Credit Stress Testing - Framework Uses & Challenges to ...

20

CREDIT STRESS TESTING – FRAMEWORK USES & CHALLENGES TO BANK MANAGEMENT USES & CHALLENGES TO BANK MANAGEMENT Jürgen Wienes Richard Vasicek Group Risk Management Enterprise Risk Solutions UniCredit Group Moody's Analytics Chicago, 16 th October 2012 UniCredit Group Moody s Analytics

Transcript of Credit Stress Testing - Framework Uses & Challenges to ...

CREDIT STRESS TESTING – FRAMEWORKUSES & CHALLENGES TO BANK MANAGEMENTUSES & CHALLENGES TO BANK MANAGEMENT

Jürgen Wienes Richard VasicekGroup Risk Management Enterprise Risk SolutionsUniCredit Group Moody's Analytics

Chicago, 16th October 2012

UniCredit Group Moody s Analytics

Maintainance Of Sustainability & Licence For An Institution:Multiple Factors Demand Sophistacted Usage Of Stress Testing

Regulatory Compliance? Systemic Contagion?g y pSolvency

Systemic Contagion?Source and Victim

Stress Test Analytics

Consistent

Analytics

Resilience To Downturn?L Ab ti C it

Investor Confidence?Loss Absorption Capacity Cost of Capital and Funding

2

Variety and Pace of New Regulations for Banking SystemMany are directed at bank capitalization with need to stress test.

3 Source: McKinsey, BCBS; Dodd-Frank Act; CRD2/3/4; EMIR

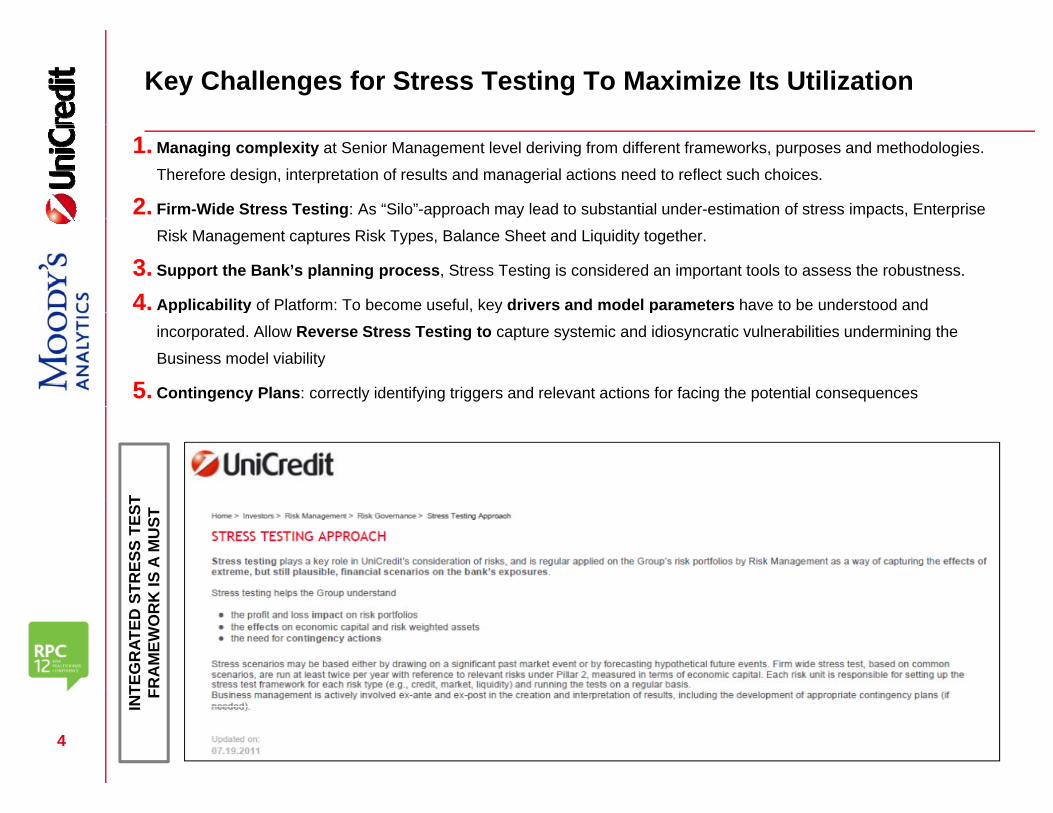

Key Challenges for Stress Testing To Maximize Its Utilization

1. Managing complexity at Senior Management level deriving from different frameworks, purposes and methodologies.

Therefore design, interpretation of results and managerial actions need to reflect such choices.

2. Firm-Wide Stress Testing: As “Silo”-approach may lead to substantial under-estimation of stress impacts, Enterprise

Risk Management captures Risk Types, Balance Sheet and Liquidity together.

3. Support the Bank’s planning process, Stress Testing is considered an important tools to assess the robustness.

4. Applicability of Platform: To become useful, key drivers and model parameters have to be understood and pp y y pincorporated. Allow Reverse Stress Testing to capture systemic and idiosyncratic vulnerabilities undermining the

Business model viability

5. Contingency Plans: correctly identifying triggers and relevant actions for facing the potential consequences

T ST

RES

S TE

STK

IS A

MU

ST

TEG

RAT

ED S

RA

MEW

OR

K

4

INT F

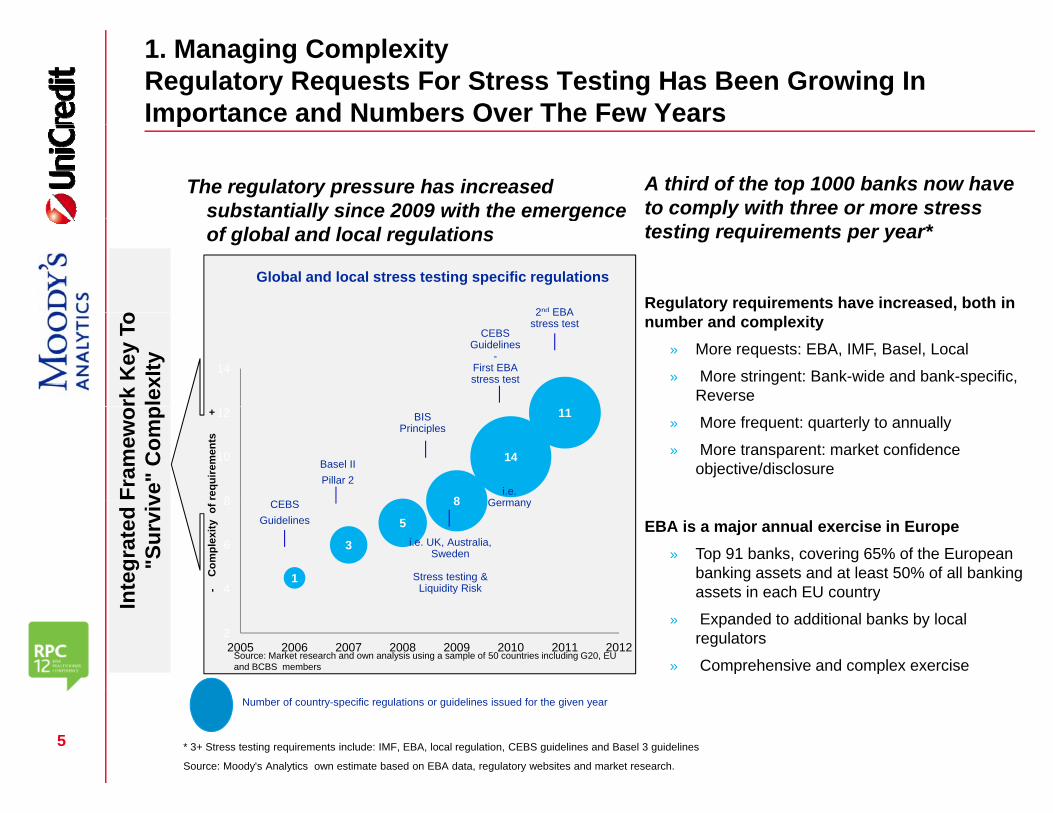

1. Managing ComplexityRegulatory Requests For Stress Testing Has Been Growing In Importance and Numbers Over The Few Yearsp

A third of the top 1000 banks now have to comply with three or more stress

The regulatory pressure has increased substantially since 2009 with the emergence

2nd EBA

Global and local stress testing specific regulations

ytesting requirements per year*

Regulatory requirements have increased, both in

y gof global and local regulations

o

14

CEBSGuidelines

-First EBA stress test

2 EBA stress test number and complexity

» More requests: EBA, IMF, Basel, Local

» More stringent: Bank-wide and bank-specific, Reverserk

Key

To

lexI

ty

8

14

11

8

10

12

requ

irem

ents

+

Basel IIPillar 2

CEBS

BISPrinciples

i.e. Germany

» More frequent: quarterly to annually

» More transparent: market confidence objective/disclosure

Fram

ewo

ve"

Com

p

1

3

5

8

4

6

8

-C

ompl

exity

of CEBS

Guidelines

i.e. UK, Australia, Sweden

Stress testing & Liquidity Risk

Germany

EBA is a major annual exercise in Europe» Top 91 banks, covering 65% of the European

banking assets and at least 50% of all banking assets in each EU countrynt

egra

ted

"Sur

viv

Source: Market research and own analysis using a sample of 50 countries including G20, EU and BCBS members

22005 2006 2007 2008 2009 2010 2011 2012

assets in each EU country

» Expanded to additional banks by local regulators

» Comprehensive and complex exercise

In

5

Number of country-specific regulations or guidelines issued for the given year

* 3+ Stress testing requirements include: IMF, EBA, local regulation, CEBS guidelines and Basel 3 guidelines

Source: Moody's Analytics own estimate based on EBA data, regulatory websites and market research.

1. Managing ComplexityDifferent types and usages of stress testing require a clear strategy for communicating results to Senior Managementg g

Types of Stress Testing

Usage of Stress Testing

Output Recipients of Stress Testing and actions deployment

Major condition

forsuccessfully

Sensitivity Analysis

Scenario Analysis

Regulatory: ICAAPEuropean Stress Test

Capital Adequacy Assessment

SupervisoryAuthority

successfullyintegratingStress Testin Bank’s

management

Reverse Stress Testing

SIFI (SystemicallyImportant Financial Institutions)Other national

Robustness ofBusiness Strategies

Top Management

Need to integrate Other national

regulators’ requests

Managerial: Risk Appetite

Strategies

Contingency Plans Managerial

different results to form a unique view on a Bank’s capital and Risk Appetite

On-going Stress TestFocus on specific sub-portfolios’

ActionsContingency

PlansDeployment

business strategy

soundness

Stress Testing is performed according to different design along intended usages (Regulatory and Managerial). All results need to be successfully and clearly communicated to a Senior Management.

vulnerabilitiesDeployment

6

To improve the communication, all the relevant stakeholder (Top Management and Business) need to be involved in the process, starting from the definition of the scenarios down to the sharing of the output and final decision process.

2. Firm-Wide Stress Testing:From Risk-wide Stress Test to Enterprise Risk ManagementUnderstanding and Capturing the Linkagesg p g g

Loans and Receivables with Banks

Loans and Receivables with

ASSETS

Ri k Wid

Credit Risk

Market Risk

Risk MapLIABILITIES

Deposit From Banks Deposits From

Customers And Debt Securities In Issue Loans and Receivables with

Customers Financial Assets held for

tradingCash and Cash Balances

Financial Investments

Risk-Wide

Integrated

Stress Test

Market Risk

Operational Risk

Financial Investment Risk

Real Estate Risk

Business Risk

Securities In Issue Financial Liabilities

Held For Trading Financial Liabilities

Designated At Fair Value

Hedging InstrumentsP i i F Ri k Financial Investments

Hedging Instruments Property, Plant and

Equipment Goodwill

Oth I t ibl A t

Business Risk Provisions For Risk And Charges

Tax Liabilities Liabilities Included In

Disposal Group Classified As Held For Sale

Many banks performed risk wide S.T. including credit Other Intangible Assets Tax Assets Non-Current Assets and

Disposal Groups Classified as Held For SaleO h A

Sale Other Liabilities Shareholders’ Equity:

Capital and ReservesAvailable-For-Sale Assets Fair Value Reserve and Cash-Flow

risk, market risk, operational risk, but ...

…. risk wide S.T. underestimates the true risk because it does not take into consideration other elements of balance sheet coming from liabilities (e.g. deposits,

Other Assets Hedging ReserveNet Profit (Loss)

Enterprise Risk Management

own bonds,…) and more in general all the liquidity risk elements. (Firm wide S.T.)

Banks have to improve S.T. methodology in order to really capture and manage all kind of risk. Vice versa a

Bank Balance Sheet Structure

Business Strategies vs. change of market trends

Enterprise Risk Managementstress scenario coming from an increase of reputational risk instead of a sovereign default or recessive outlook could affect more on the liquidity side. (The 2009 crisis provides impact both from credit and liquidity side)

7 Firm-Wide Stress Test

and liquidity side).

3. Planning Process:Stress Testing integral part the Bank’s planning process to show robustness of Strategy and Budget-Assumptions

Business Strategy

(Target volumes

P&L Forecasting

“Book Capital”Model common equity

gy g pKey performance indicators

(Target volumes, growth, risk appetite,

target rating, dividend, policy, cost

strategy, M&A,…) Balance Sheet Forecasting

q y(raises/buybacks)

Dividends/Retained earnings

Minority interestsForecasting

Inputs to stress (risk factors)

Minority interests

Sub debt maturing/issuance

Provisions/EL/Deductions

Systemic risk

Macroeconomic

factors)

• Credit drivers (PD, LGD, EAD)

• Losses (€)RegCap

RWA = f (EAD PD LGD)Scenarios(Regulatory/

Business)

Losses (€)

• Liquidity drivers (funding risk, concentration risk…)

• Market Drivers (Interest

RWA = f (EAD, PD, LGD)

ECap(rates, FX, housing prices…)

ECapEC = f (EAD, PD, LGD,

correlations)

Source: Moody's Analytics

8With all that properly defined as objective, where is an institution in its capabilities and what does

the technical platform need to provide differently to the past?

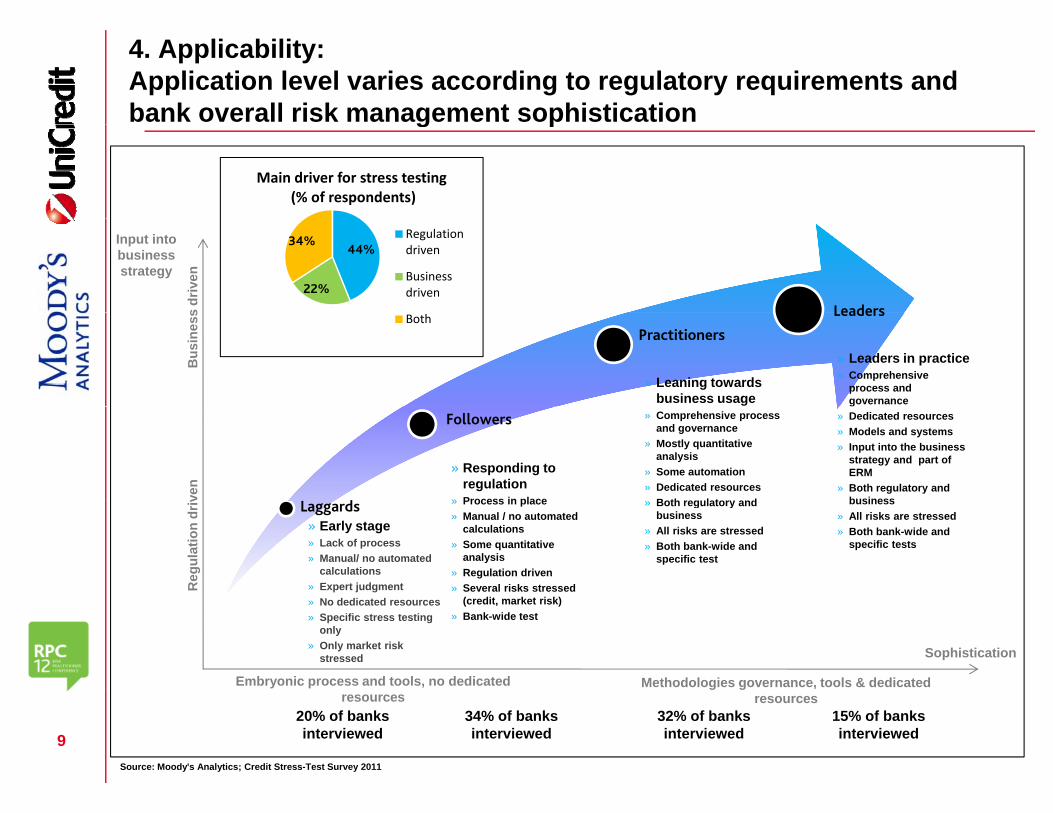

4. Applicability:Application level varies according to regulatory requirements and bank overall risk management sophisticationg p

Main driver for stress testing(% of respondents)

Leaders

Input into businessstrategy

s dr

iven

44%

22%

34% Regulation driven

Business driven

Practitioners

Leaders

» Leaders in practice » Comprehensive

process and governance

» Leaning towards business usage

Bus

ines

s Both

d

Followers » Dedicated resources » Models and systems» Input into the business

strategy and part of ERM

» Both regulatory and business

» Comprehensive process and governance

» Mostly quantitative analysis

» Some automation » Dedicated resources

Both regulatory and

» Responding to regulation

» Process in placeven

Laggards business » All risks are stressed » Both bank-wide and

specific tests

» Both regulatory and business

» All risks are stressed » Both bank-wide and

specific test

» Process in place» Manual / no automated

calculations» Some quantitative

analysis» Regulation driven » Several risks stressed

» Early stage» Lack of process» Manual/ no automated

calculations» Expert judgmentR

egul

atio

n dr

iv

(credit, market risk) » Bank-wide test

» No dedicated resources » Specific stress testing

only » Only market risk

stressed Sophistication

Methodologies governance, tools & dedicated Embryonic process and tools, no dedicated

920% of banks interviewed

34% of banks interviewed

32% of banks interviewed

15% of banks interviewed

g gresources resources

Source: Moody's Analytics; Credit Stress-Test Survey 2011

4. ApplicabilityRecent Trends in Stress Testing in order to overcomePast Shortfalls……

1.Perform portfolio analysis at Group in addition to Business Unit / Asset Class levels in order to

understand cross-correlation effects.

2.Rather than performing analysis in silo by business function, seek to establish linkages between Risk

Management, Portfolio Management, Origination, and Treasury

• Use Stress Testing to understand balance sheet behavior through sensitivities analysisUse Stress Testing to understand balance sheet behavior through sensitivities analysis

• Improve robustness of Fund Transfer Pricing and Liquidity Management through understanding of

spread decomposition (base rate, credit, optionality, margins) and sensitivities to market changes .

33.Rather than analysis performed on a top-down basis only, use Solutions that allows for bottom-up

analysis that will provide opportunities to understand Stress Test Impacts so to:

• Challenge Business Unit Planning by comparing risk / return metrics under varying potential g g y p g y g p

economic conditions in order to ensure resulting impacts are still appropriate to expectations

• Force Senior Management to maintain Oversight of Performance relative to Risk Tolerance

44.Improve upon Model Parameterization that support Stress Testing Programs

• Seek to stress key risk metrics cohesively rather than using an independent approach

• Adopt quantitative in addition to qualitative analysis to derive model risk parameterization

10

Adopt quantitative in addition to qualitative analysis to derive model risk parameterization

• Trend : Tie Model Parameterization to Macro-Economic Indicators to facilitate production of

Plausible Scenarios

4. ApplicabilitySensitivity Analysis - Understand How Resilient Your Balance Sheet Is Under Different Scenarios; Identify Vulnerabilities; y

1.What impact will an adverse scenario have on your RoA, RoE, Earnings, Capital?

2 Financial performance metrics and risk appetite are linked to planning

-25.0% Deviation from Target Value (%) – Annual Forecast

2.Financial performance metrics and risk appetite are linked to planning

-10.0%8 0%

-15.0%

-18.0%

-12.0%

8 0%

-11.0%

-20.0%

-15.0%

-10 0%

CapitalRoE

RoA

-1.0% -1.5%

-7.0%

-2.0%-4.0%-5.0%

-7.0% -8.0%

-4.0%-6.0%

-8.0%10.0%

-5.0%

0.0% Earnings

NPLs

RAROC

4.0%6.0% 5.0%

8.0% 7.0%5.0%

7.5%

5.0%

10.0%

15.0%

23.0%

20.0%

25.0%

30.0%

Recovery - 1/10 Mild - 1/25 Severe - 1/50 Extreme - 1/80

11

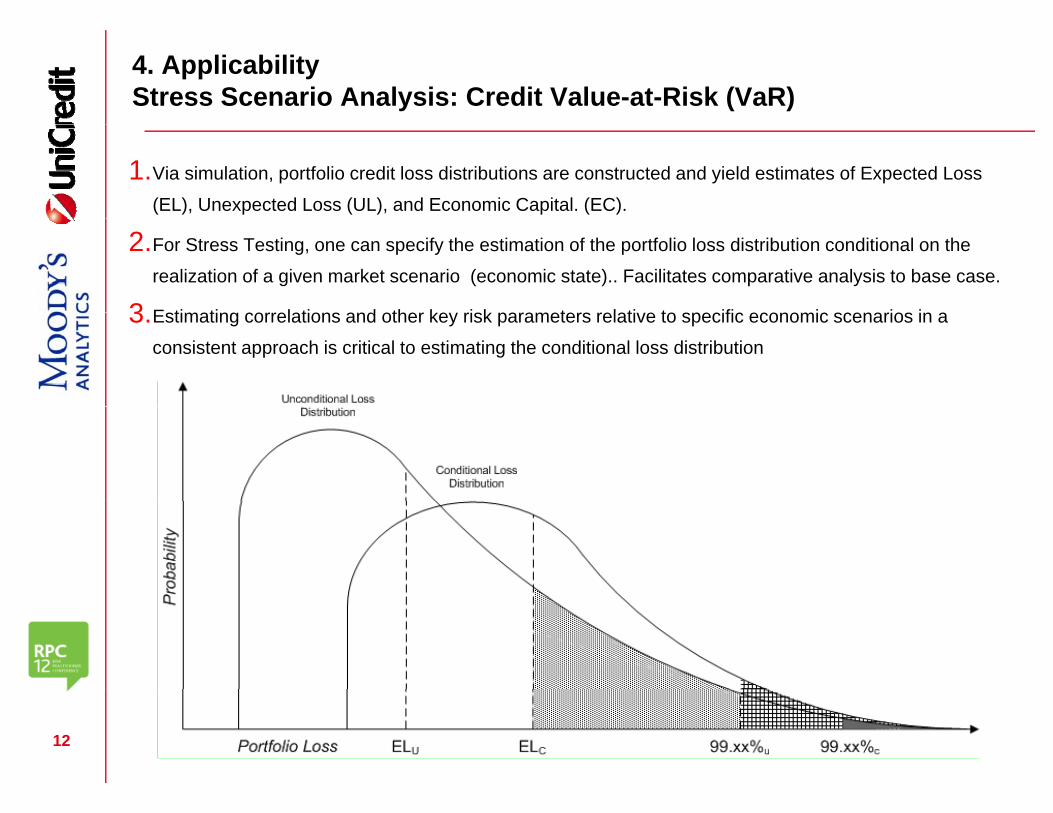

4. ApplicabilityStress Scenario Analysis: Credit Value-at-Risk (VaR)

1.Via simulation, portfolio credit loss distributions are constructed and yield estimates of Expected Loss

(EL), Unexpected Loss (UL), and Economic Capital. (EC).

2.For Stress Testing, one can specify the estimation of the portfolio loss distribution conditional on the

realization of a given market scenario (economic state).. Facilitates comparative analysis to base case.

3 E ti ti l ti d th k i k t l ti t ifi i i i3.Estimating correlations and other key risk parameters relative to specific economic scenarios in a

consistent approach is critical to estimating the conditional loss distribution

12

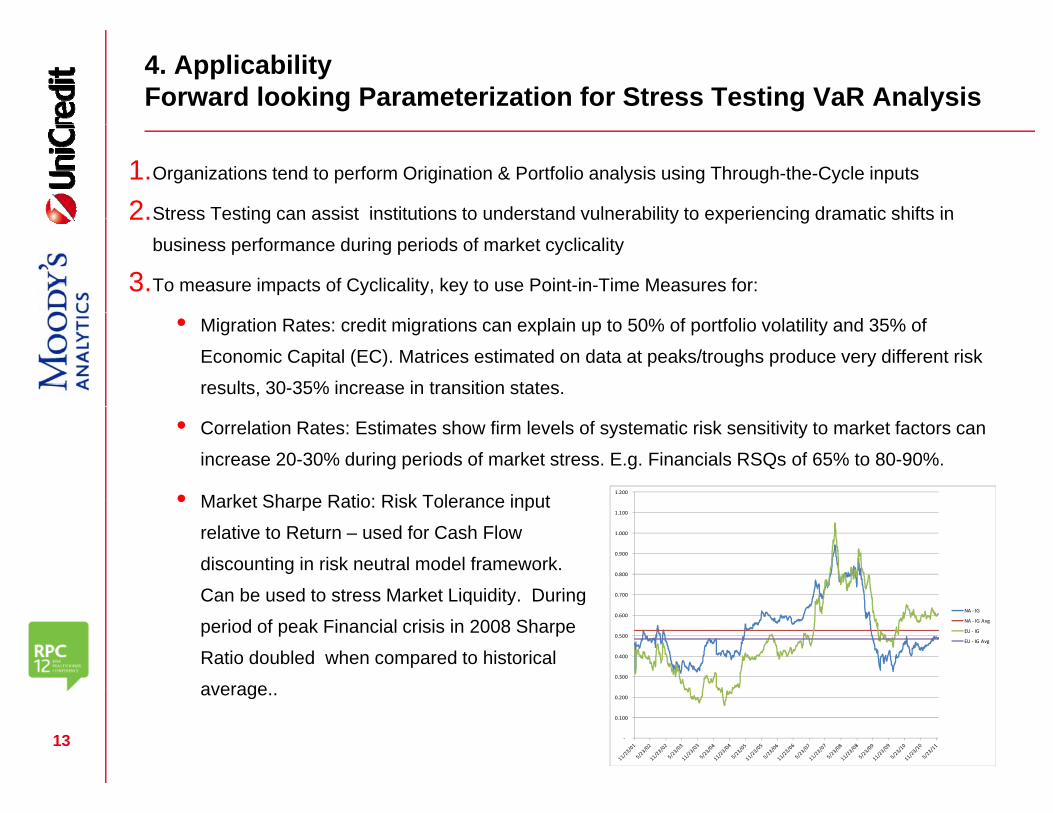

4. ApplicabilityForward looking Parameterization for Stress Testing VaR Analysis

1.Organizations tend to perform Origination & Portfolio analysis using Through-the-Cycle inputs

2.Stress Testing can assist institutions to understand vulnerability to experiencing dramatic shifts in2.Stress Testing can assist institutions to understand vulnerability to experiencing dramatic shifts in

business performance during periods of market cyclicality

3.To measure impacts of Cyclicality, key to use Point-in-Time Measures for:

• Migration Rates: credit migrations can explain up to 50% of portfolio volatility and 35% of

Economic Capital (EC). Matrices estimated on data at peaks/troughs produce very different risk

results, 30-35% increase in transition states.

• Correlation Rates: Estimates show firm levels of systematic risk sensitivity to market factors can

increase 20-30% during periods of market stress. E.g. Financials RSQs of 65% to 80-90%.

• Market Sharpe Ratio: Risk Tolerance input1.200 • Market Sharpe Ratio: Risk Tolerance input

relative to Return – used for Cash Flow

discounting in risk neutral model framework.

Can be used to stress Market Liquidity During 0 700

0.800

0.900

1.000

1.100

Can be used to stress Market Liquidity. During

period of peak Financial crisis in 2008 Sharpe

Ratio doubled when compared to historical

average0.300

0.400

0.500

0.600

0.700

NA ‐ IG

NA ‐ IG Avg

EU ‐ IG

EU ‐ IG Avg

13

average..

‐

0.100

0.200

4. ApplicabilityA framework for VaR Portfolio Analysis driven by Macroeconomic indicators to derive Scenario Loss distributionsindicators to derive Scenario Loss distributions

Macroeconomic Indicators Credit Risk Drivers (PD, Portfolio Risk – Capital

A B C

Macroeconomic Indicators ( ,LGD, Correlations)

pRequirements

A B CMacro-

economic Indicators

Common Sources of Risk

(Country/Industry)

Risk Drivers-PD, LGD,

CorrelationsPortfolio Loss Distribution

1.MA is constructing for Unicredit Group, correlation models based on regional / sector / product type

factors consistent to Unicredit’s portfolio composition. Such model also embeds macro-economic p p

indicators. Model to be used for both base case and stress testing analysis.

2.Will enable stress test analysis model parameterization of Unicredit’s internal Credit Portfolio Model to

be driven through changes in economic scenarios facilitating intuitive causal analysisbe driven through changes in economic scenarios facilitating intuitive causal analysis.

3.Such stress scenario results will provide insight as to associated changes to Portfolio Volatility and

Expected Shortfall, which are relevant for understanding:

14

• Changes in Risk Profile across Portfolio Segmentation allowing for Risk Mitigation

• Dynamic adjustments to Strategic Business Plans

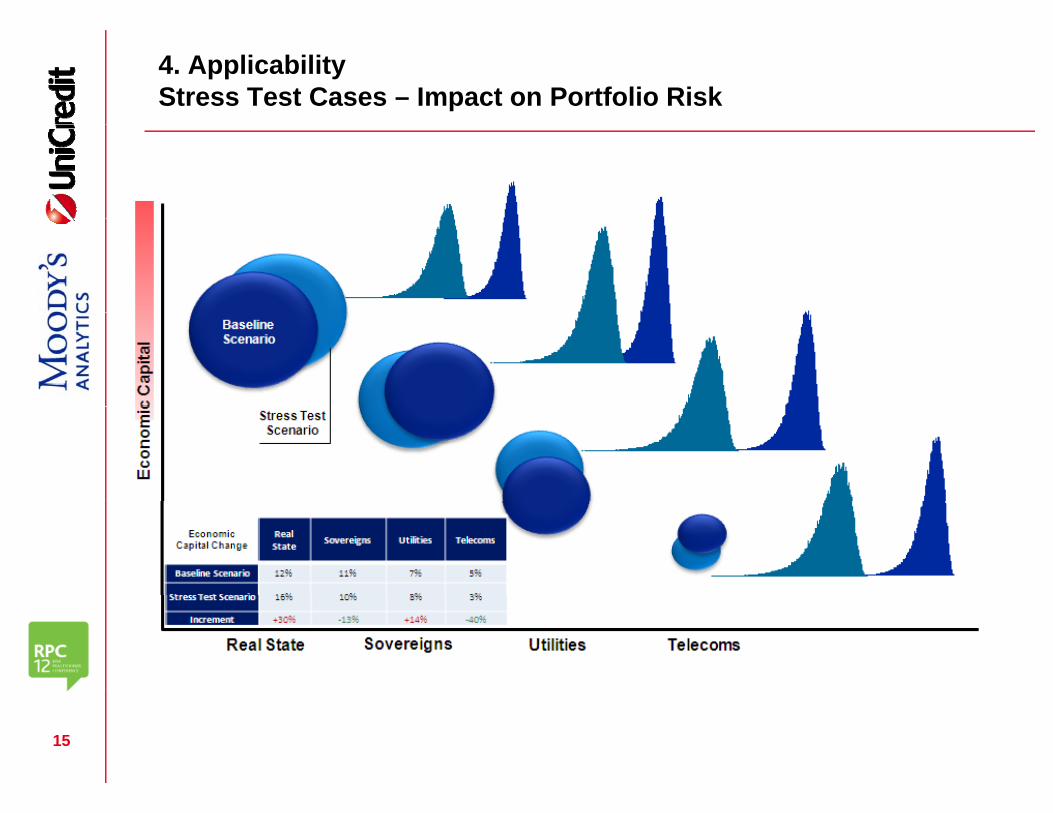

4. ApplicabilityStress Test Cases – Impact on Portfolio Risk

15

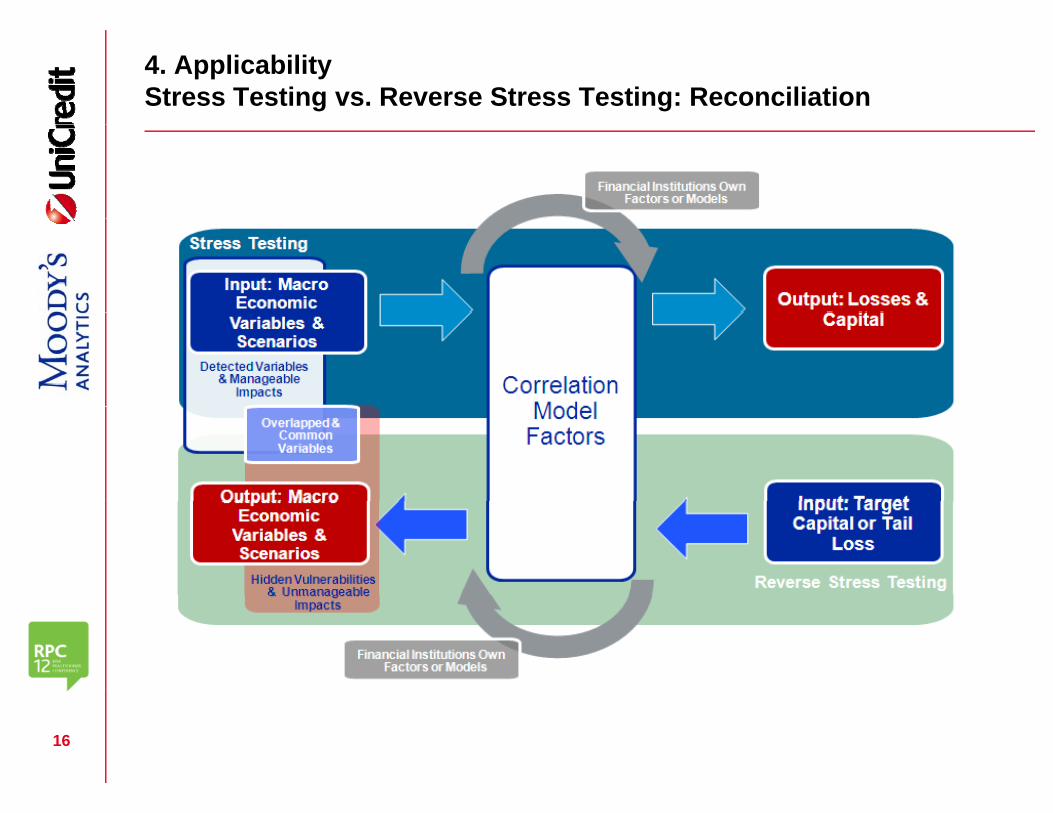

4. ApplicabilityStress Testing vs. Reverse Stress Testing: Reconciliation

16

4. ApplicabilityReverse Stress Testing is powerful tool to identify Bank’s vulnerabilities both from a systemic and an idiosyncratic standpoint

1. Using VaR Trial-by-Trial capability –given a target loss

bl id if d

y y p1. Portfolio Tail Risk and Macro Analysis

– we are able to identify and quantify in Value terms

different shock impacts in the Tail Region for each macro

0

2000

4000

6000

Capital M

illions

Tail Risk Analysis

scenario0

0 500 1000 1500 2000

Tail Exposure

2. Scenario and Contingency Analysis

2. Moody’s Analytics Reverse Stress Testing Reports help senior management to put in g p

place capital contingency plans and to develop the firm’s risk

appetite, business strategy and risk limits

17

4. CapabilitiesReverse stress testing analysisg y

Analysis offers a unique opportunity for Banks to better understand their business and

focus management’s attention on the areas where weakness could turn out to befocus management s attention on the areas where weakness could turn out to be

potentially harmful to the entire organization

1.Consistent and cohesive portfolio reverse stress testing metric

2.Flexibility, Transparency, and Usability

3.Allows for Reconciliation of Stress Testing and Reverse Stress Testing

4.Helps Institutions to Meet Regulatory Requirements

18With goals of an Organizations risk culture and stress testing framework defined, how does one

develop Contingency Planning relative to Business Strategy?

5. Contingency Plan:A Bank must complement its Business strategy with contingency plans in order for it to timely identify and address critical situationsp y y

Level A

TriggersLevel B Level C

LOSSLOSS

CORE TIER 1 RATIO

Level B actions Level C actionsLevel A actions

Postponement of capital expenditure initiatives (capital spending)

securitizations and recourse to risk mitigation

Resolution Plan

Review of credit limits changes in the overall

strategy and business plan: reduction of

exposures to specific

Actions techniques (asset hedging or selling);

addressing capital structure via reduction of share buy-back, reduction or halting of dividend

exposures to specific sectors, countries, regions, products or portfolios

tighten underwriting policies and

19

or halting of dividend payments, capital raising, sale of assets

policies and processes (i.e.. no new lending with revenue below expected loss);

Take-Aways As "Food For Thought"

Stress Testing Program has to be a consistent framework to reduce complexity and increase usefulness to Senior Management.

Involvement of and communication by all relevant stakeholder to Senior Management key. Educational Level across all levels a matter of Institution's Risk Culture.

Stress Testing is not about just keeping your Banking license – it is a daily Management Stress Testing is not about just keeping your Banking license it is a daily Management tool.

Firm-wide views essential to address Sustainability & Solvency of Business Model.

Essential to analyze Portfolio and Deal Transactions from multiple assuptions relative to: Essential to analyze Portfolio and Deal Transactions from multiple assuptions relative to:

Through the cycle analysis to support Origination and Stakeholders

Points-in-Time analysis to ensure Organization and business lines can endure CVolatility in Market Cyclicality

Adjust Business planning with changes in market conditions

Consequence management to express itself in feasable Contingency Plans.q g p g y

Mind-set from Risk Culture more important than precision to the last digit!

and many other questions searching for a solution

20

and many other questions searching for a solution.Your turn in the audience …….