Credible Loss Ratio Claims Reserves The Benktander ... Loss Ratio Claims Reserves The Benktander,...

15

Credible Loss Ratio Claims Reserves The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W. Exam 7, V1a Page 94 2014 by All 10, Inc. Sec Description 1 Introduction 2 The Collective and Individual Loss Ratio Claims Reserves 3 Credible Loss Ratio Claims Reserves 4 The Optimal Credibility Weights and The Mean Squared Error 1 Introduction Hürlimann’s paper was written after reviewing the Benktander, Neuhaus and Mack loss reserving methods. Notable differences between his method and the Benktander method reviewed in Mack (2000), Section 2, are as follows: o While Mack worked in the context of a single origin period (AY or underwriting year), Hürlimann’s approach is based on a full loss development triangle of paid claims (or incurred claims) with several origin periods. o Also, a measure of exposure like premiums for each origin period is necessary. Standard claims reserving methods include the Chain-Ladder, the Cape Cod and the Bornhuetter- Ferguson (BF) methods. o Standard methods apply chain-ladder link ratios (average ratio of cumulative paid claims between two consecutive development periods); Hürlimann’s approach is based on loss ratios (average ratio of incremental paid claims to exposure for each development period). o The key result is Theorem 6.1, which shows an optimal credibility weight for combining the chain-ladder or individual loss ratio reserve (grossed up latest claims experience of an origin period) with the BF or collective loss ratio reserve (experience based burning cost estimate of the total ultimate claims of an origin period). o The optimal credibility weights minimize simultaneously the mean squared error (MSE) and the variance of the claims reserve. The following sections in the paper are: o Section 2, which describes notation and the definition of the collective and individual loss ratio claims reserves. o Section 3, which defines the credible loss ratio claims reserves. o In Section 4, we find formulas for the optimal credibility weights, which minimize the MSEs of the credible loss ratio reserves, as well as formulas for the MSEs are derived.

Transcript of Credible Loss Ratio Claims Reserves The Benktander ... Loss Ratio Claims Reserves The Benktander,...

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 94 2014 by All 10, Inc.

Sec Description

1 Introduction

2 The Collective and Individual Loss Ratio Claims Reserves

3 Credible Loss Ratio Claims Reserves

4 The Optimal Credibility Weights and The Mean Squared Error

1 Introduction

Hürlimann’s paper was written after reviewing the Benktander, Neuhaus and Mack loss reserving methods.

Notable differences between his method and the Benktander method reviewed in Mack (2000), Section 2, are as follows:

o While Mack worked in the context of a single origin period (AY or underwriting year), Hürlimann’s

approach is based on a full loss development triangle of paid claims (or incurred claims) with several origin periods.

o Also, a measure of exposure like premiums for each origin period is necessary.

Standard claims reserving methods include the Chain-Ladder, the Cape Cod and the Bornhuetter-

Ferguson (BF) methods.

o Standard methods apply chain-ladder link ratios (average ratio of cumulative paid claims between

two consecutive development periods); Hürlimann’s approach is based on loss ratios (average ratio of incremental paid claims to exposure for each development period).

o The key result is Theorem 6.1, which shows an optimal credibility weight for combining the chain-ladder or individual loss ratio reserve (grossed up latest claims experience of an origin

period) with the BF or collective loss ratio reserve (experience based burning cost estimate of the

total ultimate claims of an origin period). o The optimal credibility weights minimize simultaneously the mean squared error (MSE) and the

variance of the claims reserve.

The following sections in the paper are:

o Section 2, which describes notation and the definition of the collective and individual loss ratio claims reserves.

o Section 3, which defines the credible loss ratio claims reserves. o In Section 4, we find formulas for the optimal credibility weights, which minimize the MSEs of the

credible loss ratio reserves, as well as formulas for the MSEs are derived.

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 95 2014 by All 10, Inc.

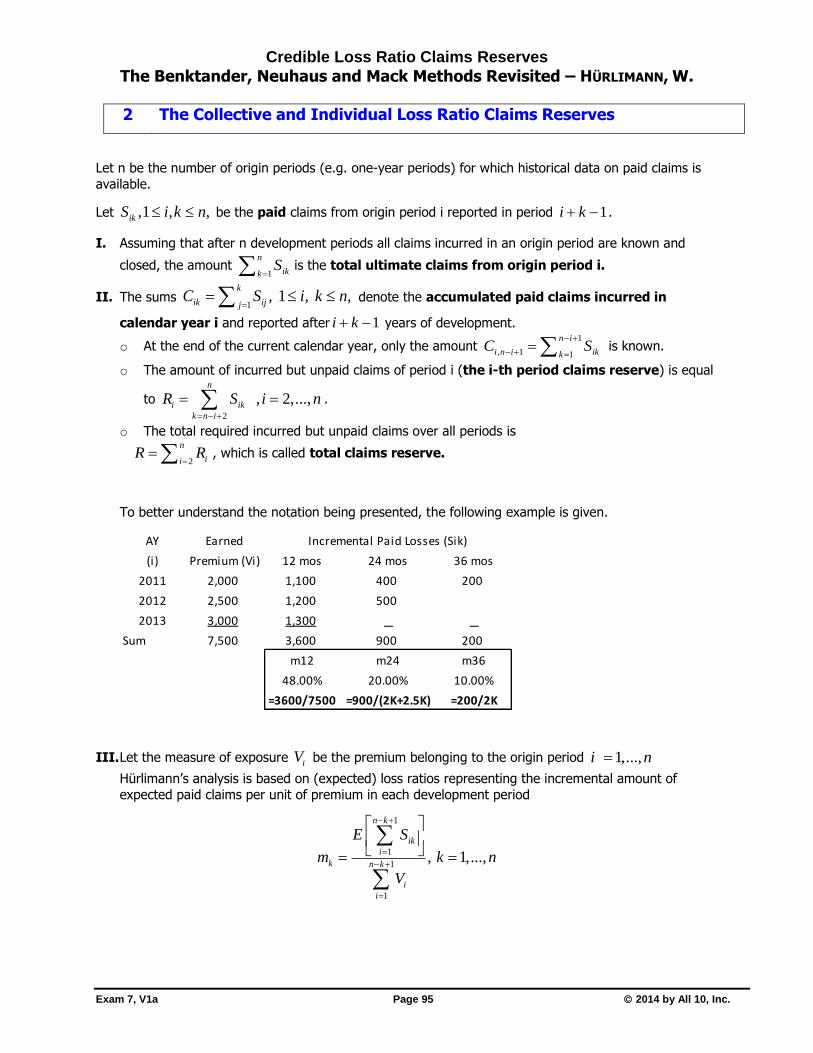

2 The Collective and Individual Loss Ratio Claims Reserves

Let n be the number of origin periods (e.g. one-year periods) for which historical data on paid claims is

available.

Let ,1 , ,ikS i k n be the paid claims from origin period i reported in period 1i k .

I. Assuming that after n development periods all claims incurred in an origin period are known and

closed, the amount 1

n

ikkS

is the total ultimate claims from origin period i.

II. The sums 1

, 1 , ,k

ik ijjC S i k n

denote the accumulated paid claims incurred in

calendar year i and reported after 1i k years of development.

o At the end of the current calendar year, only the amount 1

, 1 1

n i

i n i ikkC S

is known.

o The amount of incurred but unpaid claims of period i (the i-th period claims reserve) is equal

to 2

, 2,...,n

i ik

k n i

R S i n

.

o The total required incurred but unpaid claims over all periods is

2

n

iiR R

, which is called total claims reserve.

To better understand the notation being presented, the following example is given.

III. Let the measure of exposure iV be the premium belonging to the origin period 1,...,i n

Hürlimann’s analysis is based on (expected) loss ratios representing the incremental amount of

expected paid claims per unit of premium in each development period

1

1

1

1

, 1,...,

n k

ik

i

k n k

i

i

E S

m k n

V

AY Earned

(i) Premium (Vi) 12 mos 24 mos 36 mos

2011 2,000 1,100 400 200

2012 2,500 1,200 500

2013 3,000 1,300

Sum 7,500 3,600 900 200

m12 m24 m36

48.00% 20.00% 10.00%

=3600/7500 =900/(2K+2.5K) =200/2K

Incremental Paid Losses (Sik)

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 96 2014 by All 10, Inc.

IV. Since 1

n

kkm

represents the loss ratio over all reporting periods,

1

nBC

i i k

k

E U V m

is the expected value of the burning cost BC

iU of the total ultimate claims required for the origin

period i.

Note: This is similar to the expected value of the BF prior estimate 0U of the total ultimate claims in

Mack (2000).

V. The expected burning cost of the paid claims for the origin period i, which are required in the

current calendar period is

1

1, 1,...,

n i

i kkV m i n

VI. The loss ratio payout factor (a.k.a. loss ratio lag-factor)

1 1

1 1

1

1,...,

n i n i

i k k

k ki nBC

ik

k

V m m

p i nE U

m

is the proportion of total ultimate claims from origin period i, expected to be paid in the development

period – 1.n i

VII. The loss ratio reserve factor

2

1

1 , 1,...,

n

k

k n ii i n

k

k

m

q p i n

m

is the proportion of total ultimate claims from origin period i,

which remain unpaid in the development period – 1.n i

VIII. Total ultimate claims are obtained by grossing up the latest accumulated paid claims amount.

It is based solely on the individual latest claims experience of an origin period, and is called the individual total ultimate claims amount.

, 1, 1,...,

i n iind

i

i

CU i n

p

Note: This is similar to the chain-ladder estimate in Mack (2000).

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 97 2014 by All 10, Inc.

IX. The individual loss ratio claims reserve is

, 1 , 1, 1,...,ind ind ind ii i i n i i i i n i

i

qR U C q U C i n

p

The burning cost of the total ultimate claims produces an alternative claims reserve.

X. This is the collective loss ratio claims reserve as it depends solely on the claims experience of all

origin periods.

1

1

11

1

, , 1,...,

n k

ikncoll BC BC ii i i i i n k

ki

i

S

R q U U V i n

V

It is akin to the reserve set to the loss ratio reserving method in Mack (1997), Section 3.2.2, p. 230-

234.

XI. Collective total ultimate claims are

, 1, 1,...,coll coll

i i i n iU R C i n

This estimate is similar to the BF posterior estimate of the total ultimate claims in Mack (2000).

An advantage of the collective loss ratio claims reserve over the BF reserve in Mack (2000) is that

different actuaries will produce the same results if the same premiums are used.

This is also true for the individual claims reserve.

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 98 2014 by All 10, Inc.

3 Credible Loss Ratio Claims Reserves

Like the BF and the CL estimates in Mack (2000), the collective and individual loss ratio claims reserve estimates represent extreme positions.

o The individual claims reserve treats the latest accumulated paid claims amount , 1i n iC as fully

credible to predict future claims and ignores the burning cost BC

iU of the total ultimate claims.

o The collective claims reserve ignores , 1i n iC and relies solely on the burning cost.

I. The credible loss ratio claims reserve estimate is

1 , 1,...,i

c ind coll

i i i iR Z R Z R i n , where

Zi is the credibility weight associated to the individual loss ratio reserve.

II. The Benktander and Neuhaus Methods

A. The credibility weight should increase as the accumulated paid claims , 1i n iC develop, so Gunnar

Benktander (1976) used the credibility weight

, 1,...,GB

i iZ p i n .

The Benktander loss ratio claims reserve is

, 1,...,i

GB ind coll

i i i iR p R q R i n

B. According to Mack (1997), p. 242, Walter Neuhaus (1992) used the credibility weight

1

1 1

n i nWN

i k i kk kZ m p m

.

The Neuhaus loss ratio claims reserve is

1 , 1,...,i

WN WN ind WN coll

i i i iR Z R Z R i n .

These weights are both close to an optimal credible loss ratio claims reserve. Optimal credibility

weights are discussed in Section 6.

Next, Hürlimann shares remarks similar to those made by Mack (2000) at the end of Section 2.

o i i i iR U qU and , 1i i i i n iU R R C are not inverse to each other except for ind

i iU U .

o Similar to the "iterated BF method", there is an "iterated collective loss ratio reserving method".

Successively iterating the collective and Benktander loss ratio reserving methods, using a starting point 0

iU and doing so an infinite number of times, will lead to the individual loss ratio reserving method.

Hürlimann then restates this result, which paraphrases Theorem 1 in Mack (2000).

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 99 2014 by All 10, Inc.

Theorem 3.1. Beginning with an arbitrary starting point 0 0

i iU U , and applying the iteration rule

1

, 1, , 0,1,2,...,m mm m

i i i i i n i iR q U U C R m

will produce the following credibility weightings

between the collective and individual loss ratio reserving methods:

( ) 0

( ) 0

1

1

m m ind m

i i i i i

m m ind m

i i i i i

U q U q U

R q R q R

Begin with the collective method, which leads via the Benktander method to the individual method for m = ∞.

4 The Optimal Credibility Weights and The Mean Squared Error

Assume

BC

iU is independent from , 1,i n i iC R and , 1i i i n iU R C , and

BC ind

i i iE U E U E U (implying un-biasedness) and variance is BC

iVar U

These are similar assumptions to get Theorem 2 in Mack (2000).

Theorem 4.1. The optimal credibility weights *

iZ which minimize the mse 2

c c

i i iR E R R

is

, 1*

2

, 1

, BC

i n i i i i iii BC

i i n i i i

Cov C R p q Var UpZ

q Var C p Var U

But this is cumbersome to use. Thus, Theorem 4.2 was developed.

Theorem 4.2. The optimal credibility weights *

iZ which minimize the mse 2

c c

i i iR E R R

is

* ii

i i

pZ

p t

, where

2

2 1,...,

i i

i BC

i i i i

E Ut i n

Var U Var U E U

Note: In section 6 of the paper, we find out that i it p . However, the 2014 exam 7 syllabus states

that candidates are only responsible for pages 81 – 89, which is sections 1 - 4.

Therefore, check the current syllabus to see if the examiners place section 6 back on the syllabus.

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 100 2014 by All 10, Inc.

Formulas for the MSEs are shown next.

Theorem 4.3.

2

2

222 2

1

1

coll ii i i i

i

ind ii i i

i

ic ii i i i

i i i

qmse R E U q

t

qmse R E U

p

ZZmse R E U q

p q t

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 101 2014 by All 10, Inc.

Sample Question 1

(3.25 points) According to Hürlimann in “Credible Loss Ratio Claims Reserves” and using the data below, answer the following questions:

a (1.0 point) Calculate the incremental amount of expected paid claims per unit of premium at 12 months, 24

months and 36 months.

b (0.75 points) Calculate 2013[ ]BCE U

c (0.5 points) Calculate 2013p and 2013q

d (0.5 points) Calculate 2013

CollR

e (0.5 points) Calculate 2013

CollU

Sample Question 2

(4.0 points) According to Hürlimann in “Credible Loss Ratio Claims Reserves” and using the data below, answer the following questions:

Given that 2013 900CollR

a. (1.0 point) Calculate 2013

indR

b. (1.0 point) Calculate 2013

GBR

c. (1.0 point) Calculate 2013

WNR

d. (1.0 point) Calculate 2013

cR , using optimal credibility * ii

i i

pZ

p p

Earned

AY Premium 12 mos 24 mos 36 mos

2011 2,000 1,100 400 200

2012 2,500 1,200 500

2013 3,000 1,300

Incremental Paid Losses

Earned

AY Premium 12 mos 24 mos 36 mos

2011 2,000 1,100 400 200

2012 2,500 1,200 500

2013 3,000 1,300

Incremental Paid Losses

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 102 2014 by All 10, Inc.

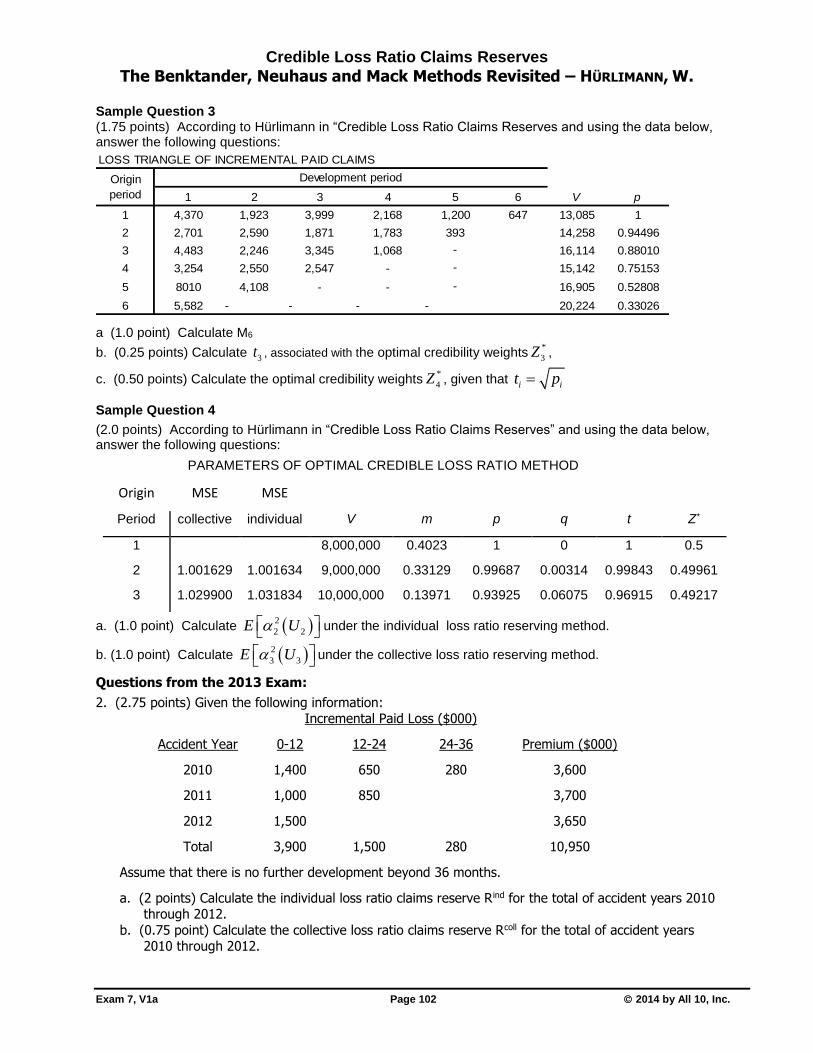

Sample Question 3 (1.75 points) According to Hürlimann in “Credible Loss Ratio Claims Reserves and using the data below, answer the following questions:

a (1.0 point) Calculate M6

b. (0.25 points) Calculate 3t , associated with the optimal credibility weights*

3Z ,

c. (0.50 points) Calculate the optimal credibility weights*

4Z , given that i it p

Sample Question 4

(2.0 points) According to Hürlimann in “Credible Loss Ratio Claims Reserves” and using the data below, answer the following questions:

PARAMETERS OF OPTIMAL CREDIBLE LOSS RATIO METHOD

Origin MSE MSE

Period collective individual V m p q t Z*

1 8,000,000 0.4023 1 0 1 0.5

2 1.001629 1.001634 9,000,000 0.33129 0.99687 0.00314 0.99843 0.49961

3 1.029900 1.031834 10,000,000 0.13971 0.93925 0.06075 0.96915 0.49217

a. (1.0 point) Calculate 2

2 2E U under the individual loss ratio reserving method.

b. (1.0 point) Calculate 2

3 3E U under the collective loss ratio reserving method.

Questions from the 2013 Exam:

2. (2.75 points) Given the following information: Incremental Paid Loss ($000)

Accident Year 0-12 12-24 24-36 Premium ($000)

2010 1,400 650 280 3,600

2011 1,000 850 3,700

2012 1,500 3,650

Total 3,900 1,500 280 10,950

Assume that there is no further development beyond 36 months.

a. (2 points) Calculate the individual loss ratio claims reserve Rind for the total of accident years 2010 through 2012.

b. (0.75 point) Calculate the collective loss ratio claims reserve Rcoll for the total of accident years 2010 through 2012.

LOSS TRIANGLE OF INCREMENTAL PAID CLAIMS

1 2 3 4 5 6 V p

1 4,370 1,923 3,999 2,168 1,200 647 13,085 1

2 2,701 2,590 1,871 1,783 393 14,258 0.94496

3 4,483 2,246 3,345 1,068 ‑ 16,114 0.88010

4 3,254 2,550 2,547 - ‑ 15,142 0.75153

5 8010 4,108 - - ‑ 16,905 0.52808

6 5,582 - - - - 20,224 0.33026

Origin

period

Development period

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 103 2014 by All 10, Inc.

Solution to Sample Question 1

(3.25 points)

a. The incremental expected paid claims per unit of premium in each development period

1

1

1

1

, 1,...,

n k

ik

i

k n k

i

i

E S

m k n

V

b. Since the sum 1

n

kkm

represents the loss ratio over all reporting periods, the quantity

1

nBC

i i k

k

E U V m

is the expected value of the burning cost BC

iU of the total ultimate claims

required for the origin period i.

2013

BCE U = 3,000 * (.48 + .20 + .10) = 2,340

c. The loss ratio payout factor (a.k.a. loss ratio lag-factor)

1 1

1 1

1

1,...,

n i n i

i k k

k ki nBC

ik

k

V m m

p i nE U

m

represents the proportion of the total ultimate claims from origin period i, which is expected to be paid in the development period n – i + 1.

The quantity 2

1

1 , 1,...,

n

k

k n ii i n

k

k

m

q p i n

m

a.k.a. loss ratio reserve factor is the proportion

of the total ultimate claims from origin period i, which remain unpaid in the development period n - i +

1.

2013

(1,100 1, 200 1,300) / 7,500 .48.6154

(1,100 1, 200 1,300) / 7,500 (400 500) / (2,000 2, 500) 200 / 2,000 .78p

2013 20131 1 .6154 .3846q p

d. The burning cost of the total ultimate claims leads to the alternative claims reserve

2013 2013 2013; .3846*2,340 900coll BC coll BC

i i iR q U R q U .

e. The associated collective total ultimate claims is given by

, 1 2013 2013 2013,1, 1,..., ; 900 1,300 2,200coll coll coll coll

i i i n iU R C i n U R C

Earned

AY Premium 12 mos 24 mos 36 mos

2011 2,000 1,100 400 200

2012 2,500 1,200 500

2013 3,000 1,300

Sum 7,500 3,600 900 200

m12 m24 m36

48.00% 20.00% 10.00%

=3600/7500 =900/(2K+2.5K) =200/2K

Incremental Paid Losses

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 104 2014 by All 10, Inc.

Solution to Sample Question 2

a. , 1 , 1, 1,...,ind ind ind ii i i n i i i i n i

i

qR U C q U C i n

p

20132013 2013 2013,1 2013 2013 2013,1

2013

.3846* * *1,300 812.50

.6154

ind ind ind qR U C q U C

p

b. , 1,...,i

GB ind coll

i i i iR p R q R i n , where , 1,...,GB

i iZ p i n

20132013 2013 2013 2013 .6154*812.5 .3846*900 846.20GB ind collR p R q R

c. 1 , 1,...,i

WN WN ind WN coll

i i i iR Z R Z R i n , where 1

1 1

n i nWN

i k i kk kZ m p m

2013 .6154*.78 .48WNZ

30132013 3013 2013 20131 .48*812.5 .52*900 858WN WN ind WN collR Z R Z R

d. 1 , 1,...,i

c ind coll

i i i iR Z R Z R i n , where * ii

i i

pZ

p t

* ii

i i

pZ

p p

*

2013 .6154 / [.6154 .6154] .4396Z

2013

* *

2013 2013 2013 20131 .4396*812.5 .5604*900 861.50c ind collR Z R Z R

Solution to Sample Question 3

a (1.0 point) Calculate M6

M6 = 647/13,085 = 0.04944593

b. (0.25 points) Calculate 3t , associated with the optimal credibility weights*

3Z ,

3 3t p associated with the optimal credibility weights*

3Z , is 3 .8801 0.93814t

c. (0.5 points) Calculate the optimal credibility weights*

4Z , given that i it p

The optimal credibility weights*

iZ which minimize the mean squared error mse 2

c c

i i iR E R R

and the variance c

iVar R is given by *

*

ii

i i

pZ

p t

* 44 *

4 4

0.751530.46436

0.75153 0.75153

pZ

p t

.

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 105 2014 by All 10, Inc.

Solution to Sample Question 4

a (1.0 point) Calculate 2

2 2E U under the individual loss ratio reserving method.

b (1.0 point) Calculate 2

3 3E U under the collective loss ratio reserving method.

Theorem 4.3. Under the assumption of model (4.4), the following formulas for the MSE hold:

2 2

2 2

2 2

3 3

(1.001634 / 0.00314) / 0.99687 317.9933

1 ; 1.0299 / [0.06075*(1 0.06075 / .96915)]

ind ii i i

i

coll ii i i i

i

qmse R E U E U

p

qmse R E U q E U

t

=15.95309

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 106 2014 by All 10, Inc.

Solutions to questions from the 2013 Exam:

2a. (2 points) Calculate the individual loss ratio claims reserve Rind for the total of AYs 2010 - 2012.

2b. (0.75 point) Calculate the collective loss ratio claims reserve Rcoll for the total of AYs 2010 - 2012.

Model Solution 1:

a. Note: This solution is designed to be instructional

Step 1: Write an equation to compute the individual loss ratio claims reserve Rind for the total of AYs 2010 – 2012.

Rind for total (2010-2012) = /i i iq p C

Step 2: To determine ip , first write an equation to compute km , the incremental amount of expected

paid claims per unit of premium in each development period.

0 12 12 24 24 36

@ ; 0.356 0.205 0.078 0.639

( )

1400 1000 1500 650 850 2800.356; 0.205; 0.078

3600 3700 3650 3600 3700 3600

k total

sum loss dev age im m

sum Premium

m m m

Step 3: Write an eq. to determine ip , the loss ratio payout factor, the proportion of the total ultimate

claims from origin period i, which is expected to be paid in the development period n – i + 1.

2010 2011

2012

/

0.356 0.205 0.078 0.356 0.205 1.000; 0.878;

0.356 0.205 0.078 0.356 0.205 0.078

0.356 0.557

0.356 0.205 0.078

ip mi to date mi

p p

p

Note: The problem states no further development beyond 36 mos. Thus 2010 20101; 1 1 0p q

Step 4: Compute iq , the loss ratio reserve factor, the proportion of the total ultimate claims from origin

period i, which remain unpaid in the development period n - i + 1.

2010 2011 20121 ; 1 1 0; 1 0.878 0.122; 1 0.557 0.443i iq p q q q

Step 5: Using the given incremental paid losses in the problem, compute iC .

2010 2011 2012

paid loss todate

1,400 650 280 2,330; 1,000 850 1,850; 1,500

iC

C C C

Step 6: Using the eq. in Step 1 and the results from Steps 3-5, compute Rind for AYs 2010 – 2012.

, 1 , 1, 1,...,ind ind ind ii i i n i i i i n i

i

qR U C q U C i n

p

2010 2011

2012

(0 /1) 2,330 0; (0.122 / 0.878) 1,850 256;

(0.443 / 0.557) 1,500 1,193;

ind ind

ind

R R

R

0 256 1,193 1,449ind

TotalR

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 107 2014 by All 10, Inc.

Solutions to questions from the 2013 Exam (continued)

Model Solution 1 (continued)

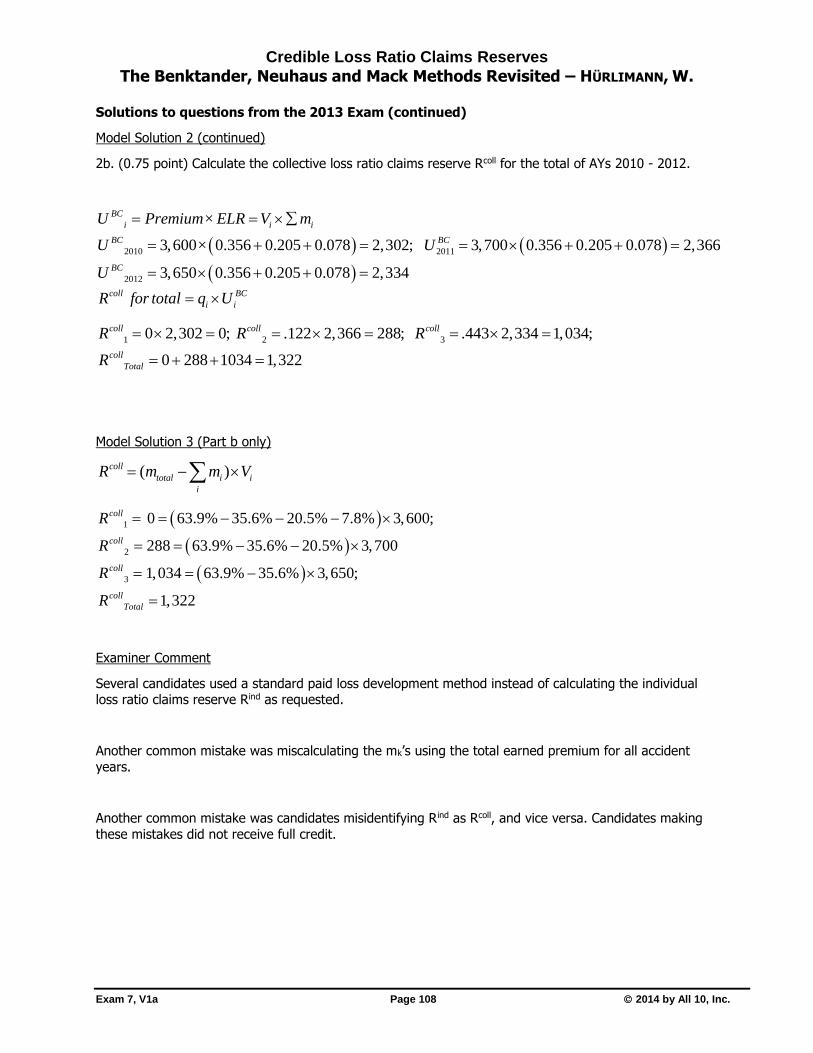

2b. (0.75 point) Calculate the collective loss ratio claims reserve Rcoll for the total of AYs 2010 - 2012.

Step 1: Write an equation to determine Rcoll for the total of AYs 2010 - 2012.

coll BC

i i i total iR for total q U q m V

Step 2: Using the eq. in Step 1, the results from part a, and the given premium, solve for coll

TotalR

1 2

3

0 .639 3,600 0; .122 .639 3,700 288

.443 .639 3,650 1,034; 0 288 1,034 1,322

coll coll

coll coll

Total

R R

R R

Model Solution 2

Note: Solution 2 simply shows what computations are needed to answer the question.

a. Rind for total (2010-2012) = /i i iq p C

0 12 12 24 24 36

( )

1400 1000 1500 650 850 2800.356; 0.205; 0.078

3600 3700 3650 3600 3700 3600

i

k

sum Loss at dev agem

sum Premium

m m m

2010 2011 2012

0.356 0.205 0.078 0.356 0.205 0.3561.000; 0.878; 0.557

0.356 0.205 0.078 0.356 0.205 0.078 0.639

i

i

i

m to datep

m

p p p

2010 2011 20121 ; 1 1 0; 1 0.878 0.122; 1 0.557 0.443i iq p q q q

2010 2011 2012

paid loss todate

1,400 650 280 2,330; C 1,000 850 1,850; C 1,500

iC

C

2010 2011

2012

2,330 /1.00 2,330 0; 1,850 / .878 1,850 256;

1,500 / .557 1,500 1,193

ind ind

ind

R R

R

0 256 1,193 1,449ind

TotalR

Credible Loss Ratio Claims Reserves

The Benktander, Neuhaus and Mack Methods Revisited – HÜRLIMANN, W.

Exam 7, V1a Page 108 2014 by All 10, Inc.

Solutions to questions from the 2013 Exam (continued)

Model Solution 2 (continued)

2b. (0.75 point) Calculate the collective loss ratio claims reserve Rcoll for the total of AYs 2010 - 2012.

2010 2011

2012

3,600 0.356 0.205 0.078 2,302; 3,700 0.356 0.205 0.078 2,366

3,650 0.356 0.205 0.078 2,334

BC

i i i

BC BC

BC

U Premium× ELR V m

U × U

U

coll BC

i iR for total q U

1 2 30 2,302 0; .122 2,366 288; .443 2,334 1,034;

0 288 1034 1,322

coll coll coll

coll

Total

R R R

R

Model Solution 3 (Part b only)

( )coll

total i i

i

R m m V

1

2

3

0 63.9% 35.6% 20.5% 7.8% 3,600;

288 63.9% 35.6% 20.5% 3,700

1,034 63.9% 35.6% 3,650;

1,322

coll

coll

coll

coll

Total

R

R

R

R

Examiner Comment

Several candidates used a standard paid loss development method instead of calculating the individual loss ratio claims reserve Rind as requested.

Another common mistake was miscalculating the mk’s using the total earned premium for all accident

years.

Another common mistake was candidates misidentifying Rind as Rcoll, and vice versa. Candidates making

these mistakes did not receive full credit.