Credit Valley Conservation - cvc.ca · common method of financing in Ontario. ... Funding the...

76

Credit Valley Conservation 2010

Transcript of Credit Valley Conservation - cvc.ca · common method of financing in Ontario. ... Funding the...

Credit Valley Conservation

2010

10527

Typewritten Text

Survey of Municipal Policies and Administrative Approaches for Overcoming Institutional Barriers to Low Impact Development

10527

Typewritten Text

10527

Typewritten Text

10527

Typewritten Text

10527

Typewritten Text

10527

Typewritten Text

10527

Typewritten Text

10527

Typewritten Text

10527

Typewritten Text

10527

Typewritten Text

10527

Typewritten Text

10527

Typewritten Text

10527

Typewritten Text

Credit River

Water Management Strategy Update –

Municipal Stormwater Financing Study

Internal Working Document

FINAL

May 2008

Credit River Water Management Strategy Update –

Municipal Stormwater Financing Study

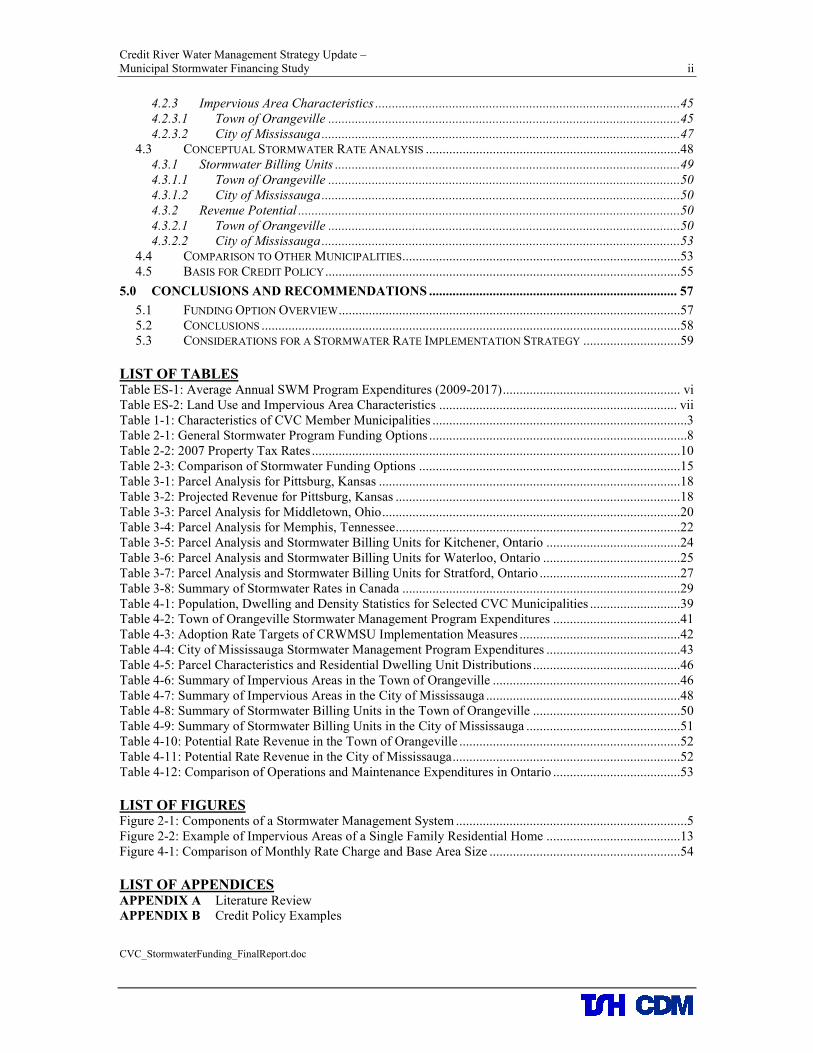

TABLE OF CONTENTS

EXECUTIVE SUMMARY............................................................................................................................

1.0 PROJECT OVERVIEW .................................................................................................................... 1

1.1 BACKGROUND ...............................................................................................................................1 1.2 STUDY TASKS ...............................................................................................................................1 1.3 PROJECT ORGANIZATION AND HIGHLIGHTS ..................................................................................2

2.0 STORMWATER FUNDING MECHANISMS................................................................................. 4

2.1 MUNICIPAL STORMWATER MANAGEMENT PROGRAMS .................................................................4 2.2 OVERVIEW OF FUNDING MECHANISMS .........................................................................................7 2.3 PROPERTY TAX ...........................................................................................................................10 2.3.1 General Tax Fund..................................................................................................................10 2.3.2 Dedicated Tax Levy ...............................................................................................................11 2.3.3 Advantages and Disadvantages .............................................................................................11

2.4 DEVELOPMENT RELATED CHARGES AND FEES............................................................................11 2.4.1 Development Charges............................................................................................................11 2.4.2 Cash-in-lieu Charges.............................................................................................................12 2.4.3 Subdivision Agreements.........................................................................................................12 2.4.4 Advantages and Disadvantages .............................................................................................12

2.5 IMPERVIOUS AREA BASED CHARGES ..........................................................................................12 2.5.1 Stormwater Rate ....................................................................................................................12 2.5.2 Advantages and Disadvantages .............................................................................................14

2.6 COMPARISON OF FUNDING OPTIONS ...........................................................................................14

3.0 REPRESENTATIVE CASE STUDIES .......................................................................................... 17

3.1 PITTSBURG, KANSAS ...................................................................................................................17 3.2 MIDDLETOWN, OHIO ...................................................................................................................19 3.3 MEMPHIS, TENNESSEE.................................................................................................................21 3.4 KITCHENER AND WATERLOO, ONTARIO......................................................................................23 3.5 STRATFORD, ONTARIO ................................................................................................................26 3.6 OTHER CANADIAN MUNICIPALITIES............................................................................................28 3.6.1 Town of Aurora, Ontario .......................................................................................................28 3.6.2 City of London, Ontario.........................................................................................................30 3.6.3 City of St. Thomas, Ontario ...................................................................................................30 3.6.4 City of Regina, Saskatchewan................................................................................................30 3.6.5 City of Saskatoon, Saskatchewan...........................................................................................30 3.6.6 City of Calgary, Alberta ........................................................................................................31 3.6.7 City of Edmonton, Alberta .....................................................................................................31 3.6.8 City of St. Albert, Alberta ......................................................................................................31 3.6.9 Strathcona County, Alberta ...................................................................................................31 3.6.10 City of Richmond, British Columbia .................................................................................32

3.7 CASE STUDY LESSONS ................................................................................................................32 3.7.1 Stormwater Funding Lessons Learned ..................................................................................32 3.7.2 Stormwater Rate Implementation Success Factors................................................................34 3.7.2.1 Public Consultation Program ...........................................................................................34 3.7.2.2 Rate Implementation Costs ...............................................................................................35 3.7.2.3 Jurisdictional Boundaries .................................................................................................35 3.7.2.4 Level of Service Flexibility................................................................................................36 3.7.2.5 Property Owner Incentives ...............................................................................................37

4.0 INITIAL PROGRAM DEFINITION.............................................................................................. 39

4.1 STORMWATER MANAGEMENT PROGRAMS IN CVC MUNICIPALITIES ..........................................39 4.1.1 Town of Orangeville ..............................................................................................................40 4.1.2 City of Mississauga................................................................................................................42

4.2 LAND USE ANALYSIS ..................................................................................................................44 4.2.1 Basis for Rate Policy .............................................................................................................44 4.2.2 Parcel Characteristics ...........................................................................................................45

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study ii

4.2.3 Impervious Area Characteristics ...........................................................................................45 4.2.3.1 Town of Orangeville .........................................................................................................45 4.2.3.2 City of Mississauga ...........................................................................................................47

4.3 CONCEPTUAL STORMWATER RATE ANALYSIS ............................................................................48 4.3.1 Stormwater Billing Units .......................................................................................................49 4.3.1.1 Town of Orangeville .........................................................................................................50 4.3.1.2 City of Mississauga ...........................................................................................................50 4.3.2 Revenue Potential ..................................................................................................................50 4.3.2.1 Town of Orangeville .........................................................................................................50 4.3.2.2 City of Mississauga ...........................................................................................................53

4.4 COMPARISON TO OTHER MUNICIPALITIES...................................................................................53 4.5 BASIS FOR CREDIT POLICY ..........................................................................................................55

5.0 CONCLUSIONS AND RECOMMENDATIONS .......................................................................... 57

5.1 FUNDING OPTION OVERVIEW......................................................................................................57 5.2 CONCLUSIONS .............................................................................................................................58 5.3 CONSIDERATIONS FOR A STORMWATER RATE IMPLEMENTATION STRATEGY .............................59

LIST OF TABLES Table ES-1: Average Annual SWM Program Expenditures (2009-2017)..................................................... vi Table ES-2: Land Use and Impervious Area Characteristics ....................................................................... vii Table 1-1: Characteristics of CVC Member Municipalities ............................................................................3 Table 2-1: General Stormwater Program Funding Options .............................................................................8 Table 2-2: 2007 Property Tax Rates ..............................................................................................................10 Table 2-3: Comparison of Stormwater Funding Options ..............................................................................15 Table 3-1: Parcel Analysis for Pittsburg, Kansas ..........................................................................................18 Table 3-2: Projected Revenue for Pittsburg, Kansas .....................................................................................18 Table 3-3: Parcel Analysis for Middletown, Ohio.........................................................................................20 Table 3-4: Parcel Analysis for Memphis, Tennessee.....................................................................................22 Table 3-5: Parcel Analysis and Stormwater Billing Units for Kitchener, Ontario ........................................24 Table 3-6: Parcel Analysis and Stormwater Billing Units for Waterloo, Ontario .........................................25 Table 3-7: Parcel Analysis and Stormwater Billing Units for Stratford, Ontario ..........................................27 Table 3-8: Summary of Stormwater Rates in Canada ...................................................................................29 Table 4-1: Population, Dwelling and Density Statistics for Selected CVC Municipalities ...........................39 Table 4-2: Town of Orangeville Stormwater Management Program Expenditures ......................................41 Table 4-3: Adoption Rate Targets of CRWMSU Implementation Measures ................................................42 Table 4-4: City of Mississauga Stormwater Management Program Expenditures ........................................43 Table 4-5: Parcel Characteristics and Residential Dwelling Unit Distributions ............................................46 Table 4-6: Summary of Impervious Areas in the Town of Orangeville ........................................................46 Table 4-7: Summary of Impervious Areas in the City of Mississauga ..........................................................48 Table 4-8: Summary of Stormwater Billing Units in the Town of Orangeville ............................................50 Table 4-9: Summary of Stormwater Billing Units in the City of Mississauga ..............................................51 Table 4-10: Potential Rate Revenue in the Town of Orangeville ..................................................................52 Table 4-11: Potential Rate Revenue in the City of Mississauga....................................................................52 Table 4-12: Comparison of Operations and Maintenance Expenditures in Ontario ......................................53

LIST OF FIGURES Figure 2-1: Components of a Stormwater Management System .....................................................................5 Figure 2-2: Example of Impervious Areas of a Single Family Residential Home ........................................13 Figure 4-1: Comparison of Monthly Rate Charge and Base Area Size .........................................................54 LIST OF APPENDICES APPENDIX A Literature Review APPENDIX B Credit Policy Examples CVC_StormwaterFunding_FinalReport.doc

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study iii

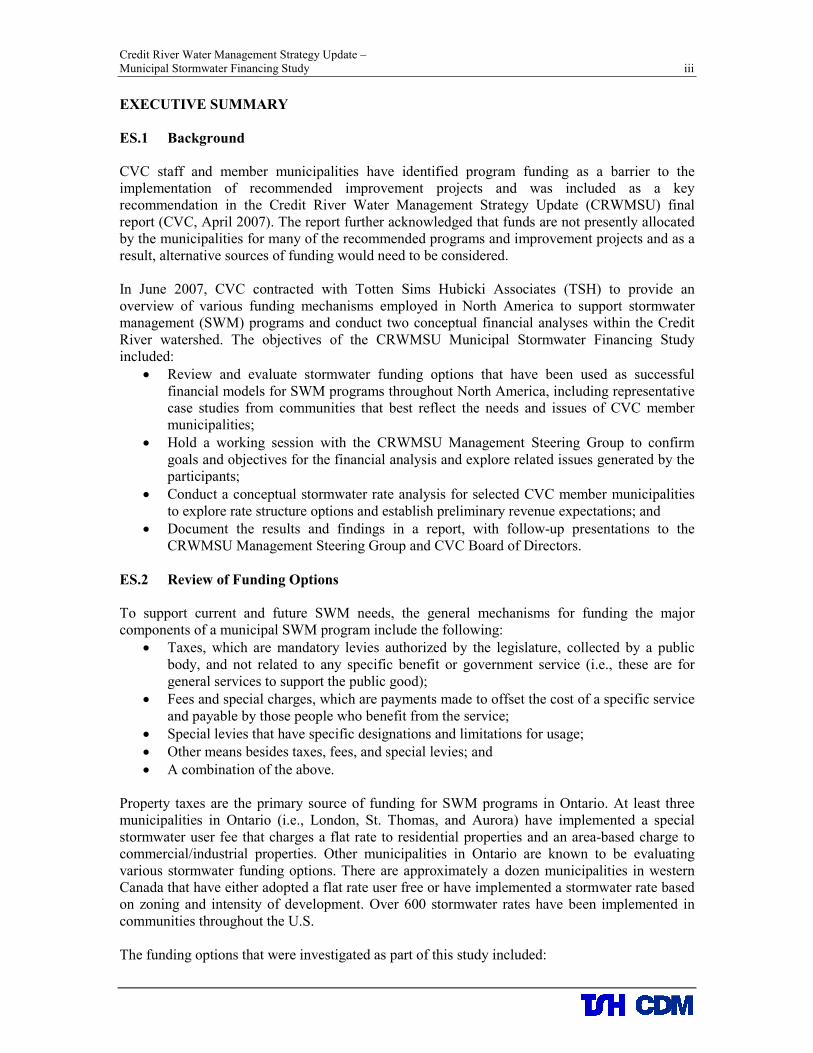

EXECUTIVE SUMMARY

ES.1 Background

CVC staff and member municipalities have identified program funding as a barrier to the implementation of recommended improvement projects and was included as a key recommendation in the Credit River Water Management Strategy Update (CRWMSU) final report (CVC, April 2007). The report further acknowledged that funds are not presently allocated by the municipalities for many of the recommended programs and improvement projects and as a result, alternative sources of funding would need to be considered. In June 2007, CVC contracted with Totten Sims Hubicki Associates (TSH) to provide an overview of various funding mechanisms employed in North America to support stormwater management (SWM) programs and conduct two conceptual financial analyses within the Credit River watershed. The objectives of the CRWMSU Municipal Stormwater Financing Study included:

• Review and evaluate stormwater funding options that have been used as successful financial models for SWM programs throughout North America, including representative case studies from communities that best reflect the needs and issues of CVC member municipalities;

• Hold a working session with the CRWMSU Management Steering Group to confirm goals and objectives for the financial analysis and explore related issues generated by the participants;

• Conduct a conceptual stormwater rate analysis for selected CVC member municipalities to explore rate structure options and establish preliminary revenue expectations; and

• Document the results and findings in a report, with follow-up presentations to the CRWMSU Management Steering Group and CVC Board of Directors.

ES.2 Review of Funding Options

To support current and future SWM needs, the general mechanisms for funding the major components of a municipal SWM program include the following:

• Taxes, which are mandatory levies authorized by the legislature, collected by a public body, and not related to any specific benefit or government service (i.e., these are for general services to support the public good);

• Fees and special charges, which are payments made to offset the cost of a specific service and payable by those people who benefit from the service;

• Special levies that have specific designations and limitations for usage;

• Other means besides taxes, fees, and special levies; and

• A combination of the above. Property taxes are the primary source of funding for SWM programs in Ontario. At least three municipalities in Ontario (i.e., London, St. Thomas, and Aurora) have implemented a special stormwater user fee that charges a flat rate to residential properties and an area-based charge to commercial/industrial properties. Other municipalities in Ontario are known to be evaluating various stormwater funding options. There are approximately a dozen municipalities in western Canada that have either adopted a flat rate user free or have implemented a stormwater rate based on zoning and intensity of development. Over 600 stormwater rates have been implemented in communities throughout the U.S. The funding options that were investigated as part of this study included:

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study iv

• Property Tax which allocates charges to property owners based on assessed value. Funding a municipal SWM program with revenue from property taxes is the most common method of financing in Ontario. As an alternative, a dedicated levy could be administered specifically for SWM. The primary advantages of using property taxes to support the municipal SWM program, either through a general tax fund or dedicated levy, is that this method is already accepted as the primary existing source of revenue for municipalities and the billing system is already established. The primary disadvantages are that the fairness and equity in allocating charges is low, it is not a sustainable revenue stream, there are no incentive opportunities to reduce stormwater runoff and pollutant discharge, and many large properties do not contribute to the funding (i.e., tax-exempt).

• Development Related Charges and Fees which allocates charges to developers to fund eligible growth-related costs. Development charges (DC) are used to pay for capital costs of SWM facilities in specific areas. Cash-in-Lieu charges can be applied to both capital and operations/maintenance costs of SWM facilities in redevelopment/infill situations, and not necessarily in the location where the development is occurring. Subdivision agreements can also be used to pay for area-specific capital works and anticipated future operations/maintenance. The primary advantage is that these methods are currently accepted by the development community. The primary disadvantages are that these methods are limited by the amount of developable land within municipality and are directly dependent on growth and economic conditions.

• Stormwater Rate which allocates charges to property owners based on the measured area of impervious ground cover (e.g., rooftops, driveways, and parking lots), which is a common indicator of the relative contribution of stormwater runoff and pollutant loading to the municipal SWM system. Funding through a stormwater rate has the primary advantages of a fair and equitable allocation of charges to property owners, it is a sustainable and dedicated funding source, provides incentive opportunities to reduce stormwater runoff and pollutant discharge, and it provides a mechanism to charge tax-exempt properties for municipal SWM services. The primary disadvantages include additional costs for rate implementation and the possibility that a new fee may not be well received by the public. A new fee structure might also be reluctantly received by municipal staff if it does not fit well within the current financial and policy framework dominated by property tax revenues.

ES.3 Case Studies and Lessons Learned

To provide an example of the application of a stormwater rate in communities with characteristics similar to CVC member municipalities, representative case studies of stormwater rate implementations were presented for the following communities:

• Pittsburg, Kansas which represents a largely rural community located in the headwaters

• Middletown, Ohio, an urbanizing community in the middle of a watershed

• Memphis, Tennessee, a large urban community at the downstream end of a watershed To add a Canadian perspective, recent stormwater rate studies in Ontario (i.e., Kitchener, Waterloo, and Stratford) were summarized along with details of stormwater financing programs from other municipalities across Canada. Based on the consultant’s experience in municipal SWM financing throughout North America, a common set of lessons learned was derived, and includes the following:

1. Recognize that one size does not fit all. Each community’s SWM program has unique needs, preferred solutions, organizational structures, staff experience and knowledge, equipment and resources.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study v

2. Collaborate with stakeholders and promote communication. Stakeholders need to be chosen carefully and representative of all the citizens and property owners who will be paying for the SWM program. Further, the facilitator at stakeholder meetings needs to ensure the facts have been presented and understood, inspire collaborative dialog, and be impartial in the decision making process yet skilled at marshalling divergent opinions toward group consensus.

3. Define the champion and home of the program. The champion or champions of the funding program can either be a respected community leader, activist, councilor or staff person. The home of the program can refer to the local government (i.e., regional or municipal level) and the department in which the program resides (e.g., Engineering, Finance, or Public Works).

4. Clearly define the health, safety and welfare benefits. The guiding principles behind the municipal SWM program should be, first and foremost, the health, safety, and welfare of its residents and business owners. Clearly documenting and defining a municipality’s SWM issues, problems and needs along with the corresponding solutions, services, and expenditures is a necessary step in identifying the optimal funding mechanism.

5. Clearly define the cost of each program element. The level of service provided by the municipality’s SWM system directly affects the overall program cost. Public trust and confidence can only be gained through a clear and transparent accounting of program costs.

6. Allocate level of service by geography. There are clear differences between SWM facilities and services in an urban versus a rural setting (e.g., curb/gutter with storm sewers versus roadside ditching). Even within a rural setting for example, there can be different service costs for operations and maintenance activities and capital projects, depending on topography and vegetation cover.

7. Pragmatically address inter-jurisdictional issues within watersheds. Political boundaries often present roadblocks to SWM. Joint initiatives can realize great cost efficiencies in SWM services and capital projects.

8. Keep abreast of new legislation and initiatives. It is also important for municipal staff to keep on top of upcoming SWM regulations, funding opportunities, and new technologies to bolster long-term program planning and identify future cost efficiencies in service delivery.

9. Provide clear documentation for customer fees. Regardless of the funding mechanism that is ultimately selected for the municipality, customer relations will be improved when an effort is made to clearly explain any new charges.

10. Establish policies to address private property issues. With an increasing focus on source or lot-level controls for SWM, it is becoming increasingly important to establish municipal policies to assist in dealing with private property issues.

ES.4 Conceptual Rate Analysis

To explore rate structure options and establish preliminary revenue expectations, a conceptual stormwater rate analysis was conducted for two CVC member municipalities. The development of a stormwater rate structure required an estimate of the annual SWM program expenditures and the impervious area characteristics of each municipality, which were selected in order to represent a cross-section of CVC communities that vary by geography, governance, population, and land use characteristics:

• Orangeville, a town located in the headwaters of the Credit Valley watershed; and

• Mississauga, a large city located at the downstream end of the Credit Valley watershed.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study vi

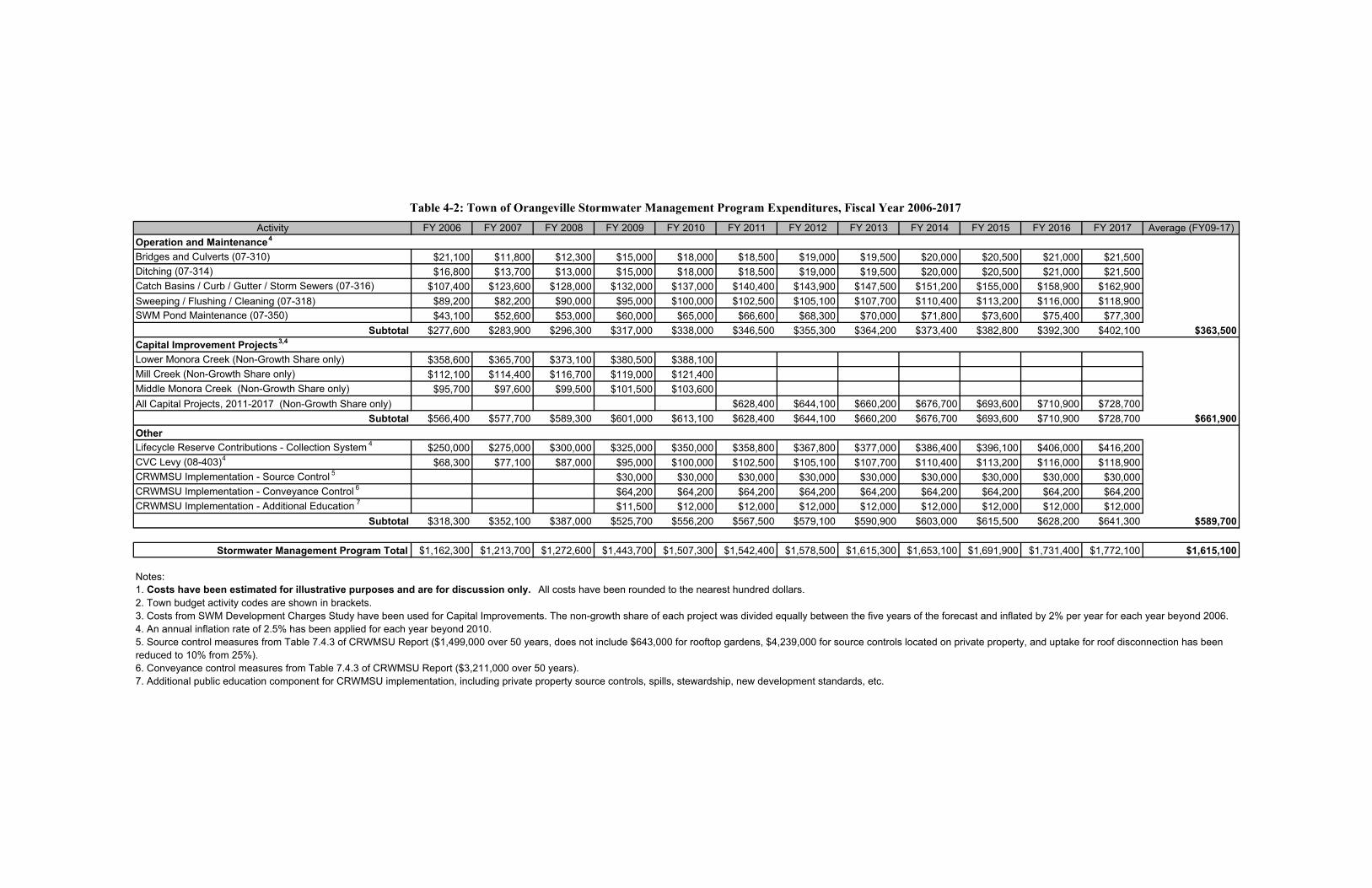

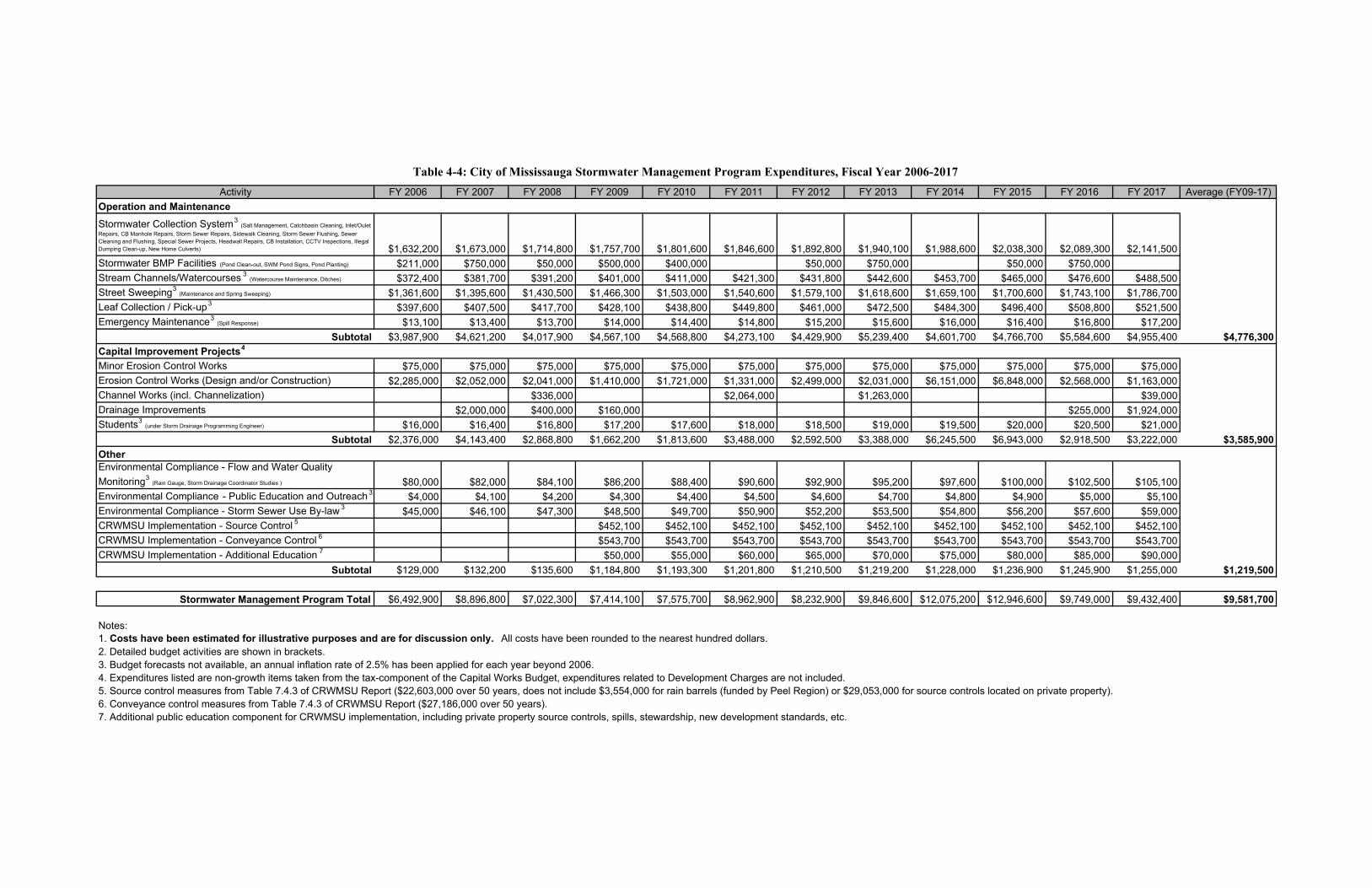

Stormwater Management Program Expenditures Table ES-1 summarizes the projected SWM program costs for Orangeville and Mississauga, which represent non-growth related expenditures (i.e., activities funded through their respective DC programs have not been included) that are needed to achieve desired level of service goals and meet regulatory compliance targets. These costs have been estimated and are for illustrative purposes in order to satisfy the objectives of this study. Further cost details would need to be investigated should the financial analysis be extended beyond the scope of this study.

Table ES-1: Average Annual SWM Program Expenditures (2009-2017) Activity Orangeville Mississauga

Operation and Maintenance $363,500 $4,776,300

Capital Improvement Projects $661,900 $3,585,900

Other Municipal SWM Program Activities $483,600 $153,700

CRWMSU Implementation $106,100 $1,065,800

Total $1,615,100 $9,581,700

Notes:

1. Costs have been estimated for illustrative purposes and are for

discussion only. In addition to the expenditure items estimated by staff in the respective municipalities, CRWMSU implementation costs from the April 2007 final report have been incorporated into the average annual expenditures. These costs are shown in the bottom row of Table ES-1 and include the following items:

• Source control measures, which are designed to reduce runoff, improve water quality and control flows that affect flooding and erosion within urban areas and are generally applied to individual lots (e.g., roof downspout disconnection, porous pavement; soak away pits, parking lots equipped with biofilters and rooftop storage);

• Conveyance control measures, which are designed to reduce runoff by encouraging higher levels of infiltration into the ground and are generally applied within the existing collection system (e.g., porous stormwater pipes, grassed swales, and dual-pipe systems where one pipe infiltrates water into the ground through a gravel filter); and

• Additional public education activities to plan, promote and implement private property source controls, stewardship practices, including landowner and community outreach to build general awareness of environmental issues within the Credit Watershed and inform citizens and business owners on best management practices (BMPs), spill prevention, and new development standards, etc.

Land Use Analysis A parcel analysis identifies the characteristics of parcels in a municipality, which in turn determines the base charge for a stormwater rate. Every parcel of land in a municipality contributes runoff to the municipal drainage system and impacts water quality in proportion to the amount of impervious area located on their property. The impervious area of a parcel refers to surfaces covered with material that is highly resistant to the infiltration of water (e.g., building rooftops, paved areas, and compacted gravel). In a typical stormwater rate study, a statistical sampling process would be conducted to provide an accurate and defensible estimate for residential impervious area determinations. For the purposes of this study however, impervious area estimates were based on land use assumptions and other information provided by the municipalities.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study vii

A summary of land use characteristics and impervious area estimates for Orangeville and Mississauga are shown in Table ES-2. The number of residential dwelling units is shown along with the percentage of detached single-family houses. The estimated impervious areas are shown in the next four rows of Table ES-2. The public right-of-way (ROW) is not typically included in the stormwater rate calculation as it is considered part of the drainage collection system.

Table ES-2: Land Use and Impervious Area Characteristics

Orangeville Mississauga

Item Count Distribution Count Distribution

Residential Dwelling Units1 9,420 60% 223,720 42%

Estimated Impervious Area (m2)

Residential 2,486,680 44% 39,398,804 23%

Non-Residential 2,260,793 40% 81,099,097 46%

Right-of-Way 962,727 17% 54,093,492 31%

Total 5,710,200 100% 174,591,393 100%

Number of Equivalent Residential Billing Units (ERUs)

Residential 9,420 52% 223,720 33%

Non-Residential 8,564 48% 460,509 67%

Right-of-Way 0 0% 0 0%

Total 17,984 100% 684,229 100%

Average ERU Size (m2) 264.0 176.1

Notes:

1. Distribution shown is the proportion of detached single family homes. In an Equivalent Residential Unit (ERU) rate structure, each residential dwelling unit is assigned one stormwater billing unit. Non-residential ERUs are assigned based on the impervious area divided by the average ERU size, which is 264 m2 (2,841 ft2) and 176 m2 (1,896 ft2) respectively for Orangeville and Mississauga, as shown in the bottom row of Table ES-2. These values fit within the typical range of 115 communities in the state of Florida of between 150 and 320 m2 (1,600 to 3,400 ft2) and can also be compared to those determined in recent stormwater rate studies conducted by the consultant team in other southern Ontario municipalities, namely:

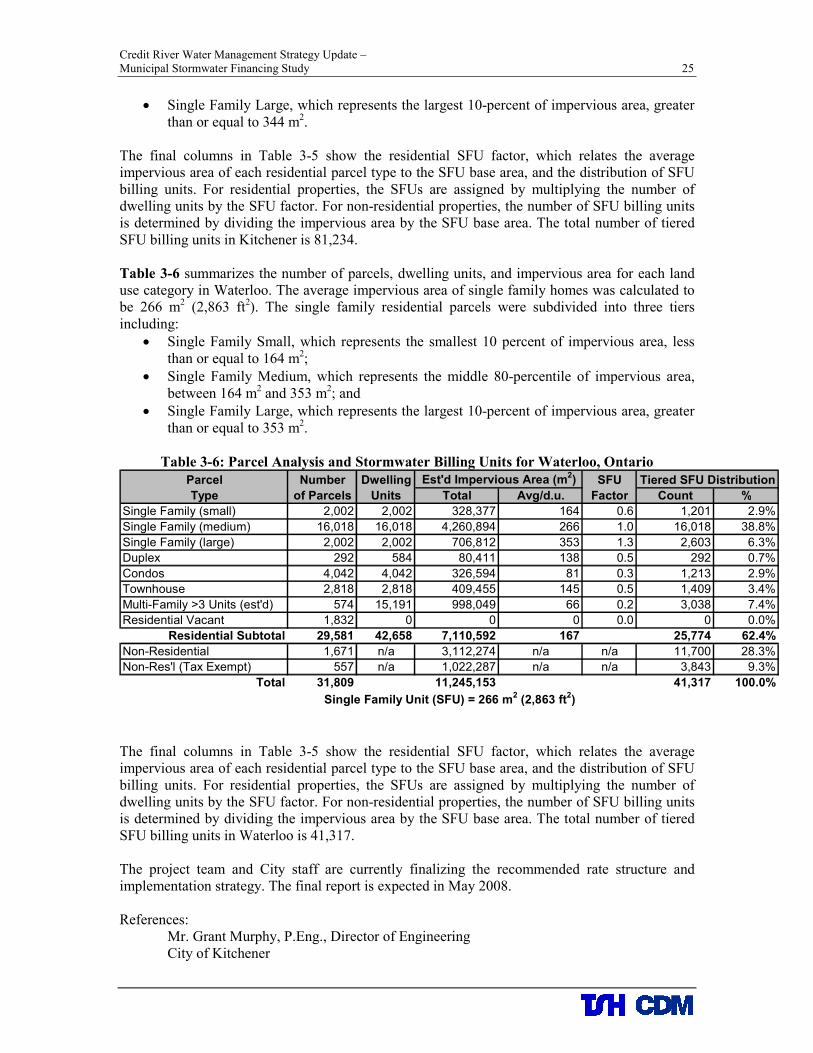

• Kitchener: 178 m2/ERU

• Stratford: 196 m2/ERU

• Waterloo: 167 m2/ERU

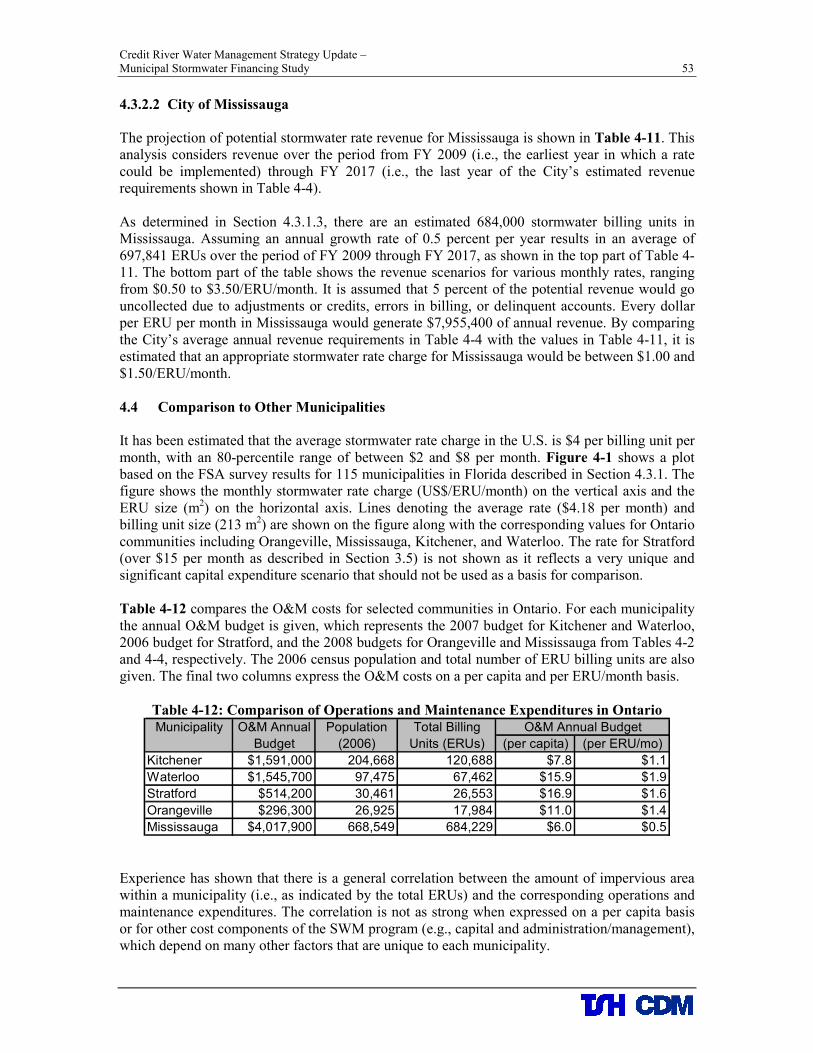

Potential Stormwater Rate Revenue By comparing the annual revenue needs with the estimated number of billing units in each community, a projection of the potential stormwater rate revenue was made. In Orangeville, every dollar per ERU per month would generate $209,350 of annual revenue and a stormwater rate charge between $7.50 and $8.00/ERU/month would support the Town’s average annual revenue requirement of $1,615,100. In Mississauga, every dollar per ERU per month would generate $7,955,400 of annual revenue and a stormwater rate charge between $1.00 and $1.50/ERU/month would support the City’s average annual revenue requirement of $9,581,700. These revenue forecasts assume an annual billing unit growth rate of 0.5 percent would be achieved and also that there would be a 5 percent reduction in rate revenue due to adjustments, credits, errors in billing, or delinquent accounts, which is typical in other jurisdictions throughout the U.S. It has been estimated that the average stormwater rate charge in the U.S. is $4 per billing unit per month, with an 80-percentile range of between $2 and $8 per month. Recent rate studies in Kitchener and Waterloo indicated base charges of $4.41 and $4.17/ERU/month, respectively.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study viii

Credit Policy Credits, if awarded, would reduce a property owner’s charge from the base stormwater rate if their on-site facilities have been property designed, constructed, and maintained to provide an appropriate level of control for flooding, erosion, and/or water quality treatment. Credits are typically awarded to any facilities that relieve the municipality of its fiscal SWM responsibilities or otherwise result in direct savings to the municipality’s SWM program. Typically, SWM facilities for urban development projects provide primarily localized benefits. For example, because stormwater detention basins for development projects control a relatively small percentage of the watershed, its benefits are typically limited to stream systems immediately downstream of the development site. Since it is unlikely that privately maintained SWM facilities significantly reduce the municipality’s system-wide costs, it is appropriate to express the benefits of these facilities in terms of potential reductions in the “local” SWM program costs. Therefore, the recommended approach to establishing a technical basis for the municipality’s credit policy is to base the “maximum total credit” (i.e., maximum stormwater rate reduction) on the total percentage of SWM program costs which provide “local” benefits. The credit factors require evaluation of the programmatic budgets for a reasonable period of time to reflect overall costs. Based on the consultant’s experience in similar jurisdictions, an initial set of credit values is suggested which add to a maximum of 50 percent credit. Upon the initial years of the stormwater rate it is advisable to further adjust such values to reflect the overall costs and benefits perceived by the municipality. ES.5 Conclusions and Recommendations

The cost of the municipal SWM programs within CVC’s jurisdiction will increase significantly in future years. Not only will costs increase due to the implementation of CRWMSU recommendations, but also as municipalities increase their stormwater level of service to address new water quality regulations, replace/rehabilitate aging infrastructure, and an increased maintenance burden as new development infrastructure is assumed. As a result, municipalities will need greater emphasis on sound asset management and financial planning, particularly a long-term outlook for municipalities with decreasing growth/development potential. A stormwater rate was chosen to be the focus of this study as it is the most fair, equitable and sustainable funding mechanism. A stormwater rate charges property owners based on their relative contribution of stormwater runoff volume and pollutant loading, whereas property tax funding is only based on assessed property value and DC is based on total number of dwelling units or land area. As a dedicated and sustainable source of funding, a stormwater rate provides more budgeting flexibility than property tax or growth-related funding. A stormwater rate also supports CRWMSU strategies by including incentives for private property source controls. Not only is there an inherent developer incentive for installing stormwater source controls (i.e., since they reduce land requirements for end-of-pipe facilities and therefore can reduce overall SWM construction costs), but property owners with source controls would be eligible for stormwater rate credits if these facilities are properly maintained. The biggest challenges for a stormwater rate are the costs associated with a rate implementation study and in achieving consensus among key stakeholders in an acceptable rate structure and credit policy details, particularly with tax-exempt property owners who would now be faced with a new charge, and commercial/industrial business owners, some of whom could be impacted greatly by redistributing the cost allocation from assessed value to an impervious area based

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study ix

charge. These challenges have been overcome in past studies through stakeholder involvement and a properly implemented public consultation program. Further, since the stormwater rate represents a major departure from current municipal financing policies, it would require a broader public finance framework, as well as a strong political will among councilors and ratepayers in order to implement. This challenge is neither unusual nor insurmountable, as experience in other jurisdictions has shown. Although the details in this report are decidedly focused on stormwater rates, it is the individual

choice of each municipality whether to pursue the funding options presented in this report. Such implementation decisions may be a function of time. That is, as growth-related development opportunities become more limited and the DC revenue potential declines, a stormwater rate program may become more attractive. Further, as municipal accounting and fiscal management policies mature and evolve, such that revenue sources are more rigorously assigned to specific cost centers, a rate program may also become more attractive. For municipalities that may choose to consider investigating a stormwater rate as an alternative method of financing their SWM program, a series of implementation steps was suggested to help provide guidance for initial dialog among municipal staff. The recommended implementation strategy includes the following items:

1. Select a Stormwater Advisory Committee (SWAC) of key community stakeholders and ratepayer representatives. A series of monthly facilitated meetings should be planned and coordinated with the stormwater rate study to solicit feedback and dialog throughout the process.

2. Conduct a parcel analysis including impervious area measurements for a representative

statistical sampling of residential properties and all non-residential properties.

3. Conduct a financial review of SWM related expenditures to determine the annual funding requirements under two level of service (LOS) scenarios: current LOS based on recent fiscal year expenditures and budget forecasts, and a sustainable LOS representing staff’s assessment of future SWM program activities and expenditures required to provide a more proactive and preventative maintenance program, additional activities to meet provincial and federal water quality requirements, manage assets in a more sustainable manner, and to meet service expectations of the public. LOS scenarios should be expressed as an annual expense averaged over a suitable planning horizon (e.g., 5 years).

4. Develop an appropriate stormwater billing unit method and rate structure based on the

parcel and financial analyses described in the preceding items. This rate would apply to all property types, regardless of tax status.

5. Consider a phase-in period to ease the transition from the current property tax based

funding. For example, a stormwater rate program may be phased-in over a four-year period with the following revenue sources:

• Year 1: Combined revenue including 25% stormwater rate + 75% property tax

• Year 2: Combined revenue including 50% stormwater rate + 50% property tax

• Year 3: Combined revenue including 75% stormwater rate + 25% property tax

• Year 4: 100% stormwater rate revenue

6. Consider a policy to reduce the property tax levy by the corresponding stormwater rate revenue amount in each year of the recommended phase-in period in Item 5.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study x

7. Examine the adoption of a stormwater rate credit policy, based on the following details:

• Credit eligibility to be determined based on the SWM practices and facilities on site (i.e., source controls).

• All non-residential properties, regardless of tax status, and communal stormwater facilities that serve large residential subdivisions (e.g., >250 lots) would be eligible for credits.

• A maximum credit of no more than 50%.

• Property owners must apply for a credit on an annual basis and certify that all facilities have been constructed, operated, and maintained as designed.

8. Based on discussions with SWAC, consider adopting policies that would benefit tax-

exempt properties, including:

• A rebate policy for tax-exempt properties currently contributing Payment In-Lieu-Of Taxes (PILOT, e.g., post-secondary schools and hospitals), that would deduct the stormwater component of their PILOT charge from their stormwater bill, which will vary in proportion to the stormwater rate revenue during the phase-in period; and

• A tax subsidy for tax-exempt properties that do not currently contribute Payment In-Lieu-Of Taxes (e.g., elementary/secondary schools, churches, and charitable organizations that are defined as exempt from taxation under the Income Tax Act).

These tax subsidies and rebates would reduce the charge to tax-exempt properties. Although this consideration apparently goes against the benefit that a rate offers a mechanism to allocate charges to tax-exempt properties, it is a reality that will likely need to be addressed during the implementation phase. Feedback from recent discussions with SWAC members in the Kitchener, Waterloo and Stratford rate studies has indicated that stormwater rate charges essentially overlap the PILOT charge and would be double-counting. Similarly, church representatives have requested special recognition in-lieu-of the valuable social and community services they provide, which were downloaded on them by the municipality. The key ingredient is to engage and work with these tax-exempt groups to determine their specific needs and resolve to achieve a balance. Since schools, churches and other such institutions often have significant impervious areas, they represent important opportunities for incentive programs to reduce stormwater runoff and pollutant loading through source controls. Further, given the nature of these properties and the citizenry that they attract, there are many opportunities for educational programs that could be factored into a credit program, rather than resorting to subsidies or rebates.

9. Investigate efficiencies in coordinating SWM services that can be shared by neighboring

municipalities, CVC, TRCA, and the regional governments. Joint initiatives that can offer services on a multi-jurisdictional basis (e.g., operations and maintenance activities, capital projects, and administrative/management services) can help to reduce the overall SWM program costs in individual municipalities. Specific examples include sharing specialized equipment and/or trained personnel, and coordinating local and regional government programs such as integrating the municipality’s pond sediment removal activities with the region’s composting program.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 1

1.0 PROJECT OVERVIEW

This section summarizes the background that led to the present study, outlines the study tasks, and highlights the project organization. 1.1 Background

The ultimate goal of the Credit River Water Management Strategy Update (CRWMSU) was to develop a watershed management strategy that could be used to ensure safe, abundant, clean water for environmentally, socially, economically healthy communities within the Credit River watershed. To achieve this goal, findings from previous Credit Valley Conservation (CVC) initiatives were integrated with the original Credit River Water Management Strategy to refine and adjust the long-term plan for managing the water and environmental resources within the watershed. A major part of this plan was the development of municipal stormwater management (SWM) program enhancements and capital improvement projects that were recommended throughout the watershed. CVC staff and member municipalities have identified program funding as a barrier to the implementation of recommended improvement projects. Among the key recommendations in the CRWMSU final report was the following item (CVC, April 2007, page 250):

“Funding: Initiate the necessary programs/policies to staff and finance a range of new

development, retrofit and restorative measures as recommended in the Strategy and

further determine appropriate program and funding requirements through the

implementation process.”

The report further acknowledged that funds are not presently allocated by the municipalities for many of the recommended programs and improvement projects and as a result, alternative sources of funding would need to be considered. In June 2007, CVC contracted with Totten Sims Hubicki Associates (TSH) to provide an overview of various funding mechanisms employed in North America to support SWM programs and conduct two conceptual financial analyses within the Credit River watershed. 1.2 Study Tasks

In order to achieve the objectives of the CRWMSU Municipal Stormwater Financing Study, a project work plan was developed featuring the following tasks:

• Task I – Stormwater Funding Options: Stormwater funding options that have been used as successful financial models for SWM programs throughout North America were reviewed and evaluated for applicability to CVC member municipalities. The findings of this evaluation are presented in Section 2 of this report.

• Task II – Stormwater Rate Framework: To help set the framework for stormwater rates in the CVC municipalities, a working session with the CRWMSU Management Steering Group was held to confirm goals and objectives for the conceptual stormwater rate analysis and explore related issues generated by the participants. Section 1.3 describes this workshop.

• Task III – Case Studies: Representative case studies of stormwater rate implementations in communities that best reflect the needs and issues of CVC member municipalities were illustrated. Case studies from recent stormwater rate studies in Ontario are included along with a description of the overall lessons learned in Section 3 of this report.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 2

• Task IV – Initial Program Definition: A conceptual stormwater rate analysis was conducted for two selected CVC member municipalities to explore rate structure options and establish preliminary revenue expectations. The results of this analysis are presented in Section 4 of this report.

• Task V – Reporting: This report documents the results and findings of Tasks I-IV described above. The overall conclusions and recommendations for this study are described in Section 5. In addition to the report, follow-up presentations to the CRWMSU Management Steering Group and CVC Board of Directors are planned.

1.3 Project Organization and Highlights

The project team comprised members of the consultant team and CVC staff, who met regularly to consider results of the rate study analysis as well as feedback from meetings with staff at CVC member municipalities. The consulting team acted under the direction of CVC project team staff which included:

• Christine Zimmer, Senior Water Resources Engineer

• John Kinkead, Director, Water Resources (Team 2) The project Advisory Committee was composed of the following individuals:

• Wendy Alexander, Director of Transportation and Infrastructure Planning, City of Mississauga

• Lincoln Kan, Manager of Environmental Services, City of Mississauga

• Jack Tupling, Public Works Director, Town of Orangeville

• Doug Jones, Director of Environmental and Development Services, Town of Orangeville

• Chris Mills, Manager of Engineering Design and Development, Town of Halton Hills

• Andrew Pearce, Manager of Engineering and Construction, Town of Caledon

• Rick Bino, Director of Engineering and Development Services, City of Brampton The consultant team included the following firms:

• Totten Sims Hubicki Associates Ltd. (TSH). TSH was the lead firm, responsible for the overall project management, data collection and management, and technical analyses performed by the consultant team. TSH has completed numerous projects and studies throughout Ontario including SWM policy development, stormwater inventory and drainage assessments, rate studies, and creek and pond rehabilitation projects.

• Camp Dresser & McKee, Inc. (CDM). CDM provided technical oversight for the stormwater financing and implementation plan. CDM has established itself as a leader in the development and implementation of stormwater rates, having conducted stormwater financing studies for over 140 communities in the U.S.

Among the project highlights were a number of meetings held with project team staff and representatives of CVC member municipalities. The purpose of the meetings was to discuss their unique SWM needs and issues, stormwater funding options that would be most appropriate for the individual communities, and related topics. The key meetings included:

• A kickoff workshop was held June 11, 2007 at the CVC office, attended by the project team and representatives of the Town of Orangeville, City of Brampton, Town of Halton Hills, and City of Mississauga.

• A working session was held July 4, 2007 at the Town of Orangeville.

• An information session was held July 9, 2007 at the Town of Caledon.

• A working session was held July 26, 2007 at the City of Mississauga.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 3

• Follow-up meetings and phone discussions with Orangeville and Mississauga staff from October through December, 2007.

• An interim report review meeting was held January 16, 2008 at the City of Mississauga.

• An interim report review meeting was held January 24, 2008 at CVC with the Town of Orangeville.

• A draft report review meeting was held April 18, 2008 at CVC with the Town of Orangeville and the City of Mississauga.

Table 1-1 summarizes basic demographic and land area information for the various CVC member municipalities. For each municipality, the upper tier municipality is given along with the latest census population from 2006, the growth rate (i.e., change in population from the last census in 2001), the population density in people per square kilometre, total land area and the percentage of land area within the CVC watershed. As described in Section 4, Orangeville and Mississauga were selected for a financial analysis of their respective SWM programs and these communities are highlighted in Table 1-1.

Table 1-1: Characteristics of CVC Member Municipalities

Municipality

Upper Tier

Municipality

Population

(2006)

Population Change,

2001-2006

Population

Density

(per km2)

Total Land

Area (km2)

Land Area Within CVC

Watershed

Township of Amaranth Dufferin County 3,845 3% 15 264 2%

City of Brampton Peel Region 433,806 33% 1,627 267 48%

Town of Caledon Peel Region 57,050 13% 83 687 45%

Township of East Garafraxa Dufferin County 2,389 8% 14 166 20%

Town of Erin Wellington County 11,148 1% 38 297 46%

Town of Halton Hills Halton Region 55,289 15% 200 276 53%

City of Mississauga Peel Region 668,549 9% 2,317 289 32%

Town of Mono Dufferin County 7,071 2% 26 278 6%

Town of Orangeville Dufferin County 26,925 7% 1,729 16 100%

Total 1,266,072 17% 499 2,539 35%

Notes:

1. Communities selected for financial analysis are highlighted.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 4

2.0 STORMWATER FUNDING MECHANISMS

This section identifies the options and available funding sources that have been used to support municipal SWM programs throughout North America. In addition, the advantages and disadvantages of the various stormwater funding options that meet the needs of CVC member municipalities are discussed.

2.1 Municipal Stormwater Management Programs

Stormwater management involves controlling the quantity and quality of runoff resulting from rainfall. Urbanization dramatically changes the runoff response characteristics of natural land surfaces and a variety of problems can result when stormwater systems and facilities are not properly managed. Stormwater problems are most evident in areas that are prone to chronic flooding or erosion, but less discernible are the long-term impacts to water quality, stream stability, and the environment in general. Stormwater management systems represent valuable public assets that provide a number of benefits for many users. A municipality’s SWM system includes watercourses, culverts, bridges, storm sewers, swales, catchbasins, inlets, outfalls, ponds and other water quality treatment devices. By controlling floodwaters and preventing pollutants from reaching our streams, rivers and lakes, SWM systems can protect the health and safety of the public and the environment as well as minimize flooding and erosion threats to public and private property. In so doing, clean and healthy water resources support public drinking water supplies and can attract local investment through increased land values. Furthermore, clean and healthy water resources can support recreational activities, tourism, business and manufacturing, as well as aquatic and terrestrial habitats that rely on water. Municipal stormwater management refers to all of the services provided by a local unit of government to properly and effectively manage stormwater within the community (i.e., collect, convey, transport, store, treat, and discharge to a downstream receiving waterbody or waterbodies). A typical municipal SWM program includes a number of components as illustrated in Figure 2-1, including:

• Design, permitting, and construction of new capital improvement projects;

• Operation and maintenance of SWM facilities;

• Asset management, valuation, and planning;

• Rehabilitation, renewal, retrofit, reconstruction or upgrade of existing facilities;

• Emergency response, recovery, and clean-up for flooding events, system failures (e.g., pipe collapses, streambank slope instabilities), spills and other water quality violations;

• Engineering and support services for review and regulation of proposed developments, inspection, monitoring, environmental compliance programs, record maintenance and document management;

• Support for public education and community involvement programs; and

• Administration, staffing, computer resources, equipment, etc., including enforcement of by-laws and detection of illicit discharges and cross-connections.

In general, municipalities are responsible for managing all aspects of stormwater within their jurisdiction, including operations and maintenance (O&M) of SWM facilities located within the public right-of-way limits or easements. The municipality does not maintain facilities that are located on private property, within regional or provincial road rights-of-way, or that fall under the jurisdiction of another governmental authority, such as CVC.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 5

StormwaterStormwaterManagementManagement

Public InvolvementPrograms

Capital Projects

Administration / Enforcement

Finance

EmergencyResponse

Operations / Maintenance

Engineering /Support Services

Figure 2-1: Components of a Stormwater Management System

Municipal ownership and operation of SWM facilities constructed by a developer are typically included as part of the formal assumption of a subdivision. This process includes an initial warranty period (i.e., typically a minimum of one year after the Municipality has issued preliminary inspection approval) in which the developer must maintain all SWM facilities, outfall structures, channel works and appurtenances. A final inspection by municipal staff is conducted to certify that all SWM facilities and related services are in a condition satisfactory to the Municipality’s standards for assumption. Once the Municipality’s financial requirements have been met (e.g., payments to cover any future anticipated maintenance or other costs associated with the assumption), formal municipal ownership of the SWM facilities begins upon Council resolution (through bylaw) that all conditions of the Subdivision Agreement and approved Engineer Plans have been fulfilled and all maintenance requirements have been completed. Stormwater problems can generally be classified into the categories listed below.

Flooding: This is probably the most visible of stormwater problems. Serious flooding presents a threat to public safety and can damage public and private property, disrupt business, and otherwise hamper normal activities within a community. Stormwater management facilities are designed to safely collect, convey or store runoff as a result of rainfall and snowmelt events. However, the recurrence frequency of these events is subject to change as a result of climate variability. During frequent rainfall events, runoff is collected in the minor system of storm sewers, swales, and roadside ditches. During the rare events in which the minor system capacity is exceeded, runoff is also conveyed through the major system that includes curb and gutter drainage in the public road right-of-way and other surface overland flow routes and storage in detention facilities or floodplain areas.

Water quality: Road salt, chemical spills, sediment and organic debris can all degrade water quality, impacting the natural environment including aquatic and terrestrial habitat as well as affecting drinking water supplies. Stormwater management systems are designed to improve the water quality of discharge of urban runoff

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 6

to receiving waterbodies, but need to be properly planned, constructed, operated, and maintained in order to do so.

Erosion: Water traveling over a bare or unprotected surface will erode the soil material, increasing sediment loads in the watercourse and also threatening the stability of the streambank and can jeopardize both public and private property if not addressed properly. Stormwater management systems are also designed to control the movement of stormwater in such a way as to minimize the erosion of streambanks, adjacent hill slopes and exposed structures.

Debris: During rainfall events, debris, trash and other deleterious material on land surfaces can be transported through the SWM system. As a result, this material may create a barrier to flow and increase the flooding potential, or it may flow to downstream watercourses and impact water quality. Routine inspection and maintenance of the stormwater collection system and other facilities, as well as an appropriate emergency response/recovery program is necessary to minimize these problems.

Despite substantial investments in municipal SWM systems and facilities, there will always be a need to invest in new capital improvement projects and to reinvest in the operation, maintenance, planning, and management of the stormwater program. Existing SWM systems may be inadequate for a variety of reasons, including:

Urbanization: Growth and development alters the amount of runoff and pollution discharged into the system. Additional impacts may include the alteration of drainage system characteristics.

Aging

infrastructure:

Pipes, culverts, bridges, pond control structures, hardened streambanks, and outfalls have a limited life expectancy and must be repaired or replaced eventually. Structural deficiencies result when aging infrastructure has exceeded its anticipated service life.

Regulatory

requirements

/design

standards:

Regulatory requirements are always changing (e.g., relaxed design standards due to limited technology, or increased design standards due to more stringent regulatory requirements, new and improved technologies, etc.). As a result, systems designed to previous criteria may be inadequate with respect to current standards. Also, the level of protection to be provided by SWM facilities is often dictated through studies and governing agencies for water quality and habitat protection.

Inadequate

planning

Problems will result if SWM programs do not proactively plan the appropriate resources, measures, and improvement projects to address needs and problems. In addition, facilities and SWM assets must be inventoried and evaluated at regular intervals.

Inadequate

maintenance:

Problems will result if SWM programs do not actively and routinely inspect and operate facilities, maintain watercourses, clean catchbasins and inlets, sweep streets/gutters, collect leaves/debris in and around SWM systems, etc.

Poor design or

faulty

construction:

Development site plans must be properly reviewed and adequately inspected during construction to minimize the potential for hazards.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 7

As noted above, municipal SWM programs represent major public investments, and capital and operating budgets are interrelated with many other municipal services and public works. The SWM programs within CVC municipalities are currently funded primarily through property taxes, with development related capital projects currently funded by development charges. Like other public works, SWM facilities have a specific design capacity and service life, regular O&M needs, and their performance decreases with age and additional demands placed on the system. As a result, stormwater facilities and related infrastructure must be inventoried, assessed, valued, and managed according to sound asset management principals in order to plan an appropriate schedule for replacement, renewal, and rehabilitation. Of all the public works provided by a municipality, SWM services are often the least understood by members of the community. Storm pipes are underground and out of sight, detention facilities and ponds are presumed to be natural features and the function of SWM facilities and practices are not easily recognized. As a result, there is little public awareness of a municipality’s SWM services, program needs, and expenditures. Stormwater management systems often only attract attention during periods of rainfall, particularly when systems fail or rainfall exceeds the design capacity resulting in property or road flooding. Furthermore, property owners have widely varying perceptions concerning how their properties generate stormwater runoff and pollution, since usage of the municipal SWM system is not based on demand like water and sewage systems (e.g., turning on a tap, flushing a toilet). This may result in the misconception that property owners cannot control the discharge of stormwater into the municipal SWM system. Unlike other public works, particularly in comparison to wastewater and potable water systems, SWM regulations and design standards are relatively new and evolving, resulting in many existing SWM systems and facilities that do not meet current federal or provincial requirements for the construction of new facilities and/or long-term maintenance. More stringent federal and provincial requirements for water quality and quantity control are also being proposed, further widening the gap to bring these publicly-owned systems into compliance. Although municipal governments are responsible for managing all aspects of stormwater within their jurisdiction, they have limited flexibility and autonomy in generating revenue (e.g., through taxes, fees, special charges, loans, bonds, grants, fines, private partnerships, etc.). Despite new regulations, there are no new federal or provincial funding sources to achieve them, increasing budgeting pressures. In Ontario, all but a handful of municipalities fund their stormwater programs through property tax revenue, and therefore annual stormwater budgets have to compete with other vital public services. Another element to note is that emergency works are often required which cannot always be foreseen or budgeted appropriately. In cases where the resource requirements placed upon a community far exceed the available resources appropriated by the elected officials, the implementation of capital projects or the extent/frequency of O&M activities, for example, becomes dependent on the availability of funds, rather than based on need. It is expected that competing demands for limited public funds will continue, forcing municipalities to pursue alternative financing mechanisms in order to provide a sustainable SWM program.

2.2 Overview of Funding Mechanisms

To support current and future SWM needs, there are four general mechanisms for funding the major components of a municipal SWM program, including:

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 8

• Taxes, which are mandatory levies authorized by the legislature, collected by a public body, and not related to any specific benefit or government service (i.e., these are for general services to support the public good);

• Fees and special charges, which are payments made to offset the cost of a specific service and payable by those people who benefit from the service;

• Special levies that have specific designations and limitations for usage;

• Other means besides taxes, fees, and special levies; and

• A combination of the above. Table 2-1 shows the funding options that have been used to support all or some portion of municipal SWM programs in North America. Property taxes are the primary source of funding for SWM programs in Ontario. At least three municipalities in Ontario (i.e., London, St. Thomas, and Aurora) have implemented a special stormwater user fee that charges a flat rate to residential properties and an area-based charge to commercial/industrial properties. Other municipalities in Ontario are known to be evaluating various stormwater funding options. There are approximately a dozen municipalities in western Canada that have either adopted a flat rate user free or have implemented a stormwater rate based on zoning and intensity of development. A list of municipalities in Canada that are known to charge a specific fee for stormwater services is included in Section 3.6.

Table 2-1: General Stormwater Program Funding Options

Category/Description Category/Description

Taxes Fees and Special Charges

Local Income Taxes Aquifer Protection Fees

Local Sales Taxes Bond Issuance Fees

Personal (Tangible) Property Taxes Connection Fees

Real (Ad Valorem) Property Taxes Construction Fees

Selective Sales Taxes Developer Charges

State/Provincial Sales and Use Taxes Direct Water Use Charges

Exactions

Impact Fees

Inspection/Monitoring/Testing Fees

Other Means Permitting Fees

Credit Enhancement Mechanisms Professional Certification Fees

Debentures/Bonds Septic System Impact Fees

Fines and Penalties Special Assessments

Grants Stormwater Rates

Loans Tolls

Public-Private Partnership Arrangements Water Rights Application Fees

Water/Wastewater Rates

Well Permit/Pumping Fees Funding opportunities for SWM projects are also possible through grants to municipalities from a variety of governmental sources. Grant programs are often very competitive, based on project merits, and in many cases require matching funds. Grants also tend to be time-limited and not a reliable or sustainable funding source. To be successful, the municipality must therefore be proactive and adequately established to take advantage of the grant program. Communities with an identified revenue stream will be in a better position to compete for and use the grant funds as they become available. Grant funding options include:

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 9

• Earmarked money from the provincial capital budget including direct grants or gas tax revenues allocated to Ontario municipalities.

• Infrastructure investment programs such as the Ontario Rural Infrastructure Investment Initiative (RIII) and the Canada-Ontario Municipal Rural Infrastructure Fund (COMRIF)

• The federal government, through the Federation of Canadian Municipalities (FCM), has established grant funding under the Green Municipal Fund that can be used to support municipal governments and their partners in developing communities that are more environmentally, socially and economically sustainable. Eligible projects may include feasibility studies, field tests, sustainable community plans, and capital projects that demonstrate municipal leadership in sustainable development and serve as examples for other communities.

• Research grants (e.g., through MOE or a federal program such as Natural Sciences and Engineering Research Council of Canada (NSERC), typically in conjunction with a local university or other partners.

An ideal funding source for a municipal SWM program would have the following characteristics:

• Costs are allocated in a fair and equitable manner;

• Provides a sustainable and dedicated funding source to support SWM program needs;

• Applicable for use on a Town-wide or City-wide basis;

• Revenue meets the requirements for the optimum level of service provided and appropriate reserve funding levels are maintained;

• Costs and benefits are equitably distributed, and are transparent and visible across the community;

• Specifically for the case of fees and special charges: sound policies are in place for credits, adjustments and appeals, and rate study recommendations are publicly supported;

• Reasonable implementation costs (e.g., in calculating charges, managing billing systems, and overall administration); and

• Consistent with provincial and federal legislation. As part of this study, a number of meetings were held with CVC member municipalities to discuss the various funding options and those that would be most appropriate for the individual communities. These meetings included:

• June 11, 2007 workshop at the CVC office;

• July 4, 2007 working session at the Town of Orangeville;

• July 26, 2007 working session at the City of Mississauga;

• Follow-up meetings and phone discussions with Orangeville and Mississauga staff from October through December, 2007;

• An interim report review meeting was held January 16, 2008 at the City of Mississauga; and

• An interim report review meeting was held January 24, 2008 at CVC with the Town of Orangeville.

Based on discussions during these meetings, it has been determined that the funding options that are most applicable to CVC member municipalities are:

• Property Tax;

• Development Related Charges and Fees; and

• Stormwater Rate

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 10

2.3 Property Tax

2.3.1 General Tax Fund

Local property taxes are the most significant revenue source to support the SWM programs in CVC member municipalities. Revenue derived from the municipality’s portion of property tax goes into a general fund which covers the operating and capital expenditures of many services across several departments. Table 2-2 show the 2007 property tax rates for various taxable/occupied classes within selected CVC member municipalities.

Table 2-2: 2007 Property Tax Rates

Tax Class

Town of Orangeville

Town of Caledon

City of Mississauga*

Residential 0.74% 0.29% 1.00%

Multi-Residential 1.98% 0.50% 1.58%

Commercial/Office Building/Shopping Centre 0.90% 0.38% 2.60%

Industrial 1.62% 0.43% 2.94% Note: *The Orangeville and Caledon values show local tax rates, Mississauga values also include

the Regional and Education tax rates. Property tax is determined based on the property value assessment multiplied by the applicable tax rate which depends on zoning/building type and taxing status. The municipality also collects tax revenue on behalf of the school boards and the upper tier government (e.g., Peel Region). In this study, only the municipal portion of taxes is considered in the evaluation. The municipality’s portion on the annual property tax bill is calculated as the assessed property value times the corresponding rate by property type shown in Table 2-2. Property tax rates are established on an annual basis by Ontario municipalities to meet their projected funding needs and in consideration of the total Current Value Assessment (CVA) of all taxable properties within their jurisdiction. Furthermore, a number of Ontario municipalities have a capping adjustment program that limits tax payments for selected property types (e.g., Commercial, Industrial and Multi-Residential Properties). Tax-exempt properties generally do not contribute to the municipality’s SWM program. Tax-exempt properties include governmental parcels (e.g., municipal, regional, provincial, and federal buildings) as well as institutional parcels (e.g., schools, hospitals, and churches) and other charitable organizations that are registered with the Canada Revenue Agency and therefore exempt from taxation under the Income Tax Act. Some municipalities charge a core service fee or tax-like payment to tax-exempt properties. For example, the federal government administers the Payments in Lieu of Taxes program which distributes funds on behalf of eligible tax-exempt institutions to property taxing authorities such as CVC member municipalities to compensate for valuable services such as SWM, sanitary sewage collections, water distribution, police protection, fire protection, waste disposal and roads. The Municipal Act authorizes a “heads and beds” charge to institutions (e.g., hospitals, post-secondary schools, and correctional facilities), where payments of $75 per person/year or per bed/year are made under this program. For example, a 400-bed hospital would contribute $30,000 to the local municipality as a payment in lieu of tax.

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 11

2.3.2 Dedicated Tax Levy

A dedicated levy can be administered specifically to raise revenue for stormwater services, such that a fixed property tax rate is applied and itemized on the property owner’s annual tax bill, as is done in other Ontario municipalities for other public services (e.g., Police, Fire, Transit, Local Improvements, etc.). A by-law would be required to dedicate these funds specifically to SWM. With the general tax fund, money to support the SWM program comes from the municipality’s overall tax rate (as shown in Table 2-2) and is not dedicated until the annual budget is set each year. 2.3.3 Advantages and Disadvantages

Funding the municipality’s SWM program through property taxes offers several advantages, including:

• Property-tax-based revenues are already accepted as the primary existing source of revenue for municipalities;

• Can be used to fund all SWM program activities; and

• The billing system is already established for property taxes. Funding the municipality’s SWM program through property taxes offers several disadvantages, including:

• Property taxes are based on a property’s assessed value, which may not equate to its runoff contribution, so the fairness and equity of this revenue source is low;

• It is not a dedicated funding source (except in the case of a dedicated tax levy as described in Section 2.3.2);

• There is an annual competition for general tax funds to support other community services and can therefore prove difficult to sustain the SWM program. For example, funding demands for public safety (e.g., police and fire) and health care decrease the ability of property taxes to support significant increases in other programs (i.e., the SWM program);

• There is no incentive to reduce stormwater runoff and pollutant discharge;

• Tax-exempt properties contribute very little or nothing to support the SWM program; and

• Less effective cash flow with a single annual bill to customers versus monthly billing (e.g., through a stormwater rate as described in Section 4).

2.4 Development Related Charges and Fees

2.4.1 Development Charges

The Ontario Development Charges Act of 1997 authorizes municipalities to pass by-laws for the recovery of costs incurred to provide services to new and re-development projects. Development charges (DC) can only be utilized to fund eligible growth-related capital costs, and only for the services for which they were collected. DC rates are often based on the number of residential dwelling units or the building floor area for non-residential developments. Area-specific DC rates can be charged depending on location. Revenue derived from DC can be applied to projects throughout the municipality. As mentioned above, it is used to cover the capital costs related to growth, which may include the following SWM program components:

• Storm sewers, drainage works and other SWM facilities;

• Erosion control works;

Credit River Water Management Strategy Update – Municipal Stormwater Financing Study 12

• Stream rehabilitation and environmental enhancement structures;

• Engineering services related to managing and administering the capital program; and

• Acquisition and installation of monitoring equipment to observe and evaluate post-construction performance.

2.4.2 Cash-in-lieu Charges

In areas where there is the potential for re-development/infill, and on-site SWM facilities are considered infeasible (e.g., by presenting an undue maintenance burden on the municipality) contributions to off-site SWM facilities can be allocated in the form of a cash-in-lieu policy. Like DC, the rates are based on the area of development (or number of dwelling units) and area-specific rates can be determined for different geographic locations within the community. Unlike DC however, revenue derived from cash-in-lieu charges can be applied to both capital and operations/maintenance costs of SWM facilities.

2.4.3 Subdivision Agreements

Another form of development related charges used in Ontario to fund the municipality’s SWM program is through the use of subdivision agreements. These are one-time agreements for area-specific capital works in new development subdivisions. Cost sharing for joint facilities can also be accommodated. The present value costs of anticipated future operations/maintenance and ongoing monitoring can also be included in the agreement. 2.4.4 Advantages and Disadvantages

Funding the municipality’s SWM program through development related charges offers several advantages, including:

• Accepted by the development community; and

• Charges are based on contributing area, which is more equitable than property value. Funding the municipality’s SWM program through development related charges offers several disadvantages, including: