

11.2%

$21.1

$4.6

$16.5$13.9

$10.0

$17.4

$19.3$1.9

$Millions

Median wealth values. Based on Bernstein’s estimates of the range of returns for the applicable capital markets over the period analyzed. Data does not represent past performance and is not a promise of actual future results or a range of future results.

landwehrma

Cross-Out

SPeciaL ediTion: ChaRiTaBle GiviNG

how and whether the activities of the donor recipient and/or trustee will cause all or a portion of the income and gain attributable to the real property to be excluded or subject to the NIIT when distributed from the CRT. Many questions remain unanswered. For example, if the trustee is an active participant on the rental property, does that immediately exclude all of the gain and income even if the donor/recipient isn’t materially participating? If the donor is an active participant on the property prior to contribution, does that mean all the gain on a subse-quent sale by the trustee of the CRT is excluded from the NIIT? Or, does that mean only pre-contribution

gain is excluded and post-contribution gain is NII? What if the active donor is also the sole trustee or co-trustee of the CRT? Hopefully, guidance is forthcoming from the Treasury Department. In all, the tier rules can become quite complicated, as noted in “Commercial Real Property,” p. 40.

Let’s assume a contribution of $10 million of unencumbered commercial real property with $8 million of unrecaptured Section 1250 gain to a Flip NIMCRUT, with a sale at $10 million at the end of the first year.60 Based on these facts, the projected median wealth values in 25 years would be $13.8 million, $15.3 million and $15.8 million, for unitrust payouts of 5 percent, 8 percent and 11.2 percent, respectively. What’s notable about the results is that, like the publicly traded stock example, the differences in personal wealth are quite small across all of the unitrust percentages. Unlike the artwork example, in which higher unitrust percentages generally provide more wealth to the donor, that isn’t necessarily the case with real property. The tax deferral and savings provided at the lower unitrust percentages are at work with real property because the

through refinancings) prior to contribution or conclude that the mortgaged property shouldn’t be contributed to a CRT.

Donors occasionally will seek to contribute an undi-vided interest in real property to a CRT and retain the rest of the interests personally. This strategy can pose a number of planning issues surrounding the self-dealing rules. The IRC provides that self-dealing includes any “direct or indirect … use by or for the benefit of, a disqualified person of the income or assets of”52 the CRT. The IRS has ruled that the co-development of real property, and the pro rata sharing of profits and income therefrom, with a disqualified person (the donor) and a PF is considered self-dealing.53 While mere co-own-ership of property between a disqualified person and a CRT may not be considered self-dealing, practitioners should be wary of any arrangement in which indirect personal benefit may be provided to a disqualified person.54 In one ruling, the IRS opined that a CRT’s ownership of property through a partnership with dis-qualified persons (the donors) and the separate sale of the CRT’s partnership interest to a non-disqualified per-son wouldn’t be considered self-dealing transactions.55 However, in coming to that conclusion, the IRS spe-cifically stressed that the CRT was selling its partnership interest “without any sale by” the disqualified persons of their interests in the partnership.56 In other words, a joint and simultaneous sale by the CRT and the disqualified persons may be considered self-dealing, particularly if it can be shown that the disqualified persons received more than they otherwise would have if they had simply sold their portions of the property separately.

Because commercial real property is depreciable, planners should be aware of how the sale of such prop-erty in a CRT will affect the taxation of the distribution under the tier rules. Generally, the sale of most com-mercial real property will give rise to “unrecaptured IRC Section 1250 gain,”57 which is taxed at a maximum federal rate of 25 percent.58 As a result, if commercial real property is sold in a CRT, the tier rules include gain taxed at 25 percent, as well as regular LTCGs at 20 percent. In addition, any gains and rental income from the property may be considered NII, depending on the active (material participation) or passive participa-tion of the parties involved (donor, recipient or trustee) and the property in question.59 It’s unclear, at this point,

oCToBeR 2014 TRusTs & esTATes / trustsandestates.com 39

The only opportunity to

contribute iRa assets to a CRT

is at the death of the account

holder.

landwehrma

Cross-Out

tax deduction is based on FMV (unlike the artwork), and the deferred gain is taxed at a higher rate due to unrecaptured Section 1250 gain (like artwork).

Qualified Retirement assetsUnlike the previous examples, assets in an individual retirement account (or other qualified retirement plan) may not be contributed to a CRT during the lifetime of the account owner without having a taxable distribution.61 As such, the only opportunity to contribute IRA assets to a CRT is at the death of the account holder. This option is especially attractive when the account holder doesn’t

have a surviving spouse, and a tax-free rollover isn’t a planning option.62 When a non-spouse beneficiary of the account holder, like a child, inherits an IRA, the child is entitled to stretch the distributions under the required minimum distribution (RMD) rules, requiring annually increasing distributions over the child’s remaining actuarial life expectancy.63 In addition, IRA assets are considered income in respect of a decedent (IRD), so unlike other assets, they aren’t entitled to a step-up in basis at the death of the account holder,64 and all distributions (whether paid over time or not) to a beneficiary are taxable as ordinary income.65 If the IRA is subject to federal estate taxes on the death of the owner, the beneficiary is entitled to an income tax deduction equal to the estate tax attributable to the inclusion of the IRA assets (IRD deduction).66 The IRD deduction is reported on a pro-rated basis as each distribution is made.67 Because a decedent’s IRA may be subject to estate taxes, and the distributions from the IRA will be taxable as ordinary income to the beneficiary without the

benefit of a step-up in basis (notwithstanding the IRD deduction), owners of large IRAs often make a charity the sole beneficiary of their IRAs (thereby eliminating the estate and income tax liability). Of course, this option provides no economic benefit to the non-spouse beneficiary. Perhaps a CRUT for the benefit of the non-spouse beneficiary and charity could be a viable planning option that could provide the best of both worlds. It would provide a partial estate tax deduction, an income stream for the life of the non-spouse beneficiary and a charitable gift on the beneficiary’s death.

Further, a number of legislative proposals have been circulating that would eliminate the ability of non-spouse beneficiaries to stretch the IRA over their lifetimes.68 Generally, pursuant to the proposals, non-spouse beneficiaries of IRAs or other qualified retirement plans would be required to take distribu-tions over no more than five years after the account holder’s death. For a beneficiary who’s age 55, the RMD is below 5 percent (the minimum percentage for a CRUT) for 10 years, and it isn’t until after the 20th year that the RMDs exceed 10 percent. After the 20th year, however, the distribution percentage increases quickly, so by the 25th year, the percentage is almost

40 TRusTs & esTATes / trustsandestates.com oCToBeR 2014

SPeciaL ediTion: ChaRiTaBle GiviNG

commercial Real PropertyCategory and class tier rules

— Bernstein Global Wealth Management

Category Class Excluded/NII* Rate Note

OrdinaryIncome TaxableInterest NII 43.4%

NetRentalIncome NII 43.4% Passive

TaxableInteres Excluded 39.6% Pre-2013

NetRentalIncome Excluded 43.4% Active

QualifiedDividends NII 23.8%

QualifiedDividends Excluded 20.0% Pre-2013

CapitalGain Short-Term NII 43.4%

Short-Term Excluded 39.6% Pre-2013

UnrecapturedßGain NII 28.8% Passive

UnrecapturedßGain Excluded 25.0% Active

Long-Term NII 23.8%

Long-Term Excluded 20.0% Pre-2013

OtherIncome Tax-ExemptInterest Excluded 0.0% Exempt

Corpus Basis n/a n/a

*Netinvestmentincome

Charitableremainder

trustdistributions

a number of legislative proposals

have been circulating that would

eliminate the ability of non-spouse

beneficiaries to stretch the iRa

over their lifetimes.

landwehrma

Cross-Out

18 percent, and by the 30th year, the percentage is 100 percent. Clearly, the current RMD rules are very favorable to IRA beneficiaries from a tax deferral stand-point. If this 5-year proposal is enacted, perhaps a CRUT would be a better alternative for the non-spouse ben-eficiary. The payment of the unitrust would effectively create a stretch of the IRA proceeds that otherwise would have to be paid out in five years.

Private Letter Ruling 199901023 (Oct. 8, 1998) is instructive on how CRTs can be used as the beneficiary of IRA assets. It involved a CRUT that was to be the recipient of retirement plan assets on the death of the taxpayer. The taxpayer’s children would be the unitrust recipients for their lifetimes or 20 years after the death of the taxpayer, whichever came first. The IRS ruled: (1) when the CRUT receives the qualified retirement proceeds, they’ll retain their character as IRD and ordi-nary income in the tier rules (first category of income); and (2) the IRD deduction will reduce the amount that’s included in the first tier. However, it goes on to say the IRD deduction is “not directly made available to the income beneficiaries under section 664(b).”69 Effectively, the ruling mandates that the IRD deduction must be allocated to either the last category of income or cor-pus. See “Individual Retirement Account and Qualified Retirement Assets,” this page, for the category and class tier rules for this example.

When the assets are distributed from the IRA, they arrive as ordinary income that’s excluded from NII.70 However, despite the fact that CRTs are tax-exempt, any subsequent gains or income realized in the CRT won’t be excluded from NII if they’re distributed to the unitrust recipient. This treatment is in contrast to the earnings realized on the assets if they had stayed in the IRA, which are excluded from the NII.71 In other words, one downside to distributing the assets to a CRT is that gains and income that might be excluded from NII may now be subject to the NIIT. Another downside to the CRT option is, as mentioned above, the unitrust recipi-ent doesn’t get the direct benefit of the IRD deduction. Instead of each distribution carrying out a proportionate deduction as it would from an IRA, the distributions are disproportionately carrying out ordinary income.

Let’s assume that on the death of the IRA owner, the IRA either passes to a non-spouse beneficiary who’s age 55 or to a 5 percent or 8 percent CRUT for the lifetime

of the non-spouse beneficiary. Also assume that the IRA assets are subject to estate taxes, the CRT results in estate tax savings because of the resulting estate tax deduction and the resulting IRD deductions are calculated as mentioned above. If the 5-year proposal passes, then based on our projections, over the next 30 years, the 5 percent or 8 percent CRUT will create 2.7 percent or 7.7 percent more wealth to the non-spouse beneficiary, respectively, as compared to inher-iting the IRA directly. In addition to generating more personal wealth, the CRUT will also provide a sig-nificant charitable gift in the future—$9.6 million or $3.9 million, respectively. If the current RMD rules remain, then the 5 percent or 8 percent CRUT will result in 10.8 percent or 7.1 percent less wealth for the non-spouse beneficiary, respectively, but still provide the same charitable gift in the future. Notwithstanding the economic detriment to the non-spouse beneficiary if the RMD rules don’t change, a CRUT is an interesting alternative for: (1) IRA owners who are worried their beneficiaries won’t limit themselves to just the RMDs

42 TRusTs & esTATes / trustsandestates.com oCToBeR 2014

SPeciaL ediTion: ChaRiTaBle GiviNG

individual Retirement account and Qualified Retirement assetsCategory and class tier rules

— Bernstein Global Wealth Management

Category Class Excluded/NII* Rate Note

OrdinaryIncome TaxableInterest NII 43.4%

IRADistributions Excluded 39.6% Exempt

TaxableInteres Excluded 39.6% Pre-2013

QualifiedDividends NII 23.8%

QualifiedDividends Excluded 20.0% Pre-2013

CapitalGain Short-Term NII 43.4%

Short-Term Excluded 39.6% Pre-2013

Long-Term NII 23.8%

Long-Term Excluded 20.0% Pre-2013

OtherIncome Tax-ExemptInterest Excluded 0.0% Exempt

IRDDeduction Excluded 0.0% Exempt

Corpus Basis n/a n/a

*Netinvestmentincome

Charitableremainder

trustdistributions

landwehrma

Cross-Out

SPeciaL ediTion: ChaRiTaBle GiviNG

necessitated by the Bush era tax cuts, which created the preferential quali-fied divided rate of 15 percent (now 20 percent) that’s still considered ordi-nary income.

10. Treas. Regs. Section 1.664-1(d)(1)(i)(a).11. Treas. Regs. Section 1.1411-3(d)(2)(ii). Undistributed net investment income

(NII) received or realized before 2013 is excluded from the net investment income tax (NIIT), even if distributed to a non-charitable beneficiary after 2013, and any NII received or realized in 2013 or thereafter is subject to the NIIT as determined at the non-charitable beneficiary’s level in the year dis-tributed. Treas. Regs. Section 1.1411-3(d)(1)(iii). The 2012 proposed Treasury regulations, REG-130507-11, 77 Fed. Reg. 72612 (Dec. 5, 2012) provided a simpli-fied method of computing the NIIT for CRTs (essentially allowing losses to be carried forward to offset income in future years). See Prop. Regs. Sec- tion 1.1411-3(d)(3). Instead, the final Treasury regulations adopted the

and would rather provide an annual payment to them for their lifetimes (beneficiaries of inherited IRAs always have the ability exhaust the IRA immediately); (2) non-spouse beneficiaries who are older than age 55 (for exam-ple, at age 70, the RMDs get very large in a short amount of time); and (3) IRA owners who wish to provide for both their heirs and charity but choose to defer the charitable gift until their heirs have gotten the eco-nomic benefit of the IRA assets for their lifetimes.

—We would like to thank Ashley E. Velategui, CFA, senior analyst, and Stephanie Shen Torosion, senior ana-lyst, at Bernstein Global Wealth Management, for their invaluable assistance with the quantitative forecasting.

endnotes1. Including the: (1) requirement of using the valuation methodology in In-

ternal Revenue Code Section 7520 (Technical and Miscellaneous Revenue Act of 1988, P.L. 100-647); (2) minimum charitable interest requirement of 10 percent under IRC Sections 664(d)(1)(A) and 664(d)(2)(A) (Taxpayer Re-lief Act of 1997), P.L. 105-34, (TRA 1997); (3) maximum non-charitable dis-tribution rate of 50 percent under Sections 664(d)(1)(A) and 664(d)(2)(A) (TRA 1997); (4) Internal Revenue Service position that for estate and gift charitable deduction purposes the charitable remainder trust (CRT) must satisfy the 5 percent exhaustion rule (Revenue Ruling 77-374, Treasury Regulations Sections 20.2055-2(b)(1) and 25.2522(c)-3(b)(1), and Rev. Rul. 70-452. See also Treas. Regs. Section 1.170A-1(e)); and (5) 110-year exhaustion test (Treas. Regs. Sections 1.7520-3(b)(2)(i), 20.7520-3(b)(2)(i) and 25.7520-3(b)(2)(i)).

2. P.L. 112-240, 126 Stat. 2313, enacted Jan. 2, 2013.3. IRC Section 1411. Part of the Health Care and Education Recon-

ciliation Act of 2010, P.L. 111-152, enacted March 30, 2010. This act amended the Patient Protection and Affordable Care Act, P.L. 111-148, enacted March 23, 2010.

4. Revenue Procedure 2013-35, Treas. Regs. Section 3.01 and IRC Section 1411(b).5. The difference between taxing the income at the highest rate against the

actual tax payable at each income threshold.6. Calculated based on $1 million of long-term capital gains (LTCGs). The margin-

al California income tax rate is 11.3 percent at $1 million of taxable income and 13.3 percent when taxable income exceeds $1.017 million.

7. Treas. Regs. Section 1.1411-3(b)(1)(iii).8. Treas. Regs. Section 1.1411-3(d).9. IRC Section 664(b) and Treas. Regs. Section 1.664-1(d)(1). Historically, the tier

rules followed a ”worst-in, first-out” distribution scheme, in which the high-est taxed income (ordinary) was distributed first, followed by short-term capital gains and then, finally, LTCGs. The “category and class” scheme was

oCToBeR 2014 TRusTs & esTATes / trustsandestates.com 43

SPoTLighT

She Seems Nice “Minerva” (221/2 in. by 18 in.) by Lucien Lévy-Dhurmer, sold for $34,446 at Christie’s recent 19th Century European Art Sale in London on Sept. 11, 2014. Minerva was the Roman goddess of wisdom and sponsor of arts, trade and strategy. She was comparable to the Greek goddess Athena.

landwehrma

Cross-Out

category and class tier method under IRC Section 664(b). There’s a limited irrevocable election to adopt the simplified method for tax years after 2012. For CRTs established in 2013 and thereafter, the election must be on the tax return for the year it was established, and for CRTs established before 2013, the election must have been made on the tax return for the first taxable year after 2012. Prop. Regs. Section 1.1411-3(d)(3).

12. Treas. Regs. Sections 1.664-1(d)(1)(i)(b) and 1.664-1(d)(1)(ii)(b).13. Treas. Regs. Section 1.664-1(d)(1)(ii)(a).14. It’s assumed throughout the article that the donors to the CRT also retain the

annual unitrust payment.15. Rev. Rul. 2014-22, (Sept. 8, 2014).16. Calculated from March 1989 to August 2014.17. IRC Sections 664(d)(1)(A) and 664(d)(2)(A); Treas. Regs. Sections 1.664-2(a)(2)(i)

and 1.664-3(a)(2)(i).18. Sections 664(d)(1)(D) and 664(d)(2)(D).19. See supra note 1.20. Projections are from Bernstein’s Wealth Forecasting System, which is based on a

Monte Carlo model that simulates 10,000 plausible paths of return for each asset class and inflation, producing a probability distribution of outcomes. However, the model goes beyond randomization by integrating the paths of return with an investor’s unique circumstances; taking the prevailing market conditions into consideration; and basing the forecasts on the building blocks of asset returns, such as inflation, yield spreads, stock earnings and price multiples. The projec-tion incorporates the linkages that exist among the returns of the various asset classes and factors in a reasonable degree of randomness and unpredictability.

In all scenarios, we’ve assumed that the donor’s personal assets and the charitable remainder unitrust (CRUT) are invested in 100 percent globally di-versified equities, comprised of 21 percent U.S. diversified, 21 percent U.S. value, 21 percent U.S. growth, 7 percent U.S. small-/mid-cap, 22.5 percent developed international and 7.5 percent emerging market stocks.

21. Unless otherwise stated, the trustee sells the contributed asset soon after contribution in the first taxable year of the CRUT.

22. Assumes an IRC Section 7520 rate of 2.4 percent, which was the prevailing rate available at the time these projections were made. See Section 7520(a) (election to pick highest rate in 3-month period including the date of contri-bution).

23. See Treas. Regs. Sections 1.664-4(a) and 1.664-4(d).24. When LTCG property is contributed to a charitable organization that’s not a pub-

lic charity, the donor’s charitable deduction is reduced by 100 percent of the appreciation attributed to the remainder interests. IRC Section 170(b)(1)(B)(ii).

25. IRC Section 170(e)(5)(B)(i).26. See Private Letter Ruling 9247017 (Aug. 24, 1997).27. IRC Sections 170(e)(5)(C)(i), (ii), and 267(c)(4).28. Supra note 11.29. IRC Section 170(e)(1)(B)(i) and Treas. Regs. Section 1.170A-4(a)(3).30. IRC Section 170(a)(3), Treas. Regs. Sections 1.664-2(d), 3(d) and PLR 9452026

(Sept. 29, 1994). The PLR involved the contribution of a rare violin to a chari-

table remainder annuity trust. The IRS ruled that the income tax deduction would be based on cost basis, and the deduction wouldn’t be allowable so long as the taxpayer retained an annuity interest, but the deduction would be allowable when the trustee sells the instrument.

31. IRC Section 170(f)(11) and Treas. Regs. Section 1.170A-13(c).32. Treas. Regs. Sections 1.664-1(a)(7) and 1.170A-13(c).33. See Treas. Regs. Section 25.2511-2(c) and IRC Sections 4947(a)(2) (subjecting

CRTs to the private foundation (PF) provisions of Sections 4940-4948) and 4941 (self-dealing). See also PLR 8842045 (July 26, 1988) (donor and a private oper-ating foundation can co-own artwork provided each pays their proportionate cost for maintenance and insurance for the artwork) and Technical Advice Memorandum 8824001 (the display of artwork owned by a PF at the residence of a disqualified person may be self-dealing if no effort is made to advertise that the public is invited to tour the premises to view the artwork). But see GCM 39770.

34. The Treasury regulations provide that the “flip” must be triggered “on a spe-cific date or by a single event whose occurrence isn’t discretionary with, or within the control of, the trustees or any other persons.” Treas. Regs. Sec-tion 1.664-3(a)(i)(c). The Treasury regulations specifically include the sale of “unmarketable assets,” which are defined as “assets that are not cash, cash equivalents, or other assets that can be readily sold or exchanged for cash or cash equivalents.” Treas. Regs. Section 1.664-1(a)(7)(i).

35. Treas. Regs. Section 1.664-3(a)(1)(i)(c)(3).36. Treas. Regs. Section 1.664-3(a)(1)(i)(b)(3), (4) and Section 643(b).37. IRC Section 1(h)(4).38. IRC Section 1221(a)(3) (excluding from the definition of capital asset, any

property created from the personal efforts of the taxpayer).39. Section 1221(a)(1) (excluding from the definition of capital asset, property pri-

marily for sale to customers in the ordinary course of the taxpayer’s trade or business).

40. Treas. Regs. Sections 1.664-2(b) and 1.664-3(b).41. IRC Section 170 and Treas. Regs. Section 1.170A-7(a)(2).42. “Negative basis” is a misnomer because property can never have a basis

that’s less than zero. It denotes situations in which debt is in excess of tax basis or partnership liabilities in excess of tax basis or negative capital ac-count in a partnership interest. See Rev. Rul. 75-194 and Goodman v. United States, 2000-1 USTC 50,162 (S.D. Fla. 1999).

43. Treas. Regs. Section 1.1001-2.44. Crane v. Commissioner, 331 U.S. 1 (1947) (amount realized on the sale of

mortgaged property includes the amount of indebtedness), Comm’r v. Tufts, 461 U.S. 300 (1983), Ebben v. Comm’r, 783 F.2d 906 (9th Cir. 1986) (gift of prop-erty subject to nonrecourse note to charity), Guest v. Comm’r, 77 T.C. 9 (1981), Treas. Regs. Section 1.1011-2(a)(3), Rev. Rul. 75-194 (gift of partnership interest to charity with the taxpayer’s share of partnership liabilities being treated as an amount realized).

45. Treas. Regs. Section 1.170A-4(c)(2)(ii).46. IRC Sections 1001, 1011(b), Treas. Regs. Sections 1.1001-2(a)(1) and 1.1011-2(b).

44 TRusTs & esTATes / trustsandestates.com oCToBeR 2014

SPeciaL ediTion: ChaRiTaBle GiviNG

landwehrma

Cross-Out

SPeciaL ediTion: ChaRiTaBle GiviNG

Section 1.408-8, Q&A-5(a).63. IRC Sections 408(d)(3)(C), 401(a)(9) and 402(c)(11). See Treas. Regs. Sec-

tion 1.401(a)(9)-6, Q&A-5.64. IRC Section 1014(c).65. IRC Sections 61(a)(14), 72, 402(a) and 408(d)(1), assuming the decedent owner

had no nondeductible contributions. See IRC Sections 72(b)(1) and (e)(8).66. IRC Section 691(c) It’s an itemized deduction but isn’t subject to the 2 percent

floor for miscellaneous itemized deductions and isn’t treated as a miscel-laneous itemized deduction for alternative minimum tax purposes on tax preferences. IRC Sections 67(b)(7) and 56(b)(1).

67. IRC Section 691(c)(2).68. Department of the Treasury, “Require Non-Spouse Beneficiaries of Deceased

Individual Retirement Account or Annuity (IRA) Owners and Retirement Plan Participants to Take Inherited Distributions over No More Than Five Years,” General Explanation of the Administration’s Fiscal Year 2015 Revenue Propos-als (March 2014), p. 179, and Joint Committee on Taxation, ‘Modification of Require Distribution Rules for Pension Plans, Description of the Chairman’s Modification to the Proposals of the “‘Highway Investment, Job Creation and Economic Growth Act of 2012’” (February 2012), p. 12.

69. PLR 199901023 ((Oct. 8, 1998).70. See Treas. Regs. Section 1.1411-3(d)(2)(iii), Ex. 1.71. IRC Section 1411(c)(5), Treas. Regs. Section 1.1411-8(a) and the final NIIT regulations.

47. PLR 9015049 ((Jan. 16, 1990). The discharge of indebtedness might also give rise to a self-dealing issue under IRC Section 4941.

48. IRC Section 514(c).49. IRC Section 664(c)(2)(A), Treas. Regs. Sections 1.664-1(c)(1), (d)(2) and 514(c)(7)

and Treas. Regs. Section 1.514(a)-1(a)(1).50. IRC Section 514(c)(2)(B). There’s a 10-year exception for mortgaged property

acquired by a charitable organization by bequest or devise (testamentary transfer) with no 5-year requirement.

51. This exception doesn’t apply if the charity, to acquire the equity in the prop-erty, assumes and agrees to pay the debt secured by the mortgage or if it makes any payment for the equity in the property owned by the taxpayer. Ibid.

52. IRC Section 4941(d)(1)(E).53. PLR 8038049 ((June 24, 1980)).54. See TAM 9646002 (PF’s maintenance of a historic plantation, which was also

the residence of a disqualified person, resulted in a private benefit and would constitute self-dealing) and GCM 39770 (advised against the favorable ruling in PLR 8842045 (July 26, 1998) and stated that the personal use of co-owned property, in this case artwork, was self-dealing, even if the costs are paid proportionately).

55. PLR 9114025 ((July 7, 1991).56. The PLR goes to conclude that “the sale by Trusts of all of their interests in

Partnership will not be self-dealing under section 4941 of the Code if H and W, simultaneously with the sale by Trusts, enter into a limited partnership arrangement with the purchaser under which H and W are given the right to sell (or will be obliged to sell) their interests in Partnership at a later time and under different conditions.” Ibid.

57. IRC Section 1(h)(6)(A) (defined as the amount of LTCG that would be treated as ordinary income if IRC Section 1250(b)(1) included all de-preciation, and the applicable percentage under Section 1250(a) were 100 percent). This convoluted definition essentially provides that the ag-gregate straight-line depreciation taken on the property will be considered unrecaptured Section 1250 gain. Under the current depreciation system, straight-line depreciation is required for all residential rental and nonresi-dential real property. IRC Section 168(b)(3)(A), (B).

58. IRC Section 1(h)(1)(E).59. The Treasury Department didn’t issue formal guidance on how the mate-

rial participation will be determined in the final NIIT regulations. It’s un-clear whether material participation will be determined at the trustee, donor or recipient level. See Frank Aragona Trust v. Comm’r, 142 T.C. No. 9 (March 27, 2014), Mattie K. Carter Trust v. U.S., 523 F. Supp.2d 536 (N.D. Tex. 2003), PLR 201029014 (July 23, 2010), TAMs 201317010 and 200733023.

60. The case study assumes no net income is payable from the real property prior to sale.

61. See IRC Section 401(a)(13)(A) (anti-alienation provision).62. A surviving spouse may rollover an individual retirement account to another

IRA or elect to treat the IRA as his own. IRC Section 402(c)(9) and Treas. Regs.

oCToBeR 2014 TRusTs & esTATes / trustsandestates.com 45

SPoTLighT

Staying Close to Shore“Fishing on the Lake” (151/8 in. by 181/4 in.) by Jules René Hervé, sold for $4,053 at Christie’s recent 19th Century European Art Sale in London on Sept. 11, 2014. Known for his paintings of cityscapes and landscapes, Hervé painted in an impressionistic style that captured the shimmering texture of the city and the softer light of the countryside.

landwehrma

Cross-Out

![1 arXiv:1803.05448v1 [astro-ph.HE] 14 Mar 2018 · The combined light curve of PG1302-102 from CRTS (black) and ASAS-SN (blue). The ASAS-SN light curve has been offset to match CRTS](https://static.fdocuments.us/doc/165x107/5ccc617388c99335448c0456/1-arxiv180305448v1-astro-phhe-14-mar-2018-the-combined-light-curve-of-pg1302-102.jpg)