Credit Scores and Scorecard Lending AGEC 489/690 Spring 2009 Slide Show #12.

22

Credit Scores Credit Scores and Scorecard and Scorecard Lending Lending AGEC 489/690 AGEC 489/690 Spring 2009 Spring 2009 Slide Show #12

-

date post

22-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of Credit Scores and Scorecard Lending AGEC 489/690 Spring 2009 Slide Show #12.

Credit Scores and Credit Scores and Scorecard Lending Scorecard Lending

AGEC 489/690AGEC 489/690

Spring 2009Spring 2009

Slide Show #12

Credit ScoringCredit Scoring FundamentalsFundamentals

A credit score is a numerical expression based on a statistical analysis of a borrower’s credit history to represent his/her creditworthinesscreditworthiness, which is the likelihood that the borrower will pay his/her debts in a timely manner.

Credit ScoringCredit Scoring FundamentalsFundamentals

A credit score is a numerical expression based on a statistical analysis of a borrower’s credit history to represent his/her creditworthinesscreditworthiness, which is the likelihood that the borrower will pay his/her debts in a timely manner.

A credit score is primarily based on credit report information obtained from credit bureaus and credit reference agencies.

Credit ScoringCredit Scoring FundamentalsFundamentals

Lenders use credit scores to evaluate the potential riskpotential risk posed by lending money and to mitigate losses due to bad debt. Lenders also use credit scores to determine who qualifies for who qualifies for a loan, at what interest, and what credit limitsa loan, at what interest, and what credit limits.

Credit ScoringCredit Scoring FundamentalsFundamentals

Lenders use credit scores to evaluate the potential riskpotential risk posed by lending money and to mitigate losses due to bad debt. Lenders also use credit scores to determine who qualifies for who qualifies for a loan, at what interest, and what credit limitsa loan, at what interest, and what credit limits.

Credit scoring is not limited to lending. Other organizations, such as mobile phone companies, insurance companies, and potential employerspotential employers are examples of other users of credit scoring.

Fundamentals Credit ScoringFundamentals Credit Scoring

A credit score is primarily based on credit report information typically from the three US credit bureaus: Experian, TransUnion and Equifax.

Fundamentals Credit ScoringFundamentals Credit Scoring

A credit score is primarily based on credit report information typically from the three US credit bureaus: Experian, TransUnion and Equifax.

There are differing approaches to calculating credit scores. The FICO is a credit score developed by Fair Issac & Company. It is used by many mortgage lenders that use a risk-based system to determine the possibility that the borrower may default on financial obligations to the lender.

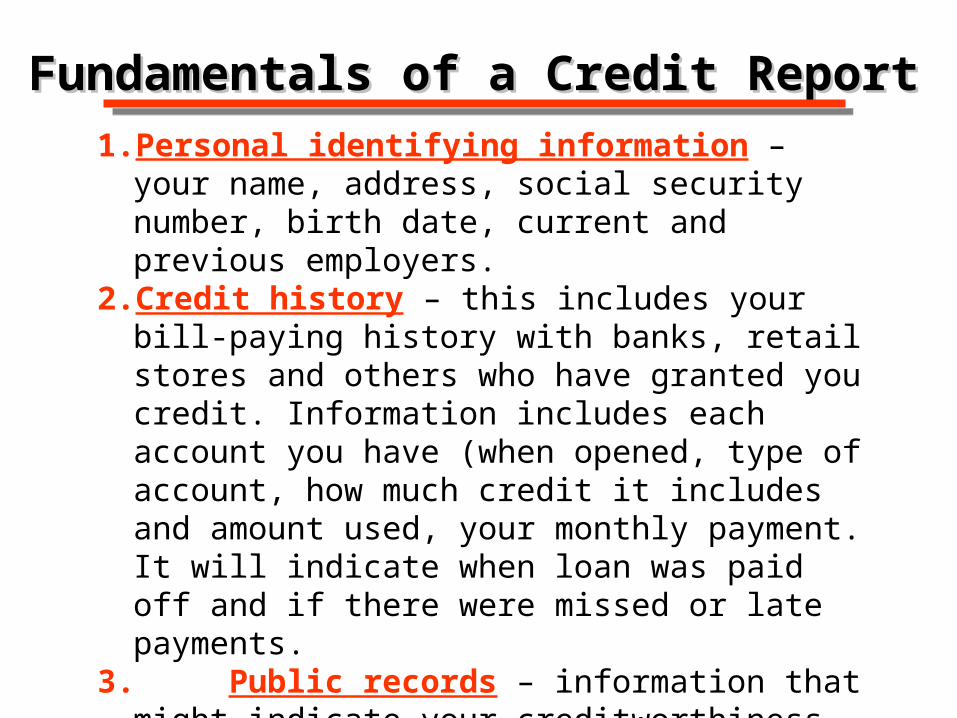

Fundamentals of a Credit ReportFundamentals of a Credit Report1. Personal identifying information – your name,

address, social security number, birth date, current and previous employers.

Fundamentals of a Credit ReportFundamentals of a Credit Report1. Personal identifying information – your name,

address, social security number, birth date, current and previous employers.

2. Credit history – this includes your bill-paying history with banks, retail stores and others who have granted you credit. Information includes each account you have (when opened, type of account, how much credit it includes and amount used, your monthly payment. It will indicate when loan was paid off and if there were missed or late payments.

Fundamentals of a Credit ReportFundamentals of a Credit Report1. Personal identifying information – your name,

address, social security number, birth date, current and previous employers.

2. Credit history – this includes your bill-paying history with banks, retail stores and others who have granted you credit. Information includes each account you have (when opened, type of account, how much credit it includes and amount used, your monthly payment. It will indicate when loan was paid off and if there were missed or late payments.

3. Public records – information that might indicate your creditworthiness, such as tax liens, court judgments and bankruptcies.

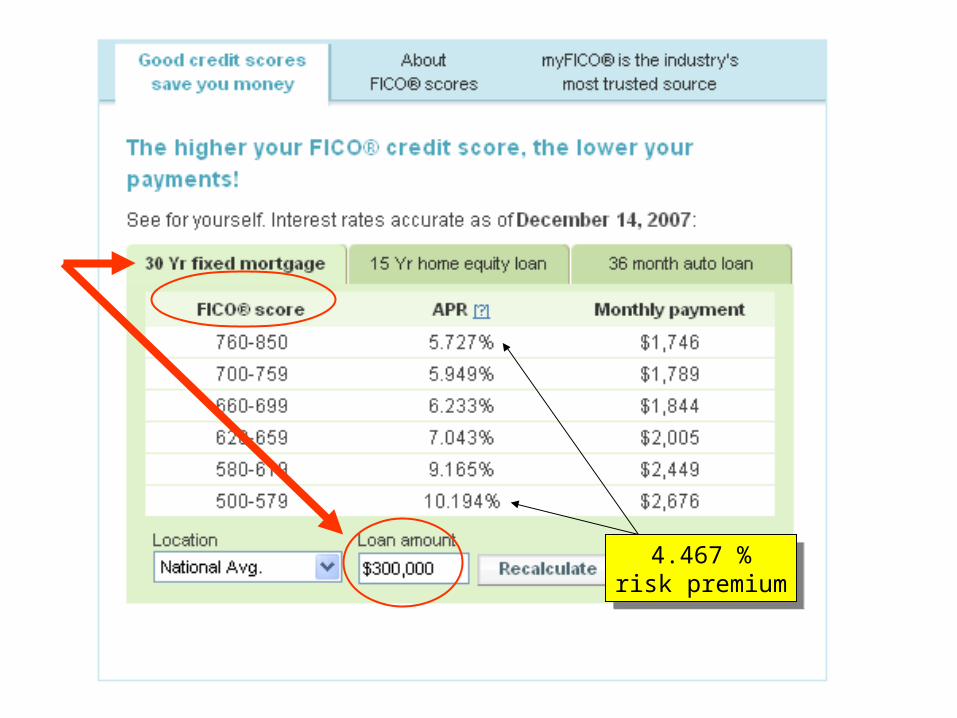

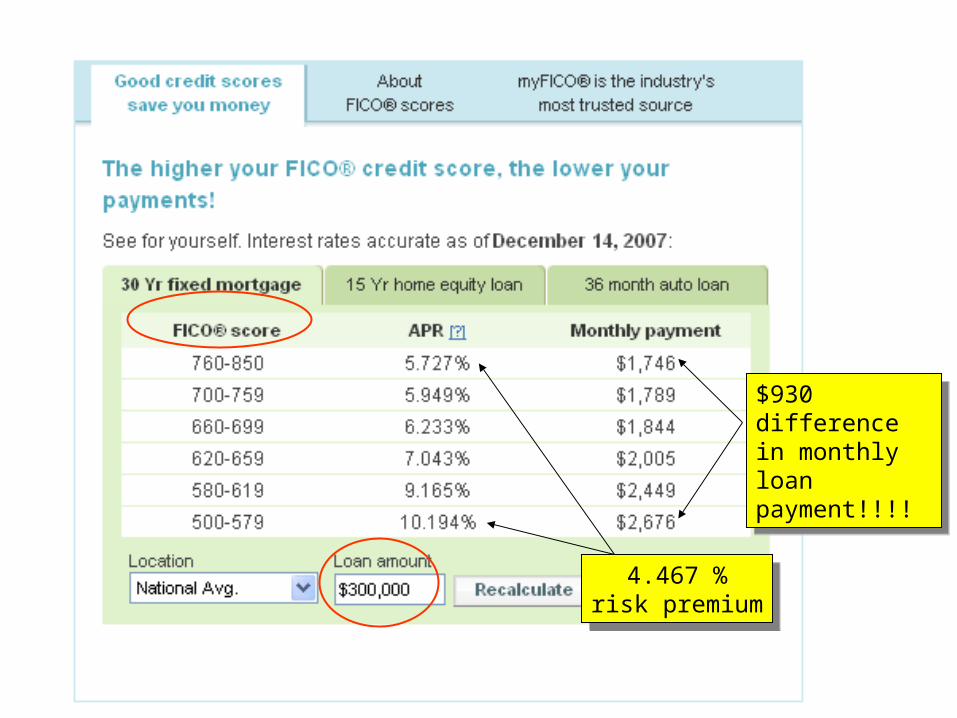

The FICO credit score is used by all three US credit bureaus. It is used by over 90% of commercial banks when analyzing mortgage loan applications.

The FICO credit score is used by all three US credit bureaus. It is used by over 90% of commercial banks when analyzing mortgage loan applications.

350 500 580 620 660 700 760 850

Loan automatically rejected below 500

Loan automatically rejected below 500

Loan automatically accepted above 500

Loan automatically accepted above 500

FICO Credit Score EmployedFICO Credit Score EmployedIn Lending DecisionsIn Lending Decisions

More information required. Riskpremium applied to interest rate.

More information required. Riskpremium applied to interest rate.

4.467 %risk premium

4.467 %risk premium

4.467 %risk premium

4.467 %risk premium

$930 difference in monthly loan payment!!!!

$930 difference in monthly loan payment!!!!

Scorecard LendingScorecard Lending

Credit StandardsCredit StandardsMost lenders use credit scores as a part of

its standards when evaluating loan applications.

Lenders also establish standards related to liquidity, solvency and debt repayment capacity (for example, a minimum current ratio of 1.50, a maximum debt ratio of 0.50, minimum term debt and capital lease coverage ratio of 1.25).

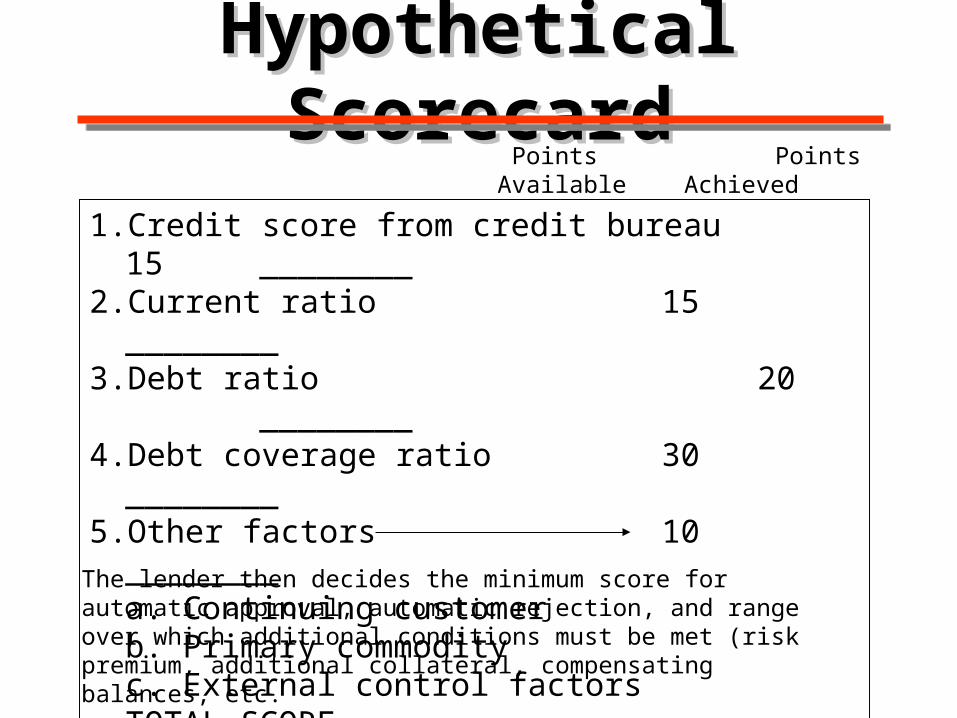

Hypothetical ScorecardHypothetical Scorecard

1. Credit score from credit bureau 15 ________2. Current ratio 15 ________3. Debt ratio 20 ________4. Debt coverage ratio 30 ________5. Other factors 10 ________

a. Continuing customerb. Primary commodityc. External control factorsTOTAL SCORE ________

Points PointsAvailable Achieved

The lender then decides the minimum score for automatic approval, automatic rejection, and range over which additional conditions must be met (risk premium, additional collateral, compensating balances, etc.

Hypothetical ScorecardHypothetical Scorecard

1. Credit score from credit bureau 15 ___12___2. Current ratio 15 ___13___3. Debt ratio 20 ___17___4. Debt coverage ratio 30 ___25___5. Other factors 10 ____9___

a. Continuing customerb. Primary commodityc. External control factorsTOTAL SCORE ___76___

Points PointsAvailable Achieved

The lender then decides the minimum score for automatic approval, automatic rejection, and range over which additional conditions must be met (risk premium, additional collateral, compensating balances, etc.

0 50 55 60 65 70 75 76 100

Loan automatically rejected below 50

Loan automatically rejected below 50

Loan automatically accepted above 75

Loan automatically accepted above 75

Credit Score Lending SheetCredit Score Lending Sheet

More information required. Riskpremium applied to interest rate.

More information required. Riskpremium applied to interest rate.

49

Hypothetical Loan RatesHypothetical Loan RatesBase cost of funds 4.0%

Score > 75 6.0%

Score = 71 – 75 7.0%

Score = 66 – 70 7.5%

Score = 61 – 65 8.0%

Score = 56 – 60 8.5%

Score = 50 – 55 9.0%