CPAR COACHING - hfmacpar.orghfmacpar.org/CPARGuides/37_51_106.pdf · CPAR COACHING Chapter 1...

198

CPAR COACHING Chapter 1 Revenue Cycle Overview 1

Transcript of CPAR COACHING - hfmacpar.orghfmacpar.org/CPARGuides/37_51_106.pdf · CPAR COACHING Chapter 1...

CPAR COACHING

Chapter 1

Revenue Cycle Overview

1

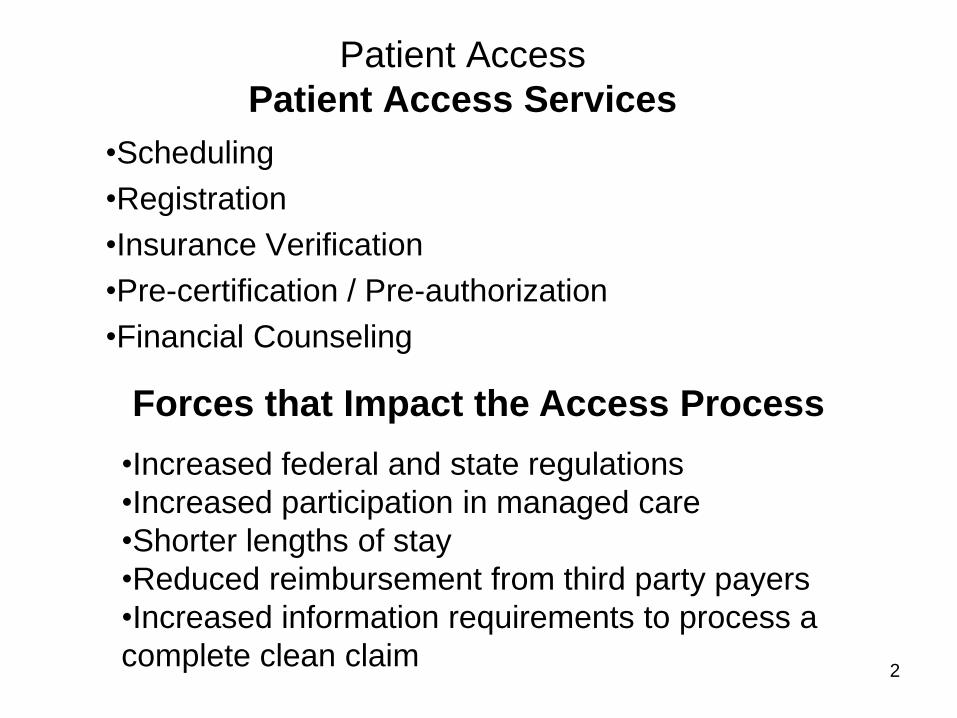

Patient Access

Patient Access Services

•Scheduling

•Registration

•Insurance Verification

•Pre-certification / Pre-authorization

•Financial Counseling

2

Forces that Impact the Access Process

•Increased federal and state regulations

•Increased participation in managed care

•Shorter lengths of stay

•Reduced reimbursement from third party payers

•Increased information requirements to process a

complete clean claim

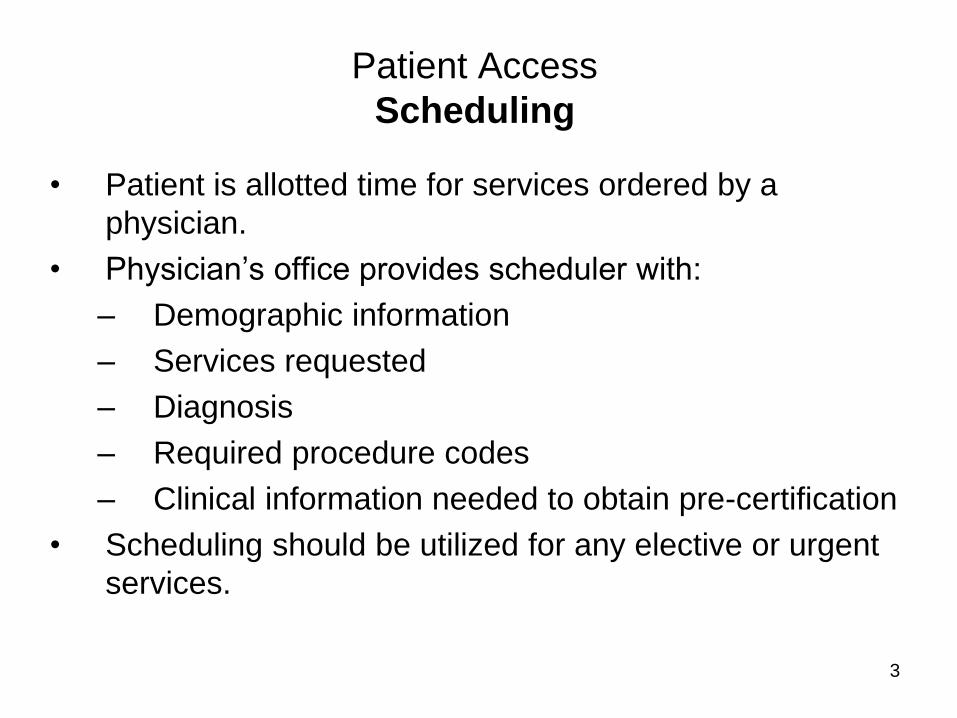

Patient Access

Scheduling

• Patient is allotted time for services ordered by a

physician.

• Physician‟s office provides scheduler with:

– Demographic information

– Services requested

– Diagnosis

– Required procedure codes

– Clinical information needed to obtain pre-certification

• Scheduling should be utilized for any elective or urgent

services.

3

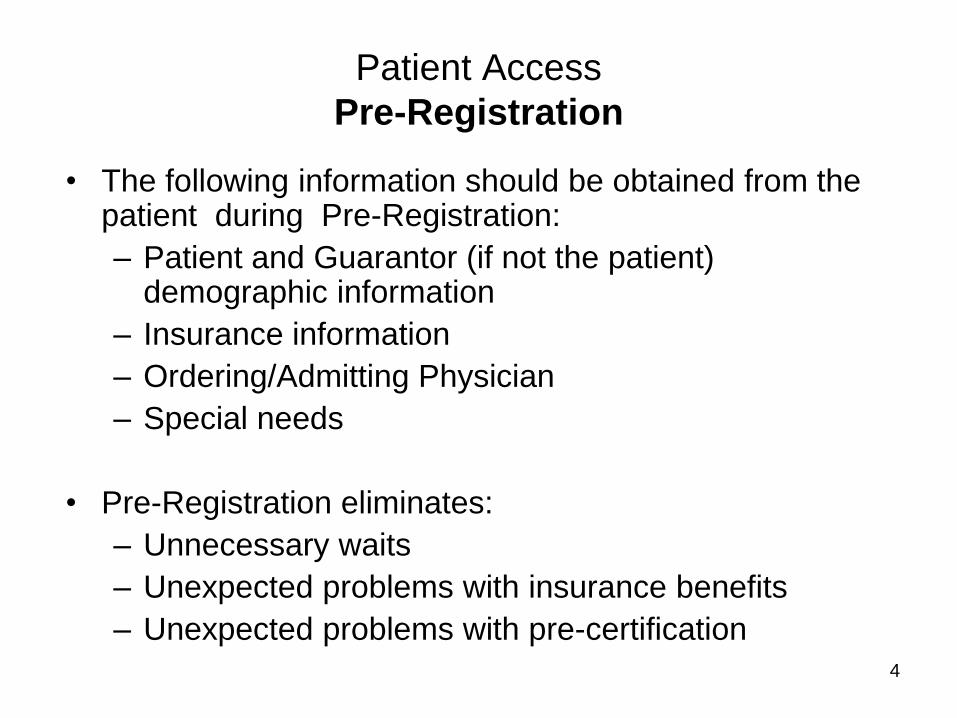

Patient Access

Pre-Registration

• The following information should be obtained from the patient during Pre-Registration:

– Patient and Guarantor (if not the patient) demographic information

– Insurance information

– Ordering/Admitting Physician

– Special needs

• Pre-Registration eliminates:

– Unnecessary waits

– Unexpected problems with insurance benefits

– Unexpected problems with pre-certification4

Patient Access

Pre-Access and Other Essential Functions

Capture all data necessary to access patient‟s ability to pay

including:

– Contacting patient‟s insurance company

• Verify benefits

• Determine pre-certification requirements

– Notify patient of services that do not meet medical

necessity

– Alert the patient of any deposits due

– Provide any pre-operative or preparatory information

5

Patient Access

Registration

• Obtain positive I.D.

• Verify existing data for accuracy

• Complete appropriate Patient Access documents:

– Advanced Directives

– HIPAA Notice of Privacy Practices and

– MSP Questionnaire

• Obtain signatures

• Collect co-pays and any other self-pay amounts

• Offer payment options

• Provide Financial Counseling with difficulty or inability to pay self-pay amounts

6

Patient Access

Insurance Verification

• Provide accurate patient/guarantor data to payer when

verifying coverage for services

• Obtain benefit levels from payer

• Provide any required advance notifications

• Obtain in-network / out-of-network status

• Pre-certification / Pre-Authorization requirements

• Involve Financial Counselors to assist in identifying

potential resolutions to ensure reimbursement

• Emergency Medical Treatment and Active Labor Act

(EMTALA) - Patients transferred from the ER to a higher

level of care cannot undergo financial screening prior to

being stabilized.

7

Patient Access

Pre-certification

Pre-certification is a managed care technique to control costs and determine medical necessity.

- Requires notifying pre-cert agency

– Meets medical necessity requirements based on

CPT or DRG information

– Notify prior to elective procedures and admissions

– Notify within 24 – 48 hours of emergency procedure/admission

– The two most common sets of criteria used in the industry are Milliman & Robertson and Interqual

– The reviewing agency issues certification/ authorization number linking the service, claim and authorization to facilitate timely reimbursement.

– Note: “Fee-for-service” Medicare does not require pre-cert or authorization – but HMO‟s usually will.

8

Patient Access

Financial Counseling

• Financial Counselors are facility gatekeepers ensuring bill for services rendered will be covered by third-party payers or by the patient!

• A strong financial counseling program includes:

– Identifying sources of potential reimbursement

– Providing clearly written policies and procedures for indigent or payment eligibility criteria

– Communicating information to the patient in a comprehensibly and culturally appropriate method

– Developing partnerships with community health and human services agencies providing a reliable referral program

– Ensuring financial counseling staff is provided ongoing educational opportunities in hospital billing, financial assistance and collection policies and procedures

9

Patient Financial Services

Revenue Cycle Overview

•The PFS Department usually includes the following areas:

Billing – COB‟s, contractual and “write-off” adjustments

Appeal of denied claims

Bad Debt, Charity Care determination

Corporate Compliance

Legal aspects of collections

Self-pay collections

• The following forces impact PFS changes:

Increasing pressure on hospital collection practices resulting in restructuring charging, collections and charity policies.

New Privacy Practice regulations by HIPAA creating new policies and procedures requiring extensive training

Changes in Medicaid and Medicare policies requiring additional training to ensure maximum reimbursements

10

Patient Financial Services

Appeals

• The methodology used by the provider to ask for

reconsideration of payment of denied claims.

• Each payer, both commercial and government, have

their own requirements for filing an appeal.

• Utilize all appeal levels offered by the payer

• Support the appeal with documentation to include:

– EOB

– Medical Records

– Correspondence from payer

– Screen prints of any pertinent notations on the account to

strengthen your defense

– Specific required documentation from payer (i.e. reconsideration

forms)

11

Patient Financial Services

Denials

• Denials = claims not paid by third-party payers.

• Types of Denials:

– Technical Denial = alleged coding or informational errors

on claims.

• Examples: not out of network coverage, wrong bill type,

claim untimely, wrong birthdate, etc.

– Clinical Denial = medical criteria is not met within industry

standards.

• Examples: no authorization, pre-existing condition,

experimental procedures, etc.

12

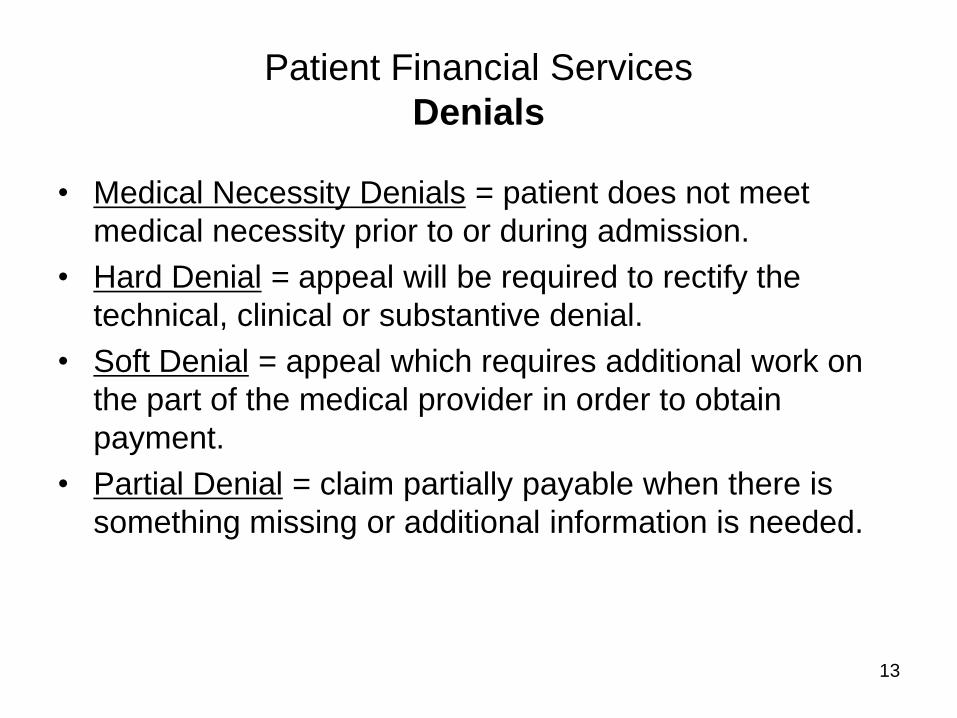

Patient Financial Services

Denials

• Medical Necessity Denials = patient does not meet

medical necessity prior to or during admission.

• Hard Denial = appeal will be required to rectify the

technical, clinical or substantive denial.

• Soft Denial = appeal which requires additional work on

the part of the medical provider in order to obtain

payment.

• Partial Denial = claim partially payable when there is

something missing or additional information is needed.

13

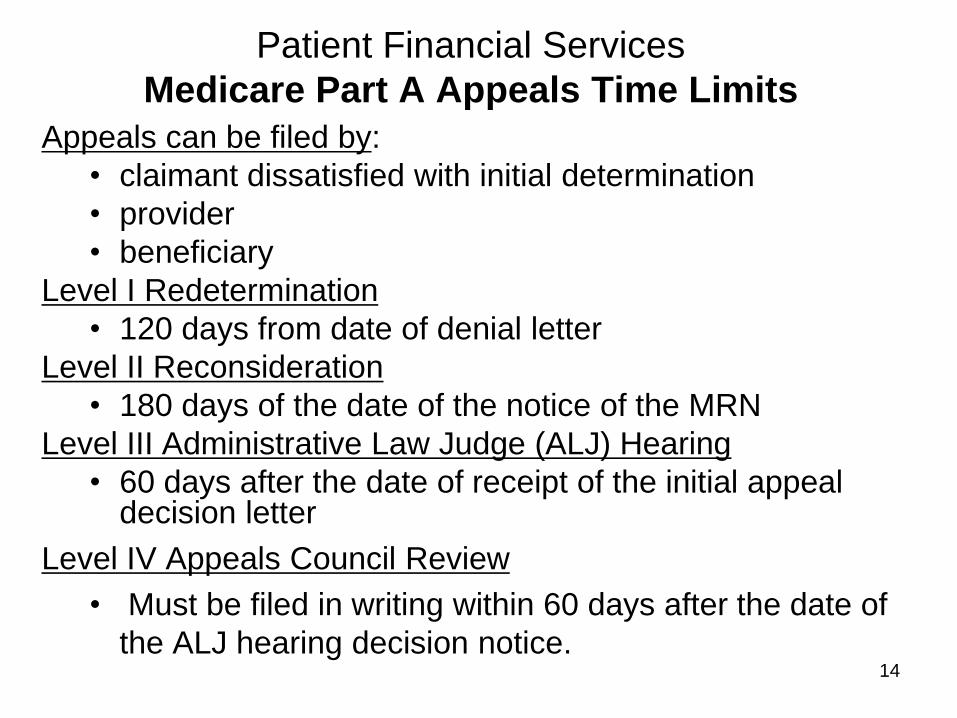

Patient Financial Services

Medicare Part A Appeals Time Limits

Appeals can be filed by:

• claimant dissatisfied with initial determination

• provider

• beneficiary

Level I Redetermination

• 120 days from date of denial letter

Level II Reconsideration

• 180 days of the date of the notice of the MRN

Level III Administrative Law Judge (ALJ) Hearing

• 60 days after the date of receipt of the initial appeal decision letter

Level IV Appeals Council Review

• Must be filed in writing within 60 days after the date of

the ALJ hearing decision notice. 14

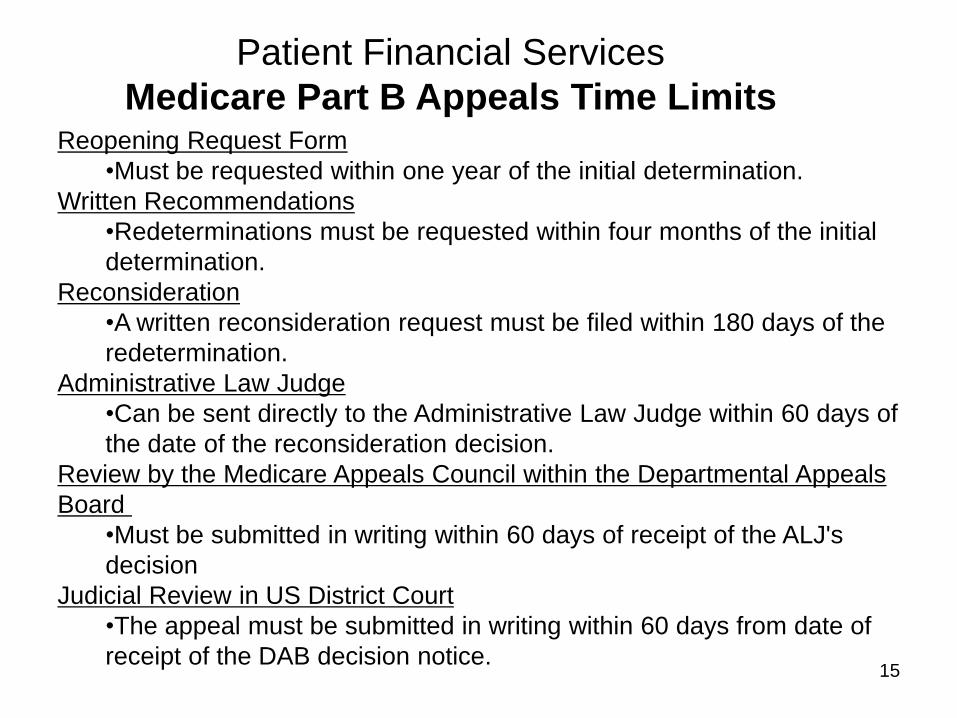

15

Reopening Request Form

•Must be requested within one year of the initial determination.

Written Recommendations

•Redeterminations must be requested within four months of the initial

determination.

Reconsideration

•A written reconsideration request must be filed within 180 days of the

redetermination.

Administrative Law Judge

•Can be sent directly to the Administrative Law Judge within 60 days of

the date of the reconsideration decision.

Review by the Medicare Appeals Council within the Departmental Appeals

Board

•Must be submitted in writing within 60 days of receipt of the ALJ's

decision

Judicial Review in US District Court

•The appeal must be submitted in writing within 60 days from date of

receipt of the DAB decision notice.

Patient Financial Services

Medicare Part B Appeals Time Limits

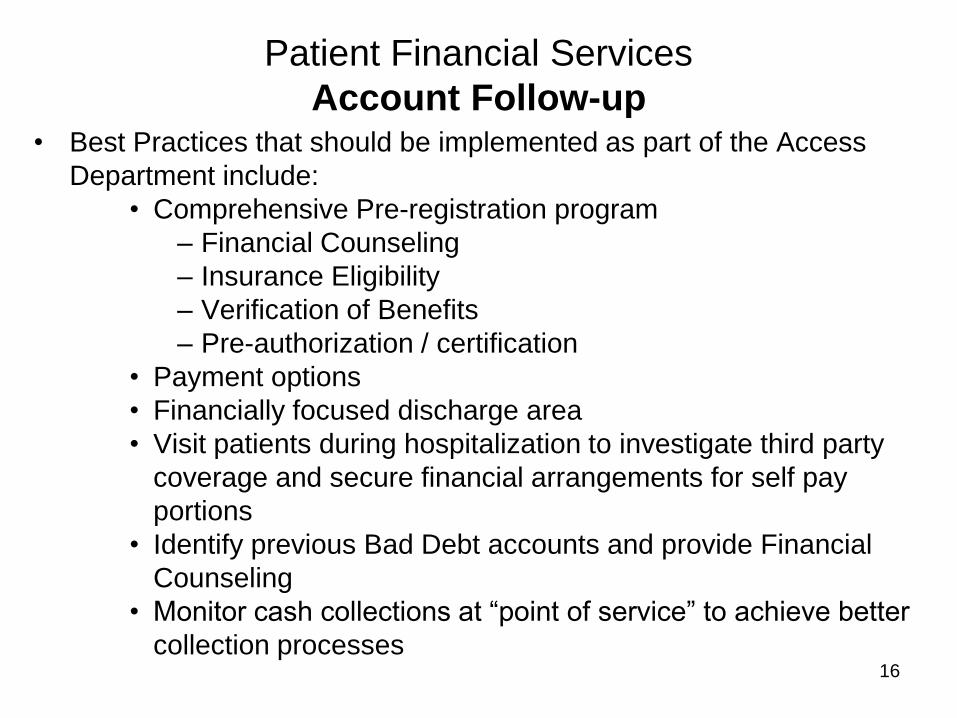

Patient Financial Services

Account Follow-up• Best Practices that should be implemented as part of the Access

Department include:

• Comprehensive Pre-registration program

– Financial Counseling

– Insurance Eligibility

– Verification of Benefits

– Pre-authorization / certification

• Payment options

• Financially focused discharge area

• Visit patients during hospitalization to investigate third party

coverage and secure financial arrangements for self pay

portions

• Identify previous Bad Debt accounts and provide Financial

Counseling

• Monitor cash collections at “point of service” to achieve better

collection processes16

Patient Financial Services

Account Follow-up

• Business Office Best Practices include:

– Separate self-pay balances based on dollar amounts

– Use telephone calls for Inpatient and high dollar Outpatient accounts

– Use written notices for small dollar Outpatient accounts

– Use credit reports for self-pay accounts

– Outsource Medicaid application processes

– Insurance vs. self-pay/patient portions

– Document all follow-up actions using standardized language / abbreviations

17

Patient Financial Services

Resolving Outstanding Claims Issues

• Claim not on file

– Review documentation

– Verify claim submission address

• Cannot identify patient/subscriber

– confirm name, DOB, SSN, employer

• Terminated coverage

– verify if individual or group terminated

– if group, who took over the group

• Medical records requested

– Determine why, what specific records are needed

– HIPAA requires disclosure of “minimum necessary”

18

Patient Financial Services

Collecting Insurance Dollars

• Know contractual obligations

• Know patient benefits

• Be prepared and organized

• Use imaging for document retrieval

• Work A/R by payer type

• Work bigger dollar accounts first

• Get the patient involved

• Be persistent

• Request to speak to a higher authority

• If insurance company never received the claim, then fax claim and a follow up call to be sure the fax was received

• Be creative

19

Patient Financial Services

Refunds and Credit Balances

• An overpayment or refund should not be considered until the appropriate

source is researched and identified

• Sources of overpayments or credits include:

– Patient payment

– Error in posting payments

– Incorrect or absent contractual

– Late credit posted after payment received

– Charge posted after submission time limit

• When two carriers pay as primary, determine who is the required

primary payer:

– Review EOB‟s

– Call the payers

– Verify with the employer

– Call the patient/guarantor20

Patient Financial Services

Transferring Patient Payments

• Transfer patient overpayment to another account:

– Outstanding patient balance due

– Outstanding insurance balance due

– Outstanding bad debt balance due

• Only if after these three categories have been

exhausted, will the overpayment be refunded to the

patient.

• Patient overpayments do not always go to the patient;

verify in the account information screens exactly who the

Guarantor is. If other than the patient, the refund goes to

the Guarantor.

21

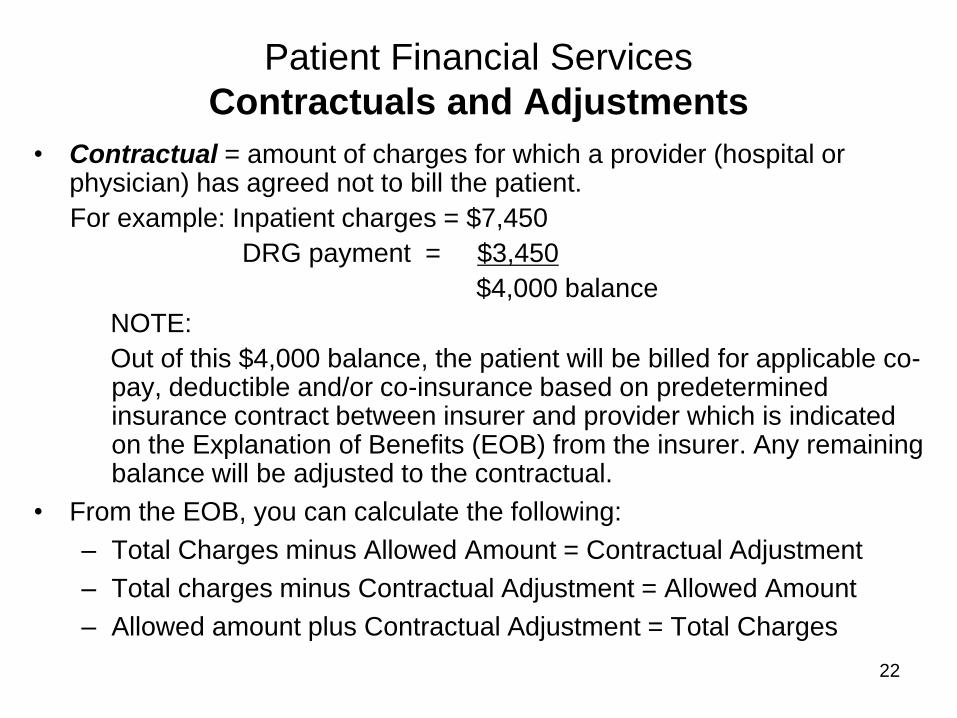

Patient Financial Services

Contractuals and Adjustments

• Contractual = amount of charges for which a provider (hospital or physician) has agreed not to bill the patient.

For example: Inpatient charges = $7,450

DRG payment = $3,450

$4,000 balance

NOTE:

Out of this $4,000 balance, the patient will be billed for applicable co-pay, deductible and/or co-insurance based on predetermined insurance contract between insurer and provider which is indicated on the Explanation of Benefits (EOB) from the insurer. Any remaining balance will be adjusted to the contractual.

• From the EOB, you can calculate the following:

– Total Charges minus Allowed Amount = Contractual Adjustment

– Total charges minus Contractual Adjustment = Allowed Amount

– Allowed amount plus Contractual Adjustment = Total Charges

22

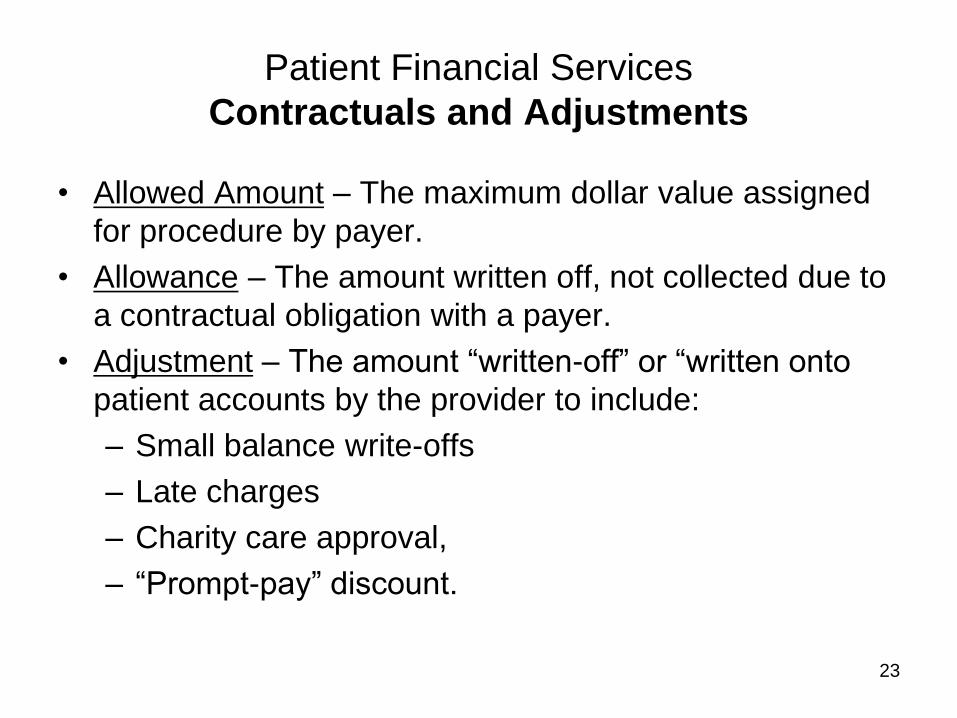

Patient Financial Services

Contractuals and Adjustments

• Allowed Amount – The maximum dollar value assigned

for procedure by payer.

• Allowance – The amount written off, not collected due to

a contractual obligation with a payer.

• Adjustment – The amount “written-off” or “written onto

patient accounts by the provider to include:

– Small balance write-offs

– Late charges

– Charity care approval,

– “Prompt-pay” discount.

23

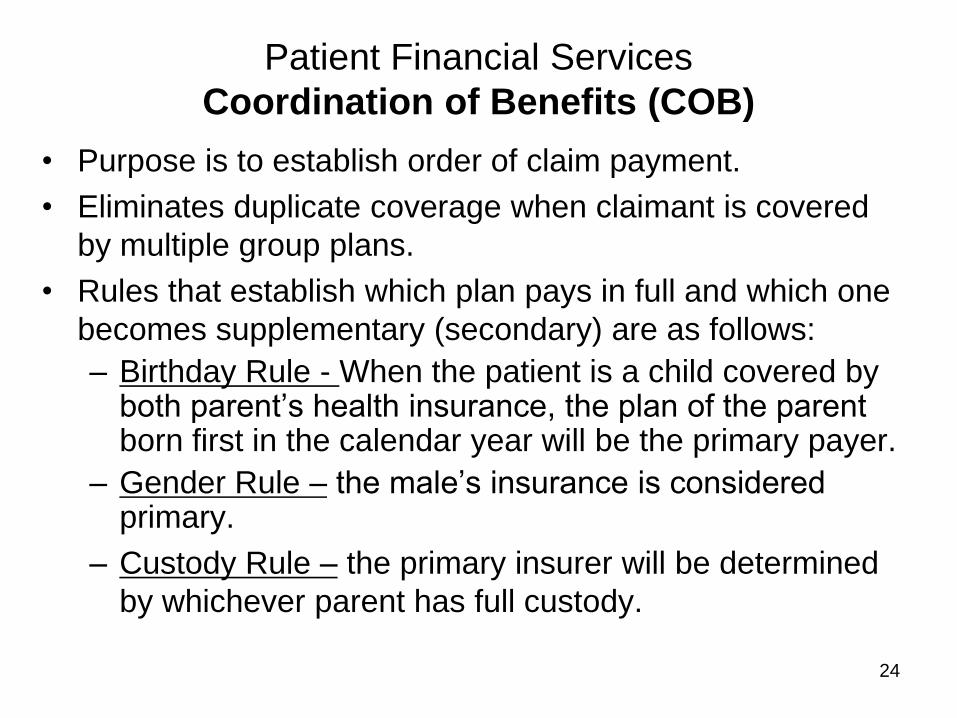

Patient Financial Services

Coordination of Benefits (COB)

• Purpose is to establish order of claim payment.

• Eliminates duplicate coverage when claimant is covered

by multiple group plans.

• Rules that establish which plan pays in full and which one

becomes supplementary (secondary) are as follows:

– Birthday Rule - When the patient is a child covered by both parent‟s health insurance, the plan of the parent born first in the calendar year will be the primary payer.

– Gender Rule – the male‟s insurance is considered primary.

– Custody Rule – the primary insurer will be determined

by whichever parent has full custody.

24

Patient Financial Services

Deductibles, Co-Insurance and Co-Payments

• Deductible - Required payment by the insured under a

health plan contract. A deductible can be required per

calendar year, per-visit, per family or per inpatient stay.

• Co-insurance - Cost sharing requirement under health

insurance policy where the insured will assume a portion or

percentage of the costs of covered services.

• Co-Payment - A set fee that a managed care patient has to

pay the provider each time care is provided in the network.

25

Patient Financial Services

Reimbursement MethodsReimbursement =Total integration of revenue cycle process to

include customer service, clinical staff , medical records, coding, admissions and scheduling , billing and collections.

• Ambulatory Payment Classifications (APC)

– Outpatient reimbursement where all services associated with a given procedure are bundled into the APC

• Capitation

– Specified amount paid periodically to provider for group of specified health services, regardless of quantity rendered

• Diagnosis Related Groups (DRGs)

– Inpatient – Utilized to pay hospital or other provider for services and categorize illness by diagnosis and treatment

• Discounted Fee-For-Service

– Provider agrees to supply services on a fee-for-service basis

• Fee-For-Service

– Where specific payment is made for specific services rendered 26

Patient Financial Services

Reimbursement Methods

• Flat Fee-Per-Case

– Paid flat fee for treatment based on diagnosis and/or presenting problem

• Per Diem Rate

– Provider is paid daily rate for specific services or outcomes, regardless of cost to provide care

• PCP Capitation

– Providers of primary care services who receive a prepayment every month

• Prospective Payment System (PPS)

– Establishes rates, prices or budgets before services are rendered and costs are incurred.

– Provider retains or absorbs a portion of difference between revenues and actual costs.

27

Patient Financial Services

Reimbursement Methods

• Periodic Interim Payments and Cash Advances

(PIP‟s)

– Payments received where the plan advances to

the hospital cash to cover expected claims

• Penalties and Withholds

– May be negotiated so that if goals are met, the

healthcare provider receives its„ withholds or

bonus. These goals are usually tied to utilization.

28

Patient Financial Services

Self-Pay Collections

• The Five Health Care Collection Control Points

– Before Admissions / Registration and before service is

provided, except when EMTALA laws apply

– At Admission / Registration

– In-house

– At discharge

– 30 days after discharge

• The best time to collect from the patient is prior to his or her

receiving the service except where EMTALA laws apply

(Emergency Medical Treatment and Labor Act). The worst time is

some time after medical service was provided.

• Calculate patient portions of an estimated hospital bill prior to the

time of service by verifying coverage limits and co-pay

requirements and applying those amounts to average charges for

service.29

Patient Financial Services

Self-Pay Collections

• Remember disclaimer statement, “this is only an estimate”

• When presenting the estimate, Patient Access staff should offer the following details:

– Reveal the range from which estimates are derived

– Clarify charges could be more or less

– Charges are based on actual services provided

– Provide a written copy of estimate including disclaimer statement

– Discuss payment options and means of payment

30

Patient Financial Services

Bad Debt, Charity and Courtesy Allowances

• Bad Debts are “total” account balances or “self-pay”

account balances considered uncollectible after attempts to

collect from payer(s), patient or guarantor.

• Allowable Bad Debts are bad debts of the provider

resulting from uncollectible deductibles and coinsurance

amounts related to specific deductibles and coinsurance

amounts.

• Charity Allowances – reductions in charges made by the

provider for services because of indigence (low income) of

the patient.

• Courtesy Allowances – reductions in charges by provider in

the form of an allowance to patients (prompt-pay),

physicians, clergy, others.31

Patient Financial Services

Billing – Discharged Not Final Billed (DNFB)

• It‟s important for the hospital to know how many

DNFB accounts are pending on the Accounts

Receivable (A/R)?

• These are unbilled accounts.

• Unbilled means no cash is coming in.

• Review reports that determine how much of the A/R

has still not been billed to the payers.

• Not yet billed accounts in the billing system should

be monitored.

32

Patient Financial Services

Patient Friendly Billing

• Clear and understandable billing statements benefit both

patients and healthcare providers.

• Providers are responsible for establishing clarity.

• Too much detail can be confusing.

• Flexible statement designs are critical.

• Bills & statements should be delivered promptly and

efficiently.

• The UB04 is the instrument used to bill healthcare services

with the exception of physician and professional fees.

• The UB04 Contains 81 data elements known as form

locators relating to the patient, provider and services

rendered. 33

Legal

Legal Aspects of “Collections”

• Four types of Consent for Treatment

– Actual or expressed – written or oral

– Implied “in fact” – consent by silence

– Implied “by law” – emergency treatment when patient

is unconscious

– Informed – Patient understands what he/she is being

treated for and what procedures he/she is having

performed.

34

Legal Aspects to Collecting

Garnishments

• Most commonly used remedy used for satisfying a

financial judgment.

• Employer or bank of debtor collects money.

• 25% of wages or salary can be garnished

• 100% of available funds in bank accounts can be

garnished.

• All money seized is sent to the county clerk and paid to

the creditor‟s attorney.

35

Legal Aspects to Collecting - Estates

• When a patient is deceased, proper procedures must be followed to

collect payment.

– Know the county where the patient last resided

– Ensure that estate has been opened by checking newspapers for

public notices

– Statement of claim must be filed with the court once an estate is

opened.

• Order of preference in payment of creditors in an estate:

1. Year„s support for family

2. Funeral expenses

3. Other necessary expenses of administration, administrative

fees of Estate

4. Reasonable expenses of last illness

5. Taxes, unpaid or other debts

6. Judgments, secured interest, and other liens

7. All other claims 36

Legal

Types of Bankruptcy

• Chapter 7 – Complete discharge of all debts

• Chapter 11 – Business reorganization

• Chapter 12 – Bankruptcies for farmers

• Chapter 13 – Reorganize debt and restructure payment

plan with bankruptcy court

37

Legal - Bankruptcy

• Person is judged to be in debt and unable to meet

their financial obligations

• Property is administered and divided among creditors

• The debtor may file to not have to deal with or be

obligated to pay creditors.

• Actions to take when dealing with a Bankrupt Debtor:

– Pull account and flag for bankruptcy

– Stop all routine collection efforts

– If partial payment is received, inquire as to

patient‟s intentions

– Document conversations with patient

– If patient is represented by an attorney, do not

contact patient. 38

Legal - Hospital Liens

• A lien applies when a person has been injured by

another party, at no fault of their own, (auto accident,

negligent condition on a property, gunshot wound, slip

and fall in a store, etc.) presents to a medical facility for

treatment of those injuries (see below for specifics

regarding which providers may file medical liens).

• Medical (Hospital) Liens are not:

– Liens against the injured party

– Liens against the patients legal representative

– Liens against property

– Liens against other assets

– Evidence of the person„s failure to pay a debt

39

Legal - “Securing” the Lien

• At least 15 days prior to the actual filing of this lien, a letter of

intent to file a lien must be sent to the patient and all known

possible responsible parties.

• This letter must contain language stating that the lien is not

against the patient, his property or assets and is not evidence of

failure to pay a debt.

• This letter of intent must be sent both certified and regular mail

and sender must retain receipt.

• The actual lien document is to be filed in the required counties

within 75 days of discharge.

• File a lien with the Clerk of the Superior Court in the county where

the patient resides as well as the county where the hospital is

located.

• Send a copy of the lien to the patient and to any other liable party.

• Once a settlement occurs and payment is received, satisfy

the lien. 40

Legal - “Perfecting” the Lien

• A Medical (Hospital) Lien must contain the following:

– Name and address of patient as it appears on the

hospital record

– Name and address of hospital

– Name and address of the operator of the hospital

– Dates of admission and discharge of patient

– Amount of the hospital bill

– Names and addresses of all known persons or

corporations allegedly liable for the injuries to the

patient

– The lien must be notarized and signed by the person

preparing the lien.

41

Compliance - HIPAA• Health Insurance Portability and Accountability Act, (HIPAA)

enacted in 1996

– HIPAA applies to all organizations that maintain and transmit protected health information (PHI).

– Two categories:

• Administrative Simplification (relevant to providers)

• Insurance Reform (relevant to payers)

• Protected health information (PHI):

– The physical or mental health or condition of a patient

– How health care is delivered

– Regarding payment for the healthcare of an individual

• Civil offenses enforced by OCR:

– $50,000 per person per violation penalty, $1.5 million per year

per incident maximum

• Criminal offenses enforced by DOJ:

– Up to $250,000 in fines

– Up to 10 years in prison.42

Corporate Compliance

• Corporate Compliance is concerned with ensuring that

healthcare providers comply with federal and state

healthcare rules and regulations.

• In 1997 the Office of Inspector General (OIG) of the

Department of Health and Human Services began formulating

and distributing compliance guidelines developed for specific

areas of healthcare.

What you should know . . .

• Name, extension of the Compliance Officer.

• Number of facility‟s compliance telephone “hot-line.”

• How to get a copy of the facility‟s Code of Conduct.

• How to get more information concerning a specific question.

43

Corporate Compliance

Seven Steps to Effective Corporate Compliance

• Written and distributed standards of conduct and policies

and procedures promoting commitment to compliance.

• Designated Chief Compliance Officer.

• Regular and effective training programs.

• Establishment of a reporting system (e.g. hotline).

• Development of system for responding to reported

compliance problems.

• Regular system of auditing and monitoring compliance

issues.

• System to investigate and re-mediate identified

problems.

44

Federal Regulations

Truth in Lending Act

• Also called “Consumer Credit Protection Act” or “Federal

Regulation Z”

• A creditor is someone who regularly extends credit that is

– Subject to finance charge or

– Amount due is payable in more than four payments.

• Consumer Credit is granted with a written agreement to

pay and must be payable to person in the contract.

• Required Disclosures include:

– Date on which finance charge begins to accrue.

– Number, amount and due date of payments.

– Total of payments.

– Method of computer default in the event of late charges.

45

Federal Regulations

Fair Credit Reporting Act

• Applies when using credit reports on consumers

related to their credit worthiness.

• Provides the maximum protection of a consumer‟s

right to privacy and confidentiality of credit reports.

• The Act includes:

– How a credit report is to be used

– What information can be released

– How to interact with consumers on what is on the

credit report

– Applicant has 30 days from denial of credit to

contact the credit reporting agency, in writing, for

information regarding the credit report46

Federal Regulations

Fair Credit Billing Act

• This act applies to all creditors who regularly extend

open-ended credit payable in more than four payments.

• Applies to all creditors who regularly extend open-ended

credit payable in more than four payments.

• If a bill is sent to the patient after service is rendered, an

extension of credit is not implied.

• Patient must notify the hospital of any error within 60

days after a statement is mailed.

• Hospital must respond to the complaint within 30 days of

receiving it.

• Error must be corrected or accuracy of statement must

be explained to the customer within a maximum of 90

days.47

Federal Regulations

Fair Debt Collection Practices Act

• This Act generally does not apply to hospitals.

• This Act provides that legal action against the customer

should not be threatened unless legal action is planned or the

collector normally brings suit on claims for similar accounts.

• Bars unscrupulous conduct of collectors.

• Never call before 8 AM or after 9 PM without the debtor

approval (debtor time)

• Never misrepresent the character, amount or legal status of

any debt

• When an attorney represents the debtor, talk only with the

attorney unless the attorney fails to respond.

• Never threaten suit, garnishment, etc. unless you intend to

take that action.

48

Coordinated Care

Medical Necessity and Outpatients• If the test or procedure is not medically necessary in accordance

with Local Medical Review Policies / Local Coverage

Determination (LCD), or CMS rules / National Coverage

Determination (NCD), then the provider must allow the physician

to update the diagnosis based on documented condition of the

patient, change the test or procedure to one that meets criteria, or

cancel the test or procedure per CMS„s rules. If not medically

necessary, the physician may change diagnosis, change

procedure or cancel procedure.

• If the physician does not change the diagnosis or procedure; and

it is not medically necessary, the patient can proceed with

procedure, however, Medicare requires that a written waiver or

Advanced Beneficiary Notice of Non-Coverage (ABN) must be

issued and explained to the patient that they now will become

financially liable for those charges. 49

Coordinated Care

Medical Necessity Criteria

• Consistent with symptoms, diagnosis of illness or injury under treatment,

– Medicare – CT Brain = Fainting, Blurred Vision

• Necessary, consistent with generally accepted professional medical standards (not experimental), and

• Most appropriate level of care in the most appropriate care setting.

– Inpatient most acute level of care

– Observation

– Outpatient

• The hospital, as a provider, has the responsibility to review each Medicare admission for Medical Necessity, which is based on criteria developed by CMS, the hospital, and by the Peer Review Organization (PRO). The PRO is a medical review organization that contracts with Medicare to review the medical necessity, appropriateness, and quality of the healthcare services or items provided or proposed to be provided to Medicare beneficiaries.

50

Coordinated Care

Utilization Management (UM)

• Determines most appropriate level of care.

• Concurrent review, continued pre-certification or authorization for:

– Initial inpatient services

– Observation – Tests or surgeries

– After discharge – Home Health, DME

• Works with clinical staff providing bedside care, other hospital departments, and community services in discharge planning and transition planning for after care.

51

Health Information Management (HIM)

Medical Records

• HIM is responsible for maintenance and protection of all medical records created in the process of providing healthcare services,

– Dictated ER report

– Interpretation of Chest x-ray

– Progress notes from Physical Therapy

• A medical record of quality and integrity is the strongest element in supporting billing and reimbursement.

– If the medical record is requested by a payer, and the documentation cannot be found or does not support the services billed, the payer can deny or recoup payment.

52

Health Information Management (HIM)

Medical Records

• Quality record = complete record

– Physician, Nurse (drug administration), Therapist,

Psychologist, Diabetes Educator

• Each record must contain information that will:

– Justify the admission,

• Physician order with appropriate diagnosis

• Test results

– Support the diagnosis, treatments, and services

– Describe the expected outcomes and actual outcomes,

– Plan for the patient‟s aftercare.

53

Health Information Management (HIM)

Medical Records - Optimizing DRG Assignment

• Diagnosis Related Group (DRG) – a patient classification

system used for inpatient reimbursement.

• DRG relates demographic, diagnostic and therapeutic

characteristics of patients to Length of stay (LOS) and

amount of resources consumed.

54

Health Information Management (HIM) - Coding

• Coding is the process of converting narrative descriptions of diseases, injuries and operations into numerical classifications called ICD-9CM codes (International Classification of Diseases, 9th Edition, Clinical Modification).

• ICD-9CM codes are numbers that identify diagnosis, complaint and symptoms which are gathered at the time of registration and documented in the medical record.

• Level I codes are the (AMA) American Medical Association„s CPT (Current Procedural Terminology). It is a listing of descriptive terms and identifying codes for reporting medical services and procedures. These codes are updated annually by the AMA.

• Level II codes are often referred to as the HCPCS (Health Care Financing Administration (HCFA) Common Procedural Coding System) codes. Level II codes are primarily used to identify products, supplies and services not included in the CPT codes assigned and are updated and maintained by CMS.

55

Health Information Management (HIM)

Coding - HCPCS Level I – CPT-4 Codes

• Common Procedural Terminology (CPT-4 codes),

– 5 digit numeric codes,

– Codes for medical services and procedures, performed by physicians in a clinical setting.

– 10000-69999 = Surgical / Invasive codes

– 70000-79999 = Radiology codes

– 80000-89000 = Laboratory / Pathology

– 90000-99000 = Physical Medicine

• Outpatient Therapy (PT, OT and Speech)

• Outpatient Visits

• Psychological services

• EMG / Neurology services

56

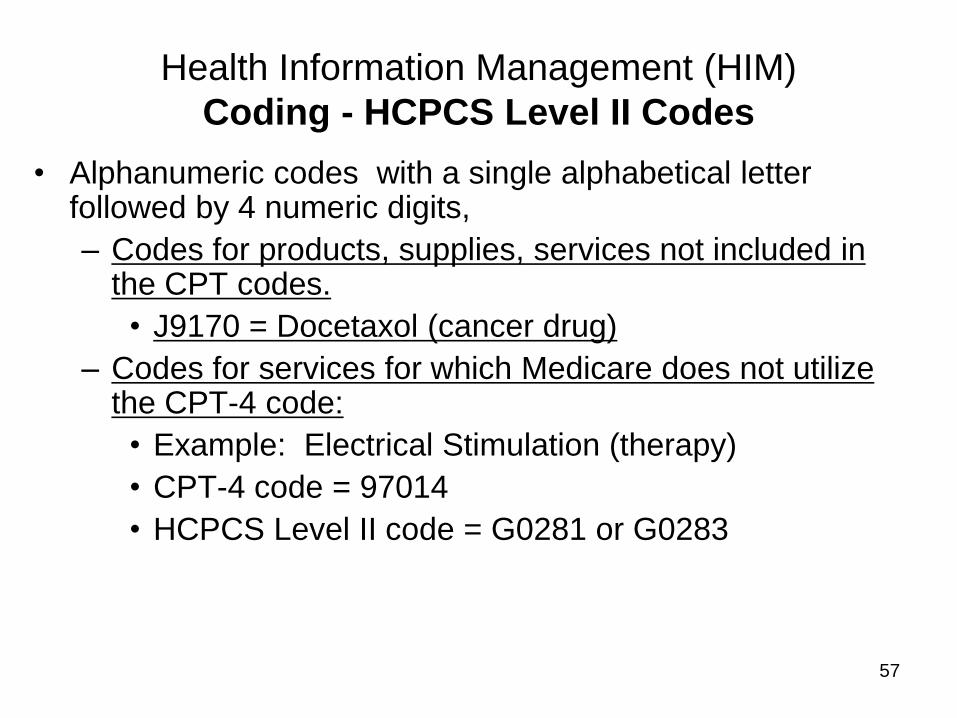

Health Information Management (HIM)

Coding - HCPCS Level II Codes

• Alphanumeric codes with a single alphabetical letter followed by 4 numeric digits,

– Codes for products, supplies, services not included in the CPT codes.

• J9170 = Docetaxol (cancer drug)

– Codes for services for which Medicare does not utilize the CPT-4 code:

• Example: Electrical Stimulation (therapy)

• CPT-4 code = 97014

• HCPCS Level II code = G0281 or G0283

57

Health Information Management (HIM)

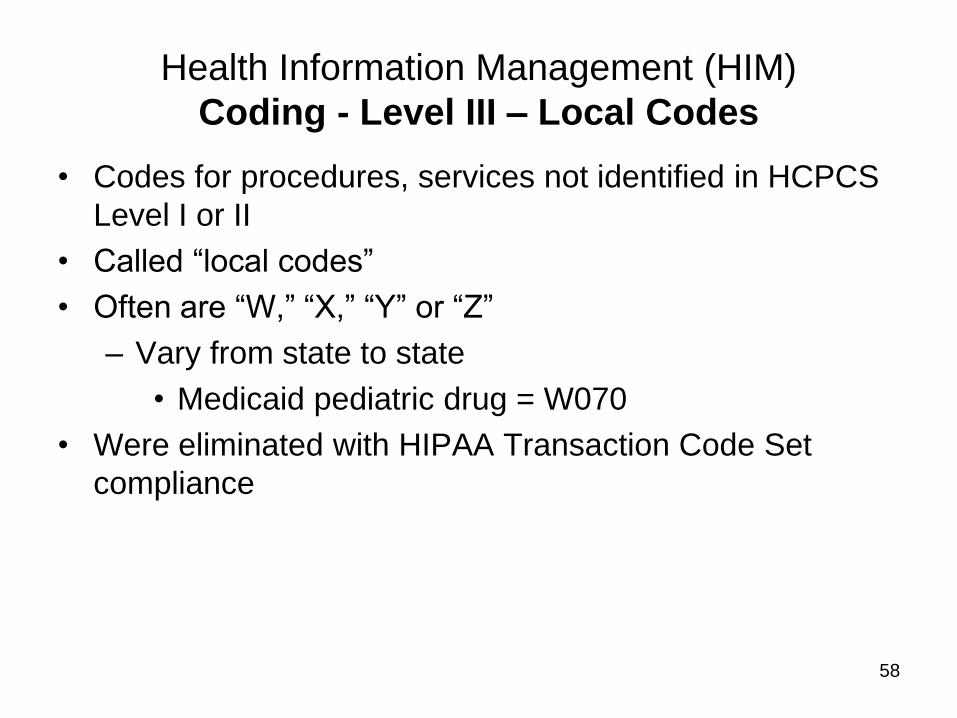

Coding - Level III – Local Codes

• Codes for procedures, services not identified in HCPCS

Level I or II

• Called “local codes”

• Often are “W,” “X,” “Y” or “Z”

– Vary from state to state

• Medicaid pediatric drug = W070

• Were eliminated with HIPAA Transaction Code Set

compliance

58

Health Information Management (HIM)

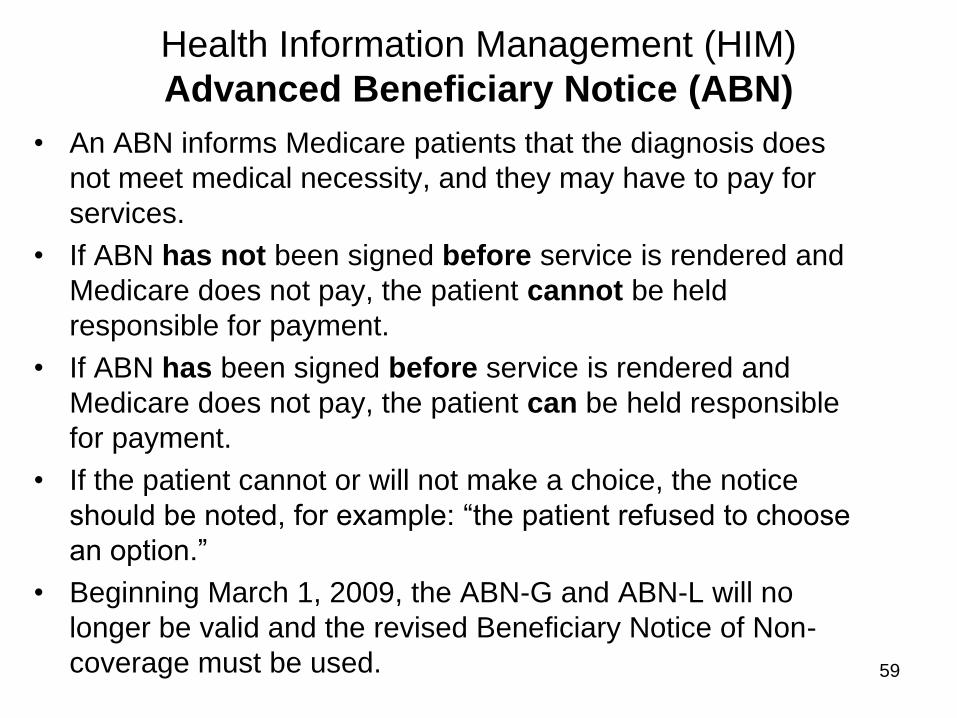

Advanced Beneficiary Notice (ABN)

• An ABN informs Medicare patients that the diagnosis does

not meet medical necessity, and they may have to pay for

services.

• If ABN has not been signed before service is rendered and

Medicare does not pay, the patient cannot be held

responsible for payment.

• If ABN has been signed before service is rendered and

Medicare does not pay, the patient can be held responsible

for payment.

• If the patient cannot or will not make a choice, the notice

should be noted, for example: “the patient refused to choose

an option.”

• Beginning March 1, 2009, the ABN-G and ABN-L will no

longer be valid and the revised Beneficiary Notice of Non-

coverage must be used. 59

CPAR COACHING

Chapter 2

General Payer Information

60

Section 2.1

Overview

Includes:

•Managed Care

•Commercial Insurance

61

What is Managed Care?• Contract with providers to give discounts on health care

services.

• A network of providers who agree

– to pre-established reimbursement programs

– which ensure appropriate use of services and

– promote quality of care.

• A health benefit plan that typically costs employees less

money when they choose a provider in the network.

• “In-network” – Payers who provide for benefits on a

prepaid basis.

• Network administered by employer‟s or an individual‟s

health plan to address appropriateness and cost of

health care delivered.

62

Interventions

• Financial incentives to use providers in-network

• Utilization Management program

• Quality Management program

• Disease or case management programs

• Programs are geared to prevent illness and injury and

promote wellness.

63

History of Managed Care

• Managed Care began in 1910 when Western Clinic in

Tacoma, Washington, offered medical services to lumber

mill owners and employees for 50 cents a month.

• Managed care has progressed through the years with

many transformations, many of which have been

regulated by state and federal laws.

• Kaiser-Permanente was the first nationally recognized

HMO, created in 1955.

64

Third Party Administrators (TPA)

• Specialize in administering health benefits plans for

employers who use their own funds to pay for health

care benefits for their employees.

• May pay claims on behalf of insurance companies.

• May provide services directly to employers at much less

cost than the insurance companies could.

65

HMO’s

• In the 1990‟s HMO‟s became a nationally accepted

alternative to indemnity insurance.

– Indemnity focus:

• Payment for unforeseen illnesses and injuries

• Individual pays deductible and perhaps a co-insurance

– HMO‟s focus:

• Minimal out-of-pocket expenses = co-pay

• Encouraged preventive screenings and annual

checkups

66

PPO Networks

• Utilizes Primary Care Physician (PCP) as

gatekeeper:

– Coordinates all health care services on patient‟s

behalf

– Reduces unnecessary /inappropriate care

– Reduces duplication of health care services

• Higher benefit for using in-network providers

• Lower benefit for using out-of-network providers

67

Next Generation of

Managed Care

• Use of new programs to tie a particular provider‟s

payment for services to the quality of care delivered:

– Pay for Performance (P4P)

– Provider Profiling

– Quality Indicators

– Report Cards

• Providers with lesser ratings = the plan pays less of the

cost of the service

68

Consumer Driven Healthcare

• The wave of the future – a system where consumers, not

the payer or insurance provider, determine how and where

to spend their healthcare allotments.

• The consumer has direct input into decisions being made

regarding their healthcare needs.

• Consumers held accountable for financial consequences

of their decisions and rewarded for appropriate behaviors.

69

Consumer Driven Healthcare

• Plans under consideration:

– Full-defined Contribution

• Employee responsible for finding & purchasing individual medical coverage.

• Employer provides funding by direct compensation or voucher

– Tiered networks

• Employers offer a choice of medical plans

– Menu-driven

• Employees access online information to customize benefit plan

– Health Savings Accounts

• Medical savings, flexible spending and health reimbursement arrangements. 70

Commercial Insurance

• Provides health care benefits through a “for-profit”

insurance company.

• Majority of commercial payers pay for covered

medical expenses using either a fee schedule or a

“Usual and Customary” payment schedule.

71

Basic Commercial Coverage

• Two basic commercial insurance coverage:

– Individual or Direct Pay Health Care Plans

– Group Health Plans

• Individual or Direct Pay Health Care Plans

– Covers subscriber, possibly subscriber‟s family

– Premiums paid by subscriber

• Group Health Plans

– Employer or organization provided

– Employer pays premiums in full or part

– Carrier is picked by employer or organization

– Covers employee, possibly employee‟s family

72

Commercial Insurance

• It is critical that healthcare personnel determine what

services are covered by insurance.

• Most commercial insurance companies require pre-

certification prior to admission.

• Assignment of benefits must be obtained from the

patient or insured.

73

Section 2.2

Government Payers

Includes:

•Medicare

•Traditional Medicaid

•Medicaid State Children‟s Health Insurance Program (S-CHIP) – PeachCare

•Medicaid Programs & Care Maintenance Organizations (CMO)

74

Medicare

• General

– The Medicare program was created by

Congress in 1965

– It is administered by the Center for Medicare

and Medicaid Services (CMS)

– The Social Security Administration (SSA) is

responsible for enrollment

75

Medicare Eligibility

• Medicare is a health insurance plan for:

– People 65 years of age and older,

– Some people with disabilities who have

been receiving Social Security for a set

amount of time (24 months in most cases)

– People with End Stage Renal Disease

(ESRD) requiring dialysis or a kidney

transplant.

76

Original Medicare Plan

• Part A

– Hospital insurance which covers IP hospital stays, Skilled Nursing Facility (SNF), Hospice, some Home Health Care, blood, IP psychiatric services

• Part B

– Medical insurance which covers OP hospital care, diagnostic tests, doctor‟s services,

77

Medicare

Coverage Options

• Original Medicare Plan

– Patients can go to any doctor, specialist,

hospital or other healthcare provider that

accepts Medicare

– Patients may be charged a deductible or co-

insurance each time they receive service from

a provider

– Deductible set annually for part B

– Deductible due per benefit period for part A

– Regular “red, white & blue” Medicare card78

Medicare

Coverage Options

• Medicare Advantage Plans (Part C)

– Patients can receive prescription drugs

– Routine or screening services are included

– Additional rules to follow. Ex: you must use

specific providers & services may need

preauthorization

– Beneficiaries may have to pay a monthly

premium for extra benefits.

– Separate Membership card from the HMO

79

Medicare Benefit Period

• A way in which Medicare measures a beneficiary‟s use

of hospital and Skilled Nursing Facility (SNF) services

• Begins the day the beneficiary is admitted to a hospital

or SNF

• Ends when the beneficiary hasn‟t received hospital or

SNF services for at least 60 consecutive days from

discharge.

80

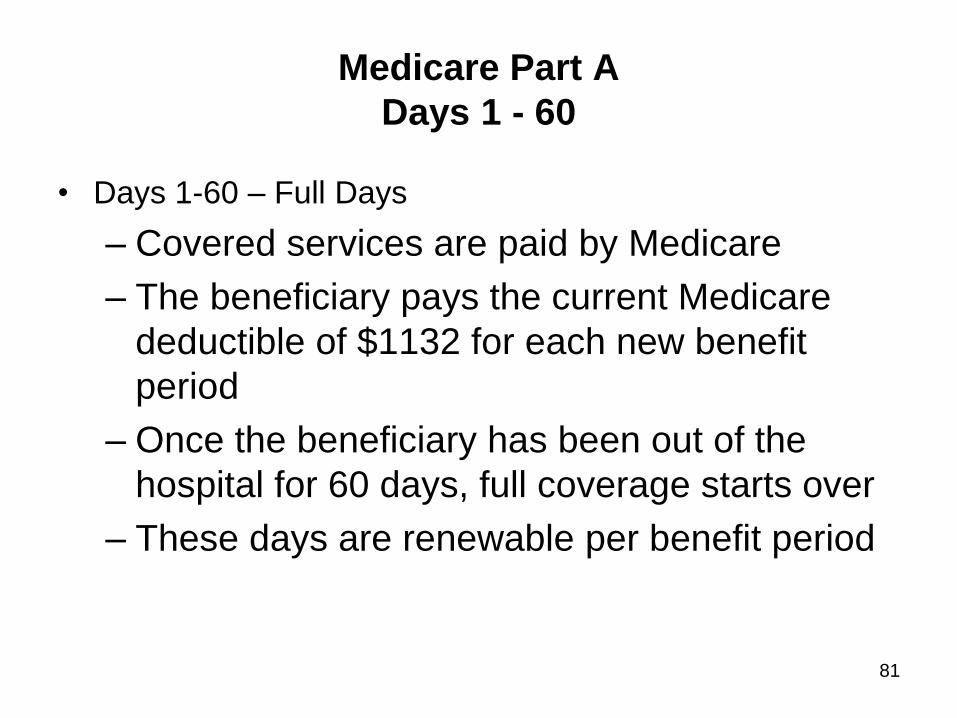

Medicare Part A

Days 1 - 60

• Days 1-60 – Full Days

– Covered services are paid by Medicare

– The beneficiary pays the current Medicare

deductible of $1132 for each new benefit

period

– Once the beneficiary has been out of the

hospital for 60 days, full coverage starts over

– These days are renewable per benefit period

81

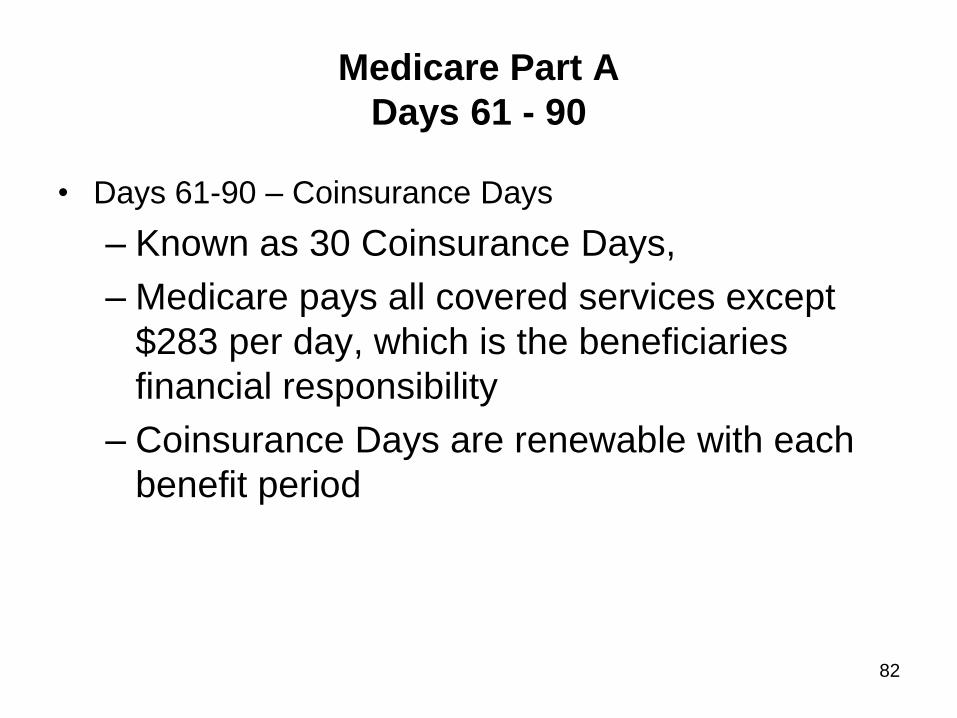

Medicare Part A

Days 61 - 90

• Days 61-90 – Coinsurance Days

– Known as 30 Coinsurance Days,

– Medicare pays all covered services except

$283 per day, which is the beneficiaries

financial responsibility

– Coinsurance Days are renewable with each

benefit period

82

Medicare Part A

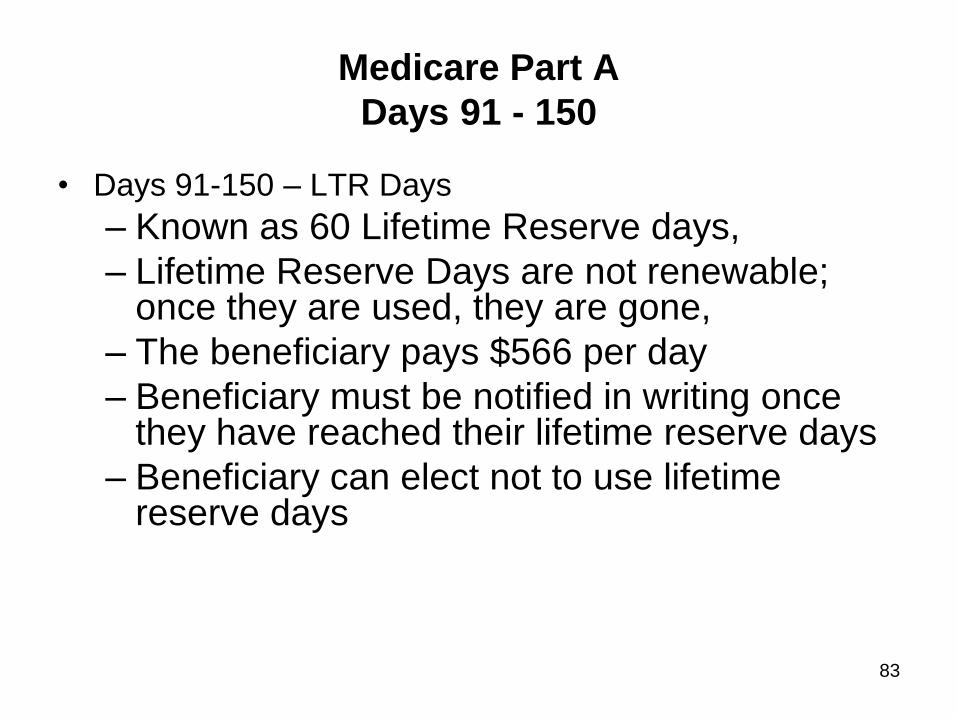

Days 91 - 150

• Days 91-150 – LTR Days

– Known as 60 Lifetime Reserve days,

– Lifetime Reserve Days are not renewable; once they are used, they are gone,

– The beneficiary pays $566 per day

– Beneficiary must be notified in writing once they have reached their lifetime reserve days

– Beneficiary can elect not to use lifetime reserve days

83

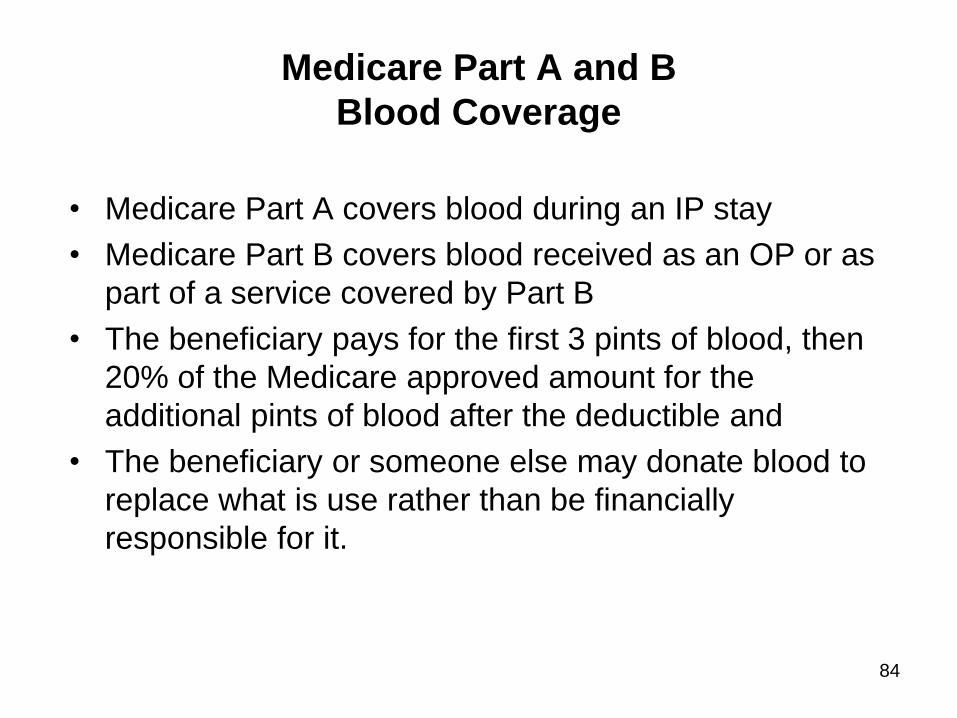

Medicare Part A and B

Blood Coverage

• Medicare Part A covers blood during an IP stay

• Medicare Part B covers blood received as an OP or as

part of a service covered by Part B

• The beneficiary pays for the first 3 pints of blood, then

20% of the Medicare approved amount for the

additional pints of blood after the deductible and

• The beneficiary or someone else may donate blood to

replace what is use rather than be financially

responsible for it.

84

Medicare Part B Coverage

• The Part B monthly premium can range between $115.40 -$369.10 per month based on the beneficiary's annual income.

• The Part B deductible is $162.00 per calendar year,

• In most cases, after satisfying the deductible, the beneficiary is responsible for the coinsurance of 20% of the allowed amount.

85

Medicare Part B Coverage

• Preventative Services

– Medicare Part B helps pay for preventative

health care services to help keep

beneficiaries healthy including:

• Glaucoma screening,

• Flu (Influenza) shot,

• Hepatitis B shot,

• Mammogram screening

86

Medicare 3 Day Rule

• Medicare requires that all diagnostic services (regardless of the diagnosis) and any related therapeutic (same diagnosis) OP services provided to the beneficiary 3 days prior to an IP admission to the same hospital be included on the IP claim and not billed separately on an OP claim.

Note: This is frequently referred to as the 72-hour rule.

87

HICN Number

• The HICN number (Health Insurance Claim Number) is

usually a 9 digit number, or Social Security number,

followed by a suffix based on type of eligibility:

• A for Wage Earner

• B for Aged Wife

• D for Aged Widow

88

Medicare Secondary Payer (MSP)

• Providers must identify any other coverage the patient

may have that could be primary to Medicare,

• All questions on the MSP Questionnaire should be asked

and answered by the patient and recorded by

Registration staff and

• The MSP information must be retained in the patient‟s

record for audit purposes.

89

MSP – Working Aged

• Beneficiary is 65 years or older and

• They have Employee Group Health Plan (EGHP)

coverage based on their own employment OR

• Based on the employment of their spouse (at any age)

and

• The EGHP has 20 or more employees,

• The EGHP will be primary to Medicare.

90

MSP - Disability

• Beneficiary is entitled to Medicare based on disability AND

• Is under 65 year of age AND

• They have Large Group Health Plan (LGHP) coverage

based on their own employment OR

• Based on the employment of their spouse or guardian AND

• The LGHP has 100 or more employees,

• The LGHP will be primary to Medicare.

91

MSP - ESRD

• Beneficiary is entitled to Medicare based on the diagnosis

of End Stage Renal Disease (ESRD) AND

• They have Employee Group Health Plan (EGHP) coverage

AND

• They have waived the self-dialysis training AND

• They have not received a kidney transplant

• The EGHP is primary to Medicare for a period of 30

months, which is the coordination period, which begins

after a 3 month waiting period, which is waived if the patient

takes the self-dialysis training or receives a transplant.

92

MSP –

Worker’s Compensation

• If the illness or injury the Beneficiary is receiving services

for is due to a work related accident or injury,

• Worker’s Compensation will be primary to Medicare.

93

Medicare Timely Filing

• The filing deadline for Medicare Part A services

is one calendar year from the date of service.

– For Inpatient services, this is one calendar

year from the date of Admission.

94

Medicare Recovery Audit Contractors (RAC)

• The RAC Program was created to safeguard the

Medicare Program and it‟s continued financial viability.

• Designed to identify and recover improper payments

made by Medicare.

• RACs are paid a contingency fee based on recoveries.

95

Traditional Medicaid

• The Georgia Medical Assistance Program or Medicaid was established to provide quality medical care to eligible persons on a cost effective basis under the provisions of Title XIX (19) of the 1965 Social Security Act.

• State administered program jointly funded by the federal government and the State of Georgia.

96

Medicaid Agencies and Functions

• Department of Community Health (DCH) state agency

with the following Medicaid functions:

– Administration

– Budget and fiscal control

– Contract Monitoring

– Polices and Procedures

– Liaison with federal agencies

97

Medicaid Agencies and Functions

• Affiliated Computer Services (ACS)/Georgia Health Partnership (GHP) are contracted with Medicaid and their functions include:

– Provider Enrollment

– Training

– Provider Services

– Telephone & electronic inquiry

– Claims processing

– Member outreach

98

Traditional Medicaid

• GMCF – Georgia Medical Care Foundation

– Sub-contractor to ACS

– Precertification / pre-authorization

– Medical review unit

– Outlier review

– Out of state services

– Pre-payment review

– Nurse aide training

– Find a Healthcare Resource

99

Medicaid Agencies and Functions

• Department of Family and Children Services

(DFCS)/Department of Human Resources

(DHR)/Social Security Administration (SSA)

– are contracted with Medicaid and their

functions include:

• Eligibility determination

• Facility licensing and

• Compliance

100

Traditional Medicaid Eligibility

• Those eligible for Medicaid receive a plastic identification

card

• The web portal is the best resource for eligibility

information

• Other eligibility forms may include:

– SSI Notification Letter,

– Temporary Medicaid Certification (Form 962),

– Retroactive Medicaid Eligibility (Form 964).

101

Traditional Medicaid

Retroactive Eligibility

• When an individual is not a Medicaid recipient on the

date medical services are provided, but it is later

determined they met eligibility criteria at the time service

was rendered, a claim may be submitted.

• ACS must receive retroactive eligibility claims

(Certification of Retroactive Medicaid Eligibility Form

964)

– within six (6) months of the month in which the

determination of retroactive eligibility is made.

• The recipient will receive a Medicaid card for ongoing

eligibility, but not for the retroactive months.

102

Traditional Medicaid with Third Party Liability

(TPL)

• Providers have an obligation to investigate and report

the existence of other insurance or liability since

Medicaid is the payer of last resort.

• Medicaid will not pay when patients are uncooperative in

furnishing TPL information or when they are using out of

network facilities to receive services.

103

Traditional Medicaid

Medically Needy Spend-Down

• Covers children under the age of 18, pregnant women, aged, blind and/or disabled persons who would otherwise not be Medicaid eligible because their monthly income exceeds eligibility payment standards.

• Individuals issued DMA 962/964 for 1st partial month of eligibility and shows beginning date of eligibility.

• DMA 400 issued to individual and indicates amount they will owe to provider.

104

Traditional Medicaid

Pre-Certification / Prior Approval

• Most inpatient and some outpatient services must

be pre-certified.

• Elective admissions and scheduled outpatient

procedures must be pre-certified prior to service.

• Urgent / emergent services must be pre-certified

within 30 calendar days and supported by

emergency conditions.

105

Traditional Medicaid Sterilization

• Medicaid is prohibited from making payment for sterilizations performed on any patient who is:

– Under 21 years of age at the time consent is signed,

– Is not mentally competent, OR

– Is institutionalized in a correctional facility, mental hospital or other rehab facility.

• Sterilization consent form (DMA 69) must be properly

completed and signed for all sterilization procedures and

attached to the claim at the time of submission.

• There is a mandatory 30 waiting period between signed

consent and sterilization.

• The signed consent expires 180 days from the date of

the recipient‟s signature.

106

Traditional Medicaid

Mammography

• Traditional Medicaid recipients are limited to one

mammogram per year unless medically justified.

• Mammography services are only reimbursed when

performed in a facility certified by the FDA.

107

Traditional Medicaid

Reimbursement

• Inpatient services are reimbursed based on a hybrid –

DRG prospective payment system based on the

Champus DRG grouper.

• Outpatient services are reimbursed based on a

determination of allowable and reimbursable costs as

determined from paid claims data.

108

Traditional Medicaid

Emergency Room Visits

• Emergency room visits that are not a true medical

emergency will be reimbursed at a all-inclusive flat rate

of $50.

• Services provided within 3 days of an IP admission or

discharge for the same or related diagnosis is

considered a part of the same admission and includes

hospital services including laboratory and radiology.

109

Traditional Medicaid

IP/OP Co-Payments

• A co-payment of $12.50 will be imposed on hospital IP

services.

• A $3.00 co-payment is due for non-emergency OP

services.

110

Traditional Medicaid

S-CHIP

• S-CHIP (State Children‟s Health Insurance Program)

– designed to provide coverage to low income

children

– family income below 200% of Federal Poverty

Level or

– whose family has an income 50% higher than

the state‟s Medicaid eligibility threshold.

• Administered by DCH a division of Medical Assistance

111

Traditional Medicaid

Peachcare for Kids

• PeachCare for Kids

– Established in 1998 to provide S-CHIP eligible

children with benefits similar to those offered

by Medicaid

– For children from birth to 18 years

• Administered by DCH, a division of DMA.

112

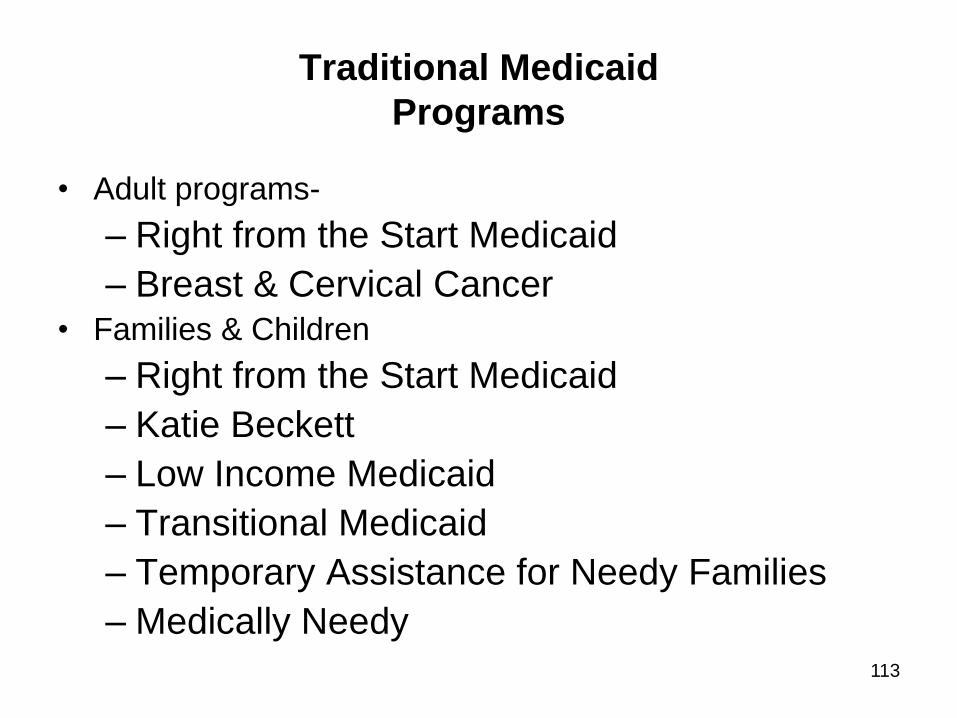

Traditional Medicaid

Programs

• Adult programs-

– Right from the Start Medicaid

– Breast & Cervical Cancer• Families & Children

– Right from the Start Medicaid

– Katie Beckett

– Low Income Medicaid

– Transitional Medicaid

– Temporary Assistance for Needy Families

– Medically Needy113

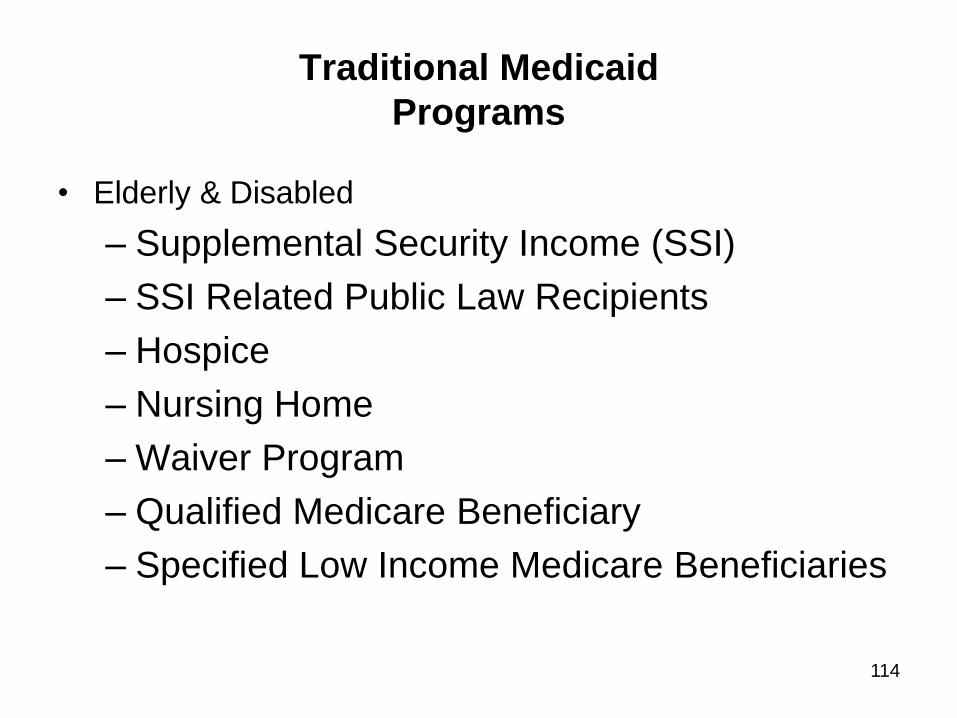

Traditional Medicaid

Programs

• Elderly & Disabled

– Supplemental Security Income (SSI)

– SSI Related Public Law Recipients

– Hospice

– Nursing Home

– Waiver Program

– Qualified Medicare Beneficiary

– Specified Low Income Medicare Beneficiaries

114

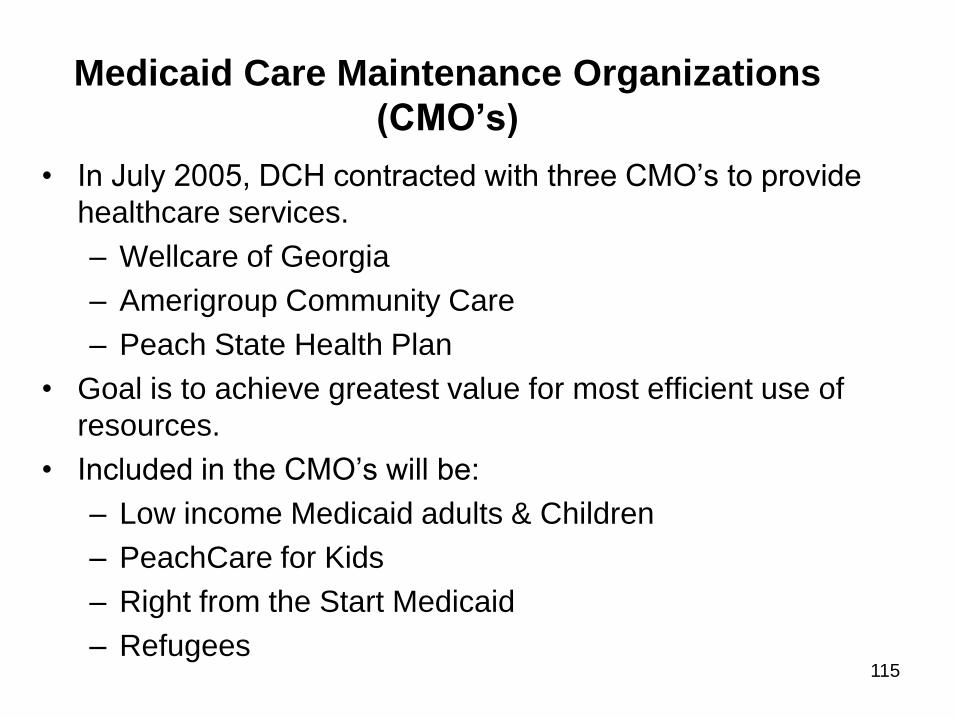

Medicaid Care Maintenance Organizations

(CMO’s)

• In July 2005, DCH contracted with three CMO‟s to provide

healthcare services.

– Wellcare of Georgia

– Amerigroup Community Care

– Peach State Health Plan

• Goal is to achieve greatest value for most efficient use of

resources.

• Included in the CMO‟s will be:

– Low income Medicaid adults & Children

– PeachCare for Kids

– Right from the Start Medicaid

– Refugees115

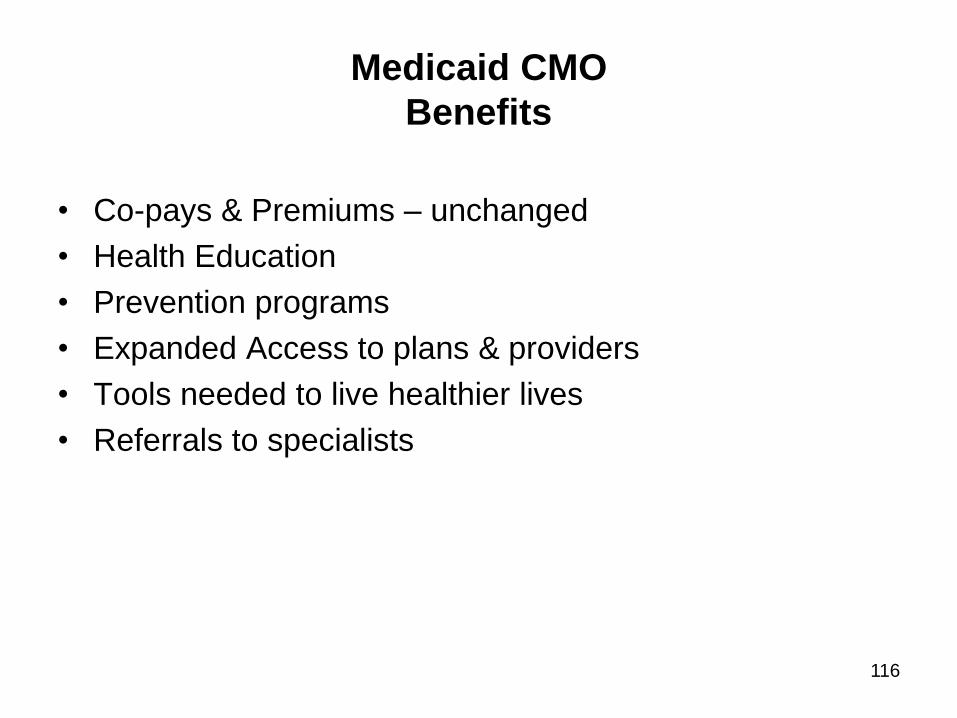

Medicaid CMO

Benefits

• Co-pays & Premiums – unchanged

• Health Education

• Prevention programs

• Expanded Access to plans & providers

• Tools needed to live healthier lives

• Referrals to specialists

116

Medicaid CMO’s

Health Plans

• Amerigroup Community Care

– The nation‟s largest company solely focused on low-income families and people with disabilities

• Wellcare

– Leading provider of government-sponsored health plans. The largest Medicaid & Medicare only contractor in the nation.

• Peach State Health Plan

– A physician-driven, Georgia based Medicaid managed care plan.

– Parent company, Centene Corporation

– To help members grow healthy & stay healthy by providing access to quality healthcare.

117

Section 2.3

Commercial Payers

Includes:

•Blue Cross Blue Shield (BCBS)

•State Health Benefit Plan (SHBP)

•TRICARE

•Workers‟ Compensation

•COBRA

•Uninsured Patients

118

Blue Cross Blue Shield

• Offers a complete line of health benefit products

• Offers electronic claims processing network system,

HMO, and a life insurance subsidiary

• The word “plan” means a separately incorporated, locally

administered corporation authorized to use the BCBS

name and symbol

119

BlueChoice HMO and POS

• BlueChoice Healthcare Plan

– Health Maintenance Organization (HMO)

• BlueChoice Option

– Point-of-Service (POS) product

– Self-referral or services by a non-participating provider are out-of-network, result in reduced level of benefits

• BlueChoice PPO

– Preferred Provider Organization (PPO)

– In-network when member selects preferred network

provider

– Out-of-network when member selects non-preferred

provider which results in a lower out-of-network

benefit rate120

Federal Employee Program

• Federal Employee Program (FEP)

– Blue Cross Blue Shield Association contracts

with the U.S. Office of Personnel

Management (OPM) to provide government-

wide service benefit plan

– Coverage for federal employees and

dependents, choices offered are:

• FEP PPO or

• FEP EPO Exclusive Provider

121

FEP Maternity Claims

• Blue Cross and FEP

– If baby is well:

• File both mother and baby charges on the same

claim

– If baby is sick:

• 1 claim for mother‟s charges and

• 1 claim for baby from date of birth

122

NASCO

• Blue Card Program for National Accounts

– A company with locations in more than one BCBS

plan area is a national account

– Accounts are administered by more than one BCBS

plan and have a control plan

– National accounts administered by BCBSGA are

handled through NASCO or National Account Service

Company Operation

123

NASCO Maternity Claims

• NASCO Accounts

– One claim when the mother and baby are in

the hospital the same number of days

– Nursery charges should be billed with

Revenue Code 171

– Add baby‟s ancillary charges to mother‟s

ancillary charges

– If sick baby, file baby charges after mother‟s

discharge on separate claim

124

BC, FEP and Medicare

• BC, FEP primary to Medicare

– when patient has Medicare and is enrolled in

active group policy

• BC may be secondary to Medicare:

– When patient is covered by retired BC group

policy

– When secondary, BC pays Part A and Part B

deductibles, coinsurance, lifetime reserve

days

125

Split Billing Year End Claims

• BCBSGA requires services that span two calendar years

be split into separate claims for each year of service for:

– State Health Benefit Plan (SHBP)

– NASCO Accounts

– Federal Employees Program (FEP)

– Out of state BC plans

126

State Health Benefits Plan (SHBP)

• The Georgia Department of Community Health (DCH)

administers the State Health Benefit Plan (SHBP) and is

governed by a 9 person board appointed by the

Governor

• SHBP provides health insurance coverage to state

employees, school system employees, retirees and their

dependents

• SHBP is a self-insured plan, with the exception of a fully

insured HMO options

127

State Health Benefits Plan (SHBP)

• The plan is funded by employer and employee

contributions

• There is no insurance company or service plan that

collects premiums and assumes risk

• The State of Georgia assumes the risk and funds the plan using tax dollars

• United Healthcare is the claim administrator and pays most claims for SHBP, PPO and HMO

• Blue Cross continues to administer benefits for the University Systems, PPO and indemnity plans.

128

SHBP Eligibility and Options

• Full-time employees of the State of Georgia, the General Assembly, or an agency, board, commission, department, county administration or contracting employer that participates in SHBP,

• Certified public school teachers or library employees,

• Employees who are eligible to participate in the Public School Employees‟ Retirement System and

• State University Employees and Dependents

• A retired employee of one of these listed groups.

• Options:

– Health Reimbursement Arrangement (HRA)

– Definity HRA (United Healthcare)

– Choice Fund HRA (CIGNA)

– HMO

– HDHP129

SHBP Claim Processing

• The deadline to request claim corrections is one (1) year

from the date of the EOB or re-filing.

• Facility claims must be filed within 90 days from the date

of discharge if SHBP is primary or secondary.

• Claims spanning calendar years are required to be split

billed and filed separately and

• Claims received with year-end overlapping dates will be

returned to the hospitals.

130

SHBP Maternity Claims

• Mother and baby charges must always be submitted on

2 separate claims

• SHBP individual deductibles, coinsurance amounts and

maximums are applied on the baby‟s and the mother‟s

charges

• The minimum maternity length of stay in compliance with

the Newborn‟s and Mother‟s Health Protection Act of

1996 is:

– 48 hours for IP care following normal delivery and

– 96 hours for cesarean section.

131

TRICARE

• TRICARE (formerly CHAMPUS) is a Department of

Defense program of healthcare for beneficiaries of the

uniformed services and

• Offers 6 options, plus a secondary coverage for

Medicare Part A and Part B beneficiaries

132

TRICARE Prime

• Plan that is similar to an HMO

• Enrollment is for 1 year

• There is an enrollment fee for retirees and their

dependents:

– $230 per individual OR

– $460 per family (payable in quarterly installments of

$115)

• There are per visit fees for retirees and their family members (co-payments),

• Active duty members and their families no longer have a co-pay for visits and

• Enrollees select a primary care manager who coordinates their healthcare, including referral to specialty providers

133

TRICARE Prime Remote (TPR)

TRICARE Prime Remote for Active Duty Family

Members (TPRADFM)

• Provides coverage to active duty service members and

their families who live in remote locations

• Utilizes a network of civilian TRICARE authorized

providers

• Must live and work in an area that is at least 50 miles or

a one hour drive away from a military treatment facility

• No enrollment fees or copays

134

TRICARE Point of Service (POS)

• Allows non-active duty service members enrolled in

TRICARE Prime, TPR or TPRADFM to receive non-

emergency care from any TRICARE-authorized provider

without referral but at higher out of pocket costs

135

TRICARE Standard and TRICARE Extra

• Fee-for-service plan available to all non-active duty

beneficiaries

• Enrollment not required

• Coverage automation as long as information is current in

DEERS

• Network/Non-network providers determine which plan

option is used.

– Network provider chosen – Extra option is used

– Non-network provider chose – Standard option is

used

136

TRICARE for Life

• Wrap-around coverage available to all Medicare-eligible

TRICARE beneficiaries regardless of age or place of

residence

• Must have both Medicare Part A and Part B

• Medicare is primary; TRICARE is secondary

137

TRICARE

DEERS

• Defense Enrollment Eligibility Reporting System –

benefits eligibility system

• All eligible beneficiaries must be entered into the DEERS

system

• Sponsors should visit the personnel office or the

Uniformed Services ID Card issuing facility to ensure

beneficiaries are entered

138

TRICARE

Newborns

• Newborn should be enrolled in DEERS as soon after birth as possible

• Newborns are covered as Prime beneficiaries for 60 days as long as another family member is enrolled in Prime

• On the 61st day, newborns will be processed as Standard and Extra if not enrolled in Prime by the sponsor

• 365 days after birth, newborn looses all TRICARE eligibility unless enrolled in DEERS.

139

TRICARE Eligibility

• The categories of individuals eligible for TRICARE

benefits are:

– Members of the Uniformed Services receiving or

entitled to receive retired, retainer or equivalent pay

based on duty in the service

– Spouses of active duty members or retirees

– Children of active duty members or retirees

– Un-remarried widowers and widows of deceased

active duty members and deceased retirees

– Children of deceased active duty members and

deceased retirees and

– Ex-spouses who have valid ID cards.

140

TRICARE Eligibility

for Children

• Children must be unmarried,

• Under the age of 21 (age 18 for CHAMPVA) and

• Financial dependence is not required except for students

and disabled children who have passed their 18 or 21st

birthday

141

TRICARE

Continued Health Care Benefit Program

• Began October 1, 1994, and extends health care

coverage when they lose military benefits

• Extends healthcare coverage for the transition period

between military benefits and civilian health care

• CHCBP Basics

– Provides continuous coverage on a temporary basis

between military benefits and civilian healthcare

coverage

– May cover for pre-existing conditions

– Comparable to TRICARE standard benefits

142

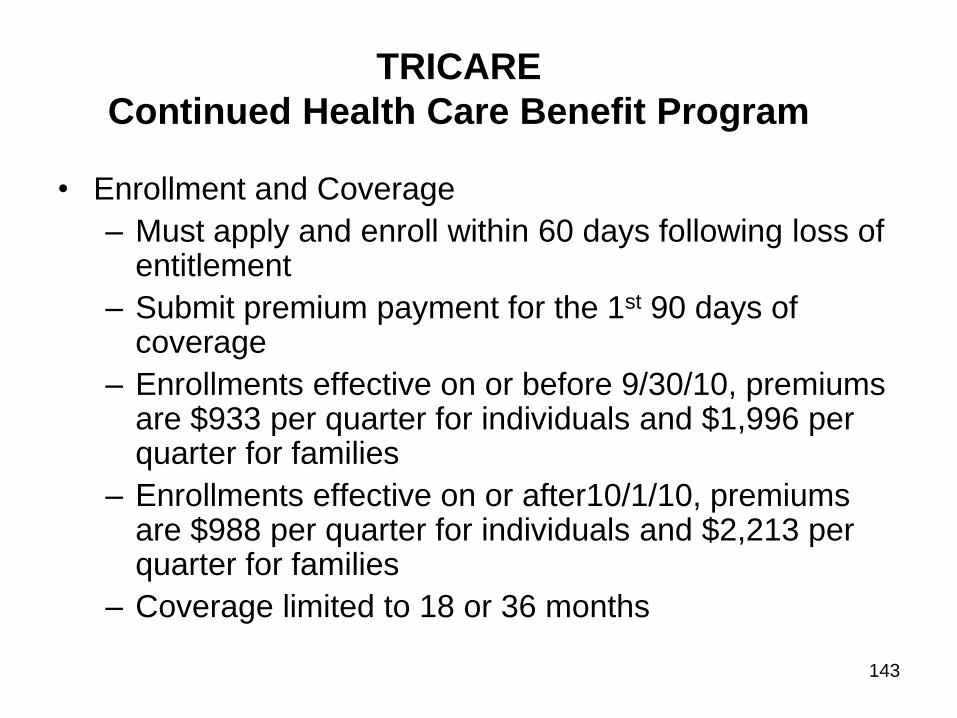

TRICARE

Continued Health Care Benefit Program

• Enrollment and Coverage

– Must apply and enroll within 60 days following loss of entitlement

– Submit premium payment for the 1st 90 days of coverage

– Enrollments effective on or before 9/30/10, premiums are $933 per quarter for individuals and $1,996 per quarter for families

– Enrollments effective on or after10/1/10, premiums are $988 per quarter for individuals and $2,213 per quarter for families

– Coverage limited to 18 or 36 months

143

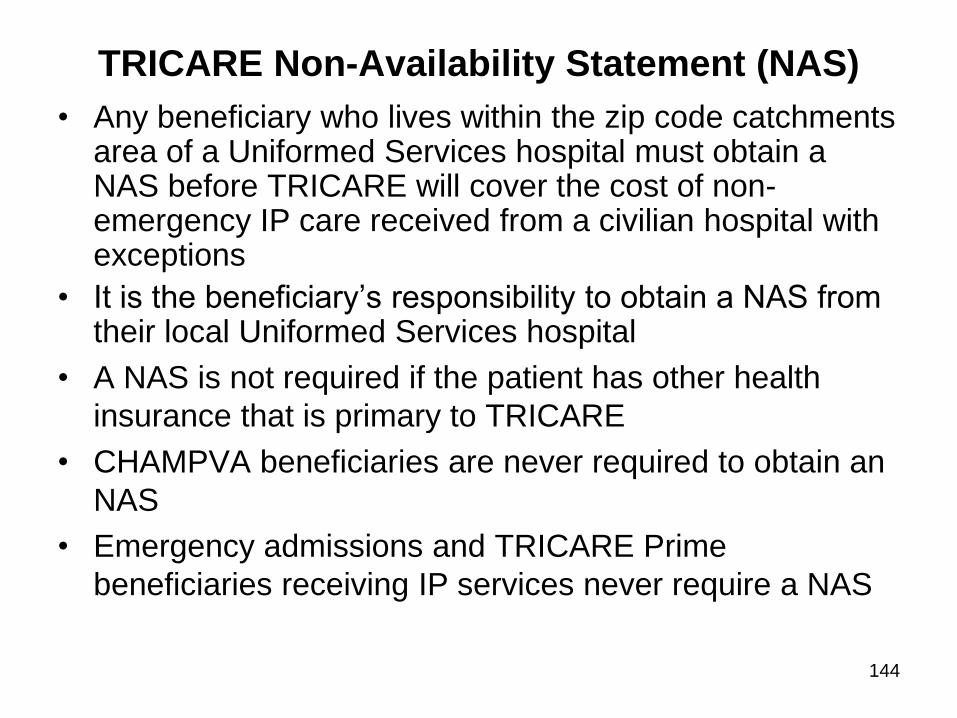

TRICARE Non-Availability Statement (NAS)

• Any beneficiary who lives within the zip code catchments area of a Uniformed Services hospital must obtain a NAS before TRICARE will cover the cost of non-emergency IP care received from a civilian hospital with exceptions

• It is the beneficiary‟s responsibility to obtain a NAS from their local Uniformed Services hospital

• A NAS is not required if the patient has other health

insurance that is primary to TRICARE

• CHAMPVA beneficiaries are never required to obtain an

NAS

• Emergency admissions and TRICARE Prime

beneficiaries receiving IP services never require a NAS

144

TRICARE

Reserve Component

• Active duty reservists, spouses and unmarried children of

the reservists on active duty for more than 30 days are

eligible for TRICARE benefits

• Retirees and their families are eligible for TRICARE

benefits

• Widows or widowers and unmarried children of deceased

active duty reservists are eligible if the sponsor was

ordered to active duty for more than 30 days

• Medal of Honor recipients and their family members are

eligible for TRICARE benefits

145

Worker’s Compensation

• Benefit program created by state law.

• Provides medical, rehabilitation, income, death and other

benefits to employees and dependents due to injury,

illness and death resulting from a compensable work-

related claim covered by the law.

• Coverage begins the first day of employment.

• Employers with 3 or more employees are required by law

to provide coverage.

• Any injury, illness or death arising out of and in the

course of employment is by definition a compensable

work-related claim.

146

Worker’s Compensation

• If employees are injured while performing assigned job

duties during assigned work hours, they are covered.

• Injuries sustained while engaging in unassigned duties,

during lunch and breaks, are not covered, and

• Injuries that occur during an employees commute to and

from work are not covered.

• If an employee is injured on the job, they should

immediately report the injury to their employer.

• Paperwork required by the company must be completed

and forwarded to the appropriate organization for

processing, including information regarding the injury.

• If an injury is serious in nature, immediate medical

attention should be provided.147

Worker’s Compensation

• Worker‟s Compensation does not provide benefits for an

injury or accident resulting from an employee‟s willful

misconduct.

• Injuries resulting from “haste” or “inattentiveness” would

be covered.

148

WC Authorization of Coverage

• Employer‟s choose an insurance company to handle worker‟s compensation cases.

• Before admission, the insurance company should be notified and verification of coverage obtained.

• The patient should have a written authorization form (possibly an incident report).

• If not, this documentation can be requested from the employer.

• It should be established with the employer whether or

not they recognize responsibility for the injury.

• If so, a letter stating this obligation should be requested.

• If verification of coverage cannot be obtained from the

employer, the hospital should make the account self-pay

until verification is received.149

WC Denial Of Coverage

• If the worker‟s compensation carrier denies the claim, the patient has the right to appeal the denial to the State Board, requesting a hearing.

• As long as the patient is appealing, the hospital cannot pursue payment from the patient.

• Inquiry regarding appeal status can be done through the carrier or State Board of Worker‟s Compensation.

150

COBRA

• Federal law – Consolidated Omnibus Budget

Reconciliation Act

– Requires most employers who sponsor group

medical plans to offer employees, their

eligible dependents, the opportunity to

purchase a temporary extension of coverage,

at group rates, when coverage under the plan

would end.

151

COBRA

Qualified Beneficiaries

• Any individual covered by the group health plan the day before a qualifying event

– Individuals covered may include:• Employee

• Employee‟s spouse

• Dependent children

• If you adopt or have a child while covered by COBRA, your newborn or adopted child is a qualified beneficiary.

152

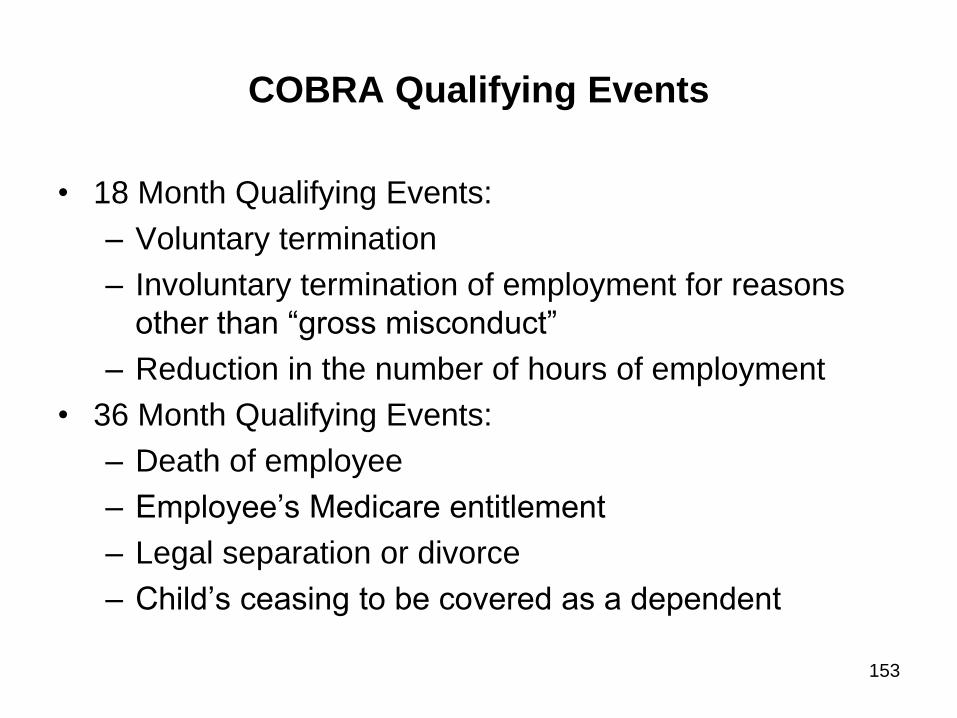

COBRA Qualifying Events

• 18 Month Qualifying Events:

– Voluntary termination

– Involuntary termination of employment for reasons

other than “gross misconduct”

– Reduction in the number of hours of employment

• 36 Month Qualifying Events:

– Death of employee

– Employee‟s Medicare entitlement

– Legal separation or divorce

– Child‟s ceasing to be covered as a dependent

153

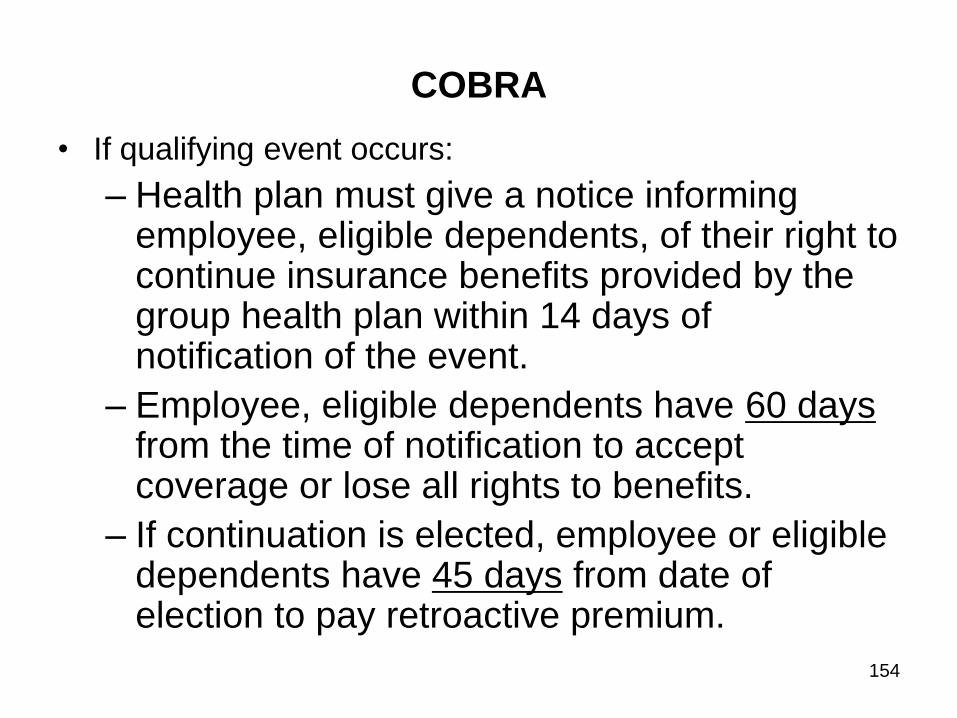

COBRA

• If qualifying event occurs:

– Health plan must give a notice informing employee, eligible dependents, of their right to continue insurance benefits provided by the group health plan within 14 days of notification of the event.

– Employee, eligible dependents have 60 daysfrom the time of notification to accept coverage or lose all rights to benefits.

– If continuation is elected, employee or eligible dependents have 45 days from date of election to pay retroactive premium.

154

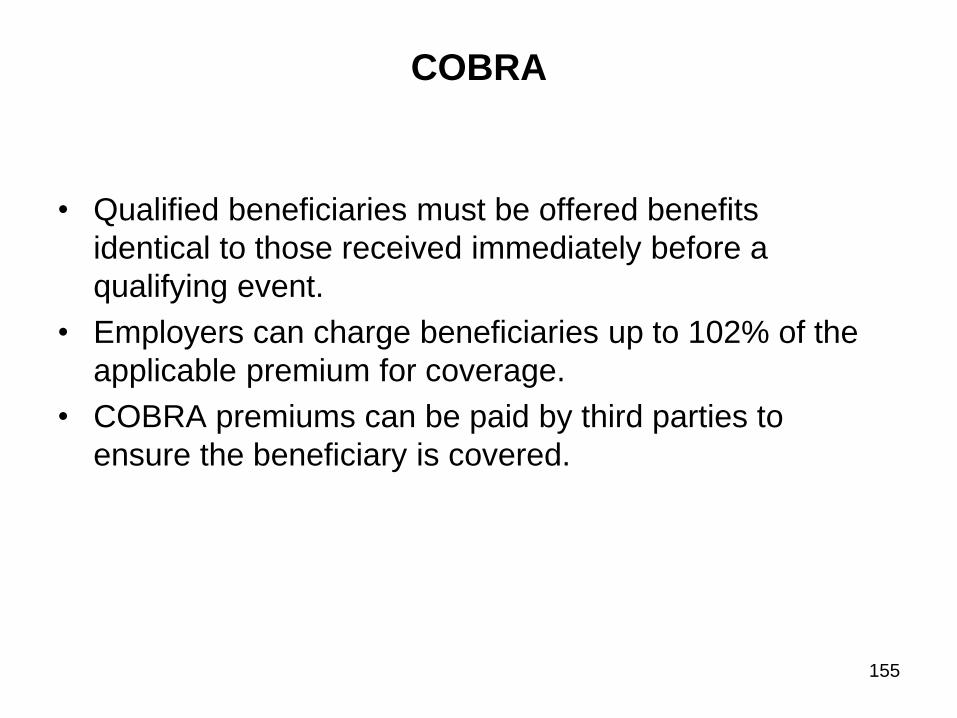

COBRA

• Qualified beneficiaries must be offered benefits

identical to those received immediately before a

qualifying event.

• Employers can charge beneficiaries up to 102% of the

applicable premium for coverage.

• COBRA premiums can be paid by third parties to

ensure the beneficiary is covered.

155

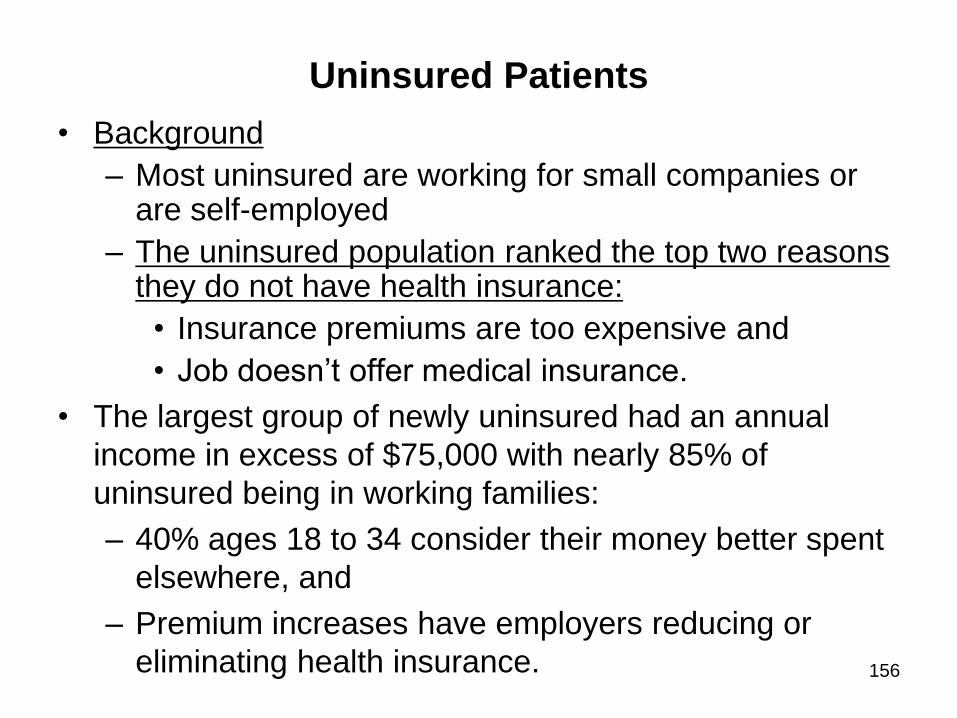

Uninsured Patients

• Background

– Most uninsured are working for small companies or are self-employed

– The uninsured population ranked the top two reasons they do not have health insurance:

• Insurance premiums are too expensive and

• Job doesn‟t offer medical insurance.

• The largest group of newly uninsured had an annual

income in excess of $75,000 with nearly 85% of

uninsured being in working families:

– 40% ages 18 to 34 consider their money better spent

elsewhere, and

– Premium increases have employers reducing or

eliminating health insurance. 156

Identifying the Nature of the Uninsured

• Pre-Access screening and Financial Counseling can

indicate if the patient needs charity assistance or not.

• Process should be designed to capture at least 85% of

uninsured patients.

• The Financial Counselor should interview the patient and

inform them of their estimated balance based on the

procedure to be performed.

157

Payment Options

– Bank notes,

– Bank financing,

– Prompt pay discounts,

– Payroll deduction, and

• Installment notes. There are many payment options you

can offer the patient including:

– Credit or debit cards,

158

Section 2.4

State Programs

Includes:

•Cancer State Aid (CSA)

•Rehabilitation Services

•Children‟s Medical Services (CMS)

•Crime Victims Compensation (CVC)

•Juvenile Justice Department

•Prisons & County Law Enforcement – State of GA

159

Cancer State Aid (CSA)

• Established by Georgia legislature

• Provides cancer treatment to uninsured and under-insured, low income cancer patients

• For hospitals to be reimbursed through Cancer State

Aid:

– Must be approved by JCAHO

– Must have Cancer Program approved by the

American College of Surgeons

• Cost of treatment is paid for by the state

• Physicians donate their services

160

Cancer State Aid (CSA)

• Eligibility Requirements:

– Must have cancer that would benefit from treatment

– Must meet income level requirements

– Must have either no or limited health insurance

– Must be resident of Georgia who is US citizen or

qualified alien

– Must be accepted for treatment by a physician

affiliated with a participating facility

– Must receive treatment at a participating facility

161

Rehabilitation Services

• Vocational Rehabilitation Services

– Available to qualified individuals to correct or

improve a physical/mental condition affecting

his/her work

– VRS payment must be accepted in full by

provider – patient can not be billed

162

Rehabilitation Services

• Eligibility

– Must be disabled

– VR services needed to gain/regain

employment

– Must received SSI, SSDI or TANF

– Georgia resident

– Must meet financial needs assessment

163

Children’s Medical Services (CMS)