credit-suisse Quarterly Review Q2/2001

31

CREDIT SUISSE GROUP QUARTERLY REVIEW 2001 Q2

-

Upload

quarterlyearningsreports2 -

Category

Economy & Finance

-

view

280 -

download

0

Transcript of credit-suisse Quarterly Review Q2/2001

CREDIT SUISSE GROUP QUARTERLY REVIEW 2001

Q2

1 Editorial

2 Financial highlights Q2/2001

4 An overview of Credit Suisse Group

8 Review of business units 8 Credit Suisse Financial Services

16 Credit Suisse Private Banking18 Credit Suisse Asset Management 20 Credit Suisse First Boston

23 Consolidated results 23 Income statement24 Balance sheet25 Off-balance sheet business25 Selected notes

Information for investors

CREDIT SUISSE GROUPMedia RelationsKarin Rhomberg Hug, Andreas HildenbrandTel. + 41 1 333 8844 Fax + 41 1 333 8877

Mailing address: P.O. Box 1, 8070 Zurich, Switzerland

Copies of all Credit Suisse Group’s financial publications may be ordered from:

CREDIT SUISSEKIDM 23Uetlibergstrasse 2318070 ZurichSwitzerlandFax + 41 1 332 7294

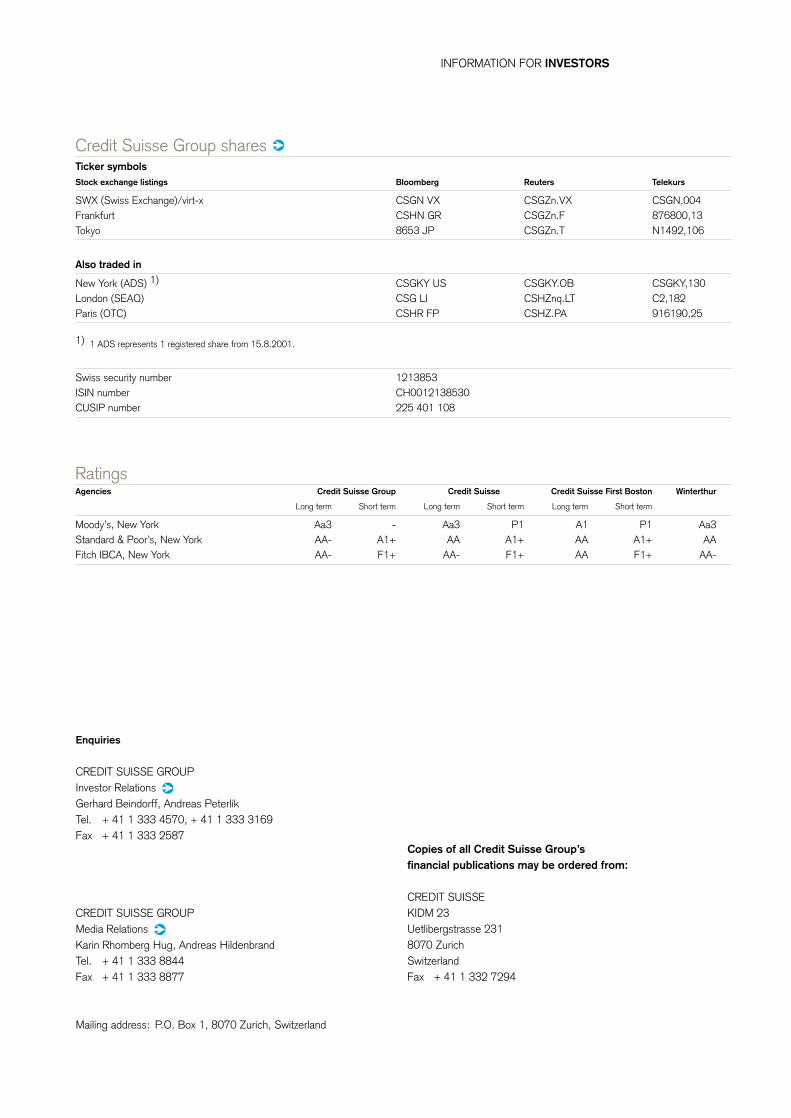

Credit Suisse Group shares Ticker symbolsStock exchange listings Bloomberg Reuters Telekurs

SWX (Swiss Exchange)/virt-x CSGN VX CSGZn.VX CSGN,004Frankfurt CSHN GR CSGZn.F 876800,13Tokyo 8653 JP CSGZn.T N1492,106

Also traded in

New York (ADS) 1) CSGKY US CSGKY.OB CSGKY,130London (SEAQ) CSG LI CSHZnq.LT C2,182Paris (OTC) CSHR FP CSHZ.PA 916190,25

1) 1 ADS represents 1 registered share from 15.8.2001.

Swiss security number 1213853 ISIN number CH0012138530 CUSIP number 225 401 108

RatingsAgencies Credit Suisse Group Credit Suisse First Boston Winterthur

Long term Short term Long term Short term Long term Short term

Moody’s, New York Aa3 - Aa3 P1 A1 P1 Aa3Standard & Poor’s, New York AA- A1+ AA A1+ AA A1+ AAFitch IBCA, New York AA- F1+ AA- F1+ AA F1+ AA-

Credit Suisse

Enquiries

CREDIT SUISSE GROUPInvestor RelationsGerhard Beindorff, Andreas PeterlikTel. + 41 1 333 4570, + 41 1 333 3169Fax + 41 1 333 2587

INFORMATION FOR INVESTORS

This symbol is used to indicate topics on which further information is available on our website. Go to www.credit-suisse.com/q2review2001/bookmarks.html to find links to the relevant information. The additional information indicated is openly accessible and does not form part of the Quarterly Review. Some areas of Credit Suisse Group’s websites are only available in English.

As already stated in the Annual Review 2000 and the Annual Report 2000/2001, Credit Suisse Group changed itsaccounting policies in the year 2000, within the framework of the Swiss Accounting and Reporting Recommendations, in order to increase the transparency for its insurance business and to align its reporting with a more internationally recog-nised standard. The Group’s half-year financial statements as of 30 June 2000 have been restated to conform with the current year’s presentation. The Group’s consolidated financial statements show both the restated (new basis) and the“previously reported” comparative figures for 30 June 2000. For detailed information, please refer to the Annual Report2000/2001, Note 2: Changes to accounting policies.

EDITORIAL

Good performance in the challenging first half of 2001

Lukas MühlemannChairman and Chief Executive Officer

Dear shareholders, clients and fellow employees

Dear readers

With a net operating profit of CHF 1.6billion and a net profit of CHF 1.3 bil-lion in the second quarter of 2001,Credit Suisse Group competed suc-cessfully with its global peers in ademanding market environment. In thefirst half of the year, we reported a netoperating profit of CHF 3.3 billion anda net profit of CHF 2.7 billion, with allbusiness units performing well.

Despite market conditions, theGroup posted a 1% increase in rev-enues over the first quarter and record-ed strong development in net newassets, which amounted to CHF 41.4billion for the first half of 2001. Totalassets under management stood atCHF 1,452.1 billion at end-June, up4.3% compared with year-end 2000.

Progress was also achieved interms of cost reduction, demonstratedby lower personnel expenses as com-pared with the first quarter. These

efforts will be continued throughout theremainder of 2001 and into 2002.

Going forward, we expect theworld’s economic climate and the situa-tion in the global financial markets to be difficult in the third and fourthquarters, affecting our core activities in the areas of asset gathering and in-vestment banking. At the same time,the fundamental soundness of ourglobal business strategy has beenproved even under these conditionsand the Group’s medium- and longer-term prospects are good.

We will continue to focus on provid-ing the best possible service for ourclients, growing our business, increas-ing our productivity, and thus furtherimproving our position in the top tier ofthe world’s leading financial institutions.

Lukas MühlemannChairman and Chief Executive OfficerAugust 2001

www.credit-suisse.com 1

CREDIT SUISSE GROUP FINANCIAL HIGHLIGHTS Q2/2001

Share data 1)

Number of shares issued in millions Shares ranking for dividend in millionsMarket capitalisation in CHF mBook value per share in CHF

Share price (as of 15 August 2001: CHF 71.25) at end of reporting periodhighlow

Average number of shares in millionsEarnings per share in CHFOperating earnings per share in CHF 4)

Earnings per share – diluted, in CHFOperating earnings per share – diluted, in CHF 4)

1) All share-related data have been adjusted for the 4-for-1 share split effective as of 15 August 2001.2) 7.6 m of the shares repurchased were approved for cancellation by the Annual General Meeting on 1 June 2001 and are not ranking for dividend.3) Adjusted for average number of shares repurchased. 4) Excl. amortisation of acquired intangible assets and goodwill.

Change vs.31 Dec. 2000

in %

00

(5 5

Change vs.2000in %

(4 (14(1

Change in %6 months

2001/2000

10(31 (18 (31(18

30 June 2001

1,203.601,196.00

88,29535.76

Q2/2001 in CHF

73.8883.1372.25

Q2/2000

3) 1,095.381.531.571.531.57

)

)))

))))

31 March 2001

1,202.992) 1,202.99

91,52934.56

Q1/2001in CHF

76.3887.0069.75

6 months 2001

1,198.962.272.782.242.76

Q2/2001

1,196.051.081.351.071.33

Q1/2001

3) 1,201.901.191.441.181.42

31 Dec. 2000

1,201.751,201.75

92,53534.08

2000in CHF

77.0097.1373.25

6 months 2000

3) 1,093.113.283.373.273.36

Share performanceSwiss Market Index Credit Suisse Group

19971996 1998 1999 2000 2001

1009080

70

60

50

40

30

20

2

Market capitalisationas of end of reporting period (in CHF bn)

90

100

80

70

50

30

20

60

40

10

0

91 92 93 94 95 96 97 98 99 00 Q2/01

Financial calendar

Third quarter results 2001 Tuesday, 20 November 2001

Investor’s Day Friday, 7 December 2001

Fourth quarter/full-year results 2001 Tuesday, 12 March 2002

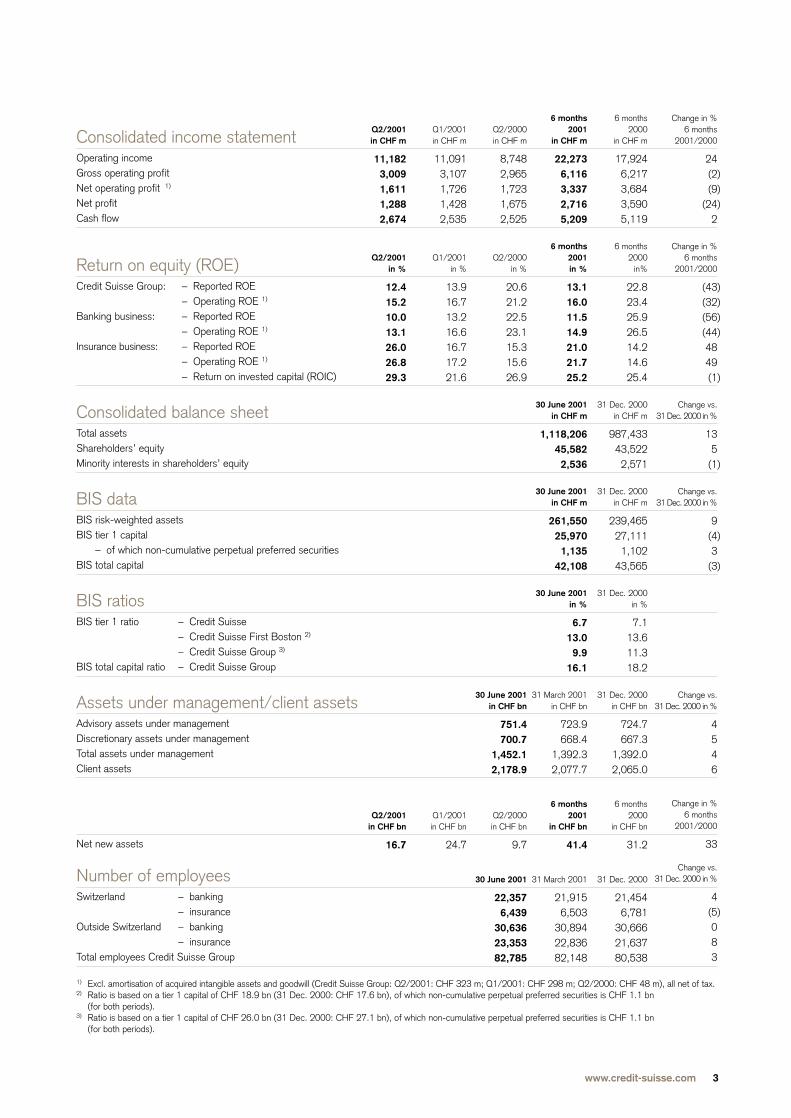

Consolidated income statementOperating incomeGross operating profitNet operating profit 1)

Net profitCash flow

Return on equity (ROE)Credit Suisse Group: – Reported ROE

– Operating ROE 1)

Banking business: – Reported ROE– Operating ROE 1)

Insurance business: – Reported ROE– Operating ROE 1)

– Return on invested capital (ROIC)

Consolidated balance sheetTotal assetsShareholders’ equityMinority interests in shareholders’ equity

BIS dataBIS risk-weighted assets BIS tier 1 capital

– of which non-cumulative perpetual preferred securitiesBIS total capital

BIS ratiosBIS tier 1 ratio – Credit Suisse

– Credit Suisse First Boston 2)

– Credit Suisse Group 3)

BIS total capital ratio – Credit Suisse Group

Assets under management/client assetsAdvisory assets under managementDiscretionary assets under managementTotal assets under managementClient assets

Net new assets

Number of employeesSwitzerland – banking

– insuranceOutside Switzerland – banking

– insuranceTotal employees Credit Suisse Group

1) Excl. amortisation of acquired intangible assets and goodwill (Credit Suisse Group: Q2/2001: CHF 323 m; Q1/2001: CHF 298 m; Q2/2000: CHF 48 m), all net of tax.2) Ratio is based on a tier 1 capital of CHF 18.9 bn (31 Dec. 2000: CHF 17.6 bn), of which non-cumulative perpetual preferred securities is CHF 1.1 bn

(for both periods).3) Ratio is based on a tier 1 capital of CHF 26.0 bn (31 Dec. 2000: CHF 27.1 bn), of which non-cumulative perpetual preferred securities is CHF 1.1 bn

(for both periods).

Change in %6 months

2001/2000

24(2(9

(242

Change in %6 months

2001/2000

(43(32(56(444849(1

Change vs.31 Dec. 2000 in %

135

(1

Change vs.31 Dec. 2000 in %

9(43

(3

Change vs.31 Dec. 2000 in %

4546

Change in %6 months

2001/2000

33

Change vs.31 Dec. 2000 in %

4(5083

)))

))))

)

)

)

)

)

6 months2000

in CHF m

17,9246,2173,6843,5905,119

6 months 2000

in%

22.823.425.926.514.214.625.4

31 Dec. 2000in CHF m

987,43343,5222,571

31 Dec. 2000in CHF m

239,46527,1111,102

43,565

31 Dec. 2000 in %

7.1 13.6 11.3 18.2

31 Dec. 2000in CHF bn

724.7667.3

1,392.02,065.0

6 months2000

in CHF bn

31.2

31 Dec. 2000

21,4546,781

30,66621,63780,538

Q2/2000in CHF m

8,7482,9651,7231,6752,525

Q2/2000in %

20.621.222.523.115.315.626.9

30 June 2001in CHF bn

751.4700.7

1,452.12,178.9

Q2/2000in CHF bn

9.7

30 June 2001

22,3576,439

30,63623,35382,785

6 months2001

in CHF m

22,2736,1163,3372,7165,209

6 months 2001in %

13.116.011.514.921.021.725.2

30 June 2001in CHF m

1,118,20645,5822,536

30 June 2001in CHF m

261,55025,9701,135

42,108

30 June 2001in %

6.713.09.9

16.1

31 March 2001in CHF bn

723.9668.4

1,392.32,077.7

6 months2001

in CHF bn

41.4

31 March 2001

21,9156,503

30,89422,83682,148

Q2/2001in CHF m

11,1823,0091,6111,2882,674

Q2/2001in %

12.415.210.013.126.026.829.3

Q2/2001 in CHF bn

16.7

Q1/2001in CHF m

11,0913,1071,7261,4282,535

Q1/2001in %

13.916.713.216.616.717.221.6

Q1/2001 in CHF bn

24.7

www.credit-suisse.com 3

AN OVERVIEW OF CREDIT SUISSE GROUP

Credit Suisse Group posted a net operating profit of CHF 1.6billion in the second quarter of 2001, representing a 7%decrease compared to the second quarter of 2000 and to thefirst quarter of 2001. Net operating profit for the first half of2001 totalled CHF 3.3 billion, down 9% year-on-year. Assetsunder management grew by 4.3% to CHF 1,452.1 billion sinceyear-end 2000, with a very strong net inflow of new assets ofCHF 41.4 billion (3.0%).

11 0917 984

3 107

483238

2 386

(22

1 773

298

1 475

1 428

1 726

Overview of business unit results

6 months 2001in CHF m

Operating incomeOperating expenses

Gross operating profit

Depreciation and write-offs on non-current assets 1)

Valuation adjustments, provisions and losses 2)

Profit before extraordinary items, taxes 1)

Extraordinary income/(expenses), net Taxes

Net operating profit before minority interests 1)

Amortisation of acquired intangible assets, and goodwill, net of tax

Net profit before minority interests

Minority interests

Net profit

Net operating profit 1)

Value added 3)

Average allocated capitalReturn on average allocated capitalReturn on average allocated capital (operating) 1)

Increased/(decreased) credit-related valuation adjustments 2)

1) Excl. amortisation of acquired intangible assets and goodwill. 2) Increased/decreased valuation adjustments taken at Group level resulting from the difference between the statistical and actual credit provisions.3) Value Added is a measure of value creation in the period under review. It is derived from Credit Suisse Group’s Value Based Analysis (VBA) and complements the per-

formance metrics which are currently used, but does not replace them. The measure is aimed at enhancing the management’s awareness of value creation. For thispurpose, accounting figures are adjusted by adding back accounting distortions such as selected non-cash charges (e.g. amortisation of goodwill), and cost of equity ischarged to the business unit as well as the consolidated accounts.

4) For the Winterthur business units within Credit Suisse Financial Services, average invested capital is used for the calculation of return on invested capital (ROIC).

Credit SuisseGroup

) 22,273) 16,157

6,116

985650

) 4,481

22(1,035

) 3,468

) 621

) 2,847

) (131

) 2,716

) 3,337

) 1,587

)

)

)

)

)

)

)

)

)

Adjustmentsincluding

CorporateCenter

(181(321

140

2049

(73

) 13) 29

(31

(9

(22

(43

(65

(74

(408

CreditSuisse

FirstBoston

13,35811,147

2,211

439390

1,382

) (1) (279

1,102

537

565

0

565

1,102

250

17,2176.6%

12.8%

0

CreditSuisseAsset

Management

794607

187

150

172

(1) (15

156

52

104

) 0

104

156

92

1,265n/an/a

–

CreditSuissePrivate

Banking

3,0811,379

1,702

2685

1,591

3) (362

1,232

8

1,224

) (11

1,213

1,221

1,095

4) 3,3734) n/a4) n/a

) 1

CreditSuisse

FinancialServices

5,2213,345

1,876

301166

1,409

8(408

1,009

33

976

(77

899

932

558

10,88717.9%18.5%

(5

4

0.91.90.7

1.5– 1.11.0

(0.(0.9(0.4

(1.3

Net new assetsCredit Suisse Financial ServicesCredit Suisse Private BankingCredit Suisse Asset Management 2)

Credit Suisse First Boston 3)

Credit Suisse Group

1) Certain restatements have been made to prior period amounts to conform to the current presentation.2) Net new discretionary assets.3) Measured as the balance from accounts opened minus accounts closed.

Assets under management/client assets

Credit Suisse Financial ServicesAssets under management

– of which discretionaryClient assets

Credit Suisse Private BankingAssets under management

– of which discretionaryClient assets

Credit Suisse Asset ManagementAssets under management

– of which discretionaryClient assets

Credit Suisse First Boston 1)

Assets under management– of which discretionary– of which Private Equity on behalf of clients

Client assets

Credit Suisse GroupAssets under management

– of which discretionaryClient assets

Change vs.31 Dec. 2000 in %

1.73.41.5

7.212.76.3

3.33.43.3

3.84.31.67.9

4.35.05.5

Change in %6 months

2001/2000

(3988

(45–

33

31 Dec. 2000in CHF bn

273.8142.6289.6

456.4108.7495.6

487.2360.1487.2

174.655.931.9

792.6

1,392.0667.3

2,065.0

6 months2000

in CHF bn

5.710.914.60.0

31.2

31 March 2001in CHF bn

276.4145.3291.7

463.6110.7502.2

485.4356.7485.4

166.955.732.0

798.4

1,392.3668.4

2,077.7

6 months2001

in CHF bn

3.520.58.0

) 9.4

41.4

30 June 2001in CHF bn

278.4147.5293.8

489.1122.5526.7

503.4372.4503.4

181.258.332.4

855.0

1,452.1700.7

2,178.9

Q2/2000 in CHF bn

0.55.34.3

(0.4

9.7

Q1/2001 in CHF bn

) 4.68.46.84.9

24.7

Q2/2001 in CHF bn

(1.112.11.24.5

16.7

)

)

Credit Suisse Group performed well inthe second quarter of 2001, despite a demanding market environmentwhich contrasted sharply with the posi-tive market developments in 2000.Net operating profit – which excludesthe amortisation of acquired intangibleassets and goodwill – was CHF 1.6billion, representing a decrease of 7%over the second quarter of 2000 andover the first quarter of 2001. CreditSuisse Group’s consolidated secondquarter results include a CHF 100 mil-lion reserve for potential writedowns inthe private equity portfolio.

Net operating profit for the first halfof 2001 amounted to CHF 3.3 billion,down 9% over the first half of 2000.

Taking into account the 4-for-1share split effective 15 August 2001,operating earnings per share for thesecond quarter of 2001 were CHF1.35, compared to CHF 1.57 for thesecond quarter of 2000 and CHF 1.44for the first quarter of 2001. Operatingearnings per share for the first half of2001 decreased to CHF 2.78 fromCHF 3.37 in the first half of 2000.

Net new assets developed verystrongly in the first half of 2001, con-tributing CHF 41.4 billion or 3.0% ofassets under management (CHF 16.7billion or 1.2% in the second quarter).The Group’s total assets under man-agement stood at CHF 1,452.1 billionas of 30 June 2001, an increase of

4.3% since year-end 2000 (4.3%since the end of the first quarter of2001). In the first half of 2001, CreditSuisse Private Banking contributedCHF 20.5 billion (CHF 12.1 billion inthe second quarter of 2001), CreditSuisse Asset Management CHF 8.0billion (CHF 1.2 billion), Credit SuisseFinancial Services CHF 3.5 billion(CHF –1.1 billion) and Credit SuisseFirst Boston CHF 9.4 billion (CHF 4.5billion) to the Group’s net new assets.

Operating income amounted toCHF 11.2 billion for the secondquarter of 2001, representing a 1%increase quarter-on-quarter. Operatingexpenses were up 2% over the firstquarter of 2001, to CHF 8.2 billion,

www.credit-suisse.com 5

AN OVERVIEW OF CREDIT SUISSE GROUP

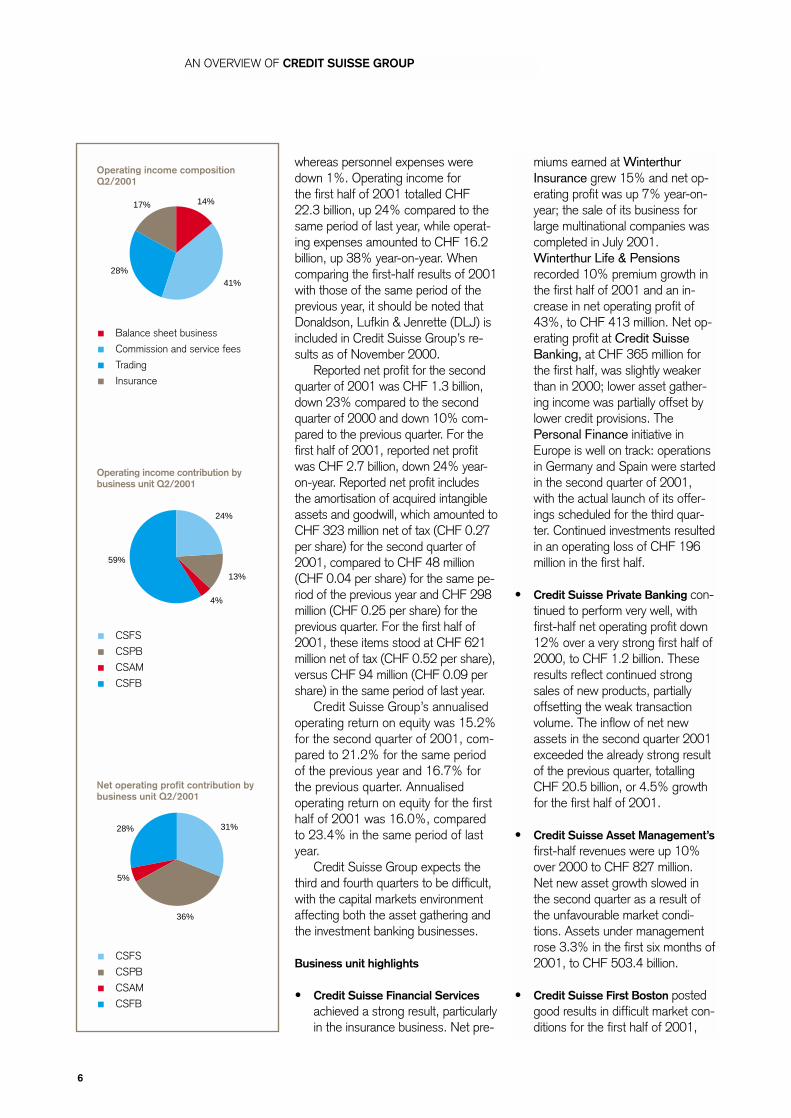

Net operating profit contribution by business unit Q2/2001

CSFS

CSPB

CSAM

CSFB

Operating income composition Q2/2001

Balance sheet business

Commission and service fees

Trading

Insurance

Operating income contribution by business unit Q2/2001

CSFS

CSPB

CSAM

CSFB

36%

5%

31%28%

4%

13%

59%

24%

41%

14%17%

28%

6

whereas personnel expenses weredown 1%. Operating income for the first half of 2001 totalled CHF22.3 billion, up 24% compared to thesame period of last year, while operat-ing expenses amounted to CHF 16.2billion, up 38% year-on-year. Whencomparing the first-half results of 2001with those of the same period of theprevious year, it should be noted thatDonaldson, Lufkin & Jenrette (DLJ) isincluded in Credit Suisse Group’s re-sults as of November 2000.

Reported net profit for the secondquarter of 2001 was CHF 1.3 billion,down 23% compared to the secondquarter of 2000 and down 10% com-pared to the previous quarter. For thefirst half of 2001, reported net profitwas CHF 2.7 billion, down 24% year-on-year. Reported net profit includesthe amortisation of acquired intangibleassets and goodwill, which amounted toCHF 323 million net of tax (CHF 0.27per share) for the second quarter of2001, compared to CHF 48 million(CHF 0.04 per share) for the same pe-riod of the previous year and CHF 298million (CHF 0.25 per share) for theprevious quarter. For the first half of2001, these items stood at CHF 621million net of tax (CHF 0.52 per share),versus CHF 94 million (CHF 0.09 pershare) in the same period of last year.

Credit Suisse Group’s annualisedoperating return on equity was 15.2%for the second quarter of 2001, com-pared to 21.2% for the same periodof the previous year and 16.7% forthe previous quarter. Annualisedoperating return on equity for the firsthalf of 2001 was 16.0%, comparedto 23.4% in the same period of lastyear.

Credit Suisse Group expects thethird and fourth quarters to be difficult,with the capital markets environmentaffecting both the asset gathering andthe investment banking businesses.

Business unit highlights

• Credit Suisse Financial Servicesachieved a strong result, particularlyin the insurance business. Net pre-

miums earned at WinterthurInsurance grew 15% and net op-erating profit was up 7% year-on-year; the sale of its business forlarge multinational companies wascompleted in July 2001.Winterthur Life & Pensionsrecorded 10% premium growth inthe first half of 2001 and an in-crease in net operating profit of43%, to CHF 413 million. Net op-erating profit at Credit SuisseBanking, at CHF 365 million forthe first half, was slightly weakerthan in 2000; lower asset gather-ing income was partially offset bylower credit provisions. ThePersonal Finance initiative inEurope is well on track: operationsin Germany and Spain were startedin the second quarter of 2001,with the actual launch of its offer-ings scheduled for the third quar-ter. Continued investments resultedin an operating loss of CHF 196million in the first half.

• Credit Suisse Private Banking con-tinued to perform very well, withfirst-half net operating profit down12% over a very strong first half of2000, to CHF 1.2 billion. Theseresults reflect continued strongsales of new products, partiallyoffsetting the weak transactionvolume. The inflow of net newassets in the second quarter 2001exceeded the already strong resultof the previous quarter, totallingCHF 20.5 billion, or 4.5% growthfor the first half of 2001.

• Credit Suisse Asset Management’sfirst-half revenues were up 10%over 2000 to CHF 827 million.Net new asset growth slowed inthe second quarter as a result ofthe unfavourable market condi-tions. Assets under managementrose 3.3% in the first six months of2001, to CHF 503.4 billion.

• Credit Suisse First Boston postedgood results in difficult market con-ditions for the first half of 2001,

holding or gaining market share inmost of its segments. Net operat-ing profit for the first six monthswas down 14% over a very strongfirst half of 2000, to CHF 1.1 bil-lion. Quarter-on-quarter resultswere in line with the industry, withrevenues down 7% in US dollarterms and operating expensesdown 6% in US dollar terms. Theprivate equity business recorded a pre-tax loss of CHF 216.8 mil-lion. The book value of the privateequity portfolio stood at CHF 4.4billion as of 30 June 2001. CreditSuisse Group has taken an addi-tional reserve of CHF 100 millionfor further potential writedowns.

• All business units continued to fo-cus on expense control in this diffi-cult market environment, with pro-grammes underway to reduceexpenses over the balance of thisyear and into 2002. Headcount atCredit Suisse First Boston has de-creased by 524 or 2% since theend of March 2001. Personnelcosts at Credit Suisse First Bostonwere reduced by 10% in US dollarterms quarter-on-quarter, and theratio of compensation to operatingincome came down to 57.6% inthe second quarter of 2001, com-pared to 60.6% for the sameperiod in 2000.

New organisation of Credit SuisseGroup as of 2002 On 12 July 2001, Credit Suisse Groupappointed John J. Mack as ChiefExecutive Officer of Credit Suisse FirstBoston and Vice-Chairman of theGroup Executive Board. It also an-nounced that on 1 January 2002,Credit Suisse Asset Management willbe combined with Credit Suisse FirstBoston, and Credit Suisse PrivateBanking with Credit Suisse FinancialServices.

As a result, Credit Suisse Groupwill be comprised of two businessunits, Credit Suisse First Boston andCredit Suisse Financial Services. TheGroup Executive Board will consist of

the following members: LukasMühlemann (Chairman and ChiefExecutive Officer), Hans-Ulrich Doerig(Vice-Chairman of the GroupExecutive Board and Chief RiskOfficer), John J. Mack (Vice-Chairmanof the Group Executive Board andChief Executive Officer of CreditSuisse First Boston), Thomas Wellauer(Chief Executive Officer of CreditSuisse Financial Services) and PhilipK. Ryan (Chief Financial Officer).

Following the reorganisation, CreditSuisse Group will report its results in aformat consistent with that used previ-ously. Within Credit Suisse FirstBoston, investment banking and assetmanagement activities will be shownseparately. Credit Suisse FinancialServices plans to show segmented re-sults for retail and corporate banking in Switzerland, worldwide private bank-ing, personal financial services foraffluent clients in Europe, the life andpensions business as well as for non-life insurance.

The integration of Credit SuissePrivate Banking into Credit SuisseFinancial Services is expected to resultin substantial cost savings andsynergies. Further details will be forth-coming as plans develop during thebalance of the current year.

Change in Board of DirectorsThomas Schmidheiny has announcedhis retirement from Credit SuisseGroup’s Board of Directors in order toconcentrate on his own businessinterests. He first joined the Board ofDirectors of the former SchweizerischeKreditanstalt in 1982, becoming amember of Credit Suisse Group’sBoard in 1989. The Board of Directorsthanks Thomas Schmidheiny for hisvaluable contribution to the success ofthe Group over these many years.

Share repurchase programme As part of its share repurchase pro-gramme approved by the AnnualGeneral Meeting on 1 June 2001, Credit Suisse Group repurchased3,735,000 shares at a par value ofCHF 20 each through a second trad-

ing line on the stock exchange from14 March to 14 August 2001. Thetotal purchase price for these shareswas CHF 1.1 billion and the averageprice per share – prior to the sharesplit on 15 August – was CHF 295.70(CHF 73.92 after the split). Out of thetotal shares repurchased, 1,900,000were cancelled on 10 August, aspreviously approved by the AnnualGeneral Meeting.

www.credit-suisse.com 7

REVIEW OF BUSINESS UNITS

Credit Suisse Financial Services

Thomas WellauerChief Executive Officer

8

Credit Suisse Financial Servicesreported a net operating profit of CHF504 million for the second quarter of2001, up 18% on the first quarter. Netoperating profit for the first half of2001 stood at CHF 932 million, down2% on the strong first half of 2000. Netnew assets totalled CHF 3.5 billion forthe first half year.

Credit Suisse Financial Servicesachieved a strong result in the secondquarter of 2001, particularly in the in-surance businesses, despite the con-

tinuing difficult market environment.Excluding the Credit Suisse PersonalFinance business unit – which is in-vesting heavily in pan-European expan-sion – net operating profit for the firsthalf of 2001 rose 13% to CHF 1.1 bil-lion, corresponding to an annualisedoperating return on average equitycapital of 22.2%.

Winterthur InsuranceIn the first half of 2001, WinterthurInsurance reported a 15% increase innet premiums earned compared with

2 4621 628

834

13186

617

(1168

450

436

4.6145.3

Overview of business area Credit Suisse Financial Services6 months 2001in CHF m

Operating incomeOperating expenses

Gross operating profit

Depreciation and write-offs on non-current assets 2)

Valuation adjustments, provisions and losses 3)

Profit before extraordinary items, taxes 2)

Extraordinary income/(expenses), netTaxes

Net operating profit before minority interests 2)

Amortisation of goodwill, net of tax

Net profit before minority interests

Minority interests

Net profit

Net operating profit 2)

Average allocated capital Return on average allocated capitalReturn on average allocated capital (operating) 2)

Increased/(decreased) credit-related valuation adjustments 3)

Assets under management in CHF bn– of which discretionary

Net new assets in CHF bnClient assets in CHF bn

1) Defined as premiums earned (net), less claims and annuities incurred and expenses for processing claims as well as provisions for future policy benefits, less commissions(net), plus investment income from insurance business; expenses from the handling of both claims and investments are allocated to revenue; personnel expenses WinterthurInsurance: CHF 224 m, Winterthur Life & Pensions: CHF 68 m; operating expenses Winterthur Insurance: CHF 94 m, Winterthur Life & Pensions: CHF 48 m.

2) Excl. amortisation of goodwill.3) Increased/decreased valuation adjustments taken at Group level resulting from the difference between the statistical and actual credit provisions.4) For Winterthur business units, average invested capital is used for calculation of return on invested capital (ROIC).

CreditSuisse

FinancialServices

5,2213,345

) 1,876

301166

) 1,409

) 8(408

) 1,009

33

976

(77

) 899

) 932

10,88717.9%18.5%

(5

278.4147.5

3.5293.8

)

)

)

)

14

)

4)

4)

4)

)

CreditSuisse

PersonalFinance

29240

(211

111

(223

(1) 28

(196

3

(199)

) 0

(199

(196

28n/an/a

) –

6.13.00.76.1

Credit Suisse

Banking

1) 1,9651) 1,2611) 704

55165

484

9) (127

366

5

361

) (1

360

365

4,39416.4%16.7%

(5

130.32.50.1

145.7

Winterthur Life &

Pensions

1) 1,4161) 6951) 721

1580

563

0) (129

434

14

420

) (21

399

413

–

109.4109.4

2.7109.4

6,465 4)

25.2% 4)

26.0% 4)

WinterthurInsurance

1,8111,149

662

770

585

0(180

405

11

394

(55

339

350

–

32.632.6n/a

32.6

eränderungseit

Q1/2000in %

388

42

103

17

15

–

10

10

70

5

19 757 -

12

Winterthur Insurance income statement (non-life business)

Gross premiums writtenReinsurance ceded

Net premiums writtenChange in provision for unearned premiums and in

provision for future policy benefits (health)

Net premiums earnedClaims and annuities incurred, netDividends to policyholders incurred, netOperating expenses, net (incl. commissions paid)

Underwriting result, net

Net investment incomeInterest received on deposits and bank accountsInterest paidOther income/(expenses) (incl. exchange rate differences) 1)

Profit before extraordinary items, taxes 1)

Extraordinary income/(expenses), netTaxes

Net operating profit before minority interests 1)

Amortisation of goodwill

Net profit before minority interests

Minority interests

Net profit

Net operating profit 1)

1) Excl. amortisation of goodwill.2) Incl. a partial recognition of CHF 43 m before tax related to the sale of Winterthur International.

6 months2000

in CHF m

8,736) (993

7,743

) (1,190

6,553) (5,069) (188) (1,960

) (664

1,12646

) (6868

508

0) (144

364

8

356

) (36

320

328

Change in %6 months

2001/2000

27) 5

30

) 115

15) 16) (3) 13

) 14

20(48

) (1(57

15

–) 25

11

38

11

) 53

6

7

V

)

)))

)

2 3

6 months2001

in CHF m

11,113) (1,046

10,067

(2,563

7,504) (5,855) (183) (2,221

) (755

1,35424

) (6729

585

0) (180

405

11

394

) (55

339

350

Q2/2000in CHF m

3,834) (436

3,398

) 70

3,468) (2,668) (94) (1,005

) (299

59423

) (342) 41

325

0) (97

228

4

224

) (26

198

202

Q1/2001in CHF m

6,774) (601

6,173

) (2,556

3,617) (2,799) (112) (1,049

) (343

5297

) (26) 43

210

0) (60

150

5

145

) (17

128

133

Q2/2001in CHF m

4,339(445

3,894

(7

3,887(3,056

(71(1,172

(412

82517

(41(14

375

0(120

255

6

249

(38

211

217

Winterthur Insurance key information(non-life business)

Combined ratio (excl. dividends to policyholders)

Claims ratio

Expense ratio

Assets under management in CHF bn

Technical provisions in CHF m

Number of employees

6 months2001

107.6%

78.0%

29.6%

31 March 2001

32.7

30,132

22,244

Q1/2001

106.4%

77.4%

29.0%

Q2/2000

105.9%

76.9%

29.0%

30 June 2001

32.6

30,339

22,516

Q2/2001

108.8%

78.6%

30.2%

6 months2000

107.3%

77.4%

29.9%

31 Dec. 2000

32.5

26,653

21,796

www.credit-suisse.com 9

REVIEW OF BUSINESS UNITS

19991999

io USD1999

io USD

464

3

Winterthur Life & Pensions income statement(life business)

Gross premiums writtenReinsurance ceded

Net premiums writtenChange in provision for unearned premiums

Net premiums earnedDeath and other benefits incurredChange in provision for future policyholder benefitsDividends to policyholders incurredOperating expenses, net (incl. commissions paid)Net investment incomeInterest received on deposits and bank accountsInterest on bonuses credited to policyholdersOther interest paidOther income/(expenses) (incl. exchange rate differences) 1)

Profit before extraordinary items, taxes 1)

Extraordinary income/(expenses), netTaxes

Net operating profit before minority interests 1)

Amortisation of goodwill

Net profit before minority interests

Minority interests

Net profit

Net operating profit 1)

1) Excl. amortisation of goodwill.

Winterthur Life & Pensions key information (life business)

Expense ratio 1)

Net return on average technical provisions 2)

Net new assets in CHF bn 3)

Assets under management in CHF bn 4)

Technical provisions in CHF m

Number of employees

1) Operating expenses/earned premiums.2) Net profit before minority interests/average technical provisions.3) Based on change in technical provisions for traditional business, adjusted for technical interests; net cash flow unit-linked business; and change in off-balance sheet

business such as funds.4) Based on savings-related provisions for policyholders plus off-balance sheet assets.

6 months2000

in CHF m

8,561) (156

8,405) 0

8,405) (4,908) (4,064) (1,161) (756

3,15044

) (58) (118) (164

370

0) (53

317

7

310

) (28

282

289

Change in %6 months

2001/2000

10) (63

11–

11) 30) (19) (46) 26

(14(16

) 24) (16) (60

52

–) 143

37

100

35

) (25

41

43

in M

in M

)

))

))

))

)

6 months2001

in CHF m

9,376) (58

9,318(11

9,307) (6,373) (3,299) (631) (953

2,71237

) (72) (99) (66

563

0) (129

434

14

420

) (21

399

413

Q2/2000in CHF m

3,340) (61

3,279) 0

3,279) (2,558) (984) (450) (363

1,37822

) (29) (59) (72

164

0) (23

141

4

137

) (14

123

127

Q2/2001in CHF m

3,187(7

3,1803

3,183(2,687(1,205

(228(581

1,91924

(40(62(27

296

0(66

230

9

221

(16

205

214

Q1/2001in CHF m

6,189) (51

6,138(14

6,124) (3,686) (2,094) (403) (372

79313

) (32) (37) (39

267

0) (63

204

5

199

) (5

194

199

6 months2001

10.2%

39 bp

2.7

31 March 2001

107.1

107,390

7,095

Q2/2000

11.1%

15 bp

0.2

30 June 2001

109.4

108,926

7,276

Q1/2001

6.1%

19 bp

2.1

Q2/2001

18.3%

21 bp

0.6

6 months2000

9.0%

35 bp

1.6

31 Dec. 2000

104.7

105,522

6,562

10

the corresponding period of the previ-ous year. All major Market Unitsachieved strong growth rates and anumber of new products werelaunched successfully.

Growth above the industry average,particularly with Churchill in the UK,

as well as rate increases impactedpremium growth. The full consolidationof NIG also contributed to a doubling of premium volume in the UK. Rate in-creases in North America, Germany andBelgium supported double-digit growthin these markets. Excluding the effectsof the NIG acquisition, net premiumsearned grew at 10% compared with thecorresponding period a year earlier.

Despite progress in expensemanagement, the combined ratio roseby 0.3 percentage points to 107.6%in the first half of 2001. This wasdriven by increased loss experience,particularly in North America, where a number of spring storms and un-favourable development in workers’compensation insurance impacted theentire sector.

Net operating profit for the first halfof 2001 stood at CHF 350 million, up7% on the corresponding figure for2000. Due to expected seasonal fac-tors and to higher investment income,net operating profit for the secondquarter of 2001 grew by 63% versusthe previous quarter.

Winterthur Life & PensionsWinterthur Life & Pensions achieved a10% rise in premiums compared withthe first half of 2000. Net new assetsstood at CHF 0.6 billion for the secondquarter and CHF 2.7 billion for the firsthalf of 2001.

Net operating profit rose signifi-cantly to CHF 413 million in the firsthalf of the year, corresponding to a43% increase on the first half of 2000.

The improved core operating per-formance in several countries, as wellas an exceptional after-tax income ofCHF 26 million net related to adjust-ments on the accounts of Winterthur

Life UK following the acquisition ofColonial, contributed to this positiveresult.

During the reporting period,Winterthur Life & Pensions made sig-nificant progress in the implementationof strategic projects and successfullylaunched several new unit-linked prod-ucts for affluent clients in the UK andJapan.

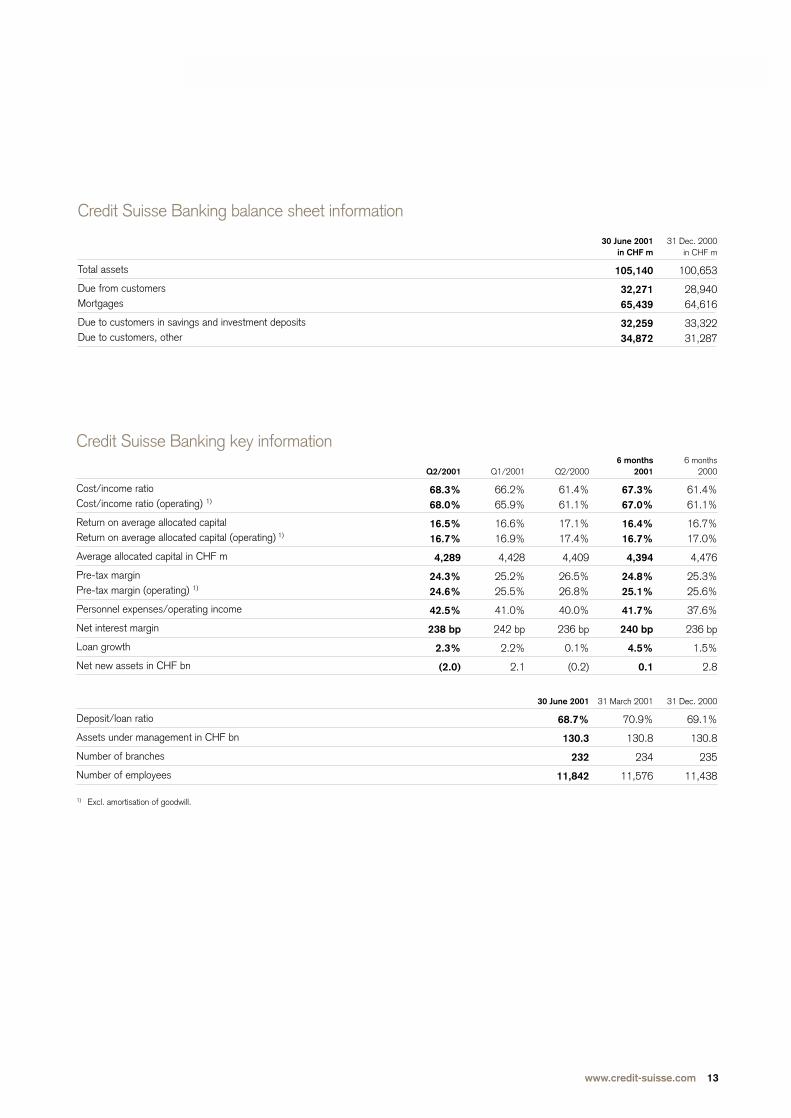

Credit Suisse BankingWith a net operating profit of CHF 365million for the first half of 2001, CreditSuisse Banking was down CHF 14million or 4% on its figure for the previ-ous year. The effects of the challengingmarket environment for asset gatheringrevenues were partially offset by lowercredit charges.

Second-quarter net operating profitdecreased by 5% versus the first quar-ter of 2001. Credit Suisse Banking

saw its operating return on equity de-cline slightly to 16.7%. The operatingcost/income ratio increased from61.1% to 67.0% in the first half of theyear, owing to lower revenue reflectinglower securities commission volume.

Mortgage volumes in the privateclient business recorded an annualisedincrease of 5%. Net new asset growthin the funds business was above aver-age at 11% on an annual basis, de-spite the difficult market environment.Major transactions in corporate clientbusiness resulted in a decrease in netnew assets from CHF 2.1 billion forthe first quarter of 2001 to CHF 0.1billion for the first half. Owing to nega-tive developments in the financial mar-kets, securities commissions dropped50% versus the first half of 2000. Incorporate client business, CreditSuisse Banking increased lendings(excl. mortgages) to customers by

www.credit-suisse.com 11

REVIEW OF BUSINESS UNITS

Credit Suisse Banking income statement 1)

Net interest incomeNet commission and service fee incomeNet trading incomeOther ordinary income

Operating income

Personnel expensesOther operating expenses

Operating expenses

Gross operating profit

Depreciation and write-offs on non-current assets 2)

Valuation adjustments, provisions and losses 3)

Profit before extraordinary items, taxes 2)

Extraordinary income/(expenses), netTaxes 4)

Net operating profit before minority interests 2)

Amortisation of goodwill, net of tax

Net profit before minority interests

Minority interests

Net profit

Net operating profit 2)

Increased/(decreased) credit-related valuation adjustments Tax on amortisation of goodwill

1) Half-year comparative figures have been adjusted to reflect the current business unit reporting structure. 2) Excl. amortisation of goodwill.3) Increased/decreased valuation adjustments taken at Group level resulting from the difference between the statistical and actual credit provisions.4) Excl. tax on amortisation of goodwill

Q2/2000in CHF m

58227985(1

945

378183

561

384

16116

252

1) (61

192

3

189

0

189

192

) (180

Change in %6 months

1) 2001/2000

6(9(8

160

1

122

8

(10

112(42

1

(59) 7

(4

(17

(3

) 0

(3

(4

) ––

))

)

)

)

)

)

)

)

)

6 months 2000

in CHF m

1,16659917710

1,952

734432

1,166

786

26283

477

22) (119

380

6

374

(1

373

379

) (660

6 months2001

in CHF m

1,232544163

) 26

1,965

820441

1,261

704

55165

484

9) (127

366

5

361

(1)

360

365

) (51

Q2/2001in CHF m

6182637922

982

417229

646

336

2279

235

7(63

179

2

177

(1

176

178

281

Q1/2001in CHF m

614281844

983

403212

615

368

3386

249

2) (64

187

3

184

) 0

184

187

(330

18% in the first half of 2001, whilealso further improving the risk structureof its credit portfolio. Credit provisionand losses decreased 42% comparedwith the first half of 2000.

In the second quarter of 2001, thenumber of Direct Net customersgrew by almost 25,000, or 9%, to313,000 (+44% versus the end ofJune 2000). The number of paymentorders executed electronically remainedstable versus the first quarter, totallingapproximately 3 million (+90% com-pared with the second quarter of2000).

12

Credit Suisse Banking balance sheet information

Total assets

Due from customersMortgages

Due to customers in savings and investment depositsDue to customers, other

30 June 2001in CHF m

105,140

32,27165,439

32,25934,872

31 Dec. 2000in CHF m

100,653

28,94064,616

33,32231,287

Credit Suisse Banking key information

Cost/income ratioCost/income ratio (operating) 1)

Return on average allocated capital Return on average allocated capital (operating) 1)

Average allocated capital in CHF m

Pre-tax margin Pre-tax margin (operating) 1)

Personnel expenses/operating income

Net interest margin

Loan growth

Net new assets in CHF bn

Deposit/loan ratio

Assets under management in CHF bn

Number of branches

Number of employees

1) Excl. amortisation of goodwill.

6 months2000

61.4%61.1%

16.7%17.0%

4,476

25.3%25.6%

37.6%

236 bp

1.5%

2.8

31 Dec. 2000

69.1%

130.8

235

11,438

6 months2001

67.3%67.0%

16.4%16.7%

4,394

24.8%25.1%

41.7%

240 bp

4.5%

0.1

31 March 2001

70.9%

130.8

234

11,576

Q2/2000

61.4%61.1%

17.1%17.4%

4,409

26.5%26.8%

40.0%

236 bp

0.1%

(0.2)

30 June 2001

68.7%

130.3

232

11,842

Q1/2001

66.2%65.9%

16.6%16.9%

4,428

25.2%25.5%

41.0%

242 bp

2.2%

2.1

Q2/2001

68.3%68.0%

16.5%16.7%

4,289

24.3%24.6%

42.5%

238 bp

2.3%

(2.0)

www.credit-suisse.com 13

REVIEW OF BUSINESS UNITS

(27

78–

5034

46

24

74(32

33

29

34

285

25

200

25

34 58

59

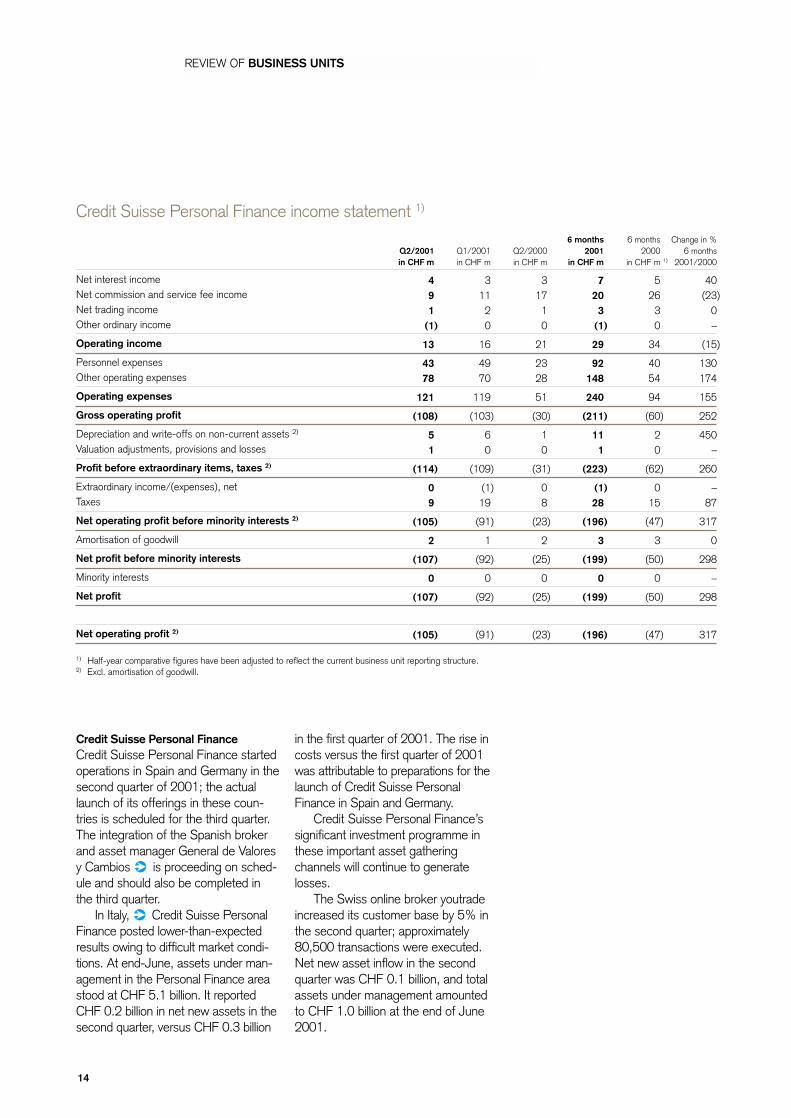

Credit Suisse Personal Finance income statement 1)

Net interest incomeNet commission and service fee incomeNet trading incomeOther ordinary income

Operating income

Personnel expensesOther operating expenses

Operating expenses

Gross operating profit

Depreciation and write-offs on non-current assets 2)

Valuation adjustments, provisions and losses

Profit before extraordinary items, taxes 2)

Extraordinary income/(expenses), netTaxes

Net operating profit before minority interests 2)

Amortisation of goodwill

Net profit before minority interests

Minority interests

Net profit

Net operating profit 2)

1) Half-year comparative figures have been adjusted to reflect the current business unit reporting structure.2) Excl. amortisation of goodwill.

Q2/2000in CHF m

31710

21

2328

51

) (30

10

) (31

) 08

) (23

2

) (25

0

) (25

) (23

Change in %6 months

1) 2001/2000

40(23

0–

(15

130174

155

) 252

450–

) 260

–87

) 317

0

) 298

–

) 298

) 317

)

)

)

6 months2000

in CHF m

5263

) 0

34

4054

94

) (60

20

) (62

) 015

) (47

3

) (50

0

) (50

) (47

6 months 2001

in CHF m

7203

(1

29

92148

240

) (211

111

) (223

(128

) (196

3

) (199

0

) (199

) (196

Q2/2001in CHF m

491

(1

13

4378

121

(108

51

(114

09

(105

2

(107

0

(107

(105

Q1/2001in CHF m

3112

) 0

16

4970

119

) (103

60

) (109

(119

) (91

1

) (92

0

) (92

) (91

Credit Suisse Personal FinanceCredit Suisse Personal Finance startedoperations in Spain and Germany in thesecond quarter of 2001; the actuallaunch of its offerings in these coun-tries is scheduled for the third quarter.The integration of the Spanish brokerand asset manager General de Valoresy Cambios is proceeding on sched-ule and should also be completed inthe third quarter.

In Italy, Credit Suisse PersonalFinance posted lower-than-expectedresults owing to difficult market condi-tions. At end-June, assets under man-agement in the Personal Finance areastood at CHF 5.1 billion. It reportedCHF 0.2 billion in net new assets in thesecond quarter, versus CHF 0.3 billion

14

in the first quarter of 2001. The rise incosts versus the first quarter of 2001was attributable to preparations for thelaunch of Credit Suisse PersonalFinance in Spain and Germany.

Credit Suisse Personal Finance’ssignificant investment programme inthese important asset gatheringchannels will continue to generate losses.

The Swiss online broker youtradeincreased its customer base by 5% inthe second quarter; approximately80,500 transactions were executed.Net new asset inflow in the secondquarter was CHF 0.1 billion, and totalassets under management amountedto CHF 1.0 billion at the end of June2001.

Credit Suisse Personal Finance key information

Personal FinanceGrowth in assets under management

– of which net new assets – of which market movement and structural effects

youtradeNumber of transactions (in ’000s)

Credit Suisse Personal FinanceAverage allocated capital in CHF m

Personal FinanceAssets under management in CHF bnNumber of clientsNumber of advisors

youtradeAssets under management in CHF bnNumber of clients

Credit Suisse Personal FinanceNumber of employees

6 months2000

30.6%31.3%

) (0.7%

234

n/a

31 Dec. 2000

4.817,898

331

0.925,228

764

)

6 months 2001

5.7%10.8%

) (5.1%

189

28

31 March 2001

4.919,381

337

0.927,267

900

Q2/2000

3.7%10.0%

) (6.3%

101

n/a

30 June 2001

5.120,097

407

1.028,656

1,011

Q1/2001

1.4%7.2%

(5.8%

108

32

Q2/2001

4.3%3.5%0.8%

81

29

www.credit-suisse.com 15

REVIEW OF BUSINESS UNITS

Credit Suisse Private Banking

Oswald J. GrübelChief Executive Officer

16

Credit Suisse Private Banking record-ed a net operating profit of CHF 576million in the second quarter of 2001.This 11% decrease on the previousquarter is attributable to lower trans-action volumes and to investments ininformation technology and training,as well as to the expansion of interna-tional business. Net new assetsamounted to CHF 20.5 billion in thefirst half of 2001, up 88% from thesame period of 2000.

At the end of the second quarter2001, Credit Suisse Private Bankingreported CHF 489.1 billion in assetsunder management, an increase of

CHF 32.7 billion or 7.2% over the endof 2000. Of this increase, CHF 20.5billion or 4.5% was attributable to netnew assets. At CHF 12.1 billion, netnew assets for the second quarterwere up 44% on the healthy first quar-ter. Owing to significantly lower trans-action volumes, operating incomedecreased by 5% to CHF 1.5 billionversus the first quarter of 2001. Thisresulted in a 4% drop in operatingincome in the first half of 2001 com-pared with the previous year. The dropin transaction-related commissionincome was partially offset by strongdemand for innovative market-neutralinvestment products.

12

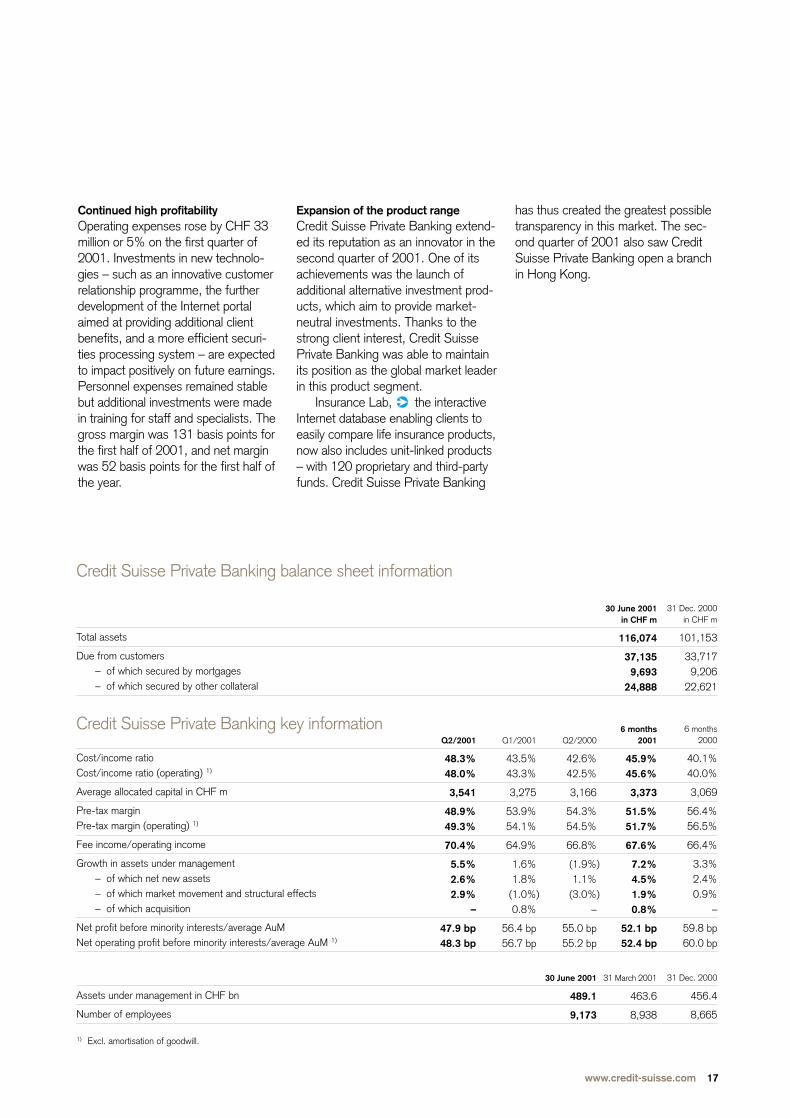

Credit Suisse Private Banking income statement

Net interest incomeNet commission and service fee incomeNet trading incomeOther ordinary income

Operating income

Personnel expensesOther operating expenses

Operating expenses

Gross operating profit

Depreciation and write-offs on non-current assets 1)

Valuation adjustments, provisions and losses 2)

Profit before extraordinary items, taxes 1)

Extraordinary income/(expenses), netTaxes

Net operating profit before minority interests 1)

Amortisation of goodwill

Net profit before minority interests

Minority interests

Net profit

Net operating profit 1)

Increased/(decreased) credit-related valuation adjustments 2)

1) Excl. amortisation of goodwill.2) Increased/decreased valuation adjustments taken at Group level resulting from the difference between the statistical and actual credit provisions.

Q2/2000in CHF m

3191,018

17017

1,524

431204

635

889

1239

838

(8) (181

649

2

647

) (6

641

643

(13

Q1/2001in CHF m

3141,024

161) 80

1,579

436237

673

906

1142

853

1) (202

652

3

649

) (7

642

645

1

Q2/2001in CHF m

2981,058

152(6

1,502

438268

706

796

1543

738

2(160

580

5

575

(4

571

576

0

Change in %6 months

2001/2000

0(2

(2664

(4

030

9

(12

30(18

(13

) –) (12

(12

100

(12

) (27

(12

(12

) –

))

)

)

)

)

)

)

)

)

)

)

6 months2000

in CHF m

6122,128

42145

3,206

874387

1,261

1,945

20104

1,821

(9) (411

1,401

4

1,397

) (15

1,382

1,386

(22

6 months 2001

in CHF m

6122,082

31374

3,081

874505

1,379

1,702

2685

1,591

) 3) (362

1,232

8

1,224

) (11

1,213

1,221

) 1

Continued high profitabilityOperating expenses rose by CHF 33million or 5% on the first quarter of2001. Investments in new technolo-gies – such as an innovative customerrelationship programme, the furtherdevelopment of the Internet portalaimed at providing additional clientbenefits, and a more efficient securi-ties processing system – are expectedto impact positively on future earnings.Personnel expenses remained stablebut additional investments were madein training for staff and specialists. Thegross margin was 131 basis points forthe first half of 2001, and net marginwas 52 basis points for the first half ofthe year.

Expansion of the product rangeCredit Suisse Private Banking extend-ed its reputation as an innovator in thesecond quarter of 2001. One of itsachievements was the launch ofadditional alternative investment prod-ucts, which aim to provide market-neutral investments. Thanks to thestrong client interest, Credit SuissePrivate Banking was able to maintainits position as the global market leaderin this product segment.

Insurance Lab, the interactiveInternet database enabling clients toeasily compare life insurance products,now also includes unit-linked products– with 120 proprietary and third-partyfunds. Credit Suisse Private Banking

has thus created the greatest possibletransparency in this market. The sec-ond quarter of 2001 also saw CreditSuisse Private Banking open a branchin Hong Kong.

Credit Suisse Private Banking balance sheet information

Total assets

Due from customers– of which secured by mortgages– of which secured by other collateral

Credit Suisse Private Banking key information

Cost/income ratioCost/income ratio (operating) 1)

Average allocated capital in CHF m

Pre-tax margin Pre-tax margin (operating) 1)

Fee income/operating income

Growth in assets under management– of which net new assets – of which market movement and structural effects– of which acquisition

Net profit before minority interests/average AuMNet operating profit before minority interests/average AuM 1)

Assets under management in CHF bn

Number of employees

1) Excl. amortisation of goodwill.

31 Dec. 2000in CHF m

101,153

33,7179,206

22,621

6 months2000

40.1%40.0%

3,069

56.4%56.5%

66.4%

3.3%2.4%0.9%

–

59.8 bp60.0 bp

31 Dec. 2000

456.4

8,665

30 June 2001in CHF m

116,074

37,1359,693

24,888

6 months2001

45.9%45.6%

3,373

51.5%51.7%

67.6%

) 7.2%4.5%

) 1.9%0.8%

52.1 bp52.4 bp

31 March 2001

463.6

8,938

Q2/2000

42.6%42.5%

3,166

54.3%54.5%

66.8%

(1.9%1.1%

) (3.0%–

55.0 bp55.2 bp

30 June 2001

489.1

9,173

Q1/2001

43.5%43.3%

3,275

53.9%54.1%

64.9%

1.6%1.8%

(1.0%0.8%

56.4 bp56.7 bp

Q2/2001

48.3%48.0%

3,541

48.9%49.3%

70.4%

5.5%2.6%2.9%

–

47.9 bp48.3 bp

www.credit-suisse.com 17

REVIEW OF BUSINESS UNITS

Credit Suisse Asset Management

18

Phillip M. ColebatchChief Executive Officer

Credit Suisse Asset Management re-ported net operating profit of CHF 88million for the second quarter of 2001,up 29% on the first quarter. Net oper-ating profit for the first half was CHF156 million, up 3% on year. This re-silience in a difficult operating environ-ment has enabled Credit Suisse AssetManagement to continue advancing itsstrategic initiatives.

During the first half of 2001, assetsunder management rose from CHF487.2 billion as of 31 December 2000to CHF 503.4 billion as of 30 June2001, an increase of 3.3%.

Discretionary assets under man-agement rose 3.4% in the first half ofthe year to CHF 372.4 billion (CHF

360.1 billion as of 31 December2000). Of this increase, CHF 8.0 bil-lion or 2.2% was attributable to netnew discretionary assets.

Revenues of CHF 827 million forthe first six months of the year were10% higher than a year ago, primarilydue to the acquisition of DLJ’s AssetManagement Group in November2000. Adjusting for DLJ, revenueswould be down by approximately 2%.Operating expenses were 14% higherthan in the first half of 2000, againalmost entirely due to the DLJ-AMGacquisition. After adjusting for thiseffect, expenses would be running at a similar level to the previous year.

In order to accelerate the develop-ment of its retail business in Europe,

Credit Suisse Asset Management income statement 1)

Management and advisory feesNet mutual fund feesOther revenues 2)

Operating income 2)

Personnel expensesOther operating expenses

Operating expenses

Gross operating profit 2)

Depreciation and write-offs on non-current assets 3)

Valuation adjustments, provisions and losses

Profit before extraordinary items, acquisition impact, taxes

Extraordinary income/(expenses), netTaxes

Net operating profit before acquisition impact, minority interests

Acquisition interest Amortisation of retention payments, acquired intangible assets

and goodwill

Net profit before minority interests

Minority interests

Net profit

Net operating profit 3)

1) Certain reclassifications have been made to prior period amounts to conform to the current presentation.2) Excl. acquisition interest.3) Excl. amortisation of acquired intangible assets and goodwill.

Q2/2000in CHF m

3016810

379

153116

269

110

50

105

) 0) (19

86

9

11

66

0

66

77

Change in %6 months

2001/2000

13292

10

214

14

1

50–

(1

–) (62

12

83

136

(19

–

(19

3

)

)

)

)

6 months 2000

in CHF m

57315226

751

308225

533

218

100

208

) 0) (39

169

18

22

129

0

129

151

6 months2001

in CHF m

57720050

827

372235

607

220

150

205

(1) (15

189

33

52

104

0

104

156

Q2/2001in CHF m

28611029

425

197122

319

106

80

98

0(2

96

8

33

55

0

55

88

Q1/2001in CHF m

2919021

402

175113

288

114

70

107

(1) (13

93

25

19

49

0

49

68

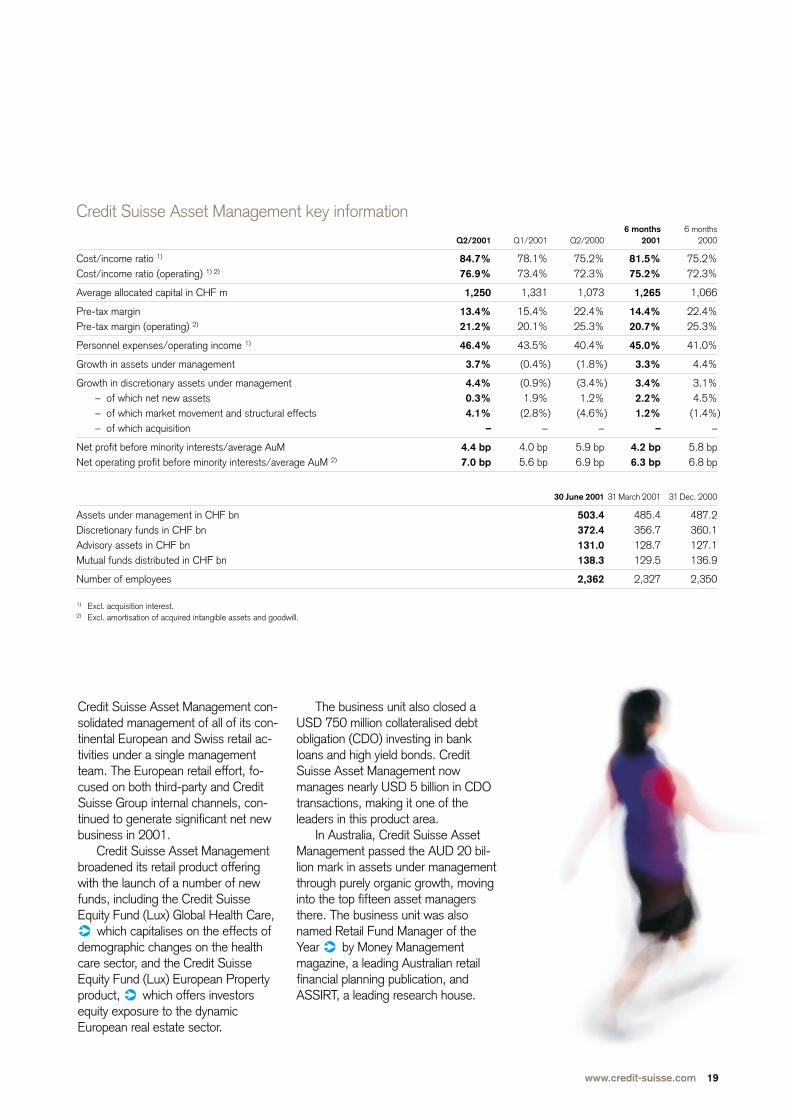

Credit Suisse Asset Management key information

Cost/income ratio 1)

Cost/income ratio (operating) 1) 2)

Average allocated capital in CHF m

Pre-tax marginPre-tax margin (operating) 2)

Personnel expenses/operating income 1)

Growth in assets under management

Growth in discretionary assets under management– of which net new assets– of which market movement and structural effects– of which acquisition

Net profit before minority interests/average AuMNet operating profit before minority interests/average AuM 2)

Assets under management in CHF bnDiscretionary funds in CHF bn Advisory assets in CHF bn Mutual funds distributed in CHF bn

Number of employees

1) Excl. acquisition interest.2) Excl. amortisation of acquired intangible assets and goodwill.

6 months2000

75.2%72.3%

1,066

22.4%25.3%

41.0%

4.4%

3.1%4.5%

(1.4%–

5.8 bp6.8 bp

31 Dec. 2000

487.2360.1127.1136.9

2,350

)

6 months2001

81.5%75.2%

1,265

14.4%20.7%

45.0%

) 3.3%

) 3.4%2.2%

) 1.2%–

4.2 bp6.3 bp

31 March 2001

485.4356.7128.7129.5

2,327

Q2/2000

75.2%72.3%

1,073

22.4%25.3%

40.4%

) (1.8%

) (3.4%1.2%

) (4.6%–

5.9 bp6.9 bp

30 June 2001

503.4372.4131.0138.3

2,362

Q1/2001

78.1%73.4%

1,331

15.4%20.1%

43.5%

(0.4%

(0.9%1.9%

(2.8%–

4.0 bp5.6 bp

Q2/2001

84.7%76.9%

1,250

13.4%21.2%

46.4%

3.7%

4.4%0.3%4.1%

–

4.4 bp7.0 bp

Credit Suisse Asset Management con-solidated management of all of its con-tinental European and Swiss retail ac-tivities under a single managementteam. The European retail effort, fo-cused on both third-party and CreditSuisse Group internal channels, con-tinued to generate significant net newbusiness in 2001.

Credit Suisse Asset Managementbroadened its retail product offeringwith the launch of a number of newfunds, including the Credit SuisseEquity Fund (Lux) Global Health Care,

which capitalises on the effects ofdemographic changes on the healthcare sector, and the Credit SuisseEquity Fund (Lux) European Propertyproduct, which offers investorsequity exposure to the dynamicEuropean real estate sector.

The business unit also closed aUSD 750 million collateralised debtobligation (CDO) investing in bankloans and high yield bonds. CreditSuisse Asset Management nowmanages nearly USD 5 billion in CDOtransactions, making it one of theleaders in this product area.

In Australia, Credit Suisse AssetManagement passed the AUD 20 bil-lion mark in assets under managementthrough purely organic growth, movinginto the top fifteen asset managersthere. The business unit was alsonamed Retail Fund Manager of theYear by Money Managementmagazine, a leading Australian retailfinancial planning publication, andASSIRT, a leading research house.

www.credit-suisse.com 19

REVIEW OF BUSINESS UNITS

Credit Suisse First Boston

John J. MackChief Executive Officer

20

Credit Suisse First Boston’s secondquarter revenues of USD 4.0 billion(CHF 6.8 billion) declined 7%compared to the first quarter. Thebusiness unit remains well posi-tioned with improved market share,although the outlook for the secondhalf appears challenging given theslowdown in the Equity andInvestment Banking divisions.

In the first half of 2001, Credit SuisseFirst Boston’s revenues of USD 8.2billion (CHF 13.8 billion) were up 39%compared to the same period of the

previous year, reflecting the acquisitionof DLJ, which closed in November2000.

Fixed Income Supported by a favourable interest rate environment in the US, the FixedIncome division continued itsstrong performance, producing secondquarter revenues of USD 1.5 billion(CHF 2.6 billion), a 6% decline fromthe record first quarter. Credit marketsrevenues increased substantiallyversus the first quarter, in part led by anumber one ranking in the expanding

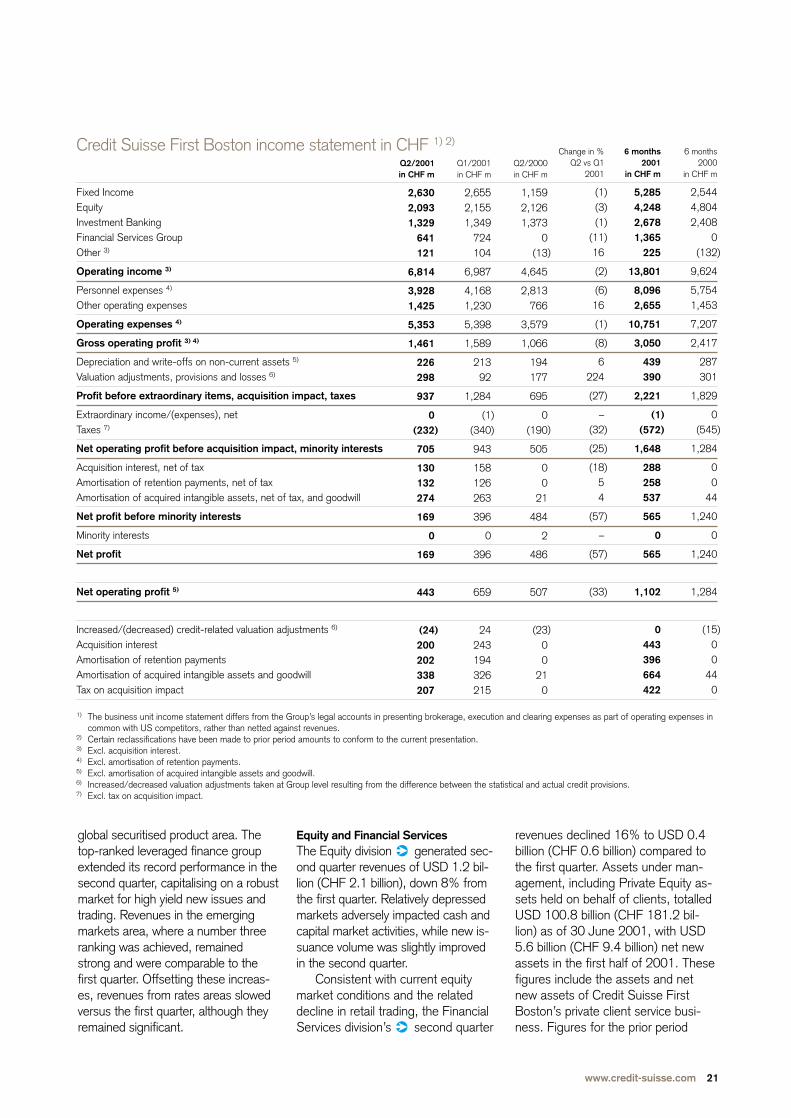

Credit Suisse First Boston income statement in USD 1) 2)

Fixed IncomeEquityInvestment BankingFinancial Services GroupOther 3)

Operating income 3)

Personnel expenses 4)

Other operating expenses

Operating expenses 4)

Gross operating profit 3) 4)

Depreciation and write-offs on non-current assets 5)

Valuation adjustments, provisions and losses 6)

Profit before extraordinary items, acquisition impact, taxes

Extraordinary income/(expenses), netTaxes 7)

Net operating profit before acquisition impact, minority interests

Acquisition interest, net of tax Amortisation of retention payments, net of tax Amortisation of acquired intangible assets, net of tax, and goodwill

Net profit before minority interests

Minority interests

Net profit

Net operating profit 5)

Increased/(decreased) credit-related valuation adjustments 6)

Acquisition interestAmortisation of retention paymentsAmortisation of acquired intangible assets and goodwillTax on acquisition impact

)

)

)

Q2/2000in USD m

7001,284

8350

(7

2,812

1,703464

2,167

645

118108

419

) 0) (114

305

00

13

292

1

293

306

(1400

130

Q1/2001in USD m

1,6201,314

82344262

4,261

2,542750

3,292

969

13056

783

(1) (207

575

9677

160

242

0

242

402

) 15148118198131

Q2/2001in USD m

1,5261,215

77137072

3,954

2,278830

3,108

846

131176

539

0(133

406

7576

160

95

0

95

255

(15116118197120

Change in %Q2 vs Q1

2001

(6(8(6

(16) 16

(7

(1011

(6

(13

1214

(31

–) (36

(29

(22(10

(61

–

(61

(37

)

6 months2000

in USD m

1,5612,9471,478

0(82

5,904

3,530891

4,421

1,483

176185

1,122

) 0) (334

788

00

27

761

0

761

788

(900

270

6 months 2001

in USD m

) 3,146) 2,529) 1,594) 812

134

) 8,215

) 4,8201,580

) 6,400

) 1,815

261232

) 1,322

(1) (340

) 981

) 171) 153

320

) 337

0

) 337

) 657

0264236395251

Credit Suisse First Boston income statement in CHF 1) 2)

Fixed IncomeEquityInvestment BankingFinancial Services GroupOther 3)

Operating income 3)

Personnel expenses 4)

Other operating expenses

Operating expenses 4)

Gross operating profit 3) 4)

Depreciation and write-offs on non-current assets 5)

Valuation adjustments, provisions and losses 6)

Profit before extraordinary items, acquisition impact, taxes

Extraordinary income/(expenses), netTaxes 7)

Net operating profit before acquisition impact, minority interests

Acquisition interest, net of tax Amortisation of retention payments, net of tax Amortisation of acquired intangible assets, net of tax, and goodwill

Net profit before minority interests

Minority interests

Net profit

Net operating profit 5)

Increased/(decreased) credit-related valuation adjustments 6)

Acquisition interestAmortisation of retention paymentsAmortisation of acquired intangible assets and goodwillTax on acquisition impact

1) The business unit income statement differs from the Group’s legal accounts in presenting brokerage, execution and clearing expenses as part of operating expenses incommon with US competitors, rather than netted against revenues.

2) Certain reclassifications have been made to prior period amounts to conform to the current presentation.3) Excl. acquisition interest.4) Excl. amortisation of retention payments.5) Excl. amortisation of acquired intangible assets and goodwill.6) Increased/decreased valuation adjustments taken at Group level resulting from the difference between the statistical and actual credit provisions.7) Excl. tax on acquisition impact.

Q2/2000in CHF m

1,1592,1261,373

0(13

4,645

2,813766

3,579

1,066

194177

695

) 0) (190

505

00

21

484

2

486

507

(2300

210

Change in % Q2 vs Q1

2001

(1(3(1

(11) 16

(2

(616

(1

(8

6224

(27

–) (32

(25

(1854

(57

–

(57

(33

)

6 months 2000

in CHF m

2,5444,8042,408

0(132

9,624

5,7541,453

7,207

2,417

287301

1,829

) 0) (545

1,284

00

44

1,240

0

1,240

1,284

(1500

440

6 months2001

in CHF m

) 5,285) 4,248) 2,678) 1,365

225

) 13,801

) 8,0962,655

) 10,751

) 3,050

439390

) 2,221

(1) (572

) 1,648

) 288258537

) 565

0

) 565

) 1,102

0443396664422

Q2/2001in CHF m

2,6302,0931,329

641121

6,814

3,9281,425

5,353

1,461

226298

937

0(232

705

130132274

169

0

169

443

(24200202338207

Q1/2001in CHF m

2,6552,1551,349

724104

6,987

4,1681,230

5,398

1,589

21392

1,284

(1) (340

943

158126263

396

0

396

659

) 24243194326215

)

)

)

global securitised product area. Thetop-ranked leveraged finance groupextended its record performance in thesecond quarter, capitalising on a robustmarket for high yield new issues andtrading. Revenues in the emergingmarkets area, where a number threeranking was achieved, remainedstrong and were comparable to thefirst quarter. Offsetting these increas-es, revenues from rates areas slowedversus the first quarter, although theyremained significant.

Equity and Financial Services The Equity division generated sec-ond quarter revenues of USD 1.2 bil-lion (CHF 2.1 billion), down 8% fromthe first quarter. Relatively depressedmarkets adversely impacted cash andcapital market activities, while new is-suance volume was slightly improvedin the second quarter.

Consistent with current equitymarket conditions and the relateddecline in retail trading, the FinancialServices division’s second quarter

revenues declined 16% to USD 0.4billion (CHF 0.6 billion) compared tothe first quarter. Assets under man-agement, including Private Equity as-sets held on behalf of clients, totalledUSD 100.8 billion (CHF 181.2 bil-lion) as of 30 June 2001, with USD5.6 billion (CHF 9.4 billion) net newassets in the first half of 2001. Thesefigures include the assets and netnew assets of Credit Suisse FirstBoston’s private client service busi-ness. Figures for the prior period

www.credit-suisse.com 21

REVIEW OF BUSINESS UNITS

31 Dec. 1999in CHF m

439,781

275,224

169,030134,40654,13223,7837,352

122,837

222,80267,1509,536

11069,55031,35712,455

1999

9,925

10,4949.9%

6.7%76.3%

19.0%

15,185

55.0%

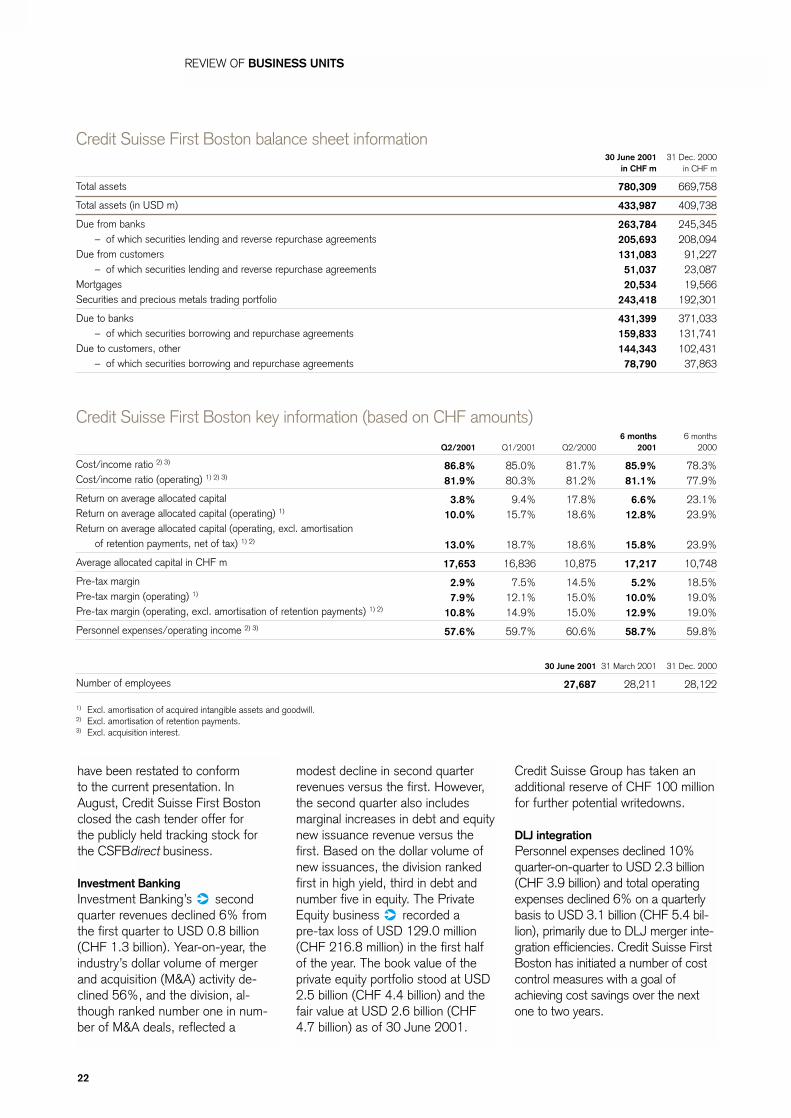

Credit Suisse First Boston balance sheet information

Total assets

Total assets (in USD m)

Due from banks– of which securities lending and reverse repurchase agreements

Due from customers– of which securities lending and reverse repurchase agreements

Mortgages Securities and precious metals trading portfolio

Due to banks– of which securities borrowing and repurchase agreements

Due to customers, other– of which securities borrowing and repurchase agreements

Credit Suisse First Boston key information (based on CHF amounts)

Cost/income ratio 2) 3)

Cost/income ratio (operating) 1) 2) 3)

Return on average allocated capitalReturn on average allocated capital (operating) 1)

Return on average allocated capital (operating, excl. amortisation of retention payments, net of tax) 1) 2)

Average allocated capital in CHF m

Pre-tax margin Pre-tax margin (operating) 1)

Pre-tax margin (operating, excl. amortisation of retention payments) 1) 2)

Personnel expenses/operating income 2) 3)

Number of employees

1) Excl. amortisation of acquired intangible assets and goodwill.2) Excl. amortisation of retention payments.3) Excl. acquisition interest.

31 Dec. 2000in CHF m

669,758

409,738

245,345208,09491,22723,08719,566

192,301

371,033131,741102,43137,863

6 months2000

78.3%77.9%

23.1%23.9%

23.9%

10,748

18.5%19.0%19.0%

59.8%

31 Dec. 2000

28,122

30 June 2001in CHF m

780,309

433,987

263,784205,693131,08351,03720,534

243,418

431,399159,833144,34378,790

6 months2001

85.9%81.1%

6.6%12.8%

15.8%

17,217

5.2%10.0%12.9%

58.7%

31 March 2001

28,211

Q2/2000

81.7%81.2%

17.8%18.6%

18.6%

10,875

14.5%15.0%15.0%

60.6%

30 June 2001

27,687

Q1/2001

85.0%80.3%

9.4%15.7%

18.7%

16,836

7.5%12.1%14.9%

59.7%

Q2/2001

86.8%81.9%

3.8%10.0%

13.0%

17,653

2.9%7.9%

10.8%

57.6%

have been restated to conform to the current presentation. InAugust, Credit Suisse First Bostonclosed the cash tender offer for the publicly held tracking stock for the CSFBdirect business.

Investment Banking Investment Banking’s secondquarter revenues declined 6% fromthe first quarter to USD 0.8 billion(CHF 1.3 billion). Year-on-year, theindustry’s dollar volume of mergerand acquisition (M&A) activity de-clined 56%, and the division, al-though ranked number one in num-ber of M&A deals, reflected a

22

modest decline in second quarterrevenues versus the first. However,the second quarter also includesmarginal increases in debt and equitynew issuance revenue versus thefirst. Based on the dollar volume ofnew issuances, the division rankedfirst in high yield, third in debt andnumber five in equity. The PrivateEquity business recorded a pre-tax loss of USD 129.0 million(CHF 216.8 million) in the first halfof the year. The book value of theprivate equity portfolio stood at USD2.5 billion (CHF 4.4 billion) and thefair value at USD 2.6 billion (CHF4.7 billion) as of 30 June 2001.

Credit Suisse Group has taken anadditional reserve of CHF 100 millionfor further potential writedowns.

DLJ integration Personnel expenses declined 10%quarter-on-quarter to USD 2.3 billion(CHF 3.9 billion) and total operatingexpenses declined 6% on a quarterlybasis to USD 3.1 billion (CHF 5.4 bil-lion), primarily due to DLJ merger inte-gration efficiencies. Credit Suisse FirstBoston has initiated a number of costcontrol measures with a goal ofachieving cost savings over the nextone to two years.

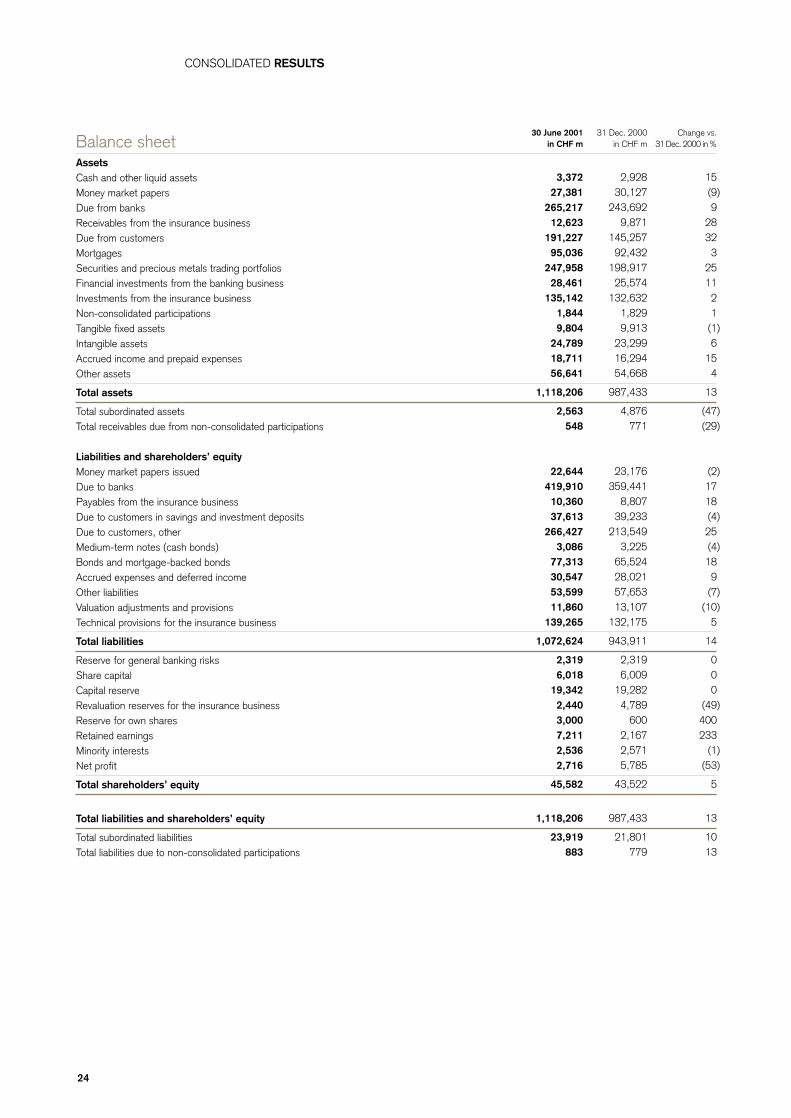

CONSOLIDATED RESULTS

Income statement 1)

Interest and discount incomeInterest and dividend income from trading portfoliosInterest and dividend income from financial investments Interest expenses

Net interest income

Commission income from lending activitiesCommissions from securities and investment transactionsCommissions from other servicesCommission expenses

Net commission and service fee income

Net trading income

Premiums earned, netClaims incurred and actuarial provisionsCommission expenses, netInvestment income from the insurance business

Net income from the insurance business

Income from the sale of financial investmentsIncome from investment activities

– from participations valued according to the equity method– from other non-consolidated participations

Real estate incomeSundry ordinary incomeSundry ordinary expenses

Other ordinary income/(expenses), net

Operating income

Personnel expensesOther operating expenses

Operating expenses

Gross operating profit

Depreciation and write-offs on non-current assetsAmortisation of goodwillValuation adjustments, provisions and losses from the banking business

Depreciation, valuation adjustments, losses

Profit before extraordinary items, taxes and minority interests

Extraordinary incomeExtraordinary expensesTaxes

Net profit before minority interests

Minority interests

Net profit

Net operating profit

1) Certain reclassifications have been made to prior period amounts to conform to the current presentation.2) For details of the changes to accounting policies, see inside cover.

Previouslyreported

6 months2000

in CHF m

11,4951,486

360) (11,010

2,331

3117,450

221) (447

7,535

5,396

13,992) (14,526) (1,061

4,356

2,761

19591771422

358) (841

) (175

17,848

8,9172,798

11,715

6,133

55983

606

1,248

4,885

44) (134) (1,084

3,711

) (101

3,610

3,693

New basis2)

Change in %6 months

2001/2000

2667

(41) 36

22

2315

234) (7

23

28

12) 6) 9

(4

23

251209

10025

(15) 42

) 14

24

3449

38

(2

120279

7

80

(24

21) (78) (17

(23

) 16

(24

(9

)

)

)

)

)

)

))

)

)

)

New basis 2)

6 months2000

in CHF m

13,1293,964

360) (14,872

2,581

3117,741

221) (491

7,782

4,901

14,958) (15,390) (1,038

4,255

2,785

19585751059

602) (1,066

) (125

17,924

8,9182,789

11,707

6,217

62594

606

1,325

4,892