cover page of economic and purpose classification publication

58

Transcript of cover page of economic and purpose classification publication

i

E C O N O M I C A N D P U R P O S E

C L A S S I F I C A T I ON O F

S T A T E G O V E R N M E N T B U D G E T

2013-2014 (Accounts)

&

2014-2015 (Revised Estimates)

DIRECTORATE OF ECONOMICS AND STATISTICS,

MADHYA PRADESH

�

�� � � �

� � � � �

� � � � � � �

� � � � �

� � � � � � � �

� � � � �

� � � � � � � � � � �

� � ��

�� �

� �� � � � � �

� � � �

� � � � � � � �

�

� � � � ��

� � �� � � � � � �

�� � � � � � � � �

� � � � � � � � � ��

� � � �� � � � �

� � � � �

� � � � � �

� � � � ��

� � � � � �

�� � � � � � � �

� � � � � � � �

� � � � � � � � �

� � � � � � ��

� � � � � ��

� � � � � �

� � �

� � � � �

� � �� � �

� � � �

� � �

� � � � � � �

� � �� � � � �

� �

��������������������� �������

���������������������� ��� ����� ��� �� ����� ����������� ����� �� ����� ��������������������

� �˘�ˇ��������� ��˘� � ˇ�������� ������� �� ��� ����� ������ � ˘��ˆ�� �������� ������ ����

�� � ����� ��� � �� ����� �� ��������˙� ˝�� ����� ��������� � ˘ ����� � �� ��� ���� ��ˇ������ ˛�

�ˆ�� �������� �� � ���˘� � ˇ������� ��ˇ�� ��˘ ���� ��� �˘� � ˇ���������� ��� �����ˇ��� ��

�° �������˙��˜ ���˘ ���� ˘������� ���� ��������ˇ������ˇˇ � ���������˘ ��� ���ˇ�� ˘���� �� �

� ��������� ������� �� ����� ˘����� ����������ˇ �� �� ˇ��� ���� �����ˇ �� ������ ��

�� ��������˙� °����� ��� � ��� ����� � ��� � ���ˇ ��ˇ� �� �˘�ˇ� ˇ�� ˘� � ����� ��������

��� ��ˇ�� �� ˘�� �� ��� �� �˙�

�

�� ˜ �� ������� �� � � ����� �� �� � � � ��� ��� �� ��� ���� ������ ˘ ˇ���� ��� � � ��

�������� � � � ��ˇ���� � �� ����� ��� �� �� ��� ��ˇ�� �� � � ����� � � � �������� � ���ˇ ��ˇ�

�� �˘�ˇ� ˇ�� ˘�� ������� ��ˇ�� �˙�˜ ��������ˇ��� !�˜°� ��� � ���� �� ��������!������ ���� ��

�ˇ ��ˇ�� ������ ���ˇ�����˘�ˇ��� � ˘� �����" ��� �� ��#�� ���˘ ��� ��������$%&'($%&)�

*�ˇˇ � ��+�� ��$%&)($%&,�*-����������������+˙���

�

˜ �� �ˇ ��ˇ� ̌ �����˘�ˇ��� � � °�� ��� �� �� �ˆ�� ������� � �� ��ˇ������ ���

�ˇ ��ˇ� ˇ��� ����� � ��� ���� ˘� �� �˘�ˇ� ˇ�� ˘ �� � ����� � � �� � ����� �˘˘�ˇ��� ˘� � ��

��� �� ����� ��ˇ�� ��� ��� ���ˇ ��˙��˝ �� ������ˇ�˘�ˇ������!������ � °���� �� ��� ��

�ˆ�� ��� ˘��ˇ��������˘ ����� � ��� ˘�� ����� ��������� ��ˇ��!����� �� ˘�� �� ��� �� ��

� ��ˇ ������� � ˘�� ��� ��� �� ���� �� �� ���� �����ˇ��� ��ˇ�˙�˜ ������!�� ���˘ ��!��� �

�������� � � ˇ�����˘�!� � �� � ��� � � �� � ����ˇ�� � �� ����� � �ˇ�������� ���� � � � �� ��� ���

� ˇ��� ���� ������� ˘�� �����ˇˇ � ���� �� ���� �������ˇ�� ˙����

�

� ˜ �� ���� ��� ̌ �����˘�ˇ��� � ������ °�� � � �� ̌ �����˘�ˇ��� � ˘� � �� ��� �� ��

�ˆ�� ���������ˇˇ ��� �� ���˘˘��� �������� ˘������ˇ����� ����������ˇ���� ��˘� � ˇ������� ��

����� ��� �� �� � � � � ˇ���� �� � �� ̌ ������� �� ��� �� � � �˙� ̃ �� �° � ������ ˘�

ˇ�����˘�ˇ��� !���.˙!��ˇ ��ˇ� � �ˇ�����˘�ˇ��� �� ������ ���ˇ�����˘�ˇ��� �����ˇ ��� ���� �

˘ ���� � /�ˇ ��ˇ(ˇ��(0��� ���1�����˘�ˇ��� /˙� ˜ ��� � �� ������ ˇ�����˘�ˇ��� � � °�� °�

� ���ˆ�� �������˘ ����������ˇ���������� ��������������������� �� ���ˇ ��ˇ�ˇ��� ����˙�

˝�� ��� � � °�� °� � �� �ˆ�� ������� � � �� �����ˇ����� � � �ˇ ��ˇ� ˇ��� ��� ��� ������������

�� ���˘˘��� ������ ���� �������� ˘������ˇ������ˇ����� �����˙��������������������������������������������������������������������

�

� ˜ ��������ˇ��� � ������ ����������� �� ���#�� ����� ������� �2����� ��°�� ��� ˇ����

�˘˘ ���� ˘��2�˙�3˙ ̇2 ��� �!�4 � ��2���ˇ� �!� ����1˙0˙�4�� !�� ��������� � ��� ��°��!�������� ��

����ˇ� ���� ��� ���-˙5˙�"� ����!�����˙�0� �������� ����� ����������� �� �� ���� ˇ��

˘�� ���-˙ ̇-�� ��������� ���2���ˇ� �˙�

�

�������˝�� ��� ���� � ��� � �� � ������� ����� ���� °���� ��� ˘ � �� ���˘��� ��� � �� � ��ˇ�� ��6���!�

���� ������ ���� ��������ˇ ��ˇ ������ � ���� �� �������� ˘�� ����� ��������� ��ˇ�� ��

˘�� �� �����" ��� �� �˙�� � ���� ��˘ ������ ���� ������°��ˇ ��˙� � � �

����� ������������������������������������������������������ ������� �������������� � � �� ������ �� �ated : 31 December ,2015 ����

Commissioner

Economics and Statistics

Madhya Pradesh

i

ii

��

� �

��

�� � � � � �

� � � � � ���

�

� � � � �

� � � � � �

� �

� � � � � �

�

��� � � �� � �

� �

��� � � � � � �

�

� � �

� � � �

C O N T E N T S

���������� ��

�� �� ���

����� ��������

���� � �

˘�ˇˆˇ˙�� ��� � �����ˇˆ ̌ ˝�˛ ���° ���ˆ ����ˇˆ ˜�

��������� ! � ��� ��������� � �� ���� � ���� ����˘��ˇ�ˆ��� � ��˙�˝˛�°�˝˛�˜ � � ��!� � �˝˛�˜�˝˛�"� #$%$!���

"#�""

�������˝� ! &� � �� ��� � ��� ���ˇ�ˆ��� � �������������� ' �� ����( ����)� *�˙�˝˛�°� ˝˛�˜ � � ��!�� �˝˛�˜�˝˛�" #$%$!���

"$

�������° ! '�ˆ�����+� � ��� � �� ���,��-� ����� - ˘�� � �˙�˝˛�°�˝˛�˜� � � ��!�� � ˝˛�˜�˝˛�"� #$%$!���

"˜

���� � ��

���%ˇ ��� � �����ˇˆ ̌ �� ˘&% ˆ˛���� ˇ ' ˆ ���

'ˇ� �ˆ˙ ˆ�

"(�")

��������� ! &��ˆ ���'������� ��� � ���%.ˆ� ������ �� � � �������˘���ˇ�ˆ��� � ��˙�˝˛�°�˝˛�˜� � � ��!�� �˝˛�˜�˝˛�"� #$%$!���

$#

�������˝ ! % � � � �ˆ��ˆ ���'������� ��� ����������� ���%.ˆ� ������� ��� � �������˘��

ˇ�ˆ��� � ��˙��˝˛�°�˝˛�˜� � � ��!

$"�$*

�������° ! % � � � �ˆ��ˆ ���'������� ��� � ��� %.ˆ� ������� ��� � �������˘��ˇ�ˆ����

� ��˙��˝˛�˜�˝˛�"� #$%$!

$+�˜#

���� � ���������������

� �ˇˆ�������ˇˆ ,��� ˙ ˆ� ˜˜�˜-

���� � �.

,ˇ˙ ,� ˆ� ���ˆ� /� ˆ���˛ ˜(�-

iii

iv

ECONOMIC CLASSIFICATION OF STATE

GOVERNMENT BUDGET

(Rs. in Lakh)

2013-2014 (ACCOUNT)

507752 54936

397093

7114

581252

2588992

2798064

571564 86137

698587

2877

932756

4383457

3298020

2014-2015 (R.E.)

Current Consumption Expenditure

Current Transfer Payment

Gross Capital Formation

Net Purchase of Land

Capital Transfer

Financial Assets

Loans and Advances

v

PURPOSE CLASSIFICATION OF STATE

GOVERNMENT BUDGET (Rs. in Lakh)

2013-2014 (ACCOUNT)

58224

0

2101930

68295

929663 925690 297315

1435255

29341

1089490

0

3022614

88189

1743327 1187604

484816

1840604

33516 1390196

182532

2014-2015 (R.E.) General Public Services Defence Education Affairs and Services Health Affaris and Services Welfare Affairs and Services Housing Community Amenities Affairs and Services Cultural, Recreaqtional, Religious Affairs and Services Economic Affairs and Services Environmental Protection Other Sevices

vi

iv

ECONOMIC CLASSIFICATION OF STATE

GOVERNMENT BUDGET

(Rs. in Lakh)

25

88992

581252

7114

397

093

54936

507752

932

756

2877

69858

7

86137

57

1564

438

3457

Current

Transfer

Payment

Gross Capital

Formation

Net Purchase

of Land

Capital

Transfer

Financial

Assets

Loans and

Advances

2013-2014 (ACCOUNT)

2014-2015 (R.E.)

33516

v

PURPOSE CLASSIFICATION OF STATE

GOVERNMENT BUDGET

(Rs. In Lakh)

1435255

297315

925690

929663

68295

2101930

0 58224

1840604

484816

1187604

1743327

88189

3022614

0

182532

Educatio

n A

ffairs a

nd

Serv

ices

Health

Affaris a

nd

Serv

ices

Welfa

re A

ffairs a

nd

Serv

ices

Housin

g C

om

munity

Am

eniti

es A

ffairs a

nd

Serv

ices

Cultu

ral,

Recre

aqtio

nal,

Relig

ious A

ffairs a

nd

Serv

ices

Econom

ic A

ffairs a

nd

Serv

ices

Environm

enta

l

Pro

tectio

n

Oth

er

Sevic

es

014 (ACCOUNT)

015 (R.E.)

�����

P A R T - I

E c o n o m i c C l a s s i f i c a t i o n o f

B u d g e t a r y T r a n s a c t i o n s

���

��������

�����

PART-I

ECONOMIC CLASSIFICATION OF BUDGETARY TRANSACTIONS

The Annual Financial Statement and the Demand for Grant in a Government Budget are drawn up in accordance with the provision under Article 202 (1) of the Constitution of India and presented to the State Legislature every year in order to secure legislative control. The expenditure in the Government Budget is generally classified department-wise and presented in the form of ‘ Demand for Grant ` for various departments. Each demand gives gross expenditure and various recoveries from other Governments or State Departments and various organisations. The recoveries are deducted from the gross expenditure to get net expenditure which are shown in the Financial Statement. Each demand specifies various items of expenditure, viz., pay of officers, pay of establishment, contingencies, etc., which are grouped under major and minor heads of accounts of expenditure.

The budget so presented reveals mere financial transactions and not the economic and social significance of the transactions. For instance, from the study of budget documents as they are, it is not possible to get a clear idea of capital formation out of budgetary resources, savings of the State Government, Government’s contribution to the generation of State Domestic Product, etc. The Government’s transactions are significant only in terms of such items in order to assess the impact of operations of the Government on the economy for purpose of formulation of correct monetary and fiscal policies and hence the need for economic classification of the State Government Budget.

The system of classification adopted here is based on a series of distinctions useful for analysing their economic impact on the rest of the economy. The term `rest of the economy’ refers to all entities other than the State Government and includes the Central Government, other State Governments, local bodies, statutory corporations or companies and individuals. `Current transactions’ are distinguished from capital transactions and under both, transactions in goods and services are separated from transfers. The current transactions of Government Administration are distinguished from the current operations of Departmental Commercial Undertakings as current expenditure of the former on wages and salaries and goods and services are final outlays but those of the latter are intermediate expenditure, such as cost of raw materials, fuels, etc. In other words, such expenditure represent expenses of production and not expenditure of final goods and services. Purely financial transactions are again separated from transactions on goods and services and transfers. The Economic Classification of the State Government Budget is presented in three Standard Tables as recommended by the Committee on Regional Accounts. These are :

TABLE - 1 : INCOME AND OUTLAY ACCOUNT OF ADMINISTRATIVE DEPARTMENTS

TABLE - 2 : PRODUCTION ACCOUNT OF DEPARTMENTAL COMMERCIAL UNDERTAKINGS

TABLE - 3 : CAPITAL FINANCE ACCOUNT OF GENERAL GOVERNMENT.

���

�����

The following is briefly a description of the derivation and rationale of each of these tables.

TABLE - 1 : INCOME AND OUTLAY ACCOUNT OF

ADMINISTRATIVE DEPARTMENTS

This account deals with the current revenue and expenditure of government administrative departments. All departments, other than those which are commercial in nature, are considered as administrative for the purpose of Economic Classification. The current expenditure of administrative departments consists of final outlays of the government on current account which represents government’s current consumption. The final outlays are made of purchase of goods and services and wages and salaries payments. Besides final outlays, government makes transfer payments, i.e., interests, grants, subsidies, scholarships, etc., to the rest of the economy which are added indirectly to the disposable income of the community. To meet these current expenditures, government appropriates a part of the income of community through a variety of taxes, miscellaneous fees, etc., accruing in the course of administration. In addition, government has an investment income from property and entrepreneurship and also receives revenue grants, etc. from the Union Government. The excess of current receipts over current expenditure denotes the `Saving’ of the government administration, available for `domestic capital formation’. Some of the items included in this account are explained below :

Compensation of employees:- This item comprises of remuneration of general government employees, such as pay of officers, pay of establishment and allowances and honoraria other than travelling and daily allowances. Wages paid to casual labour have also been taken as wages & salaries. Also included are pension payments to government employees of administrative departments.

Commodities and Services:- This item includes all expenditure under contingency, such as office supplies, rent, rates and taxes, fuel and light, printing and stationery, travel expenses, telephone and telegraph charges and other items for current operations less sales by general government of goods and services to enterprises and households. All expenditure on current repairs and maintenance is included here.

Interest :- Interest comprises interest on public debt and other obligations other than that on commercial debt which should be included in Table-2 - Production Account of Departmental Commercial Undertakings. But separate information of interest on commercial debt is not available in the budget document. Therefore, whole interest paid has been shown in Table-1.

Subsidies :- Subsidies include all grants on current account which private industries receive from the government. These may take the form of direct payments to producers or differentials between the buying and selling prices of government trading organisations. Thus, subsidies are transfers which are additions to the income of the producers from current production. The grants may, for example be based on the amount of value of commodities produced, exported or consumed, the labour or land employed in production, or the manner in which production is organised and carried on. Transfers by the public authorities to private industries for investment purpose or to cover destruction, damage and other losses in capital and working assets are classified as `CAPITAL TRANSFERS’ rather than subsidies. Current grants made to the private non-profit institutions serving households are not to be considered as subsidies. Such payments will be classified as purchase of goods and services or current transfers by general government depending on the circumstances and conditions of a given payment. Nor are grants to households classified as

���

�����

subsidies. The value of coupons made available by government agencies to specific groups of the population to enable them to obtain goods at prices lower than the current market prices are classified as current transfers to households. Under certain circumstances subsidies include the grants made by the government to public corporations for compensation of losses, i.e., negative operating surplus, and in connection with the losses of departmental commercial undertakings. Rebate on the sale of handloom cloth, loss on the sale of fertilizers, improved seeds, pesticides and agricultural implements, loss suffered by co-operative societies, etc., are treated as subsidies. The losses accrued by the departmental undertakings are treated as imputed subsidy.

Current Transfers:- Current transfers include grants to local bodies and transfers to households such as pensions for distinguished and meritorious services, territorial and political pensions, old age pensions, family allowances, prizes, gratuitous relief to famine stricken people, awards and other miscellaneous compensations and contributions, etc., to private non- profit institutions.

Saving on Current Account:- The balancing item on the current account of government administration represents the saving of this sector, i.e., surplus of current receipts over current expenditure.

Income from Property and Entrepreneurship :- This flow records the income receivable by the State Government from departmental commercial undertakings as well as the net rent, interest and dividends accruing to it from ownership of buildings and financial assets.

Direct Taxes :- The following taxes have been taken as direct taxes:

(i) Corporation tax (ii) Taxes on income (iii) Other taxes on income and expenditure (iv) Land revenue (v) Estate duty (According to System of National Accounts-U.N. this is included

under capital transfer but in our classification this has been treated as direct tax)

(vi) Taxes on immovable property other than agricultural land.

Indirect Taxes :- Indirect taxes are defined as taxes assessed on producers that are chargeable to the cost of goods and services produced or sold. They include:

(i) Customs (ii) Stamps & registration fees (iii) Union & State excise (iv ) Sales Tax (v ) Service Tax (vi) Taxes on vehicles (vii) Entertainment Tax (viiii) Taxes on goods & passengers (ix) Taxes and duties on electricity (x) Fees realised under Factories Act, fees for stamping weights and measures,

etc.

Miscellaneous Receipts:- These receipts are in the nature of fees, fines and forfeitures.

Revenue Grants, Contributions, etc.:- Grants from Government of India have been taken

���

��

TABLE - 2 : PRODUCTION ACCOUNT OF DEPARTMENTAL

COMMERCIAL UNDERTAKINGS

The Departmental Commercial Undertakings may be defined as government agencies producing goods and services that are not provided free of charge. The operations of departmental commercial undertakings, which figure in the budget, are of the nature of entrepreneurial activities of government. Current expenditure of these undertakings, like working expenses of productive enterprises constitute intermediate expenditure that enter into prices of goods and services as these are sold to other sectors of economy. Therefore, these are different in character from final outlays by administrative departments. Likewise, sale proceeds of commercial undertakings are different from the receipts (e.g. taxes) of purely administrative departments which have no income of their own and draw upon incomes of other sectors to meet out their expenditure. Other related characteristics are :

(i) Departmental Commercial Undertakings are subject to market forces, i.e., demand and supply.

(ii) The activities of such undertakings are subordinate to legislative control and are owned, run and managed by the government.

(ii) The intention to make profit is not the essential characteristic and the activities of an undertaking may be carried on deliberately at a loss.

(iv) The operations of the undertakings usually involve the use of the expensive capital equipment and the holding of stock which may be subject to large fluctuations and the provision for depreciation may, therefore, be a significant element in the total cost of operations. Independent statutory Corporations and Boards set up by the State Government are excluded from the purview of this table. In this study, the following have been considered under departmental commercial undertakings:

(a) Forests (b) Irrigation (c) Milk supply

(d) Printing Press (Printing, storage and distribution of forms and Govt. Presses ). The items under this head are self explanatory. The expenditure part of the said account spells out compensation of employees (i.e., wages and salaries), commodities and services (i.e., purchase of raw materials, expenditure on repairs and maintenance, etc.), interest, consumption of fixed capital and profits. The receipts part shows their gross sale proceeds.

��

�����

TABLE-3 : CAPITAL FINANCE ACCOUNT OF THE

GENERAL GOVERNMENT

This account is concerned with the total capital formation by government administration and departmental commercial undertakings together with capital transfer payments which are mostly for assisting capital formation. The capital expenditure of government administration and departmental commercial undertakings have been given separately whereas the sources of finance are common to both.

Change in Stocks:- Change in stocks represent the value of the physical change in raw materials, work-in- progress (other than the work-in-progress in buildings which are included in fixed capital formation) and finished products, which are held by commercial enterprises and in government stockpiles.

Gross Fixed Capital Formation:- Gross capital formation represents the gross value of goods which are added to the domestic capital stocks of the State. It comprises both expenditure on the acquisition of fixed assets and the value of physical change in stocks. The gross fixed capital formation has been classified into buildings and other construction and machinery and equipment. These terms may be specified as:

Buildings and other Construction:- Buildings include all expenditure on new construction and major alterations to residential and non-residential buildings including the value of the change in work-in-progress. Other construction includes mostly expenditure on construction of roads and bridges and works on power and irrigation projects, flood control, forest clearance, land reclamation, water supply and sanitation.

Machinery and Equipment:- This item includes expenditure incurred on the purchase of various equipment such as buses, jeeps, trucks, tractors for road haulage, power generating machinery, agricultural machinery and implements, office furniture, machinery and equipment and instruments used by professional men. Under this head the expenditure shown against renewals and replacements refers mainly to departmental commercial undertakings.

Net Purchase of Physical Assets:- The major component here is purchase of land.

Capital Transfers:- Capital transfers cover grants to finance the construction of buildings, etc. and for purchase of machinery and equipment for public works, water supply and sewage disposal schemes, etc. Capital transfers are intended to assist capital formation in other sectors of economy.

Receipts on Capital Account :- This part deals with the financing of capital formation and the sources for the same are discussed as under :

Saving :- The saving on current account is directly taken from Table -1.

���

��

Net Borrowing:- Items like internal debt, small savings, provident fund, etc. are included here.

Other Liabilities:- All investments in the share capital of statutory corporations and co-operative societies are classified as financial assets and are shown against other liabilities as a negative figure. Also included are the extra-budgetary receipts like loans from Government of India, contingency fund, deposits and advances, suspense, remittances and cash balances. Besides these, there are some funds maintained by the government like famine relief fund, road fund, etc. which are also covered here.

The three tables as explained above for Madhya Pradesh State Government budget for the years 2013-2014 (Accounts) and 2014-2015 (R.E.) are presented in the following pages.

��

��

TABLES

TABLE 1 : Income and outlay account of Administrative Departments.

TABLE 2 : Production account of Departmental Commercial Undertakings.

TABLE 3 : Capital finance account of the General Government.

��

����

��� ��

TABLE –1 INCOME AND OUTLAY ACCOUNT OF ADMINISTRATIVE DEPARTMENTS

(Rs.Lakh)

Items YEARS

2013-2014

(Accounts)

2014-2015

(R.E.)

1 2 3

Expenditure

1. Consumption expenditure

1.1 Compensation of employees

1.1.1 Wages & salaries, etc

1.1.2 Pensions

1.2 Net purchase of commodities and

services

1.2.1 Purchases

1.2.2 Maintenance & repairs

1.2.3 Less sales

2. Net interest paid

2.1 To public authorities

(a) Centre

(b) States

(c) Local bodies

2.2 To foreign

2.3 To others

3. Subsidies

4. Current transfers

4.1 To public authorities

(a) Centre

(b) States

(c) Local bodies

4.2 To rest of the world

4.3 To other sectors

5. Savings

2798064

2354417

1799466

554951

443647

527894

146151

230398

639132

63777

-

-

-

575355

404643

2184349

-

-

1403648

-

780701

1170841

3298020

2778070

2185252

592818

519950

690976

172172

343198

687487

72981

-

-

-

614506

502518

3880940

-

-

2256734

-

1624206

1566805

6. Total expenditure 7197029 9935770

Contd...

� ��

��������

TABLE -1

INCOME AND OUTLAY ACCOUNT OF ADMINISTRATIVE DEPARTMENTS

(Rs.Lakh)

Items YEARS

2013-2014

(Accounts)

2014-2015

(R.E.)

1 2 3

Receipts

7.Income from Entrepreneurship & property

7.1 Profits102389

7.2 Income from property

7.2.1 Net interest receipts

7.2.1.1 From public authority

(a) Centre

(b) States

(c) Local authorities

7.2.1.2 From foreign

7.2.1.3 From other sectors

7.2.2 Other property receipts

8. Direct taxes

8.1 Corporation Tax

8.2 Land revenue

8.3 Other taxes

9. Indirect taxes

9.1 Customs

9.2 Excise

9.3 Sales tax

9.4 Stamps & registration

9.5 Service Tax

9.6 Other taxes and duties

10. Miscellaneous receipts

11. Revenue grants from other governments

(a) Centre

(b) States

12. Total receipts

471775

102389

369386

31785

-

-

-

-

-

31785

337601

1376121

763946

12834

599341

4147232

370624

783109

1664985

328847

370060

629607

24219

1177682

1177682

-

7197029

809080

468085

340995

34965

-

-

-

-

-

34965

306030

1687473

922454

56866

708153

4506259

427856

551075

1950000

383047

485254

709027

78491

2854467

2854467

-

9935770

����

��������

TABLE-2

PRODUCTION ACCOUNT OF DEPARTMENTAL COMMERCIAL UNDERTAKINGS

(Rs.Lakh)

Items YEARS

2013-2014

(Accounts)

2014-2015

(R.E.)

1 2 3

Expenditure

1. Purchase of commodities & services (including maintenance)

2. Compensation of employees

3. Interest

4. Consumption of fixed capital

5. Profits

6. Total expenditure

Receipts

7. Sales

8. Imputed subsidy

9. Total receipts

51940

193234

-

20

102389

347583

246725

100858

347583

36152

224628

-

48

468085

728913

645917

82996

728913

����

��������

TABLE-3

CAPITAL FINANCE ACCOUNT OF THE GENERAL GOVERNMENT (Rs.Lakh)

Items YEARS

2013-2014

(Accounts)

2014-2015

(R.E.)

1 2 3

Expenditure

1. Change in stock

1.1 Administrative departments

1.2 Departmental enterprises

2. Gross fixed capital formation

(new)

2.1 Administrative departments

2.2 Departmental enterprises

3. Net purchase of physical assets

3.1 Second hand assets

(a) Administrative departments

(b) Departmental enterprises

3.2 Land

(a) Administrative departments

(b) Departmental enterprises

4. Capital transfers

4.1 To other governments

4.2 To rest of the world

4.3 To other sectors

5. Total expenditure

Receipts

6. Savings

7. Consumption of fixed capital

8. Capital transfers

8.1 From other governments

8.2 From rest of the world

9. Net borrowing

9.1 At home

9.2 Abroad

10. Other liabilities

10.1 Extra-budgetary receipts

10.2 Less - net purchase of Financial assets

11. Total receipts

(-)215

949

(-)1164

1044781

580303

464478

7114

-

-

-

7114

7114

-

397093

14934

-

382159

1448773

1170841

20

-

-

-

603352

603352

-

(-)325440

(-)270504

54936

1448773

(-)178

2

(-)180

1415673

932754

482919

2877

-

-

-

2877

2877

-

698587

53089

-

645498

2116959

1566805

48

-

-

-

1016531

1016531

-

(-)466425

(-)380288

86137

2116959

����

������������

��������

P A R T - II

P u r p o s e C l a s s i f i c a t i o n o f t h e

E x p e n d i t u r e o f G e n e r a l

G o v e r n m e n t

����

��� ��� ��

��������

PART -II

PURPOSE CLASSIFICATION OF THE EXPENDITURE OF

GENERAL GOVERNMENT

Introduction :-

The Government expenditure can be classified in accordance with [i] the economic character of the expenditure like current expenditure, capital formation, loans etc., and [ii] the purpose it is likely to serve, such as health, education, defence, etc. The former is known as economic classification and the latter is termed as the purpose classification. These two schemes are combined to form economic-cum-purpose classification.

This type of classification shows how expenditure for a particular purpose, say health, is divided between economic categories and it also shows how expenditure in a particular economic category, say capital formation is allocated to different purpose or types of public services provided. Economic-cum-purpose classification, therefore, serves as a very good guide to the policy makers for planning expenditure in the best possible manner to attain social and economic objectives of development.

The purpose of the government expenditure might be of two types (i) long term and (ii) short term. Long term expenditure might be aimed at tackling the problem of unemployment, economic development of the country and to bring about certain fundamental changes in the structure of the economy. The short term expenditure relate to immediate objectives of expenditure incurred in regard to health, defence, education, social welfare, economic services, etc. The aim of the purpose classification is, therefore, to classify expenditure in accordance with the immediate or short term social needs.

Coverage and scope :-

The purpose classification of the State Government Budget relates only to general government expenditure excluding departmental commercial enterprises. Financial investment of the government in commercial activities in terms of purchase of shares and debentures, etc., are included. Similarly, grants and loans given to commercial organisations, non-government institutions or the individuals are also included. It may, however, be pointed out that the repayment of loans are excluded. The receipts of the government do not come into the picture. However, some of the receipts like sales of goods and services produced in the government sector are taken into account in working out the expenditure on net purchase of goods and services by the general government.

Classification :-

This classification has been discussed under the following heads :

(a) Need for purpose classification, (b) Major categories, (c) Principles of classification adopted.

����

��� ��

(a) Need for purpose classification:-Entire government expenditures are recorded annually in the budget documents issued by State Government. The arrangement in regard to the presentation of the expenditure in the budgets is generally in keeping with the requirements of the legislative control, administrative accountability and auditing. The budgets are also presented under a few standard account heads of the functional character of the expenditure such as education, health, agriculture, industry, defence, etc. The expenditure shown under these account heads are not strictly in accordance with the principles of purpose classification. For instance, expenditure on medical colleges and other educational institutions are generally shown under account head medical and so on. Further, there are various account heads which pertain to so many purpose categories, such as public works department, community development, national extension services, cooperation, etc. The expenditure under these heads are not specific to any purpose categories. It becomes, therefore, essential to classify these heads of expenditure afresh.

(b) Major categories:-The purpose classification attempted for the present study is in conformity with the U.N. recommendations. U.N. has recommended classification in fourteen major categories:

(i) General Public Services (ii) Defence Affairs and Services (iii) Public Order and Safety Affairs (iv) Education Affairs and Services (v) Health Affairs and Services (vi) Social Security and Welfare Services (vii) Housing and Community Amenities, Affairs and Services (viii) Recreational, Cultural and Religious Affairs and Services (ix) Fuel and Energy Affairs and Services (x) Agricultural, Forestry, fishing and Hunting Affairs and Services (xi) Mining and Mineral Resource Affairs and Services Other than Fuels,

Manufacturing Affairs and Services and Construction Affairs and Services. (xii) Transportation and Communication Affairs and Services (xiii) Other Economic Affairs and Services (xiv) Expenditures not Classified by Major Group

We have adopted this classification for our purpose here. These major heads have been split into minor groups. In the present study we have some adjustments in the minor categories. Atomic energy has been shown as a miner head, which is not given in the U.N. Classification. Further a new major head "Environmental Protection has also been included. The whole list of major and minor purpose categories is as under:

List of purpose categories 1. General public services

1.1 General administration, external affairs, public order and safety 1.2 General research

2. Defence 3. Education Affairs And Services

3.1 Administration, Regulation And Research 3.2 Schools, Universities And Institutions Including Subsidiary

Services

� ��

��� ��

4. Health Affairs And Services (Allopathic, Ayurvadic, HomeoPathic, Unani And others ) 4.1 Administration, Regulation And Research 4.2 Hospitals, Clinics And Other Health Services

5. Welfare Affairs And Services 5.1 Social Security Affairs And Services 5.2 Social Welfare Services

6. Housing And Community, Amenities Affairs And Services 7. Cultural, Recreational And Religious Affairs And Services 8. Economic Affairs And Services

8.1 General Administration, Regulation And Research 8.2 Agriculture, Forestry, Fishing And Hunting 8.3 Mining, Manufacturing And Construction 8.4 Electricity, Gas, Steam, And Atomic Energy 8.5 Drinking Water Supply 8.6 Transportation And Communication 8.7 Other Economic Services

9. Environmental Protection 10 Other Services

(c) Principles of classification adopted:-All the items of expenditure are grouped under the appropriate categories regardless of their manner of presentation in the budget. Items which relate to more than one purpose class are first disintegrated in accordance with the details that are given in the budget, and then classified into appropriate purpose categories. In the absence of any details, either the major function of the expenditure is considered as the purpose or it is disintegrated into related purpose categories applying some suitable norms. In case of grants, loans and advances to private institutions or to individuals, if the purpose of utilisation is not specifically mentioned, classification is done on the basis of the main function of the institutions which are receiving the grants, loans and advances. In many cases neither the name of the organisations receiving the grants, loans and advances nor the purpose of utilisation is given. In such cases the classification is done on the basis of account heads under which these expenditure have been shown.

Facilities provided to employees like residential housing facility, free or subsidised medical aid, etc., are classified by the nature of the facility and not by the functional character of the office providing facilities. Accordingly loans and advances to employees for construction of houses, purchase of motor car, etc., are classified according to the types of the services likely to be obtained by the utilisation of the loans.

Pension and other retirement benefits (including employees family pension schemes) are distributed to all the purpose categories in proportion to the amount of wages and salaries attributable to different categories. The welfare pensions like old age pensions, pensions to political sufferers or to freedom fighters, etc., are however, classified under the welfare services.

Following tables give purpose classification of Madhya Pradesh State Government Budget for the years 2013-2014 (Accounts) and 2014-2015 (R.E.) (Table -1) and economic-cum-purpose classification separately for these years (Tables - 2 & 3).

� ��

����

��� ��

TABLE-1

PURPOSE CLASSIFICATION OF EXPENDITURE

OF ADMINISTRATIVE DEPARTMENTS (Rs.Lakh)

Purpose classification

2013-2014

(Accounts)

Percen-

tage

distri-

bution

2014-2015

(R.E.)

Percen-

tage

distri-

bution

Percentage

increase or

decrease in

2014-2015 Over

2013-2014 (A/C )

1 2 3 4 5 6

1. General Public Services 1089490 15.71 1390196 13.94 + 27.6

1.1 General administration, external affairs, public

order & safety

1074883 15.50 1367901 13.72 + 27.3

1.2 General research 14607 0.21 22295 0.22 + 52.6

2. Defence 29341 0.42 33516 0.34 + 14.2

3. Education Affairs and

Services

1435255 20.70 1840604 18.46 + 28.2

3.1 Administration, regulation

and research

14118 0.20 17545 0.18 + 24.3

3.2 Schools, universities

and institutions including

subsidiary services

1421138 20.49 1823059 18.28 + 28.3

4. Health Affairs and Services 297315 4.29 484816 4.86 + 63.1

4.1 Administration, regulation

and research

15254 0.22 15240 0.15 - 0.1

4.2 Hospitals, clinics & other

health services

282061 4.07 469575 4.71 + 66.5

5. Welfare, Affairs and Services 925690 13.35 1187604 11.91 + 28.3

5.1 Social Security Affairs &

services

1865 0.03 2917 0.03 + 56.4

5.2 Social Welfare Services 923825 13.32 1184687 11.88 + 28.2

6. Housing and Community

Amenities Affairs and Services

929663 13.40 1743327 17.48 + 87.5

7. Cultural, Recreational &

Religious Services

68295 0.98 88189 0.88 + 29.1

8. Economic Services 2101930 30.31 3022614 30.31 + 43.8

8.1 General administration,

regulation & research

20714 0.30 185986 1.86 + 797.9

8.2 Agriculture, forestry,

fishing & hunting

465393 6.71 648600 6.50 + 39.4

8.3 Mining, manufacturing

& construction

574336 8.28 661038 6.63 + 15.1

8.4 Electricity, gas, steam

Atomic Energy

334067 4.82 501389 5.03 + 50.1

8.5 Drinking Water Supply 167244 2.41 365651 3.67 + 118.6

8.6 Transportation and communication

461157 6.65 548911 5.50 + 19.0

8.7 Other economic services 79022 1.14 111039 1.11 + 40.5

9 Environmental Protection 0 0.00 0 0.00 0 0

10. Other Services 58224 0.84 182532 1.83 + 213.5

TOTAL 6935203 100 9973398 100 + 43.8

� ��

��������

TABLE-2 ECONOMIC-CUM-PURPOSE CLASSIFICATION OF EXPENDITURE

OF ADMINISTRATIVE DEPARTMENTS 2013-2014 (ACCOUNTS) (Rs.Lakh)

Economic Classification Current expenditure

Consumption expenditure

Wages and Commodities Less - Total Purpose Classification salaries and services Sales Consumption

including expenditure pension

1 2 3 4 5

1. General Public Services 687504 225696 12454 900746

1.1 General administration, external affairs, public

order & safety

687400 218296 7662 898034

1.2 General research 104 7400 4792 2712

2. Defence 27997 960 - 28957

3. Education Affairs and

Services

901607 25340 200849 726098

3.1 Administration, regulation

and research

13733 243 - 13976

3.2 Schools, universities

and institutions including

subsidiary services

887875 25097 200849 712123

4. Health Affairs and Services 208003 39714 5776 241941

4.1 Administration, regulation

and research

7221 7137 - 14358

4.2 Hospitals, clinics & other

health services

200782 32577 5776 227583

5. Welfare, Affairs and Services 155216 200266 4238 351244

5.1 Social Security Affairs &

services

251 152 - 403

5.2 Social Welfare Services 154965 200114 4238 350841

6. Housing & Community

Amenities Affairs and

Services

51854 12393 - 64247

7. Cultural, Recreational &

Religious Services

9234 10852 - 20086

8. Economic Services 312954 158817 6258 465513

8.1 General administration,

regulation & research

18219 1580 - 19799

8.2 Agriculture, forestry,

fishing & hunting

158319 22643 3640 177322

8.3 Mining, manufacturing

& construction

15190 6305 361 21134

8.4 Electricity, gas, steam

Atomic Energy

90 1190 - 1280

8.5 Drinking Water Supply 56515 7525 1033 63007

8.6 Transportation and

communication

54456 119332 - 173788

8.7 Other economic services 10166 242 1224 9184

9 Environmental Protection 0 0 - 0

10. Other Services 48 7 823 (-)768

TOTAL 2354417 674045 230398 2798064

Contd.....

����

��������

TABLE-2 ECONOMIC-CUM-PURPOSE CLASSIFICATION OF EXPENDITURE

OF ADMINISTRATIVE DEPARTMENTS 2013-2014 (ACCOUNTS) (Rs.Lakh)

Economic Classification

Purpose Classification

Current expenditure Total current expend-

iture (5+6+9)

Transfer payment

Subsidies Transfer to local bodies

To others Total transfer

payments (7+8)

1 6 7 8 9 10

1. General Public Services

1.1 General administration, external affairs, public

order & safety

1.2 General research

2. Defence

3. Education Affairs and Services

3.1 Administration, regulation

and research

3.2 Schools, universities

and institutions including

subsidiary services

4. Health Affairs and Services

4.1 Administration, regulation

and research

4.2 Hospitals, clinics & other

health services

5. Welfare, Affairs and Services

5.1 Social Security Affairs &

services

5.2 Social Welfare Services

6. Housing & Community

Amenities Affairs and Services

7. Cultural, Recreational &

Religious Services

8. Economic Services

8.1 General administration,

regulation & research

8.2 Agriculture, forestry,

fishing & hunting

8.3 Mining, manufacturing

& construction

8.4 Electricity, gas, steam

Atomic Energy

8.5 Drinking Water Supply

8.6 Transportation and

communication

8.7 Other economic services

9 Environmental Protection

10. Other Services

TOTAL

-

-

-

-

7881

-

7881

-

-

-

168970

-

168970

-

4847

222945

-

139855

29902

18284

-

-

34904

-

-

404643

121531

121531

-

-

387294

-

387294

-

-

-

88332

758

87574

745495

17

60979

-

10530

30323

-

19815

311

-

-

--

1403648

25449

16261

9188

250

293664

13

293651

41458

19

41439

241551

-

241551

11092

28936

79309

244

58992

3686

10314

3141

24

2910

-

58992

780701

146980

137792

9188

250

680958

13

680945

41458

19

41439

329883

758

329125

756587

28953

140288

244

69522

34009

10314

22956

333

2910

-

58992

2184349

1047726

1035826

11900

29207

1414937

13989

1400949

283399

14377

269022

850097

1161

848936

820834

53886

828746

20043

386699

85045

29878

85963

174123

46998

-

58224

5387056

Contd...

����

��������

TABLE-2

ECONOMIC-CUM-PURPOSE CLASSIFICATION OF EXPENDITURE OF ADMINISTRATIVE DEPARTMENTS 2013-2014 (ACCOUNTS)

(Rs.Lakh)

Economic Classification

Purpose Classification

Capital expenditure

Gross Capital Formation

Buildings and other

Construction s

Machinery and

equipment

Change in stock

Gross capital formation (11+12+13)

1 11 12 13 14

1. General Public Services 1.1 General administration,

external affairs, public order & safety

1.2 General research 2. Defence

3. Education Affairs and Services 3.1 Administration, regulation

and research 3.2 Schools, universities

and institutions including subsidiary services

4. Health Affairs and Services 4.1 Administration, regulation

and research 4.2 Hospitals, clinics & other

health services 5. Welfare Affairs and Services

5.1 Social Security Affairs & services

5.2 Social Welfare Services

6. Housing & Community

Amenities Affairs and Services

7. Cultural, Recreational &

Religious Services

8. Economic Services 8.1 General administration,

regulation & research 8.2 Agriculture, forestry,

fishing & hunting 8.3 Mining, manufacturing

& construction 8.4 Electricity, gas, steam

Atomic Energy

8.5 Drinking Water Supply 8.6 Transportation and

communication 8.7 Other economic services

9 Environmental Protection

10. Other Services

TOTAL

21164 20447

717 134

12928 -

12928

10192 82

10110

70960 704

70256

48941

8884

382914 316

28282

7569

14

68159 278574

---

-

556117

13892 13892

--

3561 129

3432

3724 795

2929

654 -

654

12

497

1846 355

874

276

-

222 23

96 -

-

24186

949 949

--

--

-

-

-

-

-

-

-

-

-

--

-

-

-

--

--

-

949

36005 35288

717 134

16489 129

16360

13916 877

13039

71614 704

70910

48953

9381

384760 671

29156

7845

14

68381 278597

96 --

-

581252

Contd....

����

��������

TABLE-2

ECONOMIC-CUM-PURPOSE CLASSIFICATION OF EXPENDITURE

OF ADMINISTRATIVE DEPARTMENTS 2013-2014 (ACCOUNTS)

(Rs.Lakh)

Economic Classification

Purpose Classification

Capital expenditure

Purchase

of assets -

land

Less-sale

of assets-

land

Capital Transfers

To local

bodies

To others

1 15 16 17 18

1. General Public Services

1.1 General administration, external affairs, public order & safety

1.2 General research

2. Defence

3. Education Affairs and Services 3.1 Administration, regulation

and research 3.2 Schools, universities

and institutions including subsidiary services

4. Health Affairs and Services 4.1 Administration, regulation

and research 4.2 Hospitals, clinics & other

health services

5. Welfare, Affairs and Services 5.1 Social Security Affairs &

services 5.2 Social Welfare Services

6. Housing and Community

Amenities Affairs and Services

7. Cultural, Recreational &

Religious Services

8. Economic Services 8.1 General administration,

regulation & research 8.2 Agriculture, forestry,

fishing & hunting 8.3 Mining, manufacturing

& construction 8.4 Electricity, gas, steam

Atomic Energy 8.5 Drinking Water Supply

8.6 Transportation and communication

8.7 Other economic services

9 Environmental Protection

10. Other Services

TOTAL

800

800

-

-

--

-

-

-

-

-

-

-

75

-

6239

-

202

-

-

-6037

-

-

-

7114

12868

-

2066

-

-

-

-

2066

-

-

-

-

14934

4324

2334

1990

-

2829 -

2829

--

-

1047 -

1047

42955

5028

325976

-

5464

2903

304175

10834

2400

200

--

382159

Contd.....

����

��������

TABLE-2

ECONOMIC-CUM-PURPOSE CLASSIFICATION OF EXPENDITURE

OF ADMINISTRATIVE DEPARTMENTS 2013-2014 (ACCOUNTS)

(Rs.Lakh)

Economic Classification

Purpose Classification

Capital expenditure Grand

Total

(10+22) Finan-

cial

Assets

Loans and

advances

Total capital

expenditure

(14 to 21)To local

bodies

To

others

1 19 20 21 22 23

1. General Public Services 1.1 General administration,

external affairs, public order & safety

1.2 General research

2. Defence

3. Education Affairs and

Services 3.1 Administration, regulation

and research 3.2 Schools, universities

and institutions including subsidiary services

4. Health Affairs and Services 4.1 Administration, regulation

and research 4.2 Hospitals, clinics & other

health services

5. Welfare, Affairs and

Services 5.1 Social Security Affairs &

services 5.2 Social Welfare Services

6. Housing and Community

Amenities Affairs and

Services

7. Cultural, Recreational &

Religious Services

8. Economic Services 8.1 General administration,

regulation & research 8.2 Agriculture, forestry,

fishing & hunting

8.3 Mining, manufacturing & construction

8.4 Electricity, gas, steam Atomic Energy

8.5 Drinking Water Supply 8.6 Transportation and

communication 8.7 other economic services

9 Environment protection

10 Other Services

TOTAL

--

--

-

-

-

-

-

-

1150

-

1150 -

-

53786 -

9072

43407

-

--

1307

-

-

54936

--

--

-

-

-

-

-

-

685

-

--

-

-

-

--

-

-

-

685

635 635

--

1000

-

1000

-

-

-

1782

-

1782 3293

-

500357 -

34800

435136

-

--

30421

-

-

507067

41764 39057

2707

134

20318

129

20189

13916 877

13039

75593

704

74889 108829

14409

1273184 671

78694

489291

304189

81281 287034

32024

-

-

1548147

1089490 1074883

14607

29341

1435255

14118

1421138

297315 15254

282061

925690

1865

923825 929663

68295

2101930 20714

465393

574336

334067

167244 461157

79022

-

58224

6935203

����

��� ��

TABLE-3 ECONOMIC-CUM-PURPOSE CLASSIFICATION OF EXPENDITURE

OF ADMINISTRATIVE DEPARTMENTS 2014-2015 (RE) (Rs.Lakh))

Economic Classification

Purpose Classification

Current Expenditure

Consumption Expenditure Wages and

salaries including pension

Commodities and Services

Less – Sales

Total Consumption Expenditure

1 2 3 4 5

1. General Public Services

1.1 General administration,

external affairs, public

order & safety

1.2 General research

2. Defence

3. Education Affairs and Services

3.1 Administration, regulation

and research

3.2 Schools, universities

and institutions including

subsidiary services

4. Health Affairs and Services

4.1 Administration, regulation

and research

4.2 Hospitals, clinics & other

health services

5. Welfare, Affairs and

Services

5.1 Social Security Affairs &

services

5.2 Social Welfare Services

6. Housing and Community

Amenities Affairs and

Services

7. Cultural, Recreational &

Religious Services

8. Economic Services

8.1 General administration,

regulation & research

8.2 Agriculture, forestry,

fishing & hunting

8.3 Mining, manufacturing

& construction

8.4 Electricity, gas, steam

Atomic Energy

8.5 Drinking Water Supply

8.6 Transportation and

communication

8.7 Other economic services

9 Environmental Protection

10. Other Services

TOTAL

812631

812490

141

30228

1028148

17039

1011109

266993

9000

257992

184777

495

184282

65018

12239

377989

22925

198993

19563

210

67164

56752

12382

-

47

2778070

322503

315611

6892

1747

32247

325

31922

47442

5800

41642

230200

253

229947

22618

10605

195177

6379

41866

11545

3518

129332

2175

362

-

609

863148

13214

9464

3750

-

304033

-

304033

8522

-

8522

7320

-

7320

-

-

5955

-

3615

313

-

1025

-

1002

-

4154

343198

1121920

1118637

3283

31975

756362

17364

738998

305913

14800

291112

407657

748

406909

87636

22844

567211

29304

237244

30795

3728

195471

58927

11742

-

(-)3498

3298020

Contd.....

� ��

��������

TABLE-3 ECONOMIC-CUM-PURPOSE CLASSIFICATION OF EXPENDITURE

OF ADMINISTRATIVE DEPARTMENTS 2014-2015 (RE) (Rs.Lakh)

Economic Classification

Purpose Classification

Current expenditure

Transfer payment

Subsidies Transfer to

local

bodies

To others Total

Transfer

Payment

(7+8)

Total

current

expendi-

ture

(5+6+9)

1 6 7 8 9 10

1. General Public Services 1.1 General administration,

external affairs, public order & safety

1.2 General research

2. Defence

3. Education Affairs and

Services 3.1 Administration, regulation

and research 3.2 Schools, universities

and institutions including subsidiary services

4. Health Affairs and Services 4.1 Administration, regulation

and research 4.2 Hospitals, clinics & other

health services

5. Welfare, Affairs And

Services 5.1 Social Security Affairs &

services 5.2 Social Welfare Services

6. Housing And Community

Amenities Affairs And

Services

7. Cultural, Recreational &

Religious Services

8. Economic Services 8.1 General administration,

regulation & research 8.2 Agriculture, forestry,

fishing & hunting 8.3 Mining, manufacturing

& construction 8.4 Electricity, gas, steam

Atomic Energy 8.5 Drinking Water Supply 8.6 Transportation and

communication 8.7 Other economic services

9 Environmental Protection

10. Other Services

TOTAL

--

-

-

7700

-

7700

--

-

221395

-

221395

-

5275

268147 150890

56635

13000

-

--

47622

-

-

502517

144147 144147

-

-

438703

-

438703

--

-

112819

2092

110727

1489813

18

71234 -

7604

34703

-

28923 4

-

-

-

2256734

42645 28039

14606

444

569381

31

569350

160974 61

160913

344885

-

344885

16396

33176

270525 239

234781

13307

8058

7603 20

6517

-

185780

1624206

186792 172186

14606

444

1008084

31

1008053

160974 61

160913

457704

2092

455612

1506209

33194

341759 239

242385

48010

8058

36526 24

6517

-

185780

3880940

1308712 1290823

17889

32419

1772146

17395

1754751

466887 14861

452025

1086756

2840

1083916

1593845

61313

1177117 180433

536264

91805

11786

231997 58951

65881

-

182282

7681477

Contd.....

����

��� ��

TABLE-3 ECONOMIC-CUM-PURPOSE CLASSIFICATION OF EXPENDITURE

OF ADMINISTRATIVE DEPARTMENTS 2014-2015 (RE) (Rs.Lakh)

Economic Classification

Purpose Classification

Capital expenditure

Gross capital formation

Buildings and other

construction

Machinery and other equipment

Change in stock

Gross capital

formation (11+12+13)

1 11 12 13 14

1. General Public Services 1.1 General administration,

external affairs, public order & safety

1.2 General research 2. Defence 3. Education Affairs and Services

3.1 Administration, regulation and research

3.2 Schools, universities and institutions including subsidiary services

4. Health Affairs and Services 4.1 Administration, regulation

and research 4.2 Hospitals, clinics & other

health services 5. Welfare Affairs And

Services 5.1 social security affairs &

services 5.2 Social Welfare Services

6. Housing And Community Amenities Affairs And Services

7. Cultural, Recreational & Religious Services

8. Economic Services 8.1 General administration,

regulation & research 8.2 Agriculture, forestry,

fishing & hunting 8.3 Mining, manufacturing

& construction 8.4 Electricity, gas, steam

Atomic Energy 8.5 Drinking Water Supply 8.6 Transportation and

communication 8.7 Other economic services

9 Environmental Protection 10. Other Services TOTAL

42485 40094

2391 390

45822

-

45822

13535 313

13222

97713

77

97636

32720

17028

635378 1927

37296

8829

35

98927 488364

---

885071

19962 19962

-707

16192

150

16042

4394 66

4328

1124

-

1124

2027

393

2884 1126

1048

398

-

227 25

60 --

47683

2 2

---

-

-

--

-

-

-

-

-

-

--

-

-

-

--

---2

62449 60058

2391 1097

62014

150

61864

17929 379

17550

98837

77

98960

34747

17421

638262 3053

38344

9227

35

99154 488389

60 --

932756

Contd.....

� ��

��� ��

TABLE-3 ECONOMIC-CUM-PURPOSE CLASSIFICATION OF EXPENDITURE

OF ADMINISTRATIVE DEPARTMENTS 2014-2015 (RE) (Rs.Lakh)

Economic Classification

Purpose Classification

Capital expenditure

Purchase of

assests-land

Less-sale of

assets-land

Capital transfers

To Local

bodies

To Others

1 15 16 17 18

1. General Public Services 1.1 General administration, external affairs, public

order & safety 1.2 General research

2. Defence

3. Education Affairs and

Services 3.1 Administration, regulation

and research 3.2 Schools, universities

and institutions including subsidiary services

4. Health Affairs and Services 4.1 Administration, regulation

and research 4.2 Hospitals, clinics & other

health services

5. Welfare, Affairs And

Services 5.1 Social Security Affairs &

services 5.2 Social Welfare Services

6. Housing And Community

Amenities Affairs And

Services

7. Cultural, Recreational &

Religious Services

8. Economic Services 8.1 General administration,

regulation & research 8.2 Agriculture, forestry,

fishing & hunting 8.3 Mining, manufacturing

& construction 8.4 Electricity, gas, steam

Atomic Energy 8.5 Drinking Water Supply 8.6 Transportation and

communication 8.7 Other economic services

9 Environmental Protection

10. Other Services

TOTAL

413 413

-

-

-

-

-

-

-

-

-

-

-

-

-

2464 -

883

10

-

-1571

-

-

-

2877

-

-

-

-

-

-

-

-

-

-

-

-

-

50089

-

3000

-

-

-

-

-3000

-

-

-

53089

6022 4007

2015

-

5944

-

5944

--

-

1200

-

1200

65021

9455

560856 -

38793

2295

489568

30000 -

200

-

-

645498

Contd.....

� ��

����

��� ��

TABLE-3 ECONOMIC-CUM-PURPOSE CLASSIFICATION OF EXPENDITURE

OF ADMINISTRATIVE DEPARTMENTS 2014-2015 (RE) (Rs.Lakh)

Economic Classification

Purpose Classification

Capital expenditure Grand Total

(10+22) Financial

assets Loans and advances Total

capitalTo local To others bodies expendi-

ture (14 to 21)

1 19 20 21 22 23

1. General Public Services

1.1 General administration, external affairs, public

order & safety

1.2 General research

2. Defence

3. Education Affairs and Services

3.1 Administration, regulation

and research

3.2 Schools, universities

and institutions including

subsidiary services

4. Health Affairs and Services

4.1 Administration, regulation

and research

4.2 Hospitals, clinics & other

health services

5. Welfare, Affairs And

Services

5.1 Social Security Affairs & services

5.2 Social Welfare Services

6. Housing & Community

Amenities Affairs And

Services

7. Cultural, Recreational &

Religious Services

8. Economic Services

8.1 General administration,

regulation & research

8.2 Agriculture, forestry,

fishing & hunting

8.3 Mining, manufacturing

& construction

8.4 Electricity, gas, steam

Atomic Energy

8.5 Drinking Water Supply

8.6 Transportation and

communication

8.7 Other economic services

9 Environmental Protection

10. Other Services

TOTAL

-

-

-

-

-

-

-

-

-

-

100

-

100

5

-

86032

2500

5100

73101

-

1500

-

3831

-

-

86137

12600

12600

-

-

500

-

500

-

-

-

711

-

711

80

-

554883

-

29216

484600

-

-

-

41067

-

250

569024

-

-

-

-

-

-

-

-

-

-

-

-

-

2540

-

-

-

-

-

-

-

-

-

-

-

2540

81484

77078

4406

1097

68458

150

68308

17929

379

17550

100848

77

100771

149482

26876

1845497

5553

112336

569233

489603

133654

489960

45158

-

250

2291921

1390196

1367901

22295

33516

1840604

17545

1823059

484816

15240

469575

1187604

2917

1184687

1743327

88189

3022614

185986

648600

661038

501389

365651

548911

111039

-

182532

9973398

� ��

��������

P A R T - III

R e c o n c i l i a t i o n S t a t e m e n t s

����

������������

��������

PART - III

RECONCILIATION STATEMENTS

A reconciliation of the figures of revenue and expenditure given in the budget (Financial Statement ) and in the economic and purpose classification is given below. The various adjustments made in the classification to arrive at the figures mentioned are spelt out in detail in the following statements :

(Rs.Lakh)

Items YEARS

2013-2014

(Accounts)

2014-2015

(R.E.)

1 2 3

Current Account: Revenue

Current revenue of Government

administration as shown in the

Financial Statement

Less

1. Revenue attributable to Departmental

Commercial Undertakings-commercial

receipts (Table -2)

2. Pension Adjustments

3.Revenue receipts netted against revenue expenditure- sale of goods and services (Table-1)

4. Revenue receipts netted against

capital expenditure-sale of assets-Land

5. Fund (Borrowing Account) Revenue

6. Sale of Financial Assets

Add

1. Surplus transferred by Departmental

Commercial Undertakings (Table-2)

Total adjustments

Current revenue of Government

administration-administrative

departments as shown in the

economic classification of the

budget (Table-1)

7578522

246725

3162

230398

-

-

3597

102389

(-) 381493

7197029

10462110

645917

5311

343198

-

-

-

468085

(-)526340

9935770

����

��������

(Rs.Lakh)

Items YEARS

2013-2014 (Accounts)

2014-2015 (R.E.)

1 2 3

Total Expenditure

As per Consolidated Fund shown in the

Financial Statement

Less

1. Current expenditure of Departmental Commercial Undertakings (Table-2)

2. Capital formation in Departmental

Commercial Undertakings (Table-3)

3. Net purchase of physical assets in

Departmental Commercial

Undertakings-land (Table-3)

4. Revenue receipts netted against

revenue expenditure (Table-1)

5. Revenue receipts netted against capital expenditure

6. Fund (Borrowing account)

7. Interest (Table-1)

8. Repayment of public debt

9. Other Debt (Borrowing Account)

10. Pension Adjustments

11. Sale of Financial Assets

Add

1. Imputed subsidy

Total adjustment

Total expenditure as shown in the

economic-cum-purpose classification

of the budget

8976444

245194

463314

-

230398

-

156838

639132

400464

-

3162

3597

100858

(-) 2041241

6935203

12339986

260828

482739

-

343198

-

151791

687487

518231

-

5311

-

82996

(-) 2366588

9973398

����

��������

P A R T - IV

S o m e S i g n i f i c a n t M a g n i t u d e s

����

��� ��� ��

��������

PART-IV

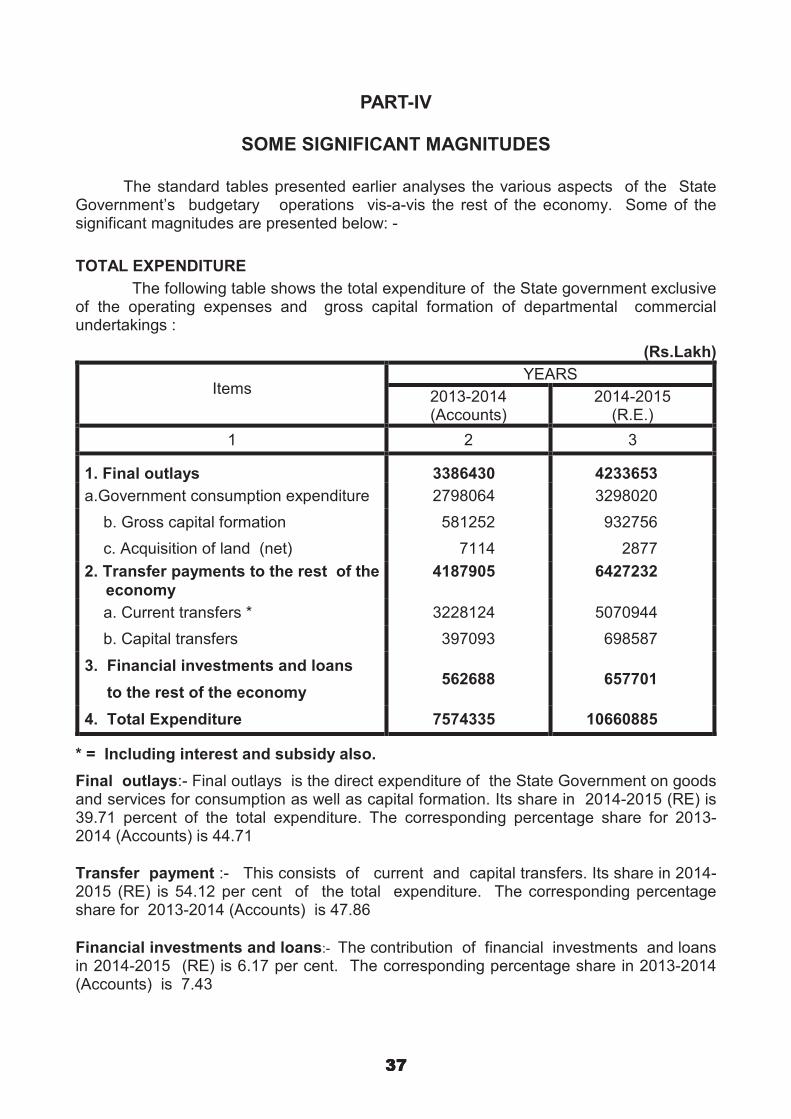

SOME SIGNIFICANT MAGNITUDES

The standard tables presented earlier analyses the various aspects of the State Government’s budgetary operations vis-a-vis the rest of the economy. Some of the significant magnitudes are presented below: -

TOTAL EXPENDITURE

The following table shows the total expenditure of the State government exclusive of the operating expenses and gross capital formation of departmental commercial undertakings :

(Rs.Lakh)

Items YEARS

2013-2014 (Accounts)

2014-2015 (R.E.)

1 2 3

1. Final outlays 3386430 4233653

a.Government consumption expenditure 2798064 3298020

b. Gross capital formation 581252 932756

c. Acquisition of land (net) 7114 2877

2. Transfer payments to the rest of the

economy

4187905 6427232

a. Current transfers * 3228124 5070944

b. Capital transfers

3. Financial investments and loans

397093 698587

to the rest of the economy 562688 657701

4. Total Expenditure 7574335 10660885

* = Including interest and subsidy also.

Final outlays:- Final outlays is the direct expenditure of the State Government on goods and services for consumption as well as capital formation. Its share in 2014-2015 (RE) is 39.71 percent of the total expenditure. The corresponding percentage share for 2013-2014 (Accounts) is 44.71

Transfer payment :- This consists of current and capital transfers. Its share in 2014-2015 (RE) is 54.12 per cent of the total expenditure. The corresponding percentage share for 2013-2014 (Accounts) is 47.86

Financial investments and loans:- The contribution of financial investments and loans in 2014-2015 (RE) is 6.17 per cent. The corresponding percentage share in 2013-2014 (Accounts) is 7.43

����

��� ��

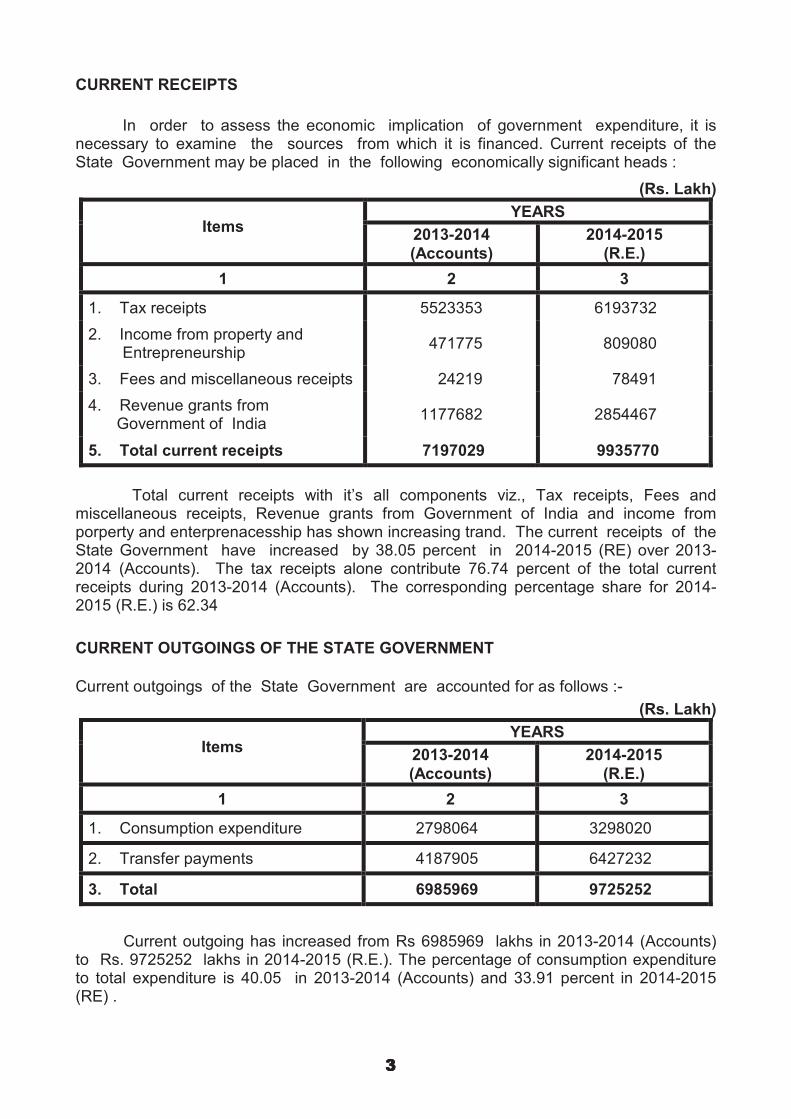

CURRENT RECEIPTS

In order to assess the economic implication of government expenditure, it is necessary to examine the sources from which it is financed. Current receipts of the State Government may be placed in the following economically significant heads :

(Rs. Lakh)

Items YEARS

2013-2014

(Accounts)

2014-2015

(R.E.)

1 2 3

1.

2.

3.

4.

5.

Tax receipts

Income from property and Entrepreneurship

Fees and miscellaneous receipts

Revenue grants from Government of India

Total current receipts

5523353

471775

24219

1177682

7197029

6193732

809080

78491

2854467

9935770

Total current receipts with it’s all components viz., Tax receipts, Fees and miscellaneous receipts, Revenue grants from Government of India and income from porperty and enterprenacesship has shown increasing trand. The current receipts of the State Government have increased by 38.05 percent in 2014-2015 (RE) over 2013-2014 (Accounts). The tax receipts alone contribute 76.74 percent of the total current receipts during 2013-2014 (Accounts). The corresponding percentage share for 2014-2015 (R.E.) is 62.34

CURRENT OUTGOINGS OF THE STATE GOVERNMENT

Current outgoings of the State Government are accounted for as follows :-

(Rs. Lakh)

Items YEARS

2013-2014

(Accounts)

2014-2015

(R.E.)

1 2 3

1. Consumption expenditure 2798064 3298020

2. Transfer payments 4187905 6427232

3. Total 6985969 9725252

Current outgoing has increased from Rs 6985969 lakhs in 2013-2014 (Accounts) to Rs. 9725252 lakhs in 2014-2015 (R.E.). The percentage of consumption expenditure to total expenditure is 40.05 in 2013-2014 (Accounts) and 33.91 percent in 2014-2015 (RE) .

� ��

��� ��

Net receipts from borrowing and extra-budgetary resources have been shown in the accounts given below :-

BORROWING ACCOUNT

2013-2014 (ACCOUNTS)

(Rs. Lakh)

Items Receipts Expenditure

1 2 3

I. Borrowing at home

1. Internal debt

2. Small savings, provident funds, etc.

3. Other debt

Total

Net receipts

II. Borrowing abroad

1. External debt

2. Other debt

Total

Net receipts

III. Extra budgetary receipts and

adjustments for cash balance

1. Loans from Govt. of India

2. Loans and advances by State Govt.

3. Inter-state settlement

4. Contingency fund

5. Reserve funds

6. Deposits and advances

7. Suspense & miscellaneous

8. Remittances

9. Cash balance

10.Funds - revenue account

11.Funds - capital account

12.Funds - commercial account

Total

Net receipts

832838

278403

-

1111241

603352

-

-

-

-

121244

9323

244

-

161200

1036884

24747987

1560217

(-)26275

-

-

-

27610824

(-) 270504

324262

183627

-

507889

-

-

-

-

76202

507752

236

-

64394

1085759

24441152

1531654

17321

156838

-

20

27881328

� ��

����

��� ��

BORROWING ACCOUNT 2014-2015 (RE)

(Rs. Lakh)

Items Receipts Expenditure

1 2 3

I. Borrowing at home

1. Internal debt

2. Small savings, provident funds, etc.

3. Other debt

Total

Net receipts

II. Borrowing abroad

1. External debt

2. Other debt

Total

Net receipts

III. Extra budgetary receipts and

adjustments for cash balance

1. Loans from Govt. of India

2. Loans and advances by State Govt.

3. Inter-state settlement

4. Contingency fund

5. Reserve funds

6. Deposits and advances

7. Suspense & miscellaneous

8. Remittances

9. Cash balance

10. Funds - revenue account

11. Funds - capital account

12. Funds - commercial account

Total

Net receipts

1353429

266533

-

1619962

1016531

-

-

-

-

265671

2741

-

50000

221288

1766588

17293812

1366135

17321

-

-

-

20983736

(-) 380288

427648

175783

-

603441

-

-

-

-

90583

571564

-

80000

200963

1737047

17209848

1335107

(-)12927

151791

-

48

21364024

� ��

��������

NET SURPLUS OF DEPARTMENTAL COMMERCIAL UNDERTAKINGS

Net surplus of the departmental commercial undertakings, as measured by the

excess of gross receipts over operating expenses, indicate the financial results of the

working of these undertakings. It is also instrumental in augmenting the current receipts of

the government administration. The derivation of the net surplus is shown below :-

(Rs. Lakh)

Items YEARS

2013-2014

(Accounts)

2014-2015

(R.E.)

1 2 3

1. Gross receipts * 347583 728913

2. Operating expenses 245194 260828

3. Net surplus / Deficit (1-2) 102389 468085

* = Including imputed subsidy.

The above table presents the net surplus / deficit of the departmental

commercial undertakings. The net surplus in 2013-2014 (AC) is Rs 102389 It has

increased in 2014-2015 (RE) to Rs 468085 lakh.

����

��������

ESTIMATES OF NET PRODUCT FROM PUBLIC ADMINISTRATION

(Rs. Lakh)

Items YEARS

2013-2014

(Accounts)

2014-2015

(R.E.)

1 2 3

Administration

1. Total wages and salaries

Less wages and salaries in :

2354417 2778070

2. Construction

(Repairs and maintenance)

81681 94891

3. Water supply 54870 65206

4. Other services 1090302 1270675

a. Education 887875 1011109

b. Medical and public health 200782 257992

c. Sanitation 1645 1574