Criteo 101criteo.investorroom.com/download/CRTO+101+Presentation...Investor Presentation November...

83

Criteo 101 Investor Presentation November 2017

Transcript of Criteo 101criteo.investorroom.com/download/CRTO+101+Presentation...Investor Presentation November...

1

Criteo 101Investor PresentationNovember 2017

2

This presentation contains “forward-looking” statements that are based on our management’s beliefs and assumptions and on information currently available to management. Forward-looking statements include information concerning our possible or assumed future results of operations, business strategies, financing plans, projections, competitive position, industry environment, potential growth opportunities, potential market opportunities and the effects of competition. Forward-looking statements include all statements that are not historical facts and can be identified by terms such as “anticipates,” “believes,” “could,” “seeks,” “estimates,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “will,” “would” or similar expressions and the negatives of those terms. Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Forward-looking statements represent our management’s beliefs and assumptions only as of the date of this presentation. You should read the Company’s most recent Annual Report on Form 10-K filed on March 1, 2017, including the Risk Factors set forth therein and the exhibits thereto, completely and with the understanding that our actual future results may be materially different from what we expect. Except as required by law, we assume no obligation to update these forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in the forward-looking statements, even if new information becomes available in the future.This presentation includes certain non-GAAP financial measures as defined by SEC rules. As required by Regulation G, we have provided a reconciliation of those measures to the most directly comparable GAAP measures, which is available in the Appendix slides.

Safe harbor statement

3

• Ticker: CRTO

• Stock Exchange: NASDAQ Global Market

• CUSIP: 226718104

• Number of shares

outstanding: 65.3M

• Stock Ownership*:

* As of June 30, 2016

• 2016 Financials

• Revenue: $1,799M, +36% at cc

• Revenue ex-TAC: $730M, +37% at cc

• Adjusted EBITDA: $225M, +55% at cc

• Adj. EBITDA margin: 30.8% of Revenue ex-TAC

93%

4% 3%

Free float

Founders & mgmt

VCs

Stock information and selected financials

4

17,000+ retailer and

brand clients

campaigns in 95+

markets

2,700+ employees

30 officesworldwide

1.2B+ active

monthly shoppers

$550B+annual

commerce sales

$27B annual

post-click sales

Selected KPIs

5

Jean-Baptiste RudelleExecutive Chairman and Co-Founder, 47K-Mobile, Lucent, Roland Berger

Eric EichmannChief Executive Officer, 49Living Social, Rosetta Stone, McKinsey & Co.

Dan TeodosiuChief Technology Officer, 50Google, Microsoft, Hewlett-Packard

Mollie SpilmanChief Operating Officer, 49Millenial Media, Yahoo, Advertising.com, Time Warner

Benoit FouillandChief Financial Officer, 52SAP, Business Objects

Jonathan OpdykeChief Strategy Officer, 40HookLogic, Xerox, Beyond Interactive

Tom AurelioExecutive Vice President, Human Resources, 51Priceline, GE, Symantec, CheerNetworks

Management team

Patrick WyattSenior Vice President, 34Yahoo, Estin & Co.

6

Build the highest performing and open commerce marketing ecosystem

Connect shoppers to the things they need and love

Deliver performance at scale to the retailers and brandswho participate

Our vision

7

Technology Performance

Scale Global Presence

Commerce marketing is deeply rooted in our DNA

8

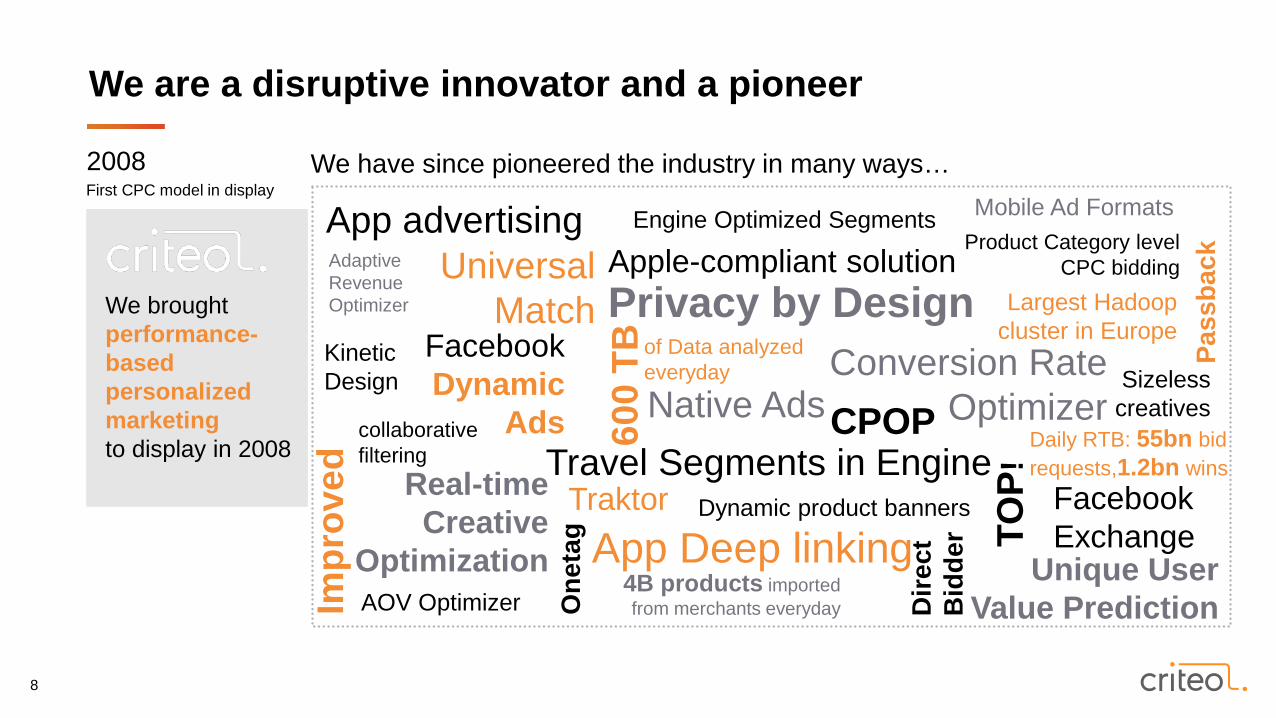

We broughtperformance-based personalized marketing to display in 2008

We have since pioneered the industry in many ways…2008First CPC model in display

We are a disruptive innovator and a pioneer

Real-time Creative

OptimizationAOV Optimizer

Privacy by Design

Facebook Exchange

Universal Match

Apple-compliant solution

Travel Segments in Engine

Conversion Rate Optimizer

4B products imported from merchants everyday

TOP!

Daily RTB: 55bn bid requests,1.2bn wins

Product Category level CPC bidding

600

TB of Data analyzed everyday

Largest Hadoop cluster in Europe

Impr

oved

collaborative filtering

Dynamic product bannersTraktor

Engine Optimized Segments

Pass

back

Sizelesscreatives

One

tag App Deep linking Unique User

Value Prediction

Mobile Ad FormatsApp advertising

Native Ads

AdaptiveRevenue Optimizer

Kinetic Design

Facebook Dynamic

Ads CPOP

Dire

ct

Bid

der

9

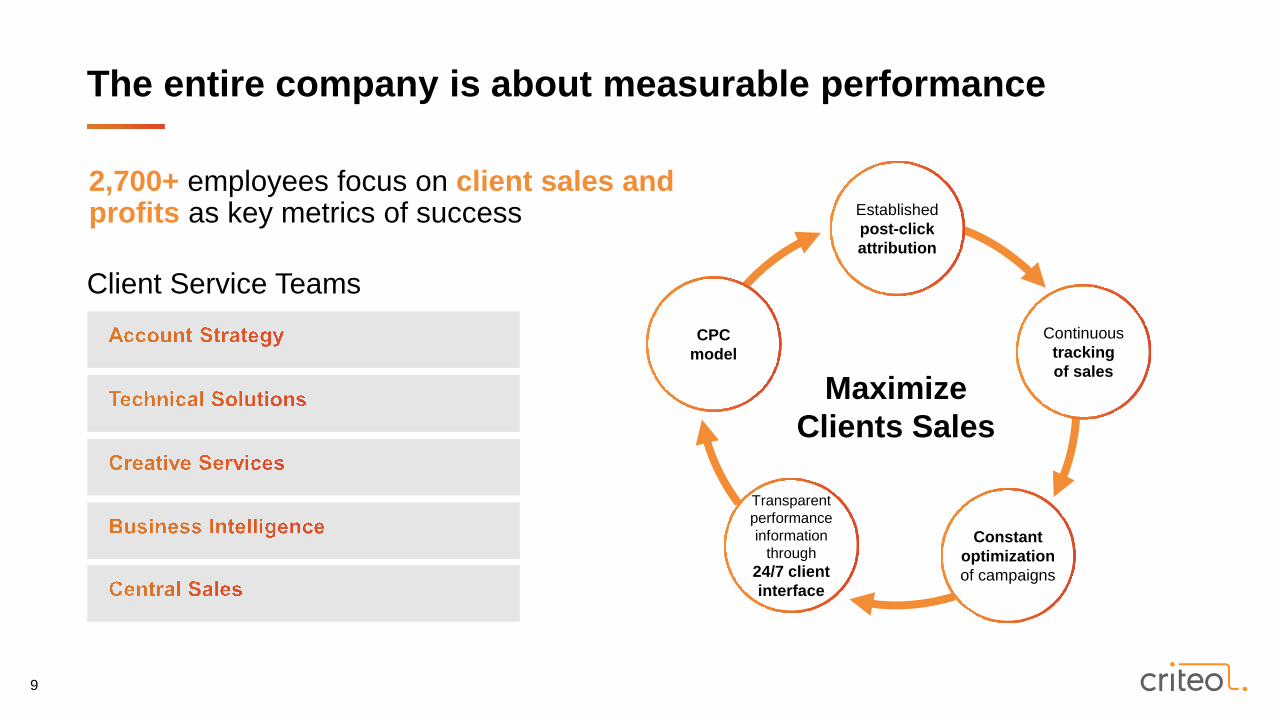

2,700+ employees focus on client sales and profits as key metrics of success

CPC model

Transparent performance information

through24/7 client interface

Constant optimization of campaigns

Continuous tracking of sales

Established post-click attribution

Maximize Clients Sales

The entire company is about measurable performance

Client Service Teams

10

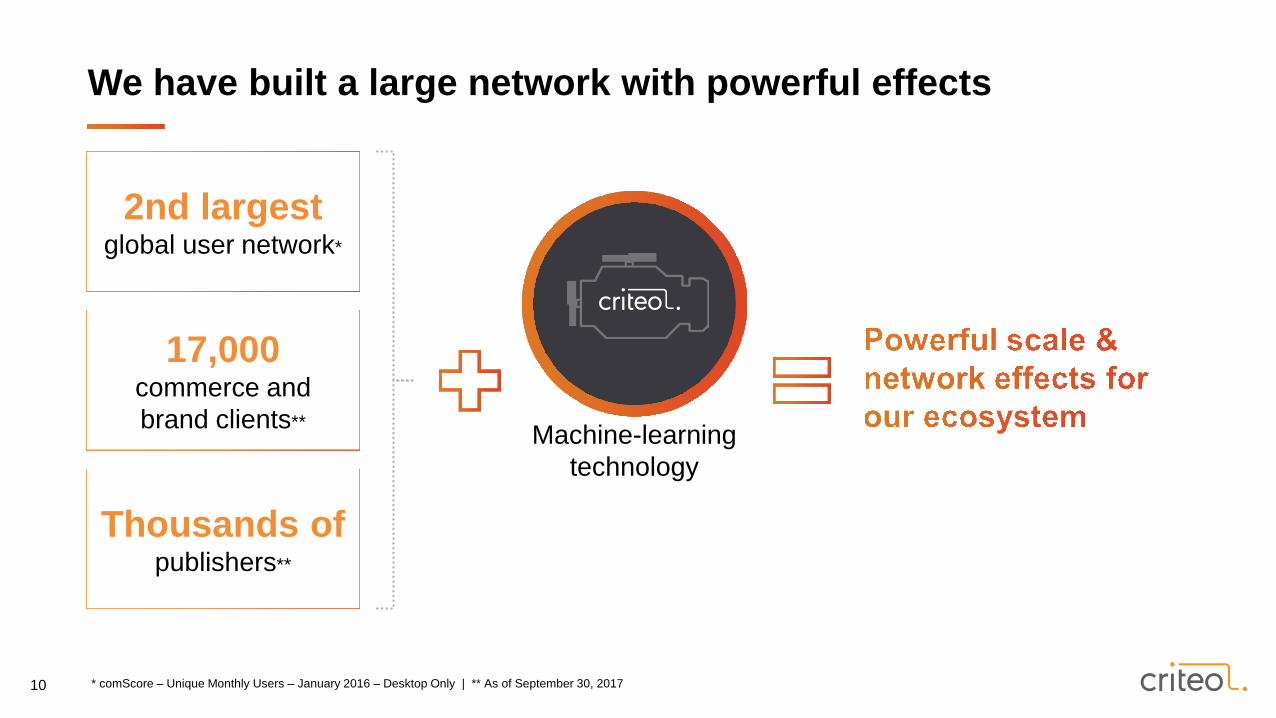

2nd largestglobal user network*

17,000commerce and brand clients**

Thousands ofpublishers**

* comScore – Unique Monthly Users – January 2016 – Desktop Only | ** As of September 30, 2017

Machine-learning technology

We have built a large network with powerful effects

11

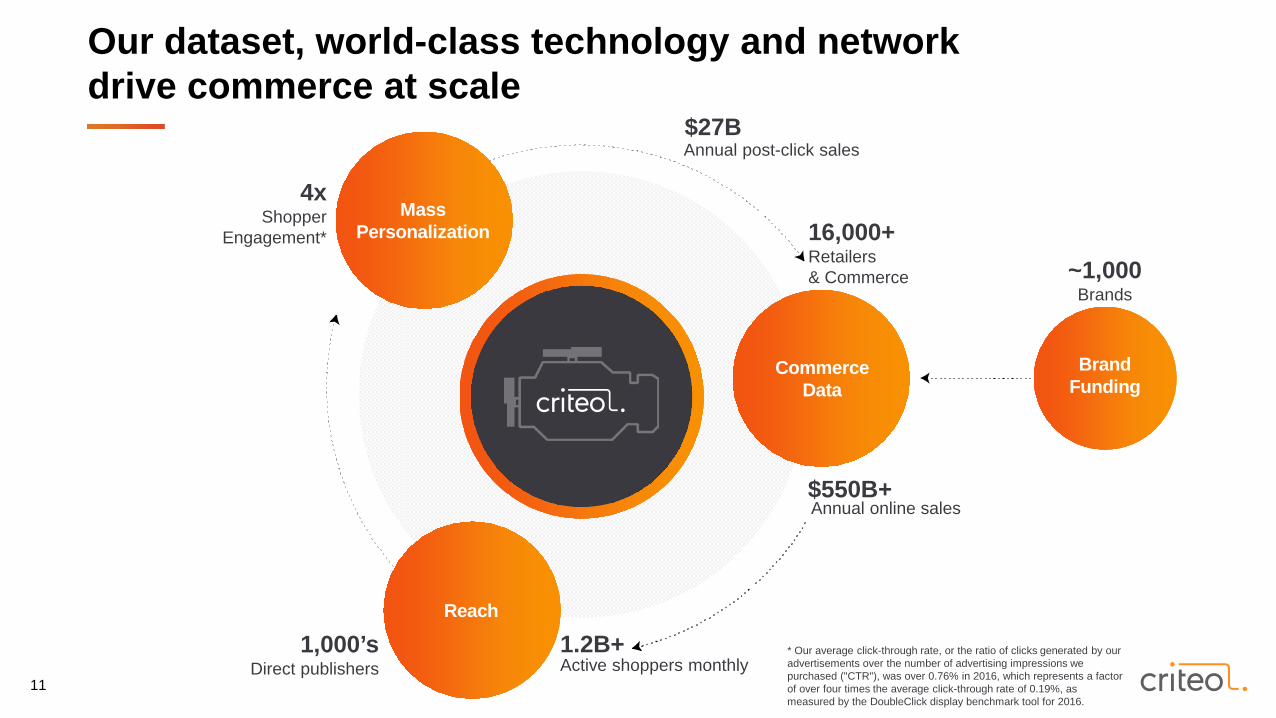

Our dataset, world-class technology and network drive commerce at scale

CommerceData

Reach

16,000+ Retailers & Commerce ~1,000

Brands

1,000’sDirect publishers

4xShopper

Engagement*

$550B+Annual online sales

1.2B+Active shoppers monthly

Brand Funding

$27BAnnual post-click sales

MassPersonalization

* Our average click-through rate, or the ratio of clicks generated by ouradvertisements over the number of advertising impressions we purchased ("CTR"), was over 0.76% in 2016, which represents a factor of over four times the average click-through rate of 0.19%, as measured by the DoubleClick display benchmark tool for 2016.

12

• Actionable data: granular shopper intent and purchase history

• Technology: integrated commerce marketing technology optimized to drive sales and profits

• Scale: maximizing performance and reach across the shopper’s online journey

• Shopper Graph: built through collaboration and data sharing among participants in our ecosystem

A level playing field for retailers and brands requires collaboration in an open ecosystem

Four key pillars support our Commerce Marketing Ecosystem

Data

Technology

Scale

Shopper Graph

13

Boston2012

Barcelona2014

Tokyo 2011

Singapore 2013

São Paulo 2011

Shanghai 2016

Palo Alto2009

New York 2011

Chicago2012

London2008

Madrid 2014

Paris2005

Stockholm 2010

Milan 2012

Munich 2010

Amsterdam2011

Beijing 2013

Seoul 2010

Sydney 2011

Dubai2015

Moscow 2014

San Francisco2014

Osaka 2014Los Angeles

2015

Miami2015

Istanbul2015

Toronto2015

New Delhi2016

nationalities

Grenoble2014

offices in countriesCampaigns in countries

We are a truly global company

Ann Arbor2008

14

Market and Trends

15

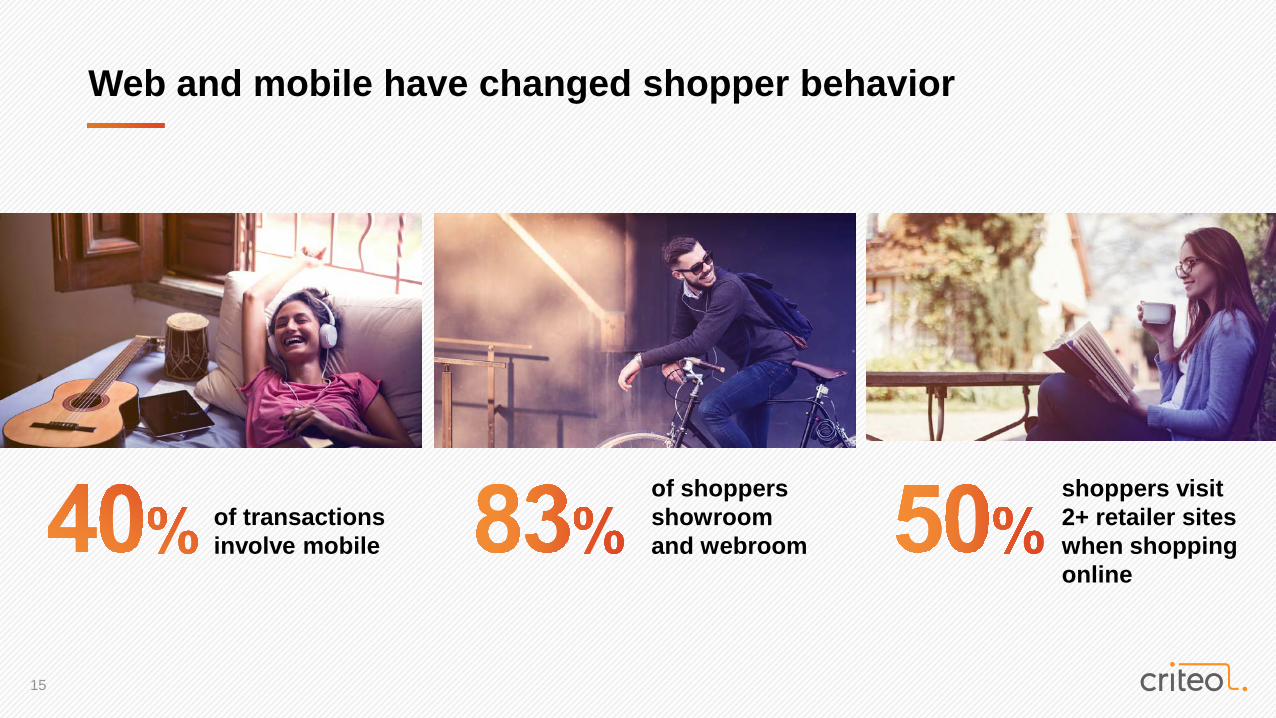

of shoppers showroomand webroom

shoppers visit 2+ retailer sites when shopping online

of transactionsinvolve mobile

Web and mobile have changed shopper behavior

16

Shopper Data• Mass Scale

• Granularity

• Real-Time Accessibility

Activation of Data• Predictive Technology

• Real-time Dynamic Optimization

• Reach at Scale

• Great Real Estate

• Merchandising

Success factors have changed for retailers (and brands)

YESTERDAY TODAY

17

Technology / AI

Media

Brands

Others

Others

Others

Granular shopper information at massive scale

Partial, fragmented, unstructuredview of the shopper

Data OthersOfflineOnline

Data-Driven Marketing Is Critical for Retailers and Brands

18

We are theleader in Commerce Marketing.

is quickly emerging as the next big digital marketing category after Search and Social

Centers on inspiring people to buy things

Measured by performance – directly driving sales and profits

Not limited to digital

20

Commerce marketing has always been our core

Criteo’s original technology was a product recommendation engine for retail

This engine formed the basis of Criteo Dynamic Retargeting

Primarily applied to online commerce: retail, travel and classified

Expanding to include data cooperative across retailers to build an omni-retailer solution

Expanding to include offline data for a full omnichannel solution

21

Products and Technology

22

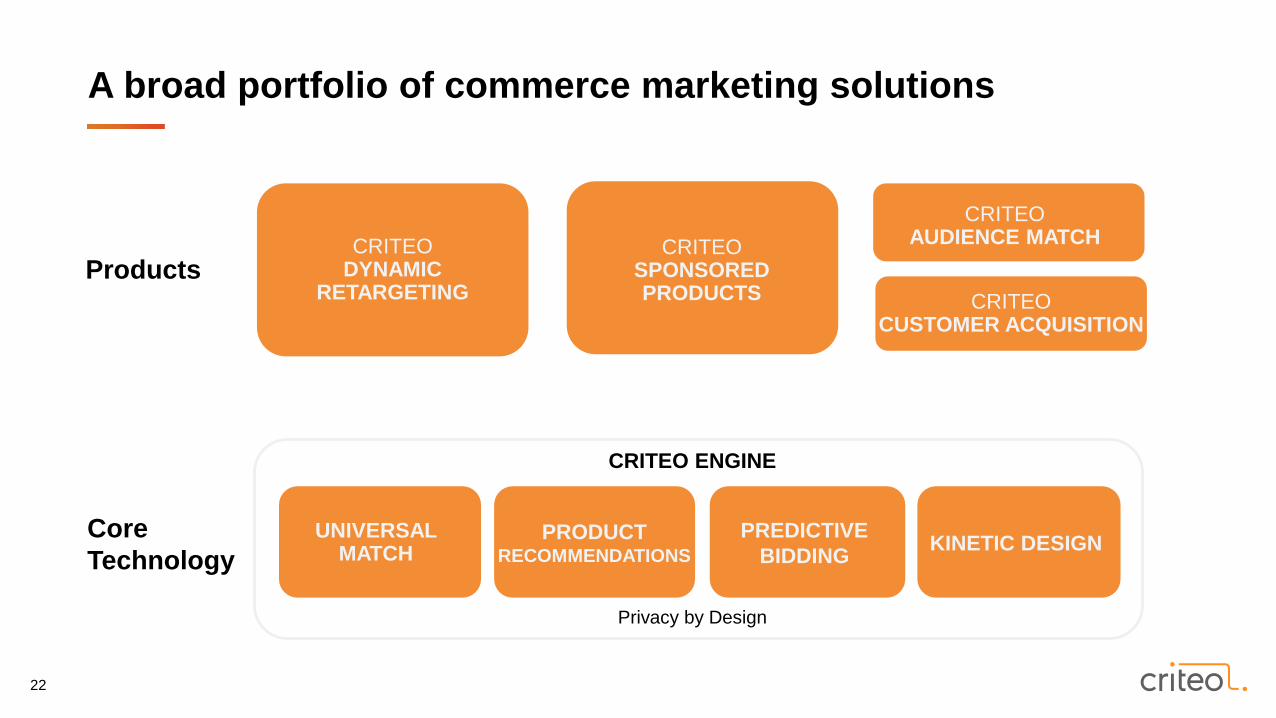

CRITEODYNAMIC

RETARGETING

CRITEOAUDIENCE MATCH

CoreTechnology

Privacy by Design

Products

UNIVERSAL MATCH

PRODUCTRECOMMENDATIONS

PREDICTIVE BIDDING KINETIC DESIGN

CRITEO ENGINE

A broad portfolio of commerce marketing solutions

CRITEOSPONSOREDPRODUCTS CRITEO

CUSTOMER ACQUISITION

23

publisher.com

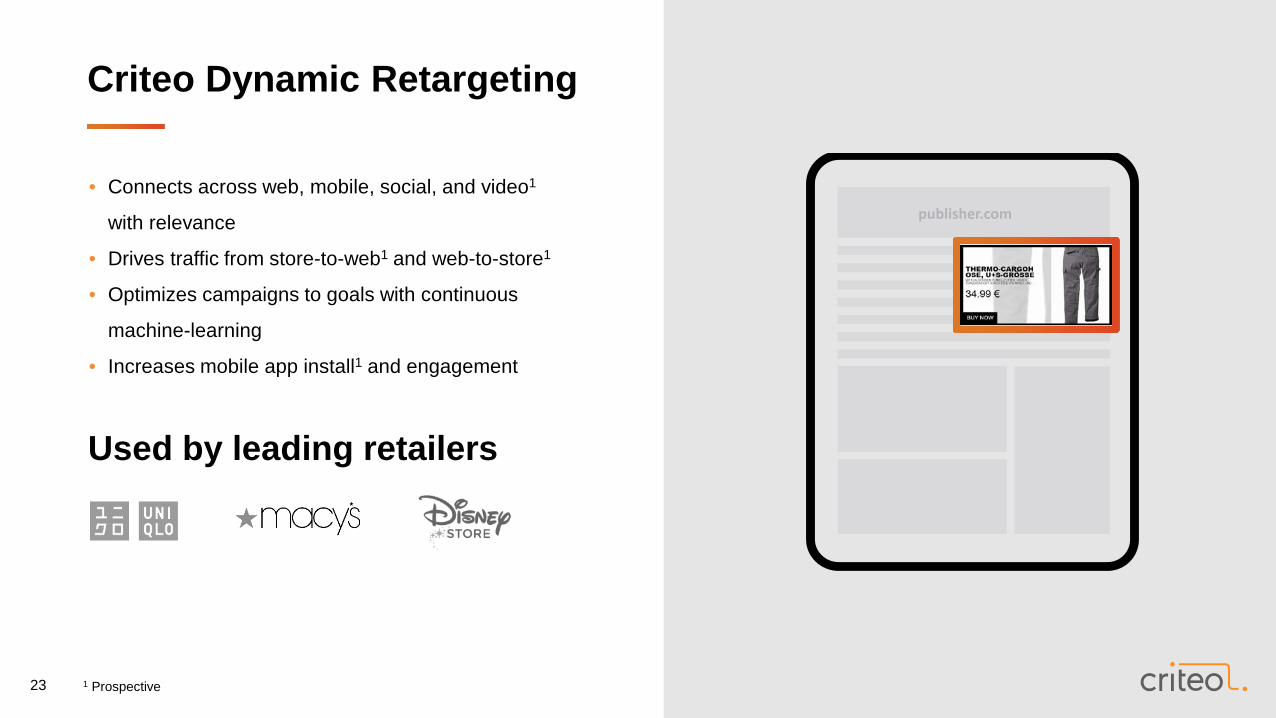

Criteo Dynamic Retargeting

1 Prospective

Used by leading retailers

• Connects across web, mobile, social, and video1

with relevance

• Drives traffic from store-to-web1 and web-to-store1

• Optimizes campaigns to goals with continuous

machine-learning

• Increases mobile app install1 and engagement

24

Criteo Sponsored Products

1 Prospective

• Monetizes brand partners via native ads across

web and app

• Retains shoppers in retailer store to buy

Participating brands

25

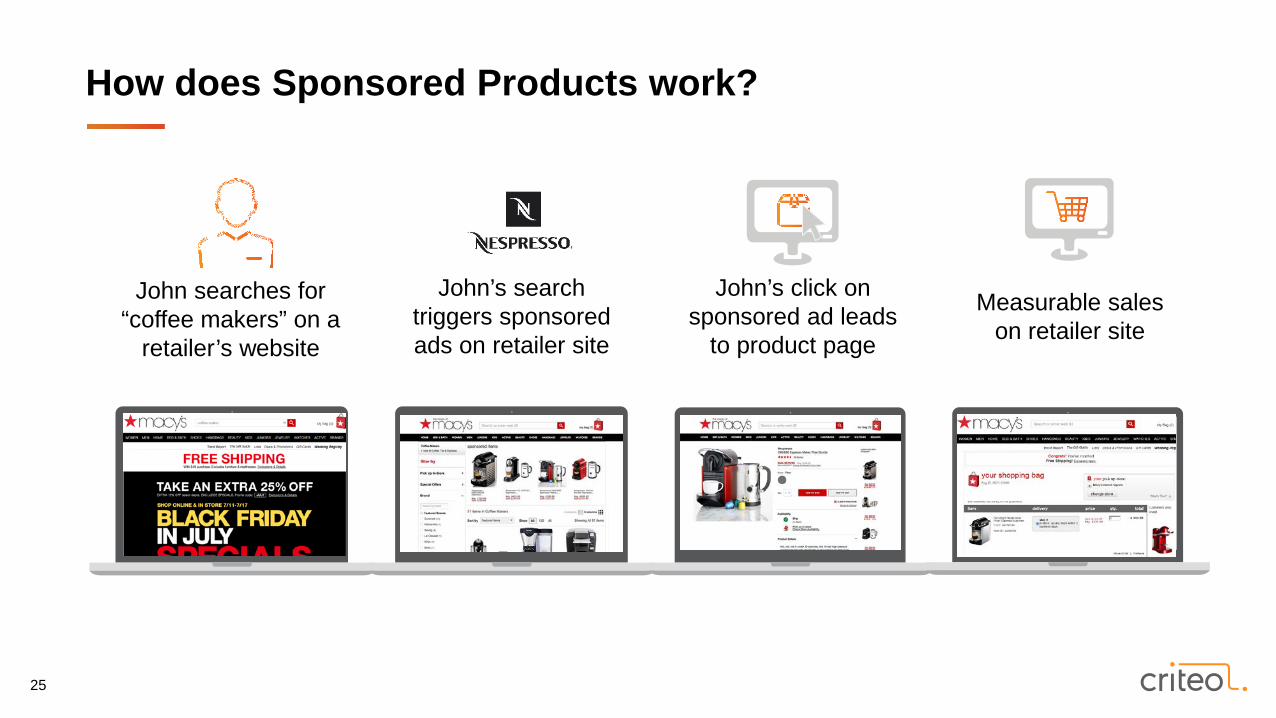

John searches for “coffee makers” on a

retailer’s website

John’s search triggers sponsored ads on retailer site

John’s click on sponsored ad leads

to product page

Measurable sales on retailer site

How does Sponsored Products work?

26

Criteo Audience MatchBETA

What it does• Identify your audience and campaign objective• Pass the audience list you want to target• Match your audience in Criteo’s identity graph• Deliver personalized ads to drive engaged traffic to your store

Benefits• Drive new sales by re-engaging shoppers• Bring qualified traffic to your site

27

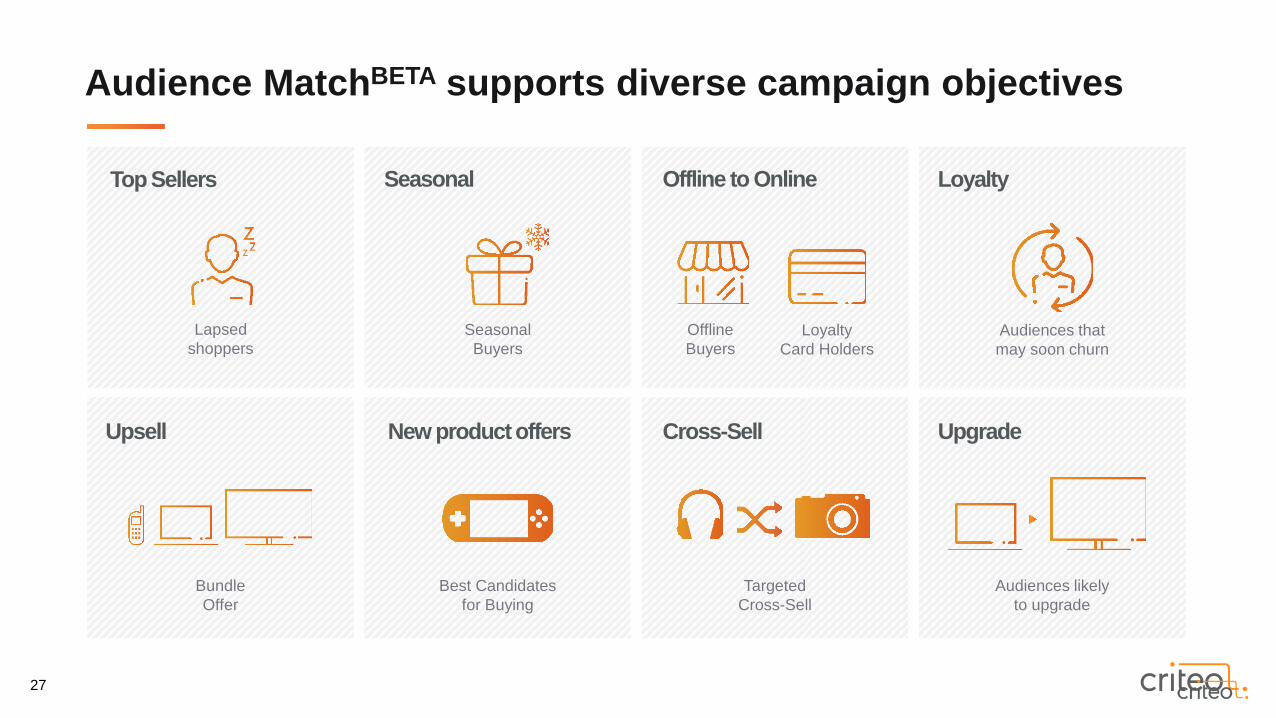

Audience MatchBETA supports diverse campaign objectives

Top Sellers Offline to Online Loyalty

Upsell New product offers Cross-Sell Upgrade

Seasonal

Lapsed shoppers

OfflineBuyers

LoyaltyCard Holders

Audiences that may soon churn

BundleOffer

Best Candidates for Buying

TargetedCross-Sell

Audiences likelyto upgrade

SeasonalBuyers

28

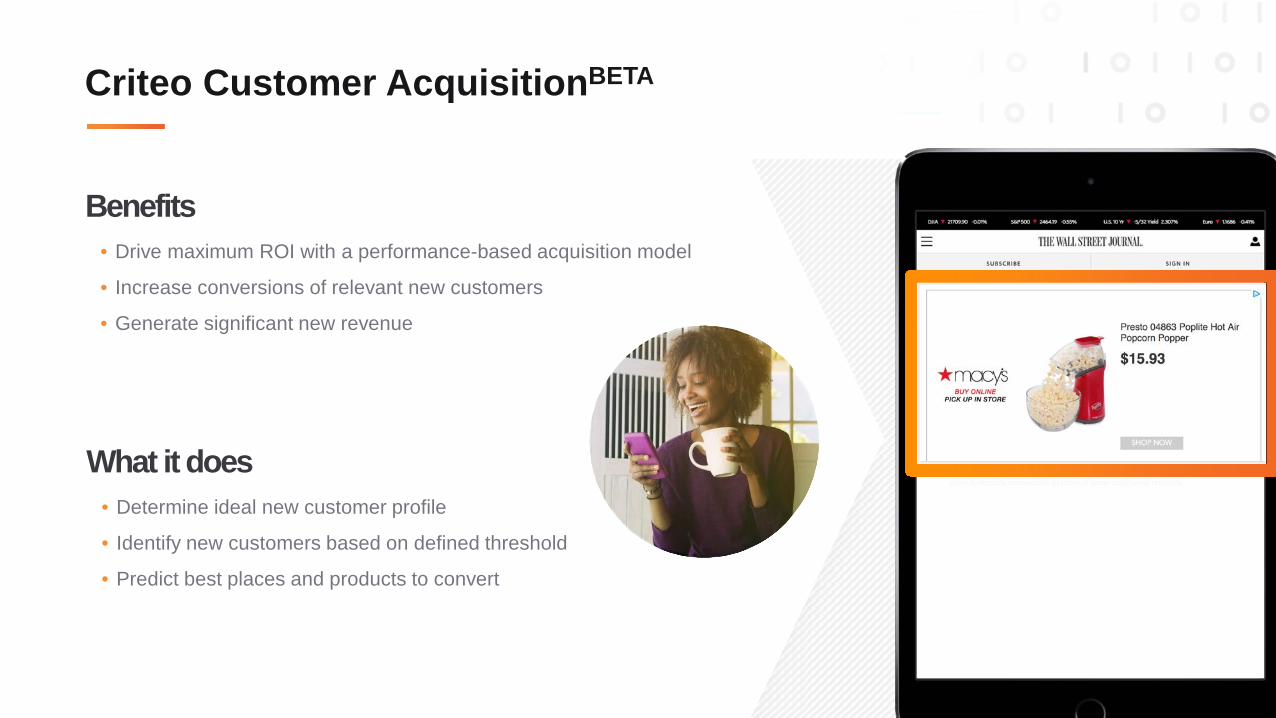

Criteo Customer AcquisitionBETA

What it does• Determine ideal new customer profile

• Identify new customers based on defined threshold

• Predict best places and products to convert

Benefits• Drive maximum ROI with a performance-based acquisition model

• Increase conversions of relevant new customers

• Generate significant new revenue

29

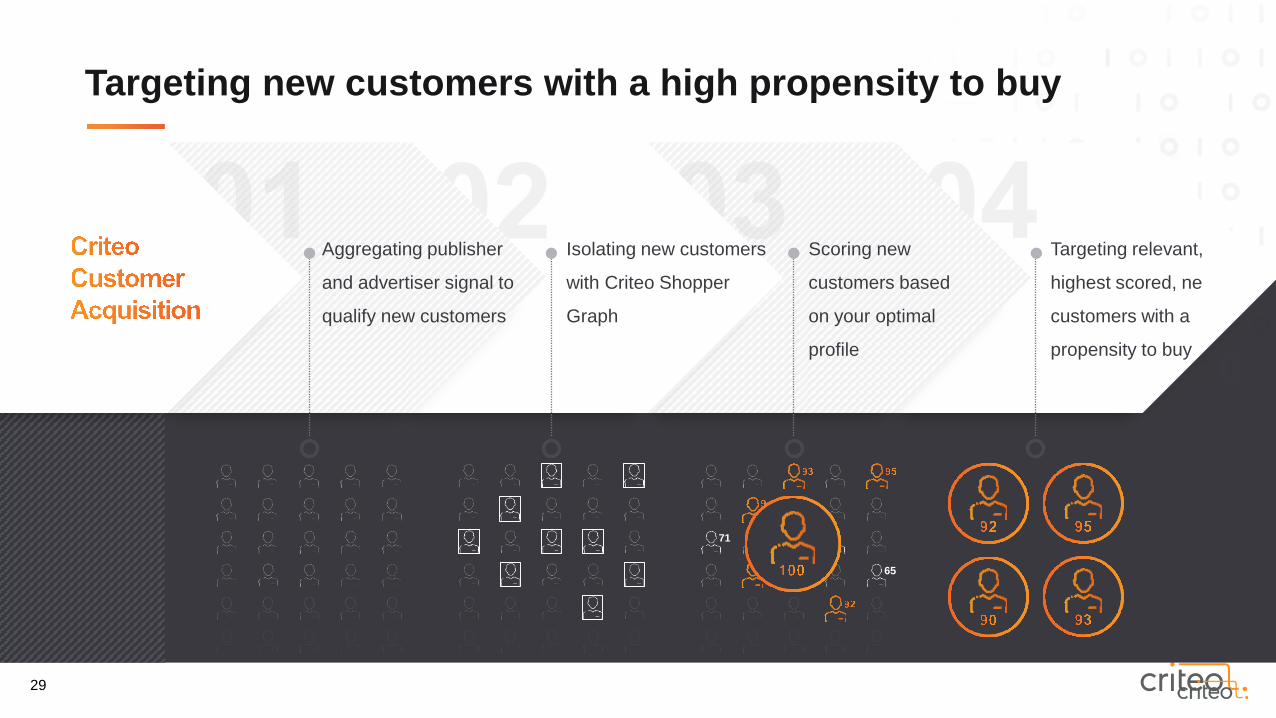

Targeting new customers with a high propensity to buy

Targeting relevant,

highest scored, ne

customers with a

propensity to buy

Scoring new

customers based

on your optimal

profile

Isolating new customers

with Criteo Shopper

Graph

Aggregating publisher

and advertiser signal to

qualify new customers

71

65

30

Creates Product

Recommendation

Personalized creative

Unique user value

predictionClient 2Client 3Client 4Client 5

For each user

Internal advertiser

auctionPublisher/

platform bidCustom ad

serving

Less than 100ms to perform the entire process 37,000 ads served/sec600,000+ RTB bids/sec

Client 1Creates Product

Recommendation

Personalized creative

Unique user value

predictionCreates Product

Recommendation Personalized

creative

Unique user value

predictionCreates Product

Recommendation Personalized

creative

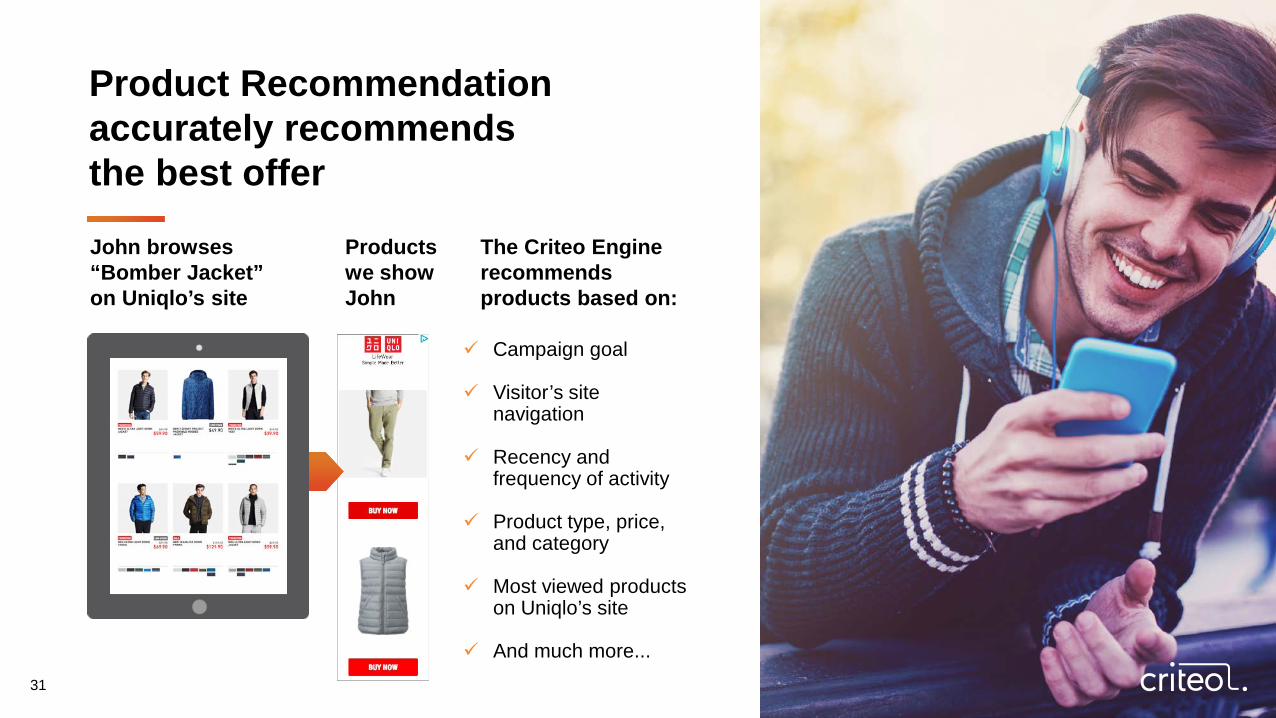

Unique user value

prediction

Our Engine solves highly complex problems in real time

31

Campaign goal

Visitor’s site navigation

Recency and frequency of activity

Product type, price, and category

Most viewed products on Uniqlo’s site

And much more...

The Criteo Enginerecommends products based on:

Productswe showJohn

John browses“Bomber Jacket”on Uniqlo’s site

Product Recommendationaccurately recommendsthe best offer

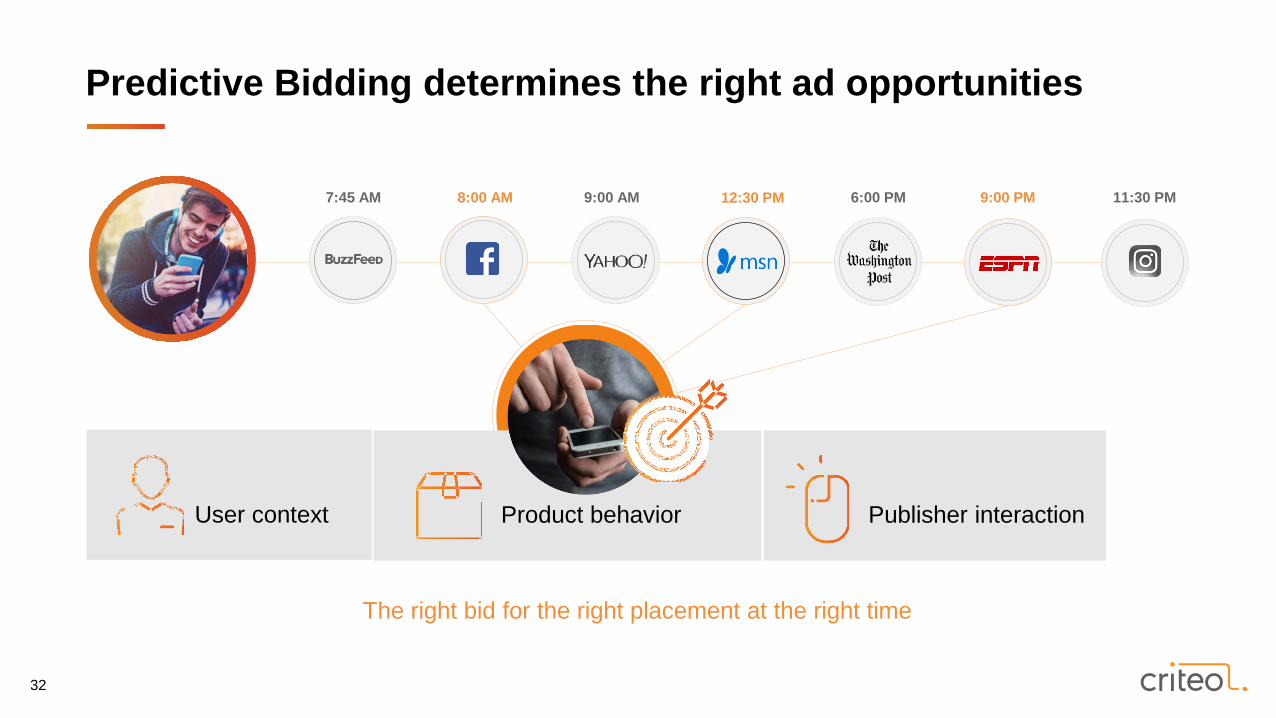

32

7:45 AM 8:00 AM 9:00 AM 12:30 PM 6:00 PM 9:00 PM 11:30 PM

The right bid for the right placement at the right time

User context Publisher interactionProduct behavior

Predictive Bidding determines the right ad opportunities

33

Kinetic Design delivers perfectly branded ads, optimized for every user

34

We are creating the Criteo Shopper Graph

Three trusted data collectives

Carefully designed using our guiding principles

OpenTwo-way exchange of data

TransparentClear and permission-based usage

SecureHighest data security and privacy

FairValue gained exceeds contribution

One of the World’s Largest Data Sets on Shoppers

35

Identity Graph: Matching of cross-device, same device, and online/offline

Already available

Criteo’s advantages• 75%+ of commerce clients participate: 10,000+ partners

• 2B+ IDs and growing

• Global coverage

• Already one of the best identity graphs

• Similar match rates as Google and Facebook

• Bridge between online and offline

36

Interest Map: shopper interest across products

Criteo’s advantages• Access to 4B+ products

• $550B+ of online sales

• 21B+ shopping interactions

• Unified through a Universal Catalog

• Understanding of performance of product attributes

Availability• Building applications and underlying infrastructure

37

Measurement Network: brand conversion and sales across retailers

Criteo’s advantages• SKU-level sales attribution for brands across retailers

• Deterministic measurement, not extrapolated panels

• Nearly 100 retailers participating via Sponsored Products

• Plans to widen to all Criteo retailers with new applications

• Beginning to add offline sales attribution

Already available

38

Business Model

39

All our products are performance based.

We deliver measurable sales and profits for retailer and brand clients.

40

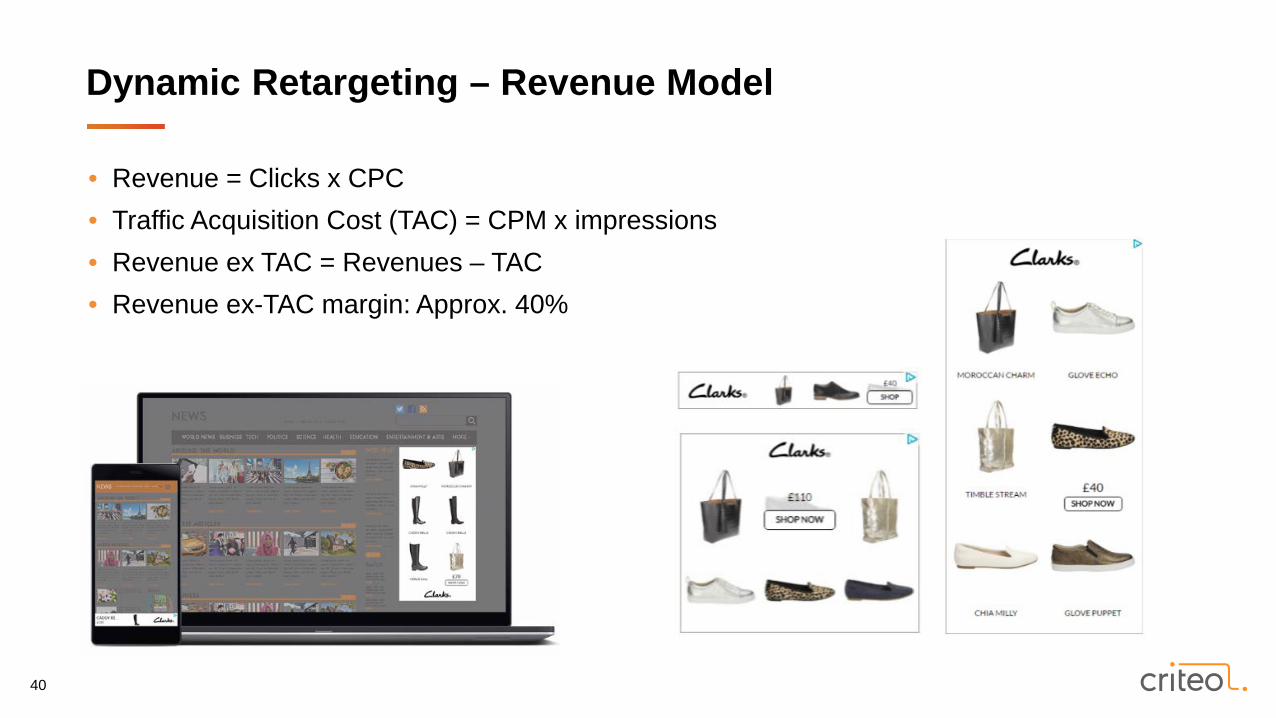

• Revenue = Clicks x CPC• Traffic Acquisition Cost (TAC) = CPM x impressions• Revenue ex TAC = Revenues – TAC• Revenue ex-TAC margin: Approx. 40%

Dynamic Retargeting – Revenue Model

41 CPM = Cost per Thousand impressions, CTR = Click-through rate, CR = Conversion rate, AOV = Average Order Value

Client 4

We take CPC bids from clients

Clients

$0.30 x 0.95% = $2.85

We convert those bids into pCPM (predicted CPM)

CPC x CTR = pCPM(predicted CPM) Publishers

$0.50 x 0.75% = $3.75

$0.40 x 0.61% = $2.44

$0.80 x 0.45% = $3.60

$2.00

Clearing Price (CPM)

Highest bidder

Predicting the right bid for the highest value client

Bid = α × CPC × pCTR × pCR × pAOV

Client 1

Client 2

Client 3We buy

inventory in real time from

publishers

42

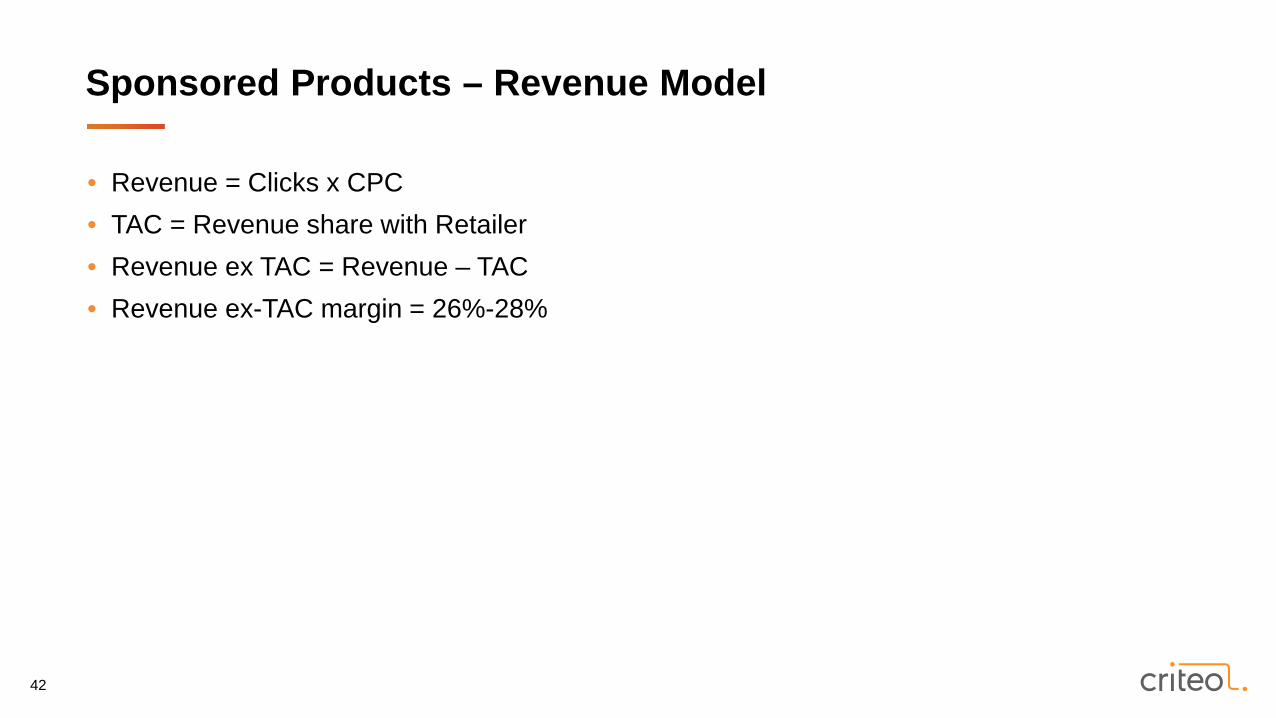

• Revenue = Clicks x CPC • TAC = Revenue share with Retailer • Revenue ex TAC = Revenue – TAC• Revenue ex-TAC margin = 26%-28%

Sponsored Products – Revenue Model

43

Differentiated in Marketing

Attractive Direct

Sticky Elastic Demand

1 On average over the last four quarters through Q3 2017; Criteo Dynamic Retargeting only2 Last twelve months to Q3 2017; Criteo Dynamic Retargeting only3 On average over the last 24 quarters through Q3 2017; Criteo Dynamic Retargeting only4 On average over the last four quarters through Q3 2017. Criteo Dynamic Retargeting only: Represents uncapped budgets of our clients, which are either contractually uncapped or so large that the budget constraint does not restrict ad buys

Our business model hasunique attributes

87%Direct relationships

with clients2

920Net client additions

per quarter1

90%Client retention rate3

78%Of Revenue ex-TAC from

uncapped budgets4

44

Clients

45 * 17,299 clients at the end of Q3 2017

Direct relationships with many premium commerce and brand clients

Commerce | Retail, Travel and Classifieds Brands

46 UV: Unique Visitors

• Field sales & account management

• High value, low volume

• Longer sales cycles

• White glove service

• Local in-market sales teams

• Inside sales & account management

• High volume, lower value

• Shorter sales cycles

• High degree of automation

• Regional hubs and satellite offices

Top-tier comScore sites(typically top-100)

Min. ~40k UV/month

A tiered go-to-market approach

47 Internal Criteo estimates

<25%Midmarket penetration

~60,000 addressable clients worldwide in Retail, Travel and Classifieds (excluding CSP)

50%Tier 1

penetration

A large opportunity to win new clients

48

PublisherInventory

49

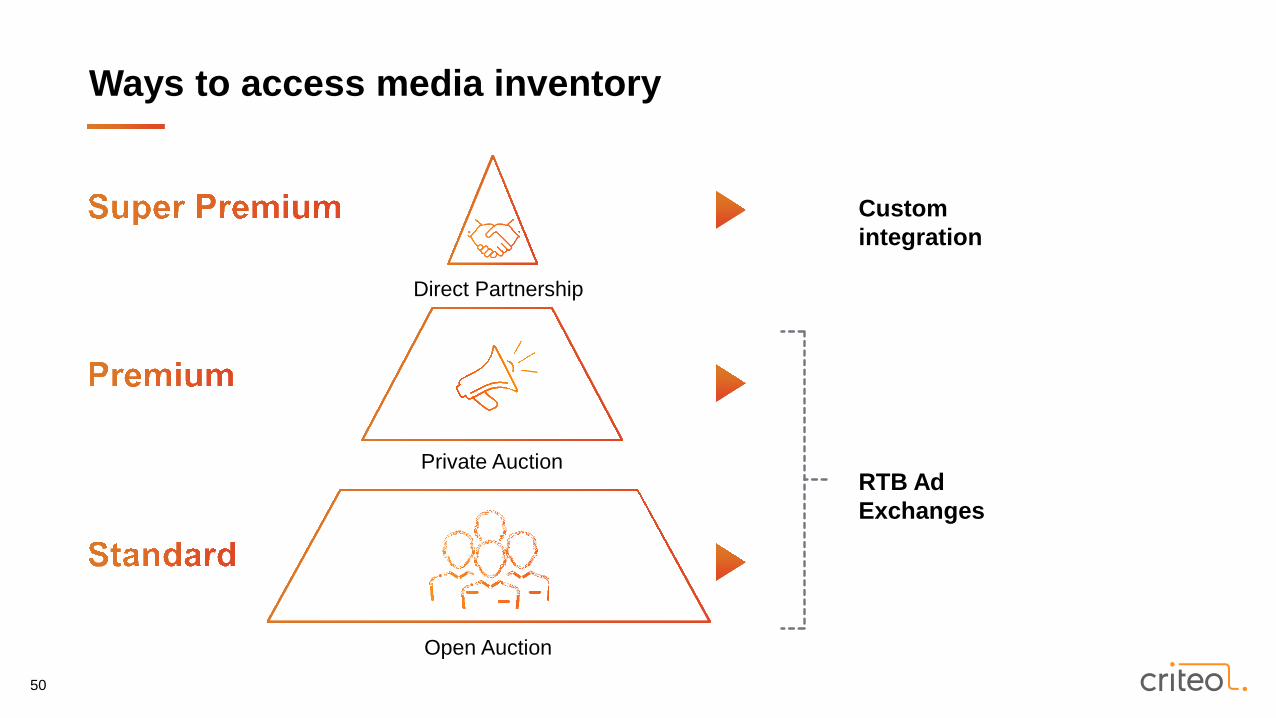

PREFERRED ACCESS TO PREMIUM MEDIA INVENTORY

PREFERRED ACCESS TO RETAILER INVENTORY

ALL MAJOR PUBLIC EXCHANGES, GLOBAL AND LOCAL

Direct partnerships with large high-quality publishers worldwide

50

Direct Partnership

Private Auction

Open Auction

RTB Ad Exchanges

Custom integration

Ways to access media inventory

51

Our two-tiered publisher organization

52

Transition to Mobile Social Native

Multiple Devices Header BiddingAd Blocking

Changing consumer behavior Evolving technology

Programmatic

Our sophisticated technology drives more value for publishers

In App

The publisher environment is constantly evolving

53

Ad blocking is an opportunity for players with:• The right business model

• The right technology stack

• The right expertise in user privacy

• Premium demand

Our Position • Promote acceptable ad programs

• Invest in native

• Support an open tracking standard

• Define standards for retargeting

We have always delivered user-friendly ads

54

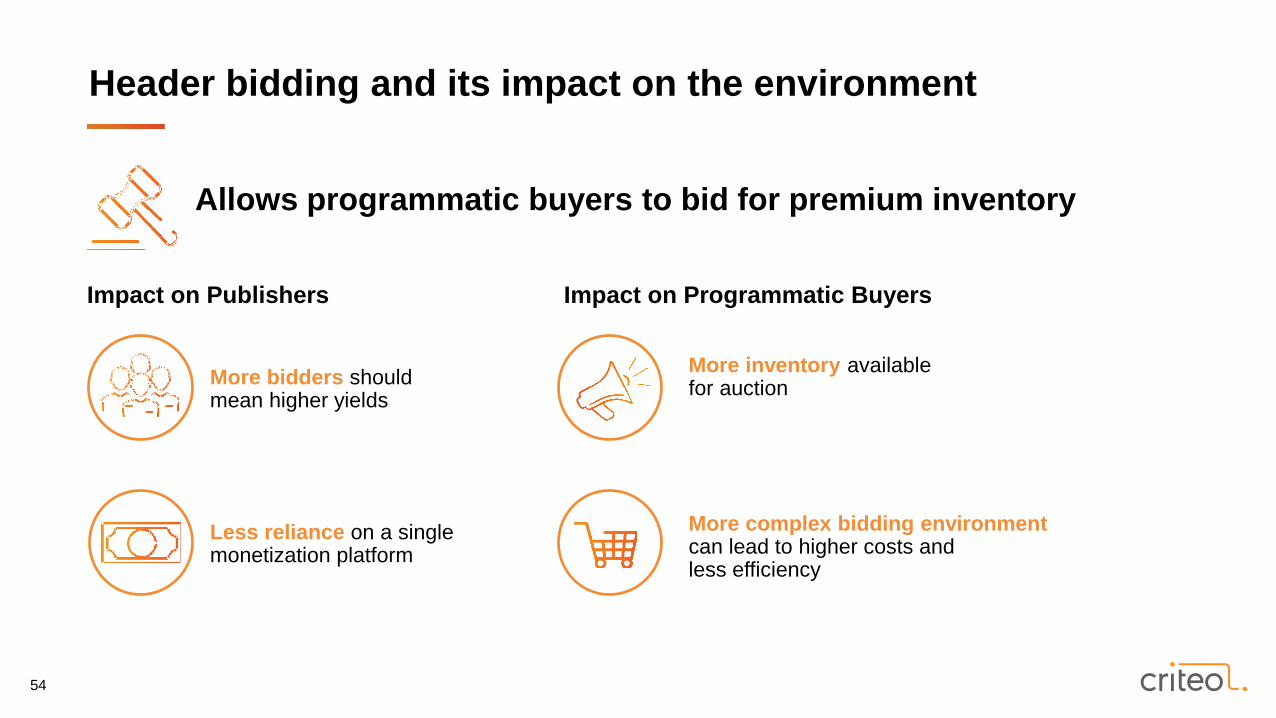

More bidders should mean higher yields

Less reliance on a single monetization platform

Allows programmatic buyers to bid for premium inventory

Impact on Publishers Impact on Programmatic Buyers

More inventory available for auction

More complex bidding environment can lead to higher costs andless efficiency

Header bidding and its impact on the environment

55

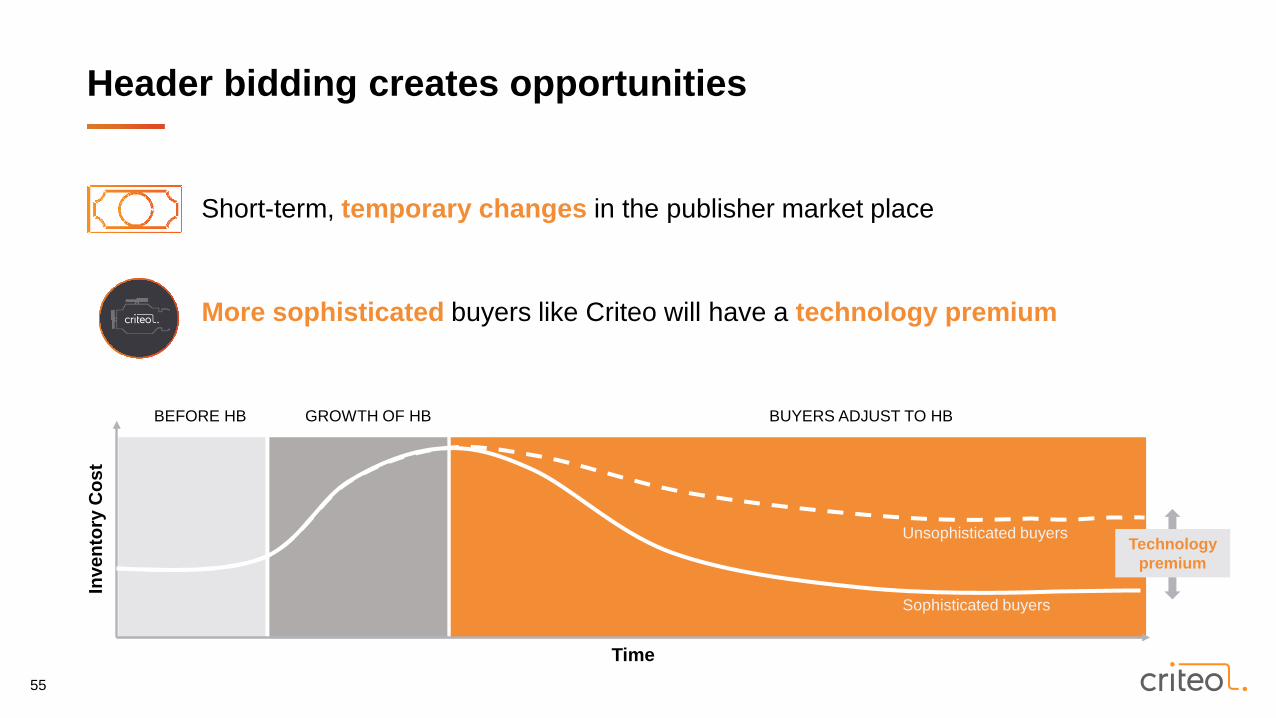

Short-term, temporary changes in the publisher market place

More sophisticated buyers like Criteo will have a technology premium

Time

BEFORE HB GROWTH OF HB

Inve

ntor

y C

ost

BUYERS ADJUST TO HB

Unsophisticated buyers

Sophisticated buyers

Technology premium

Header bidding creates opportunities

56

• Criteo Direct Bidder (CDB) allows Criteo to bid on publisher inventory directly through the ad server

without the need to funnel demand through Supply Side Platforms (SSPs) or exchanges.

• Benefits for the publisher:

• all of the Criteo bid goes to the publisher; none is taken by the SSP for fees (typically 10%-20%)

• user matching between the Publisher and Criteo is much more timely and complete than

matching reliant on a third party

• +20-40% spend with publishers on the same inventory that was previously accessed through RTB

• Launched in Q2, already connected to 950 publishers at the of Q3 2017

Criteo Direct Bidder: A direct path to Criteo’s unique demand

57

Competitive Position

58

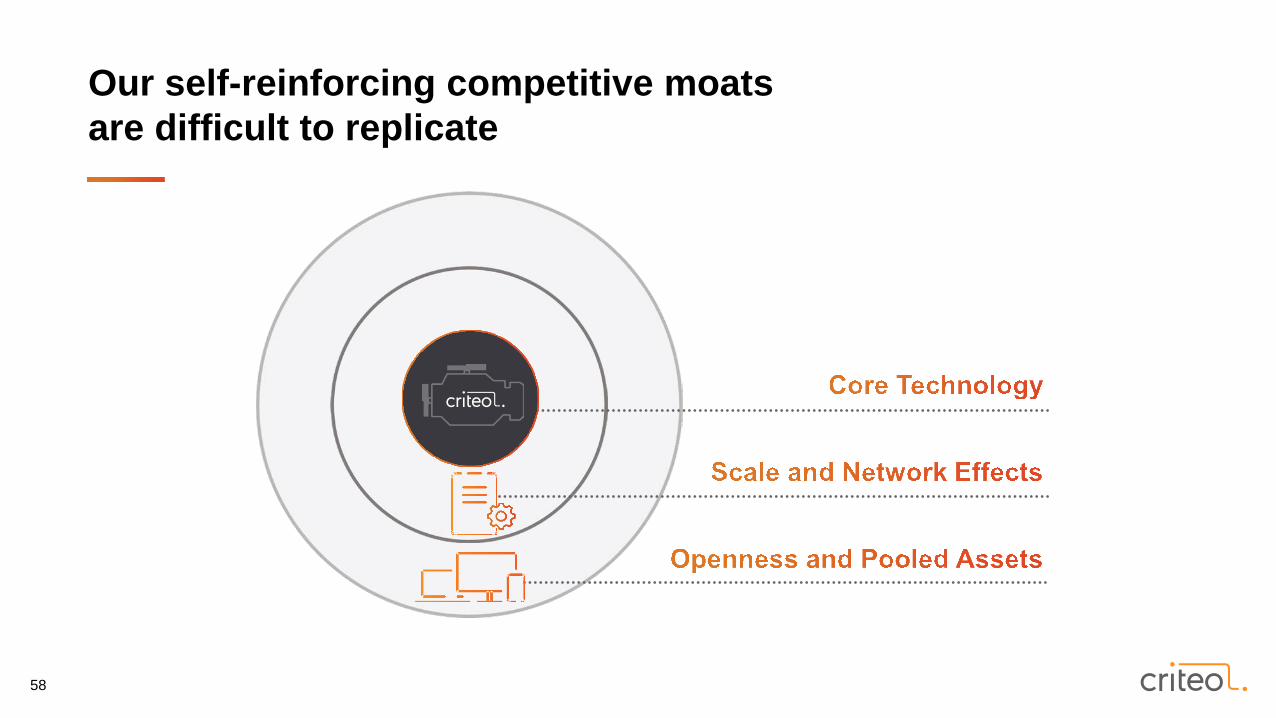

Our self-reinforcing competitive moats are difficult to replicate

59

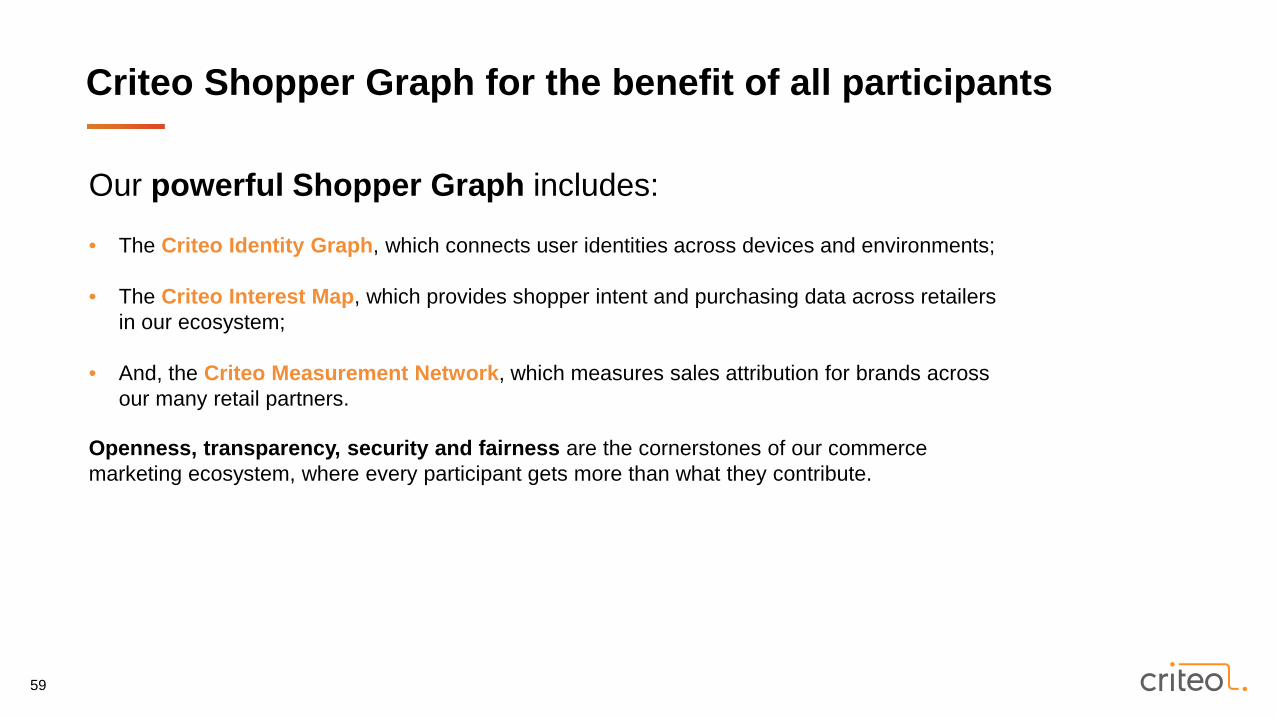

Criteo Shopper Graph for the benefit of all participants

Our powerful Shopper Graph includes:

• The Criteo Identity Graph, which connects user identities across devices and environments;

• The Criteo Interest Map, which provides shopper intent and purchasing data across retailers in our ecosystem;

• And, the Criteo Measurement Network, which measures sales attribution for brands across our many retail partners.

Openness, transparency, security and fairness are the cornerstones of our commerce marketing ecosystem, where every participant gets more than what they contribute.

60

CLOSED

OPEN

WORKFLOW AUTOMATION PREDICTIVE PERFORMANCE

Criteo’s Position in Commerce Marketing

Note: based solely on Criteo’s qualitative assessment

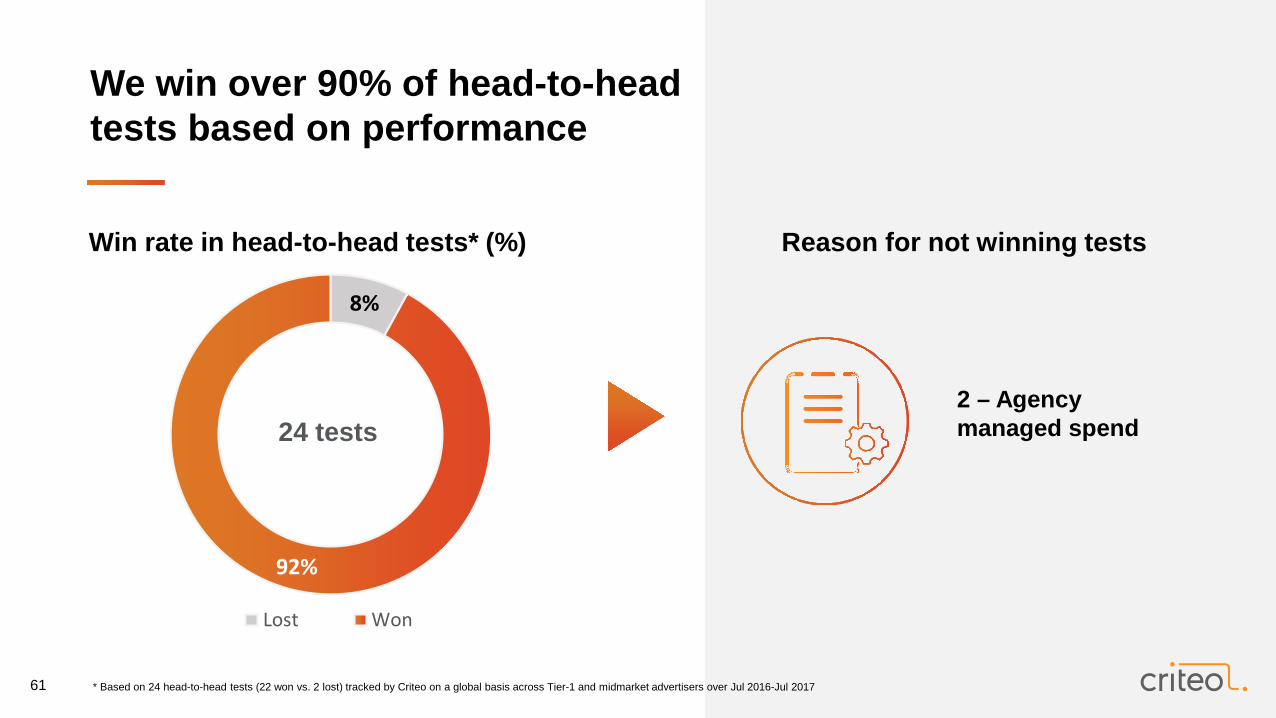

61 * Based on 24 head-to-head tests (22 won vs. 2 lost) tracked by Criteo on a global basis across Tier-1 and midmarket advertisers over Jul 2016-Jul 2017

8%

92%

Lost Won

Win rate in head-to-head tests* (%) Reason for not winning tests

2 – Agency managed spend24 tests

We win over 90% of head-to-head tests based on performance

62

Solid track record of execution

63 * Annual average of quarterly client retention rates, defined as the percentage of live clients during the previous quarter that continued to be live during the current quarter

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q3 11Q4 11Q1 12Q2 12Q3 12Q4 12Q1 13Q2 13Q3 13Q4 13Q1 14Q2 14Q3 14Q4 14Q1 15Q2 15Q3 15Q4 15Q1 16Q2 16Q3 16Q4 16Q1 17Q2 17Q3 17

Clients Retention rate

Client retention rate* (%) Clients Revenue ex-TAC ($ millions)

0

50

100

150

200

250

Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17

World class client retention and fast growth

64

Revenue ex-TAC ($ millions)

0

10

20

30

40

50

60

70

80

90

Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17

Adjusted EBITDA ($ millions)

Strong profitability and high predictability

50

70

90

110

130

150

170

190

210

230

250

Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17

Actuals Guidance

65

Financials

66

147

238

403

534

730

889

FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 LTM Q32017

1 We define Revenue ex-TAC as our revenue excluding traffic acquisition costs, or TAC, generated over the applicable measurement period. Revenue ex-TAC is not a measure calculated in accordance with U.S. GAAP. Please see the Appendices for a reconciliation of Revenue ex-TAC to Revenue, the most directly comparable GAAP measure. 2 We define Adjusted EBITDA as our consolidated earnings before financial income (expense), income taxes, depreciation and amortization, adjusted to eliminate the impact of equity awards compensation expense, pension service costs, acquisition-related costs and deferred price consideration. Adjusted EBITDA is not a measure calculated in accordance with U.S. GAAP. Please see the Appendices for a reconciliation of Adjusted EBITDA to net income, the most directly comparable GAAP measure.

Revenue ex-TAC1 ($M) Adjusted EBITDA2 ($M)

+43%CAGRHigh

growthExpandingprofitability

2242

105

143

225

273

FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 LTM Q32017

Solid financial track record since IPO

67

REVENUE EX-TAC ($M) ADJUSTED EBITDA ($M) FREE CASH FLOW ($M)

+31%* +34%* +206%

* At constant currency

Rapid, profitable growth and strong cash flow

142

190

9M 2016 9M 2017

27

83

9M 2016 9M 2017

505

664

9M 2016 9M 2017

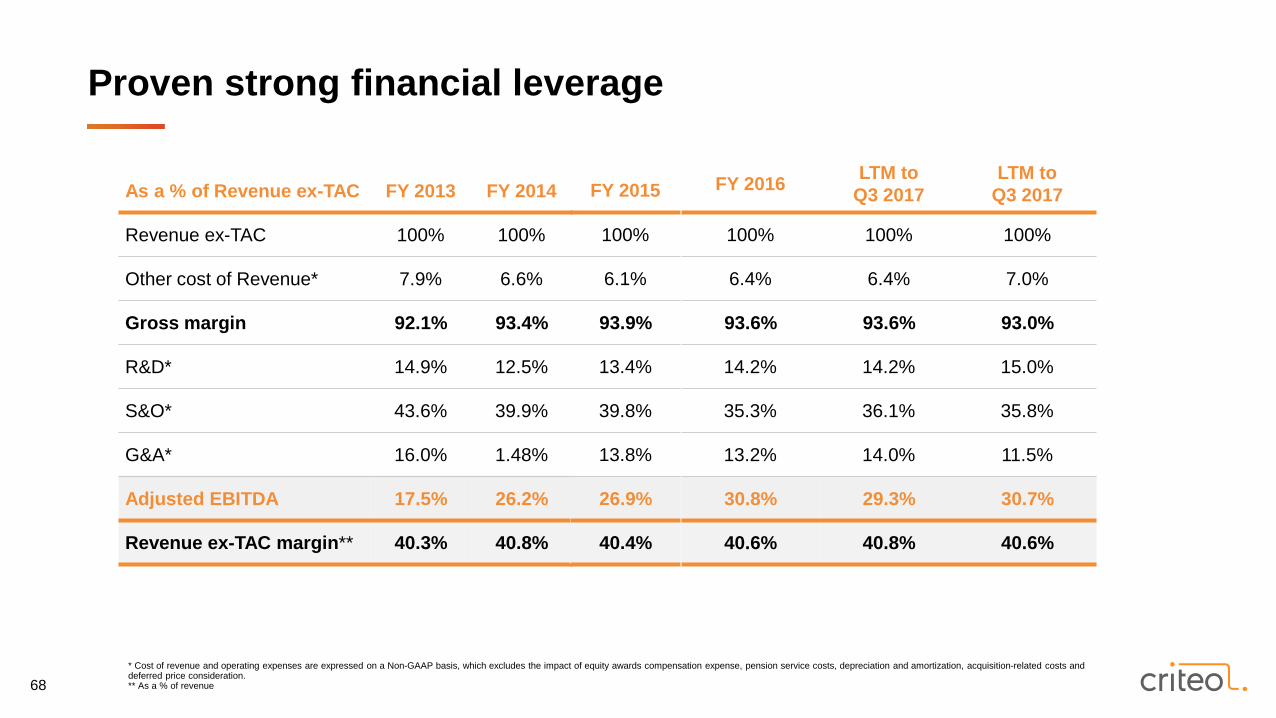

68* Cost of revenue and operating expenses are expressed on a Non-GAAP basis, which excludes the impact of equity awards compensation expense, pension service costs, depreciation and amortization, acquisition-related costs and deferred price consideration. ** As a % of revenue

Proven strong financial leverage

As a % of Revenue ex-TAC FY 2013 FY 2014

Revenue ex-TAC 100% 100%

Other cost of Revenue* 7.9% 6.6%

Gross margin 92.1% 93.4%

R&D* 14.9% 12.5%

S&O* 43.6% 39.9%

G&A* 16.0% 1.48%

Adjusted EBITDA 17.5% 26.2%

Revenue ex-TAC margin** 40.3% 40.8%

FY 2015

100%

6.1%

93.9%

13.4%

39.8%

13.8%

26.9%

40.4%

FY 2016 LTM to Q3 2017

LTM to Q3 2017

100% 100% 100%

6.4% 6.4% 7.0%

93.6% 93.6% 93.0%

14.2% 14.2% 15.0%

35.3% 36.1% 35.8%

13.2% 14.0% 11.5%

30.8% 29.3% 30.7%

40.6% 40.8% 40.6%

69

Technology innovation

Broadersupply

Upselling incremental products and channels

Operating excellence and productivity

spending budgets at limited incremental costs

Powered by a combination of

Strong drivers for further operating leverage

70

SMARTINVESTING

Robust operating cash flow enables smart investment

71* Based on a $3B+ market capitalization, pursuant to the 2017 AGM authorization to issue up to 15,6m shares** Only for M&A

Strong balance sheet

1,211

1,358

Dec. 2016 Sep. 2017

Total assets (in $M) Financial liabilities(in $M)

Very low debt

Dec. 2016 Sep. 2017

868

Cash & cashequivalents (in $M)

Significantcash pile

270

358

Dec. 2016 Sep. 2017

>20% of assets

$358Mcash

As of September 30, 2017

€350M committed financing

$750M equity raise capacity*

Share buy-back authorization**

Our financial structure offers significant flexibility

72

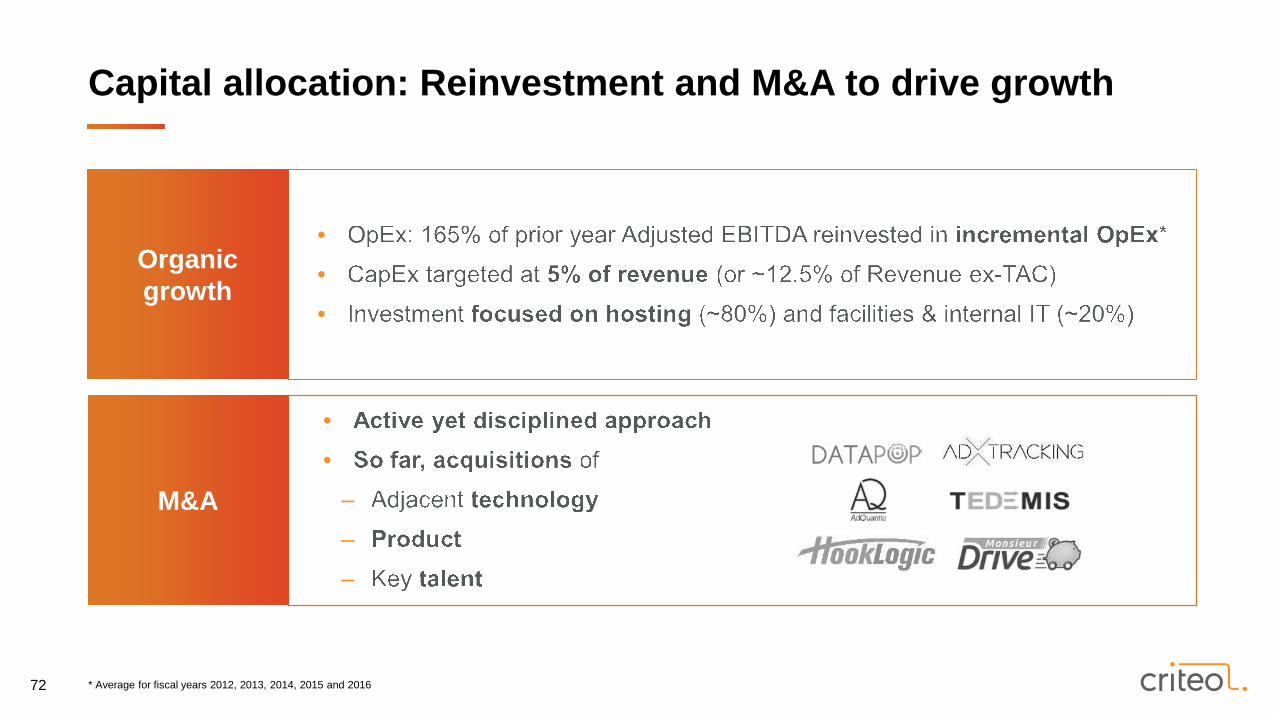

••

–––

•••

Organicgrowth

M&A

Capital allocation: Reinvestment and M&A to drive growth

* Average for fiscal years 2012, 2013, 2014, 2015 and 2016

73

Growth Strategy

74

Growth strategy based on two strong pillars

, expand our partner base

Increase our

• Expand worldwide

• Grow clients worldwide

• Scale and drive international expansion of

• Enhance

• Leverage our powerful

• Upsell across the shopper journey

• Broaden across mediaand retailers

75

Technology Innovation

New Supply

Revenue ex-TAC uplift (%)

Conversion Optimization+20% uplift

Dynamic Creative Optimization+10% uplift

+8% upliftRevenue Optimization

+6% upliftRTB integration improvement

+36% uplift in Japan

+5% uplift Worldwide

+10% upliftNative+3% uplift

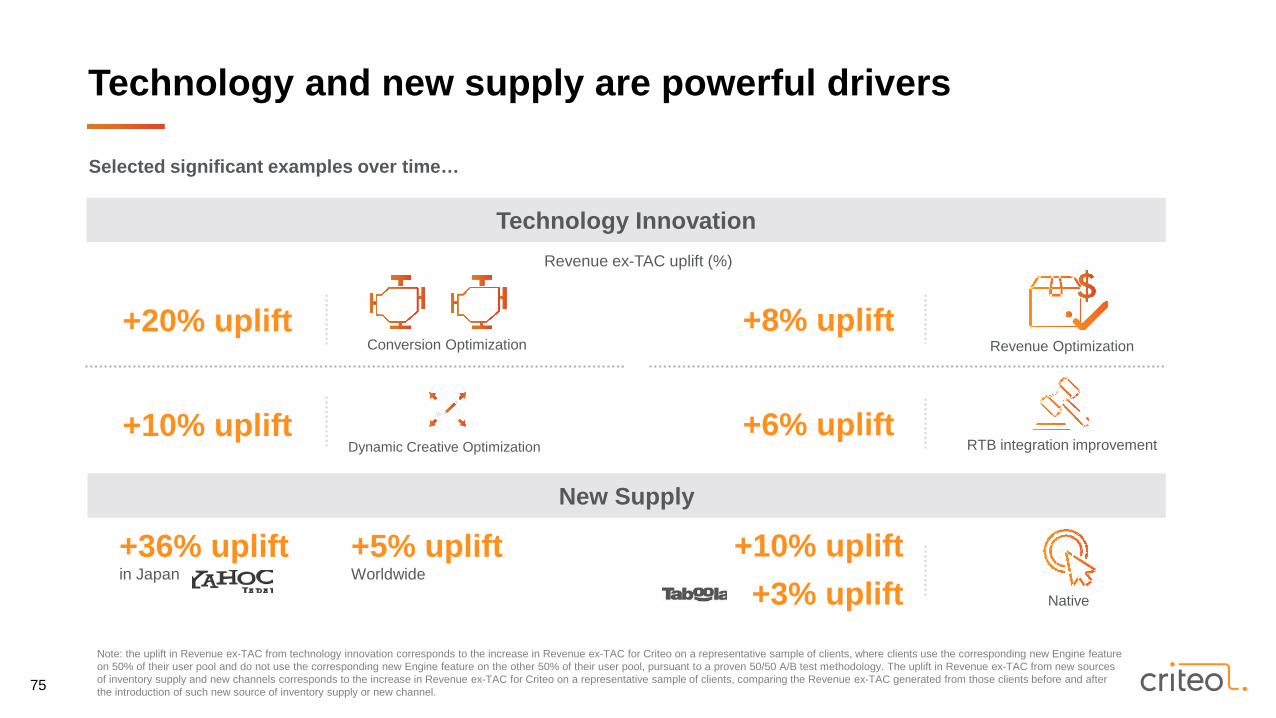

Selected significant examples over time…

Note: the uplift in Revenue ex-TAC from technology innovation corresponds to the increase in Revenue ex-TAC for Criteo on a representative sample of clients, where clients use the corresponding new Engine feature on 50% of their user pool and do not use the corresponding new Engine feature on the other 50% of their user pool, pursuant to a proven 50/50 A/B test methodology. The uplift in Revenue ex-TAC from new sources of inventory supply and new channels corresponds to the increase in Revenue ex-TAC for Criteo on a representative sample of clients, comparing the Revenue ex-TAC generated from those clients before and after the introduction of such new source of inventory supply or new channel.

Technology and new supply are powerful drivers

76

Solutions to Engage Across the Shopper Journey

77

We Are Working to Cover the Full Shopper Journey for Retailers and Brands

1. Feature of Criteo Dynamic Retargeting

Acquire Convert Re-engage, Cross-sell Upsell

ONLINE

OMNICHANNEL

• Criteo Customer Acquisition BETA • Criteo Dynamic Retargeting • Criteo Audience MatchBETA

• Criteo Sponsored Products OffsiteBETA

• Criteo Sponsored Products • Criteo Sponsored Products OffsiteBETA

• Criteo Dynamic Retargeting Store-to-web Retargeting1BETA

• Criteo Audience MatchBETA

78

Investment SummaryLarge market opportunityCommerce Marketing is quickly emerging as the next big digital marketing category after Search and Social

Clear strategyBuild the highest performing and open commerce marketing ecosystem

Strong competitive moatsTechnology, scale and network effects, openness and shopper graph

Proven track-recordStrong client growth while maintaining 90% retention*

Exceeded expectations for 16 consecutive quarter

Attractive financial profileStrong growth, increasing profitability and cash flow

* Dynamic Retargeting

79

IR Contacts

Edouard LassalleVP, Head of Investor Relations32, rue Blanche75009 Paris+33 1 7621 [email protected]

Friederike EdelmannDirector, Investor Relations387 Park Ave South, 12th FloorNew York, NY 10016+1 917 837 8617 [email protected]

ir.criteo.com

80

Appendices

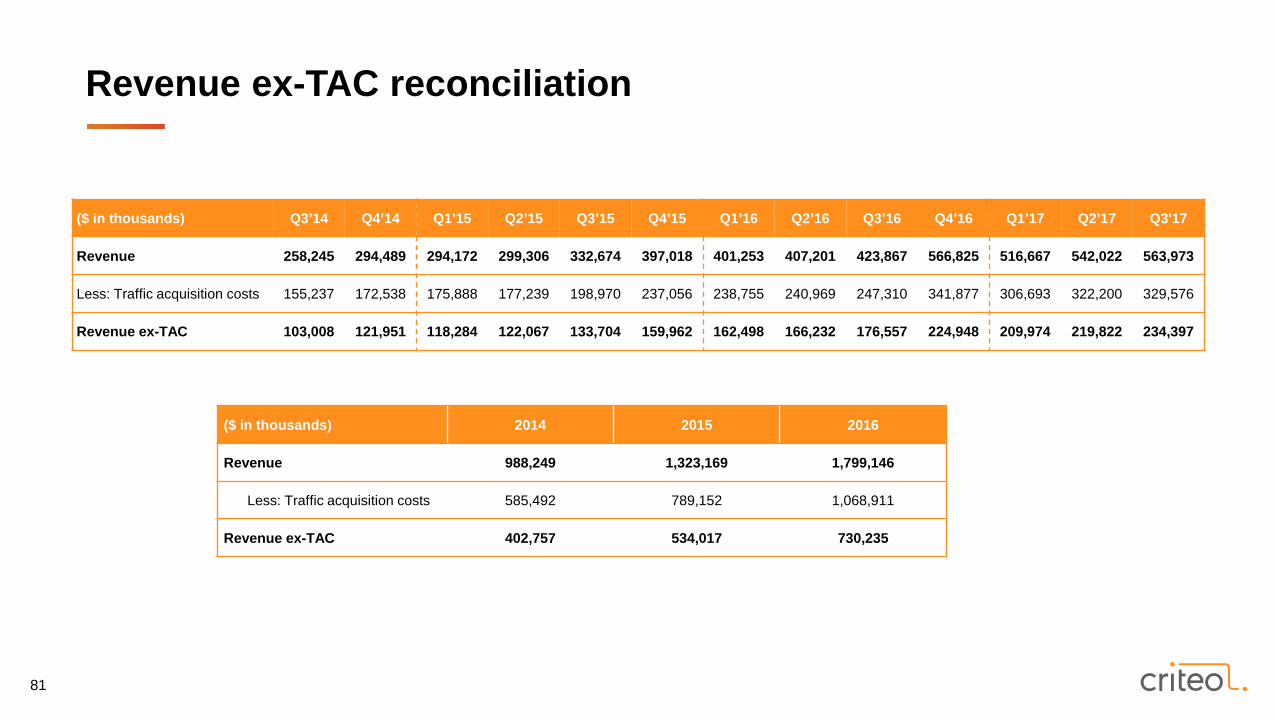

81

($ in thousands) 2014 2015 2016

Revenue 988,249 1,323,169 1,799,146

Less: Traffic acquisition costs 585,492 789,152 1,068,911

Revenue ex-TAC 402,757 534,017 730,235

Revenue ex-TAC reconciliation

($ in thousands) Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16 Q3’16 Q4’16 Q1’17 Q2’17 Q3'17

Revenue 258,245 294,489 294,172 299,306 332,674 397,018 401,253 407,201 423,867 566,825 516,667 542,022 563,973

Less: Traffic acquisition costs 155,237 172,538 175,888 177,239 198,970 237,056 238,755 240,969 247,310 341,877 306,693 322,200 329,576

Revenue ex-TAC 103,008 121,951 118,284 122,067 133,704 159,962 162,498 166,232 176,557 224,948 209,974 219,822 234,397

82

Adjusted EBITDA reconciliation

($ in thousands) Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16 Q3’16 Q4’16 Q1’17 Q2’17 Q3'17 2014 2015 2016

Net income 15,439 22,893 13,617 3,929 5,793 38,938 18,527 13,339 14,724 40,740 14,518 7,505 22,269 46,896 62,276 87,329

Adjustments:

Financial (income) expense (7,502) (1,473) (3,920) 2,546 6,650 (735) 1,317 94 570 (1,435) 2,333 2,094 2,886 (11,390) 4,541 546

Provision for income taxes 4,205 4,118 7,143 1,365 5,388 (4,378) 7,944 4,450 7,574 13,161 4,201 3,665 7,858 17,578 9,517 33,129

Equity awards compensation expense

5,754 6,142 6,317 5,325 4,600 7,748 8,370 7,695 13,965 13,229 14,940 14,918 22,028 19,601 23,989 43,259

Pension service costs 125 129 112 110 110 109 129 131 132 133 290 299 320 504 441 524

Depreciation and amortization expense 8,256 9,001 8,428 10,278 11,892 13,967 12,516 13,300 14,771 16,190 20,167 22,306 23,755 31,213 44,565 56,779

Acquisition-related costs - - - - - - - 148 1,793 980 6 - - - - 2,921

Acquisition-related deferred price consideration 128 110 109 115 54 (2,172) 40 44 3 (3) - - - 950 (1,894) 85

Restructuring - - - - - - - - - - - 3,299 - - - -

Total net adjustments 10,966 18,027 18,189 19,739 28,694 14,539 30,316 25,862 38,808 42,255 41,936 46,581 56,847 58,456 81,159 137,243

Adjusted EBITDA 26,405 40,920 31,806 23,668 34,487 53,477 48,843 39,201 53,532 82,995 56,454 54,086 79,116 105,352 143,435 224,572

83

($ in thousands) Q3 2016 Q3 2017

CASH FROM OPERATING ACTIVITIES 43,631 61,727

Acquisition of intangible assets, property, plant and equipment (15,792) (20,999)

Change in accounts payable related to intangible assets, property, plant and equipment (4,115) (6,774)

FREE CASH FLOW 23,724 33,954

Free Cash Flow reconciliation