Creating value in the coming decade - Deloitte México value in the coming decade. A strategic view...

40

Creating value in the coming decade. A strategic view of banking and financial sector synergies in Greater China Deloitte China Research and Insight Centre A Thought Leadership Paper for the Asian Financial Forum 2010

Transcript of Creating value in the coming decade - Deloitte México value in the coming decade. A strategic view...

Creating value inthe coming decade.A strategic view of banking and financial sector synergies in Greater China

Deloitte China Research and Insight Centre

A Thought Leadership Paper for the Asian Financial Forum 2010

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Our first objective . . .

2

This packet is based on a wide range of sources and discussions.

The findings and viewpoints of the Asian Financial Forum Deloitte workshop provides a

bridge to the next step.

The next step is to focus on specific ideas and suggestions, based on select interviews

with participants in and expert observers of the financial services transformation in

Greater China and Asia.

. . . is to propose a framework for organising quantitative

and other information to participate in a practical

discussion of the regions within Greater China and of

Greater China in Asia

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Summary and overview I

3

Incre

asin

g

inte

ractions

Inte

gra

tion &

diffe

rentiation

Ma

rkets

&

reg

ula

tion

Creating value in the coming decade

In this unique moment, when China’s emergence in the world converges

with unprecedented stress in the global financial order and stability, we

expect deep transformation of the interactions of the economies of the

Chinese Mainland, Hong Kong SAR and Taiwan, and in turn the

interactions of Greater China and the Asian region.

In the course of the next decade, two strong forces will interact, with the

potential to create huge value for the economies of Greater China as a

whole and for innovative service enterprises and companies, especially in

financial services. These are the forces bringing about integration of some

elements and the forces maintaining differentiation and specialisation.

The evolution of the integration of the Chinese Mainland, Hong Kong SAR

and the development of well-differentiated areas of specialisation are

shaped by both regulations and market forces. The detailed analysis of

these forces can be of great value to government and business leaders.

Optimising both regulatory progress and market activity will contribute to a

sustainable recovery and a major role for Greater China in the new global

order.

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Summary and overview II

4

Several categories of Mainland trade and investment agreements have

developed quickly over the last few years. These include CEPA agreements

with Hong Kong SAR, trade and investment MOUs with Taiwan, and Free

Trade and currency agreements with Asian neighbors. Major changes in

RMB rules and roles open the door to new business opportunities.

Financial service companies have extended their reach across Greater

China regions and across Asian national borders, through M&A, branch-

building, and other forms of investment. IPOs in all of China’s markets will

become more diverse and international, and hundreds of new equity

investors are becoming active with RMB and foreign funds.

The global crisis has triggered potentially deep reform of financial service

regulations, enforcement, reporting rules, and risk management. Mastering

best practices and high levels of compliance with new standards and

regulations will become increasingly important for China’s financial service

companies as they grow in size, footprint, and global importance.

Re

gu

lato

ry

pro

gre

ss

Ma

rket-

dri

ven

tre

nds

Glo

bal co

nte

xt

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Our major premises . . .

5

The Chinese Mainland, Hong Kong SAR and Taiwan will experience

more -

• Strategic specialisation will bring prosperity, productivity, and efficiency to all regions

• Business and government leaders are in the process literally of spelling out detailed

plans for the future roles of their regions

• Orderly market growth is a combination of effective regulation and market-driven

business innovation, in balance

• Increasing consolidation of

sectors

• Interlinked ownership

• Strategic partnerships

• Alignment of regulations

and process

Clarification, variation,

articulation of the unique

commercial and regulatory

features that support the

planned growth model

Integration

Differentiation

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Entering the second decade of the 21st Century . . .

6

• The global financial crisis is a watershed event that marks both new

opportunity and responsibility for Asia

• China, as the dragon head of Asia, is experiencing wave after wave of

major financial system reform. We must understand China within its

own historical and regulatory context that takes into account the

country's 3-decades of developments and shifts toward a market

economy from a planned economy

• Everyone understands that the stakes are high and so is the potential

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Markets and regulations will interact to create the new

financial environment

7

Asian market dynamics

• Trade regulations/agreements

• Investment regulations/agreements

• Currency regulations/agreements

• Financial service supervision

Greater China

• Macro-economic results

• Consumers and producers

• Specialisation

Taiwan

Hong Kong Mainland

Asian policies/agreements

Greater China

Taiwan

Hong KongMainland

integration

differentiation

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Within Greater China, the future roles of regions will be

defined by both integration and differentiation

8

1. Regulatory trends

Freer flow of goods and investment capital, with increased integration of banking and other financial services and increased inter-operability of equity markets and financial instruments. But strong regulatory differences will remain.

2. Market trends

Goods and service markets will simultaneously move toward harmonisationand strengthened regional specialisation, driven by consumers, enterprise skills, and resources. Macro growth and sector growth among regions will be coupled, but in some cases inversely.

1. Regulatory questions

For banks and equity markets, what will be the future regulations and exchange values of the RMB, HK$, NT$, and US$?For financial services in each region, what are the biggest opportunities for strong service differentiation and growth?

2. Market questions

In real estate & equity markets, what will be the financial service and arbitrage opportunity from strong moves in the three regions?Among macro-economic factors and commercial sectors, which will trend together, which differently, and which inversely?

Creating value in the coming decade

Greater China

Taiwan

Hong KongMainland

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Key financial management trends emerged from recent

economic meetings in Beijing - RMB value and control

9

• The RMB may appreciate against the US$ but will do so in a well-managed and

gradual way. Premier Wen Jiabao recently told Xinhua News Agency (27 Dec

2009) that China will not bow to pressure from other countries to revalue RMB

• In the face of lasting export contraction and concerns about further job losses in

export business, the leaders will focus on domestic issues and keeping exports

competitive

• In terms of RMB value, the Economic Work Committee focused on the threat of

inflation, which some appreciation could help curtail

• In terms of RMB control, pursuing an international role for the RMB, leaders are

liberalising both trade and investment regulations, most recently moving to

make the RMB a legal tender for certain investment activities in Hong Kong

SAR. The expansion of RMB use in Hong Kong SAR is a major step

• Moderating the appreciation of assets, especially real estate and equities, is a

cornerstone commitment but it is weighed against maintaining an attractive

capital gain opportunity to draw and hold investment

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Liquid stores of value: will there be realignment of the HK$?

10

2005a 2006a 2007a 2008a 2009b 2010c 2011c 2012c 2013c

Rmb:US$ (year-end) 8.07 7.81 7.31 6.84 6.8 6.43 6.34 6.09 6.01

HK$:US$ (year-end) 7.75 7.78 7.8 7.75 7.8 7.8 7.8 7.8 7.8

NT$:US$ (year-end) 32.85 32.6 32.44 32.86 32.59 31.82 31.08 30.22 29.39

a Actual. b Economist Intelligence Unit estimates. c Economist Intelligence Unit forecasts.

Source: http://www.goldprice.org/gold-price-per-gram.html

Five year gold prices (2005-2009)

Currencies over the years

5 Year Gold Price in USD/oz 5 Year Gold Price in HKD/oz 5 Year Gold Price in RMB/g

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

This trend creates valuable opportunities for financial services

to innovate and expand - regulation

11

Area of regulation Example key issues

Currency Valuations and linkages, roles and scope of use, authorised

footprint.

Banking regulation Licensed service scope, interest rates, fund policies and

reserve requirements, branch policy, ownership.

Other financial services Licensed business scope, capital requirements, branch policy,

ownership.

Central Bank policy Primary goals, credit availability, inflation guidelines,

governance, commercial and policy bank relationship.

Taxation Architecture of taxation, VAT, capital gains, corporate income,

IIT, transactions, property.

Where change is occurring . . .

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

This trend creates valuable opportunities for financial services

to innovate and expand - markets

12 Creating value in the coming decade

Market issues Example key issues

Bank specialisation Configurations of merchant, investment, retail, and trust

services, mass market, hi-net worth market.

Innovation capacity Internet, consumer credit and credit/debit devices, transaction

fulfillment, diverse deposit and loan instruments.

Financial service

infrastructure

IT, legal, HR and all forms of support that are based in critical

mass and a developed sector.

Ownership and autonomy Ownership, governance, control structures, owner types

(State/ public/ private, foreign/domestic) .

Footprint One region, cross-region, Greater China, Asia region, Global,

service and footprint growth strategies, controls.

Where change is occurring . . .

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Overview of terms and expectations of the Chinese Mainland -

Hong Kong SAR special agreements

13

The level and complexity of financial service activities across the Chinese

Mainland and Hong Kong SAR borders, in some cases with Shenzhen, makes

it difficult to identify key agreements.

CEPA was certainly an important step, first signed in June 2003, because it

formalised a process for planning cross-border service activities, and it

provided an important legal platform for innovative relationships and structures,

including new customs procedures.

First impact was on Hong Kong SAR exports, for which duty free access to

China markets was phased in, with local processing and content requirements

to make sure they truly originated in Hong Kong SAR. In the first 18 months of

CEPA, over 2,700 certificates of origin were issued representing Hong Kong

SAR exports of over HK$1 billion.

Since the original signings, a series of CEPA agreements has opened up 42

service categories with over 250 specific measures liberalising trade.

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

CEPA milestones

14

Issue date Implementation

date

Contents

1st Supplementary

CEPA

Agreement

27 Oct 2004 27 Oct 2004 • Repeal more regulatory/legal restrictions on Hong Kong SAR’s mainland-

bound businesses activities on legal service, accounting, medical service,

audio & video products, construction, distribution, bank services, securities,

transportation, logistics areas; and

• Expand business scope for Hong Kong SAR permanent residents

registering businesses on the Chinese Mainland.

2nd CEPA Agreement 18 Oct 2005 18 Oct 2005 • Zero-tariff placed on all imported goods originally made in Hong Kong SAR,

effective on 1 Jan 2006; and

• On the basis of original commitment, more liberal market entry polices

awarded to Hong Kong SAR companies in ten areas – legal service,

accounting, audio & video production, construction, distribution, bank,

securities, tourism, transportation and individual businesses.

3rd CEPA Agreement 27 June 2006 27 June 2006 • The mainland government agreed to adopt 15 regulatory measures to

facilitate the opening process to Hong Kong SAR businesses from lowering

registration thresholds, larger shareholding status to less regulatory

restrictions for opening new businesses on the mainland.

4th CEPA Agreement 29 June 2007 1 Aug 2008 • Expand the number of opened areas to 38 from original 27, adding sports

service, environment and other items.

5th CEPA Agreement 30 Sept 2008 30 Sept 2008 • Specify detailed opening measures for 29 service trade items; and

• Grow the opening items to 40;

6th CEPA Agreement 9 May 2009 1 Oct 2009 • Detail 29 concrete measures for opening up, covering 20 key service sectors

i.e. bank service, tourism, securities, exhibition, transportation, legal service,

etc. ; and

• Expand the list to 42 items after adding R & D and railway transportation

service.

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

CEPA - Main impact and statistical results

15

What are the main impacts of CEPA agreements?

• The zero-tariff policy awarded to the goods originally made in Hong Kong SAR by CEPA supports the development of local manufacturing business

• Thanks to CEPA offering some 250+ investment perks in 42 industries that feature lower entry requirement, broader scope of business/operational area and others, Hong Kong SAR investors can compete with mainland counterparts on an equal footing

• CEPA drew additional investment into Hong Kong SAR, including new manufacturing cateogories, because of CEPA access to the Chinese Mainland markets

• CEPA constructs a formalised business/regulatory framework, laying a solid ground for the entities on two sides to cooperate on broader spectrum of businesses including e-commerce, legal service, intellectual property protection, food safety and other areas

What have been the results?

According to the PRC Ministry of Commerce, CEPA has had a large beneficial impact in Hong Kong SAR in terms of economic growth

• Annual Growth Rate (2003-2008) Vs Annual Growth Rate (1997-2002)

• GDP: 6.3% vs. -1.0%

• Stock market capitalisation: 13.4% vs. 2.1%

• Total retail sales: 9.6% vs. -5.6%

• Total trade volume with the Chinese Mainland: 18.4% vs. 6.4%.

• Unemployment rate: 4.1% (end of 2008) vs. 8.7% (end of 2003)

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Some significant basic regulatory changes are underway

between Hong Kong SAR and the Chinese Mainland that will

offer business opportunities

16

Promoting integration Sustaining differentiation

Certain outcomes

Unknown outcomes

New business models

New Financial services

Regulatory intensity

Increased complexity

Real estate impact

Stock market impact

CNY/HK$/US$ impact

• All forms of taxation

• Customs

• Currency regulation

• Banking regulation

• Equity markets

• Insurance

• Judiciary

• Information freedom

• CEPA driven border

openings

• CNY use for capital

transactions

• CNY bond market

• CNY banking and trade

settlement

• Freer, faster travel

• Financial service

providers /branches

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

After a decade of market-driven Mainland-Taiwan investment

and trade, formal activity surged in 2008

17

Chen Yunlin (陳雲林), chief of the Chinese Mainland’s Association for Relations Across the

Taiwan Straits (ARATS) has met with his Taiwanese counterpart, Chiang Pin-kung (江丙坤),

chair of the Straits Exchange Foundations (SEF) four times since mid 2008.

• Cross-Strait Agreement on Travel to Taiwan by Mainland Residents (海峽兩岸關於大陸居民赴台灣旅遊協議)

• Texts of Minutes of Talks on Cross Strait Charter Flights (between ARATS and SEF)(海峽兩岸包機會談紀要)

June

2008

• Cross Strait Flight Cargo Agreement (海峽兩岸空運協議)

• Cross Strait Food Safety Agreement (海峽兩岸食品安全協議)

• Cross Strait Marine Shipping Agreement (海峽兩岸海運協議)

• Cross Strait Postal Service Agreement (海峽兩岸郵政協議)

November

2008

• Cross-Strait Financial Cooperation Agreement (海峽兩岸金融合作協議)

• Supplementary Agreement on Cross Strait Air Cargo Transportation (海峽兩岸空運補充協議)

• Agreement on Cross Strait Judicial Mutual Support and Crackdown on Crimes (海峽兩岸共同打擊犯罪及司法互助協議)

April

2009

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Mainland-Taiwan investment and trade talks continued at a

quick pace throughout 2009

18

A fourth formal ARATS-SEF meeting began on 22 December, 2009, intended to

refine the details and implementation plans for previous agreements, including the

“Memorandum for Understanding Cross Strait Financial Supervision Cooperation

(兩岸金融監理合作瞭解備忘錄)” signed 17 November, 2009. Of all the agreements

signed, the agreements on financial cooperation are the most significant. Contents

covered many topics but at a general level:

• Financial supervision - Mutually support financial/monetary oversight and

information sharing to maintain cross-strait financial stability; open representative

offices of relevant agencies in each other’s jurisdiction

• Financial supervision - Construct a mechanism to jointly oversee/manage cross-

strait bank, securities/futures and insurance markets

• Currency management - Arrange for commercial banks initially to undertake

currency exchange, supply and recycling, leading to a cross-strait currency

settlement mechanism

• Branches for financial service providers - Agreement to hold further talks on

financial institutions establishing operational branches in each other's jurisdiction

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Taiwan companies listed in the Chinese Mainland

19

Company name Stock exchange

& ticker

Listed date

(yyyy/mm/dd)

Note

Chunghwa Picture Tubes (中華映管)

<the shell company is Mindong Electric閩東機電>

000536 - SZ 2009/02 Backdoor

listing

Hanbell Precise Machinery Company

(漢鐘精機)

002158 - SZ 2007/08/17 IPO

Gem Year Industrial Co Ltd

(晋億實業)

601002 - SH 2007/01/26 IPO

Shenzhen Hsin-Tech

(深圳信隆實業)

002105-SZ 2007/01/12 IPO

Guangzhou Seagull Kitchen And Bath Products

Company (海鷗衛浴)

002084 - SZ 2006/11/24 IPO

Shenzhen Globe Union Industrial

(深圳成霖潔具)

002047-SZ 2005/05/31 IPO

Zhejiang King Refrigeration Industry Co.

(浙江國祥製冷)

600340 -SH 2003/12/15 IPO

Tsann Kuen (China) Enterprise Co., Ltd

(厦門燦坤)

(B) 200512-SZ 1993/06/30 IPO

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Chinese Mainland/Hong Kong SAR/Taiwan financial services

M&A increased rapidly in the last half of the decade

20

2005 2006 2007 2008 2009 YTD*

Chinese Mainland Hong Kong SAR 122 1,564 688 7,108 3,030

Chinese Mainland Taiwan 87 - 11 2

Hong Kong SAR Chinese Mainland 843 2,332 5,894 3,388 3,969

Taiwan Chinese Mainland 76 6 33 1 3

Total 1,041 3,989 6,615 10,508 7,003

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2005 2006 2007 2008 2009 YTD*

Announced Chinese Mainland/Hong Kong SAR/Taiwan cross border M&A in financial services sector (Deal value in US$M)

TW -> China mainland

HK -> China mainland

China mainland -> TW

China mainland-> HK

Creating value in the coming decade

n Taiwan Chinese Mainland

n Hong Kong SAR Chinese Mainland

n Chinese MainlandTaiwan

n Chinese MainlandHong Kong SAR

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Selected strategy considerations on regional expansion

21

Using the Cross Border Dynamics

...in Hong Kong SAR ...in the Chinese Mainland ... In Taiwan

Hong Kong SAR Banks...

• Capture opportunities related to increased trade and consumer flows through Hong Kong SAR

• Leverage increased FX opportunities related to currency convergence

• Capitalise on stock market activities and increased private banking demand, leveraging the specific Hong Kong SAR service culture and professional environment

• Protect market and staff share against incoming competition

• Consider M&A opportunities • Use Hong Kong SARs international set up as a

gateway for China business and as AP HQ• Hong Kong SAR-bound IPO for mainland

companies

• Focus on IB activities in Shanghai and Shenzhen

• Focus on trade activities of Hong KongSAR companies in the mainland and service companies in the mainland with interests in Hong Kong SAR

• Selectively expand into the mainland with branches and acquisitions, leveraging the Hong Kong SAR specific expertise, service culture and technology in profitable niches

• Targeting high-income population

• Focus on IB activities related to the stock market

• Service corporate business with cross regional trade flow

Chinese Mainland Banks...

• Use Hong Kong SAR as a hub for international expansion

• Use economies of scale for efficient retail value proposition in Hong Kong SAR

• Establish IB activities using HK as a further incubator area

• Use Hong Kong SAR as a hub for private banking activities of mainland HNWI

• Expand into Hong Kong SAR based on regional and international trade flows

• Leverage strength in RMB business activities to profit from the regional expansion of the Chinese currency

• Use Hong Kong SAR as a resource base

• Offer mainland customers services through Hong Kong SAR, focusing on IB, private banking and corporate finance activities

• Use Hong Kong SAR service culture, products and technology as a model for further differentiation and upgrade of mainland banking services

• Expand and keep existing market shares in the face of competitions from Hong Kong SAR and foreign rivals

• Expand into Taiwan, leveraging cross border trade flows and the mutual cultural heritage

• Focus both on retail and corporate business

• Offer Taiwan IPOs to mainland customers who can benefit from the specific strategic set up of the Taiwan Stock Exchange

• Use Taiwan as a resource base• Mainland tourists

Taiwanese Banks...

• Use Hong Kong SAR as an additional base for both PRC and international business

• Service Taiwanese corporate and private businesses in the mainland, leveraging cross border activities, production and trade flow

• Exploit the Chinese Mainland retail and corporate opportunities in selected areas, leveraging products, service culture and technology

• Focus on Chinese Mainland companies using Taiwan as a technology hub

• Focus on incoming mainland tourists asbanking clients

• Introduce Chinese Mainland companies to the Taiwan stock market

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Chinese Mainland banks in Hong Kong and Hong Kong banks

in Chinese Mainland

22

• BOC in Hong Kong SAR: Since established on 1 October 2001, BOCHK has combined the businesses of 10 banks

in Hong Kong SAR originally belonging to the Bank of China Group. In addition, it holds shares in Nanyang

Commercial Bank Ltd and Chiyu Banking Corporation Ltd, as well as BOC Credit Card (International) Ltd. With

over 270 branches, 470 ATMs and other distribution channels, a leading listed commercial bank group and also

one of the three note-issuing banks in Hong Kong SAR.

• CCB in Hong Kong SAR: China Construction Bank in Hong Kong has two organisations, CCB Asia and CCB

International, covering commercial and investment banking. The purchase of AIG Finance (Hong Kong) Ltd gained

the credit card business. Adding to 22 branches and two Premier Centers at the end of the 2008, CCB plans to

open at least seven new branches. The network expansion plans also include opening a third Premier Select

Centre in Hong Kong SAR and 12 to 15 branches annually in Hong Kong SAR over the next three years.

• ICBC in Hong Kong SAR : Industrial and Commercial Bank of China has three organisations in Hong Kong SAR,

ICBC Asia, ICBC East Asia and ICBC International, focusing on commercial banking operations.

• China Merchants in Hong Kong SAR: China Merchants purchased the Wing Lung Bank, Hong Kong SAR’s fourth

largest independent bank, citing Hong Kong SAR’s close ties to global financial markets and is highly compliant

with international business models and legal systems.

• CITIC in Hong Kong SAR: On 8th of May 2009,CITIC Bank concluded a share purchase agreement with CITIC

Groups for 70% of CITIC Int’l Financial Holdings Ltd as a platform to expand into international operations.

• Hong Kong SAR banks in China: Wing Hang Bank, which located its headquarters in Shenzhen, reported giving

positive considerations to opening branches in places like Foshan, Dongguan and Zhongshan. Bank of East Asia

announced it planned to open four branches within two years, and both Hang Seng Bank and HSBC have

announced plans or expressed interest in opening branches on the mainland.

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Chinese Mainland banks in Taiwan and Taiwan banks in

Chinese Mainland

23

On the Chinese Mainland side

• Bank of China and ICBC are aiming to be the first of Chinese Mainland lenders

to have branches in Taiwan

• China Construction Bank, Bank of Communications , and China Merchants Bank

plan to build presence in Taiwan once when regulations permit

• It's expected that Chinese Mainland and Taiwan banks will open branches in

each other's markets during the first quarter of 2010 as the just-signed MOU

takes effect within 60 days

On the Taiwan side

• Bank of Taiwan (BOT) was officially granted permission to set up an office in

Shanghai, a milestone in financial cooperation

• Bloomberg reported Cathay Financial Holdings and Mega Financial are set for

expansion on the mainland

• Fubon Bank plans to increase its stake in Xiamen City Commercial Bank; and

the bank is also among the bidders for Morgan Stanley's stakes in the Chinese

investment bank - CICC

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Special zones of Chinese Mainland-Taiwan interaction

24

• As the first Chinese company to be listed in Taiwan, Shenzhen Keen High

Technologies, began trading on Taiwan's Emerging Stock Market in November of

this year and plans to move to the OTC in six months

• Billed as the "frontline platform" for exchanges with Taiwan, Fuzhou (the capital of

Fujian province) keeps close economic trade tie-up and frequent personnel

exchanges with Taiwan. Fuzhou hosts about 3,000 Taiwan-funded companies

and over 20,000 Taiwan businessmen and their families

• Recent movements of Fuzhou: 100 billion yuan investment in railway construction

allows Fujian to be connected with Yangtze River Delta, Pearl River Delta and

other mainland places

• The PRC Ministry of Commerce (MOC) is planning to establish some new

Taiwanese investment zones in Fuzhou, Xiamen and Quanzhou, and lift

restrictions on petty trade across the Taiwan Strait - e.g. shipping companies of

both Chinese Mainland and Taiwan can enjoy tax exemptions on their business

income for ships plying between Fujian’s coastal regions and the three offshore

islands of Taiwan

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Chinese Yuan activity in Hong Kong SAR

25

At the end of 2008, 39 licensed banks were conducting RMB business in Hong Kong SAR.

RMB deposits reached RMB56 billion by the end of 2008, up 68% over 2007. The increase

occurred mainly in the first half of 2008, when the RMB was on the trend of appreciation.

In July 2009, a pilot scheme for the use of RMB in settling cross border trade between the

Chinese Mainland and Hong Kong SAR was launched. The scheme allows cross border

trade to be denominated and settled in Hong Kong SAR in RMB. Previously, these were

settled in other currencies such as the US dollar, exposing importers and exporters to

currency exchange risks. Under the pilot scheme, qualified companies in Shanghai and

four cities in Guangdong (Guangzhou, Shenzhen, Zhuhai, and Dongguan) can settle trades

in RMB with their counterparts in Hong Kong SAR, Macau SAR, and countries of ASEAN.

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Equity markets - Hong Kong SAR and the Chinese

Mainland stocks

26

• After over a decade of the Chinese Mainland listings in Hong Kong SAR - Hong

Kong SAR remains an accessible but differentiated IPO opportunity for mainland

enterprises, usually supporting lower multiples than Shanghai and Shenzhen but

additional international exposure and elevated status

• Chinese Mainland companies accounted for 60% of total market capitalisation -

A total of 1,083 companies were listed on the main board of the HKEx as of end-

2008, including 10 foreign companies and 464 mainland China incorporated

enterprises and companies incorporated outside China but controlled by

mainland entities. Another 176 companies were listed on the Growth Enterprise

Market (GEM). Chinese Mainland companies accounted for 60% of the total

market capitalisation (main board and GEM) at the end of 2008, up from 58% in

2007 and 39% in 2006

• Can Hong Kong SAR become a focus of BRIC and other emerging market

listings? The interesting and unique history of the Rusal listing process

demonstrates the attractiveness of Hong Kong SAR, and that will be

strengthened if China wealth continues to outpace global wealth growth and

access to Hong Kong SAR markets for the Chinese Mainland investors

continues to improve

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Chinese Mainland stocks in Hong Kong SAR have performed

more steadily than index averages

27

• The Hang Seng Index (HSI), is a free-float, market-weighted index of a selection of companies

• Hang Seng Composite Index tracks the movement of the top 200 listed stocks by market

capitalisation

• Hang Seng China Enterprises Index, tracks the movement of Chinese Mainland-incorporated

enterprises or H-shares

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Equity markets - Taiwan and foreign investors

28

• The TSE had 728 listed firms by the end of August 2009

• All foreign investors can now invest in the securities market after registering with

the Taiwan Stock Exchange Co (TSEC) and obtaining an investment ID. Each

foreign institutional investor (FINI) is allowed to invest directly in the stock

market, with no upper limits. Foreign individual investors (FIDIs) previously faced

a limit of US$5m, but the TSE had it removed on 20 October 2008

• According to the Securities and Futures Bureau of Taiwan, the cumulative FINI

investment in the securities markets as of June 2009 totaled US$134.3billion,

down from US$144.2billion one year earlier

• As the first Chinese Mainland company listed in Taiwan, Shenzhen Keen High

Technologies, began trading on Taiwan's Emerging Stock Market November

2008 and planned to move to the OTC board

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Equity markets - IPO trends

29

• In 2009, 69 companies went public in Hong Kong SAR with US$ 51.3 billion

raised. For the first time ever, Hong Kong SAR IPOs raised more money than all

of the US exchanges. 80% of the listings were Chinese Mainland corporations

• 9 companies went public in Shanghai with total proceeds of US$18.2 billion

• Yet, it was a mixed year for Hong Kong SAR, with over half of the twenty largest

listings currently traded under their opening price, underperforming the Hang

Seng index by an average of 15%. Some sectors, like real estate, grew cold

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Overview of Shanghai’s proposed role as an international

financial centre

30

• In ten years, when Shanghai expects to reach its goal as an international financial center, it will have developed areas of specialisation in financial services and services broadly.

• Hong Kong SAR and Taiwan service sectors will complement and compete with Shanghai in various ways.

Framework and measures for developing Shanghai into an international financial centre

• The PRC government’s main targets: by 2020, build Shanghai to be an international financial centre consistent with China’s economic strength and status

- By 2020, Shanghai should have:

- a multi-functional and highly internationalised financial market system

- a pool of internationally competitive financial institutions, including Private Equity, Venture, and other funds

- a strong pool of financial professionals

- a strong infrastructure for competing globally

- a compatible system of taxation, credit, regulation and law

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Shanghai dominates the national financial services

landscape - by certain measures

31 Creating value in the coming decade

. . . But the largest are HQ’d in Beijing and Shenzhen

and its Guangdong surroundings have become the

meeting place of the Chinese Mainland and Hong

Kong SAR banks

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Shanghai dominates the national financial services

landscape - by certain measures

32

Shanghai Mainland financial service shares

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

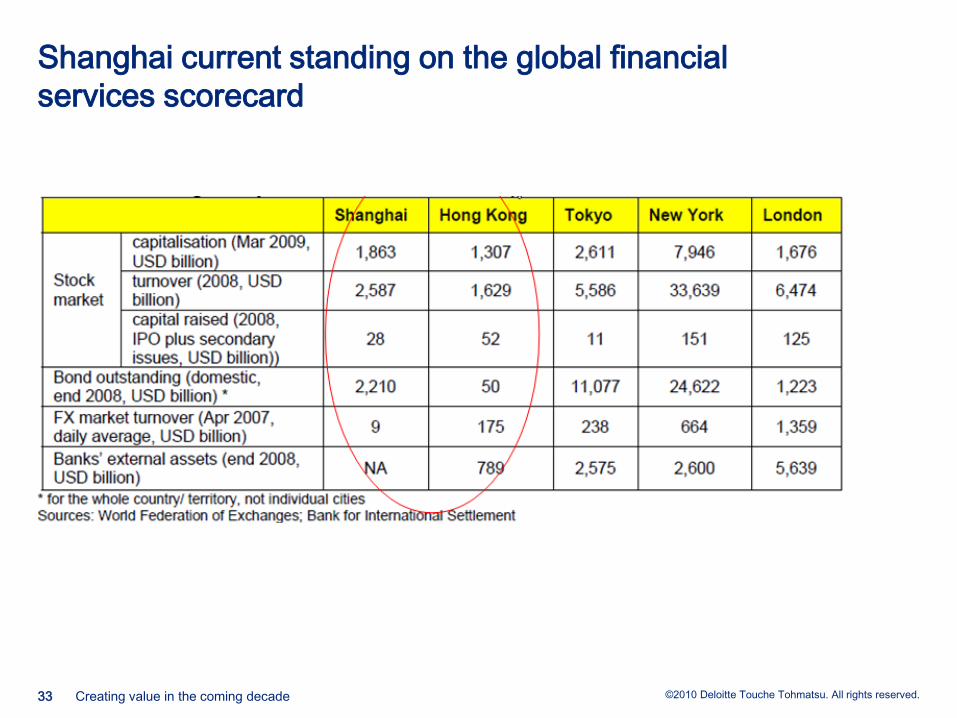

Shanghai current standing on the global financial

services scorecard

33 Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

There are models outside Asia of strong economies based on

special financial services environments

34

Switzerland has significant similarities to Hong Kong SAR

• Services, and mostly financial services, are a very high component of GDP

• Promotes its own currency next to a dominant neighbor

• Attracts international head quarters based on stable and efficient systems combined with very low taxation

• Has both strong "local" characteristics yet is also extremely international. Zurich is often called a "global village“

• Promotes its financial services industry successfully by building regulatory barriers to the rest of Europe, mainly by its banking secrecy and taxation rules

• There is a continuous discussion as to whether Switzerland at some point in time will be forced to enter the EU, and if the current model is sustainable

Euro in Swiss Francs (CHF)

CHF- A Stable Currency

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

In terms of our analytic model, how has Switzerland integrated

and how has it differentiated?

35

• Long promoted free trade and was a founder of EFTA

• Ranks 16 of 178 in "Ease of doing business index "

• Has signed 2 agreements with the EU to promote free trade with neighboring countries. Basically, as a EU citizen or company, dealing with Switzerland works like dealing with any other EU state

• Neutral country with no conflicts since the 19th century. High quality military force firmly protects Swiss borders

• Not part of the EU, and does not intend to become EU member; Entered the UN very late (only in 2002)

• Has retained the CHF, even though most of Europe is Euro; CHF is deemed as a safe haven

• Strong focus on competitiveness, attracting key head quarters of MNCs, through very low taxes (both corporate & individual)

• Financial services sector promotes privacy, security, & confidence

• Some local protectionism on home made products

Integration

Differentiation

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

The impacts of global regulatory and practice changes

36

• As local or independent banks become national or regional in their footprints, robust processes for compliance with current and prospective global banking standards and practices will gain importance

• Advanced capabilities in these areas could constitute a competitive advantages for financial institutions with longer exposure to global marketplace relationships than the major Chinese Mainland ones

• Banks that have developed in economies that support more independent financial institutions than the Chinese Mainland in the first decades of reform are likely to be faster in achieving advanced capabilities in these areas

1. Beyond Basel II

2. Key trends in financial reporting and accounting

3. Stress testing of financial institutions

Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Type of regulation Potential impacts

Capital requirements • Definition of „predominant Tier I capital“

• Significant restrictions of using subordinated capital

• Deduction of minority interest from capital

• Phase out of innovative hybrid instruments

• Introduction of overall maximum leverage ratio

• Capital buffers to cope with pro-cyclical effects of regulation

Liquidity risk regulation • Introduction of short term liquidity and long term net stable funding

ratios, as well as liquidity monitoring ratios

• Requirements to keep highly liquid assets

• Requirement for liquidity risk stress testing and adequate risk mitigation

Credit risk regulation • Increased use of stress testing and scenario analysis

• Additional capital charged for trading related credit exposures

(derivatives, repo and securities financing)

• Strengthened criteria for external ratings eligibility under Basel II

Pillar 2 of Basel II • Regulators are expected to reinforce overall risk management

capabilities of banks, including the efficiency and effectiveness of risk

appetite setting and board involvement (Pillar 2 of BII)

Accounting convergence • Due to the crisis, IASB and FASB have speeded up their efforts to

simplify and make accounting rules for financial instruments more

efficient

• Recent developments are IFRS 9, as well as several exposure drafts

(e.g. on loan loss provisioning)

Linking compensation to

risk taking

• Several regulators and the BCBS have introduced concepts to require

financial institutions to restrict undue risk taking of financial institutions

based on compensation rules

• As local or independent banks become national or regional in their footprints, robust processes for compliance with current and

prospective global banking standards and practices will gain importance

• Irrespective of the specifics of local and regional legislation, it is to be expected that some major trends in international

regulation will have significant influence on Asian and Greater China regulatory developments. Here are some examples:

Impacts of global regulatory changes

37 Creating value in the coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.38

Areas

Regulatory

environment

Monetary & fiscal

policy environment

Major transformation of the Western financial services industry

Financial services

marketplace

Risk environment

Client behavior

HR

Technology and

innovation

Other

Shift of financial strength and

market power from West to East , and away from Hedge

Funds

Corporate bonds substitute

bank loans

Turmoil entails increased fraud

and operational risk

Overall significant loss of

credibility of Western financial system

Expansion of cross border

cooperation of regulators

Tightened capital requirements

and liquidity risk regulationIncreased discussion of board

responsibility

Reform of Standards (“Basel

III”), with a focus on making rules “anti-cyclic”

Fundamental change of

competitive landscape and business models, massive

deleverage

High volatility of market data /

valuations and wide spreads –“market hysteria”

Global recession leads to

further increased levels of NPLs and capital shortage

Flight to security – massive

funds parked with few choices of safe haven remaining

Capital increases become

more and more difficult

Cost cutting becomes key

objective

Changes in accounting

framework (trend to globalisation of IFRS)

Unexpected domino effects

and surprising bad (and sometimes good) news

continue

Ownership and governance

issues in financial services, through Nationalisation

HR availability changing

dramatically through restructuring/job-cuts

Downturn leads to strong

change in demand for products and credit

Intensifying market

Consolidation - take-oversthrough low valuations

Exploding growth of state

deficits, leading to changes in State ratings

Trend to regulatory

protectionism due to nationalisations

Further bank failures and

liquidity crunch, irrespective of “rescue” measures

Moral hazard through political

intervention

Deflationary environment, with

risk of hyper inflation in the future

Widely diverse use of “rescue”

schemes, e.g. bad banks, TARP, deposit insurance

programs, etc

Unclear effect of

discontinuance of state stimulus packages

Delay of important investments

due to loss of business and capital

Regulatory driven innovation

Rating agencies lose influence

and become subject to supervision

Regulators under strong

pressure as to their role in some of the casualties (e.g.

SEC / Madoff)

Compensation becomes widely

discussed issue and regulatory focus

Difficulty to keep best people in

profitable areas within “wounded” institutions

Strong impact of crisis

management on trust in currency and increased

isolation of interests

(“De-Globalisation”)

Swift sentiment swings in

investment behavior

Uncertainty and State

intervention may cause delay / failure of corporate

restructuring

Pressure to create market

interconnectivity and data management standardisation

Fast shifts in importance of

asset/instrument classes make investments difficult

Motivational deficits due to

“depression blues”

Inability to make bold decisions

and overreactions as leadership patterns

The difficulties of the Western financial services industry and the related developments of state rescue and stimulus packages of key

economic areas are further external factors that need to be considered by financial institutions in the Greater China area.

Creating value in coming decade

©2010 Deloitte Touche Tohmatsu. All rights reserved.

Some key questions to address in Hong Kong SAR

and Taiwan

39

1. What are the key potential areas for Hong Kong and Taiwan to

supplement/enhance cross-border investments between and among the Chinese

Mainland, Hong Kong SAR and Taiwan enterprises?

2. In light of the fact that Hong Kong SAR and Taiwan do not have foreign

exchange control measures, what is the potential for Hong Kong SAR and

Taiwan to participate in and enhance inter-regional and global cross-border trade

with the Chinese Mainland, by serving as the offshore foreign exchange centre?

3. What is the possibility for the Chinese Mainland and/or Hong Kong SAR and/or

Taiwan financial institutes to form joint ventures and alliances for better

penetration of target markets within each other’s jurisdiction and with high levels

of commercial synergy?

4. Assuming continued strong wealth creation in the Chinese Mainland, what

services in retail and commercial banking will be possible by regulation and

profitable for Hong Kong SAR and Taiwan financial service providers?

5. How might blue chip/sizeable companies strategically utilise the four stock

exchanges of the Chinese Mainland, Hong Kong SAR and Taiwan and how will

they evolve?

Creating value in the coming decade

About Deloitte China Research and Insight Centre

The Deloitte China Research and Insight Centre (“CRIC”) was established by Deloitte China in 2008 to provide our clients in China and around the world with information on

developments in China which may be relevant to their businesses.

The CRIC publications range from in-depth reports examining critical issues and trends to executive briefings which update on new developments and their impact. CRIC also

contributes to the development of Deloitte global research publications in collaboration with research centres around the Deloitte global organisation.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member

firms in more than 140 countries, Deloitte brings world-class capabilities and deep local expertise to help clients succeed wherever they operate. Deloitte’s more than 168,000

professionals are committed to becoming the standard of excellence.

Deloitte’s professionals are unified by a collaborative culture that fosters integrity, outstanding value to markets and clients, commitment to each other, and strength from

cultural diversity. They enjoy an environment of continuous learning, challenging experiences, and enriching career opportunities. Deloitte’s professionals are dedicated to

strengthening corporate responsibility, building public trust, and making a positive impact in their communities.

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of member firms, each of which is a legally separate and independent entity.

Please see www.deloitte.com/cn/en/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu and its member firms.

Deloitte’s China practice provides services through a number of legal entities and those entities are members of Deloitte Touche Tohmatsu (Swiss Verein).

We are one of the leading professional services providers in the Chinese Mainland, Hong Kong SAR and Macau SAR. We have over 8,000 people in thirteen offices including

Beijing, Chongqing, Dalian, Guangzhou, Hangzhou, Hong Kong, Macau, Nanjing, Shanghai, Shenzhen, Suzhou, Tianjin and Xiamen.

As early as 1917, we opened an office in Shanghai. Backed by our global network, we deliver a full range of audit, tax, consulting and financial advisory services to national,

multinational and growth enterprise clients in China.

We have considerable experience in China and have been a significant contributor to the development of China’s accounting standards, taxation system and local professional

accountants. We also provide services to around one-third of all companies listed on the Stock Exchange of Hong Kong.

These materials and the information contained herein are provided by Deloitte Touche Tohmatsu and are intended to provide general information on a particular subject or

subjects and are not an exhaustive treatment of such subject(s).

Accordingly, the information in these materials is not intended to constitute accounting, tax, legal, investment, consulting, or other professional advice or services. The

information is not intended to be relied upon as the sole basis for any decision which may affect you or your business. Before making any decision or taking any action that

might affect your personal finances or business, you should consult a qualified professional adviser.

These materials and the information contained therein are provided as is, and Deloitte Touche Tohmatsu makes no express or implied representations or warranties regarding

these materials or the information contained therein. Without limiting the foregoing, Deloitte Touche Tohmatsu does not warrant that the materials or information contained

therein will be error-free or will meet any particular criteria of performance or quality. Deloitte Touche Tohmatsu expressly disclaims all implied warranties, including, without

limitation, warranties of merchantability, title, fitness for a particular purpose, noninfringement, compatibility, security, and accuracy.

Your use of these materials and information contained therein is at your own risk, and you assume full responsibility and risk of loss resulting from the use thereof. Deloitte

Touche Tohmatsu will not be liable for any special, indirect, incidental, consequential, or punitive damages or any other damages whatsoever, whether in an action of contract,

statute, tort (including, without limitation, negligence), or otherwise, relating to the use of these materials or the information contained therein.

If any of the foregoing is not fully enforceable for any reason, the remainder shall nonetheless continue to apply.

©2010 Deloitte Touche Tohmatsu. All rights reserved. Member of Deloitte Touche Tohmatsu