![COURT OF QUEEN’S BENCH OF MANITOBA · 2 [2] Queen’s Bench File No. CI 13-01-86371 (“first action”) is between the plaintiff and both defendants, Delta Air Lines, Inc. (“Delta”)](https://static.fdocuments.us/doc/165x107/5b7ab8de7f8b9a460c8c6db7/court-of-queens-bench-of-2-2-queens-bench-file-no-ci-13-01-86371-first.jpg)

Court of Queen’s Bench of Alberta - · PDF fileCourt of Queen’s Bench of Alberta...

49

Court of Queen’s Bench of Alberta Citation: Servus Credit Union Ltd v Parlee, 2015 ABQB 700 Date: 20151105 Docket: 1504 00261 Registry: Grande Prairie Between: Servus Credit Union Ltd. Plaintiff - and - Alfred Philip Parlee and Clara Vivian Parlee Defendants

-

Upload

nguyenphuc -

Category

Documents

-

view

220 -

download

3

Transcript of Court of Queen’s Bench of Alberta - · PDF fileCourt of Queen’s Bench of Alberta...

Court of Queen’s Bench of Alberta

Citation: Servus Credit Union Ltd v Parlee, 2015 ABQB 700

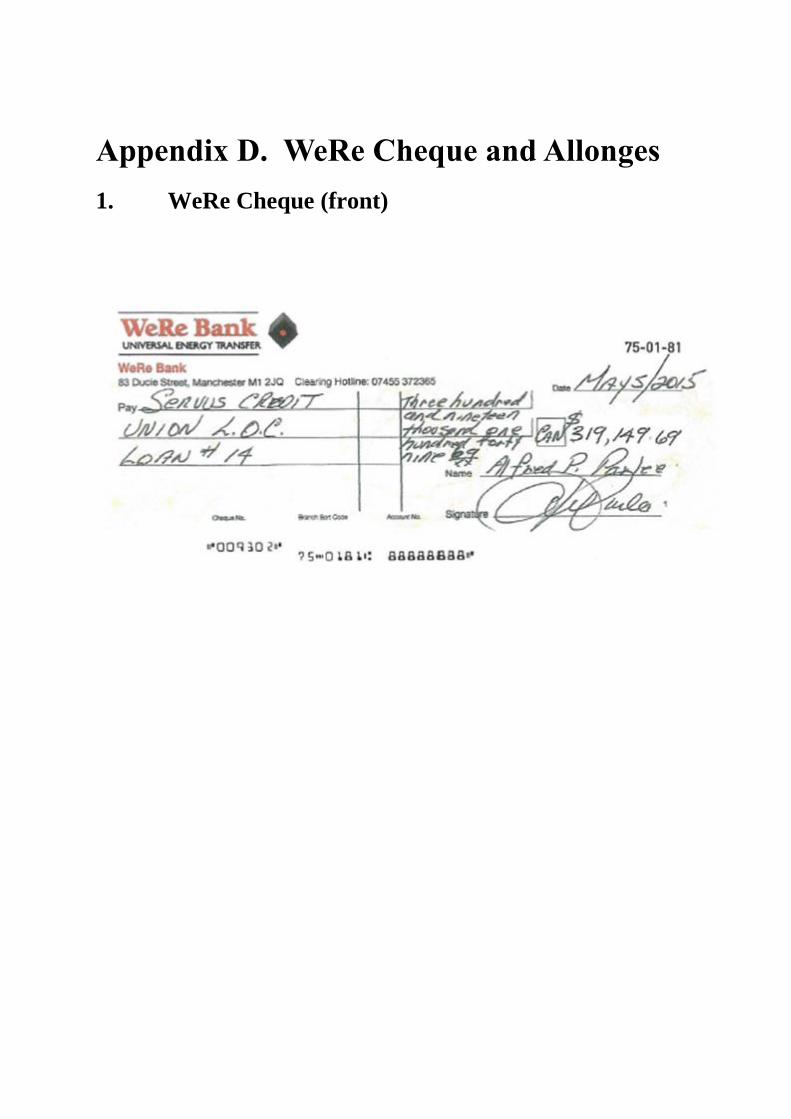

Date: 20151105

Docket: 1504 00261

Registry: Grande Prairie

Between:

Servus Credit Union Ltd.

Plaintiff

- and -

Alfred Philip Parlee and Clara Vivian Parlee

Defendants

_______________________________________________________

Memorandum of Decision

of

W.S. Schlosser, Master in Chambers

_______________________________________________________

Table of Contents

I. Introduction

II. The October 1, 2015 Hearing

III. Background and Timeline

IV. Analysis

A. Quo Warranto Application

B. The Parlees Have Paid the Outstanding Debt

1. The “Freeman Legal Services” “A4V” Scam

2. The WeRe Bank

3. The Private Indemnity Bond

4. Conclusion - Pseudolegal Payment Schemes Have No Effect

V. Conclusion and Costs

VI. Disposition

Appendix A. Writ of Quo Warranto Documents

1. Foisted Quo Warranto Challenge

2. Writ of Quo Warranto

Appendix B. Private Indemnity Bond - Non-Negotiable

Appendix C. Correspondence from Freeman Legal Services

Appendix D. WeRe Cheque and Allonges

1. WeRe Cheque (front)

2. Allonge

Appendix E. May 19, 2015 “Notice of Protest...”

Appendix F. June 10, 2015 “Notices of Protest Sent’

The writing in black is Herr “I vos only obeying orders” Schlosser’s rantings. The blue or

purple mine!

EVERYTHING LISTED BY THIS BENT AND CORRUPT, BOUGHT AND PAID FOR

JUDGE IS AN EXERCISE IN “selective conclusioning” WHICH IS THE TRICK OF

TRICKS OF THESE JACKALS SOMETIMES REFERRED TO AS JUDGES. You will find

no reference here to the inequity of the system generally, no reference to the reams of

illogical conclusions which people have railed at before in past “trails” – no references to

even the policy documents of the banks themselves suggesting “something is not quite right”.

No reference to deficit spending whereby the US Govt is trading at 19 trillion in a whole – no

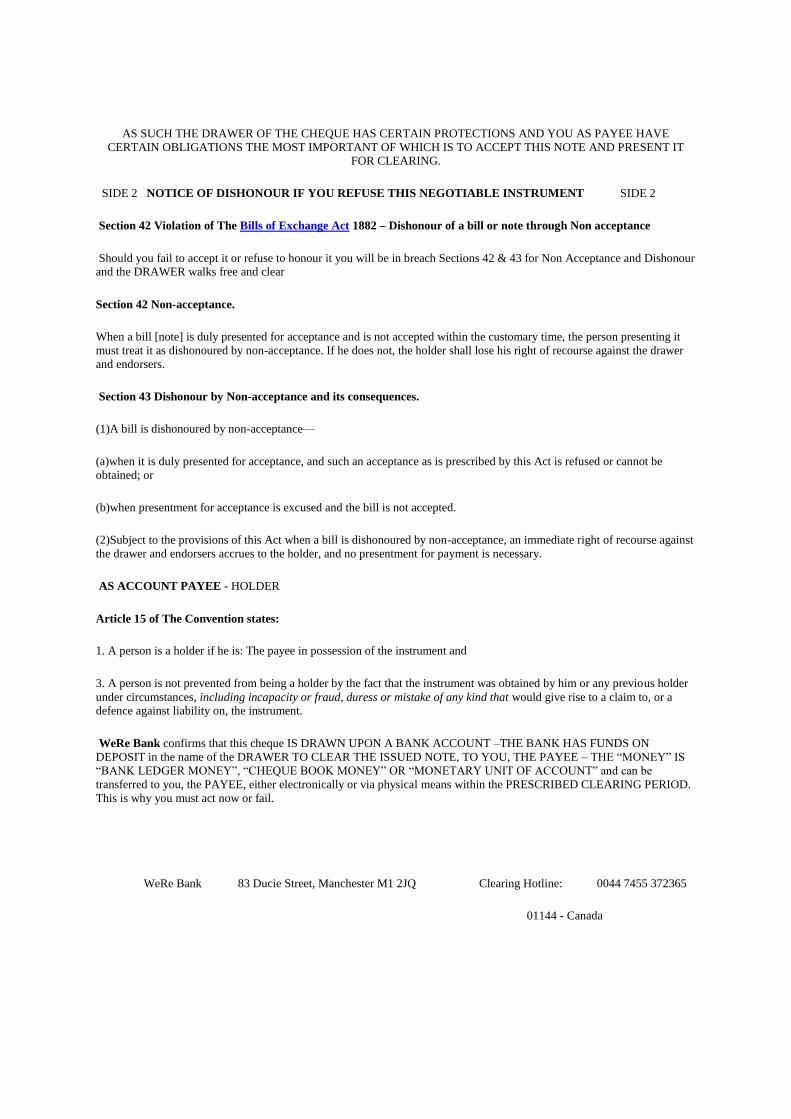

reference to the banking systems which ruined Ireland, Iceland and Europe and the world.

Mr Parlee MUST insist on a trial by a jury of his peers in Chancery/Equity Division as this is

to do with a TRUST PROPERTY and has no place anywhere else.

The PROOF?

Two parties arguing over a title to land is proof absolute that there are 2 titles: The Legal and

the beneficial. SERVUS cannot possibly have them both otherwise Mr Parlee would never

have been allowed onto the property and allowed to “enjoy the use of it” for all these years.

Equally Mr Parlee does NOT possess both titles otherwise SERVUS would not be in the

picture.

The injustice of one word only being raised against WeRe Bank is enough to send this man

Schlosser to trial in front of our International Common Law Court of Record 750181….the

many will see him purged.

ReMember ReMember – Ye Old Knight’s Templar maxim:

“Wrap tour enemy in one of three things: debt, litigation or a shroud!”

I. Introduction TWO QUESTIONS TO BEGIN WITH AND TWO WHICH SEEM NOT

TO HAVE BEEN ASKED OR ANSWERED:

1.“Where are the original wet signature documents (THE NOTE)

evidencing the loan obligation of Mr Alfred and Clara Parlee to Servus

Credit Union?

2. Where is the injured party?

We should first recall that Canada is home to some of the Freedom

Movement Greats such as Rob Menard as well as Dean Clifford – it is not

by accident therefore that some of the strongest resistance to the words of

TRUTH will cause such an outage of ridicule and painfully defective denial

by the Judiciary and their Legal Lap Dogs LLC.

Also we must address the initial situation arising here: “Why did Mr Alf

Parlee and his wife find themselves in such a position in the first place?

Was it due to SCAM artists – yes it was and these scammers were the

Property Taxation Bureaux as well Servus Credit Union – SERV-US being

a Roman name by the way, with similar overtones to the Roman Centurion

helmet of AMEX. This build up of a repossession situation was in

existence prior to WeRe Bank coming on the scene. Should we not first

address the “Five Fraudulent Facts of Finance Liar and Perverter of the

Nature of Man Schlosser?

The True Nature of Scam and Fraud is best watched here

https://youtu.be/DyV0OfU3-FU

and read here briefly:

FOUR FRAUDULENT FACTS FOR FINANCE COMMITTED

BY SERVUS Step 1: Fraud in the Inducement

“… is intended to and which does cause one to execute an instrument, or make an

agreement…

The misrepresentation involved does not mislead one as the paper he signs but rather

misleads as to the true facts of a situation, and the false impression it causes is a basis of a

decision to sign or render a judgment” Source: Steven H. Gifis, ‘Law Dictionary’, 5th

Edition, Happauge:

Barron’s Educational Series, Inc., 2003, s.v.: ‘Fraud’.

The first violation is the fraud the borrower is induced into committing by pledging as

collateral property which he/she does NOT own or have title to. The bank is complicit in that

it accepts the fraudulent pledge -

Step 2: Fraud in Fact by Deceit (Obfuscation and Denial) and Theft

“ACTUAL FRAUD. Deceit. Concealing something or making a false representation with an evil intent [scanter]

when it causes injury to another…”. Source: Steven H. Gifis, ‘Law Dictionary’, 5th Edition,

Happauge: Barron’s Educational Series, Inc., 2003, s.v.: ‘Fraud’.

“THE TORT OF FRAUDULENT DECEIT… The elements of actionable deceit are: A

false representation of a material fact made with knowledge of its falsity, or recklessly, or

without reasonable grounds for believing its truth, and with intent to induce reliance thereon,

on which plaintiff justifiably relies on his injury…”. Source: Steven H. Gifis, ‘Law

Dictionary’, 5th Edition, Happauge: Barron’s Educational Series, Inc., 2003, s.v.: ‘Deceit’.

The failure by the bank to disclose the true nature of the contract – the bank calls it a loan

leading the borrower to believe that he/she is receiving a loan of EXISTING MONEY but the

bank knows full well that all it has done is to create a brand new promise to pay – simply

typed onto the computer key board/ledger book. A promise the bank knows that in all

probability it will never have to fulfil. Also see UCC 1-201 (24) & 3-104 it is our signature

on the note which makes it a negotiable instrument. See also Bills of Exchange Act 1882

Step 3: Theft by Deception and Fraudulent Conveyance THEFT BY DECEPTION:

“FRAUDULENT CONCEALMENT… The hiding or suppression of a material fact or

circumstance which the party is legally or morally bound to disclose…”.

Also failure by SERVUS acting as Securities Agent on behalf of the principle to disclose the

true nature of the contract. The bank calls it a loan but it is NO SUCH THING!

“The test of whether failure to disclose material facts constitutes fraud is the existence of a

duty, legal or equitable, arising from the relation of the parties: failure to disclose a material

fact with intent to mislead or defraud under such circumstances being equivalent to an actual

‘fraudulent concealment’…”.

To suspend running of limitations, it means the employment of artifice, planned to prevent

inquiry or escape investigation and mislead or hinder acquirement of information disclosing a

right of action, and acts relied on must be of an affirmative character and fraudulent…”.

Source: Black, Henry Campbell, M.A., Black’s Law Dictionary’, Revised 4th Edition, St

Paul: West Publishing Company, 1968, s.v. ‘Fraudulent Concealment’.

FRAUDULENT CONVEYANCE:

‘FRAUDULENT CONVEYANCE… A conveyance or transfer of property, the object of

which is to defraud a creditor, or hinder or delay him, or to put such property beyond his

reach…”.

“Conveyance made with intent to avoid some duty or debt due by or incumbent on person

(entity) making transfer…”. This is FACT as A.PARLEE could not have lodged as security

for the loan an asset to which “at the time the deed was executed and the loan agreement

signed” he possessed NO TITLE or equitable or proprietary interest in WHATSOEVER!

Rebuttal required: -

Step 4. VIOLATION OF NATURAL LAW AND IMPOSSIBILITY OF CONTRACT

Common law states that one cannot give better title than one has. As SERVUS has NO

TITLE to any property it having NOT been able to produce original wet signature mortgage

documents then it cannot lay claim to anything. This is simply evidenced by the question: “If

everything was contingent upon the signature of A. PARLEE then without that signature

WHAT DID SERVUS CREDIT UNION HAVE? They had nothing and there was nothing

monetized until the moment A.PARLEE signed a Promissory Note – a promise to pay $£ x

over n years at % interest.

Loan should be invalid as unless the system – totally outside the control of A.PARLEE –

ensures a 100% recycling of principle + interest (p+i%) then some borrowers are going to

default. (P is less than P+i%)

Rebuttal required:

The main reason the Parlees are being pilloried here is because they had the audacity to

challenge the system – challenge it NOT with a WeRe Bank cheque BUT challenge the

“corporatocracy” and the filthy lying fraudulent hyena flesh-tearing judiciary and its

PayMaster banking colleagues. Club Canada is particularly hell bent in squashing anyone

using “freeman on the land type language]

[1] This is a case where all of the participants have become victims of a pseudo legal

scam.[YES this is so true and it’s called the Queens’ Bench Division of the Canadian Courts

System – a legal circus of performers of dubious human credentials who swear black is blue

then blue is black – as it suits - First and foremost the definition of a scam is ….Invariably

scam artists rely of small numbers of gullible people sworn to “secrecy” or offered “special

access” or “special entry points” into a scheme which can make them rich or offer them

“what they want!” For example if a court could pretend to offer justice to a “select” few who

came across its doors from time to time, and all dealings within were to be kept secretive,

couldn’t be recorded or filmed for fear of exposure of the Cronyism therein and be so set up

so that the defendant in such as, say, an action brought against him by against the banks or

loan companies, could never win in a million years - now that would be some scam would it

not? Is it possible…..read on

In no case is the WeRe Bank facility of Debt Settlement in this category. It does not offer a

special return or a special “get rich quick reward” neither does it offer to put large amounts of

money into the VICTIMs hands. What it does do is show them the nature of money

CREATION and supported by the IMF (see IMF Chicago Plan as well as 2014 Q1 Bank of

England doc on Monetary Reform referred to infra) and all Central Banks of the world and

shows how to produce FOR THEMSELVES A VALID PROMISSORY NOTE which if the

promise of a man has no value in this instance then it has no value in commerce banking and

finance full stop.

If Herr Schlosser wishes to defeat the effectiveness of the weapons which WeRe Bank

delivers to its members then it must demolish the entire infrastructure, architecture and

furniture which is “global banking, commerce, finance and insurance and trade”. Do you

think they’ll go there?]

The court and Judge Schlosser are then “hoist on their own petard”. We also note that the

Judge in not an impartial and fair examiner having taken both an Oath of Office and Oath of

Allegiance to the Queen of England via the Canadian Bar Association’s back-door. He is also

the Keeper of the Gate to ensure that the lies, subterfuge and deceit of the likes of Servus

Credit Union, the law firm they employed – and members of the judiciary stay “JUICED IN”

to the plot. Who can protest otherwise? In the UK for example in the last 20 years according

to the Council of Mortgage Lenders, 3 million homes have been repossessed and in this time

NOT one defendant has succeeded in the Minnesota Credit River mind-set decision (See

http://www.constitutionalconcepts.org/creditriver.htm).

This judge is partial to using the word SCAM and it is of relevance that scammers are NOT

usually attention seekers and do not, as a rule, promote their scams actively on the Internet

via videos over YouTube and via websites and revel in full-on confrontation with the

supposed Regulatory Authorities. It is also a moot point is anyone has in recent times

attempted to SCAM AN ENTIRE PLANET?] This judgment explains my refusal to interfere

[ “refusal to interfere” is judge speak means closing and protecting the Masonic Juiced in

court slush fund and Protectionist Oath which Schlosser and Co have sworn – “Protect the

Trust at all costs!”] with a court-ordered [the 12 Presumption of a Roman Curia must be

rebutted were they?] foreclosure of property formerly owned by Alfred and Clara Parlee. As

a direct result of the scam the foreclosure process was unnecessarily long, complicated, and

costly. The Parlees attempted to implement futile, pseudo-legal schemes to save their home.

Instead it cost them not only their home but also whatever equity they had.[Sounds like

someone’s being punished here, does it not?]

[2] There are some apparent winners. These are the scam artists[the Parlees were not

preyed upon by WeRe Bank - this infers “victimisation.” WeRe Bank stepped into HELP –

this Bank was a result of the work which had preceded called Debt Assumption offered via

Freeman Legal Services. The Parlees were victims of the “p < p + i%” as the entire financial

system is designed to have a certain but indeterminate number of people{identified} become

bankrupt within any given period of time as there is not enough circulation of M0, M1 and

M2 money supply]who preyed on the Parlees and exploited their desperate situation. One is

known: a UK resident named Peter Smith[technically a French resident actually Herr

Schlosser], or, as he prefers to call himself, “Peter of England”.[So he implies here that I am

a con-man too! Maybe he means that I am attempting to gain peoples’ confidences – don’t

politicians do that too? Do they singularly fail to deliver EVERY TIME the election promises

they make or declare in their manifestos?] The other con-person cannot be identified from the

materials received by the Court. There is an accompanying cast of lesser characters, including

an Alberta lawyer[ a brave and awakening soul who should be thanked for his bravery and

taking on this nest of vipers] who may have breached his professional duties[ a veiled threat

to be careful of “embarrassing the court – which is judge speak for breaking their secret oath

to render every defendant liable] by endorsing legally ineffective and fraudulent documents

as a notary, thereby adding an air of legitimacy to documents that are profoundly at odds with

any accepted legal ideas: see Re Boisjoli, 2015 ABQB 629 (CanLII) at paras 121-24.

[3] And then there is the Court, where this drama played out. This written decision is the

last Scene in what I expect might be the first Act of this drama; appeals being Act II.

[4] This foreclosure appears to be the first occasion a Commonwealth court has

commented on (and denounced) this specific Organized Pseudolegal Commercial Argument

[“OPCA”] ‘money for nothing’ scheme: the WeRe Bank. [The money for nothing scam is in

fact the truest thing that this “rogue” has mentioned – the IMF Chicago Plan and BOE Q1

2014 doc explains supra. See the history of the Bank of England, Bank for International

Settlements and history of the Federal Reserve as well as JFK’s comments about it.]

[5] The OPCA term was coined by Rooke ACJ in Meads v Meads, 2012 ABQB 571

(CanLII), 543 AR 215 to describe a collection of pseudolegal concepts advanced on a

commercial basis by scammers and conmen, “OPCA gurus”, who promote allegedly legal

procedures that supposedly: [Could these be people like Rob Menard and Dean Clifford?]

i) bend courts into submission, [Sounds like a war to me with such language -

courts are administrative and of little relevance these days other than as

enforcement tribunals – they are neither fair or impartial and they neither

adhere to common law principles and practices]

ii) nullify state authority, or [the state only can operates via consent – the state is

a non-existent entity which when searched for cannot be found]

iii) as is the case here, provide free money.[WeRe Bank only opens the door to the

Wizard of Oz. Toto the little dog pulls away the curtain for everyone to see the

deceit of the “money go around” which is the Banking Business and

malpracticed over the eons. If you want to see real free money then look to the

Central Bank of Canada, the FED, the BOE and the BIS]

[6] All are false.[The truth to a liar is what…..?] Many are contempt of court: Fearn v

Canada Customs, 2014 ABQB 114 (CanLII), 586 AR 23, per Tilleman J, (though in a

criminal context). None provide any benefit, except to those who sell these concepts for

profit.[False - nothing is sold for profit – the collective base of the trust invests the funds

received for the benefit of all.]

II. The October 1, 2015 Hearing

[7] On October 1, 2015 I heard an ill-defined application[Alf mixed jurisdiction too and

was not so well informed even though I had spoken to him in the weeks prior to this case

commencing the documents he’d already submitted and the “tack” was already set.] by Mr.

Alfred Parlee in relation to an August 13, 2015 order of Master Smart that foreclosed the

Parlees from their rural property near Sexsmith, Alberta. The Parlees had been given 30 days

to exit the property. They did not do so, and, so on September 29, 2015, the Parlees were

removed from it with the assistance of the RCMP. [There is a massive miscarriage of justice

here. There is a dispute of title to the property – two titles must exist as there was a physical

possessor and also someone not in physical possession. This evidences and there must exist a

trust. The beneficial title and the legal titles are separated. The Parlees hold the beneficial and

the Servus Credit Union hold the legal title. No dispute there. So why in a 40 page document

here of our good honest open and public protector badge of honour Schlosser does he not

mention the Chancery Equity Divisional ]

[8] This seems to have been an unexpected outcome for the Parlees. As at the date of the

hearing, their personal property and vehicles remained on the land that now belonged to the

lender. Rules 9.27 and 9.28 deal with removal, storage and sale of personal property and

abandoned goods. I encouraged the Parlees to come to an agreement about the orderly

removal of those personal goods

[9] Mr. Parlee had filed documents after August 13, 2015. These formed the foundation,

such as it was, for the October 1, 2015 hearing. When the hearing commenced Mr. Parlee

expressed surprise and concern that this was a public hearing. He was “a private man” and

said this hearing should have been “a private session”. Court hearings are open to the public

and recorded[ recorded BUT not public courts of record as there is a direct prohibition for

taking any recordings or having film made in order to protect the protagonists], except in

well-defined exceptional circumstances. Mr. Parlee objected to any participation of counsel

for Servus, saying: “You are not supposed to be speaking on my behalf”, which they were

not.[He was factually correct as the parties to the original contract were not there – neither

could SERVUS provide an injured party – not did SERVUS prove they had the original loan

document – neither did SERVUS make a statutory declaration that they had NOT monetized

Mr Parlee’s Original Note or trade it. Without the Original Document SERVUS CREDIT

UNION should never have been allowed through the door!]

[10] Having reviewed Mr. Parlee’s materials I asked if his objective was to nullify Master

Smart’s foreclosure order. Mr. Parlee confirmed that was a part of his intention, but he also

wanted the Court:

... to identify the trust, and to discuss other relevant trusts relating to the

subject matter. I have an interest in the case, the trusts are the judge, the court

clerk, the court, the indemnity bond, the mortgage, the payment office PGT,

the treasury board, the bank, the Servus Credit Union Ltd., the taxation officer,

and the prosecutor. Some of these trusts have been breached. I have vested

interests and properties to these different entities that show I have an adverse

claim on these subject matters. {This is a bit confusing but you can see why

Schlosser was NOT going to allow any of this to be discussed}

Therefore I require return on my interest. I order return on my interest from

CRA, and I order clear title to the property with no labelling encumberances. I

also order the return of the interests and principle to be paid immediately to

my business name. ... I order the clear title to the property. ...

As a private man I make these orders in full due respect. The indemnity bond

that was accepted by the court was for one million dollars.

[11] The Canada Revenue Agency was not a participant in this action, but would have

received notice of the steps. As counsel for Servus explained, Mr. Parlee appeared to be

referring to two Canada Revenue Agency writs, both in the amount of $212,507 and costs:

one filed in 2013 and the second, which appears to be a duplicate, in 2015: ITA v Parlee,

Ottawa ITA-6247-13 (Federal Court). Since those writs had a lower priority than the Servus

interest on the Parlee Lands, they were foreclosed off title.

[12] Mr. Parlee said he has “100% legal title to the estate”,[This was an incorrect

statement on Mr Parlee’s part – he had beneficial ownership and title BUT Servus had legal

title] and relied on documents in an Affidavit he had filed on July 20, 2015. He claimed his

signature “... creates the currency.” [This is a truism – does the judge not wish to discuss

this?]His authority to sign comes from his certificate of live birth. His documents were no

different from others used in international commerce. They had been filed to the treasury

board who “would look after everything.” He argued that “UCC 3603” and its Bills of

Exchange Act equivalent meant the Parlees’ debt was discharged. He concluded:

I made order as a private person. ... Sir, I order this case closed, and all settlements looked

after. I’m asking for an order to have this case sealed, and my files returned to me. I order

this.

[13] I responded that the Court would not acceed to Mr. Parlee’s orders. I dismissed Mr.

Parlee’s application, with written reasons to follow.

III. Background and Timeline

[14] As noted, the Parlee Lands are located outside of Sexsmith, Alberta and include the

Parlees’ residence. The debt was $331,807.26.

[15] The Parlees entered into a Line of Credit agreement with Servus which permitted the

Parlees to overdraw their chequing account by up to $320,000, with 1% interest per annum.

The Line of Credit was secured by a mortgage.

[16] One term of the agreements with Servus was that the Parlees would pay the County

property taxes for the Parlee Lands. Failure to do was a default on the Mortgage. The Parlees

did not pay their property taxes for several years[ so the scam artist, Peter of England took

advantage of these poor people who had “decided of their own accord” for a protracted

period of time to NOT pay these punitive taxation charges – Peter the Predator was just

sitting there waiting for the Parlees to fall into the orbit of his dastardly machinations] and the

County registered a tax notification against title. Servus then paid the overdue property taxes

and issued a demand. When the demand was not met, Servus commenced foreclosure

proceedings.

[17] On May 5, 2015 the Parlees sent Servus what purported to be a cheque drawn on an

institution named the “WeRe Bank”.

[18] The Parlees filed a Statement of Defence on May 7, 2015. It claims that County taxes

for the Parlee lands had been paid on December 19, 2014:

... in good faith by a signed acceptance Tender Instrument as per Canada Bills of Exchange

Act, RSC 1985 c-B-4 current to April 22, 2015 Section 57, 80, 81, 82, 84, 95. and UN

Convention on Bills of Exchange and Promissory Notes 1988 Article 41, 43 and 71..es) ...

A non valid response from the County of Grande Prairie # 1 sent December 29, 2015 was

received by defendant so an Affidavit of non-response was sent January 17, 2015.

Servus Credit Union initiated foreclosure action against defendants with Minos Stewart

Masson (solicitors) based on presumption that taxes of $11,782.31 were still outstanding .

My Line of Credit was in good standing and payments were made faithfully for many years

then account was frozen and I could not make my truck payment. These procedures caused

me great stress, harm and anxiety of which I will seek compensation from all parties jointly

and severally. I believe these actions against me the defendant were not lawful and had

principles of Fraud and Extortion as my presentment for Tender Payment was within the

guidelines of the bills of Exchange Act and the UN Convention for Bills of Exchange and

Promissory Notes.

A cheque from WeRe Bank for $319,149.69 was sent by me to Dan Heinman Senior

Manager corp. Services (ServusCredit Union) May 05, 2015 for the original Line of Credit

Amount. ...

[If the nature of this case is about money and it is – then what does t matter who pays the

DEBT (so called) or how? However, if the nature of the game is coercion, control,

intimidation and punishment at any cost then that COST is NOT required off anyone – the

name of their game is sociopathic and psychopathic infliction of pain, harm distress and

punishment!]

[Sic.]

[19] The Parlees sought $30,000.00 in damages, re-instatement of the Line of Credit and

nullification of any associated charges

[20] The “WeRe Cheque” was rejected by Servus on May 11, 2015. Servus insisted on

payment by certified cheque or bank draft; Servus had “... no intention of engaging in

discussion with [Mr. Parlee] regarding [his] ‘freeman theories of money and banking’.”[What

this means is that the system “we use” is the system and the nature of the creation of money

as freely and openly admitted and referred to by the Bank of England, The IMF, The ECB as

well as the Federal Reserve and the World Bank – the basis of ALL Quantitive Easing and

funding of the 19 trillion debt of the United States and the indebtedness and bankruptcy of

Canada too, is predicated upon]

[21] Mr. Parlee responded on May 19, 2015 with a document titled:

Notice of Protest and included Info from Canadian Bills of Exchange Act

R.S.C., 1985, c. B-4, UN Convention on International Bills of Exchange and

Promissory Notes (1988), Financial Administration Act R.S.C., 1985, F-11

(Interpretation of Money), Black's Law 9th

Edition (payment

(14c)(Acceptance) in Regard to Correspondence received May 15, 2015 and

sent May 11, 2015, Non Acceptance of Cheque to Servus Credit Union for $

319, 149.69

[22] This document is reproduced in Appendix E, but also features a postage stamp in the

lower right corner, which Mr. Parlee has signed across. As with other documents reproduced

in the appendices, the content is, in some cases, redacted to remove sensitive or redundant

information. The appendix documents generally reproduce the formatting of the original

items.

[23] On June 3, 2015 Servus applied for summary judgment, a 30 day redemption period,

with two affidavits in support:

• Greg Schindel’s Affidavit of Value consisting of a May 25, 2015 exterior appraisal of

the Parlee Lands and concluding that the fair market value was $350,000.00. The

property includes one two-story residence, and minor outbuildings and utility

improvements.

• Sharon Boser’s Affidavit of Default documenting the history and state of the

Overdraft Agreement and related Mortgage. The Parlees’ last payment was in March,

2015. A demand letter was issued on March 30, 2015. The Mortgage includes as

terms that the Parlees agree:

1. to pay any outstanding liens, taxes, or other encumbrances on the Parlee

Lands; and

2. if the Parlees allow the Mortgage to go into default then will pay all legal costs

associated with enforcing the Mortgage on a solicitor and own client

indemnity basis.

As noted Servus paid outstanding property taxes ($11,782.31) on the Parlee Lands on

March 27, 2015 to avoid sale of the Parlee Lands due to tax arrears.[Before WeRe

Bank was operational]

The Boser affidavit includes unorthodox documents received from the Parlees and

copies of related communications. These are discussed in more detail below in Part

IVB2 of this judgment: “The WeRe Bank”.

[24] On June 10, 2015, Mr. Parlee wrote to Servus requesting information on what steps

Servus had taken to contact and obtain funds from the WeRe Bank in relation to the WeRe

Cheque. Also attached was a document titled “NOTICES of PROTEST SENT” (Appendix F)

that indicated Mr. Parlee had taken steps within a timeline set by the UK Bills of Exchange

Act 1888 and the “UN Convention 1988 on International Bills of Exchange and Promissory

Notes.”[At this point Servus could not possibly know whether WeRe Bank had sufficient

funds to pay/honour the cheque if presented via a normal channel of “Special Presentation”.

As Mr Parlee had offered a payment and as Servus had refused to either accept it or present it

then both Section 42 Non Acceptance and 43 Dishonour by Non Acceptance were invoked]

[25] On June 25, 2015 Mr. Parlee and counsel for Servus appeared before Master

Breitkreuz. The learned Master:

1. concluded Mr. Parlee’s explanation of the WeRe Bank and WeRe Cheque was

“gobbledygook”;[ This is selective conclusioning. So we have the very nature

of a “trust” here containing trust property – not discussed. We have the nature

of promissory notes and their legal validity dismissed also, we have the nature

of an IOU and nature of money creation dismissed out of hand and we have

the arena in which it is discussed “openly biased and hostile and protective of

the status quo!” We also have Servus Credit Union or whatever they are,

colluding with the judiciary to maintain the “Rule of Tyranny” not law.]

2. found Mr. Parlee had not proven he had provided any payment to Servus;

[Mr Parleee had delivered a Promissory Note duly completed for the sum of

£150,000 to WeRe Bank. This promissory note is the underpinning of ALL

and we mean ALL commercial transactions on this planet. A man’s promise to

his fellow is all there really is. So why does Schlosser neither comment upon it

nor refer to the fact that a Promissory Note brings money into being? ]

3. determined the debt then to be $334,837.01; and

4. ordered summary judgment;

5. provided a 30 day redemption period, failing which the land would be offered

for sale by tender. [And who was lined up as buyer for the “sale by tender?”]

The next hearing was scheduled for August 13, 2015. Mr. Parlee’s response was “I do not

consent.”

[26] Mr. Parlee, on July 3, 2015, wrote to counsel for Servus and complained that WeRe

Bank had the necessary funds ready to be transferred, demanded evidence of why Servus

considered WeRe Bank to be a fraud, and asked why Servus has not attempted to clear the

WeRe Cheque. He then warned that failure to provide a satisfactory response in five days will

result in “lasting tacit agreement through acquiescence” settling the dispute with Servus over

the WeRe Cheque in the Parlees’ favour, cancelling the August 13, 2015 hearing, and

resulting in a damages award.[This seems about as fair a conclusion as could be imagined and

presented by Servus dishonouring the courtesy offered by Mr Alf Parlee and facilitated for

him by WeRe Bank – the analogy here is like going to a restaurant ordering a meal. When it

comes time to pay and you call the waiter over to proffer payment – his reaction is ridiculous

because instead of accepting the money[ or using the card to enter payment] he calls the

police on you for non-payment and forecloses on your home for the non-payment of a debt

WHICH YOU HAD ALREADY OFFERED TO PAY AND IN FACT HAD PAID IN Mr

Parlee’s case! The nature of SERVUS CREDIT UNION obligation to Mr Parlee surely was

to do everything in its power to receive “extinction of the debt (so called) from an instrument.

To offer them a promissory note as payment and they PRETENDING THEY DON’T KNOW

WHAT TO DO WITH IT should have led the judge to say two word – “Case dismissed!” ]

[27] Mr. Parlee also filed a number of documents prior to the August 13, 2015 hearing,

including:

• A July 20, 2015 Affidavit by Mr. Parlee with many attachments that relate to two

general subjects:

1) the WeRe Bank and WeRe Cheque, and

2) a trust and ownership structure between ALFRED PHILIP PARLEE and Alfred P.

Parlee; and

• A July 22, 2015 Affidavit by Mr. Parlee attaching a “NOTICE OF TRESPASS ON

MY PRIVATE PROPERTY” alleging misconduct by counsel for Servus, demanding

that he be disbarred for intimidation and unethical practice, $15 million in damages,

and “I order this case dismissed.” The trespass is:

... No one can use MY NAME or g mail without my consent. I am

OWNER and no one can tell me different. All affidavits of ownership

of Name and Birth Certificate are filed with the Court and are

notarized and authenticated ...

This issue of trespassing and unethical behaviour has caused damage to

the owner of my Estate and created damage on my PRIVATE

PROPERTY. This is unacceptable and requires compensation. No-

body or no-one has authority over THIS BODY. I am owner of Estate

as per filed notarized and authenticated documents.

[Emphasis in original.]

• An Affidavit filed July 25, 2015 which attaches a “SECOND NOTICE OF

TRESPASS ON MY PRIVATE PROPERTY” that repeats the content of the

July 22 “Notice”.

[28] After hearing the somewhat cryptic submissions from Mr. Parlee concerning

ownership issues, foreclosure was ordered by Master Smart on August 13, 2015. Master

Smart rejected Mr. Parlee’s submission that his title to the Parlee Lands could not be

challenged. The Parlees had 30 days to vacate the property.

[29] Mr. Parlee followed this with two apparently separate processes which led to the

October 1, 2015 hearing before me:

[It was myself, Peter of England, who suggested a Writ of Quo Warranto to Mr Parlee at

quite an advanced stage in this saga]

• A “Quo Warranto” declaration to nullify the August 13, 2015 foreclosure order of

Master Smart (Appendix A1). The materials associated the Quo Warranto process

were in two Affidavits of Mr. Parlee, filed August 26 and September 8, 2015. The

August 26, 2015 document is a “Writ of QUO WARRANTO TO DETERMINE

JURISDICTION OF” that places a seven day deadline on Master Smart to take

certain steps.

The September 8, 2015 Affidavit attaches a “WRIT of QUO WARRANTO

CHALLENGE OF JURISDICTION” (Appendix A2) that declares since Master Smart

did not respond to the Aug. 26 document that the August 13, 2015 foreclosure order is

“NULL AND VOID”. This Affidavit also attaches Criminal Code, RSC 1985, c C-46,

s 337 and a letter from Servus’ counsel that attaches the August 13, 2015 order. The

letter is marked in diagonally marked in red marker: “NULL and VOID”.

• Documents attached to two September 10, 2015 Affidavits:

o A “PRIVATE INDEMNITY BOND - NON-NEGOTIABLE” (see Appendix B)

for $1 million that promised payment by “DEBTOR” “ALFRED PHILIP

PARLEE”, “Indemnitee” to the “Indemnifier”, the Court Clerk or agents. This

is a “SPECIAL DEPOSIT” to “ZERO, SETTLE, and CLOSE ... COURT

ORDER File # 1504 00261”. The Bond instructs it “shall be Ledgered as an

ASSET for the needs of the Court of Queen’s Bench ... “ and that the Bond “...

expires the moment the man, alfred philip parlee, dies.”

o An “Indemnity Agreement” dated September 10, 2015 that the Clerk of the

Court Grande Prairie will hold harmless and indemnify “ALFRED PHILIP

PARLEE” for any legal action, including criminal proceedings, for up to $10

million per legal action. The “Indemnity Agreement” has one signature, that of

Mr. Parlee.

[30] This was followed on September 18, 2015 by an Application from Mr. Parlee that

states:

Note INDEMNITY AGREEMENT

Remedy claimed or sought: LEDGER INDEMNITY bond filed September

10/15 with Court of Queen’s Bench GRANDE PRAIRIE. Exhibit “A”

Grounds for making this application: The Indemnity bond # APP 100915 Can.

Is to pay Court FILE #1504 00261. As title holder of Birth Certificate I am

authorized to sign INDEMNITY BOND.

Material or evidence relied on: Authenticated Birth records and BIN numbers

filed with Court of Queen’s Bench July 20/15

Applicable rules: As owner + title holder of BIRTH CERTIFICATE my

signature creates value. I am surety and Birth certificate is the security.

Applicable Acts and regulations: UCC-3603 3-603 Bills of Exchange 80, 81

(Canadian) #337 Criminal Code of Canada.

[31] What followed was the October 1, 2015 hearing.

[What you see above is a bit of a dog’s breakfast of reasoning and the law and process is

rather mixed up – the fact that poor Mr Parlee had little help in this matter is quite evident]

IV. Analysis

[32] The fairest way to provide the written judgment that I promised Mr. Parlee is to treat

the documents he filed after the August 13, 2015 foreclosure order as two separate

applications:

1. a Quo Warranto application to declare the August 13, 2015 foreclosure as null

and void because it was made without jurisdiction, as supported by Mr.

Parlee’s July 20 Affidavit documents; and

2. an application to reverse the foreclosure and return possession of the Parlee

Lands to the Parlees because they had (over)satisfied the outstanding mortgage

debt with a $1 million “PRIVATE INDEMNITY BOND - NON-

NEGOTIABLE”, or via other means in the July 20, 2015 Affidavit documents.

[33] These two issues are to some degree intertwined as Mr. Parlee responded to the

foreclosure with a cascading series of applications, and by the manner in which Mr. Parlee

advanced his application on October 1, 2015.

A. Quo Warranto Application

[34] I reject Mr. Parlee’s Quo Warranto application. The application makes two demands:

l. That you, MASTER L.A. Smart, shall produce unto this living man, within the period of 7

days from the date hereof, a sworn affidavit, sworn under your own hand with full, unlimited

personal liability, under penalty of perjury, to the effect that you did, articulate, sign and

swear an Oath of Office of Judge, to act under the authority of the ENTITY, and that you do,

at all times, operate in strict compliance with that oath of office in the ordinary course of your

duties, without fear, favour or exception, under Rule of Law.

2. That you shall present and deliver by certified mail, to this living man, within the same 7

days, true and certified documentary evidence and proofs (i.e. statement, acceptance or

declaration) signed under my hand and seal, that I did grant you unto YOU, and or unto the

ENTITY, or unto any other person, permission, authority or consent; including but not

limited to, YOU, the ENTITY, the principal of the ENTITY, or the founding principal of the

ENTITY, to honour any judgment, order, decision or verdict of the said parties, in any cause

or matter in which I may have been involved. [Emphasis added.]

The “ENTITY” is defined elsewhere as the Alberta Court of Queen’s Bench.

[35] First, the Quo Warranto application was not filed in a manner that meets the Alberta

Rules of Court, Alta Reg 124/2010, s 3.15(1)(a) which, if it had any application to this

situation, would require an application for judicial review. If there were to be a challenge of

Master Smart’s Order, it would be required to take the form of an appeal under Rule 6.14.

[I believe that it was Peter of England who suggested this line of challenge The Writ]

[So was this just a filing error? If it was under common law then a simple written or verbal

request could have sufficed – but not in this sham of a court]

[36] I will also say at this stage that the prerogative writ of Quo Warranto has become

almost [almost pregnant is NOT pregnant and almost vestigial is NOT gone] entirely

vestigial, having been taken over by modern procedure. It was popular in the 13th

century,

being extensively used by Edward I, but the sun has set on it: Principles of Administrative

Law, Jones and deVillars, 6th

ed, p.676 and Holdsworth, A History of English Law, l 229.

[37] Second, Mr. Parlee’s August 25, 2015 document reproduced in Appendix A(1) is a

‘foisted unilateral agreement’, or, more correctly in this instance, a ‘foisted unilateral judicial

review’, where the failure to respond purports to crystalize a result in Mr. Parlee’s favour.

[What about adhesion contracts for parking and adhesion contracts for loans for property -

are these not in effect “unilaterally foisted”? ]

[38] The “foisted unilateral” language comes from Meads v Meads, where Rooke ACJ

debunked the common OPCA concept that in contract silence means agreement. [What of

non rebuttal of claims in common law courts? Non rebuttal is taken as acquiescence –

PERIOD!] This is one of the first things taught in law school; even the greenest law student

will have learned it in her salad days (“an offeror may not arbitrarily impose contractual

liabilities upon an offeree merely by proclaiming that silence shall be deemed consent”);

Felthouse v Bindley, (1862) 11 CBNS 869 Miller 35 MLR 489, Cheshire, Fifoot &

Furmstons Law of Contract 15th

ed., p.61.

[39] The same is true for judicial proceedings. “Silence means victory” only where that

result is provided by the Rules, other legislation, or the common law.[Common law was not

evident in that court of Herr Schlosser and is NEVER offered – it has to be fought for these

days] The procedure for judicial review in Alberta is governed by the Rules. Mr. Parlee’s

Quo Warranto “judgment” (Appendix A (2)) has no legal force because his Quo Warranto

application (even if it had been filed correctly) has not been adjudicated by the appropriate

body.[What this means is that the Attorney General {AG} of Canada – the juiced in

Comptroller has to ALLOW you to have PERMISSION to obtain it. Can you ever win with

these serpents?]

[40] A third basis on which Mr. Parlee’s Quo Warranto application fails is that it is

presumes that a judicial officer has an obligation, on demand, to provide evidence of their

Oath of Office. In fact the opposite is true. No litigant has a right to question a judge or

master on their oath of office.[WHAT MISPLACED ARROGANCE. This is totally untrue –

a PUBLIC servant as this Schlosser is, MUST affirm that he has so taken his Oath of Office

and Oath of Allegiance. Has he in fact EVER sworn an Oath? If he has then why would there

be a problem of him admitting it in a PUBLIC arena which is a court ? Recently in a case in

the UK in Doncaster High Court with 4 witnesses present, myself included, a Deputy District

Judge said he did not know what we were on about when we asked him if he had Sworn an

Oath of Allegiance to the Crown – he professed to state also that he “did not have to and had

no idea what we were on about”. Upon telephoning the Ministry of Justice, Petty France, the

next day in London and speaking to their Judicial Appointments section it was confirmed

that EVERY JUDGE AND MAGISTRATE MUST SWEAR THESE OATHS] Instead, it is

up to a litigant to provide positive evidence to challenge the jurisdiction of these

presumptively authorized parties: Fearn v Canada Customs, 2014 ABQB 114 (CanLII) at

paras 83-87, 586 AR 23.

[What Mr Parlee should have said, maybe, is “I am placing you Judge Schlosser on your Oath

and making this venue now a Court of Public Record – here is my Recorder and here are my

witnesses.]

[41] A fourth defect in Mr. Parlee’s Quo Warranto application is that he demands proof

that he had agreed or consented to Master Smart’s having jurisdiction over the foreclosure

matter. It seems Mr. Parlee concluded he is outside court authority because of his inherent

“sui iuris” [sic] authority that flows from “Divine Cannon Law” and his being a “living

human being”. Religious belief and religious law does not trump Canadian law: Meads v

Meads, at paras 276-285; R v Lindsay, 2011 BCCA 99 (CanLII) at paras 31 and 32 (failure to

file tax returns), 302 BCAC 76, leave refused [2011] SCCA No 265. Individual consent is not

required for the operation of Canadian law or, for that matter taxation: Meads v Meads, at

paras 405-410; R v Jennings, 2007 ABCA 45 (CanLII) at para 6, 72 WCB (2d) 360, Lynch v

Canada North-West Land Co. (1891) 1891 CanLII 60 (SCC), 19 SCR 204 at 208-10.[So

what Schlosser is stating here very clearly which runs contrary to every jurispudential tome

written and flies in the face of common sense and social structures of all governments and

governance is that THE CONSENT OF THE PEOPLE IS NOT A REQUIREMENT to quote

him verbatim: “ individual consent is not required for the operation of Canadian law” But

what law are they offering here to Mr Parlee – Private law, Administrative law, Law

Merchant, Admiralty or Maritime, Talmudic?][Jewdiciary]

[42] Last, I note that the August 25, 2015 document includes an Internet address link to a

July 11, 2013 “Apostolic Letter” by Pope Francis. This specific document has been

previously rejected as having no legal effect in Canada: Alberta Treasury Branches v

Nielson, 2014 ABQB 383 (CanLII) at paras 27-29, 14 CBR (6th) 177, per Smart, M. citing;

Claeys v Her Majesty et al, 2013 MBQB 313 (CanLII) at para 18, 300 Man R (2d) 257.

[You see how he cleverly places the word “legal” in italics? What does he mean by so

doing?]

[43] Mr. Parlee’s Quo Warranto materials also attach the text of Criminal Code, s 337:

337. Everyone who, being or having been employed in the service of Her Majesty in right of

Canada or a province, or in the service of a municipality, and entrusted by virtue of that

employment with the receipt, custody, management or control of anything, refuses or fails to

deliver it to a person who is authorized to demand it and does demand it is guilty of an

indictable offence and liable to imprisonment for a term not exceeding fourteen years.

[This will possibly be referring to the Demand made on the Public Servant Schlosser to

provide evidence that he was On Oath?]

[44] Section 337’s relevance is not obvious from Mr. Parlee’s materials or his

submissions. It has no application to Mr. Parlee’s Quo Warranto application. This provision

was recently interpreted in Ambrosi v British Columbia (Attorney General), 2014 BCCA

123 (CanLII) at para 53, 353 BCAC 244, leave denied [2014] SCCA No 320. Bennett JA

concluded s 337 “...was enacted to prevent theft by public employees of the monies,

documents, or other chattel they possessed by virtue of their employment.” No prosecution

has ever been conducted on the basis of s 337: Ambrosi, at para 45.[Wait for it!]

[45] Mr. Parlee’s Quo Warranto materials have no legal relevance, or effect.

[Well that is that then – let’s all go home!]

B. The Parlees Have Paid the Outstanding Debt

[46] I cannot, and, in any case, would not challenge the conclusion of Master Breitkreuz

that Mr. Parlee’s explanation of the WeRe Bank is gobbledygook, and Master Smart’s

finding that the Parlees do not have some form of absolute, invulnerable title on the Parlee

Lands.

[47] Mr. Parlee’s claims that he has, one way or another, already paid Servus everything

required by law. There are three separate payment scams: One is historic; the other two are

relevant to the October 1, 2015 proceeding.

1. The “Freeman Legal Services” “A4V” Scam

[48] The first point at which the Parlees were victimized actually precedes the foreclosure,

but it is involved in that scenario. The event that precipitated the foreclosure was Servus’s

response to the Parlees’ failure to pay their Grande Prairie No 1 County property taxes. The

Servus payment occurred on March 27, 2015. That same day counsel for Servus telephoned

the Parlees to inquire if those taxes had been paid. A fax from “Alfred Philip Parlee Living

Soul” was received by counsel on the same day, and ultimately attached as Exhibit E of the

Boser June 3, 2015 affidavit. In the fax cover sheet Alfred Parlee explains that the property

taxes had been paid on December 19, 2014 with “an A4V or bill of exchange” for $11,782.31

Since that document was not rejected by the County it was accepted “per Bills of Exchange ...

and amount owing is now zero.” [Again this was long before WeRe Bank ever came upon the

scene. See the efficacy of A4V – this all boils down to the creation of a Trust following

Bretton Woods in 1944 and the fact that the USA and Canada as well as most countries have

been rendered bankrupt following WW2.]

[49] Mr. Parlee continues:

I have all receipts and paper work on file and am confident that the Bill of'

Exchange Act is still in effect and what I have done as far as set off and

settlement as a remedy is perfectly legitimate and lawful. I have included 3

pages of legal info from F.L.S. on International Bills of Exchange and

International Promissory Notes which explains payment, acceptance, protest

etc. Please read carefully as there is liability for violation of International Law

and UN Conventions. The County of Grande Prairie has violated principles of

the Bills of Exchange Act and is also liable. I have given my Power of

Attorney for debt assumption and set off to Freeman Legal Services and WeRe

Bank and they will be in touch as I will forward this fax to Peter of England.

Thank-you and God Bless. [Emphasis in original.]

The three page document from “Freeman Legal Services” is reproduced in Appendix A.

[50] I do not believe there is much need to elaborate[No siree! Let’s shake that tree lest

something falls out!] on the “A4V” ‘money for nothing’ scam as it has been described in

detail in Meads v Meads, at paras 531-543, and more recently in Re Boisjoli, 2015 ABQB

629 (CanLII) at paras 38-42. In brief, “A4V” is a fraud [ 1. It cannot be a fraud because it is

firmly encapsulated in the Uniform Commercial Code see

https://www.law.cornell.edu/ucc/3/3-303 Article 3 - 303 as well as the Bills of Exchange

Act]where the conman claims that bills and other financial obligations may be paid by

drawing funds from a fictitious government-operated bank account.[No it does NOT! It

simply treats the bill being sent as a “method of seeking money when there exists no contract

“prima facie” for the demand being made. A classic example would be a parking ticket

demand, or demand for taxes. As there is no consent – no agreement from the individual –

then the Sexsmith property tax dept fire off a “bill/Order/demand”. It is backed by nothing so

they are searching for value and when you receive this you can either a)Ignore it = dishonour

= value to them in their system as they’ll take you to court, b)Pay it with money from your

bank account, c) Sign it as accepting it for value but the signature in effect acts as an

endorsement on the NOTE – see the significance of EVERY BANK endorsing a cheque or

asking you to ENDORSE IT AT THE CHASHIERS WINDOW before they’ll allow you to

pay it in. Ever wondered why?]

The form promoted by Freeman Legal Services is different from previously documented

variants because its secret source of funds is a trust fund set up in World War II by the

western allies to finance European post-war reconstruction and re-integration.

[51] This is at least as imaginary a source for free money as the Sovereign Citizen

variation where citizens serve as human collateral for bank-to-government loans indexed by

birth certificate numbers. The Freeman Legal Services letter also include other commonplace

false OPCA motifs such as the supremacy of commercial law and that the US Uniform

Commercial Code has universal, transnational application: Meads v Meads, at para 150.[As

in fact it must have as UNIDROIT Rome state it is private commercial law and is the flux for

the global movement of goods and services; see http://www.unidroit.org/]

[52] The Parlee’s “A4V” payment to the County was worthless. As Richard JA observed

in Bossé v Farm Credit Canada, 2014 NBCA 34 (CanLII) at para 42, 419 NBR (2d) 1, leave

denied [2014] SCCA 354:

In my view, this is a case where [Farm Credit Canada] has been subjected to

wrongdoing that is reprehensible, scandalous and outrageous. Whittled down to its core, this

was a simple claim on a debt that should have been decided on summary judgment with

perhaps a simple trial on the quantum. Instead, it turned into a litigation nightmare for FCC,

requiring it to repeatedly respond to motions, applications and allegations that were each

ultimately found to be frivolous or without any merit. Moreover, the Bosses made claims and

advanced defences that any reasonable person would know were devoid of merit. It defies

logic that one could print out bonds for any sum of money, let alone significant amounts, and

simply say to one’s creditors “here, go away, you have been paid.” I am convinced the

Bosses knew this. Their persistence and the vigour with which they challenged or sought to

challenge virtually every ruling made against them convinces me they engaged in litigation

warfare against FCC as an obstructionist tactic in the hope they would deplete not necessarily

FCC’s resources but rather its resolve to obtain judgment for the balance of the debt owed.

(emphasis added)

[53] But the Parlees fell for it. This is the first way the Parlees were victimized by “Peter

of England”.[This does not make sense at all – Acceptance for Value is a fully fledged

commercial method of payment. The wealth of the world is a fact. Those in the higher

echelons of commerce and finance know it as does Schlosser]

2. The WeRe Bank

[54] After Servus commenced its foreclosure on the Parlee Lands, the Parlees attempted

to pay off the outstanding Mortgage/Line of Credit debt with a “WeRe Cheque” (July 20,

2015 Affidavit, Exhibit “E”). This document and an accompanying item, a two-sided

“allonge”, were received by Servus on May 5, 2015, and are reproduced in Appendix D.

[55] The June 3 Boser, June 23 Kendrick, and July 20 Parlee affidavits provide more

information about the WeRe Bank, WeRe Cheques, and their associated scheme. At first

glance the WeRe Cheque appears to be a conventional cheque drawn from a bank for a

customer, in this case Alfred Parlee. However, there are irregularities. WeRe Bank subtitles

itself as “Universal Energy Transfer”. Comparison of the Parlees’ WeRe Cheque with other

WeRe Cheques discloses they all have an identical “Branch Sort Code”[There is only one

branch, for the moment, so only need for one sort code which just so happens to be the ID

Ref number for the International Common Law Court of Record] and “Account Number”:

“75-0181: 88888888”. Perhaps unsurprisingly, a list of UK banks compiled by the Bank of

England (Kendrick Affidavit, Exhibit “F”) does not include “WeRe Bank” or any financial

institution with a similar name.[ WeRe proud to say that is the case – WeRe Bank is NOT

registered with the Cabal’s Country Club Collusionists. But a sort code is just an address.

What Schlosser does here is “distract” – what does it matter what is on the cheque if the

nature of this BUSINESS is “the getting of money to Servus” why would they care if the

“amount proffered” was written on the back of a cow? They wouldn’t now would they? A

cheque is just an instruction and can be written upon anything at all.]

[56] Another irregularity documented in the June 23 Kendrick Affidavit is that the WeRe

Bank does not participate in the Society for Worldwide Interbank Financial

Telecommunication [“SWIFT”] system for inter-bank transfer of electronic funds. Instead,

WeRe Bank has its own “highly secure format” protocols: “SWALLOW [Secure Waygate -

Allow]” and “SPIT: [Secure Protocol Information Transaction]”. “Peter of England” instructs

that banks are to send a scanned copy of the WeRe Cheque to his email account and then

“Funds can be sent electronically Via “SWALLOW”. The WeRe Bank warns:

The Bank MUST present the cheque for clearing - no question, no debate, no wiggle room!

It’s the LAW.

[57] A printout of WeRe Bank website (June 23 Kendrick Affidavit, Exhibit “E”) could

be a satire of modern conspiratorial motifs, but it instead seems to be marketed as the truth.

The WeRe Bank introduces itself in this manner:

WeRe Bank

The Free Fair and Final Private Bank System

Created under Common Law and Regulated Under Common Law Court of Record 750181

Providing "Legal Money with Finality of Settlement"

DIRECTIVE

"To Free Mankind From The Paralyzing, Restricting, Fear-based Monopoly and Control

Agenda of “money scarcity” Which The Global Ruling Elite Have Imposed With “ruthless

and vicious” Determination Upon All Peoples Of Earth."

WeRe Private Banking System

is based locally and delivers Free, Fair and Final (3Fs) payment for TIME ACTIVITY with

LEGAL MONEY.

LEGAL MONEY IS FINALITY OF SETTLEMENT ON THE SPOT OF TIME

FINALITY OF SETTLEMENT IS ECONOMIC AND SOCIAL FREEDOM

“Aren’t you fed up with the constant hassle of never having enough of anything left at the

end of every month?”

“Aren’t you “tired of being tired” due to too much work, not enough time, constant threats,

coercion, duress, bullying, intimidation and the use of force to extract money from you by the

greedy corporations, police authorities, speed camera agencies, taxation authorities, local

councils, bailiffs, debt collection agencies and Court Enforcement Officers and HMRC or the

IRS?”

“Are you not “fed up to the back-teeth” with the constant lies of politicians and government

assuring you that there “just isn’t any more money for the public services, the NHS, the

roads, schools, students, or you and your family when there sure as hell seems to be no

shortage for them and theirs and the HS2 vanity projects?”

Well, if you've had enough of all of this – we have some very good news for you!

If you are exhausted with fighting then:

STOP!

STOP RIGHT NOW!

STOP IT THIS VERY MOMENT!

“Don’t Fight it! Just Pay it!”

The WeRe Bank chequeing account from ReMovement provides you with ASSURED

DEBT ERADICATION ON ALL “PUBLIC SIDE OF THE LEDGER LIABILITIES” ...

[58] In this context, ‘conventional money’ is worthless:

You were convinced to accept worthless money, the PROMISSORY NOTE/SCAM, for the

promise/lie of further wealth somewhere and at some time in the future in return for going

without in the moment of now.

[59] Presumably, that is why WeRe Bank does not even deal in money, but instead trades

in “Re”, “units of time and space”:

WeRe Bank’s principal trading asset is called the Re. It is a unit of space and

time and has Value as it is “exchangeable” or trade-able.” Units are created

through expenditure of effort over time and we hold these units “on account”

and pay them out to our customers. The units are (energy × expended time =

REWARD) based upon exceptionally sound principles of Albert Einstein’s (e

= mc²), where m = mass, c = speed/time, e=energy (General Theory of

Relativity). This equation, upon reflection is the only SOUND premise for a

unit of exchange/currency in this world. Units are denominated in 2 skill/time

classes: [Emphasis in original.]

[60] Still, if money is worthless, it seems strange that “Peter of England” requires that his

customers first pay £35 up front as a “Joining Fee”,[incorrect this is the set-up fee + I have

not stated that “money is worthless” only that “fiat currency is!” Equally I have reiterated

time after time that we MUST SCALE THEIR FORTRESS WALLS WITH THEIR ROPES

AND LADDERS. This is an exercise in change absolute. Until we can build sufficient mass

and have the Re sublimate the other ruinous currency that they’d pollute us with then what

else is there to use? If nothing else we must be “practical” – printers, postal services, design,

transport companies don’t take our unit for the moment. Simply put – simply understood.]

and then a £10 monthly subscription fee [this is a membership fee to ReMovement and is like

an affiliation with a club or union]. You also need to complete and submit a £150,000.00

promissory note to WeReBank. Conveniently, the template can be downloaded from its

website. [Schlosser VERY SIGNIFICANTLY does not mention here THAT THIS

PROMISSORY NOTE IS A NONSENSE, WORTHLESS OR GOBBLEDY GOOK!]

a. WeRe Bank is a Fraud [No it is not!]

[61] The first basic reason why the WeRe Cheque was not a payment is simply because

WeRe Bank is a fraud.[Please define fraud – we don’t seek to deceive and no one is at a loss

iif our processes are followed. The DEBTOR gains release from debt – the PAYEE gains

“monetary unit of account” and has his liability/exposure eradicated. The bank too finds a 3rd

party source for additional “funds” to keep it’s PONZI scheme going. This we apologise

for…but the shelf life is now short ] It is not a regulated UK bank.[We do not need to be

regulated as we operate under common and natural law of the land and as banking has been

around before the FCA, before the Bank of England or the IMF, World Bank etc then we

have historical precedent on our side]The WeRe Bank never promises to make payments to

recipients of WeRe Cheques. It only transfers “Re” energy units.[100% incorrect –WE DO

MAKE PROMISES TO PAY THE PAYEE IN THE CURRENCY OF HIS/HER COUNTRY

TOO! We only offer the “Re” as a private trading unit on the membership side – though it

will become the PlanetReServe monetary unit of account in due course. So the “coup de

grace” here is: “If WeRe Bank was, let’s say/suppose, receiving valid and signed promissory

notes to the value of £n – would this make them of any worth, at all, to anyone, anywhere? If

the answer to this ONE question is “Yes!” then WeRe winners and Alf should still have his

property] It might as well promise to transfer magic beans. Imaginary energy units are not a

form of currency and they do not pay debts.[Then Herr Schlosser – what do you call the US

National debt for example at $19 trillion? Is this REAL or IMAGINARY? The US

government and ther US Treasury would call it “imaginary” as a) they just create it out of

thin air and the Bank of England Confirms that: Money creation in the modern economy - Bank of England www.bankofengland.co.uk/.../qb14q1prereleasemoneycreation.pdf

by M McLeay - Cited by 109 - Related articles Money creation in the modern economy. By Michael McLeay, Amar Radia and Ryland Thomas of the Bank's Monetary Analysis Directorate.(1). Overview. Money Creation in the Modern Economy Overview: Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money. The reality of how money is created today differs from the description found in some economics textbooks:

[62] Our Court is not the first entity to reach that conclusion. On September 17, 2015 the

UK Financial Conduct Authority issued a consumer notice that WeRe Bank’s payment

scheme was false[ TOTALLY INCORRECT IT SAID NO SUCH THING – it only proferred

the opinion that as far as it was aware to date no cheques had been honoured”{ None of these

institutions has accepted the cheques as legitimate payment} and that its users could face legal

consequences. The Central Bank of Ireland [Yes this paragon of virtue which sold the Irish

people and nation into Debt Slavery via a several billion Euro bail out which immediately

went out the back door and back to Brussels the very next day - BUT which the “people of

Ireland” will be expected to pay off over the next millennium]on October 19, 2015 issued a

press release that the WeRe Bank is not authorized to carry out banking or other financial

services, and activities of that kind are a criminal offence.[But this “trade restriction”

attempted to be placed on a trading partner is totally contrary to Article 101 of the Treaty of

Rome is it not? Collusion and monopolistic cartel and price gouging actions are anti-trust

violations punishable by imprisonment and fines!]

b. Non-Canadian Authorities are not Binding

[63] There are legal defects as well. Reviewing the “allonge” and “Peter of England’s”

communication indicates that the recipient of a WeRe Cheque is supposedly bound by the

procedures in the UK Bills of Exchange Act and the UN Convention on Bills of Exchange

and Promissory Notes. UK law no longer applies in Canada. International treaties only have

any force and effect inside this country if the treaty’s provision are enacted as Canadian

legislation or put in effect by government order: Capital Cities Communications Inc. v

Canadian Radio-Television Commission, 1977 CanLII 12 (SCC), [1978] 2 SCR 141 at 188,

81 DLR (3d) 609. Canadian governments are free to ignore and act in conflict with its

international treaty agreements: R v Hape, 2007 SCC 26 (CanLII) at paras 53-54, [2007] 2

SCR 292. [Well, that’s some “get out of jail card is it not? They don’t have to abide by

International Law! So does that mean the Geneva Convention are irrelevant and the 1987

Convention Against Torture and Other Cruel Inhuman Degrading Treatment or Punishment]

[64] There is another reason why the treaty identified by “Peter of England” is irrelevant (at

least if he is attempting to identify The United Nations Convention on International Bills of

Exchange and International Promissory Notes (New York, 1988)) - Canada has not ratified that

treaty.[Yes they have by implication and useage!] As for its precursor, The Convention for the

Settlement of Certain Conflicts of Laws in connection with Bills of Exchange and Promissory

Notes (Geneva, 7 June 1930), Canada never signed it.[Why not? Maybe they just forgot – this is

a ReMinder …get it signed!] What is perhaps even more ironic is that the home jurisdiction of

“Peter of England”, the United Kingdom, which is not a participant in either treaty.[ Now that is

ironic!]

c. No Obligation to Accept Non-Cash Payments

[65] Beyond that, Servus’s refusal to accept a particular form of payment is entirely legal.

The WeRe Bank materials (see Appendix D(2)) rely on an obiter statement of Lord Denning in

Fielding & Platt Ltd v Najjar, [1969] 2 All ER 150 at 152 (UK CA):

“We have repeatedly said in this court that a Bill of Exchange or a Promissory Note is to be

treated as cash. It is to be honored unless there is some good reason to the contrary”.

WeRe cannot agree that Servus can specify a particular form of payment – electrical forms of

money transfer merely “subjugate and entrap” the

[66] This exact quote and its potential relevance in Canada was recently considered by

Rooke ACJ in Re Boisjoli at paras 30-36, where an analogous argument was made by a

vexatious OPCA litigant who claimed to have forced payment of a debt with a promissory

note and the Bills of Exchange Act. Rooke ACJ adopted the Scottish Court of Sessions

(Scotland’s highest civil court) reasoning and conclusion in Child Maintenance and

Enforcement Commission v Wilson, 2014 SLR 46 at paras 10-11, [2013] CSIH 95, where

that Court came to a number of conclusions, including that a bill of exchange, such as a

cheque, may only extinguish an existing debt if the creditor agrees with that mechanism of

payment. The ‘near cash’ theory has no application to these facts. A creditor may always

insist on payment in legal tender.[ And this is exactly what the WeRe Bank Debt Settlement

Facility offers. Legal Tender is a NOTE – a bank note at that. It is just a promissory note is it

not? So all we have to conclude now is that if a NOTE issued can be a Promissory Note and a

Note can be legal tender can a note be legal tender if it is issued by the Guarantor and Surety

on ALL notes? That individual as part of the collective drives to the VERY HEART NOW

OF SCHLOSSER’S CLAIM THAT “”this is a free money scam” and there is no thing as

“free money”. The absolute and final “buck stops here” responsibility of the nation’s debt and

obligation(s) is the citizen which seems to be Mr Parlee. His NOTE is therefore good and the

debt paid in Legal and Lawful tender!]

[67] WeRe Bank documents proclaim that any alleged dispute over the WeRe Cheque

would not be addressed in a Canadian court, but instead “ultimately arbitrated” via trial by

jury before the “International Common Law Court of Record 750181”. This institution is

purportedly the high court of the jurisdiction: “There is NO COURT WITHIN ENGLAND

SUPERIOR TO A COMMON LAW COURT DULY CONVENED”. I will simply observe

the International Common Law Court is unknown to either myself or, apparently, the UK

courts. It is never mentioned even once in any of the jurisprudence archived on the British

and Irish Legal Information Institute (BaiLII) website. [But they will know of it – soon

enough, as in fact the do so now!”]

[68] Even if Lord Denning’s dicta were binding on me, these facts are all “good reasons”

to refuse Mr. Parlee and “Peter of England’s” so-called bill of exchange.

d. WeRe Bank Three/Five Letters Scheme [This is not our “scheme” – He is possibly

mixing it up with the Getoutofdebtfree site]

[69] It appears the WeRe Bank scheme may also incorporate a variation on the Three/Five

Letters foisted unilateral agreement scheme that I reviewed in Bank of Montreal v

Rogozinsky, 2014 ABQB 771 (CanLII) at paras 55-73, (and see also Re Boisjoli at paras 49-

57). This is a set of documents that purportedly crystalize a result if the recipient does not

respond.

[70] The May 19, 2015 “Notice of Protest...” and June 10, 2015 “Notices of Protest Sent”

(see Appendices E, F) have parallels to documents used in the Three/Five Letters process.

[71] An interesting aspect of these two documents is that one of the witnesses is a “Tel

Sutherland” of Grande Prairie. A person of that same name and location unsuccessfully

attempted to pay a court judgment by writing “Accepted for Value” on the judgment and by

attaching his birth certificate,, which was annotated with the instruction to “Deposit to court

file”: Underworld Services Ltd. v Money Stop Ltd., 2012 ABQB 327 (CanLII), 545 AR 102

(or contempt hearing before Veit, J.) This is another obvious attempt to use the “A4V”

‘money for nothing’ scam. Sutherland in 2013 was found guilty of contempt of court for

failing to provide documents to the Canada Revenue Agency and is now in jail: Canada

(National Revenue) v Money Stop Ltd., 2013 FC 133 (CanLII) 427 FTR 107; Canada

(National Revenue) v Money Stop Ltd., 2013 FC 684 (CanLII), 2013 DTC 5121.

e. “Peter of England”

[72] A disturbing window into the OPCA world and the WeRe Bank fraud is provided by

email correspondence between Alfred Parlee and “Peter of England” found in the Affidavits.

On May 20, 2015 Mr. Parlee writes “Peter of England” requesting advise, he needs support

“... because these lawyers can rattle my chain.” “Peter of England” replies:

Tell them that you want a firm statement on why they are "perverting the course of justice"

and ask them why a cheque drawn on a bank does NOT equate to "money"?

Send this to him again and ask him to affirm that he can rebut this Allonge in a court of law

and if he cannot he should IMMEDIATELY take legal advice from the City of London.

...

Stand firm with him - tell him you'll see him in court and you will personally be be looking at

liens being placed upon him and his business - ask him "under full commercial liability and

penalty of perjury" why he claims the cheque is not good?

These cheques are clearing in the UK- we have had Chyrsler and ClBC on the phone to us.

We have become the Bankers Prayer - we are their life-line, without us their is no more

liquidity in the market

This is NOT freeman mumbo jumbo but international banking practice - tell

[email protected] then we'll assure his sorry ass that if he goes to court he's going to get

hammered!

...[This seems to be cut and pasted mumbo jumbo ---]

He/they has/have to realize, eventually, these arrogant hyenas, that their are bigger creatures

in the jungle than they!

He should step very carefully this one!

Peter

[73] Mr. Parlee writes “Peter of England” once more on June 17, 2015 asking for advice

“... as the hearing is next week. I am worried.” Peter responds with:

Please send him this and tell him the days of ReTribution are upon him. His time is passed

his number has been called.

More than this Alf I cannot do

[74] These communications are a discomforting glimpse into how OPCA gurus work:

making false promises and callously goading their customers into ill-advised action. The

evidence I received makes it obvious that “Peter of England” is entirely willing to ruin the

finances of his customers, and even put them at risk of criminal prosecution for passing bad

cheques.[The cheques are NOT bad and it is very interesting to point out that no one has been

challenged on this “passing” of bad cheques!”] His reward is a paltry £35.00.

3. The Private Indemnity Bond

[75] Mr. Parlee’s July 20, 2015 Affidavit discloses a third OPCA scheme. It has a number

of ‘ingredients’:

1. a copy of Mr. Parlee’s Alberta birth certificate,

2. a copy of Mr. Parlee’s Alberta Registration of Live Birth,

3. a printout of the “Cestui Que Vie Act 1666”

4. a July 9, 2015 “Affidavit for the Ownership” document where:

I, Alfred P. Parlee, grantor, am the absolute and legal owner for the

ALFRED PHILIP PARLEE, (date for Registration June 7, 1949),

Registration Number 1949-08-010689, a corporate entity with Record

number 010689 (and under the constructive trust(s); there being with

the ministry, crown corporation, government agency or SUCH

(Schools, Universities, Colleges, Hospitals))) custody, with and all