CREDIT REPAIR COURSE

31

The educational investment in yourself, with a monetary return on investment! By: Joel Drotts Juris Doctorate IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 1

-

Upload

joel-drotts -

Category

Education

-

view

200 -

download

2

Transcript of CREDIT REPAIR COURSE

The educational investment in yourself, with a monetary return on investment!

By: Joel Drotts Juris Doctorate

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100.

1

Welcome to the smartest investment in YOURSELF, you have EVER made! The $100.00 you just spent for the purchase of this educational course will empower you financially beyond anything you have ever experienced before! What this course does is give you all the tools, procedures, and laws you need to repair your own credit! Moreover, we give you precise pre-written letters which you can and will alter to send to those creditors and credit reporting corporations that are standing in the way of your obtaining better credit.

That's right.... With this course and its included tools, you will be able to repair and protect your own credit exactly the way the professionals do it! Of course the professional so called “credit counselors” don't want this information to get out to the public, but lucky for us we never cared for them or their questionable business practices and in fact business model any way. We'll just have to console ourselves with the knowledge that this educational course and included tools, will continue to help thousands of Americans to experience true financial empowerment by teaching them exactly how to repair and improve their own credit scores by often unbelievable increases (At least those smart enough to purchase this course from us.)!

What's makes this truly an investment in yourself that keeps on giving, is once you have mastered the procedures, used the tools, and significantly improved your own credit score with the big three credit reporting companies, you will be able to teach other American's how to do so as well. We encourage you to teach these techniques to your friends, families, and loved ones. Yes, it means we will probably make less money. Once again we'll just have to console ourselves with the knowledge we've helped so many of our country-men and country-women win a war they didn't know they are currently fighting, let alone losing that war. The war which I am speaking about, is the war to gain and maintain good credit in America!

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 2

1. CREDIT COUNSELORS ARE USELESS CONARTISTS!

Credit repair COMPANIES. Who needs them! Even when you can find an honest one that isn't hell-bent on further ripping you off, you just can't shake that sinking feeling in your gut that they're bilking you even further for your hard earned dollars.

Do you know why you feel that way?

It's because they ARE shamelessly bilking you, and all the while claiming to helping YOU out?!? These so called “credit-counselor” crooks and their industry built on shameless lies and consumer ignorance have even gone so far as to get legislation passed that says if you go financially belly-up (a.k.a. Bankrupt), the Court can order you to go get ripped off by one of these crooks.

Can you imagine?

You're already financially hard-up and strapped, and these jerks want to charge you an additional hundreds, if not thousands of dollars, to do exactly what we're about to teach you to do for yourself for $100.00. If that's not criminal, I don't know what is!

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 3

But why the big credit hub-bub, bub?

Why are so many people so interested in your credit rating,

and whether or not you have always “been a responsible

consumer?” As if your credit-score has anything to do with

responsibility, maturity, ethical behavior, or even your

ability to pay your bills.

As you'll soon find out, no matter what you do or did, you

would have ended up in the credit dog house. Think about

it. The reason is is that the system with which we live

which places so much emphasis on credit and debt was

designed by an elite few companies and industries so they

can control all the money, continue to control all the

money, and live lives people like you and I can only dream

about.

Meanwhile, we stress, starve, and struggle just to get even

the tiniest of crumbs these fat-cats accidently allow to

“trickle down” to us common-folks, as they scarf down the

entirety of the credit and financial cake of the country,

which was originally meant to be for all to enjoy.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 4

I tell you these things, not because I am a windbag, know I have a captive audience in the purchasers of this course,

so I’d figure I’d get on my soapbox about the need for financial reform and abolishment of the Federal Reserve

System, our fiat currency not under Congressional control, and Quantitative Easing (OK, there may be just a little

bit of truth in that statement), but because unfortunately financial problems can and often do make individuals feel

like they are some how worth less than other people.

Being broke, in debt, or even just poor can often make some people feel hopeless, stressed out to a point of

causing medical conditions, have a low sex drive, obsess about money and finances, depressed, and a whole litany

of horrible and unneeded feelings of self-persecution, guilt, low self-esteem, and even self-hatred. What's worse is

our entire society is designed to make you feel exactly that way, when and if you do end up in the financial dog

house.

Well, I'm hear to tell you, you don't have to feel that way any more. It isn't true it the least, and being wealthy or

having good credit bares absolutely no reflection on who you are as a person, your moral fiber, your ability to

control yourself, or your value as a human. It's simply not real. Those feelings of guilt or self-doubt? You don't need

them any more, and they're doing you no favors! That frustration you feel? We'll get that one too, as things start to

clear up for you. You are hereby taking complete control of your financial house and credit, the world be damned,

because you and this course are going to get you back on top or take you to places long denied you before!

Can you feel that? That is empowerment! That is the feeling of knowing for an absolute fact that while the house

may be a mess right now, you WILL get in cleaned up, and in order! YOU WILL be the one that determines just house

clean that house will be! This is your financial house, and it's time for you to own it like it is!!!

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 5

I want you to do something for me. I want you to stop reading in

a minute, stand-up, go look into a mirror or reflective surface,

and say this to yourself: “My credit is my bitch! It is merely three

little numbers controlled by three vindictive pimps, and I'll be

damned if that little bitch and her three pimps are going to ruin or

dictate the happiness in my life! They are all my bitches, and

bitches ain't shit to me!”

It is called self-empowering proclamation. By trash talking a

problem (Especially a big one), you are subconsciously owning

and overcoming that problem. That’s why I don't care if you're a

man, a woman, old, young, black, white, yellow, brown, green,

orange, or blue! See, you are now in what may be the most

important fight of your adult life, for some more than others,

and we're going to get dirty. This will not always be pleasant,

and certainly not always easy. However, you are stronger than

your opponents, and with this course you are now smarter as

well! The only way this will not work, is if you allow it not to

work! That is what ownership and empowerment truly mean,

and from this day going forward you are the new boss of your

financial house!

HERE ME ROAR!

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 6

WHAT YOU NEED BEFORE WE START, AND HOW LONG THIS WILL TAKE! A. Credit reports from each big three!

Equifax (www.equifax.com) P.O. Box 740241. Atlanta, GA 30374-0241. 1-800-685-1111.

Experian (www.experian.com) P.O. Box 2104. Allen, TX 75013-0949. 1-888-EXPERIAN (397-3742)

Trans Union (www.transunion.com) P.O. Box 1000. Chester, PA 19022. 1-800-916-8800.

I recommend purchased credit reports, as opposed to the free ones they are required to grant you annually, from each of the three credit reporting agencies. This should cost $30-$60, which is bull if you ask me. However, I recommend the purchased reports, because unfortunately even though by law they must grant you one free credit report annually, at current no one seems to be enforcing the sophistication or quality level of those free reports. Therefore, it is often better to buy the report from them. Even the cheapest one they offer, is purposely better than the free ones, which are always almost useless in the quality and level of detail contained in those credit reports.

Now, should you not be able to afford to buy the reports, then you demand from them repeatedly and in writing your one free copy that they must give you as a matter of Federal law.

If they refuse, you inform them that you will be informing the FTC, about their belief that they no longer must obey the Fair Credit Reporting Act. If they still refuse, then report this fact to the FTC.

That is what the FTC is there for, and why you pay taxes. So, if they play games, then you get your tax dollars worth of credit enforcement and alert the Federal Trade Commission. We need these reports, because those are the reports we will be cleaning. We need to know what we are looking at, and what is dirtying up your financial credit house!

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 7

B. A calendar that you can mark dates in, which you can check on a regular basis. The reason being is many of our

techniques are subject to legal time constraints, which we will be utilizing to our advantage. However, when you

attempt to control the clock, you must be sure to keep a steady and constant eye on that clock in order to reap the

intended benefits. This entire process will take 45-90 days, depending on what is wrong with your credit score.

C.

A pen or ink-jet in your printer with a lot of ink, and a bunch of paper. You will be becoming a professional letter

writer by the time this is all done, and you will be on first name basis with the post-office workers nearest your house.

That's just a fact. Watch... You'll see.

D. A strong a patient mental attitude. You can improve your credit drastically, if you follow these instructions. However,

you MUST… MUST… MUST!!! follow these instructions. We will get through it.

So lets begin shall we. Throughout this course I will be referring to letters or contracts given you to cut, paste, and

personalize as tools. This is to impress upon you that the entirety of these tools must be utilized or copied, altered,

and pasted, as well as for the fact that’s what these legal codicils are! Tools to work on your credit-score with! Tool one

is for people really in trouble. The below tool below is for those currently receiving collections letters and phone calls.

You start here. Cut and paste the letter below, filling in your name and the name of collection agency. You can use this

one if you need extra time and plan to pay. It gives you 30 days extra. THIS IS A 17 STEP PROCESS, BEGIN:

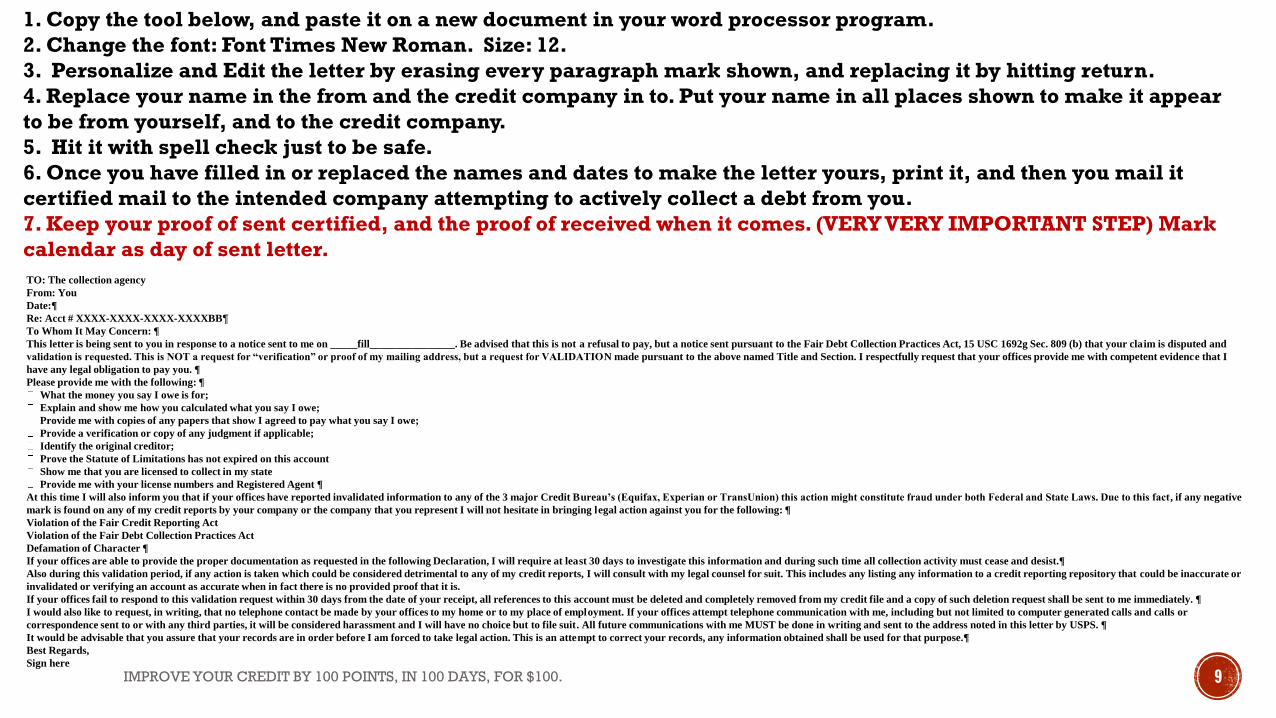

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 8

TO: The collection agency

From: You

Date:¶

Re: Acct # XXXX-XXXX-XXXX-XXXXBB¶To Whom It May Concern: ¶

This letter is being sent to you in response to a notice sent to me on _____fill________________. Be advised that this is not a refusal to pay, but a notice sent pursuant to the Fair Debt Collection Practices Act, 15 USC 1692g Sec. 809 (b) that your claim is disputed and

validation is requested. This is NOT a request for “verification” or proof of my mailing address, but a request for VALIDATION made pursuant to the above named Title and Section. I respectfully request that your offices provide me with competent evidence that I

have any legal obligation to pay you. ¶

Please provide me with the following: ¶

What the money you say I owe is for;

Explain and show me how you calculated what you say I owe;

Provide me with copies of any papers that show I agreed to pay what you say I owe;

Provide a verification or copy of any judgment if applicable;

Identify the original creditor;

Prove the Statute of Limitations has not expired on this account

Show me that you are licensed to collect in my state

Provide me with your license numbers and Registered Agent ¶

At this time I will also inform you that if your offices have reported invalidated information to any of the 3 major Credit Bureau’s (Equifax, Experian or TransUnion) this action might constitute fraud under both Federal and State Laws. Due to this fact, if any negative

mark is found on any of my credit reports by your company or the company that you represent I will not hesitate in bringing legal action against you for the following: ¶

Violation of the Fair Credit Reporting Act

Violation of the Fair Debt Collection Practices Act

Defamation of Character ¶

If your offices are able to provide the proper documentation as requested in the following Declaration, I will require at least 30 days to investigate this information and during such time all collection activity must cease and desist.¶

Also during this validation period, if any action is taken which could be considered detrimental to any of my credit reports, I will consult with my legal counsel for suit. This includes any listing any information to a credit reporting repository that could be inaccurate or

invalidated or verifying an account as accurate when in fact there is no provided proof that it is.

If your offices fail to respond to this validation request within 30 days from the date of your receipt, all references to this account must be deleted and completely removed from my credit file and a copy of such deletion request shall be sent to me immediately. ¶

I would also like to request, in writing, that no telephone contact be made by your offices to my home or to my place of employment. If your offices attempt telephone communication with me, including but not limited to computer generated calls and calls or

correspondence sent to or with any third parties, it will be considered harassment and I will have no choice but to file suit. All future communications with me MUST be done in writing and sent to the address noted in this letter by USPS. ¶

It would be advisable that you assure that your records are in order before I am forced to take legal action. This is an attempt to correct your records, any information obtained shall be used for that purpose.¶

Best Regards,

Sign here

1. Copy the tool below, and paste it on a new document in your word processor program.

2. Change the font: Font Times New Roman. Size: 12.

3. Personalize and Edit the letter by erasing every paragraph mark shown, and replacing it by hitting return.

4. Replace your name in the from and the credit company in to. Put your name in all places shown to make it appear

to be from yourself, and to the credit company.

5. Hit it with spell check just to be safe.

6. Once you have filled in or replaced the names and dates to make the letter yours, print it, and then you mail it

certified mail to the intended company attempting to actively collect a debt from you.

7. Keep your proof of sent certified, and the proof of received when it comes. (VERY VERY IMPORTANT STEP) Mark

calendar as day of sent letter.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 9

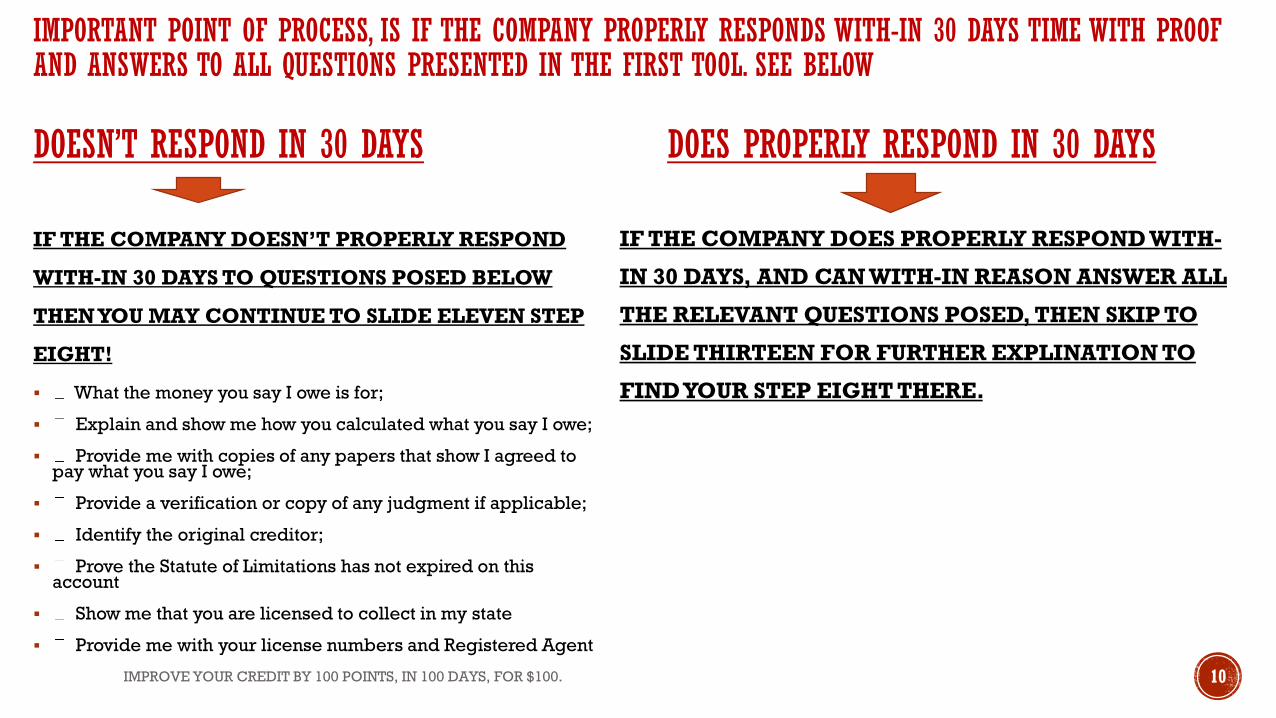

IMPORTANT POINT OF PROCESS, IS IF THE COMPANY PROPERLY RESPONDS WITH-IN 30 DAYS TIME WITH PROOF AND ANSWERS TO ALL QUESTIONS PRESENTED IN THE FIRST TOOL. SEE BELOW

DOESN’T RESPOND IN 30 DAYS DOES PROPERLY RESPOND IN 30 DAYS

IF THE COMPANY DOESN’T PROPERLY RESPOND

WITH-IN 30 DAYS TO QUESTIONS POSED BELOW

THEN YOU MAY CONTINUE TO SLIDE ELEVEN STEP

EIGHT!

What the money you say I owe is for;

Explain and show me how you calculated what you say I owe;

Provide me with copies of any papers that show I agreed to pay what you say I owe;

Provide a verification or copy of any judgment if applicable;

Identify the original creditor;

Prove the Statute of Limitations has not expired on this account

Show me that you are licensed to collect in my state

Provide me with your license numbers and Registered Agent

IF THE COMPANY DOES PROPERLY RESPOND WITH-

IN 30 DAYS, AND CAN WITH-IN REASON ANSWER ALL

THE RELEVANT QUESTIONS POSED, THEN SKIP TO

SLIDE THIRTEEN FOR FURTHER EXPLINATION TO

FIND YOUR STEP EIGHT THERE.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 10

San Francisco After Dark By Joel Drotts

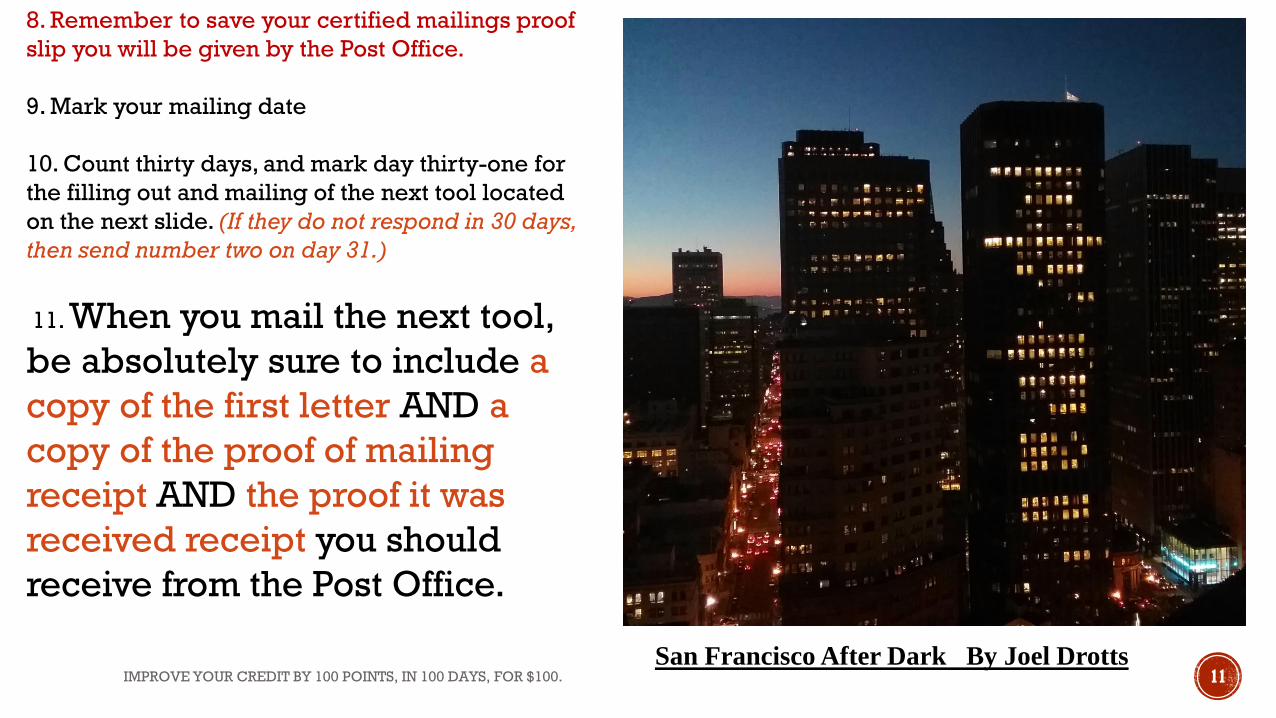

8. Remember to save your certified mailings proof

slip you will be given by the Post Office.

9. Mark your mailing date

10. Count thirty days, and mark day thirty-one for

the filling out and mailing of the next tool located

on the next slide. (If they do not respond in 30 days,

then send number two on day 31.)

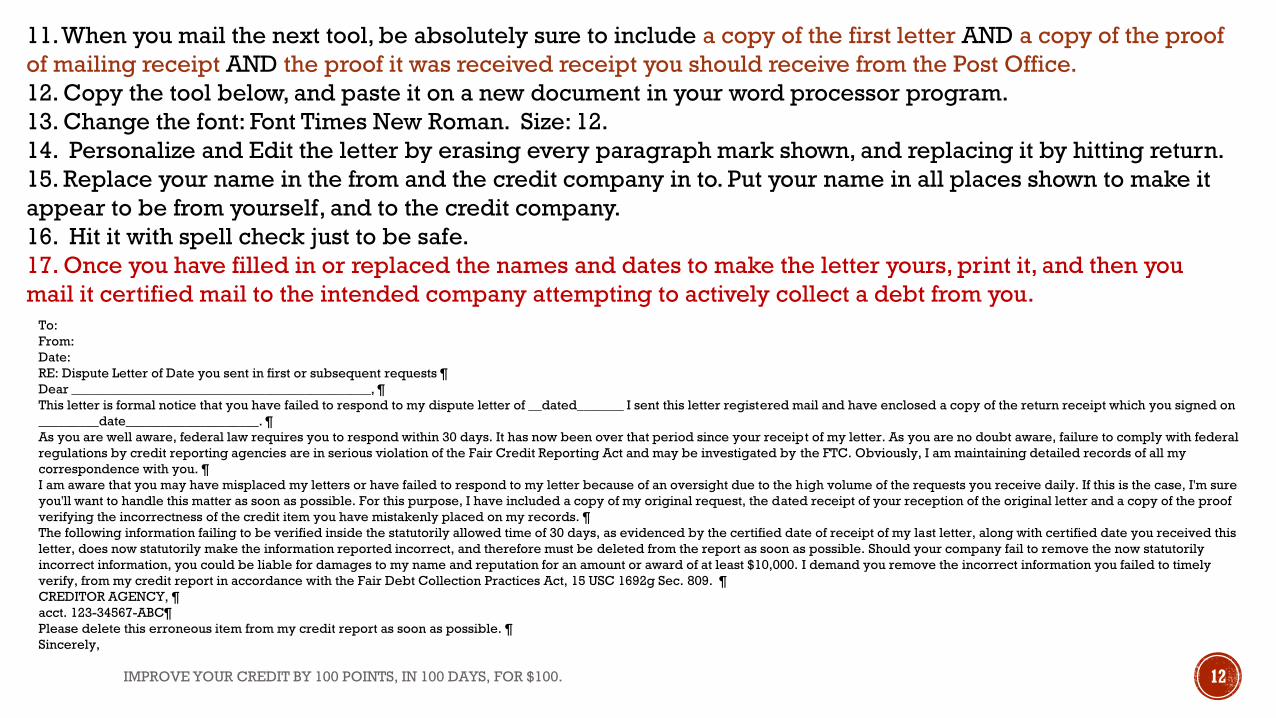

11. When you mail the next tool,

be absolutely sure to include a

copy of the first letter AND a

copy of the proof of mailing

receipt AND the proof it was

received receipt you should

receive from the Post Office.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 11

To:

From:

Date:

RE: Dispute Letter of Date you sent in first or subsequent requests ¶

Dear _____________________________________________, ¶

This letter is formal notice that you have failed to respond to my dispute letter of __dated_______ I sent this letter registered mail and have enclosed a copy of the return receipt which you signed on

_________date____________________. ¶

As you are well aware, federal law requires you to respond within 30 days. It has now been over that period since your receipt of my letter. As you are no doubt aware, failure to comply with federal

regulations by credit reporting agencies are in serious violation of the Fair Credit Reporting Act and may be investigated by the FTC. Obviously, I am maintaining detailed records of all my

correspondence with you. ¶

I am aware that you may have misplaced my letters or have failed to respond to my letter because of an oversight due to the high volume of the requests you receive daily. If this is the case, I'm sure

you'll want to handle this matter as soon as possible. For this purpose, I have included a copy of my original request, the dated receipt of your reception of the original letter and a copy of the proof

verifying the incorrectness of the credit item you have mistakenly placed on my records. ¶

The following information failing to be verified inside the statutorily allowed time of 30 days, as evidenced by the certified date of receipt of my last letter, along with certified date you received this

letter, does now statutorily make the information reported incorrect, and therefore must be deleted from the report as soon as possible. Should your company fail to remove the now statutorily

incorrect information, you could be liable for damages to my name and reputation for an amount or award of at least $10,000. I demand you remove the incorrect information you failed to timely

verify, from my credit report in accordance with the Fair Debt Collection Practices Act, 15 USC 1692g Sec. 809. ¶

CREDITOR AGENCY, ¶

acct. 123-34567-ABC¶

Please delete this erroneous item from my credit report as soon as possible. ¶

Sincerely,

11. When you mail the next tool, be absolutely sure to include a copy of the first letter AND a copy of the proof

of mailing receipt AND the proof it was received receipt you should receive from the Post Office.

12. Copy the tool below, and paste it on a new document in your word processor program.

13. Change the font: Font Times New Roman. Size: 12.

14. Personalize and Edit the letter by erasing every paragraph mark shown, and replacing it by hitting return.

15. Replace your name in the from and the credit company in to. Put your name in all places shown to make it

appear to be from yourself, and to the credit company.

16. Hit it with spell check just to be safe.

17. Once you have filled in or replaced the names and dates to make the letter yours, print it, and then you

mail it certified mail to the intended company attempting to actively collect a debt from you.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 12

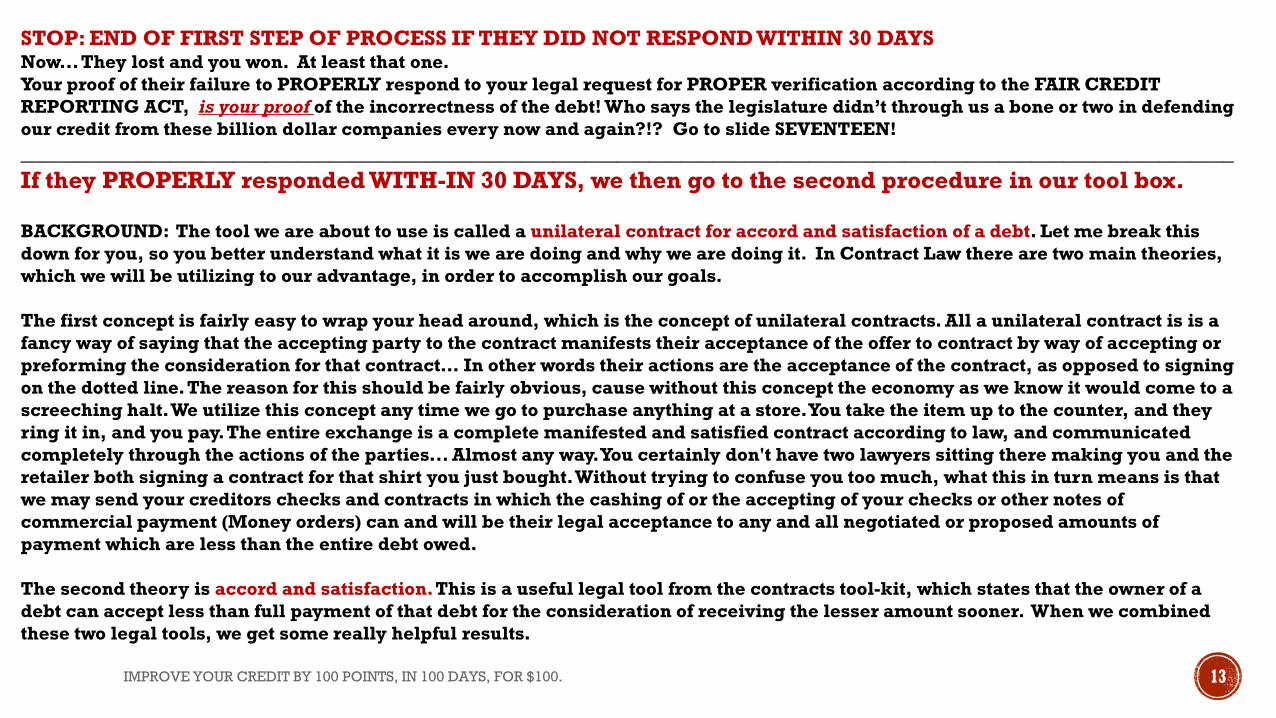

STOP: END OF FIRST STEP OF PROCESS IF THEY DID NOT RESPOND WITHIN 30 DAYS Now... They lost and you won. At least that one.

Your proof of their failure to PROPERLY respond to your legal request for PROPER verification according to the FAIR CREDIT

REPORTING ACT, is your proof of the incorrectness of the debt! Who says the legislature didn’t through us a bone or two in defending

our credit from these billion dollar companies every now and again?!? Go to slide SEVENTEEN!

__________________________________________________________________________________________________________________

If they PROPERLY responded WITH-IN 30 DAYS, we then go to the second procedure in our tool box.

BACKGROUND: The tool we are about to use is called a unilateral contract for accord and satisfaction of a debt. Let me break this

down for you, so you better understand what it is we are doing and why we are doing it. In Contract Law there are two main theories,

which we will be utilizing to our advantage, in order to accomplish our goals.

The first concept is fairly easy to wrap your head around, which is the concept of unilateral contracts. All a unilateral contract is is a

fancy way of saying that the accepting party to the contract manifests their acceptance of the offer to contract by way of accepting or

preforming the consideration for that contract… In other words their actions are the acceptance of the contract, as opposed to signing

on the dotted line. The reason for this should be fairly obvious, cause without this concept the economy as we know it would come to a

screeching halt. We utilize this concept any time we go to purchase anything at a store. You take the item up to the counter, and they

ring it in, and you pay. The entire exchange is a complete manifested and satisfied contract according to law, and communicated

completely through the actions of the parties... Almost any way. You certainly don't have two lawyers sitting there making you and the

retailer both signing a contract for that shirt you just bought. Without trying to confuse you too much, what this in turn means is that

we may send your creditors checks and contracts in which the cashing of or the accepting of your checks or other notes of

commercial payment (Money orders) can and will be their legal acceptance to any and all negotiated or proposed amounts of

payment which are less than the entire debt owed.

The second theory is accord and satisfaction. This is a useful legal tool from the contracts tool-kit, which states that the owner of a

debt can accept less than full payment of that debt for the consideration of receiving the lesser amount sooner. When we combined

these two legal tools, we get some really helpful results.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 13

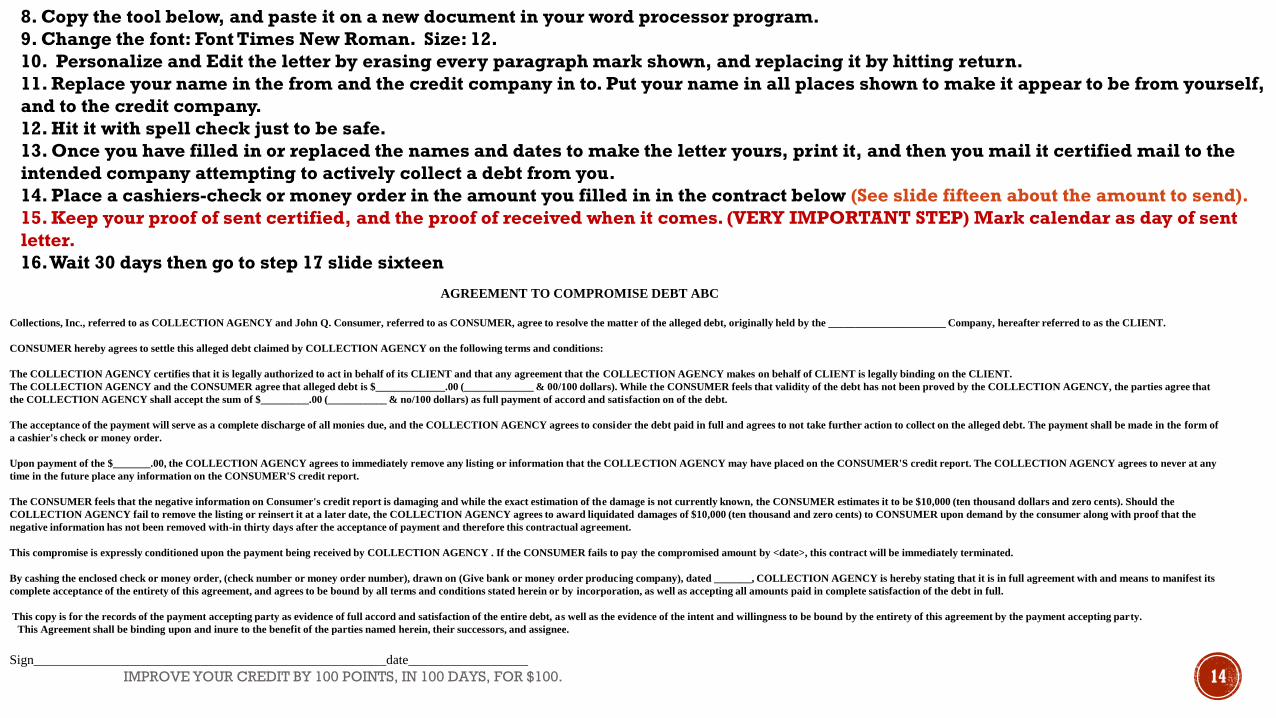

AGREEMENT TO COMPROMISE DEBT ABC

Collections, Inc., referred to as COLLECTION AGENCY and John Q. Consumer, referred to as CONSUMER, agree to resolve the matter of the alleged debt, originally held by the ______________________ Company, hereafter referred to as the CLIENT.

CONSUMER hereby agrees to settle this alleged debt claimed by COLLECTION AGENCY on the following terms and conditions:

The COLLECTION AGENCY certifies that it is legally authorized to act in behalf of its CLIENT and that any agreement that the COLLECTION AGENCY makes on behalf of CLIENT is legally binding on the CLIENT.

The COLLECTION AGENCY and the CONSUMER agree that alleged debt is $_____________.00 (_____________ & 00/100 dollars). While the CONSUMER feels that validity of the debt has not been proved by the COLLECTION AGENCY, the parties agree that

the COLLECTION AGENCY shall accept the sum of $_________.00 (___________ & no/100 dollars) as full payment of accord and satisfaction on of the debt.

The acceptance of the payment will serve as a complete discharge of all monies due, and the COLLECTION AGENCY agrees to consider the debt paid in full and agrees to not take further action to collect on the alleged debt. The payment shall be made in the form of

a cashier's check or money order.

Upon payment of the $_______.00, the COLLECTION AGENCY agrees to immediately remove any listing or information that the COLLECTION AGENCY may have placed on the CONSUMER'S credit report. The COLLECTION AGENCY agrees to never at any

time in the future place any information on the CONSUMER'S credit report.

The CONSUMER feels that the negative information on Consumer's credit report is damaging and while the exact estimation of the damage is not currently known, the CONSUMER estimates it to be $10,000 (ten thousand dollars and zero cents). Should the

COLLECTION AGENCY fail to remove the listing or reinsert it at a later date, the COLLECTION AGENCY agrees to award liquidated damages of $10,000 (ten thousand and zero cents) to CONSUMER upon demand by the consumer along with proof that the

negative information has not been removed with-in thirty days after the acceptance of payment and therefore this contractual agreement.

This compromise is expressly conditioned upon the payment being received by COLLECTION AGENCY . If the CONSUMER fails to pay the compromised amount by <date>, this contract will be immediately terminated.

By cashing the enclosed check or money order, (check number or money order number), drawn on (Give bank or money order producing company), dated _______, COLLECTION AGENCY is hereby stating that it is in full agreement with and means to manifest its

complete acceptance of the entirety of this agreement, and agrees to be bound by all terms and conditions stated herein or by incorporation, as well as accepting all amounts paid in complete satisfaction of the debt in full.

This copy is for the records of the payment accepting party as evidence of full accord and satisfaction of the entire debt, as well as the evidence of the intent and willingness to be bound by the entirety of this agreement by the payment accepting party.

This Agreement shall be binding upon and inure to the benefit of the parties named herein, their successors, and assignee.

Sign_____________________________________________________date__________________

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 14

8. Copy the tool below, and paste it on a new document in your word processor program.

9. Change the font: Font Times New Roman. Size: 12.

10. Personalize and Edit the letter by erasing every paragraph mark shown, and replacing it by hitting return.

11. Replace your name in the from and the credit company in to. Put your name in all places shown to make it appear to be from yourself,

and to the credit company.

12. Hit it with spell check just to be safe.

13. Once you have filled in or replaced the names and dates to make the letter yours, print it, and then you mail it certified mail to the

intended company attempting to actively collect a debt from you.

14. Place a cashiers-check or money order in the amount you filled in in the contract below (See slide fifteen about the amount to send).

15. Keep your proof of sent certified, and the proof of received when it comes. (VERY IMPORTANT STEP) Mark calendar as day of sent

letter.

16. Wait 30 days then go to step 17 slide sixteen

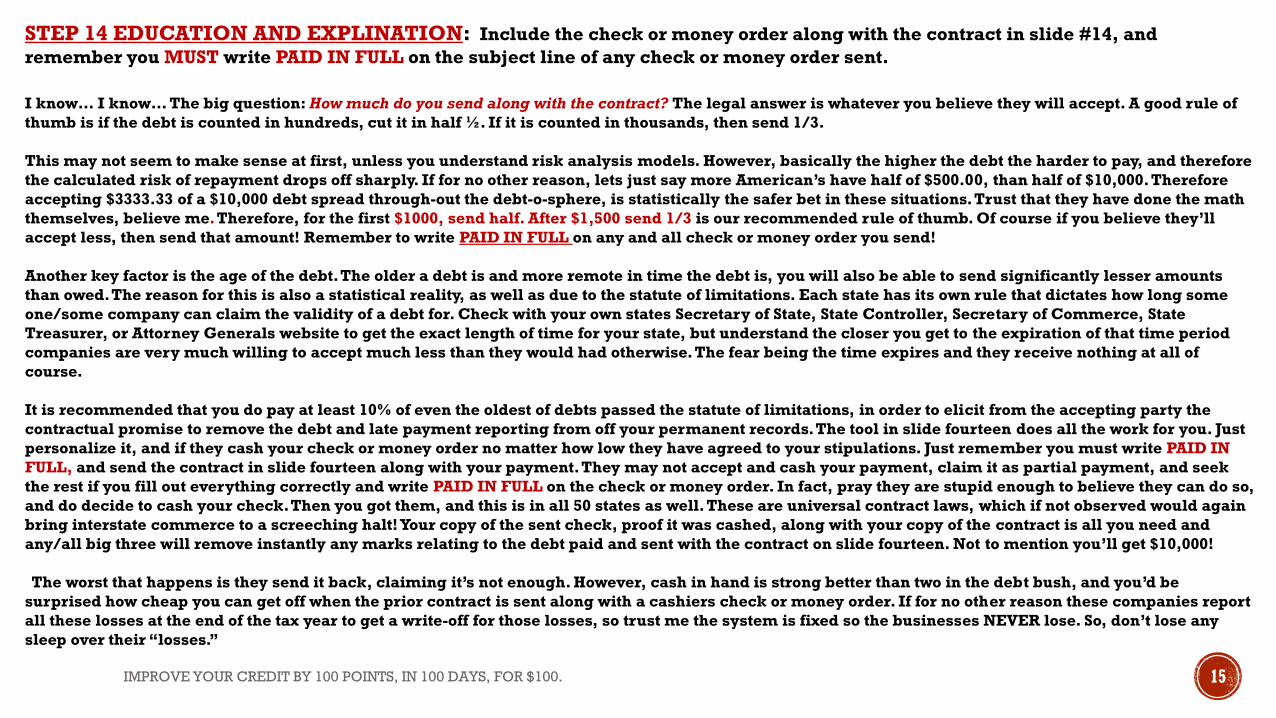

STEP 14 EDUCATION AND EXPLINATION: Include the check or money order along with the contract in slide #14, and

remember you MUST write PAID IN FULL on the subject line of any check or money order sent.

I know… I know… The big question: How much do you send along with the contract? The legal answer is whatever you believe they will accept. A good rule of

thumb is if the debt is counted in hundreds, cut it in half ½. If it is counted in thousands, then send 1/3.

This may not seem to make sense at first, unless you understand risk analysis models. However, basically the higher the debt the harder to pay, and therefore

the calculated risk of repayment drops off sharply. If for no other reason, lets just say more American’s have half of $500.00, than half of $10,000. Therefore

accepting $3333.33 of a $10,000 debt spread through-out the debt-o-sphere, is statistically the safer bet in these situations. Trust that they have done the math

themselves, believe me. Therefore, for the first $1000, send half. After $1,500 send 1/3 is our recommended rule of thumb. Of course if you believe they’ll

accept less, then send that amount! Remember to write PAID IN FULL on any and all check or money order you send!

Another key factor is the age of the debt. The older a debt is and more remote in time the debt is, you will also be able to send significantly lesser amounts

than owed. The reason for this is also a statistical reality, as well as due to the statute of limitations. Each state has its own rule that dictates how long some

one/some company can claim the validity of a debt for. Check with your own states Secretary of State, State Controller, Secretary of Commerce, State

Treasurer, or Attorney Generals website to get the exact length of time for your state, but understand the closer you get to the expiration of that time period

companies are very much willing to accept much less than they would had otherwise. The fear being the time expires and they receive nothing at all of

course.

It is recommended that you do pay at least 10% of even the oldest of debts passed the statute of limitations, in order to elicit from the accepting party the

contractual promise to remove the debt and late payment reporting from off your permanent records. The tool in slide fourteen does all the work for you. Just

personalize it, and if they cash your check or money order no matter how low they have agreed to your stipulations. Just remember you must write PAID IN

FULL, and send the contract in slide fourteen along with your payment. They may not accept and cash your payment, claim it as partial payment, and seek

the rest if you fill out everything correctly and write PAID IN FULL on the check or money order. In fact, pray they are stupid enough to believe they can do so,

and do decide to cash your check. Then you got them, and this is in all 50 states as well. These are universal contract laws, which if not observed would again

bring interstate commerce to a screeching halt! Your copy of the sent check, proof it was cashed, along with your copy of the contract is all you need and

any/all big three will remove instantly any marks relating to the debt paid and sent with the contract on slide fourteen. Not to mention you’ll get $10,000!

The worst that happens is they send it back, claiming it’s not enough. However, cash in hand is strong better than two in the debt bush, and you’d be

surprised how cheap you can get off when the prior contract is sent along with a cashiers check or money order. If for no other reason these companies report

all these losses at the end of the tax year to get a write-off for those losses, so trust me the system is fixed so the businesses NEVER lose. So, don’t lose any

sleep over their “losses.”

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 15

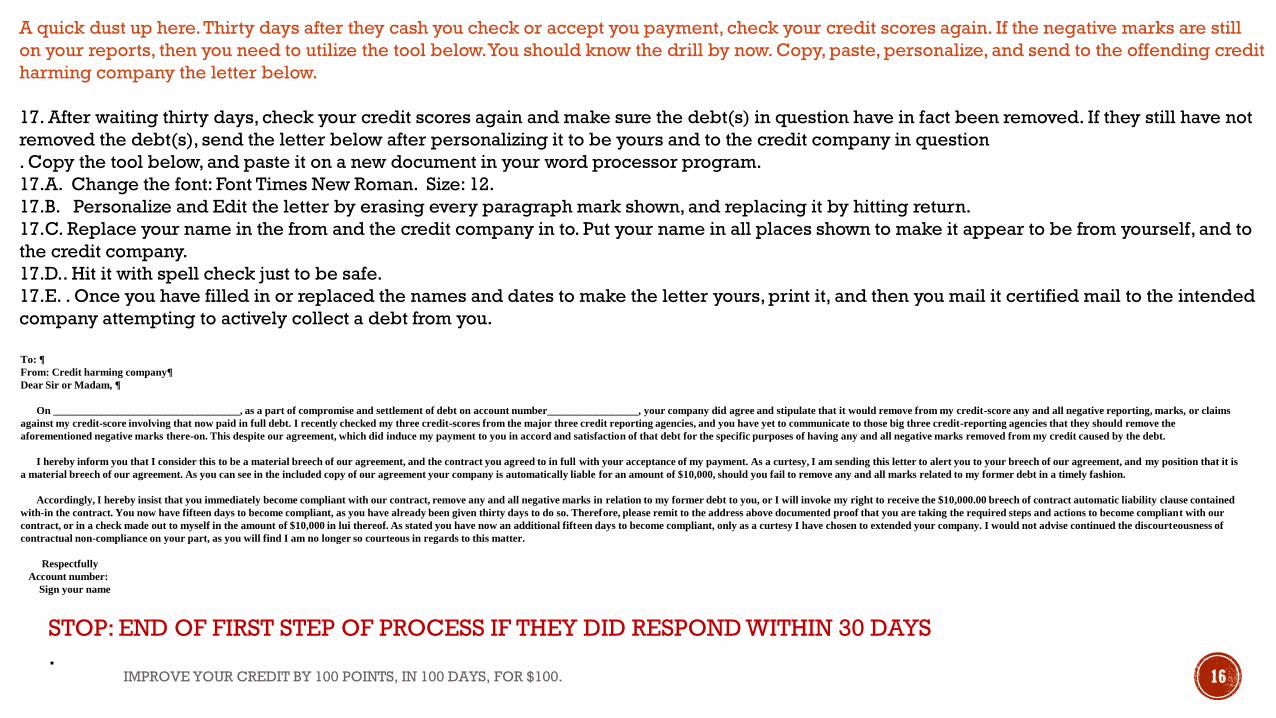

To: ¶

From: Credit harming company¶

Dear Sir or Madam, ¶

On ___________________________________, as a part of compromise and settlement of debt on account number_________________, your company did agree and stipulate that it would remove from my credit-score any and all negative reporting, marks, or claims

against my credit-score involving that now paid in full debt. I recently checked my three credit-scores from the major three credit reporting agencies, and you have yet to communicate to those big three credit-reporting agencies that they should remove the

aforementioned negative marks there-on. This despite our agreement, which did induce my payment to you in accord and satisfaction of that debt for the specific purposes of having any and all negative marks removed from my credit caused by the debt.

I hereby inform you that I consider this to be a material breech of our agreement, and the contract you agreed to in full with your acceptance of my payment. As a curtesy, I am sending this letter to alert you to your breech of our agreement, and my position that it is

a material breech of our agreement. As you can see in the included copy of our agreement your company is automatically liable for an amount of $10,000, should you fail to remove any and all marks related to my former debt in a timely fashion.

Accordingly, I hereby insist that you immediately become compliant with our contract, remove any and all negative marks in relation to my former debt to you, or I will invoke my right to receive the $10,000.00 breech of contract automatic liability clause contained

with-in the contract. You now have fifteen days to become compliant, as you have already been given thirty days to do so. Therefore, please remit to the address above documented proof that you are taking the required steps and actions to become compliant with our

contract, or in a check made out to myself in the amount of $10,000 in lui thereof. As stated you have now an additional fifteen days to become compliant, only as a curtesy I have chosen to extended your company. I would not advise continued the discourteousness of

contractual non-compliance on your part, as you will find I am no longer so courteous in regards to this matter.

Respectfully

Account number:

Sign your name

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 16

A quick dust up here. Thirty days after they cash you check or accept you payment, check your credit scores again. If the negative marks are still

on your reports, then you need to utilize the tool below. You should know the drill by now. Copy, paste, personalize, and send to the offending credit

harming company the letter below.

17. After waiting thirty days, check your credit scores again and make sure the debt(s) in question have in fact been removed. If they still have not

removed the debt(s), send the letter below after personalizing it to be yours and to the credit company in question

. Copy the tool below, and paste it on a new document in your word processor program.

17.A. Change the font: Font Times New Roman. Size: 12.

17.B. Personalize and Edit the letter by erasing every paragraph mark shown, and replacing it by hitting return.

17.C. Replace your name in the from and the credit company in to. Put your name in all places shown to make it appear to be from yourself, and to

the credit company.

17.D.. Hit it with spell check just to be safe.

17.E. . Once you have filled in or replaced the names and dates to make the letter yours, print it, and then you mail it certified mail to the intended

company attempting to actively collect a debt from you.

STOP: END OF FIRST STEP OF PROCESS IF THEY DID RESPOND WITHIN 30 DAYS

.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 17

WELCOME BACK TEAM! OK SO NO MATTER WHICH PROCESS YOU HAD TO USE, YOU SHOULD

END UP HERE WHEN DONE!

QUICK POINTS OF ORDER:

1.

This system is also not effective on COURT ORDERED government fines, fees, medical billings UNLESS

PURCHASED BY A DEBT COLLECTOR, or college tuition loans from the government WHEN COLLECTED BY THE

GOVERNMENT. Sorry, I didn't make the rules, just merely telling you the ones I know work. However, Visa,

MasterCard, any third-party purchaser of debt or third-party collection company (No matter what!), or a rent-to-

own store you're all clear. Just know that large ticket items often serve as the collateral on the loan you take out to

purchase said items. Besides, we're not teaching you how to duck and dodge your bills, merely better handle, and

handle without harm to your credit score the bills you got piling up.

2.

This does not work with utility companies that are currently providing you services. If you are having trouble

paying those bills, contact the company and ask if they or your state have low income aid or programs available.

3.

Repeat the two prior procedures for every single outstanding debt showing on every one of your three credit

reports.

You just kept yet another

hit off your permanent

record, while managing

to pay only a fraction of

the debt you originally

owed. Feeling powerful

yet? Whose da' man or

woman? You da' woman

or man!!!! I told you

they'd be your bitch!

_______________________

Go on to procedure two,

beginning on slide

nineteen!!

18

As it is with all things in life, you may not be able to dispute them all away. You’ve followed the directions on the first eighteen slides, and this creditor just absolutely refuses to work with you on the amount of the debts, and is demanding payment in full no matter what (WHICH IS THEIR LEGAL RIGHT TO DO.), then I suggest the following process:

1. Pay as fast as possible, and possibly negotiate payment plan.

2. Thus far we’ve tried to threatened, negotiated, bargained, and more. Unfortunately, none of that has apparently worked. Therefore, now we beg!

That’s right… We put out the former fire on our tongues, dip them in sugar, and ever so sweetly and respectfully send a personal letter to the CEO of the company that has thus far refused to remove the negative marks from your credit-score. If not the CEO, the highest corporate officer whose name, title, and mailing address you can find.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 19

Company name

Address

Re: Acct # XXXX-XXXX-XXXX-XXXX

Dear CEO of company,

I am writing to you today regarding my credit card account #********************* which I had during ______________________________. The purpose of my correspondence is to see if you would be willing to make a "goodwill" adjustment on the reporting of this

account to the three credit agencies.

During the time period this account was established I had was very happy with the service, I was however not the ideal customer and made mistakes with my handling of the account. I should have kept better records regarding the account and I take full responsibility. I

became aware of the unpaid balance when I got a copy of my credit report in __________date_____________________.

I know that payment was my responsibility and I am not attempting to justify this breach of my user agreement, I was however hoping you might review the circumstances under which this non-payment occurred and consider removing the negative trade line associated

with this account from my three credit reports.

As soon as I became aware of the balance I contacted ----------------- and paid the balance in full. I provide this not to justify why the account was unpaid, but rather to show that the issue with ----------- is not a good indicator of my actual credit worthiness. I hope that ---------

------- is willing to work with me on erasing this mark from my credit reports.

I would like to STRESS that the information currently being reported IS accurate, (I am not disputing anything with ---------------). I am simply asking -------------for a courtesy gesture of goodwill in having the credit bureaus remove this account from my report. I do

recognize that this request is unique and that it may not be ------------- normal policy. Please consider that the Fair Credit Reporting Act does not demand that all accounts be reported, only that any account that is reported be reported accurately. Therefore, a company does

have legal discretion and permission to remove any account it chooses from the credit report. I'm hoping that ------------- will do that in my case for this account.

Your kind consideration in this matter is greatly appreciated.

Best Regards

3. Research the company you owe money to on-line. Figure out that companies structure, core corporate

officers, get the name of the CEO or other officer you plan to write, get the mailing address, and send a

letter like the one below. It is suggested you cut and paste the prefabricated letter below, but adding

your own listed hardships.

4. Now, be sure to send it by name to the person you determine to have the ability and authority to speak

for the company in question, in regards to matters such as these. It should be manager or better!

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 20

PROCEDURE TWO: MARKS OTHER THAN DEBTS

Moving on to the other things that go bump in the night on your credit score, which make it go down like a drunken' prom-date. This is where we contest those nicks and scrapes life leaves on our credit reports.

In law there is a theory, “blanket denial.” Well, that's exactly how we are going to treat the big three credit reporters, and those whom claim a right to cast aversions on your good name and reputation publicly, OK? Therefore, everything found on your credit reports now gets automatically denied and contested.

Why? Well, they should not be allowed to say these things about you if they can't prove those things... right? Of course I'm right, because if they can not prove those debts are valid, that you were late, or whatever it is they want to say on those reports it is slander and you can sue for libel!

BELOW ARE TWO DIFFERENT LETTERS READY FOR YOU TO DO JUST WHAT I'M TALKING ABOUT! By law they must prove or remove! That is your new saying for the big three credit agencies: They must PROVE or REMOVE the negative reported actions.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 21

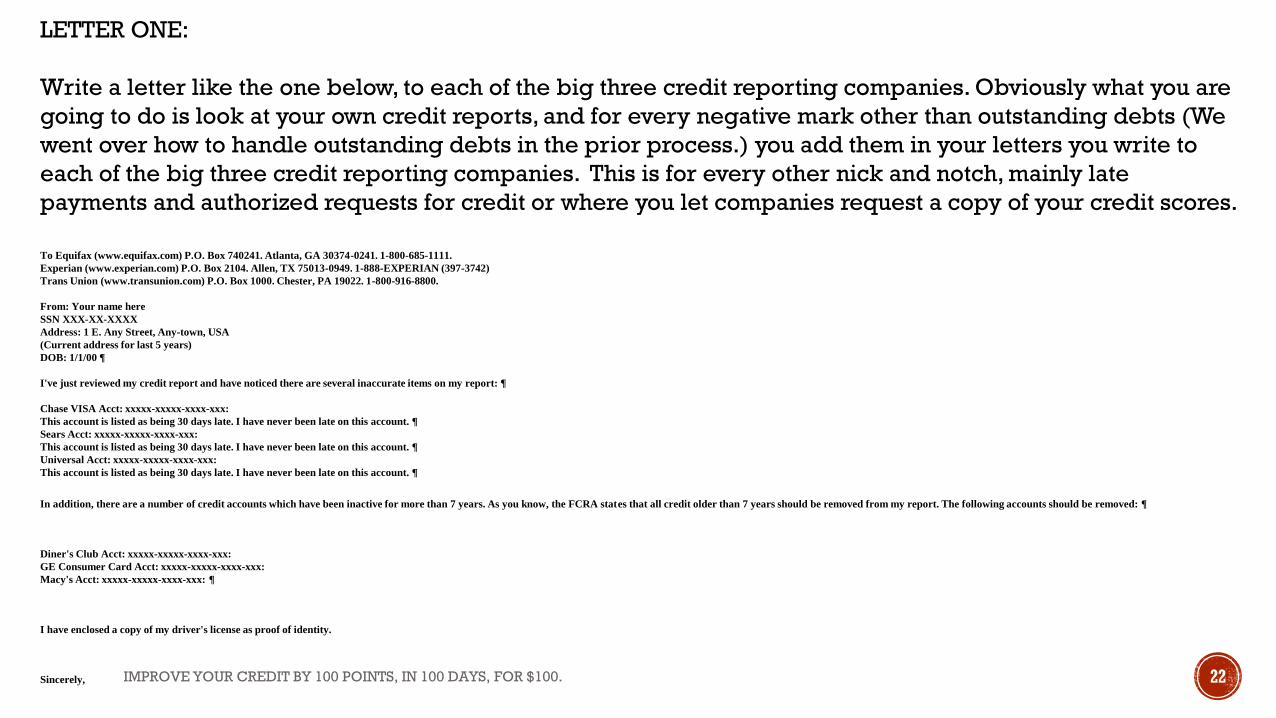

To Equifax (www.equifax.com) P.O. Box 740241. Atlanta, GA 30374-0241. 1-800-685-1111.

Experian (www.experian.com) P.O. Box 2104. Allen, TX 75013-0949. 1-888-EXPERIAN (397-3742)

Trans Union (www.transunion.com) P.O. Box 1000. Chester, PA 19022. 1-800-916-8800.

From: Your name here

SSN XXX-XX-XXXX

Address: 1 E. Any Street, Any-town, USA

(Current address for last 5 years)

DOB: 1/1/00 ¶

I've just reviewed my credit report and have noticed there are several inaccurate items on my report: ¶

Chase VISA Acct: xxxxx-xxxxx-xxxx-xxx:

This account is listed as being 30 days late. I have never been late on this account. ¶

Sears Acct: xxxxx-xxxxx-xxxx-xxx:

This account is listed as being 30 days late. I have never been late on this account. ¶

Universal Acct: xxxxx-xxxxx-xxxx-xxx:

This account is listed as being 30 days late. I have never been late on this account. ¶

In addition, there are a number of credit accounts which have been inactive for more than 7 years. As you know, the FCRA states that all credit older than 7 years should be removed from my report. The following accounts should be removed: ¶

Diner's Club Acct: xxxxx-xxxxx-xxxx-xxx:

GE Consumer Card Acct: xxxxx-xxxxx-xxxx-xxx:

Macy's Acct: xxxxx-xxxxx-xxxx-xxx: ¶

I have enclosed a copy of my driver's license as proof of identity.

Sincerely, IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 22

LETTER ONE:

Write a letter like the one below, to each of the big three credit reporting companies. Obviously what you are

going to do is look at your own credit reports, and for every negative mark other than outstanding debts (We

went over how to handle outstanding debts in the prior process.) you add them in your letters you write to

each of the big three credit reporting companies. This is for every other nick and notch, mainly late

payments and authorized requests for credit or where you let companies request a copy of your credit scores.

Your Name Date

123 Your Street Address

Your City, ST 01234

The Credit Bureau

Bureau Address

Any town, State 56789

Dear Credit Bureau,

This letter is a formal complaint that you are reporting inaccurate credit information. I am very distressed that you have included the below information in my credit profile due to its damaging effects on my good credit standing. As you are no doubt aware, credit

reporting laws ensure that bureaus report only accurate credit information. No doubt the inclusion of this inaccurate information is a mistake on either your or the reporting creditor's part. Because of the mistakes on my credit report, I have been wrongfully denied

credit recently for a <insert credit type for which you were denied here>, which was highly embarrassing and has negatively impacted my lifestyle.

optional With the proof I'm attaching to this letter, I'm sure you'll agree it needs to be removed ASAP. The following information therefore needs to be verified and deleted from the report as soon as possible:

CREDITOR AGENCY, acct. 123-34567-ABC

Please delete the above information as quickly as possible.

Sincerely,

Your Name

SSN# 123-45-6789

Attachment included.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 23

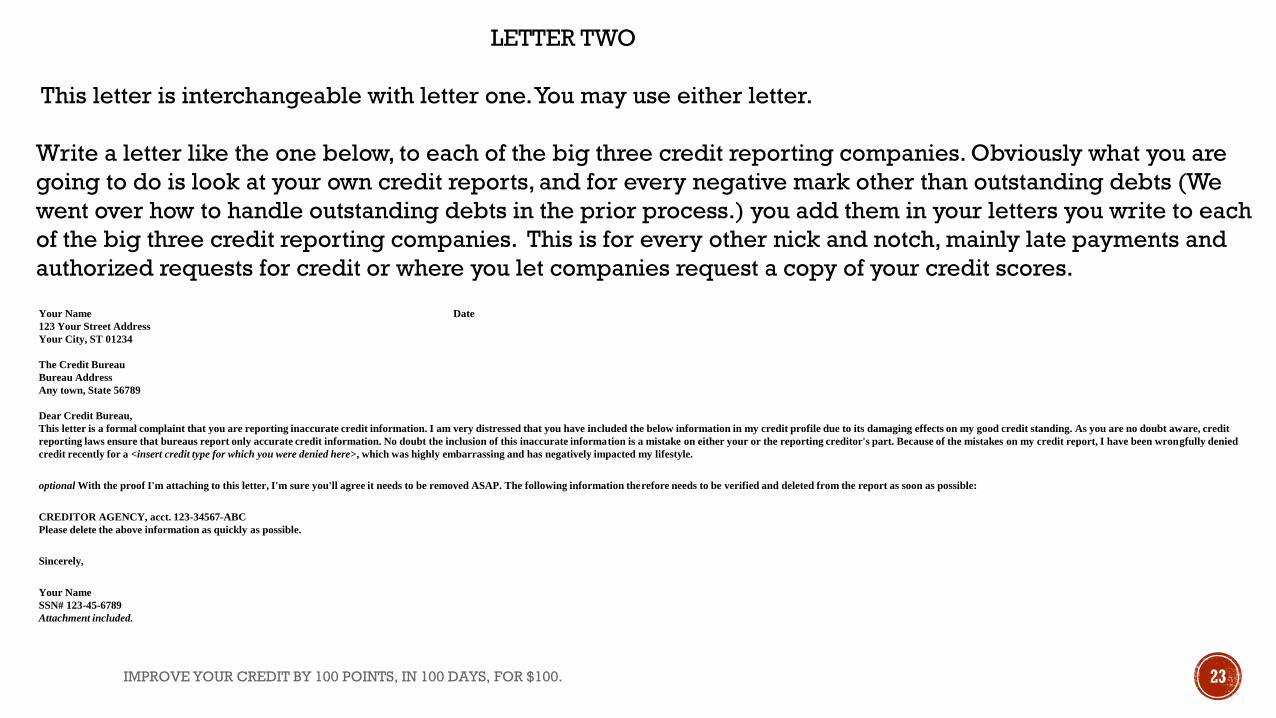

LETTER TWO

This letter is interchangeable with letter one. You may use either letter.

Write a letter like the one below, to each of the big three credit reporting companies. Obviously what you are

going to do is look at your own credit reports, and for every negative mark other than outstanding debts (We

went over how to handle outstanding debts in the prior process.) you add them in your letters you write to each

of the big three credit reporting companies. This is for every other nick and notch, mainly late payments and

authorized requests for credit or where you let companies request a copy of your credit scores.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 24

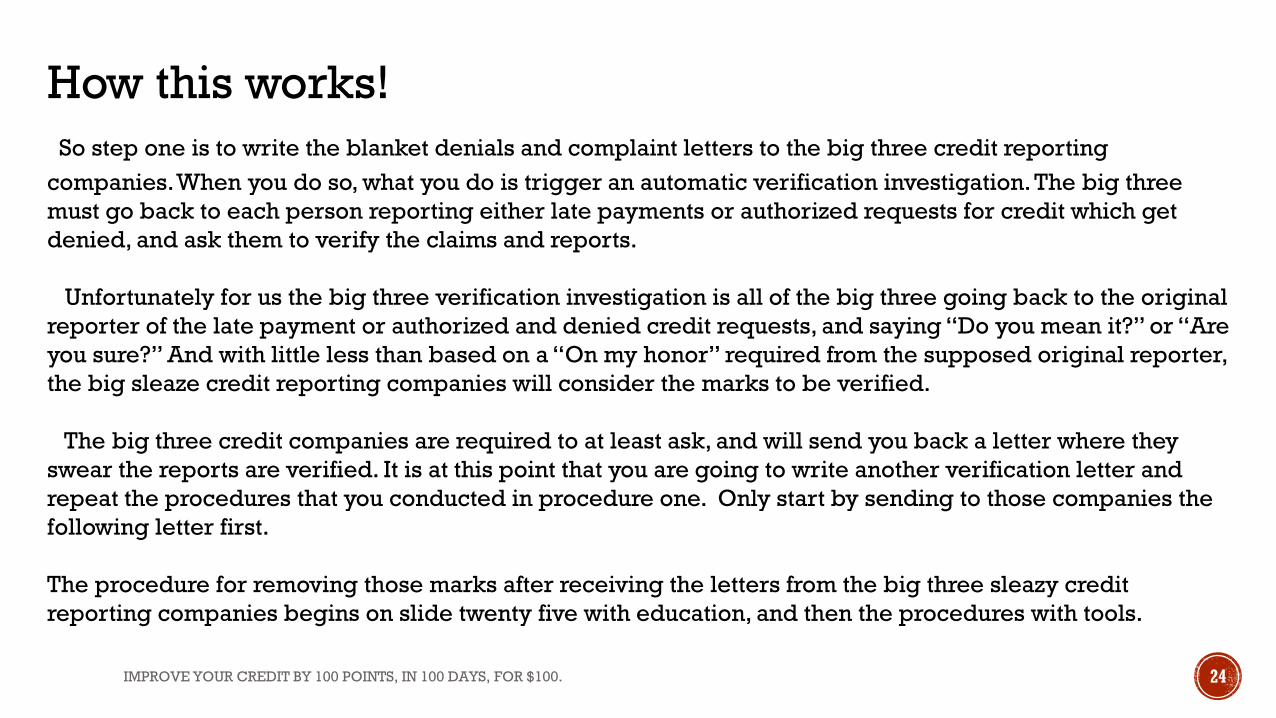

How this works!

So step one is to write the blanket denials and complaint letters to the big three credit reporting

companies. When you do so, what you do is trigger an automatic verification investigation. The big three

must go back to each person reporting either late payments or authorized requests for credit which get

denied, and ask them to verify the claims and reports.

Unfortunately for us the big three verification investigation is all of the big three going back to the original

reporter of the late payment or authorized and denied credit requests, and saying “Do you mean it?” or “Are

you sure?” And with little less than based on a “On my honor” required from the supposed original reporter,

the big sleaze credit reporting companies will consider the marks to be verified.

The big three credit companies are required to at least ask, and will send you back a letter where they

swear the reports are verified. It is at this point that you are going to write another verification letter and

repeat the procedures that you conducted in procedure one. Only start by sending to those companies the

following letter first.

The procedure for removing those marks after receiving the letters from the big three sleazy credit

reporting companies begins on slide twenty five with education, and then the procedures with tools.

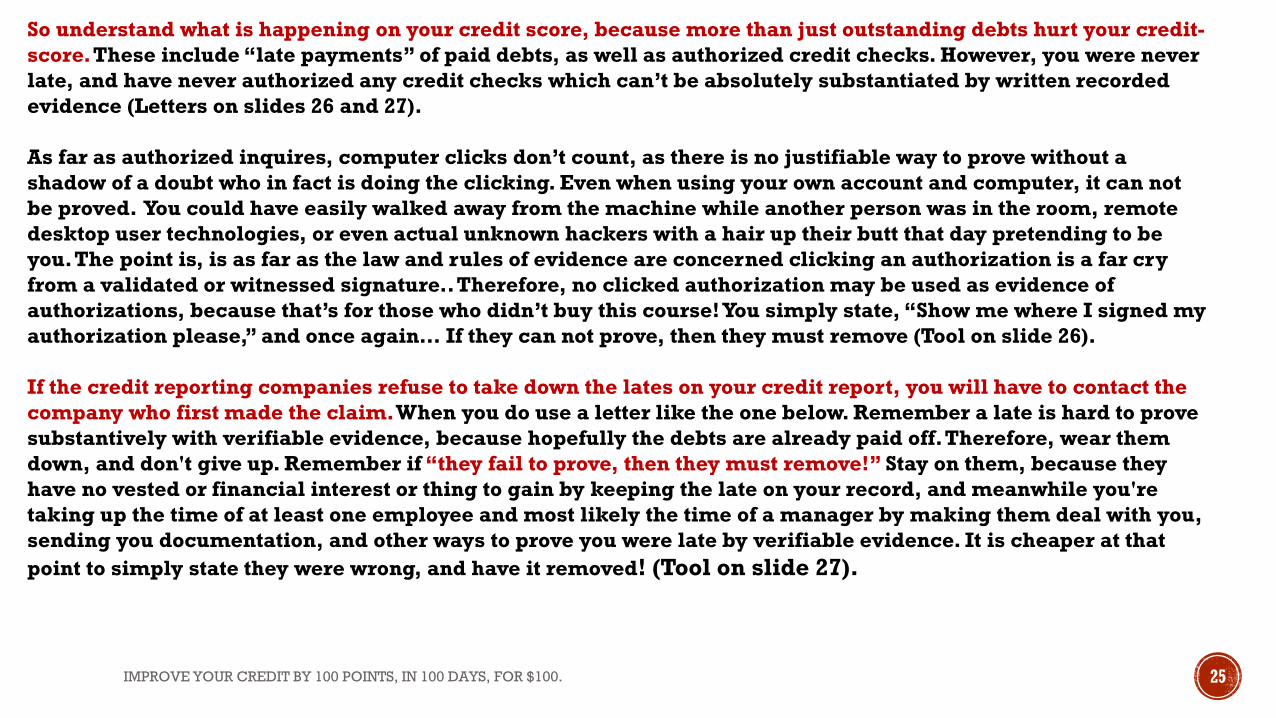

So understand what is happening on your credit score, because more than just outstanding debts hurt your credit-

score. These include “late payments” of paid debts, as well as authorized credit checks. However, you were never

late, and have never authorized any credit checks which can’t be absolutely substantiated by written recorded

evidence (Letters on slides 26 and 27).

As far as authorized inquires, computer clicks don’t count, as there is no justifiable way to prove without a

shadow of a doubt who in fact is doing the clicking. Even when using your own account and computer, it can not

be proved. You could have easily walked away from the machine while another person was in the room, remote

desktop user technologies, or even actual unknown hackers with a hair up their butt that day pretending to be

you. The point is, is as far as the law and rules of evidence are concerned clicking an authorization is a far cry

from a validated or witnessed signature.. Therefore, no clicked authorization may be used as evidence of

authorizations, because that’s for those who didn’t buy this course! You simply state, “Show me where I signed my

authorization please,” and once again… If they can not prove, then they must remove (Tool on slide 26).

If the credit reporting companies refuse to take down the lates on your credit report, you will have to contact the

company who first made the claim. When you do use a letter like the one below. Remember a late is hard to prove

substantively with verifiable evidence, because hopefully the debts are already paid off. Therefore, wear them

down, and don't give up. Remember if “they fail to prove, then they must remove!” Stay on them, because they

have no vested or financial interest or thing to gain by keeping the late on your record, and meanwhile you're

taking up the time of at least one employee and most likely the time of a manager by making them deal with you,

sending you documentation, and other ways to prove you were late by verifiable evidence. It is cheaper at that

point to simply state they were wrong, and have it removed! (Tool on slide 27).

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 25

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 26

Re: Unauthorized Credit Inquiry

Dear American Express,

I recently received a copy of my Experian credit report. The credit report showed a credit inquiry by your company that I do not recall authorizing. You are not allowed to put an inquiry on my file unless I have authorized it.

Please have this inquiry removed from my credit file because it is making it very difficult for me to acquire credit.

I have sent this letter certified mail because I need your prompt response to this issue. Please be so kind as to forward me documentation that you have had the unauthorized inquiry removed.

If you find that I am remiss, and you did have my authorization to inquire into my credit report, then please send me proof of my written verified signature in which I do with knowing purpose authorize your company to make a

credit inquiry on my credit reports.

Thanking you in advance,

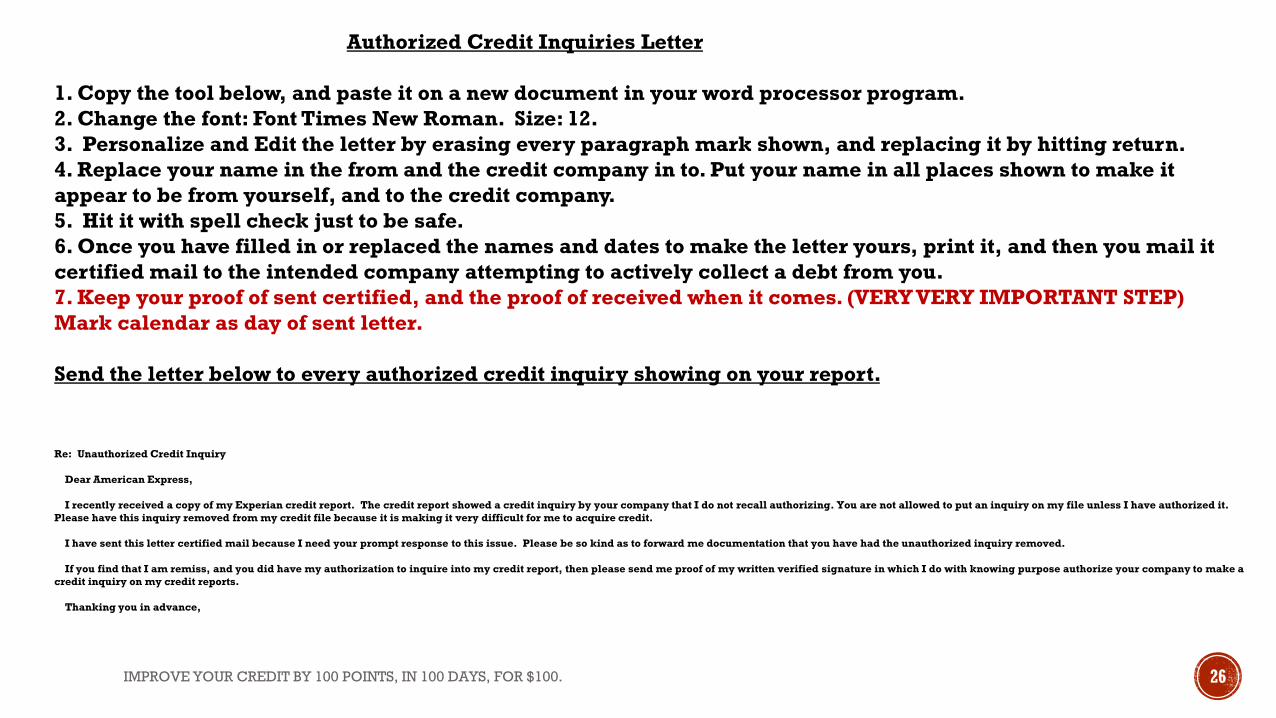

Authorized Credit Inquiries Letter

1. Copy the tool below, and paste it on a new document in your word processor program.

2. Change the font: Font Times New Roman. Size: 12.

3. Personalize and Edit the letter by erasing every paragraph mark shown, and replacing it by hitting return.

4. Replace your name in the from and the credit company in to. Put your name in all places shown to make it

appear to be from yourself, and to the credit company.

5. Hit it with spell check just to be safe.

6. Once you have filled in or replaced the names and dates to make the letter yours, print it, and then you mail it

certified mail to the intended company attempting to actively collect a debt from you.

7. Keep your proof of sent certified, and the proof of received when it comes. (VERY VERY IMPORTANT STEP)

Mark calendar as day of sent letter.

Send the letter below to every authorized credit inquiry showing on your report.

To Whom It May Concern:

I recently pulled my credit report from Experian and TransUnion and to my amazement, saw that you recently have decided to report me 30 days late on this account in _____date_________. I immediately disputed this information with Experian and

TransUnion and the results of the investigation came back "verified". Not only was I never late on this account, but according to the Fair Credit Reporting Act (FCRA), as the information furnisher, you are required to notify me of the insertion of negative

listings.

Since I have disputed the lates with the credit bureaus, and you obviously "verified" them, I am very curious as to what kinds of "records" you may have for this alleged account. Under the FCRA, you are required to conduct an investigation on this account if I

request it. I therefore am submitting my written request to you to conduct an investigation. Per the FCRA, you have 30 days to conduct this investigation and respond to my request. If you do not respond within this time period, per the FCRA, you must remove

this negative information.

Sincerely,

<Your name>

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 27

Reported late Payments Letter

1. Copy the tool below, and paste it on a new document in your word processor program.

2. Change the font: Font Times New Roman. Size: 12.

3. Personalize and Edit the letter by erasing every paragraph mark shown, and replacing it by hitting return.

4. Replace your name in the from and the credit company in to. Put your name in all places shown to make it appear

to be from yourself, and to the credit company.

5. Hit it with spell check just to be safe.

6. Once you have filled in or replaced the names and dates to make the letter yours, print it, and then you mail it

certified mail to the intended company attempting to actively collect a debt from you.

7. Keep your proof of sent certified, and the proof of received when it comes. (VERY VERY IMPORTANT STEP) Mark

calendar as day of sent letter.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 28

To:

From:

Date:

RE: Dispute Letter of Date you sent in first or subsequent requests ¶

Dear _____________________________________________, ¶

This letter is formal notice that you have failed to respond to my dispute letter of __dated_______ I sent this letter registered mail and have enclosed a copy of the return receipt which you signed on

_________date____________________. ¶

As you are well aware, federal law requires you to respond within 30 days. It has now been over that period since your receipt of my letter. As you are no doubt aware, failure to comply with federal

regulations by credit reporting agencies are in serious violation of the Fair Credit Reporting Act and may be investigated by the FTC. Obviously, I am maintaining detailed records of all my

correspondence with you. ¶

The following information failing to be verified inside the statutorily allowed time of 30 days, as evidenced by the certified date of receipt of my last letter, along with certified date you received this

letter, does now statutorily make the information reported incorrect, and therefore must be deleted from the report as soon as possible. Should your company fail to remove the now statutorily

incorrect information, you could be liable for damages to my name and reputation for an amount or award of at least $10,000. I demand you remove the incorrect information you failed to timely verify,

from my credit report in accordance with the Fair Debt Collection Practices Act, 15 USC 1692g Sec. 809. ¶

CREDITOR AGENCY, ¶

acct. 123-34567-ABC¶

Please delete this erroneous item from my credit report as soon as possible. ¶

Sincerely,

Your name

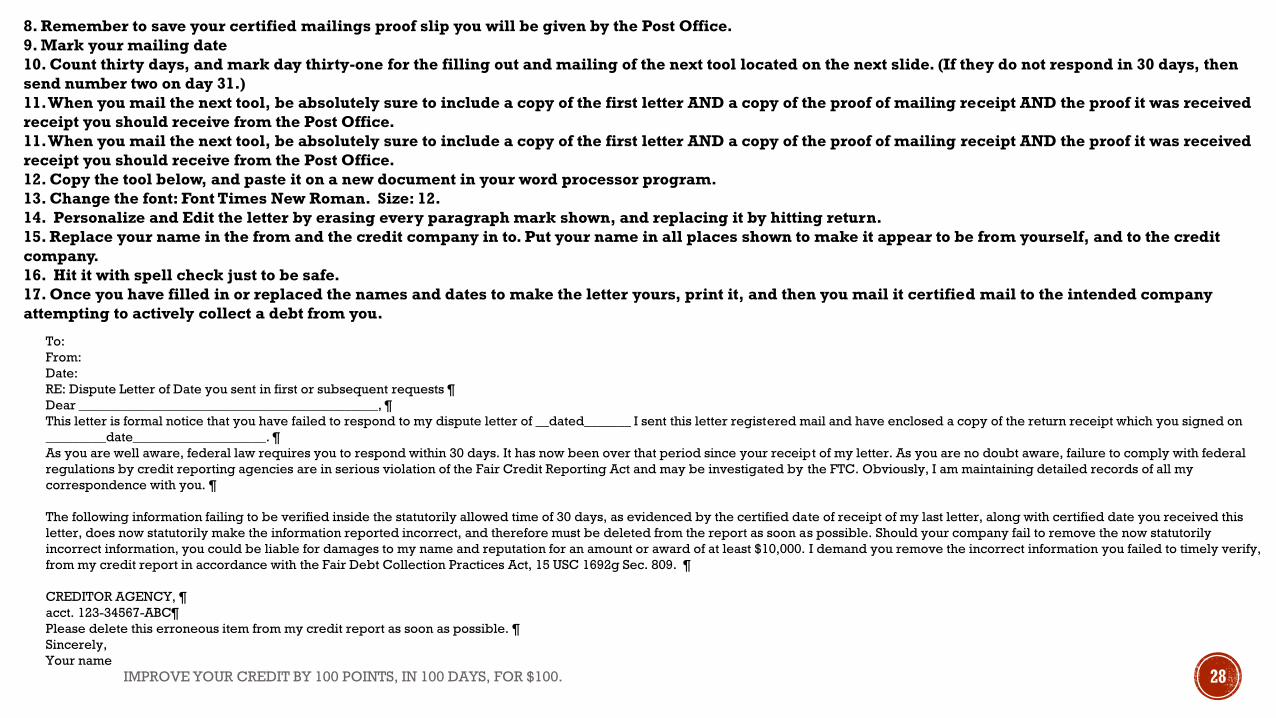

8. Remember to save your certified mailings proof slip you will be given by the Post Office.

9. Mark your mailing date

10. Count thirty days, and mark day thirty-one for the filling out and mailing of the next tool located on the next slide. (If they do not respond in 30 days, then

send number two on day 31.)

11. When you mail the next tool, be absolutely sure to include a copy of the first letter AND a copy of the proof of mailing receipt AND the proof it was received

receipt you should receive from the Post Office.

11. When you mail the next tool, be absolutely sure to include a copy of the first letter AND a copy of the proof of mailing receipt AND the proof it was received

receipt you should receive from the Post Office.

12. Copy the tool below, and paste it on a new document in your word processor program.

13. Change the font: Font Times New Roman. Size: 12.

14. Personalize and Edit the letter by erasing every paragraph mark shown, and replacing it by hitting return.

15. Replace your name in the from and the credit company in to. Put your name in all places shown to make it appear to be from yourself, and to the credit

company.

16. Hit it with spell check just to be safe.

17. Once you have filled in or replaced the names and dates to make the letter yours, print it, and then you mail it certified mail to the intended company

attempting to actively collect a debt from you.

As promised follow

these steps and use

these tools to gain at

least 100 points on

your credit-score, in

less than 100 days,

and for the price of

$100.00.

You are welcome!29

And of course its

equally amazing

author…. Me! Please

check the final slide

for all legal

disclaimers. Have a

great day, and an

amazing life full of

good credit! Until

next time, Goodbye

and nanu-nanu!30

WARRANTY AND LEGAL DISCLAIMER!By utilizing this course or educational product you hereby agree to all of the following stipulations and statements both now and

at all times in the future:

1.Joel Drotts is the sole copyright creator and owner of this course as well as any and all the content, media, writings, photos, names,

intellectual property, any and all derivative works, right to grant or revoke licenses there to, as well as to profit therefrom, which are

contained herein literally, constructively, by reference, or by way of incorporation. Furthermore, you shall respect that copyright

and/or intellectual property and not seek to or actually undertake any actions which may harm those aforementioned copyrights.

2.You understand and agree that Joel Drotts as the course creator, any companies or affiliates aiding in the sales and marketing of

this course are not licensed attorneys. Nothing in contained in the course should be viewed or used as legal advice, nor is it meant to

be legal advice. Nothing found in the course material should in any way be substituted for the sound legal advice of a licensed

attorney. Anything construed as legal advice is clearly subjective on the part of the reader as it is not the actual intent of the creator

and owner of this course.

3.You agree and understand that the course is sold as is, and future results may vary separately from user to user. Success is not now

or at any point guaranteed

4.Your $100.00 purchase was for a single copy of this course, which you agree not to re-sell, copy, or otherwise infringe upon.

5.You agree to hold this course and it's creator, promoters, sellers, and marketers harmless from any and all harms that may occur

caused by your use of this course no matter how those said harms may occur.

6.You agree that the controlling legal jurisdiction shall be San Francisco, California, and the United States of America.

7.The course creators can amend this contract, at any time, for any reason what-so-ever without your permission or knowledge.

8. The course creator and owner does with specificity hereby reserve to himself exclusively any and all rights, powers, and privileges

found in any laws not mentioned directly in this contract agreement.

IMPROVE YOUR CREDIT BY 100 POINTS, IN 100 DAYS, FOR $100. 31

![Semester Course Code Course Title Credit. Mathematics Elective(Pass) Course Course Structure Semester Course Code Course Title Credit I ET-5 ... Text Books : [1] Mathematical Analysis;](https://static.fdocuments.us/doc/165x107/5ad3ba107f8b9a482c8e2526/semester-course-code-course-title-credit-mathematics-electivepass-course-course.jpg)