Welcome to Croatia. CROATIA Plitvica UNESCO protected national park Prehistoric Croatia.

Croatia Country Financial Accountability Assessment

May 12, 2005 Operations Policy and Services Europe and Central Asia Region

Document of the World Bank

CURRENCY EQUIVALENT 1 HRK = 0.17450 US$ (MAY 12, 2005)

FISCAL YEAR JANUARY 1 – DECEMBER 31

ABBREVIATIONS AND ACRONYMS

ASA Act on State Audit BA (Organic) Budget Act BFU Budget and Finance Unit BU Budget User CAAT Computer Assisted Auditing Techniques CARDS Community Assistance for Reconstruction,

Development and Stability CAS Country Assistance Strategy CFAA Country Financial Accountability Assessment CIA Certified Internal Auditor CNB Croatian National Bank COA Chart of Accounts COM Council of Ministers COSO Committee of the Sponsoring Organization of the

Treadway Commission CPAR Country Procurement Assessment Report CRU Control and Revision Unit EBF Extra-Budgetary Funds EC European Communities ECA Europe and Central Asia Region ECSPE Europe and Central Asia Region, Poverty

Reduction/Economic Management Department, World Bank

ECSPS Europe and Central Asia, Operations and Policy Services, World Bank

EDIS Extended Decentralized Implementation Systems ESA European System of Accounts ESW Economic and Sector Work EUG European Implementing Guidelines for the

INTOSAI Auditing Standards FINA Financial Agency FMS Financial Management Specialist FY Fiscal/Financial Year GDP Gross Domestic Product GSF Government Financial Statistics GSFM GFS Manual HABOR Croatian Agency for Bank Reconstruction and

Development HBU Head of a Budget User HRK Croatian Kuna IAS International Accounting Standards IASB International Accounting Standards Board IAU Internal Audit Unit IBRD International Bank for Reconstruction and

Development IFAC International Federation of Accountants IIA Institute of Internal Auditors IMF International Monetary Fund INTOSAI International Organization of Supreme Audit

Institutions

INTOSAIAS INTOSAI Auditing Standards IPSAS International Public Sector Accounting Standards ISA International Standards on Auditing ISPA Instrument for Structural Policies for Accession ISPPIA International Standards for the Professional

Practice of Internal Auditing LCSPE Latin America & Caribbean Region, Sector Unit

for Economic Policy, World Bank MOF Ministry of Finance MP Member of Parliament MTEF Medium Term Expenditure Framework MTSA Regulation on Methods in Managing the Treasury

Single Account etc (OG No.97/1995) OECD Organization for Economic Cooperation and

Development OFB Ordinance on Financial Reporting and Budgetary

Accounting OPCFM Operations Policy & Country Services, Financial

Management, World Bank PAL Programmatic Adjustment Loans PDMS Public Debt Management Section PEFA Public Expenditure and Financial Accountability PEIR Public Expenditure and Institutions Review PFM Public Financial Management PIFC Public Internal Financial Control ROSC Reports on the Observance of Standards and

Codes SAA Stability and Association Agreement SAF State Accounting and Financial Reporting SAP Trademark of financial accounting and

management information system SAI Supreme Audit Institution SAO State Audit Office SAPARD Special Accession Program for Agriculture and

Rural Development SIGMA Support for Improvement in Governance and

Management in Central and Eastern Europe SNA System of National Accounts SOE Socially or State-Owned Enterprise TA Technical Assistance TSA Treasury Single Account TRM Treasury Reference Model USAID United States Agency for International

Development

Regional Vice-President: Shigeo Katsu, ECA Vice-Presidency Country Director: Anand Seth, ECCU5

Sector Director: Alain Colliou, ECSPS Sector Manager: John Hegarty, ECSPS, Financial Management

Task Team Leader: Johannes Stenbaek Madsen, ECSPS, Financial Management

TABLE OF CONTENTS

PREFACE...........................................................................................................................I

EXECUTIVE SUMMARY ............................................................................................ IV

SUMMARY OF RECOMMENDATIONS AND TECHNICAL ASSISTANCE ACTION PLAN............................................................................................................XIII

CHAPTER 1: COUNTRY, ECONOMIC AND ADMINISTRATIVE BACKGROUND ............................................................................................................... 1

CHAPTER 2: ASSESSMENT FRAMEWORK ............................................................ 4

CHAPTER 3: BUDGETING ........................................................................................... 8 I. BACKGROUND AND ASSESSMENT FRAMEWORK ........................................................... 8 II . FINDINGS .................................................................................................................. 11 III. SUMMARY OF FINDINGS AND ASSESSMENT OF FIDUCIARY RISK.............................. 20 IV. RECOMMENDATIONS.......................................................................................... 21

CHAPTER 4: TREASURY AND CASH MANAGEMENT....................................... 22 I. BACKGROUND AND ASSESSMENT FRAMEWORK ......................................................... 22 II. FINDINGS................................................................................................................... 24 III. SUMMARY OF FINDINGS AND ASSESSMENT OF FIDUCIARY RISK.............................. 31 IV. RECOMMENDATIONS................................................................................................ 32

CHAPTER 5: ACCOUNTING AND FINANCIAL REPORTING ........................... 34 I. BACKGROUND AND ASSESSMENT FRAMEWORK ......................................................... 34 II. FINDINGS................................................................................................................... 36 III. SUMMARY OF FINDINGS AND ASSESSMENT OF FIDUCIARY RISK.............................. 43 IV. RECOMMENDATIONS................................................................................................ 43

CHAPTER 6: INTERNAL CONTROL AND INTERNAL AUDIT.......................... 45 I. BACKGROUND AND ASSESSMENT FRAMEWORK ......................................................... 45 II. FINDINGS................................................................................................................... 48 III. SUMMARY OF FINDINGS AND ASSESSMENT OF FIDUCIARY RISKS ............................ 56 IV. RECOMMENDATIONS................................................................................................ 57

CHAPTER 7: EXTERNAL AUDIT AND LEGISLATIVE OVERSIGHT .............. 58 I. BACKGROUND AND ASSESSMENT FRAMEWORK ......................................................... 58 II. FINDINGS................................................................................................................... 61 III. SUMMARY OF FINDINGS AND ASSESSMENT OF FIDUCIARY RISK.............................. 68 IV. RECOMMENDATIONS................................................................................................ 68

CHAPTER 8: LOCAL AND REGIONAL SELF-GOVERNMENT UNITS............ 70 I. BACKGROUND AND ASSESSMENT FRAMEWORK.......................................................... 70 II. FINDINGS................................................................................................................... 71 III. SUMMARY OF FINDINGS AND ASSESSMENT OF FIDUCIARY RISK.............................. 74 IV. RECOMMENDATIONS................................................................................................ 74

CHAPTER 9: CAPACITY DEVELOPMENT ............................................................ 75

I. RECENT TA ACTIVITIES IN THE FIELD OF PFM............................................................ 75 II. ASSESSMENT OF TA ABSORPTION CAPACITY, IMPACT AND COORDINATION .............. 76 III. GENERAL ASSESSMENT OF PFM CAPACITY DEVELOPMENT NEEDS........................... 77 IV. RECOMMENDATIONS................................................................................................ 79

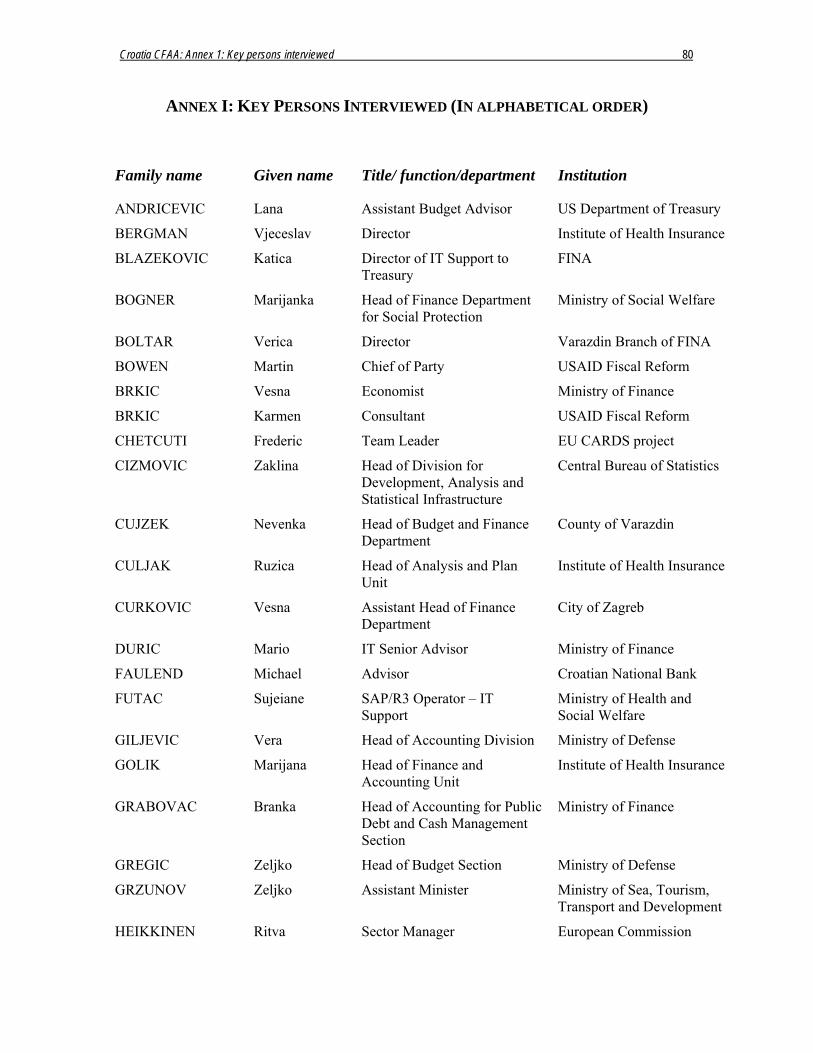

ANNEX I: KEY PERSONS INTERVIEWED (IN ALPHABETICAL ORDER) .... 80

ANNEX II. FIDUCIARY RISK INDICATORS AND INTERPRETATION........... 84

ANNEX III. OVERALL ASSESSMENT OF FIDUCIARY RISK ............................ 92

LIST OF TABLES AND BOXES

TABLE 1. STANDARDS AND CODES PROMOTING FINANCIAL ACCOUNTABILITY................... 4 BOX 1: PRINCIPLE OF SOUND FINANCIAL MANAGEMENT .................................................... 5 TABLE 2. FIDUCIARY RISK INDICATORS............................................................................... 5 TABLE 3. REVISED BUDGET PREPARATION CYCLE ............................................................ 13 TABLE 4. STATE BUDGET REVENUE AND EXPENDITURE OUTTURNS 2001-2003 ............... 16 TABLE 5 . VARIATION BETWEEN BUDGETED EXPENDITURE AND OUTTURN PER FUNCTION OF

GOVERNMENT ............................................................................................................ 18 BOX 2. THE TREASURY LEDGER SYSTEM.......................................................................... 23 BOX 3. TRANSACTION SYSTEM PROCESS ........................................................................... 28 TABLE 6. ANNUAL FINANCIAL STATEMENTS .................................................................... 38 BOX 4. INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL

AUDITING .................................................................................................................. 47 BOX 5. A WEAK INTERNAL CONTROL FRAMEWORK IN THE PUBLIC DEBT MANAGEMENT

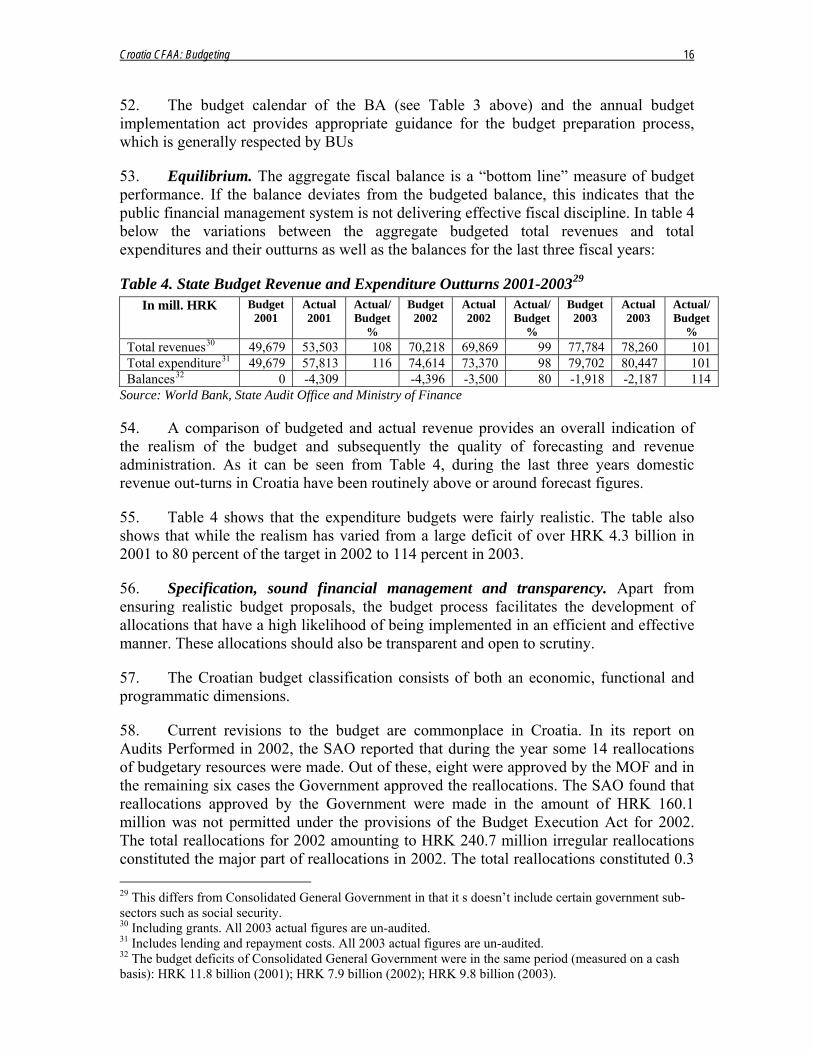

SECTION..................................................................................................................... 54 BOX 6 . FIFTEEN STEPS TO ESTABLISHING AN INTERNAL AUDIT UNIT............................... 56 BOX 7. OVERVIEW OF THE INTOSAI AUDITING STANDARDS ........................................... 59 TABLE 7. CARDS 2003 EXTERNAL AUDIT TWINNING PROJECT ACTIVITIES..................... 63 BOX 8. TASKS AND RESPONSIBILITIES OF TOWNS, MUNICIPALITIES AND COUNTIES .......... 71 BOX 9. EDIS ACCREDITATION CRITERIA. ANNEX TO COUNCIL REGULATION (EC,

EURATOM) NO. 1266/1999 ........................................................................................ 78

Croatia: Country Financial Accountability Assessment i

PREFACE

This report was prepared following missions to Croatia in December 2003 and March 2004 by a World Bank Task Team that consisted of Andy Macdonald (Consultant, Former Comptroller General and Chief Information Officer for the Government of Canada); Matthew Andrews, (Public Sector Management Specialist, ECSPE); and Johannes Stenbæk Madsen, (Task Team Leader, Financial Management Specialist, ECSPS).

The CFAA team would like to emphasize that the accuracy of this report’s findings and recommendations depended largely on the feedback from their Croatian counterparts, including State Secretary of the Ministry of Finance (MOF), Martina Dalić; Assistant Ministers to the MOF Amalija Ikšić, Josip Kulišić, Ivan Novačić and Niko Raič; as well as Assistant Auditors General Lidija Pernar, Ljerka Lindsbauer and Hrvoje Kordić.

The CFAA is based on discussions with public officials and an analysis of data gathered during the missions. The Parliament (the Sabor), the Government and the State Audit Office fully supported the CFAA missions and engaged in dialogue with the Bank team. Particularly important was the input of Šime Prtenjača, who as Head of the Sabor’s Budget Committee, provided essential insight to the processes relating to the external and parliamentary oversight of the Government.

Objectives and Scope of the CFAA

The CFAA is a diagnostic tool designed to enhance the World Bank’s knowledge of public financial management (PFM) and accountability arrangements in client countries. It supports both (a) the World Bank’s fiduciary responsibilities by identifying the strengths and weaknesses of PFM arrangements so that the potential risks to the use of Bank funds can be assessed and managed; and (b) the World Bank’s development objectives by facilitating a common understanding by the borrower, the World Bank, and development partners that leads to the design and implementation of capacity-building programs to improve the country’s PFM. CFAAs are not audits; they are not intended to be and they do not provide assurance on the specific uses to which World Bank funds have been or may be applied.

The overall objective of the CFAA is to provide relevant information to the World Bank and the government on the public sector financial accountability arrangements in Croatia and to jointly develop a program for reforms and capacity building to improve transparency and accountability for the use of public funds. To the extent that analytical work was already available, the CFAA has updated and deepened the knowledge in areas where more specific, detailed proposals are needed. Specific objectives of the CFAA include: (i) to update knowledge of primary public financial accountability institutions, and; (ii) to identify the most significant fiduciary risks and related capacity issues that require the Croatian government’s attention.

Croatia: Country Financial Accountability Assessment ii

Priority areas of Attention

While covering all key issues of the CFAA guidelines of May 2003, the CFAA explicitly identifies the international standards, codes and laws that constitute the assessment framework for this report. With a view to the specific requirements of the EU, and subsequently the Croatian administration’s preparedness for EU membership, the EC financial regulation1 constitutes an important part of the assessment framework for the priority areas listed below.

The following broad topics are addressed in the CFAA:

• Budgeting;

• Treasury and cash management;

• Accounting and financial reporting;

• Internal control and internal audit;

• External audit and legislative oversight;

• Financial accountability arrangements for sub-national government;

• Capacity development.

Benchmarking and Assessment of Fiduciary Risk

While covering the main issues of the World Bank’s internal May 2003 CFAA guidelines, the report also benchmarks the Croatian PFM system against the international standards, codes and laws that constitute the assessment framework (see Chapter on CFAA Assessment Framework, p. 5). Given the relevance of EU requirements to Croatia the EC financial regulation constitutes an important part of this framework.

As well as benchmarking against the standards, codes and international regulations, the CFAA also presents a normative rating of fiduciary risk for each component reviewed; it is based on a four-step scale, including low, moderate, significant and high2. For each of the components the fiduciary risk is rated using a set of indicators listed in Annex II. The annex also presents an interpretation of the indicators and an objective justification for the rating given for the individual PFM components. The methodology for fiduciary risk indicators and interpretations in Annex II was developed by World Bank staff and PEFA3 Secretariat staff, working with their PEFA partners, as performance indicators for PFM, as part of an effort to strengthen approaches to PFM reform. PEFA is a partnership program of the World Bank, the European Commission, the UK Department for International Development, the Swiss State Secretariat for Economic Affairs, the French Ministry of Foreign Affairs, the Norwegian Ministry of Foreign Affairs and the International Monetary Fund (IMF). The PFM performance indicators and interpretations

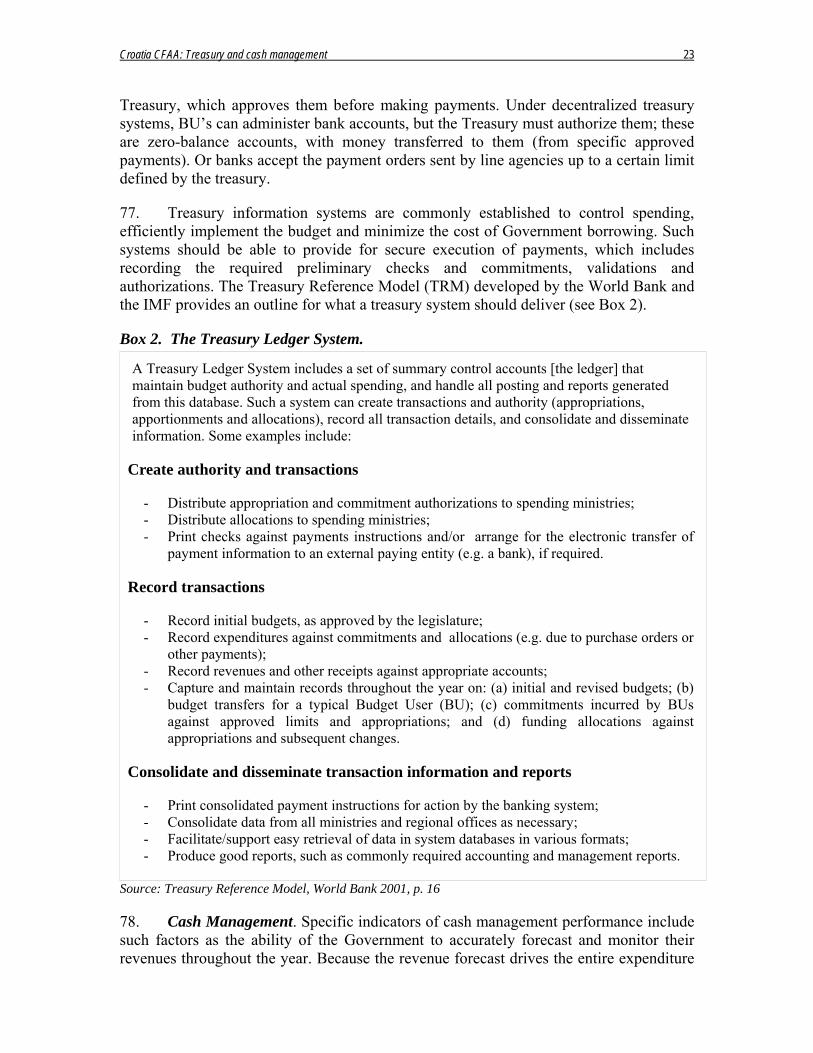

1 Council regulation No. 1605/2002 on the financial regulation applicable to the general budget of the European Communities. 2 The fiduciary risk is the risk of funds not being spent for the purpose(s) for which they were appropriated. 3 Stands for Public Expenditure and Financial Accountability.

Croatia: Country Financial Accountability Assessment iii

have recently been used in assessments of financial accountability arrangements in a number of other countries in Europe and elsewhere, including in relatively advanced and middle-income economies similar to Croatia.

Whereas the fiduciary risk ratings can be used for the purpose of comparison or benchmarking, they do not provide quantitative information about the probabilities of funds not being spent for the intended purposes.

For an overall risk rating and a summary of the fiduciary risk assessment, please see Annex III titled Overall Assessment of Fiduciary Risk. The detailed interpretation of the individual risk indicators is offered in Annex II.

Acknowledgements

The team acknowledges the extensive cooperation and assistance from the staff of various institutions that contributed to the CFAA, including officials and staff of the Government, State agencies and multilateral organizations. In addition, grateful thanks go to Country Director, Anand Seth; to Country Manager, Indira Konjhodžić; and to Operations Advisor, Albert Martinez, for taking a great interest and engaging in the work with the CFAA team. Further, the team would like to thank John Hegarty (Manager, Financial Management, ECSPS); Pascale Kervyn de Lettenhove (ECSPS); Ranjan Ganguli (ECSPS), Sanja Madžarević-Šujster (Senior Country Economist, ECSPE); Srebrenka Gudan (Consultant, ECSPE); Ljiljana Tarade (Assistant, ECCU5); the PAL team leader Satu Kahkonen (ECSPE); and peer reviewers Ritva Heikkinen (European Commission, EC Delegation Zagreb); Brian Olden (IMF, Fiscal Affairs department); Stephen MacLeod (OECD, SIGMA) and Simon Bradbury (World Bank, LOA), who offered much appreciated comments and inputs; and to Roula Balkash (Assistant, ECSPS); Susan Middaugh (Consultant, ECSPS) and Sioban Farey (Consultant, ECSPS) who assisted with the formatting and editing of this report.

Croatia CFAA: Executive Summary iv

EXECUTIVE SUMMARY

General

As a candidate country to the European Union (EU), Croatia currently focuses much of its modernization efforts on meeting the requirements of the acquis communautaire4. These include meeting the requirements related to Public Financial Management (PFM). In the EU accession context this primarily concerns Chapter 28 on financial control5 and the issues captured under the European Commission’s concept, Public Internal Financial Control (PIFC).

In this context, the relevance of the Country Financial Accountability Assessment (CFAA) is evident. It assesses the legal framework, institutional capacity and practices for the core financial control processes such as budgeting, treasury and cash management, accounting, financial reporting, internal control, internal audit, external audit and parliamentary oversight. In this CFAA, topics related to financial accountability arrangements for sub-national governments and PFM capacity development provide for a more complete analysis of the PFM arrangements and fiduciary risks. The basic approach of the CFAA has been to compare the PFM practices in Croatia with those promoted by relevant international standards also including a specific set of indicators of fiduciary risk.6

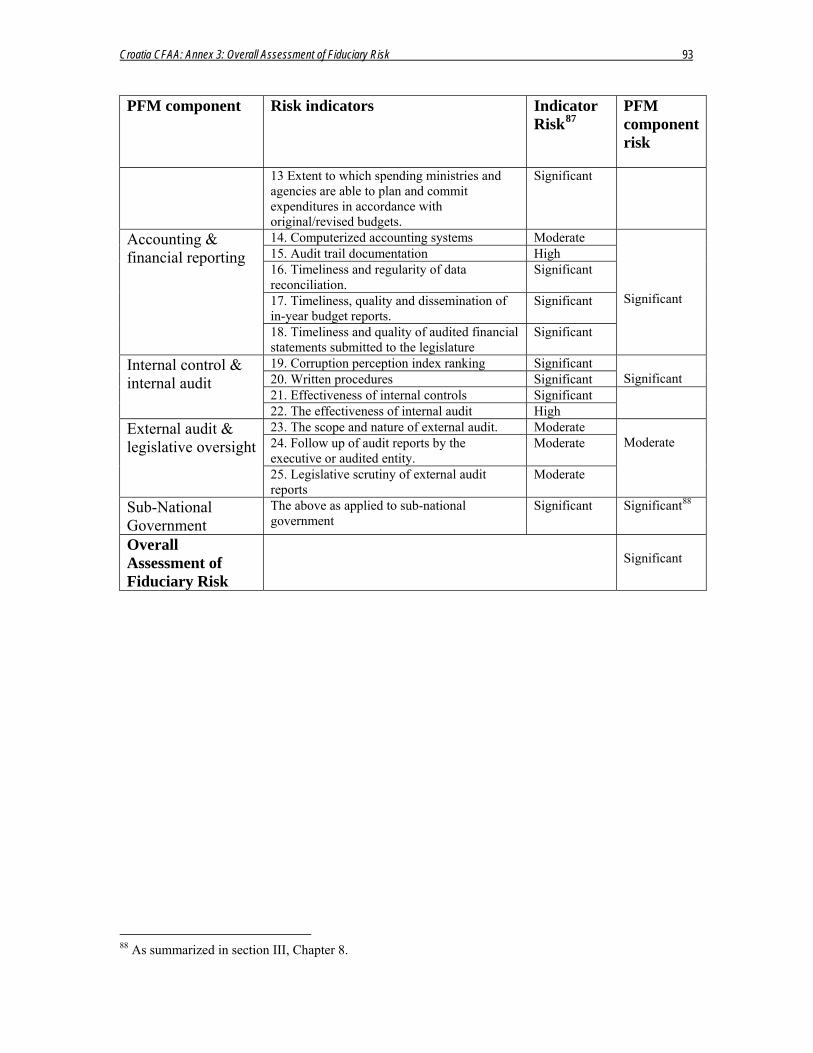

Having assessed the preceding aspects of PFM in Croatia, this report concludes that the overall fiduciary risk is significant.7

Most of the weaknesses in the PFM arrangements revolve around inefficiencies and weaknesses in the existing financial accounting and management systems. The Croatian Treasury within the Ministry of Finance (MOF) relies on a SAP8 payment and financial accounting system to process and record revenues and expenditures to and from a Treasury Single Account (TSA) held at the Croatian National Bank. Whereas the SAP system can process and record all payments made from the TSA, the Treasury has to rely on separate reports from Budget Users (BUs) for reconciliation and commitment accounting purposes. Although the most significant ones have now been integrated, several Extra-budgetary Funds and Agencies (EBFs) do not manage their finances via the

4 A French term which refers to the entire complex of European Community legislation that affects Member States of the European Union. 5 The European Council (of EU Heads of State and Governments) in Copenhagen in June 1993 decided that accession to the EU would require: (i) that the candidate country has achieved stability of institutions guaranteeing democracy, the rule of law, human rights and respect for and protection of minorities; (ii) the existence of a functioning market economy as well as the capacity to cope with competitive pressures and market forces within the Union; (iii) the ability to take on the obligations of membership, including adherence to the aims of political, economic and monetary union. Since then, the requirement under (iii) has been evaluated in 29 separate policy areas or “chapters.” Chapter 28 relates to financial control arrangements in the government administration. 6 The standards are listed in Chapter 2. Fiduciary risk indicators are listed in Table 2 of that chapter. 7 The fiduciary risk for the individual components of PFM as well as the overall fiduciary risk of the PFM system is measured on a scale from low, moderate, significant to high. See Annex III for Overall Assessment Fiduciary Risk and Annex II for a detailed interpretation of the specific risk indicators applied. 8 Trademark for a high capacity computerized payment and accounting system.

Croatia CFAA: Executive Summary v

TSA. There are a multitude of financial accounting and management systems among BUs and EBFs, which are not interfaced with the SAP system. The SAP system is under-utilized and the further rollout and development of the system is currently stalled by ineffective management. The Government’s decision to implement modified accrual-based accounting rules from the fiscal year 2002 was taken without due consideration of the state of the current system infrastructure. Consequently, the annual financial reporting from BUs and the compilation and presentation of the Government’s consolidated financial statements for the fiscal year 2002, were significantly delayed and contained unreliable data. This was further complicated by the adoption of an overly ambitious statutory reporting calendar for BUs.

The internal control framework9 of the Government administration has several weaknesses and is not supported by a general system of internal audit, though this is a statutory requirement of the organic Budget Act. Although the absence of internal audit means that an important assurance function for the efficient and effective functioning of systems is missing, the Government’s external auditor, the State Audit Office, does provide a basic external assurance function vis-à-vis Parliament (the Sabor). This report identifies shortcomings in the SAO’s legal framework and practices that could jeopardize its independence and thereby limit its effectiveness. At the local level the problems in the PFM arrangements identified at the national level also prevail. With respect to capacity development, the number of staff in key PFM functions, such as financial control, accounting and auditing, are inadequate and training capacities are lacking. Finally, the leadership role of the Ministry of Finance in reforming PFM is severely undermined by a lack of intra-ministerial coordination, management and administrative capacity in general.

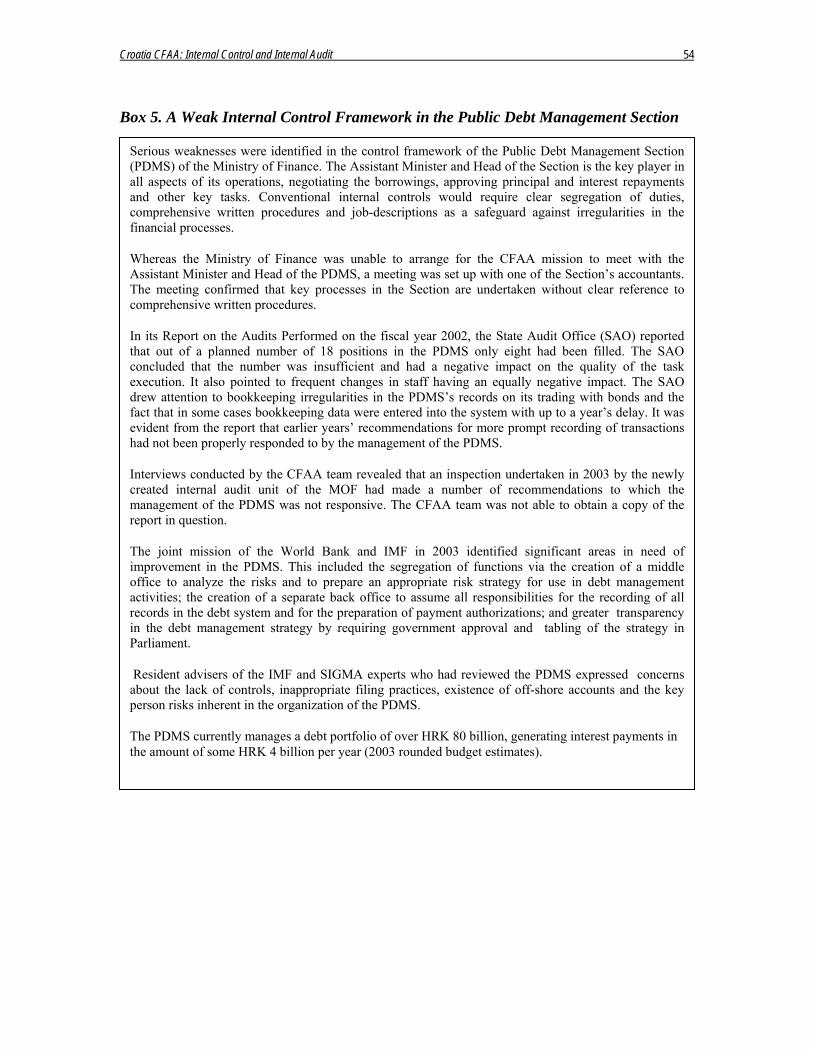

A specific and very serious deficiency identified in this report is the lack of a sound internal control framework in the Ministry of Finance’s Public Debt Management Section. The problems identified include a lack of appropriate segregation of duties, understaffing and a management with a history of ignoring technical advice, including advice from its auditors. These findings are corroborated by reports from the external auditor, the World Bank and IMF assessments. Considering the large sums of money involved, the CFAA recommends that the Croatian Government take action urgently to rectify the situation. See Box 5 in Chapter 6 for details.

This report offers a number of recommendations to address the identified shortcomings and to mitigate the associated risks. The following recommendations should be given the highest priority: (i) the Minister of Finance should assign an Assistant Minister to develop and implement a strategic vision for the future evolution and rationalization of the Government’s financial systems; (ii) the MOF should commission an independent systems audit of the SAP system; and (iii) the MOF should establish an inter-ministerial steering committee led by the State Secretary to oversee the development of the SAP system. The Government has started taking a number of actions in this field, including the undertaking of a study of existing financial management information systems and the drafting of a financial management information system development strategy.

9 As defined by COSO – the Committee of Sponsoring Organizations of the Treadway Commission.

Croatia CFAA: Executive Summary vi

In addition to the above, a number of recommendations should and could be implemented almost immediately. These include: (i) the MOF already completed and issued the Rulebook on internal audit as referred to the organic Budget Act (BA)10; (ii) the MOF initiating the legislative changes needed to establish internal audit in the most significant EBFs; (iii) BUs and MOF appointing financial controllers as required by the BA, and; (iv) the State Audit Office initiating the proposed legislative changes to the Act on State Audit. For all aspects of Public Financial Management, this report points out specific challenges that Croatia is facing in its endeavor to meet the benchmarks represented by the acquis communautaire and the requirements for Public Internal Financial Control (PIFC).

A more detailed assessment of specific elements of PFM, recommendations on how to modernize PFM in line with relevant international standards and the importance of mitigating fiduciary risks are summarized below:

Budgeting

The lack of budget comprehensiveness poses a fiduciary risk. Although the organic Budget Act of 2003 included the regulation of key aspects of the EBF’s (Extra-budgetary Funds and Agencies) budget preparation and financial management, EBFs remain excluded from certain provisions of that Act, including provisions requiring internal audit.

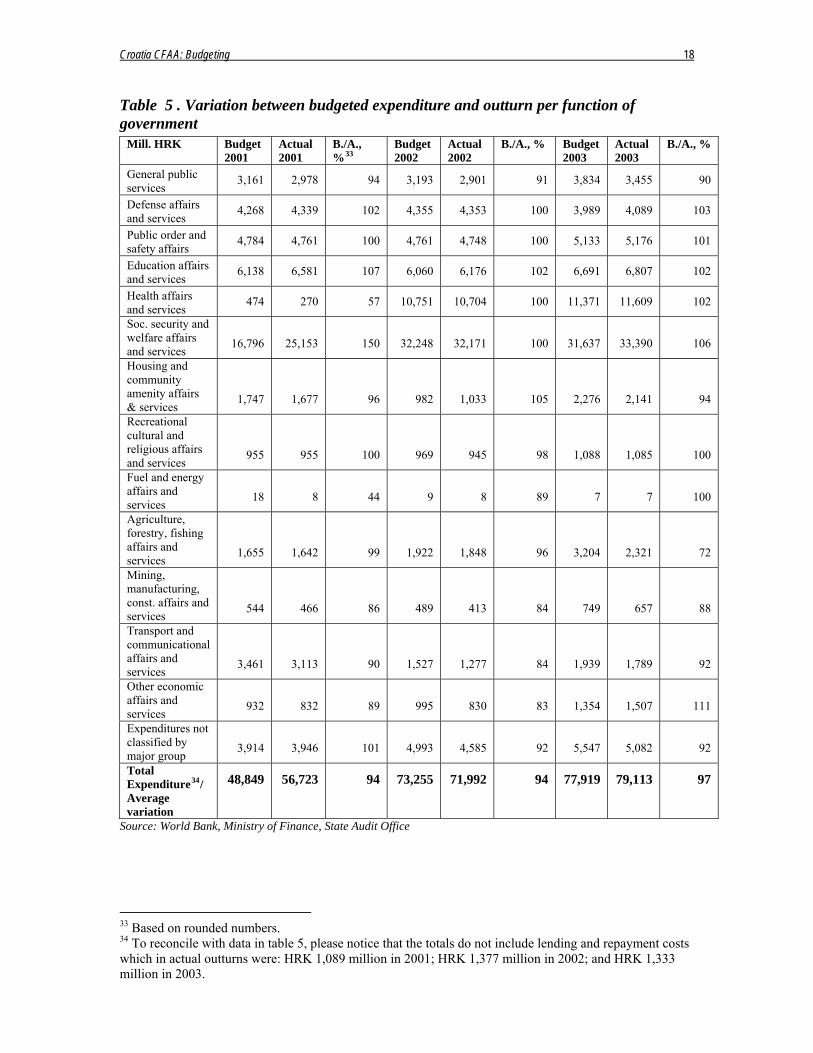

The current process for preparing and revising the budget appears to promote budget realism, but it does not provide for strategic budgeting or for the effective monitoring of allocations. The budget classification includes administrative, economic, functional and programmatic classifications but the budget as it is presented to Parliament offers little information or direction about policies and strategies. The frequent budget revisions in the course of the year could also undermine the strategies and policies that might be reflected in the budget. Still, the variations between budget figures and actual outturns at the functional level of the budget are generally small. The Ministry of Finance, which has very limited policy analysis capacity, does not analyze budget proposals to assess their strategic content. While the strong performance of budgets in achieving targets thus suggests low fiduciary risk, there is a moderate risk that the budget will fail to ensure efficient and effective resource allocations.

Budget users are given clear guidance for the preparation of budget submissions and generally adhere to the budget calendar. The budget does not as yet provide the type of information required to show key expenditure types or policy development. The program and medium-term budgeting innovations are tenuous, dependent on significant capacity building and cultural change in the Ministry of Finance and in the line ministries. Furthermore, this kind of budgetary approach requires a more active role of the Parliamentary oversight committee. Whereas parliamentary scrutiny covers aggregates and detailed estimates of expenditure and revenue, Parliament (the Sabor) appears to 10 By the time of the report release, the MOF issued the Rulebook in August 2004.

Croatia CFAA: Executive Summary vii

have accepted a limited oversight role and weak administrative capacity. There is a risk that the budget will continue to fail to reflect a strategic, medium-term policy agenda and to facilitate transparency.

Considering the different indicators, the CFAA finds the fiduciary risk associated with budgeting to be moderate. The CFAA recommends that the MOF:

• Integrate all EBFs into the State budget and the Treasury Single Accounts system or alternatively make them subject to the similar budgeting, control and audit arrangements.

• Build on its recent work in the Bureau of Macroeconomic Forecasting to further strengthen the forecasting function in the Ministry of Finance in order to ensure full transparency and timely production of forecasts, and enhanced usefulness to Budget Users (BUs).

• Strengthen the Medium Term Expenditure Framework, based on a program classification and multi-year forecast.

• Develop further the analytical capacity in the budget process by training budget analysts in the Ministry of Finance and line ministries.

• Strengthen the role of the Parliamentary Budget Committee by focusing its mandate on budget analysis and improving its technical support.

Treasury and Cash Management

There is a multiplicity of financial management systems that are uncoordinated and un-regulated. In addition, the strategic advantages of relying more on the main service provider FINA,11 for the continued development the SAP system and other financial systems among BUs, have not been considered. The future development of the Treasury’s SAP system and its relationship to a large number of independent, uncoordinated financial accounting systems in budget entities has not been defined. This report suggests that components missing from the Treasury SAP system have increased the risk of budget over-expenditures. The absence of a multi-period commitment control module and the lack of any development activity to implement it is a serious shortcoming. Moreover, the cash management module’s partial implementation increases the risk of inefficient cash management and potential estimation errors in the budget releases to budget entities that result in expenditure arrears. The most recent available data suggests that Government arrears constitute six percent of the Government’s consolidated budget. This indicates that there is a significant risk that Government payments are not made on time.

The implementation and development of the Treasury’s SAP system has not had the strong management direction and support that such projects require. There is no senior MOF manager of the system who can establish clear requirements and deadlines, and drive the project team to succeed. Nor is there evidence of strong involvement by those MOF units that are the logical users of the system; and line ministry staff are also

11 The Financial Agency, Croatian abbreviation.

Croatia CFAA: Executive Summary viii

conspicuously absent. This situation guarantees that the requisite systems changes will not occur in the timeframe that is necessary; projects of lower priority or questionable value may be implemented at significant cost and limited benefit. A clear review of the entire project by an independent, outside expert, is warranted.

The existence of some 3,200 budget user bank accounts in private banks poses a fiduciary risk to the average HRK 500 million cash balances on deposit. In addition to being an example of poor cash management, this situation increases the fiduciary risk.

In summary, the risk resulting from the Treasury and cash management systems is rated as significant.

The CFAA recommends that the MOF:

• Assign to an Assistant Minister the responsibility for the formulation and implementation of a strategic vision for the future evolution and rationalization of all of the financial systems in the Government of Croatia. To ensure management ownership of the SAP systems, the same Assistant Minister should be responsible for the MOF System Improvement Section;

• Commission an independent systems audit of the SAP system by an

internationally recognized external auditor or management consultancy with extensive financial and IT experience. The audit should investigate, among others, means to increase SAP’s functionality for both the MOF and the BUs;

• Establish a Steering Committee, chaired by the State Secretary with senior representation from all affected MOF sectors, BUs, ministries and FINA, to oversee the development of SAP. This body could also assist in the development and implementation of the strategic vision for the evolution of the Government’s financial systems;

• Implement the Treasury Single Account (TSA) by closing all entity private bank accounts and consolidating them into the TSA.

• Immediately implement the SAP module to process multi-period commitments.

Accounting and Financial Reporting

A significant improvement was made as the MOF, for the first time, presented a set of consolidated financial statements for the execution of the state budget 2002. The recording and processing of transactions was, however, not prompt and it prevented a timely aggregation at the line ministry and MOF level. For the same reason, the consolidated financial statements for the state budget were not prepared within the statutory deadline, which seemed ambitious when compared to the deadlines set out in the EC financial regulation. Consequently, the SAO’s audit of the consolidated financial statements for the fiscal year 2002 was partly based on draft statements. One of the reasons for the delays in reporting appear to have been the change of accounting rules, involving an ambitious acceleration of the time-line for the BUs’ compilation of their

Croatia CFAA: Executive Summary ix

financial statements. The changes also involved an equally ambitious move from cash to modified accrual-based accounting principles. This move was only partially successful. Furthermore, the change does not affect the accounting entries for expenditures at the Treasury, which continues to be done on a cash basis. Due to the set-up of the Treasury’s SAP system it cannot generate a complete electronic audit trail for all types of transactions. In conclusion, accounting data related to the execution of the expenditure budget 2002 were most likely not reliable. Adding to the fiduciary risk is the existence of a multitude of accounting systems, which are often outdated and do not meet current standards for security and data protection. Based on the preceding, the fiduciary risk associated with accounting and financial reporting is considered significant.

Based on the above the CFAA recommends MOF should:

• Take action to ensure that the statutory rulebooks12 and appropriate guidelines and training opportunities be offered to all accountants and other staff of Budget and Finance Units of all BUs in order to ensure an effective implementation of the new accounting rules.

• Reinforce the State Accounting and Financial Reporting Section, in order to be able to provide more support to BUs in the application of the new accounting rules, including the statutory formats and deadlines for financial reporting.

• Extend the statutory deadlines for delivery of the annual financial statements and initiate the necessary amendments of the Budget Act and the Ordinance on Financial reporting and Budgetary accounting (OFB).

• Prioritize the recruitment of accountants and other accounting staff given the profundity of the current reform the Government should make and the importance of increasing capacity.

• Consider a strategy to effectively support a modernization of the state administration’s accounting system, which should be based on a detailed review and due consideration of different possible solutions.

Internal Control and Internal Audit

Whereas a number of Rulebooks and regulations provide the regulatory framework for procedures and physical controls, a proper segregation of duties, appropriate staffing, exemplary management behavior and other key components in a sound internal control framework often do not exist. The Public Debt Management Section of the MOF offers one such an example. Also, there are numerous examples of Rulebooks mentioned in laws, which have not yet been issued. The Budget Users’ financial controllers required by the Budget Act (BA) have typically not yet been recruited or assigned to the task. The current control environment is not robust enough to mitigate the risk of official corruption and conflicts of interest. The introduction of internal audit via the BA is a positive development. The CARDS project in support of establishing internal audit units (IAUs) is well conceived and has a realistic and robust plan for a progressive implementation across the Government. It must be strongly supported because it offers

12 As required by the Organic Budget Act.

Croatia CFAA: Executive Summary x

the best path to conformance with Chapter 28 of the acquis communautaire and a PIFC-compliant internal control and audit system. The CFAA offers practical guidance for BUs, who wants to establish such a unit. Weighing the different fiduciary risk indicators, the CFAA finds the risk associated with the internal control framework, including internal audit to be significant.

The CFAA recommends that:

• The MOF eliminate the identified weaknesses in the internal control framework of the Public Debt Management Section of the MOF, given considerable risks and the large sums involved.

• The MOF issue all statutory Rulebooks and the necessary detailed guidelines that concern internal control as a matter of priority. MOF and other BUs must subsequently take steps to develop appropriate written procedures for financial processes.

• The MOF establish an internal audit function by proposing changes in laws affecting all EBFs, and key entities receiving or managing public funds, with the inclusion of FINA.

• The BUs should hire an individual or assign an existing staff member as soon as possible, to perform the role of Financial Controller in accordance with the provisions of the BA. This should be a person other than the Chief Accountant.

• The MOF provide a strong champion for change for the new internal control and audit system, and should develop and promulgate its draft PIFC policy with a vision of its internal control system and a strategic vision of its internal control system that is consistent with the Budget Act and the ongoing EU funded technical assistance activities.

External Audit and Parliamentary Oversight

The Act on State Audit provides a broad mandate for those public funds and institutions that it is required to audit as well as the audit standards and methods it can apply. However, the act has shortcomings that should be addressed by the State Audit Office (SAO) and Parliament (the Sabor) as a matter of priority.

One shortcoming is that the SAO is not formally required to provide a statement of assurance on the execution of the state budget. The SAO is however required to report to the Sabor annually on the audits performed and it does offers an opinion based on audits of the full set of Government financial statements. Due to the nature of its legal mandate and the methods applied this however does not constitute a formal statement of assurance on the Government consolidated financial statements or the execution of the state budget.

The SAO’s legal framework does not guarantee its financial independence from the government, which currently makes it subject to the MOF’s budget supervision. Whereas the Act on State Audit (ASA) explicitly provides a mandate for it, the SAO still has not piloted any audits of economy, efficiency or effectiveness. The SAO’s reports are

Croatia CFAA: Executive Summary xi

perceived to be authoritative and the Sabor acts on audit recommendations. There are indications that the Sabor considers the SAO’s reports rather narrow in focus and scope. The combined fiduciary risk associated with external auditing and Parliamentary oversight is considered moderate.

The CFAA recommends:

• The ASA be amended to ensure that the SAO budget is presented directly to Parliament without prior adjustments by the MOF. The MOF’s right to exercise budget supervision over the SAO should subsequently stop, while the annual financial statement of the SAO be made subject to an independent external audit appointed by Parliament.

• The ASA be amended so that the SAO will be formally required to submit a statement of assurance on the execution of the State Budget as to whether the Government’s consolidated financial statements gives a true and fair view of its financial position and the sources and uses of funds. In doing so, the SAO should seek to apply the International Standards on Auditing (ISA) and develop its competencies accordingly.

• The ASA should be amended to allow the SAO to audit all EU funds. The SAO should consider positively the challenge of auditing and becoming a certifying body for future EU funded programs in Croatia.

• SAO take concrete initiatives to pilot audits of economy, efficiency and effectiveness (performance or value-for-money audits) in line with the recommendations of the 1999 CFAA, the 2002 SIGMA peer review and the World Bank’s Public Expenditure and Institution Review 2002.

• The SAO and the Sabor should jointly consider the establishment of a specialized Public Accounts Committee, for example, as a sub-committee of the Budget Committee.

Sub-national Government

On the whole, the budgeting practices of sub-national governments are sound. They provide reasonable assurance that the budget reflects the priorities of local and regional interests and political parties. These practices also effectively prevent over-borrowing at the sub-national level and the generation of contingent liabilities at the state level. That being said, the existence of a great number of bank accounts owned by local government increases the risk of public funds following channels outside the formal processes set out in the BA. The ongoing process of decentralization, combined with recent changes in accounting rules have caused problems in the reliability of financial reporting to the MOF, The SAO provides external audit arrangements with appropriate frequency and provides a safeguard against the misuse of funds. The SAO’s resources are, however, spread thinly at the sub-national level. Generally speaking, the transparency of the PFM system seems greater at the sub-national level than at the state level. More direct lines of accountability between the citizen and the elected representative should reinforce this. Based on the concrete concerns related to cash management, the reliability of financial

Croatia CFAA: Executive Summary xii

reporting and internal control, the fiduciary risk associated with the PFM and financial accountability arrangements for sub-national governments is rated significant.

The CFAA recommends the following:

• The MOF should issue all the statutory rulebooks and guidelines on internal audit and accounting referred to in the Budget Act, which also applies to sub-national government. Furthermore, it should offer appropriate training for their effective application. Local and regional administrations should prepare to implement the intentions of the new act, including steps to establish Internal Audit Units.

• The practice of engaging and educating citizens in local budget expenditures, as done in the town of Varazdin, is a best practice in ensuring transparency and accountability. The concrete practice of public campaigns (for example, via the distribution of flyers) to inform citizens about the use and sources of the local budget should be expanded to other sub-national government administrations.

Capacity Development

The number and capability of staff in newly established and specialized PFM functions are inadequate; financial controllers and internal auditors are one such example. In addition, staff responsible for bookkeeping, accounting and financial reporting do not know how to undertake the changes to the accounting regime required by the Budget Act. A similar situation exists for the Ordinance on Financial Reporting and Budgetary Accounting (OFB) for Budget Users. These professional groups are essential to the PFM; and the Croatian government needs to address this problem, which can also have an impact on the administration’s ability to develop implementing agencies for EU pre-accession and structural funds.

The CFAA recommends that MOF should:

• Designate a responsible senior management position at the Director level (minimum) to oversee the development of the comprehensive training strategy, in consultation with the donor community, planned and current training providers and the professional associations of accounting and auditing in Croatia.

Croatia CFAA: Summary of Recommendations and Technical Assistance Action Plan xiii

SUMMARY OF RECOMMENDATIONS AND TECHNICAL ASSISTANCE ACTION PLAN

TA Timing13Summary of Recommendations Proposed Development Activities Responsibility

BUDGETING (MODERATE RISK)

1. Integrate all existing EBFs into the State budget and the Treasury Single Accounts system, or alternatively make them subject to similar budgeting, control and audit arrangements.

2. Strengthen the forecasting function in the Ministry of Finance.

3. Strengthen the Medium Term Expenditure Framework, based on a program classification and multi-year forecast.

4. Develop further the analytical capacity in the budget process by training budget analysts in the Ministry of Finance and line ministries.

5. Strengthen the role of the Parliamentary Budget Committee by focusing its mandate on budget analysis and improving its technical support.

Assistance to develop program budgeting and the comprehensive budget manual (3) can be provided from the on-going US treasury project and the WB IDF Grant for Strengthening Budget Manamagent. Assistance the implementation of other recommendations may also be provided from the USAID Fiscal Reform Project and the European Union’s CARDS 2005 program. It should however be noted that the USAID fiscal reform project comes to an end in September 2004. For more accurate references to these projects, see Chapter 9.

Parliament

(Sabor) Council of Ministers (COM)

Ministry of Finance (MOF)

Short Term

(1)-(3) Medium

Term (4)-(5)

13 Short term = < 1year; Medium term = 2-4 years; Long term = > 4 years.

Croatia CFAA: Summary of Recommendations and Technical Assistance Action Plan xiv

Summary of Recommendations Proposed Development Activities Responsibility TA Timing

TREASURY & CASH MANAGEMENT (SIGNIFICANT RISK)

1. The MOF should assign to an Assistant Minister the responsibility for the formulation and implementation of a strategic vision for the future evolution and rationalization of all of the financial systems in the Government of Croatia and to be responsible for the MOF System Improvement Section.

2. The MOF should initiate an independent systems audit of the SAP system by an internationally recognized external auditor or management consultancy with extensive financial and IT experience.

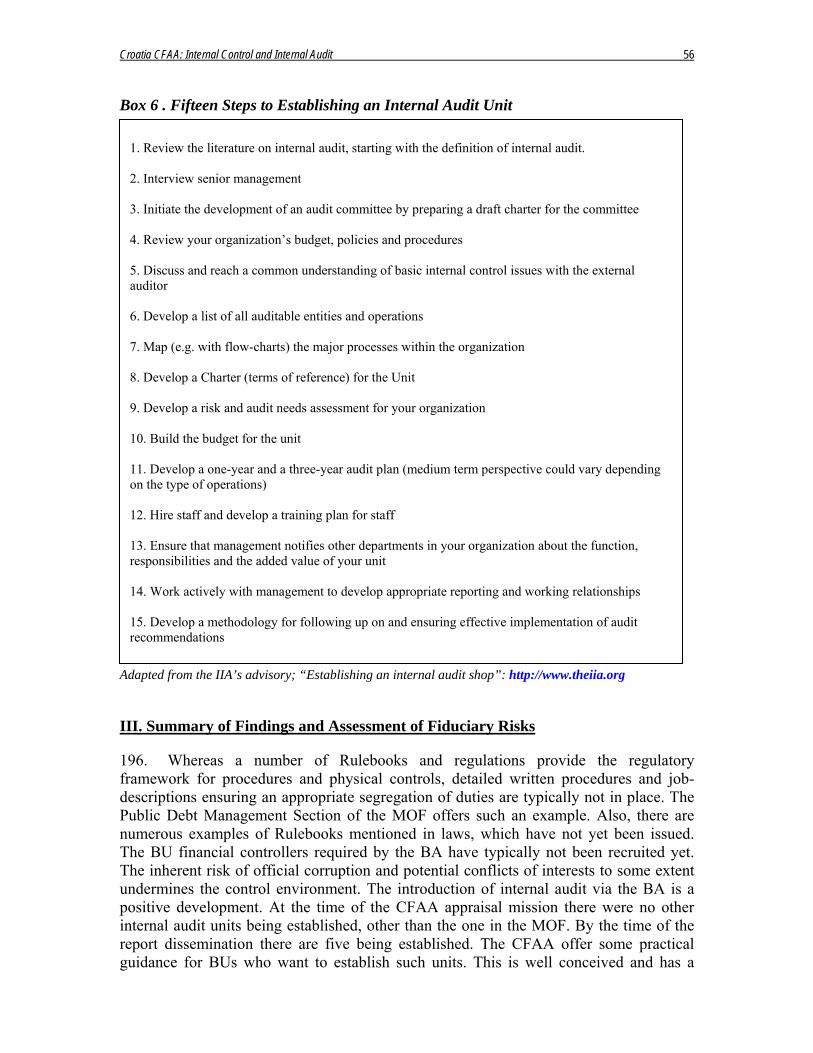

3. The MOF should establish a Steering Committee, chaired by the State Secretary with senior representation from all affected MOF sectors, line ministries and FINA, to oversee the development of SAP and assist in the development and implementation of the strategic vision for the evolution of the Government’s financial systems.

4. The MOF should implement the Treasury Single Account by closing all entity private bank accounts and consolidating them into the TSA.

5. The MOF should immediately implement the SAP module to process multi-period commitments.

(1), (3), (4) and (5) to be initiated immediately by the MOF. FINA with the support of MOF could initiate implementation of recommendation (6). Funding for (2) may be available from the EU, but could be advised by World Bank specialist. For more accurate project references, see Chapter 9.

Government/COM

MOF

Short Term

(All)

Croatia CFAA: Summary of Recommendations and Technical Assistance Action Plan xv

Summary of Recommendations Proposed Development Activities Responsibility TA Timing

ACCOUNTING & FINANCIAL REPORTING (SIGNIFICANT RISK) 1. The MOF should take action to ensure that all statutory rulebooks and other appropriate guidelines and training opportunities be offered to the staff of all Budget Users’ (BUs) Budget and Finance Units (BFUs). 2. The State Accounting and Financial Reporting Section of the MOF should be reinforced in order to be able to provide more support to BUs in the application of the new accounting rules. 3. The MOF should extend the statutory deadlines of delivery of the annual financial statements and initiate the necessary amendments of the Budget Act and the Ordinance on Financial and Budgetary Accounting (OFB). 4. The current reform the Government should make the recruitment of accountants and other accounting staff a matter of priority. 5. The MOF should consider a strategy to effectively support a modernization of the state administration’s accounting systems, which should be based on a detailed review and due consideration of different possible solutions.

Besides the more immediate action that the Government needs to adopt, recommendation (1) could be implemented with the assistance from the CARDS 2002 Public Debt Management project and the joint World Bank-IMF program on Central Government Management and debt Market. Technical assistance not currently available. Additional budgetary resources will be required.

MOF

Short Term

(1) Medium

Term (2)+(3)

Croatia CFAA: Summary of Recommendations and Technical Assistance Action Plan xvi

Summary of Recommendations Proposed Development Activities Responsibility TA Timing

INTERNAL CONTROL & INTERNAL AUDIT (SIGNIFICANT RISK) 1. The Government should take immediate action to eliminate the weaknesses in the internal control framework of the Public Debt Management Section of the MOF. 2. The MOF should issue all statutory Rulebooks and other necessary guidelines relating to internal audit and internal control. 3. The MOF and other BUs should take steps to develop appropriate, detailed written procedures for financial processes. 4. Propose changes in law to require an internal audit function to be established in all EBFs and any other entities that receives or manages public funds, including FINA. 5. Budget Users should hire individuals or assign responsibilities to existing staff in order to establish a Financial Controller in accordance with the provisions of the Budget Act. 6. The MOF should provide a strong champion of change for the new internal control and audit system, and should develop and promulgate its draft PIFC policy paper with a strategic vision of its internal control system and a risk-assessment based approach to management, that is consistent with the Budget Act and the ongoing EU funded technical assistance activities.

Most of the issues are addressed under the CARDS 2002 internal audit and PIFC project. In terms of follow-up, the European Commission has indicated that it has only programmed the roll out of internal audit to lower levels of government in connection with CARDS 2004, whereas the CARDS 2002 project focuses on the central level of the government administration. A PIFC Development Strategy was adopted by the Government and the MOF in September 2004. The Rulebook on internal audit was issued in August 2004.

MOF

CARDS project on PIFC and internal audit

Short Term

(1)-(3)

Medium Term (4)

Croatia CFAA: Summary of Recommendations and Technical Assistance Action Plan xvii

Summary of Recommendations Proposed Development Activities Responsibility TA Timing

EXTERNAL AUDIT & PARLIAMENTARY OVERSIGHT (MODERATE RISK) 1. The ASA should be amended to ensure that the SAO budget is presented directly to Parliament without prior adjustments by the MOF; the annual financial statement of the SAO should be subject to an independent external audit appointed by Parliament.

2. The ASA should be amended so that the SAO will be formally required to produce a positive statement of assurance on the execution of the State Budget while seeking to apply ISA.

3. The ASA should be amended to allow the SAO to audit all EU funds and SAO should consider positively the challenge of auditing future EU funded programs in Croatia.

4. In line with the recommendations of the 1999 CFAA, the 2002 SIGMA peer review and the 2002 PEIR, it is recommended that the SAO take concrete initiatives to pilot audits of economy, efficiency and effectiveness (performance or value-for-money audits).

5. The SAO and the Sabor should jointly consider the establishment of a specialized Public Accounts Committee, for example as a sub-committee to the Budget Committee.

The necessary technical assistance could be provided from the CARDS 2003 twinning project. For accurate reference see Chapter 9.

SAO Sabor

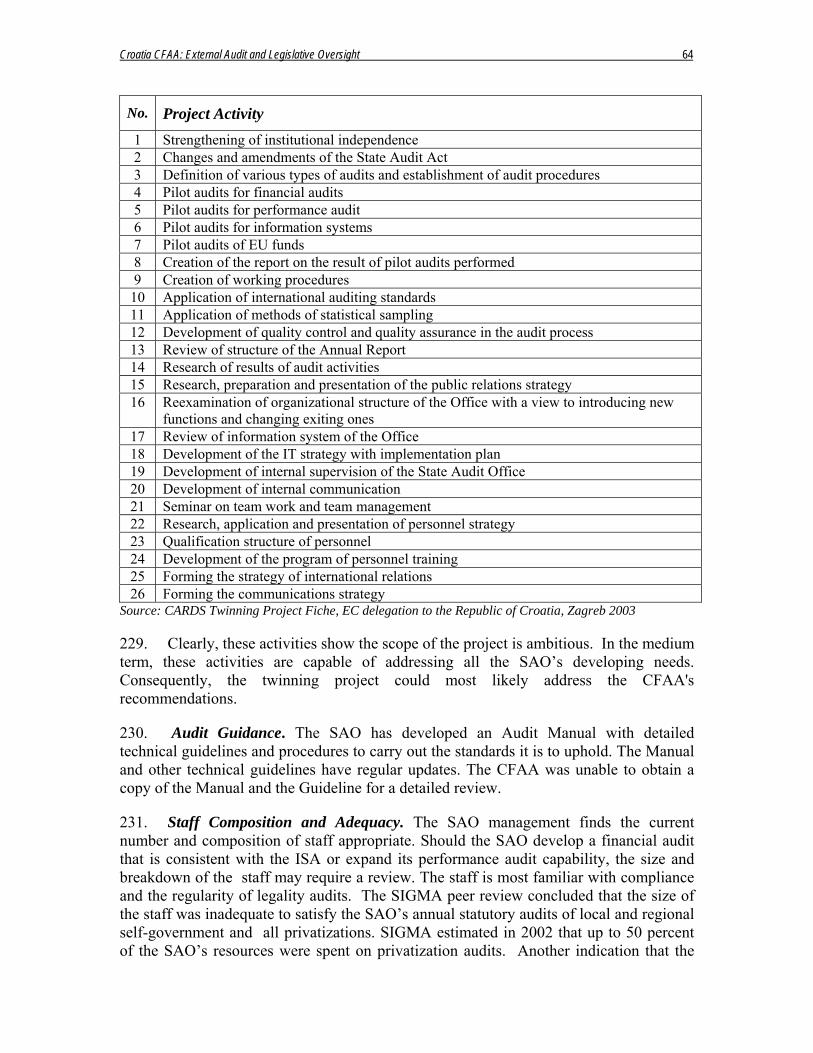

Short Term

(1), (4)

Medium term

(2), (3), (5)

Croatia CFAA: Summary of Recommendations and Technical Assistance Action Plan xviii

Summary of Recommendations Proposed Development Activities Responsibility TA Timing

SUB-NATIONAL GOVERNMENT (SIGNIFICANT RISK) 1. As at the state level, the MOF should issue all the statutory14 rulebooks and guidelines on internal audit and accounting referred to in the BA; the MOF should also offer appropriate training for their effective application. In addition, local and regional administrations should prepare to implement the BA new intentions, including steps to establish IAUs.

2. The practice of engaging and educating citizens in local budget expenditures, as done in the town of Varazdin, should be expanded to other sub-national government administrations.

Implementation of (1) could be supported by the EU’s CARDS 2004 program.

MOF

Short Term

14 As required by the organic Budget Act.

Croatia CFAA: Summary of Recommendations and Technical Assistance Action Plan xix

Summary of Recommendations Proposed Development Activities Responsibility TA Timing

CAPACITY DEVELOPMENT 1. Designate a responsible senior management position at Director level (minimum) to oversee the development of a comprehensive training strategy, in consultation with the donor community, planned and current training providers and the professional associations of accounting and auditing in Croatia.

Technical Assistance may be needed, but significant budgetary resource must be mobilized.

COM MOF

Donors

Medium

Term (All)

Croatia CFAA: Country and Economic Background 1

CHAPTER 1: COUNTRY, ECONOMIC AND ADMINISTRATIVE BACKGROUND

Economic Background 1. Currently, Croatia’s economy is characterized by a slowdown. The industrial output growth rate has recovered slightly following a period of stagnation; it has generally low growth rates, low inflation and high unemployment. In the fourth quarter of 2003, industrial production reached a 5.6 percent annual growth rate. In the same period the Consolidated General Government deficit reached HRK 3.5 billion or approximately 1.8 percent of GDP. In the last quarter of 2003, public debt was 55.5 percent of GDP15. The growth in Croatia’s public debt has become an issue of concern. The repayment costs, including interests have been steadily increasing from HRK 2.4 billion in 1999, to an estimated HRK 4.5 billion in 2003, or close to 5 percent of total expenditure of the general government16.

2. Croatia’s relationship to the EU is defined via the Stabilization and Association Agreement (SAA). The process of approaching the EU included the initiation of reforms in all areas of the acquis communautaire, including those linked to financial control (Chapter 28). Following the European Commission’s positive communication of April 20, 2004, concerning Croatia’s application for EU membership, Croatia formally became a candidate country to the European Union (EU).

3. In its opinion of April 2004, the European Commission stated that Croatia could be considered a functioning market economy. The Commission also noted however, that the working of market mechanisms still was in need of some improvement. Among the issues emphasized by the Commission was the fact that enterprise restructuring and privatization has been slower than expected and that certain large state and formerly socially-owned enterprises continues to play a significant role in the economy. Also, the need for reforms of the fiscal and social security systems as well as the public administration were said to be in-complete. The Commission also stressed that fiscal consolidation needed to be vigorously pursued.

Administrative Background

4. The Croatian budgetary system has undergone several reform or reform attempts during the last three to four years. This has included a change of accounting principles; the first consolidation of the government’s accounts; the addition of budget classifications; the initiation of program budgeting; the introduction of a Treasury Single Account and a computerized Treasury system. In fact, the development of a treasury system had already started by 1995. At the same time, the administrative capacity of the key institutions for budgetary control has been called into question. It has been argued that the amounts allocated for professional improvement of budget professionals of Parliament, Government (Council of Ministers) and Ministry of Finance are insufficient. This argument is being supported by the fact that even when the budgets for the three institutions have steadily increased over the last three FYs, the budgets for professional

15 World Bank data. 16 Newsletter of the Institute of Public Finance, No. 12, December 2003

Croatia CFAA: Country and Economic Background 2

training have not or they continued to be financed at a very modest level17. To judge from the current debate among professionals in Croatia, it seems evident that the Public Financial Management system is under some stress, which is bound to influence the regularity and effectiveness of services in key administrative bodies such as the Ministry of Finance.

5. Stress on the administration also appears to be generated from deficiencies in the framework for the civil service in general. The Law on Civil Servants and Support Staff of 2001 provides a legal basis for the status of civil servants. The Law does not make any distinction between state officials (political appointees; they are covered by a separate legislation) and civil servants, thereby leaving unresolved issues such as status, role and obligations of political personnel in the civil service, tenure of political appointees within the civil service, modalities for the conversion of the status of political appointees to that of civil servants. The current number of administrative rulebooks and inconsistencies between them create the conditions for a multitude of civil service management standards. The Law suffers from further deficiencies, especially with regard to a system of promotions, mobility, separation from service and disciplinary measures. The rules governing recruitment and selection of candidates could also be improved. A point of discussion is whether the salaries of civil servants are too low to attract adequate numbers of young and educated professionals to work in the state administration, especially as they have to have the same or higher education than those working in other sectors. There is no central training institution for civil servants, or a Government training program. However, following the adoption of the Law on the Organization and Scope of the Ministries and State Administrative Organizations of December 22, 2003 and a Decree on the Internal Structure of the Central State Office for Administration adopted in January 2004, a Civil Service Training Center for training and education of state employees has been created. Also, a new draft Civil Service Law has recently been prepared with assistance from the EU’s CARDS 2001 program. If approved in Parliament, the law will bring Croatian legislation into line with EC standards.

6. The backbone of public financial management in the former Yugoslavia was the Social Accounting Service, which was the sole institution responsible for executing financial transactions within the Yugoslav territory. In 1993, the Service on Croatian territory was transformed into the Institute for Payment Transactions (ZAP), which gradually improved the technological and organizational aspects of its business, while maintaining its monopoly on a number of basic banking services. Although a monopoly, it gained a reputation of efficiency in its operations, which included processing of some 500,000 transactions in real time on a daily basis. With the government’s reform of the transactions system, certain ZAP services were discontinued to allow the development of a competitive market for financial services in Croatia. Continuing its operation under the name FINA (Financial Agency) the institution today plays a major role both in collecting state revenues, handling cash and providing system support and maintenance for the Treasury. In this respect FINA is a unique institution. With its 179 branches, sub-branches and offices it plays a key role in Public Financial Management in Croatia.

17 Newsletter of the Institute of Public Finance, No. 11 and No. 13, December 2003

Croatia CFAA: Country and Economic Background 3

Relationship to the CAS, lending program and policy dialog with country authorities

7. Since Croatia joined the World Bank in 1993, the Bank has provided financial support, technical assistance, policy advice and analytical services to Croatia. These activities formed the basis of the Country Assistance Strategy (CAS), which was developed in close cooperation with the Croatian government. The current CAS covers a three-year period of 1999-2003; a new CAS is in preparation. The CFAA has advised in the drafting of the CAS.

8. As of December 2003, the World Bank’s active portfolio at the end of 2003 consisted of 11 projects; these projects represented loans to the amounts of US$ 448 million; and of that, US$122million has been disbursed so far. In addition, five projects representing an indicative total loan amount of US$232 million are in preparation. Finally, the Croatian government is discussing a large Programmatic Adjustment Loan (PAL). Whereas specific amounts have not yet been agreed to, the loan is likely to be around $150 million. The World Bank will be supporting the implementation of a broad set of Government policies over a three-year period. One of the policy areas covered by the PAL is public expenditure management. The exact topics are still to be determined and the CFAA will advise on the choice of focus areas.

9. Whereas lending initially focused on investment in infrastructure reconstruction after the war, more recently, the World Bank’s assistance has expanded to include the health, agriculture and forestry sectors, enterprise and financial sector reform, capital market development, as well as judicial and pension system reform. In determining the specific policy areas to be covered by the PAL, the World Bank is working closely together with the European Commission to make sure the PAL addresses priorities relevant for EU accession.

Croatia CFAA: Budgeting 4

CHAPTER 2: ASSESSMENT FRAMEWORK

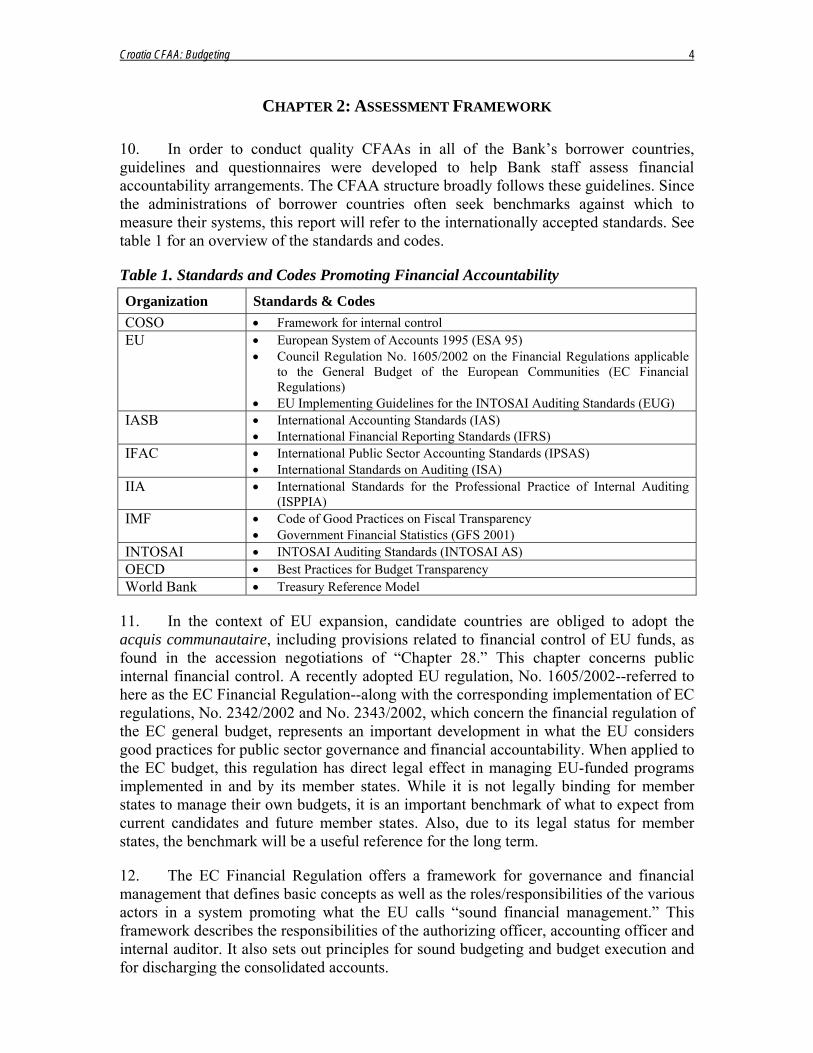

10. In order to conduct quality CFAAs in all of the Bank’s borrower countries, guidelines and questionnaires were developed to help Bank staff assess financial accountability arrangements. The CFAA structure broadly follows these guidelines. Since the administrations of borrower countries often seek benchmarks against which to measure their systems, this report will refer to the internationally accepted standards. See table 1 for an overview of the standards and codes.

Table 1. Standards and Codes Promoting Financial Accountability Organization Standards & Codes COSO • Framework for internal control EU

• European System of Accounts 1995 (ESA 95) • Council Regulation No. 1605/2002 on the Financial Regulations applicable

to the General Budget of the European Communities (EC Financial Regulations)

• EU Implementing Guidelines for the INTOSAI Auditing Standards (EUG) IASB • International Accounting Standards (IAS)

• International Financial Reporting Standards (IFRS) IFAC • International Public Sector Accounting Standards (IPSAS)

• International Standards on Auditing (ISA) IIA • International Standards for the Professional Practice of Internal Auditing

(ISPPIA) IMF • Code of Good Practices on Fiscal Transparency

• Government Financial Statistics (GFS 2001) INTOSAI • INTOSAI Auditing Standards (INTOSAI AS) OECD • Best Practices for Budget Transparency World Bank • Treasury Reference Model

11. In the context of EU expansion, candidate countries are obliged to adopt the acquis communautaire, including provisions related to financial control of EU funds, as found in the accession negotiations of “Chapter 28.” This chapter concerns public internal financial control. A recently adopted EU regulation, No. 1605/2002--referred to here as the EC Financial Regulation--along with the corresponding implementation of EC regulations, No. 2342/2002 and No. 2343/2002, which concern the financial regulation of the EC general budget, represents an important development in what the EU considers good practices for public sector governance and financial accountability. When applied to the EC budget, this regulation has direct legal effect in managing EU-funded programs implemented in and by its member states. While it is not legally binding for member states to manage their own budgets, it is an important benchmark of what to expect from current candidates and future member states. Also, due to its legal status for member states, the benchmark will be a useful reference for the long term.

12. The EC Financial Regulation offers a framework for governance and financial management that defines basic concepts as well as the roles/responsibilities of the various actors in a system promoting what the EU calls “sound financial management.” This framework describes the responsibilities of the authorizing officer, accounting officer and internal auditor. It also sets out principles for sound budgeting and budget execution and for discharging the consolidated accounts.

Croatia CFAA: Budgeting 5

13. The EU text uses the term “management board” to describe “the main internal body responsible for taking decisions on financial and budgetary matters, irrespective of the name given to it in the constituent instrument of the Community body” (Article 2, paragraph 2, Regulation No. 2343/2002). The CFAA uses it interchangeably with “senior management” and “management group.” The EU principle of “sound financial management” is defined in Box 1.

Box 1: Principle of Sound Financial Management

Article 25

Budget appropriations shall be used in accordance with the principle of sound financial management, that is to say, in accordance with the principles of economy, efficiency and effectiveness.

Official Journal of the European Communities, L 357/81, December 31, 2002 (Commission Regulation No. 2343/2002)

Fiduciary Risk

14. According to Article III, Section 5 of the IBRD’s Articles of Agreement – General Provisions Relating to Loans and Guarantees, fiduciary risk relates to the possibility of Bank loans or guarantees not being used exclusively for the purposes for which they were granted. The CFAA addresses a part of the fiduciary risk by assessing whether the systems in place support the use of Bank proceeds for their intended purpose. However, it does not constitute an actual audit of the use of the proceeds, nor the economy, efficiency and effectiveness of this use.

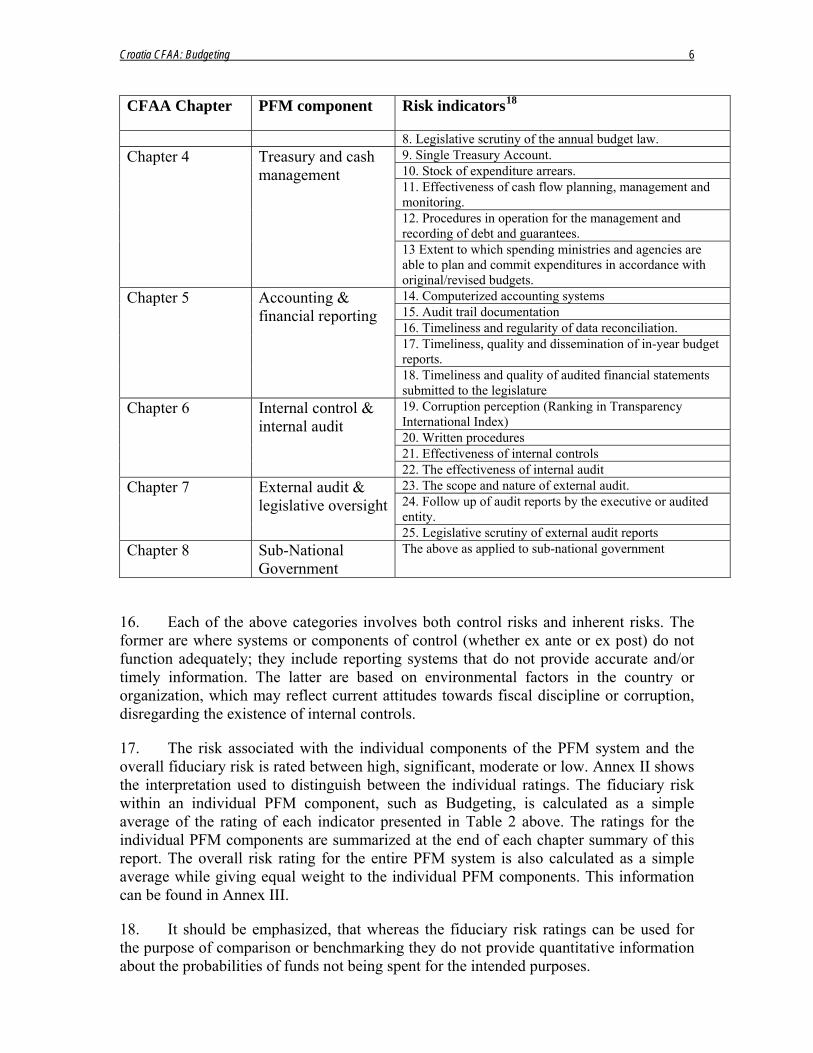

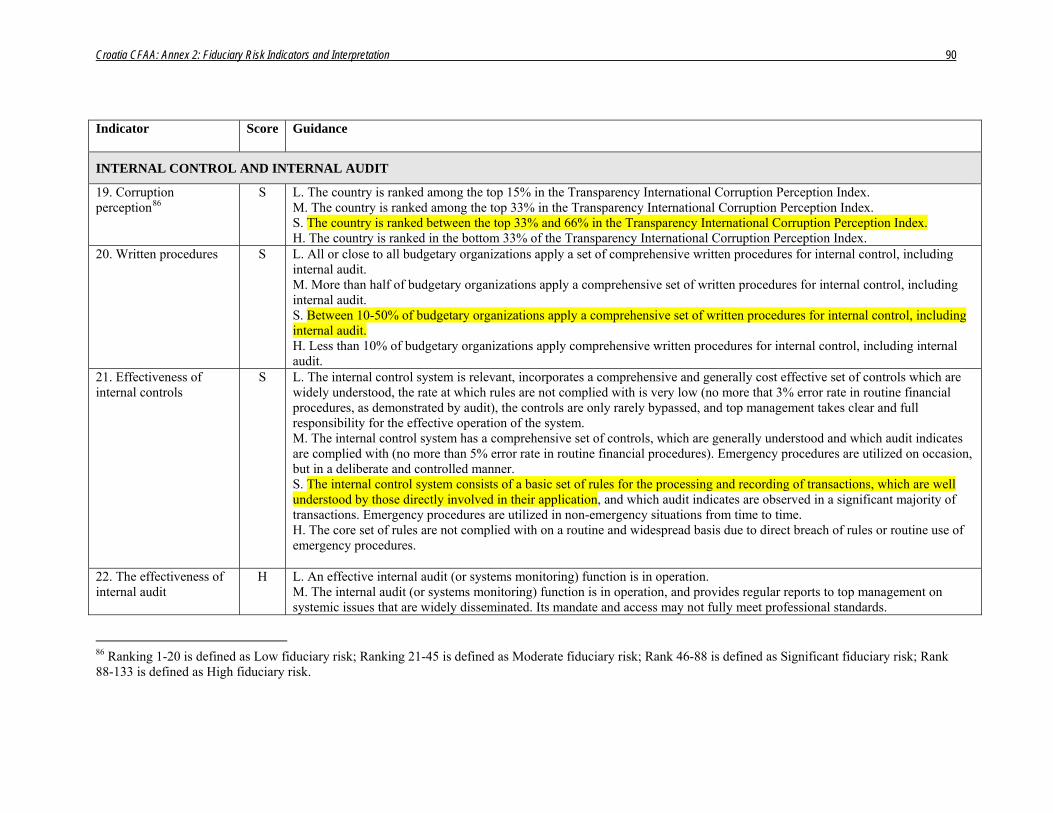

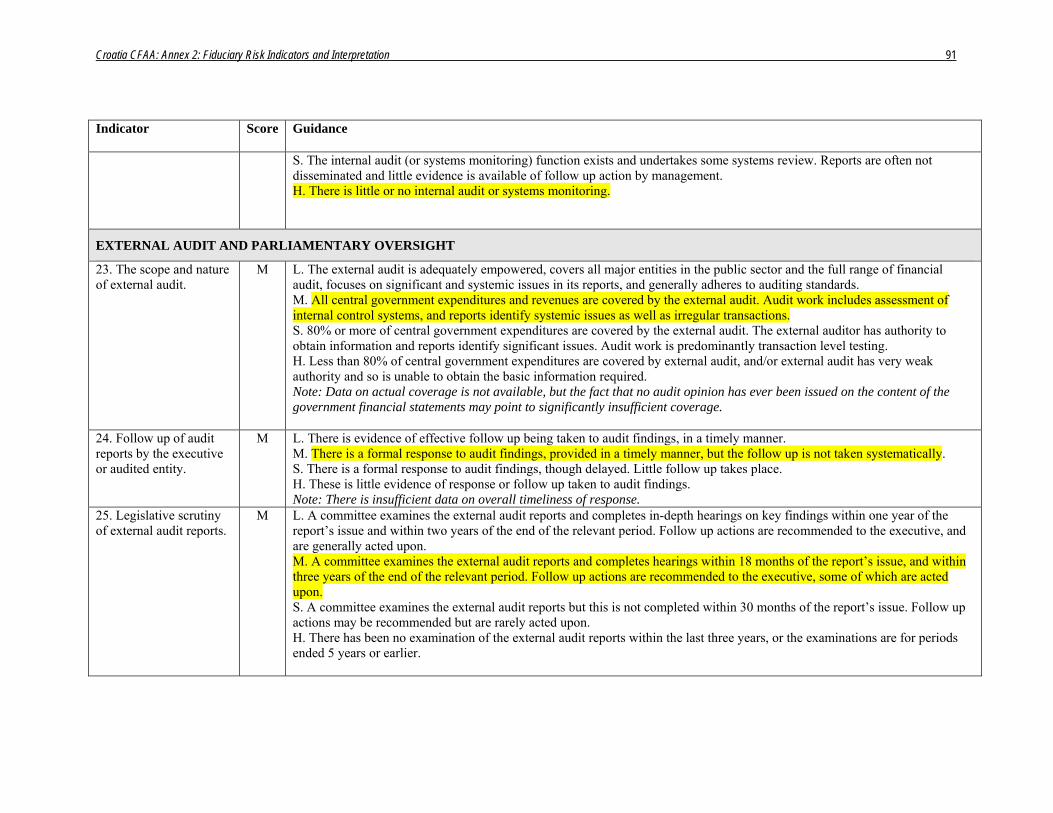

15. The specific indicators used to assess the fiduciary risk for each PFM component and CFAA chapter are listed in table 2 below.

Table 2. Fiduciary Risk Indicators CFAA Chapter PFM component Risk indicators18

1. Aggregate fiscal deficit compared to original budget. Chapter 3 Budgeting

2. Composition of expenditure out-turn compared to original approved budget.

3. Extent to which budget reports include all significant expenditures on central government activities, including those funded by donors.

4. Adequacy of information on fiscal projections, budget and outturns provided in budget documentation. 5. Administrative, economic, functional and programmatic classification of the budget. 6. Extent of multi-year perspective in fiscal planning, expenditure policy-making and budgeting 7. Orderliness and participation in the annual budget process.

18 See Annex II for elaboration and interpretation of risk indicators.

Croatia CFAA: Budgeting 6

Risk indicators18CFAA Chapter PFM component

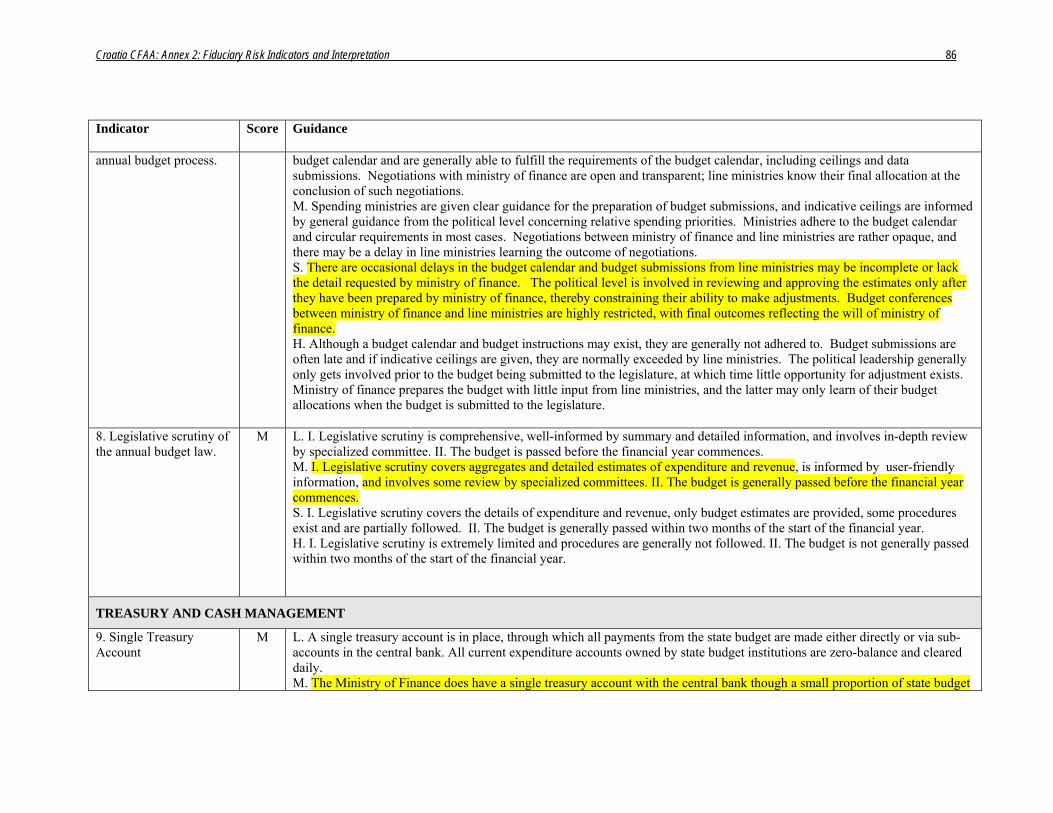

8. Legislative scrutiny of the annual budget law. 9. Single Treasury Account. 10. Stock of expenditure arrears. 11. Effectiveness of cash flow planning, management and monitoring.

Chapter 4 Treasury and cash management

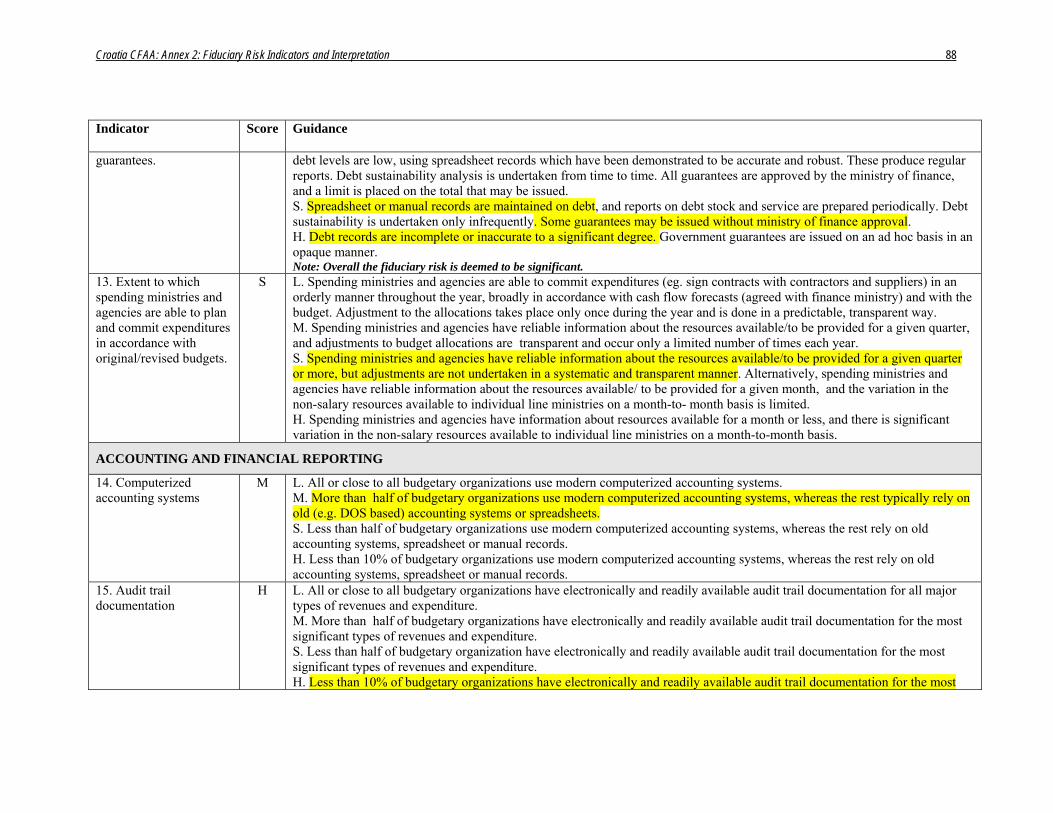

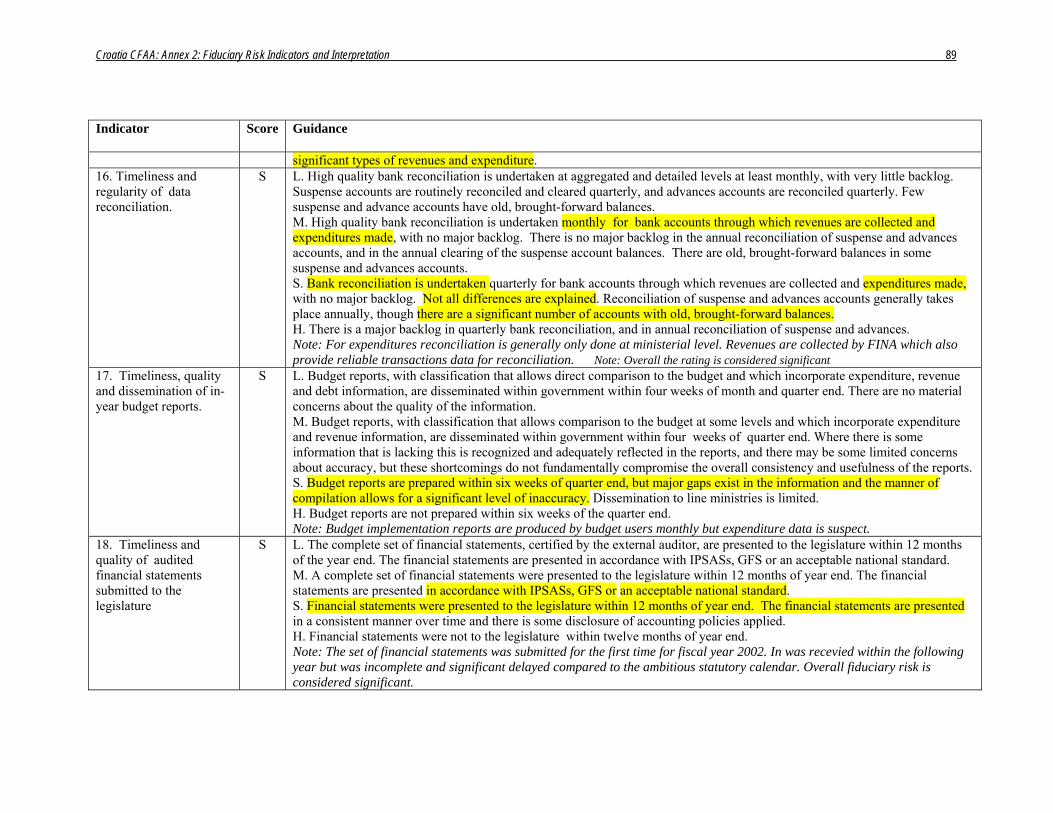

12. Procedures in operation for the management and recording of debt and guarantees. 13 Extent to which spending ministries and agencies are able to plan and commit expenditures in accordance with original/revised budgets. 14. Computerized accounting systems 15. Audit trail documentation 16. Timeliness and regularity of data reconciliation.

Chapter 5 Accounting & financial reporting

17. Timeliness, quality and dissemination of in-year budget reports. 18. Timeliness and quality of audited financial statements submitted to the legislature 19. Corruption perception (Ranking in Transparency International Index) 20. Written procedures

Chapter 6 Internal control & internal audit

21. Effectiveness of internal controls 22. The effectiveness of internal audit 23. The scope and nature of external audit. 24. Follow up of audit reports by the executive or audited entity.

Chapter 7 External audit & legislative oversight

25. Legislative scrutiny of external audit reports Chapter 8 Sub-National

Government The above as applied to sub-national government

16. Each of the above categories involves both control risks and inherent risks. The former are where systems or components of control (whether ex ante or ex post) do not function adequately; they include reporting systems that do not provide accurate and/or timely information. The latter are based on environmental factors in the country or organization, which may reflect current attitudes towards fiscal discipline or corruption, disregarding the existence of internal controls.

17. The risk associated with the individual components of the PFM system and the overall fiduciary risk is rated between high, significant, moderate or low. Annex II shows the interpretation used to distinguish between the individual ratings. The fiduciary risk within an individual PFM component, such as Budgeting, is calculated as a simple average of the rating of each indicator presented in Table 2 above. The ratings for the individual PFM components are summarized at the end of each chapter summary of this report. The overall risk rating for the entire PFM system is also calculated as a simple average while giving equal weight to the individual PFM components. This information can be found in Annex III.

18. It should be emphasized, that whereas the fiduciary risk ratings can be used for the purpose of comparison or benchmarking they do not provide quantitative information about the probabilities of funds not being spent for the intended purposes.

Croatia CFAA: Budgeting 7

Fiduciary Risk Indicators and Benchmarking Against Standards

19. Whereas a rating of the fiduciary risk is used to summarize and prioritize the findings in different areas of PFM, the report basically provides for a comparison between Croatian and good international practice in the field of PFM as these are expressed in international standards for financial management. This includes a benchmarking against relevant provisions of the Financial Regulation of the European Communities in the field of budgeting, accounting and auditing, as well as against internationally recognized standards for accounting and auditing.

20. Croatia’s ranking in the Transparency International Corruption Perception Index 2003 as 59 out of 133 countries19, is used as a fiduciary risk indicator under the heading “internal control”. The CFAA is not intended to cover issues pertaining to official corruption, nor is it intended to assess the specific methods used in detecting corruption.

19 See Annex II for interpretation.

Croatia CFAA: Budgeting 8

CHAPTER 3: BUDGETING

I. Background and Assessment Framework

Background

21. In the late 1990s, the functioning of the state budget system began to be matter of concern for the Croatian government. The budget was not comprehensive; and the public finance sector consisted of a significant number of extra-budgetary funds and agencies (EBFs) and a great number of state enterprises with poor financial reporting. Furthermore, while expenditures were specified at a high level of detail in the annual budget presented to the Sabor, it lacked a strategic policy driven direction and a matching budget classification.

22. The 2002 Public Expenditure and Institutional Review (PEIR)20 noted that the Government had made some progress since its independence; it had passed a new organic Budget Act (BA) and implemented a multi-year investment program. The PEIR noted that the major components of the budget process are in the hands of the BUs, including policy and planning and that the role of the Ministry of Finance is weak. The Ministry of Finance did not set standards for the decentralized budget development taking place in the spending entities; it plays a limited role in coordinating government-wide financial issues. The MOF also failed to provide a basic analysis of the budgetary impact of policy issues, a common and vital role that typically facilitates effective budget negotiations and Cabinet decision-making.

23. Weaknesses like these are largely responsible for the lack of discipline in the budget formulation process (for example, BUs commonly developed highly inflated proposals), the lack of strategic orientation in the budget, and the lack of realism in budget documents.

24. The PEIR identified four areas for the Government to focus its public expenditure and financial management reforms: strengthening the central entities responsible for budgeting, treasury and internal control; developing standardized accounts, budgets and PFM procedures; improving internal control and audit; bringing all revenues and expenditures (including EBFs) on-budget to improve transparency and resource allocation efficiency.

25. In focusing on necessary reforms in the budget formulation process, the PEIR also addressed problems in developing the macroeconomic framework for the budget, budget analysis and preparation cycle. Key recommendations to deal with weaknesses in these areas included: (1) fostering improved budget forecasts through collecting and analyzing economic forecasts from a number of leading private and public sector agencies to determine median parameters; (2) amending the budget law to provide greater transparency to economic estimates underlying the budget; (3) establishing an explicit multi-year framework to support improved budget decision-making; (4) improving

20 World Bank, Improving Fiscal Sustainability and Enhancing Effectiveness in Croatia – A Public Expenditure and Institutional Review, March 2002.

Croatia CFAA: Budgeting 9

sectoral analysis in the budget and the budget analysis capacity of the Ministry of Finance; (5) establishing the Budget Office in Law; (6) improving the strategic orientation of budgets through the introduction of a program classification; (7) getting line ministries to formulate their budgets prior to receipt of the MOF call letter; and (8) requiring that the Council of Ministers budget for the full cost of mandatory programs -- unless specific legislation to alter the program to meet a lower budget is prepared and submitted with the annual budget.

26. More recently, in the 2004 Overview of Foreign Technical Assistance (hereafter referred to as the Donors’ Report),21 the World Bank, EU, USAID, US Treasury and the IMF jointly identified a number of technical assistance-supported reforms for the new government. These reforms resonate with the PEIR proposals. They include strengthening macroeconomic forecasting and medium-term fiscal planning, creating linkages to the annual budget plan, clearly defining budget preparation responsibilities and facilitating provision of a budget manual, capturing commitments in the General Ledger accounting system and improving budget monitoring.

Assessment Framework

27. It is generally agreed that management of public expenditures should be aimed at ensuring:

• Aggregate fiscal discipline, to achieve macroeconomic stability;

• Allocative efficiency, which involves prioritizing programs according to Government policies and selecting the most cost-effective programs and projects;

• Efficiency and effectiveness in delivering public services. To achieve these goals, the budget process should adhere to basic principles and appropriate methods developed.

28. EC Budgetary Principles. To meet the above objectives, budget managers in EU member state administrations must observe the budgetary principles laid down in the EC financial regulations, when managing EU funds. A summary of the principles is listed below:22

• Unity and accuracy (comprehensiveness). Because the budget forecasts and authorizes revenues and expenditures, all of these must be included.