Creating Financial Awareness of Clients...

2

Creating Financial Awareness of Clients: Communication Methodologies that Work Diksha Singh and John Arun, IFMR LEAD In recent years, financial capability has emerged as a key strategic objective to complement the financial inclusion and consumer protection agendas of policymakers and practitioners around the world: • Governments in 45 countries of different income-levels, including India, have stepped up the efforts to design and implement National Strategies for Financial Education 1 and financial service providers are increasingly looking to integrate financial awareness and advisory services for clients into their existing service lines • Traditional models such as classroom-based training are not always cost-effective scale (Schoar et al), and impose implicit transaction and opportunity costs on clients. Moreover, there is little rigorous evidence on their impact in improving financial awareness and promoting behavioral change Innovative Experiments from the Field Product/Model Advantages Challenges 1. Heuristics-based financial training for microentrepreneurs • Micro and small entrepreneurs often lack the necessary financial capabilities to make complex business and financial decisions. • A heuristics-based approach focuses on delivering simple rules-of-thumb pointers to clients instead of in-depth information about financial concepts. • Combined with the rapid diffusion of mobile phone services across India, rules-of-thumb based training offers an emerging opportunity for financial service providers to build financial capability at scale. Leverages Interactive Voice Response technology to deliver training modules to client’s mobile phones, and SMS reminders to nudge them to make sound financial decisions. Both these technologies can be cost- effective at scale It simplifies content into easy- to-understand and remember thumb rules, thereby lowering the cognitive load on clients Onboarding clients to the new technology platform Evidence from a randomized evaluation of this approach in parts of Karnataka and Madhya Pradesh suggests that keeping clients engaged over voice messages and ensuring follow-up on training modules after they sign up for the training can be challenging 2. Integrating mobile financial education and mobile financial services • Launched with the aim to increase the capability of microcredit borrowers, mostly women, to adopt mobile phones as a channel for financial services such as loan repayments • Grameen Foundation India tied up with a mobile money services provider and a microfinance institution Sonata to deliver mobile banking services and education to Sonata’s female borrowers in Uttar Pradesh. As of May 2016, 23,222 of Sonata’s clients have Using a human-centered design approach, the service providers mapped the roles, capabilities and influence of each member in the client’s ecosystem and used the learnings to design financial education models and training materials. Approach focuses on addressing pain points for Since it is an agent-assisted model of delivery, it relies on the understanding and acceptance of technology by front-line agents; Ensuring scalability while maintaining standardization of content 1 http://www.oecd.org/finance/financial-education/G20_OECD_NSFinEd_Summary.pdf 33% of adults globally are financially literate (S&P Global Finlit Survey, 2014) Only 24% of adults in India are financially literate (S&P Global Finlit Survey, 2014) Women in India exhibit lower levels of financial literacy as compared to men. (Financial Literacy and Inclusion in India, NCFE)

Transcript of Creating Financial Awareness of Clients...

CreatingFinancialAwarenessofClients:CommunicationMethodologiesthatWorkDikshaSinghandJohnArun,IFMRLEAD

Inrecentyears, financialcapabilityhasemergedasakeystrategicobjectivetocomplementthefinancial inclusionandconsumerprotectionagendasofpolicymakersandpractitionersaroundtheworld:

• Governments in 45 countries of different income-levels, including India, have stepped up the efforts todesign and implement National Strategies for Financial Education1 and financial service providers areincreasingly looking to integrate financial awareness and advisory services for clients into their existingservicelines

• Traditionalmodels suchasclassroom-basedtrainingarenotalwayscost-effectivescale (Schoaretal),andimposeimplicittransactionandopportunitycostsonclients.Moreover,there is littlerigorousevidenceontheirimpactinimprovingfinancialawarenessandpromotingbehavioralchange

InnovativeExperimentsfromtheField

Product/Model Advantages Challenges

1. Heuristics-basedfinancialtrainingformicroentrepreneurs

• Micro and small entrepreneurs often lack thenecessary financial capabilities to makecomplexbusinessandfinancialdecisions.

• A heuristics-based approach focuses ondelivering simple rules-of-thumb pointers toclients instead of in-depth information aboutfinancialconcepts.

• Combined with the rapid diffusion of mobilephone services across India, rules-of-thumbbased trainingoffersanemergingopportunityforfinancialserviceproviderstobuildfinancialcapabilityatscale.

Leverages Interactive VoiceResponse technology todeliver training modules toclient’s mobile phones, andSMSreminderstonudgethemto make sound financialdecisions. Both thesetechnologies can be cost-effectiveatscale

Itsimplifiescontent intoeasy-to-understand and rememberthumbrules,therebyloweringthecognitiveloadonclients

Onboarding clients to thenewtechnologyplatform

Evidence from arandomized evaluation ofthis approach in parts ofKarnataka and MadhyaPradesh suggests thatkeeping clients engagedover voice messages andensuring follow-up ontrainingmodulesaftertheysignupforthetrainingcanbechallenging

2. Integratingmobilefinancialeducationandmobilefinancialservices

• Launched with the aim to increase thecapability of microcredit borrowers, mostlywomen, toadoptmobilephonesasa channelforfinancialservicessuchasloanrepayments

• Grameen Foundation India tied up with amobile money services provider and amicrofinance institution Sonata to delivermobile banking services and education toSonata’sfemaleborrowersinUttarPradesh.AsofMay 2016, 23,222 of Sonata’s clients have

Using a human-centereddesign approach, the serviceproviders mapped the roles,capabilities and influence ofeach member in the client’secosystem and used thelearnings to design financialeducationmodelsandtrainingmaterials. Approach focuseson addressing pain points for

Sinceitisanagent-assistedmodel of delivery, it relieson the understanding andacceptance of technologybyfront-lineagents;

Ensuring scalability whilemaintainingstandardizationofcontent

1http://www.oecd.org/finance/financial-education/G20_OECD_NSFinEd_Summary.pdf

33%ofadultsgloballyarefinanciallyliterate(S&PGlobalFinlitSurvey,2014)

Only24%ofadultsinIndiaarefinanciallyliterate(S&PGlobalFinlitSurvey,2014)

WomeninIndiaexhibit lowerlevels of financial literacy ascompared to men. (FinancialLiteracyandInclusioninIndia,NCFE)

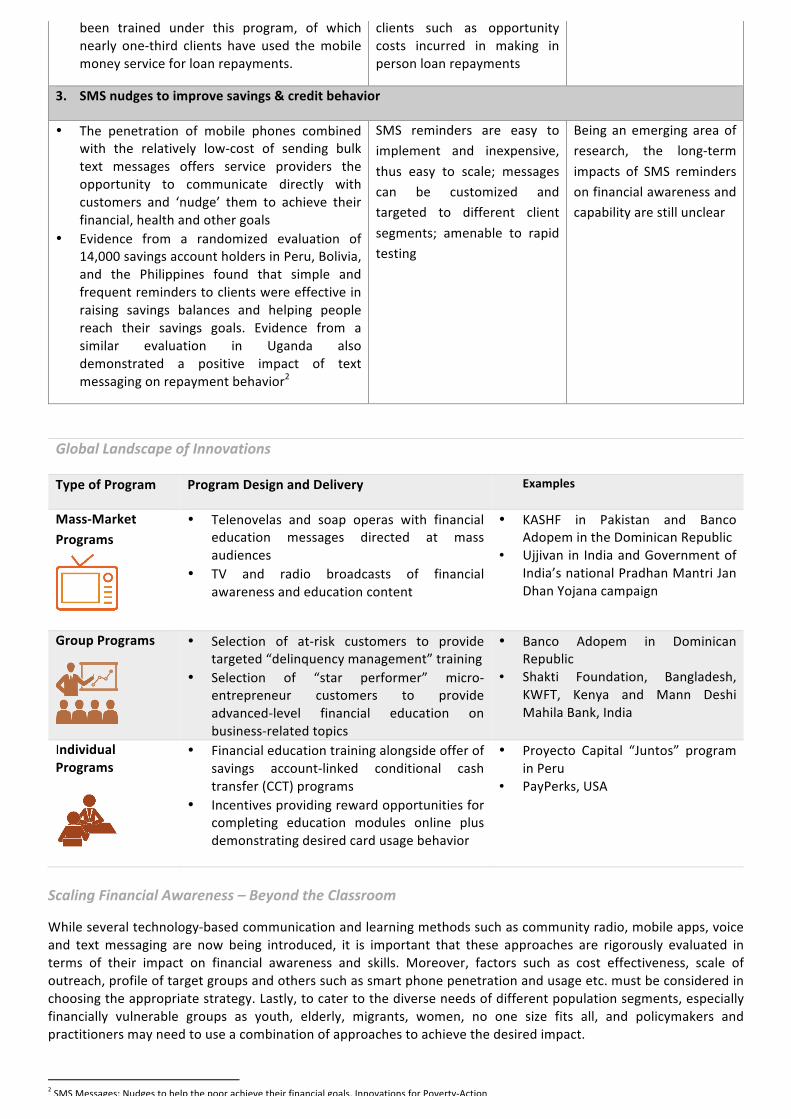

been trained under this program, of whichnearly one-third clients have used themobilemoneyserviceforloanrepayments.

clients such as opportunitycosts incurred in making inpersonloanrepayments

3. SMSnudgestoimprovesavings&creditbehavior

• The penetration of mobile phones combinedwith the relatively low-cost of sending bulktext messages offers service providers theopportunity to communicate directly withcustomers and ‘nudge’ them to achieve theirfinancial,healthandothergoals

• Evidence from a randomized evaluation of14,000savingsaccountholdersinPeru,Bolivia,and the Philippines found that simple andfrequentreminderstoclientswereeffectiveinraising savings balances and helping peoplereach their savings goals. Evidence from asimilar evaluation in Uganda alsodemonstrated a positive impact of textmessagingonrepaymentbehavior2

SMS reminders are easy toimplement and inexpensive,thus easy to scale; messagescan be customized andtargeted to different clientsegments; amenable to rapidtesting

Being anemerging areaofresearch, the long-termimpacts of SMS remindersonfinancialawarenessandcapabilityarestillunclear

GlobalLandscapeofInnovations

TypeofProgram ProgramDesignandDelivery Examples

Mass-MarketPrograms

• Telenovelas and soap operas with financialeducation messages directed at massaudiences

• TV and radio broadcasts of financialawarenessandeducationcontent

• KASHF in Pakistan and BancoAdopemintheDominicanRepublic

• Ujjivan in IndiaandGovernmentofIndia’snationalPradhanMantriJanDhanYojanacampaign

GroupPrograms

• Selection of at-risk customers to providetargeted“delinquencymanagement”training

• Selection of “star performer” micro-entrepreneur customers to provideadvanced-level financial education onbusiness-relatedtopics

• Banco Adopem in DominicanRepublic

• Shakti Foundation, Bangladesh,KWFT, Kenya and Mann DeshiMahilaBank,India

IndividualPrograms

• Financialeducationtrainingalongsideofferofsavings account-linked conditional cashtransfer(CCT)programs

• Incentivesprovidingrewardopportunitiesforcompleting education modules online plusdemonstratingdesiredcardusagebehavior

• Proyecto Capital “Juntos” programinPeru

• PayPerks,USA

ScalingFinancialAwareness–BeyondtheClassroom

Whileseveraltechnology-basedcommunicationandlearningmethodssuchascommunityradio,mobileapps,voiceand textmessaging are now being introduced, it is important that these approaches are rigorously evaluated interms of their impact on financial awareness and skills. Moreover, factors such as cost effectiveness, scale ofoutreach,profileoftargetgroupsandotherssuchassmartphonepenetrationandusageetc.mustbeconsideredinchoosingtheappropriatestrategy.Lastly,tocatertothediverseneedsofdifferentpopulationsegments,especiallyfinancially vulnerable groups as youth, elderly, migrants, women, no one size fits all, and policymakers andpractitionersmayneedtouseacombinationofapproachestoachievethedesiredimpact.

2SMSMessages:Nudgestohelpthepoorachievetheirfinancialgoals,InnovationsforPoverty-Action