Criminal Insider Trading: Prosecution, Legislation, and

21

Stanford University From the SelectedWorks of Steven Brody Fall October 25, 2009 Criminal Insider Trading: Prosecution, Legislation, and Justification Steven Brody Available at: hps://works.bepress.com/steven_brody/1/

Transcript of Criminal Insider Trading: Prosecution, Legislation, and

Stanford University

From the SelectedWorks of Steven Brody

Fall October 25, 2009

Criminal Insider Trading: Prosecution,Legislation, and JustificationSteven Brody

Available at: https://works.bepress.com/steven_brody/1/

Criminal Insider Trading:

Prosecution, Legislation, and Justification

Steve Brody Stanford Law School [email protected]

2

Table of Contents

I. Introduction........................................................................................................................ 3

II. The Early Years of Insider Trading (1934-1987)............................................................. 3

III. Ivan Boesky and the Modern Era of Insider Trading Legislation................................... 6

IV. 1987 to Present................................................................................................................ 9

V. Insider Trading Legislation and the “Ratchet” Effect .................................................... 11

VI. Prosecutorial Discretion: Plea Bargaining and Gains ................................................... 13

A. Gains Calculation........................................................................................................ 14

VII. Do Criminal Sanctions Work?..................................................................................... 18

VIII. Conclusion.................................................................................................................. 20

3

I. Introduction

Since the passage of the Securities Exchange Act of 1934, insider trading has been

codified as a federal crime. For many years, however, civil cases were rare, and criminal

prosecutions resulting in prison terms were nearly unheard of. Yet during the 1980’s, white

collar crime—and insider trading in particular—became the subject of more public scrutiny

than it had ever previously received. During this period, major developments occurred in the

criminalization, prosecution, and sentencing of those who had committed securities fraud. High

profile cases of inside traders like Ivan Boesky and Dennis Levine made targets of federal

prosecutions household names and the faces of a new generation of robber barons. Boesky’s

highly-publicized prosecution and subsequent plea bargain resulting in a three and a half year

prison sentence and a $100M fine1, was a watershed in an area of criminal law that had rarely

seen offenders incarcerated. In the years since, securities fraud and other forms of white collar

crime have been the focus of increasingly vigorous criminal prosecution and draconian

legislation—often in the absence of compelling evidence that such prosecutions serve their

stated deterrent purpose. This paper attempts to plot the course of these developments and the

driving forces behind them. It also considers the process itself, including prosecutorial

discretion and sentencing, and the dubious logic of deterrence through criminal sanctions.

II. The Early Years of Insider Trading (1934-1987)

Insider trading was first addressed by statute with the passage of the Securities

Exchange Act of 1934. On the heels of the “Great Crash” of 1929, and in response to public

1 Going After The Crooks, TIME, Dec. 1, 1986, available at http://www.time.com/time/magazine/article/0,9171,962963,00.html.

4

pressure, Congress launched investigations into the cause of the collapse and the subsequent

global depression. Concluding that the cause was largely widespread purchase of inflated

securities by insolvent investors using margin accounts, congress created the Securities and

Exchange Commission and passed the 1934 Act.2 Liability for insider trading was specifically

enshrined in the Act, though many insider trading prosecutions include charges of wire fraud,

tax fraud, perjury, and obstruction of justice.3 Criminal liability for a violation of the act at the

time of its passage was limited to a fine of not more than $100,000 and incarceration for not

more than 5 years.4

Though the 1934 SEA was meant to address the government’s conclusion that the crash

had been precipitated in part by the “manipulative operations by corporate ‘insiders,’” insider

trading was rarely prosecuted in the commission’s early years.5 In fact, the SEC’s first annual

report for 1935 made no mention of insider trading. Not until the SEC’s 25th annual report in

1959, did the organization start to focus on “curb[ing] the misuse of ‘inside’ information,”

having found that “[a]mong the practices revealed by the Commission's investigation, were the

purchase and sale of portfolio securities by and between the company, its management officials

and other affiliated interests, for the personal profit of the insiders.”6 The annual report also

emphasized the SEC’s commitment to assist in and encourage the criminal prosecution of

insider trading by the Justice Department7, stating:

2 1935 Annual Report of the Securities Exchange Commission, available at http://www.sec.gov/about/annrep.shtml 3 Ralph S. Janvey, SEC Investigation of Insider Trading, SECURITIES REGULATION LAW JOURNAL, Vol. 13, No. 4, Winter 2004. 4 15 U.S.C. § 78ff(a)(1934) 5 1935 Annual Report of the Securities Exchange Commission, available at http://www.sec.gov/about/annrep.shtml 6 1959 Annual Report of the Securities Exchange Commission, available at http://www.sec.gov/about/annrep.shtml 7 The SEC is not itself able to bring criminal actions; rather it provides its findings to the Attorney General’s office with a recommendation to file charges.

5

The Commission believes that only criminal prosecution will effectively stop those who show such a contemptuous disregard for the law. The Commission has, therefore, placed increased emphasis in its work upon the prosecution of such offenders. In fiscal 1959 the Commission referred to the Department of Justice 45 cases for criminal prosecution, one of the highest number of referrals in the Commission’s history, and referrals are continuing at approximately the same rate in fiscal 1960 . . . The Commission believes [] that its policy of pressing for criminal prosecution of violators of the Federal securities laws is the most effective deterrent to fraud in the sale of securities and must be vigorously pursued.8

Nevertheless, in the forty years between 1944 and 1984, the SEC brought just 129 civil

insider trading actions, a mere fraction of which were accompanied by criminal prosecutions.9

The Supreme Court’s holdings in United States v. Chiarella10 and Dirks v. SEC11, both of

which affirmed the requirement of a fiduciary duty for liability, made that much harder the

prosecution of a crime already difficult to detect and prove. Moreover, even where the SEC

was successful in civil actions, relief was limited to disgorgement and injunction against future

trading.12 Federal judges expressed their frustration with this remedy; one wrote: "Mere

disgorgement [] is not much of a deterrent. An insider can trade on nonpublic information

secure in the knowledge that if he is caught he need only restore his illicitly acquired

proceeds."13 Indeed, not only were the sanctions limited, the attitude of corporate executives to

insider trading was positively blasé. A 1961 study of 1700 corporate executives found that they

did not regard trading on the basis of inside information immoral—with fully 42% saying they

8 Id. 9 1984 Annual Report of the Securities Exchange Commission, available at http://www.sec.gov/about/annrep.shtml 10 445 U.S. 222 (1980). 11 463 U.S. 646 (1983). 12 Donald C. Langevoort, INSIDER TRADING REGULATION, ENFORCEMENT AND PREVENTION § 8:1 (2009) 13 S.E.C. v. Randolph, 564 F. Supp. 137 (N.D. Cal. 1983).

6

would use inside information to purchase and profit on securities, and 61% saying they would

expect their colleagues to do the same.14

In an attempt to remedy the lack of effective deterrent, and at the behest of the SEC, in

1984 Congress passed the Insider Trading Sanctions Act (ITSA) which authorized the SEC to

seek a fine of treble gains (in addition to disgorgement), and increased the maximum criminal

fine from $10,000 to $100,000.15 Following the passage of ITSA , the number of civil insider

trading actions brought by the SEC jumped from 13 in 1984, to 20 in 1985.16 Similarly, the

period from 1984 to 1987 saw a substantial rise in the number of criminal prosecutions. The

Southern District of New York (responsible for the vast majority of criminal insider trading

actions17) had prosecuted a total of twelve criminal cases before 1984; by 1987, it had handled

another thirty-eight.18

III. Ivan Boesky and the Modern Era of Insider Trading Legislation

In 1986, a previously little-known arbitrageur, Ivan Boesky was charged by the SEC

and the Justice Department with amassing approximately $200M using inside information to

make massive stock purchases mere days in advance of takeover announcements by some of

the country’s largest corporations. TIME magazine called the scandal, which ultimately

implicated many of new York’s top traders, “Wall Street’s Watergate,” referring to Boesky’s

14 Laurence A. Steckman, Risk Arbitrage and Insider Trading: A Functional Analysis of the Fiduciary Concept Under Rule 10b-5, 5 TOURO L. REV. 121 at fn 97. 15 See 1984 amendment to 15 U.S.C.A. § 78ff. 16 1985 Annual Report of the Securities Exchange Commission, available at http://www.sec.gov/about/annrep.shtml. 17 Harvey L. Pitt et al, Insider Trading and SEC Enforcement: Litigating and Settling SEC Insider Trading Enforcement Cases, 358 Practicing Law Institute 43, 154 (1988). 18 Face the Nation (CBS News television broadcast Feb. 22, 1987).

7

crime of “ripping off millions of dollars by trading on knowledge not available to the general

public . . . [by] taking unfair advantage of price movements in a broad range of stocks.”19

The scandal sparked a vigorous prosecution led by then Attorney General Giuliani.

Boesky eventually plead guilty and was sentenced a three-year prison term (in addition to a

civil penalty of $50M and disgorgement of another $50M—the result of a separate action by

the SEC). In 1986, some fifty years after the passage of the Securities Exchange Act of 1934,

insider trading was still subject to a theoretical maximum sentence of five years in prison, but

in practice, Boesky’s three year term was uniquely harsh.20 The prison sentence—the third

longest insider trading sentence ever imposed—sent shockwaves of fear through the financial

world when it was handed down.21 The government lauded the sentence as a major step

forward in its campaign of deterrence through criminal sanctions. The New York Times

reported, “The United States Attorney, Rudolph W. Giuliani, . . . called the three-year prison

term ‘a heavy sentence,'' emphasizing its importance to deterring white-collar crime. He said it

was ''well deserved and very well balanced.’”22

A a new era in the prosecution of inside traders followed. On the heels of the October

19, 1987 “Black Monday” crash—the single largest one-day loss in the history of trading on

Wall Street—politicians came under tremendous pressure to rectify what were widely

perceived by the public as major failures in market regulation. Senate debates on congressional

financial reform were peppered with references to “nothing short of a white collar crime wave

with respect to insider trading” and panic over even legal practices common in the market:

19 Going After The Crooks, TIME, Dec. 1, 1986, available at http://www.time.com/time/magazine/article/0,9171,962963,00.html. 20 15 U.S.C. § 78ff(a) (1987) 21 Id., but note that the plea was not to insider trading, but rather to wire fraud. 22 TIME Magazine, supra note 19

8

“Even where white collar crime is absent, we suffer economic crime. Raiders devastate healthy

companies, larding once trim firms with huge debt burdens.”23

The Federal Sentencing Guidelines, promulgated the same year as the crash, were

another step forward in the campaign of criminal prosecution of white collar crime—and

insider trading in particular—which would continue for the next forty years. The Guidelines

expressly classified insider trading as a “serious” offense because “[u]nder present sentencing

practice, courts sentence to probation an inappropriately high percentage of offenders guilty of

certain economic crimes, such as . . . insider trading.”24 Prior to the Guidelines, some 59% of

fraud defendants received nothing more than probation, and the average prison time served was

seven months.25 The new Guidelines called for a term of from thirty-seven to forty-six months

for insider trading resulting in gains exceeding a comparatively modest $5M.26

Though lenient by today’s standards, the authors of the Guidelines plainly regarded

inside traders as deserving of more stringent punishment than other forms of white and blue

collar theft, including larceny and embezzlement. In particular, larceny, embezzlement, and

other forms of theft had base offense levels of four, whereas as insider trading had a base

offense level of eight.27 Thus, for gains exceeding $5M, conviction in 1987 of insider trading

could result in a prison term nearly double that for a conviction of embezzling the same

amount.28

23 134 CONG. REC. S17278-02, available at 1988 WL 178496 24 U.S. SENTENCING GUIDELINES MANUAL § 5A (1988) 25Stephanos Bibas, White Collar Plea Bargaining and Sentencing After Booker, 47 WM. AND MARY L. REV. 721, 723 (2005) 26 U.S. SENTENCING GUIDELINES MANUAL § 5A (1988) 27 U.S. SENTENCING GUIDELINES MANUAL §§ 2B1.1, 2F1.2 (1987) 28 Id.

9

IV. 1987 to Present

Yet in spite of these legislative developments and the government’s assurances in 1987

that criminal insider trading sanctions were serving their deterrent purpose, both the frequency

and severity of those sanctions have continued to increase ever since. The Boesky scandal was

followed by a new flurry of legislative action, resulting in the Insider Trading and Securities

Fraud Enforcement Act of 1988 (ITSFEA). Under ITSFEA, criminal penalties would rise

substantially, with the maximum fine increasing from $100,000 to $1M for individuals, from

$500,000 to $2.5M for all other entities (previously only exchanges were subject to this

provision), and a new maximum prison term of ten years.29 Civil penalties, too, expanded, as

securities firms—not just individuals—were subject to treble damages under the Act for

“failing to take adequate steps to supervise their employees and prevent insider trading

violations.”

The House Report that accompanied the proposed legislation described its objectives:

The Insider Trading and Securities Fraud Enforcement Act of 1988 represents the response of this Committee to a series of revelations over the last two years concerning serious episodes of abusive and illegal practices on Wall Street. In the view of the Committee, the present enforcement framework should be strengthened to curtail continuing insider trading and other market abuses. This legislation embodies a series of statutory changes the Committee views as necessary to enhance deterrence against insider trading, and where that deterrence fails, to augment the current methods of detection and punishment of this behavior. Particularly in the aftermath of the stock market crash of October 19, 1987, the Committee views these steps as an essential ingredient in a program to restore the confidence of the public in the fairness and integrity of our securities markets.30

The bill further encouraged the continued and vigorous criminal prosecution of insider trading:

The Committee's interest in the maximum jail term is an explicit congressional statement of the heightened seriousness with which insider trading and other securities fraud offenses should be viewed. Although the legislation does not

29 Id. 30 H.R. REP. NO.100-910 (1988)

10

include an explicit mandatory minimum sentence the Committee believes in the strongest possible manner that courts should impose jail terms for the commission of these crimes, and expects that raising the ceiling will increase the certainty of substantial prison sentences.31

As a means to encourage such prosecutions, and in light of “the difficulties in detection

and prosecution, and recognizing the finite resources at the Commission and the Department of

Justice,” the Act granted the SEC the authority to award bounty payments for information

leading to successful criminal prosecutions.32

Most recently, in 2002, on the heels of the Enron scandal, Congress passed the

Sarbanes-Oxley Act, increasing the maximum penalty for insider trading to twenty years and a

fine of $5M.33 The sentencing guidelines were adjusted accordingly. Ivan Boesky’s sentence

looks downright brief in retrospect. Today, a violation of 78ff(a) compounded by gains of

$364M (Boesky’s $200M, adjusted for inflation) would earn a federal recommendation of

more than nineteen years in prison. In a modern version of the Boesky scandal, Worldom CEO

Bernie Ebbers was convicted of violations of section Rule 10b-5, as well as conspiracy, and

false filings. He was sentenced to twenty-five years in prison, a term the Second Circuit

affirmed for lack of abuse of discretion, but which it described as “harsh” and “longer than the

sentences routinely imposed by many states for violent crimes, including murder, or other

serious crimes such as serial child molestation.”34

31 Id. 32 Id. 33 15 U.S.C. § 78ff(a) (2002). 34 United States v. Ebbers, 458 F3d 110, 129 (2d Cir. 2006).

11

V. Insider Trading and the “Ratchet” Effect

White collar sentencing has thus been subject to what has been termed a “ratchet

effect.”35 With little regard for whether the steadily increasing sentences are correlated to an

increase in deterrence, Congress has readily passed stricter and stricter maximum sentences

(and indeed, minimum sentences, by amendment to the Federal Sentencing Guidelines) in

response to periodic public outrage at such high-profile cases as the Boesky scandal. These

scandals have given lawmakers the opportunity to “compete to prove their toughness on

crime.”36

Indeed, the ratchet effect likely has less to do with effective deterrence and more to do

with pleasing constituents. Congress has been happy to overreact, according to Professor

Thomas Joo, in his article, Legislation and Legitimation: Congress and Insider Trading in the

1980s.37 Joo argues that the unprecedented increases in criminal and civil sanctions of the

1980s were not efforts to stabilize the market, but rather “Congress's need to legitimate itself in

the eyes of the American public during a time of economic uncertainty” when “average voters

[were] plagued by economic fears.”38

This kind of congressional self-legitimation requires a public outcry. Constituents,

more than ever attuned to market fluctuations and attendant scandals, have been happy tp

oblige. In the last forty years, the stock market has become an increasingly significant source

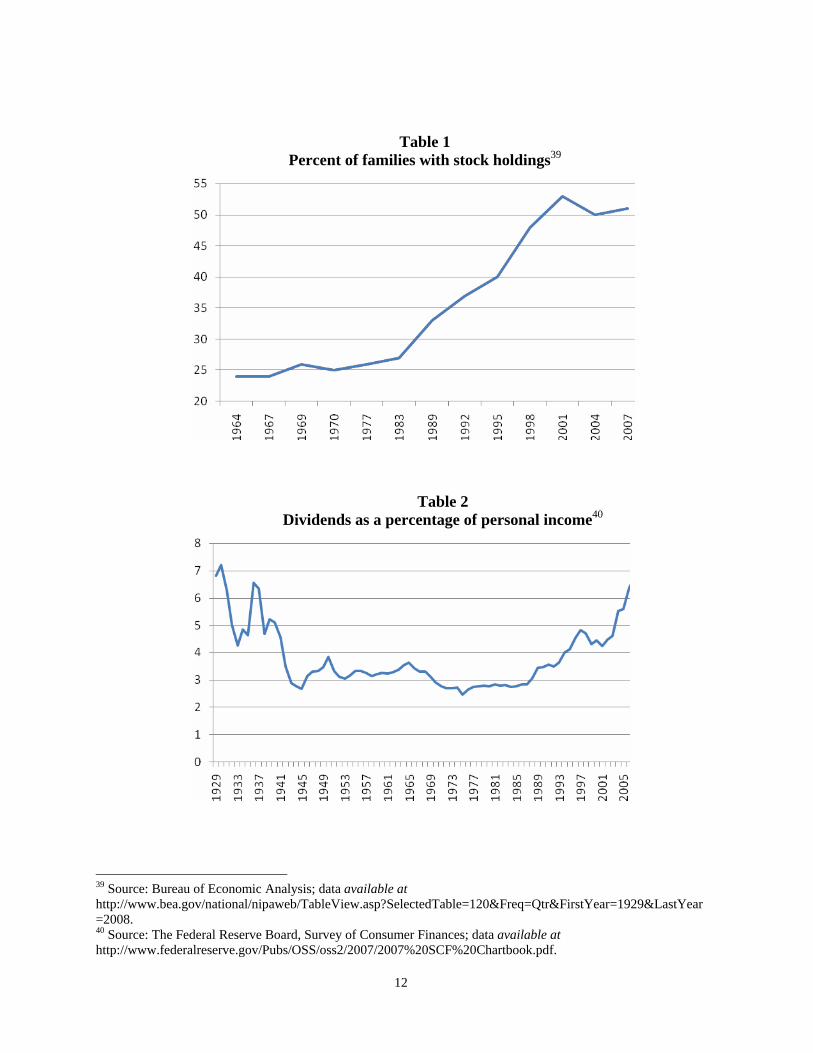

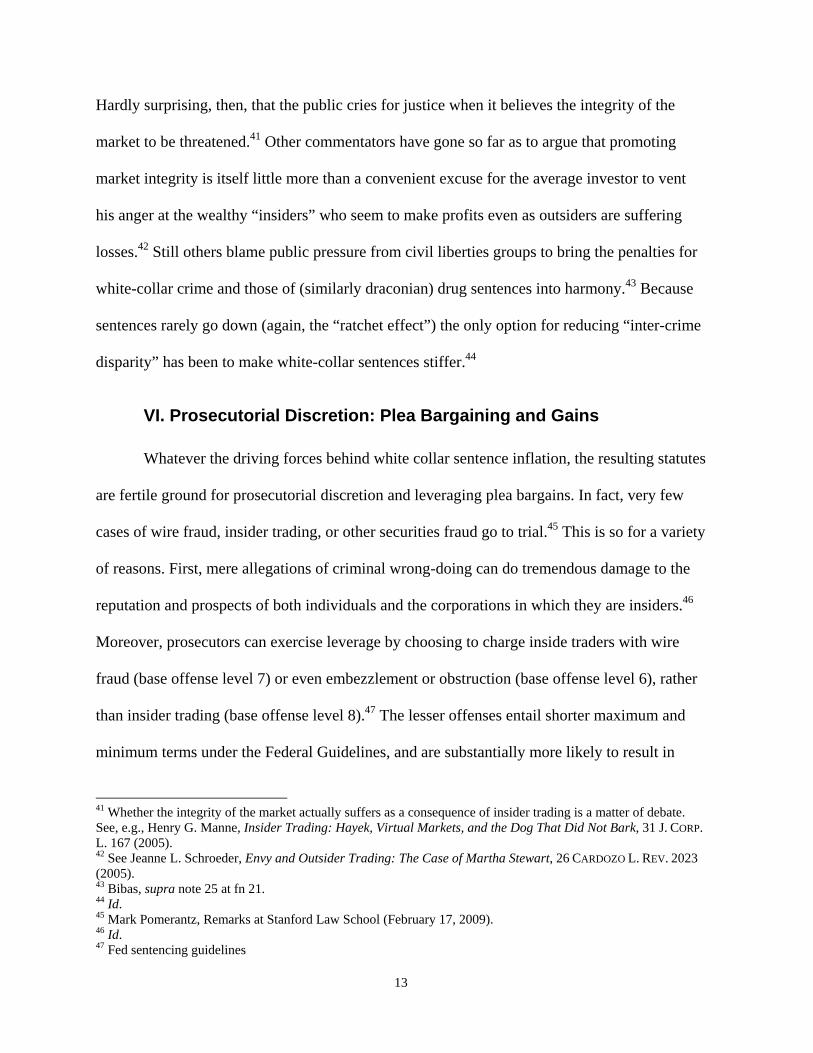

of income and a popular place to invest. In 1964 less than a quarter of American households

held securities. Today the figure is well over half, with dividends as a percentage of personal

income having nearly tripled in the same period (see Tables 1 and 2).

35 See Bibas, supra note 25 at 721. 36 Id. 37 Thomas Joo, Legislation and Legitimation: Congress and Insider Trading in the 1980s, 82 IND. L.J. 575 (2007). 38 Id. at 576, 581.

12

Table 1 Percent of families with stock holdings39

Table 2

Dividends as a percentage of personal income40

39 Source: Bureau of Economic Analysis; data available at http://www.bea.gov/national/nipaweb/TableView.asp?SelectedTable=120&Freq=Qtr&FirstYear=1929&LastYear=2008. 40 Source: The Federal Reserve Board, Survey of Consumer Finances; data available at http://www.federalreserve.gov/Pubs/OSS/oss2/2007/2007%20SCF%20Chartbook.pdf.

13

Hardly surprising, then, that the public cries for justice when it believes the integrity of the

market to be threatened.41 Other commentators have gone so far as to argue that promoting

market integrity is itself little more than a convenient excuse for the average investor to vent

his anger at the wealthy “insiders” who seem to make profits even as outsiders are suffering

losses.42 Still others blame public pressure from civil liberties groups to bring the penalties for

white-collar crime and those of (similarly draconian) drug sentences into harmony.43 Because

sentences rarely go down (again, the “ratchet effect”) the only option for reducing “inter-crime

disparity” has been to make white-collar sentences stiffer.44

VI. Prosecutorial Discretion: Plea Bargaining and Gains

Whatever the driving forces behind white collar sentence inflation, the resulting statutes

are fertile ground for prosecutorial discretion and leveraging plea bargains. In fact, very few

cases of wire fraud, insider trading, or other securities fraud go to trial.45 This is so for a variety

of reasons. First, mere allegations of criminal wrong-doing can do tremendous damage to the

reputation and prospects of both individuals and the corporations in which they are insiders.46

Moreover, prosecutors can exercise leverage by choosing to charge inside traders with wire

fraud (base offense level 7) or even embezzlement or obstruction (base offense level 6), rather

than insider trading (base offense level 8).47 The lesser offenses entail shorter maximum and

minimum terms under the Federal Guidelines, and are substantially more likely to result in

41 Whether the integrity of the market actually suffers as a consequence of insider trading is a matter of debate. See, e.g., Henry G. Manne, Insider Trading: Hayek, Virtual Markets, and the Dog That Did Not Bark, 31 J. CORP. L. 167 (2005). 42 See Jeanne L. Schroeder, Envy and Outsider Trading: The Case of Martha Stewart, 26 CARDOZO L. REV. 2023 (2005). 43 Bibas, supra note 25 at fn 21. 44 Id. 45 Mark Pomerantz, Remarks at Stanford Law School (February 17, 2009). 46 Id. 47 Fed sentencing guidelines

14

probation in lieu of incarceration.48 Not surprisingly, as a result, plea bargaining is particularly

common in white collar prosecutions.49 Indeed, a study of all insider trading prosecutions

conducted by the Department of Justice between 1980 and 1989 found that nearly seventy-five

percent of defendants pleaded guilty (and a meager three percent of those charged were

ultimately found not guilty at trial).50 The dangers of fighting a charge of insider trading are

thus manifest. In 2004, Jamie Olis, the chief figure in the Dynegy accounting scandal received

a twenty-four year sentence for misrepresenting his company’s revenues, while his co-

conspirators accepted deals limiting their sentences to a maximum of five years.51 Olis’s

sentence, however, was later reduced to six years on the ground that that damages had been

improperly calculated.52 The case is illustrative of the significance of damages calculation in

white-collar crime, another grey area of the law and an opportunity for prosecutors to over-

charge, as discussed below.

A. Gains Calculation

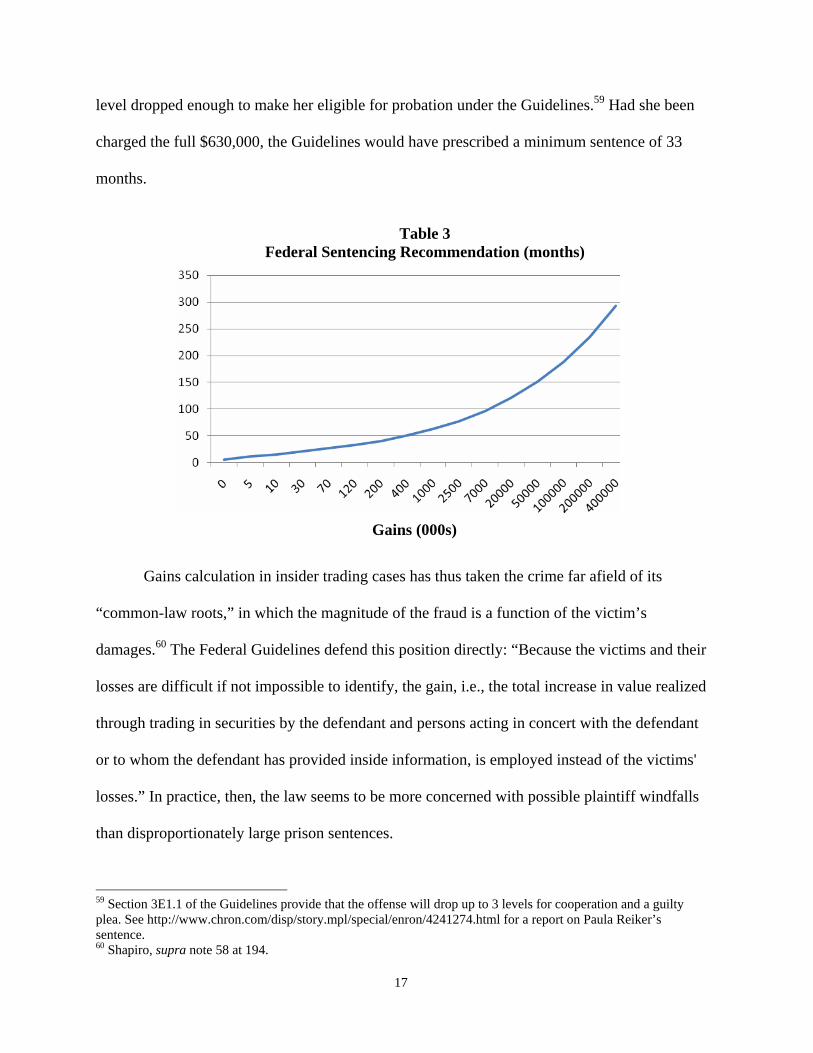

Because the recommended prison term for a given insider trading action is a function of

the profits to or loss avoided by the individual (“gains”), determination of this sum is a

component in any such action (see Table 3). Civil and criminal insider trading cases differ in

the manner in which they calculate gains. In a civil case, calculating the amount to be

disgorged from the defendant is based on a so-called “market absorption” approach, according

to which “the amount . . . is generally the difference between the value of the shares when the

insider sold them while in possession of the material, nonpublic information, and their market 48 Bibas, supra note 25 at 727 49 Pomerantz, supra at note 41. See also Elizabeth Szockyj & Gilbert Geis, Insider Trading Patterns and Analysis, Journal of Criminal Justice Vol. 30 No. 4 (2002). 50 Id. at pg. 281, The results for civil actions were not much better (4.8% found not guilty). 51 Bibas, at 727. 52Stockmarket Fraud, THE ECONOMIST, Sept. 7, 2006, available at http://www.economist.com/finance/displaystory.cfm?story_id=7880472.

15

value a reasonable time after public dissemination of the inside information.” 53 This approach

is highly susceptible to miscalculation. Stock prices are a function of dozens of factors,

including "changed economic circumstances, changed investor expectations, new industry-

specific or firm-specific factors, conditions, or other events, which taken separately or together

account for some or all of that lower [or higher] price."54

Isolating the effects of insider trading on a given security is thus necessarily imprecise.

In a simple example, suppose the insider purchases his company’s common stock in

anticipation of favorable profits statement he knows will drive the price up. If, prior to the

profits statement, the unanticipated dissolution of a competitor drives the share price up further

than the statement alone would have, then measuring the price differential from time of

purchase to time of announcement would result in gains that do not correlate with the value of

the misused information, and too large a fine for the defendant—a potential windfall for the

plaintiff.55

Calculation of gains in criminal prosecutions is even more clumsy. Rejecting the

“market absorption” approach, courts have assessed “gain” simply as the profit realized on the

transaction (gross sale receipts less purchase price). The rationale, as the Eight Circuit phrased

it in United States v. Mooney,56 seems to be that “the defendant's gain is not dependent ‘on the

gyrations of the stock market’ . . . ; it is the inside trader who chooses the timing of his

transactions—his purchases as well as his sales.”57 In other words, the (apparently irrebuttable)

presumption is that the trader’s crime spans the period from the purchase of the stock to its

53 SEC v. Happ, 392 F3d 12, 31 (1st Cir. 2004). 54 Dura Pharmaceutical, Inc. v. Broudo, 544 U.S. 336, 343 (2005). 55 See, e.g., United States v. Olis, 429 F.3d 540, 546 (5th Cir. 2005) (“Government's [frequent] use of stock prices the day before and the day after the revelation of the fraud [does] not account either for the actual price at which most holders purchased the company's shares, or for the influence of outside factors on the change in price”). 56 425 F.3d 1093 (8th Cir. 2005) 57 Id. at 1099

16

sale, regardless of when he may have come into possession of the inside information—let alone

when he may have formed intent. Given that the purchase may have been made years before

the acquisition of the information and the sale of the stock, this method of calculation threatens

a federal sentencing recommendation grossly out of proportion to the crime.

Gains calculation in cases where the insider information is never made public may be

still further disconnected from the actual misdeed or value of the misappropriated information.

Per ITSFEA, “[I]n situations in which the information is never fully disseminated to the public,

the profit gained or loss avoided [will] be measured by the difference between the purchase or

sale price and the value the security would have had at the time of the violation if the

information had been publicly disseminated, based upon the facts and circumstances of the

case.”

Some academics have called for courts to address these issues in gains calculation, and

courts have indicated a willingness to consider expert testimony to address the complexity of

the calculation in the sentencing context.58 In the meantime, prosecutors may adopt various

means to calculate gains for the purposes of pleas, thereby manipulating the maximum

recommended prison terms under the Guidelines. The case of former Enron executive, Paula

Reiker, is illustrative. Reiker exercised 18,380 options at her strike price of $15.51 in advance

of a loss report by Enron that drove the price down slightly less than a dollar. Her net profit on

the transaction was some $630,000, but the loss avoidance was only $18,000. By pleading

guilty to charges of insider trading with gains stipulated at the lower amount, Reiker’s offense

58 Alexandra Shapiro, Measuring “Gain” Under the Insider Trading Sentencing Guideline Based on Culpability for the deception, 20 FED. SENT’G. REP. 194, 198 (2008).

17

level dropped enough to make her eligible for probation under the Guidelines.59 Had she been

charged the full $630,000, the Guidelines would have prescribed a minimum sentence of 33

months.

Table 3

Federal Sentencing Recommendation (months)

Gains calculation in insider trading cases has thus taken the crime far afield of its

“common-law roots,” in which the magnitude of the fraud is a function of the victim’s

damages.60 The Federal Guidelines defend this position directly: “Because the victims and their

losses are difficult if not impossible to identify, the gain, i.e., the total increase in value realized

through trading in securities by the defendant and persons acting in concert with the defendant

or to whom the defendant has provided inside information, is employed instead of the victims'

losses.” In practice, then, the law seems to be more concerned with possible plaintiff windfalls

than disproportionately large prison sentences.

59 Section 3E1.1 of the Guidelines provide that the offense will drop up to 3 levels for cooperation and a guilty plea. See http://www.chron.com/disp/story.mpl/special/enron/4241274.html for a report on Paula Reiker’s sentence. 60 Shapiro, supra note 58 at 194.

Gains (000s)

18

In theory, strict application of sentencing ranges prescribed by the Federal Guidelines is

a thing of the past.61 In 2005, the Court held in United States v. Booker62 that mandatory

application of the Guidelines is unconstitutional. Nonetheless, the number of federal sentences

falling within the Guidelines fell a mere 2.8% between 2002 and 2006.63 In short, while the

Guidelines are no longer mandatory, they remain a highly influential. In conjunction with the

vague statutory language of Rule 10b-5, the similarly broad scope of other crimes such as

federal wire fraud and obstruction, and the freedom prosecutors have to interpret the

defendant’s grains, the Guidelines remain a powerful tool for leveraging plea bargains and

imposing harsh sentences in insider trading actions.

VII. Do Criminal Sanctions Work?

In spite of the many tools at the prosecutor’s disposal, studies suggest that illicit trading

by corporate insiders remains rife. In fact, according to one such study, the “volume of trading

performed by corporate insiders has increased fourfold since 1984 and ‘excess returns’ per

trade (returns attributable to inside information) have doubled.”64 While some maintain that

these investors are simply better at picking stocks, this seems improbable, in view of the fact

that they are the only group that can consistently out-perform the market, including mutual

fund managers who have equal access to sophisticated investment and analysis tools.65

61 By statute, departures were limited to cases where "there exists an aggravating or mitigating circumstance of a kind, or to a degree, not adequately taken into consideration by the Sentencing Commission in formulating the guidelines that should result in a sentence different from that described." PRACTICE UNDER THE FEDERAL SENTENCING GUIDELINES (PRFSG) 62 543 U.S. 220 (2005) 63See Department of Justice Fact Sheet, available at http://www.usdoj.gov/opa/documents/United_States_v_Booker_Fact_Sheet.pdf . 64Jesse M. Fried, Reducing the Profitability of Corporate Insider Trading Through Pretrading Disclosure, 71 S. CAL. L. REV. 303, 306 (1998). 65 Id. at 322.

19

Even setting aside questions of whether criminal sanctions serve their deterrent purpose

in cases of insider trading, it remains unclear that the practice threatens market integrity in the

first place. Such fears are irrational, according to Dean Emeritus, Henry Manne of George

Mason University School of law, who argues that the existence of insiders trading on non-

public information does not damage the outside trader:

[I]t's very clear that that person is in the stock market, an anonymous market, to sell the shares and doesn't care who buys them. If there's information out there, it may be an insider has it. It doesn't make any difference. Once you make a decision to sell, you don't lose anything when there's an additional buyer in the market, because that person happens to have information. That's absurd.66

A ban on insider trading would do nothing to improve the lot of the uninformed investor, but

rather “those with better access to information, such as brokers, would reap some of the gains

from inside information.” Expenditure by brokers to obtain information that is freely available

to insiders would be inefficient, goes the theory, and in either case the gap between the

informed and the uninformed remains in place.67

Moreover, in view of the fact that “a corporate insider trades on information that is

essentially undiscoverable—such as his intuition, based on all of the information available to

him” the probability of being caught, if the insider is careful is “virtually zero.”68 Manne

claims that for this reason “the SEC does not win many of the cases they bring, and they don't

bring many.”69

Finally, for a successful criminal prosecution, the information used by the insider must

be “material.” This precludes prosecution for so-called “submaterial” information that, while

66 Larry Elder, Legalize Insider Trading, CAPITALISM MAGAZINE, September 24, 2004 (interviewing Henry Manne), available at http://www.capmag.com/article.asp?ID=3933. 67 Dennis W. Carlton & Daniel R. Fischel, The Regulation of Insider Trading, 35 STAN. L. REV. 857, 888 (1983). 68 Fried, at fn 112. 69 See Elder, supra note 66.

20

not legally material, is nonetheless non-public and advantageous to the insider. Consider that

“[k]nowledge that one of the firm's top managers is dispirited because of family problems or

because preliminary reports on a new technological process show that costs are running much

higher than expected are examples of valuable information that is almost surely not material in

a legal sense.”70

Perhaps the best argument that market integrity is compromised by insider trading is

that it is perceived to be so, and where the market is concerned, investor confidence is as much

a part of stability as corporate bottom lines. In any case, it’s clear that much controversy still

exists with respect to the basic premise on which the criminalization of insider trading rests.

VIII. Conclusion

The history of legislation against insider trading has been one of scandal followed by

congressional reaction (or, some might say, overreaction). Criminal sanctions, one of society’s

preferred means of expressing moral opprobrium, have been readily supported by the public

and enacted by lawmakers. The result is a poorly-defined crime, the punishment for which

many believe has become grossly excessive. No doubt new scandals will unfold, as they have

consistently since the 1980s, and with them new opportunities to apply the “ratchet” effect.

With greater private investment in the stock market, investors have more to lose and more to be

angry about. Meanwhile, the media is keen to and adept at demonizing white collar criminals,

particularly in a time of economic crisis such as the present. Just this year, Bernard Madoff

walked a gauntlet to the courthouse past hissing and insults that seemed positively medieval.

Exactly how congress will move to appease its angry constituents is not yet clear, but if history

is any judge, it won’t likely be by relaxing criminal sanctions.

70 Carlton & Fischel, at 887.