Crnogorski Telekom a.d. Podgorica · Szasz Daniel, age 37, is an economist. He started his career...

113

Crnogorski Telekom a.d. Podgorica 2008 Annual Report Crnogorski Telekom a.d. Podgorica 2008 Annual Report

Transcript of Crnogorski Telekom a.d. Podgorica · Szasz Daniel, age 37, is an economist. He started his career...

Crnogorski Telekom a.d. Podgorica2008 Annual Report

Crn

ogor

ski T

elek

om a

.d. P

odgo

rica

2008

Ann

ual R

epor

t

1

ContentsOur Mission / Our Vision 3

Our Values 5

To our shareholders 6Letter to our shareholders Crnogorski Telekom‘s Board of Directors The Management Committee of Crnogorski Telekom

Introduction 16General informationCompetitionRegulatory environment

Our strategy 22

Human resources 26

Corporate social responsibility 28

Services 30

The financial year 2008 37Management report for the 2008 financial yearCrnogorski Telekom a.d. Financial statementsReport of independent registered public accounting firmBalance sheetsIncome statementsCashflow statementsStatements of changes in equityNotes to the consolidated financial statements

Further information 110

2

3

Our MissionWe are the first choice for communication and infotainment. We guarantee persistent customer focus, reliability and continuous innovation. Crnogorski Telekom remains the best place to work at in Montenegro. We create an organization that encourages inno-vation and rewards performance. We build a company we are proud working for. We take our social responsibility seriously. We stretch boundaries, create and capture new opportunities and continuously strive for profitability and operational excellence.

Our Vision

We will become and remain market leader in whatever we do. We wish to be perceived as the most customer-oriented company in the country.We build a broadband society, delivering broadband products everywhere to everyone.We look after company’s money as if it was our own.We care and continuously strive for the satisfaction of our employees.We deliver quality and innovative services.We capture all growth opportunities.

Our

Mis

sion

/ O

ur V

isio

n

4

5

Our Values

Customer centricityCustomer needs and satisfaction drive CT business practice and development.

IntegrityWe follow the highest ethical standards in whatever we do.

SuccessWe continuously exceed expectations of our customers, employees and owners.

InnovationWe create an atmosphere that encourages change for the better.

TeamworkWe build the culture of an integrated company where every voice is heard and every person receives respect. We are making ourselves accountable for each other, commit-ting to high standards of performance in everything we do.

PassionWe do not run our business: we LIVE it. We are proud to work for the company where our dedication makes a difference.

Our

Val

ues

6

Dear Shareholders,

I am delighted to inform you about the main details of the business operations of Crnogorski Telekom in 2008. Despite significant changes in the regulatory and competitive environ-ment, our company has managed not only to maintain its overall leading position in the Montenegrin telecommunications sector, but also to improve it in certain segments. The key to our success lies in the customer focus and broad range of high quality telecommunica-tions products and services offered in the best networks.

2008 was a financially and operationally successful year and it was in line with expectations. In the fixed-telephony segment of our business, we maintained a stable customer base, almost doubling our ADSL customer number and had great sales success with our Extra TV service. In the mobile-telephony segment of our business, we maintained our leadership in the postpaid market, achieved higher market share and further improved coverage and network quality.

However, it was also a year of challenges and difficulties, especially in wholesale operations. Changes in the regulatory framework made it possible for our biggest customers to esta-blish direct links with their mother and sister companies in the neighboring countries and consequently dramatically reduce wholesale revenues, thus significantly contributing to an overall decrease in revenues of Crnogorski Telekom a.d. of 13% compared to 2007, which resulted in a drop of EBITDA without special impacts of €6.9 million. We experienced a reduction in mobile voice retail revenues and voice retail revenues in the fixed-telephony segment as a consequence of tariff rebalance in 2007 and fixed-to-mobile switching. It is very important to point out that we managed mainly to offset the aforementioned drop by a significant revenue increase in ADSL, Extra TV and data transfer (leased lines and Mipnet) as well as overall higher mobile segment revenues.

In 2008 we continued improving efficiency and increasing cost control, as we introduced changes in our organizational model and further reduced our headcount by 103 employees.

7

As for T-Com, the customer number of 170,000 decreased only by 2.5% year-on-year which is a significantly lower figure than in other European countries. Thanks to the strong focus on our strategic broadband services, the number of ADSL customers reached almost 28,000, while Extra TV service had more than 17,500 customers at the end of the year.

In a year of intense competition, T-Mobile managed to increase its customer base, maintain leadership in the postpaid segment and increase SIM market share to 36.1% at the end of 2008 (33.8% in 2007). The total customer number increased by 24% compared to 2007, amounting to more than 506,000. Out of that figure, almost 90,000 relates to postpaid cu-stomers, enabling us to remain postpaid market leaders. During the same period, mobile penetration in Montenegro increased to a level of 185% at the end of 2008.

2008 will be remembered as the year in which we paid out the highest dividend in the histo-ry of our company and Montenegro, exceeding €22 million.

Crnogorski Telekom is well-known for its employees, their knowledge, expertise and dedica-tion. I would like to use this opportunity to thank them one more time for their hard work and contribution to the successes of the company.

Finally, I sincerely thank you, our shareholders, for the trust shown. We are going to continue striving for operational excellence and sustainable profitability through providing permanent innovations and keeping customer focus. We are convinced we will meet your expectations.

Daniel Szasz, Chairman of the Board of Directors

To o

ur s

hare

hold

ers

8

Dániel Szász, Chairman of the Board of Directors of Crnogorski Telekom a.d.

Szasz Daniel, age 37, is an economist. He started his career at General Motors Group, where he held various managerial and treasury leadership positions since 1994 at Opel companies in Hungary and Germany. He delivered tasks of GM Daewoo Central and Eastern Europe managing director from 2002. He was appointed Chief Financial Officer of T-Online Hungary Plc. (former Axelero LLc.) effective of January 1, 2004. His treasury expertise benefited the profitability of Hungary’s leading Internet carrier, which has incessantly improved since 2004. Szasz Daniel contributed to the spiraling penetration of broadband internet, which constitutes one of Magyar Telekom Group’s business areas that demonstrate the most dynamic growth. In addition, he also played a major role in achieving and managing to keep a market leadership position of the Internet portal (origo) as well as in T-Online Hungary acquisitions like the iWiW community portal and Ad-network online marketing carrier. In 2007, he was appointed Chairman of the Board of Directors and Chairman of the Management Committee of Crnogorski Telekom.

Daniel Szasz Gereon Hammel Tripko Krgović Gabor Pal Hans-Peter Schultz Janos Szabo Denes Szluha

Gereon Hammel

Gereon Hammel was born in May 1968 and holds a business degree.In 1989 he started his professional career at the Bayer AG Group Germany in the Fast Moving Consumer Goods business unit. From 1992 he managed the Household Detergent business of Bayer Italy. In 1994 he moved back to Germany and was appointed as regional manager for the Bayer subsidiaries in Scandinavia, Poland and Africa. In 2000 he built up a Regional Financial Controlling and participated as a member of the management team in the development of a regional head office based in the UK for the UK, Scandinavia, Finland, France, Poland, Russia and Africa.In 2001 he moved to Michael Page Frankfurt an international recruitment consultancy and was responsible in advising companies in their job vacancies and the Executive Search of Finance positions.In August 2002 he joined T-Mobile International’s Joint Venture Management and was responsible for projects in the Cen-tral Eastern European region (CEE) and since 2006 he is Vice President for T-Mobile International’s Joint Venture Manage-ment in Hungary and Montenegro and responsible for projects in CEE.

Crnogorski Telekom‘sBoard of Directors

9

Dénes Szluha

Dénes Szluha was born in Budapest in 1968. He qualified with a degree at the Szent István Universtity, Gödöllő in 1994, majoring in economics. His career started at the marketing department of Shell Gas Hungary than continued at the adviso-ry firm Deloitte. In 1998 he joined the leading Hungarian private equity fund manager with investors such as EBRD, Bank Vontobel, Dresdner Kleinwort Wasserstein. He was responsible as an investment manager for acquisitions, portfolio ma-nagement and sale of major investments in primarily the IT and telecommunications industry. In 2002 he joined Matáv (today Magyar Telekom or MT) as senior project manager. Currently he holds the position of International Portfolio Ma-nagement Director. In his current capacities his team is responsible for managing international portfolio companies. He is Board member in Makedonski Telekom, T-Mobile Macedonia, Crnogorski Telekom and is the Chairman of the Board in the Bulgarian Orbitel.

János Szabó

János Szabó was born in Hódmezovásárhely (Hungary) in 1961. He qualified with a degree at the Budapest University of Economics in 1986 majoring in international relations.

After working in foreign services for three years, he continued in various finance and consultant positions in the private business sector. He became Director Finance of Delco Remy Hungary (subsidiary of a US based automotive supplier) in 1995. Later he was deputy general manager of the operation, responsible for sales, purchasing and operations.

In 1998 he was moved to the position of Director Finance Europe in charge of the finance activities of the European opera-tions. Later he has become CFO and managing director of a joint venture between Delco Remy and Hitachi. Since April, 2003 he is the director finance of the Wireline Services LOB of Magyar Telekom. The role has been extended to network and IT operations in 2006. He is member of the BoD, and chairman of AC of MakTel.From January 2008 he is Director of Group Controlling Directorate.

Hans-Peter Schultz

Hans-Peter Schultz was born in 1958. He is married, with two children. He graduated as Electrical engineer in 1981.After joining Deutsche Telekom in 1985 he was working in different positions and projects in DT’s international business. Until 2001 he was responsible for both international affairs and projects mainly in South-East Europe. In 1996 he joined Deutsche Telekom’s Moscow Office where he managed the restructuring of DT’s satellite business, the integration of regional mobile businesses into DT’s affiliate “Mobile TeleSystems” and the introduction of Global One Russia.In 2002 Hans-Peter Schultz moved back to Deutsche Telekom in Bonn were he was responsible for DT’s business in Israel in the “Region CEE, Middle East”. In the new Headquarters of T-Home he manages T-Home’s business in Slovakia.

Gábor Pál

Born in Budapest, 1968. Earned his degree at the Finance and Logistics Management faculty of the Budapest University of Economics in 1993, followed by a second degree at the Programmer Mathematician faculty of Eötvös Lóránd University in 1994. He participated in the PhD program of the Budapest University of Economics from 1996.

He started to work for NN Hungary Insurance Company as insurance mathematician in 1993, followed by his employment by Westel Mobile Co. Ltd. from 1994 as financial analyst. In 2000 he was promoted director of finance of the company, and became executive director of finance as of January 1, 2004 at Westel and the renamed on May 3, 2004 company, T–Mobi-le Hungary Ltd. After the merge of T-Mobile Hungary with Magyar Telekom Plc. in March 1996, he is director of finance and controlling of the Mobile Services Line of Business at Magyar Telekom. Since January 2008 Strategy, Planning and Control director of Consumer Business Unit of Magyar Telekom Plc.

Participated in several Magyar Telekom acquisition projects in the region. Former member of the BoD of Mobimak in Macedonia, currently member of the BoD at Telekom Crna Gora, Makedonski Telekom. Member of the BoD of M Factory Zrt, Budapest.

Tripko Krgović

Tripko Krgović is born in 1977, in Belgrade. He is married, and has one child. He finished his basic and master studies on Faculty of Economics in Podgorica. His professional carrier began in 1996 in family business. From 2004 he works in Securities Commission, in market supervision department. In 2005 he holds position of Investment manager in Moneta Investment Fund. From 2006 he is Chief executive officer of Moneta Broker-Diler AD Podgorica. Beside Crnogorski Tele-kom, he is Board member of Otrantkomerc, AD Ulcinj. He is the member of Minority Shareholders Council and a represent of minority shareholders in several Montenegrin companies.

To o

ur s

hare

hold

ers

10

Daniel Szasz, Chairman of the Board of Directors and Chairman of the Management Committee of Crnogorski Telekom

Szasz Daniel, age 37, is an economist. He started his career at General Motors Group, where he held various managerial and treasury leadership positions since 1994 at Opel companies in Hungary and Germany. He delivered tasks of GM Daewoo Central and Eastern Europe managing director from 2002. He was appointed Chief Financial Officer of T-Online Hungary Plc. (former Axelero LLc.) effective of January 1, 2004. His treasury expertise benefited the profitability of Hungary’s leading Internet carrier, which has incessantly improved since 2004. Szasz Daniel contributed to the spiraling penetration of broadband internet, which constitutes one of Magyar Telekom Group’s business areas that demonstrate the most dynamic growth. In addition, he also played a major role in achieving and managing to keep a market leadership position of the Internet portal (origo) as well as in T-Online Hungary acquisitions like the iWiW community portal and Ad-network online marketing carrier. In 2007, he was appointed Chairman of the Board of Directors and Chairman of the Management Committee of Crnogorski Telekom.

Georg Mündl, Chief Executive Officer of T-Mobile Crna Gora and Chief Marketing Officer of Crnogorski Tele-kom Group

Born in 1965. He holds a Master of Science degree in Electrical Engineering from Technical University of Vienna. In 1991 he joined Siemens AG Austria, where he held various positions in different Company divisions. In 2006 he joined Max. Mobil.Telekommunikations Service GMBH, as Deputy Sales Director, and from 1998 as Director of Residential Sales. In 2000 he became Executive Director International Business, responsible for SE-Europe operations. In 2000 he moved to Croatia, joining HT Hrvatske Telekomunikacije d.d, where he was delegated by T-Mobile International to build the Mobile Business Unit of Croatian Telecom. In 2001 he became the Member of the International Marketing Board of T-Mobile International and later that year, the Executive Director and Member of the Board for the mobile Business & CMO. In 2004 he joined T-Mobile Austria GmbH as Member of Management Board and CMO. In 2007, he moved to Montenegro, where he was appointed CMO in Crnogorski Telekom. In 2008 he was appointed CEO of T-Mobile Crna Gora.

Slavoljub Popadić, Chief Executive Officer Crnogorski Telekom a.d.

Born in 1965. He holds a degree in electronic and telecommunication from University of Montenegro. He started his ca-reer in 1991 at Republic Secretariat for Development, Podgorica, first as a main network and system engineer and then as a Leader of development of network and IT systems of Governmental bodies in Montenegro. In 2001 he joined Crnogorski Telekom group as a CEO of Internet Crna Gora. In April 2005, after the acquisition of Crnogorski Telekom by the Magyar Telekom, he became a Group network development director and Management Committee member of Crnogorski Tele-kom. In August 2006 he was appointed as a CEO of Crnogorski Telekom responsible for fixed business in the Company (T-Com). As of December 2008 he is Vice chairman of the Management Committee.

The Management Committee of Crnogorski Telekom

Chairman of the Board of Directors, Daniel Szasz T-Com Chief Executive Officer, Slavoljub PopadićT-Mobile Chief Executive Officer /Marketing Chief Officer, Georg Mündl Strategy and Business Development Officer, Zoltan Pinkola Chief Human Resources Officer, Beata Prisztacs Chief Technical Officer, Eva Ulićević Chief Financial Officer, Ferenc VaczlavikRegulatory, Government Relations and Legal Officer, Tibor Vidos Chief Sales Officer, Milija Zeković

11

From left to right: Daniel Szasz, Chairman of the Board of Directors and Chairman of the Management Committee, Georg Mündl, Chief Executive Officer of T-Mobile Crna Gora and Chief Marketing Officer, Slavoljub Popadić, Chief Executive Officer T-Com

12

From left to right: Ferenc Vaczlavik, Chief Financial Officer, Zoltan Pinkola, Strategy and Business Development Officer, Beata Prisztacs, Chief Human Resources Officer

13

To o

ur s

hare

hold

ers

Eva Ulićević, Chief Technical Officer, Milija Zeković, Chief Sales Officer, Tibor Vidos, Regulatory & Government Relations and Legal Officer

14

Zoltan Pinkola, Strategy and Business Development Officer

Born in 1972. Holds a degree in economics. Started his career with an international audit and financial advisory firm, Mazars in Budapest where he managed statutory audits, due diligence reviews of privatized companies and lead miscella-neous financial consultancy assignments through four years. He joined HBO Europe in 1997, holding various managerial positions initially in the Finance area, successively transferring to Business Development, managing projects related to the territorial expansion of HBO in Central Europe and to the launch of new pay TV channels and services in the region.He has joined Magyar Telekom in March 2006, and Crnogorski Telekom in July 2006. He has been a member of the Ma-nagement Committee of the Group and has fulfilled various executive positions since then. He holds the position of Strate-gy and Business Development Officer since October 2007.

Beata Prisztacs, Chief Human Resources Officer

Beata Prisztacs was born in 1970 in Pecs, Hungary. She graduated in 1993 on the Economics Faculty of Pecs University. She started her career in the Tourist Office of County Baranya in Pecs, first as marketing manager and later as director of the company.

In 1998 she joined Magyar Telekom and while working in different areas of the company she gained experience in the field of Controlling, Sales and Human Resources. In 2003 she moved to Skopje, to the Macedonian subsidiary of Magyar Telekom as senior consultant to the CHRLO, later as director of the HR Area. In 2006 she was also appointed as CEO of the Macedonian consulting subsidiary of the Group. From 1st January 2008 she was appointed CHRO of Crnogorski Telekom.

Eva Ulićević, Chief Technical Officer of Crnogorski Telekom

Born in 1970. She holds a degree in Mathematical Science and Master of Mathematical Science. She started her career on 1993 at Mathematical Faculty of Montenegro University in Podgorica, as the Assistant to the Professor. From 1996 she worked in ProMonte GSM Podgorica as Deputy of CIO. In 2000 she was engaged as the Team Leader of Oracle Academic Initiative Project while 2001 she worked in SEMA (LHS) Communications Systems Inc, Miami Florida USA as Senior Soft-ware Analyst Engineer for BSCS. From 2002 she is working for Crnogorski Telekom Group at the several executive posi-tions: CIO of MONET (nowadays T-Mobile Montenegro), IT Director of Crnogorski Telekom Group (2005), current one is CTO of Crnogorski Telekom Group (2006).

15

Ferenc Vaczlavik, Chief Financial Officer

Ferenc Vaczlavik was born in Budapest (Hungary) in 1974. He qualified with a master degree at the Budapest University of Economic Sciences in 1997 majoring in accounting.He started his career at Investel Zrt, the financial subsidiary of Magyar Telekom (at that time called Matav). After the merging of Investel’s staff into Magyar Telekom’s Finance Area, he continued working at the Treasury Department of Ma-gyar Telekom. In 2002, he joined the team of Magyar Telekom’s newly acquired subsidiary in Macedonia, as the senior consultant to the CFO. In 2005 he became the CEO of Magyar Telekom’s Macedonian consulting subsidiary. After his return to Hungary in 2006, he continued working at Magyar Telekom’s subsidiary for TETRA services, Pro-M Zrt., as a finance manager. From 1 February, 2007 he is the CFO of Crnogorski Telekom Group.

Tibor Vidos, Regulatory & Government Relations and Legal Officer

Born in 1954. He holds a degree in physics and a doctorate in biology from the Eötvös University of Sciences in Budapest. In 1989 after having spent several years in academic research he became the executive secretary of a political party duri-ng the democratic transition of Hungary. In 1991 he established the Hungarian subsidiary of the then market leading British lobby firm GJW Government Relations which he managed until 2000. Between 2000 and 2003 he assisted the democratic development of Indonesia by working there as the Director of Political Party Programs of the National Demo-cratic Institute (NDI). Between 2003 and 2004 he was the Chief External Relations Officer of Invitel; one of the incumbent fixed line telephone operators in Hungary. He joined Crnogorski Telekom in April 2005 as Regulatory and Government Relations Director. He holds his current position since January 2008.

Milija Zeković, Chief Sales Officer

Born in 1971. He holds a degree in Economics from University of Montenegro. After completing studies in 1995 he started his career at „Kartonka“, Podgorica, where he worked as production and sales manager, and under extremely difficult economic conditions in country, he founded the first Montenegrin manufacturing factory for the paper containers. When Monet (now T-Mobile Crna Gora) was funded in 2000, he started to work as Sales Manager. He has 9 years of experience within the Crnogorski Telekom group. In 2006 he became the Director of Sales for residential users and small and medium enterprises. In July 2008 he was appointed CSO of Crnogorski Telekom, responsible for development and creation of sales strategy, management and control of sales channels, presentation of all products and services to all existing and potential clients, and development and management of sales processes in company.

To o

ur s

hare

hold

ers

16

Introduction

17

General informationCrnogorski Telekom is the biggest telecommunication company in Montenegro. It provi-des full range of telecommunication services on the Montenegrin market, as it has two subsidiaries: T-Mobile CG, which is a mobile telecommunication service provider, and Internet Crna Gora, which is an Internet services provider.

Crnogorski Telekom is the principal fixed line service provider in Montenegro. Its exclu-sive rights in fixed line telecommunications services expired in December 2003. Crno-gorski Telekom provides local, national and international services, in addition to a wide range of telecommunications services involving leased line circuits, data networks.

Following a successful privatization tender, between March and May 2005, Magyar Tele-kom obtained 76.53 percent interest in Crnogorski Telekom and thus became the majo-rity owner of the Company.

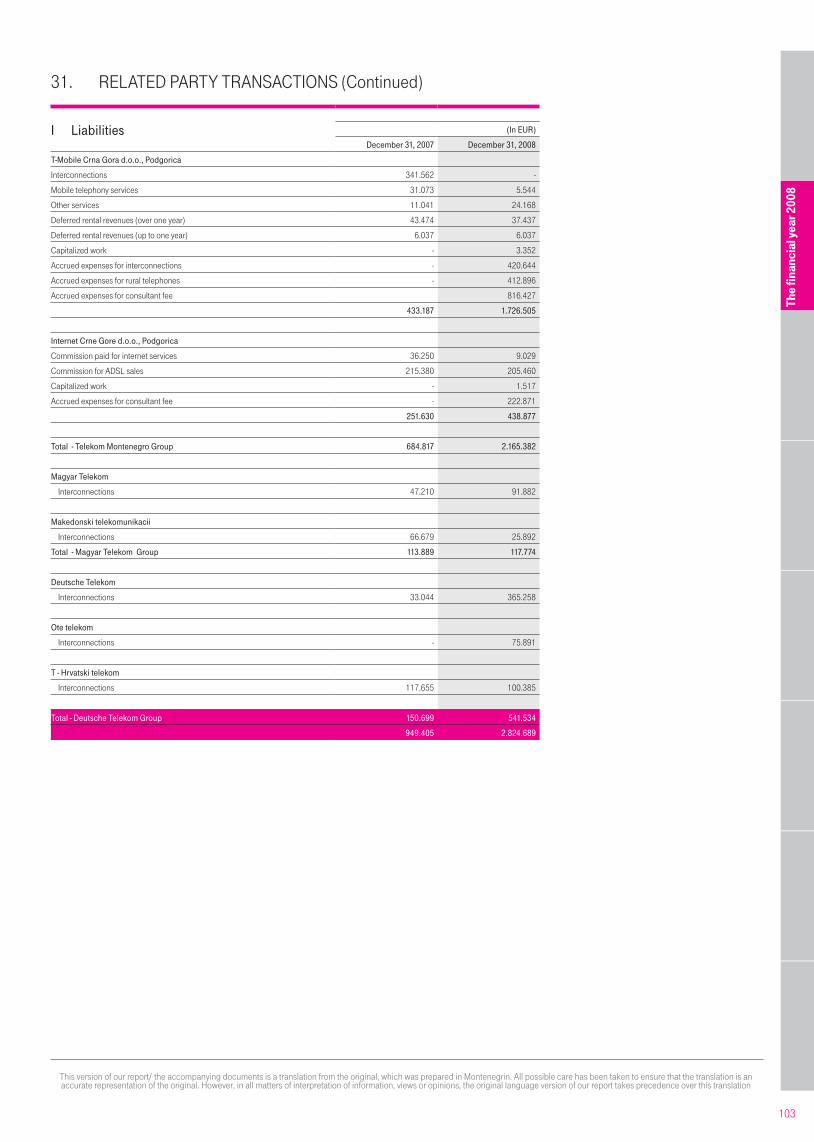

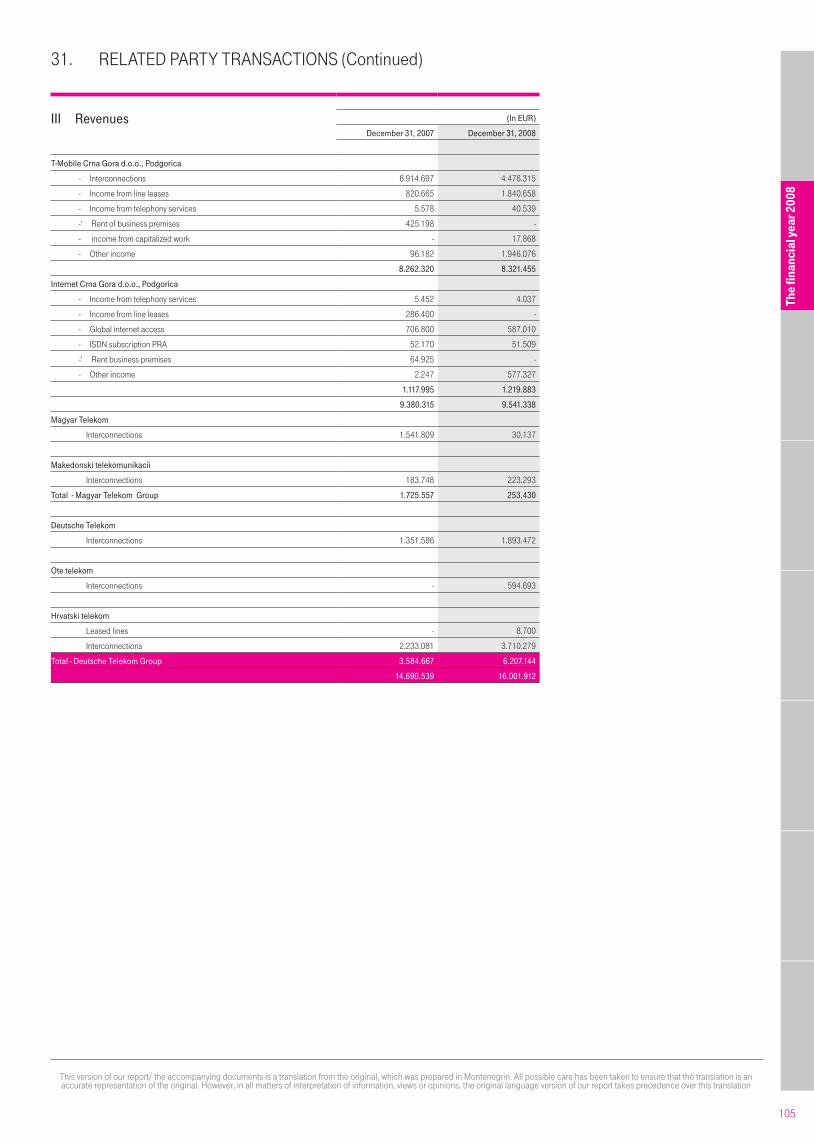

Deutsche Telekom AG is the ultimate controlling owner of Magyar Telekom holding 59.21% of the issued shares. Deutsche Telekom (DT) Group and Magyar Telekom Group have a number of fixed line and mobile telecom service provider subsidiaries worldwide, with whom the Crnogorski Telekom Group has regular transactions. Related party transaction details are given in the note 31 of Crnogorski Telekom a.d. Financial Statements.

For the past four years, Crnogorski Telekom’s major operational goals were to further digitalize the fixed line network and to increase the capacity and reliability of data net-work, consequently creating conditions for increase of subscribers of broadband and voice services. The digitalization rate reached 100 percent by the end of 2007 and ADSL coverage exceeded 90% of PSTN customer base by the end of 2008.

In December 2007 Crnogorski Telekom started IPTV service and at the moment it is the sole provider on the Montenegrin market capable to offer a broad range of multimedia services and to start with 3Play and 4play services on the carrier grade level.On June 26, 2006 the Shareholders Assembly of Crnogorski Telekom approved the proposal of the Board of Directors to adopt the “T” brand in the Montenegrin market. On September 26, 2006, the fixed line operations became T-Com Crna Gora (“T-Com CG”) and the mobile business changed its name to T-Mobile Crna Gora (“T-Mobile CG”), while the fixed line parent company and the group was renamed to Crnogorski Telekom.

Intr

oduc

tion

18

19

In 2007, a new mobile and fixed line operator entered into the Montenegrin telecommunications market - the third mobile ope-rator and licensed operator for development and exploitation of WiMAX-based network, launched its WiMAX network.

In the third quarter of 2007 and the first quarter of 2008, eight licenses for VoIP operators were issued as well. Two of them signed agreements on interconnection and access with T-Com in July 2008. They are able to offer outgoing call services to our customers through carrier selection and freephone service, but they do not terminate international traffic.

Fixed-mobile service substitution is expected to become increa-singly significant. The high mobile penetration and the introduc-tion of a third mobile operator in 2007 have intensified this trend.

Nine Multichannel Multipoint Distribution Service (“MMDS”) and CATV licenses were awarded at the beginning of 2007. Some of the cable operators have declared their intention to provide Inter-net and telephony services. Terms and conditions for joint usage of our underground infrastructure have been published in 2008, but currently only three of them are using this possibility at five municipalities in Montenegro (in total length of less than 20 km). MMDS and satellite operators, who were able to start first with service provisioning and who are not dependant on our infra-structure, are currently market leaders in CATV segment.

Strong competition is developing in wholesale segment as well. It is expected that significant players like Telekom Srbija, National Broadcasting Company and Electricity Company will enter in Internet and data wholesale business after significant invest-ments in their communications infrastructure have been realized during 2008.

Competition

Intr

oduc

tion

20

Regulatory environment

Following the privatization of Crnogorski Telekom, the gradual liberalization of the telecommunications markets in Montenegro has started and this process has become more pronounced in recent years. The legal environment is rapidly changing. A new competition law came into force on January 1, 2006 and the consumer protection law was adopted in May 2007. The new law on Electronic Communications was adopted in Montenegro by the Parliament on July 29, 2008. The Government expects that the new EU conform law will speed up the development of electronic communications networks and services; stimulate competiti-on; provide open and equal access to networks and electronic communications services; improve efficiency and introduce new tech-nologies and services; provide efficient customer protection; provide easy access to information on tariffs and services; stimulate Inter-net usage and encourage investment in the telecommunications sector. The Agency for Electronic Communications shall conduct a market analysis and identify operators with SMP within one year from the day the law on Electronic Communications enters into force and to prescribe SMP operators to introduce remedies as defined by the relevant EU directives. Until SMP operators are identified it shall be considered that Crnogorski Telekom is an operator with SMP in the markets of fixed voice telephony network and services, including the market of access to network for data transfer and leased lines, while all telephone network operators (including T-Mobile Crna Gora) are operators with SMP in markets of termination of calls in their respective networks. The law on Electronic Communications however does not prescribe what obligations the SMP operators have to fulfill before the first market analysis is completed. The aim of these obligations is to significantly lower the market entry barriers for new providers in the telecommunications markets.

21

Regulatory fees Under the new regulatory regime Crnogorski Telekom will have to pay a fee for market supervision, numeration fees and radio frequency fees. These fees shall be paid according to the previ-ous regulatory regime until December 31, 2008 and from Janua-ry 1, 2009 according to the new one if the Regulator adopts the related bylaws by the end of the year. The new fees might be higher than the ones paid under the previous law when a flat 1 percent gross revenue fee was paid.

Carrier selection New RIO of Crnogorski Telekom was published in April 2008. Carrier Selection was included in the new RIO. Currently, four operators (beside Crnogorski Telekom andT Mobile Crna Gora) have been assigned with Carrier Selection code, but only one of them signed interconnection agreement with Crnogorski Telekom in July 2008, with Carrier Selection included.

Sharing of infrastructure The RIO also defines terms and conditions of collocation, for the purpose of interconnection realized at Crnogorski Telekom’s premises. This includes renting of space at buildings, masts and ducts as well. RIO conditions are valid only for operators looking

for interconnection/access while usage of infrastructure by ope-rators for other purposes is subject to commercial negotiations.

Termination of calls Fixed termination fee (“FTR”) has been reduced by 10 percent from 1 July, 2008. National termination fee is now 0.027 EUR/min, while local termination is 0.0225 EUR/min. Termination of international calls in Crnogorski Telekom’s network transited by domestic operators is subject of commercial negotiations with competitors. Additional reduction of FTR and the intention to equalize fees regardless of traffic origin have been announced by the Agency for Electronic Communications together with the introduction of cost-based termination in the forthcoming period. Local authorities in Montenegro have the authority to levy munici-pal taxes on telecommunications equipment placed under roads, resulting in a high degree of uncertainty for Crnogorski Telekom with respect to the overall tax liabilities.

Montenegro and the European Union Montenegro became an independent state in 2006 and signed a Stabilization and Association Agreement with the European Uni-on at the end of 2007. The Interim Stabilization and Association Agreement came into force on January 1, 2008. Montenegro has submitted its application for membership in the EU in December 2008.

Intr

oduc

tion

22

Our strategy

23

Evolving focus

2007 was the year where the foundations of long-term competitiveness were laid down with significant changes for Crnogorski Telekom both on the structural and technologi-cal level.The technological developments of 2007 (such as the launch of mobile broadband network as the first operator in Montenegro, and the Extra TV service providing a set of features and degree of interactivity unique in the broadcast market) have solidified the position of Crnogorski Telekom as the leading service company in the infotainment industry.

In 2008, we have strengthened our position in the broadband and broadcast markets. By the end of 2008, we have served over 27,800 customers with broadband access and connected more than 17,500 Extra TV homes. We have also launched best-in-class mobile broadband services, providing high-speed nomadic access to our customers in the country and abroad. O

ur s

trat

egy

24

Four strategic goalsThe strategy of Crnogorski Telekom relies on four principal building blocks:

1. Operational efficiency 2008 was the year of organizational restructuring. This mani-fested in a significant headcount rationalization of 103 emplo-yees on Group level. Such headcount reductions would have been impossible without a major revision of the organization charts of Crnogorski Telekom. The changes included a simplifi-cation of reporting lines and the elimination of managerial layers – which made the organizational structure leaner and less hierar-chical.

The Group also executed a broad-scope business process reen-gineering project, where more than fifty business processes were redesigned or established as completely new processes to sup-port the growing need for performance and efficiency and to be able to provide even better customer experience.

2. Superior service experience The development of employees with an orientation on customer needs is playing a crucial role in the way we live our business. Technology is changing rapidly in the industry where we operate. Continuous and systematic investment into the development of our employees remains one of the highest priorities.

We are striving to get closer to our existing and future customers; we have continued expanding our sales network and have made additional steps towards guaranteeing the availability of our ser-vices either in our integrated T-Shop network or through high-quality partner shops in the country. The 14 shops operated by the Group are unique in terms of coverage and the availability of products compared to competitors. We have – as the first tele-communication operator in the country – launched a webshop, offering the convenience of ordering products and services to our customers – wherever they are.

25

3. Service expansion The customers of Crnogorski Telekom have and will constantly benefit from the fact that their provider is the member of a highly recognized international operator.

These synergies guarantee that world-class service innovation is brought to Montenegro as they emerge internationally.Crnogorski Telekom is determined to constantly stretch the boundaries of its activities and will – through prudent innovation - enter new industry segments which have not been part of the traditional telecommunication activities. In 2008 we started esta-blishing our presence in the media segment and we will continue paving the road to the goal of becoming a veritable “Three Screen” company: the services and applications we deliver will be made available to our customers on each interface they use (mobile handsets, PC or television), wherever they are, whatever they do.

By putting our entertainment services to the service of the tou-rism industry, we have also brought unique, tailor-made products to our business customers.

4. Full broadband potential The expansion of services which rely on broadband technology is a core element of our business strategy.

The fixed line broadband access services offered by ADSL deli-ver the highest bandwidth and most reliable service available on the Montenegrin telecommunication market.

T-Mobile has launched in 2008 mobile internet packages which deliver world-class nomadic broadband experience on the whole territory of the country and worldwide.

Extra TV has become by the end of 2008 a product available for masses of customers - especially with the new entry-level pa-ckages launched in November 2008.

The broadband expansion strategy of Crnogorski Telekom deve-loped during 2008 identified certain barriers to the mass expan-sion broadband internet access services in the country. We have started the implementation of a program with the determination of systematically destroying those barriers. The program has been addressing the fields of education, infrastructure, financial constraints of end users and content and online application de-velopment, and will continue during the coming years.

Our

str

ateg

y

26

Human resources

27

Main company focuses in 2008 related to human resources management in Crnogorski Telekom Group covered headcount efficiency increase, improvement of service culture and increase in employee satisfaction.

Headcount efficiency In October 2008, Crnogorski Telekom Group successfully com-pleted a program for headcount rationalization which resulted in efficiency increase of 11%. The company implemented several steps in an effort to streamline the Group`s operating structure and, with the re-organization of Technical Area, leaner and more flexible organizational structure was achieved. Apart from the achieved headcount efficiency, this headcount rationalization program will have a significant impact on the em-ployee related expenses in the coming years.

In 2008, the salaries of employees in Crnogorski Telekom Group were increased starting from June 2008. Considering that the cost of living was rapidly increasing in the last 5 years, manage-ment agreed to increase the salaries of employees in Crnogorski Telekom A.D. by 26,5% and T-Mobile Crna Gora and Internet Crna Gora by 13,4%. This adjustment reduced the differences in salaries of the same job positions within the group and resulted in a significant increase of the satisfaction of our employees.

Improvement of service culture and custo-mer satisfaction

Improvement of service quality, customer satisfaction and effici-ency was one of the key objectives of Service Culture program in 2008. In order to achieve these key objectives, customer orienta-tion trainings were organized for technical, sales and contact centre staffs that are in direct contact with the customers.

The project “Shop Day” was developed to enable the manage-ment to better get to know customers and their needs through direct shop experience. This was a great opportunity to raise the management’s awareness for customer issues and the opera-tions of the frontline. Received feedback, with proposals for im-provement of our sales and support processes, was positive.

Knowing that a great employee experience drives a great custo-mer experience, HR Area started with improvement of HR pro-cesses in the frame of the “Service DNA” project. The changes implemented with the aim the processes to be more customer oriented and the HR staff to demonstrate a convincing service attitude and consequently to become ambassadors of our company’s values and service culture.

Spirit@telekom Pulse Check Survey enables us to have an overview on the gene-ral atmosphere in the company in a frequent manner, every se-cond month. The survey provides the opportunity to systematical-ly support the change processes globally and at short intervals. The management receives up-to-date information on the status of current changes from employees’ perspective.

Spirit@telekom is supplemented by the bi-annual employee sur-vey, which goes in detail in terms of questions regarding emplo-yees’ direct working conditions and which is consequently analy-zed in greater depth. The employee survey was conducted during the fall of 2008 and the analysis of the results will be available at the beginning of 2009, building the basis for impro-vement actions during the year.

Hum

an re

sour

ces

28

Corporate social responsibility

29

The concept of Corporate Social Responsibility has an important role in Crnogorski Telekom. Being a leading company in the country, Crnogorski Telekom is proactively involved in all areas important for Montenegrin society.

Following the codes of business ethics and corporate governance, as well as by understanding the needs of the community, Crnogor-ski Telekom gives its contribution to the development of Montenegrin society.

Special attention is dedicated to building relationships with employees, customers, shareholders and business partners. Numerous sponsorships and donations that bring additional investments in education, sports, culture and health prove that corporate social responsibility is treated with a strategic importance in Crnogorski Telekom.

Internet in schools Being the leading broadband provider in the country, Crnogorski Telekom is responsible to be the first partner of the country on its way to becoming an information society. In order to enable Inter-net to become a part of everyday lives of majority of Montenegrin citizens, together with the Government of Montenegro, the Com-pany initiated a project aiming to increase the level of informatics literacy and internet penetration in Montenegro.

Within this project, the company organized internet workshops in 40 schools, in 21 Montenegrin municipalities, with a motto »Inter-net is a game played your whole life«. The goal of this strategic project is to bring to attention the importance of Internet to the young population. The first phase of the project enabled all ele-mentary and high schools to have their own web presentation, whose content will further be developed by pupils and their te-achers.

In addition, for the second year in a row, Crnogorski Telekom enables free Internet access via ADSL to all elementary and high schools in the country. The project was implemented together with Ministry of Education and Science, and it started in 2006.

In order to increase the level of conciousness about the impor-tance of information technologies among young population, Crnogorski Telekom awarded 94 elementary and high school pupils with free Internet. The project was implemented in coope-ration with the Exam centre of Montenegro, and the pupils could choose whic type of connection they prefer – T-Com ADSL or T-Mobile Mobile Internet.

Sponsorships and donations

Sports, cuture, education, health and ecology were identified as five focus areas for sponsorship and donation activities. Beside stretegic partnerships that Crnogorski Telekom has with impor-tant institutions, the company cooperates with numerous NGOs that gather persons with dissabilities, as well as with organisa-tions that work on development of civil society in Montenegro.

In Company‘s sponsorship strategy, sports have a special place, since this is an important area for developing a healthy, modern and advanced society. In 2008 Crnogorski Telekom was a gol-den sponsor of Montenegrin Olympic Comitee, and hence, has been able to offer an important support in the first, historic ap-pearance of Montenegrin team on the Olympic games in Beijing.

In accordance with the Hybrid Sponsorship Strategy of Deutsche Telekom, in 2008 the company introduced football as a strate-gic area for sponsoring activities. T-Com became the golden sponsor of Montenegrin Football Association, Football Club Bu-ducnost and the general sponsor of T-Com First Montenegrin Football League. Besides, T-Com brand was linked to University league in indoor football and football league for elementary school pupils called T-Com Kids Cup.

T-Mobile was, traditionally for the sixth year in a row, the sponsor of Woman‘s Handball Club Buducnost T-Mobile, one of the most successfull sports clubs in the country.

In 2008, Crnogorski Telekom continued its support to health institutions in Montenegro. On the occasion of New Year and Christmas holidays, the company donated 30 000 euros to the Health institution »Dom Zdravlja Podgorica«. This institution, that takes care abouth the health of 200 000 habitants of Podgorica, used this donation for the purchase of ultrasound equipment.

Cor

pora

te s

ocia

l res

pons

abili

ty

30

Services

31

TelephonyOn the September 1st 2007 Crnogorski Telekom introduced the tariff rebalancing in fixed line prices which targeted equalizing of the prices for business and residential segment. Rebalancing targeted decreasing of gap between domestic traffic tariffs and international tariffs. That was a one of tools preventing potential actions of competitors in fixed line of business. Results were expected revenue decrease in Business segment with almost the same structure of MOU. In residential segment there is higher traffic towards internatio-nal destinations, with expected decrease in dial up traffic.During 2008 number of residential customers decreased for 2,4% while number of business customers decreased by 2,9% resulting in total customer number decrease of 2,5%, which is significantly lower churn than in other European countries. Decrease in residenti-al segment is mainly caused by bad debt disconnections.

Loyalty program

In August 2008, “Ritam Klub” was introduced, the first joined fix and mobile loyalty program. This program was specifically difficu-lt and challenging from both technical a marketing point of view. In this loyalty program customers are collecting points - dukati and can exchange them for 3 types of prizes:

1. Traffic and subscription (minutes, SMSs, prepaid refills, ADSL subscriptions, IPTV subscription, etc.); 2. Internal goods (handsets, ADSL Modems, etc.); 3. External goods (video cams, mp3, keyboards, DVDs, etc).

Also, thanks to the fact it is a joint loyalty program of T-Com and T-Mobile, customers can collect and join dukati (points) of both T-Com and T-Mobile and exchange it for the prizes of both opera-tors.

OCPs and Flat packages

Alternative fixed voice technologies (4 WiMax licensed operators and 8 licensed VoIP operators) increased competition in fixed voice retail. Thus, T Com introduced International OCPs – Ino and Ino Favorit packages (focus on top 20 international calling directions for additional payment and free minutes or discounted prices, competitive to VOIP prices) in October 2008 in order to prevent potential churn and to sustain international revenue. This offer represented competitive advantage and would allow us to react in accordance with market needs. In case that International traffic of T-Com starts to drop suddenly due to impact of competi-tion, we will be prepared to refresh our OCP offer and start ag-gressive campaign.

T Com introduced flat fixed packages – Komfor and Komfor+ packages - offering unlimited calls towards the T-Com fixed net-work in Montenegro (local and long distance) 100 extra minutes for calls within the fixed network in Serbia (Komfor+ ). These packages were planned to be churn prevention for 2009 and to represent milestone that our competition will have to achieve.

Serv

ices

32

InternetIn 2008, the main focus of our marketing activities was to incre-ase ADSL sales and to successfully introduce IPTV service (un-der brand name Extra TV). In order to profit from our market posi-tion and to stimulate growth of non-voice revenues, several actions and promotions have been implemented. Customer number has grown almost double. In order to achieve that growth in Broadband segment we introduced new restructured ADSL offer with affordable Flat packages in September 2008 with great success, reaching almost 28 thousand customers at the end of the year.

Extension of ADSL access network was performed in 2 phases with internal resources engaged on implementation. The co-verage was extended to 93% until EOY 2008 and continued without interruption. Capacity was extended to 52 thousand ADSL ports (used for broadband Internet and IPTV). All DSLAMs are ADSL2+ capable and IPTV ready. Also, as result of 2008 roll-out 17 new locations were introduced, totaling in 139 loca-tions. Crnogorski Telekom intends to deploy a software platform for remote management of xDSL CPE (Auto-Configuration Server – ACS) with main functions: auto-configuration and dynamic service provisioning, software/firmware image management, status and performance monitoring and diagnostic.

TelevisionDuring 2007 T-Com started with IPTV service, named “Extra TV”, as answer to competitive environment on Montenegrin market. The aim of the project was to implement MSTV system including major IP network upgrade extensively exploring DT Group syner-gies. Commercial launch of ExtraTV service was in November 2007 with IPTV platform capacity to support 13.000 customers. During 2008, upsizing of Microsoft IPTV platform was successful-ly finished. Platform now can support up to 38.000 customers. Extra TV launch was the most successful one in DT Group. At the end of 2008 17.531 customers were connected.

For load sharing of unicast traffic, D-servers are now implemen-ted on few new locations (till now D-Servers were only on central location in Podgorica). One location (Bijelo Polje) is dedicated for users in north region of country and two locations (Kotor and Bar) are dedicated for users in south region of country. Users from central part of country are guided to existing D-Servers in Podgorica. As a very important service quality indicator, D-server logging is also successfully implemented parallel with platform upsizing project. Thanks to this, we now have very useful system for user problem identification. Error logs classified on many parameters help us to locate and identify problems on user or IPTV location level.

In September we implemented IPTV reporting system. Reports are divided in few categories: Live TV reports, VoD reports, DVR reports, STB reports and Menu Usage reports. Parallel with re-porting system, project of creating professional backup and recovery system is successfully finished.

There is a long list of ExtraTV additional features implemented through developed applications in 2008. (Billing information, package changer, stock exchange reports, Ritam klub, game portal, remote recording & mobile EPG, TV web portal, weather forecast, etc…).

Several pilot projects started in 2008.

33

OtherImplementation of new Montenegrin numbering plan was suc-cessfully finished this year. Parallel usage of new and old national area and short codes was implemented in all relevant systems.

Implementation of new national Internet domain (.me) was suc-cessfully implemented during 2008. Also, we started with imple-mentation of parallel usage (12 months) of public mail addresses and web domains.

Sales channelsCrnogorski Telekom has developed different sales channels in order to provide best services to residential and business custo-mers. Crnogorski Telekom’s direct sales channels consist of own shop network (14 joint T-Mobile and T-Com shops), Key Account Managers and SME Coordinators. Crnogorski Telekom’s indirect sales channels include the partner shop’s network, dealers, web sales, “door to door” sales and Call Center. Business customers are served by Key Account Managers taking care of the top 300 clients and SME Coordinators who are in charge for SME and SOHO companies. Top clients are divided by industries (e.g. banks, hotels, large manufacturers, government, etc.) and small companies are divided by regions.

Extra TV service for hotels.

First phase of this project is implemented in Hotel City in Podgori-ca. The hotel guests have live TV stream with hotel channel list (28 channels available). Also, small customization of user inter-face (new channel list, hotel logo, one free of charge sample of VoD content) was part of this first phase. In the second phase, VoD content delivering and charging will be enabled. In the third phase, we plan to integrate hotel management system with our IPTV system.

Mobile TV

Testing period started in June as a free service to all T-Mobile postpaid customers. This project is result of synergy between T-Com and T-Mobile (channel acquisition headend system is used from T-Com Extra TV system, Streaming and VoD servers are implemented in service part of T-Mobile network).

VDSL pilot project

Pilot project of VDSL2 access technology started in July of 2008 in order to introduce higher speed for customers with copper wire lines. First test users in two areas of Podgorica are con-nected to VDSL access equipment. Available bandwidth confi-gured for end users is 30 Mbps in downstream and 10 Mbps in upstream, which is enough to give customer possibility for two STBs (with HD streams) and 10 Mbps of Internet (up to 30 Mbps in case of not using TV service).

HDTV pilot project

HDTV pilot project started in September 2008. On 10th Septem-ber first free-to-air channel Arte HD transmitted over IPTV test platform using Motorola’s encoder.

Serv

ices

34

The financial year 2008

35

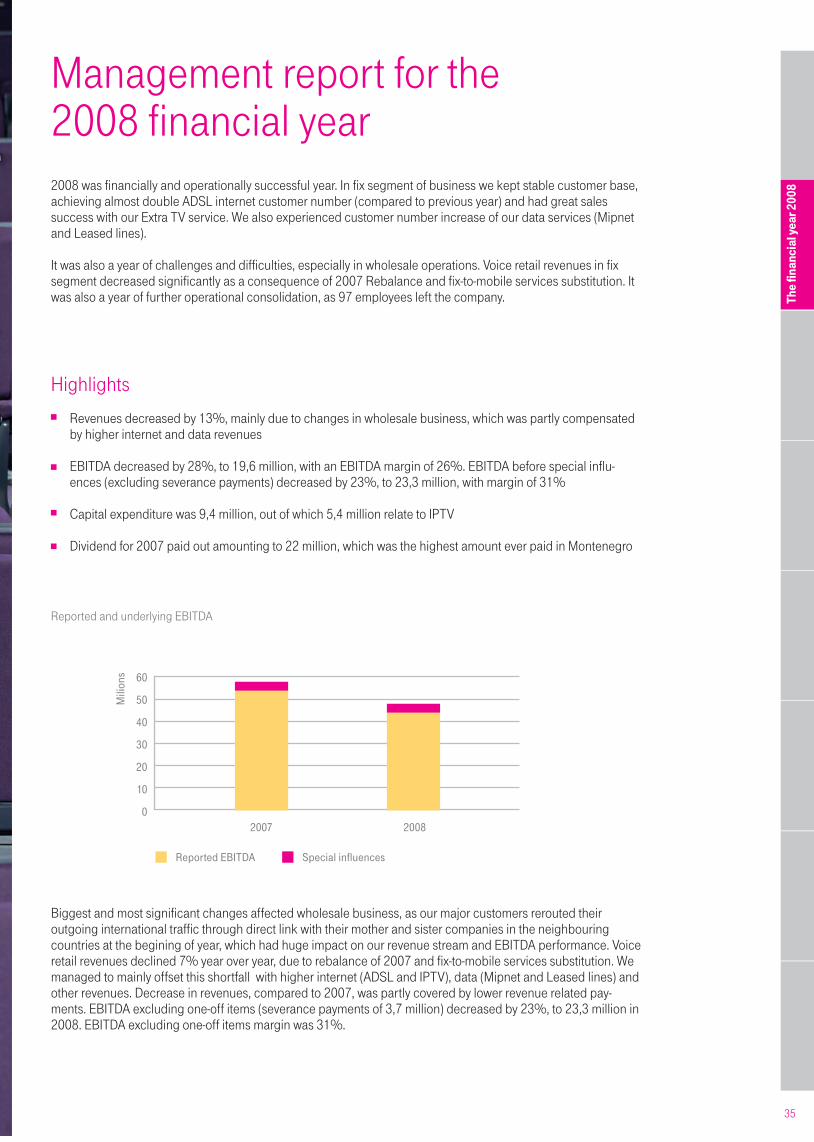

Management report for the2008 financial year2008 was financially and operationally successful year. In fix segment of business we kept stable customer base, achieving almost double ADSL internet customer number (compared to previous year) and had great sales success with our Extra TV service. We also experienced customer number increase of our data services (Mipnet and Leased lines).

It was also a year of challenges and difficulties, especially in wholesale operations. Voice retail revenues in fix segment decreased significantly as a consequence of 2007 Rebalance and fix-to-mobile services substitution. It was also a year of further operational consolidation, as 97 employees left the company.

Highlights

Revenues decreased by 13%, mainly due to changes in wholesale business, which was partly compensated by higher internet and data revenues

EBITDA decreased by 28%, to 19,6 million, with an EBITDA margin of 26%. EBITDA before special influ-ences (excluding severance payments) decreased by 23%, to 23,3 million, with margin of 31%

Capital expenditure was 9,4 million, out of which 5,4 million relate to IPTV

Dividend for 2007 paid out amounting to 22 million, which was the highest amount ever paid in Montenegro

Biggest and most significant changes affected wholesale business, as our major customers rerouted their outgoing international traffic through direct link with their mother and sister companies in the neighbouring countries at the begining of year, which had huge impact on our revenue stream and EBITDA performance. Voice retail revenues declined 7% year over year, due to rebalance of 2007 and fix-to-mobile services substitution. We managed to mainly offset this shortfall with higher internet (ADSL and IPTV), data (Mipnet and Leased lines) and other revenues. Decrease in revenues, compared to 2007, was partly covered by lower revenue related pay-ments. EBITDA excluding one-off items (severance payments of 3,7 million) decreased by 23%, to 23,3 million in 2008. EBITDA excluding one-off items margin was 31%.

Reported and underlying EBITDA

The

finan

cial

yea

r 200

8

0

10

2007

Reported EBITDA

2008

20

30

40

50

60

Mili

ons

Special influences

36

Customers number of 170 thousand decreased only 2,5% year over year. Thanks to the strong focus on broad-band services, the number of ADSL internet customers reached almost 28 thousand, while Extra TV service counted more than 17,5 thousand customers.

0

20

2007 2008

40

60

80

Mili

ons

Wholesale voice Retail voice Internet Data Other

Revenue structure

0

20

174,6

14,4

170,2

27,8

2,417,5

2007

ADSL Internet customers Extra TV customers

40

60

80

100

120

140

160

180

200

Thou

sand

s

2008

Fix RPC

37

The

finan

cial

yea

r 200

8

Crnogorski Telekom a.d. Podgorica

International Financial Reporting StandardsFinancial Statements andIndependent Auditor’s Report

For the year ended 31 December 2008

38

39

Contents

Independent Auditor’s Report 40

Standalone Financial Statements:

Balance Sheet 43

Income Statement 44

Statement of Changes in Equity 45

Cash Flow Statement 46

Notes to the Financial Statements 47

The

finan

cial

yea

r 200

8

INDEPENDENT AUDITOR’S REPORT

The

finan

cial

yea

r 200

8

INDEPENDENT AUDITOR’S REPORT

42

43

The

finan

cial

yea

r 200

8

BALANCE SHEET

ASSETS (in EUR)

As at December 31,

Note 2007 2008

Non current assets

Property, plant and equipment 5 90.114.835 88.485.089

Intangible assets 4 8.086.609 7.890.156

Investments in subsidiaries and associates 6 21.855.370 21.855.370

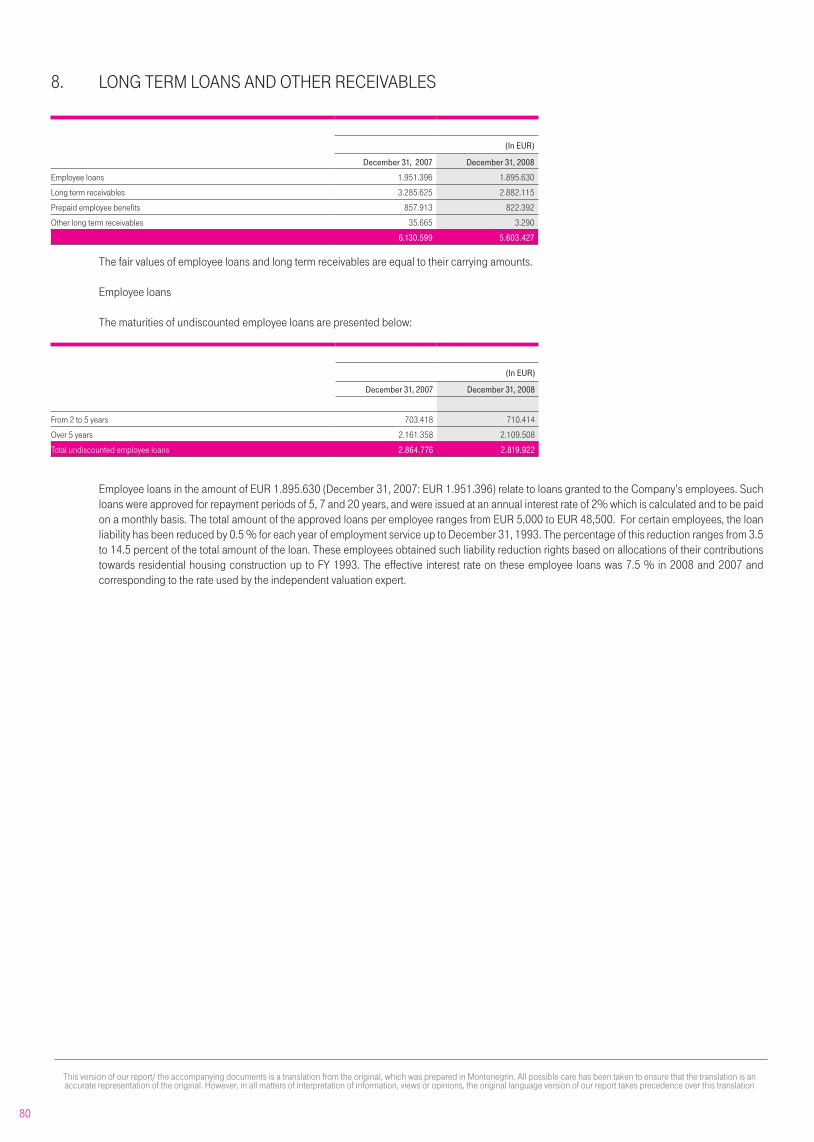

Long term loans and other receivables 8 6.130.599 5.603.427

Available for sale financial assets 7 24.371 25.374

Total non current assets 126.211.784 123.859.416

Current assets

Inventories 9 2.057.730 1.597.100

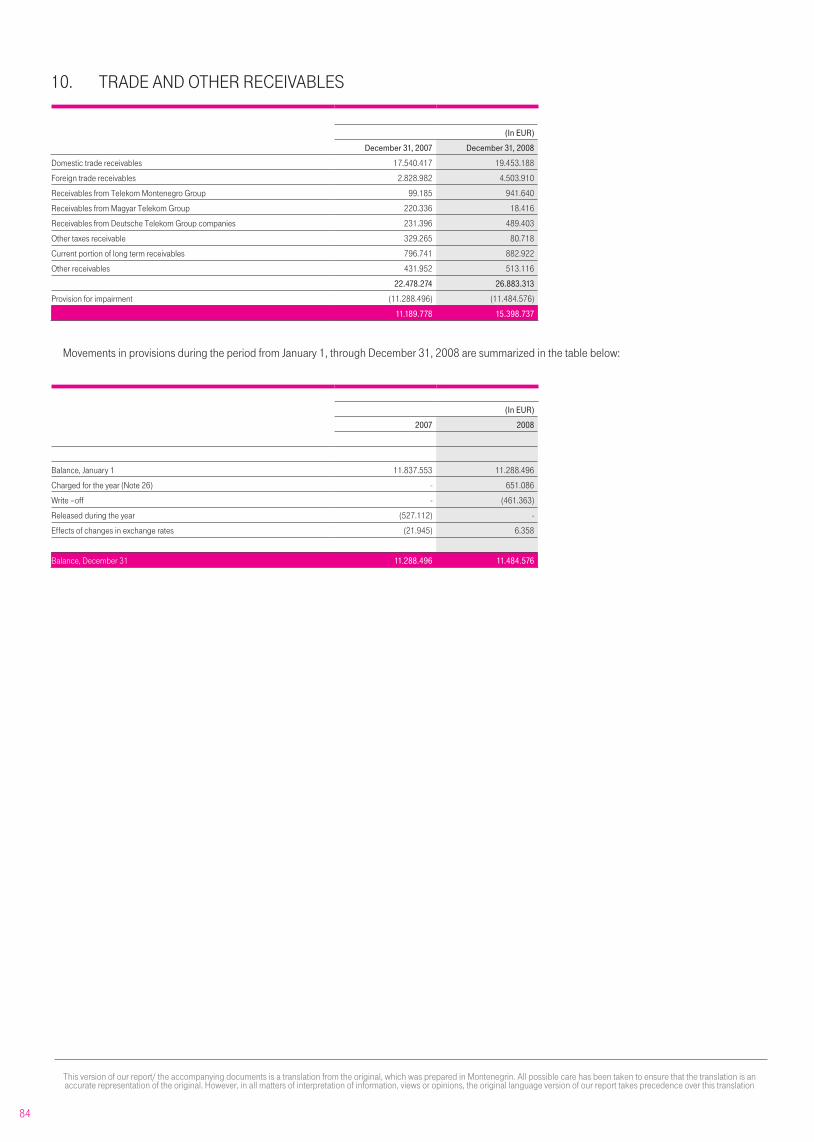

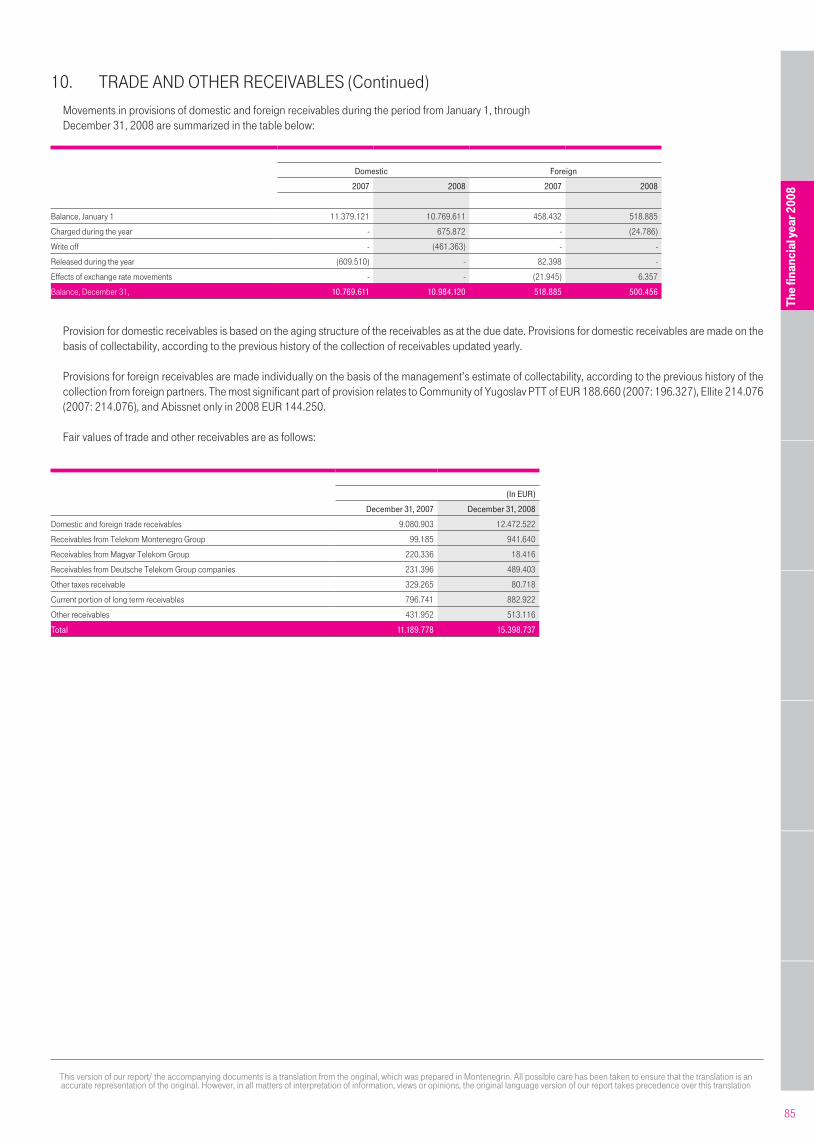

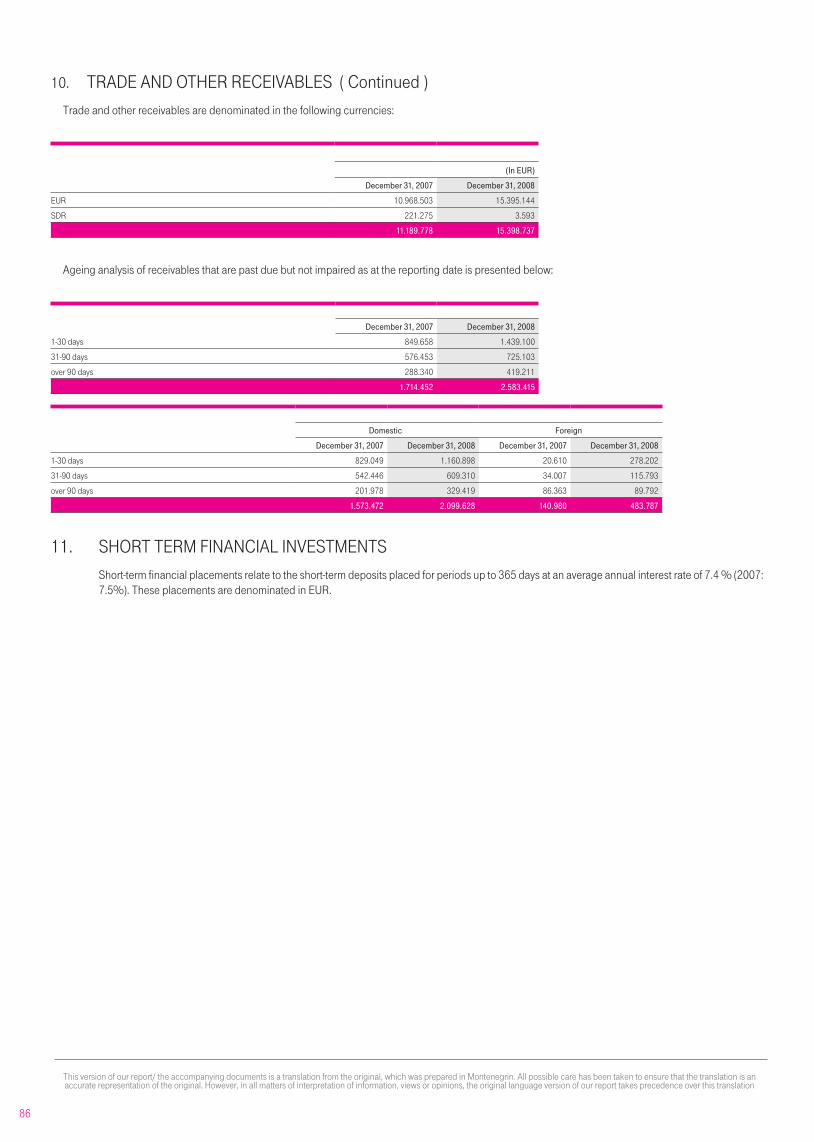

Trade and other receivables 10 11.189.778 15.398.737

Current income tax prepayments - 928.583

Short term financial placement 11 20.500.000 30.000.000

Advances and prepaid expenses 12 4.920.008 4.687.361

Cash and cash equivalents 13 26.014.007 5.630.418

Restricted cash 14 299.630 312.265

Total current assets 64.981.153 58.554.464

Total assets 191.192.937 182.413.880

EQUITYShareholders’ equity

Share capital 16 140.996.394 140.996.394

Retained earnings 23.733.086 10.898.899

Statutory reserves 17 684.256 1.984.002

Total shareholders’ equity 165.413.736 153.879.295

LIABILITIESCurrent liabilities

Trade and other payables 20 8.248.514 10.285.871

Accrued liabilities and advances 21 7.894.785 9.872.484

Provision for liabilities and charges 18 5.175.445 5.181.172

Current income tax payable 1.632.548 -

Total current liabilities 22.951.292 25.339.526

Non current liabilities

Deferred income tax liability 19 2.297.979 2.393.509

Provision for liabilities and charges 18 529.930 801.550

Total non current liabilities 2.827.909 3.195.059

Total liabilities 25.779.201 28.534.585

Total liabilities and equity 191.192.937 182.413.880

The accompanying notes on pages 47 to 109 are an integral part of these financial statements.

These financial statements have been approved for issue by the Board of Directors of Crnogorski Telekom A.D. on 24 March 2009 and are signed on their behalf by

________________________ ______________________ ________________________ Slavoljub Popadić Dragan Mićović Slaviša JovanoviċChief Executive Officer Accounting Director Accounting Manager

This version of our report/ the accompanying documents is a translation from the original, which was prepared in Montenegrin. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version of our report takes precedence over this translation

44

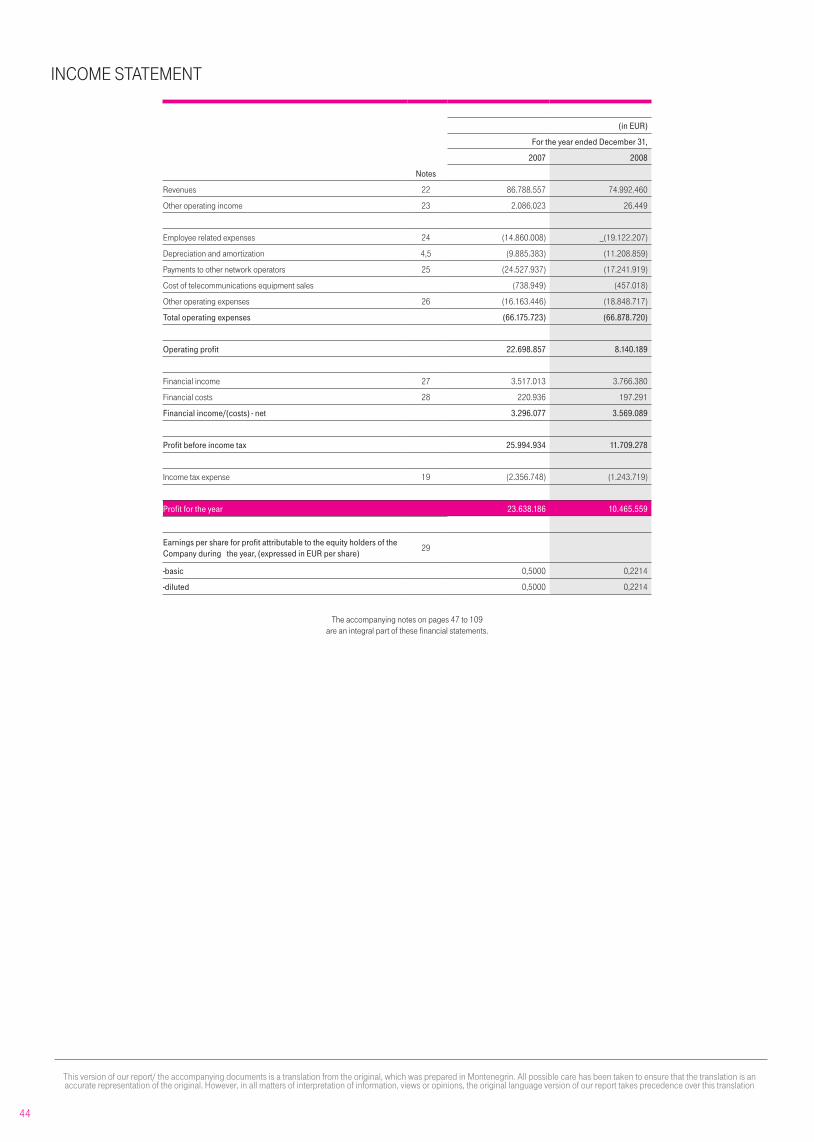

INCOME STATEMENT

(in EUR)

For the year ended December 31,

2007 2008

Notes

Revenues 22 86.788.557 74.992.460

Other operating income 23 2.086.023 26.449

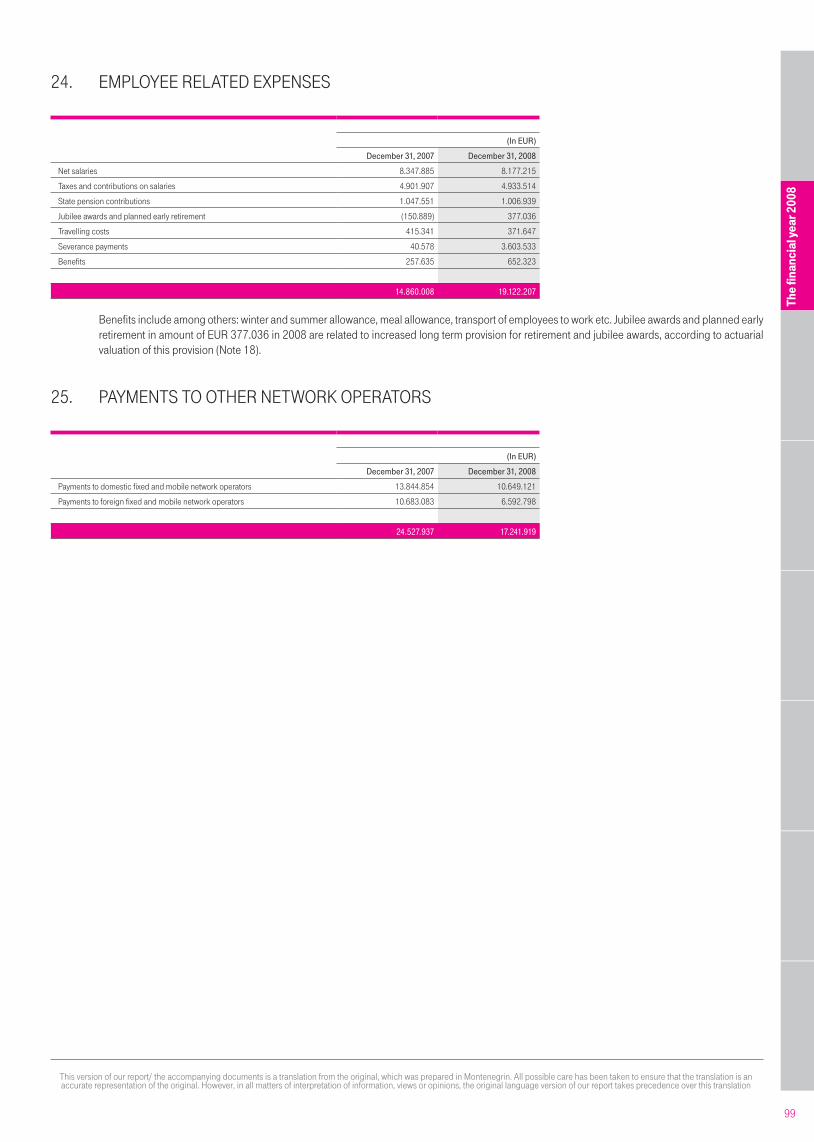

Employee related expenses 24 (14.860.008) _(19.122.207)

Depreciation and amortization 4,5 (9.885.383) (11.208.859)

Payments to other network operators 25 (24.527.937) (17.241.919)

Cost of telecommunications equipment sales (738.949) (457.018)

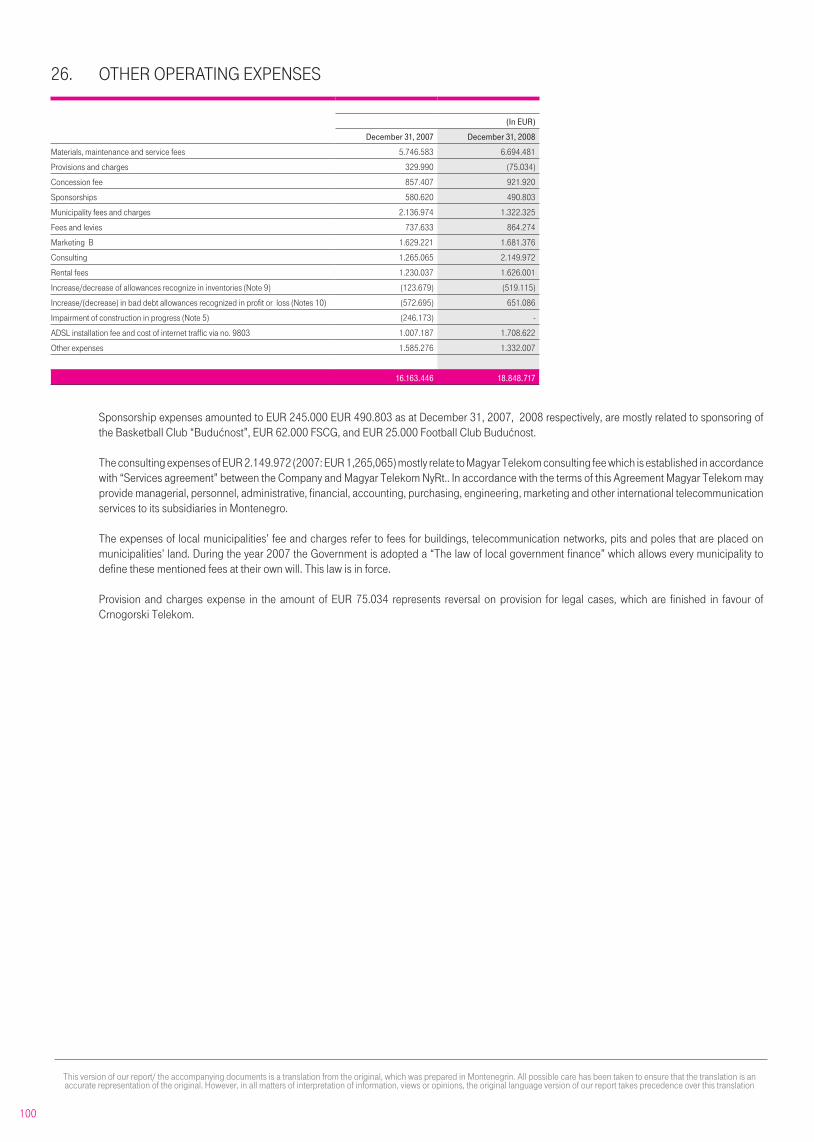

Other operating expenses 26 (16.163.446) (18.848.717)

Total operating expenses (66.175.723) (66.878.720)

Operating profit 22.698.857 8.140.189

Financial income 27 3.517.013 3.766.380

Financial costs 28 220.936 197.291

Financial income/(costs) - net 3.296.077 3.569.089

Profit before income tax 25.994.934 11.709.278

Income tax expense 19 (2.356.748) (1.243.719)

Profit for the year 23.638.186 10.465.559

Earnings per share for profit attributable to the equity holders of the Company during the year, (expressed in EUR per share)

29

-basic 0,5000 0,2214

-diluted 0,5000 0,2214

The accompanying notes on pages 47 to 109are an integral part of these financial statements.

45

STATEMENT OF CHANGES IN EQUITYFor the year ended December 31, 2008

(In EUR)

Share capital Statutory reserves Retained earnings Total

Balance, January 2007 140.996.394 - 9.079.156 150.075.550

Dividends - - (8.300.000) (8.300.000)

Allocation of retained earnings - 684.256 (684.256) -

Profit for the year - - 23.638.186 23.638.186

Balance, December 31, 2007 140.996.394 684.256 23.733.086 165.413.736

Balance, January 2008 140.996.394 684.256 23.733.087 165.413.736

Dividends - - (22.000.000) (22.000.000)

Allocation of retained earnings - 1.299.747 (1.299.747) -

Profit for the year - - 10.465.559 10.465.559

Balance, December 31, 2008 140.996.394 1.984.002 10.898.899 153.879.295

The accompanying notes on pages 47 to 109are an integral part of these financial statements.

The

finan

cial

yea

r 200

8

46

CASH FLOW STATEMENTFor the year ended December 31, 2008

(In EUR)

Notes 2007 2008

Cash flows from operating activities

Cash generated from operations 36 23.393.101 18.537.665

Income tax paid (1.207.062) (3.709.318)

Interest paid (10.816) (1.931)

Net cash flows from operating activities 22.175.223 14.826.415

Cash flows from investing activities

Purchase of tangible and intangible assets 4,5 (8.650.365) (9.383.664)

Short term financial placement (20.500.000) (9.500.000)

Interest received 2.837.670 3.258.017

Proceeds from disposal of non current assets 1.116.898 -

Release of deposit for sold investment in Crnogorska Komercijalna Banka 12 - 1.856.059

Net cash flows from investing activities (25.195.797) (13.769.589)

Cash flows from financing activities

Dividends paid to shareholders and minority interest (8.066.315) (21.440.415)

Repayment of loans and other borrowings (526.680) -

Net cash flows from financing activities (8.592.995) (21.440.415)

Change in cash and cash equivalents (11.613.569) (20.383.589)

Cash and cash equivalents, beginning of year 13 37.627.576 26.014.007

Cash and cash equivalents, end of year 13 26.014.007 5.630.418

The accompanying notes on pages 47 to 109are an integral part of these financial statements.

47

1. FOUNDATION AND ACTIVITIESTelekom Crne Gore A.D., Podgorica (“Telekom” or the “Company”) was founded and registered with the Commercial Court of Podgorica under Decision numbered Fi. 5490/98 of December 31, 1998, subsequent to the completion of the ownership transformation and separation processes of the telecommunication and postal businesses of the Public Enterprise of Post, Telegraph and Telecommunications of the Republic of Montenegro (“JP PTT Crna Gora”).

In accordance with the Republic of Montenegro Company Law, the Company was newly registered on November 6, 2002 into the Central Registry of the Commercial Court of Podgorica under registration inscription numbered 4-0000618/001.

The Company’s principal activities are involved in: the maintenance and utilization of the Republic of Montenegro telecommunication system, the development of telecommunication technologies, and in the provision of telecommunication services.

The Company is the principal provider of fixed telephony services in the Republic of Montenegro, as well as of the local, national and international telephony services, in addition to a wide range of other telecommunication services involving leased circuits, data networks, telex and telegraph services. In accordance with the Republic of Montenegro Telecommunications Law, the Company’s market position as an exclusive supplier of fixed-line telephony services was officially suspended on December 31, 2003.

During 2000, Telekom rolled out a GSM 900 mobile network and in the May 2000 launched its commercial operation as a provider of mobile telephony. On July 28, 2000 Telekom registered Monet D.O.O. (“Monet”) as it’s fully owned subsidiary and subsequently transferred the mobile telephony business to Monet. The Montenegro mobile telephony market is liberalized and Monet (present name T Mobile Crna Gora d.o.o., Podgorica) competes with another operator “Pro Monte” D.O.O.

Following the decision of Deutsche Telekom and Magyar Telekom, on May 23, 2006 the General Assembly of Telekom Crna Gora A.D. approved the introduction of the „T“ brands in Montenegro. On July 3, 2006 the General Assembly of „Telekom Crna Gora A.D.“ approved the change of the Company’s name to „Crnogorski Telekom A.D.“. The new Company name was registered on September 25, 2006 at the Court of Registrar of the Republic of Montenegro under registration number 4-0000618/14.

Following a successful privatization tender Crnogorski Telekom A.D., Podgorica (former Telekom Crna Gora A.D.) was acquired by Magyar Telekom NyRt. (hereinafter referred as to Magyar Telekom). Magyar Telekom obtained control of Crnogorski Telekom A.D., Podgorica on March 31, 2005 and by the end of 2005 it had a 76.53% stake.. The Company owns 100% of the capital of T Mobile Crna Gora d.o.o. (former Monet d.o.o.), the Montenegrin mobile company and 100% of the share capital of Internet Crna Gora . On 7 March, 2005 Telekom acquired additional 15% shares. Deutsche Telekom AG is the ultimate controlling owner of Magyar Telekom holding 59.21% of the issued shares.

The

finan

cial

yea

r 200

8

48

1. FOUNDATION AND ACTIVITIES (Continued)Telekom is domiciled in Podgorica, in the Republic of Montenegro at the following street address: Moskovska 29. at December, 2008, Telekom had 697 employees (December 31, 2007 – 706 employees).

Investigation into certain consultancy contracts

As previously disclosed, in the course of conducting their audit of Magyar Telekom’s 2005 financial statements, PricewaterhouseCoopers Könyvvizsgáló és Gazdasági Tanácsadó Kft. (“PWC”) identified two contracts the nature and business purposes of which were not readily apparent to them. In February 2006, Magyar Telekom’s Audit Committee retained White & Case (the “independent investigators”), as its independent legal counsel, to conduct an internal investigation into whether the Company had made payments under those, or other contracts, potentially prohibited by U.S. laws or regulations, including the Foreign Corrupt Practices Act (“FCPA”), or internal Company policy. The Audit Committee also informed the U.S. Department of Justice (“DOJ”) and the U.S. Securities and Exchange Commission (“SEC”), and the Hungarian Supervisory Financial Authority of the internal investigation.

Based on the documentation and other evidence obtained by it, White & Case preliminarily concluded that there was reason to believe four consulting contracts entered into in 2005 were entered into to serve improper objectives, and further found that, during 2006, certain employees had destroyed evidence that was relevant to the investigation. The internal investigation is continuing into these and other contracts identified by the independent investigators.

In 2007 the Supreme State Prosecutor of the Republic of Montenegro informed the Board of Directors of Crnogorski Telekom, of her conclusion that the contracts subject to the internal investigation in Montenegro included no elements of any type of criminal act for which prosecution would be initiated in Montenegro.

Hungarian authorities also commenced their own investigations into Magyar Telekom’s activities in Montenegro. The Hungarian National Bureau of Investigation has informed Magyar Telekom that it closed its investigation as of May 20, 2008 without identifying any criminal activity.

United States authorities commenced their own investigations concerning the transactions which are the subject of our internal investigation, to determine whether there have been violations of U.S. law. During 2007, the U.S. authorities expanded the scope of their investigations to include an inquiry into our actions taken in connection with the internal investigation and our public disclosures regarding the internal investigation.

We cannot predict when the internal investigation or the ongoing Government investigations will be concluded, what the final outcome of those investigations may be, or the impact, if any, they may have on our financial statements or results of operations. Government authorities could seek criminal or civil sanctions, including monetary penalties, against us or our affiliates, as well as additional changes to our business practices and compliance programs.

49

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

2.1. Basis of Preparation and Presentation of the Financial Statements

The financial statements of Crnogorski Telekom A.D., Podgorica, have been prepared in accordance with the International Financial Reporting Standards issued by the International Accounting Standards Board (IASB) and effective at the time of preparing the financial statements and with the requirements of the Law on Accounting and Auditing of Montenegro. The financial statements have been prepared under historical cost convention, except for fair value of available for sale investments as disclosed in the accounting policies below.

The Company maintains its accounting records and prepares its statutory financial statements in conformity with the Accounting and Auditing Law of the Republic of Montenegro (Official Gazette of the Republic of Montenegro numbered 69/2005) and specifically, in accordance with the relevant decision pertaining to the application of International Accounting Standards in the Republic of Montenegro (Official Gazette of the Republic of Montenegro numbered 69/2002). Pursuant to the aforecited provisions, the International Financial Reporting Standards (IFRS) were applied for the first time as the Company’s primary basis of accounting for the reporting year commencing on January 1, 2003.

The official currency in the Republic of Montenegro and the Company’s functional currency is Euro (EUR).

The Company has also prepared consolidated financial statements in accordance with IFRS for the Company and its subsidiaries (the “Group”). In the consolidated financial statements, subsidiary undertakings - which are those companies in which the Company, directly or indirectly, has an interest of more than half of the voting rights or otherwise has power to exercise control over the operations - have been fully consolidated.

Users of these stand-alone financial statements should read them together with the Group’s consolidated financial statements as at and for the year ended December 31, 2008 in order to obtain full information on the financial position, results of operations and changes in financial position of the Group as a whole.

Initial application of standards interpretations and amendments to standards and interpretations in the financial year

In the current year, the Company has adopted all of the new and revised Standards and Interpretations issued by the International Accounting Standards Board (the IASB) and the International Financial Reporting Interpretations Committee (the IFRIC) of the IASB that are relevant to its operations and effective for annual reporting periods beginning on 1 January 2008. The initial application of these pronouncements did not have a material impact on the presentation of the Company’s results of operations, financial position or cash flows. Listed below are those new or amended standards or interpretations:

The

finan

cial

yea

r 200

8

50

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

2.1. Basis of Preparation (continued)- IAS 39 (Amended) - Financial Instruments: Recognition and Measurement. The IASB published on October 14, 2008 amendments to IAS 39

and IFRS 7 - Financial Instruments: Disclosures. The amendments relate to the possibility to reclassify financial instruments measured at fair value through profit of loss. So far, reclassifications in and out of this category were not allowed. The amendment now enables under certain circumstances a reclassification. If based on the new rules a reclassification is done, the amended IFRS 7 demands additional disclosures. The amendments had no effect on Crnogorski Telekom’s equity or Net income or implications for reporting. As the Company did not make and does not intend to make such reclassifications. The amendment is effective from July 2008.

- IFRIC 11 Interpretation to IFRS 2 - Company and Treasury shares transactions. Under IFRS 2 it was not defined exactly how it should be calculated where the employees of a subsidiary received the shares of a parent. IFRIC 11 clarifies that certain types of transactions are accounted for as equity-settled or cash-settled transactions under IFRS 2. It also addresses the accounting for share-based payment transactions involving two or more entities within one company. The Company applied this Interpretation from January 1, 2008, but as no such transactions have happened so far, it did not have an impact on the Company’s accounts.

- IFRIC 14 Interpretation on IAS 19 - The Limit on Defined Benefit Assets, Minimum Funding Requirements and their Interaction. IFRIC 14 provides general guidance on how to assess the limit in IAS 19 Employee Benefits on the amount of the surplus that can be recognized as an asset. It also explains how the pensions asset or liability may be affected when there is a statutory or contractual minimum funding requirement. This Interpretation is not applicable to the Company as the Company has no funded defined post-retirement benefit schemes.

Standards, interpretations and amendments issued that are not yet effective

The Company has chosen not to early adopt the following standard and interpretations that were issued but not yet effective for accounting periods beginning on 1 January 2008. Listed below are those new or amended standards or interpretations:

- Amendment to IAS 1, Presentation of Financial Statements – Capital Disclosures (effective from 1 January 2008). The amendment to IAS 1 introduces disclosures about the level of an entity’s capital and how it manages capital in accordance with internal and external (regulatory) requirements.

The Company assessed the impact of the amendment to IAS 1, and concluded that no additional disclosures are necessary in the financial statements as the Company does not have any specific internal and external requirements related to capital management.

51

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

2.1. Basis of Preparation (continued)- IAS 27 (Amendment), ‘Consolidated and separate financial statements’ (effective from 1 January 2009). The amendment is part of the IASB’s

annual improvements project published in May 2008. Where an investment in a subsidiary that is accounted for under IAS 39, ‘Financial instruments: recognition and measurement’, is classified as held for sale under IFRS 5, ‘Non-current assets held-for-sale and discontinued operations’, IAS 39 would continue to be applied. The amendment will not have an impact on the Company’s operations because it is the Company’s policy for an investment in subsidiary to be recorded at cost in the standalone accounts of each entity. IAS 28 (Amendment), ‘Investments in associates’ (and consequential amendments to IAS 32, ‘Financial Instruments: Presentation’ and IFRS 7, ‘Financial instruments: Disclosures’) (effective from 1 January 2009). The amendment is part of the IASB’s annual improvements project published in May 2008. Where an investment in associate is accounted for in accordance with IAS 39 ‘Financial instruments: recognition and measurement’, only certain rather than all disclosure requirements in IAS 28 need to be made in addition to disclosures required by IAS 32, ‘Financial Instruments: Presentation’ and IFRS 7 ‘Financial Instruments: Disclosures’. The amendment will not have an impact on the Company’s operations because it is the Company’s policy for an investment in an associate to be equity accounted in the Company’s consolidated accounts.

- IAS 31 (Amendment), ‘Interests in joint ventures’ (and consequential amendments to IAS 32 and IFRS 7) (effective from 1 January 2009). The amendment is part of the IASB’s annual improvements project published in May 2008. Where an investment in joint venture is accounted for in accordance with IAS 39, only certain rather than all disclosure requirements in IAS 31 need to be made in addition to disclosures required by IAS 32, ‘Financial instruments: Presentation’, and IFRS 7 ‘Financial instruments: Disclosures’. The amendment will not have an impact on the Company’s operations as there are no interests held in joint ventures.

- IAS 38 (Amendment), ‘Intangible assets’ (effective from 1 January 2009). The amendment is part of the IASB’s annual improvements project published in May 2008. The amendment deletes the wording that states that there is ‘rarely, if ever’ support for use of a method that results in a lower rate of amortisation than the straight-line method. The amendment will not have an impact on the Company’s operations, as all intangible assets are amortised using the straight-line method.