CREDIT CARD - A THEORETICAL FRAMEWORK - Shodhganga

62

lxxxv Chapter II CREDIT CARD - A THEORETICAL FRAMEWORK 2.1. INTRODUCTION Oxford Dictionary and Thesaurus defines “credit card authorizing purchase of goods on credit”. Credit cards are innovative instruments in the area of financial services offered by commercial banks. The concept of credit cards was first developed by Diners’ club founder Frank McNamara, an American businessman who found himself without cash at a weekend resort founded Diner’s card in 1950. American Express issued their first credit card in 1958. Bank of America issued the Bank Americard (now Visa) bank credit card later in 1958. Right from that time, the commercial banks and non-banking companies in the USA adopted the concept of credit cards to develop their business. Barclays Bank was the first bank to introduce credit card in 1966 in Britain. 102 The credit card business got momentum in the sixties and a number of banks entered the field in a big way. Credit card culture is an old hat in western countries. In India, it is relatively a new concept that is fast catching on. The present trend indicates that the coming years will witness a burgeoning growth of credit cards which will lead to a cashless society. Credit has become an important vehicle of trade promotion. Credit cards provide convenience and safety to the buying process. One of the important reasons for the popularity of credit cards is the sea change witnessed in consumer behaviour. Credit cards enable an individual to purchase products or services without paying immediately. The buyer only needs to present the credit cards at the cash counter and sign the bill. Credit card can, therefore, be considered as a good substitute for cash or cheques. 103 102 http://inventors.about.com/od/cstartinventions/a/credit_cards.htm. 103 S. Gurusamy (2007). Merchant Banking and Financial Services. Chennai: Vijay Nicole Imprints Private Limited, p.344.

Transcript of CREDIT CARD - A THEORETICAL FRAMEWORK - Shodhganga

lxxxv

Chapter II

CREDIT CARD - A THEORETICAL FRAMEWORK

2.1. INTRODUCTION

Oxford Dictionary and Thesaurus defines “credit card authorizing purchase

of goods on credit”. Credit cards are innovative instruments in the area of financial

services offered by commercial banks. The concept of credit cards was first

developed by Diners’ club founder Frank McNamara, an American businessman

who found himself without cash at a weekend resort founded Diner’s card in 1950.

American Express issued their first credit card in 1958. Bank of America issued the

Bank Americard (now Visa) bank credit card later in 1958. Right from that time, the

commercial banks and non-banking companies in the USA adopted the concept of

credit cards to develop their business. Barclays Bank was the first bank to introduce

credit card in 1966 in Britain.102

The credit card business got momentum in the sixties and a number of banks

entered the field in a big way. Credit card culture is an old hat in western countries.

In India, it is relatively a new concept that is fast catching on. The present trend

indicates that the coming years will witness a burgeoning growth of credit cards

which will lead to a cashless society. Credit has become an important vehicle of

trade promotion. Credit cards provide convenience and safety to the buying process.

One of the important reasons for the popularity of credit cards is the sea change

witnessed in consumer behaviour. Credit cards enable an individual to purchase

products or services without paying immediately. The buyer only needs to present

the credit cards at the cash counter and sign the bill. Credit card can, therefore, be

considered as a good substitute for cash or cheques.103

102 http://inventors.about.com/od/cstartinventions/a/credit_cards.htm. 103 S. Gurusamy (2007). Merchant Banking and Financial Services. Chennai: Vijay Nicole

Imprints Private Limited, p.344.

lxxxvi

A Credit card is a card or mechanism which enables cardholders to purchase

goods, travel and dine in a hotel without making immediate payments. The holders

can use the cards to get credit from banks up to 50 days free of cost. The credit card

relieves the consumers from botheration of the carrying cash and ensures safety. It is

a convenience of extended credit without formality. Thus credit card is a passport to,

“safety, convenience, prestige and credit.”104 A credit card is a plastic card having a

magnetic strip, issued by a bank or business authorizing the holder to buy goods or

services on credit. Any card, plate or coupon book that may be used repeatedly to

borrow money or buy goods and services on credit is called credit card.105

A credit card is a card establishing the privilege of the person to whom it is

issued to charge bills. Most retail firms accept credit cards. Credit cards allow

consumers to make purchases without paying cash immediately or establishing credit

with individual stores. They eliminate the need to check credit ratings and to collect

cash from individual customers. The issuing institution establishes the card’s terms,

including the interest rate, annual fees, penalties, the grace period, and other features.

Credit card debt is typically an unsecured debt. Repossession is not easily

accomplished by the lender to ensure payment. Banks have often priced the product

assuming maximum risk exposure.106

A credit card is a device which enables the holder to obtain goods on credit

from specified supplies. The holder of the card, in some cases, has to pay the yearly

subscription and the suppliers also have to pay commission on sales to the bank or

the body issuing the card. The suppliers are paid promptly and so are protected

against bad debts, while the holder makes a single monthly payment to cover all his

purchases for that period. Credit cards are issued only after the applicant’s credit

worthiness has been accepted as satisfactory. According to credit rating, holder of

104 E. Gordon and K. Natarajan (2006). Financial Markets and Services. New Delhi: Himalaya

Publishing House, pp.414. 105 http://www.advfn.com/money-words_term_1199_credit_card.html. 106 C.J. Woelfel (1994). Encyclopedia of Banking and Finance. New Delhi: S. Chand and

Company Limited, pp.267.

lxxxvii the credit card may be allowed a specified amount of credit from one month to

another.107

A credit card, as the name indicates, enables the cardholder to enjoy credit

from the issuing bank for a specific period after the purchases. During this

intervening period, the cardholder is allowed to use the card for incurring further

expenses.108 A bankcard is used to make an electronic withdrawal from funds on

deposit in a bank, as in purchasing goods or obtaining cash advances. Credit cards

are one of the most popular forms of payment for consumer goods and services in the

United States.

2.2. HISTORY AND DEVELOPMENT OF CARD

As far back as the late 1800s, consumers and merchants exchanged goods

through the concept of credit, using credit coins and charge plates as currency. It

was not until about half a century ago that plastic payments as we know them today

became a way of life. The most common pre-plastic credit instruments were charge

plates, celluloid “coins” and charge coins.109

The concept of using a card for purchases was described in 1887 by Edward

Bellamy in his Utopian novel Looking Backward. Bellamy used the term credit card

eleven times in his novel.110 In the early 1900s, oil companies and department stores

issued their own proprietary cards. Such cards were accepted only at the business

that issued the card and in limited locations. While modern credit cards are mainly

used for convenience, these predecessor cards were developed as a means of creating

customer loyalty and improving customer service.111 The modern credit card was

107 J.L. Hamson (1970). The Structure of Modern Commerce. London: The English Language

Boom Society and Maclonaled and Evans Ltd., p.170. 108 RBI (1994). Report of the Committee on Technology Issues Relating to Payment System,

Cheque Clearing and Security Settlement in the Banking Industry, Mumbai: RBI, pp.75. 109 http://www.creditcards.com/credit-card-news/credit-cards-history-1264.accessed on

December 18, 2007. 110 E. Bellamy (1888). Looking Backward 2000-1887 (Utopion novel). United States: William Ticknor Publisher, pp.470.

111 S. Sienkiewicz (2007). in a paper for the Philadelphia Federal Reserve Bank entitled “Credit cards and payment efficiency.” Published December 18. papers.ssrn.com/sub/papers cfm?abstract Id=927493.

lxxxviii the successor of a variety of merchant credit schemes. It was first used in the 1920s

in the United States, specifically to sell fuel to accepting each other's cards. Western

Union had begun issuing charge cards to its frequent customers in 1914. Some

charge cards were printed on paper card stock, but were easily counterfeited.

The Charga-Plate was an early predecessor to the credit card and used during

the 1930s and late 1940s. Charga-Plate was a trademark of Farrington Manufacturing

Co. Charga-Plates was issued by large-scale merchants to their regular customers,

much like department store credit cards of to-day. The first bank card, named

"Charg-It," was introduced in 1946 by John Biggins, a banker in Brooklyn. When a

customer used it for a purchase, the bill was forwarded to Biggins' bank. The bank

reimbursed the merchant and obtained payment from the customer. Purchases could

only be made locally, and “Charg-It” cardholders had to have an account at Biggins'

bank. In 1951, the first bank credit card appeared in New York's Franklin National

Bank for loan customers. It also could be used only by the bank account holders.112

The concept of paying different merchants using the same card was invented

in 1950 by Ralph Schneider and Frank X. McNamara, founders of Diners Club, to

consolidate multiple cards. The Diners Club, which was created partially through a

merger with Dine and Sign, produced the first "general purpose" charge card, and

required the entire bill to be paid with each statement. That was followed by Carte

Blanche and in 1958 by American Express which created a worldwide credit card

network.113 The Bank of America created the Bank Americard in 1958, a product

which, with its overseas affiliates, eventually evolved into the Visa system.

MasterCard came to being in 1966 when a group of credit-issuing banks established

Master Charge. It received a significant boost when Citibank merged its proprietary

‘Everything Card’, launched in 1967, into Master Charge in 1969. The fractured

nature of the U.S. banking system meant that credit cards became an effective way

for those who were traveling around the country to move their credit to places where

112 http://www.creditcards.com/credit-card-news/credit-cards-history, accessed on December 18,

2007, IST 18.00 hrs. 113 http://en.wikipedia.org/wiki/Diners_Club_IST16.00hrs_20th _October_2008 (accessed).

lxxxix they could not directly use their banking facilities. In 1966, Barclaycard in the UK

launched the first credit card outside the U.S.114

There are now countless variations on the basic concept of revolving credit

for individuals (as issued by banks and honoured by a network of financial

institutions), including organization-branded credit cards, corporate-user credit cards,

store cards and so on.115

2.3. FEATURES OF CARD

The features of modern credit cards such as owner identification, credit limit

for its cardholders and floor limit for its merchant establishments, convenience and

safety to add value of cards, wider usage or popularity all over the world and

dependence on technology to keep operating cost to the minimum, have been a

runaway success for credit cards.116

Along with convenient, accessible credit, credit cards offer consumers an

easy way to track expenses, which is necessary for both monitoring personal

expenditures and the tracking of work-related expenses for taxation and

reimbursement. Credit cards are accepted worldwide, and are available with a large

variety of credit limits, repayment arrangement, and other perks (such as rewards

schemes in which points earned by purchasing goods with the card can be redeemed

for further goods and services or credit card cash back). Some countries, such as the

United States, the United Kingdom, and France, limit the amount for which a

consumer can be held liable due to fraudulent transactions as a result of a consumer's

credit card being lost or stolen. A credit card is part of a system of payments named

after the small plastic card issued to users of the system. The issuer of the card grants

a line of credit to the consumer (or the user) from which the user can borrow money

for payment to a merchant or as a cash advance to the user. A credit card is different

from a charge card, which requires the balance to be paid in full each month. In

114 www.mastercards.com 115 http://en.wikipedia.org/wiki/creditcard. 116 S. Gurusamy (2007). op. cit., p.343.

xc contrast, credit cards allow the consumers to 'revolve' their balance, at the cost of

having interest charged. Most credit cards are issued by local banks or credit unions,

and have the same shape and size, as specified by the ISO 7810 standard.117

2.4. EVOLUTION AND GROWTH OF CARD

The number of credit and debit card users in India is climbing fast, and rising

affluence is likely to erode Indians’ lingering reluctance to spend on credit. Indians

have traditionally valued thrift and frugality. But the spread of affluence in the wake

of rapid economic growth is challenging these values, at least for many middle-class

and high-income families. One sign of this is the phenomenal growth in the number

of credit and debit cards in India—in the past three years, the number of credit cards

has more than doubled and the number of debit cards has almost quadrupled.

Credits cards are a relatively recent development. The VISA Company, for

example, traces its history back to 1958 when the Bank of America began its Bank

Americard program. In the mid-1960s, the Bank of America began to license banks

in the United States the rights to issue its special Bank Americards. In 1977 the name

Visa was adopted internationally to cover all these cards. VISA became the first

credit card to be recognized worldwide.118

Credit cards are relatively new to India. Andhra Bank and Central Bank of

India introduced credit cards in 1981. As of now there are about more than dozen

major banks in Indian and foreign which have entered this line of business, besides

some non-banking institutions. Since the plastic money has become as good as legal

tender more people are using them in their day-to-day activities. The attitude of

people towards credit cards has changed.

A phenomenal amount of money moves get transacted nowadays through

electronic transfer, credit cards and debit cards. The Indian credit card market is in

its growth phase, it recorded a growth of about 30 per cent a year. Debit cards are

117 http://en.wikipedia.org/wiki/credicard. 118 http://www.corporate.visa.com

xci growing at 40 per cent. The RBI data put total electronic transaction in the country at

over Rs.2,35,000 crores in 2006-07. This increased to Rs.3,60,000 crores in the first

10 months (April-January) of 2007-08. At the end of April-January 2007-08, all of us

together held about 27.5 million credit cards transacted Rs.47,476 crores through

these cards in 10 months of the year.119

The Indian credit cards industry is still in a relatively nascent stage when

compared to economies in West Asia, a survey by Master Card International.

According to the survey results, only 14 per cent of Indians currently own a credit

card. This is in sharp contrast to countries such as the United Arab Emirates and

Kuwait where 63 per cent and 50 per cent of respondents, respectively, own a credit

card. The results indicate that the high growth potential for the payment card

industry in India,

In terms of the single most important factor influencing choice of credit card,

30 per cent of Indians say they are influenced by the credit card brand, closely

followed by 23 per cent who choose a credit card depending on the credit limit.

Interestingly, 8 per cent of cardholders say they are influenced by the card design,

while only 5 per cent and 2 per cent cardholders say they are influenced by the

interest rate and the bank staff recommendations respectively.120

2.4.1. Drivers of growth in card payment market

Several factors have combined to fuel the astonishing growth in the use of

credit and debit cards in India. Apart from the convenience offered by cards, these

factors include the following:

1. Rising consumerism

2. Improved payment infrastructure

3. Competition and lower costs

4. Co-branding

119 Priya Ranjan Dash. “Your credit card under watch.” Financial Chronicle. Chennai, (April

17, 2008), p.16. 120 Business Line. New Delhi (December 27, 2007). Survey accessed online on 17th Dec., 2007.

xcii

xciii 2.4.2. Credit card outstanding rising in India

The outstanding on plastic cards has risen by more than 50 per cent to Rs

19,345 crores as on February 15, 2008 according to the RBI. The credit card industry

in India is still nascent according to VISA. Indians make just 1 per cent of their total

purchases by credit cards against 20 per cent by Koreans. The global average is

around 9 per cent. The Indian Credit Card market is expected to touch 55 million

cards by 2010-2011.121

2.4.3. Indian credit card user base grows 30% YoY

India had just 3.5 million credit cards in 2000. As of March-2006, the number

has swelled to 19 million, by January 2007 there were 22 million credit cards in

India at the end of April-March 2007-08, all together held about 28 million credit

cards and Indian had already transacted Rs.56,846 crores through these cards in the

year. It represents the average growth of 30 per cent yearly. Not just the number of

users have increased, but also the average spending has gone up from $368

(Rs.16,560) in 2000 to $437 (Rs.19,665) in 2006 and in 2007-08 to Rs.56,846

crores.122

2.4.4. SBI to increase co-branding credit business

SBI card which is a subsidiary of the State Bank of India and operating as an

NBFC is exploring the option of tying up with regional banks to expand its national

footprint. SBI card has forged alliance with United Bank of India and Catholic

Syrian Bank, as first step in this direction. It also has alliance with the Indian

Railways, Tatas, Hero Honda for co-branded. The credit card industry in India is

growing annually at the rate of 30 per cent, while SBI has been growing at the rate of

45 per cent. SBI is one of the big players of credit cards in India with 3.6 million

customers.123

121 www.cardbhai_com/reliance_creditcard_launched_creditcard_in.html (Accessed on May

05, 2008) at 10.58 p.m. 122 Ibid. 123 Ibid.

xciv 2.5. PLASTIC CARD TREND

2.5.1. Volume and value of transaction in India

By January 2004, there were 10 million credit cards in India. The number of

debit cards was much larger at 18 million. Although there are fewer credit than debit

cards in circulation, the total volume and value of credit card transactions is much

higher. One of the reasons for the rise is easier to obtain credit than personal loans.

TABLE 2.1 Volume and value of credit and debit card transaction in Indian banking

(Volume in Lakh and Value (Rs.) in crore)

Credit card transaction Debit card transaction Year

Volume Value Volume Value

2003-04 1,002 17,663 377.57 4,874

2004-05 1,295 25,686 415.32 5,361

2005-06 1,561 33,886 456.86 5,897

2006-07 1,695 41,361 601.77 8,172

2007-08 2,282 57,985 883.06 12,521

2008-09 2,596 65,356 1,276.54 18,547

% Growth 2008-09

over 2007-08 13.76 12.71 44.56 48.13

Source: Reserve Bank of India, Money and Banking - Monthly Bulletin (May 2009).

The above table shows that the value and volume of credit and debit card

during the financial year between 2003-04 and 2008-09. It reveals that the number of

credit and debit card transaction grew by 159 per cent and 238 per cent respectively

in six financial year ending on March 2009. The value of credit and debit card

transactions were also increased to 270 per cent and 281 per cent respectively in the

same period.

In the previous year ending 2008-09 over 2007-08, credit and debit card

transaction growing up in 13.76 per cent by volume and 44.56 per cent by value and

xcv 12.71 per cent and 48.13 per cent in value respectively in the same period. It is

concluded that there was a growth of credit and debit cards by volume and value in

India.

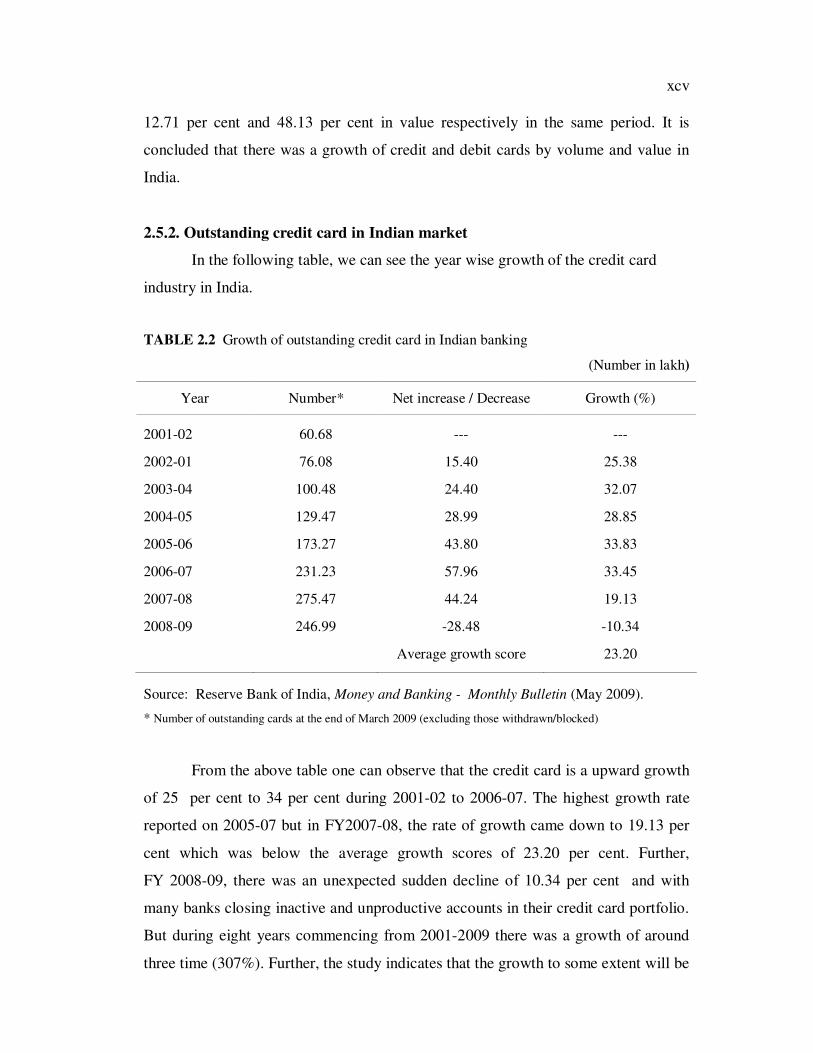

2.5.2. Outstanding credit card in Indian market

In the following table, we can see the year wise growth of the credit card

industry in India.

TABLE 2.2 Growth of outstanding credit card in Indian banking

(Number in lakh)

Year Number* Net increase / Decrease Growth (%)

2001-02 60.68 --- ---

2002-01 76.08 15.40 25.38

2003-04 100.48 24.40 32.07

2004-05 129.47 28.99 28.85

2005-06 173.27 43.80 33.83

2006-07 231.23 57.96 33.45

2007-08 275.47 44.24 19.13

2008-09 246.99 -28.48 -10.34

Average growth score 23.20

Source: Reserve Bank of India, Money and Banking - Monthly Bulletin (May 2009).

* Number of outstanding cards at the end of March 2009 (excluding those withdrawn/blocked)

From the above table one can observe that the credit card is a upward growth

of 25 per cent to 34 per cent during 2001-02 to 2006-07. The highest growth rate

reported on 2005-07 but in FY2007-08, the rate of growth came down to 19.13 per

cent which was below the average growth scores of 23.20 per cent. Further,

FY 2008-09, there was an unexpected sudden decline of 10.34 per cent and with

many banks closing inactive and unproductive accounts in their credit card portfolio.

But during eight years commencing from 2001-2009 there was a growth of around

three time (307%). Further, the study indicates that the growth to some extent will be

xcvi impacted by the current financial turmoil and credit squeeze. Bankers will also

become a little more conscious while doing risk evaluation of card applicants upon

expiration of the card, banks did not renew for some customers and some canceled

the cards voluntarily or by force due to more default rate and credit losses of the

banks. It could also be customer consolidation because multiple cards becoming

unmanageable by the users. The overall trend will remain positive over the past

periods. It is concluded that there was a growth of credit card business in India and

the need for credit does not diminish.

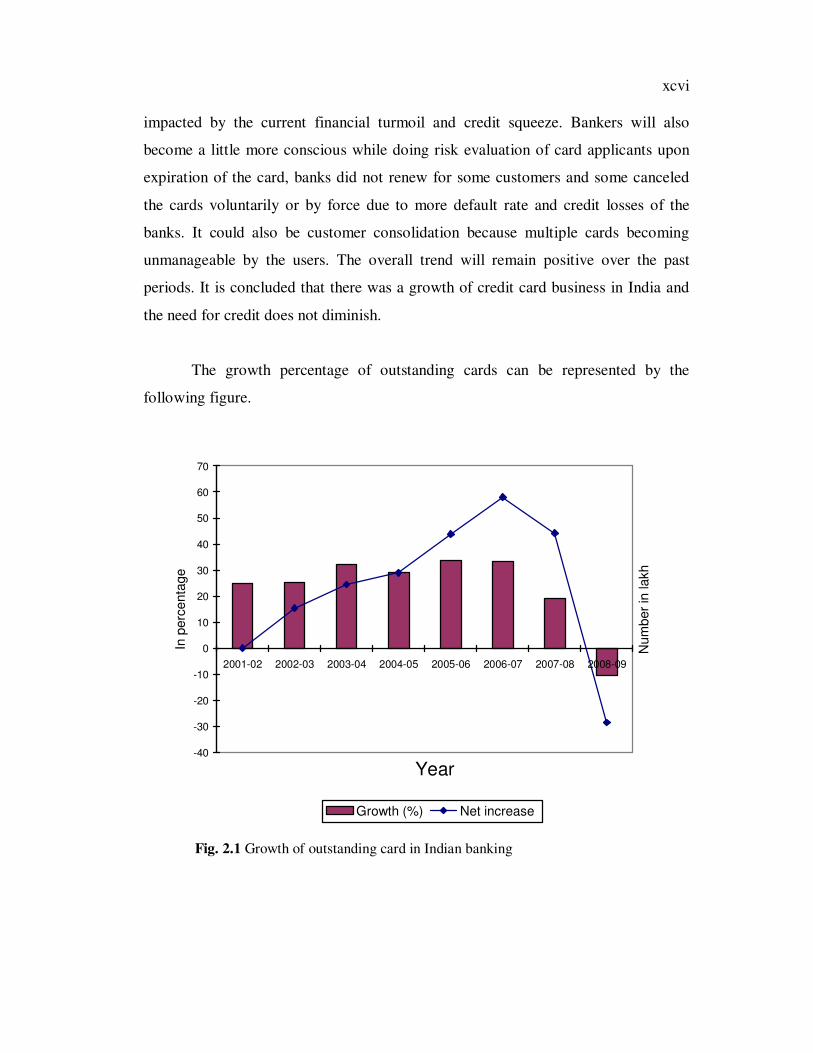

The growth percentage of outstanding cards can be represented by the

following figure.

-40

-30

-20

-10

0

10

20

30

40

50

60

70

2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09

Year

In p

erc

enta

ge

Num

ber

in lakh

Growth (%) Net increase

Fig. 2.1 Growth of outstanding card in Indian banking

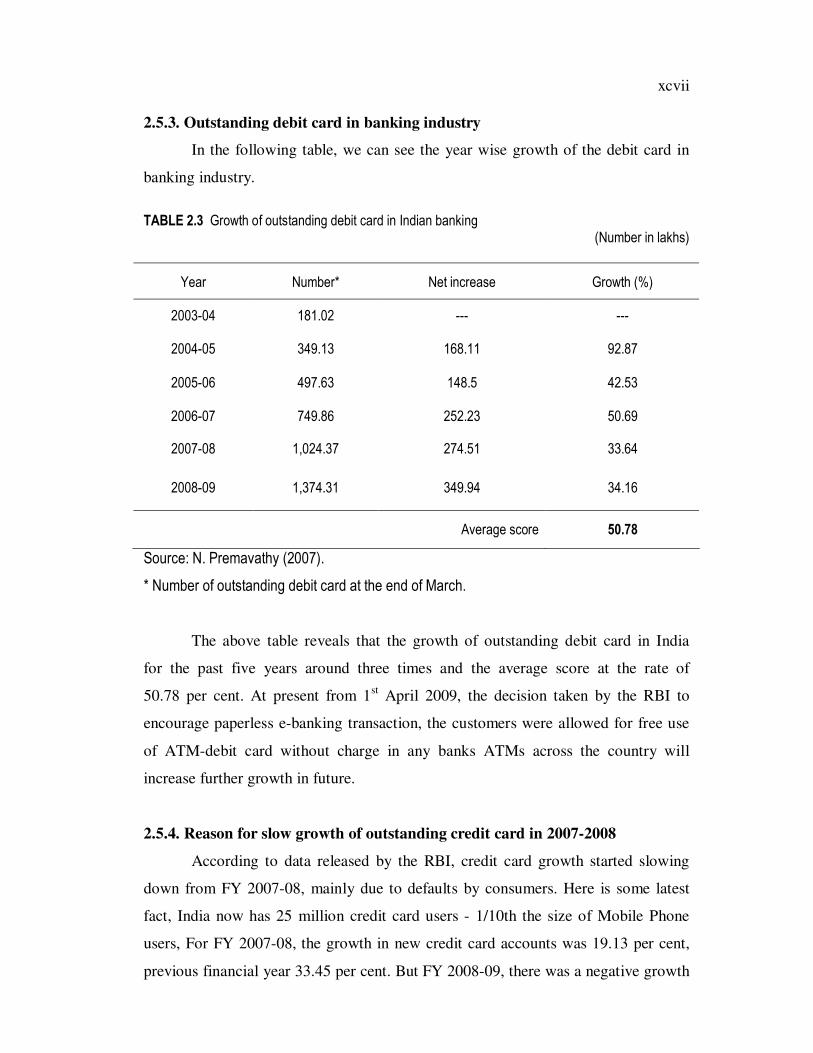

xcvii 2.5.3. Outstanding debit card in banking industry

In the following table, we can see the year wise growth of the debit card in

banking industry.

TABLE 2.3 Growth of outstanding debit card in Indian banking (Number in lakhs)

Year Number* Net increase Growth (%)

2003-04 181.02 --- ---

2004-05 349.13 168.11 92.87

2005-06 497.63 148.5 42.53

2006-07 749.86 252.23 50.69

2007-08 1,024.37 274.51 33.64

2008-09 1,374.31 349.94 34.16

Average score 50.78

Source: N. Premavathy (2007).

* Number of outstanding debit card at the end of March.

The above table reveals that the growth of outstanding debit card in India

for the past five years around three times and the average score at the rate of

50.78 per cent. At present from 1st April 2009, the decision taken by the RBI to

encourage paperless e-banking transaction, the customers were allowed for free use

of ATM-debit card without charge in any banks ATMs across the country will

increase further growth in future.

2.5.4. Reason for slow growth of outstanding credit card in 2007-2008

According to data released by the RBI, credit card growth started slowing

down from FY 2007-08, mainly due to defaults by consumers. Here is some latest

fact, India now has 25 million credit card users - 1/10th the size of Mobile Phone

users, For FY 2007-08, the growth in new credit card accounts was 19.13 per cent,

previous financial year 33.45 per cent. But FY 2008-09, there was a negative growth

xcviii of -10.34 per cent. ICICI Bank is now the largest credit card issuing bank in India

with 9 million cards on March end 2008. Defaulters on credit card are up by 12 per

cent when compared to 10 per cent in FY 06-07. One of the reasons attributed to

higher default rate in other retail debt is demanding higher EMIs which have put

pressure on individuals. Also over leveraging up to 20 times their annual income on

loans has led to the rise of defaulters. International financial crisis is also another

reason to reduce the borrowing power and increase the default rates of customers.124

2.5.5. Negative growth of outstanding credit card in 2008-2009

Credit losses on credit cards in India are relatively high at Rs.3,420 per active

card per year vis-a-vis Rs.3,070 in the US and Rs.1,220 in Australia, according to a

study commissioned by MasterCard’s India Cards Council (ICC). The study pointed

out that insufficient inputs were used to check the credit-worthiness of applicants and

absence of annual fees encouraged customers to hold cards from multiple banks,

resulting in a high level of inactive cards. Hence, none of the issuers have been

aggressively marketing cards in the past few months. Credit card norms have been

tightened. Issuers have raised the minimum income requirements across the board

and also the cut-off scores for issuances on these cards.125

The negative impact of the economic slowdown is clearly showing on the

credit cards segment. The number of outstanding credit cards declined drastically by

25 million in FY ending on March, 2009 from 28 million on March, 2008. The credit

card business is facing a slowdown as rising defaults have prompted banks to tighten

due-diligence procedures. The new issuance of cards has seen a slowdown because

of credit losses. Recently, State Bank of India admitted that its losses on the credit

card business were of the order of Rs.150 crores and non performing assets (NPAs)

on this portfolio had touched a whopping 16.5 per cent during the financial year

ending on 2007-08.126 The Indian credit card market the number of outstanding

cards at the end of March 2009 was reduced (25 million) due to blocked and

124 www.cardbhai_com. March 05, 2008 at 11.05 p.m. 125 Ibid. 126 www.creditcard.india.com

xcix withdrawn of inactive cards. This may reduce more default rate and credit losses of

banks in India.

2.6. MAJOR BANKS ISSUING CARD IN INDIA

The major credit card issuers in India are as follows:

1. ABN AMRO credit card 11. HDFC credit card 2. Andhra Bank card 12. HSBC bank card 3. Axis Bank Credit cards 13. ICICI credit card 4. Bank of Baroda credit card or

BoB credit card 14. Indian Overseas Bank card

5. Bank of India card 15. Stand Chart credit card 6. Barclays Bank credit card. 16. State Bank of India credit card

(SBI credit card) 7. Canara Bank card 17. Syndicate bank card 8. Central Bank of India card 18. Union Bank card 9. CITI Bank card 19. Vijaya bank card

10. Corporation Bank card

2.6.1. Big players in India’s credit card industry

ICICI Bank leads the pack with a 30 per cent market share and has issued

5 million credit cards by the end of March 2006. At present upto March 2008, ICICI

Bank is the largest credit card provider in the country with 9 million credit cards, has

shown a growth of around 20-22 per cent, lower than the average growth of 30 per

cent it has seen in the past three years. HDFC Bank (after merger with Centurion

Bank of Punjab) has become the second largest credit card issuer in India beating

Citibank and SBI-GE Money in the race. HDFC Bank now has a base of 4.3 million

credit card customers while CITI India has around 3.4 million and SBI-GE Capital

have around 3.6 million customers at the end of FY 2008. HSBC credit card base 3.5

m by 31 March 2008. ICICI Bank, HDFC, HSBC, SBI and Citi Bank have over 80

per cent share of the Indian credit card industry.127

2.7. CLASSIFICATION OF CREDIT CARD

Before we apply for a credit card it is always better to know what type of

credit card is best suited to our profile. Catering to different types of consumer

127 www.businessline.in/webextras.

c needs, credit card companies issue several types of credit cards. Each type has its

own benefits. They can be classified as follows:

ci 2.7.1. Based on Franchise / Tie-up

i. Proprietary Card: Cards that are issued by the banks themselves without any

tie-up, are called proprietary cards. A bank issues such cards under its own

brand. Examples include SBI Card, CanCard of Canara Bank, Citicard.

ii. Master Card: This is a type of credit card issued under the umbrella of

MasterCard International. The issuing bank has to obtain a franchise from the

MasterCard Corporation of the USA. The franchised cards will be honoured in

the MasterCard network.

iii. VISA Card: This type of credit card can be issued by any bank having tie-up

with VISA International Corporation, USA. The banks that issue such cards

are said to have a franchise of VISA International. The advantage of a VISA

franchise is that one can avail the facility of the VISA network for transactions.

iv. Domestic tie-up Card: These cards are issued by a bank having a tie-up with

domestic card brands such as CanCard and Indcard are called ‘Domestic cards’

2.7.2. Based on geographical validity

i. Domestic Card: Cards that are valid only in India and Nepal are called

‘domestic cards’. They are issued by most of the banks in India all transactions

will be in rupees.

ii. International and Global Card: Credit cards with international validity are

called ‘international cards’. They are issued to people who travel abroad

frequently. They are honoured in every part of the world except India and

Nepal. The cardholder can make purchases in foreign currencies subject to RBI

sanction and FERA rules and regulations.

2.7.3. Based on the issuer category.

1. Individual Card: These are the non-corporate credit cards that are issued to

individuals. Generally, all brands of credit cards are issued to individuals.

ii. Corporate Card: They are credit cards issued to corporate and business

firms. The executives and top officials of the firms use them. They bear the

names of the firms, and the bills are paid by the firms.

cii 2.7.4. Based on mode of credit recovery

i. Revolving Card: This type of credit card is based on the revolving credit

principle. A credit limit is fixed on the amount of money one can spend on the

card for a particular period. The cardholder has to pay a minimum percentage of

the outstanding credit which may vary from 5 to 10 percent at the end of a

particular period. Interest varying from 30 to 36 percent per annum is charged

on the outstanding amount.

ii. Charge Card: A charge card is not a credit instrument, it is a convenient mode

of making payment. This facility gives a consolidated for a specific periods and

bills are payable in full on presentation. There is neither interest liability nor no

per-set spending limits.

2.7.5. Based on status of Card

i. Standard Card: Credit cards that are regularly issued by all card-issuing

banks are called ‘standard cards’. With these cards, it is possible for a

cardholder to make purchases without having to pay cash immediately. They

however, offer only limited privileges to cardholders. Some banks issue

standard cards under the Brand name “Classic” cards, which are generally

issued to salaried people.

ii. Business Card: Business cards also known as ‘Executive cards’, are issued to

small partnership firms, solicitors, firms of chartered accountants, tax

consultants and others, for use by executives on their business trips. They

enjoy higher credit limits and more privileges than the standard cards.

iii. Gold Card: The gold card offers high value credit for elite. It offers many

additional benefits and facilities such as higher credit limits, more cash

advance limits that are not available with the standard or the executive

cards.128

2.7.6. Innovative card

In addition, credit cards which have evolved into a variety of innovative cards

over the years are also issued by banks.

128 N. Premavathy (2007). Financial Services and Stock Exchanges. Chennai: Sri Vishnu

Publications, pp.5.10-5.14.

ciii i. ATM Card: ATM cards allow customers to access their accounts at any

time-24 hours a day, every day of the year, through Automated Teller

Machines. Customers can withdraw cash, transfer funds, find out their

account balance and perform other banking and financial transactions with

the help of ATMs.

ii. Debit Card: A debit card, like an ATM card, directly accesses a customer’s

account. It is a hybrid of ATM and credit card. The card directly debits a

designated savings bank account. Whereas in the case of credit cards, a grace

credit period of 20 to 50 days for making the payment is available, no such

credit period is allowed under debit cards. These cards can be used either at

merchant locations who have this facility to buy goods and services or at

ATMs. Presently, ATM-Cum Debit cards issued by Indian banks are in use.

iii. Prepaid Card: Prepaid cards are also known as ‘Stored Value Cards’. These

cards are with stored value paid in advance by the holder. The card issuer and

the service provider are identical. They are also called Limited Purpose

Prepaid Cards which can be used for a limited number of well -defined

purposes. Its use is often restricted to a number of identified points of sales

within a specified location

iv. Private Label Card: These cards are uniquely tied to the retailer issuing the

card and can be used only in that retailer’s stores. A bank, on the basis of a

contractual agreement with the retailer extends credit under this type of card.

v. Affinity Group Card: These are credit cards designed for a collection of

individuals with some form of common interest or relationship, such as

professional, alumni, retired persons’ organizations, sports teams, schools, or

service organizations. This credit card carries the logo of the affiliated

organization on the card design and brings special benefits and discounts on

products from that company. In case the affiliated company is a charity or

non-profit organization, a part of the credit card expenses go into the affiliate

organization's account. For example: The Help Age India Credit Card issued

by ICICI bank.129

129 www.icicicard.com

civ vi. Smart Card: A smart card is a credit card sized plastic card with an

embedded computer chip. The chip allows the card to carry a much greater

amount of information than a magnetic strip card. The telecom industry,

was perhaps the pioneer in smart cards, the most prominent being Subscriber

Identity Module (SIM) cards in the GMS digital cellular network. Using

special terminals designated to interact with the embedded chip, the card can

perform special functions. This is essentially a prepaid card.

vii. Chip Card: A chip card is a plastic card with an embedded integrated circuit

or as microchip as opposed to magnetic strips on a conventional card. The

chip can be used on existing debit and credit cards as well as on emerging

products like stored value cards. Inserting the card in a pin-pad effects the

transaction, and the value on it reduces accordingly. It is re-loadable and

disposable. The idea is to do away with the trouble of carrying cash. The

chip card also scores over the magnetic card, in that it can retain 50 to 60 of

the latest transactions, which can be produced on demand. It is also

considered more durable and secure since the cardholder alone can access it

through a Personal Identification Number (PIN).

viii. Co-branded card: The Times Card, a co-branded credit card, is the first of

its kind, from a publishing house in the Asian subcontinent. This is a co-

branded credit card of Times of India Group and Citibank MasterCard. The

co-branding concept caught the credit card industry the world over during the

last five years.130

2.7.7. Other types of credit card

i. Special purpose Card: The eighties saw the development of special purpose

cards. A host of special purpose cards were issued by departmental stores,

airlines, oil companies. For instance, the International Bank of Asia in Hong

Kong launched the first ‘women only’ card, ‘My card’ in the year 1988.

A highly encouraging membership and increasing potential of such special

purpose cards are called “Lady’s card” in Malaysia. In 1990, the Green card

130 N. Premavathy (2007). op.cit., pp.5.10-5.14.

cv

was launched in the U.K and Europe to promote contributions towards the

protection of the environment. HDFC issued ‘My City’ credit cards used in

particular city with special discount offer for oil and petrol and also an offer

for cash back. AXIS Bank also offers special purpose credit cards like Gift

card, Travel currency card and Remittance card.131

ii. Add-on card: An add-on card is more of an additional Credit card that the

customer can apply in the name of their family members (father, mother,

sister, brother, spouse, children), within the overall credit limit. Family

members applying for Add-on cards have to be 18 years and above. All the

payments for the services made from Add-on card(s) is done by the original

cardholders. Most banks allow for at least two Add-on cards.

iii. Photo card: If a card comes with the imprinted photo, then it is a Photo

card. This type of card is considered safer as it is easier to identify the credit

card user. It also serves as more identity card.

iv. Power card: It is a comprehensive credit card product that enables banks and

financial industry to enter into issuing and acquiring business of Credit

Cards. The basic advantage of this efficient tool is to improve productivity

and control the risks involved in day-to-day activities of any financial

institutions in credit cards. The product is 24 × 7, multi language, multi

currency, multi-bank and multi country.

v. Regular credit card: This is the most basic type of credit card. It has a low

credit limit and the most basic status among various credit cards. Credit card

companies can club various other reward programs like travel rewards, cash

back offers to enhance its value and appeal to customers.

vi. Silver credit card: Silver credit cards have higher eligibility criteria than

regular credit cards. They bring more benefits to the customers, and have

higher credit limits than regular credit cards.

vii. Gold credit card: Gold credit cards have a higher status and credit limits

than silver credit cards. Needless to say these types of credit cards have

higher income requirements as their eligibility criteria. In addition to the

131 http://www.apnaloan.com/credit-card-india/axis-bank-(uti)/index.html

cvi

regular benefits, banks extend special privileges to their gold credit card

holders.

viii. Platinum or Titanium credit card: These types of credit cards bring more

benefits to credit card holders than regular, silver or gold card. These credit

cards generally have platinum or titanium hue and are issued to a select class

of clients who have excellent financial background and good income levels.

Platinum credit cards have personal concierge services, in addition to

exclusive platinum benefits.

ix. Signature credit card: A league of its own, the Signature Credit Cards

usually have no pre-set spending limits, personal concierge service, signature

travel, and lounge and membership benefits. Offered to a very elite group

these credit cards, requires an excellent financial status. On June 9, 2007

ICICI bank introduced the Visa Signature Card and became the first credit

card issuer in India to launch a premium credit card. This has a joining fee of

Rs.25,000/- and an annual fee of Rs.2,500/-. The exclusivity of this signature

card is exemplified by the statement.

x. Credit cards by invitation only: The earliest of the elite, no one can apply

for these card. For example, the American Express Black Credit Card,

popularly called the Centurion Card, is issued by invitation to the most

exclusive and elite, to those who spend a certain minimum amount (which

can run into crores of rupees). These cards have huge annual fees and

minimum spending levels. In fact, these credit cards are so exclusive, that

they have an aura of mystery surrounding them and are considered status

symbols.

xi. Reward card: There are cards which offer rewards for specific kinds of

purchases. For example, the Airline Reward Card offer rewards on air travel,

Cash back card offer cash rewards on every card purchases, Fuel Reward

Card offer rebates on petroleum and other fuel purchases from specified

outlets and preferred partners. Similarly, Hotel Reward Card give rebates on

hotel stay and related expenses and Health Rewards Card give benefits on

medical expenses, health treatments and related activities. The rewards

cvii

offered by credit card companies in alliance with various brands and stores,

make them more attractive for the credit card holders.

xii. Student credit card: As the name implies, these credit cards are especially

designed for students and help them start their credit card journey. These

bring lots of rewards especially suited for students, which help them save

time, money and enjoy their student life. They are a first step towards

building credit history. A good credit history goes a long way in creating a

relationship with banks helping to secure much needed loans and credit in the

future.

xiii. Special feature credit card: Credit cards can also be grouped on the basis of

their features. For example, based on their introductory interest rates, credit

cards can be low introductory interest credit cards, or 0 (zero) Interest credit

cards. The Zero introductory interest credit cards provide interest free credit

(0%) for a specified time period, which is called the introductory period.

Similar is the case with credit cards that come without any annual fee what so

ever and are called ‘no annual fee’ credit cards.

xiv. Balance transfer credit card: Credit card companies provide lucrative

offers with 0 per cent introductory interest or low introductory interest

charges on balance transfers. This allows credit card holders to transfer the

outstanding balances on their existing credit cards to a credit card with low or

zero interest on balance transfers. This brings them a lot of savings in the

interest rates. The balance transfer credit cards may charge a balance transfer

fees for every such operation.132

xv. Kisan Credit Card (KCC): The Kisan Credit Card Scheme aims at

providing need based and timely credit support to the farmers for their

cultivation needs as well as non-farm activities and cost effective manner to

bring about flexibility and operational freedom in credit utilization. The

Kisan Card is for a period of 3 years subject to an annual review. It was

launched in 1998-99 by the Government of India in consultation with the

Reserve Bank of India and National Bank for Agricultural and Rural

132 www.creditcards.com

cviii

Development is a huge hit with the farmers in India. According to the RBI,

presently there are about 66.56 million Kisan Credit Cards in use across

India, which have been issued by various banks.133

xvi. Secured credit card: Secured credit card is a type of credit card secured by a

deposit account owned by the cardholder. This deposit is held in a special

savings account. The cardholder of a secured credit card is still expected to

make regular payments, as with a regular card, but should they default on a

payment, the card issuer has the option of recovering the cost of the

purchases paid to the merchants out of the deposit. The advantage of the

secured card for an individual with negative or no credit history is that most

companies report regularly to the major credit bureaus. This allows for

building of positive credit history.134

2.8. CREDIT CARD OPERATION CYCLE135

The credit card operation comprises the following steps as follows:

i. Credit purchases: A Cardholder purchases goods/services and gives the credit

card.

ii. Processing of credit card: A Merchant establishment delivers goods after

taking an authenticated credit card and noting the number and taking signatures

on certain forms.

iii. Raising of bill: The Merchant establishment raises the bill for the purchase and

sends it to the credit card issuing bank for payment.

iv. Marking payment: The issuing bank pays the amount to the merchant

establishment.

v. Bill to cardholder: The issuing bank raises bill on the credit cardholder and

sends it for payment.

vi. Card Payment: The credit cardholder makes the payment to the issuing bank.

133 http://www.rupeetimes.com/news/credit_cards/kisan_credit_cards_becoming_increasingly_

popular_with_farmers_1235.html. 134 http://en.wikipedia.org/wiki/credit_card#parties_involved. 135 S.Gurusamy (2007), op.cit., p.340.

cix

Fig. 2.2. Mechanics of credit card operation. Source: S. Gurusamy (2007).

2.9. PARTIES IN A CREDIT CARDS136

The following important parties involved in the operation of credit cards are:

Credit cardholders: The person named on the card. This may be customer of a

bank to whom the card has been issued or any such person to whom the bank has

issued a card authorized by the customer of the bank to hold and use the card. This

individual is also responsible for payment of all charges made to that card. The

holder of the credit card who uses to make a purchase is called the consumer.

Card-issuing bank: The financial institution or other organization that issued the

credit card and also responsible for billing the cardholders for charges. The bank

bills the consumer for repayment and bears the risk that the card is used fraudulently.

The issuing bank extends a line of credit to the consumer. Liability for non-payment

is then shared by the issuing bank and acquiring bank.

136 www.reuters.com

Contract for credit card(1) Issue of Credit card(2)

Payment of Credit card

Pur

chas

e of

Goo

ds

and

Ser

vice

s (3

)

Cha

rgin

g of

cre

dit c

ard

and

rais

ing

bill

(4)

Submission of Bill for collection (5)

Payment for bills (6)

Card

issuing

bank

Merchant

Establishment

Merchant’ s Bank

Card user/ customer

C

lear

ing

and

settl

emen

ts (7)

cx Merchant Establishments: The individual or business accepting credit cards for

sold products or services to the cardholders.

Acquiring bank: The financial institution accepts payment for the products or

services on behalf of the merchant establishments.

Independent sales organization: Resellers (to merchants) of the services of the

acquiring bank. i.e outside services providers for marketing of cards .

Merchant account: This could refer to the acquiring bank or the independent sales

organization, but in general is the organization that the merchant deals with.

Credit card association: An association of card-issuing banks such as Visa,

MasterCard, Discover, American Express that set transaction terms for merchants,

card-issuing banks, and acquiring banks.

Transaction network: The system that implements the mechanics of the electronic

transactions. May be operated by an independent company, and one company may

operate multiple networks. Transaction processing networks include Cardnet,

Nabanco, Omaha, Paymentech, NDC Atlanta, Nova, Vital, Concord EFSnet, and

Visa Net.

Affinity partner: Some institutions lend their names to an issuer to attract customers

that have a strong relationship with that institution, and get paid a fee or a percentage

of the balance for each card issued using their name. Examples of typical affinity

partners are sports teams, universities, charities, professional organizations, and

major retailers.

2.10. CREDIT CARD TRANSACTION137

The flow of information and money between these parties in the credit cards

always through the card associations is known as the interchange, and it consists of

the following steps.

Authorization: The cardholder pays for the purchase and the merchant submits the

transaction to the acquirer (acquiring bank). The acquirer verifies the credit card

number, the transaction type and the amount with the issuer (Card-issuing bank) and

reserves that amount of the cardholder's credit limit for the merchant. An

137 http://en.wikipedia.org/wiki/credit_card

cxi authorization will generate an approval code, which the merchant stores with the

transaction.

Batching: Authorized transactions are stored in "batches", which are sent to the

acquirer. Batches are typically submitted once per day at the end of the business day.

If a transaction is not submitted in the batch, the authorization will stay valid for a

period determined by the issuer, after which the held amount will be returned to the

cardholder's available credit ( authorization hold).

Clearing and settlement: The acquirer sends the batch transactions through the

credit card association, which debits the issuers for payment and credits the acquirer.

Essentially, the issuer pays the acquirer for the transaction.

Funding: Once the acquirer has been paid, the acquirer pays the merchant, the

merchants receives the amount totaling the funds in the batch minus the “discount

rate,” which is the fee the merchant pays the acquirer for processing the transactions.

Charge backs: A chargeback is an event in which money in a merchant account is

held due to a dispute relating to the transaction. Charge backs are typically initiated

by cardholders. In the event of a chargeback, the issuer returns the transaction to the

acquirer for resolution. The acquirer then forwards the chargeback to the merchant,

who must either accept the chargeback or contest it.

2.11. REWARDS

Many credit card customers receive rewards, such as frequent flier points, gift

certificates, or cash back as an incentive to use the card. Rewards are generally tied

to purchasing an item or service on the card, which may or may not include balance

transfers, cash advances, or other special uses. Depending on the type of card,

rewards will generally cost the issuer between 0.25 and 2.0 per cent of the spread.

Networks such as Visa or MasterCard have increased their fees to allow issuers to

fund their rewards system.

2.12. INTERCHANGE FEE

Merchants must pay interchange fees to the card-issuing bank and the card

association. For a typical credit card issuer, interchange fee revenues may represent

about a quarter of total revenues. These fees are typically from 1 to 6 percent of each

cxii sale, but will vary not only from merchant to merchant (large merchants can

negotiate lower rates )but also from card to card, with business cards and rewards

cards generally costing the merchants more to process. The interchange fee that

applies to a particular transaction is also affected by many other variables including

the type of merchants. Interchange fees may consume over 50 per cent of profits

from card sales for some merchants (such as supermarkets) that operate on slim

margins. In some cases, merchants add a surcharge to the credit cards to cover the

interchange fee.

2.13. GLOBAL PLAYER IN CREDIT CARD MARKET

2.13.1. MasterCard: MasterCard is a product of MasterCard International and along

with VISA is distributed by financial institutions around the world. Cardholders

borrow money against a line of credit and pay it back with interest if the balance is

carried over from month to month. Its products are issued by 25,000 financial

institutions in 220 countries and territories. In 1998, it had almost 700 million cards

in circulation, whose users spent $650 billion in more than 16.2 million locations.

The company, which had been organized as a cooperative of banks, had an initial

public offering on May 25, 2006 at $39.00 USD. The stock is traded on the NYSE

under the symbol MA.138

2.13.2. VISA card: A VISA card is a product of VISA USA and along with Master

Card is distributed by financial institutions around the world. Visa Inc. commonly

referred to as VISA, is a multinational corporation based in San Francisco,

California, USA. The company operates the world's largest retail electronic payment

network, managing payments among financial institutions, merchants, consumers,

businesses and government entities. Before Visa Inc's IPO in early 2008, it was

operated as a cooperative of some 21,000 financial institutions that issued and

marketed Visa products including credit and debit cards. A VISA cardholder

borrows money against a credit line and repays the money with interest if the balance

is carried over from month to month in a revolving line of credit. Nearly 600 million

cards carry one of the VISA brands and more than 14 million locations accept them.

138 http://mastercard.com

cxiii In 2006, according to The Nilson Report, Visa held 44 per cent of the credit card

market share and 48

per cent of the debit card market share in the United States. Visa Inc. is the world’s

largest payments company, with more than US$ 4.0 trillion of total volume as of

March 31, 2008.139

2.13.3. American Express: The world’s favourite card is American Express Credit

Card. More than 57 million cards are in circulation and growing and it is still

growing further. Around US $ 123 billion was spent last year through American

Express Cards and it is poised to be the world’s no.1 card in the near future. In a

regressive US economy last year, the total amount spent on American Express cards

rose by 4 percent. They are very popular in the U.S., Canada, Europe and Asia and

are used widely in the retail and everyday expenses segment.140

2.13.4. Diners Club International: Diners Club International, originally founded as

Diners Club, is a charge card company formed in 1950 by Frank X. McNamara,

Ralph Schneider and Casey R. Taylor. When it first emerged, it became the first

independent credit card company in the world. Diners Club is the world's no.1

Charge Card. Diners Club cardholders reside all over the world and the Diners Card

is a all time favourite for corporate. There are more than 8 million Diners Club

cardholders around the world. They are affluent and are frequent travelers in premier

businesses and institutions, including Fortune 500 companies and leading global

corporations. In April 2008, Discover Card and Citibank announced that Discover

would purchase the Diners Club Network from Citi for $165 million. Discover Bank

has no plans on issuing Diners Club branded cards. Discover purchased the network,

but not the licensees issuing the cards. The deal was completed on July 1, 2008.141

2.13.5. Discover Card: The Discover Card was originally introduced by Sears in

1985, and was a unit of Dean Witter, which merged with Morgan Stanley in 1997. In

2007, the unit was spunoff as an independent, publicly traded company. To-day,

Discover is headquartered in the Chicago suburb of Riverwoods, IIinois. Discover

Financial Services is an American financial services company, which issues the

139 www.corporate.visa.com 140 www.americanexpress.com 141 www.dinersclub.com

cxiv Discover Card and operates the Discover and Pulse networks. Discover Card is the

third largest credit card brand in the United States, when measured by cards in force,

with nearly 50 million cardholder.142

2.13.6. JCB Card (Japan Credit Bureau): Japan Credit Bureau, usually

abbreviated as JCB, is a credit card company based in Tokyo, Japan. Founded in

1961, it established dominance over the Japanese credit card market when it

purchased Osaka Credit Bureau in 1968 and its cards are now issued in 20 different

countries. Fifty-nine million JCB card members worldwide use their cards to

purchase over US$62.7 billion of goods and services annually in 190 countries

worldwide. JCB also operates a network of membership lounges targeting Japanese,

Chinese, and Korean travelers in Europe, Asia, and North America. The JCB

philosophy of “identify the customer’s needs and please the customer with service

from the Heart” is paying rich dividends as their customers spend US$ 43 billion

annually on their JCB cards.143

2.14. CREDIT CARD NUMBERING

The numbers found on credit cards have a certain amount of internal

structure, and share a common numbering scheme. The card number's prefix, called

the Bank Identification Number, is the sequence of digits at the beginning of the

number that determine the bank to which a credit card number belongs. This is the

first six digits for bank card associations such as MasterCard and Visa cards. The

next nine digits are the individual account number, and the final digit is a validity

check code. In addition to the main credit card number, credit cards also carry issue

and expiration dates (given to the nearest month), as well as extra codes such as issue

numbers and security codes. Not all credit cards have the same sets of extra codes

nor do they use the same number of digits.

2.15. CREDIT CARD IN ATM

Many credit cards can also be used in an ATM to withdraw money against

the credit limit extended to the card, but many card issuers charge interest on cash

142 www.discover.com 143 www.jcbinternational.com

cxv advances before they do so purchases. The interest on cash advances is commonly

charged from the date of the withdrawal is made, rather than the monthly billing

date. Many card issuers levy a commission or for ATM charges for cash

withdrawals, even if the ATM belongs to the same bank as the card issuer.

cxvi 2.16. CREDIT CARD SYSTEM

2.16.1. Interest charges

Credit card issuers usually waive interest charges if the balance is paid in full

each month, but typically will charge full interest on the entire outstanding balance

from the date of each purchase if the total balance is not paid. The credit card may

simply serve as a form of revolving credit, or it may become a complicated financial

instrument with multiple balance segments each at a different interest rate, possibly

with a single umbrella credit limit, or with separate credit limits applicable to the

various balance segments. Interest rates can vary considerably from card to card, and

the interest rate on a particular card may jump dramatically if the card user is late

with a payment on that card or any other credit instrument, or even if the issuing

bank decides to raise its revenue.

2.16.2. Fees charged to customers144

Interest free credit period is applicable only on retail purchases and if previous

months balance outstanding is paid in full. It may vary from banks for 20-50 days.

The major fees are for:

• No joining fees, annual fees and renewal fees are applicable on the primary

and secondary card member unless indicated by the banks.

• Late payments or overdue payments (30% of minimum amount due, subject

to minimum of Rs.400 and maximum of Rs.600)

• Charges that result in exceeding the credit limit on the card (whether done

deliberately or by mistake), called over limit fees (2.5% of over limit amount,

subject to a minimum of Rs.500)

• Returned cheque fees or payment processing fees (Rs.250 )

• Cash advances and transaction fees (2.50% on advanced amount, subject to a

minimum of Rs.300) on Easy deposit card – NIL for ICICI Bank ATM cash

withdrawals fees.

• Transactions in a foreign currency (3.5% of the amount).

144 www.icicibank.com

cxvii

• Outstation Cheque Processing Fee (1% of the cheque value, subject to

minimum of Rs.100)

• Dial-a-Draft – Transaction Fee (3% of the draft value amount subject to a

minimum of Rs.300)

• Railway Booking Surcharge (1.80% for Internet transactions and 2.5% for

other bookings)

• Fee on Cash payment at Branches(Rs.100)

Interest will be charged if cardholder do not pay back the previous bills is full, and

also on all cash advances from the data of transaction until date of settlement.

2.16.3. Grace period

A credit card's grace period is the time the customer has to pay the balance

before interest is charged to the balance. Grace periods vary, but usually range from

20 to 50 days depending on the type of credit card and the issuing bank. Some

policies allow for reinstatement after certain conditions are met. Usually, if a

customer is late paying the balance, finance charges will be calculated and the grace

period does not apply. Finance charges incurred depend on the grace period and

balance, with most credit cards there is no grace period if there is any outstanding

balance from the previous billing cycle or statement (i.e. interest is applied on both

the previous balance and new transactions). However, there are some credit cards

that will apply finance charge only on the previous or old balance, excluding new

transactions.

2.16.4. Benefits to customers

Because of intense competition in the credit card industry, credit card

providers often offer incentives such as frequent flyer points, gift certificates, or cash

back (typically up to 1 to 5 percent based on total purchases) offers try to attract

customers to their programs. Low interest credit cards or even 0 per cent interest

credit cards are available.

2.16.5. Benefits to merchants

cxviii

For merchants, a credit card transaction is often more secure than other forms

of payment, such as cheques because the issuing bank commits to pay the merchant

the moment the transaction is authorized, regardless of whether the consumer

defaults on the credit card payment . In most cases, cards are even more secure than

cash, because they discourage theft by the merchant's employees and reduce the

amount of cash on the premises. Prior to credit cards, each merchant had to evaluate

each customer's credit history before extending credit. That task is now performed by

the banks which assume the credit risk.145

2.17. MARKETING OF CREDIT CARD

Marketing is a business term referring to the promotion of products,

especially advertising and branding. The term developed from the original meaning

which referred literally to going to market, as in shopping, or going to a market to

sell goods or services. Customer satisfaction is the key concept of any marketing like

credit cards. It is rightly pointed out by Mahatma Gandhiji, “A Customer is the most

important visitor of our premises. He is not dependent on us. We are dependent on

him. He is not the interruption to our work. He is the purpose of it. He is not an

outsider to our business. He is part of it .We are not doing a favour by serving him.

He is doing us a favour by giving an opportunity to do so.” It is a sad commentary

on our banks that they either do not find time to take customers seriously or lack to

carry out customer survey. Banks should adopt a marketing approach stating the

philosophy. “Customer is the king” let’s find about him and serve him – How do we

do that? By satisfying his needs.146

The concept of marketing is customer satisfaction, it includes identifying the

most profitable market at present and in future, assessing present and future needs of

customers, setting business development goals and making plans to meet them, and

managing the various services and promoting them to achieve the plans. In this

background, the researcher conducted a survey on the credit cardholder’s

satisfactions among the banks in this study area. The satisfaction can be tested by

145 http://en.wikipedia.org/wiki/credit_card 146 B. Chand (1994). Marketing of Services. Jaipur and New Delhi: Rawat Publication, p.88.

cxix way of product awareness, level of satisfactions and dissatisfaction, problems

perceived by them. This study has also been assessed for shifting options given by

the users among the banks in this area. This research will help the banks to market

their credit cards and aim to improve their sales by enhancing the usage of cards

among the existing cardholders and also attracting new users by way of successful

marketing of their products.

2.17.1. Mode of marketing

The marketing of credit cards in banks is carried out through any one of the

following important modes.

2.17.1.1. Direct marketing

Any medium that can be used to deliver a communication to a customer can

be employed in direct marketing. Direct marketing is a sub-discipline and type of

marketing. There are two main definitional characteristics which distinguish it from

other types of marketing. The first is that it attempts to send its messages directly to

consumers, without the use of intervening media. This involves commercial

communication (direct mail, e-mail, and telemarketing) with consumers or

businesses, usually unsolicited. The second characteristic is that it is focused on

driving purchases that can be attributed to a specific "call-to-action." This aspect of

direct marketing involves an emphasis on trackable, measurable positive responses

from consumers regardless of medium.147

2.17.1.2. Direct mail

The most common form of direct marketing is direct mail, sometimes called

junk mail, used by advertisers who send paper mail to all postal customers in an area

or to all customers on a list. If the advertisement asks the prospect to take a specific

action, for instance, call a free phone number or visit a website, then the effort is

considered to be direct response advertising. It includes advertising circulars,

catalogs, free trial CDs, pre-approved credit card applications, and other unsolicited

147 http://en.wikipedia.org/wiki/direct_marketing

cxx merchandising invitations delivered by mail to homes and businesses, or delivered to

consumers' mailboxes by delivery services other than the Post Office.

2.17.1.3. Telemarketing

The second most common form of direct marketing is telemarketing, in

which marketers contact consumers by phone. The unpopularity of cold call

telemarketing (in which the consumer does not expect or invite the sales call) has led

some US states and the US federal government to create "no-call lists" and

legislation including heavy fines. This process may be outsourced to specialist call

centres. In the US, a national do-not-call list went into effect on October 1, 2003.

Under the law, it is illegal for telemarketers to call anyone who has registered

themselves on the list. After the list had operated for one year, over 62 million

people had signed up. The telemarketing industry opposed the creation of the list, but

most telemarketers have complied with the law and refrained from calling people

who are on the list. India has passed legislation to create a similar National ‘Do Not

Call’ List with effect from 5th June, 2007 by TRAI notification act.148 In other

countries, it is voluntary, such as the New Zealand Name Removal Service.

2.17.1.4. Email Marketing

E-mail marketing is a form of direct marketing which uses electronic mail as

a means of communicating commercial or fund raising messages to an audience. In

its broadest sense, every e-mail sent to a potential or current customer could be

considered e-mail marketing. It is sending e-mails with the purpose of enhancing the

relationship of a merchant with its current or previous customers and to encourage

customer loyalty and repeat business, sending e-mails with the purpose of acquiring

new customers or convincing current customers to purchase something immediately,

adding advertisements to e-mails sent by other companies to their customers, and

sending e-mails over the Internet, as e-mail did and does exist outside the Internet.

148 www.ndceregistry.gov.in

cxxi Researchers estimate that United States firms alone spent US$400 million on e-mail

marketing in 2006.149

149 The Power of Direct Marketing. ROI, Sales, Expenditure and Employment in the U.S. –

2006-2007 edition.” Direct Marketing Association, (October 2006).

cxxii 2.17.1.5. Broadcast faxing

A fourth type of direct marketing, broadcast faxing, is now less common than

the other forms. This is partly due to laws in the United States and elsewhere which

make it illegal. When sending documents to people at large distances, faxes have a

distinct advantage over postal mail in that the delivery is nearly instantaneous, yet its

disadvantages in quality have relegated it to a position beneath email as the

prevailing form of electronic document transferal.

2.17.1.6. Voicemail marketing

A fifth type of direct marketing has emerged out of the market prevalence of

personal voice mailboxes, and business voicemail systems. Voicemail marketing

presented a cost effective means by which to reach people with the warmth of a

human voice. Abuse of consumer marketing applications of voicemail marketing

resulted in an abundance of "voice-spam", and prompted many jurisdictions to pass

laws regulating consumer voicemail marketing. More recently, businesses have

utilized guided voicemail (a application where pre-recorded voicemails are guided

by live callers) to accomplish personalized business-to-business marketing formerly

reserved for telemarketing. Because guided voicemail is used to contact only

businesses, it is exempt from ‘Do Not Call’ regulations in place for other forms of

voicemail marketing.

2.17.2. Couponing

Couponing is used in print media to elicit a response from the reader. An

example is a coupon which the reader cuts out and presents to a super-store check-

out counter to avail of a discount. Coupons in newspapers and magazines cannot be

considered direct marketing, since the marketer incurs the cost of supporting a third-

party medium (the newspaper or magazine).

2.17.3. Direct television response marketing

Direct marketing on TV has two basic forms. They are long form (usually

half-hour or hour-long segments that explain a product in detail and are commonly

referred to as infomercials) and short form which refers to typical 0:30 second or

cxxiii 0:60 second commercials that ask viewers for an immediate response. A related form

of marketing is infomercials. They are typically called direct response marketing

rather than direct marketing because they try to achieve a direct response via

broadcast on a third party's medium, but viewers respond directly via telephone,

SMS or internet.

2.17.4. Direct selling

Direct selling is the sale of products by face-to-face contact with the customer,

either by having sales people approach potential customers in person. Direct selling

is a retail channel for the distribution of goods and services. At a basic level it may

be defined as marketing and selling products, person-to-person away from a fixed

retail location. Sales are typically made through party plan and other personal contact

arrangements. The direct personal presentation, demonstration, and sale of products

and services to consumers, usually in their homes or at their jobs. The industry is

global and growing. Recent figures show almost fifty-five million people are

involved and in 2007 it is estimated that worldwide retail sales accounted for more

than US$111 Billion.150

2.17.5. Integrated Campaigns

A comprehensive direct marketing campaign employs a mix of channels. It is

not unusual for a large campaign to combine direct mail, telemarketing, radio and

broadcast TV, as well as online channels such as email, search marketing, social

networking and video. In a survey conducted by the Direct Marketing Association, it

was found that 57 per cent of the campaigns studied were employing integrated

strategies. Of those, almost half (47%) launched with a direct mail campaign,

typically followed by e-mail and then telemarketing.151

2.17.6. Direct response marketing

150 http://en.wikipedia.org/wiki/direct_selling. 151 “The Integrated Marketing Mix.” BtoB Magazine (July 14, 2008) Available online at

www.scribd.com/19408443/marketing.>

cxxiv Direct response marketing is a form of marketing designed to solicit a direct

response which is specific and quantifiable. The delivery of the response is direct

between the viewer and the advertiser, that is, the customer responds to the marketer

directly. Marketers use broadcast media to get customers to contact them directly. It

is direct response marketing because the communications from the customer to the

marketer is direct. Direct response seeks to elicit action. It is inherently accountable

since results can be tracked and measured. Furthermore, direct response campaigns

perform best if the underlying strategies and tactics are highly competitive.

2.17.7. Database marketing

Database marketing is a form of direct marketing using databases of

customers or potential customers to generate personalized communications in order

to promote a product or service for marketing purposes. The “database” is usually

name, address, and transaction history details from internal sales or delivery systems,

or a bought-in compiled “list” from another organization, which has captured that

information from its customers. Typical sources of compiled lists are charity

donation forms, application forms for any free product or contest, product warranty

cards, subscription forms, and credit application forms.

Advertisers often refine direct mail practices into targeted mailing, in which

mail is sent out following database analysis to select recipients considered most

likely to respond positively. For example a person who has demonstrated an interest

in receiving credit cards may receive direct mail for credit cards related products or

perhaps for goods and services that are appropriate for cardholders. This use of

database analysis is a type of database marketing.

2.17.8. Personalized marketing

Personalized marketing (also called personalization, and sometimes called

one-to-one marketing) is an extreme form of product differentiation. Whereas

product differentiation tries to differentiate a product from competing ones,